Abstract

This paper investigates the role of normative environmental configuration forces on small and medium-sized enterprises (SMEs) adopting sustainable development practices in South Africa. A research survey was performed, and data were gathered from SMEs utilizing owners and managers as respondents. Non-probability sampling at the hand of the convenience method was utilised and 220 respondents constituted the final sample. The analysis of data constituted factor analysis and hypotheses were tested through the structural equation modelling technique. The study hypothesised that normative forces have an impact on the participation of SMEs in the extents of sustainability practices, namely social, environmental and economic. The results led to the supporting of all the hypotheses postulated in the study. Thus, the major recommendation was to support the training, networking and professional affiliations of SMEs in sustainable development issues in order to ensure proliferation of sustainable development amongst these firms.

1. Introduction

The World Bank has acknowledged that there are more than 60 ways in which small and medium-sized enterprises (SMEs) are defined in 75 countries [1]. According to Asamoah [2], the most prevalent and broadly quoted definition of SMEs is the one provided by the European Union (EU). The EU definition provides for a headcount classification of SMEs utilising the number of employees and turnover. The mid-sized category has less than 50 employees and an annual turnover of £10 million whilst a micro firm has less than ten employees and an annual turnover of less than £2 million. Furthermore, in the European Union an SME is defined as a business with a total number of employees which is less than 250, with a maximum annual turnover of £50 million and a balance sheet amounting to £43 million. Asamoah [2] states that the financial maximum amount of turnover and the balance sheet total for SMEs were increased to these recent levels after considering the increased productivity within the Union [3]. However, the EU definition’s major shortcoming is that it lacks universal applicability because it is too all-embracing for it to be applied to several countries. As such, it is urged that researchers need to utilise definitions of SMEs that are relevant to their target group (operational definition) [4].

Hence, research in the area of SMEs has been broadly conducted, globally, with the endeavour of enhancing the survival and success of SMEs [5]. Consistently, Rodríguez-Gutiérrez et al. [6] indicate that empirical studies towards the SME sector have increased more in the last decade than ever before. This is as a result of the substantial input of this business sector towards the definitive performance of economies of the world. As such, the prominent contention that large corporations are the chief players towards the economic growth are being revisited as the essence of SMEs cannot be underrated in the contemporary business milieus [7]. The aptitudes of the SME sector are undoubtedly consistent and underpinned in the values of sustainable development. Contemporarily, within the sustainable development discourse, SMEs are deemed as apparatuses of economic growth, poverty reduction, rural area emancipation and advancement, innovation and job creation [7,8,9]. However, in as much as SMEs make these contributions, there are still numerous apprehensions pertaining to SMEs within the discourse of sustainable development. Sentiments in latent academic works evidently point out that the philosophies and strategies of SMEs concerning environmentalism considerably contrast with those of large businesses [10]. For example, latent academic writings in the realm of sustainability propose that the subsequent deleterious and combined bearing of small businesses (pertaining to the transpiring ruining of the environment) can prevail over that of large firms [11]. Notably, the majority of SMEs perceive their ‘hustle and bustle’ to be of insignificant environmental consequence when contrasted with large firms [12]. Thus, Revell and Blackburn [8] opine that costs that are associated with the absence of environmental management are not a concern for a larger part of SMEs. Subsequently, as posited directly above, the accumulation of SMEs’ bearing tied with their non-effect attitude in environmental discourse posit a potential overwhelming environmental effect by SMEs, discretely and jointly.

Sustainable development is a recent global environmental phenomenon which is underpinned by three primary dimensions, namely economic, environmental and ecological [13]. The concept of sustainable development has been defined primarily from Brundtland’s perspective [13]. According to the Brundtland commission, sustainable development pertains to development that transpires without jeopardizing the developmental potential of the upcoming generations [14]. Prominently, sustainable development has been deemed as attaining a balance of economic, social and environmental goals. In the context of business, there is an ongoing research concerning how businesses respond towards attaining this equilibrium. This study aims to investigate the extent of contribution made by normative environments within a country to explain how firms, particularly SMEs react in the face of sustainable development. Broadly, institutional forces are argued to impact any organisational field and are very instrumental in explaining transformations that occur in macro-environments [15]. Some latent literature suggests that organisations, through coercive pressures, can be pressured towards adopting sustainability practices [16,17,18]. Others suggest that mimetic pressures i.e., through copying each other, is the other way in which organisations adapt when exposed to new environmental variables [19,20]. However, there are limited studies that have sought to establish to what extent is the adoption of sustainable development a matter of professionalism and normative configurations. Normative configuration is concomitant of moral and professional forces that influence the behaviour of firms in responding towards environmental factors [21,22].

2. Literature Review

2.1. Normative Configuration

Normative configuration is the reinforcement and diffusion of behavioural norms within an industry that prescribes legitimacy of firms to operate within that particular industry and comes as a result of firms interacting [23,24]. Normative isomorphism under the theory of institutional organisational isomorphism has been utilised in latent literature to describe the forces that transpire when normative configuration is at play [24,25,26]. Basically, two mechanisms, namely professional networks and formal education, are observed as major contributing mechanisms with regards to normative isomorphism. Industries are identified with forces of professionalisation which basically prescribe acceptable norms and behaviours which are collectively shared by members and define the state of affairs, methods of work and legitimacy in a given industry [24]. González [25] notes that the growth of professional networks spanning organisations and the formal education from university specialists and institutions providing professional training are critical in producing organisational behavioural norms.

It is acknowledged that normative mechanisms of isomorphism are a result of normative institutions which introduce prescriptive, evaluative and obligatory aspects within a society which determine choice-making [26]. For instance, professional associations are critical normative forces which prescribe authentication mechanisms in the form of a set of rules and norms. The legitimisation power held by professional associations is enshrined in their provision of self-regulation prescribed in codes of conduct, licensing and certification requirements. Consequently, this influences the behaviour of firms belonging to a particular industry or society. Under normative isomorphism, moral values determine legitimacy, and these should be found in the codes of conduct, licensing and certification requirements [27].

The professionalism of employees within an industry is one other critical factor observed to invoke commonalities which lead to normative configuration. As firms seek to achieve superior performance, standards of professionalism and professional practice are increased for employees. Consequently, members belonging to a particular profession share ideas and inherit techniques that are regarded by the professional group to be updated and effective. Thus, these interactions among members of the same profession institute and reinforce practices which are held to be acceptable and legitimate within the given profession. This results in homogeneous perceptions, behaviours and practices in the form of normative isomorphism [28]. In line with normative isomorphism, a study by Gretzinger et al. [29] found that SMEs in Denmark and Germany utilised professional consultancy and cooperated with their counterparts in developing new products.

2.2. Sustainable Development

The concept of sustainability is allied and habitually traded in literature with notions like corporate social responsibility (CSR) and business sustainability [23,30]. Together these concepts continuously draw consideration in contemporary business research works as well as well as corporate boardrooms [30,31]. The declaration by World Commission on Environment and Development (WCED) specifies that sustainable development entails attaining progress that concurrently encapsulates lasting economic, societal and ecological values and goals [32]. Accordingly, from the firms’ perspective, sustainable development attainment means that they have a duty to apply these values (economic success, societal welfare and environmental advancement) in their offerings, procedures and strategies. However, antagonism transpires in different sectors of the business world pertaining to the sustainability philosophy which entails equating the three primary dimensions of sustainability (environmental, social and economic). Herein, the antagonists’ argument is that environmental integrity and social equity stand in conflict with economic prosperity [32].

The idea of value creation is at the centre of the economic sustainability dimension and is simplified as prices exceeding costs. Jamali and Mirshak [33] indicate that economic sustainability is progressively assumed to denote producing added value in a comprehensive manner, relative to traditional financial accounting approaches. Economic sustainability considers the longevity of a firm and research propounds that there has been a decline in corporate life-span due to heightened competition and notion of creative destruction [34]. Consistently, the dimension of economic sustainability refers to the elements of the firm that need to be upheld in order to continue in the market in the long run [35]. Literature purports the existence of a business case for SMEs to venture into sustainability practices which can be as a result of normative configuration whereby firms deem that it a good practice to balance environmental and social initiatives together with economic goals [36]. Furthermore, the influence of normative pressures has emanated from the recognition of the vitality of businesses in the wider society to the extent that institutions of tertiary education are widening their attention towards sustainability as part of their curriculum [37]. Thus, graduates from various disciplines are entering the business world possessing knowledge and training on sustainability together with related fields such as business ethics and corporate social responsibility [37]. The expected impact of normative configuration of firms towards sustainability adoption is therefore profound. Contrarily, normative configuration can potentially work in opposition to economic sustainability. Consultants, who are a vital aspect of the normative system, play a critical role in mediating the link between the fields and firms [15]. Latent literature indicates that the embeddedness of consultants and firms within similar systems constrains the potential of firms to generate innovations and creative ideas which are paramount to economic sustainability [15]. Accordingly, the following hypothesis has been posited:

H1:

Perceived normative pressures are significantly and positively related to social sustainability of SMEs.

Environmental sustainability by businesses concerns aiming at minimising the magnitude of their green footmark [32]. In the past decade global industrial production has enlarged by over 100-times and it is expected that this output will consume 50% of available resources and produce a 20% increase of the current carbon dioxide level [38]. The world population is expected to double from 5.5 billion to 11 billion by 2030 and sustainability concerns such as loss of biodiversity, waste and deforestation are increasing [39]. In this regard, Martinez-Conesa et al. [35] emphasise that as far as the environmental dimension is concerned, preserving the environment and enhancing the issue of environmental performance are central with regards to sustainability issues. From the 1960s through to the inception of the 1970s, interests regarding firms’ responsibility in pollution and environmental protection were ignited [40]. It is argued that SMEs are the leading contributors towards carbon dioxide emissions, pollution and commercial wastes [41]. Comparatively, normative institutions have been found to impose enormous sway towards the embracing of sustainable environmental practices by various large corporations and their subsidiaries [42]. More specifically, a qualitative study in Pakistan established that normative forces had a strong influence towards the adoption of good environmental practices by SMEs within the leather industry [43]. In this regard, normative mechanisms and professionalisation that transpire around SMEs have the potential to increase their environmental sustainability responsiveness [36]. Herein, the following hypothesis has been formulated:

H2:

Perceived normative pressures are significantly and positively related to environmental sustainability of SMEs.

On the other hand, social sustainability encompasses three dimensions, explicitly, environmental measurement, stakeholder monitoring and social concerns monitoring [44]. Initially, environmental measurement embroils businesses appraising social-economies and environmental concerns and responding appropriately. Moreover, stakeholder management concerns businesses responding to outer societal entities and their surroundings. Social sustainability entails the creation and dissemination of value for the stakeholders by businesses in an equitable manner. Last but not least, social management focuses on social concerns, inter alia, abstaining from the utilisation of juvenile labour, not creating socially detrimental products and services and not performing in unprincipled activities [45]. Social sustainability aspires to minimise disparities that transpire on demographic substantive issues such as inequalities in cultural disparities [39]. The concept of legitimacy that is embedded in the theory of institutional theory is equated to the principle of “social contract” that transpires between a firm and the society [36]. While legitimacy has been originally regarded as a matter of survival, lately it has been deemed as a matter of aligning with views, behaviours and actions that emanate from the societal norms and values [15]. Herein, firms get to adopt social activities due to cultural and not political forces within the society which anticipate businesses making contributions towards the society with managers and owners of SMEs having convictions to be generous towards the needs of societies [36]. As such, the following hypothesis has been put forward:

H3:

Perceived normative pressures are significantly and positively related to economic sustainability of SMEs.

Commonly, when measuring sustainable development researchers choose and enumerate indicators that pertain to each of the dimensions of sustainable development, namely economic, environmental and social [46]. These three scopes of sustainable development have been regarded in many studies as crucial measurement parts for firms that need to be involved in sustainable practices [47]. Sustainability indicators can be categorised into process-based or product-based [48]. In this case, process-based indicators are regarded as sustainability practices or antecedents. On the other hand, product-based indicators refer to sustainability performances or outcomes. Sustainability indicators can be derived from any area of sustainability such as environmental aspects (biodiversity, air and water pollution, energy, recycling), working conditions issues (health and safety, training, education) as well as human rights matters (e.g., child labour, discrimination) [48]. To measure sustainable development, scales utilised in past studies [47,48,49] were adopted in this study. Appendix A contains the specific questionnaire items.

3. Research Methodology

The positivism paradigm used for the study at hand is fostered within the premises of the positivism epistemic stance. Herein, positivism is defined as a paradigm whereby facts get to be clearly definite and results can be measured. Ontologically, the objectivism position and the main rationale for selecting this viewpoint is that the knowledge required is about sustainable development and normative pressures is regarded as an external social reality which needs to be considered as an objective reality [50]. The research utilised a quantitative research methodology using the survey research technique and a standardised self-administered questionnaire was utilised. Person-to-person drop-off and electronic mail (e-mail) methods were employed in administering the questionnaire. A questionnaire primarily comprising 5-point Likert scale style of questionnaire items operationalised on previous academic works was utilised in this study. Likert scales are deemed to be highly reliable and result in massive quantities of data as compared to other forms of scales. They are also relatively quick and easy to formulate [51].

The study area for this research was the north-eastern province of South Africa, Limpopo Province which is on the periphery of South Africa, marking the borders with Botswana, Mozambique and Zimbabwe. Limpopo is the fifth largest province of South Africa, encompassing 125,754 square kilometers and 5,404,868 people [52]. Non-probability sampling was utilised and this choice was mainly based on the practicality of the given sampling techniques. The absence of a reliable population listing or sampling frame automatically discredits the use of probability sampling. Probability sampling is often preferred to non-probability sampling due to the representativeness of the sample to its population [53]. However, non-probability sampling is often the only option when the population cannot be reasonably ascertained.

The aspect of sample size determination has been a highly contentious subject within the structural equation modelling (SEM) community [54,55]. Westland [54] argues that although the utilisation of SEM in research is significantly increasing, the subject of sample size determination remains a serious vexation amongst SEM-based studies. However, sample elements of 30 to 500 are reckoned apt for the common use in most researches [56]. Other researchers argue that in SEM, sample sizes should be sum of latent variables multiplied by 10, which is regarded to be inadequate in certain sections of research [54,55]. Thus, they suggest that the use of a ratio r which is calculated by looking at the number of measured items divided by the total number of constructs. Herein, with 26 items being measured at the hand of 3 constructs, the r would be 8. These researchers then argue that for an r equal to 5, the minimum sample size should be 150. Whilst, for r = 2 the minimum sample size should be 400, when r = 3 the minimum sample is 200 and when r = 12 a sample size of at least 50 is deemed appropriate [54].

For data analysis, the structural equation modelling (SEM) approach was utilised because it simultaneously assesses regression paths, thereby making it superior to traditional modes of analysis such as regression, ANOVA and correlation analysis. SEM was applied using the prominent two-staged technique constituting measurement and structural model. The measurement model was conducted through confirmatory factor analysis (CFA) and structural model was instrumental for path analysis. Exploratory factor analysis (EFA) was conducted as well as preliminary assessments constituting measures of normality, outliers and missing values. Data analysis also constituted assessments for validity and reliability. Data obtained from the survey was entered and analysed at the hand of the Statistical Package for Social Sciences (SPPS) (IBM, New York, NY, USA) Version 24.0 and AMOS (IBM, New York, NY, USA) version 24.0. SPSS was utilised to conduct descriptive statistics as well as preliminary analysis. Prior to conducting SEM, preliminary data analysis was conducted on assessments of missing values, outliers and normality.

4. Results

The survey was originally conducted by distributing 400 questionnaires, with 246 being received for data-capturing, totaling to an initial response rate of 61.5%. The received questionnaires were further subjected to data cleaning whereby some more questionnaires were dropped primarily for inadequate responses and 222 entries were in the end utilised. Thus, the eventual ultimate survey response ratio was 55.5%. Of these respondents, Table 1 reveals that largely males (53%), in the age category of 31–40 years (40%) as well as owners and not managers (55%) largely dominated the sample. On the other hand, firms that were surveyed in the sample predominantly had 6–20 employees (43%) and were based in urban areas (80%). Finally, the sample was comprised of small businesses that were from the retail and wholesale sector (41%), with other sectors contributing smaller percentages.

Table 1.

Demographics and firms’ characteristics.

4.1. Preliminary Analysis

Little’s missing completely at random (MCAR) assessment was performed through SPSS and an insignificant outcome was established for each construct reflecting that the missing values were missing not at random (MNAR) [57]. The expectation–maximisation method was utilised to address the missing values because of its merits of sufficiently estimating the missing values in a non-normal data distribution. Outliers were assessed using boxplots and stem and leaf diagrams. Outliers that transpired on more than one questionnaire item were completely removed from the data. Normality of the data was ascertained through the absolute values of skewness and kurtosis for each observed variable. The data in the study was deemed normal since all the values were within the range of −2 and +2 [58]. After these assessments, the eventual sample size of 222 was utilised for further analysis in SEM. In EFA, some of the questions from the questionnaire that seldom loaded impeccably on a single construct were dropped in further analysis. Table 2 displays the outcomes of normality assessments, descriptive analysis, as well as the outstanding questionnaire items which were lastly involved in the model from EFA per each observed variable.

Table 2.

Descriptive statistics and normality tests.

4.2. Measurement Model

The standardised loadings (SFLs) for all items reflect on adequacy of the measures on their respective constructs (see Table 2). All the SFLs surpass the acclaimed cut-off rate of 0.50 with the majority of them exceeding 0.70, thus signifying satisfactory internal consistency [59]. As reflected in Table 3, reliability was established through Cronbach’s alpha (CRa) and composite reliability (CR) statistics. The results show that all values of CRa and CR were above the acclaimed threshold 0.70 [60] to substantiate the reliability for the study. Convergent validity was ascertained through AVE values and accordingly, the values were above the recommended 0.5 [61]. Divergent validity was determined using construct correlations and square root of AVE contrasted. The results were satisfactory as shown by the inter-construct correlations that were all below 0.8 and the square root of AVE values being higher than the relative inter-construct correlation coefficients.

Table 3.

Reliability, validity and model adequacy.

Having satisfied the above prerequisites for SEM, CFA was then performed through AMOS version 24 software and satisfactory factor loadings on the entire unobservable variables. The model fitness indices were indicative for further respecification, and evaluation of standardised residuals revealed that one observable variable (Env4) pertaining to the environmental sustainability latent variable had poor residual values (3.016 and 2.666) which were beyond the prescribed threshold of within ±2.58 values [62]. Thus, it was dropped for potential fitness problems in the subsequent model which eventually had a significant chi-square (chi-square = 263.118) signifying a poor model fit. However, the chi-square is deemed to be significant on large sample sizes of over 200 elements. Nevertheless, the other fit indices NFI = 0.948, CFI = 0.923, TLI = 0.916, SRMR = 0.049, RMSEA = 0.085 and the chi-square/df = 2.530 dictate acceptable good fitness.

4.3. Structural Equation Modelling

The outcomes of SEM analysis which reviewed the goodness of fit indices reflected acceptable model fit to the data, irrespective of the poor chi-square fitness results (chi-square = 548.657). As suggested, the chi-square is vulnerable to huge samples that surpass 200 elements [62]. However, other fit indices signified acceptable model fitness, thus, GFI = 0.864, NFI = 0.932, CFI = 0.936, TLI = 0.907, AGFI = 0.887, RMSEA = 0.087, SRMR = 0.0602, chi-square/df = 2.267.

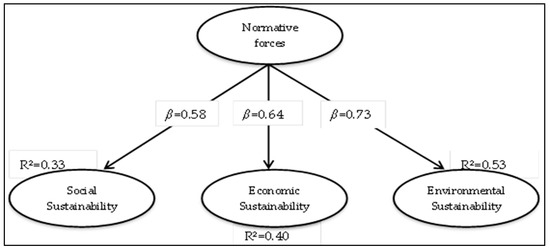

The R-squared (R2) measurements (as presented in Figure 1) depict variance explained relating to the model capability in envisaging the dependent or exogenous variables. The R2 statistics for the dependent constructs, namely economic (0.40), environmental (0.53) and social sustainability (0.33), signify suitability of the model utilised in predicting the exogenous variables. Table 4 illustrates the research hypotheses formulated relating to the endogenous latent (normative) and exogenous latent (economic, environmental and social) variables were found to positively significant according to the structural model diagrammatically outlined in Figure 1.

Figure 1.

Structural model.

Table 4.

Results of hypotheses testing using standardised estimates.

To evaluate the path coefficients of the hypothesised relationships, the standardised regression weights were utilised. The results of SEM reflected that path coefficients for normative isomorphic pressures and social (0.577, p < 0.001), environmental (0.728, p < 0.001) as well as economic (0.636, p < 0.001) sustainable development practices were all found to be significant and positive. Thus, altogether the hypotheses that were formulated in this study were confirmed by the data when subjected to testing at an alpha significance level of 0.05. Based on the high path coefficients from the SEM analysis, there is resounding evidence to suggest that the normative environmental factors would go along in being a motive and a driver towards the active participation of SMEs in sustainability. This finding supports studies by Perez-Batres [63] and González [25] which established that elements such as business publications, training and development at business schools and other educational venues contribute to homogenisation behaviours within an organisational field. The contribution of these factors emanates from their consistency with cultural support for the norms and values of CSR which are closely related to sustainable development. According to González [25] firms are prone to respond in a sustainable manner if they are members of trade or employer associations structured in a manner that encourages sustainable behaviour. However, as far as environmental sustainability is concerned, these findings contradict findings in studies by Jalaludin et al. [64] and Jamil et al [17] which established that normative pressures did not affect environmental management.

5. Conclusions

Overall, the study investigated the extent of normative configuration in sustainable development practices of SMEs in South Africa. The empirical results established that normative forces have a significant and positive relationship with economic, environmental and social sustainability practices. Thus, normative isomorphic pressures significantly and positively influenced all the types of sustainable development practices in this study. This means that the more normative pressures existed, the more firms were bound to adopt economic, environmental as well as social sustainable development practices. Factors that are found under normative pressures, such as sustainable development education, networks, trainings, professionalisation and ethics are critical towards making SMEs become more sustainable in their behaviours. This suggests that normative pressures have a significant role to play in configuring SMEs towards sustainable development practices. Contrary to popular belief that SMEs are reluctant to practice sustainable development and fully venture into sustainability issues, this study presents fresh and exciting findings [11,12]. The study shows that normative configuration is essential in ensuring the spread of sustainable development practices amongst SMEs. The study clarifies and presents how there is a consistency in the way in which SMEs are influenced by normative forces similar to large corporations in the adoption of sustainability practices [42].

Furthermore, in line with normative isomorphism, a study by Gretzinger et al. [29] found that SMEs in Denmark and Germany utilised professional consultancy and cooperated with their counterparts in developing new products. Today, one of the strategies used is rather to co-operate than to compete with contestants in the industry, as a way of gaining economic performance. By so doing, firms form regional clusters along social proximity where they share resources and knowledge thereby increasing their survival [65]. Isomorphism suggests that organisational fields or industries follow an evolutionary path from diversity to homogeneity. Research by González, [25] and Cheng and Yu [65] found that isomorphic forces occupy a significant protagonist position in sustainability practices for SMEs. Thus, according to the results established in this study, small firms are expected to be utilising uniform strategies as they are shaped by similar forces.

With increasing calls for firms to become active in sustainable development aspects, the study stands to contribute towards the discourse of sustainable development theoretically and practically. Whilst numerous trends have marked several dispensations in the history of commerce across the world, the sustainable development discourse seems to be perpetual in nature with its prominence poised to gather momentum in the future. The need for training and development, professionalism, values and norms within the discourse will be at the centre of sustainability across industries. In this regard, this study is pre-emptive, and the findings are indicative of the benefits of normative configuration in the discourse. Thus, findings of this study can be referenced as justification of how normative configuration influences adoption of sustainable development. For theory, the study presents a holistic approach towards the concept of sustainable development. Most studies that have investigated sustainable development dimensions, namely economic, environmental and social, have taken an individualistic and disaggregated approach. This is contradictory to the spirit and values of the sustainable approach which requires that an integrative approach be utilised.

Furthermore, there are some grassroot sentiments embedded in the findings of this study which have implications for policy and strategy formulation. Policy-makers need to be cognisant of the vital role played by normative configuration in sustainable development as echoed in this study. The relationship between normative forces and sustainable development practices that has been established in this study indicate that governments and policy-makers need to prioritise the increase of training facilities in order to enhance the involvement of SMEs in sustainable development. In this regard, future studies can be conducted to investigate which specific normative configuration factors have an impact on sustainable development practices by firms. Also, research can be conducted in the future to ascertain the same problem with large businesses which will significantly give impetus to the direction suggested in this study. The major weakness of this study is the geographical limitation and the lack of consideration towards specificities of SMEs. This study considered SMEs in general and there is a need to streamline research pertaining to the different characteristics of SMEs such as age, type and location.

Funding

This research received no external funding.

Acknowledgments

The researcher offers recognition to the University of Limpopo for financial assistance received for the publication costs of this research paper.

Conflicts of Interest

The author declares no conflict of interest.

Appendix A. Questionnaire Items

Table A1.

Indicate the degree of your agreement to the following statements on a scale of 1 = Strongly Disagree and 5 = Strongly Agree.

Table A1.

Indicate the degree of your agreement to the following statements on a scale of 1 = Strongly Disagree and 5 = Strongly Agree.

| Normative Pressures Our Sustainable Development Practice are Because… | |||||

|---|---|---|---|---|---|

| sustainable business practices have been widely adopted by our suppliers currently | 1 | 2 | 3 | 4 | 5 |

| sustainable business practices are widely adopted by our customers currently | 1 | 2 | 3 | 4 | 5 |

| sustainable business practices are widely adopted by our competitors currently | 1 | 2 | 3 | 4 | 5 |

| our employees consider sustainability as part of their professionalism. | 1 | 2 | 3 | 4 | 5 |

| sustainable practices are provided to us as part of training in our industry | 1 | 2 | 3 | 4 | 5 |

| Ecologically we… | |||||

| focus on environmental issues | 1 | 2 | 3 | 4 | 5 |

| efficiently utilise available resources | 1 | 2 | 3 | 4 | 5 |

| continuously monitor environmental issues | 1 | 2 | 3 | 4 | 5 |

| prioritise recycling, reusing or reduction of waste | 1 | 2 | 3 | 4 | 5 |

| efficiently use energy | 1 | 2 | 3 | 4 | 5 |

| focus on renewable energy | 1 | 2 | 3 | 4 | 5 |

| replace harmful chemicals or materials with less hazardous alternatives | 1 | 2 | 3 | 4 | 5 |

| follow prescriptions by Environmental Management Agency disposal. | 1 | 2 | 3 | 4 | 5 |

| Economically we… | |||||

| place emphasis on efficiency and productivity | 1 | 2 | 3 | 4 | 5 |

| strive to survive in the industry | 1 | 2 | 3 | 4 | 5 |

| regard saving money as important for the business. | 1 | 2 | 3 | 4 | 5 |

| adhere to tax requirements | 1 | 2 | 3 | 4 | 5 |

| offer products and services that are essential for the customers | 1 | 2 | 3 | 4 | 5 |

| prioritise long-term profitability regardless of short-term losses | 1 | 2 | 3 | 4 | 5 |

| Socially we… | |||||

| put regard on current activities in the society | 1 | 2 | 3 | 4 | 5 |

| prioritise the welfare of our surrounding communities | 1 | 2 | 3 | 4 | 5 |

| provide entitlements to workers. | 1 | 2 | 3 | 4 | 5 |

| promote gender equality | 1 | 2 | 3 | 4 | 5 |

| promote equity and safety of the community. | 1 | 2 | 3 | 4 | 5 |

| contribute towards improvement of educational status | 1 | 2 | 3 | 4 | 5 |

| uphold civil and human rights of individuals | 1 | 2 | 3 | 4 | 5 |

References

- Eze, U.C.; Goh, G.G.G.; Goh, C.Y.; Tan, T.T. Perspectives of SMEs on knowledge sharing. VINE 2013, 43, 210–236. [Google Scholar]

- Asamoah, E.S. Customer based brand equity (CBBE) and the competitive performance of SMEs in Ghana. J. Small Bus. Enterp. Dev. 2014, 21, 117–131. [Google Scholar] [CrossRef]

- European Union 2015. User Guide to the SME Definition. Available online: https://ec.europa.eu/regional_policy/sources/conferences/state-aid/sme/smedefinitionguide_en.pdf (accessed on 12 July 2017).

- Abor, J.; Quartey, P. Issues in SME Development in Ghana and South Africa. Int. Res. J. Financ. Econ. 2010, 39, 218–228. [Google Scholar]

- Vegholm, F. Relationship marketing and the management of corporate image in the bank-SME relationship. Manag. Res. Rev. 2011, 34, 325–336. [Google Scholar] [CrossRef]

- Rodríguez-Gutiérrez, M.J.; Moreno, P.; Tejada, P. Entrepreneurial orientation and performance of SMEs in the services industry. J. Organ. Chang. Manag. 2015, 28, 194–212. [Google Scholar] [CrossRef]

- Wang, Y. What are the biggest obstacles to growth of SMEs in developing countries? An empirical evidence from an enterprise survey. Borsa Istanb. Rev. 2016, 16, 167–176. [Google Scholar] [CrossRef]

- Revell, A.; Blackburn, R. The business case for sustainability? An examination of small firms in the UK’s construction and restaurant sectors. Bus. Strategy Environ. 2007, 16, 404–420. [Google Scholar] [CrossRef]

- Marika, A.; Giovanni, A. A process-based operational framework for sustainability reporting in SMEs. J. Small Bus. Enterp. Dev. 2012, 19, 669–686. [Google Scholar]

- Masocha, R. Delineating Small Businesses’ Performance from a Contemporary Sustainable Development Approach in South Africa. Acta Univ. Danubius. 2018, 14, 192–206. [Google Scholar]

- Musa, H.; Chinniah, M. Malaysian SMEs Development: Future and Challenges on Going Green. Procedia Soc. Behav. Sci. 2016, 224, 254–262. [Google Scholar] [CrossRef]

- Ghazilla, R.A.R.; Sakundarini, N.; Abdul-Rashid, S.H.; Ayub, N.S.; Olugu, E.U.; Musa, S.N. Drivers and barriers analysis for green manufacturing practices in Malaysian SMEs: A Preliminary Findings. Procedia Cirp. 2015, 26, 658–663. [Google Scholar] [CrossRef]

- Lele, S.M. Sustainable development: A critical review. World Dev. 1991, 19, 607–621. [Google Scholar] [CrossRef]

- Green, K.W.; Toms, L.C.; Clark, J. Impact of market orientation on environmental sustainability strategy. Manag. Res. Rev. 2015, 38, 217–238. [Google Scholar] [CrossRef]

- Glover, J.L.; Champion, D.; Daniels, K.J.; Dainty, A.J.D. An Institutional Theory perspective on sustainable practices acrossthe dairy supply chain. Int. J. Prod. Econ. 2014, 152, 102–111. [Google Scholar] [CrossRef]

- Joseph, C.; Taplin, R. Local government website sustainability reporting: A mimicry perspective. Soc. Responsib. J. 2012, 8, 363–372. [Google Scholar] [CrossRef]

- Jamil, C.Z.M.; Mohamed, A.A.; Muhammad, F.; Ali, A. Environmental management accounting practices in small medium manufacturing firms. Procedia Soc. Behav. Sci. 2015, 172, 619–626. [Google Scholar] [CrossRef]

- Zhu, Q.; Sarkis, J. The moderating effects of institutional pressures on emergent green supply chain practices and performance. Int. J. Prod. Res. 2007, 45, 4333–4355. [Google Scholar] [CrossRef]

- Diabat, A.; Govindan, K. An analysis of the drivers affecting the implementation of green supply chain management. Resour. Conserv. Recycl. 2011, 55, 659–667. [Google Scholar] [CrossRef]

- Martínez-Ferrero, J.; García-Sánchez, I. Coercive, normative and mimetic isomorphism as determinants of the voluntary assurance of sustainability reports. Int. Bus. Rev. 2017, 26, 102–118. [Google Scholar] [CrossRef]

- Di Maggio, P.J.; Powell, W.W. The Iron Cage Revisited: Institutional Isomorphism and Collective Rationality in Organisational Fields. Am. Sociol. Rev. 1983, 48, 147–160. [Google Scholar] [CrossRef]

- Masocha, R.; Fatoki, O. The Role of Mimicry Isomorphism in Sustainable Development Operationalisation by SMEs in South Africa. Sustainability 2018, 10, 1264. [Google Scholar] [CrossRef]

- Wu, T.; Daniel, E.M.; Hinton, M.; Quintas, P. Isomorphic mechanisms in manufacturing supply chains: A comparison of indigenous Chinese firms and foreign-owned MNCs. Supply Chain Manag. Int. J. 2013, 18, 161–177. [Google Scholar] [CrossRef]

- González, J.M.G. Determinants of socially responsible corporate behaviours in the Spanish electricity sector. Soc. Responsib. J. 2010, 6, 386–403. [Google Scholar] [CrossRef]

- Kshetri, N. The development of market orientation: A consideration of institutional influence in China. Asia Pac. J. Mark. Logist. 2009, 2, 19–40. [Google Scholar] [CrossRef]

- Wahid, F.; Sein, M.K. Institutional entrepreneurs. Transform. Gov. People Process Policy 2013, 7, 76–92. [Google Scholar] [CrossRef]

- Chiang, C. Insights into current practices in auditing environmental matters. Manag. Audit. J. 2010, 25, 912–933. [Google Scholar] [CrossRef]

- Gretzinger, S.; Hinz, H.; Matiaske, W. Cooperation in Innovation Networks: The Case of Danish and German SMEs. Manag. Rev. 2010, 21, 193–216. [Google Scholar] [CrossRef]

- Windolph, S.E.; Schaltegger, S.; Herzig, C. Implementing corporate sustainability: What drives the application of sustainability management tools in Germany? Sustain. Account. Manag. Policy J. 2014, 5, 378–404. [Google Scholar] [CrossRef]

- Thiel, M. Unlocking the social domain in sustainable development. World J. Sci. Technol. Sustain. Dev. 2015, 12, 183–193. [Google Scholar] [CrossRef]

- Galpin, T.; Whittington, J.L.; Bell, G. Is your sustainability strategy sustainable? Creating a culture of sustainability. Corp. Gov. 2015, 15, 1–17. [Google Scholar] [CrossRef]

- Jamali, D.; Mirshak, R. Corporate Social Responsibility (CSR): Theory and Practice in a Developing Country Context. J. Bus. Ethics 2007, 72, 243–262. [Google Scholar] [CrossRef]

- Wilson, J.P. The triple bottom line. Int. J. Retail. Distrib. Manag. 2015, 43, 432–447. [Google Scholar] [CrossRef]

- Martinez-Conesa, I.; Soto-Acosta, P.; Palacios-Manzano, M. Corporate social responsibility and its effect on innovation and firm performance: An empirical research in SMEs. J. Clean. Prod. 2017, 142, 2374–2383. [Google Scholar] [CrossRef]

- Roszkowska-Menkesa, M.; Aluchna, M. Institutional Isomorphism and Corporate Social Responsibility: Towards A Conceptual Model. J. Posit. Manag. 2017, 8, 3–16. [Google Scholar] [CrossRef]

- Sherif, S.F. The Role of Higher Education Institutions in Propagating Corporate Social Responsibility Case Study: Universities in the Middle East. Int. J. Educ. Res. 2015, 3, 217–226. [Google Scholar]

- Gomes, C.M.; Kneipp, J.M.; Kruglianskas, I.; da Rosa, L.A.B.; Bichueti, R.S. Management for sustainability: An analysis of the key practices according to the business size. Ecol. Indic. 2015, 52, 116–127. [Google Scholar] [CrossRef]

- Sen, S.K. Symbiotic linkage of sustainability, development and differentiation. Compet. Rev. 2014, 24, 95–106. [Google Scholar]

- Stubblefield Loucks, E.; Martens, M.L.; Cho, C.H. Engaging Small- and Medium-sized Businesses in Sustainability. Sustain. Account. Manag. Policy J. 2010, 1, 178–200. [Google Scholar] [CrossRef]

- Baden, D.A.; Harwood, I.A.; Woodward, D.G. The effect of buyer pressure on suppliers in SMEs to demonstrate CSR practices: An added incentive or counterproductive? Eur. Manag. J. 2009, 429–441. [Google Scholar] [CrossRef]

- Bijkerk, D. Environmental CSR and Sustainable Initiatives: The Underlying Mechanisms of Isomorphic Pressures. Master’s Thesis, University of Amsterdam, Amsterdam, The Netherlands, 2016. [Google Scholar]

- Wahga, A.; Blundel, R.; Schaefer, A. Understanding the Drivers of Sustainable Entrepreneurial Practices in Pakistan’s Leather Industry: A Multi-Level Approach. Int. J. Entrep. Behav. Res. 2018, 24, 382–407. [Google Scholar] [CrossRef]

- Vallance, S.; Perkins, H.C.; Dixon, J.E. What is social sustainability? A clarification of concepts. Geoforum 2011, 42, 342–348. [Google Scholar] [CrossRef]

- Jӓmsӓ, P.; Tӓhtinen, J.; Ryan, A.; Pallari, M. Sustainable SMEs network utilization: The case of food enterprises. J. Small Bus. Enterp. Dev. 2011, 18, 141–615. [Google Scholar] [CrossRef]

- Zhou, L.; Keivani, R.; Kurul, E. Sustainability performance measurement framework for PFI projects in the UK. J. Financ. Manag. Prop. Constr. 2013, 18, 232–250. [Google Scholar] [CrossRef]

- Adebanjo, D.; Teh, P.; Ahmed, P.K. The impact of external pressure and sustainable management practices on manufacturing performance and environmental outcomes. Int. J. Oper. Prod. Manag. 2016, 36, 995–1013. [Google Scholar] [CrossRef]

- Gualandris, J.; Golini, R.; Kalchschmidt, M. Do supply management and global sourcing matter for firm sustainability performance? Int. Study Supply Chain Manag. Int. J. 2014, 19, 258–274. [Google Scholar] [CrossRef]

- Høgevold, N.M.; Svensson, G.; Klopper, H.B.; Wagner, B.; Valera, J.C.S.; Padin, C.; Ferro, C.; Petzer, D. A triple bottom line construct and reasons for implementing sustainable business practices in companies and their business networks. Corp. Gov. 2015, 15, 427–443. [Google Scholar] [CrossRef]

- Sachdeva, J.K. Business Research Methodology; Himalaya Publishing House: Mumbai, India, 2013; pp. 69–205. [Google Scholar]

- Cooper, D.R. ; Schindler. P. Business Research Methods, 10th ed.; Mcgraw-Hill: New York, NY, USA, 2008; pp. 564–626. [Google Scholar]

- StatsSA. Provincial Profile: Limpopo, Census 2011. Available online: http://www.statssa.gov.za/publications/Report-03-01-78/Report-03-01-782011.pdf (accessed on 18 May 2017).

- Bryman, A.; Bell, E. Research Methodology: Business and Management Contexts; Oxford University Press: Cape Town, South Africa, 2011; pp. 355–362. [Google Scholar]

- Westland, J.C. Lower bounds on sample size in structural equation modeling. Electron. Commer. Res. Appl. 2010, 9, 476–487. [Google Scholar] [CrossRef]

- Nicolaou, A.I.; Masoner, M.M. Sample size requirements in structural equation models under standard conditions. Int. J. Account. Inf. Syst. 2013, 14, 256–274. [Google Scholar] [CrossRef]

- Sekaran, U.; Bougie, R. Research Methods for Business: A Skill Building Approach, 5th ed.; John Wiley & Sons Ltd.: West Sussex, UK, 2009; pp. 103–135. [Google Scholar]

- Little, R.J.A.; Rubin, D.B. Statistical Analysis with Missing Data; John Wiley & Sons: New York, NY, USA, 1987. [Google Scholar]

- Tabachnick, B.; Fidell, L. Using Multivariate Statistics, 5th ed.; Pearson Education: Boston, MA, USA, 2007. [Google Scholar]

- Hair, J.; Hult, T.; Ringle, C.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM); Sage Publications, Inc.: Thousand Oaks, CA, USA, 2014. [Google Scholar]

- Chinomona, R.; Pretorius, M. SME Manufacturers’ Cooperation and Dependence on Major Dealers’ Expert Power in Distribution Channels. SAJEMS Ns 2011, 14, 170–187. [Google Scholar] [CrossRef][Green Version]

- Chin, W.W. The partial least squares approach to structural equation modelling. Mod. Methods Bus. Res. 1998, 295, 295–336. [Google Scholar]

- Byrne, B.M. Structural Equation Modelling with Amos-Basic Concepts, Applications and Programming, 2nd ed.; Taylor and Francis Group, LLC: New York, NY, USA, 2006. [Google Scholar]

- Perez-Batres, L.A.; Miller, V.V.; Pisani, M.J. Institutionalizing sustainability: An empirical study of corporate registration and commitment to the United Nations Global compact guidelines. J. Clean. Prod. 2011, 19, 843–851. [Google Scholar] [CrossRef]

- Jalaludin, D.; Sulaiman, M.; Ahmad, N.N.N.D. Understanding Environmental Management Accounting adoption: A New Institutional Sociology Perspective. Soc. Responsib. J. 2011, 7, 540–557. [Google Scholar] [CrossRef]

- Galbreath, J. To cooperate or compete? Looking at the climate change issue in the wine industry. Int. J. Wine Bus. Res. 2015, 27, 220–238. [Google Scholar] [CrossRef]

- Cheng, H.; Yu, C.J. Adoption of Practices by Subsidiaries and Institutional Interaction within Internationalised Small-and Medium-Sized Enterprises. Manag. Int. Rev. 2012, 52, 81–105. [Google Scholar] [CrossRef]

© 2019 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).