Cashless Transactions: A Study on Intention and Adoption of e-Wallets

,

,  ,

,  and

and

Abstract

1. Introduction

Context of the Adoption of e-Wallets in Indonesia

2. Literature Review

2.1. Theoretical Foundation

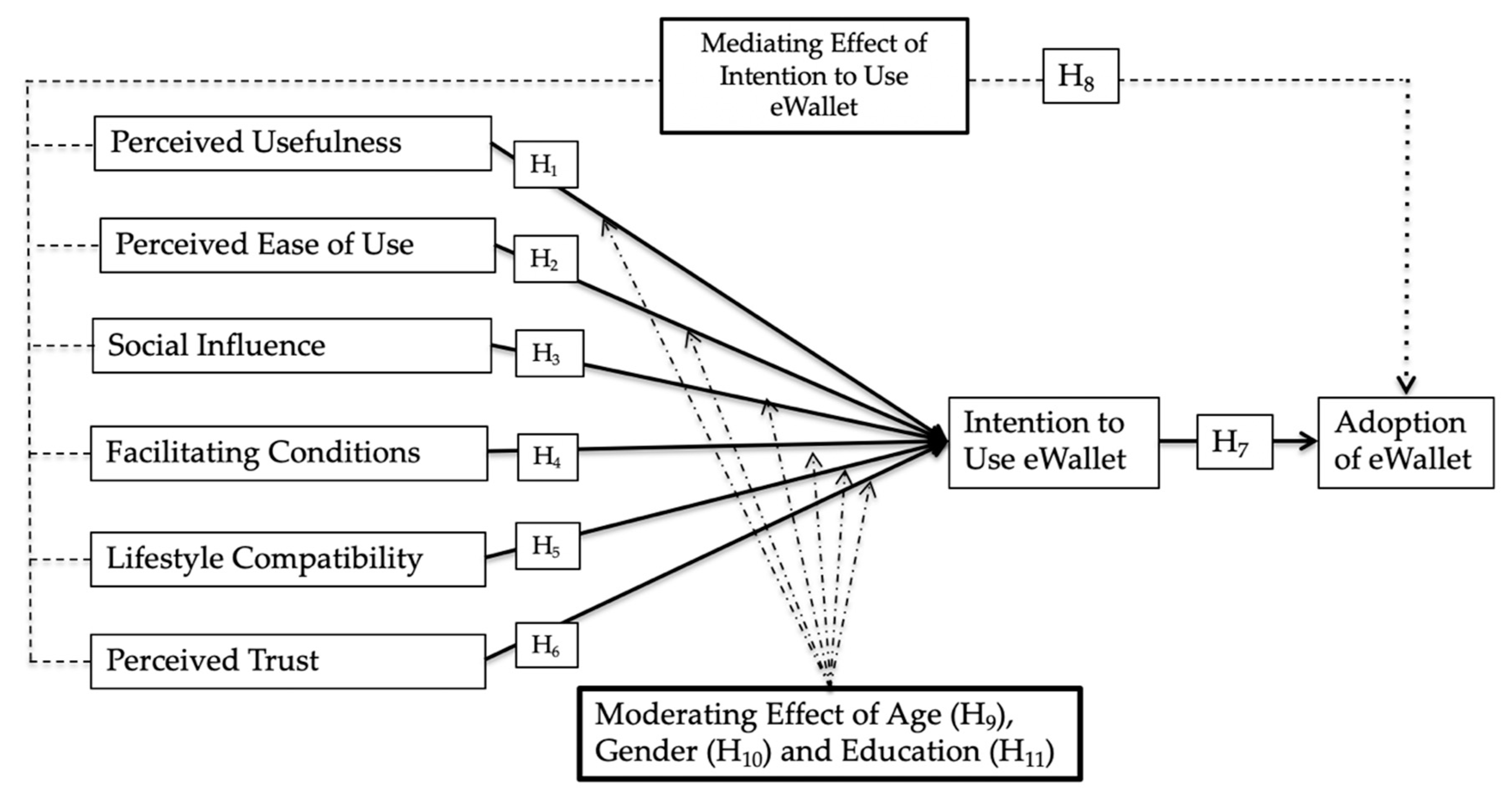

2.2. Factors Affecting Intention to Use e-Wallet

2.2.1. Perceived Usefulness

2.2.2. Perceived Ease of Use

2.2.3. Social Influence

2.2.4. Facilitating Conditions

2.2.5. Lifestyle Compatibility

2.2.6. Perceived Trust

2.2.7. Intention to Use an e-Wallet

2.3. Mediating Effect of Intention to Use e-Wallet

2.4. Moderating Effect of Age, Gender and Education

3. Research Methodology

3.1. Data Collection and Sample Design

3.2. Measurement and Scales

3.3. Data Analysis Method

4. Data Analysis

4.1. Demographic Characteristics

4.2. Validity and Reliability

4.3. Path Analysis

4.4. Mediation

4.5. Moderation

5. Discussion

6. Conclusions

7. Limitation

8. Future Research

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Bibri, S.E. The IoT for smart sustainable cities of the future: An analytical framework for sensor-based big data applications for environmental sustainability. Sustain. Cities Soc. 2018, 38, 230–253. [Google Scholar] [CrossRef]

- Capgemini. World Payment Report. 2019. Available online: https://worldpaymentsreport.com/wpcontent/uploads/sites/5/2019/09/World-PaymentsReport-WPR-2019.pdf (accessed on 2 April 2020).

- Li, C.; Mirosa, M.; Bremer, P.J. Review of Online Food Delivery Platforms and their Impacts on Sustainability. Sustainability 2020, 12, 5528. [Google Scholar] [CrossRef]

- Sohail, A.; Shobhit, A.; Saurabh, S.; Akhilesh, V.; Varma, C.P. Development of Advance Digital Mobile Wallet. Int. J. Sci. Res. Dev. 2018, 6, 2758–2760. [Google Scholar]

- Ganderbal, T. E-commerces; Department of Information Technology, Central University of Kashmir: Ganderbal, Kashmir, 2020; pp. 1–23. [Google Scholar]

- Suleman, D.; Zuniarti, I. Sabil Consumer Decisions toward Fashion Product Shopping in Indonesia: The effects of Attitude, Perception of Ease of Use, Usefulness, and Trust. Manag. Dyn. Knowl. Econ. 2013, 7, 133–146. [Google Scholar] [CrossRef]

- Rocha, V.; van Praag, M. Mind the gap: The role of gender in entrepreneurial career choice and social influence by founders. Strateg. Manag. J. 2020, 41, 841–866. [Google Scholar] [CrossRef]

- Widodo, M.; Irawan, M.I.; Sukmono, R.A. Extending UTAUT2 to Explore Digital Wallet Adoption in Indonesia. In Proceedings of the 2019 International Conference on Information and Communications Technology (ICOIACT), Yogyakarta, Indonesia, 24–25 July 2019; pp. 878–883. [Google Scholar]

- Belanche, D.; Flavián, M.; Pérez-Rueda, A. Mobile Apps Use and WOM in the Food Delivery Sector: The Role of Planned Behavior, Perceived Security and Customer Lifestyle Compatibility. Sustainability 2020, 12, 4275. [Google Scholar] [CrossRef]

- Soodan, V.; Rana, A. Modeling customers’ intention to use e-wallet in a developing nation: Extending UTAUT2 with security, privacy and savings. J. Electron. Commer. Organ. 2020, 18, 89–114. [Google Scholar] [CrossRef]

- Venkatesh, V.; Thong, J.Y.; Xu, X. Consumer acceptance and use of information technology: Extending the unified theory of acceptance and use of technology. MIS Q. 2012, 36, 157–178. [Google Scholar] [CrossRef]

- Statista McKinsey. Unlocking Indonesia’s Digital Opportunity. 2020. Available online: http://www.mckinsey.com/industries/consumer-packaged-goods/ourinsights/three-myths-about-growth-in-consumer-packaged-goods (accessed on 21 October 2020).

- Barata, A. Strengthening National Economic Growth and Equitable Income Through Sharia Digital Economy in Indonesia. J. Islam. Monet. Econ. Financ. 2019, 5, 145–168. [Google Scholar] [CrossRef]

- International Trade Administration. Indonesian E-Wallet Market-Digital Payments Are Trending Upward in Indonesia. Available online: https://www.trade.gov/market-intelligence/indonesia-e-wallet-market (accessed on 2 April 2020).

- Ajzen, I. The theory of planned behavior. Organ. Behav. Hum. Decis. Process. 1991, 50, 179–211. [Google Scholar] [CrossRef]

- Venkatesh, V.; Morris, M.G.; Davis, G.B.; Davis, F.D. User Acceptance of Information Technology: Toward a Unified View. MIS Q. 2003, 36, 425–478. [Google Scholar] [CrossRef]

- Rahi, S.; Mansour, M.M.O.; Alghizzawi, M.; Alnaser, F.M. Integration of UTAUT model in internet banking adoption context: The mediating role of performance expectancy and effort expectancy. J. Res. Interact. Mark. 2019, 13, 411–435. [Google Scholar] [CrossRef]

- Chandra, S.; Kumar, K.N. Exploring factors influencing organizational adoption of augmented reality in ecommerce: Empirical analysis using technology-organization-environment model. J. Electron. Commer. Res. 2018, 19, 237–265. [Google Scholar]

- Lim, F.-W.; Ahmad, F.; Talib, A.N.A. Behavioural Intention towards Using Electronic Wallet: A Conceptual Framework in the Light of the Unified Theory of Acceptance and Use of Technology (UTAUT). Imp. J. Interdiscip. Res. 2019, 5, 79–86. [Google Scholar]

- Ajmera, H.; Bhatt, V. Factors affecting the consumer’s adoption of E-wallets in India: An empirical study. Alochana Chakra J. 2020, 9, 1081–1093. [Google Scholar]

- Shankar, A.; Datta, B. Factors Affecting Mobile Payment Adoption Intention: An Indian Perspective. Glob. Bus. Rev. 2018, 19, S72–S89. [Google Scholar] [CrossRef]

- Lwoga, E.T.; Lwoga, N.B. User Acceptance of Mobile Payment: The Effects of User-Centric Security, System Characteristics and Gender. Electron. J. Inf. Syst. Dev. Ctries. 2017, 81, 1–24. [Google Scholar] [CrossRef]

- Liu, G.-S.; Tai, P.T. A Study of Factors Affecting the Intention to Use Mobile Payment Services in Vietnam. Econ. World 2016, 4, 249–273. [Google Scholar] [CrossRef]

- Intarot, P. Influencing Factor in E-Wallet Acceptant and Use. Int. J. Bus. Adm. Stud. 2018, 4, 167–175. [Google Scholar]

- Chawla, D.; Joshi, H. Role of Mediator in Examining the Influence of Antecedents of Mobile Wallet Adoption on Attitude and Intention. Glob. Bus. Rev. 2020. [Google Scholar] [CrossRef]

- Hamid, A.A.; Razak, F.Z.A.; Abu Bakar, A.; Abdullah, W.S.W. The Effects of Perceived Usefulness and Perceived Ease of Use on Continuance Intention to Use E-Government. Procedia Econ. Finance. 2016, 35, 644–649. [Google Scholar] [CrossRef]

- Grover, P.; Kar, A.K.; Janssen, M.; Ilavarasan, P.V. Perceived usefulness, ease of use and user acceptance of blockchain technology for digital transactions—insights from user-generated content on Twitter. Enterp. Inf. Syst. 2019, 13, 771–800. [Google Scholar] [CrossRef]

- Peng, S.; Yang, A.; Cao, L.; Yu, S.; Xie, D. Social influence modeling using information theory in mobile social networks. Inf. Sci. 2017, 379, 146–159. [Google Scholar] [CrossRef]

- Sarika, P.; Vasantha, S. Impact of mobile wallets on cashless transaction. Int. J. Recent Technol. Eng. 2019, 7, 1164–1171. [Google Scholar]

- Martins, C.; Oliveira, T.; Popovič, A. Understanding the Internet banking adoption: A unified theory of acceptance and use of technology and perceived risk application. Int. J. Inf. Manag. 2014, 34, 1–13. [Google Scholar] [CrossRef]

- Chaouali, W.; Ben Yahia, I.; Souiden, N. The interplay of counter-conformity motivation, social influence, and trust in customers’ intention to adopt Internet banking services: The case of an emerging country. J. Retail. Consum. Serv. 2016, 28, 209–218. [Google Scholar] [CrossRef]

- Hossain, M.A.; Hasan, M.I.; Chan, C.; Ahmed, J.U. Predicting User Acceptance and Continuance Behaviour Towards Location-based Services: The Moderating Effect of Facilitating Conditions on Behavioural Intention and Actual Use. Australas. J. Inf. Syst. 2017, 21, 1–22. [Google Scholar] [CrossRef]

- Tarhini, A.; Elyas, T.; Akour, M.A.; Al-Salti, Z. Technology, Demographic Characteristics and E-Learning Acceptance: A Conceptual Model Based on Extended Technology Acceptance Model. High. Educ. Stud. 2016, 6, 72. [Google Scholar] [CrossRef]

- Peñarroja, V.; Sánchez, J.; Gamero, N.; Orengo, V.; Abad, A.Z. The influence of organisational facilitating conditions and technology acceptance factors on the effectiveness of virtual communities of practice. Behav. Inf. Technol. 2019, 38, 845–857. [Google Scholar] [CrossRef]

- Lin, H.-F. An empirical investigation of mobile banking adoption: The effect of innovation attributes and knowledge-based trust. Int. J. Inf. Manag. 2011, 31, 252–260. [Google Scholar] [CrossRef]

- Shaw, N.; Sergueeva, K. The non-monetary benefits of mobile commerce: Extending UTAUT2 with perceived value. Int. J. Inf. Manag. 2019, 45, 44–55. [Google Scholar] [CrossRef]

- Herrero, A.; Perez, A.; Bosque, I.R. Values and lifestyles in the adoption of new technologies applying VALS scale. Acad. Mark. Stud. J. 2014, 18, 37–56. [Google Scholar]

- Hoque, M.Z.; Alam, M.N. What determines the purchase intention of liquid milk during a food security crisis? The role of perceived trust, knowledge, and risk. Sustainability 2018, 10, 3722. [Google Scholar] [CrossRef]

- Sullivan, Y.W.; Kim, D.J. Assessing the effects of consumers’ product evaluations and trust on repurchase intention in e-commerce environments. Int. J. Inf. Manag. 2018, 39, 199–219. [Google Scholar] [CrossRef]

- Kim, S.Y.; Kim, J.U.; Park, S.C. The Effects of Perceived Value, Website Trust and Hotel Trust on Online Hotel Booking Intention. Sustainability 2017, 9, 2262. [Google Scholar] [CrossRef]

- Wong, W.H.; Mo, W.Y. A Study of Consumer Intention of Mobile Payment in Hong Kong, Based on Perceived Risk, Perceived Trust, Perceived Security and Technological Acceptance Model. J. Adv. Manag. Sci. 2019, 7, 33–38. [Google Scholar] [CrossRef]

- Wijayanthi, I. Behavioral Intention of Young Consumers towards E-Wallet Adoption: An Empirical Study among Indonesian Users. Russ. J. Agric. Socio-Econ. Sci. 2019, 85, 79–93. [Google Scholar] [CrossRef]

- Fishbein, M.; Ajzen, I. Predicting and Changing Behavior; Psychology Press Taylor & Francis Group: New York, NY, USA, 2011. [Google Scholar]

- Nikou, S.A.; Economides, A.A. Computers & Education Mobile-based assessment: Investigating the factors that in fluence behavioral intention to use. Comput. Educ. 2017, 109, 56–73. [Google Scholar]

- Choi, Y.; Sun, L. Reuse Intention of Third-Party Online Payments: A Focus on the Sustainable Factors of Alipay. Sustainability 2016, 8, 147. [Google Scholar] [CrossRef]

- Xie, J.; Lin, R. Understanding the Adoption of Third-Party Online Payment: An Empirical Study of User Acceptance of Alipay in China. Master’s Thesis, Jönköping University, Jönköping, Sweden, 2014. Available online: https://www.diva-portal.org/smash/get/diva2:733072/fulltext01 (accessed on 22 November 2020).

- Hwang, J.; Kim, H. Consequences of a green image of drone food delivery services: The moderating role of gender and age. Bus. Strat. Environ. 2019, 28, 872–884. [Google Scholar] [CrossRef]

- Schmuck, D.; Matthes, J. How Anti-immigrant Right-wing Populist Advertisements Affect Young Voters: Symbolic Threats, Economic Threats and the Moderating Role of Education. J. Ethn. Migr. Stud. 2014, 41, 1577–1599. [Google Scholar] [CrossRef]

- Cai, Z.; Fan, X.; Du, J. Gender and attitudes toward technology use: A meta-analysis. Comput. Educ. 2017, 105, 1–13. [Google Scholar] [CrossRef]

- Pandey, S.; Chawla, D. Engaging m-commerce adopters in India: Exploring the two ends of the adoption continuum across four m-commerce categories. J. Enterp. Inf. Manag. 2019, 32, 191–210. [Google Scholar] [CrossRef]

- Karjaluoto, H.; Shaikh, A.A.; Leppäniemi, M.; Luomala, R. Examining consumers’ usage intention of contactless payment systems. Int. J. Bank Mark. 2019, 38, 332–351. [Google Scholar] [CrossRef]

- Cepeda-Carrion, G.; Cegarra-Navarro, J.-G.; Cillo, V. Tips to use partial least squares structural equation modelling (PLS-SEM) in knowledge management. J. Knowl. Manag. 2019, 23, 67–89. [Google Scholar] [CrossRef]

- Peng, D.X.; Lai, F. Using partial least squares in operations management research: A practical guideline and summary of past research. J. Oper. Manag. 2012, 30, 467–480. [Google Scholar] [CrossRef]

- Hair, J.F., Jr.; Black, W.C.; Babin, B.J.; Andreson, R.E. Multivariate Data Analysis, 7th ed.; Pearson: Edinburgh, UK, 2014. [Google Scholar]

- Fornell, C.; Larcker, D.F. Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Kline, E.; Wilson, C.; Ereshefsky, S.; Tsuji, T.; Schiffman, J.; Pitts, S.; Reeves, G. Convergent and discriminant validity of attenuated psychosis screening tools. Schizophr. Res. 2012, 134, 49–53. [Google Scholar] [CrossRef]

- Halttunen, V. Consumer Behavior in Digital Era General Aspects and Findings of Empirical Studies on Digital Music with a Retrospective Discussion. Ph.D. Thesis, University of Jyväskylä, Jyväskylän Yliopisto, Finland, 2016. Available online: https://jyx.jyu.fi/bitstream/handle/123456789/49620/1/978-951-39-6642-3_vaitos28052016.pdf (accessed on 22 November 2020).

- Iskandar, Y.H.P.; Subramaniam, G.; Majid, M.I.A.; Ariff, A.M.; Rao, G.K.L. Predicting healthcare professionals’ intention to use poison information system in a Malaysian public hospital. Health Inf. Sci. Syst. 2020, 8, 6. [Google Scholar] [CrossRef]

{kind=link}

| N | % | |

|---|---|---|

| Gender | ||

| Female | 285 | 56.9 |

| Male | 216 | 43.1 |

| Total | 501 | 100 |

| Age Group | ||

| Below 20 years | 129 | 25.7 |

| 20–29 years | 307 | 61.3 |

| 30–39 years | 31 | 6.2 |

| 40 and above | 34 | 6.8 |

| Total | 501 | 100 |

| Education | ||

| High school | 167 | 33.3 |

| Diploma | 9 | 1.8 |

| Bachelor | 263 | 52.5 |

| Master | 51 | 10.2 |

| Total | 501 | 100 |

| Employment Status | ||

| Student | 332 | 66.3 |

| Worker | 169 | 33.7 |

| Total | 501 | 100.0 |

| Variables | No. Items | Mean | SD | CA | DG rho | CR | AVE | VIF |

|---|---|---|---|---|---|---|---|---|

| PU | 5 | 4.164 | 0.643 | 0.834 | 0.835 | 0.883 | 0.603 | 2.819 |

| PE | 6 | 4.045 | 0.628 | 0.859 | 0.893 | 0.901 | 0.620 | 2.754 |

| SI | 5 | 3.854 | 0.676 | 0.788 | 0.790 | 0.855 | 0.543 | 3.210 |

| FC | 5 | 3.670 | 0.756 | 0.839 | 0.842 | 0.886 | 0.609 | 3.492 |

| LM | 4 | 3.854 | 0.754 | 0.866 | 0.868 | 0.909 | 0.714 | 4.002 |

| PT | 6 | 4.013 | 0.705 | 0.896 | 0.897 | 0.920 | 0.659 | 3.188 |

| IEW | 6 | 4.008 | 0.658 | 0.887 | 0.889 | 0.914 | 0.641 | 1.000 |

| AEW | 5 | 3.727 | 0.786 | 0.841 | 0.856 | 0.887 | 0.614 |

| PU | PE | SI | FC | LM | PT | IEW | AEW | |

|---|---|---|---|---|---|---|---|---|

| Fornell-Larcker Criterion | ||||||||

| Perceived Usefulness | 0.776 | |||||||

| Perceived Ease of Use | 0.721 | 0.787 | ||||||

| Social Influence | 0.659 | 0.639 | 0.737 | |||||

| Facilitating Conditions | 0.617 | 0.651 | 0.736 | 0.780 | ||||

| Compatibility | 0.636 | 0.652 | 0.696 | 0.781 | 0.845 | |||

| Perceived Trust | 0.624 | 0.618 | 0.686 | 0.646 | 0.766 | 0.812 | ||

| Intention to Use e-Wallet | 0.651 | 0.650 | 0.689 | 0.676 | 0.764 | 0.766 | 0.801 | |

| Adoption of e-Wallet | 0.586 | 0.536 | 0.620 | 0.645 | 0.680 | 0.651 | 0.742 | 0.784 |

| Heterotrait-Monotrait Ratio (HTMT) | ||||||||

| Perceived Usefulness | - | |||||||

| Perceived Ease of Use | 0.854 | - | ||||||

| Social Influence | 0.814 | 0.804 | - | |||||

| Facilitating Conditions | 0.732 | 0.771 | 0.909 | - | ||||

| Compatibility | 0.748 | 0.762 | 0.843 | 0.912 | - | |||

| Perceived Trust | 0.716 | 0.709 | 0.812 | 0.735 | 0.864 | - | ||

| Intention to Use e-Wallet | 0.758 | 0.752 | 0.825 | 0.782 | 0.872 | 0.859 | - | |

| Adoption of e-Wallet | 0.692 | 0.625 | 0.760 | 0.763 | 0.791 | 0.740 | 0.849 | - |

| PU | PE | SI | FC | LM | PT | IEW | AEW | |

|---|---|---|---|---|---|---|---|---|

| Using an e-wallet makes it easier for me to conduct my daily transactions | 0.801 | 0.608 | 0.498 | 0.522 | 0.493 | 0.478 | 0.523 | 0.441 |

| Using an e-wallet allows me to manage my transactions more efficiently | 0.808 | 0.560 | 0.500 | 0.493 | 0.499 | 0.469 | 0.502 | 0.466 |

| Using an e-wallet increases my productivity | 0.777 | 0.519 | 0.523 | 0.521 | 0.541 | 0.511 | 0.513 | 0.509 |

| Using an e-wallet enables me to accomplish tasks e.g., payments more quickly | 0.784 | 0.604 | 0.516 | 0.432 | 0.472 | 0.514 | 0.495 | 0.392 |

| Overall, I believe an e-wallet is more useful than traditional ways of conduct transactions | 0.707 | 0.504 | 0.519 | 0.421 | 0.462 | 0.447 | 0.490 | 0.463 |

| Learning how to use an e-Wallet is easy for me | 0.611 | 0.863 | 0.483 | 0.529 | 0.555 | 0.474 | 0.536 | 0.406 |

| My interaction with an e-Wallet is clear and understandable | 0.641 | 0.797 | 0.535 | 0.537 | 0.534 | 0.556 | 0.548 | 0.467 |

| I find an e-wallet easy to use | 0.615 | 0.862 | 0.518 | 0.519 | 0.541 | 0.518 | 0.541 | 0.435 |

| It is easy for me to become skillful at using an e-wallet | 0.285 | 0.319 | 0.425 | 0.307 | 0.279 | 0.308 | 0.279 | 0.249 |

| It is easy for me to remember how to perform task with an e-wallet | 0.607 | 0.880 | 0.515 | 0.550 | 0.532 | 0.491 | 0.550 | 0.472 |

| I like the fact that payments done through an e-wallet require minimum effort | 0.561 | 0.848 | 0.551 | 0.582 | 0.574 | 0.528 | 0.551 | 0.457 |

| People who influence my behavior think that I should use an e-wallet | 0.558 | 0.629 | 0.661 | 0.505 | 0.501 | 0.490 | 0.488 | 0.405 |

| People who are important to me think that I should use an e-wallet | 0.482 | 0.419 | 0.800 | 0.524 | 0.532 | 0.503 | 0.515 | 0.506 |

| e-wallets are widely used by people in my community | 0.484 | 0.370 | 0.782 | 0.528 | 0.523 | 0.524 | 0.529 | 0.494 |

| Almost all my friends use e-wallets | 0.471 | 0.501 | 0.719 | 0.540 | 0.519 | 0.546 | 0.541 | 0.427 |

| My family members use e-wallets | 0.429 | 0.441 | 0.715 | 0.623 | 0.482 | 0.454 | 0.457 | 0.447 |

| I am given the necessary support and assistance to use an e-wallet | 0.408 | 0.432 | 0.546 | 0.750 | 0.481 | 0.414 | 0.454 | 0.461 |

| I have the financial and technological resources required to use an e-wallet | 0.478 | 0.424 | 0.625 | 0.761 | 0.564 | 0.448 | 0.520 | 0.524 |

| I have access to the software and hardware required to use an e-wallet | 0.544 | 0.577 | 0.557 | 0.837 | 0.641 | 0.539 | 0.564 | 0.533 |

| The e-wallet services I use are well integrated and provided in a stable service infrastructure | 0.453 | 0.537 | 0.534 | 0.786 | 0.643 | 0.472 | 0.525 | 0.500 |

| My service provider/operator facilitates the use of an e-wallet | 0.509 | 0.555 | 0.608 | 0.762 | 0.696 | 0.625 | 0.562 | 0.493 |

| Using e-wallet services is compatible with all aspects of my lifestyle | 0.492 | 0.539 | 0.566 | 0.715 | 0.792 | 0.594 | 0.624 | 0.521 |

| Using e-wallet services fits into my lifestyle | 0.525 | 0.540 | 0.615 | 0.655 | 0.843 | 0.661 | 0.607 | 0.565 |

| Using e-wallet services fits well with the way I like to purchase products and services | 0.507 | 0.528 | 0.570 | 0.638 | 0.876 | 0.631 | 0.672 | 0.618 |

| Using e-wallets is completely compatible with my current situation | 0.623 | 0.597 | 0.601 | 0.638 | 0.866 | 0.698 | 0.673 | 0.590 |

| I trust that a transaction conducted through an e-wallet is secure and private | 0.599 | 0.556 | 0.544 | 0.546 | 0.701 | 0.726 | 0.642 | 0.548 |

| I trust payments made through e-wallet channels will be processed securely | 0.412 | 0.436 | 0.529 | 0.473 | 0.557 | 0.809 | 0.559 | 0.513 |

| I believe my personal information on an e-wallet will be kept confidential | 0.512 | 0.528 | 0.566 | 0.501 | 0.610 | 0.880 | 0.625 | 0.552 |

| I believe e-wallet providers keeps customers’ best interests in mind | 0.426 | 0.417 | 0.514 | 0.464 | 0.529 | 0.821 | 0.573 | 0.473 |

| I believe that in case of any issue, the e-wallet service provider will provide me assistance | 0.528 | 0.518 | 0.609 | 0.577 | 0.655 | 0.816 | 0.634 | 0.497 |

| I believe that the e-wallet service providers follow consumer laws | 0.534 | 0.530 | 0.565 | 0.566 | 0.650 | 0.812 | 0.677 | 0.570 |

| Assuming that I have access to e-wallet, I intend to use it | 0.502 | 0.520 | 0.572 | 0.540 | 0.573 | 0.741 | 0.708 | 0.502 |

| I intend to use an e-wallet if the cost and times is reasonable for me | 0.492 | 0.472 | 0.537 | 0.502 | 0.589 | 0.609 | 0.797 | 0.588 |

| I intend to use an e-wallet in the future | 0.521 | 0.530 | 0.525 | 0.543 | 0.586 | 0.583 | 0.742 | 0.504 |

| I intend to increase my use of e-wallets in the future | 0.517 | 0.544 | 0.573 | 0.585 | 0.652 | 0.593 | 0.841 | 0.647 |

| I intend to continue using an e-wallet more frequently in the future | 0.557 | 0.528 | 0.569 | 0.527 | 0.611 | 0.580 | 0.863 | 0.654 |

| I intend to use an e-wallet in my daily life | 0.535 | 0.530 | 0.535 | 0.550 | 0.653 | 0.583 | 0.842 | 0.655 |

| I often use an e-wallet to manage my account. | 0.433 | 0.434 | 0.467 | 0.512 | 0.554 | 0.514 | 0.643 | 0.817 |

| I often use an e-wallet to transfer and remit money. | 0.456 | 0.395 | 0.527 | 0.521 | 0.557 | 0.552 | 0.615 | 0.821 |

| I often use an e-wallet to make payments. | 0.548 | 0.458 | 0.512 | 0.532 | 0.531 | 0.536 | 0.591 | 0.820 |

| I subscribe to financial products that are exclusive to mobile banking. | 0.526 | 0.542 | 0.522 | 0.561 | 0.597 | 0.558 | 0.617 | 0.811 |

| On average, how often have you used an e-wallet per month? (Never, 1 to 5 times; 6 to 10 times; 11 to 15 times; More than 15 times) | 0.303 | 0.225 | 0.390 | 0.382 | 0.399 | 0.360 | 0.405 | 0.631 |

| Hypo | Beta | CI-Min | CI-Max | t | p | r2 | f2 | Q2 | Decision | |

|---|---|---|---|---|---|---|---|---|---|---|

| Factors affecting Intention to Use e-Wallet | ||||||||||

| H1 | PU  IEW IEW | 0.108 | 0.033 | 0.175 | 2.566 | 0.005 | 0.132 | Accept | ||

| H2 | PE IEW | 0.099 | 0.027 | 0.173 | 2.237 | 0.013 | 0.000 | Accept | ||

| H3 | SI IEW | 0.110 | 0.024 | 0.195 | 2.075 | 0.019 | 0.726 | 0.014 | 0.451 | Accept |

| H4 | FC IEW | 0.048 | −0.037 | 0.137 | 0.916 | 0.180 | 0.002 | Reject | ||

| H5 | LM IEW | 0.265 | 0.178 | 0.358 | 4.875 | 0.000 | 0.005 | Accept | ||

| H6 | PT IEW | 0.339 | 0.255 | 0.416 | 6.979 | 0.000 | 0.013 | Accept | ||

| Factor affecting adoption of e-Wallet | ||||||||||

| H7 | IEW AEW | 0.742 | 0.701 | 0.783 | 28.780 | 0.000 | 0.551 | 0.005 | 0.330 | Accept |

| Beta | CI-Min | CI-Max | T | p | Decision | |

|---|---|---|---|---|---|---|

| PU IEW AEW | 0.080 | 0.024 | 0.134 | 2.503 | 0.006 | Accept |

| PE IEW AEW | 0.073 | 0.021 | 0.128 | 2.225 | 0.013 | Accept |

| SI IEW AEW | 0.082 | 0.018 | 0.144 | 2.073 | 0.019 | Accept |

| FC IEW AEW | 0.035 | −0.028 | 0.103 | 0.912 | 0.181 | Reject |

| LM IEW AEW | 0.197 | 0.133 | 0.268 | 4.843 | 0.000 | Accept |

| PT IEW AEW | 0.252 | 0.188 | 0.313 | 6.762 | 0.000 | Accept |

| Beta | CI-Min | CI-Max | t | p | Decision | |

|---|---|---|---|---|---|---|

| Moderating Effect of Age | ||||||

| PU IEW | (0.050) | (0.107) | 0.004 | 1.550 | 0.061 | No Moderation |

| PE IEW | (0.051) | (0.110) | 0.003 | 1.526 | 0.064 | No Moderation |

| SI IEW | (0.055) | (0.112) | 0.015 | 1.414 | 0.079 | No Moderation |

| FC IEW | 0.005 | (0.064) | 0.070 | 0.125 | 0.450 | No Moderation |

| LM IEW | 0.125 | 0.047 | 0.202 | 2.653 | 0.004 | Moderation |

| PT IEW | 0.033 | (0.028) | 0.086 | 0.929 | 0.177 | No Moderation |

| Moderating Effect of Gender | ||||||

| PU IEW | (0.067) | (0.124) | (0.010) | 1.993 | 0.023 | Moderation |

| PE IEW | 0.054 | (0.001) | 0.106 | 1.616 | 0.053 | Moderation |

| SI IEW | (0.048) | (0.117) | 0.010 | 1.256 | 0.105 | No Moderation |

| FC IEW | (0.078) | (0.140) | (0.015) | 2.022 | 0.022 | No Moderation |

| LM IEW | 0.082 | 0.014 | 0.147 | 2.090 | 0.019 | Moderation |

| PT IEW | 0.010 | (0.041) | 0.074 | 0.285 | 0.388 | No Moderation |

| Moderating Effect of Level of Education | ||||||

| PU IEW | 0.036 | (0.039) | 0.115 | 0.788 | 0.216 | No Moderation |

| PE IEW | 0.074 | (0.007) | 0.161 | 1.422 | 0.078 | No Moderation |

| SI IEW | (0.033) | (0.129) | 0.061 | 0.565 | 0.286 | No Moderation |

| FC IEW | (0.066) | (0.178) | 0.033 | 0.997 | 0.160 | No Moderation |

| LM IEW | (0.030) | (0.146) | 0.073 | 0.445 | 0.328 | No Moderation |

| PT IEW | 0.033 | (0.055) | 0.123 | 0.614 | 0.270 | No Moderation |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yang, M.; Mamun, A.A.; Mohiuddin, M.; Nawi, N.C.; Zainol, N.R. Cashless Transactions: A Study on Intention and Adoption of e-Wallets. Sustainability 2021, 13, 831. https://doi.org/10.3390/su13020831

Yang M, Mamun AA, Mohiuddin M, Nawi NC, Zainol NR. Cashless Transactions: A Study on Intention and Adoption of e-Wallets. Sustainability. 2021; 13(2):831. https://doi.org/10.3390/su13020831

Chicago/Turabian StyleYang, Marvello, Abdullah Al Mamun, Muhammad Mohiuddin, Noorshella Che Nawi, and Noor Raihani Zainol. 2021. "Cashless Transactions: A Study on Intention and Adoption of e-Wallets" Sustainability 13, no. 2: 831. https://doi.org/10.3390/su13020831

APA StyleYang, M., Mamun, A. A., Mohiuddin, M., Nawi, N. C., & Zainol, N. R. (2021). Cashless Transactions: A Study on Intention and Adoption of e-Wallets. Sustainability, 13(2), 831. https://doi.org/10.3390/su13020831