1. Introduction

Sustainable Development Goals (SDG) were set by the United Nations (UN) and came into force in 2016. Over 190 UN member states, including Turkey, have signed them. These goals focus on three main objectives: to end economic poverty around the world, to preserve the planet, and to ensure peace and wellbeing of all people. These objectives are very important for all countries, and climate change is one of the main issues needing immediate action considering SDG. To achieve SDG, one necessity is that environmental, social, and governance (ESG) considerations should form the main principle in making investment decisions in the financial sector. Environmental considerations might include climate change mitigation and adaptation, biodiversity preservation, and circular economy; social considerations might include addressing inequality, inclusiveness, and human rights considered under governance and collaboration of public and private institutions. Making financial decisions with this perspective would lead to increased support for sustainable projects and help eliminate investing in harmful activities to the planet.

This study aims to contribute to the broad topic of sustainable finance from a specific and significant perspective by exemplifying adoption and promotion of sustainable finance through fintech solutions for emerging market economies by presenting the case of Turkey. Since these countries do not have sufficient capital, resources, and technology to sustain their production processes, sustainable finance becomes very critical to support ESG principles in decision making. It presents an extreme challenge to change these countries’ economic models and production systems. For instance, in Turkey, many companies operate with very low levels of working capital and are in constant need of financing to survive. Under these restraining conditions, it becomes an even bigger challenge to adapt the production systems to be environmentally friendly.

In Turkey, the main source of financing are bank loans. Thus, the banking system is instrumental in regulating and conducting sustainable finance transactions. Moreover, 99.8% of the enterprises in Turkey are SMEs in need of financing to survive [

1]. Hence, via loans and credits, banks can allocate funds with more favorable conditions to produce low-impact-on-climate goods, commodities, and services.

On the other hand, climate change has an intense effect on banks’ credit policies due to potential damage and value loss in collaterals for loans. According to World Bank, Turkey is “highly susceptible to climate-related financial risks, especially in relation to water scarcity, natural hazards, and the high share of fossil fuel in its energy consumption” and that the country is exposed to climate and environment migration more than other countries “due to its geopolitical position” [

2]. According to [

3], there is a clear upward trend in the annual climate-related events recorded in Turkey between 1971 and 2019.

Commercial banks account for more than 90% of total assets of the financial sector in Turkey, and the growth of the banking sector has been supported by the increase in the participation of the state in the sector, particularly due to balance sheet expansion of state-owned banks [

4]. As of September 2022, there are 51 banks in Turkey; 35 of these are deposit banks and 16 of them are development and investment banks. Both categories include state-owned banks, private banks with national capital, and private banks with foreign capital. The total number of bank branches within Turkey’s borders is 9663, so the average number of bank branches is approximately 190 per bank nationwide, located over 81 provinces [

5]. Hence, most banks in Turkey heavily adopt traditional banking, i.e., with physical presence and branch operations. For Turkey, with the banking sector as the pillar of the financial system, lacking the ESG perspective in making financial decisions would create irreversible damage to economic indicators and can cause the system to collapse. Awareness of this critical situation prompted Turkey to create the national sustainable banking strategic plan for 2022–2025 [

6].

At the same time, Turkish financial system has been adapting to global updates on regulations for financial activities such as Payment Systems Directive 2 (PSD2) and has been passing several very important regulations to empower the legal structure in adapting to the use of new technologies such as electronic money and digital banking. Enabling technology to provide new banking and financial solutions under a carefully planned legal structure boosted the fintech sector in Turkey starting with the Law on Payment Systems passed in 2013. These two streams of simultaneous developments in sustainable finance and fintech could empower each other if directed well, and this paper aims to present the case of Turkey, providing a detailed analysis of past and potential future accomplishments.

This study pertains to two research streams, sustainable finance (see [

7] for a comprehensive review of literature) and fintech solutions. Since sustainable finance requires an effective legal infrastructure, a major part of the literature on this important topic is dedicated to legal and regulatory framework and its development. One of the most recent updates on the legal structure of sustainable finance with a global effect is the EU taxonomy. Developing a taxonomy takes precedence over many actions to empower the financial system for sustainability applications. It provides the means to a better Environmental Impact Assessment as it helps to detect whether a project inadvertently contributes to an action that is harming the environment [

8]. The EU Taxonomy is anticipated to change the mindset of decision making by simultaneously supporting sustainable actions and the “Do No Significant Harm” principle at the same time [

9]. Taxonomy development is seen as an important tool for achieving SDG, and the United Nations Development Programme (UNDP) also announced SDG finance taxonomy [

10]. In addition, World Bank released a guide on developing a national green taxonomy [

11]. Forming a taxonomy is included within the first set of targets with the highest precedence in Turkey’s strategic plan on sustainable banking [

6], and regulations are anticipated to answer this need for the Turkish financial ecosystem.

Another research topic within sustainable finance has been the assessment of feasibility of applying sustainability and ESG perspectives in existing banking and finance applications (e.g., for home loans [

12]). These studies demonstrate the factors preventing effective adoption of ESG principles in finance. Since a major set of such factors is ineffective risk assessment and management, analysis and categorization of financial risks related to climate change and other sustainability aspects has been the focus of many studies (see [

13] for a comprehensive review on climate-related prudential risks in banking).

Addressing financial risks and analyzing related data is also included in the main targets of Turkey’s sustainable banking strategic plan [

6]. Risk assessment and other data-oriented necessities of sustainable finance requires technological solutions, created by talented and innovative human capital to respond to the needs of customers of the financial system. These necessities led to the growth of the fintech sector in many countries including Turkey. As fintech ecosystems form one of the pillars to successfully apply sustainable finance, this mutually strengthening relationship has been the focus of recent studies (see [

14] for a preliminary assessment of green fintech and sustainable digital finance in achieving environmental goals).

Moreover, Turkey’s financial system includes participation (Islamic) finance, and there has been widely adopted successful fintech applications applying ESG principles to participation finance in Turkey that are discussed in the following sections. Since many emerging economies also adopt participation finance, Turkey presents a more representative example of analyzing the role of fintech in promoting sustainable finance for such economies (see [

15] for an evaluation of fintech ecosystem in Turkey in terms of financial markets and financial stability).

For reasons stated above, leveraging the mutual relationship between sustainable finance and fintech is very important for emerging economies. This study focuses on achieving this objective in the case of Turkey regarding the recently announced strategic initiatives and planned developments for the financial system. To our knowledge, such an analysis has not been provided in the literature yet, and the study presents important insights and examples on managing the transition to a sustainable financial system in an emerging economy via benefiting from fintech solutions.

As main contributions, the study demonstrates the steps traced by Turkey in terms of regulations and forming the start-up ecosystem to develop its fintech sector to its current level. Then, it emphasizes the strategic action plans Turkey is aiming to execute for sustainable finance. Then, a through discussion is provided on how these two simultaneous development processes are streamlined to promote sustainable finance via fintech. Namely, we present the underlying trends and specific fintech solutions such as contactless payment and contract systems and microfinance provided by mobile carriers and agricultural loans with more favorable terms to underbanked farmers that helped Turkey achieve a high level of financial inclusivity and an increasing trend in promoting responsible consumption and production. Then, from the findings on upcoming developments in Turkey’s financial and fintech ecosystem such as opening of Istanbul Financial Center, a discussion is provided on the potential fintech solutions needing to be prioritized to increase the effectiveness of the fintech sector in promoting sustainable finance for Turkey. More specifically, the emphasis will be on increasing the use of new generation technologies such as Big Data, Artificial Intelligence, and blockchain to aggregate data from various resources on climate change and combine it with the current data collected in Turkey’s fintech system such as insurance databases to improve climate change-related risk assessment and management for green loans and to form the basis for a national carbon trading mechanism. Such solutions could help improve the progress made by the banking system in increasing loans for renewable energy and other sustainability projects and comply with upcoming international regulations such as carbon border adjustment mechanism.

In the following sections, review of the literature and the materials and methods used in the case study are presented, then an analysis of development and structure of the fintech sector in Turkey and its sustainable finance strategies is provided. Based on these analyses, a discussion will be provided on the status and agenda of fintech on promoting sustainable finance in Turkey including past and potential future accomplishments. Finally, a summary of the findings and policy recommendations as well as recommendations for future empirical studies are included in the conclusion section.

2. Review of the Literature

The emerging literature on the domain of fintech and sustainable finance can broadly be summarized under three major strands, namely innovation, green finance, and digitalization. Propositions put forward by the leading studies in these key areas are summarized in

Table 1. While a comprehensive review of the literature is beyond the scope of the present article, the propositions put forward with respect to the relationship between green finance and fintech by some studies are noteworthy.

For instance, regarding the commercial and competitive impact of fintech on banking, Elsaid (2021) argues that fintech firms could take some market share away from banks, and could even substitute banks, which necessitates banks to adopt innovations and advanced technologies [

16]. The author also suggests that both fintech firms and banks can benefit from strategic partnerships and cooperation. This important proposition has been shared by many other authors in the existing literature (See, inter alia, [

17,

18]).

Regarding the supportive impact of fintech on sustainable finance, Cen and He (2018) explain that fintech supports sustainable finance by reducing transaction costs and improving capital efficiency, lowering information asymmetries, and enhancing risk management, and by making green finance more inclusive [

19]. Mejia-Escobar et al. (2020) also emphasize that sustainable financial products flourish in the fast-improving fintech ecosystem, especially from a social and financial inclusivity perspective in the Latin American context [

20]. Likewise, regarding the role fintech plays in facilitating the development of green finance, Yang (2020) explains that fintech does this by decreasing bank credit risk, enhancing the regulation level, stimulating product innovation, and the perfection of the information-sharing mechanism [

18]. Moro-Visconti et al. (2020) also lends support to these propositions by explaining that fintech will lead to greater access to finance and investment through improved financial inclusion [

21].

Financial inclusion is one of the main benefits particularly relevant to developing countries since not only individuals but many SMEs contributing to production need access to financial services due to lack of capital. For green finance to be effectively within the main principles of allocating funds to practices in line with SDGs, it is critical to include and tend to economic and social needs of as many companies as possible in the financial system. Tseng et al. (2018) found that economic and social aspects of sustainable supply chain finance have an impact on the environmental aspects [

22]. For inclusion of financially disadvantaged individuals contributing to production, Anshari et al. (2018) provide design of a fintech-enabled digital marketplace empowering farmers with crowdfunding and payment systems [

23].

On the other hand, some authors focused on the cumulative impact of fintech and sustainability on the financial services industry, arguing that they are concurrently causing a major transformation in finance. For instance, Hommel and Bican (2020) discuss that collaboration between fintech and traditional institutions comprise partnering, outsourcing, or investment as venture capitalists [

24]. While this is a valid argument, Puschmann et al. (2020) investigate this partnership from a different perspective, arguing that “green FinTech” remains under-researched, but digitization and sustainability are clearly the core drivers of a change in the financial services industry [

25]. The authors particularly discuss that green fintech has an impact along the entire value chain of financial services including customer-to-customer, business-to-customer, and business-to-business service areas. Similarly, Chueca Vergara and Ferruz Agudo (2021) conclude that sustainable finance and fintech have many aspects in common, and that fintech can make financial businesses more sustainable overall by promoting green finance [

26].

From the review of the relevant literature, it can be concluded that the existing studies in this new domain are characterized by a specific focus on isolated aspects of innovation, green fintech, and digitalization. Therefore, it can be argued that the existing literature falls short of providing a comprehensive perspective yet. While the literature includes a plethora of studies attempting to explain the relationship between fintech and sustainable finance, the existing literature can be criticized on the grounds that it lacks case studies examining country experiences reflecting different financial and regulatory systems and different levels of advancement in sustainable finance practices.

New generation technologies (e.g., blockchain) are not mature, and their development needs to be followed closely in different country-specific examples. Turkey sets an important example uniting participation (Islamic) finance with fintech that could help achieve SDGs. As Aysan and Bergigui (2021) states, the potential of participation finance in accelerating the transition to circular economy could be realized by scaling up the use of blockchain for participation finance services [

27]. As further examples, pilot studies are conducted to design the best use of these new generation technologies such as profiling individual risk preferences to prepare for robo-advising in Hong Kong [

28] and Germany [

29]. Rizwan and Mustafa (2022) investigate the factors determining the decision to fund in a crowdfunding platform in Pakistan [

30]. Each country has different dynamics for forming regulations; therefore, the joint development of fintech revolution and sustainable finance may progress with different trends, justifying the need for presenting different examples from different countries in anticipation of global compatibility needs for the future.

The present article aims to contribute to the literature via responding to the research gap of case studies examining country experiences for advancement of sustainable finance through fintech by reviewing the case of Turkey. Given Turkey is one of the largest emerging market economies in the world (ranked 19 in 2021 by gross domestic product [

31]) with a strong banking system and high adoption of technology, this country-specific experience with fintech adoption can serve as a case study for other emerging economies and developing countries alike.

While contributing to the existing broader literature on sustainable finance, the present analysis deviates from other similar case studies. According to a comprehensive review of the earlier case studies in the literature by Puschmann et al. (2020), existing country-specific studies focus on specific aspects of green fintech, lacking a comprehensive perspective [

25]. The authors themselves provide a case study of Switzerland reviewing the role of green fintech startups as well as the services offered by the incumbents.

The existing literature comprises only a few other country-specific studies which focus on different aspects of sustainability. For instance, Tao and Azhgaliyeva (2018) study the role of green fintech on economic and financial development in the case of Singapore [

46], Deng et al. (2019) explore the role of fintech on sustainable development in the case of China [

47], and Lee and Kim (2015) study the fintech industry in Korea [

48]. To our knowledge, there is no other study that reviews the role of fintech from a comprehensive perspective. In particular, the existing studies do not review policy developments with the aim of providing policy recommendations and implications for other countries.

Our analysis is somewhat similar to the case study by Puschmann et al. (2020) on Switzerland in terms of the countries’ environmental footprints and the importance of their financial services industries in their economies [

25]. However, our case study offers a novel contribution in the sense that we go one step further, focusing more on policy aspects and providing policy lessons for other countries.

More precisely, we provide a comprehensive review of the recently announced strategic initiatives and policies. This is in line with the recommendations set forth in the earlier studies (see, inter alia, Puschmann et al. (2020) [

25]) that future analyses should focus on country specific policy developments. We believe that this is indeed a novel and important contribution as alignment of national fintech laws around the world will depend on policy lessons and country-specific experiences.

3. Materials and Methods

For this case study, a thorough analysis of Turkey’s fintech sector was conducted via first reviewing the laws, secondary legislations, and other regulations entered into force to form the legal infrastructure of the fintech sector. Web links to all these documents are provided in the references including the ones that are written in Turkish. English translations of the titles of the web pages are provided for readers to note and follow if required. Then, research conducted and reported by government offices such as Finance Office of the Presidency of Turkey and private auditing companies such as KPMG and EY were reviewed to further report on the characteristics of Turkey’s fintech sector and details of planned developments such as Istanbul Financial Center.

To review and present details of contribution of current Turkish fintech companies to sustainable finance, more detailed information such as company value propositions, descriptions, and level of experience were collected via subscription to Startups.watch. Startups.watch is a research platform serving as Turkish Startup Ecosystem Intelligence providing a database of over 8000 startups on different sectors including fintech, artificial intelligence, insurtech, and edutech. The platform verifies all transactions forming the data with the chamber of commerce data and provides publicly accessible reports such as snapshots of Turkish fintech ecosystem. Whenever possible, links were provided within the text to these freely available reports, and the platform was noted as the source for numerical data and examples of value propositions of Turkish fintech companies when discussed in the text.

In Turkey, regulations and strategies for the national finance ecosystem are determined by different government entities, namely, Central Bank of Turkey, Banking Regulation and Supervision Agency (BRSA), Capital Markets Board of Turkey, Insurance and Private Pension Regulation and Supervision Agency, Ministry of Treasury and Finance for the Republic of Turkey. Each government office and ministry oversee different parts of the finance ecosystem; for instance, payment systems are governed by Central Bank of Turkey, and sustainable banking strategies has been formed mainly by BRSA. In terms of regulatory and supervisory practices, Turkish regulators are among the first 20–25 countries in the world to take climate-related prudential risks into account (see [

13]).

As green loans and bonds to support renewable energy investment and other projects has been implemented mainly by traditional banks, the banking sector and the regulatory body governing it had been tasked with forming the national strategic action plan for sustainable banking in Turkey. To review and analyze the progress of Turkey in sustainable finance, reports and statistics provided by the government offices above were also analyzed, and where applicable, other governing offices’ action plans have been reviewed. For example, since the EU Green Deal includes Carbon Border Adjustment Mechanism (CBAM), the Green Deal Action Plan of Turkey was formed and announced by Ministry of Trade, and the titles and web links for all these reports were referred to within text and listed in references with English translations where required.

Turkey’s potential for sustainable finance and existing strong banking system merits analysis and valuable recommendations from global institutions such as the World Bank; where applicable, reviews from these institutions were also included in discussions on Turkey’s potential in developing its sustainable finance strategies further. These reports and data from Turkish and global resources were used to conduct the case study in the role of fintech in promoting sustainable finance in Turkey, presenting the accomplished achievements so far, and the potential to be realized.

5. The Current Status and Agenda of Fintech in Promoting Sustainable Finance in Turkey

We will first discuss how the fintech sector in Turkey helps promoting the sustainable banking action plan (2022–2025) and can do more on this as this plan is the main sustainable finance strategy document of Turkish banking ecosystem which involves the Turkish fintech ecosystem. As the first set of objectives aim to establish a data infrastructure for assessing climate change related financial risks, brief descriptions of these risks will be provided in

Table 5 below.

Transitional risks arise from the actions needed to be executed during transition to a low-carbon economy. Many fintech contributions for assessment and management of these risks would also help Turkey execute its “Green Deal Action Plan”, and the emphasis will be on how these contributions could help address this action plan as well. Then, a discussion will be provided on how fintech sector in Turkey helps promoting social sustainability in finance.

5.1. The Current Status and Agenda of Fintech Sector in Turkey in Assessing Climate Change Related Physical Risks

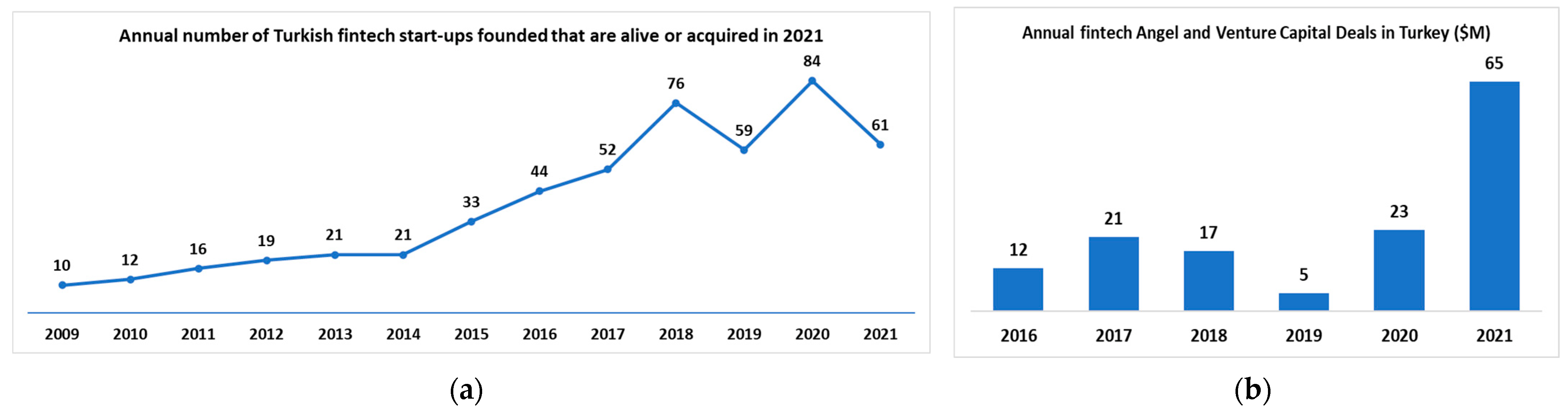

Existing value propositions by Turkish fintech start-ups include AI-based risk pricing tools for the insurance industry, “data as a service” focused on risk, marketing, and operations solutions, and insurance and claims management platform. Physical risks are closely associated with insurance, and insurance has been one of the top five most preferred categories for areas of activity among Turkish fintech companies since 2016 [

52]. Insurance Law No. 5684 entered into force in 2007 [

53], so the insurance sector in Turkey has been operating under a legal infrastructure for almost two decades. This history brings a significant amount of data available for analysis, especially with new generation technologies such as Big Data and AI.

As Turkish fintech start-ups as the above listed ones continue to emerge with a focus on risk assessment and management via these new generation technologies, Turkish fintech sector could provide analysis of insurance data, cross-reference of it with current climate change effects around the world and provide scenario analysis and simulations for monetary valuation of climate change related physical risks. These analyses could further enhance value propositions of Turkish fintech companies focused on credit scoring.

Banking technology has also been among the top five most preferred areas of activity for Turkish fintech companies since 2016 [

51], and it is essential to form a data infrastructure for reflecting the effect of climate change-related risks on balance sheets of banks and account for these risks in capital adequacy ratio calculations to increase the financial stability of Turkey’s banking sector via fintech sector [

66]. Many significant effects of climate change can be analyzed with such data. For example, a statistically significant relationship was found between delays in loan repayment for agricultural, energy, food, and lumber production loans in Antalya, Turkey (located on the south coast of Turkey) and extreme weather events as well as deviation in rainfall and average temperature [

67].

5.2. The Current Status and Agenda of Fintech Sector in Turkey in Assessing Climate Change Related Transitional Risks

With the development of a taxonomy to categorize different actions from the perspective of climate change and sustainability, carbon emissions could be measured systematically and can be included with climate events to calculate trade losses as well as financial losses due to transitional risks. For instance, lack of a carbon pricing mechanism would impose additional costs for exports to EU due to CBAM and could also cause loss of trade altogether because of competition from other countries for trade. Even before establishment of a national carbon pricing mechanism and market, through the Turkish fintech sector, it could be possible for Turkish exporters to EU to benefit from international climate markets via Distributed Ledger Technology or Blockchain. Climatecoin in Switzerland offers a carbon credit market represented by tokens to compensate for carbon emissions via contributing to climate change mitigation projects [

14]. There are currently more than 20 Turkish fintech companies providing blockchain technology-oriented solutions [

52], which would allow Turkish producers to connect to international markets and perform carbon trading.

As discussed in the above example for physical risks, agriculture is one of the sectors that could be significantly affected by climate change. For instance, climate change and the resulting rise in temperatures will lead to higher evaporation, lower rainfall, and hence higher irrigation needs in Mediterranean regions [

68]. They may also make growing some fruits in these regions infeasible. These changes will affect farmers’ repayment capacity and values of their collateral, and fintech solutions could help mitigate potential financial losses by careful risk assessment and resulting recommendations made to farmers on their financing decisions. Some Turkish fintech companies that are focusing on agricultural financing solutions offer seed, feed, and fertilizer sales via loans, rural agricultural insights, and financial management solutions for farmers and dealers in agriculture [

52].

Transitioning to a circular economy emphasizes lifecycle impact assessment for products, rather than measuring the impact on the climate during the production phase only. To achieve this, AI, Big Data analytics, and blockchain technologies can be combined by fintech companies’ services to process large amounts of data for measuring lifecycle impact of a product to the climate and to increase pricing accuracy and reliability [

14]. Turkey has been monitoring and reporting installation-level Green House Gas emissions since 2015 for energy and industry sectors (e.g., coke, metals, cements, chemicals) [

2]. Enhancing this monitoring and reporting system could affect investor preferences favorably as well as provide evidence on the causes of any changes observed. Since payment systems has been the dominant area of activity for the Turkish fintech sector and there is high adoption rate for electronic payments, Turkish fintech companies already have vast amounts of data created in real time on changes in consumer preferences and can incorporate any promotional campaigns via many payment products such as reward or bonus programs on card payments.

As financial consequences of climate change-related risks are assessed through fintech solutions involving high amounts of data processing from various disparate sources such as weather reports and government and academic databases, applying the “Do No Significant Harm” principle of EU taxonomy would be more achievable, and this would help avoid loss of reputation risks on loan and other financial decisions.

5.3. The Current Status and Agenda of Fintech Sector in Turkey in Increasing Sustainable Loans and Funds and Strengthening Collaboration of Stakeholders in Sustainable Finance

In line with the second set of objectives in BRSA’s strategy document, Turkey needs to increase green loans provided and funds made available for sustainability-oriented projects and activities. Turkey has made significant progress in providing loans for renewable energy. Turkish Development and Investment Bank (TKYB) issued Turkey’s first green/sustainable bond in the international capital markets in 2016, and Garanti BBVA followed in 2019. Sekerbank provided a green loan (EKOkredi) to finance energy efficiency projects of SMEs, individuals, and industrial and agricultural enterprises. In 2020, 40% of the loans extended by Turkish banks to the energy sector were used for renewable energy projects. Thus, the Turkish banking sector continued to contribute to increasing the share of renewable energy in the energy sector.

Turkey also has made significant progress in Participation (Islamic) finance. Islamic finance is a powerful tool to support sustainable finance, and Islamic fintech solutions provided by the Turkish fintech sector could boost loans provided for renewable energy and other sustainability projects. Islamic banks could help form Islamic fintech companies in Turkey; for instance, Kuveyt Turk has opened Architect, an Islamic financial technology company, and its fintech solutions have been adopted both in Turkey and abroad [

69]. Istanbul Financial Center (IFC) will focus on Islamic finance as the other core strategic foci along with fintech, and it is expected to accelerate Turkey’s growth on providing fintech solutions in sustainable finance [

2]. IFC is expected to transform Istanbul to a financial hub, providing a nurturing ecosystem not only for fintech, but all stakeholders of Turkey’s finance ecosystem.

Forming a comprehensive data source with data extracted from multiple sources combining climate related and financial data, processed via AI, Big Data, blockchain, and other new-generation technologies could help Turkey increase use of public funds for sustainability projects such as Sustainable Cities Program for ILBANK, which is a state-owned development and investment bank. As an example, this project provides funds for renewable energy and waste management [

2].

5.4. The Current Status and Agenda of Fintech Sector in Turkey in Increasing Social Sustainability

Turkish fintech companies contributed significantly to increase financial inclusivity. Such Turkish fintech solutions helped increase financial literacy and guide consumer behavior towards a savings rather than consume-and-waste perspective (e.g., Manibux), these solutions are usually combined with payment services via a card provided. As payment services are the fintech solutions where Turkey’s fintech ecosystem has the greatest strength, there is significant potential in socially sustainable fintech applications. This and similar projects contribute to the Sustainable Development Goal “Responsible Consumption and Production”.

Turkish fintech solutions contributed to financial inclusivity from the supply side as well, by providing payment-oriented fintech solutions such as developing mobile apps to use cell phones as POS devices and allowing SMEs to benefit from financial services and connect with consumers who prefer to use credit cards instead of cash [

55]. The fintech solutions for agricultural loans discussed above also contribute to increase financial inclusivity by allowing farmers access loans with favorable rates and payment terms. Turkish fintech solutions on payment systems further contribute to decrease operational and other expenses for SMEs and increase their access to financial resources better than traditional banking solutions. In this regard, Turkish fintech companies demonstrated significant growth and contributed to the Turkish financial system greatly.

As telecommunication and Participation (Islamic) finance are other strong aspects of the Turkish financial system, there have been fintech solutions provided with collaboration between them in microfinance. Since cell phone usage is highly adopted in Turkish consumer segments of all levels of earning, microfinance applications diffused via mobile service providers could help promote financial inclusivity and social sustainability (e.g., Financell provided by Turkcell).

We finalize the discussion with

Table 6 below which summarizes the past and potential future accomplishments of the Turkish fintech sector particularly pertaining to promoting sustainable finance.

6. Conclusions, Discussions, and Recommendations

In this study, we presented the case of Turkey for the status and agenda of fintech in promoting sustainable finance. Turkey is one of the largest emerging market economies in the world [

31] with a strong banking system and high adoption of technology, so it has great potential to benefit from fintech solutions to boost sustainable finance. The study provided a detailed presentation of the development and structure of the fintech sector in Turkey and its current strategic action plans for sustainable finance from various sources of data including a research platform for Turkish start-up ecosystem intelligence, many reports, statements of regulations from Turkish governmental offices and auditing companies, and documents released on Turkey’s development on sustainable and green finance by global institutions.

A detailed discussion was then presented on the status and agenda of fintech in promoting sustainable finance in Turkey. We found that Turkey has made a high level of progress in increasing financial inclusivity for underbanked individuals and SMEs. Turkey was able to provide contactless payment and contract systems and microfinance by mobile carriers and other online platforms to complete transactions such as opening an account in minutes to increase access of disadvantaged consumers and companies to the financial system. Turkey was also able to promote the responsible consumption goal for sustainable development by improving fintech solutions on payment systems via adding educational content to the applications.

Based on this analysis, several policy recommendations and implications have emerged, which are broadly in line with the propositions of earlier studies in the literature. To begin with, as our analysis has clearly shown, the Turkish financial services sector has already started benefiting from converging digitalization and sustainability. As discussed by George and Schillebeeckx (2021) [

32], new digital technologies are expected to further empower novel sustainability solutions. This has already been happening in Turkey. By adopting PSD2 and putting in force the Law on Payment Systems, policy makers have paved the way to the adoption of new technologies with respect to payments (

Table 2). Policymakers in other countries should follow suit to be able to reap the full benefits of financial innovation.

As Babarinde et al. (2020) [

38] suggests, it is vital that the banking industry keeps pace with the digital innovations. In Turkey, the banking sector started supporting and promoting fintech through establishing their own technology subsidiaries and exploring new financial technologies. Other countries should also note that several Turkish banks have also started to sponsor incubators and accelerators to support emerging fintech startups, while others have started establishing venture funds and investments in fintech (

Table 4).

Furthermore, with the new regulations on open banking and BaaS, Turkey is expected to benefit from its high level of e-commerce turnover to increase access to loans and at the same time better measure the impact of them on the environment by providing instantaneous data collection on the purchases they are used for. A key finding of the present analysis is that fintech has started to redefine the financial services sector in Turkey. Our analysis therefore lends support to Palmie et al. (2019) [

35] who argue that the fintech ecosystem has disrupted the financial services industry.

Our analysis on the Turkish experience with fintech is in line with the proposition of Elsaid (2021) that fintech firms are expected to steal some market share away from banks but are not expected to substitute banks completely [

16]. Our analysis particularly lends support to Moro-Visconti et al. (2020) [

21] and Kabulova and Stankevičienė (2020) [

41], who discuss that fintech is expected to reshape the financial industry by cutting costs, improving the quality of financial services, and creating a more diverse and more stable financial landscape.

Turkey has made significant progress on increasing financial inclusivity through fintech-based online payment and loan applications pertaining to underbanked groups such as farmers since many Turkish fintech companies work on this for their value propositions (

Table 3). This is well aligned with the emphasis in the recent literature on: providing more opportunities of financial inclusivity via digitalization to increase agricultural and other activities conducted with the ESG perspective (Mejia-Escobar et al. (2020) [

20]); filling the lack of access to financial services by the underbanked (Varga (2018) [

42]) through emphasizing digital money (Gálvez-Sánchez et al. (2021) [

43]); and using interoperable electronic payments systems as one of the pillars for an economy to leverage fintech for sustainable development (Arner et al. (2020) [

45]).

With the Secondary Legislation on Equity-Based and Debt-Based Crowdfunding by Capital Markets Board of Turkey passed in 2021, Turkey will be able to align the use of crowdfunding more effectively with other fintech applications such as digital payment to enhance its digital marketplace for financial inclusivity of farmers and agricultural sustainability to realize the models proposed in the literature (Anshari et al. (2018) [

23]). As financial inclusivity is especially important for emerging economies, Turkey’s progress in this aspect via first strengthening the legislative structure with consecutive regulations as well as amendments to the previous ones for compatibility with global regulations such as PSD2, and then having the banking sector and other strong stakeholders supporting the fintech start-ups (

Table 4) to achieve innovative solutions represents an effective roadmap for other emerging economies.

As discussed by Hommel and Bican (2020) [

24], fintech has a technological advantage over traditional financial institutions through “customer-centricity” and enhanced efficiency. Our analysis is particularly in line with Rose (2020) [

37], who explains that mechanisms such as distributed ledgers and other financial technologies may increase trust and reduce transaction costs in traditional finance. Malamas et al. (2020) [

36] emphasize the potential benefits of a blockchain-enabled issuance architecture for green bonds, and Deschryver and Mariz (2020) [

40] conclude that the full potential of green bonds to finance sustainability goals has not been achieved.

Coupled with Aysan and Bergigui’s (2021) [

27] conclusion on the benefit of the use of blockchain in participation finance for adapting to climate change and transition to circular economy, we believe an important milestone for Turkey to promote sustainable finance with fintech would be extending the use of blockchain in fintech. There are currently 79 fintech start-ups with blockchain in their value propositions whereas there are 228 payment-oriented fintech start-ups (

Table 3); thus, we expect the share of blockchain-oriented companies to increase in Turkey’s fintech sector as well as other countries, especially the ones applying participation finance. Our analysis has emphasized the importance of increasing the use of new-generation technologies such as Big Data, Artificial Intelligence, and Blockchain to combine data from various resources on climate change with the existing data in the Turkish fintech ecosystem. Certainly, this applies to other countries as well.

It is also clear that fintech and innovation will present reputational gains for the financial services industry as suggested by Anagnostopoulos (2018) [

33]. Other benefits include risk mitigation, which is also discussed in detail by Acar and Citak [

17]. Our analysis lends support to Yang (2020) [

18], who discusses that fintech can facilitate the development of green finance by decreasing bank credit risk, enhancing the regulation level, stimulating product innovation, and the perfection of the information-sharing mechanism. It is noteworthy that some Turkish banks have started providing open banking products to support the growth of fintech businesses by making their APIs available. It is recommended that banking sector regulators adopt similar policies particularly with respect to banks’ APIs.

Our analysis also concurs with Cen and He (2018), who explain that fintech promotes both green finance and sustainable development [

19], and Chueca Vergara and Ferruz Agudo (2021) [

26] who discuss that fintech can make financial businesses more sustainable overall by promoting green finance. Our analysis is therefore also aligned with Chen and Volz (2020) [

39] who discuss that fintech may help to mobilize financial resources for sustainable infrastructure investments. Likewise, our analysis also lends support to Puschmann et al. (2021) [

25] who argue that “green fintech” can also alleviate the impact of climate change as it has an impact along the whole value chain of financial services. For a country with an upward trend in the annual recorded climate-related events, this is a particularly important point to consider. Policy makers in other countries would be well-advised to take these points into consideration.

It is evident that there are challenges with respect to development of fintech and there are various considerations and barriers that need to be addressed to achieve green finance as discussed by Nikolaou (2018) [

34]. In Turkey, some banks have tech subsidiaries, incubators/accelerators, and/or corporate venture capital funds. Looking forward, with the upcoming developments such as the sandbox environment to be built in Istanbul Financial Center, such fintech solutions could be developed much faster with collaboration between banking and fintech sectors and regulatory institutions. Turkey, therefore, is set to serve as an inspiring role model for other countries in terms of adopting the related regulations and forming a start-up ecosystem to facilitate the development of their fintech sectors.

Finally, limitations and future directions related to this article can serve as guidelines for researchers about what can be explored further in future research. For instance, due to data availability issues with respect to fintech and innovations, we have not been able to carry out an empirical analysis. Due to the lack of time series data, we have not been able to carry out an econometric analysis to explore the impact of fintech on the banking sector. Likewise, the existing studies lacked empirical findings based on which we could come up with policy lessons for Turkey. Researchers would be advised to collect cross-sectional data on the adoption of fintech by using relevant proxies to be able to carry out econometric research.

{kind=link}