Abstract

This study aims to investigate the dynamic correlations among carbon emission reduction, total cost savings, and asset investments in the industrial sector in China. This study uses the panel vector autoregressive (PVAR) model and the generalized method of moments (GMM) model to obtain three conclusions based on Chinese industrial industry data from 2005–2019. (1) The interaction between carbon emission reduction and cost reduction is bidirectional. A carbon emission decrease can result in persistent cost cutting, while measures in shrinking costs lead to reducing carbon emissions with lasting effects. Moreover, carbon emission decline has strong inertia, while cost reduction is softer. (2) Green investment promotes reducing carbon emissions and is efficient and sustainable. Conversely, completing carbon reduction milestones will inhibit asset expansion in the subsequent period. (3) China’s industrial sector has already achieved the “synergy of emission reduction and cost decrease” development model. The transmission chain “asset investment–carbon emission decline–cost decrease–carbon emission abatement” has been established. Nonetheless, a gap remains between the mature cycle of decarbonization, cost saving, and effectiveness. Finally, it is recommended that the government focuses on the synergistic effect of carbon and cost reduction, encourages continuous green investment, and systematically organizes decarbonization actions. This study provides a basis for increasing the interest of companies in transitioning to a low-carbon economy, contributing to the simultaneous realization of green development and economic benefits.

1. Introduction

Reducing carbon emissions is viewed as the primary strategy for mitigating global warming, and speeding the transition to a low-carbon economy is one of the most important collective goals. The adoption and implementation of the Kyoto Protocol, the Paris Agreement, and the Glasgow Climate Convention have accelerated the process of low-carbon attention and emission reduction by many institutions [1], transforming their behavior and output. As the largest producer of carbon emissions [2], China’s rapid economic growth has coincided with a rapid increase in carbon emissions. This “high energy consumption and high emission” development model is a typical issue for emerging nations, and it reveals a significant obstacle to the economy and society’s green development and sustainable operation [3]. The industrial sector is one of the most significant sources of energy and fuel consumption and carbon emission production, according to Carbon Emission Accounts and Datasets (CEADs), as Figure 1 shows, producing roughly 85% of China’s carbon emissions. The secondary industry consequently plays a crucial role in reaching low-carbon emissions goals.

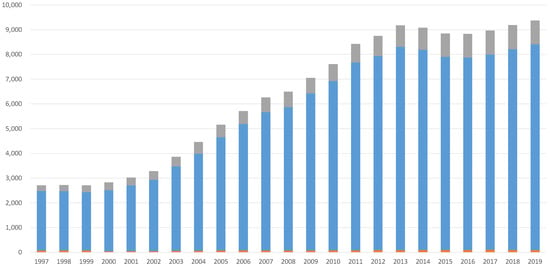

Figure 1.

China’s carbon emissions by industry.

China announced at the 75th session of the United Nations General Assembly in 2020 that it would try to reach carbon neutrality by 2060 and peak its carbon dioxide (CO2) emissions by 2030. In the context of the carbon-peaking and carbon neutrality objectives, the Chinese government has released carbon-peaking implementation plans for major sectors and industries to minimize carbon emissions. Due to each industry’s unique characteristics, distinct features of energy consumption and CO2 emissions are displayed [4], and carbon emissions alter business operations and the course of the industry [5]. To confront the challenges of economic development and environmental protection, a thorough understanding of the impact factors and impacts of emission reduction should be undertaken before policy strategy development and industrial development planning.

Organizational managers actively monitor the risks and opportunities that climate change concerns bring to their organizations’ development [6]. The impact of carbon emissions at the industrial scale may be achieved through creative adjustments and efficient allocation [7], which raises overall technological productivity and efficiency. Reducing carbon emissions is a long-term process intimately tied to company development objectives. As the Chinese government’s requirements for industrial emissions reduction improve, carbon reduction investment decisions have a growing effect on business operations. The process of carbon pollution decline penetrating the business reallocates resources, which affects not only the cost burden, asset structure, and potential carbon benefits of carbon emission measures but also the company’s willingness to cut emissions and the efficacy of emission reduction. With the implementation of low-carbon regulations such as carbon tax, carbon quota, and green investment, carbon dioxide emissions have started impacting manufacturers’ overall costs [8] and asset structure [9]. However, the existing literature has not clarified the interaction of these factors.

In light of current declining economic trends, producers spontaneously engage in cost cutting and asset structure optimization, which is the strategic decision of most enterprises and industries. Some scholars have elaborated on the logic of the economic costs and asset structure of the low-carbon transition. Developed nations have a stronger capacity to transform into a low-carbon economy because they can afford the expenditures associated with the adoption [10]. In contrast, in developing and underdeveloped countries and regions, cleaner production is not a natural or preferred behavior of most producers due to the unaffordable expense and unavailability of investments in green technologies [11]. In addition, several studies have examined how the effectiveness of carbon reduction can be increased by significantly increasing investment in clean energy and low-carbon production [12,13].

Reviewing existing studies, more linkages between decarbonization and shifts in costs and investments have yet to be explicitly stated. Cost and asset systems are significant manifestations of business and strategic shifts, as well as fundamental components of the process of creating corporate value. In a complex organizational setting, the investment in carbon abatement projects is characterized by large scale, irreversibility, and risk [5]. However, the public believes that investments in carbon-reduction-related technologies, such as carbon capture and utilization (CCU) and CO2 capture and storage (CCS), are environmentally friendly and necessary to help mitigate the global warming process [14,15,16]. Therefore, it is essential to conduct an in-depth analysis of the effects of implementing the greenhouse gas mitigation strategy on the economic and organizational levels, particularly in terms of modifications in costs and assets.

Based on previous studies, a variety of research questions raised by implementing carbon reduction strategies, producers’ awareness of cost inflation, and alterations in asset structure have yet to be addressed. The industrial sector serves as an indispensable organization for economic development and carbon reduction. Is its trend of CO2 production improving or worsening as a result of its strategic adjustments, such as cost cutting or asset restructuring? How do emissions reductions affect expenses? How do cost-cutting methods impact emissions? Do green investments and adjustments in asset allocation contribute to reductions in carbon emissions? What influence does carbon reduction have on asset strategy? Are cost reduction methods related to asset modifications? These issues are both sophisticated and relevant to the low-carbon transition plans and routine operations of the industrial sector and require immediate study and response.

In order to address the above issues and to explore carbon reduction pathways and the implications for the industrial sector, this paper empirically examines the dynamic link between carbon emission reduction, cost savings, and asset investment using a panel dataset of industrial industries from 2005 to 2019 using the PVAR series of models. The PVAR model includes the GMM model, the Granger causality test, the impulse response function analysis, and the variance decomposition analysis. These models specifically stated how these components interact from both static and dynamic angles.

This study provided a basis for developing low-carbon policies and strategies for the government and industrial sectors. It also explored pathways for decarbonization efficiency and operational performance and helped industries and enterprises to achieve green development and economic development simultaneously. The following are the primary contributions of our study.

First, this study took a macro and holistic view of the interplay of decisions in the industrial sector. Previous research concentrated on the one-way and independent cost-efficiency analysis of reducing carbon emissions and the influence of green investment on reducing emissions. This study explored quantitatively, for the first time, the dynamic link between CO2 reductions, cost changes, and asset increases.

Second, this research expands the research boundary of carbon reduction mechanisms. Instead of starting from a provincial or urban perspective, we focused on the industrial sector level, in line with the overall sustainability research theme. The study also adopted the first difference method in the treatment of indicator data, which allowed for the more precise observation of indicator variations, while also improving the stability of the model.

Third, the mechanisms of carbon reduction impact at the system level in China’s industrial sector were explored. This paper proposes a synergistic mechanism of “synergy of emission reduction and cost decrease” and a transmission mechanism of “asset investment–carbon emission decline–cost saving–carbon emission decrease”.

This paper consists of five sections. The first section is an introduction, followed by a literature review. The third section describes the PVAR model, variables, and datasets. The fourth section presents the results of the GMM model, the Granger causality test, the impulse response function analysis, and the variance decomposition analysis. The final section incorporates a conclusion and policy implications.

2. Nexus of Carbon Emission, Cost Savings, and Asset Investment

In this section, we review the research on carbon emissions, costs, and assets in order to determine the probable links between them. Reducing carbon emissions is a critical issue for the industrial sector’s green sustainability, and cost systems define the organization’s total profit level and approach development, while asset adjustments represent the organization’s vision and long-term goals.

2.1. Nexus of Carbon Emission and Cost Savings

Environmental effects and production costs are primary concerns for low-carbon transition, and numerous studies have established the correlation between carbon emissions and expense variations. Implementing carbon emission regulations would lead to modifications to organizational charges [17], and some researchers have found that carbon reduction behaviors result in new expenditures. Yang and Chen [18] contended that the production fees of eco-friendly, low-carbon products are greater than those of traditional products. Andersson [19] also believed that decarbonizing resource-intensive and natural-resource-based industries significantly raises production costs. Reducing greenhouse gas emissions generates additional costs for substituting clean energy, investment in green equipment, raw material upgrades, technological development, and modification of operational and managerial processes [20].

Nevertheless, several studies have found that carbon deductions have a noteworthy effect on cost reductions. Even if there are many uncertainties in the path of abatement benefit presentation, it will realize both abatement cost reduction and efficiency improvement [21]. Wang et al. [22] combined the directional distance function model and sensitivity analysis to calculate marginal abatement cost. They concluded that the carbon control target policy should concentrate on decreasing carbon abatement costs. Utilizing low-carbon technology and carbon trading systems to reduce carbon emissions and related expenses is favorable [23]. If insufficient emission allowances are available, manufacturers must modify or close processes and factories or purchase extra emission credits in order for emission reductions to be cost-effective. A decrease in CO2 generates additional income for businesses through energy consumption reduction, carbon trading systems, productivity enhancement, management optimization [24], and low-carbon policy incentives [25], including tax incentives.

In addition, cost changes can affect carbon emissions, but there is not much research on this topic. Zhang and Zhang [26] utilized a multiobjective genetic algorithm on the sustainable design of reinforced concrete elements and discovered that a 5–6% increase in cost resulted in a 14.7% decrease in emissions. Another study [27] showed that reducing fuel consumption or employing low-carbon technologies can reduce marginal costs while decreasing greenhouse gas emissions. Lastly, extensive research has investigated the relationship between carbon emission decline and price adjustments. Cheng et al. [28] demonstrated that aggressive cost-cutting tactics can result in substantial environmental benefits and that an emphasis on environmental protection can also produce economic advantages. Carbon emissions and costs exhibit a learning effect [29] and contribute to the optimization of each other. The scholarly community has not yet reached a solid conclusion regarding the relationship between emission drops and cost shrinking, as it is a systematic and dynamic process.

2.2. Nexus of Carbon Emission and Asset Investment

The majority of research on the linkages between asset development and carbon emission has focused on the unidirectional influence of investment on CO2 change. Adjustments in green capital have a notable impact on carbon emissions, and some of this research corroborates the “investment promotion theory” [30]. Through game theory, genetic algorithms, and cross-sectional augmented autoregressions, this research suggests that higher carbon emission reduction efficiency encourages investment in green assets and low-carbon ventures. Zhang et al. [31] discovered that enhancing the capacity of organizational managers to make carbon resource investment decisions can further cut emissions and operational expenses. In contrast, the “investment disincentive theory” [32,33,34] proposes that investment expansion leads to higher carbon emissions. Although this influence weakens over time, carbon regulation and carbon reduction diminish the value of corporate assets and investments.

Reducing carbon emissions and investing in assets have long been the top priorities for industry and businesses. Carbon emissions create new investment opportunities, and the fraction of emissions reductions attributable to low-carbon projects will continue to increase [35]. Managers achieve their emission reduction objectives through asset diversification, such as upgrading low-carbon equipment, renewable energy machinery, and free-carbon technology [36]. When the organization’s carbon emissions are less than the specified value and gain through various routes, or when the value of carbon-emitting affects the firm’s asset structure, emissions become an asset [8,37]. Kozera et al. [38] demonstrated that the greater the investment in establishing a low-carbon economy, the greater its economic potential. Consequently, green investments can provide prospects for sustainable business growth.

However, investment flows from high-carbon to low-carbon technologies are also risky, and regulations can stimulate investment by boosting returns and eliminating risks [39]. Moreover, lessening carbon emissions may have an inverse relationship with corporate asset growth. As the synchronization of carbon emissions with economic growth [40] highlights the downward economic trend and negative capacity pressure, reducing carbon emissions inhibits the behavior of corporate assets in this instance. Regardless, there is also a complex dynamic effect between their effects.

2.3. Nexus of Asset Investment and Cost Savings

Regarding the relationship between asset growth and cost consequences, cost-effectiveness has been one of the most critical factors influencing corporate asset development [41]. Toptal et al. [42] stated that induced asset expansion and enhanced investment efficiency could achieve both carbon emission and cost optimization. Nevertheless, the cost-effectiveness of asset investment may need to be demonstrated during the firm’s long-term evolution [13,43]. Although each sector and organization’s marginal abatement costs vary significantly due to their unique characteristics, most subjects can profit from carbon abatement investments [44]. According to a study by Zou and Zhong [45], carbon compliance demands can increase enterprises’ capital intensity, incur higher expenses, and even experience output losses. Therefore, subsidizing operating costs will encourage enterprises to make carbon emission reduction related investments [46]. This practice will increase the cost-effectiveness of associated property transformation initiatives.

Consequently, lower costs will encourage sectors and companies to invest in assets [27]. The strategic choice of asset investment is directly connected to cost restrictions and predicted profits [47], with investment costs having the most significant influence during the evolutionary process and the profit growth coefficient coming into play at the start of the period. In addition, industry considerations play a significant influence in this process [48]. The relationship between changes in corporate assets and expenses is interrelated and mutually influential, exhibiting a continual progression.

2.4. Literature Gap

Based on the above analysis, related scholars agree that a relationship exists between carbon emission reduction, cost, and asset investment. As a result, due to the diversity of research objects, methods, and time periods, scholars have yet to reach a consensus regarding the logical relationships between the three. There are still several gaps in the present body of research.

- (1)

- The majority of previous research focuses on the single causality between the two, ignoring the potential reverse impacts of cost reduction on CO2 emissions and carbon emissions on asset adjustments and missing a systemic level to determine the dynamic mutual interaction between the three.

- (2)

- The existing literature focuses primarily on carbon emissions and the exploration of decarbonization pathways, with little attention paid to the impact of CO2 reduction on organizational subsystems. Nonetheless, evaluating the anticipated impact of reducing carbon emissions is the central focus of the low-carbon transformation of enterprises.

- (3)

- The subjects of most studies are regional and predominantly provincial or focus on a particular industrial subsector. Few studies have examined carbon emission control from a sectoral perspective. This perspective provides a panorama of the overall impact of reducing carbon emissions and the factors involved.

To fill in these gaps, we analyze carbon emission reduction, cost savings, and asset investment using the first difference between two consecutive years. From the perspective of a complex system, we utilize a panel vector autoregressive (PVAR) model to explain the three factors’ logical mechanisms and dynamic evolution. Our study will broaden the perspective of carbon emissions and research, which will be valuable for enhancing the motivation and voluntary emission reduction in industries and businesses, as well as providing a benchmark for the transition of businesses into low-carbon entities.

3. Method

3.1. The PVAR Model

The panel vector autoregressive model (PVAR) is an excellent statistical analysis tool for mining the relationship between variables. Holtz-Eakin et al. [49] created the PVAR, and scholars like Pesaran and Smith [50] made it more applicable. PVAR combines panel data with the vector autoregressive model (VAR), which may account for the time and space dimensions of the data. It considers all variables to be endogenous, has no prior limitations on the relationship between variables, and is devoid of any attitude and theoretical limits, allowing it to thoroughly examine the dynamic interplay between variables in reality. In addition, PVAR can effectively account for individual and temporal impacts. Therefore, it is appropriate to use it to analyze the intricate interaction between carbon emission decline, cost cutting, and asset investment. The PVAR model is depicted by Equation (1):

where represents the individual industry, expresses the time (year), and means the lag order. is the column vector of endogenous variables, represents the intercept term vector, and is the lag variable coefficient matrix. is the jth order lag term of endogenous variables, expresses the individual fixed effects matrix, is the time fixed effects matrix, and is the random perturbation term.

The PVAR model consists of multiple components. First, we need to evaluate the stability of the data and choose the appropriate lag order. Second, in light of the cross-sectional heterogeneity [51], we use the GMM approach to estimate the interactions between variables and conduct stability tests to determine their stability. Then, Granger causality tests are performed to establish the causative relationship between variables. The next step is the impulse response function. It aims to examine the effect of a future shock of one variable on the others. Finally, we finish variance decomposition to determine the proportional contribution of orthogonal unit shocks to each factor, which explains the magnitude of the total effect.

3.2. Variables and Data

Reduced carbon emissions are institutions’ systematic endeavors and strategic conduct. The incremental advantages brought about by these actions should include not only environmental advantages but also benefits to all elements of the business affected by the decision. These benefits will surface in both the short and long run. Thus, we utilized the total value to indicate each system’s current state and the change in value to reflect how each system’s modification has affected the others.

The first difference can be well represented by the changes in factors [52]. It is a technique for dealing with time series data and panel data, as well as a modification in modeling that offers considerable benefits, particularly when there are unmeasured variables. The following are the principal benefits: (1) The first difference satisfies the necessity for representing the indicator’s accurate meaning and is utilized to depict the indicator’s change [53]. (2) The first difference is effective in dynamic panel modeling because it can eliminate both fixed effects and enhance the stability of indicators, as well as address the potential effects of nonstationarity; it also tackles the problem of random parameters [54]. (3) The first difference is also one of the instrumental approaches for GMM estimation, which improves the stability of estimates, hence boosting the credibility of the GMM model and the PVAR model. Hence, we selected the first-order difference of carbon emissions, prime costs, and total assets to reflect their variations.

3.2.1. The Carbon Emission Reduction

The carbon emission reduction is the two-year change in the industry’s carbon emissions. Calculating the annual carbon output value for each industry was the first step. Then, we calculated the carbon emission values using the China Energy Statistical Yearbook’s energy data (2005–2019). The calculation method conforms to the IPCC Guidelines for National Greenhouse Gas Inventories (2006). The formula for the calculation is shown in Equation (2):

where reflects the overall carbon emissions and represents the consumption of the ith energy source. ) is the average low-calorific value of the kth energy source in the China Energy Statistical Yearbook. ) is the IPCC-provided carbon emission factor for the kth energy source.

Figure 2 displays the carbon emissions of each industrial subindustry from 2005 to 2019 in China. Based on each industry’s annual carbon emissions (), we employed the backward first difference method, taking into account the index’s positive factor. As shown in Equation (3), we used the difference between the carbon emissions of industry in the current year and the previous year to calculate the carbon emission reduction () in industry in the current year, represented as a first differential label.

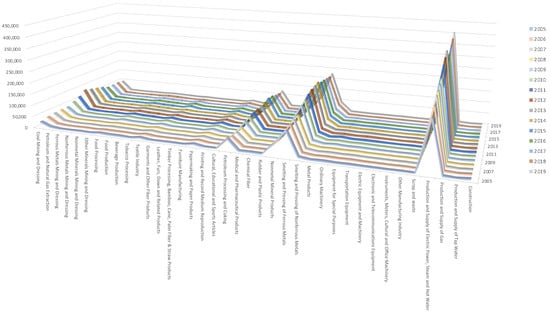

Figure 2.

Carbon emissions by industrial subindustry in China.

3.2.2. Cost Savings

Within a complex system, the potential impact of carbon emission cutting and asset expansion on industrial costs is uncertain. We referred to particular academics [55,56] and utilized the prime costs of each industry for two consecutive years rather than the industry’s total costs (). Data come from the China Industrial Statistics Yearbook (2005–2019). In China, the prime costs indicate the cost related to the central business. Thus, we narrow the scope of the impact analysis by excluding the costs for activities unrelated to their primary activity. Next, by using the backward first difference approach to compute the current year’s cost reduction for each industry, as seen in Equation (4), we determined the current year’s cost savings () for each industry, while taking the cost indicator’s positivity into account.

3.2.3. Asset Investment

Industry and commercial assets are resources that have economic value and can provide owners with rewards. Changes in investment in organizational assets can capture a variety of emission reduction strategies, including energy use reduction, substitution, and elimination. Based on the findings of earlier researchers [57,58], we used the difference between the total assets of the two previous years as a proxy for the asset investment () of the ith industry in the current year. Data are from the China Industrial Statistics Yearbook (2005–2019). To ensure the positivity of the indicator, we calculated the asset investment () of industry for the current year by the forward first difference method, as shown in Equation (5).

3.3. Control Variables

In order to help the model results be more reasonable and reliable and to alleviate the problem of omitted variable bias, two control variables are set in this paper.

(1) Increased gross industrial output (): Economic growth is one of the important factors that leads to increased carbon emissions [59]. At the same time, the optimistic outlook represented by economic growth also leads sectors and firms to increase their investments to enlarge the possibility of obtaining greater profits in the future. Therefore, the forward first difference between the two years of gross industrial output is used as the increased gross industrial output. In order to ensure the positive nature of the indicator, Equation (6) calculates the industrial sector’s gross industrial output ():

(2) Increased business revenue (): As is well known, revenue and costs tend to be positively correlated. In addition, increased revenue increases the likelihood of investment [60]. Therefore, this paper includes increased business revenue as a control variable. Considering the positivity of the indicator, the forward first difference method of two years’ business income was used to represent the increased business income (), as shown in Equation (7):

3.4. Data Processing

All the data were from the China Energy Statistical Yearbook’s energy data (2005–2019) and China Industrial Statistics Yearbook (2005–2019). The data came from various sources compiled by different sectors. Therefore, there were disparities in the caliber of industrial industry norms across multiple yearbooks within the statistical period. We established the following universal quality standards, and the industry adjustments are shown in Table 1.

Table 1.

Industry adjustments.

Following compilation, we identified 42 industrial sectors spanning the years from 2005 to 2019. Then, we deflated TC and AI, using 2005 as the base year. After calculating carbon emission and processing the first difference data, we acquired 588 samples and 2940 observations. Table 2 displays description and descriptive statistics for the observations. Moreover, we can observe from Figure 3 that the total carbon emissions and the total cost of Chinese industry have been decreasing during the observation period, and asset investment has always been increasing. Moreover, the increasing trend of all variables is becoming slower. So, there is a relationship between carbon emissions, total costs, and asset investment in Chinese industry, but this link has not been unraveled yet.

Table 2.

Descriptive Statistics of Variables.

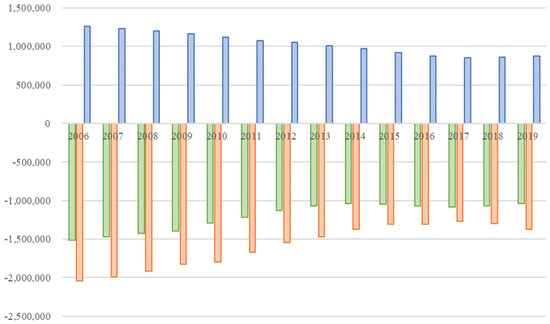

Figure 3.

Trends of ∆CE, ∆TC, and ∆AI.

4. Results and Discussion

4.1. Data Stationarity Test and Optimal Lag Order

To effectively avoid “pseudoregression” and ensure the correctness of the model estimate, we conducted a series of panel unit root tests to assess the panel data’s stability. Table 3 displays the results of these tests. The tests for stationarity consist of the IPS test, the LLC test, the HT test, and the Breitung test. We used these methods to test data stability, except the LLC test, since the LLC type applies to long panel data. At a confidence level of 1%, all variables are statistically significant, ruling out the presence of a panel unit root. Thus, all variables have stable data.

Table 3.

Stability Test of variables.

Then, we utilized the modified Bayesian information criterion (MBIC), modified Akaike information criterion (MAIC), and modified quasi-information criterion (MQIC) to find the ideal lag order that model needs, as shown in Table 4. Under the constraints of the consistent moments model selection criterion, all values at lag 1 are minimal. This result indicates that the initial difference can stabilize all series and satisfy the PVAR model’s requirements. Therefore, we set the optimal model lag period 1.

Table 4.

Test of optimal lag order of the PVAR model.

4.2. GMM Estimation

We estimated the PVAR model for 28 industries using the generalized method of moments (GMM) model. Table 4 demonstrates the relationship between carbon emission decrease, cost reduction, and asset adjustments.

4.2.1. The Carbon Emission Reduction Equation

The carbon emission reduction equation is primarily used to test the impact of carbon emission decrease itself, cost savings, and increased asset investment growth on carbon emission reduction. The results indicate that all the factors substantially positively affect decreasing carbon emissions.

Reducing carbon emissions has a self-reinforcing mechanism. Each 1% reduction in carbon emissions drives an additional 0.567% reduction in carbon emissions. This suggests that carbon mitigation activities in China’s industrial sector can contribute to the next phase of green development. Therefore, CO2 reduction actions are a sustainable and continuous process.

Organizational and institutional cost cutting is also an efficient means of reducing carbon emissions, as demonstrated by the correlation between every 1% of cost cutting and a 0.286% reduction in carbon emissions. This percentage also suggests that cost reductions in the industrial sector also contributed to lower carbon emissions over the sample period. This is consistent with Cheng, Chen, and Chen [28]’s findings for China. Thus, most cost-cutting initiatives implemented across industries are not short-sighted but are long-term proactive measures. They encourage synergistic optimization in terms of cost cutting and emission reduction.

According to GMM estimates, a 1% increase in investment will result in a 0.630% decrease in emissions. This finding suggests that asset expansion can contribute to the greening process of China’s industrial sector throughout the observed period. This finding is consistent with the “investment promotion theory” of several scholars. It is also in line with the conclusions by Chen et al. [61] and He et al. [62], who also used China’s industrial sector as a sample. Therefore, China’s industrial sector should continue to optimize its investment structure and gradually release the investment dividend to promote a low-carbon transition.

4.2.2. The Cost Savings Equation

The cost savings equation examines the effects of carbon emission reduction, cost reduction itself, and increased asset investment on cost savings. Reducing carbon emissions has a significant positive association with cost reductions, whereas cost reduction and asset increase have negative correlations.

Carbon reduction can contribute to the reduction in total costs in the industrial sector. Each 1% reduction in carbon emissions can result in 1.0380% of cost cutting. Although implementing carbon reduction strategies requires initial investments such as hiring consultants, purchasing equipment, and process reorganization, the cost savings from adopting low-carbon behaviors outweigh the expenses. This is consistent with Zhang, Guo, Tan, and Randhir [31]’s view. Thus, in the setting of China’s industrial sector, the low-carbon transition helps companies and sectors to achieve competitive advantage and creates a win–win in terms of environmental benefits, economic benefits, and corporate value.

However, in disagreement with Andersson [19]’s discussion on the EU-15, this study concluded that decarbonization would substantially increase production costs and thus reduce economic welfare. This may be due to the fact that the sample of this study is drawn from industrial sectors represented by energy-intensive and natural-resource-based industries, and the observation period is only seven years, which does not allow us to observe the secular impact of decarbonization on all industrial sectors. Therefore, discussing the long-term effects and conducting an impulse response function analysis is necessary.

Since cost reduction has a negative effect on itself, the approach to reducing costs is not a long-term answer. Cost reduction is also inversely associated with increased investment in assets. This phenomenon shows that green investment in China’s industrial sector is still in its infancy, and it will take several years for asset adjustments to become cost-effective. The insignificance of these two indicators may be attributable to the heavy price of cost cutting, as well as the cumulative and lagging nature of the cost benefits of asset intensification [13,43].

4.2.3. The Asset Investment Equation

The asset investment equation is used to test the effects of carbon emission reduction, cost reduction, and itself. The estimated coefficient of CO2 emission reduction on investment in assets is significantly negative, whereas the coefficients of cost-effectiveness and investment in assets are positive but not statistically significant.

A reduction in carbon emission appears to discourage asset expansion. Every 1% reduction in carbon emissions is associated with a 0.1908% decrease in asset investment. There are two possible explanations for this. One is that the reduction in carbon emissions reflects a negative assessment of future development driven by an economic slump [40], hence shrinking capital and halting all outward expansion and transformational behaviors. The second factor is the shortsightedness of businesses, which take a wait-and-see approach to further asset development after attaining specific emission reduction goals.

Cost reduction has a favorable influence on asset investment, and asset growth also has a specific self-promoting effect. The insignificance of the two indicators could be attributable to the fact that numerous confounding variables influence corporate actions in a complex system (Table 5).

Table 5.

GMM Estimation Results of the PVAR Model.

4.3. Stability Test and Granger Causality Test

We calculated the eigenvalues of the PVAR unit root to determine the model’s stability. In Figure 4, the black dot represents the eigenvalues of , and . It can be observed that all eigenvalues are within the unit circle, demonstrating that the model’s long-term evolution is stable.

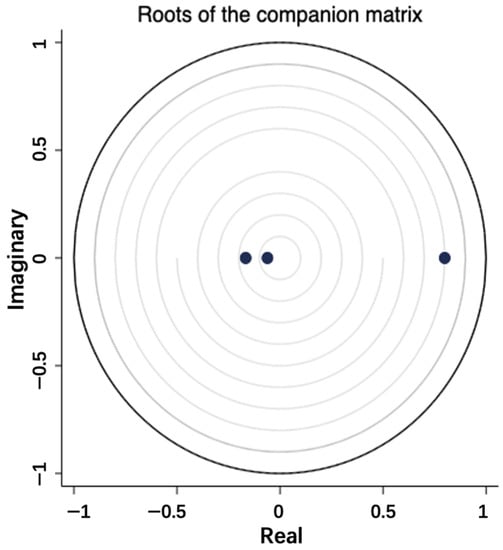

Figure 4.

Stability test of PVAR model.

Next, we conducted the Granger causality tests to identify the causative relationship between carbon emission decrease, cost drop, and asset increase. Table 6 shows a two-way Granger causation between carbon emission reduction and cost savings, carbon emission reduction, and asset investment but not between asset investment and cost savings.

Table 6.

Granger causality test results of the PVAR model.

4.4. Impulse Response Function Analysis

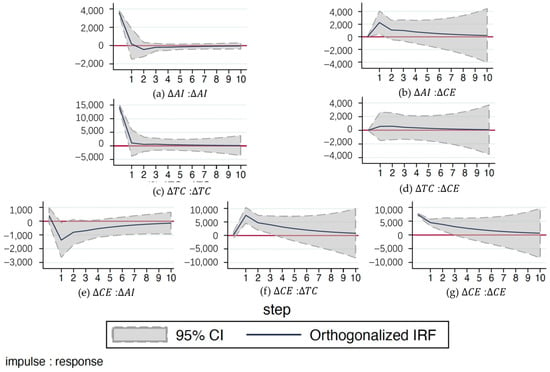

Impulse response function analysis (IRF) is the observation of a variable’s current and future response path in response to a standardized shock to another variable while controlling for all other simulation variables. To determine the dynamic relationship between carbon emission reduction, cost savings, and asset investment, we performed 1000 Monte Carlo simulations of the variables. As cost reductions and asset investment do not satisfy the Granger causality test, other factors with a link are examined. Figure 5 displays the impulse response functions of asset investment, cost savings, and carbon reduction.

Figure 5.

Impulse response diagram of PVAR model.

Figure 5a,c,g depicts the influence of the three factors on themselves. When asset investment, cost reduction, and carbon emission reduction each experience shocks of their own, they all reach a zenith in the current era and then begin to decline. In period 2, asset investment falls to a negative value, and this negative impact diminishes until it is eliminated in period 6. However, there has always been a favorable response to cost reduction and carbon emission cutting. The positive impact of reducing carbon emissions is more pronounced and long-lasting, whereas cost shrinking has a more negligible impact and fades by period 6. This trend suggests that increasing asset investment temporarily restricts asset growth, that cost reduction generates a moderate self-reliance mechanism in development, and that carbon emission reduction has a more robust and long-lasting self-driven mechanism. Thus, from a sustainability perspective, low-carbon emission reduction is a sustainability decision. This is consistent with the view in the GMM estimation model. The industrial sector should adhere to low-carbon emission reduction initiatives and promote green and clean production. Moreover, sustained cost reduction will bring some economic benefits, but it is not something that should be sustained in the long run. Continued investment expansion is also not conducive to sustainable development [63].

Figure 5 depicts the effects of cost reduction and investment on carbon emission reduction at (b) and (d). In the first phase, asset adjustments and cost reduction have a favorable impact on CO2 reduction, but subsequently, the benefit gradually wanes. In period 8, the effect of cost shrinking on CO2 reduction decelerates and disappears, while the effect of asset diversification on carbon emission decreases continues through period 10. This situation suggests that both asset investment and cost reduction are viable long-term strategies for reducing carbon emissions, whereas asset growth is more effective and far-reaching. Cost-saving measures are mainly based on changes to the existing base to achieve emission reductions. Asset investments have impacted the technology and structure in production through the addition of new low-carbon projects and equipment, increasing the efficiency of emission reductions.

Figure 5 depicts the effects of carbon emission reduction on cost reduction and investment in (e) and (f). In Figure 5e, when cost savings are affected by carbon emission reduction, the positive impact is substantial in the initial period, and the positive trend decreases but persists over time. It demonstrates that decreasing carbon emissions contributes to short-term and long-term cost reductions. In Figure 5f, the increasing asset exhibits a positive reaction in the first period after the impact of CO2 control. However, the response turns negative in the next period, and the negative effect slows in the later period but remains constant. This tendency implies that shrinking greenhouse gas boosts asset development in the short term and that in the long run, industrial firms will reduce asset investment due to the achievement of their emission-limited target, which is consistent with the GMM estimation results.

4.5. Variance Decomposition Analysis

Variance decomposition analysis measures the degree to which each stochastic perturbation term contributes to the variance of the expected mean of the endogenous variables. It may examine the impact of structural shocks on changes in the endogenous variables of the impulse function and discover stochastic disturbances inside the model. Table 7 displays the results of a variance decomposition performed on the three variables to further investigate the degree of interaction between them. Carbon reduction, cost changes, and asset increase are all vital strategic decisions and essential operational systems in the organization’s operations. Changes in any variable have a range of direct and indirect consequences on other variables.

Table 7.

Variance decomposition of the PVAR model.

In terms of carbon emission reduction, the variance contribution of carbon emission decline comes primarily from itself. The ratio remains constant at 91.8%, demonstrating that carbon emission decrease has tremendous inertia. Moreover, asset investment and cost reduction donations are beginning to emerge. The rate of investment in assets remains unchanged at 7.2%, while the rate of cost reduction is minimal at 0.1%. These findings, compatible with GMM estimation and Granger causality results, suggest that reducing carbon emissions heavily depends on investment in assets and that cost reduction adds little to emission abatement.

In terms of cost reduction, the impact of cost reduction on itself diminished period by period to 60.98%. It is substituted by the contribution of carbon emission decline to cost reduction, which climbs from 0.02% in the first period to 35.80% in the tenth period. In comparison, asset investment has a 3.2% impact on cost reduction. This conclusion suggests that the self-inertia of cost reduction is weakening, as carbon emission reduction has a burgeoning impact on costs. Asset intensification has virtually no effect on cost changes.

In terms of asset investments, the effects of own and cost reductions both somewhat reduced over the change period, with the effects of own falling by 1.84% and cost reductions dropping by 6.04%. In contrast, the contribution of carbon reduction to investment in assets rose progressively from 0.38% to 8.26%, a 7.8% rise. This inclination demonstrates that asset expansion is initially restricted by cost and investment practices. Nevertheless, in recent years, CO2 controlling has become an increasingly prominent method for restructuring the asset structure of businesses.

In conclusion, the abovementioned changes illustrate the emergence and expansion of carbon emission reduction strategies. Carbon emission reduction has played an increasing role in the operation of industrial enterprises and has become one of the essential strategies. Its impact on cost reduction and asset development is also increasing. This conclusion is in agreement with Liu et al. [64]’ s. In the context of China’s dual carbon targets, the Chinese industrial sector is increasingly emphasizing carbon emission reduction. The government has adopted multiple policies to stimulate spontaneous green and sustainable development. At the same time, low-carbon investments and investment structure optimization have a more substantial impact on carbon reduction and cost optimization, while a single cost-compression exercise reduces economic viability. This is consistent with the conclusions obtained from the pulse analysis. Lastly, businesses and institutions are placing a greater emphasis on the synergistic growth of low-carbon cost reduction.

4.6. Dynamic Interaction Mechanism

We displayed a series of PVAR models. All variables in the model passed the IPS, HT, and Breitung tests, and the optimal lag period was determined to be 1. According to GMM’s estimations, a 1% reduction in emissions would result in a 1.038% reduction in costs and a 0.198% reduction in asset investment. A 1% increase in investment would result in a 0.630% reduction in emissions, but a 1% decrease in costs would result in only a 0.286% reduction in CO2 emissions. The variables subsequently passed the unit root stability test.

The Granger causality test also demonstrated the existence of bidirectional causation between carbon emissions and cost reduction and carbon emissions and asset investment. On the contrary, no causality existed between cost reduction and asset investment. Then, we conducted the impulse response function analysis on the variables with two-way causality and found that carbon emission decline is self-sustaining and has significant inertia. Cost reduction has a slighter self-sustaining inertia. In contrast, asset changes limit investment in the subsequent phase. Both cost decrease and asset growth can aid the process of reducing emissions, although the benefit of asset investment is more substantial and lasting. The favorable impact of carbon emissions on cost reduction is constant and enduring, whereas the impact on asset development is negative.

The variance decomposition analysis of the variables concludes with the following findings: asset increase contributes more to reducing carbon emissions than cost reduction, whereas the self-drive of carbon emission decrease is more robust than both. The auto drive of cost reduction lessens, while the contribution of asset investment to cost reduction grows. In recent years, the impact of carbon emission reduction has intensified on asset adjustments, which are most impacted by self and cost savings.

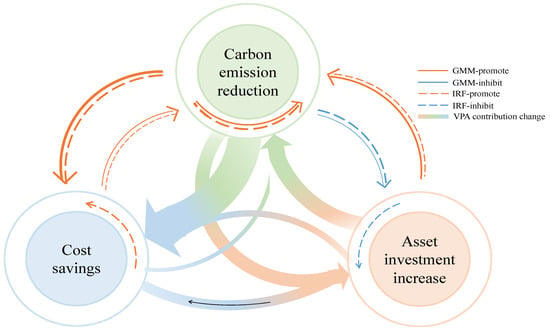

Figure 6 depicts an integration of the resulting relationships for all models, demonstrating the dynamic interaction mechanism of carbon emission reduction, cost savings, and asset investment. In the diagram, the orange line represents the facilitative effect, the blue line indicates the inhibitory effect, and the line’s thickness symbolizes the degree of influence. Additionally, the types of lines illustrate the various methodologies. The solid line denotes the GMM model, the long-dashed line means impulse response, and the streamlined type signifies variance decomposition analysis results.

Figure 6.

Dynamic interaction mechanism among carbon emission reduction, total cost savings, and asset investments.

In general, China’s industrial sector shows a pattern of “synergy of emission reduction and cost decrease”. CO2 reduction and cost reduction in the industrial sector are mutually reinforcing. Cost-saving measures in the industrial sector lead to a reduced carbon footprint, and carbon reduction measures can be cost-effective. In this context, corporate decisions and reforms are often upgraded in terms of process optimization and technological upgrades, which help to achieve both environmental and economic benefits.

From a chain perspective, the Chinese industrial sectors have developed a transmission chain consisting of “asset investment–carbon emission decline–cost saving-carbon emission decrease”. Investment in assets encourages lessening carbon emissions and further promotes cost decreases, and cost shrinking feeds back to provide secondary emission reduction. However, China’s investment in low-carbon assets is still in its infancy, and the long-term cost benefits have not yet materialized, preventing the formation of a complete cycle of carbon emission reduction conduction.

5. Conclusions and Political Implications

Our research offers a novel approach to examining the relationship between carbon emissions, cost savings, and asset investment. We developed a PVAR series model to examine the interaction mechanism between the three variables for 28 industrial sectors in China from 2005 to 2019. We investigated the interaction mechanism of the three variables from both static and dynamic viewpoints, and by integrating the findings mentioned above, as presented in Figure 6, we reached the following conclusions:

- (1)

- Emission reduction and cost savings are coupled. Reducing carbon emissions and lowering costs have considerable bidirectional causality. Reducing carbon emissions can result in substantial short-term and long-term cost decreases, and low-carbon cost reduction measures can reduce CO2. In addition, carbon emission reduction is supported by a robust process of self-reliance and inertia. Cost cutting possesses some inertia, though it is softer than emission control.

- (2)

- Green investment encourages the reduction in emissions. Reducing carbon emissions and investing in assets have substantial bidirectional causality. Companies are more accepting of asset diversification for energy reduction and carbon transition. Compared with cost reduction, asset expansion can significantly enhance the industry’s carbon reduction effect. Moreover, China’s industrial sector is still in the investment growth phase, and the investment dividend is emerging gradually. Nonetheless, due to the achievement of milestones and the short-sightedness of businesses, carbon emission decreases will impede corporate asset expansion to some extent.

- (3)

- Decarbonization, cost saving, and synergy can be developed in a coordinated way. Currently, China’s industrial sector has already achieved the “synergy of emission reduction and cost decrease” development model. Moreover, a transmission chain of “asset investment–carbon emission decline–cost saving-carbon emission decrease” has been formed, but the asset investment at this stage is not yet cost-effective.

Accordingly, we propose the following policy recommendations in light of the previous findings: First, in a downward economic trend, both reasonable cost cutting and green development goals of enterprises should be taken seriously at the same time. The government should stimulate the industrial sector and enterprises to find a cost-effective green transformation path using regulations and policies. Second, the government ought to encourage companies to make sustainable green investments and upgrade their asset mix. Increased research on and development of green technologies and investment in green equipment are also critical. Thirdly, emission reduction entities should utilize the dual effect of carbon emission reduction and cost savings to support green processes. They must systematically promote corporate energy conservation, emission reduction, and carbon reduction in order to realize environmental benefits, reinforce competitive advantages, and constantly increase value.

However, we clearly recognized that the current research is merely a preliminary examination of the impact and influencing factors of carbon reduction at this time. Although this study draws several novel conclusions, its data subjects and research viewpoints limit the generalizability of its outcomes. For validation in the following studies, longer years, more subjects, and different perspectives, such as country-level, firm-level, and program-level, are required. In addition, our study treats all industrial sectors as homogeneous subjects and does not take into account their emission reduction techniques, preferences, or industry features. Thus, the results cannot be applied to the practices of all industries and businesses. In the future, it may be feasible to investigate further consequences of decreasing CO2 and more factors that affect carbon emission reduction.

Author Contributions

Conceptualization, X.W.; Software, X.W.; Writing—original draft, X.W.; Writing—review & editing, X.S. and K.B. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by Office of Jiangsu Provincial Academic Degrees Committee, grant number 2022 Graduate Research and Innovation Projects of Jiangsu Province KYCX22_3741.

Data Availability Statement

All the data were from the China Energy Statistical Yearbook’s energy data (2005–2019) and China Industrial Statistics Yearbook (2005–2019).

Conflicts of Interest

The authors declare no conflict of interest.

References

- Hussain, A.; Perwez, U.; Ullah, K.; Kim, C.-H.; Asghar, N. Long-term scenario pathways to assess the potential of best available technologies and cost reduction of avoided carbon emissions in an existing 100% renewable regional power system: A case study of Gilgit-Baltistan (GB), Pakistan. Energy 2021, 221, 119855. [Google Scholar] [CrossRef]

- Wang, Y.; Yang, H.; Sun, R. Effectiveness of China’s provincial industrial carbon emission reduction and optimization of carbon emission reduction paths in “lagging regions”: Efficiency-cost analysis. J. Environ. Manag. 2020, 275, 111221. [Google Scholar] [CrossRef] [PubMed]

- Li, Z.-Z.; Li, R.Y.M.; Malik, M.Y.; Murshed, M.; Khan, Z.; Umar, M. Determinants of carbon emission in China: How good is green investment? Sustain. Prod. Consum. 2021, 27, 392–401. [Google Scholar] [CrossRef]

- Tang, B.-J.; Ji, C.-J.; Hu, Y.-J.; Tan, J.-X.; Wang, X.-Y. Optimal carbon allowance price in China’s carbon emission trading system: Perspective from the multi-sectoral marginal abatement cost. J. Clean. Prod. 2019, 253, 119945. [Google Scholar] [CrossRef]

- Wang, J.; Rickman, D.S.; Yu, Y. Dynamics between global value chain participation, CO2 emissions, and economic growth: Evidence from a panel vector autoregression model. Energy Econ. 2022, 109, 105965. [Google Scholar] [CrossRef]

- Piecyk, M.I.; McKinnon, A.C. Forecasting the carbon footprint of road freight transport in 2020. Int. J. Prod. Econ. 2010, 128, 31–42. [Google Scholar] [CrossRef]

- Hu, Y.; Ren, S.; Wang, Y.; Chen, X. Can carbon emission trading scheme achieve energy conservation and emission reduction? Evidence from the industrial sector in China. Energy Econ. 2020, 85, 104590. [Google Scholar] [CrossRef]

- Liu, Y.; Tian, L.; Xie, Z.; Zhen, Z.; Sun, H. Option to survive or surrender: Carbon asset management and optimization in thermal power enterprises from China. J. Clean. Prod. 2021, 314, 128006. [Google Scholar] [CrossRef]

- Nidumolu, R.; Prahalad, C.K.; Rangaswami, M.R. Why sustainability is now the key driver of innovation. Harv. Bus. Rev. 2009, 87, 56–64. [Google Scholar]

- Chang, T.-H.; Huang, C.-M.; Lee, M.-C. Threshold effect of the economic growth rate on the renewable energy development from a change in energy price: Evidence from OECD countries. Energy Policy 2009, 37, 5796–5802. [Google Scholar] [CrossRef]

- Bersalli, G.; Menanteau, P.; El-Methni, J. Renewable energy policy effectiveness: A panel data analysis across Europe and Latin America. Renew. Sustain. Energy Rev. 2020, 133, 110351. [Google Scholar] [CrossRef]

- Lee, J.; Yang, J.-S. Global energy transitions and political systems. Renew. Sustain. Energy Rev. 2019, 115, 109370. [Google Scholar] [CrossRef]

- Nemet, G.F.; Jakob, M.; Steckel, J.C.; Edenhofer, O. Addressing policy credibility problems for low-carbon investment. Glob. Environ. Chang. 2017, 42, 47–57. [Google Scholar] [CrossRef]

- Liu, B.; Xu, Y.; Yang, Y.; Lu, S. How public cognition influences public acceptance of CCUS in China: Based on the ABC (affect, behavior, and cognition) model of attitudes. Energy Policy 2021, 156, 112390. [Google Scholar] [CrossRef]

- Sitinjak, C.; Ebennezer, S.; Ober, J. Exploring Public Attitudes and Acceptance of CCUS Technologies in JABODETABEK: A Cross-Sectional Study. Energies 2023, 16, 4026. [Google Scholar] [CrossRef]

- Nielsen, J.A.E.; Stavrianakis, K.; Morrison, Z. Community acceptance and social impacts of carbon capture, utilization and storage projects: A systematic meta-narrative literature review. PLoS ONE 2022, 17, e0272409. [Google Scholar] [CrossRef]

- Anderson, J.J.; Rode, D.; Zhai, H.; Fischbeck, P. Transitioning to a carbon-constrained world: Reductions in coal-fired power plant emissions through unit-specific, least-cost mitigation frontiers. Appl. Energy 2021, 288, 116599. [Google Scholar] [CrossRef]

- Yang, H.; Chen, W. Retailer-driven carbon emission abatement with consumer environmental awareness and carbon tax: Revenue-sharing versus Cost-sharing. Omega 2018, 78, 179–191. [Google Scholar] [CrossRef]

- Andersson, F.N.G. Effects on the manufacturing, utility and construction industries of decarbonization of the energy-intensive and natural resource-based industries. Sustain. Prod. Consum. 2020, 21, 1–13. [Google Scholar] [CrossRef]

- Zhang, Q.; Tang, W.; Zhang, J. Green supply chain performance with cost learning and operational inefficiency effects. J. Clean. Prod. 2016, 112, 3267–3284. [Google Scholar] [CrossRef]

- Guo, J.-X.; Tan, X.; Gu, B.; Qu, X. The impacts of uncertainties on the carbon mitigation design: Perspective from abatement cost and emission rate. J. Clean. Prod. 2019, 232, 213–223. [Google Scholar] [CrossRef]

- Wang, Z.; Chen, H.; Huo, R.; Wang, B.; Zhang, B. Marginal abatement cost under the constraint of carbon emission reduction targets: An empirical analysis for different regions in China. J. Clean. Prod. 2020, 249, 119362. [Google Scholar] [CrossRef]

- Cui, L.-B.; Fan, Y.; Zhu, L.; Bi, Q.-H. How will the emissions trading scheme save cost for achieving China’s 2020 carbon intensity reduction target? Appl. Energy 2014, 136, 1043–1052. [Google Scholar] [CrossRef]

- Helistö, N.; Kiviluoma, J.; Holttinen, H. Long-term impact of variable generation and demand side flexibility on thermal power generation. IET Renew. Power Gener. 2018, 12, 718–726. [Google Scholar] [CrossRef]

- Khajehpour, H.; Saboohi, Y.; Tsatsaronis, G. On the fair accounting of carbon emissions in the global system using an exergy cost formation concept. J. Clean. Prod. 2021, 280, 124438. [Google Scholar] [CrossRef]

- Zhang, X.; Zhang, X. Sustainable design of reinforced concrete structural members using embodied carbon emission and cost optimization. J. Build. Eng. 2021, 44, 102940. [Google Scholar] [CrossRef]

- Rafique, A.; Williams, A.P. Reducing household greenhouse gas emissions from space and water heating through low-carbon technology: Identifying cost-effective approaches. Energy Build. 2021, 248, 111162. [Google Scholar] [CrossRef]

- Cheng, F.; Chen, T.; Chen, Q. Cost-reducing strategy or emission-reducing strategy? The choice of low-carbon decisions under price threshold subsidy. Transp. Res. Part E Logist. Transp. Rev. 2022, 157, 102560. [Google Scholar] [CrossRef]

- Yu, B.; Wang, J.; Lu, X.; Yang, H. Collaboration in a low-carbon supply chain with reference emission and cost learning effects: Cost sharing versus revenue sharing strategies. J. Clean. Prod. 2020, 250, 119460. [Google Scholar] [CrossRef]

- Shen, Y.; Su, Z.-W.; Malik, M.Y.; Umar, M.; Khan, Z.; Khan, M. Does green investment, financial development and natural resources rent limit carbon emissions? A provincial panel analysis of China. Sci. Total Environ. 2021, 755, 142538. [Google Scholar] [CrossRef]

- Zhang, C.; Guo, S.; Tan, L.; Randhir, T.O. A carbon emission costing method based on carbon value flow analysis. J. Clean. Prod. 2020, 252, 119808. [Google Scholar] [CrossRef]

- Lin, B.; Wang, M. Dynamic analysis of carbon dioxide emissions in China’s petroleum refining and coking industry. Sci. Total Environ. 2019, 671, 937–947. [Google Scholar] [CrossRef]

- Dong, H.; Liu, W.; Liu, Y.; Xiong, Z. Fixed asset changes with carbon regulation: The cases of China. J. Environ. Manag. 2022, 306, 114494. [Google Scholar] [CrossRef] [PubMed]

- Li, J.; Li, S. Energy investment, economic growth and carbon emissions in China—Empirical analysis based on spatial Durbin model. Energy Policy 2020, 140, 111425. [Google Scholar] [CrossRef]

- Jiang, K.-J.; Zhuang, X.; He, C.-M.; Liu, J.; Xu, X.-Y.; Chen, S. China’s low-carbon investment pathway under the 2 °C scenario. Adv. Clim. Chang. Res. 2016, 7, 229–234. [Google Scholar] [CrossRef]

- Tamazian, A.; Rao, B.B. Do economic, financial and institutional developments matter for environmental degradation? Evidence from transitional economies. Energy Econ. 2010, 32, 137–145. [Google Scholar] [CrossRef]

- Wang, M.; Dang, C.; Wang, M.; Wang, S. Carbon emission permits: A new asset, Chinese potential market and allocation mechanism. Adv. Inf. Sci. Serv. Sci. 2012, 4, 406–414. [Google Scholar]

- Kozera, A.; Satoła, Ł.; Standar, A.; Dworakowska-Raj, M. Regional diversity of low-carbon investment support from EU funds in the 2014–2020 financial perspective based on the example of Polish municipalities. Renew. Sustain. Energy Rev. 2022, 168, 112863. [Google Scholar] [CrossRef]

- Schmidt, T.S. Low-carbon investment risks and de-risking. Nat. Clim. Chang. 2014, 4, 237–239. [Google Scholar] [CrossRef]

- Charfeddine, L.; Al-Malk, A.Y.; Al Korbi, K. Is it possible to improve environmental quality without reducing economic growth: Evidence from the Qatar economy. Renew. Sustain. Energy Rev. 2018, 82, 25–39. [Google Scholar] [CrossRef]

- Ji, L.; Huang, G.; Niu, D.; Cai, Y.; Yin, J. A Stochastic Optimization Model for Carbon-Emission Reduction Investment and Sustainable Energy Planning under Cost-Risk Control. J. Environ. Inform. 2020, 36, 107–118. [Google Scholar] [CrossRef]

- Toptal, A.; Özlü, H.; Konur, D. Joint decisions on inventory replenishment and emission reduction investment under different emission regulations. Int. J. Prod. Res. 2014, 52, 243–269. [Google Scholar] [CrossRef]

- Xian, Y.; Wang, K.; Wei, Y.M.; Huang, Z. Opportunity and marginal abatement cost savings from China’s pilot carbon emissions permit trading system: Simulating evidence from the industrial sectors. J. Environ. Manag. 2020, 271, 110975. [Google Scholar] [CrossRef] [PubMed]

- Xian, Y.; Wang, K.; Wei, Y.-M.; Huang, Z. Would China’s power industry benefit from nationwide carbon emission permit trading? An optimization model-based ex post analysis on abatement cost savings. Appl. Energy 2019, 235, 978–986. [Google Scholar] [CrossRef]

- Zou, H.; Zhong, M.R. Factor reallocation and cost pass-through under the carbon emission trading policy: Evidence from Chinese metal industrial chain. J. Environ. Manag. 2022, 313, 114924. [Google Scholar] [CrossRef] [PubMed]

- Zhang, X.; Gan, D.; Wang, Y.; Liu, Y.; Ge, J.; Xie, R. The impact of price and revenue floors on carbon emission reduction investment by coal-fired power plants. Technol. Soc. Chang. 2020, 154, 119961. [Google Scholar] [CrossRef]

- Zhu, G.; Pan, G.; Zhang, W. Evolutionary game theoretic analysis of low carbon investment in supply chains under governmental subsidies. Int. J. Environ. Res. Public Health 2018, 15, 2465. [Google Scholar] [CrossRef] [PubMed]

- Wordsworth, A.; Grubb, M. Quantifying the UK’s incentives for low carbon investment. Clim. Policy 2003, 3, 77–88. [Google Scholar] [CrossRef]

- Holtz-Eakin, D.; Newey, W.; Rosen, H.S. Estimating vector autoregressions with panel data. Econom. J. Econom. Soc. 1988, 56, 1371–1395. [Google Scholar] [CrossRef]

- Pesaran, M.H.; Smith, R. Estimating long-run relationships from dynamic heterogeneous panels. J. Econom. 1995, 68, 79–113. [Google Scholar] [CrossRef]

- Pesaran, M.H. Estimation and inference in large heterogeneous panels with a multifactor error structure. Econometrica 2006, 74, 967–1012. [Google Scholar] [CrossRef]

- Zhang, K.; Dong, J.; Huang, L.; Xie, H. China’s carbon dioxide emissions: An interprovincial comparative analysis of foreign capital and domestic capital. J. Clean. Prod. 2019, 237, 117753. [Google Scholar] [CrossRef]

- Anderson, T.W.; Hsiao, C. Formulation and estimation of dynamic models using panel data. J. Econom. 1982, 18, 47–82. [Google Scholar] [CrossRef]

- Han, C.; Phillips, P.C. First difference maximum likelihood and dynamic panel estimation. J. Econom. 2013, 175, 35–45. [Google Scholar] [CrossRef]

- Więcek, D. Implementation of artificial intelligence in estimating prime costs of producing machine elements. Adv. Manuf. Sci. Technol. 2013, 37, 44–52. [Google Scholar] [CrossRef]

- Akcelik, R.; Besley, M. In Operating cost, fuel consumption, and emission models in aaSIDRA and aaMOTION. In Proceedings of the 25th Conference of Australian Institutes of Transport Research (CAITR 2003), Adelaide, Australia, 3–5 December 2003; pp. 1–15. [Google Scholar]

- Guo, C.; Jiraporn, P. Customer satisfaction, net income and total assets: An exploratory study. J. Target. Meas. Anal. Mark. 2005, 13, 346–353. [Google Scholar] [CrossRef]

- Utama, C.A. Company disclosure in Indonesia: Corporate governance practice, ownership structure, competition and total assets. Asian J. Bus. Account. 2012, 5, 75–108. [Google Scholar]

- Long, X.; Naminse, E.Y.; Du, J.; Zhuang, J. Nonrenewable energy, renewable energy, carbon dioxide emissions and economic growth in China from 1952 to 2012. Renew. Sustain. Energy Rev. 2015, 52, 680–688. [Google Scholar] [CrossRef]

- Podrecca, E.; Carmeci, G. Fixed investment and economic growth: New results on causality. Appl. Econ. 2001, 33, 177–182. [Google Scholar] [CrossRef]

- Chen, X.; Luo, Z.; Wang, X. Impact of efficiency, investment, and competition on low carbon manufacturing. J. Clean. Prod. 2017, 143, 388–400. [Google Scholar] [CrossRef]

- He, Y.; Fu, F.; Liao, N. Exploring the path of carbon emissions reduction in China’s industrial sector through energy efficiency enhancement induced by R&D investment. Energy 2021, 225, 120208. [Google Scholar]

- Lu, J.; Li, B.; Li, H.; Zhang, Y. Sustainability of enterprise export expansion from the perspective of environmental information disclosure. J. Clean. Prod. 2020, 252, 119839. [Google Scholar] [CrossRef]

- Liu, J.; Sun, Y.H.; Wang, K.; Zou, J.; Kong, Y. Study on mid-and long-term low carbon development pathway of China’s industry sector. Clim. Chang. Res. 2018, 14, 513–521. [Google Scholar]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).