Community Perceptions on the Critical Success Factors of Hotels’ Community-Based Corporate Social Responsibility

, and

, and

Abstract

1. Introduction

1.1. Critical Success Factors for Implementing CSR

1.2. The Conceptual Background of the Study

2. Hypothesis Development

- Top management devotion (TMD) to CSR

- Formal CSR Strategic Plan and Practices (SPPs)

- Consumer-oriented strategy (COS)

- Implanting CSR into the organisational culture and citizen behaviour (OCCB)

- Employee devotion to CSR (ED)

- Stakeholder engagement (SE)

- Participation in community-related development activities (CB)

- Knowledge sharing (KS)

- Laws and social norms (LSNs)

- CSR project management and committees (PMCs)

- Finance preparedness (FP)

- Measurement and report of CSR performance (MRP)

3. Methodology

3.1. Questionnaire Design

3.2. Validity and Reliability of Quantitative Instrument

4. Results

4.1. Assessment of Measurement (Outer) Model

4.2. Individual Item Reliability

4.3. Internal Consistency Reliability

4.4. Convergent Validity

4.5. Discriminant Validity

4.6. Summary of Measurement Model

4.7. Assessment of the Significance of the Structural (Inner) Model and the Effect of Predictors on CSR

4.8. Assessment of Variance Explained in the Endogenous Latent Variable

4.9. Assessment of Predictive Relevance

5. Discussion and Conclusions

6. Limitation and Direction for Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Hessekiel, D. 2023 CSR Trend Forecasts. Available online: https://www.forbes.com/sites/davidhessekiel/2023/01/19/23-csr-trend-forecasts/?sh=49bac63825ff (accessed on 19 January 2023).

- Wuncharoen, C. Corporate Social Responsibility in Hotels business. J. Manag. Sci. 2013, 30, 143–158. [Google Scholar]

- Urip, S. CSR Strategies: Corporate Social Responsibility for a Competitive Edge in Emerging Markets; John Wiley & Sons: Singapore, 2010. [Google Scholar]

- Kasim, A.; Khuadthong, B.; Jailani, N.; Mokhtar, M.F.; Radha, J.Z.R.R.R.; Leong, M. The Importance of Community Perspectives on Hotel Community-Related CSR: A Position Paper. Sustainability 2022, 14, 4636. [Google Scholar] [CrossRef]

- Gursoy, D.; Boğan, E.; Dedeoğlu, B.B.; Çalışkan, C. Residents’ perceptions of hotels’ corporate social responsibility initiatives and its impact on residents’ sentiments to community and support for additional tourism development. J. Hosp. Tour. Manag. 2019, 39, 117–128. [Google Scholar] [CrossRef]

- Boğan, E.; Dedeoğlu, B.B. The effects of hotel employees’ CSR perceptions on trust in organization: Moderating role of employees’ self-experienced CSR perceptions. J. Hosp. Tour. Insights 2019, 2, 391–408. [Google Scholar] [CrossRef]

- Abaeian, V.; Khong, K.W.; Kyid Yeoh, K.; McCabe, S. Motivations of undertaking CSR initiatives by independent hotels: A holistic approach. Int. J. Contemp. Hosp. Manag. 2019, 31, 2468–2487. [Google Scholar] [CrossRef]

- Xuerong, P.; Jiang, W.; Ya’Nan, L. Corporate Social Responsibility Practices in Chinese Hotel Industry: A Content Analysis of Public CSR Information of Top 15 Chinese Hotel-management Companies. Tour. Trib. Lvyou Xuekan 2013, 28, 52–61. [Google Scholar]

- Carè, R.; Rania, F.; Lisa, R.D. Critical Success Factors, Motivations, and Risks in Social Impact Bonds. Sustainability 2020, 12, 7291. [Google Scholar] [CrossRef]

- Kahreh, M.S.; Mirmehdi, S.M.; Eram, A. Investigating the critical success factors of corporate social responsibility implementation: Evidence from the Iranian banking sector. Corp. Gov. Int. J. Bus. Soc. 2013, 13, 184–197. [Google Scholar]

- Corporate Responsibility Forum. 12 Critical Success Factors for CSR. 2004. Available online: http://corporateresponsibilityforum.blogspot.com/2004/07/12-critical-success-factors-for-csr.html (accessed on 25 December 2016).

- Nyuur, R.B.; Ofori, D.F.; Debrah, Y. Corporate social responsibility in SubSaharan Africa: Hindering and supporting factors. Afr. J. Econ. Manag. Stud. 2014, 5, 93–113. [Google Scholar]

- Peng, W.; Xin, B.; Kwon, Y. Optimal strategies of product price, quality, and corporate environmental responsibility. Int. J. Environ. Res. Public Health 2019, 16, 4704. [Google Scholar] [CrossRef]

- Sangle, S. Critical Success Factors for Corporate Social Responsibility: A Public Sector Perspective. J. Corp. Soc. Responsib. Environ. Manag. 2009, 17, 205–214. [Google Scholar] [CrossRef]

- Singchoo, P. Success Factors for CSR. 2012. Available online: https://www.gotoknow.org/posts/535674 (accessed on 25 January 2017).

- Woo, C. CSR. 2013. Available online: http://www.businesscircle.com.my/success-factors-in-csr-integration/ (accessed on 21 December 2016).

- Zahidy, A.A.; Sorooshian, S.; Abd Hamid, Z. Critical success factors for corporate social responsibility adoption in the construction industry in Malaysia. Sustainability 2019, 11, 6411. [Google Scholar] [CrossRef]

- Khuadthong, B.; Kasim, A. Critical success factors for community-related corporate social responsibility in the hotel sector: A literature review. In The Routledge Handbook of Community-Related Tourism Management; Taylor & Francis Group: Abingdon, UK, 2020; pp. 307–320. [Google Scholar]

- Dos Santos, L.I.; Anholon, R.; da Silva, D.; Etulain, C.R.; Rodrigues, V.S.; Leal Filho, W. Corporate social responsibility projects: Critical success factors for better performance of Brazilian companies and guidelines to qualify professionals and entrepreneurs. Int. Entrep. Manag. J. 2022, 18, 1685–1706. [Google Scholar] [CrossRef]

- Mastrangelo, L.; Cruz-Ros, S. Crowdfunding success: The role of co-creation, feedback, and corporate social responsibility. Int. J. Entrep. Behav. Res. 2020, 26, 449–466. [Google Scholar] [CrossRef]

- Chatterjee, S.; Chaudhuri, R.; Vrontis, D.; Thrassou, A. Corporate social responsibility in post COVID-19 period: Critical modeling and analysis using DEMATEL method. Manag. Decis. 2022, 60, 2694–2718. [Google Scholar] [CrossRef]

- Fuzi, N.M.; Habidin, N.F.; Hibadullah, S.N.; Ong, S.Y.Y. CSR practices, ISO 26000 and performance among Malaysian automotive suppliers. Soc. Responsib. J. 2017, 13, 203–220. [Google Scholar] [CrossRef]

- Zhang, Q.; Oo, B.L.; Teck-Heng Lim, B.T. Key practices and impact factors of corporate social responsibility implementation: Evidence from construction firms. Archit. Manag. 2022, 30, 2124–2154. [Google Scholar] [CrossRef]

- Lechuga Sancho, M.P.; Jorge, M.L.; Madueño, J.H. Design and validation of an instrument of measurement for corporate social responsibility practices in small and medium enterprises. Soc. Responsib. J. 2021, 17, 1150–1174. [Google Scholar] [CrossRef]

- Jalilvand, M.R.; Pool, J.K.; Jamkhaneh, H.B.; Tabaeeian, R.A. Total quality management, corporate social responsibility and entrepreneurial orientation in the hotel industry. Soc. J. 2018, 14, 601–618. [Google Scholar] [CrossRef]

- Songsom, A. Development of Indicators and a Scale for Measuring Innovativeness: A Case Study of Small and Medium Enterprises in Songkhla Province. Econ. Bus. Adm. J. Kasertsart Univ. 2017, 55, 210–218. [Google Scholar]

- Teeeraputtigunchai, B.; Somsak, R.; Wanmakok, A. Factors, Process, Outcomes, and Impacts of SCG (Lampang)’s CSR Project Operation Driven under Community-related Research Project Concept. J. J. Thammasat Univ. 2021, 14, 234–267. [Google Scholar]

- Peredo, A.M.; Chrisman, J.J. Toward a theory of community-based enterprise. Acad. Manag. Rev. 2006, 31, 309–328. [Google Scholar] [CrossRef]

- Adewuyi, A.O.; Olowookere, A.E. CSR and sustainable community development in Nigeria: WAPCO, a case from the cement industry. J. Soc. Responsib. 2010, 6, 522–535. [Google Scholar] [CrossRef]

- Ghaderi, Z.; Mirzapour, M.; Henderson, J.C.; Richardson, S. Corporate social responsibility and hotel performance: A view from Tehran, Iran. Tour. Manag. Perspect. 2019, 29, 41–47. [Google Scholar] [CrossRef]

- Thou, M.Y.; Signal, M. A review of the business case for CSR in the hospitality industry. Int. J. Hosp. Manag. 2019, 84, 102330. [Google Scholar]

- Gürlek, M.; Tuna, M. Corporate social responsibility and work engagement: Evidence from the hotel industry. Tour. Manag. Perspect. 2019, 31, 195–208. [Google Scholar] [CrossRef]

- Theodoulidis, B.; Diaz, D.; Crotto, F.; Rancati, E. Exploring corporate social responsibility and financial performance through stakeholder theory in the tourism industries. Tour. Manag. 2017, 62, 173–188. [Google Scholar] [CrossRef]

- Jupe, R. Disclosures in Corporate Environmental Report: A Test of Legitimacy Theory; Kent Business School: Canterbury, UK, 2005. [Google Scholar]

- Suchman, M. Managing Legitimacy: Strategic and Institutional Approaches. Acad. Manag. Rev. 1995, 20, 57l–610. [Google Scholar] [CrossRef]

- Ueki, Y. Top Management Devotion to CSR. 2013. Available online: https://www.jal.com/en/csr/devotion/ (accessed on 4 March 2017).

- Jayashree, S.; Malarvizhi, C.A.; Mayel, S.; Rasti, A. Significance of Top Management Devotion on the Implementation of ISO 14000 EMS towards Sustainability. Middle East J. Sci. Res. 2015, 23, 2941–2945. [Google Scholar] [CrossRef]

- Rangan, K.; Chase, L.A.; Karim, S. Why Every Company Needs a CSR Strategy and How to Build It; Harvard Business School: Canterbury, UK, 2012; Available online: http://www.hbs.edu/faculty/Publication%20Files/12-088.pdf (accessed on 18 February 2017).

- Kotler, P.; Lee, N. Corporate Social Responsibility; John Wiley & Sons: Hoboken, NJ, USA, 2005. [Google Scholar]

- Baker, J. The Rise of the Consumers: Why Businesses need to Open Up. The Guardian, Thursday, April 2015. Available online: https://www.theguardian.com/women-in-leadership/2015/apr/02/the-rise-of-the-conscious-consumer-why-businesses-need-to-open-up (accessed on 23 September 2022).

- PPAI Publications. Corporate Social Responsibility Increasingly Important to Consumers. 2015. Available online: http://pubs.ppai.org/2015/07/corporate-social-responsibility-increasingly-important-to-consumers/ (accessed on 31 March 2017).

- Grover, P.; Kumar Kar, A.; Ilavarasan, P.V. Impact of corporate social responsibility on reputation—Insights from tweets on sustainable development goals by CEOs. Int. J. Inf. Manag. 2019, 48, 39–52. [Google Scholar] [CrossRef]

- Übius, Ü.; Alas, R. Organizational Culture Types as Predictors of Corporate Social Responsibility. Eng. Econ. 2009, 1, 90–99. [Google Scholar]

- Watkins, M.D. What Is Organizational Culture? And Why Should We Care? 2013. Available online: https://hbr.org/2013/05/what-is-organizational-culture (accessed on 10 May 2017).

- Aladwan, K.; Bhanugopan, R.; D’Netto, B. The effects of human resource management practices on employees’ organizational devotion. Int. J. Organ. Anal. 2015, 23, 472–492. [Google Scholar] [CrossRef]

- Tuan, L.T. From corporate social responsibility, through entrepreneurial orientation, to knowledge sharing: A study in Cai Luong (Renovated Theatre) theatre companies. Learn. Organ. 2015, 22, 74–92. [Google Scholar] [CrossRef]

- Van Den Hooff, B.; De Ridder, J.A. Knowledge sharing in context: The influence of organizational devotion, communication climate and CMC use on knowledge sharing. J. Knowl. Manag. 2004, 8, 117–130. [Google Scholar] [CrossRef]

- Farmakia, A.; Farmakis, P. A stakeholder approach to CSR in hotels. Ann. Tour. Res. 2018, 68, 58–60. [Google Scholar] [CrossRef]

- Katsoulakos, T.; Katsoulacos, Y. Corporate responsibility, strategic management and the stakeholder view of the firm. Corp. Gov. 2007, 7, 344–354. [Google Scholar] [CrossRef]

- Buhmann, K. Corporate social responsibility: What role for law? Some aspects of law and CSR. Corp. Gov. 2006, 6, 188–202. [Google Scholar] [CrossRef]

- Carlon, D.M.; Downs, A. Stakeholder Valuing: A Process for Identifying the Interrelationships between Firm and Stakeholder Attributes. Adm. Sci. 2014, 4, 137–154. [Google Scholar] [CrossRef]

- Bohdanowicz, P.; Zientara, P. Corporate Social Responsibility in Hospitality: Issues and Implications. A Case Study of Scandic Hotels. Scandinavian. J. Hosp. Tour. 2008, 8, 271–293. [Google Scholar] [CrossRef]

- Aqueveque, C.; Rodrigo, P.; Duran, I.J. Be bad but (still) look good: Can controversial industries enhance corporate reputation through CSR initiatives? Bus. Ethics A Eur. Rev. 2018, 27, 222–237. [Google Scholar] [CrossRef]

- Kusumastuti, D. Corporate Social Responsilility (Csr) Fund Management Model in Local Government to Realize Justice and Law Certainty. Int. J. Bus. Econ. Law 2018, 16, 178. [Google Scholar]

- Visser, W. Corporate social responsibility in developing countries. In The Oxford Handbook of Corporate Social Responsibility; Crane, A., McWilliams, A., Matten, D., Moon, J., Siege, D., Eds.; Oxford University: Oxford, UK, 2008; pp. 473–479. [Google Scholar]

- Eisenberg, M.A. Corporate law and social norms. Columbia Law Rev. 1999, 99, 1253–1292. [Google Scholar] [CrossRef]

- Project Management Institute. The Value of Project Management. 2010. Available online: https://www.pmi.org/-/media/pmi/documents/public/pdf/white-papers/value-of-project-management.pdf (accessed on 29 August 2016).

- Wiśniewski, M. CSR Risk Management. Forum Sci. Oeconomia 2015, 3, 17–24. [Google Scholar]

- Mohyletska, U. How does CSR Affect Companies’ Financial Performance? 2021. Available online: https://www.ecohz.com/blog/how-does-csr-affect-companies-financial-performance (accessed on 23 December 2022).

- The Global Reporting Initiative. The Benefits of Sustainability Reporting. 2011. Available online: https://www.globalreporting.org/resourcelibrary/The-benefits-of-sustainability-reporting.pdf (accessed on 3 April 2017).

- Faems, D. Moving forward quantitative research on innovation management: A call for an inductive turn on using and presenting quantitative research. R D Manag. 2020, 50, 352–363. [Google Scholar] [CrossRef]

- Siljaru, T. Research and Statistical Analysis with SPSS and Amos, 13th ed.; SR Printing Mass Product: Bangkok, Thailand, 2012. [Google Scholar]

- Saengpikul, A. Research Methodology for Tourism and Hospitality; Dhurakijpundit University Press: Bangkok, Thailand, 2013. [Google Scholar]

- Isaac, S.; Michael, W.B. Handbook in Research and Evaluation; Educational and Industrial Testing Services: San Diego, CA, USA, 1995. [Google Scholar]

- Neuman, W.L. Social Research Methods: Qualitative and Quantitative Approaches, 3rd ed.; Allyn and Bacon: Boston, MA, USA, 1997. [Google Scholar]

- Sekaran, U. Research Methods for Business: A Skill-Building Approach, 3rd ed.; John Wiley & Sons: Hoboken, NJ, USA, 2000. [Google Scholar]

- Brislin, R.W. Translation and Content Analysis of Oral and Written Material. In Handbook of Cross-Cultural Psychology; Triandis, H.C., Berry, J.W., Eds.; Allyn & Bacon: Boston, MA, USA, 1980; pp. 389–444. [Google Scholar]

- Kassim, M.N. Determinants of Customer Satisfaction and Retention in the Cellular Phone Market of Malaysia. Ph.D. Thesis, Southern Cross University, Lismore, Australia, 2001. [Google Scholar]

- Henseler, J.; Ringle, C.M.; Sinkovics, R.R. The use of partial least squares path modeling in international marketing. Adv. Int. Mark. 2009, 20, 277–319. [Google Scholar]

- Hair, J.F., Jr.; Hult, G.T.M.; Ringle, C.M.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling. Long Range Planning 46, 1st ed.; Sage: Singapore, 2014. [Google Scholar]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis, 7th ed.; Upper Saddle River; Prentice Hall: Hoboken, NJ, USA, 2010. [Google Scholar]

- Hair, J.F.; Ringle, C.M.; Sarstedt, M. PLS-SEM: Indeed a silver bullet. J. Mark. Theory Pract. 2011, 19, 139–151. [Google Scholar] [CrossRef]

- Duarte, P.A.O.; Raposo, M.L.B. A PLS model to study brand preference: An application to the mobile phone market. In Handbook of Partial Least Squares: Concepts, Methods and Applications; Springer: Berlin/Heidelberg, Germany, 2010; pp. 449–485. [Google Scholar]

- Hulland, J. Use of partial least squares (PLS) in strategic management research: A review of four recent studies. Strateg. Manag. J. 1999, 20, 195–204. [Google Scholar] [CrossRef]

- Sun, W.; Chou, C.P.; Stacy, A.W.; Ma, H.; Unger, J.; Gallaher, P. SAS and SPSS macros to calculate standardized Cronbach’s alpha using the upper bound of the phi coefficient for dichotomous items. Behav. Res. Methods 2007, 39, 71–81. [Google Scholar] [CrossRef]

- Hair, J.F.; Hult, G.T.M.; Ringle, C.M.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM), 2nd ed.; Sage: Thousand Oaks, CA, USA, 2017. [Google Scholar]

- Peterson, R.A.; Kim, Y. On the relationship between coefficient alpha and composite reliability. J. Appl. Psychol. 2013, 98, 194–198. [Google Scholar] [CrossRef]

- McCrae, R.R.; Kurtz, J.E.; Yamagata, S.; Terracciano, A. Internal consistency, retest reliability, and their implications for personality scale validity. Personal. Soc. Psychol. Rev. 2011, 15, 28–50. [Google Scholar] [CrossRef]

- Götz, O.; Liehr-Gobbers, K.; Krafft, M. Evaluation of structural equation models using the partial least squares (PLS) approach. In Handbook of Partial Least Squares; Springer: Berlin/Heidelberg, Germany, 2010; pp. 691–711. [Google Scholar]

- Hair, J.F.; Risher, J.J.; Sarstedt, M.; Ringle, C.M. When to use and how to report the results of PLS-SEM. Eur. Bus. Rev. 2019, 31, 2–24. [Google Scholar] [CrossRef]

- Fornell, C.; Larcker, D.F. Structural equation models with unobservable variables and measurement error: Algebra and statistics. J. Mark. Res. 1981, 18, 382–388. [Google Scholar] [CrossRef]

- Chin, W.W. Commentary: Issues and Opinion on Structural Equation Modeling. MIS Q. 1998, 22, 7–16. [Google Scholar]

- Yany, G.; Robert, F. The effects of relationship quality on customer retaliation. Mark. Lett. 2006, 17, 31–46. [Google Scholar]

- Henseler, J.; Ringle, C.M.; Sarstedt, M. A New Criterion for Assessing Discriminant Validity in Variance-Based Structural Equation Modeling. J. Acad. Mark. Sci. 2015, 43, 115–135. [Google Scholar] [CrossRef]

- Henseler, J.; Hubona, G.; Ray, P.A. Using PLS path modeling in new technology research: Updated guidelines. Ind. Manag. Data Syst. 2016, 116, 2–20. [Google Scholar] [CrossRef]

- Kline, B.P. Principles and Practice of Structural Equation Modeling, 3rd ed.; Guilford Press: New York, NY, USA, 2011. [Google Scholar]

- Clark, L.A.; Watson, D. Constructing validity: Basic issues in objective scale development. Psychol. Assess. 1995, 7, 309–319. [Google Scholar] [CrossRef]

- Teo, T.S.H.; Srivastava, S.C.; Jiang, L. Trust and electronic government success: An empirical study. J. Manag. Inf. Syst. 2008, 25, 99–132. [Google Scholar] [CrossRef]

- Gold, A.H.; Malhotra, A.; Segars, A.H. Knowledge management: An organizational capabilities perspective. J. Manag. Inf. Syst. 2001, 18, 185–214. [Google Scholar] [CrossRef]

- Ringle, C.M.; Wende, S.; Becker, J.M. SmartPLS 3. Boenningstedt: SmartPLS GmbH. 2015. Available online: https://www.smartpls.com (accessed on 6 June 2022).

- Falk, R.F.; Miller, N.B. A Primer for Soft Modeling; University of Akron Press: Akron, OH, USA, 1992. [Google Scholar]

- Geisser, S. A predictive approach to the random effect model. Biometrika 1975, 61, 101–107. [Google Scholar] [CrossRef]

- Stone, M. Cross-validatory choice and assessment of statistical predictions. J. R. Stat. Soc. 1974, 36, 111–147. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Sources and Context of Study | CSFs for CSR | |

|---|---|---|

| Corporate Responsibility Forum (2004) [11] The EU’s multi stakeholder forum on CSR in 2004 | 1. Devotion from key people 2. Integrating values and vision of CSR into business and culture 3. Integrating CSR into strategic management and operations 4. Setting appropriate goals and targets, related to core business 5. Communicating CSR aims and activities in a transparent way 6. Openness to learning improvement and innovation | 7. Engagement with external stakeholders 8. Involving employees in implementing CSR 9. Sharing experience and learning with stakeholders 10. The accessibility to effective initiatives 11. The existence of an appropriate legal environment 12. Awareness and responding to company issues |

| Kahreh et al. (2013) [10] The banking sector of Iran | 1. Communicating purpose, vision, and values consistent with business 2. Information provision 3. Knowledge sharing 4. Cooperation 5. Legal norms 6. Employee volunteering 7. Community involvement 8. Involvement of the board of directors 9. Inspirational leadership 10. Financial orientation of organisation 11. Customer satisfaction and loyalty 12. Organisational brand 13. Employee devotion to CSR 14. Financial performance/preparedness | 15. Social norms and the impact of community factors 16. Transformation of stakeholders’ needs into business strategy 17. Organisational culture 18. Competitive orientation 19. Organisational citizenship behaviour 20. Formal strategic planning 21. High level of communication in organisation 22. Presence of a CSR committee 23. Top management devotion to CSR |

| Nyuur et al. (2014) [12] Manufacturing, mining and extraction, retail, services, ICT, financial, and other sectors in Sub-Saharan Africa | 1. Leadership and governance 2. The availability of CSR policy framework within organisation 3. Project management 4. Monitoring, evaluation, and reporting 5. Enable to engage and communicate constantly with all stakeholders | 6. Staff engagement 7. Governments’ ability to create a conducive environment for CSR 8. The mutual exchange of CSR benefits between companies and communities 9. Funding |

| Insurance company in Thailand | 1. Allocation of adequate budgets throughout the project 2. Top management devotion to CSR 3. Integrating CSR into everyday operational practice | 4. Staff engagement 5. Formal strategic planning and CSR measurement 6. Focus on quality of CSR 7. Project management |

| Sangle (2009) [14] Indian public sector | 1. Integrating CSR with functional strategies of organisation 2. Organisational ability to management stakeholder groups 3. Ability to evaluate CSR benefits 4. Top management support 5. Integrating values and vision of CSR into organisational culture | 6. Openness to learning improvement and innovation 7. Employee involvement in implementing CSR 8. Sharing experience, learning from and with peers 9. Government support 10. Non-governmental organisations’ (NGOs) support 11. Society support |

| Singchoo (2012) [15] The director of the sustainable business development institute at Thammasat University Thailand | 1. Leadership and governance 2. Participation of all sectors in CSR strategic planning process 3. Concerning consumers and market 4. Environmental management within organisations and society 5. CSR knowledge management and knowledge transfer to stakeholders 6. Ability of HRM | 7. Internal and external organisational communication 8. Resource management with reducing environmental and social impact 9. Obeying laws and participation in community and social development 10. Disclosure of CSR information |

| Woo (2013) [16] | 1. Leadership and corporate tone 2. Line leadership and local support 3. Embed CSR into HRM 4. Stakeholder engagement and supply chain management | 5. Integrate CSR into marketing strategy 6. CSR measurement and communication |

| Xuerong et al. (2013) [8] Chinese hotel industry | 1. Implementing CSR in the internal and external organisation 2. Providing accommodation and support for governmental activities | 3. More responsibility to all stakeholders 4. Linking CSR to core business 5. Disclosure of CSR information |

| Researchers | [19] | [20] | [26] | [27] | [21] | [22] | [23] | [24] | [25] |

|---|---|---|---|---|---|---|---|---|---|

| CSFs for CSR | |||||||||

| 1. Top management devotion to CSR | √ | √ | √ | √ | √ | √ | √ | ||

| 2. Formal CSR strategic plan and practices | √ | √ | √ | √ | √ | ||||

| 3. Consumer-oriented strategy | √ | √ | √ | √ | √ | ||||

| 4. Implanting of CSR into the organisational culture and citizen behaviour | √ | √ | √ | √ | √ | √ | |||

| 5. Employee devotion to CSR | √ | √ | √ | √ | √ | √ | √ | √ | √ |

| 6. Stakeholder engagement | √ | √ | √ | √ | √ | √ | √ | ||

| 7. Participation in community-related activities | √ | √ | √ | √ | √ | √ | √ | ||

| 8. Knowledge sharing | √ | ||||||||

| 9. Laws and social norms | √ | √ | √ | ||||||

| 10. CSR project management and committees | √ | √ | |||||||

| 11. Financial performance | √ | √ | √ | √ | √ | ||||

| 12. Measurement and report of CSR performance | √ | √ | √ |

| Scales | No. of Items | Cronbach’s Alpha |

|---|---|---|

| 1. Top management devotion to CSR 2. Formal CSR strategic plan and practices 3. Consumer-oriented strategy 4. Implanting CSR into the organisational culture and citizen behaviour 5. Employee devotion to CSR 6. Stakeholder engagement 7. Participation in community-related CSR 8. Knowledge sharing 9. Laws and social norms 10. CSR project management committees 11. Financial performance/preparedness 12. Measurement and report of CSR performance | 3 3 3 3 3 3 3 3 3 3 3 3 | 0.863 0.868 0.799 0.888 0.859 0.945 0.888 0.863 0.869 0.861 0.926 0.912 |

| Total | 0.979 |

| Variables | Operational Definition |

|---|---|

| 1. Top management devotion to CSR | Vision and support of management level to make hotels’ community-related CSR successful |

| 2. Formal CSR strategic plan and practices | Clear plan and direction to bring the CSR concept to everyday operational practice |

| 3. Consumer-oriented strategy | Strategy to ensure quality and safe products and services for customers |

| 4. Implanting CSR into the organisational culture and citizen behaviour | The embedment of shared beliefs held by organisational members to make the whole organisation concerned about CSR |

| 5. Employee devotion | Motivated staff that actively volunteer for CSR |

| 6. Stakeholder engagement | local stakeholders have the chance to engage in the decision-making process |

| 7. Participation in community-related development activities | Hotels take responsibility for developing the areas in which they operate |

| 8. Knowledge sharing | Knowledge sharing to support the exchanging of experiences and knowledge between hotels and the locals |

| 9. Laws and social norms | CSR programs that are in line with laws and social norms |

| 10. CSR project management committees | CSR project management committee that works on CSR from conception to completion |

| 11. Financial performance/preparedness | Allocation of an adequate budget throughout the project. |

| 12. Measurement and report of CSR performance | Measuring and reporting the performance of CSR upon project completion |

| Frequency | Percentage | |

|---|---|---|

| Involved directly in a hotel’s community-related CSR | ||

| Yes | 256 | 95.9 |

| No | 11 | 4.1 |

| District | ||

| Ayer Hangat | 18 | 6.7 |

| Bohor | 12 | 8.2 |

| Kedawang | 46 | 17.2 |

| Kuah | 112 | 41.9 |

| Ulu Melaka | 13 | 8.6 |

| Padang Mat Sirat | 46 | 17.2 |

| Age | ||

| Less than 30 years old | 105 | 39.3 |

| 31–40 years old | 89 | 33.3 |

| 41–50 years old | 40 | 15.0 |

| 51–60 years old | 21 | 7.9 |

| More than 60 years old | 12 | 4.5 |

| Gender | ||

| Male | 112 | 41.9 |

| Female | 155 | 58.1 |

| Highest Education Level | ||

| Vocational education | 44 | 16.5 |

| Higher vocational education/SPM | 111 | 41.6 |

| Bachelor’s degree | 87 | 32.6 |

| Master’s degree | 7 | 2.6 |

| Others | 18 | 6.7 |

| Employment Status | ||

| Government | 38 | 14.2 |

| Private | 104 | 39.0 |

| Business | 17 | 6.4 |

| Self-Employed | 64 | 24.0 |

| Unemployed | 44 | 16.5 |

| Estimated Monthly Income | ||

| Less than RM2000 | 178 | 66.7 |

| RM2000–RM4000 | 77 | 28.8 |

| RM4001–RM6000 | 10 | 3.7 |

| RM6001–RM8000 | 2 | 0.7 |

| Main Variable | Latent Construct and Indicator | Loading | Cronbach’s Alpha | Composite Reliability | AVE |

|---|---|---|---|---|---|

| TMD | B1 | 0.986 | 0.984 | 0.989 | 0.969 |

| B2 | 0.990 | ||||

| B3 | 0.997 | ||||

| SPP | B4 | 0.768 | 0.813 | 0.887 | 0.725 |

| B5 | 0.933 | ||||

| B6 | 0.845 | ||||

| COS | B7 | 0.813 | 0.818 | 0.892 | 0.734 |

| B8 | 0.872 | ||||

| B9 | 0.883 | ||||

| OCCB | B10 | 0.954 | 0.894 | 0.935 | 0.829 |

| B11 | 0.813 | ||||

| B12 | 0.957 | ||||

| ED | B13 | 0.842 | 0.821 | 0.893 | 0.737 |

| B14 | 0.873 | ||||

| B15 | 0.86 | ||||

| SE | B16 | 0.861 | 0.835 | 0.901 | 0.752 |

| B17 | 0.88 | ||||

| B18 | 0.86 | ||||

| CB | B19 | 0.84 | 0.813 | 0.889 | 0.728 |

| B20 | 0.858 | ||||

| B21 | 0.861 | ||||

| KS | B22 | 0.866 | 0.837 | 0.902 | 0.754 |

| B23 | 0.865 | ||||

| B24 | 0.873 | ||||

| LSN | B25 | 0.868 | 0.837 | 0.902 | 0.754 |

| B26 | 0.883 | ||||

| B27 | 0.855 | ||||

| PMC | B28 | 0.877 | 0.808 | 0.886 | 0.722 |

| B29 | 0.841 | ||||

| B30 | 0.831 | ||||

| FP | B31 | 0.838 | 0.801 | 0.883 | 0.715 |

| B32 | 0.851 | ||||

| B33 | 0.848 | ||||

| MRP | B34 | 0.858 | 0.833 | 0.900 | 0.749 |

| B35 | 0.853 | ||||

| B36 | 0.885 |

| CB | CE | COS | ED | FP | KS | LSN | MRP | OCCB | PMC | SPP | TMD | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| CB | 0.853 | |||||||||||

| CE | 0.732 | 0.867 | ||||||||||

| COS | 0.672 | 0.738 | 0.856 | |||||||||

| ED | 0.728 | 0.808 | 0.789 | 0.858 | ||||||||

| FP | 0.758 | 0.658 | 0.655 | 0.685 | 0.846 | |||||||

| KS | 0.783 | 0.768 | 0.675 | 0.741 | 0.75 | 0.868 | ||||||

| LSN | 0.734 | 0.754 | 0.679 | 0.733 | 0.749 | 0.783 | 0.868 | |||||

| MRP | 0.718 | 0.692 | 0.638 | 0.69 | 0.82 | 0.741 | 0.777 | 0.866 | ||||

| OCCB | 0.699 | 0.761 | 0.751 | 0.74 | 0.616 | 0.676 | 0.647 | 0.61 | 0.911 | |||

| PMC | 0.759 | 0.735 | 0.674 | 0.721 | 0.784 | 0.795 | 0.778 | 0.814 | 0.625 | 0.85 | ||

| SPP | 0.63 | 0.666 | 0.765 | 0.705 | 0.574 | 0.606 | 0.642 | 0.583 | 0.678 | 0.617 | 0.851 | |

| TMD | 0.539 | 0.651 | 0.703 | 0.675 | 0.537 | 0.619 | 0.605 | 0.575 | 0.636 | 0.613 | 0.737 | 0.984 |

| CB | SE | COS | ED | FP | KS | LSN | MRP | OCCB | PMC | SPP | TMD | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| B1 | 0.532 | 0.637 | 0.672 | 0.664 | 0.523 | 0.611 | 0.595 | 0.561 | 0.622 | 0.596 | 0.723 | 0.986 |

| B2 | 0.523 | 0.625 | 0.682 | 0.648 | 0.506 | 0.594 | 0.583 | 0.554 | 0.623 | 0.588 | 0.719 | 0.99 |

| B3 | 0.536 | 0.66 | 0.722 | 0.681 | 0.555 | 0.623 | 0.608 | 0.582 | 0.633 | 0.624 | 0.734 | 0.977 |

| B4 | 0.337 | 0.357 | 0.44 | 0.388 | 0.267 | 0.285 | 0.366 | 0.305 | 0.368 | 0.326 | 0.768 | 0.456 |

| B5 | 0.593 | 0.616 | 0.709 | 0.673 | 0.539 | 0.557 | 0.605 | 0.552 | 0.646 | 0.573 | 0.933 | 0.713 |

| B6 | 0.612 | 0.657 | 0.739 | 0.67 | 0.584 | 0.626 | 0.611 | 0.567 | 0.647 | 0.611 | 0.845 | 0.661 |

| B7 | 0.553 | 0.6 | 0.813 | 0.622 | 0.523 | 0.536 | 0.513 | 0.493 | 0.626 | 0.515 | 0.625 | 0.576 |

| B8 | 0.585 | 0.658 | 0.872 | 0.699 | 0.549 | 0.596 | 0.59 | 0.555 | 0.656 | 0.606 | 0.631 | 0.615 |

| B9 | 0.588 | 0.638 | 0.883 | 0.702 | 0.606 | 0.6 | 0.633 | 0.585 | 0.648 | 0.604 | 0.708 | 0.616 |

| B10 | 0.65 | 0.684 | 0.653 | 0.642 | 0.552 | 0.609 | 0.568 | 0.549 | 0.954 | 0.551 | 0.604 | 0.567 |

| B11 | 0.608 | 0.674 | 0.716 | 0.701 | 0.57 | 0.606 | 0.613 | 0.562 | 0.813 | 0.587 | 0.618 | 0.593 |

| B12 | 0.649 | 0.719 | 0.682 | 0.679 | 0.561 | 0.629 | 0.588 | 0.556 | 0.957 | 0.569 | 0.628 | 0.577 |

| B13 | 0.611 | 0.699 | 0.68 | 0.842 | 0.582 | 0.619 | 0.616 | 0.58 | 0.632 | 0.621 | 0.63 | 0.581 |

| B14 | 0.617 | 0.704 | 0.659 | 0.873 | 0.583 | 0.622 | 0.634 | 0.604 | 0.63 | 0.606 | 0.568 | 0.563 |

| B15 | 0.645 | 0.677 | 0.691 | 0.86 | 0.6 | 0.665 | 0.636 | 0.592 | 0.641 | 0.629 | 0.617 | 0.593 |

| B16 | 0.587 | 0.861 | 0.596 | 0.681 | 0.544 | 0.646 | 0.633 | 0.588 | 0.658 | 0.608 | 0.525 | 0.511 |

| B17 | 0.634 | 0.88 | 0.696 | 0.725 | 0.61 | 0.7 | 0.65 | 0.62 | 0.667 | 0.656 | 0.638 | 0.616 |

| B18 | 0.682 | 0.86 | 0.627 | 0.695 | 0.558 | 0.65 | 0.678 | 0.591 | 0.656 | 0.648 | 0.567 | 0.566 |

| B19 | 0.84 | 0.589 | 0.536 | 0.603 | 0.628 | 0.641 | 0.599 | 0.582 | 0.59 | 0.635 | 0.489 | 0.414 |

| B20 | 0.858 | 0.646 | 0.6 | 0.636 | 0.663 | 0.688 | 0.643 | 0.61 | 0.626 | 0.634 | 0.561 | 0.473 |

| B21 | 0.861 | 0.639 | 0.585 | 0.624 | 0.65 | 0.676 | 0.638 | 0.646 | 0.574 | 0.674 | 0.564 | 0.494 |

| B22 | 0.682 | 0.672 | 0.598 | 0.628 | 0.646 | 0.866 | 0.687 | 0.633 | 0.587 | 0.661 | 0.525 | 0.527 |

| B23 | 0.714 | 0.677 | 0.595 | 0.666 | 0.67 | 0.865 | 0.653 | 0.647 | 0.616 | 0.704 | 0.537 | 0.56 |

| B24 | 0.646 | 0.651 | 0.565 | 0.638 | 0.639 | 0.873 | 0.697 | 0.651 | 0.559 | 0.709 | 0.516 | 0.527 |

| B25 | 0.684 | 0.644 | 0.606 | 0.646 | 0.685 | 0.693 | 0.868 | 0.677 | 0.588 | 0.667 | 0.556 | 0.502 |

| B26 | 0.631 | 0.679 | 0.583 | 0.654 | 0.655 | 0.696 | 0.883 | 0.685 | 0.555 | 0.695 | 0.558 | 0.53 |

| B27 | 0.592 | 0.642 | 0.58 | 0.607 | 0.607 | 0.648 | 0.855 | 0.661 | 0.541 | 0.664 | 0.559 | 0.547 |

| B28 | 0.663 | 0.646 | 0.598 | 0.635 | 0.652 | 0.704 | 0.671 | 0.698 | 0.522 | 0.877 | 0.58 | 0.553 |

| B29 | 0.66 | 0.646 | 0.586 | 0.662 | 0.685 | 0.713 | 0.67 | 0.682 | 0.598 | 0.841 | 0.501 | 0.555 |

| B30 | 0.61 | 0.577 | 0.53 | 0.536 | 0.664 | 0.603 | 0.64 | 0.696 | 0.469 | 0.831 | 0.488 | 0.446 |

| B31 | 0.689 | 0.625 | 0.588 | 0.628 | 0.838 | 0.653 | 0.643 | 0.686 | 0.558 | 0.705 | 0.521 | 0.518 |

| B32 | 0.642 | 0.532 | 0.544 | 0.567 | 0.851 | 0.607 | 0.642 | 0.702 | 0.538 | 0.645 | 0.478 | 0.42 |

| B33 | 0.592 | 0.512 | 0.528 | 0.544 | 0.848 | 0.641 | 0.615 | 0.692 | 0.467 | 0.639 | 0.457 | 0.421 |

| B34 | 0.597 | 0.576 | 0.521 | 0.559 | 0.7 | 0.626 | 0.625 | 0.858 | 0.507 | 0.69 | 0.47 | 0.474 |

| B35 | 0.647 | 0.623 | 0.577 | 0.615 | 0.712 | 0.678 | 0.685 | 0.853 | 0.552 | 0.717 | 0.533 | 0.509 |

| B36 | 0.621 | 0.596 | 0.558 | 0.617 | 0.716 | 0.622 | 0.705 | 0.885 | 0.526 | 0.706 | 0.51 | 0.509 |

| CB | CE | COS | ED | FP | KS | LSN | MRP | OCCB | PMC | SPP | TMD | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| CB | ||||||||||||

| SE | 0.888 | |||||||||||

| COS | 0.824 | 0.893 | ||||||||||

| ED | 0.89 | 0.876 | 0.86 | |||||||||

| FP | 0.839 | 0.804 | 0.806 | 0.844 | ||||||||

| KS | 0.85 | 0.818 | 0.814 | 0.894 | 0.816 | |||||||

| LSN | 0.887 | 0.802 | 0.816 | 0.882 | 0.812 | 0.833 | ||||||

| MRP | 0.873 | 0.829 | 0.77 | 0.834 | 0.804 | 0.888 | 0.829 | |||||

| OCCB | 0.821 | 0.883 | 0.881 | 0.866 | 0.73 | 0.783 | 0.749 | 0.709 | ||||

| PMC | 0.836 | 0.893 | 0.824 | 0.882 | 0.875 | 0.865 | 0.845 | 0.893 | 0.735 | |||

| SPP | 0.742 | 0.773 | 0.802 | 0.827 | 0.672 | 0.695 | 0.749 | 0.676 | 0.763 | 0.726 | ||

| TMD | 0.603 | 0.718 | 0.783 | 0.75 | 0.603 | 0.683 | 0.667 | 0.634 | 0.68 | 0.683 | 0.799 |

| Assessment | Criterion | Comment | Results |

|---|---|---|---|

| Internal Consistency | CR | Exceeded 0.08, thus demonstrating internal consistency | Achieved |

| Indicator Reliability | Indicator Loading | All items loaded more than 0.5, demonstrating indicator reliability | Achieved |

| Convergent Validity | AVE | Each construct has an AVE value more than 0.5, thus demonstrating convergent validity. | Achieved |

| Discriminant Validity |

| Square root of the AVE values should be greater than the correlations among the latent constructs Loadings of each indicator were highest for their designated construct | Achieved Achieved |

| The value was less than 1 | Achieved |

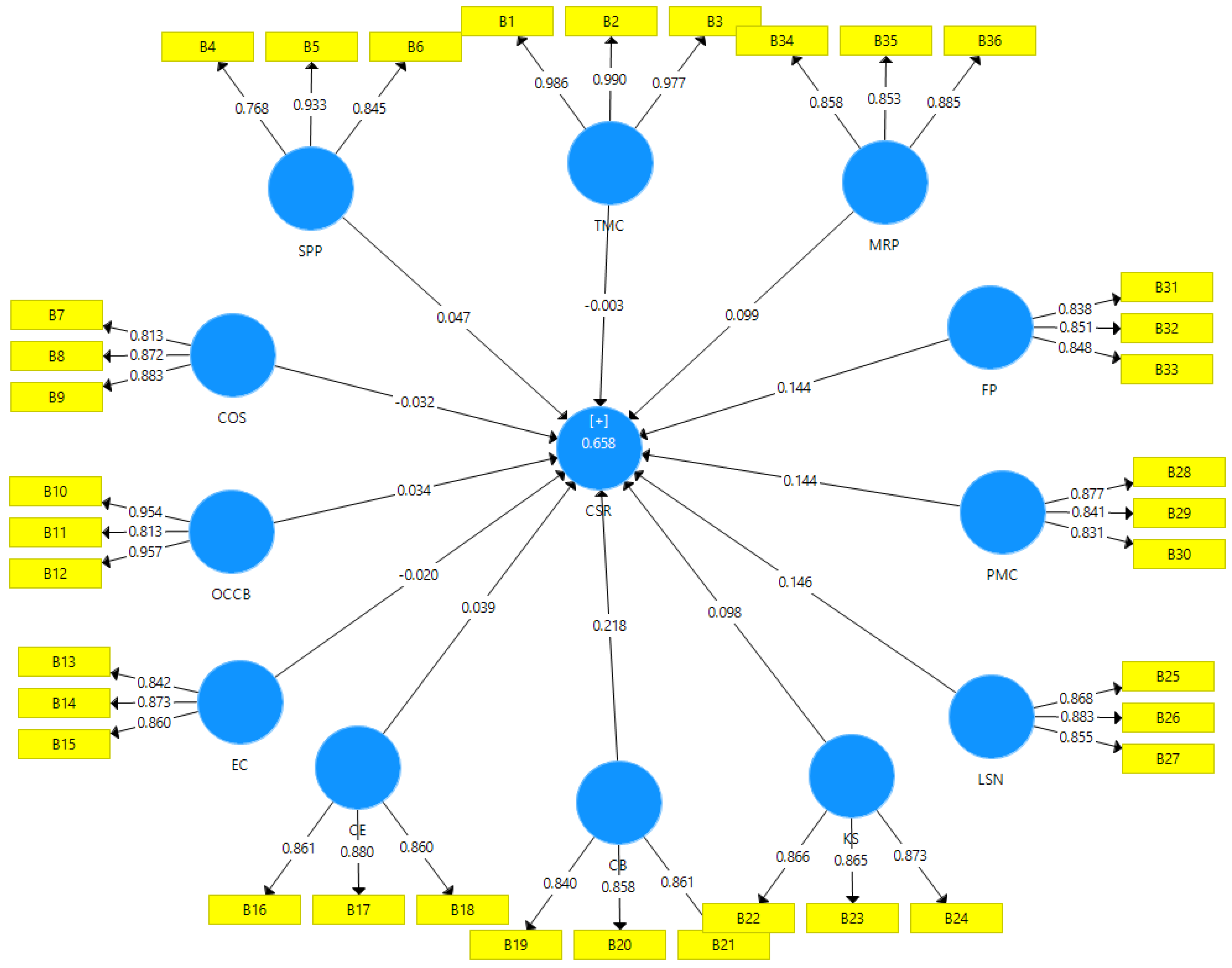

| Original Sample (O) | Sample Mean (M) | Standard Deviation (STDEV) | T Statistics (|O/ STDEV|) | p Values | |

|---|---|---|---|---|---|

| CB ≥ CSR | 0.218 | 0.217 | 0.069 | 3.169 | 0.002 |

| SE ≥ CSR | 0.039 | 0.047 | 0.064 | 0.612 | 0.541 |

| COS ≥ CSR | −0.032 | −0.035 | 0.066 | 0.476 | 0.635 |

| ED ≥ CSR | −0.02 | −0.018 | 0.07 | 0.285 | 0.776 |

| FP ≥ CSR | 0.144 | 0.144 | 0.07 | 2.061 | 0.040 |

| KS ≥ CSR | 0.098 | 0.095 | 0.072 | 1.367 | 0.172 |

| LSN ≥ CSR | 0.146 | 0.143 | 0.064 | 2.264 | 0.024 |

| MRP ≥ CSR | 0.099 | 0.098 | 0.069 | 1.437 | 0.151 |

| OCCB ≥ CSR | 0.034 | 0.033 | 0.063 | 0.538 | 0.591 |

| PMC ≥ CSR | 0.144 | 0.146 | 0.068 | 2.11 | 0.035 |

| SPP ≥ CSR | 0.047 | 0.051 | 0.054 | 0.866 | 0.387 |

| TMD ≥ CSR | −0.003 | −0.003 | 0.055 | 0.058 | 0.953 |

| Latent Variable | R Square | R Square Adjusted |

|---|---|---|

| CSR | 0.658 | 0.650 |

| Total | SSO | SSE | Q2 Statistics (1-SSE/SSO) |

|---|---|---|---|

| CSR | 522 | 200.925 | 0.615 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kasim, A.; Jailani, S.N.; Mokhtar, M.F.; Radha, J.Z.R.R.R.; Khuadthong, B.; Fong, M.L.S. Community Perceptions on the Critical Success Factors of Hotels’ Community-Based Corporate Social Responsibility. Sustainability 2023, 15, 9842. https://doi.org/10.3390/su15129842

Kasim A, Jailani SN, Mokhtar MF, Radha JZRRR, Khuadthong B, Fong MLS. Community Perceptions on the Critical Success Factors of Hotels’ Community-Based Corporate Social Responsibility. Sustainability. 2023; 15(12):9842. https://doi.org/10.3390/su15129842

Chicago/Turabian StyleKasim, Azilah, Siti Noormala Jailani, Muhammad Fauzi Mokhtar, Jasmine Zea Raziah Radha Rashid Radha, Bussalin Khuadthong, and Maebel Leong Sai Fong. 2023. "Community Perceptions on the Critical Success Factors of Hotels’ Community-Based Corporate Social Responsibility" Sustainability 15, no. 12: 9842. https://doi.org/10.3390/su15129842

APA StyleKasim, A., Jailani, S. N., Mokhtar, M. F., Radha, J. Z. R. R. R., Khuadthong, B., & Fong, M. L. S. (2023). Community Perceptions on the Critical Success Factors of Hotels’ Community-Based Corporate Social Responsibility. Sustainability, 15(12), 9842. https://doi.org/10.3390/su15129842