1. Introduction

Environment plays a key role in economic activities by directly providing inputs to produce goods and services or through indirect services provided by ecosystems [

1,

2]. Natural resources are therefore vital to ensuring growth and economic development for present and future generations [

3]. The Brundtland report defines sustainable development as one which satisfies present needs without compromising the capacity of future generations to meet their own needs—that is, the degree to which natural capital must be saved, which includes the sum of all environmental goods used by the society for three fundamental purposes: environmental services, resources provision, and waste disposal [

4,

5,

6].

According to [

7], the economy is sustainable only if natural ecosystems are resilient. As such, it is important to understand the dynamics and processes by which nature self-sustains and continues to exist despite disturbances and changes, or, in the words of [

8], its capacity for resilience. This concept is related to an ecosystem’s ability to absorb changes and shocks while keeping the same relation between its populations and functions so that it allows for the provision of environmental goods and services [

9,

10]. These changes are measured from the moment a specific ecological threshold is exceeded, which leads to substantial degradation or collapse of the ecosystem, causing permanent loss of natural capital. Resilience allows the ecosystem to return to a similar state after a disturbance, depending on how close or far it is from that threshold. This concern also extends to the protection of water bodies and drinking water supply [

11].

Until the 1960s, economic models assumed the existence of endless natural resources. According to [

12], inputs would become products without consideration of the impacts of pollution, or of the fact that consuming them might cause their disappearance, such that the economy was formally isolated from environmental dynamics. As of the 1970s, negative externalities caused to the environment due to production and consumption activities took on a fundamental role in economic formulation with the development of the first general equilibrium model (GEM), which represented these market failures [

13,

14]. In the 1990s, concern extended to incorporate not only the depletion of natural resources but also the loss of environmental quality or pollution into economic models [

15].

Environmental policies have promoted actions aimed at controlling environmental externalities created by economic activities. These correspond to command and control (CAC) regulations, economic incentives, or a combination of both. This combination is known as “hybrids” [

16], and it is increasingly being studied given that hybrids combine the benefits of CAC and economic incentives, which are juxtaposed to find optimal combinations for the conservation of natural resources at socially desirable levels [

17,

18]. In an emerging country such as Colombia, the water pollution policy is based on a set of norms including information systems, the definition of areas in which economic activities can be carried out, requirements for environmental management plans, the firms’ 1% earmarking for environmental conservation, and the requirement of leaving used land in the exact condition it was found, in addition to a hybrid of norms on the discharge of pollutants (another CAC regulation) and taxes that will be analyzed in this paper. CAC regulations have changed substantially. Before current Resolution 631 of 2015 by the Ministry of the Environment and Sustainable Development, the allowed pollutants discharged into the water were based on a percentage of the level of pollution; now, it is based on specific amounts of discharged pollutants, which are stricter for companies that meet the percentages but whose amounts emitted are high.

Research around the environmental regulatory framework on water pollution in Colombia has shown that the permitted discharges are the same for all polluting agents, regardless of the characteristics of the receiving sources or economic, environmental, and social circumstances, which generates environmentally, technically, socially insufficient, and unsustainable results [

19,

20]. When the impact on pollution levels to assess the effectiveness of taxes was estimated, the results showed diminishing water pollution in the industrial sector, but residential consumers did not respond to these incentives [

21]. However, that study did not consider the existing CAC standards economic agents must also comply with. Likewise, Ref. [

22] studied the impact of applying different taxes on sewage utility fees to residential consumers, finding that the water pollution decrease is significantly low since homes cannot control organic material and suspended solids disposal, based on the costs of sewage services. In addition, taxes harm the lowest-income populations.

Another study recommended using mixed instruments coordinated by different government sectors that allow for the implementation of a national tax to achieve the desired environmental results [

23]. Other studies show a confusing relationship between taxes and CAC regulations that has not been considered in the present study [

24]. However, the combination of economic incentives including license fees, standards, charges, and subsidies reinforced by active enforcement, should lead to an overall improvement in environmental compliance [

25].

We propose a GEM with a body of water endowment that considers its depletion from one period to another due to the relationship between its capacity for resilience and the cumulative effects of pollution over time [

26]; that is, the model includes a body of water as a restriction on the economic system operation, given the basic input for supplying a vital public utility service such as drinking water. This paper tests a hybrid instrument, including taxes and CAC regulations (pollution limits), to reduce water pollution, where taxes are at the upper limit equivalent calculated as the marginal damage produced by pollution on the drinking water supply sector (Pigouvian taxes), and the polluting sector has the option of using an abatement technology to comply with this hybrid environmental regulation. Our article focuses on reviewing to what extent the new CAC regulation would allow for ensuring sustainability in supplying drinking water, as well as on the effects on the different economic sectors and social welfare.

This paper includes five sections besides the introduction. The

Section 2 reviews the literature on hybrid environmental policy instruments; the

Section 3 is a critical review of the evolution of Colombian hybrid instruments to reduce water pollution; the

Section 4 proposes and develops the GEM; the

Section 5 applies and evaluates these policies in the model; and

Section 6, some conclusions and future avenues are presented.

2. Hybrid Water Pollution Policies

The goal of environmental policies is to reduce pollution to a socially desirable level, which, at its best, must align the compensation required for the damage and the social costs associated with the production of polluting goods. Unless the costs of pollution are prohibitively high compared to the social benefits of production, the economic efficiency solution will imply a strictly positive level of pollution. Pollution reduction is introduced using two types of instruments: market (economic) instruments and CAC regulations. Their first aim is to benefit firms that strive to reduce levels of pollution emitted and to punish those that do not reduce it, including setting taxes and permitting auctions. The second regulatory measure relates to mandatory or optional technical and quantity standards regarding permitted pollution levels [

27,

28].

As advised by mainstream economic literature, economic incentives are preferred over other tools, but their effectiveness depends on the ability of the regulator to correctly determine a tax equal to the marginal damage produced by the negative externality [

29]. Moreover, taxes can potentially yield other benefits beyond addressing a country’s fiscal needs [

30]. In addition, the effectiveness of assigning tradable permits depends on additional variables beyond the definition of property rights and low transaction costs [

31]. Likewise, a polluting firm faced with a CAC regulation is bound to maintain the standard required without concern for reducing its emissions to levels below those demanded, which is not the case with taxes, which encourage cost reduction to reduce tax payments [

32].

Evidence concerning environmental pollution and the choice of policy instruments shows that their isolated application will not always have the desired effect since, in several cases, this is insufficient when bearing in mind the complexity of environmental problems. The use of hybrids between standards and economic incentives begins to be appreciated when it is recognized that environmental taxes, among other limitations, do not create incentives to abate emissions per se but rather limit purchases of an item linked with emissions [

33]. The only reason for using pure regulatory instruments, whether prices or CAC regulations, would be the simplicity of some policy issues, a benefit that is outweighed by inefficiency costs [

34].

When taxes and standards are not individually well designed, they could be combined in such a way that economic incentives reduce abatement costs and standards mitigate risks in the amount of pollution [

35]. Hybrids make it easier for regulators to be aware of and monitor developments in abatement technologies [

36], although the institutional development required to implement expanded or more complex policy instruments must be considered [

37].

Uncertainty about the costs of abatement technologies is a major constraint to the use of environmental charges, and hybrids are preferred because they reduce the expected social costs of pollution, i.e., the sum of the costs of damage to the environment and society and the costs of pollution abatement [

16]. Hybrids make it possible to consider complex abatement technology types required to analyze the regulatory instruments selection process considering the costs of available technologies; their degree of substitutability; information asymmetries; and public funds [

38]. From a dynamic perspective, the component related to standards design will depend on firms’ strategies and technological possibilities, given that mitigation costs are unknown [

39]. When uncertainty is extended to pollution mitigation benefits, economic hybrids between fees and charges—including non-linear tariffs—are also preferred [

40].

The existence of different dimensions (political, economic, social, etc.) and several simultaneous trade-offs, such as income distribution, uncertainty, administrative costs, fiscal costs, costs related to monitoring and control, and political feasibility, justify the use of hybrids [

18]. Other papers have mentioned the following as the main criteria to be considered in the construction of hybrids: efficiency under uncertainty, commitment, credibility, flexibility, international issues, and political economy. Both multiple and hybrid instruments are problematic when they are inconsistent with each other, leading to perverse consequences if the interactions between different policies are not carefully considered. It is also necessary to differentiate hybrids from multiple instruments-when applied by different regulatory agencies [

41].

The sequential decision process between the environmental regulator and firms has also been analyzed as an interaction game, showing that if economic incentives fail, environmental objectives can still be achieved by regulatory constraints through hybrid environmental policies [

42].

There should be more applied research to identify potential interactions and select the most economically efficient mix between taxes and standards [

18,

43,

44]. The application of hybrids can result, for example, in redundancy or conflicting measures that increase regulatory management costs unnecessarily with little net benefit to society [

45].

As it is not common in economic analysis to study market failures simultaneously and there is a widespread belief in the fundamental importance of price signals, the most recent or most appreciated analyses focus on studying the properties of hybrids among market instruments only. In the case of the simultaneous use of environmental carbon fees and Cap and Trade, these have been found to ease reduction of firms’ mitigation costs albeit at the expense of more uncertainty about emissions reductions [

46]. Different tradeoffs are also faced when using environmental fees and Feed-in-Tariffs, the latter understood as long-term contracts to renewable energy producers that are mandatory or preferential [

47].

Environmental charges or the combination of different market instruments that are transferred to an increase in the prices of final goods are subject to increase social sensitivity, making them increasingly politically unfeasible. This motivates the use of hybrids between economic instruments and CAC standards in the belief that there will be fewer increases in the prices of final goods [

46,

48].

As general recommendations for the design of hybrid policies, the cited authors highlight avoiding instrument overlapping (except when they can mutually strengthen each other or when they address distinct aspects of the environmental problem), reinforcing instruments that control total pollution levels with those addressing other “multi-aspect” problems (where, when, how, etc.), and using information mechanisms for appropriate monitoring and application. Each government’s capabilities vary regarding intensity of resources, precision of focus, political risk, and ideological and financial limitations, which affects the technical feasibility, political acceptability, and economic viability of the instruments to achieve specific goals [

49]. This means that those responsible for creating hybrid policy options must be sensitive to the behavioral motivations of the target populations and examine the political and economic context before recommending one or several instruments to decision-makers.

3. Hybrid Instruments to Reduce Water Pollution: The Colombian Case

Although water pollution environmental policy in Colombia includes a complex set of norms, standards, and taxes, we focus on analyzing the effect of the hybrid instrument which is composed of pollution limits and taxes (compensatory taxes from here on). Despite the fact limits are a quantity-focused instrument, it may be more accurate to describe them as hybrid instruments, where pollution above the specified limits is possible if a compensatory tax is paid [

16,

41].

CAC regulations date from Presidential Decree 1594 of 1984, updated through Resolution 631 of 2015 by the MADS (see also Presidential Decree 3930 of 2010 and Decree 4728 of 2010 by the Ministry of the Environment, Housing, and Territorial Development). Decree 1594 allows discharge limits as a percentage of total pollutants, without surpassing global limits defined in a 15-year plan for a specific river basin. It also distinguishes between new and existing polluters and is laxer with the latter (

Table 1). In addition, it determines some specific amounts for waste, such as arsenic (Ar), barium (Ba), and cadmium (Cd), but does not include nitrates or phosphates, nor does it establish limits for dissolved oxygen (DO) or turbidity, which are more important than biochemical oxygen demand (BOD) and total suspended solids (TSS), respectively, as suggested by a study on river basins in the U.S. carried out during the 1970s [

50].

Under Resolution 631 of 2015 (Current CAC), allowed emissions are differentiated by economic sector, and measurements change by transitioning from percentages to specific values to protect minimal levels to ensure water bodies keep their assimilation capacity. This change is more restrictive for companies complying with depletion percentages since they need to substantially modify their abatement technologies, and even replace their whole production systems to comply with the specific values. In addition, emissions are broken down into many more parameters than in the earlier CAC regulation. (The sector average for regulated pollution parameters is six. For the manufacturing sector, for example, pH, chemical oxygen demand (COD), BOD, TSS, sedimentable solids (SS), fats, oils, grease, phenols, total hydrocarbons, chlorides, sulfides, and six more types of metals and alkaloids are included. However, another fourteen parameters are under “analysis and report,” which will require visits by the environmental authority to set the specific values of these parameters, making the regulatory process more costly. The new CAC regulation also does not include dissolved oxygen (DO) or turbidity either). This resolution does not consider overall maximum values by economic sector, nor does it particularize the regulation depending on the characteristics of the recipient body of water. Moreover, compensatory taxes are to be paid for only two types of dumping (TSS and biochemical oxygen demand) and charged if and only if the dumping is made directly to the bodies of water.

Environmental Taxes

The environmental tax (called a compensatory tax) has a precedent in Law 99 of 1993 which stipulates:

The direct or indirect use of the atmosphere, water, and soil to introduce or dispose of agricultural, mining, or industrial waste or refuse, sewage or wastewater of any origin, smoke, vapors, and noxious substances that are the result of anthropogenic activities or are man-made, or economic or service activities, whether for profit or not for profit, shall be subject to the payment of compensatory taxes for the negative consequences of said activities.

Its regulation has undergone successive changes, distancing it from its original conception, which required that the tax considered the social and environmental costs of the damage and the costs of recovering the affected body of water. Presidential Decree 3100 of 2003 set the following tax to be paid:

where

is the minimum tax to be paid and

is a regional factor by type of pollutant

i, with

i = TSS, BOD, and updates are made using the Consumer Price Index.

Decree 2667 of 2012 by the MADS specifies that the amount to be paid (AP) for these two types of dumping shall be:

where

is a conversion factor for each type of pollutant

i.

must be understood as an adjustment factor such that the AP may cover the Social and environmental costs of dumping, but following overall and individual reduction goals, which begin at a minimum of 1 and increase by 0.5 units annually if goals are not met. According to Decree 901 of 1997 by the Ministry of the Environment, these increases must be quarterly, and the amount to be paid included the value of depreciation of the affected resource considering the social and environmental costs of the damage according to the reduction goals. In addition, the costs of recovering the resource were supposedly included in the minimum tax ().

Finally, in Decree 2667 of 2012 the regional factor is calculated as follows:

that is, based on a base value

plus the ratio between the total pollutant load dumped by polluting firms in the body of water (

) and the overall goal (

), and with an ad hoc limit not greater than 5.5 (See Presidential Decree 3100 of 2003 for a previous proposal).

Since these discharging goals are subject to “social consensus” between the regional regulators (the Autonomous Regional Corporations (ARCs), the polluting agents, and affected parties), and because they can be particularized by economic activity, a departure from the required technical goals per body of water is possible. In addition, in practice, less than half of the ARCs apply the regional factor, and the amount to be paid is the minimum tax, which is relatively low [

51]. For any given body of water, there is no clarity regarding how the initial calculation was made and, as has already been mentioned, only two types of dumping are taxed. Since the basis of the compensation tax, called Tm, was set in 1988, its value has barely exceeded the negligible threshold of COP 100 (in 2016 Colombian currency) or 0.003 USD per Kg of pollutant load (BOD). In addition, of the seven parameters to be measured, only TSS and BOD are measured, and parameters such as temperature, pH, dissolved oxygen, and turbidity are ignored [

22,

51].

Finally, both the control of dumping and the charging of compensatory taxes are subject to processes of measurement, monitoring, and control by the ARCs, which are difficult to carry out given their limited technical and financial capabilities concerning such a complex task and the pressure from interest groups with greater power in the regulation [

22]. By way of an example, the 2014–2018 National Development Plan aimed to increase the tax for water use, or what is charged for use of this environmental service provided by nature, from COP 1 to USD 15 to reach USD 35 by 2018, which is ludicrous when compared to other nearby countries. The initiative finally did not prosper due to the pressure of interest groups that argued for an enormous loss in competitiveness.

4. An Economic GEM Model Constrained by A Body of Water’s Capacity for Resilience

Let us have a GEM with a representative consumer and three sectors: a polluting sector X, a clean sector Y, and a public utility service-producing sector N which uses a body of water that faces a negative externality arising from the production of X. The preferences and technologies are given by the following system of Cobb–Douglas equations:

where each

stands for the input of

to produce good

in time

, and H and M are the sectorial-specific productivity levels. However, to model N, this research assumes a specific functional form considering: an initial body of water A, a function

that represents the negative externality caused by X on A (

being a damage proportionality parameter), and a marginal contribution of Y resources dedicated to trying to maintain, increase, or change its amount (

) such that N reacts to this externality striving to keep balance.

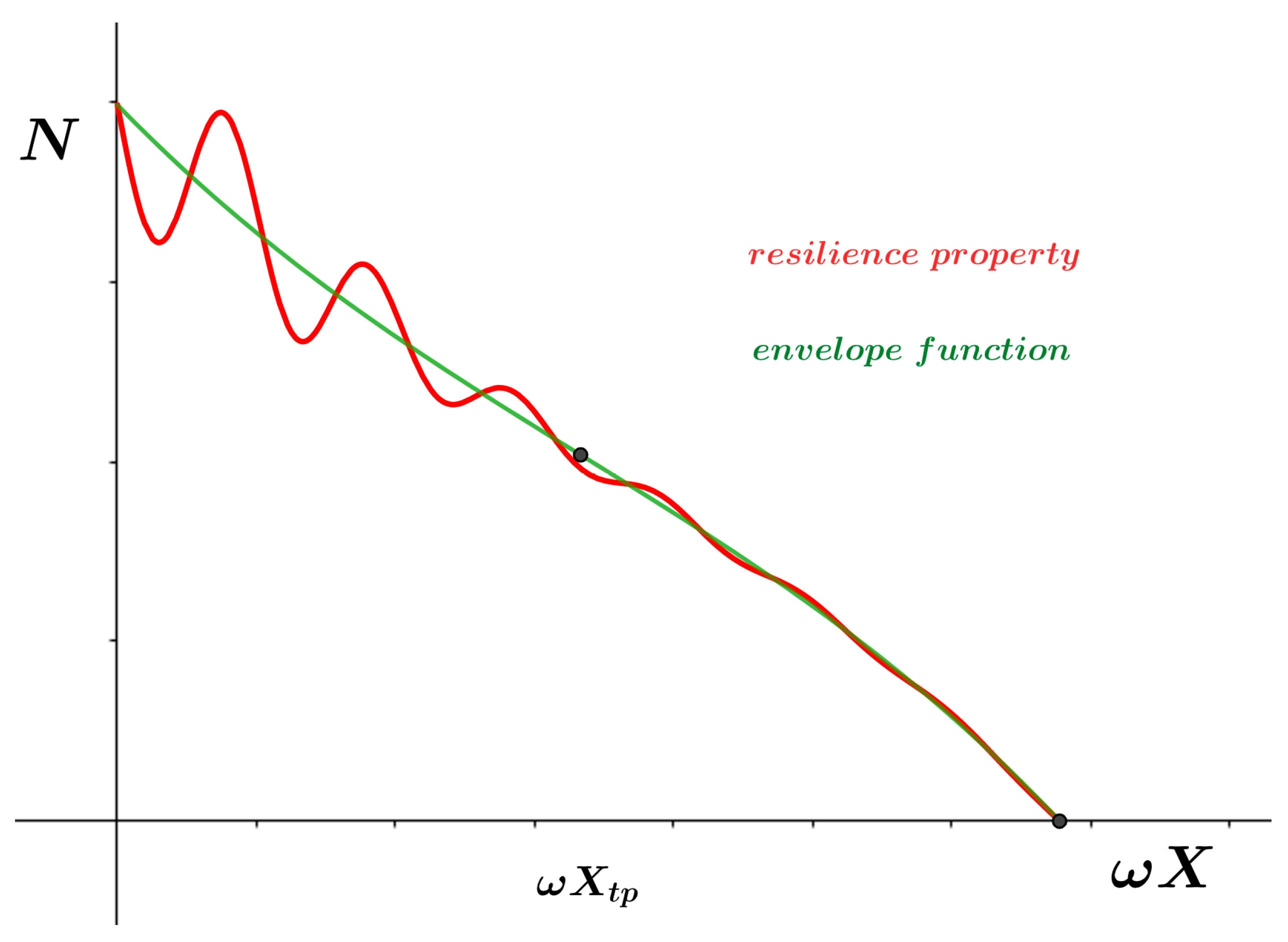

Function

denotes the envelope function (green line on

Figure 1) of trajectory oscillations that accounts for the resilience property (red line) and is characterized by representing a tipping point (

) at which concavity changes (moving from convex to concave), which reflects the fact that the production of N is not sustainable beyond a certain level of pollution (

Figure 1). Decreases in the red line show the initial effect of pollution, and increases show how, without external intervention, it will partially regain resilience levels. The problem is that pollution depletes any capacity for regeneration beyond level

. The envelope function simplifies this behavior and shows that the pollution level that depletes the quantity of N and its resilience capacity in the production occurs exactly at the graph’s inflection point (

). Stock A is renewed naturally period by period as if it were a body of water that receives a flow of water each period allowing it to be refilled. However, A behaves also in a degenerative way, given that it is renewed in each period, albeit at a lower initial level in every subsequent period. It is hence assumed that nature is resilient but accumulates a burden from the deterioration caused by pollution over time [

52,

53].

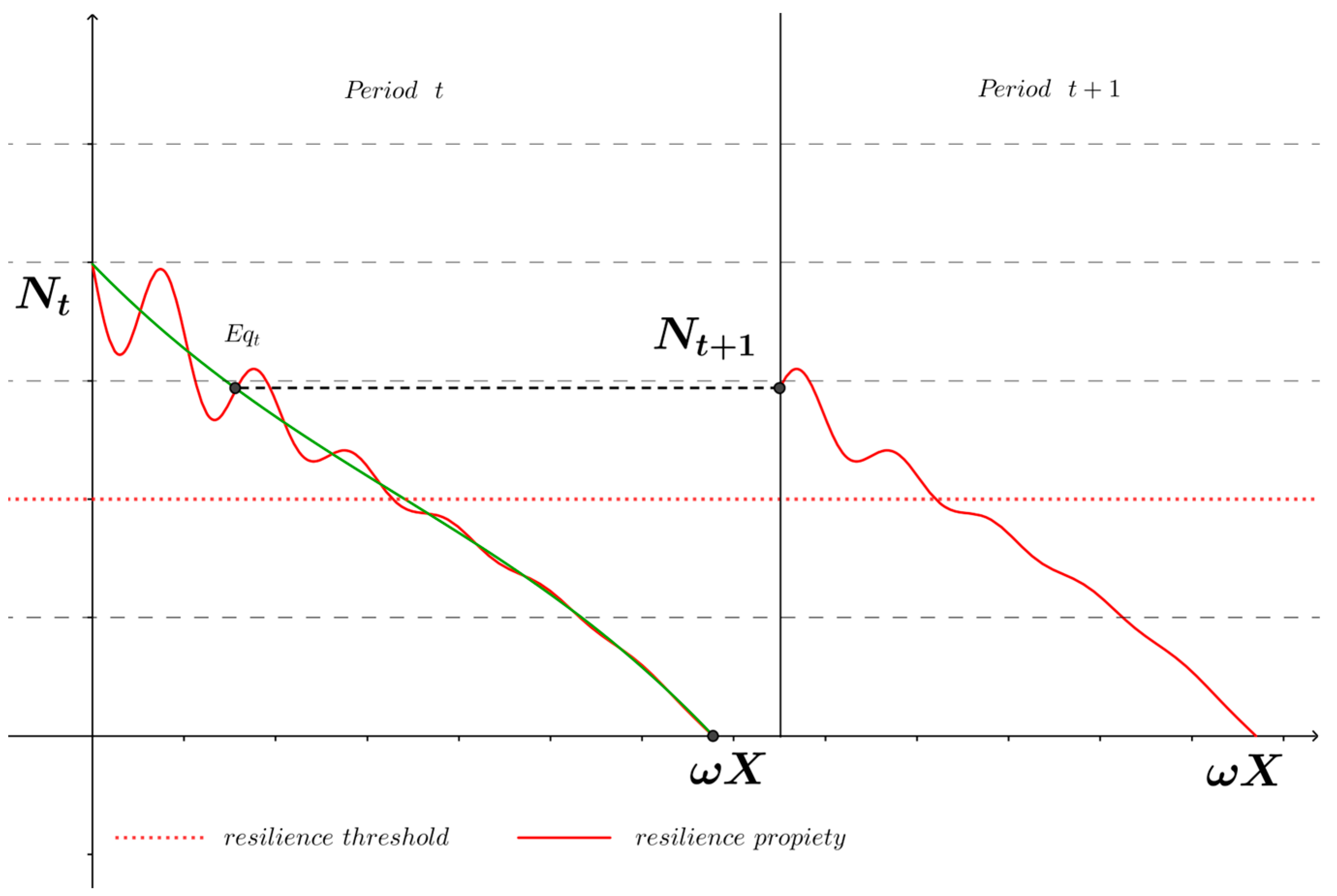

The parameter

indicates pollution caused by X in period

, and r is the value that displaces function

to the left such that the initial natural capital

will be equal to the equilibrium value in period

for each

. This value is calculated using the following equation:

, in which

would be the value of the public utility service after equilibrium and

will be the initial value for the following period.

Figure 2 shows this transition.

To model

, in this paper, we propose a functional form with the following characteristics:

The next equation allows us to reproduce these properties:

where

, to indicate that productivity of the resources used to increase the production of N or reverse the loss of resilience is extremely low.

This modeling proposal of using a simple ecological–economic model, where a GEM is used to model the ecosystem’s resilience property as if it were an economic insurance value, is not new; several authors refer to “resilience” as something that protects from a non-desired state [

9,

54,

55]. Indeed, ecosystem resilience can mitigate consumer and firms’ uncertainty or potential negative disturbances to the economy. Our proposed model shows that the resilience of an ecosystem can recover in the event of a small change in pollution (X)—oscillation of the curve around the point where the slope is zero—but that in the event of strong disturbances, it gradually loses its capacity to recover after a perturbation, and when the ecosystem reaches a tipping point, it collapses.

4.1. Market Equilibrium

In this simple economy, resources are allocated through the market mechanism, which means that prices will ensure that market equilibrium is reached, agents will maximize their objective functions, and their decisions will be compatible in the sense that supply will be equal to demand simultaneously in each market. Every agent resolves the following problem for each period:

We assume that to produce N, only “green” inputs that do not cause environmental damage are used.

Finally, the representative consumer maximizes its utility function subject to the budget restriction given by the benefits from sectors X, Y, and N.

As a result, the maximum demands for inputs, products, and consumption are obtained. To find market equilibrium, the development of the model requires finding prices (

) such that:

Defining, according to Walras’ Law, market must be in equilibrium. Although the N sector will be affected by the cumulative effect of pollution, it is assumed that this sector and all others are short-sighted because they have no concern about the future and do not take internal measures to try to reduce the effects of the pollution generated by others.

4.2. A Model with Hybrid Water Pollution Policies and Abatement Technologies

To analyze the Colombian environmental pollutant discharge regulation, it is convenient to include a pollution abatement technology in the model with which the polluting sector may comply with the CAC regulation. The modeling was carried out under the following assumptions: end-of-pipe abatement technology is available for sector X; payment is made by purchasing input

—that is, the good provided by sector Y; this service allows for the use of that technology which cleans pollution generated in the production of X such that

. Therefore, pollution goes from

to (

. With end-of-pipe technology, we assume that the CAC regulation is implemented by reducing pollution through cleaning the pollution generated by the plant rather than generating lower levels of pollution per product unit (changing the production process). Several new water treatment technologies are available, including the solar photocatalysis process, inverse osmosis water filters, or the traditional multi-stage filtration technology [

56,

57,

58,

59].

The problem for sector X will then be to maximize the profit function knowing that it must pay a tax for the residual pollution:

Making the corresponding calculations, we obtain that the demand for

will be such that it increases as tax increases, as follows:

With .

4.3. Determining Pigouvian Taxes in an Optimal Allocation Model

Pigouvian taxes consist of setting a tax equal to the value of the negative marginal damage of activities X on N to reestablish economic efficiency of the market. Marginal damage is obtained by solving optimal allocation, which accounts for this marginal damage. To reach the optimal allocation, the following problem is proposed:

The control variables are

, and the Lagrange function is given by:

Differentiating on

and equaling to zero:

Clearing the multipliers yields sector X marginal equality:

The above describes the optimal production for X. Observe that if there were no externalities,

,

would be higher. For the market equilibrium to replicate this result, the Pigouvian tax is calculated as:

The new optimization problem for X will then be:

In turn, this tax enters the income of the representative consumer as a lump sum transfer .

5. Impacts of Colombia’s Hybrid Water Pollution Policies on the Proposed Model

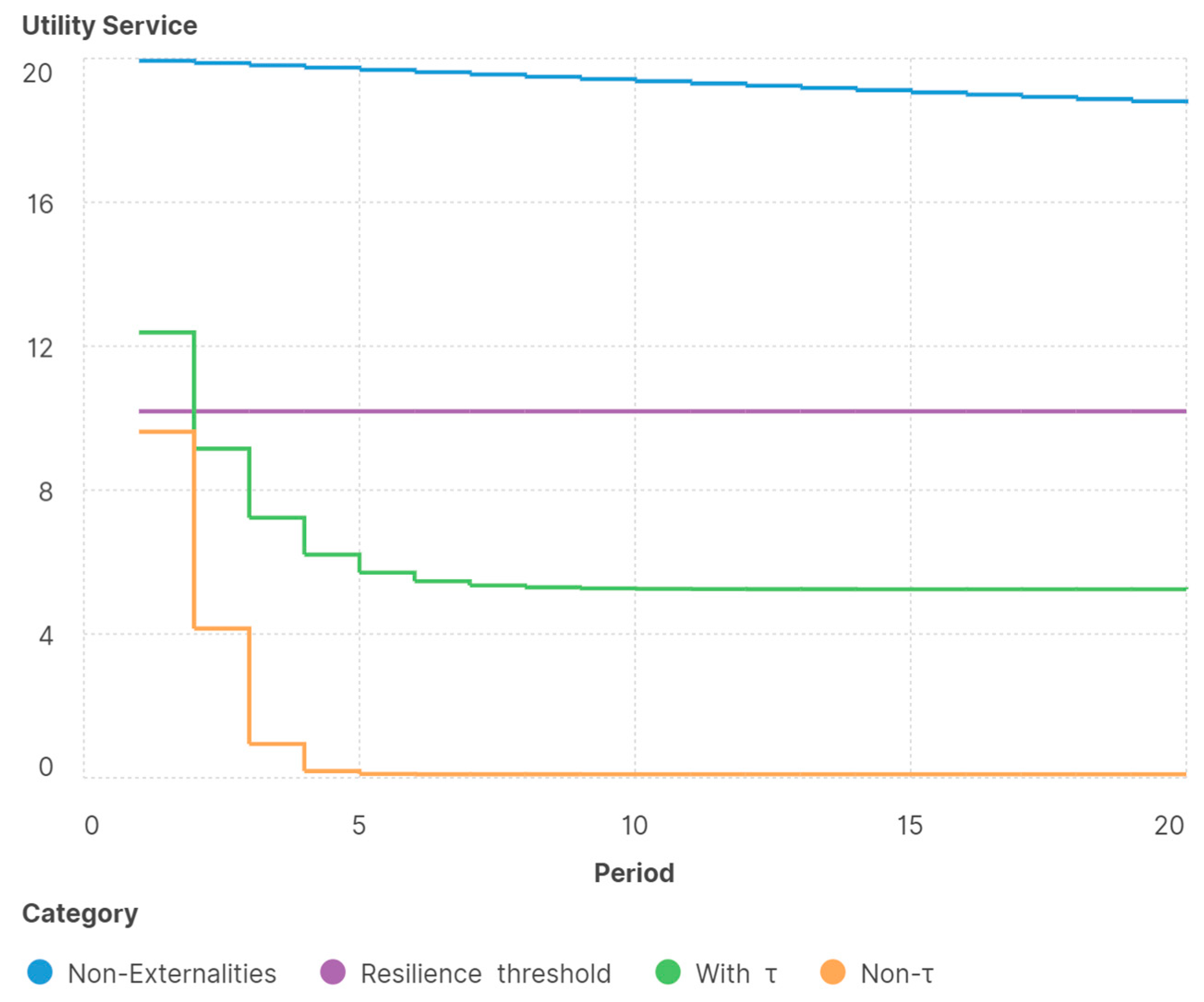

This section examines Colombia’s hybrid water pollution policies described above according to different scenarios of negative effects on bodies of water and the public utility service produced. First, it analyzes what happens when there is no regulation (that is,

).

Figure 3 allows us to distinguish how in this situation the body of water is depleted in the first period. Moreover, pollution eliminates its resilience capacity (red dotted line). The level is given by the pollution tipping point beyond which the level of a body of water loses its resilience capacity. The introduction of a Pigouvian tax, in which the tax rate corresponds to the value of the marginal damage obtained from the optimal allocation model, partially corrects the situation, and also prevents loss of resilience capacity. This occurs because the tax levied is equal to the value of the social marginal damage

in each period, but the pollution allowed by the tax has a cumulative effect over time. In contrast, in a world without externalities, the body of water is depleted at a low rate which corresponds to the expenditure of the public utility service by the agents of this economy at price

.

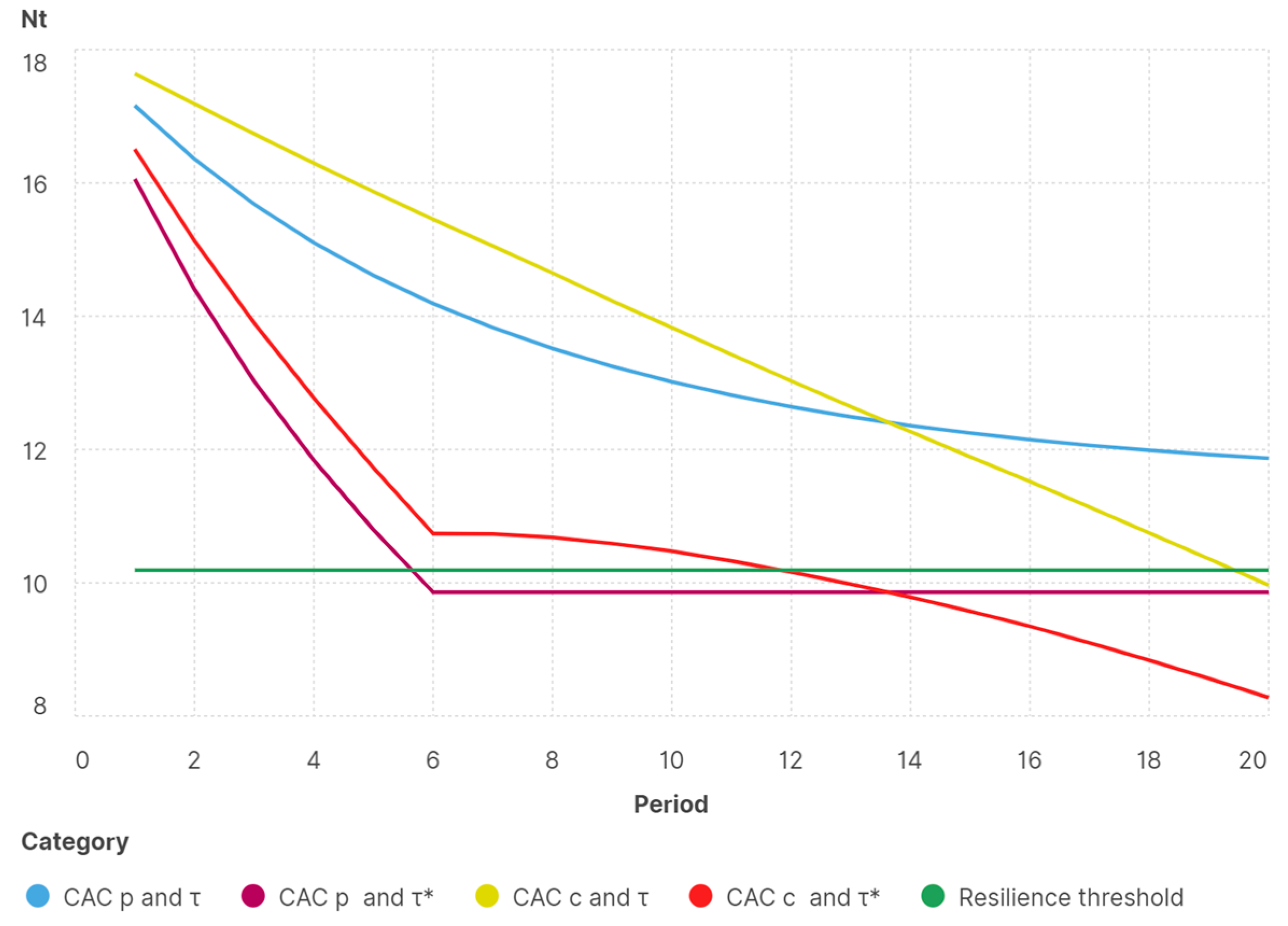

Second,

Figure 4 shows the impacts on N as a consequence of the implementation of hybrid policies adding various levels of compensatory taxes

, although lesser than the Pigouvian tax,

, and CAC norms. The dumping regulation that was previously in force in Colombia required firms to use an abatement technology that guaranteed dumping would not exceed

and established the levying of a tax

for this net level of pollution. The new CAC regulation

establishes that the polluting sector must reduce its emissions by a specific amount in milligrams per liter regardless of the production quantity and the polluting sector. We assume that this current limit is equivalent to a reduction percentage

much smaller than

, i.e.,

.

Figure 4 allows us to compare the effects of both regulations on the proposed model and to analyze the impact of the Pigouvian tax

. As it was explained in the

Section 3 of this paper, the goal of including this last scenario in the analysis is explained by the fact that effective implementation of the regulation before 2015 was associated with a hybrid with a relatively low compensatory tax that did not correspond to the marginal damage caused by pollution.

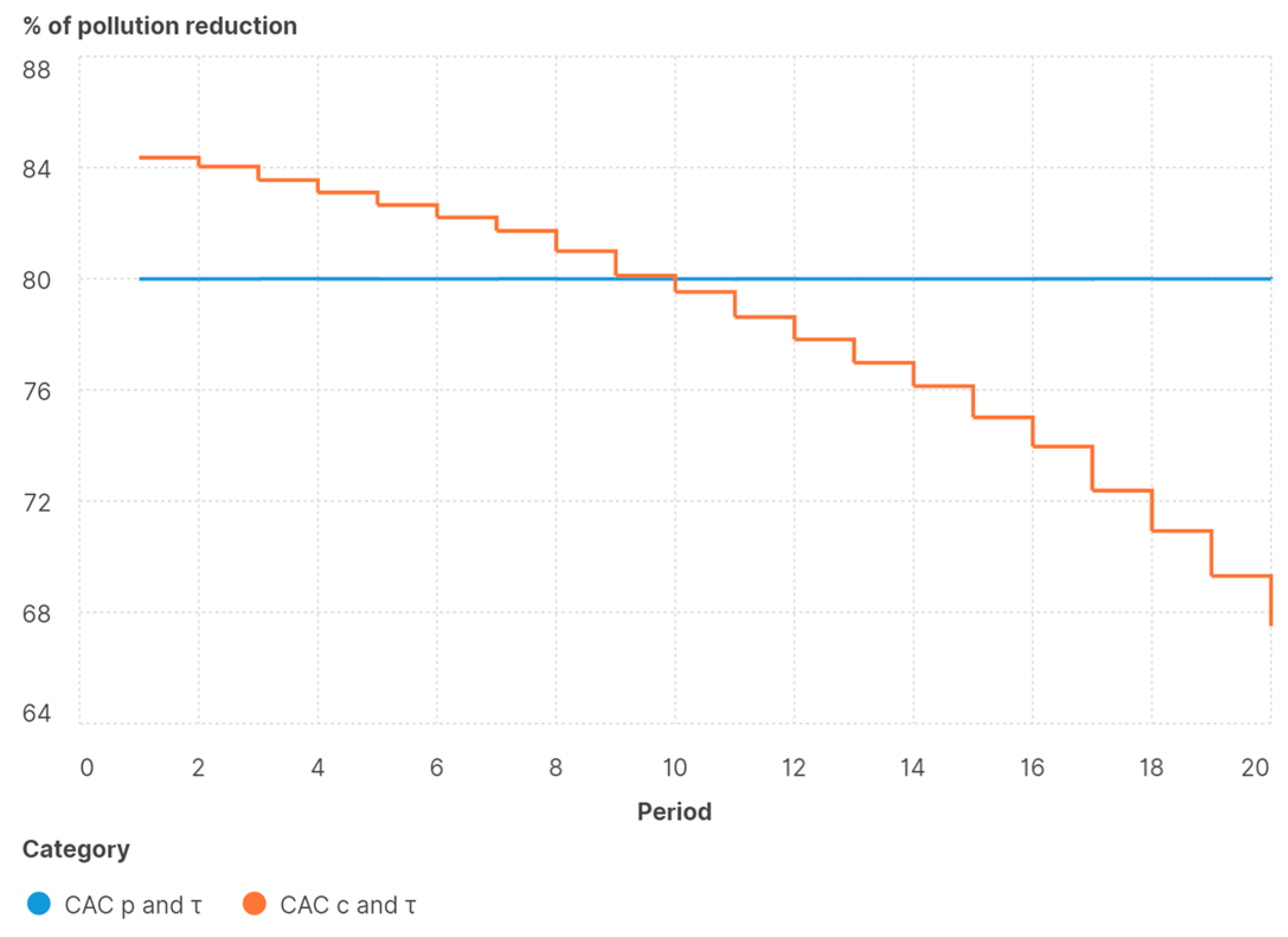

As can be seen, the hybrid

and

maintain higher levels of natural capital during the first periods compared to

and

. However, in the last periods, the provision of the public utility service reaches unsustainable levels when the body of water reduces the required level of resilience, which does not occur with

and

. This is also evident in

Figure 5, where it is observed that the pollution reduction percentage obtained by using abatement technology is lesser in the long term for the

regulation, while the previous CAC always maintained a fixed percentage. This result enables us to determine that

is more effective in maintaining body of water levels, but it also depletes the resilience capacity in further periods than those permitted by

. This implies that the specific magnitude of allowed emissions in the

should be reviewed. It can also be seen that if only a Pigouvian tax

is charged, damages caused will not be recuperated when the impacts of pollution are cumulative. Therefore, this Pigouvian tax must be accompanied by a CAC regulation that adjusts the magnitude of allowed emissions unless there is a means to calculate the cumulative value of the marginal damage over time and bring them to present value.

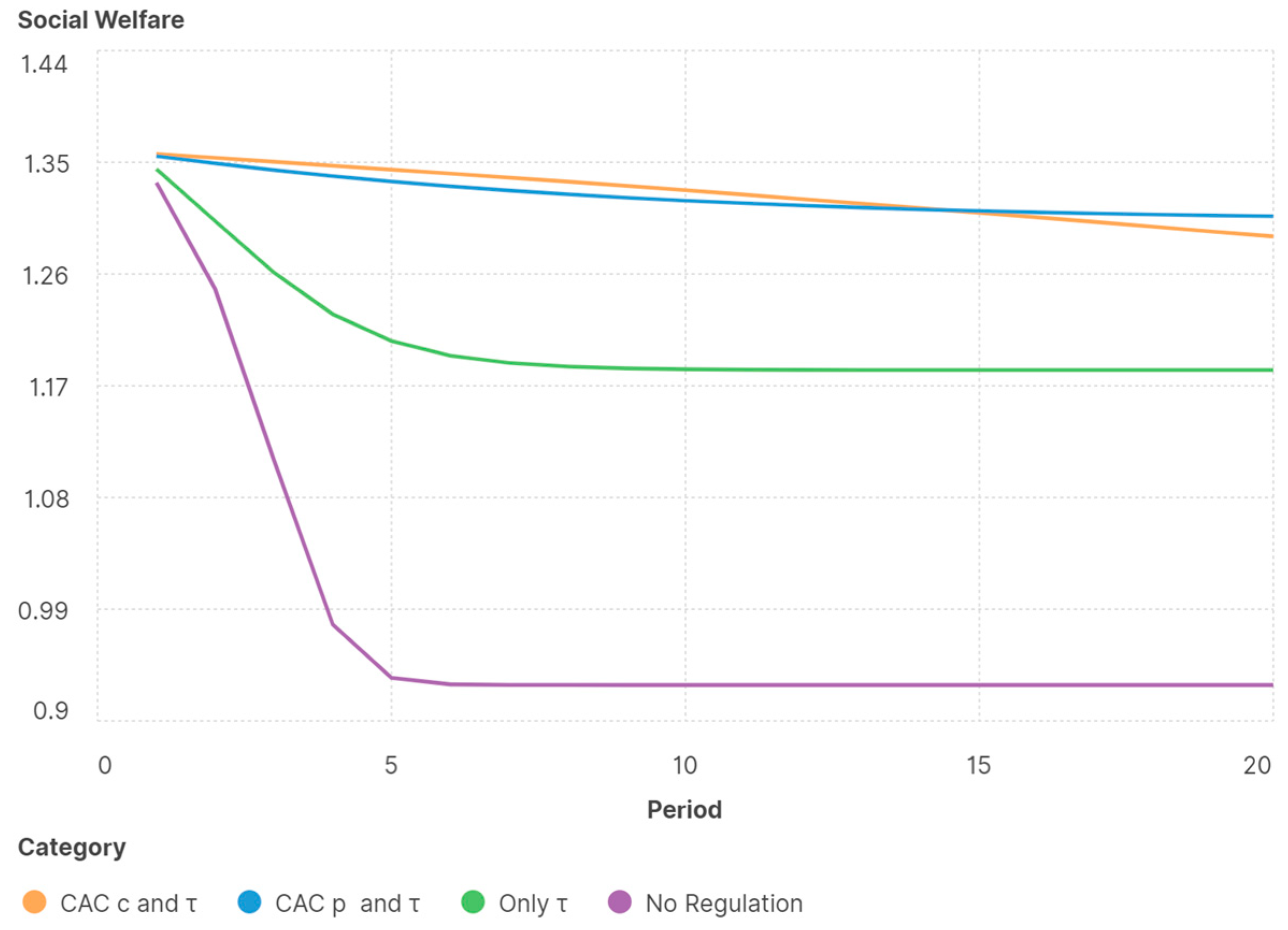

After analyzing public service provision with the two CAC regulations, it is convenient to understand the effects of these regulations on social welfare, which is obtained by measuring the indirect utility function of the representative consumer in the 20 periods analyzed (

Figure 6).

It is worth noting both welfare earnings associated with the use of the hybrid policy and a greater level of welfare when the is applied, in contrast to what occurred with the . However, this welfare will be maintained or increased if and only if the specific magnitude of permitted emissions is revised. Welfare earnings are associated here with hybrid policies based on a tax equal to marginal damage (Pigouvian Tax). The calculation by the regulatory authority of the environmental (compensatory) tax is linear and does not consider the effect of pollution over time. For this reason, the modeling was conducted both with a linear environmental tax and with a Pigouvian tax without cumulative effects. The provision of the public service is reduced but it is still above the critical tipping point so that resilience and welfare can be maintained during the different periods. Finally, under any regulation, welfare decreases marginally over time because of the importance of N in the economy. The effects of these environmental policies were tested for different parameters of consumer preferences, environmental damage, and production and abatement technologies. Parameters representing current and previous CAC were also varied. The results confirm the effects found on the public utility service provision and social welfare.

6. Conclusions

Using a general equilibrium model, it is possible to approximate an economic system in which a polluting sector creates negative externalities that affect water provision. This study aimed to incorporate the accumulation of pollution over time to determine the resilience capacity of the bodies of water or their capacity to regenerate. The provision of a fundamental public utility service shows how drinking water is infringed on, given this resilience capacity restriction. We analyzed whether a hybrid policy instrument which is composed of pollution limits and taxes is viable from the point of view of guaranteeing drinking water and to evaluate impacts on the social welfare.

When there are hybrid instruments, the effects are more appropriate than when only a standard environmental tax is charged, such that hybrid should be equal to the sum of a CAC norm that allows discharge limits as a percentage of total pollutants and a Pigouvian tax which is much higher than the compensatory tax defined in the Colombian law. As such, these results are consistent with the literature that establishes hybrid environmental policy instruments recommended in situations where there is more than a market failure, which, in this case, corresponds to environmental externalities, the difficulties faced by the regulator in measuring the marginal damage, and to cumulative effects of pollution over time, which are usually not included in the calculation of a Pigouvian tax.

Likewise, when the current pollution limits (CAC regulation) are contrasted, it becomes evident that although it seems better than the previous CAC regulation that guaranteed pollution would not exceed a percentage of the pollution, it eventually depletes its potential to reduce damage due to pollution. The establishment of permitted specific amounts of pollutants discharged into the bodies of water does not consider the cumulative degradation undergone by them over time. It is recommendable to periodically revise the permitted amounts to guarantee that they will always be above those that were allowed by the earlier CAC regulation. Notice that, in practice, this periodical revision will impose higher adjustment costs on the largest companies, a scenario which should be further analyzed.

The availability and adoption of abatement technologies is a key feature not only for the conservation of bodies of water but also for the polluting sector to follow CAC regulations. An extension of this model would involve the study of the effects of incentives and subsidies on pollution abatement technologies investment.

It is necessary to consider both the inclusion of different firms and abatement technology options and also different combinations of hybrid instruments’ effects on the selection of technologies that maintain a body of water’s capacity for resilience and maximize social welfare. It is very interesting to analyze the problems of interaction between firms and the decision to innovate or buy pollution abatement technologies.

A later development should include a model in which the effects on the social welfare of different discount rates may be observed, as well as other characteristics so that the model will have more dynamic attributes, for example, intertemporal decisions for consumers or firms. The inclusion of uncertainty could also be important in the model given the technical difficulty of measuring a body of water’s capacity for resilience, as well as the risks which are difficult to assess in the evolution of environmental regulations and technological options.

We assumed that the regulator could determine the optimal hybrid between pollution limits and an environmental tax, considering that the pollutant discharge limits should be adjusted over time and the tax should be approximated to the Pigouvian tax. It is also assumed that there is a direct relationship between production and pollution and that the vector of different pollutants has been reduced to only one pollutant. All this creates regulatory policy challenges which demand much greater flexibility in the selection of different hybrids over time, a difficult situation to overcome in the case of an emerging economy with weaknesses in the regulatory institutional framework concerning its technical and enforcement capabilities.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}