Study on Low-Carbon Technology Investment Strategies for High Energy-Consuming Enterprises under the Health Co-Benefits of Carbon Emission Reduction

Abstract

:1. Introduction

2. Literature Review

3. Problem Description and Basic Assumptions

4. Model Construction and Solution

4.1. The Construction and Solution of Investment Strategy Model of No Carbon Emission Reduction Subsidy

4.2. Construction and Solution of Investment Strategy Model under Cost Subsidy

4.3. Construction and Solution of Investment Strategy Model under Product Subsidy

5. Numerical Algorithms and Simulations

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Parameter | β | Q0 | α | C | A | |

|---|---|---|---|---|---|---|

| Value | 10 (t) | 100,000 (104 CNY/pcs) | 20,000 (pcs) | 30 (104 CNY/pcs) | 0.8 (104 CNY/pcs) | 150,000 (t) |

5.1. The Impact of Carbon Emission Right Price

5.2. The Impact of Carbon Tax Rate

5.3. The Impact of Sensitivity Coefficient of Consumer Low Carbon Level

5.4. The Impact of Repayment Rate

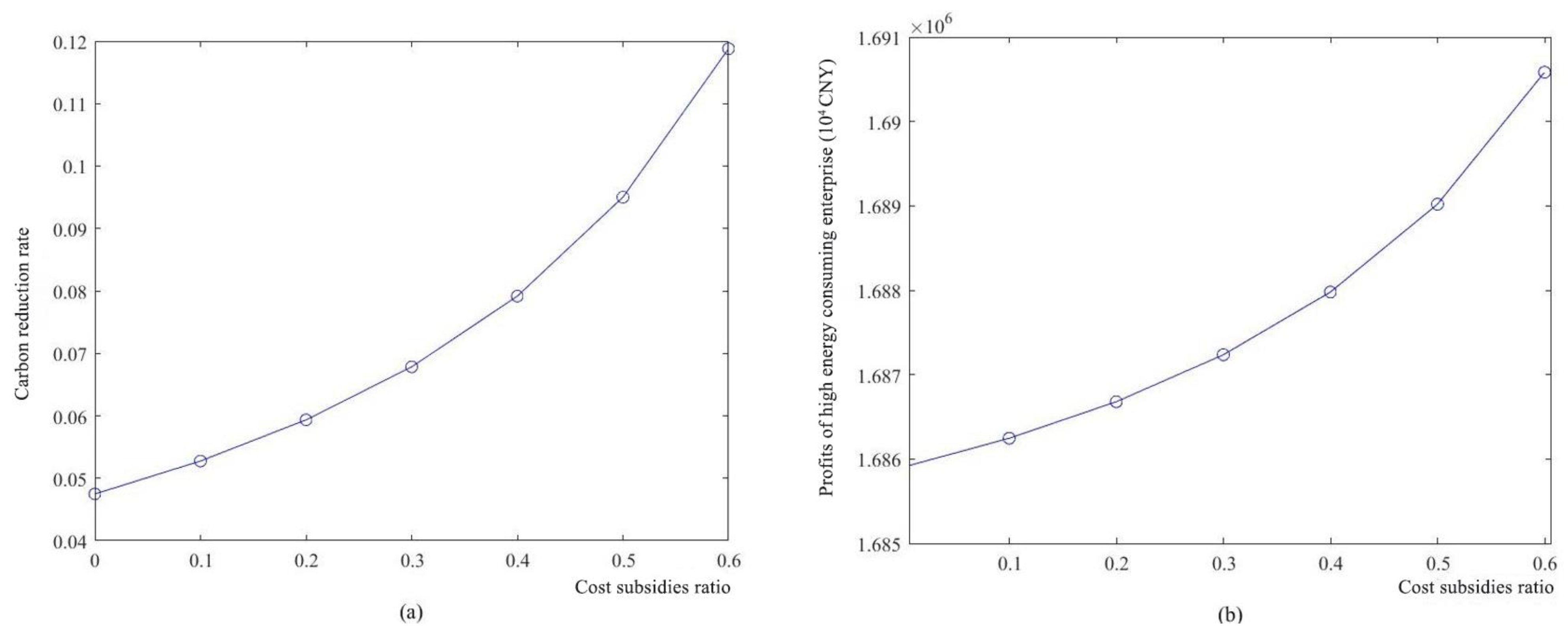

5.5. The Impact of Cost Subsidies Ratio

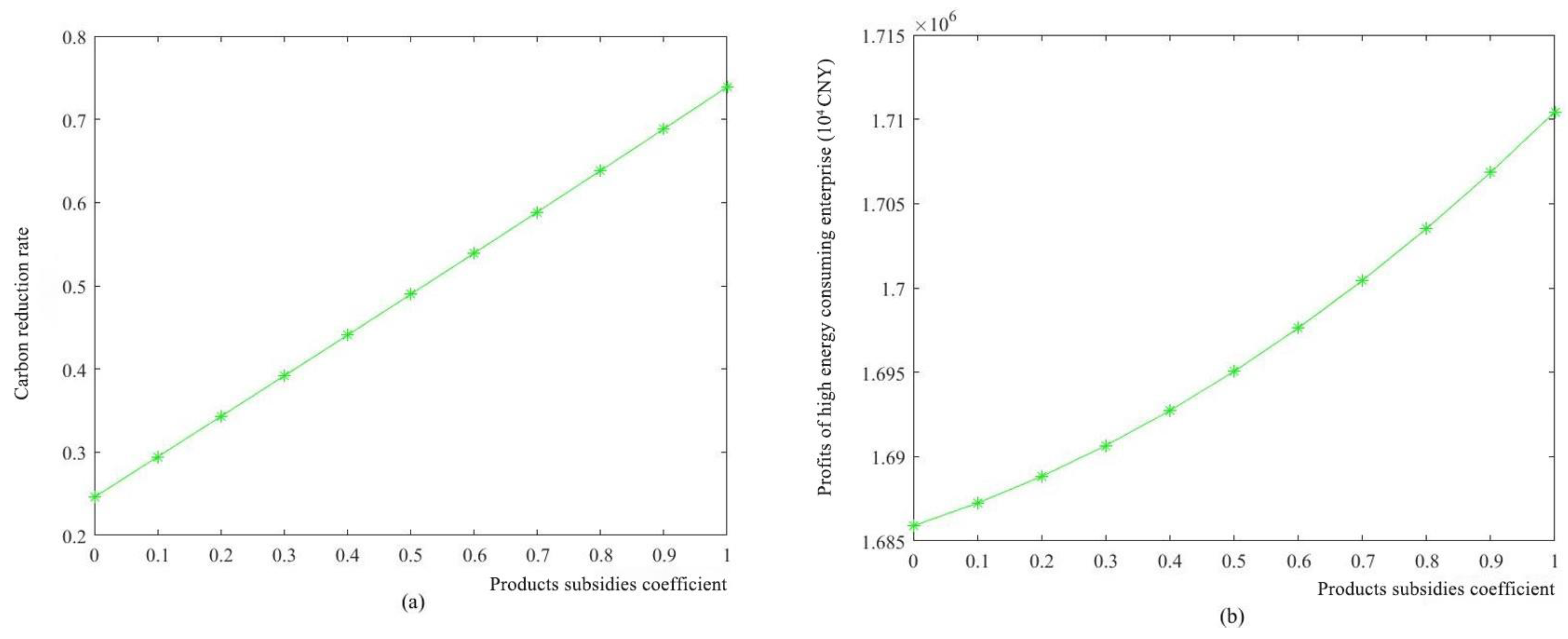

5.6. The Impact of Products Subsidies Coefficient

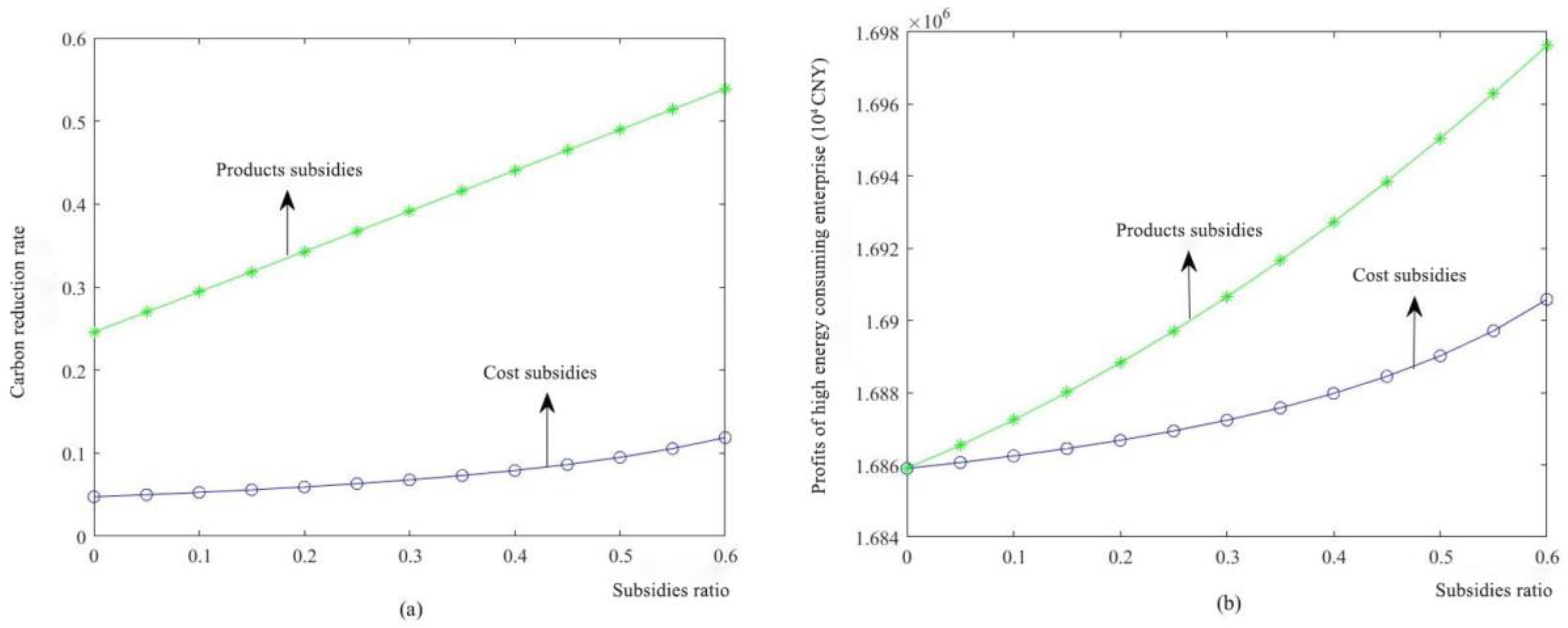

5.7. The Impact of Different Subsidies Ratio

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Romanello, M.; Di Napoli, C.; Drummond, P.; Green, C.; Kennard, H.; Lampard, P.; Costello, A. The 2022 report of the Lancet Countdown on health and climate change: Health at the mercy of fossil fuels. Lancet 2022, 400, 1619–1654. [Google Scholar] [CrossRef] [PubMed]

- Jiang, B.; Li, Y.; Yang, W. Evaluation and treatment analysis of air quality including particulate pollutants: A case study of Shandong province, China. Int. J. Environ. Res. Public Health 2020, 17, 9476. [Google Scholar] [CrossRef] [PubMed]

- Tong, D.; Geng, G.; Zhang, Q.; Cheng, J.; Qin, X.; Hong, C.; He, K.; Davis, S.J. Health co-benefits of climate change mitigation depend on strategic power plant retirements and pollution controls. Nat. Clim. Chang. 2021, 11, 1077–1083. [Google Scholar] [CrossRef]

- Yang, W.; Hu, Y.; Ding, Q.; Gao, H.; Li, L. Comprehensive Evaluation and Comparative Analysis of the Green Development Level of Provinces in Eastern and Western China. Sustainability 2023, 15, 3965. [Google Scholar] [CrossRef]

- Liu, Q.; Zhu, Y.; Yang, W.; Wang, X. Research on the impact of environmental regulation on green technology innovation from the perspective of regional differences: A quasi-natural experiment based on China’s new environmental protection law. Sustainability 2022, 14, 1714. [Google Scholar] [CrossRef]

- Liu, Z.; Sun, W.; Hu, B.; Han, C.; Ieromonachou, P.; Zhao, Y.; Zheng, J. Research on supply chain optimization considering consumer subsidy mechanism in the context of carbon neutrality. Energies 2023, 16, 3147. [Google Scholar] [CrossRef]

- Lv, B.; Zhang, G.; Liu, Y. Nash game equilibrium model of the closed-loop supply chain network considering carbon tax mechanism and product green degree. China Popul. Resour. Environ. 2019, 29, 59–69. [Google Scholar]

- Ma, C.; Yang, H.; Zhang, W.; Huang, S. Low-carbon consumption with government subsidy under asymmetric carbon emission information. J. Clean. Prod. 2021, 318, 128423. [Google Scholar] [CrossRef]

- Yang, L.; Xu, M.; Yang, Y.; Zhang, X. Comparison of subsidy schemes for carbon capture utilization and storage (CCUS) investment based on real option approach: Evidence from China. Appl. Energy 2019, 255, 113828. [Google Scholar] [CrossRef]

- Aryanpur, V.; Fattahi, M.; Mamipour, S.; Ghahremani, M.; Gallachóir, B.Ó.; Bazilian, M.D.; Glynn, J. How energy subsidy reform can drive the Iranian power sector towards a low-carbon future. Energy Policy 2022, 169, 113190. [Google Scholar] [CrossRef]

- Abrell, J.; Kosch, M.; Rausch, S. Carbon abatement with renewables: Evaluating wind and solar subsidies in Germany and Spain. J. Public Econ. 2019, 169, 172–202. [Google Scholar] [CrossRef]

- Adekunle, I.A.; Oseni, I.O. Fuel subsidies and carbon emission: Evidence from asymmetric modelling. Environ. Sci. Pollut. Res. 2021, 28, 22729–22741. [Google Scholar] [CrossRef] [PubMed]

- Pan, K.; He, F. Does Public Environmental Attention Improve Green Investment Efficiency?—Based on the Perspective of Environmental Regulation and Environmental Responsibility. Sustainability 2022, 14, 12861. [Google Scholar] [CrossRef]

- Liu, L.; Zhao, Z.; Zhang, M.; Zhou, D. Green investment efficiency in the Chinese energy sector: Overinvestment or underinvestment? Energy Policy 2022, 160, 112694. [Google Scholar] [CrossRef]

- Yu, W.; Liu, S.; Ding, L. Efficiency Evaluation and Selection Strategies for Green Portfolios under Different Risk Appetites. Sustainability 2021, 13, 1933. [Google Scholar] [CrossRef]

- Liu, Z.; Lang, L.; Hu, B.; Shi, L.; Huang, B.; Zhao, Y. Emission reduction decision of agricultural supply chain considering carbon tax and investment cooperation. J. Clean. Prod. 2021, 294, 126305. [Google Scholar] [CrossRef]

- Ohlendorf, N.; Flachsland, C.; Nemet, G.F.; Steckel, J.C. Carbon price floors and low-carbon investment: A survey of German firms. Energy Policy 2022, 169, 113187. [Google Scholar] [CrossRef]

- Meng, Z.; Sun, H.; Liu, X. Impact of green fiscal policy on the investment efficiency of renewable energy enterprises in China. Environ. Sci. Pollut. Res. 2022, 29, 76216–76234. [Google Scholar] [CrossRef]

- Najafi, P.; Talebi, S. Using real options model based on Monte-Carlo Least-Squares for economic appraisal of flexibility for electricity generation with VVER-1000 in developing countries. Sustain. Energy Technol. Assess. 2021, 47, 101508. [Google Scholar] [CrossRef]

- Liu, Z.; Huang, Y.; Shang, W.; Zhao, Y.; Yang, L.; Zhao, Z. Precooling Energy and Carbon Emission Reduction Technology Investment Model in a Fresh Food Cold Chain based on a Differential Game. Appl. Energy 2022, 10, 119945. [Google Scholar] [CrossRef]

- Bakker, S.J.; Kleiven, A.; Fleten, S.E.; Tomasgard, A. Mature offshore oil field development: Solving a real options problem using stochastic dual dynamic integer programming. Comput. Oper. Res. 2021, 136, 105480. [Google Scholar] [CrossRef]

- Ofori, C.G.; Bokpin, G.A.; Aboagye, A.Q.; Afful-Dadzie, A. A real options approach to investment timing decisions in utility-scale renewable energy in Ghana. Energy 2021, 235, 121366. [Google Scholar] [CrossRef]

- Owen, R.; Brennan, G.; Lyon, F. Enabling investment for the transition to a low carbon economy: Government policy to finance early stage green innovation. Curr. Opin. Environ. Sustain. 2018, 31, 137–145. [Google Scholar] [CrossRef]

- Xia, X.; Chen, W.; Liu, B. Optimal production decision and financing strategy for a capital-constrained closed loop supply chain under fairness concern. J. Clean. Prod. 2022, 376, 134256. [Google Scholar] [CrossRef]

- Chaudhari, U.; Bhadoriya, A.; Jani, M.Y.; Sarkar, B. A generalized payment policy for deteriorating items when demand depends on price, stock, and advertisement under carbon tax regulations. Math. Comput. Simul. 2023, 207, 556–574. [Google Scholar] [CrossRef]

- Wu, T.; Kung, C.C. Carbon emissions, technology upgradation and financing risk of the green supply chain competition. Technol. Forecast. Soc. Chang. 2020, 152, 119884. [Google Scholar] [CrossRef]

- Spasenic, Z.; Makajic-nikolic, D.; Benkovic, S. Risk assessment of financing renewable energy projects: A case study of financing a small hydropower plant project in Serbia. Energy Rep. 2022, 8, 8437–8450. [Google Scholar] [CrossRef]

- Gu, G.; Zhang, W.; Cheng, C. Mitigation effects of global low carbon technology financing and its technological and economic impacts in the context of climate cooperation. J. Clean. Prod. 2022, 381, 135182. [Google Scholar] [CrossRef]

- Bhadoriya, A.; Jani, M.Y.; Chaudhari, U. Combined Effect of Carbon Emission, Exchange Scheme, Trade Credit, and Advertisement Efforts in a Buyer’s Inventory Decision. Process Integr. Optim. Sustain. 2022, 6, 1043–1061. [Google Scholar] [CrossRef]

- Yu, L.; Zhang, B.; Yan, Z.; Cao, L. How do financing constraints enhance pollutant emissions intensity at enterprises? Evidence from microscopic data at the enterprise level in China. Environ. Impact Assess. Rev. 2022, 96, 106811. [Google Scholar] [CrossRef]

- Al Mamun, M.; Boubaker, S.; Nguyen, D.K. Green finance and decarbonization: Evidence from around the world. Financ. Res. Lett. 2022, 46, 102807. [Google Scholar] [CrossRef]

- Luo, R.; Fan, T.; Xia, H. The game analysis of carbon reduction technology investment on supply Chain under carbon cap-and-trade rules. Chin. J. Manag. Sci. 2014, 22, 44–53. [Google Scholar]

- National Bureau of Statistics of China. China Steel Yearbook 2022; National Bureau of Statistics of China: Beijing, China, 2022.

- Baoshan Iron and Steel Co., Ltd. 2022 Sustainable Development Report. Available online: http://www.sse.com.cn/disclosure/listedinfo/announcement/c/new/2023-04-28/600019_20230428_FG11.pdf (accessed on 25 May 2023).

- Lin, Y.; Yang, H.; Ma, L.; Li, Z.; Ni, W. Low-carbon development for the iron and steel industry in China and the world: Status quo, future vision, and key actions. Sustainability 2021, 13, 12548. [Google Scholar] [CrossRef]

| Parameter | Meaning | Parameter | Meaning |

|---|---|---|---|

| Wholesale prices of products of energy-consuming enterprises | Cost subsidy ratio | ||

| Retail price | Product subsidy coefficient | ||

| Carbon trading price | Unit production cost | ||

| Carbon emissions per unit product before low-carbon technology investment | Carbon tax rate | ||

| Low-carbon technology investment after the unit product carbon emissions | Carbon emission quotas for energy-consuming enterprises | ||

| Level of carbon emission reduction after high energy-consuming enterprises invest in low-carbon technology | Potential market demand | ||

| Cost coefficient of high energy-consuming enterprises investing in low carbon technology | Profits of energy-consuming enterprises | ||

| Consumer price elasticity coefficient | Retailer profit | ||

| Consumer low carbon level sensitivity coefficient | Lending rate |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, Z.; Sun, W. Study on Low-Carbon Technology Investment Strategies for High Energy-Consuming Enterprises under the Health Co-Benefits of Carbon Emission Reduction. Sustainability 2023, 15, 8872. https://doi.org/10.3390/su15118872

Liu Z, Sun W. Study on Low-Carbon Technology Investment Strategies for High Energy-Consuming Enterprises under the Health Co-Benefits of Carbon Emission Reduction. Sustainability. 2023; 15(11):8872. https://doi.org/10.3390/su15118872

Chicago/Turabian StyleLiu, Zheng, and Wenzhuo Sun. 2023. "Study on Low-Carbon Technology Investment Strategies for High Energy-Consuming Enterprises under the Health Co-Benefits of Carbon Emission Reduction" Sustainability 15, no. 11: 8872. https://doi.org/10.3390/su15118872

APA StyleLiu, Z., & Sun, W. (2023). Study on Low-Carbon Technology Investment Strategies for High Energy-Consuming Enterprises under the Health Co-Benefits of Carbon Emission Reduction. Sustainability, 15(11), 8872. https://doi.org/10.3390/su15118872