4.1. Cassava-Based Bioplastic Value Chain Analysis

Various natural resources and crops play a significant role in the research and development of bio-based products (e.g., bioplastics and biofuels) and provide a potential opportunity to build a high-value economy. In this study, the development of cassava-based bioplastics is a great example of the high-value-based production of the Thai agriculture sector towards sustainable development, aiming to increase the product value, the income of the farmers, and opportunities for green businesses. Since the cost of imported bioplastics is high, various main crops containing sugar (e.g., sugar cane) and starch (e.g., corn, rice and cassava starch) have been researched and developed for bioplastic production. Due to the low product costs and oversupply of cassava production, cassava starch is a potential feedstock for bioplastic production [

25]. The development of bioplastics based on thermoplastic cassava starch consists of an analysis of the cassava-based bioplastic value chain, a price comparison of different plastic resin types and production costs, and their value-added benefits to cassava roots.

The stakeholders in the value chain of cassava-based bioplastic resins and products in Thailand are shown in

Figure 2. The core actors in the value chain of bioplastic resins and products from cassava include input suppliers, bio-resin producers, bioplastic compounders, converters, distributors, and end-users. Cassava supply from primary and secondary industries has become important to bio-resin producers and bioplastic compounders, leading to the production cost of bioplastic resins, which drives impacts along the value chain. The produced bioplastics are utilized for various applications, such as packaging, tableware, medical devices, or agricultural items.

Bio-resin producers—the process of bio-resin production starts from starch from agricultural products (e.g., corn, cassava, rice, and sugar cane). Starch is then converted to sugar and processed via fermentation and polymerization to produce bioplastic resins (e.g., PBS and PLA). Two major bioplastic resin manufacturers in Thailand are PTT MCC Biochem Company Limited and Total-Corbion. PTT MCC possesses the first biobased PBS plant in the world with a total production of 20,000 T per year, while Total-Corbion, headquartered in the Netherlands, produces PLA with a total capacity of 75,000 T per year. Other companies import bio-resins (e.g., PBAT) for bioplastic compounding and converting. In addition, starch can be directly converted into bio-resins called “TPS” by plasticization with plasticizers under the application of heat and shear [

40]. Ingredion (Thailand) Company Limited, Siam Modified Starch Company Limited (SMS), Thai wah Public Company Limited, and Mitrphol Biotech Company Limited are major TPS manufacturers and suppliers in Thailand. The SMS company offers modified tapioca starch for its use in various industries, including foods and non-foods (e.g., paper, health care, and textiles). SMS innovates cassava starch for “TAPIOPLAST” bioplastics, which are composed of 30–50% TPS blended with PBAT or PLA. The main businesses of Thai wah are divided into tapioca starch and starch-related products, food products, and biodegradable products. Thai wah offer “ROSECO”, which is a thermoplastic starch (TPS) resin made from tapioca, which can be applied to single-use plastics, bags, and agricultural goods. Mitrphol Biotech is a new player in bioplastic products made from cassava and sugar under “Planex” biodegradable plastic products and “Canex” compostable food packaging.

Bioplastic compounders—the process of compounding starts from the blending of bio-resins with other substances, such as plastics, functional additives, and fillers (biomass or cassava starch), to create plastic compounds. For example, TPS resins are blended with other plastics (e.g., PLA, PBAT) in the presence of additives before being converting into bioplastic products.

Converters—the process of bioplastic conversion involves the forming of bioplastic products, including post-processing, to obtain finished goods (e.g., films, sheets, bags, boxes, packaging, tableware, toys, and electronic parts). Plastic processors or convertors account for 71% of all plastic manufacturers in Thailand. Converting bioplastic products is successfully achieved using the same or slightly modified machines as conventional plastics. Although local plastic converters can adapt and process bioplastic products, some barriers, including the processing conditions, properties of bio-resin, and the efficiency of the machines, need to be studied further. Converting processes include blow molding, injection molding, extrusion, and thermoforming. Injection molding is the major converting process for bioplastics.

Distributors—bioplastic products are packed for distribution and distributed to wholesalers and HORECA (hotels, retailers, and cafe-catering), which may involve marketing activities, services, and connections to end-users. Note that not all businesses are willing to shift from petroleum-based plastics to bioplastics from cassava. Most of the additional costs of bioplastics will be incurred by green businesses and might be passed onto customers.

Users or Consumers—major users include green businesses and end consumers who are concerned about environmental impacts. Bioplastic products are often produced and suitable for short-term and single-use applications such as rigid or flexible packaging, bio waste bags, and agricultural-related products. However, bioplastic applications are developed for long-term use in several sectors such as electronic parts, construction, automotive, and transportation.

The largest exporter of cassava provides a strong advantage in cost reduction of bioplastic resin and products, value-added benefits, and raw material supply continuity. The number of cassava starch factories in Thailand has increased in recent years. Leading cassava starch factories have expanded their businesses to biodegradable resins and products, including Ingredion (Thailand) Company Limited, Siam Modified Starch Company Limited (SMS), Thai wah Public Company Limited, and, and Mitrphol Biotech Company Limited. These companies innovated the use of cassava starch compounded with PLA and PBAT to produce bioplastic products. Various bioplastic products (e.g., shopping bags, plant pots, cutlery, and single-use rigid plastic) are produced under blow film extrusion, injection molding, and thermoforming. With the strong upstream supply of raw materials and midstream manufacturers of cassava sectors, the bioplastics from cassava provide a potential opportunity for the bioplastic industry and cassava starch industries.

Biodegradable plastics are categorized based on their origins, including fossil-based biodegradable and bio-based biodegradable materials [

70]. For fossil-based biodegradable plastics, PBAT and PBS are used to produce bioplastic bags and cups; however, these biodegradable polyesters must be imported and have high costs when compared to conventional plastics. They are often blended with other biodegradable resins (e.g., PLA) to improve their properties. Due to the high cost of fossil-based biodegradable plastics, bio-based ones have been developed, including PLA and starch blends. PLA is one of the most common biodegradable plastics and is suitable for food packaging applications (e.g., rigid and semi-rigid plastic products), for which there is increasing demand in various applications. Starch blends are complex mixtures of starch (e.g., corn and cassava) with biodegradable resins (e.g., PLA, PBAT, and PBS), aiming to reduce costs and improve the properties of the final products, such as water resistance compared with starch and flexibility and composability compared with polyesters.

In this study, the production cost of bioplastic PLA/TPS blend resin was assessed and compared with those of conventional plastic and commercial bioplastic resins. TPS from cassava starch was blended with PLA for bioplastic resin; this was modified from the previously reported formulae [

42,

44,

45].

Table 2 presents the comparison of the prices of bioplastic resins to conventional petroleum-based plastics (base value = 100). The developed PLA/TPS blend resins are cheaper than PLA bioplastic resins and 54.5% more expensive than conventional plastic resins (PP and PE). The applications of bioplastic PLA/TPS blend resins are based on single-use items such as food trays, tableware such as spoons, forks, knives, carrier bags, and waste bags. Thus, the bioplastics from cassava provide a potential opportunity for the bioplastic industry and cassava sectors.

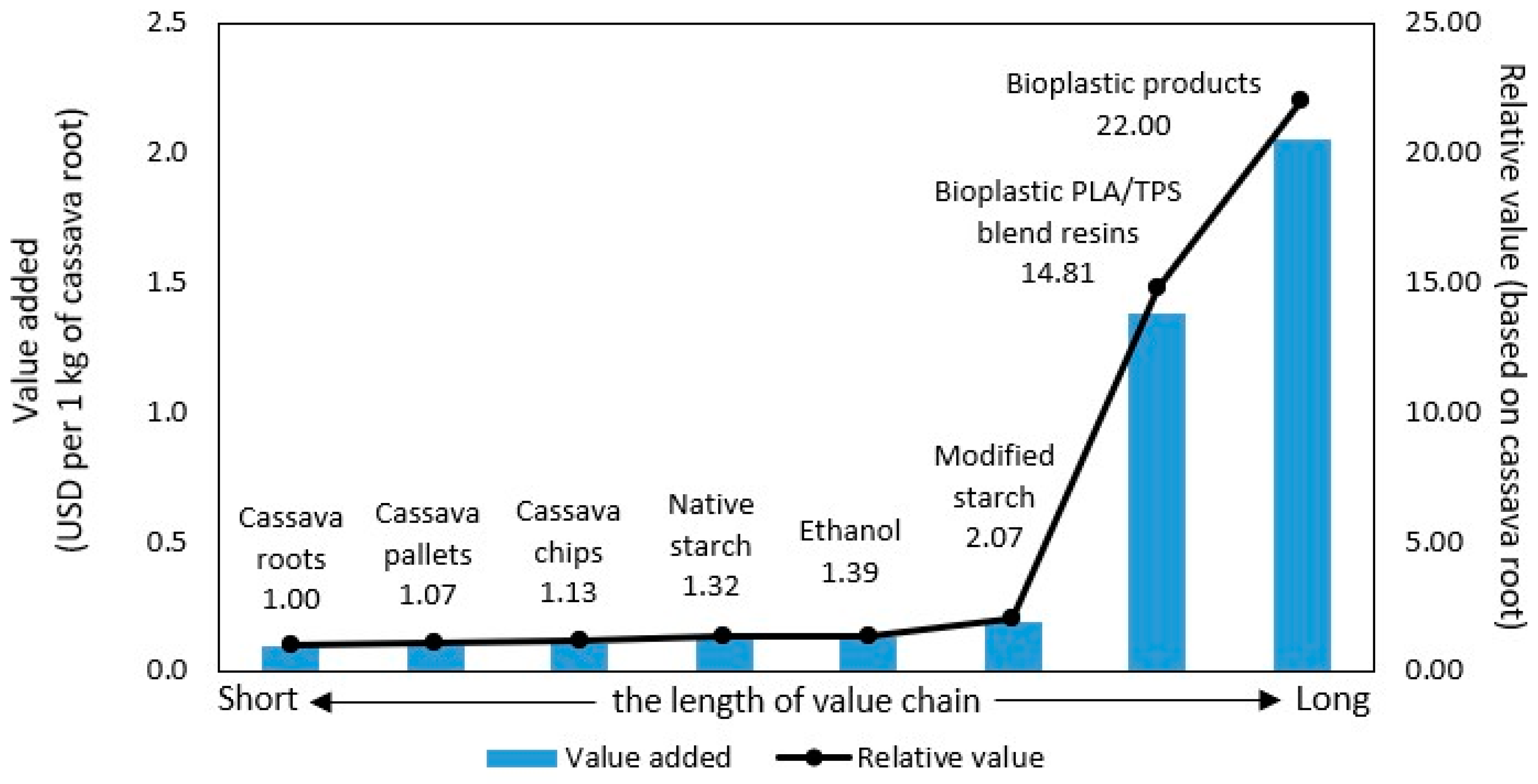

Considering the value-added benefits compared to 1 kg of cassava roots, the value chains from fresh cassava roots to valued-added products are presented in

Figure 3. The bioplastic resins (TPS from cassava starch blended with PLA) generate 14.8 times the value-added benefits of cassava roots, and bioplastic products (e.g., single-use packaging including food trays and tableware) could generate 22 times the value-added benefits of cassava roots, as shown in

Figure 3. For existing cassava products in Thailand, cassava starch creates 1.3–2 times the value-added benefits of cassava roots. The value-added benefits of the cassava value chain are associated with cassava value-adding activities and circular approaches such as processing into various high-value-based products and exploring the possibility of converting waste from processing into energy or bio-based materials.

4.2. Consumer Acceptance of Bioplastics from Cassava

This section shows the findings on consumer acceptance of bioplastics from cassava, a statistical description of respondents’ characteristics, and the results of a cluster analysis. This provides a distribution of clusters that accept bioplastic products by analyzing the willingness to pay for bioplastic products from cassava. The bioplastic products in this study are bioplastic cutlery, including spoons, forks, and knives, which are developed from a PLA/TPS blend.

4.2.1. Descriptive Statistics of Sample

A survey of 915 respondents was carried out, as presented in

Table 3. The majority of the respondents were female (56.8%) and aged between 21 and 37 years old (41.1%) and 38 and 53 years old (38.6%), respectively. Most consumers had a bachelor’s degree (52.3%) with a monthly income of more than 1113 USD (54.1%). When buying takeaway food, the largest proportion of the respondents use plastic cutlery (spoons, forks, and knives) and throw it into the bin (61.9%), followed by those who do not use plastic cutlery but keep it for next time (13.2%). Only 12.3% of total respondents prefer not to receive plastic cutlery.

4.2.2. Segmentation among Green Consumers

The two-step cluster analysis divides the 915 respondents into five clusters, and each cluster has more than 100 respondents, as shown in

Table 4. The cluster criteria (BIC = 6905.49 and the ratio of BIC changes = 0.213) demonstrate that the optimal number of clusters is five. The fifth cluster has the most respondents (258 respondents), while the first cluster has the fewest respondents (120 respondents). Five segments describe green consumer preference and the acceptance of bioplastic products. The characteristics of each constructed segment are described as follows.

Cluster 1 is called the brown segment (13.7%) and consists of a wide age range between 18 and 64 years old, with the lowest educational levels among other segments. The individuals in this segment have negative attitudes in relation to biodegradable products, with the lowest willingness to pay for green products. They have little concern about environmental concerns and do not support any business that preserves the environment.

Cluster 2 is called the young light green segment (21.8%) and mainly involves young people (aged between 18 and 37 years old) with positive attitudes toward the environment, although they do not take environmental actions (e.g., decrease the number of plastic uses). They slightly support biodegradable products and are willing to pay a little more for green products.

Cluster 3 is called the young green activism segment (19.2%) and mostly consists of young people (aged between 18 and 37 years old) with high educational levels (bachelor’s degree and higher). They consider that individual action does make prominent contributions to the environment. They are activists who support any business that carry out environmental activities. The individuals in this segment strongly believe that biodegradable products can reduce environmental problems and should be substituted for single-use plastic packaging. Compared to the other segments, this group is greener and adopt biodegradable products sooner.

Cluster 4 is called the skeptical green segment (21.8%) and contains aging adults (aged over 54 years old). They have a positive attitude towards environmental impacts and are curious about packaging before making purchase decisions. They are willing to pay extra for green products, although they are sensitive to economic factors. They express themselves to be skeptical about the beneficial information on green products.

Cluster 5 is called the green segment (29.4%) and mainly consists of middle-aged adults aged between 38 and 54 years old. This segment earns the highest average income and has the highest education levels among all the segments. This segment has a favorable position in all environmental aspects and slowly adopts biodegradable products. They tend to use biodegradable products when ordering a takeaway.

4.2.3. Consumer Acceptance of Bioplastic Products

To address consumer acceptance of bioplastic products from cassava, an analysis of the additional willingness to pay in monetary terms and the intention to buy the bioplastic products was applied and the participants were segmented into five clusters, as presented in

Table 5. The respondents were asked whether they are willing to pay extra for bioplastic cutlery when ordering takeaway at a price of 3.62 USD. The findings showed that the majority of respondents (81.3%) are willing to pay an additional price for bioplastic products in a price range between 0.38 and 0.51 USD per set of bioplastic cutlery (spoons, forks, and knives), which accounts for 11–15.4% of the price of a takeaway order. Cluster 3, the young green activism group (19.2%), is willing to pay the highest extra for bioplastic cutlery products at 0.51 USD, while Cluster 4, the skeptical green group (15.9%), is willing to pay the lowest extra at 0.37 USD. The evidence in Cluster 2 and Cluster 4 indicated that they are really aware of the environment but are not willing to pay extra to support green products. Considering the intention to buy, Cluster 3, Cluster 4, and Cluster 5 are more likely to buy bioplastic products than greater than 40% of all respondents. The main reasons for not buying bioplastic cutlery products from cassava are physical properties that do not reach consumer preferences; for example, bioplastic cutlery has limited application to hot foods. Another reason is substituting products revealing that 26 respondents prefer other reusable materials (e.g., stainless cutlery) to any plastic cutleries. A common reason is price sensitivity, where Cluster 1 had the highest number of respondents unwilling to pay more among the other clusters. It is worth noting that 19 respondents doubt the biodegradation process of bioplastics from cassava and its impact on the environment. A few respondents are not familiar with bioplastics from cassava, thus they may take more time than others to adopt bioplastic products. Lastly, 10 respondents do not trust the safety of bioplastic products when applied to food products. The findings indicated that bioplastic products made from cassava have great potential in the Thai market, but gaps in research and development for various application uses need to be addressed.

The proportion of consumer acceptance of bioplastic products from cassava accounts for 48.6% of all respondents, consisting of Cluster 3, the young green activism group (19.2%), and Cluster 5, the green group (29.4%), with a willingness to pay more than 0.44–0.51 USD or 13.2–15.4% of the price of a takeaway order. Unsurprisingly, the rest (51.4%) are considered as the late majority who are more skeptical about product adoption and tend to need additional activities (e.g., promotions and advertising by the businesses and green agents) to encourage them to use bioplastic products from cassava. It is worth noting that the brown segment (13.7%) from the late majority (51.4%) are less likely to accept bioplastic products and have little concern about environment issues.

4.3. Challenges and Opportunities in Moving toward the Bioplastic Industry

This section highlights challenges and opportunities for the development of bioplastics from cassava, as presented in

Table 6. The descriptive summary data of opportunities and challenges obtained by interviewing value chain actors include bio-plastic compounders and converters, cassava industries, retailers and restaurants, the government agency, and reviews by the authors. Regarding the abovementioned evidence, sustainability aspects consisting of economic, environmental, and social issues with bioplastics from cassava in Thailand were explored.

To develop bioplastics from cassava, some significant drivers have created opportunities in the bioplastic market in Thailand. Global demands and cooperations focused on sustainability and green products drive the changes in Thai cassava production to high-value-based products (e.g., bioplastics, medical products, and devices). In Thailand, the BCG economy plans aim to drive the economy through innovation, creativity, and technology toward sustainable ways, which generate opportunities for high-value-based products like cassava and investment promotion policies (e.g., research and development, value-added creation, tax incentives). The Thai government promotes the development of the first five S-curve industries, including next-generation automotive, smart electronics, affluent medical and wellness tourism, agriculture and biotechnology, and food for the future. In addition, Thailand’s taxonomy framework was used to classify economic activities to push environmental sustainability and reduce carbon emissions. Due to the oversupply of cassava production in Thailand and low raw material costs, cassava starch is a suitable feedstock for bio-based products. With these advantages, cassava processors can expand their production lines to high-value-based products (e.g., TPS from cassava starch blended with PLA) and reuse their waste or by-products, leading to an increase in demand for cassava, which makes the cassava value chain more sustainable. In terms of infrastructure and the ecosystem, technological changes and innovations provide opportunities to SMEs and businesses related to cassava and its products. These changes include the integration of digital solutions, data analytics, and connectivity to improve efficiency, productivity, and customer experiences. For domestic demand, increasing consumer awareness of environmental impacts leads to them seeking green products that are good for the planet. The evidence from the findings in this study indicated that 48.6% of all respondents are likely to adopt bioplastic products from cassava; however, less than 50% of these groups are willing to pay for them.

Several challenges occur in the development of bioplastics from cassava in Thailand. The most important barrier is the production cost of bioplastic resins, followed by the unclear standard of bioplastics and the narrow application use of bioplastics from cassava. The production cost of bioplastics is higher than that of petroleum-based plastics. High input supplies continuously increase and are unsteady, for example, due to labor costs, energy costs, and logistic challenges. In addition, the lack of experts in bioplastic fields may hinder the bioplastic sector. The standards and labels for bio-based and biodegradable plastics in Thailand do not provide clear procedures and specifications on types of bioplastics and biodegradable processes. This gap gives opportunities to overclaim bioplastic products, leading to misunderstandings by consumers. Moreover, the functions and physical properties of bioplastics from TPS/PLA blends are limited when compared to commercial plastics such as low heat resistance, stickiness surface, and soft texture, which restrict the application use of bioplastics from cassava. On the upstream sector the bargaining power of bioplastic resin suppliers is high since a few bioplastic resin producers are located in Thailand and resin prices depend on the international market, leading to unstable prices of bioplastic resins (e.g., PLA, PBAT, and PBS) and shortages in their supply. Furthermore, climate events, natural disasters, and diseases from cassava (e.g., cassava mosaic virus) provide severe impacts on cassava production yields and the quality of cassava roots, including the starch contents. In terms of competition among businesses in the bioplastics industry, the development of bioplastics for compounders and converters does not require high investment and advanced technology, so competitive levels among existing plastic businesses are high. This also leads to low barriers to new players entering (e.g., cassava processors) the bioplastic industry. On the other hand, several options of substitute products (e.g., paper, stainless steel, and wood) provide similar functions and at cheaper costs. Businesses and consumers can purchase specially imported corn-based bioplastic products, which are mainly produced in China instead of bioplastic products from cassava. In addition, an inefficient waste management system and the linkage of supply chain actors do not support the post-consumption of bioplastics.

Considering the impact of each stage of the value chain based on three sustainability dimensions, economic, environmental, and social aspects, on bioplastics from cassava, the key aspects of a sustainable cassava value chain are described.

Economic impacts: cassava is not used for food consumption but is mainly produced as low-value-based products such as dried cassava for animal feeds and cassava starch for industries. Considering high-value products (e.g., bioplastics from TPS blends) and implementing cassava waste or by-products (e.g., cassava pulp/peel), cassava processors can increase the demand for cassava and improve its long-term economic viability. Bioplastics from cassava generate an economic value 14.8–22 times greater than cassava roots. In addition, the results of this study indicated that almost half of the respondents (48.6%) accept bioplastic products from cassava and are willing to pay more than 13.2–15.4% of the price of a takeaway order for them. Due to demand, a new market sector on bioplastics has emerged and driven the need for the use of cassava applications in the plastic and cassava industries, as well as green businesses and retailers. This shift not only enhances the profitability of the processors but also benefits farmers and related stakeholders. These lead to the improvement of a sustainable cassava value chain, which can enhance the productivity and competitiveness of the cassava and bioplastic sectors.

Social impacts: growth in the cassava and bioplastic sectors can improve the level of unemployment and drive workers to upskill on agricultural technology to enhance productivity and prevent climate change and cassava disease, as well as learn more about bioplastics and renewable sources from by-products. Sharing knowledge on sustainable practices (e.g., use less pesticides) from cassava processors and bioplastic industries with farmers and end-users is also important.

Environmental impacts: an increase in the use of single-use plastics and plastic items (e.g., food trays, containers, cutlery, straws, and plastic bags) has adversely affected plastic wastes and carbon emission. In addition, cassava farming and its industries can produce severe environmental impacts (e.g., soil degradation and wastes from cassava production) if they do not consider sustainable practices and maintain soil conditions. The development of bioplastics from cassava would provide alternatives to plastics from bio-based materials, which may reduce carbon emissions. Moreover, the waste management of bioplastics is different from petroleum-based plastics. Bioplastics from cassava are compostable depending on many parameters. The biodegradation of cassava edible bioplastic in plantation soil was higher than that in landfill soil [

72].

{kind=link}

{kind=link}

{kind=link}