Abstract

This study conducts a bibliometric analysis of research on sustainability committees. Specifically, our paper analyses the development of this field of research by identifying the most influential articles, authors, and relevant research themes, and highlighting potential future lines of research. Our sample is composed of the publications from the main collection of the Clarivate Analytics Web of Science database (WOS) for the period 1900–2021. Our findings stress the interdisciplinary nature of research about sustainability committees. In addition, our evidence emphasizes the need for more research to understand how firms respond to regulatory and societal pressures on sustainability matters. In addition, the network analysis highlights the main research themes and provides a basis for recognizing future research opportunities. Our paper is the first to perform a comprehensive bibliometric analysis for sustainability committees. Our evidence presents relevant implications for academics in the definition of their research projects.

1. Introduction

Corporate governance mechanisms are crucial in firms’ sustainable development and, particularly, boards of directors are the central decision-making authority in a company, standing responsible for sustainable challenges [1]. Boards generally delegate specific tasks to board subcommittees, which are in charge of strategic planning and play an important role in the oversight of corporate policies [2]. Specifically, the existence of a sustainability committee at a board level may help the organization to improve the development and implementation of sustainable strategies [3,4]. This remains a key issue nowadays since sustainability has become an important part of a business to gain competitive advantage and companies are enhancing their efforts to integrate sustainable policies into their overall strategy [5]. Given the unprecedented relevance of sustainability, which has arisen as a major topic worldwide, sustainability committees have gained great attention from policy-makers, professional bodies, and academics alike.

In the regulatory and professional sphere, the importance of sustainability committees has been progressively considered by many international organisms [6,7,8,9,10,11], which have emphasized the role of this mechanism in corporate strategy, as this committee is expected to assist key board decisions in terms of sustainable reporting practices, environmental actions, environmental innovation, and monitoring of risks related to climate change, among others. However, currently, regulators do not oblige companies to establish a sustainability committee or similar, nor is it even required for institutions to have a CSR expert, so it is a completely voluntary matter [12]. Even though companies are adapting to regulatory changes and demands related to sustainability matters, many of the functions assigned to this area sometimes end up in other committees. From an academic standpoint, previous research has underlined that sustainability committees have been established to comply with corporate governance recommendations [13] as well as to exhibit the responsibility of top management [14]. Since directors are experts who lead board decisions, it is supposed that sustainability committees help companies to implement sustainable strategies [15] and mediate between financial and non-financial interests [16]. In addition, these committees are expected to enhance the board monitoring regarding corporate social responsibility actions adopted by firms. Hence, analyzing the impact, composition, and effectiveness of such committees has become a relevant area of investigation. In this regard, research on sustainability committees has significantly evolved in the last years, and recent streams of studies increasingly focus on the impact of these committees on sustainable performance [15,16,17] and sustainability reporting [18,19,20], as main strategies to achieve a firm’s sustainable development. In general, recent studies have evidenced that the existence of sustainability committees enhances environmental, social, and governance performance [12,14], boosting CSR involvement, and lessening CSR differences, improving dialogue between stakeholders [13].

Nonetheless, the existing research on this matter still remains scarce and very fragmented, and much more evidence concerning the role of sustainability committees is needed, especially in the current scenario, where corporate sustainability has become fundamental in political and professional agendas. The purpose of our paper is to carry out a bibliometric analysis of the literature concerning sustainability committees to guide future research on this topic.

Bibliometric analysis offers a visualization of the publication patterns in research. The possible hidden patterns of the previous literature are also highlighted [21], which favors the positioning of new research. Furthermore, bibliometric analysis is capable of capturing the evolution of the field [22], analyzing long periods, historical development, and current and future trends [23]. All this makes bibliometric analysis a guide for future research [24]. Although bibliometric studies have become popular in different research fields, these analyses remain relatively occasional in the literature on corporate governance. In particular, bibliometric analyses regarding the board of directors have focused on board diversity [25,26,27], interlocking directorates [28,29], the audit committee [30], and the relation between boards and reporting practices [31,32]. Our study is the first to perform a comprehensive bibliometric analysis across the entire WOS principal collections database for sustainability committee research. In this paper, 182 research publications from the WOS will be analyzed by using VOSviewer software.

In line with recent bibliometric studies [26,27,33,34], this paper aims at answering several research questions (RQ) to identify current dynamics and the intellectual structure of research on sustainability committees: (RQ1) What is the volume of publication over the years? (RQ2) Which are the most productive countries? (RQ3) Which publications are the most cited in the research period? (RQ4) Who are the most influential and productive authors? (RQ5) What are the most important research topics studied and the potential research gaps opportunities? Therefore, our paper outlines the research regarding sustainability committees and provides several contributions to the literature. First, our study pinpoints the development of the publications, the institutional contexts in which this topic has been explored, and the main documents and authors within this line of research. This enables identifying settings where future research may focus to gain a more accurate view of outstanding research. At the same time, the identification of the main documents in this research field is a crucial outcome in bibliometric analyses for scholars to position their future studies. Second, our findings provide an overview of the main themes and intellectual structure of sustainability committee research. This is fundamental for academics to understand the state-of-the-art and define future research avenues as this enables categorizing current research topics and recognizing trends. Third, we discuss the future research agenda by responding to relevant questions regarding research on sustainability committees, such as: what has already been done and what is unknown?; what theoretical approaches have been employed and how can they be extended?; and what can be the future lines of research?

2. Data and Methodology

2.1. Data

Our sample is composed of documents from the main collection of Clarivate Analytics Web of Science for the period 1900–2021 (the Web of Science collects information from 1900 to the present). Specifically, we focus on the publications including the terms “Sustainability Committee”, “CSR Committee”, or “Environmental Committee” in the title, abstract, or keywords. As a result, the sample consists, of 182 documents.

These publications belong to different research categories, such as “Business”, “Chemistry”, “Economics”, “Environmental Sciences”, “Management”, “Oceanography”, and “Transportation”, which denotes the multidisciplinary nature of this topic. For this reason, it is not convenient to develop a stage to filter the documents, therefore all the categories are included in the study.

2.2. Methods

A wide-ranging bibliometric analysis is performed to explore the intellectual structure of research on sustainability committees. Bibliometric analysis has been used in different research areas and it is generally defined as “the application of mathematical and statistical methods to books and other media” [35]. Bibliometric analysis provides some advantages to synthesizing the research developed in a specific area. First, it allows presenting the historical development and systematizing of the research published so far [23]. This is possible due to the analysis and control of research activity over long periods of time [22]. In addition, the use of different databases enables a massive control of documents [36,37]. Second, the results of the bibliometric analysis allow the elaboration of work guides for academics [24], as well as the presentation of research trends in recent years [38]. Finally, considering the above, this analysis permits identifying “hidden patterns” in the research developed, which is important for new academics to position future research [21]. The software used to run the bibliometric analysis is VOSviewer, since it includes tools, such as zooming, scrolling, search, and enables a high-quality graphic representation of bibliometric maps [39].

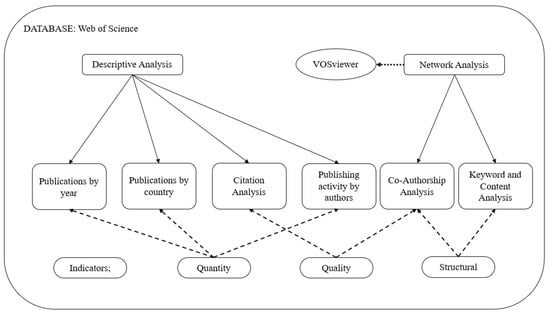

Our bibliometric study is composed of two types of analysis, descriptive analysis, and network analysis. The descriptive analysis allows recognition of the number of publications over the years, the research activity developed in different geographical areas as well as the productivity and impact of the authors. In addition, it also contains a citation analysis, which remains vital for scholars to recognize the most relevant literature in a specific research area. On the other hand, the network analysis is composed of a Co-Authorship Analysis and a Keyword Analysis, which focuses on intellectual mapping based on the analysis of the occurrence of the keywords within the publications from our sample. This analysis permits identifying the most relevant topics in the research area, as well as approaching the most incipient lines of study and, therefore, finding gaps in the literature on the sustainability committee.

To develop these analyses, three different indicators are generally considered in the literature [40]: (1) quantity indicators, referring to productivity in research; (2) quality indicators, where the impact on the research is obtained; (3) structural indicators, which measure the connections of multiple variables. The structure of our bibliometric analysis is presented in Figure 1.

Figure 1.

Bibliometric analysis structure. Source: own elaboration.

3. Results

3.1. Descriptive Analysis

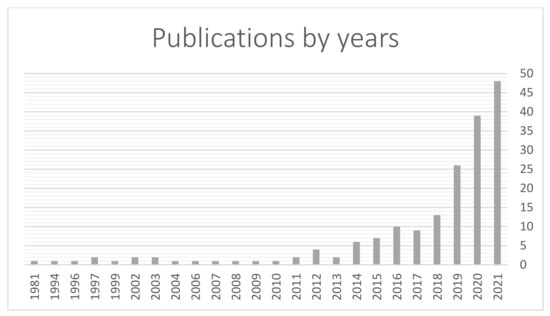

3.1.1. Publications by Year (RQ1)

Figure 2 shows the evolution of annual publications. Two different stages can be seen: from 1981 to the mid-2010s, and from then to the present. In this regard, from the first publication until 2013 there are no more than 5 articles per year. Although the search developed in WOS is filtered from 1900, the moment from which the database stores information, to 2021, it was in the late 1970s when the need for new business strategies and practices to promote and protect the environment was incorporated into professional and regulatory debates. Specifically, in the US (Resource Conservation and Recovery Act (RCRA)1 5 in 1976 and the Comprehensive Environmental Response Compensation and Liability Act (CERCLA)I’ in 1980 (commonly referred to as the “Superfund”1 7), several laws were enacted concerning this issue, but they did not have a positive impact because they involved elevated costs for companies, and this led to a slow application of the norm. Consequently, it was not until 1981 when the first article “Environmental Committee Sees Need for Testing and Performance Standards” was published in the Journal of Civil Engineering [41]. Since then, the concern for environmental matters has evolved from engineering and environmental sciences to fields related to business and management, especially in the aftermath of the proliferation of organisms calling for the sustainable development of firms. In this sense, in the past decade, Directive 2014/95/EU intensified the requirements for corporate disclosure on sustainability matters [42]. In 2015 the Sustainable Development Goals (SDG) were presented [43], setting out several challenges for firms to guide their future policies to contribute to global sustainable development. In addition, the Paris Agreement, signed in 2015 [44], stressed the need for the limitation of global warming and made firms responsible for sustainable behavior to mitigate climate change by minimizing greenhouse gases (GHG) and the carbon footprint. Therefore, more evidence on the role of sustainability committees in the current scenario is timely and relevant. Accordingly, an exponential increase in publications can be observed in the last few years.

Figure 2.

Sustainability Committee publications by year. Source: own elaboration.

3.1.2. Publications by Countries (RQ2)

The number of publications by country is measured by the affiliation of the authors. Table 1 shows a total of 58 countries from different continents. Significant research activity is developed in Anglo-Saxon countries, where the number of publications is higher, as illustrated by the USA (45), the United Kingdom (35), and Australia (18). Some European countries present between 10 and 20 publications. Yet, these figures are still very low to provide definitive and conclusive evidence regarding sustainability committees, especially considering the challenges that they must currently face. In particular, the implementation of corporate initiatives to achieve SDGs and the coming of stronger legislation on corporate sustainability matters in developed countries [11,45] (for example, the proposal for a Corporate Sustainability Reporting Directive, released in April 2021 by the European Commission), represents an unprecedented milestone for companies in their sustainable development agenda, and the role of sustainability committees is expected to be decisive.

Table 1.

Publications by countries.

In addition, despite the debate concerning the impact of emerging countries on sustainability publications in countries such as China (13), Turkey (9), South Africa (7), India (5), and Malaysia (5) are extremely low. Nevertheless, it is known that developing countries, such as China and Turkey, are incorporating recommendations and regulations to stand out in terms of sustainability [46,47].

3.1.3. Citation Analysis (RQ3)

The citation analysis shows the most influential papers in the research concerning sustainability committees, which is vital for academics to identify the most relevant previous literature and position their studies [48]. In this analysis, global citations are presented, so the citations made by papers both within the sample, and outside of the sample are considered [26].

Table 2 presents the 20 most cited papers. As expected, given the novelty of this research field, the citations of the papers included in our sample remain relatively low. Only three papers exceed 200 citations: Berrone & Gómez-Mejia (2009) [49], Liao et al., (2015) [18], and Schraufnagel et al., (2019) [50] with 504, 463, and 275 citations respectively.

Table 2.

Citation analysis. Top 20 publications.

A closer look at these documents and the journals where they are published confirms the multidisciplinary character of the research on sustainability committees. Indeed, just these 20 papers have been published in numerous different research categories: Biochemistry Molecular Biology, Business, Business Finance, Critical Care Medicine, Engineering Environmental, Environmental Science, Green Sustainable Science Technology, Management, and Respiratory System, among others.

3.1.4. Author’s Impact and Productivity (RQ4)

Nowadays it is more and more common to develop a research project sharing authorship with specialists in the field from other institutions and even from other countries. The network of professionals that is currently being created is increasingly dense, so it is necessary for researchers to perform more specialized studies and connect with those authors who have a greater impact on research [51]. Therefore, this analysis will be helpful for academics to implement a more centralized and specialized study on the topic in question [23] as well as establish contact with the most relevant researchers, thus making sharing ideas or even working on a new paper possible.

This analysis includes 528 authors who are part of the sample. Table 3 displays the 20 authors with the greatest impact, the number of publications, and their affiliations. The impact has been measured by the authors’ citations [52]. As expected, the number of citations of these authors is moderate, with only nine of them exceeding 500 citations, and Schraufnagel, D.E. having the highest number of citations (693).

Table 3.

Author analysis. Top 20 authors.

3.2. Network Analysis

3.2.1. Co-Authorship Analysis (RQ4)

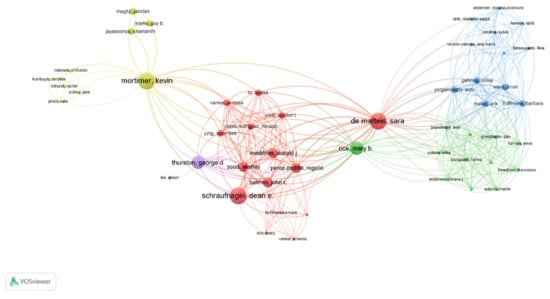

The analysis of co-authorship, through the research of networks, enables us to know the existing relationships between the authors within our sample. This is important for academics so that they can position their work and find future collaborations with the rest of the authors.

In Figure 3 we can find the most significant network of co-authorship. Within 528 authors participating in the sample, a list of 50 authors who have collaborated with each other is presented. Different clusters can be observed, which include different groups of authors who, having collaborated more with each other, have a stronger relationship. A more in-depth analysis of the authors that make up these clusters reveals that these groups of authors focus on research areas such as “Environmental Science”, “Green sustainable Science technology” and “Environmental studies”. This highlights the lack of strong research networks in other areas like Business or Management.

Figure 3.

Co-authorship analysis.

3.2.2. Keywords Co-Occurrence Analysis (RQ5)

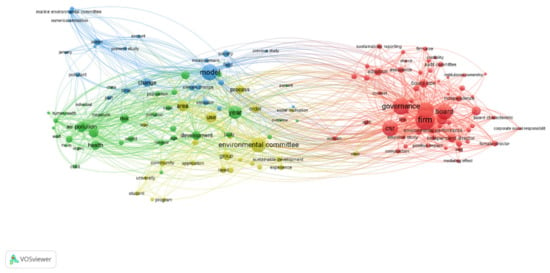

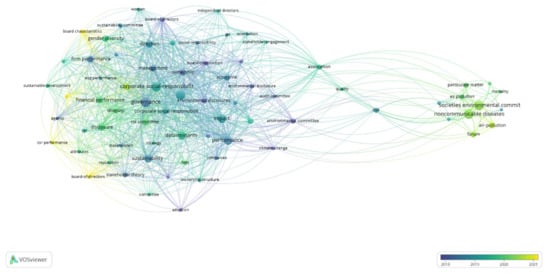

This analysis is divided into two stages. First, the words that co-occur the most within sustainability committee research, with a minimum of 5 times, both in the titles, keywords, and abstracts of the papers, are included in the VOSviewer software creating a network. Figure 4 presents the map with the relationships between the keywords. This mapping technique is useful since it connects the keywords by creating different clusters, which facilitates the thematic grouping of the words. This analysis is highly relevant since it provides a picture of the research themes and allows recognition of research trends. This is fundamental for scholars in the identification of research gaps and in the positioning of their papers. Second, once the different themes are sorted by the clusters, we proceed to analyze the words that most co-occur in each of them. This is displayed in Table 4.

Figure 4.

Keywords analysis.

Table 4.

The 10 keywords that co-occur the most for each cluster.

Figure 4 provides interesting information regarding the research themes by highlighting the existence of four different clusters. First, the red cluster focuses on corporate governance, including keywords like “board”, “board size”, “board independence”, “independent director”, “audit committee”, and “institutional ownership”. Second, the green cluster relates to human care, and contains keywords such as “air pollution”, “exposure”, “body”, “risk”, “health”, “population”, and “child”, among others. Third, the blue cluster considers the use of resources, comprising terms like “emissions”, “climate change”, “water”, “marine environmental committee”, and “ocean model”. Finally, the yellow cluster focuses on keywords related to management, for instance, “committee”, “experience”, “organization”, and “system”.

Furthermore, to understand the development of sustainability committee research and its current trends, an additional analysis is performed to examine how these clusters have evolved. This is presented in Figure 5. To that end, this cluster analysis is replicated only for the last four years of our study and brings to light that research on the field of corporate governance has clearly been strengthened. The configuration of this committee as well as its interaction with the board of directors’ characteristics remains a major research theme.

Figure 5.

Overlay keywords analysis (2018–2021).

4. Discussion

Table 5 provides a summary of the research questions and the main findings. On the one hand, the descriptive analysis indicates that, despite the urgency and importance of the integration of sustainability in the business field, the number of publications on sustainability committees still remains low (RQ1), which emphasizes the need for more research to understand how firms respond to regulatory and societal pressures on sustainability matters. At the same time, this analysis displays the contexts that have been most analyzed and which ones may benefit from further exploration (RQ2). While the mainstream of research has been developed in Anglo-Saxon countries, future studies can definitely explore other institutional contexts with different features, such as individual continental European countries and emerging economies. In addition, our findings indicate the existence of a very fragmented literature, composed of studies with different focuses, and highlight the main documents and authors in this research field (RQ3 and RQ4). This is relevant for scholars to position their future research.

Table 5.

Summary of the main findings.

On the other hand, the network analysis identifies author collaboration (RQ4) within the research field and shows a small group of interconnected scholars. However, the interconnection is still limited in business and management, and we encourage researchers to enhance their international collaboration to expand frameworks regarding sustainability committees, especially in these fields. Since sustainable development is a global challenge, collaborative and integrative approaches may be needed to develop more conclusive evidence. Therefore, future studies might gather and analyze more data on authorships. In addition, the cluster analysis (RQ5) reveals important patterns related to the development of the discipline and provides a basis for recognizing and addressing gaps in the existing literature, which represents key information for academics in guiding their research. Specifically, this analysis suggests that future studies can delve into more specific themes and theoretical approaches, still little explored, thus offering great research opportunities.

First, with regards to the research themes, in light of the increasing pressures for firms to develop sustainable strategies, studies may investigate in-depth concerning: (a) the composition of sustainability committees; and (b) their effects on companies’ outcomes. This would provide valuable evidence for policymakers in refining their corporate governance reforms, and for firms in defining their corporate governance mechanisms.

In relation to the composition of sustainability committees (a), the cluster analysis reveals a clear research gap regarding the examination of the relevance of specific characteristics of sustainability committee members, such as their demographic features (gender, age, nationality), human capital (experience, tenure) or social capital (interlocking). There is no single approach to sustainability committees. Researchers would need to reflect on the measures for the composition of these committees, as different options can be considered. In this regard, the individual characteristics of directors can be further studied. The design of multidimensional constructs integrating various characteristics may represent an alternative measure. In addition, future studies can also consider variables that measure the interaction among personal characteristics of sustainability committee members.

On the other hand, the analysis of the impact of sustainability committees (b) also represents an important research opportunity. In this sense, it is essential to ascertain how these committees can respond to the enhanced sustainability reporting standards, since the existing evidence is negligible. In the United States and the European Unión, regulation is increasingly forcing firms to disclose detailed information on climate change (use of energy, greenhouse gases emission, transition, and physical risks). In the European context, the coming regulations are even stronger and will require corporate information on other specific issues, such as water resources, biodiversity, and the circular economy. In addition, it is a central issue to study how these committees can address specific SDGs related to corporate policies (for instance, linked to sustainable investment, environmental innovation, energy policies, and climate change, among others). The study of how sustainability committees impact both the reporting process and the implementation of SDG would improve our knowledge about the contribution of these committees to firms’ sustainable development.

Second, in relation to the theoretical frameworks, our network analysis detects a lack of theoretical guidance. Future studies need to investigate the theoretical foundations that can better describe the role of sustainability committees. In this regard, it is important to know whether the decision-making process within this committee may be explained under other frameworks generally employed in the literature on boards of directors (agency theory, resource dependence theory, upper echelons theory, stakeholder theory, among others). From an agency perspective, directors in the sustainability committee should act as a supervisory mechanism of managers and safeguard the interests of the shareholders in terms of sustainable performance [53]. Under the resource dependence theory [54], it is interesting to identify how the skills of sustainability committee members may affect the decision-making process. Upper echelons theory [55] assumes that strategic decisions within the sustainability committee are determined by the directors’ behavioral factors and personality characteristics. Stakeholder theory [56] relies on the idea that the decision-making process within the sustainability committee is conditioned by the engagement of directors with the stakeholders of a firm.

5. Conclusions

Our paper performs a bibliometric analysis of research on sustainability committees across the entire WOS. Using descriptive analysis and network analysis, our study provides a further understanding of sustainability committee research and offers novel insights regarding the intellectual structure of research on this topic.

Our findings have direct implications for academics. As was explained above, academics can use our evidence to understand the intellectual structure of research on sustainability committees and, therefore, position their studies and manage long-term research projects [57]. In addition, our evidence may have implications for public bodies, since bibliometric analyses have recently become a tool for the evaluation of the productivity of academics, as well as other larger units such as departments, universities, or research institutions [58,59].

Finally, several limitations found in this analysis should be considered. First, the main collection of the WOS that has been used is recognized as one of the most relevant in research; notwithstanding, alternative databases have not been considered. Logically, this would broaden the overview of the existing research. Second, the database does not include normative documents or documents from international organizations, so the study is only based on the academic context. The inclusion of regulatory and professional documents could complement our analysis by showing the evolution of sustainability committees from a different perspective. Third, the bibliometric analysis run is a statistical study of a descriptive nature, which means that the content of the relevant documents remains beyond our scope. Therefore, for future research, we suggest extending this study by exploring the content of the documents included in each of the clusters obtained in the study. This could provide a more accurate view of the topics, theories, and methodologies employed in the literature.

Author Contributions

M.D.A.-R.: Conceptualization, methodology, software, validation, formal analysis, writing—original draft preparation; F.B.-U.: Conceptualization, formal analysis, writing—review and editing; E.M.-U.: Conceptualization, formal analysis, writing—review and editing. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Conflicts of Interest

The authors declare no conflict of interest.

References

- EY. De Qué Hablan los Consejos de Administración; EY: London, UK, 2022. [Google Scholar]

- Detthamrong, U.; Chancharat, N.; Vithessonthi, C. Corporate governance, capital structure and firm performance: Evidence from Thailand. Res. Int. Bus. Financ. 2017, 42, 689–709. [Google Scholar] [CrossRef]

- Orazalin, N. Do board sustainability committees contribute to corporate environmental and social performance? The mediating role of corporate social responsibility strategy. Bus. Strat. Environ. 2019, 29, 140–153. [Google Scholar] [CrossRef]

- Pranugrahaning, A.; Donovan, J.D.; Topple, C.; Masli, E.K. Corporate sustainability assessments: A systematic literature review and conceptual framework. J. Clean. Prod. 2021, 295, 126385. [Google Scholar] [CrossRef]

- Teixeira, G.F.G.; Junior, O.C. How to make strategic planning for corporate sustainability? J. Clean. Prod. 2019, 230, 1421–1431. [Google Scholar] [CrossRef]

- Canadian Institute of Chartered Accountings (CICA). Practice Guide: Engagements to Audit GHG Emissions Information; Canadian Institute of Chartered Accountings: Toronto, ON, USA, 2003. [Google Scholar]

- International Auditing and Assurance Standards Board (IAASB). Approved Project Proposal: Assurance Engagements on Carbon Emissions Information; International Auditing and Assurance Standards Board: New York, NY, USA, 2007. [Google Scholar]

- Securities and Exchange Commission (SEC). Commission Guidance Regarding Disclosure Related to Climate Change; SEC: Washington, DC, USA, 2010. [Google Scholar]

- Deloitte. The Audit Committee Frontier—Addressing Climate Change; Deloitte: London, UK, 2021. [Google Scholar]

- KPMG. The Top Issues for Audit Committees in 2021; KPMG: Amstelveen, The Netherlands, 2021. [Google Scholar]

- Securities and Exchange Commission (SEC). The Enhancement and Standardization of Climate-Related Disclosures for Investors; SEC: Washington, DC, USA, 2022. [Google Scholar]

- García-Sánchez, I.M.; Gómez-Miranda, M.E.; David, F.; Rodríguez-Ariza, L. The explanatory effect of CSR committee and assurance services on the adoption of the IFC performance standards, as a means of enhancing corporate transparency. Sustain. Account Manag. Policy J. 2019, 10, 773–797. [Google Scholar] [CrossRef]

- Elmaghrabi, M.E. CSR committee attributes and CSR performance: UK evidence. Corp. Gov. Int. J. Bus. Soc. 2021, 21, 892–919. [Google Scholar] [CrossRef]

- Velte, P. Women on management board and ESG performance. J. Glob. Resp. 2016, 7, 98–109. [Google Scholar] [CrossRef]

- Biswas, P.K.; Mansi, M.; Pandey, R. Board composition, sustainability committee and corporate social and environmental performance in Australia. Pacific. Account. Rev. 2018, 30, 517–540. [Google Scholar] [CrossRef]

- Velte, P.; Stawinoga, M. Do chief sustainability officers and CSR committees influence CSR-related outcomes? A structured literature review based on empirical-quantitative research findings. J. Manag. Control 2020, 31, 333–377. [Google Scholar] [CrossRef]

- Jia, J.; Chapple, L.E. The corporate sustainability committee and its relation to corporate environmental performance. Medit. Account. Res. 2022. [Google Scholar] [CrossRef]

- Liao, L.; Luo, L.; Tang, Q. Gender diversity, board independence, environmental committee and greenhouse gas disclosure. Br. Account. Rev. 2015, 47, 409–424. [Google Scholar] [CrossRef]

- Dienes, D.; Sassen, R.; Fischer, J. What are the drivers of sustainability reporting? A systematic review. Sustain. Account. Manag. Policy J. 2016, 7, 154–189. [Google Scholar] [CrossRef]

- Tingbani, I.; Chithambo, L.; Tauringana, V.; Papanikolaou, N. Board gender diversity, environmental committee and greenhouse gas voluntary disclosures. Bus. Strateg. Environ. 2020, 29, 2194–2210. [Google Scholar] [CrossRef]

- Daim, T.U.; Rueda, G.; Martin, H.; Gerdsri, P. Forecasting emerging technologies: Use of bibliometrics and patent analysis. Technol. Forecast. Soc. Chang. 2006, 73, 981–1012. [Google Scholar] [CrossRef]

- Hota, P.K.; Subramanian, B.; Narayanamurthy, G. Mapping the intellectual structure of social entrepreneurship research: A citation/co-citation analysis. J. Bus. Eth. 2019, 66, 89–114. [Google Scholar] [CrossRef]

- Ferreira, J.J.M.; Fernandes, C.I.; Ratten, V. A co-citation bibliometric analysis of strategic management research. Scientometrics 2016, 109, 1–32. [Google Scholar] [CrossRef]

- Albort-Morant, G.; Leal-Rodríguez, A.L.; Fernández-Rodríguez, V.; Ariza-Montes, A. Assessing the origins, evolution and prospects of the literature on dynamic capabilities: A bibliometric analysis. Eur. Res. Manag. Bus. Econ. 2018, 24, 42–52. [Google Scholar] [CrossRef]

- Amorelli, M.F.; García-Sánchez, I.M. Trends in the dynamic evolution of board gender diversity and corporate social responsibility. Corp. Soc. Responsib. Environ. Manag. 2021, 28, 537–554. [Google Scholar] [CrossRef]

- Kent-Baker, H.; Pandey, N.; Kumar, S.; Haldar, A. A bibliometric analysis of board diversity: Current status, development, and future research directions. J. Bus. Res. 2020, 108, 232–246. [Google Scholar] [CrossRef]

- Mumu, J.R.; Saona, P.; Haque, M.S.; Azad, M.A.K. Gender diversity in corporate governance: A bibliometric analysis and research agenda. Gend. Manag. Int. J. 2021, 37, 328–343. [Google Scholar] [CrossRef]

- Drago, C.; Aliberti, L.A. Interlocking Directorship Networks and Gender: A Bibliometric Analysis. In IPAZIA Workshop on Gender Issues; Springer: Cham, Switzerland, 2018; pp. 115–136. [Google Scholar]

- Caiazza, R.; Simoni, M. Directorate ties: A bibliometric analysis. Manag. Decis. 2019, 57, 2837–2851. [Google Scholar] [CrossRef]

- Behrend, J.; Eulerich, M. The Intellectual Structure of Audit Committee Research: A Bibliometric Analysis (1969–2020). SSRN Electron. J. 2022. [Google Scholar] [CrossRef]

- Baatwah, S.R.; Salleh, Z.; Ahmad, N. Whether Audit Committee Financial Expertise Is the Only Relevant Expertise: A Review of Audit Committee Expertise and Timeliness of Financial Reporting. Issues Soc. Environ. Account. 2013, 7, 86–101. [Google Scholar] [CrossRef]

- Samaha, K.; Khlif, H.; Hussainey, K. The impact of board and audit committee characteristics on voluntary disclosure: A meta-analysis. J. Int. Account. Audit. Tax. 2015, 24, 13–28. [Google Scholar] [CrossRef]

- Ellili, N.O.D. Bibliometric analysis on corporate governance topics published in the journal of Corporate Governance: The International Journal of Business in Society. Corp. Gov. 2022. [Google Scholar] [CrossRef]

- Hallinger, P.A. Meta-Synthesis of Bibliometric Reviews of Research on Managing for Sustainability, 1982–2019. Sustainability 2021, 13, 3469. [Google Scholar] [CrossRef]

- Pritchard, A. Statistical bibliography or bibliometrics? J. Doc. 1969, 24, 348–349. [Google Scholar]

- Zupic, I.; Čater, T. Bibliometric methods in management and organization. Organ. Res. Methods 2015, 18, 429–472. [Google Scholar] [CrossRef]

- Feng, Y.; Zhu, Q.; Lai, K.H. Corporate social responsibility for supply chain management: A literature review and bibliometric analysis. J. Clean. Produc. 2017, 158, 296–307. [Google Scholar] [CrossRef]

- Flores-Sosa, M.; Avilés-Ochoa, E.; Merigó, J.M. Exchange rate and volatility: A bibliometric review. Int. J. Financ. Econs. 2022, 27, 1419–1442. [Google Scholar] [CrossRef]

- Van Eck, N.J.; Waltman, L. Software survey: VOS viewer, a computer program for bibliometric mapping. Scientometrics 2010, 84, 523–538. [Google Scholar] [CrossRef] [PubMed]

- Durieux, V.; Gevenois, P.A. Bibliometric indicators: Quality measurements of scientific publication. Radiology 2010, 255, 342–351. [Google Scholar] [CrossRef] [PubMed]

- Environmental Committee Sees Need for Testing and Performance Standards. Civ. Eng. 1981, 51, 16.

- Council Directive 2014/95/EU of the European Parliament and of the Council of 22 October 2014 Amending Directive 2013/34/EU as Regards Disclosure of Non-Financial and Diversity Information by Certain Large Undertakings and Groups; European Union: Maastricht, The Netherlands, 2014.

- United Nations (UN). Draft Outcome Document of the United Nations Summit for the Adoption of the Post-2015 Development Agenda; A/69/L.85; United Nations: New York, NY, USA, 2015. [Google Scholar]

- United Nations (UN). Paris Agreement Convention on Climate Change (UNFCCC); United Nations: New York, NY, USA, 2015. [Google Scholar]

- European Commission (CSRD). Proposal for a Directive of The European Parliament and of The Council amending Directive 2013/34/EU, Directive 2004/109/EC, Directive 2006/43/EC and Regulation (EU) No 537/2014, as Regards Corporate Sustainability Reporting; European Commission: Luxembourg, 2021. [Google Scholar]

- China Banking Regulatory Commission (CBRC). Green Credit Key Performance Indicators (KPIs); China Banking Regulatory Commission (CBRC): Beijing, China, 2014. [Google Scholar]

- Ministry of Development of the Republic of Turkey. Report on Turkey’s Initial Steps towards the Implementation of the 2030 Agenda for Sustainable Development; Ministry of Development: Ankara, Turkey, 2016. [Google Scholar]

- Pattnaik, D.; Hassan, M.K.; Kumar, S.; Paul, J. Trade credit research before and after the global financial crisis of 2008–A bibliometric overview. Res. Int. Bus. Financ. 2020, 54, 101287. [Google Scholar] [CrossRef]

- Berrone, P.; Gomez-Mejia, L.R. Environmental performance and executive compensation: An integrated agency-institutional perspective. Acad. Manag. J. 2009, 52, 103–126. [Google Scholar] [CrossRef]

- Schraufnagel, D.E.; Balmes, J.R.; Cowl, C.T.; De Matteis, S.; Jung, S.H.; Mortimer, K.; Wuebbles, D.J. Air pollution and noncommunicable diseases: A review by the Forum of International Respiratory Societies’ Environmental Committee, Part 2: Air pollution and organ systems. Chest 2019, 155, 417–426. [Google Scholar] [CrossRef]

- Cisneros, L.; Ibanescu, M.; Keen, C.; Lobato-Calleros, O.; Niebla-Zatarain, J. Bibliometric study of family business succession between 1939 and 2017: Mapping and analyzing authors’ networks. Scientometrics 2018, 117, 919–951. [Google Scholar] [CrossRef]

- Merigó, J.M.; Yang, J.B. Accounting Research: A Bibliometric Analysis. Aust. Account. Rev. 2017, 27, 71–100. [Google Scholar] [CrossRef]

- Fama, E.F.; Jensen, M.C. Separation of ownership and control. J. Law Econ. 1983, 26, 301–325. [Google Scholar] [CrossRef]

- Pfeffer, J.; Salancik, G. The External Control of Organizations: A Resource-Dependence Perspective; Harper and Row: New York, NY, USA, 1978. [Google Scholar]

- Hambrick, D.C.; Mason, P.A. Upper echelons: The organization as a reflection of its top managers. Acad. Manag. Rev. 1984, 9, 193–206. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Pitman: London, UK; Boston, MA, USA, 1984. [Google Scholar]

- Merediz-Solà, I.; Bariviera, A.F. A bibliometric analysis of bitcoin scientific production. Res Int Bus Financ. 2019, 50, 294–305. [Google Scholar] [CrossRef]

- Waltman, L.; Calero-Medina, C.; Koste, J.; Noyons, E.C.M.; Tijssen, R.J.W.; Van Eck, N.J.; van Leeuwen, T.N.; van Raan, A.F.J.; Visser, M.S.; Wouters, P. The Leiden ranking 2011/2012: Data collection, indicators, and interpretation. J. Am. Soc. Inf. Sci.Technol. 2012, 63, 2419–2432. [Google Scholar] [CrossRef]

- Ellegaard, O.; Wallin, J.A. The bibliometric analysis of scholarly production: How great is the impact? Scientometrics 2015, 105, 1809–1831. [Google Scholar] [CrossRef] [PubMed]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).