1. Introduction

With the rise of 5G, big data, artificial intelligence, blockchain, and other digital technologies, the wave of digitalization has swept the world, and the world has entered the era of the digital economy [

1]. Residents’ consumption has turned to the online environment and presents a trend of personalization, differentiation, and diversification [

2]. The emergence of COVID-19 has accelerated the pace of digital economy construction [

3].

In the banking industry, new financial services such as digital renminbi, online loan issuance, intelligent wealth management, online account managers, and fund screening continue to emerge. It is digital technology that promotes the digital transformation of commercial banks and enhances the competitiveness of commercial banks and customer service capabilities. At the same time, the People’s Bank of China issued two fintech development plans in 2019 and 2022, emphasizing that financial institutions should accelerate digital transformation [

4]. In 2022, the “14th Five-Year” Digital Economy Development Plan issued by the State Council of China pointed out that it is necessary to accelerate the digital transformation of the financial sector and promote the in-depth application of digital technologies such as big data, artificial intelligence, and blockchain in commercial banks and other fields [

5].

As a traditional industry, commercial banks are the pioneers of informatization [

6]. Facing the advent of the digital economy and the Internet economy, if the survival and development of commercial banks are to adapt to the development of the times, they need to continue to carry out digital transformation [

7]. At the same time, commercial banks, as an essential part of the financial system, are actively or passively undergoing a digital transformation under the impact of the digital economy and financial technology [

8]. Commercial banks mainly use digital technologies such as artificial intelligence, big data, cloud computing, and blockchain to digitally adjust their traditional business products, service methods, and organizational structures [

9]. The comprehensive digital transformation of commercial banks is a problem and an ongoing task for commercial banks.

How does the digital transformation of commercial banks affect operational capabilities?

First, commercial banks’ digital transformations will reduce operating costs and management expenses. After a bank’s digital transformation, the number of customers visiting the store will decrease, and the bank will “reduce face and press counters”, the area used by business outlets, rent expenses, and compress counters, which will liberate some tellers who can then be invested in marketing lines and improving bank performance. At the same time, the number of employees in the operation line will decrease sharply, the number of employees required will decrease, and the number of new employees recruited will decrease, thereby saving human resource costs [

10].

Secondly, commercial banks’ digital transformations will increase interest and non-interest income [

11]. After a bank’s digital transformation, optimizing the loan process will improve the efficiency of the loan business and increase the number of loan customers, and the enrichment of loan products will increase the types of loan customers [

12]. Interest income from loans will increase the interest income of commercial banks. The introduction of online customers will increase the sales of gold, insurance, and precious metals and increase the non-interest income of commercial banks [

13].

Finally, the digital transformation of commercial banks will improve the efficiency of bank operations. After the digital transformation of banks, the internal efficiency of commercial banks will be improved, thereby improving the financial performance of commercial banks [

14]. After digital transformation, commercial banks’ internal approval (office, human resources, etc.), business approval (loan placement, sales, wealth management, etc.), and risk control (post-loan review reminder, whether loan funds have been embezzled, etc.) will all be streamlined. This can improve work efficiency and allow employees to better invest in marketing. The digital transformation of banks can realize financial sharing [

15]. When reimbursing accounts, grassroots sub-branches and outlets only need to submit the original bills, and grassroots financial personnel need to review and upload their bills. Financial approval and reimbursement can be directly handled by superior branches or provincial branches, which improves the internal financial efficiency of the bank, saves staff time costs, and improves the marketing, service to customers, and financial performance of the commercial bank. After a bank’s digital transformation, the head office can obtain the deposit status of the branches under its jurisdiction, and the assets and liabilities department of the head office can conduct lending and centralized investment to maximize the benefits of assets. Subordinate branches are priced according to the FTP of the head office, which can obtain a stable income, avoid idle funds, improve the bank’s financial management efficiency, and thus improve the financial performance of the commercial bank [

16].

There are very few studies on the impact of digital bank transformation on the operational capabilities of commercial banks, and most of them are based on literature reviews, quantitative research, and case analysis. Even fewer studies have used Chinese commercial banks as research samples and conducted empirical analysis. Naimi-Sadigh, Asgari, and Rabiei [

9] pointed out that in the era of the digital economy, digital technology is the primary support for the digital transformation of commercial banks. Commercial banks can improve efficiency and enhance operating capabilities and profitability through digital transformation. At the same time, their study examined the current progress and outcomes of digitization. However, few related studies are based on the financial and banking industries, and many studies still need to be based on literature reviews and quantitative research. The research described business models in the era of the digital economy. It also discussed commercial banks’ ICT vision, goals, and mission statements through the case analysis method. The position of commercial banks in the current market was determined, and a four-step model was used to draw a commercial bank capability gap matrix analysis to describe banks’ digitalization strategy. Tang and Yang [

17] studied the impact of digital bank transformation and corporate performance in sustainable development and carried out a case study using behavioral integration as an intermediary variable. The bank’s efficiency, operating capacity, growth, and profitability were analyzed in the study. Banks’ digital transformations can improve bank efficiency, operating capacity, growth, and profitability, thereby improving corporate performance. However, the nature of digital transformation should cause us to question some aspects. At the same time, how should we understand the digital transformation of banks? The impact of digital transformation on commercial banks is not only at the economic and social levels. Specifically, the operational effect is not only the result of a commercial bank’s actions but also the result of the environment in which it operates. Therefore, it is necessary to introduce corresponding moderator variables for further research, such as COVID-19.

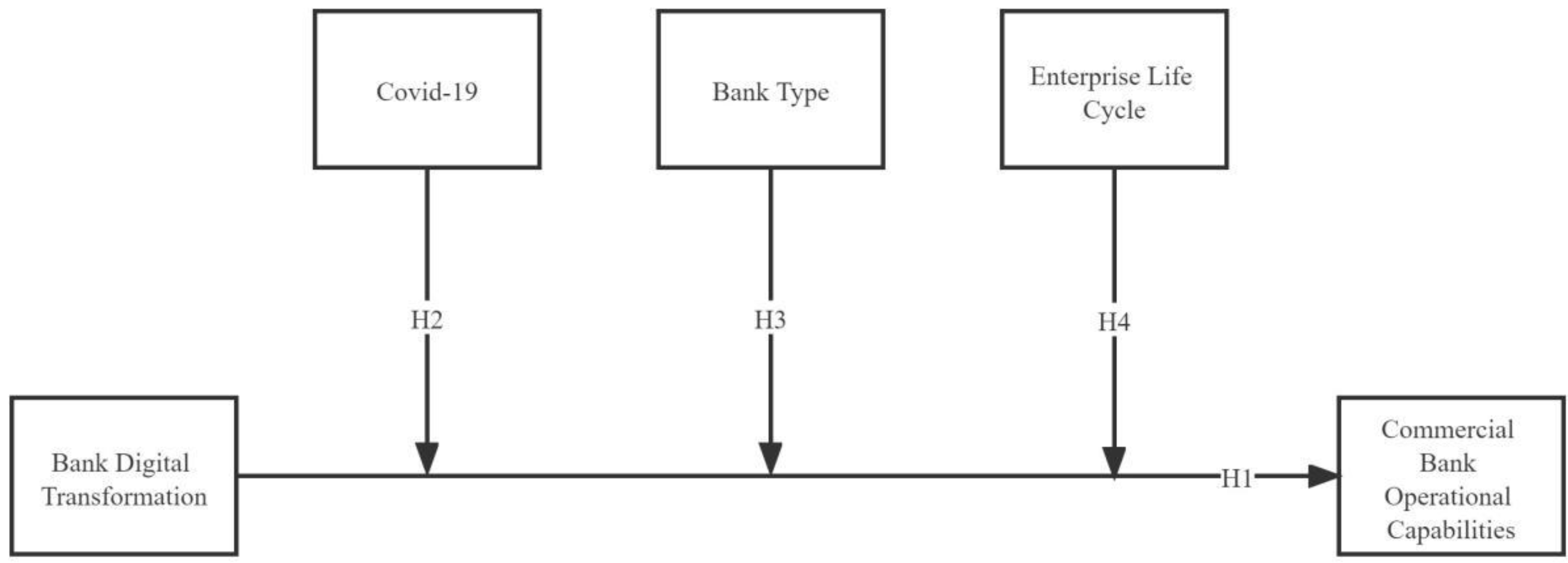

Based on the above background, this study explores the relationship between the digital transformation of banks and the operational capabilities of commercial banks through empirical analysis. At the same time, the new crown epidemic, bank category, and enterprise life cycle are introduced as adjustment variables. Empirical research was carried out with data from Chinese commercial banks.

Compared with the existing literature, this paper makes the following contributions: First, taking the digital transformation of commercial banks as an entry point, it expands the research on the operational capabilities of commercial banks. Existing studies have explored the relationship between commercial bank governance structure, bank capability models, strategic investors, etc., and commercial bank financial performance. However, few pieces of literature have focused on the impact of commercial bank digital transformation on operational capabilities. Second, this paper examines the impact of COVID-19 on the operational capabilities of commercial banks during the digital transformation of banks. Third, the impact of digital bank transformation and commercial bank operating capabilities is analyzed from the perspective of heterogeneity, which provides a helpful reference for commercial banks to formulate differentiated digital transformation strategies. Fourth, by introducing the enterprise life cycle, this study examines the impact of the digital transformation of commercial banks in different life cycles on their operational capabilities.

2. Literature Review and Theoretical Hypotheses

Operational capability is the ability of commercial banks to survive and develop, reflecting the operational, income-generating, and sustainable development capabilities of commercial bank managers [

18]. Banks’ digital transformation is needed for the sustainable development of commercial banks. It is also a response to the policies of the Chinese government and a manifestation of the management capabilities of managers. Based on agency theory and signal transmission theory, after the digital transformation of banks, the impact on the financial performance of commercial banks can allow investors and shareholders to understand the results of the digital transformation of banks and the operational capabilities of commercial banks. The result of the digital transformation of banks reflects the performance of managers, and it is also related to the positions and salaries of managers, which affects their employment status. The operational capability of commercial banks reflects the operational capabilities of managers. Based on the theory of information asymmetry, shareholders and investors reduce information asymmetry through financial statements, operating conditions, and managers’ operating capabilities to understand commercial banks better.

The operational capability of a commercial bank mainly depends on how it effectively uses funds to improve and increase its business activities [

19]. After the digital transformation of banks, based on big data, commercial banks can screen high-quality customers, allocate limited funds to customers with good credit and the ability to repay, and provide different loan interest rates according to qualifications to maximize the use of funds and improve their operational capabilities, thereby improving their financial performance [

20]. Based on big data, commercial banks can promote different products to different customers, directly contact customers through smart outbound calls, liberate account managers, allow account managers to have time to market to critical customers, improve their operational capabilities, and thus enhance their profitability and financial performance. The digitization of commercial banks’ credit systems can simplify business processes and enable better post-loan management. For abnormal loans and customers whose loans are not used according to regulations, they can be identified in advance and tracked after the loan, effectively reducing non-performing loans and non-performing loan rates. After a bank’s digital transformation, the excess funds of the branch can be lent to other banks and other branches in the system to maximize the use of funds and improve the operational capabilities of commercial banks, thereby improving their financial performance [

21]. Kwan et al. (2021) showed that banks with better IT resources experienced larger reductions in physical branch visits and larger increases in website traffic during the pandemic, implying a larger shift to digital banking [

22]. Khalifaturofi‘ah et al. (2022) showed that banks with better IT resources provide a higher number of cheaper and faster guaranteed loans and lend more in areas where they have no bank branches [

23].

A commercial bank’s operating capability’s strength reflects its long-term and sustainable profitability and is an essential indicator that regulators and investors value. Based on signal transmission theory, commercial banks have solid operational capabilities, are more likely to attract investors’ attention, and can improve their financing capabilities and sustainable development capabilities. Therefore, this study proposes Hypothesis 1:

Hypothesis 1 (H1): The digital transformation of banks has improved the operational capabilities of commercial banks.

The emergence of COVID-19 at the end of 2019 has had a massive impact on the economy and travel of various countries. Jin et al. [

24] showed that COVID-19 significantly impacted the tourism industry. Sohibien et al. [

25] took Indonesia as a sample, and their research showed that COVID-19 had a significant impact on the financial industry’s operating performance and financing belt. Here comes the negative. With the implementation of various restrictive epidemic prevention policies, business operations and people’s travel were greatly restricted. Therefore, ample data information, contactless service models, and online Internet products developed rapidly during the COVID-19 pandemic. The development of digital technology can use its Internet technology to meet non-contact needs during the epidemic. At the same time, it can meet customers’ shopping, consumption, and financial needs. In China, COVID-19 has also significantly impacted the financial industry, especially the banking industry. Due to the emergence of third-party payment platforms such as the Internet, online banking, and Alipay, the number of commercial banks’ in-store customers has decreased, and deposits have been lost. Commercial banks have begun or have already carried out digital transformation. The emergence of COVID-19 has accelerated the process of the digital transformation of commercial banks. However, customers are restricted from traveling, causing many customers to lose their source of income. The non-performing loan ratio of commercial banks and the number of overdue credit card customers continue to increase [

26]. Commercial banks have adopted measures such as lowering interest rates or delaying repayment times to reduce the non-performing loan ratio. At the same time, Phan Thi Hang [

27] also proposed how commercial banks can prevent credit crises in the post-COVID-19 period. However, it is undeniable that the emergence of COVID-19 has made it difficult for commercial banks to recover funds, has affected the number of funds, and has affected the profitability of commercial banks. The decrease in customer income and purchasing power has led to a decrease in the non-interest income of commercial banks and affected their profits, thus affecting their operational ability and financial performance. Before and after the outbreak of COVID-19, there were significant differences in commercial banks’ operational capabilities, operating capabilities, and profitability.

Given the magnitude of the COVID-19 pandemic, governments and central banks around the world implemented a range of fiscal [

28] and monetary policies [

29,

30] to mitigate the economic hardship caused by the public health crisis. China itself did a relatively good job controlling the pandemic after the first wave in 2020, but the combination of economic policies and public health interventions affected banks’ performances.

The massive liquidity injection by central banks of developed and emerging market economies generated a search-for-yield effect with abnormal capital flows to emerging markets such as China [

29]. Chinese banks may have benefitted from this injection of liquidity, which coincided with the growing adoption of digital technologies by Chinese banks.

Fiscal policies implemented by the governments of developed nations (e.g., the US) were particularly aggressive. Whereas fiscal policies aiming to provide financial backing to businesses and banks can be construed as government guarantees, the associated capital outlays affect the credibility of future fiscal policies. More specifically, government guarantees affect the banking sector [

31], and increased government deficits (due to fiscal stimuli) affect the real economy through their effect on fiscal multipliers [

32].

Therefore, this study proposes Hypothesis 2:

Hypothesis 2 (H2): The emergence of COVID-19 has negatively affected the ability of the digital transformation of banks to improve the operational capabilities of commercial banks.

Chinese commercial banks are classified according to different natures. They are mainly divided into the central bank, policy banks, large state-owned commercial banks, joint-stock commercial banks, city commercial banks, rural commercial banks, and foreign banks [

33]. Different types of commercial banks have different advantages and characteristics.

In China, the types of banks can be divided into rural commercial banks and non-rural commercial banks [

34]. Rural commercial banks are joint-stock local financial institutions formed by farmers, rural industrial and commercial households, corporate legal persons, and other economic organizations within their jurisdiction. As essential financial support for serving “Sannong,” rural commercial banks can not only open up the “last mile” of financial services after digital transformation but can also analyze the financial needs of all social strata and groups through big data and increase the added value of financial products and service stickiness.

The digital transformation of banks will increase business operating costs [

35]. Commercial banks must invest a lot of technical personnel, research, and development expenses into their digital transformation. According to statistics from the China Banking and Insurance Regulatory Commission, in 2020, commercial banks’ total investment in information technology funds reached CNY 207.8 billion, a year-on-year increase of 20%. Some commercial banks’ technology investments accounted for 4% of their operating income [

36]. According to data from the Kubei Research Institute, there are 42 listed banks in China’s A-share market. Among them, 22 disclosed the amount of science and technology investment in 2021, totaling CNY 168.132 billion. Furthermore, three commercial banks invested more than CNY 20 billion in technology in 2021, which were all large state-owned banks. China Merchants Bank is the joint-stock bank with the highest investment, reaching CNY 13.291 billion. According to the annual reports released by listed banks, the commercial banking industry is increasing investment in technology capital and introducing technology talents to accelerate the realization of banks’ digital transformation. The increase in scientific research personnel has increased the management expenses of commercial banks; the investment in research and development expenses has increased the operating costs of commercial banks. Rural commercial banks have the advantages of localization, capital management and control, and information acquisition efficiency; they have the disadvantages of weak resistance to risks, small service areas, a single-business structure, and a lack of human resources.

Through digital transformation, the disadvantages of rural commercial banks can be effectively improved, but large amounts of scientific and technological personnel and research and development expenses are required. At the same time, rural commercial banks have the characteristics of a small scale and many outlets, leading to relatively large resistance for rural commercial banks when the digital transformation of banks affects the operational capabilities of commercial banks. Therefore, this study proposes Hypothesis 3:

Hypothesis 3 (H3): The digital transformation of banks plays a minor role in improving the operational capabilities of rural commercial banks compared to non-rural commercial banks.

The digital transformation of banks needs to invest a lot of personnel and expenses and sometimes needs to obtain financing, e.g., from the capital market. Investment and risk are related, and financing difficulties are more concentratedly reflected in certain specific periods of commercial banks. According to enterprise life cycle theory, a commercial bank can be regarded as a living organization that needs to go through the development stages of germination, growth, maturity, decline, and elimination [

37]. In different life cycle stages, there are significant differences in various aspects, such as cash flow and financing constraints. Therefore, commercial banks need to choose different solutions. When commercial banks are in different life cycle stages, the impact of bank digital transformations on commercial banks’ operational capabilities may be different. From the perspective of financing needs and banks’ digital transformation capabilities, commercial banks in the growth and maturity stages have more significant potential and financing needs than commercial banks in the recession and phase-out stages. According to the theory of financial exclusion and life cycle, investors will reduce financing support for commercial banks in the recession and phase-out stages and increase financing support for commercial banks in the growth and maturity stages. It is easier for growing and mature commercial banks that have obtained financing support from investors to realize digital transformation. At the same time, the digital transformation of banks also has different impacts on the operational capabilities of commercial banks in different life cycles. When a commercial bank is in the growth and maturity stages, it is easier to obtain the support of investors and shareholders, thereby increasing the investment support of scientific and technological personnel and research and development expenses, which is conducive to improving the commercial bank’s operational capabilities, operating capabilities, and profitability.

Therefore, this paper proposes Hypothesis 4:

Hypothesis 4 (H4): Compared with commercial banks in the recession and phase-out periods, commercial banks in the growth and maturity stages have a more significant impact on the digital transformation of banks in improving the operational capabilities of commercial banks.

{kind=link}