Abstract

This research aims to investigate the effect of COVID-19 on the performance of small and medium enterprises (SMEs) in emerging markets in Iran, Iraq and Jordan. In order to collect the required data, a standard questionnaire provided in the literature was used. The research period is the second quarter of 2022, and its population includes managers, accountants and auditors engaged in listed and non-listed companies. The research findings indicate that the outbreak of COVID-19 has affected SMEs’ performance in investigated emerging markets. For the first time, this research has examined the impact of COVID-19 on the performance of SMEs in emerging markets. The research was conducted in the three countries of Iran, Iraq and Jordan, which have different environmental conditions indicating the impact of contextual factors on the effects of the spread of COVID-19. The results can be useful for different parties, such as SMEs’ owners and regulatory bodies in similar markets.

1. Introduction

The rapid outbreak of the COVID-19 pandemic has significantly affected economies and financial markets [1,2,3,4,5], companies [1,6,7,8], especially small and medium enterprises (SMEs), as well as their performance [9,10,11]. Therefore, it is necessary to study how such a particular condition has affected business performance, particularly SMEs, as they are both large in number and more sensitive to crises than public companies [12].

The pandemic has caused a sharp increase in uncertainty and various effects on people’s activities [13]. Prior studies [5,11,14,15] also show that pandemics affect different sectors and industries differently. Thus, in some industries, such as health and food, there has been an increase and, in others, a decrease in demand and prosperity [14]. In general, the conditions resulting from the pandemic have caused extensive and unexpected changes in the performance of companies compared to managers’ expectations [11]. Measures taken to deal with the pandemic have also affected economic activity worldwide [11]. Therefore, it is necessary to investigate how the new situation has affected companies’ performance, as this crisis may cause new challenges for business units [16], especially SMEs.

The new situation also provides a unique opportunity to investigate the effects of the pandemic on the SMEs’ performance in different markets, especially emerging markets such as Iran, Iraq and Jordan, which are less regulated and efficient than developed ones [17]. Reviewing the related literature indicates that little research has been conducted on SMEs in emerging markets and no research has been conducted comparatively in three countries: Iran, Iraq and Jordan. The results will show whether, due to different environmental conditions in these countries, the effects of the pandemic on the performance of SMEs are different.

In recent years, Iran has been classified as a country with a high economic vulnerability due to less connection to other economies. Simultaneously, suffering low resilience because of economic sanctions [18,19]. The pandemic raised health and living costs, leading to more severe budget deficits resulting in the bankruptcy of some businesses [20], especially SMEs. On the other hand, following the occupation of ISIS and the civil wars, Iraq has become a disorderly country with low security, weakening the country’s power to deal with this disease [21]. With the closure of major commercial sectors during the quarantine and subsequent systematic curfew, local markets faced reduced customer demand for products and services due to movement restrictions and the suspension of business activities [22]. Reduced domestic demand and capital flows to emerging countries such as Jordan intensified the contraction of GDP by increasing global investment risk [23]. The pandemic has negatively affected businesses due to government responses and changes in the work environment [22]. These conditions provide a unique opportunity to investigate the pandemic’s effects on different environments comparatively, leading to identifying whether contextual factors can affect the pandemic effects.

Based on the presented arguments, this study aims to investigate and comparatively identify the effects of the pandemic on SMEs’ performance in these emerging markets, i.e., Iran, Iraq and Jordan. The results presented in this article can help stakeholders, including legislators, capital market regulators and companies in other markets, especially emerging markets, to deal with the effects of the pandemic and other similar crises. The article has five sections: introduction, literature review, research method, results, discussion and conclusion.

2. Theoretical Foundation and Hypothesis Development

The pandemic has been a significant health crisis worldwide, and different countries and regions have been affected by this epidemic [24]. Due to the highly spreadable nature of the pandemic, countries were forced to adopt quarantine measures, including import restrictions, to prevent the transmission of the virus, which will severely affect businesses [25], especially their performance. In this regard, few studies have examined [11,26,27] the impact of the pandemic on firm performance. According to real options theory, managers delay investment when uncertainty increases, which may lead to the loss of profitable projects [28]. Real options theory is based on the fact that management can substitute decisions as it acquires more information. So, if the future conditions are suitable, the project may be expanded to use these conditions. In other words, the real options theory requires dynamic decision-making [29].

Also, according to the resource-based perspective, business units with valuable resources are more likely to achieve higher financial performance [30]. The outbreak increased shareholder uncertainty and risk, leading to decreased companies’ financing options [31]. The productivity and income of the companies have also been greatly reduced due to the implementation of quarantine measures, which has inevitably led to a decrease in performance [32]. Ref. [27] shows that companies’ return on assets (ROA) has a negative and significant relationship with the epidemic’s severity. Ref. [33] found that the pandemic’s effects reduce financial institutions’ efficiency. Prior research [11,14,27,34,35] also show that the pandemic has a negative and significant impact on the performance of companies, i.e., SMEs. Accordingly, the first hypothesis of the research is as follows:

Hypothesis 1.

There is a negative and significant relationship between the pandemic and financial performance of SMEs.

2.1. The Pandemic and Communication Performance

The spread of this pandemic severely affected the global economy and financial markets worldwide [1,6,7,8]. Quarantine and social distancing restrictions and business closures have been part of the policies and efforts of nations to control the pandemic [36,37]. In other words, the COVID-19 restrictions reduced companies’ physical (due to business closures and social distancing) and non-physical connections [36]. Effective communication for business units is considered an essential factor in reducing tensions, fluctuations and risks leading to high performance requiring individuals, teams and organizations to come together in a functional system and work together towards a common goal [38,39,40,41]. During the pandemic period, it is expected that the communication performance of SMEs has decreased; therefore, the second hypothesis is stated as follows:

Hypothesis 2.

There is a negative and significant relationship between the pandemic and communication performance of SMEs.

2.2. The Pandemic and Internal Processes

In the era of technology, this is the first time the world has faced such a transformation in lifestyle [8,42]. It has caused a change in the activities of many businesses worldwide [2,10] as well as their internal processes [21]. Due to the changes created by the pandemic, businesses need to review their processes and continuous monitoring is needed more than ever [1]. This is a severe warning for managers and business owners who should review and redesign their processes during this period [9]. Therefore, we expect that, in the time of the pandemic, managers of SMEs have turned to reconsider the processes of their business units to improve the performance of companies, so the third hypothesis of the research is as follows:

Hypothesis 3.

There is a positive and significant relationship between the pandemic and changes in SMEs’ internal processes.

2.3. The Pandemic and the Innovation of Companies

Company innovations may include new practices, processes, structures and techniques, which can significantly improve effectiveness [43,44], adaptability of business units [45] and the way they achieve goals [46]. Ref. [47] also defines innovation as introducing a new product and production method, opening a new market, accessing a new source of materials and reorganizing an industry. The importance of innovation can be seen after the epidemic as the demand for medical equipment, drugs and advanced IT solutions has increased [12].

Having an innovation for business units to increase performance has long been one of the most critical issues [48]. A firm’s innovation appears to be a multidimensional concept, meaning that it includes various theoretical and empirical components that may/may not be related to each other [49]. Some research programs encourage researchers to move away from focusing only on specific aspects of company’s performance and instead adopt a more comprehensive and creative approach [50,51]. Ref. [52] points out that, in today’s dynamic and chaotic world, business environment changes or company strategies may require a revision of their performance measures [7]. Companies’ innovation to improve performance has always been the attention of management teams and researchers [35]. Therefore, identifying or creating innovation factors during the pandemic can lead companies to surpass their competitors. For example, commercial banks that used e-banking and promoting internet methods performed better during the pandemic than their competitors [53]. Thus, according to what was said, it is expected that the pandemic has a significant impact on the innovation of companies, i.e., SMEs; therefore, the fourth hypothesis of the research is stated as follows:

Hypothesis 4.

There is a positive and significant relationship between the pandemic and SMEs’ innovation.

3. Research Methods

This research is practical in terms of purpose and type and is based on the analysis of data collected in a survey. In order to design the required questionnaire for doing the research, a questionnaire developed by [54] was considered. In addition, according to the literature, the questions were classified into four groups, including financial performance [11,14], communication performance [36,38], changes in the internal process [1,21] and innovation [7,53]. The financial performance group includes 20 questions, the communication performance group consists of 7 questions; the changes in internal process group includes 5 questions; and the innovation part includes 6 questions. In addition, according to the country’s structure and culture, several questions appropriate to the research topic were added to the questionnaire to measure the variables better. The study population of the current research consists of CEOs, financial managers, accountants, internal auditors and external auditors of listed and non-listed companies in Iran, Iraq and Jordan. The questionnaire was distributed virtually and through e-mail among the members of the statistical sample. Finally, 236 questionnaires from Iran, 197 from Iraq and 69 from Jordan have been collected. The collected questionnaires relate to 10 different industries and are coded from 1 to 10. Variance analysis test was applied to analyze the collected data and compare the results per the classification provided. SPSS and SmartPLS 3 statistical software were also used in this process.

4. Results

Table 1 and Table 2 show the frequency of demographic data in Iran, Iraq and Jordan. According to Table 1, most of the respondents to the questionnaire in all three countries were men. Most of respondents in Iran are between 25 and 30 years old, and in Iraq and Jordan, 36 and 40 years old. Also, the largest group in all three countries has a bachelor’s degree, and the largest number of respondents in all three countries are accountants. According to Table 2, among the respondents in the three countries, the most work experience is related to the accounting group. The largest group of respondents in Iran has less than five; in Iraq, they have twenty-one and over; and in Jordan, they have five to ten years of work experience, which in all three countries are related to the chemical, manufacturing and pharmaceutical industries, respectively.

Table 1.

The Frequency of demographic data (gender, age, education and occupation).

Table 2.

The frequency of demographic data of the three countries of Iran, Iraq and Jordan (work history including duration and work experience, industry).

According to Table 2, the completed questionnaire has covered ten industries coded from one to ten.

Before examining the research hypotheses, the validity and reliability of the research questionnaire are examined. Table 3 shows Cronbach’s alpha, composite reliability and extracted mean-variance indicators. The alpha coefficient for the Iranian questionnaire is equal to 0.881; for the Iraqi questionnaire, it is equal to 0.814; for the Jordanian questionnaire, it is equal to 0.852, which is in the appropriate range.

Table 3.

The Reliability and validity findings of the research.

The AVE index in Table 3 states that the average extracted variance of each model dimension has a value greater than 0.5. Therefore, the convergent validity of the model is confirmed. According to Table 3, the AVE value for the model’s variables is higher than 0.5, so, the convergence index can be used for the convergence validity of the measurement model.

In order to measure the goodness of fit of the current research, two indices are used, the results of which are presented in Table 4. It can be concluded that the model fitting is suitable for the data of Iran, Iraq and Jordan and the results will be reliable.

Table 4.

The goodness of fit criteria.

In Table 5, the results of the average equality test of the three countries of Iran, Iraq and Jordan are presented in order to investigate the impact of the pandemic on the financial performance of SMEs. Accordingly, the columns that have been specified show a significant difference in the average of the three countries at the 95% confidence level. Other columns indicate equality and no difference between the average financial performance of the three countries.

Table 5.

The results of variance analysis of the average financial performance of Iran, Iraq and Jordan.

In Table 6, the results of the average equality test of the three countries are presented in order to investigate the impact of the pandemic on the communication performance of SMEs. The average answers are equal to each other. Therefore, there is no significant difference between the countries. The only difference is related to the rental conditions between the lessor and the tenant. The rental condition in Iraq has been less affected by the spread of this disease compared to Iran and Jordan.

Table 6.

The results of the analysis of the variance of the average communication performance of Iran, Iraq and Jordan.

Table 7 shows the results of the average equality test investigating the impact of the pandemic on companies’ business processes. The average answers received by the three countries in the field of the effect of corona on the processes are equal to each other. Therefore, there is no significant difference between the received answers. The only difference between the three countries in this area is related to the fact that the companies in Jordan have developed and implemented at their own expense a less protective program to protect employees against the corona disease than in Iran and Iraq.

Table 7.

The results of the variance analysis test of the average changes in internal processes of Iran, Iraq and Jordan.

Table 8 shows the results of the average equality test investigating the impact of the pandemic on the performance of competitive advantage. The average answers received are equal to each other. Therefore, there is no significant difference between the received answers. The only difference between the three countries in this area is related to the fact that the compensation for the decrease in the volume of online sales in Jordan is less than in Iran and Iraq.

Table 8.

The results of the analysis of the variance of the average innovation performance of Iran, Iraq and Jordan.

The questionnaire includes four parts (Table 9): financial performance (including twenty questions), communication performance (seven questions), business processes (five questions) and innovation performance (six questions). In Table 9, Cronbach’s alpha of each part of the questionnaire is also presented. It is for the Iran questionnaire in the range between 0.839 and 0.993, for Iraq in the range between 0.685 and 0.922 and for Jordan in the range between 0.653 and 0.969, indicating a good internal structure.

Table 9.

Components; Number of questions, Cronbach’s alpha and factor analysis results.

In Table 10, the descriptive statistics of the research variables, including financial performance, communication, innovation and business processes, for the three countries of Iran, Iraq and Jordan, are presented separately. The average responses received for the financial performance of Jordan, Iran and Iraq, respectively, are equal to 2.440, 2.448 and 2.519. Considering that the answers are coded from one to five from completely agree to completely disagree, the coronavirus’s spread has affected Jordan’s financial performance more than Iran and Iran more than Iraq. Similarly, the coronavirus outbreak has affected the communication performance of Iran more than Iraq and Iraq more than Jordan. Despite the wide spread of this disease, business processes have been affected more in Iraq than Iran and Iran more than Jordan. Also, the pandemic has affected Iraq’s innovation performance more than Iran and Iran more than Jordan.

Table 10.

The Descriptive statistics of hidden variables of the study.

The relationship between the four functional components of the company and the significance level of this relationship have been measured. According to Table 11, all four components have a positive and significant effect on each other at the 99% level. In Table 12 and Table 13, according to the results of Iran, the positive and significant correlation of four variables is clearly shown. Therefore, the spread of the coronavirus has reduced the financial performance, communication, innovation and changes in internal processes simultaneously and in the same direction in all three countries.

Table 11.

The Correlation matrix of research components for Iranian data.

Table 12.

Correlation matrix of research components for Iraqi data.

Table 13.

Correlation matrix of research components for Jordanian data.

The results of testing research hypotheses are presented in Table 14. As can be seen from the Table 14, all the hypotheses are approved. They indicate that the pandemic has a negative and significant relationship with financial performance, which approves the first hypothesis. This result is similar to the results of some prior research e.g., [11,54,55,56,57], although other research provides different results [58,59]. The results also show that the pandemic has a negative and significant relationship with communication performance, approving the second hypothesis, which is similar to [60]’s findings. A positive and significant relationship between the pandemic and changes in internal processes supports the third hypothesis, which is consistent with [61]’s results. In addition, the pandemic has a positive and significant relationship with innovation supporting the fourth hypothesis, consistent with [22,62]’s findings. Comparing the findings also shows no significant difference between the countries, implying that the pandemic has similar significant effects on different emerging markets investigated.

Table 14.

Hypotheses test results.

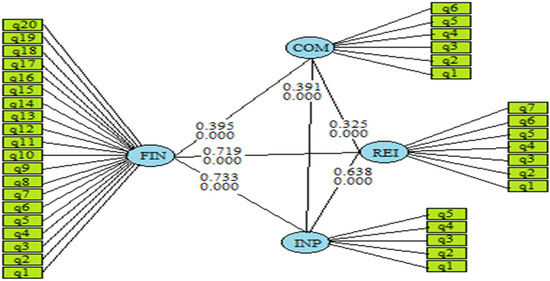

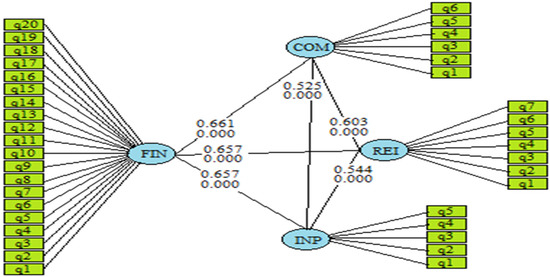

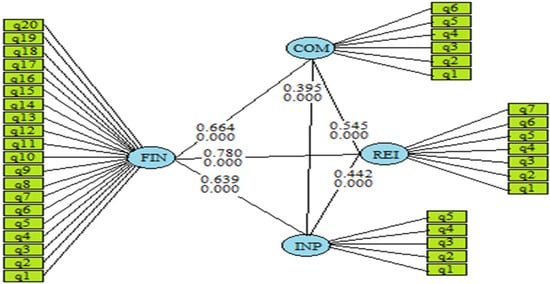

In Figure 1, Figure 2 and Figure 3, respectively, the output and the effect of hidden and obvious variables of Iran, Iraq and Jordan questionnaires are drawn. The results of Table 10, Table 11, Table 12 and Table 13, and the output of PLS 3 software indicate a strong positive correlation between the four functional components of SMEs.

Figure 1.

The effect of the obvious and hidden variables of Iran’s data.

Figure 2.

The effect of obvious and hidden variables of Iraq data.

Figure 3.

The effect of obvious and hidden variables of Jordanian data.

The research results indicate the high impact of the outbreak of the corona disease on the performance of SMEs in the three countries of Iran, Iraq and Jordan. Also, the effect of performance sub-indices, including financial performance, communication, innovation and changes in internal processes by industry, was investigated using the data collected from the Iran, Iraq and Jordan questionnaire. Examining research hypotheses from different methods does not differ significantly from each other, which indicates the strength of the results.

5. Discussion

The results of the research data analysis support all the hypotheses indicating that the spread of the coronavirus has affected SMEs’ performance in different emerging markets (Iran, Iraq and Jordan). They show a negative relationship between the pandemic and financial performance, implying that the limitations imposed on the SMEs lead them to lower financial performance. This result is consistent with prior research e.g., [11,14,27,33,35] indicating that COVID-19 negatively affects companies’ financial performance. There is a negative relation between the pandemic and communication performance, as the pandemic has reduced face-to-face communication. This result is consistent with [60]’s findings. In addition, the results show a positive relation between the pandemic and changes in SMEs’ internal processes. The pandemic has forced SMEs to apply more advanced technologies and methods such as digital marketing and trading and automation of internal processes, resulting in increased changes in business processes. This is in line with prior research e.g., [22,61,63]. In addition, the pandemic has caused companies to be more active in research and development activities resulting in more innovation. This is consistent with prior research [62,64,65]. There is no significant difference between the countries, although the level of effect differs in different markets. For example, the findings show that it has affected Jordan’s financial performance more than Iran’s and Iran’s more than Iraq’s because, with the spread of the corona disease, Jordan has had a greater decrease in the company’s future cash flows and a greater increase in price fluctuations compared to Iran and Iraq. In addition, the decrease in the prices of goods in Iran has been more intense than in Iraq and Jordan. Similarly, the pandemic has affected Iran’s communication performance more than Iraq and Iraq more than Jordan. The findings imply that the pandemic has resulted in decreased financial and communication performance and increased changes in SMEs’ internal processes and innovation. The COVID-19 pandemic caused a decrease in the performance of SMEs. It may be a result of increased social distancing and the closure and reduction in the activity of most economic enterprises and SMEs in countries. Companies try to use more advanced technologies in this situation, resulting in increased changes in internal processes and innovation.

6. Conclusions

The study provides important findings about the impact of the COVID-19 outbreak on the performance of SMEs in emerging markets in Iran, Iraq and Jordan. As a result of the pandemic, financial and communication performance decreased and changes in internal processes and innovation increased in SMEs in the emerging markets investigated. Although the pandemic put some limitations on the SMEs’ operations resulting in decreased financial and communication performance, it has forced them to apply more advanced and sophisticated technologies and methods in their business activities and processes, resulting in increased changes in internal processes and innovation. The results also show that the pandemic has similarly affected SMEs’ performance in different countries with different contextual factors, although the effect level differs.

These findings have several important implications. First, they can help SMEs’ owners better understand the pandemic’s potential effects on different aspects of their companies’ performance. Secondly, they guide the regulatory bodies and other related parties to support SMEs in dealing with the pandemic’s effects and similar events. The study has some limitations regarding sampling as it includes only SMEs. In addition, it only focuses on SMEs in three emerging markets. Therefore, future studies need to examine other companies and markets.

Author Contributions

Methodology, M.A.B.V.; Formal analysis, S.H.; Investigation, S.J.M.; Resources, B.K.A.A. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

Data will be available at request.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Chen, H.C.; Yeh, C.W. Global financial crisis and COVID-19: Industrial reactions. Financ. Res. Lett. 2021, 42, 101940. [Google Scholar] [CrossRef] [PubMed]

- Zou, P.; Huo, D.; Li, M. The impact of the COVID-19 pandemic on firms: A survey in Guangdong Province, China. Glob. Health Res. Policy 2020, 5, 41. [Google Scholar] [CrossRef] [PubMed]

- Liu, L.; Wang, E.Z.; Lee, C.C. Impact of the COVID-19 pandemic on the crude oil and stock markets in the US: A time-varying analysis. Energy Res. Lett. 2020, 1, 13154. [Google Scholar] [CrossRef]

- Iyke, B.N. COVID-19: The reaction of US oil and gas producers to the pandemic. Energy Res. Lett. 2020, 1, 13912. [Google Scholar] [CrossRef]

- Phan, D.H.B.; Narayan, P.K. Country responses and the reaction of the stock market to COVID-19—A preliminary exposition. Emerg. Mark. Financ. Trade 2020, 56, 2138–2150. [Google Scholar] [CrossRef]

- Piccarozzi, M.; Silvestri, C.; Morganti, P. COVID-19 in management studies: A systematic literature review. Sustainability 2021, 13, 3791. [Google Scholar] [CrossRef]

- Islam, D.M.Z.; Khalid, N.; Rayeva, E.; Ahmed, U. COVID-19 and financial performance of SMEs: Examining the nexus of entrepreneurial self-efficacy, entrepreneurial resilience and innovative work behavior. Rev. Argent. Clínica Psicológica 2020, 29, 587. [Google Scholar]

- Xu, L.; Yang, S.; Chen, J.; Shi, J. The effect of COVID-19 pandemic on port performance: Evidence from China. Ocean Coast. Manag. 2021, 209, 105660. [Google Scholar] [CrossRef]

- Fu, M.; Shen, H. COVID-19 and corporate performance in the energy industry. Energy Res. Lett. 2020, 1, 1–4. [Google Scholar] [CrossRef]

- Khatib, S.F.; Nour, A.N.I. The impact of corporate governance on firm performance during the COVID-19 pandemic: Evidence from Malaysia. J. Asian Financ. Econ. Bus. 2021, 8, 0943–0952. [Google Scholar]

- Shen, H.; Fu, M.; Pan, H.; Yu, Z.; Chen, Y. The impact of the COVID-19 pandemic on firm performance. Emerg. Mark. Financ. Trade 2020, 56, 2213–2230. [Google Scholar] [CrossRef]

- Markovic, S.; Koporcic, N.; Arslanagic-Kalajdzic, M.; Kadic-Maglajlic, S.; Bagherzadeh, M.; Islam, N. Business-to-business open innovation: COVID-19 lessons for small and medium-sized enterprises from emerging markets. Technol. Forecast. Soc. Chang. 2021, 170, 120883. [Google Scholar] [CrossRef]

- Baker, S.; Bloom, N.; Davis, S.; Terry, S. COVID-induced economic uncertainty and its consequences. Behav. Exp. Financ. 2020, 27, 100326. [Google Scholar] [CrossRef]

- Veselinova, E.; Samonikov, M.G. The Impact of COVID-19 Pandemic on Firms Performance: Analysis of the Companies from the MBI10 Index. J. Econ. 2021, 6, 174–184. [Google Scholar] [CrossRef]

- Baek, S.; Mohanty, S.K.; Glambosky, M. COVID-19 and stock market volatility: An industry level analysis. Financ. Res. Lett. 2020, 37, 101748. [Google Scholar] [CrossRef]

- Kraus, S.; Clauss, T.; Breier, M.; Gast, J.; Zardini, A.; Tiberius, V. The economics of COVID-19: Initial empirical evidence on how family firms in five European countries cope with the corona crisis. Int. J. Entrep. Behav. Res. 2020, 26, 1067–1092. [Google Scholar] [CrossRef]

- Bagherpour, M.A.; Monroe, G.S.; Shailer, G. Government and managerial influence on auditor switching under partial privatization. J. Account. Public Policy 2014, 33, 372–390. [Google Scholar] [CrossRef]

- Briguglio, L.P. Exposure to external shocks and economic resilience of countries: Evidence from global indicators. J. Econ. Stud. 2016, 43, 1057–1078. [Google Scholar] [CrossRef]

- Cannavale, C.; Zohoorian Nadali, I.; Esempio, A. Entrepreneurial orientation and firm performance in a sanctioned economy–does the CEO play a role? J. Small Bus. Enterp. Dev. 2020, 27, 1005–1027. [Google Scholar] [CrossRef]

- Didier, T.; Huneeus, F.; Larrain, M.; Schmukler, S.L. Financing firms in hibernation during the COVID-19 pandemic. J. Financ. Stab. 2021, 53, 100837. [Google Scholar] [CrossRef]

- Ahmed, S.Y. Impact of COVID-19 on Performance of Pakistan Stock Exchange No. 101540; MPRA Paper: Lahore, Pakistan, 2020. [Google Scholar]

- Abuhussein, T.; Barham, H.; Al-Jaghoub, S. The effects of COVID-19 on small and medium-sized enterprises: Empirical evidence from Jordan. J. Enterprising Communities People Places Glob. Econ. 2023, 17, 334–357. [Google Scholar] [CrossRef]

- World Bank. Jordan Economic Update, October 2020. Available online: https://thedocs.worldbank.org/en/doc/1466316030473586160280022020/original/7mpoam20jordanjorkcm.pdf (accessed on 20 January 2021).

- Kano, L.; Hoon Oh, C. Global Value Chains in the Post-COVID World: Governance for Reliability. J. Manag. Stud. 2020, 57, 1773–1777. [Google Scholar] [CrossRef]

- Gil-Alana, L.A.; Monge, M. Crude Oil Prices and COVID-19-Persistence of the Shock. Energy Res. Lett. 2021, 1, 1–4. [Google Scholar] [CrossRef]

- Alsamhi, M.H.; Al-Ofairi, F.A.; Farhan, N.H.; Al-Ahdal, W.M.; Siddiqui, A. Impact of Covid-19 on firms’ performance: Empirical evidence from India. Cogent Bus. Manag. 2022, 9, 2044593. [Google Scholar] [CrossRef]

- Hu, S.; Zhang, Y. COVID-19 pandemic and firm performance: Cross-country evidence. Int. Rev. Econ. Financ. 2021, 74, 365–372. [Google Scholar] [CrossRef]

- Ming, Z.; Ping, Z.; Shunkun, Y.; Ge, Z. Decision-making model of generation technology under uncertainty based on real option theory. Energy Convers. Manag. 2016, 110, 59–66. [Google Scholar] [CrossRef]

- Song, P. R&D Investment Strategies of Firms: Renewal or Abandonment. A Real Options Perspective. Ph.D. Thesis, Georgia State University, Atlanta, GA, USA, 2009. [Google Scholar]

- Yang, S.; Kang, H.H. Is synergy always good? Clarifying the effect of innovation capital and customer capital on firm performance in two contexts. Technovation 2008, 28, 667–678. [Google Scholar] [CrossRef]

- Shafeeq Nimr Al-Maliki, H.; Salehi, M.; Kardan, B. The effect of COVID 19 on risk-taking of small and medium-sized, family and non-family firms. J. Facil. Manag. 2023, 21, 298–309. [Google Scholar] [CrossRef]

- Jorgensen, S.C.; Kebriaei, R.; Dresser, L.D. Remdesivir: Review of pharmacology, pre-clinical data, and emerging clinical experience for COVID-19. Pharmacother. J. Hum. Pharmacol. Drug Ther. 2020, 40, 659–671. [Google Scholar] [CrossRef]

- Zheng, C.; Zhang, J. The impact of COVID-19 on the efficiency of microfinance institutions. Int. Rev. Econ. Financ. 2021, 71, 407–423. [Google Scholar] [CrossRef]

- Harel, R. The Impact of COVID-19 on Small Businesses’ Performance and Innovation. Glob. Bus. Rev. 2021, 1–22. [Google Scholar] [CrossRef]

- Golubeva, O. Firms’ performance during the COVID-19 outbreak: International evidence from 13 countries. Corp. Gov. 2021, 21, 1011–1027. [Google Scholar] [CrossRef]

- Elmarzouky, M.; Albitar, K.; Hussainey, K. Covid-19 and performance disclosure: Does governance matter? Int. J. Account. Inf. Manag. 2021, 29, 776–792. [Google Scholar] [CrossRef]

- Wu, S.; Zhou, W.; Xiong, X.; Burr, G.S.; Cheng, P.; Wang, P.; Niu, Z.; Hou, Y. The impact of COVID-19 lockdown on atmospheric CO2 in Xi’an, China. Environ. Res. 2021, 197, 111208. [Google Scholar] [CrossRef]

- Fodor, O.C.; Flestea, A.M. When fluid structures fail: A social network approach to multi-team systems’ effectiveness. Team Perform. Manag. 2016, 22, 156–180. [Google Scholar] [CrossRef]

- Xie, C.; Wu, D.; Luo, J.; Hu, X. A case study of multi-team communications in construction design under supply chain partnering. Supply Chain Manag. 2010, 15, 363–370. [Google Scholar] [CrossRef]

- Izam Ibrahim, K.; Costello, S.B.; Wilkinson, S. Key practice indicators of team integration in construction projects: A review. Team Perform. Manag. 2013, 19, 132–152. [Google Scholar] [CrossRef]

- Sha’ar, K.Z.; Assaf, S.A.; Bambang, T.; Babsail, M.; Fattah, A.A.E. Design–construction interface problems in large building construction projects. Int. J. Constr. Manag. 2017, 17, 238–250. [Google Scholar] [CrossRef]

- Goswami, B.; Mandal, R.; Nath, H.K. COVID-19 pandemic and economic performances of the states in India. Econ. Anal. Policy 2021, 69, 461–479. [Google Scholar] [CrossRef]

- Vaccaro, I.G.; Jansen, J.J.; Van Den Bosch, F.A.; Volberda, H.W. Management innovation and leadership: The moderating role of organizational size. J. Manag. Stud. 2012, 49, 28–51. [Google Scholar] [CrossRef]

- Mothe, C.; Uyen Nguyen Thi, T. The link between non-technological innovations and technological innovation. Eur. J. Innov. Manag. 2010, 13, 313–332. [Google Scholar] [CrossRef]

- Gorzelany-Dziadkowiec, M. COVID-19: Business innovation challenges. Sustainability 2021, 13, 11439. [Google Scholar] [CrossRef]

- Birkinshaw, J.; Hamel, G.; Mol, M.J. Management innovation. Acad. Manag. Rev. 2008, 33, 825–845. [Google Scholar] [CrossRef]

- Schumpeter, J.A.; Grzywicka, J.; Górski, J. Teoria Rozwoju Gospodarczego; Państwowe Wydawnictwo Naukowe: Kasinka Mała, Poland, 1960. [Google Scholar]

- Devinney, T.M.; Yip, G.S.; Johnson, G. Using frontier analysis to evaluate company performance. Br. J. Manag. 2010, 21, 921–938. [Google Scholar] [CrossRef]

- Fernández-Temprano, M.A.; Tejerina-Gaite, F. Types of director, board diversity and firm performance. Corp. Gov. 2020, 20, 324–342. [Google Scholar] [CrossRef]

- Ferreira, A.; Otley, D. The design and use of performance management systems: An extended framework for analysis. Manag. Account. Res. 2009, 20, 263–282. [Google Scholar] [CrossRef]

- Giovannoni, E.; Pia Maraghini, M. The challenges of integrated performance measurement systems: Integrating mechanisms for integrated measures. Account. Audit. Account. J. 2013, 26, 978–1008. [Google Scholar] [CrossRef]

- Melnyk, S.A.; Bititci, U.; Platts, K.; Tobias, J.; Andersen, B. Is performance measurement and management fit for the future? Manag. Account. Res. 2014, 25, 173–186. [Google Scholar] [CrossRef]

- Chavda, M.V. Effectiveness of E-banking during COVID 19 Pandemic. Int. J. Adv. Res. Comput. Commun. Eng. 2021, 10, 1–5. [Google Scholar] [CrossRef]

- El-Mousawi, H.; Kanso, H. Impact of COVID-19 outbreak on financial reporting in the light of the international financial reporting standards (IFRS) (an empirical study). Res. Econ. Manag. 2020, 5, 21–38. [Google Scholar] [CrossRef]

- Dai, R.; Feng, H.; Hu, J.; Jin, Q.; Li, H.; Wang, R.; Xu, L.; Zhang, X. The impact of COVID-19 on small and medium-sized enterprises (SMEs): Evidence from two-wave phone surveys in China. China Econ. Rev. 2021, 67, 101607. [Google Scholar] [CrossRef]

- Martin, D.; Neale, E.A.; Bertini, R.; Smith-Omomo, J.; Aymerich, O. Impact of Covid-19 on Small-and Medium-sized Enterprises in Iraq; Working Paper; Economic Research Forum (ERF): Baghdad, Iraq, 2022. [Google Scholar]

- Atayah, O.F.; Dhiaf, M.M.; Najaf, K.; Frederico, G.F. Impact of COVID-19 on financial performance of logistics firms: Evidence from G-20 countries. J. Glob. Oper. Strateg. Sourc. 2022, 15, 172–196. [Google Scholar] [CrossRef]

- Cui, L.; Kent, P.; Kim, S.; Li, S. Accounting conservatism and firm performance during the COVID-19 pandemic. Account. Financ. 2021, 61, 5543–5579. [Google Scholar] [CrossRef]

- Ren, Z.; Zhang, X.; Zhang, Z. New evidence on COVID-19 and firm performance. Econ. Anal. Policy 2021, 72, 213–225. [Google Scholar] [CrossRef]

- Rahman, M.D.; Mutsuddi, P.; Roy, S.K.; Amin, M.; Jannat, F. Performance efficiency evaluation of information and communication technology (ICT) application in human resource management during COVID-19 pandemic: A study on banking industry of Bangladesh. South Asian J. Soc. Stud. Econ. 2020, 8, 46–56. [Google Scholar] [CrossRef]

- Siagian, H.; Tarigan, Z. The central role of it capability to improve firm performance through lean production and supply chain practices in the COVID-19 era. Uncertain Supply Chain Manag. 2021, 9, 1005–1016. [Google Scholar] [CrossRef]

- Behbahaninia, P.S.; Golbidi, M. The effect of R&D activities on the market response and company’s performance during the shock caused by the COVID-19 pandemic in Iran. J. Appl. Account. Res. 2022, 23, 884–896. [Google Scholar] [CrossRef]

- Lestari, D.; Siti, M.; Wardhani, W.; Yudaruddin, R. The impact of COVID-19 pandemic on performance of small enterprises that are e-commerce adopters and non-adopters. Probl. Perspect. Manag. 2021, 19, 467. [Google Scholar] [CrossRef]

- Christa, U.; Kristinae, V. The effect of product innovation on business performance during COVID 19 pandemic. Uncertain Supply Chain Manag. 2021, 9, 151–158. [Google Scholar] [CrossRef]

- Sharma, G.D.; Kraus, S.; Srivastava, M.; Chopra, R.; Kallmuenzer, A. The changing role of innovation for crisis management in times of COVID-19: An integrative literature review. J. Innov. Knowl. 2022, 7, 100281. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).