Abstract

Population growth and urbanization in Thailand has generated negative environmental externalities and the underuse of agricultural materials. Plastics from cassava present an alternative that helps reduce the use of non-biodegradable petroleum-based plastics and can reshape a sustainable cassava value chain. The objectives of this study are to evaluate the cassava value chain, consumer acceptance, and the opportunities and challenges for developing bioplastics from cassava in Thailand. We analyze the value added to different applications of cassava products and investigate the consumer acceptance of bioplastic from cassava using a two-step cluster analysis. From an economic perspective, bioplastics based on cassava add a value of 14.8–22 times that of cassava roots. We conducted a survey of 915 respondents and found that consumer acceptance of bioplastic products from cassava accounts for 48.6% of all respondents, but few are willing to pay extra for them. We also found that the development of cassava-based bioplastic not only positively contributes to economic aspects but also generates beneficial long-term impacts on social and environmental aspects. Considering cassava supply, bioplastic production, and potential consumer acceptance, the development of bioplastics from cassava in Thailand faces several barriers and is growing slowly, but is needed to drive the sustainable cassava value chain. This study provides guidelines for businesses and the government to adopt bioplastics from cassava.

1. Introduction

Cassava is one of the carbohydrate crops that accounts for 10% of total carbohydrate crop consumption in the world after maize, wheat, rice, and potato [1]. Cassava has been used for 4F sectors, including food for humans, feed for animals, fuel for renewable energy, and factories using cassava materials [2]. In Thailand, cassava is not only used for food consumption but is also mainly produced as low-value-based products such as dried cassava for animal feeds and cassava starch for industries [3]. Thailand is the world’s largest exporter of cassava, with a market share of 55.53% of the total global cassava export in 2020 [4]. Thailand exports about 73% of the total cassava production, divided into cassava starch (44.1%), cassava chips (28.2%), and cassava pellets (0.3%) [2]. In 2021, Thailand produced 34.1 million tons of fresh cassava roots, with a total production area of 1.59 million hectares [5].

Market volatility, demand shifts, input supply challenges, and changes in climate events can generate shock and instability in the cassava value chain. Price fluctuations and the global market uncertainties of cassava production have led to lower profitability for farmers and a disruption to the flow of suppliers and buyers in the value chain [4]. The price of cassava widely fluctuates over a year depending on various factors, including the price of substitute products, government intervention, technology availability, and agricultural policy from importing countries, especially China [6,7]. The reduction in the price gap between cassava and other carbohydrate crops and the limitation of value-adding alternatives lead to a lack of competitive advantage in the cassava sector in Thailand.

Facing sustainability and environmental challenges, the bio-based, circular, and green (BCG) economy plan was drawn up to drive policies in the agricultural and industrial sectors. Following the implications of the sustainable development goals (SDGs), Thailand aims to move toward sustainable development coupled with the 20-year national strategy (2018–2037) by exploring value-added agriculture to create new value with the circular economy in agricultural materials and waste, as well as encouraging future industries and services with technology and innovations [8]. The development of the cassava value chain through bioplastic production addresses SDG target 10, where integrating related stakeholders in the value chain gives them an opportunity to participate in income growth, and SDG target 12, where the use of technology moves towards more sustainable patterns of consumption and production (e.g., agricultural waste is perceived as a valuable resource rather than a disposal problem). The circular economy approach seeks to minimize waste and maximize resource efficiency by promoting the reuse, recycling, and repurposing of materials [9,10]. The by-products of cassava starch production (e.g., cassava pulp and cassava peel) are usually used for animal feeds, compost, and produced biogas.

In the past five years, materials and waste from cassava were developed into high-value-added products through innovative processes, especially bio-based materials and products, such as packaging, bioplastics, or construction materials. However, the development of bioplastics from cassava has moved slowly due to limited opportunities for stakeholders in the cassava value chain through processing or value-added activities, as well as limited responses to bioplastics from cassava in the domestic market. Until now, a value chain analysis of bioplastics from cassava in Thailand has not yet been conducted. The production of bioplastics from cassava has the potential to reshape a sustainable cassava value chain. Many studies have focused on the performance improvement of bioplastics from cassava; however, research on the feasibility of these bioplastics for the cassava value chain is limited. To launch bioplastics from cassava into the market, studies on consumer acceptance and production costs are necessary. Thus, this study aims to assess the opportunities and challenges associated with the development of cassava-based bioplastics in Thailand. Moreover, the value chain, consumer acceptance, price comparison between bioplastic resins, and sustainability aspects of bioplastics from cassava were analyzed and discussed. Due to the simple process, low investment, and technology availability of TPS, the present work hence focuses on bioplastic products based on a thermoplastic cassava starch blend (as a case study). This study could serve as a guide for policymakers on the alternative choices to help sustain the cassava value chain, reduce the use of non-biodegradable petroleum-based plastics, minimize the number of imported bioplastics, and promote the utilization of cassava, which is a cheap and abundant feedstock in Thailand.

The next two sections introduce the background and research methods. Afterwards, the empirical section of the paper consists of three parts: the value chain analysis of bioplastics from cassava, the consumer acceptance of bioplastic products, and the opportunities and barriers of bioplastic from cassava based on the sustainability aspects. The two last sections include a discussion and conclusion.

2. Background

2.1. Cassava Sector in Thailand

Thailand is the third largest cassava grower in the world, with a total production of more than 30 million tons per year, after Nigeria and Congo. Cassava production is mostly located in Northeastern Thailand. More than 90% of its production takes place on small family farms, averaging 2.56–3.2 ha per household. From 2021 to 2022, the number of cassava farmer families was 738,153 households, with a production cost of 52.24 USD/ton [4]. The exchange rate used when converting the figures is 1 USD to 35.93 THB [11]. Even though cassava can be planted and harvested throughout the year, the major harvesting season in Thailand typically spans from October to March. This leads to the common problem of oversupply in the cassava value chain, giving the lowest cassava prices over the harvesting seasons and farmers suffering from income uncertainty. Although a government policy (e.g., income guarantee and price support) was implemented to guarantee cassava prices and boost farmers’ income, these schemes do not provide sustainable solutions to the stakeholders, especially farmers [12]. Value addition and circular practices can enhance market competitiveness and create additional revenue streams through sustainable development [3,9]. The BCG economy in Thailand allows new product developments and emerging new production on a number of alternative materials from agricultural resources. The lack of collaboration among cassava industry stakeholders, limited value addition, and constraints in accessing finance and resources can restrict the ability to capture higher prices, increase profitability, and shift to high-value-based products.

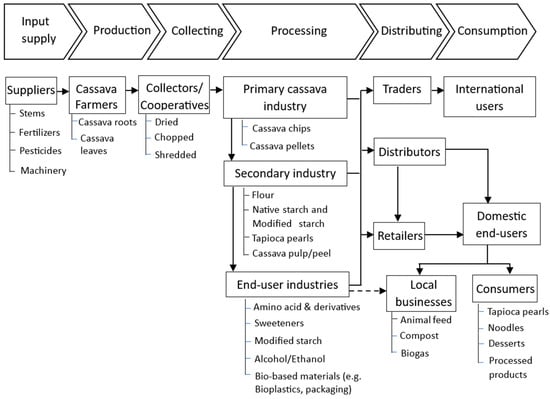

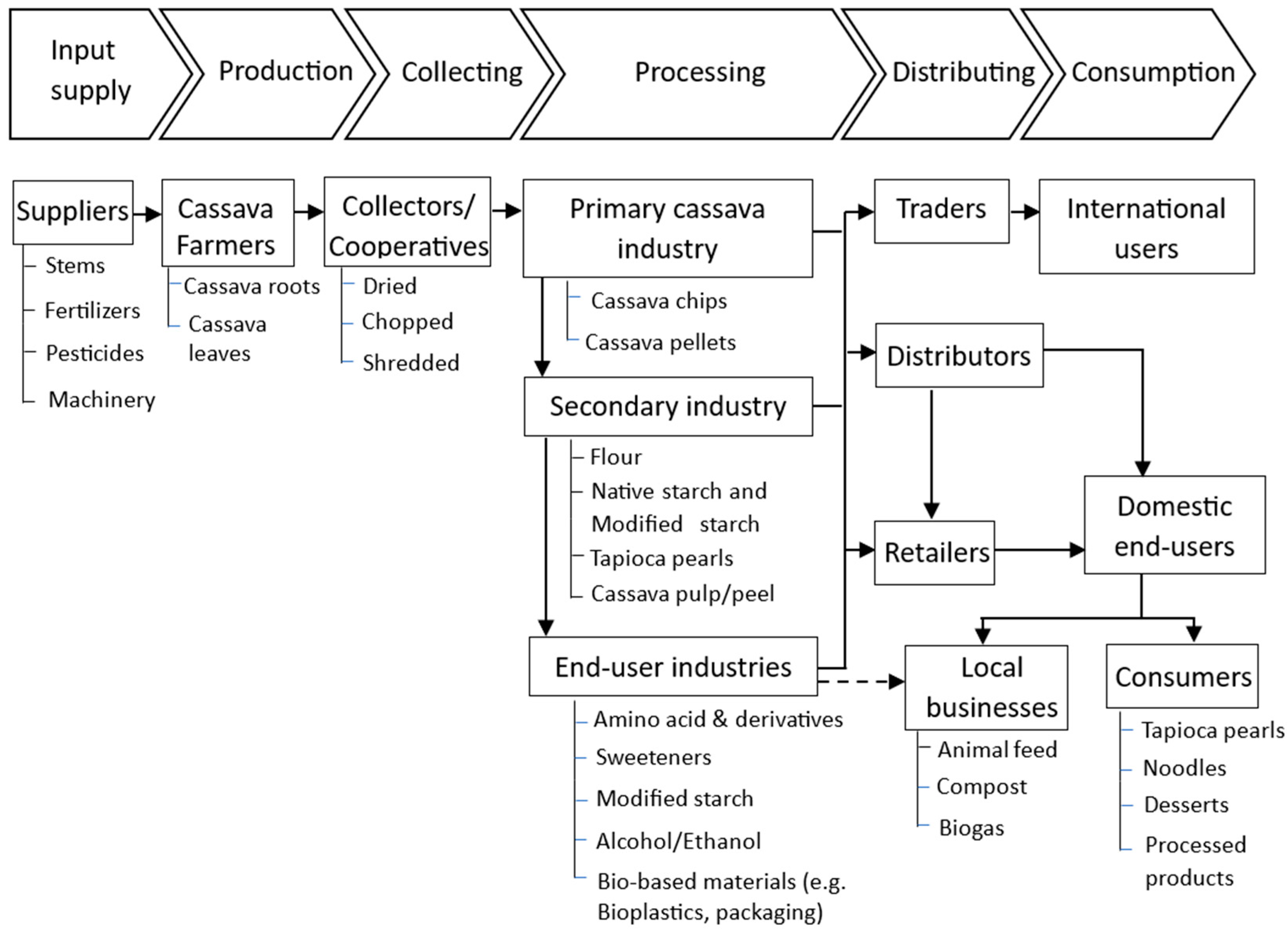

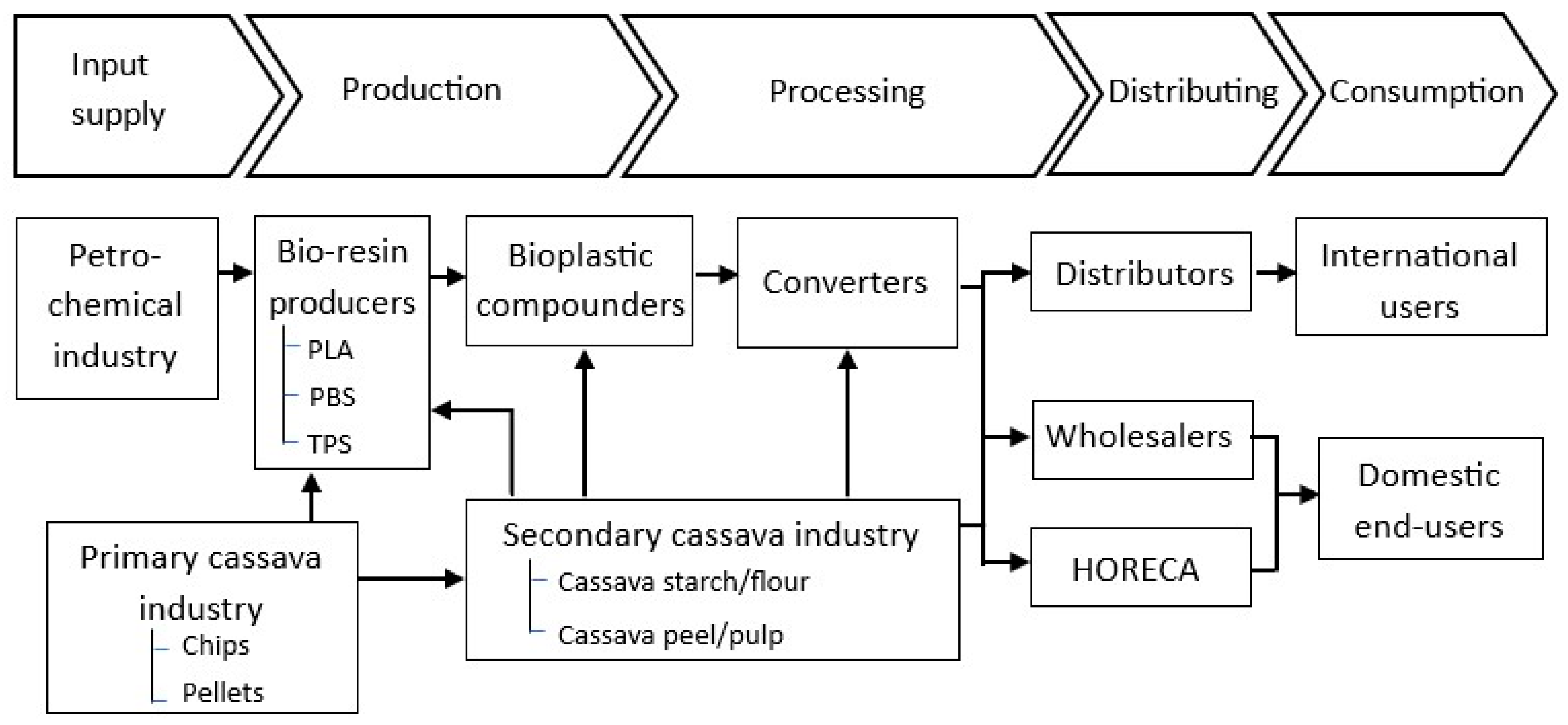

The cassava value chain refers to the sequence of activities and interactions among different actors involved in the value-added process, from production, processing, distribution, and the final market of cassava and its derived products [7,13,14,15]. The cassava value chain in Thailand starts from input supply to consumption and includes various stakeholders and products, as shown in Figure 1. The core actors include input suppliers, producers or farmers, processors, traders, distributors, and end-users [7,16]. Suppliers provide inputs such as cassava stem cuttings, fertilizers, pesticides, and machinery to cassava farmers. Cassava farmers cultivate and manage cassava crops, including land preparation, planting, crop maintenance, and harvesting. Farmers face some agricultural risks, e.g., extreme temperatures and rainfalls leading to pests, plant diseases, and damage in some cassava production areas [17]. These cause low crop yields, low flour content, and high production costs. Thus, some farmers turned to new varieties that contain greater starch content and gain higher prices [7,17]. Farmers harvest the roots and distribute them to collectors or primary processors, who carry out activities such as cleaning, sorting, and packaging. After harvesting, the cassava roots must be processed immediately to prevent spoilage and preserve quality. Cassava cultivation practices can vary based on local conditions and infrastructures, climate, and farming systems. Additionally, a proper knowledge of pest and disease management, as well as good agricultural practices, is crucial to ensure successful cassava production and minimize post-harvest losses [18,19].

Figure 1.

Cassava value chain in Thailand. Source: adapted from [2,16].

Cassava roots can be processed into various products, such as flour, starch, chips, foods, or bio-based materials, depending on the levels of industries and application uses [2,7]. Primary cassava processors transform the harvested cassava roots into intermediate products, such as cassava chips or grated cassava. Secondary processors convert intermediate cassava products into value-added products, such as cassava flour, cassava starch and derivatives, ethanol, and by-products, including cassava pulp and peels. End-user industries (e.g., food and non-food industries such as paper and textiles) process cassava starch into tapioca pearls, modified starch, sweeteners, amino acids, and alcohols. Cassava wastes are processed as biogas, compost, and animal feeds. Processed cassava products are packaged and prepared for distribution and are supplied for both local and export markets.

Addressing the segments of cassava products in Thailand, Table S1 shows that 32% of the total cassava root supply was processed into cassava chips and pellets, while 60.8% of the total supply was processed to cassava starch and derivatives [2,20]. A large portion of Thai cassava production (72.8%) is primarily supplied to export markets, while the remaining portion (27.2%) is allocated to the domestic market. In the domestic market, cassava is either consumed directly or utilized as a material for industries. The balance of production, domestic uses, and export indicate the opportunities in processing or value-added activities to utilize materials and waste from cassava in order to enhance the sustainability of the cassava value chain and generate higher value-added cassava products.

2.2. Bioplastic Industry

Conventional plastics, e.g., polyethylene (PE) and polypropylene (PP), are derived from petroleum resources or made from fossil fuels. These petroleum-based plastics are mostly non-biodegradable and always remain in the environment after use, causing harm to life and pollution and landscape problems. Although recycling is a suitable solution to reduce their environmental impact, less than 20% of these plastics are recycled nowadays [21] due to the performance deterioration of the recycled plastics and low process and cost efficiencies. Biodegradable plastics are alternatives to non-biodegradable petroleum-based plastics and are suitable for some applications, particularly short-life, disposable, and single-use items. Biodegradable plastics are defined as plastics whose degradation takes place through the action of natural microorganisms and fall under the umbrella of bioplastics. Some of these biodegradable plastics are derived from bio-based feedstocks such as polylactic acid (PLA), polybutylene succinate (PBS), polybutylene succinate-co-butylene adipate (PBSA), thermoplastic starch (TPS), and other starch blends, while the others are made from petroleum resources such as polybutylene adipate terephthalate (PBAT) [22]. Nevertheless, the properties and characteristics of the abovementioned biodegradable plastics differ depending on their chemical and packing structures. PLA, the most widely used bioplastic, has high strength and stiffness and slow crystallization, making it suitable for rigid products. In contrast, PBAT is more flexible and tougher than PLA; it is thus used to produce films and bags or is sometimes blended with PLA to impart toughness. The outstanding heat resistance of PBS, which is more flexible than PLA but stiffer than PBAT, makes it practical for paper-container-coating applications for hot foods and drinks. Thailand is the 11th largest global exporter of plastic resins and products and ASEAN’s second largest exporter of plastics. The gross domestic product (GDP) of the plastic industry in 2019 accounts for 6.1% of the total GDP, with a growth rate per year of 2–3% [23]. In 2019, plastic resins were domestically produced at about 9 million tons per year, and about 2 million tons were imported. About 44% of all plastic resins are used for domestic production, which is divided into packaging (36%), construction (16%), textile (14%), other (12%), consumer goods (10%), transportation (7%), and electronic parts (4%) [23].

Recently, there have been growing concerns about the environmental impacts of plastics, especially single-use plastic products, awaking many industries invested in the research and development of new or innovative products to respond to shifting market demands and global trends. An increasing number of biodegradable plastic manufacturers from renewable resources (e.g., PLA derived from sugarcane or cassava and PBS) are located in Thailand, and current plastic converters are expanding the production lines of bioplastics. The process of converting resins to plastic products involves melting, molding, cooling the molded plastic, and finally processing it to the finished goods. Moving toward the BCG economy, the concept of the BCG economy will support changes in not only circular but also bio-based and green production and consumption and promote new ways of value creation [24]. The Thai government has committed resources towards increased funding for research and development into bio-based products by partnering with a range of academic institutes, research centers, and the private sector. Thailand has positioned itself to become a global bioplastic hub because of an abundance of plant-based feedstocks, especially cassava and sugar cane. Thailand is the world’s largest cassava exporter (with 64 cassava starch factories). Bioplastics produced through the processing of cassava or sugar cane are cheaper than corn starch [25]. However, only 1% of all cassava and sugar cane production is currently used for bioplastic materials. A significant role in the research and development of bio-based products (e.g., bioplastics and biofuels) and government actions would provide a potential opportunity for plastic converters and related industries to build a high-value economy.

2.3. Reviews of Bioplastics from Cassava

Cassava, or tapioca, one of the Thai economic crops, consists mainly of starch, which can be used as a valuable feedstock to produce monomers via fermentation for various bioplastics such as PLA and PBS. However, many advanced technologies, including biotechnology, chemistry, and polymerization, are required to acquire those bioplastics with satisfactory performance, making them expensive. In some cases, cassava starch and flour [26,27,28,29] and cassava pulp [30,31] have been added as fillers into thermoplastic materials [26,27,28,31,32] to reduce costs and increase the bulk of these plastics. However, only a limited amount of cassava has been filled into plastics to avoid significant performance deterioration.

On the other hand, cassava starch and flour can be directly converted to TPS by plasticization using the existing technologies and machines, e.g., extruders [26,33,34,35,36,37,38,39,40,41,42,43,44,45,46,47,48,49,50] and internal mixers [51,52,53,54], which are commonly used for conventional plastics. TPS has been produced not only from native cassava starch but also from modified cassava starches [32,39,47,49,50,51,55,56]. Although modified starch imparts hydrophobicity, its high cost and capability to improve the performance and processability of TPS should be optimized and considered. The performance of TPS was also tuned by varying plasticizer types and contents [45] and other additives [40]. However, TPS has high moisture absorption, which causes poor mechanical and barrier properties. Therefore, blending TPS with other plastics, either non-biodegradable petroleum-based plastics [34,41,55,56] or biodegradable plastics such as PLA [35,38,39,42,43,44,46], PBAT [35,36,37,47,48,49,50], PBS [38], and PBSA [43], is an alternative to overcome the above limitations of TPS and meanwhile reduce the cost of the final blends. The biodegradability of biodegradable polyesters is retained or even better when they are blended with TPS.

To improve the compatibility between hydrophilic TPS and relatively more hydrophobic plastics and the performance of the TPS-based blends, various compatibilizers [41,43] were added. The effects of agricultural wastes, such as duckweed biomass [42], cassava pulp [46], oil palm mesocarp fiber waste [57], and rice husk [58], and naturals fibers, such as jute fibers [53], coir fibers [44], kapok fibers [53], cellulose fibers [54], and bagasse fibers [59], on the properties of TPS-based blends were recently investigated. Other additives, including inorganic compounds [34,36,49] and bioactive substances [48,50,51,55,56], were also incorporated into TPS-based blends to obtain functional properties such as antimicrobial and antioxidant activities.

Considering the converting processes of TPS and its blends, TPS itself could be blown into films [40,45] for further producing bags and wrap films; nonetheless, its blends provide the blown films with better processibility and performance [34,36,37,38,41,43,47,48,49,50]. In addition, TPS-based blends have been cast into sheets [35,39,55,56] for producing food trays. Some of them were improved in terms of their toughness and barrier properties, particularly against oxygen gas, via biaxial stretching [35,39]. Injection molding is one of the most popular techniques used to prepare specimens for rigid TPS-based composites [42,44,46] such as tableware, cutlery, and pots.

3. Materials and Methods

This study includes three parts: the value chain analysis of bioplastics from cassava, the consumer acceptance of bioplastic products, and the opportunities and challenges of bioplastic from cassava based on sustainability aspects. Both qualitative and quantitative approaches were conducted. For the first part, the bioplastic value chain related to the cassava sectors [7,13,14,15] and the value added to cassava along the value chain were analyzed [13,60]. A comparison of prices between bioplastic resins from cassava and conventional petroleum-based plastics (base price = 100) was performed as a case study. Relative price was calculated by dividing the price of bioplastics (USD/kg) by the price of conventional petroleum-based plastics (USD/kg) [13,61,62].

To estimate how the value of cassava products compares to the value of cassava roots, the value-added benefits of 1kg of cassava root were calculated. The cassava products were converted using conversion factors (Table S1) to compare to 1kg of cassava root. The comparison of the value-added to 1 kg of cassava roots is expressed by using the relative value without considering the production costs [13,61,62]. The relative value was calculated by dividing the price of cassava product (USD/1 kg of cassava root) by the price of cassava root (USD/kg).

The second part investigates the consumer acceptance of bioplastics from cassava. The analysis of consumer acceptance of bioplastics from cassava was focused on the application of single-use items. Herein, bioplastic cutlery products were therefore selected. Data on consumers were collected through face-to-face interviews from August to October 2020. The sample size was targeted at least 400 respondents [63], and sampling was conducted through a purposive sampling approach. The target group was the Thai population aged 18 or older who have experienced using plastic cutlery products or food services. Respondents were randomly interviewed at the selected restaurants. The data were screened to remove answers that were not feasible, leaving 915 respondents for the statistical analysis. The questionnaire included demographics, behavior of using tableware plastics (spoons, forks, knives) in food consumption, lifestyle, attitudes toward the environment [64], and acceptance of biodegradable plastics. The willingness to pay for bioplastics from cassava and the intention to buy them were also analyzed.

A two-step cluster analysis is one of the most reliable in terms of the number of clusters detected [65,66], so this technique was used to segment consumer acceptance for bioplastics from cassava. The criteria factors, including demographic factors (3 variables) and environmental factors (10 variables), that were used in the model are presented in Table 1. The algorithm groups the observed variables into clusters using the approach criterion [67]. The optimal number of clusters was selected by using the statistical test on the Bayesian Information Criterion (BIC) as the cluster criteria [65,66,68]. Smaller values of the BIC indicate better models, and the ratio of BIC changes must be large enough to determine the optimal cluster [67,69].

Table 1.

Criteria factors of segmentation.

Finally, the opportunities and barriers of bioplastics from cassava in Thailand were examined to drive a sustainable value chain for cassava and the potential opportunities for the bioplastics industry. Primary and secondary data were collected from in-depth interviews with several stakeholders in the bioplastic sectors and reviews of the relevant literature. Interviews with stakeholders are important to understand the real situation and gain insight into bioplastics and cassava industries. Interviews were conducted with 8 stakeholders, including bio-plastic compounders and converters (2 businesses), cassava industries (4 businesses), retailers and restaurants (5 businesses), and the government agency (1 agent). Analyses of the interview contents were used to describe challenges and opportunities for the development of bioplastics from cassava and the assessment of sustainability aspects, including economic, environmental, and social issues [60], where economic aspects were evaluated from the value chain analysis and the analysis of the consumer acceptance of bioplastics from cassava.

4. Results

4.1. Cassava-Based Bioplastic Value Chain Analysis

Various natural resources and crops play a significant role in the research and development of bio-based products (e.g., bioplastics and biofuels) and provide a potential opportunity to build a high-value economy. In this study, the development of cassava-based bioplastics is a great example of the high-value-based production of the Thai agriculture sector towards sustainable development, aiming to increase the product value, the income of the farmers, and opportunities for green businesses. Since the cost of imported bioplastics is high, various main crops containing sugar (e.g., sugar cane) and starch (e.g., corn, rice and cassava starch) have been researched and developed for bioplastic production. Due to the low product costs and oversupply of cassava production, cassava starch is a potential feedstock for bioplastic production [25]. The development of bioplastics based on thermoplastic cassava starch consists of an analysis of the cassava-based bioplastic value chain, a price comparison of different plastic resin types and production costs, and their value-added benefits to cassava roots.

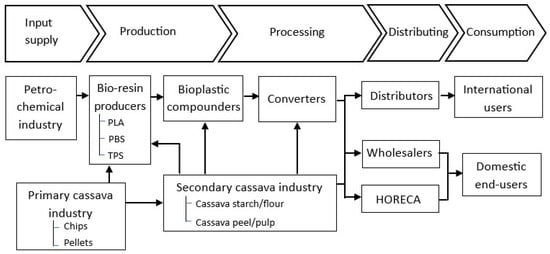

The stakeholders in the value chain of cassava-based bioplastic resins and products in Thailand are shown in Figure 2. The core actors in the value chain of bioplastic resins and products from cassava include input suppliers, bio-resin producers, bioplastic compounders, converters, distributors, and end-users. Cassava supply from primary and secondary industries has become important to bio-resin producers and bioplastic compounders, leading to the production cost of bioplastic resins, which drives impacts along the value chain. The produced bioplastics are utilized for various applications, such as packaging, tableware, medical devices, or agricultural items.

Figure 2.

Value chain of bioplastic resins and products. Source: Author’s collections.

- Bio-resin producers—the process of bio-resin production starts from starch from agricultural products (e.g., corn, cassava, rice, and sugar cane). Starch is then converted to sugar and processed via fermentation and polymerization to produce bioplastic resins (e.g., PBS and PLA). Two major bioplastic resin manufacturers in Thailand are PTT MCC Biochem Company Limited and Total-Corbion. PTT MCC possesses the first biobased PBS plant in the world with a total production of 20,000 T per year, while Total-Corbion, headquartered in the Netherlands, produces PLA with a total capacity of 75,000 T per year. Other companies import bio-resins (e.g., PBAT) for bioplastic compounding and converting. In addition, starch can be directly converted into bio-resins called “TPS” by plasticization with plasticizers under the application of heat and shear [40]. Ingredion (Thailand) Company Limited, Siam Modified Starch Company Limited (SMS), Thai wah Public Company Limited, and Mitrphol Biotech Company Limited are major TPS manufacturers and suppliers in Thailand. The SMS company offers modified tapioca starch for its use in various industries, including foods and non-foods (e.g., paper, health care, and textiles). SMS innovates cassava starch for “TAPIOPLAST” bioplastics, which are composed of 30–50% TPS blended with PBAT or PLA. The main businesses of Thai wah are divided into tapioca starch and starch-related products, food products, and biodegradable products. Thai wah offer “ROSECO”, which is a thermoplastic starch (TPS) resin made from tapioca, which can be applied to single-use plastics, bags, and agricultural goods. Mitrphol Biotech is a new player in bioplastic products made from cassava and sugar under “Planex” biodegradable plastic products and “Canex” compostable food packaging.

- Bioplastic compounders—the process of compounding starts from the blending of bio-resins with other substances, such as plastics, functional additives, and fillers (biomass or cassava starch), to create plastic compounds. For example, TPS resins are blended with other plastics (e.g., PLA, PBAT) in the presence of additives before being converting into bioplastic products.

- Converters—the process of bioplastic conversion involves the forming of bioplastic products, including post-processing, to obtain finished goods (e.g., films, sheets, bags, boxes, packaging, tableware, toys, and electronic parts). Plastic processors or convertors account for 71% of all plastic manufacturers in Thailand. Converting bioplastic products is successfully achieved using the same or slightly modified machines as conventional plastics. Although local plastic converters can adapt and process bioplastic products, some barriers, including the processing conditions, properties of bio-resin, and the efficiency of the machines, need to be studied further. Converting processes include blow molding, injection molding, extrusion, and thermoforming. Injection molding is the major converting process for bioplastics.

- Distributors—bioplastic products are packed for distribution and distributed to wholesalers and HORECA (hotels, retailers, and cafe-catering), which may involve marketing activities, services, and connections to end-users. Note that not all businesses are willing to shift from petroleum-based plastics to bioplastics from cassava. Most of the additional costs of bioplastics will be incurred by green businesses and might be passed onto customers.

- Users or Consumers—major users include green businesses and end consumers who are concerned about environmental impacts. Bioplastic products are often produced and suitable for short-term and single-use applications such as rigid or flexible packaging, bio waste bags, and agricultural-related products. However, bioplastic applications are developed for long-term use in several sectors such as electronic parts, construction, automotive, and transportation.

The largest exporter of cassava provides a strong advantage in cost reduction of bioplastic resin and products, value-added benefits, and raw material supply continuity. The number of cassava starch factories in Thailand has increased in recent years. Leading cassava starch factories have expanded their businesses to biodegradable resins and products, including Ingredion (Thailand) Company Limited, Siam Modified Starch Company Limited (SMS), Thai wah Public Company Limited, and, and Mitrphol Biotech Company Limited. These companies innovated the use of cassava starch compounded with PLA and PBAT to produce bioplastic products. Various bioplastic products (e.g., shopping bags, plant pots, cutlery, and single-use rigid plastic) are produced under blow film extrusion, injection molding, and thermoforming. With the strong upstream supply of raw materials and midstream manufacturers of cassava sectors, the bioplastics from cassava provide a potential opportunity for the bioplastic industry and cassava starch industries.

Biodegradable plastics are categorized based on their origins, including fossil-based biodegradable and bio-based biodegradable materials [70]. For fossil-based biodegradable plastics, PBAT and PBS are used to produce bioplastic bags and cups; however, these biodegradable polyesters must be imported and have high costs when compared to conventional plastics. They are often blended with other biodegradable resins (e.g., PLA) to improve their properties. Due to the high cost of fossil-based biodegradable plastics, bio-based ones have been developed, including PLA and starch blends. PLA is one of the most common biodegradable plastics and is suitable for food packaging applications (e.g., rigid and semi-rigid plastic products), for which there is increasing demand in various applications. Starch blends are complex mixtures of starch (e.g., corn and cassava) with biodegradable resins (e.g., PLA, PBAT, and PBS), aiming to reduce costs and improve the properties of the final products, such as water resistance compared with starch and flexibility and composability compared with polyesters.

In this study, the production cost of bioplastic PLA/TPS blend resin was assessed and compared with those of conventional plastic and commercial bioplastic resins. TPS from cassava starch was blended with PLA for bioplastic resin; this was modified from the previously reported formulae [42,44,45]. Table 2 presents the comparison of the prices of bioplastic resins to conventional petroleum-based plastics (base value = 100). The developed PLA/TPS blend resins are cheaper than PLA bioplastic resins and 54.5% more expensive than conventional plastic resins (PP and PE). The applications of bioplastic PLA/TPS blend resins are based on single-use items such as food trays, tableware such as spoons, forks, knives, carrier bags, and waste bags. Thus, the bioplastics from cassava provide a potential opportunity for the bioplastic industry and cassava sectors.

Table 2.

Price comparison of plastic resin type.

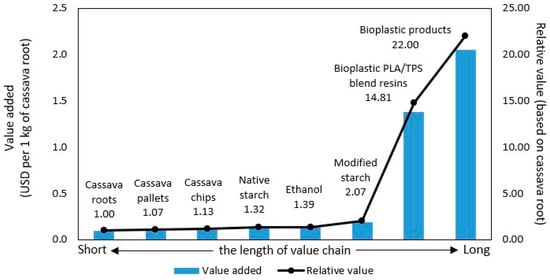

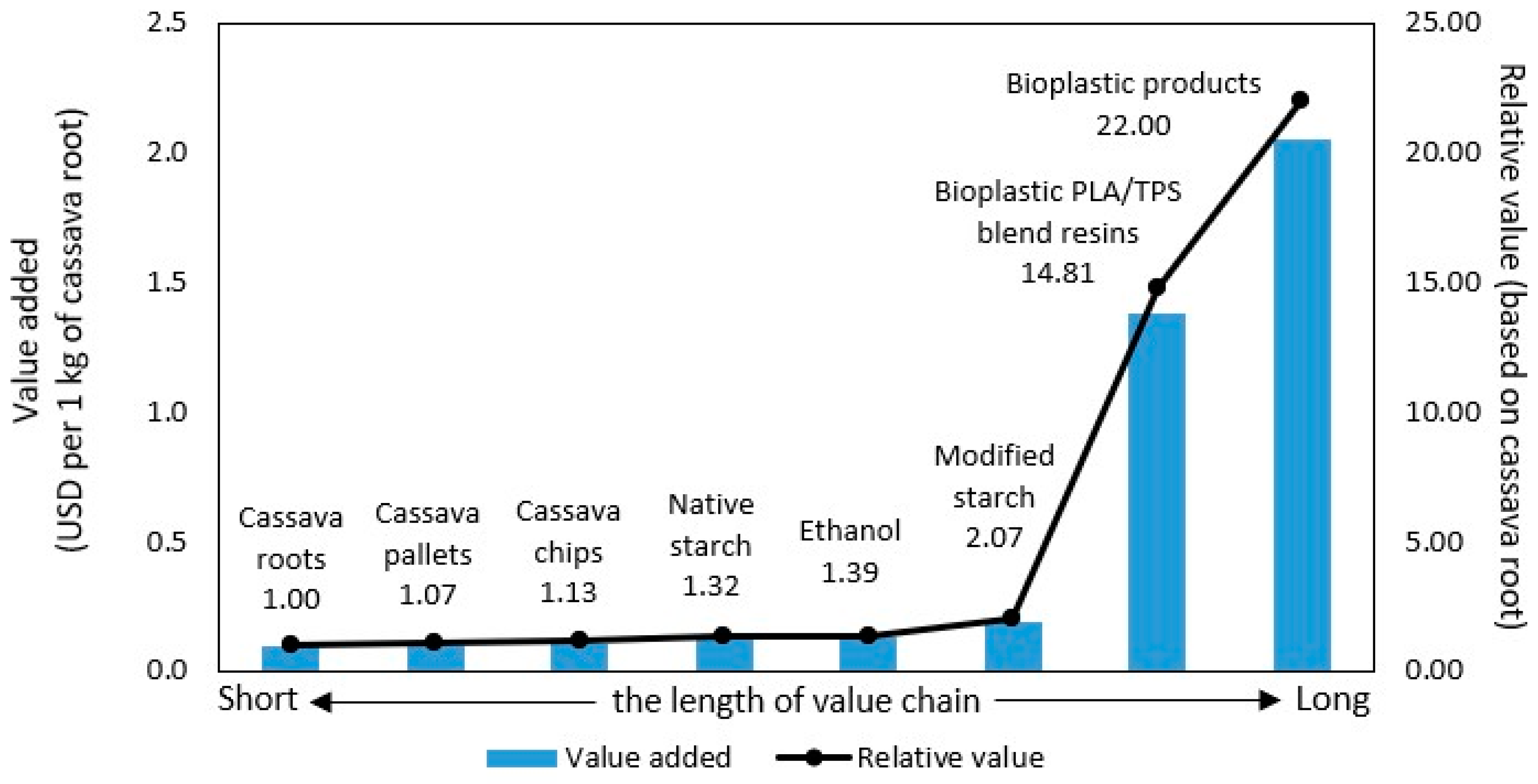

Considering the value-added benefits compared to 1 kg of cassava roots, the value chains from fresh cassava roots to valued-added products are presented in Figure 3. The bioplastic resins (TPS from cassava starch blended with PLA) generate 14.8 times the value-added benefits of cassava roots, and bioplastic products (e.g., single-use packaging including food trays and tableware) could generate 22 times the value-added benefits of cassava roots, as shown in Figure 3. For existing cassava products in Thailand, cassava starch creates 1.3–2 times the value-added benefits of cassava roots. The value-added benefits of the cassava value chain are associated with cassava value-adding activities and circular approaches such as processing into various high-value-based products and exploring the possibility of converting waste from processing into energy or bio-based materials.

Figure 3.

Value added to 1 kg of cassava root. Source: [71] and interviews with bioplastic stakeholders.

4.2. Consumer Acceptance of Bioplastics from Cassava

This section shows the findings on consumer acceptance of bioplastics from cassava, a statistical description of respondents’ characteristics, and the results of a cluster analysis. This provides a distribution of clusters that accept bioplastic products by analyzing the willingness to pay for bioplastic products from cassava. The bioplastic products in this study are bioplastic cutlery, including spoons, forks, and knives, which are developed from a PLA/TPS blend.

4.2.1. Descriptive Statistics of Sample

A survey of 915 respondents was carried out, as presented in Table 3. The majority of the respondents were female (56.8%) and aged between 21 and 37 years old (41.1%) and 38 and 53 years old (38.6%), respectively. Most consumers had a bachelor’s degree (52.3%) with a monthly income of more than 1113 USD (54.1%). When buying takeaway food, the largest proportion of the respondents use plastic cutlery (spoons, forks, and knives) and throw it into the bin (61.9%), followed by those who do not use plastic cutlery but keep it for next time (13.2%). Only 12.3% of total respondents prefer not to receive plastic cutlery.

Table 3.

Characteristics of surveyed individuals.

4.2.2. Segmentation among Green Consumers

The two-step cluster analysis divides the 915 respondents into five clusters, and each cluster has more than 100 respondents, as shown in Table 4. The cluster criteria (BIC = 6905.49 and the ratio of BIC changes = 0.213) demonstrate that the optimal number of clusters is five. The fifth cluster has the most respondents (258 respondents), while the first cluster has the fewest respondents (120 respondents). Five segments describe green consumer preference and the acceptance of bioplastic products. The characteristics of each constructed segment are described as follows.

Table 4.

Cluster analysis result.

Cluster 1 is called the brown segment (13.7%) and consists of a wide age range between 18 and 64 years old, with the lowest educational levels among other segments. The individuals in this segment have negative attitudes in relation to biodegradable products, with the lowest willingness to pay for green products. They have little concern about environmental concerns and do not support any business that preserves the environment.

Cluster 2 is called the young light green segment (21.8%) and mainly involves young people (aged between 18 and 37 years old) with positive attitudes toward the environment, although they do not take environmental actions (e.g., decrease the number of plastic uses). They slightly support biodegradable products and are willing to pay a little more for green products.

Cluster 3 is called the young green activism segment (19.2%) and mostly consists of young people (aged between 18 and 37 years old) with high educational levels (bachelor’s degree and higher). They consider that individual action does make prominent contributions to the environment. They are activists who support any business that carry out environmental activities. The individuals in this segment strongly believe that biodegradable products can reduce environmental problems and should be substituted for single-use plastic packaging. Compared to the other segments, this group is greener and adopt biodegradable products sooner.

Cluster 4 is called the skeptical green segment (21.8%) and contains aging adults (aged over 54 years old). They have a positive attitude towards environmental impacts and are curious about packaging before making purchase decisions. They are willing to pay extra for green products, although they are sensitive to economic factors. They express themselves to be skeptical about the beneficial information on green products.

Cluster 5 is called the green segment (29.4%) and mainly consists of middle-aged adults aged between 38 and 54 years old. This segment earns the highest average income and has the highest education levels among all the segments. This segment has a favorable position in all environmental aspects and slowly adopts biodegradable products. They tend to use biodegradable products when ordering a takeaway.

4.2.3. Consumer Acceptance of Bioplastic Products

To address consumer acceptance of bioplastic products from cassava, an analysis of the additional willingness to pay in monetary terms and the intention to buy the bioplastic products was applied and the participants were segmented into five clusters, as presented in Table 5. The respondents were asked whether they are willing to pay extra for bioplastic cutlery when ordering takeaway at a price of 3.62 USD. The findings showed that the majority of respondents (81.3%) are willing to pay an additional price for bioplastic products in a price range between 0.38 and 0.51 USD per set of bioplastic cutlery (spoons, forks, and knives), which accounts for 11–15.4% of the price of a takeaway order. Cluster 3, the young green activism group (19.2%), is willing to pay the highest extra for bioplastic cutlery products at 0.51 USD, while Cluster 4, the skeptical green group (15.9%), is willing to pay the lowest extra at 0.37 USD. The evidence in Cluster 2 and Cluster 4 indicated that they are really aware of the environment but are not willing to pay extra to support green products. Considering the intention to buy, Cluster 3, Cluster 4, and Cluster 5 are more likely to buy bioplastic products than greater than 40% of all respondents. The main reasons for not buying bioplastic cutlery products from cassava are physical properties that do not reach consumer preferences; for example, bioplastic cutlery has limited application to hot foods. Another reason is substituting products revealing that 26 respondents prefer other reusable materials (e.g., stainless cutlery) to any plastic cutleries. A common reason is price sensitivity, where Cluster 1 had the highest number of respondents unwilling to pay more among the other clusters. It is worth noting that 19 respondents doubt the biodegradation process of bioplastics from cassava and its impact on the environment. A few respondents are not familiar with bioplastics from cassava, thus they may take more time than others to adopt bioplastic products. Lastly, 10 respondents do not trust the safety of bioplastic products when applied to food products. The findings indicated that bioplastic products made from cassava have great potential in the Thai market, but gaps in research and development for various application uses need to be addressed.

Table 5.

Consumer acceptance of bioplastic products from cassava.

The proportion of consumer acceptance of bioplastic products from cassava accounts for 48.6% of all respondents, consisting of Cluster 3, the young green activism group (19.2%), and Cluster 5, the green group (29.4%), with a willingness to pay more than 0.44–0.51 USD or 13.2–15.4% of the price of a takeaway order. Unsurprisingly, the rest (51.4%) are considered as the late majority who are more skeptical about product adoption and tend to need additional activities (e.g., promotions and advertising by the businesses and green agents) to encourage them to use bioplastic products from cassava. It is worth noting that the brown segment (13.7%) from the late majority (51.4%) are less likely to accept bioplastic products and have little concern about environment issues.

4.3. Challenges and Opportunities in Moving toward the Bioplastic Industry

This section highlights challenges and opportunities for the development of bioplastics from cassava, as presented in Table 6. The descriptive summary data of opportunities and challenges obtained by interviewing value chain actors include bio-plastic compounders and converters, cassava industries, retailers and restaurants, the government agency, and reviews by the authors. Regarding the abovementioned evidence, sustainability aspects consisting of economic, environmental, and social issues with bioplastics from cassava in Thailand were explored.

Table 6.

Challenges and opportunities for the development of bioplastics from cassava.

To develop bioplastics from cassava, some significant drivers have created opportunities in the bioplastic market in Thailand. Global demands and cooperations focused on sustainability and green products drive the changes in Thai cassava production to high-value-based products (e.g., bioplastics, medical products, and devices). In Thailand, the BCG economy plans aim to drive the economy through innovation, creativity, and technology toward sustainable ways, which generate opportunities for high-value-based products like cassava and investment promotion policies (e.g., research and development, value-added creation, tax incentives). The Thai government promotes the development of the first five S-curve industries, including next-generation automotive, smart electronics, affluent medical and wellness tourism, agriculture and biotechnology, and food for the future. In addition, Thailand’s taxonomy framework was used to classify economic activities to push environmental sustainability and reduce carbon emissions. Due to the oversupply of cassava production in Thailand and low raw material costs, cassava starch is a suitable feedstock for bio-based products. With these advantages, cassava processors can expand their production lines to high-value-based products (e.g., TPS from cassava starch blended with PLA) and reuse their waste or by-products, leading to an increase in demand for cassava, which makes the cassava value chain more sustainable. In terms of infrastructure and the ecosystem, technological changes and innovations provide opportunities to SMEs and businesses related to cassava and its products. These changes include the integration of digital solutions, data analytics, and connectivity to improve efficiency, productivity, and customer experiences. For domestic demand, increasing consumer awareness of environmental impacts leads to them seeking green products that are good for the planet. The evidence from the findings in this study indicated that 48.6% of all respondents are likely to adopt bioplastic products from cassava; however, less than 50% of these groups are willing to pay for them.

Several challenges occur in the development of bioplastics from cassava in Thailand. The most important barrier is the production cost of bioplastic resins, followed by the unclear standard of bioplastics and the narrow application use of bioplastics from cassava. The production cost of bioplastics is higher than that of petroleum-based plastics. High input supplies continuously increase and are unsteady, for example, due to labor costs, energy costs, and logistic challenges. In addition, the lack of experts in bioplastic fields may hinder the bioplastic sector. The standards and labels for bio-based and biodegradable plastics in Thailand do not provide clear procedures and specifications on types of bioplastics and biodegradable processes. This gap gives opportunities to overclaim bioplastic products, leading to misunderstandings by consumers. Moreover, the functions and physical properties of bioplastics from TPS/PLA blends are limited when compared to commercial plastics such as low heat resistance, stickiness surface, and soft texture, which restrict the application use of bioplastics from cassava. On the upstream sector the bargaining power of bioplastic resin suppliers is high since a few bioplastic resin producers are located in Thailand and resin prices depend on the international market, leading to unstable prices of bioplastic resins (e.g., PLA, PBAT, and PBS) and shortages in their supply. Furthermore, climate events, natural disasters, and diseases from cassava (e.g., cassava mosaic virus) provide severe impacts on cassava production yields and the quality of cassava roots, including the starch contents. In terms of competition among businesses in the bioplastics industry, the development of bioplastics for compounders and converters does not require high investment and advanced technology, so competitive levels among existing plastic businesses are high. This also leads to low barriers to new players entering (e.g., cassava processors) the bioplastic industry. On the other hand, several options of substitute products (e.g., paper, stainless steel, and wood) provide similar functions and at cheaper costs. Businesses and consumers can purchase specially imported corn-based bioplastic products, which are mainly produced in China instead of bioplastic products from cassava. In addition, an inefficient waste management system and the linkage of supply chain actors do not support the post-consumption of bioplastics.

Considering the impact of each stage of the value chain based on three sustainability dimensions, economic, environmental, and social aspects, on bioplastics from cassava, the key aspects of a sustainable cassava value chain are described.

Economic impacts: cassava is not used for food consumption but is mainly produced as low-value-based products such as dried cassava for animal feeds and cassava starch for industries. Considering high-value products (e.g., bioplastics from TPS blends) and implementing cassava waste or by-products (e.g., cassava pulp/peel), cassava processors can increase the demand for cassava and improve its long-term economic viability. Bioplastics from cassava generate an economic value 14.8–22 times greater than cassava roots. In addition, the results of this study indicated that almost half of the respondents (48.6%) accept bioplastic products from cassava and are willing to pay more than 13.2–15.4% of the price of a takeaway order for them. Due to demand, a new market sector on bioplastics has emerged and driven the need for the use of cassava applications in the plastic and cassava industries, as well as green businesses and retailers. This shift not only enhances the profitability of the processors but also benefits farmers and related stakeholders. These lead to the improvement of a sustainable cassava value chain, which can enhance the productivity and competitiveness of the cassava and bioplastic sectors.

Social impacts: growth in the cassava and bioplastic sectors can improve the level of unemployment and drive workers to upskill on agricultural technology to enhance productivity and prevent climate change and cassava disease, as well as learn more about bioplastics and renewable sources from by-products. Sharing knowledge on sustainable practices (e.g., use less pesticides) from cassava processors and bioplastic industries with farmers and end-users is also important.

Environmental impacts: an increase in the use of single-use plastics and plastic items (e.g., food trays, containers, cutlery, straws, and plastic bags) has adversely affected plastic wastes and carbon emission. In addition, cassava farming and its industries can produce severe environmental impacts (e.g., soil degradation and wastes from cassava production) if they do not consider sustainable practices and maintain soil conditions. The development of bioplastics from cassava would provide alternatives to plastics from bio-based materials, which may reduce carbon emissions. Moreover, the waste management of bioplastics is different from petroleum-based plastics. Bioplastics from cassava are compostable depending on many parameters. The biodegradation of cassava edible bioplastic in plantation soil was higher than that in landfill soil [72].

5. Discussion

With notable agriculture-based GDP and rich biodiversity, Thailand has a competitive advantage for bio-based production. Various natural resources and economic crops play a significant role in the research and development of bio-based products (e.g., bioplastics and biofuels) and provide a potential opportunity to build a high-value economy. With the strong upstream cassava supply and midstream manufacturers (cassava and plastic industries), bioplastics from cassava emerge as a new sector that drives a sustainable cassava value chain. Relevant issues on the development of bioplastic industries along with the cassava value chain were discussed. The cassava value chain involves collaboration and coordination among stakeholders at each stage to ensure smooth and efficient operations, quality control, and market access. By optimizing the value chain, stakeholders aim to enhance productivity, increase profitability, and promote sustainability in the cassava value chain. However, the linkage between the stakeholders in the cassava value chain is vulnerable, leading to ineffective collaboration, high costs of cassava production, weak bargaining power, and a lack of knowledge sharing among cassava farmers and industries.

Due to a few bio-resin producers, the cost of bioplastics is still high compared with conventional plastics, so bioplastic products are slightly competitive with commercial plastic products. This study revealed that the price of bioplastic resins based on cassava, e.g., the PLA/TPS blend, is 36.4% higher than the price of conventional plastic resins.

With inadequate technology availabilities and limited research and development of bioplastics in Thailand, the functional properties of bioplastics are not satisfactory to particular applications (as shown in Table 5) and businesses, for example, heat resistance, texture, and appearance. In addition, the shift of cassava products to bio-based materials has raised significant costs for production, technology adjustment, and highly skilled labor. Therefore, more research and development on bioplastics, support from the government, and encouragement for public–private partnerships, are needed to serve the market and make the business financially viable.

To address the technology required for the development of bioplastics based on thermoplastic cassava starch/flour, extrusion becomes the most important technology for manufacturing these types of bioplastics because it possibly provides a continuous production process with a high throughput rate. Applying high shear and heat during the extrusion process can overcome the high viscosity of bioplastics based on thermoplastic cassava starch/flour, which is caused by their high molecular weight and highly branched molecular chains of starch polymers, particularly amylopectin, making them thermally processable like conventional plastics. Apart from their poor processibility, the high moisture/water absorption of cassava-based bioplastics also brings poor mechanical and barrier properties and surface stickiness to the final products. Though many ongoing research efforts have been made to reduce moisture/water absorption and improve the mechanical properties of thermoplastic cassava starch/flour-based bioplastics by blending them with other polymers, compounding them with various types of additives, and making composites with natural fibers and inorganic fillers, the development to reduce the surface stickiness of bioplastic products from cassava, which is one attribute concerning consumer acceptance, is lacking. A reduction in the product’s surface stickiness is necessary, especially for commercialization.

Regarding cassava starch’s uses in both food and several industries, there might be a trade-off between the application of cassava for foods and non-foods. The balance between the application and use of cassava must be considered by policymakers to provide national goals and direction for policy.

Since Thai consumers are unacquainted with bioplastics from cassava, adopting technology takes time to gain acceptance and growth opportunities in the market. The lack of knowledge on bio-based products and awareness of the environmental impacts in Thai society should be considered. Even though increasing green consumers have an awareness of environmental impacts, few consumers are willing to pay for the additional cost of bioplastic products. This study revealed that five clusters of consumers are concerned about the environment at different levels, and 51.4% of respondents do not support environmentally friendly activities and are skeptical about bioplastic products. Product label information and communication activities play prominent roles in influencing people’s intention to buy bioplastic products. On the other hand, the green clusters (48.6%) are more likely to accept bioplastic products from cassava and are willing to pay extra. It is worth mentioning that the actual usage of bioplastics from cassava may be lower than the estimated value when facing free tableware plastics. Hence, strengthening market linkage, promoting marketing activities (e.g., providing content or games on the benefits of using bioplastics from cassava), and educating the market on the benefits of bioplastics from cassava are required to boost the use of bioplastic products and market demand.

Addressing the sustainability of the cassava value chain requires a holistic approach that involves collaboration among various stakeholders along with government support policies (e.g., tax incentives and carbon emission campaigns). Due to the high cost of bioplastics, additional tax incentives should be provided to green businesses who use bioplastics from cassava. Encouraging cassava and plastic industry collaboration, knowledge sharing, and collective actions of cassava chain actors would strengthen the chain activities and promote competitiveness. Moreover, promoting value addition and diversification by developing cassava through a process with higher value or value-added activities would generate the ability to capture higher prices and increase profitability.

6. Conclusions

This paper evaluates the opportunities and challenges for developing bioplastics from cassava and assesses the sustainable cassava value chain in Thailand. Even though the nation’s directions on the BCG economy provide advantages in the development of cassava-based bioplastics, some challenges need to be considered, especially the production cost of bioplastic resins, the unclear standard of bioplastics, and the limited application and uses of bioplastics from cassava. The findings revealed the economic benefits of using cassava for bioplastic production, as cassava-based bioplastics created 14.8–22 times the value of cassava roots and had a positive impact on social and environmental aspects. In terms of demand, the results indicated that green consumer preference and the acceptance of bioplastic products were segmented into five groups. Almost half (48.6%) of the respondents, including the young green activism group (19.2%) and green group (29.4%), are willing to accept bioplastics from cassava and their actual willingness to pay extra might be affected by personal preferences and external factors (e.g., marketing activities, promotion offered by the businesses, and government campaigns). Different segments will accept bioplastics from cassava in different ways, considering different demographic variables (age, income, and education levels) and environmental factors. The main reasons for not using bioplastics from cassava are that the respondents are unsatisfied with their physical properties, they have a preference for other materials, and they do not accept the additional price of bioplastics compared with commercial plastics. To overcome challenges in developing bioplastics from cassava, the government should provide tax incentives to green businesses that shift to bioplastics from cassava and encourage investment in bioplastic resin industries in Thailand. A collaboration among stakeholders (e.g., cassava and plastic industries, HORECA businesses, retailers, and public sectors) is required to drive the usage of bioplastics from cassava. Funding by the government should focus on research and development to improve the properties of bioplastics from cassava (e.g., surface stickiness and heat resistance) and the technology required (e.g., extrusion), as well as provide training programs for bioplastic productions. In guiding the adoption of bioplastics, the government should reconsider the standard of bioplastic labeling to reflect the applications and uses of biodegradable processes and be relevant to public recognition, as well as promote public awareness of environmental impacts and the benefits of using bioplastics. The availability of bioplastic products from cassava in various channels and business sectors can accelerate consumer adoption and the development of the bioplastics. To encourage the continued growth of the bioplastic industry, building networks between producers and consumers and the linkage among the stakeholders are prominently required to drive the bioplastic industry and sustain the cassava value chain.

To continue developing the sustainable cassava value chain and drive the production of bioplastics from cassava, research on implementing circular economy approaches in the cassava value chain, including upcycling cassava materials and waste into valuable products and sustainable farming practices for cassava, should be considered for future research. To measure the sustainability impacts, a life cycle assessment (LCA) to evaluate the environmental and social impacts of cassava-based bioplastics compared to traditional petroleum-based plastics should be conducted. In addition, an analysis of the cost-effectiveness of scaling up cassava-based bioplastic production and future studies on the improvement of the properties and performance of cassava-based bioplastics would provide additional benefits to bioplastic production and the adoption of bioplastic products.

Supplementary Materials

The following supporting information can be downloaded at https://www.mdpi.com/article/10.3390/su152014713/s1, Table S1: The segments of cassava products used in Thailand (2021). References [2,20] have been mentioned in Supplementary Materials.

Author Contributions

Conceptualization, A.L. and R.Y.; methodology, A.L. and R.Y.; investigation, A.L. and R.Y.; data curation and analysis, A.L.; writing—original draft preparation, A.L.; writing—review and editing, A.L. and R.Y.; visualization, A.L.; finalizing the manuscript, A.L. and R.Y. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by the National Science and Technology Development Agency (NSTDA), Thailand [grant number P-17-50300].

Institutional Review Board Statement

The study was conducted according to the guidelines of the Declaration of Helsinki and approved by the Kasetsart University Research Ethics Committee (study code, KUREC-SS63/043; COE No. COE63/070) and date of approval: 18 March 2020).

Informed Consent Statement

Not applicable.

Data Availability Statement

The data presented in this study are available on request from the corresponding author. The data are not publicly available due to privacy and ethical restrictions.

Acknowledgments

The authors would like to thank stakeholders in the cassava and bioplastic sectors for valuable information and suggestions for interview data. We also thank the participants for completing the questionnaire.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Food and Agriculture Organization of the United Nations (FAO). FAOSTAT: Crops and Livestock Products. 2019. Available online: https://www.fao.org/faostat/en/#data/QCL (accessed on 15 April 2023).

- Sowcharoensuk, C. Industry Outlook 2023–2025: Cassava Industry; Krungsri Research. 2023. Available online: https://www.krungsri.com/en/research/industry/industry-outlook/agriculture/cassava/io/cassava-2023-2025 (accessed on 25 June 2023).

- Chancharoenchai, K.; Saraithong, W. Sustainable Development of Cassava Value Chain through the Promotion of Locally Sourced Chips. Sustainability 2022, 14, 14521. [Google Scholar] [CrossRef]

- Office of Agricultural Economics (OAE). Information on Agricultural Economic Commodities 2022; Ministry of Agriculture and Cooperatives: Bangkok, Thailand, 2023. Available online: https://www.oae.go.th/assets/portals/1/files/jounal/2566/commodity2565.pdf (accessed on 3 June 2023).

- Office of Agricultural Economics (OAE). Agricultural Statistics of Thailand 2022; Ministry of Agriculture and Cooperatives: Bangkok, Thailand, 2023. Available online: https://www.oae.go.th/assets/portals/1/files/jounal/2566/yearbook2565.pdf (accessed on 10 June 2023).

- Kaplinsky, R.; Terheggen, A.; Tijaja, J. China as a final market: The Gabon timber and Thai cassava value chains. World Dev. 2011, 39, 1177–1190. [Google Scholar] [CrossRef]

- Arthey, T.; Orawan Srisompun, O.; Zimmer, Y. Cassava Production and Processing in Thailand: A Value Chain Analysis Commissioned by FAO; Agri Benchmark. 2018. Available online: http://www.agribenchmark.org/fileadmin/Dateiablage/B-Cash-Crop/Reports/CassavaReportFinal-181030.pdf (accessed on 12 September 2023).

- Office of the National Economic and Social Development Council (NESDC). National Strategy (2018–2037); Office of the National Economic and Social Development Council, Office of the Prime Minister: Bangkok, Thailand, 2018. Available online: http://nscr.nesdc.go.th/wp-content/uploads/2019/10/National-Strategy-Eng-Final-25-OCT-2019.pdf (accessed on 29 April 2023).

- Barros, M.V.; Salvador, R.; do Prado, G.F.; de Francisco, A.C.; Piekarski, C.M. Circular economy as a driver to sustainable businesses. Clean. Environ. Syst. 2021, 2, 100006. [Google Scholar] [CrossRef]

- Lavelli, V. Circular food supply chains–Impact on value addition and safety. Trends Food Sci. Technol. 2021, 114, 323–332. [Google Scholar] [CrossRef]

- Bank of Thailand. Daily Foreign Exchange Rates; Bank of Thailand. 2023. Available online: https://www.bot.or.th/en/statistics/exchange-rate.html (accessed on 16 September 2023).

- Pannakkong, W.; Parthanadee, P.; Buddhakulsomsiri, J. Impacts of harvesting age and pricing schemes on economic sustainability of cassava farmers in Thailand under market uncertainty. Sustainability 2022, 14, 7768. [Google Scholar] [CrossRef]

- Porter, M.E. Competitive Advantage: Creating and Sustaining Superior Performance; Free Press: New York, NY, USA, 1985. [Google Scholar]

- Kaplinsky, R.; Morris, M. A Handbook for Value Chain Research; University of Sussex, Institute of Development Studies: Brighton, UK, 2000; Volume 113. [Google Scholar]

- Darko-Koomson, S.; Aidoo, R.; Abdoulaye, T. Analysis of cassava value chain in Ghana: Implications for upgrading smallholder supply systems. J. Agribus. Dev. Emerg. Econ. 2020, 10, 217–235. [Google Scholar] [CrossRef]

- Kaplinsky, R.; Tijaja, J.; Terheggen, A. What Happens When the Market Shifts to China? The Gabon Timber and Thai Cassava Value Chain; World Bank: Washington, DC, USA, 2010; pp. 303–334. [Google Scholar]

- ASEAN Food Security Information System. The Study of Cassava Supply Chain in Kanchanaburi Thailand; Office of Agricultural Economics, Ministry of Agriculture and Cooperatives: Bangkok, Thailand, 2019. Available online: https://aptfsis.org/uploads/normal/ISFAS%20Project%20in%20Thailand/The%20Study%20of%20Cassava%20Supply%20Chain%20in%20Kanchanaburi%20Thailand.pdf (accessed on 12 September 2023).

- Howeler, R.H. Agronomic practices for sustainable cassava production in Asia. In Cassava Research and Development in Asia, Proceedings of the Seventh Regional Workshop; Bangkok, Thailand, 28 October–1 November 2002, Centro Internacional de Agricultura Tropical (CIAT), Cassava Office for Asia: Bangkok, Thailand; pp. 288–314.

- Kansup, J.; Amawan, S.; Wongtiem, P.; Sawwa, A.; Ngorian, S.; Narkprasert, D.; Hansethasuk, J. Marker-assisted selection for resistance to cassava mosaic disease in Manihot esculenta Crantz. Thai Agric. Res. J. 2020, 38, 68–79. (In Thai) [Google Scholar]

- Office of Industrial Economics (OIE). Industry Statistics 2023; Office of Industrial Economics, Ministry of Industry: Bangkok, Thailand, 2023. Available online: https://www.oie.go.th/ (accessed on 29 April 2023).

- Pollution Control Department. Action Plan on Plastic Waste Management Phase II (2023–2027); Ministry of Natural Resources and Environment. 2023. Available online: https://www.pcd.go.th/publication/28484 (accessed on 25 April 2023).

- European Commission. Directorate-General for Environment. Relevance of Biodegradable and Compostable Consumer Plastic Products and Packaging in a Circular Economy; Office of the European Union: Luxembourg, 2020; Available online: https://op.europa.eu/en/publication-detail/-/publication/3fde3279-77af-11ea-a07e-01aa75ed71a1/language-en (accessed on 10 April 2023).

- Khanunthong, A. Industry Outlook 2021–2023: Plastics; Krungsri Research. 2021. Available online: https://www.krungsri.com/en/research/industry/industry-outlook/petrochemicals/plastics/io/io-plastics-21 (accessed on 2 May 2023).

- National Science and Technology Development Agency (NSTDA). BCG-Action-Plan-2564–2570; Ministry of Higher Education, Science, Research and Innovation, 2021. Available online: https://waa.inter.nstda.or.th/stks/pub/bcg/20211228-BCG-Action-Plan-2564-2570.pdf (accessed on 29 April 2023).

- Thailand Board of Investment (BOI). Thailand’s Bioplastics Industry; Office of the Prime Minister, 2017. Available online: https://www.boi.go.th/upload/content/BOI-brochure%202017-bioplastics-20171114_19753.pdf (accessed on 15 March 2023).

- Petnamsin, C.; Termvejsayanon, N.; Sriroth, K. Effect of Particle Size on Physical Properties and Biodegradability of Cassava Starch/Polymer Blend. Kasetsart J. (Nat. Sci.) 2000, 34, 254–261. [Google Scholar]

- Tanrattanakul, V.; Panwiriyarat, W. Compatibilization of low-density polyethylene/cassava starch blends by potassium persulfate and benzoyl peroxide. J. Appl. Polym. Sci. 2009, 114, 742–753. [Google Scholar] [CrossRef]

- Thitisomboon, W.; Opaprakasit, P.; Jaikaew, N.; Boonyarattanakalin, S. Characterizations of modified cassava starch with long chain fatty acid chlorides obtained from esterification under low reaction temperature and its PLA blending. J. Macromol. Sci. Part A 2018, 55, 253–259. [Google Scholar] [CrossRef]

- Srisuwan, Y.; Baimark, Y. Improvement in Thermal Stability of Flexible Poly(L-lactide)-b-poly(ethylene glycol)-b-poly(L-lactide) Bioplastic by Blending with Native Cassava Starch. Polymers 2022, 14, 3186. [Google Scholar] [CrossRef] [PubMed]

- Kangwanwatthanasiri, P.; Suppakarn, N.; Ruksakulpiwat, C.; Yupaporn, R. Biocomposites from Cassava Pulp/Polylactic Acid/Poly(butylene Succinate). Adv. Mater. Res. 2013, 747, 367–370. [Google Scholar] [CrossRef]

- Nithikarnjanatharn, J.; Samsalee, N. Effect of cassava pulp on Physical, Mechanical, and biodegradable properties of Poly(Butylene-Succinate)-Based biocomposites. Alex. Eng. J. 2022, 61, 10171–10181. [Google Scholar] [CrossRef]

- Suttiruengwong, S.; Sotho, K.; Seadan, M. Effect of Glycerol and Reactive Compatibilizers on Poly(butylene succinate)/Starch Blends. J. Renew. Mater. 2014, 2, 85–92. [Google Scholar] [CrossRef]

- Lopattananon, N.; Thongpin, C.; Sombatsompop, N. Bioplastics from Blends of Cassava and Rice Flours: The Effect of Blend Composition. Intern. Polym. Process. 2012, 27, 334–340. [Google Scholar] [CrossRef]

- Thipmanee, R.; Lukubira, S.; Ogale, A.A.; Sane, A. Enhancing distributive mixing of immiscible polyethylene/thermoplastic starch blend through zeolite ZSM-5 compounding sequence. Carbohydr. Polym. 2016, 136, 812–819. [Google Scholar] [CrossRef]

- Katanyoota, P.; Jariyasakoolroj, P.; Sane, A. Mechanical and barrier properties of simultaneous biaxially stretched polylactic acid/thermoplastic starch/poly(butylene adipate-co-terephthalate) films. Polym. Bull. 2022, 80, 5219–5237. [Google Scholar] [CrossRef]

- Yimnak, K.; Thipmanee, R.; Sane, A. Poly(butylene adipate-co-terephthalate)/thermoplastic starch/zeolite 5A films: Effects of compounding sequence and plasticizer content. Int. J. Biol. Macromol. 2020, 164, 1037–1045. [Google Scholar] [CrossRef]

- Garalde, R.A.; Thipmanee, R.; Jariyasakoolroj, P.; Sane, A. The effects of blend ratio and storage time on thermoplastic starch/poly(butylene adipate-co-terephthalate) films. Heliyon 2019, 5, e01251. [Google Scholar] [CrossRef]

- Jariyasakoolroj, P.; Chirachanchai, S. In Situ Chemical Modification of Thermoplastic Starch with Poly(L-lactide) and Poly(butylene succinate) for an Effectively Miscible Ternary Blend. Polymers 2022, 14, 825. [Google Scholar] [CrossRef] [PubMed]

- Jariyasakoolroj, P.; Tashiro, K.; Chinsirikul, W.; Kerddonfag, N.; Chirachanchai, S. Microstructural Analyses of Biaxially Oriented Polylactide/Modified Thermoplastic Starch Film with Drastic Improvement in Toughness. Macromol. Mater. Eng. 2019, 304, 1900340. [Google Scholar] [CrossRef]

- Dang, K.M.; Yoksan, R. Development of thermoplastic starch blown film by incorporating plasticized chitosan. Carbohydr. Polym. 2015, 115, 575–581. [Google Scholar] [CrossRef] [PubMed]

- Khanoonkon, N.; Yoksan, R.; Ogale, A.A. Effect of stearic acid-grafted starch compatibilizer on properties of linear low density polyethylene/thermoplastic starch blown film. Carbohydr. Polym. 2016, 137, 165–173. [Google Scholar] [CrossRef] [PubMed]

- Yoksan, R.; Boontanimitr, A.; Klompong, N.; Phothongsurakun, T. Poly(lactic acid)/thermoplastic cassava starch blends filled with duckweed biomass. Int. J. Biol. Macromol. 2022, 203, 369–378. [Google Scholar] [CrossRef] [PubMed]

- Yoksan, R.; Dang, K.M. The effect of polyethylene glycol sorbitan monostearate on the morphological characteristics and performance of thermoplastic starch/biodegradable polyester blend films. Int. J. Biol. Macromol. 2023, 231, 123332. [Google Scholar] [CrossRef] [PubMed]

- Chotiprayon, P.; Chaisawad, B.; Yoksan, R. Thermoplastic cassava starch/poly(lactic acid) blend reinforced with coir fibres. Int. J. Biol. Macromol. 2020, 156, 960–968. [Google Scholar] [CrossRef]

- Dang, K.M.; Yoksan, R. Thermoplastic starch blown films with improved mechanical and barrier properties. Int. J. Biol. Macromol. 2021, 188, 290–299. [Google Scholar] [CrossRef]

- Jullanun, P.; Yoksan, R. Morphological characteristics and properties of TPS/PLA/cassava pulp biocomposites. Polym. Test. 2020, 88, 106522. [Google Scholar] [CrossRef]

- Wongphan, P.; Panrong, T.; Harnkarnsujarit, N. Effect of different modified starches on physical, morphological, thermomechanical, barrier and biodegradation properties of cassava starch and polybutylene adipate terephthalate blend film. Food Packag. Shelf Life 2022, 32, 100844. [Google Scholar] [CrossRef]

- Wongphan, P.; Nerin, C.; Harnkarnsujarit, N. Enhanced compatibility and functionality of thermoplastic cassava starch blended PBAT blown films with erythorbate and nitrite. Food Chem. 2023, 420, 136107. [Google Scholar] [CrossRef]

- Phothisarattana, D.; Harnkarnsujarit, N. Migration, aggregations and thermal degradation behaviors of TiO2 and ZnO incorporated PBAT/TPS nanocomposite blown films. Food Packag. Shelf Life 2022, 33, 100901. [Google Scholar] [CrossRef]

- Katekhong, W.; Wongphan, P.; Klinmalai, P.; Harnkarnsujarit, N. Thermoplastic starch blown films functionalized by plasticized nitrite blended with PBAT for superior oxygen barrier and active biodegradable meat packaging. Food Chem. 2022, 374, 131709. [Google Scholar] [CrossRef] [PubMed]

- Phiriyawirut, M.; Duangsuwan, T.; Uenghuab, N.; Meena, C. Effect of Octenyl Succinate Starch on Properties of Tapioca Thermoplastic Starch Blends. Key Eng. Mater. 2017, 751, 290–295. [Google Scholar] [CrossRef]

- Pichaiyut, S.; Uttaro, C.; Ritthikan, K.; Nakason, C. Biodegradable thermoplastic natural rubber based on natural rubber and thermoplastic starch blends. J. Polym. Res. 2022, 30, 23. [Google Scholar] [CrossRef]

- Prachayawarakorn, J.; Chaiwatyothin, S.; Mueangta, S.; Hanchana, A. Effect of jute and kapok fibers on properties of thermoplastic cassava starch composites. Mater. Des. 2013, 47, 309–315. [Google Scholar] [CrossRef]

- Wattanakornsiri, A.; Pachana, K.; Kaewpirom, S.; Traina, M.; Migliaresi, C. Preparation and Properties of Green Composites Based on Tapioca Starch and Differently Recycled Paper Cellulose Fibers. J. Polym. Environ. 2012, 20, 801–809. [Google Scholar] [CrossRef]

- Promsorn, J.; Harnkarnsujarit, N. Oxygen absorbing food packaging made by extrusion compounding of thermoplastic cassava starch with gallic acid. Food Control 2022, 142, 109273. [Google Scholar] [CrossRef]

- Promsorn, J.; Harnkarnsujarit, N. Pyrogallol loaded thermoplastic cassava starch based films as bio-based oxygen scavengers. Ind. Crops Prod. 2022, 186, 115226. [Google Scholar] [CrossRef]

- Saepoo, T.; Sarak, S.; Mayakun, J.; Eksomtramage, T.; Kaewtatip, K. Thermoplastic starch composite with oil palm mesocarp fiber waste and its application as biodegradable seeding pot. Carbohydr. Polym. 2023, 299, 120221. [Google Scholar] [CrossRef] [PubMed]

- Boonsuk, P.; Sukolrat, A.; Bourkaew, S.; Kaewtatip, K.; Chantarak, S.; Kelarakis, A.; Chaibundit, C. Structure-properties relationships in alkaline treated rice husk reinforced thermoplastic cassava starch biocomposites. Int. J. Biol. Macromol. 2021, 167, 130–140. [Google Scholar] [CrossRef]

- Kaewtatip, K.; Thongmee, J. Preparation of thermoplastic starch/treated bagasse fiber composites. Starch Stärke 2014, 66, 724–728. [Google Scholar] [CrossRef]

- Fearne, A.; Martinez, M.G.; Dent, B. Dimensions of sustainable value chains: Implications for value chain analysis. Supply Chain Manag. Int. J. 2012, 17, 575–581. [Google Scholar] [CrossRef]

- Porter, M.E. What Is Strategy? Harvard Business Review, November–December 1996. Available online: https://hbr.org/1996/11/what-is-strategy (accessed on 30 June 2023).

- Samuelson, P.; Nordhaus, W. Economics, 19th ed.; McGraw Hill: New York, NY, USA, 2009. [Google Scholar]

- Cochran, W.G. Sampling Techniques, 3rd ed.; John Wiley & Sons: New York, NY, USA, 1977. [Google Scholar]

- Susanty, A.; Akshinta, P.Y.; Ulkhaq, M.M.; Puspitasari, N.B. Analysis of the tendency of transition between segments of green consumer behavior with a Markov chain approach. J. Model. Manag. 2022, 17, 1177–1212. [Google Scholar] [CrossRef]

- Chiu, T.; Fang, D.; Chen, J.; Wang, Y.; Jeris, C. A robust and scalable clustering algorithm for mixed type attributes in large database environment. In Proceedings of the Seventh ACM SIGKDD International Conference on Knowledge Discovery and Data Mining—KDD ’01, San Francisco, CA, USA, 26–29 August 2001; ACM Press: New York, NY, USA, 2001; pp. 263–268. [Google Scholar]

- Bacher, J.; Wenzig, K.; Vogler, M. SPSS Twostep Cluster—A First Evaluation; Universität Erlangen-Nürnberg: Erlangen, Germany, 2004; pp. 1–20. [Google Scholar]

- IBM. TwoStep Cluster Analysis. IBM SPSS Statistics Information Center: IBM Corporation. 2021. Available online: https://www.ibm.com/docs/en/spss-statistics/25.0.0?topic=features-twostep-cluster-analysis (accessed on 30 June 2023).

- Norusis, M. SPSS 15.0 Advanced Statistical Procedures Companion; Prentice Hall Press: Hoboken, NJ, USA, 2007. [Google Scholar]

- Harantová, V.; Mazanec, J.; Štefancová, V.; Mašek, J.; Foltýnová, H.B. Two-step cluster analysis of passenger mobility segmentation during the COVID-19 pandemic. Mathematics 2023, 11, 583. [Google Scholar] [CrossRef]

- European Commission. Directorate-General for Environment. Biobased Plastic—Sustainable Sourcing and Content: Final Report; Office of the European Union. 2022. Available online: https://data.europa.eu/doi/10.2779/668096 (accessed on 20 April 2023).

- Thai Tapioca Trade Association (TTTA). Prices 2023. Available online: https://ttta-tapioca.org (accessed on 3 June 2023).

- Isroi, I.; Supeni, G.; Eris, D.D.; Cahyaningtyas, A.A. Biodegradability of Cassava Edible Bioplastics in Landfill Soil and Plantation Soil. J. Kim. Dan Kemasan 2018, 40, 129–140. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).