Abstract

Environmental, social, and governance (ESG) integration is an increasingly popular and innovative investing strategy that requires companies to be transparent about their ESG practices to facilitate investors’ decisions. In the palm oil sector, companies are addressing ESG risks by adopting and disclosing ESG efforts to improve access to financing. This study seeks to broaden existing research on ESG transparency and firms’ financial indicators by using firm valuation as a financial indicator and investigating the moderating role of firm size in the palm oil sector. It first investigates whether ESG transparency has a direct positive or negative effect on firm valuation. Transparency is measured using the Zoological Society of London’s (ZSL) Sustainability Policy Transparency Toolkit (SPOTT) 2021 assessment, which provides scores for palm oil companies’ total, environmental, social, and governance disclosures. Firm valuation is measured by the price-to-earnings ratio (P/E), a widely used ratio calculated by dividing the share price by earnings per share. The study also explores the moderating role of firm size, using accounting-based measures such as revenue and assets, in strengthening the relationship between ESG transparency and firm valuation. The results show statistically significant negative relationships between ESG transparency and firm valuation. Companies with stronger ESG transparency are valued at a discount relative to companies with weaker ESG transparency. Additionally, the results find that firm size plays a moderating role such that larger firms strengthen the negative relationships between all transparency measures and firm valuation. These findings encourage constructive action for various stakeholders and provide implications for future research to support mainstreaming sustainable palm oil.

1. Introduction

Palm oil is the world’s most produced, consumed, and traded vegetable oil. It is the most land-efficient crop, utilizing only 6% of cultivated land for vegetable oils globally but contributes over a third of the total output [1], making it difficult to substitute. The oil palm crop is a commodity widely used across products such as cooking oil, processed food, cosmetics, cleaning products, animal feed, and biofuel [2]. Almost half of the world’s population depends on palm oil for their diets [3]. Palm oil is produced in tropical countries, with production dominated by developing countries such as Indonesia and Malaysia, which account for 83% of global production, with 59% produced by Indonesia (44.7 million tonnes) and 24% produced by Malaysia (18.1 million tonnes) [4]. The crop is a key contributor to economic development. It has alleviated poverty for millions of people [5], created jobs, developed rural infrastructure [6], and strengthened exports for producing countries [7].

However, palm oil’s growing importance to global economies has placed companies in the sector under more scrutiny than any other agricultural commodity due to their involvement with unsustainable practices. Linking sustainability to the environmental, social, and governance (ESG) context, the sector generates several negative externalities to society. Clearing land for expansion has resulted in environmental concerns from deforestation and peatland degradation, which significantly account for the 23% of greenhouse gas (GHG) emissions attributed to agriculture, forestry, and other land uses [8]. This has resulted in the recurring transboundary haze in Southeast Asia, causing respiratory issues and fatalities, leading to billions of dollars in damage [9]. Furthermore, palm oil production impacts the highest number of threatened species when compared to other oil crops [10]. Social issues such as forced labor have led to the United States (US) placing sanctions on companies [11], while governance issues such as corruption [12] and incomplete traceability [6,13,14] have raised greenwashing risks. These issues have eroded investor and consumer confidence in the sector. With the world population estimated to grow from 8.0 billion in 2022 to 9.7 billion by 2050 [15], future demand for palm oil is forecasted to grow further. Production could rise four to six times from 73.8 million metric tonnes in 2020 to 264 to 447 million metric tonnes by 2050 [16], creating opportunities for producers to expand production capacities. With few productive oil crop substitutes, it is therefore critical for palm oil companies to expand their involvement with sustainable practices such as those that protect forests and peatlands, optimize land use efficiency, improve grievance mechanisms, and strengthen transparency. Regulations and engagement efforts from several stakeholder groups in society have also emerged to mainstream sustainable palm oil.

Globally, sustainability has become an increasingly important priority to provide for the needs of present and future generations. ESG was coined as a framework for sustainability in a financial sector initiative to integrate non-financial indicators in financial markets [17]. Companies with better ESG management can raise shareholder value by better managing ESG risks, foreseeing regulatory changes or consumer trends, and entering new markets or lowering costs. In other words, companies concerned with ESG would thrive by satisfying shareholders and societal stakeholders such as regulatory bodies and consumers. If ESG risks are left unaddressed, companies can incur financial risks through compliance and reputational risks, higher operational costs, lower revenues [18], lower equity value of shares, and reduced access to financial resources to maintain and grow their operations. This can consequently reflect poor growth opportunities and investment returns, which are embedded in firm valuation measures that investors use for analysis.

Investors have responded to ESG risks by adopting ESG integration as an innovative strategy for sustainable investing. ESG integration is defined by the United Nations Principles for Responsible Investment (UNPRI) as “the systematic and explicit inclusion of material ESG factors into investment analysis and decisions” [19]. The Global Sustainable Investment Alliance’s (GSIA) 2020 report shows that ESG integration (USD 25.2 trillion) has overtaken negative and exclusionary screening (USD 15.9 trillion) as the most common sustainable investment strategy [20]. It evidences the need for a sustainable transition through innovative approaches to better investor engagement. Investors are closing this gap by increasingly seeking non-financial benefits by focusing on ESG transparency, which is commonly associated with sustainability reporting, corporate social responsibility (CSR), and ESG disclosures. These can help firms and investors unlock a significant pool of untapped financial resources to catalyze the transition toward a more sustainable world.

Sustainable finance through ESG integration thus plays a vital role in achieving sustainable palm oil production. The World Wide Fund for Nature Inc. (WWF) warned that divestment could erode the sustainability of the sector [21]. Instead, institutional investors need to improve their capacity to engage with palm oil companies such as by enhancing policy disclosures, which would facilitate the uptake of ESG integration. The UNPRI Investor Working Group on Sustainable Palm Oil also engaged with palm oil companies, banks, and shareholders to instill stewardship efforts to transform the palm oil sector to become more sustainable [22]. Additionally, several supporting initiatives are being developed to encourage companies to increase their ESG transparency to support ESG integration. As such, in addition to improving their practices, palm oil companies are increasingly raising their efforts in ESG transparency to gain stakeholder trust and a competitive advantage for their efforts toward sustainable palm oil. While production continues to grow, deforestation for the commodity decreased by 82% in the last decade to 45,285 hectares annually from 2018 to 2020 [23], evidencing that sustainable palm oil is attainable. Research outside the palm oil sector shows linkages between ESG transparency and financial indicators of firms [24] to justify the case for ESG integration. ESG transparency can improve stakeholder trust, minimize reputational risk, avoid compliance costs, reduce operational risks, and create long-term value for stakeholders [17,18,25]. Yet, there remains a degree of skepticism as to whether the relationship between ESG transparency and financial indicators is positive or negative. Some studies also found that individual environmental, social, and governance components could influence financial indicators more than overall ESG [26,27,28]. Few studies have used firm valuation measured by the price-to-earnings ratio (P/E) as a financial indicator, despite being the most popular valuation tool used by investors [29,30,31]. Additionally, some studies found that larger firms are equipped with more resources and capacity to engage in ESG, suggesting that firm size has a moderating role in strengthening the relationship [32,33]. Only a handful of direct relationships have been found within the palm oil sector using financial indicators such as stock performance [34,35,36,37]. Research on the moderating role of firm size in the sector is absent. However, a growing body of evidence in the sector suggests that ESG transparency can influence firm valuation, and that firm size has a moderating effect. Hence, this study seeks to contribute to the existing literature by being the first to investigate the relationships between ESG transparency and firm valuation, and the moderating role of firm size in the global palm oil sector.

The results find that there is a negative relationship between ESG transparency and firm valuation, and that larger firms do strengthen the negative direct relationship between ESG transparency and firm valuation. This indicates that the innovative strategy of ESG integration may be lacking in the sector and larger companies are susceptible to more scrutiny. The findings call for more engagement with investors and financiers to improve sentiment for ESG integration and strengthen companies’ competitive advantage toward mainstreaming sustainable palm oil.

As an overview, this paper reviews the existing literature in Section 2 to contextualize the basis for the authors’ research questions, methodology, analysis, and discussion. Section 3 develops the conceptual framework and the subsequent hypotheses for the study. Section 4 details the methods adopted to conduct the research study, including the justifications for data sources, variables used, and the model tests that are conducted. Section 5 presents the results of the study and analyzes whether the hypotheses in question can be accepted or rejected. Section 6 discusses the interpretation of the study, along with recommendations and implications for future research. The final section summarizes the paper and concludes with how the study contributes to the existing literature.

2. Literature Review

This section explores the applications of existing organizational theories to justify how providing stakeholder transparency on ESG practices translates to financial benefit through ESG integration. The literature review then draws inspiration from similar studies between ESG performance and financial indicators conducted beyond the palm oil sector, and highlights research that uses variables such as firm valuation and firm size that can be considered for the palm oil sector.

2.1. Stakeholder Transparency

ESG risks call for stronger regulation, penalties, and transparency to prevent companies from behaving unsustainably and minimize externalities conveyed. Companies are expected to internalize sustainability into their strategy and culture to attain competitive advantage while reducing risks [38] such as legal, reputational, and financial risks that can divert resources away from main businesses. With ESG considerations embedded into their practices, companies should communicate their ESG efforts by establishing a comprehensible metric of externalities involving the ecosystem and stakeholders [39], which improves stakeholder transparency.

The treatment of ESG transparency overlaps with that of sustainability reporting, corporate social responsibility (CSR) reporting, and ESG disclosures in the literature. Commonality exists in that both reporting and disclosure aim to address transparency to stakeholders. While sustainability addresses a broader definition, CSR and ESG cover aspects of sustainability. Through ESG, sustainability is categorized into three components—environmental, social, and governance—and has become the most extensively used measurement of sustainability standards in current practice to hold companies accountable [40].

The percentage of Fortune Global 250 firms allocating portions of their annual reports and CSR reporting to CSR activities grew from 44% in 2011 to 78% in 2017 [25], showcasing the growing norms of communicating sustainability among businesses. High ESG performance can provide “insurance-like” protection as these firms gain stakeholder trust and experience less criticism from stakeholders such as investors and regulatory bodies [41,42]. Clark, Feiner, and Viehs (2015) [43] note that the future of sustainable investing will involve active ownership by multiple stakeholder groups, which aligns with the growing trend of ESG integration.

Companies providing stakeholder transparency on ESG practices can be rationalized by existing organizational theories. In this paper’s context, there also exist various supporting initiatives to encourage palm oil companies to communicate their efforts.

2.1.1. Theoretical Underpinnings

Providing transparency about ESG efforts draws on existing organizational concepts of agency theory, legitimacy theory, stakeholder theory, and signal theory for substantiating the relationship between ESG transparency and firm valuation.

Legitimacy theory suggests that companies are operating in ways accepted by society to attain a social license to operate [44]. Corporations will legitimize their actions through ESG transparency to ensure their continuing existence. Society may penalize firms for their negligence or reluctance towards ESG activities which can threaten firm survival. This theory is most cited among research papers exploring the relationship between sustainability and financial indicators.

Similarly, stakeholder theory originated from R. Edward Freeman in 1984, who argued that companies should consider other members of society who have connections to business activities to influence the success of products and services [45]. This is backed by other studies [46,47] where other stakeholders in society include employees, customers, suppliers, financiers, communities, and government. Societal stakeholders are thus key motivators for companies to engage in ESG practices [48]. By doing so, ESG practices could increase shareholder value by improving reputation which attracts more customers, improving productivity for trained employees [49], and minimizing regulatory costs.

The agency theory is based on two main pillars: the principal–agent relationship and the separation between ownership and control [50]. The principal, otherwise the company owner or shareholder, delegates the managing power to the agent to act in the best interests of the principal [51,52]. However, agents may pursue their own interests at the expense of the principal, resulting in agency cost and conflict [53]. Principals are more focused on the long term while agents are more focused on short-term benefits. For this paper, ESG disclosures are perceived to reduce agency costs via information asymmetry, which arises from the separation between ownership and control [54]. The stronger the disclosure, the greater the transparency. ESG transparency can thus help reduce compliance costs, which can influence the risk profile and valuation of the firm [55,56].

The signaling theory suggests that companies will reduce information symmetry present in imperfect markets by sharing information with stakeholders. ESG transparency hence signals a firm’s credibility and commitment towards sustainability to external stakeholders [57,58].

Therefore, these theories provide the basis for why ESG transparency signals to stakeholders the extent to which the company is operating sustainably, making ESG integration an innovative sustainable investing strategy for firms to gain a competitive advantage. ESG transparency can be used to legitimize corporate activities towards creditors and shareholders, thus incentivizing efforts to engage in sustainability [59]. This implies that higher ESG transparency reduces agency costs, and signals legitimacy to various stakeholder groups that firms have low compliance risk and minimal reputational risk, and hence deserve stronger valuation. Companies that behave less responsibly will be punished by the market [60,61,62] and this can be reflected by a decrease in performance, such as sales and earnings, which are linked to their valuations.

2.1.2. Supporting Initiatives

To facilitate transparency, there exist several regulations and initiatives by different stakeholder groups in society that can be applied across sectors, with some developed for the palm oil sector itself. These include regulations, mandates by public exchanges, voluntary initiatives, certification schemes, and data and reporting platforms that enable stakeholders to access information about companies’ practices.

Regulations

Reporting regulations have been on the rise to motivate companies to strengthen their sustainability disclosures [63]. Within the EU, the EU Taxonomy Regulation aims to develop a classification system for economic activities that are environmentally sustainable [64]. Additionally, the EU’s Sustainable Finance Disclosure Regulation (SFDR) addresses ESG reporting obligations by requiring financial market participants to share how sustainability risks are managed [64]. Newer developments include the European Sustainability Reporting Standards (ESRS) for entities subject to the Corporate Sustainability Reporting Directive (CSRD), which are required to be applied by large companies in their 2024 annual reports [65]. These are mandated by the European Commission, based on draft standards developed by EFRAG (the European Financial Reporting Advisory Group) [66]. At a global scale, the International Sustainability Standards Board (ISSB), set up by the International Financial Reporting Standards (IFRS) Foundation [67], published its first sustainability-related disclosure standards known as IFRS S1 and IFRS S2, building upon existing market standards, to establish the global baseline for sustainability-related disclosures [68]. These are critical in unifying standards on sustainability and promoting more transparent and credible ESG data and disclosures for stakeholders.

Public Exchanges

Public exchanges help foster market confidence by strengthening governance to promote ESG disclosures through listing requirements. This helps to protect companies’ reputations and facilitates competition among companies [69]. In 2015, when the UN Sustainable Stock Exchanges (SSE) initiative launched its Model Guidance, less than a third of stock exchanges in the world provided ESG guidance, and by mid-2020 more than half of SSE’s members published ESG guidance [70]. Public exchanges have mandated sustainability reporting for listed companies across Singapore, Hong Kong, Indonesia, Malaysia, and Thailand [71], and large listed companies in Europe and the United Kingdom (UK) [72]. For India, it will be mandated for the top 1000 largest companies from fiscal years 2022 to 2023 [71].

Voluntary Initiatives

To address information asymmetry about non-financial concerns between companies and investors [73], there exists a wide range of standards and frameworks available for assessing ESG transparency through sustainability reporting and ESG disclosures. These include the UN Global Compact Network (GCN), the Global Reporting Initiative (GRI), the Sustainability Accounting Standards Board (SASB), and the International Integrated Reporting Council (IIRC). There are also several data providers such as Bloomberg, Sustainalytics, Standard and Poor’s (S&P), and Morgan Stanley Composite Index (MSCI) who have their ESG metrics. These frameworks and databases have comprehensive guidelines covering ESG considerations, but these are not consistently used across industries and firms. Despite enabling transparency, the inconsistency makes the extent and quality of ESG disclosure heterogeneous [29], creating challenges for stakeholders to assess and compare ESG performance.

Principle-based voluntary ESG initiatives have progressively been established to strengthen private investments, such as the UNPRI, UN Environment Programme (UNEP) Finance Initiative, Equator Principles, and Principles for Sustainable Insurance [74]. In response to managing heterogeneous disclosures, the UNPRI, GSIA and the CFA Institute formed a collaboration to create an authoritative resource that harmonizes the different terms and definitions relating to ESG investment to make ESG disclosures more comparable and enhance the investors’ decision making while minimizing legal, compliance, and reputation risks [75].

Certification

In the palm oil sector, certification is commonly used for companies to transparently communicate commitments to ESG. The most globally recognized is the Roundtable on Sustainable Palm Oil (RSPO), a voluntary certification set up in 2004 to promote sustainable palm oil [76]. Its members comprise stakeholder groups in the value chain from producers, processors, traders, manufacturers, retailers, investors, and NGOs [77]. The RSPO collaborates with government bodies to formulate legislative frameworks. However, its high visibility and association with greenwashing have highlighted weaknesses and garnered doubts about the certification’s credibility [4], as observed in the earlier examples of labor challenges. RSPO certification is also costly to adopt, as it excludes smaller companies and smallholders from being recognized as sustainable. Nonetheless, its Principles and Criteria (P&C) have continually been revised and strengthened over time [78], reflecting its progressive nature. Certification is still beneficial in demonstrating a commitment to sustainability and improved branding. Since its inception, approximately 20% of palm oil produced globally is certified sustainable by RSPO [79].

At a national level, the top-producing countries of Indonesia and Malaysia established Indonesian Sustainable Palm Oil (ISPO) and Malaysian Sustainable Palm Oil (MSPO) in their respective countries. Compared with RSPO, studies consistently found RSPO to be the most robust, comprehensive, and ambitious in criteria, followed by MSPO, and ISPO the least [76,77,80,81,82]. As such, some studies do not count MSPO and ISPO as certified sustainable palm oil (CSPO) [2,4,78]. Indirectly, they demonstrate that the stringent nature of RSPO and its high costs make it challenging to attain. Instead, ISPO and MSPO are perceived more as stepping stones for smaller companies and smallholders in the top two producing countries to adopt sustainable practices [83].

Data and Reporting Platforms

The rise in data and reporting platforms boosts transparency and traceability for the palm oil sector. These platforms include satellite-based deforestation monitoring systems such as the World Resources Institute’s (WRI) Global Forests Watch program [84], Suitability Mapper [85], Forest Cover Analyzer [86], Trase [87], and RSPO PalmTrace [88]. These platforms enhance supply chain mapping and enable better planning of land use strategies and sustainable palm oil production.

Moreover, data platforms such as the Zoological Society of London’s (ZSL) Sustainability Policy Transparency Toolkit (SPOTT) [89] and WWF’s Palm Oil Buyer’s Scorecard [90] go beyond the requirements of certification to rank companies on their sustainability disclosures over the years. For example, the SPOTT initiative is an annual assessment of soft commodity producers, processors, and traders on the ESG-related public disclosure of their organization, policies, and practices [89]. They produce separate assessments for palm oil, timber and pulp, and natural rubber. They actively collaborate with industry players including the RSPO [91] and all members of the value chain—governments, financiers, producers, consumers, investors, and NGOs—to adopt strategic measures to improve the sustainability of palm oil while achieving supply chain transparency [92]. At its inception in 2014, only large publicly listed companies were initially assessed [93], as they were perceived to have the largest environmental impact, greater access to resources, and more pressure to improve compared to smaller companies. However, smaller and privately owned companies were subsequently added as stakeholders sought to ensure holistic efforts of transparency in the sector. Smaller companies have shown improvement rates similar to those of larger companies due to increased pressure on the sector throughout SPOTT assessments from 2014 to 2018 [93]. The indicator framework has also been revised and expanded to include indicators beyond “Environmental” considerations to provide a comprehensive scope of ESG, and it is considered to have reached a point of maturity [93].

2.2. Integrating Sustainability with Finance

Several studies beyond the palm oil sector find that transparency on ESG can have a relationship with various financial indicators. These relationships conducted across sectors and countries extend support for ESG integration. Common variables such as firm valuation and firm size are studied further to rationalize the relationships. Drawing inspiration from these studies, the literature links back to the palm oil context by reviewing existing research in the sector to identify gaps and opportunities that this paper can help to address.

Since 1970, over 2000 studies have been conducted [24] to marry the relationship between the non-financial indicators of sustainability with financial indicators. This demonstrates the push for ESG integration into financial considerations, building the foundations for sustainable investments. However, the findings of prior research have been mixed. There could be significant positive or negative relationships, or no significant relationships. In Friede, Busch, and Bassen’s (2015) [24] analysis, most studies found a positive relationship between ESG and firms’ financial indicators, a quarter had a neutral relationship, while a tenth reflected a negative relationship. These studies are scoped differently using inconsistent measures for sustainability [30] as well as financial indicators. Moreover, results were also mixed as to whether total ESG or isolated environmental (E), social (S), or governance (G) components held more weight in determining financial indicators. Isolating the components also helped to remove the effects of netting, as a negative indicator in one component could be negated by a strength in another [94].

Many studies found a positive relationship between ESG and organizations’ financial indicators [24,43,95] such as lowered cost of capital, better operational performance, and improved stock price performance and market value. Higher ESG performance inherently protects firms by portraying a positive reputation to shareholders [41]. An analysis of 52 studies based on 33,878 observations finds that corporate social performance is positively correlated with corporate market value [26], suggesting that the S component holds more weight. A global study of 44 countries concluded with statistical significance that ESG scores were heterogeneous, where overall ESG scores and E scores had positive effects, while S and G scores had negative effects [27]. In Germany, a significantly positive relationship was found between ESG and accounting-based firm performance, and G was found to be the strongest determinant factor [28], possibly due to the German Corporate Governance Code introduced in 2002 where firms are obligated to report CSR. This demonstrates how regulating authorities have a positive influence over companies’ actions. At the industrial level, a study of large manufacturing companies in the US during the 1980s found that those with higher profits tended to be more socially responsible with reduced risk [96]. Another study on the real estate sector in developed countries found a positive relationship between ESG disclosure with financial performance, where E was also significant in influencing return on capital (ROC) [29]. As for the pharmaceutical industry in Italy, G was positively related to financial performance [97], where good corporate behaviours through compensation, management of fraud, ethics and values, transparency, and anti-corruption could be linked with companies’ operations and relative market performance.

Amongst those with neutral relationships, it is possible that the costs of demonstrating ESG were net off by financial benefits [98,99]. Similarly, no significance was found in another study on Italian blue-chip companies between ESG scores and abnormal returns, evidencing that social responsibility was not a reliable indicator for leverage [100]. These examples suggest that ESG disclosures have no relevance in determining any financial benefit.

Of those with negative relationships, a study on Northern European firms also found a negative relationship between ESG and P/E [31], with a weak correlation suggesting that investors interested in ESG were not necessarily concerned with the high returns. In terms of risk, a negative relationship was found between E and S disclosures on total risk, as corporate transparency increased the reputation and trust of stakeholders [101]. Similarly, the ESG performance of textile and apparel firms helped to reduce volatility and market risk [102].

As opposed to a linear relationship, Nofsinger, Sulaeman, and Varma’s (2019) [94] study of E and S components found that institutional investors demonstrated an asymmetric preference for strong and weak CSR attributes. Investment portfolios that avoided or had few weak ES stocks generated higher alphas than those with a greater fraction of weak ES. Institutional investors were averse to ES weaknesses through divestment but appeared ambivalent towards ES strengths because CSR was also linked with agency costs that eroded economic benefit [94]. This aligns with the findings of Krüger (2015) that the stock market responds weakly negatively to positive ESG news [103] and that firms with strong CSR records had more liability due to greater scrutiny of negative events [104]. In this regard, minimizing risk through divestment appeared to dominate investors’ decision-making process.

Amongst the literature review, few studies were conducted on the palm oil sector using other financial indicators. Those conducted on palm oil either had only an environmental focus or were exclusive to RSPO certification rather than overall ESG transparency, which could be reflected in other measures that were more inclusive of smaller firms. For studies with an environmental focus, markets were found to be sensitive to negative environmental events, as the 2015 haze crisis had significantly negative impacts on abnormal stock returns for palm oil companies in Southeast Asia [34]. Separately, a positive relationship was found between environmental disclosure and return on assets (ROA) for Malaysian companies, which were explained to have a larger firm size than Indonesian companies [105]. For studies exclusive to RSPO certification, nine Indonesian RSPO-certified companies were found to have a 2.28 times appreciation in share price between 2005 and 2016 compared to uncertified companies [35]. Climate Advisers also established a palm oil index that found 18 RSPO-certified firms outperforming non-certified counterparts by about 25% over 6.5 years [36]. Mixed results were observed in another study of 64 palm oil firms, where Malaysian RSPO-certified firms had poorer risk-adjusted performance than their respective non-certified peers, while the Indonesian RSPO-certified portfolio fared better than its peers, implying RSPO had limited influence on stock performance [37]. Tey and Brindal (2020) [37] identified that RSPO certification requires economies of scale that are more suited for larger farm operations and that palm oil investors may benefit more from small-cap companies in Malaysia. They also raised the need for an easily understood and accepted ESG framework, as opposed to RSPO certification, to provide a more robust view for developing the basis of investing for growth through a sustainability standard. This spurs further investigation into the palm oil sector that goes beyond certification and assesses overall ESG transparency. It will also respond to Godfrey and Hatch (2007) [106], who called for industry-specific research, as differences among industries can become obscured when ranked by the same criteria. Comparisons within industries provide more clarity on relevant and meaningful sustainability considerations.

2.2.1. Firm Valuation

Studies in previous literature have used various financial indicators such as market value, ROA, ROC, P/E, stock returns, and dividend yield. This study will focus on the valuation of a company to be given by P/E because far fewer studies have used P/E, despite it being the top-used measure for valuing companies [107]. It is calculated as the share price divided by earnings per share. Earnings per share is the net income over a certain period, typically a fiscal year, divided by the total number of shares outstanding at the point in time.

The rationale for using P/E is that investors can apply ESG investing principles to guide their decisions to purchase company shares, which are reflected by the share price. As a ratio, P/E standardizes stocks of different prices and earning levels, making it useful for comparing its performance across time or with competitors in the same industry [108].

Future value creation is a key component in firm valuation [109]. It reflects growth, characterized by the size of a company’s investments, the excess investment returns relative to the cost of capital, and the length of time a company can find value-creating investment opportunities [110]. It is unlikely for a company’s P/E to revert to historically higher levels unless growth prospects and return on incremental capital remain consistent with historic levels, which are difficult to maintain. This explains why stocks with a high P/E are growth stocks that signify overvaluation, as fast growth and high volatility are expected.

Meanwhile, a low P/E represents value stocks, which typically represent companies that have slowed in growth. Value stocks indicate modest expectations of future value creation and, if the company is stable, they can present opportunities for attractive returns. A low P/E could signify undervaluation or that the company has slowed in growth with low volatility. Investors prefer to invest in company stocks with low P/E because it also represents a low price for a high earning, deeming it a value stock with higher returns anticipated [111]. Therefore, P/E ratios help to identify valuation premiums or discounts, as well as risk and growth opportunities. Studies show that portfolios with low ratios tend to provide abnormal or higher risk-adjusted returns [112,113,114].

Conversely, high P/E ratios can also be associated with slow growth [115]. Investors could change perspectives and view investments as less risky, causing demand and hence prices to increase. Such an example was when the COVID-19 virus impacted global economies in 2020, and companies with the highest ESG rankings were found to be trading at a 30% premium relative to poor performers by referencing their forward P/E [116]. This was due to high capital inflows into ESG funds causing an ESG bubble, suggesting that the P/E values of ESG investments were overvalued. Within the short period from April to June 2020, more than USD 70 billion was poured into ESG equity funds, surpassing annual flows [40]. Markets viewed ESG funds as less risky than non-ESG funds during COVID-19 when uncertainty was high, and demand for ESG funds grew, raising the P/E despite market conditions which implied slowed growth. Separately, Goldman Sachs Equity Research also hinted at a positive relationship, where global companies highly aligned with the EU Taxonomy were valued at a 37% P/E sector-relative premium, while low carbon-emitting companies in the Asia Pacific were trading at a 28% P/E premium over their high carbon-emitting peers [71]. Companies being transparent about their sustainability efforts appeared to encourage ESG integration as an innovative strategy for improving their valuation.

The rise of ESG presents many opportunities for sustainable investments. Studies remain inconclusive about the relationship between ESG transparency and P/E. Jitmaneeroj (2018) [30] found a positive relationship between the governance component and P/E in US companies, as companies focused on corporate governance practices during the 2008–2009 financial crisis and less on environmental and social factors. Almeyda and Darmansyah (2019) [29] and Junius, Adisurjo, Rijanto, and Adelina (2020) [117] found no statistical significance between ESG with P/E in the real estate sector and four ASEAN countries, respectively. Meanwhile, Svensson (2020) [31] found a negative relationship with P/E in Northern Europe companies. Hence, ESG could be suggested to have a neutral, positive, or negative relationship with P/E.

Therefore, by recognizing that ESG performance is linked with providing stakeholders with transparency on high performers, companies with high ESG transparency could have low P/E as they are expected to have higher returns than companies with low ESG transparency. Alternatively, high ESG transparency could also be associated with high demand and hence high P/E, as they are viewed as relatively low risk.

2.2.2. Firm Size

Firm size is frequently found to be related to firms’ sustainability-related decisions. Larger firms are usually more involved with CSR compared to smaller firms [118]. Many studies commonly use market capitalization, assets, and revenue as a control variable to control for the effect of size [28,32,49,53,119]. They imply that larger firms have a greater influence on societal stakeholders (e.g., larger consumer outreach and more employees) and are thus more closely monitored by the public, incentivizing them to better disclose their sustainability efforts [33,120]. They are also better positioned to reduce regulatory pressures from governments via the legitimacy theory [121], which explains why some public exchanges have stricter reporting requirements for larger firms. Larger firms are characterized by economies of scale [122], with more monetary, intellectual, and physical resources available to invest in ESG, and set exemplary models as market leaders [102]. Larger firms that invest in ESG can thus reduce firm risk, create a positive reputation for the firm, gain stakeholder trust, and gain a competitive advantage. However, the direction of the relationship between firm size, CSR performance, and financial indicators can be positive or negative [31].

While the benefits outweigh the costs for larger firms, the case is the opposite for smaller firms. ESG disclosure raises the cost of capital for listed small and medium-sized enterprises (SMEs) [123] as their firm characteristics differ from large firms by having simpler reporting structures, limited financial and human resources, and hence limited sustainability management tools [124], which changes the effectiveness of ESG disclosure.

To a lesser extent, studies also consider interaction effects between firm size with disclosure to explore firm-level heterogeneity since larger firms have greater propensity to attain better ESG performance. However, the interaction effects were found to be inconclusive. Krueger, Sautner, Tang, and Zhong (2021) [33] found a negative interaction between firm size and mandatory disclosure, indicating that smaller firms had less availability of ESG reporting, and were thus associated with poorer ESG performance than larger firms. Sánchez-Infante Hernández, Yañez-Araque, and Moreno-García (2020) [32] found that firm size had a significant moderating effect, where larger firms had stronger relationships between CSR and economic performance. On the other hand, Lin, Cheah, Azali, Ho, and Yip (2019) [125] had a counterintuitive finding that smaller firms in the automotive industry had higher efficiency with higher green innovation investment returns, and generated more profits than large firms that were too aggressive in investments and had lower financial performance.

As for firm size in the palm oil sector, empirical studies on the moderating role of firm size were not found. However, research finds that larger firms are perceived similarly to have greater propensity and hence expectations to adopt sustainable practices. The 2020 Annual Communication of Progress (ACOP) reports submitted by RSPO members found that the progress of the biggest players across the supply chain is considered too slow, especially for processors and traders, where nine of the ten biggest players were less than 30% certified [126]. Amongst growers, only three of the top ten achieved at least 80% certification. Companies with the largest land area and volumes of palm oil handled still fell short of certification. These companies are expected to have significant leverage with more responsibility to take up RSPO certification and were called to take urgent action to close the certification gap, as larger players have added responsibility to raise their uptake of sustainable palm oil.

The current literature commonly polarizes palm oil producers as large or small, without distinguishing medium-sized companies or smallholders [127]. Thus, policies and initiatives rarely target medium-sized companies. They may also lack the capacity to adopt ESG commitments given the numerous frameworks and guidelines for companies to adhere to. Some smaller companies can also have sustainable practices in place that are not incorporated into the policy framework, or they may only sell to the domestic market, and hence do not require an RSPO certification. The MSPO and ISPO certifications and standards such as the SPOTT framework help to be more inclusive toward varying firm sizes, as they look beyond the price premium and stringent criteria associated with RSPO certification to assess companies on their sustainability efforts. Efforts are still needed for more inclusive support toward smaller companies, including strengthening the acceptance for MSPO and ISPO to be recognized by international stakeholders.

2.2.3. Valuation for Palm Oil Companies

The valuation of palm oil companies was previously found to be positively influenced by economic indicators such as inflation, exchange rates, and the world crude palm oil (CPO) price [128]. In recent years, however, the correlation between companies’ share prices and CPO prices began to show a disconnect due to rising ESG concerns. The correlation between CPO prices and the Bursa Malaysia Plantation Index, which tracks 43 listed planters, weakened from 0.75 in 2020 to 0.22 in early 2021 when CPO prices rose beyond RM 3500 per tonne [129]. Similar observations were found between the CPO and the Kuala Lumpur Plantation Index (KLPI) up until August 2021 [130]. The portrayal of weak ESG practices, through the US Customs and Border Protection’s (CBP) ban on FGV Holdings Bhd and Sime Darby Plantation due to the use of forced labor, were cited to have eroded the share price of Malaysian planters. Investors’ growing ESG concerns appear to have overtaken economic indicators in influencing the valuation of palm oil companies. This reaffirms the need for companies to be transparent about ESG efforts for addressing investor concerns to encourage uptake of ESG integration as an innovative sustainable investing strategy.

A descriptive study performed by a global financial institution on 15 palm oil companies in 2021 identified similarly that ESG risks have caused the sector to trade at a record low P/E, which is a 72% discount below peak P/E [131]. This is wider than other ESG-excluded names in tobacco and thermal coal sectors. In other words, the palm oil sector was valued at a discount despite efforts to improve practices. Even with volatile market movements due to the Russia–Ukraine war and Indonesia’s temporary export ban on palm oil in 2022, another study by Foo [132] on five palm oil companies in 2022 suggested that the sector was still valued at 13-year lows since the Global Financial Crisis in 2009. This was reaffirmed by Rijk, Miraningrum, and Piotrowski (2022) [133], who found that Wilmar, the largest company in the palm oil supply chain, reached its lowest P/E in history as of March 2022 due to reputational impacts caused by poor transparency relating to forest and sustainability risks, calling for better transparency of “No Deforestation, No Peat and No Exploitation” (NDPE) policy execution and uptake of certified palm oil. As these studies are mainly descriptive, they inspire an opportunity to conduct empirical research to validate if there is any statistical significance between ESG transparency and the P/E valuation discount of palm oil companies, instead of looking at stock returns or ROA conducted by previous studies.

3. Conceptual Development

Derived from the literature review, this section builds the conceptual framework and develops the testable hypotheses.

The growing adoption of ESG integration and the rise in stakeholder initiatives such as regulations, certifications, and reporting platforms have pressured companies to address the ESG risks of the palm oil sector and become more transparent by communicating their efforts towards sustainable palm oil production. Theoretical applications can be applied as companies achieve their social license to operate via the legitimacy theory, address stakeholder concerns on ESG risks via the stakeholder theory, act as agents on behalf of their shareholders via the agency theory, and reduce information asymmetry via the signaling theory to signal their commitment towards sustainability, all of which are expected to have an impact on firm valuation.

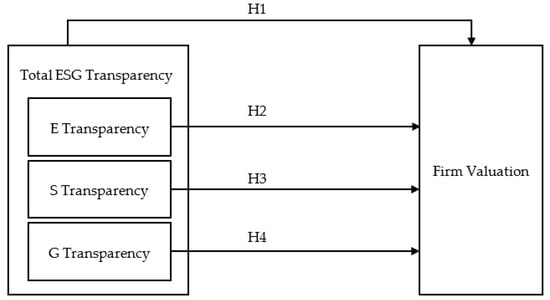

3.1. Direct Relationship

The literature review references studies outside the palm oil sector that suggest a possible direct relationship between ESG transparency and financial indicators, but the results were inconclusive as to whether the relationship was positive or negative. The relational ambiguity could suggest both scenarios. With firm valuation as a popular indicator used by investors, ESG transparency could have a positive relationship with firm valuation. Firms with higher ESG transparency could be valued at a premium compared to firms with less transparency. They could be high in demand and viewed as relatively low in risk. This is demonstrated by the ESG bubble in 2020 [116] and the need to align with regulations such as the EU Taxonomy [71], which are relevant to the palm oil sector. On the other hand, it is also possible that ESG transparency could be negatively related to firm valuation. Firms with higher ESG transparency could instead be undervalued stocks relative to those with lower ESG transparency. They would be preferred by investors as they potentially present a higher return for their low price relative to earnings [111,113]. Therefore, the conceptual framework is first developed by hypothesizing that the construct of ESG transparency could have a direct effect on firm valuation where the direction is either (a) positive or (b) negative.

Most studies investigate overall ESG, with the view that the management of environmental, social, and governance issues are intertwined. For example, the absence of corruption in governance could ensure strong enforcement of penalties towards environmental and social compliance. Alternatively, good governance that signals 100% traceability can mitigate the negative impacts of deforestation (environmental) and land use conflicts (social). By addressing all three aspects, companies benefit financially and attain a competitive advantage [38] as they are protected against compliance and reputational risks. Initiatives such as certification, where RSPO-certified companies outperformed non-certified counterparts [36], help to address such risks. This derives the first hypothesis that total ESG transparency has a direct positive or negative relationship with firm valuation.

H1a:

Total ESG transparency will have a positive relationship with firm valuation.

H1b:

Total ESG transparency will have a negative relationship with firm valuation.

Studies also find that the direct relationship could be observed for individual environmental, social, and governance components as they can have netting effects on one another [94] or even be heterogeneous, providing a mix of positive and negative relationships [27]. Therefore, each component should be considered for influencing firm valuation.

In the palm oil sector, the environmental (E) component could be directly related to firm valuation. Research on the environmental effects received more attention given increasing regulations relating to deforestation, transboundary haze, and the urgency of climate-related risks, such as declaring GHG emissions as part of the 2015 Paris Agreement. Erian (2016) [34] found that the 2015 haze crisis had significant negative impacts on abnormal stock returns of listed palm oil companies, implying that markets are sensitive to the knowledge of environmental events. Environmental indicators are also based on various scientific tools that ease data collection and facilitate extensive scientific research. Furthermore, the earlier years of SPOTT assessments entailed only environmental considerations before including social and governance [93], evidencing that environmental considerations hold more weight in attaining a competitive advantage than social or governance efforts. Thus, transparency about environmental efforts is suggested to have more influence on firm valuation than social and governance efforts. This derives the second hypothesis that environmental transparency has a direct positive or negative relationship with firm valuation.

H2a:

Environmental transparency will have a positive relationship with firm valuation.

H2b:

Environmental transparency will have a negative relationship with firm valuation.

It is also possible that financial indicators in the palm oil sector could be driven by the social (S) component or even both environmental and social components found in other studies [26,94]. Social issues have gained traction in recent years. The sanctions on FGV Holdings and Sime Darby over forced labor allegations highlight the increasing consideration of social issues, as the sanctions were key in influencing the share prices of Malaysian planters [130]. Social considerations could hold more weight in attaining a competitive advantage than environmental or governance considerations. This derives the third hypothesis that social transparency has a direct positive or negative relationship with firm valuation.

H3a:

Social transparency will have a positive relationship with firm valuation.

H3b:

Social transparency will have a negative relationship with firm valuation.

Governance (G) can also be a key driver of firm valuation. Velte (2017) [28] notes that the introduction of legislation such as the Corporate Governance Code possibly resulted in governance being the strongest driver for firm performance. Jitmaneeroj (2018) [30] also found a positive relationship between governance and P/E in US companies, as companies focused on corporate governance practices during the 2008–2009 financial crisis. Initiatives such as increased regulations, improvements to certifications, and companies disclosing their commitments highlight efforts for more transparency and better governance. The rise of data and reporting platforms to promote 100% traceability and improve transparency also reflects the emerging importance of governance in the sector. Greenwashing claims and investor aversion can hence be reduced by improving the credibility of deforestation commitments. Governance considerations could hold more weight in attaining a competitive advantage than environmental or social considerations. This derives the fourth hypothesis that governance transparency has a direct positive or negative relationship with firm valuation.

H4a:

Governance transparency will have a positive relationship with firm valuation.

H4b:

Governance transparency will have a negative relationship with firm valuation.

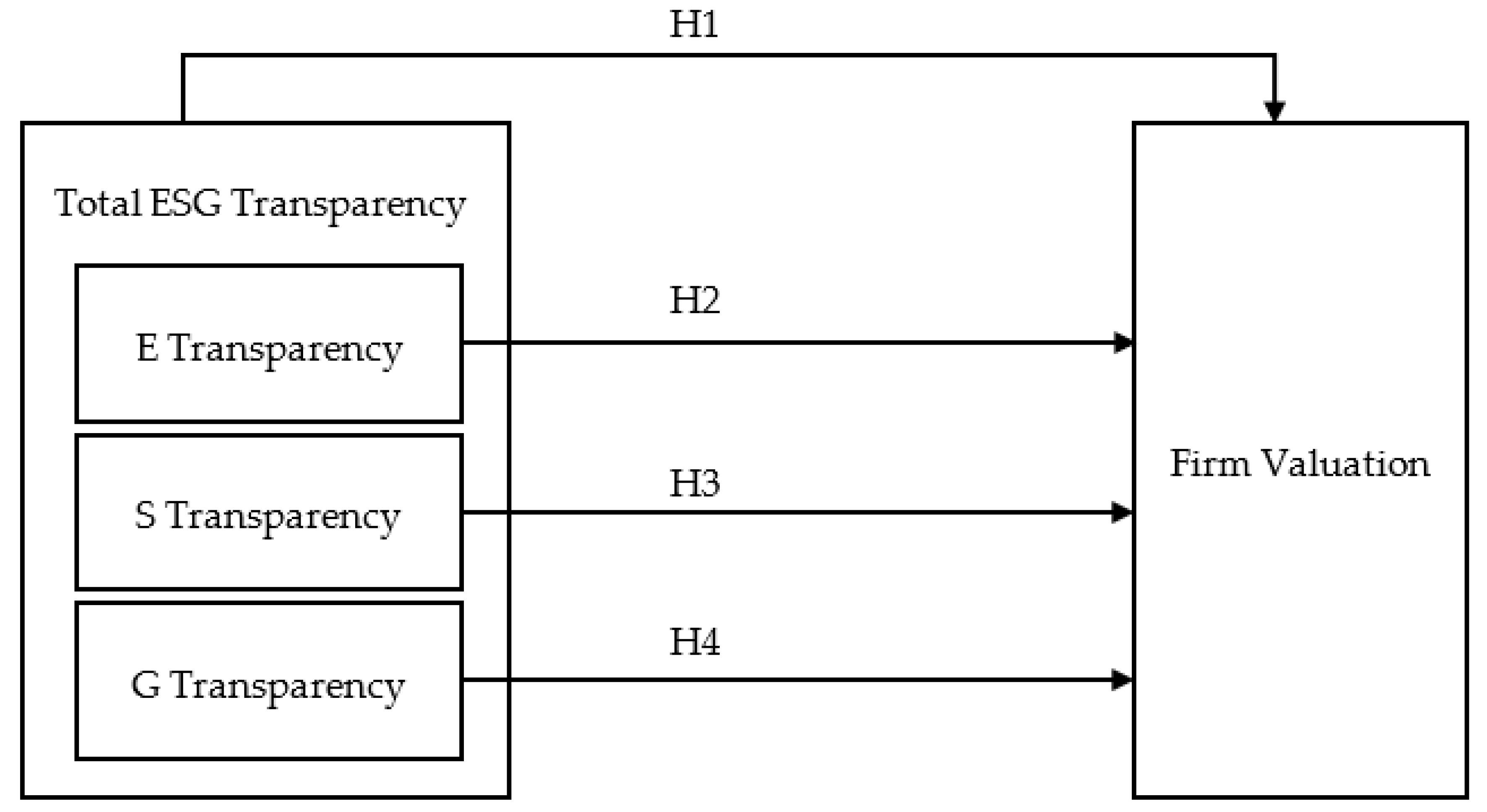

Figure 1 summarizes the conceptual framework for the direct relationship between transparency and firm valuation in hypotheses 1 to 4.

Figure 1.

Conceptual framework for the direct relationship.

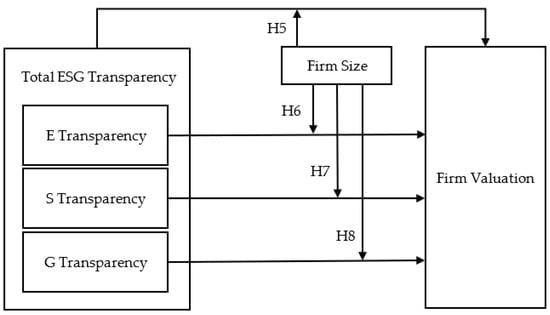

3.2. Moderating Role of Firm Size

The literature review also observes that firm size could be another construct that moderates the relationship between ESG and financial indicators [32,33]. Compared with smaller companies, larger companies are more cost-effective and have greater capital to address ESG concerns. They also face more pressure to be more sustainable. This is reiterated by how some public exchanges mandate sustainability reporting for larger listed companies (e.g., Europe, UK, India). Large companies are hence perceived to be more responsive by enhancing ESG transparency to improve their competitive advantage, as they have capabilities to adhere to higher sustainability standards and have less ESG risk associated with traceability and compliance as compared to smaller companies. In palm oil’s context, the analysis of ACOP reports singled out larger players to increase their uptake of sustainable palm oil [126]. Thus, the earlier conceptual framework can be expanded upon to derive the fifth hypothesis that firm size plays a moderating role in the relationship between total ESG transparency and firm valuation.

H5a:

Firm size will moderate the positive effect of total ESG transparency on firm valuation such that when firm size increases, the positive effect is larger.

H5b:

Firm size will moderate the negative effect of total ESG transparency on firm valuation such that when firm size increases, the negative effect is larger.

Firm size could also have significant interaction with individual ESG components. In assessing sector valuation, Abdullah, Hamzah, Ali, Tseng, and Brander (2020) [105] found a significantly positive relationship between environmental disclosure and ROA in Malaysian companies that were larger in firm size relative to Indonesian companies. This derives the sixth hypothesis that firm size plays a moderating role in the relationship between environmental transparency and firm valuation.

H6a:

Firm size will moderate the positive effect of environmental transparency such that when firm size increases, the positive effect is larger.

H6b:

Firm size will moderate the negative effect of environmental transparency on firm valuation such that when firm size increases, the negative effect is larger.

In the social aspect, the penalties in reaction to forced labor allegations and poor working conditions were also imposed on large companies such as Sime Darby, which impacted their share prices linked to firm valuation [130]. However, Sime Darby engaged the necessary resources to review their operations and reimbursed workers [134]. This evidences that large firms have capacities to respond to regulatory pressures and right their wrongs on social factors to maintain a competitive advantage. This derives the seventh hypothesis that firm size plays a moderating role in the relationship between social transparency and firm valuation.

H7a:

Firm size will moderate the positive effect of social transparency on firm valuation such that when firm size increases, the positive effect is larger.

H7b:

Firm size will moderate the negative effect of social transparency on firm valuation such that when firm size increases, the negative effect is larger.

As for governance, large companies are expected to have the resources to adopt sustainability management tools to uphold strong governance standards. However, due to Wilmar’s governance issues relating to poor transparency and weak uptake of certified palm oil, the industry leader reached its lowest P/E in history [133]. This evidences that large firms are under more scrutiny for their governance standards to maintain a competitive advantage. This derives the eighth hypothesis that firm size plays a moderating role in the relationship between governance transparency and firm valuation.

H8a:

Firm size will moderate the positive effect of governance transparency on firm valuation such that when firm size increases, the positive effect is larger.

H8b:

Firm size will moderate the negative effect of governance transparency on firm valuation such that when firm size increases, the negative effect is larger.

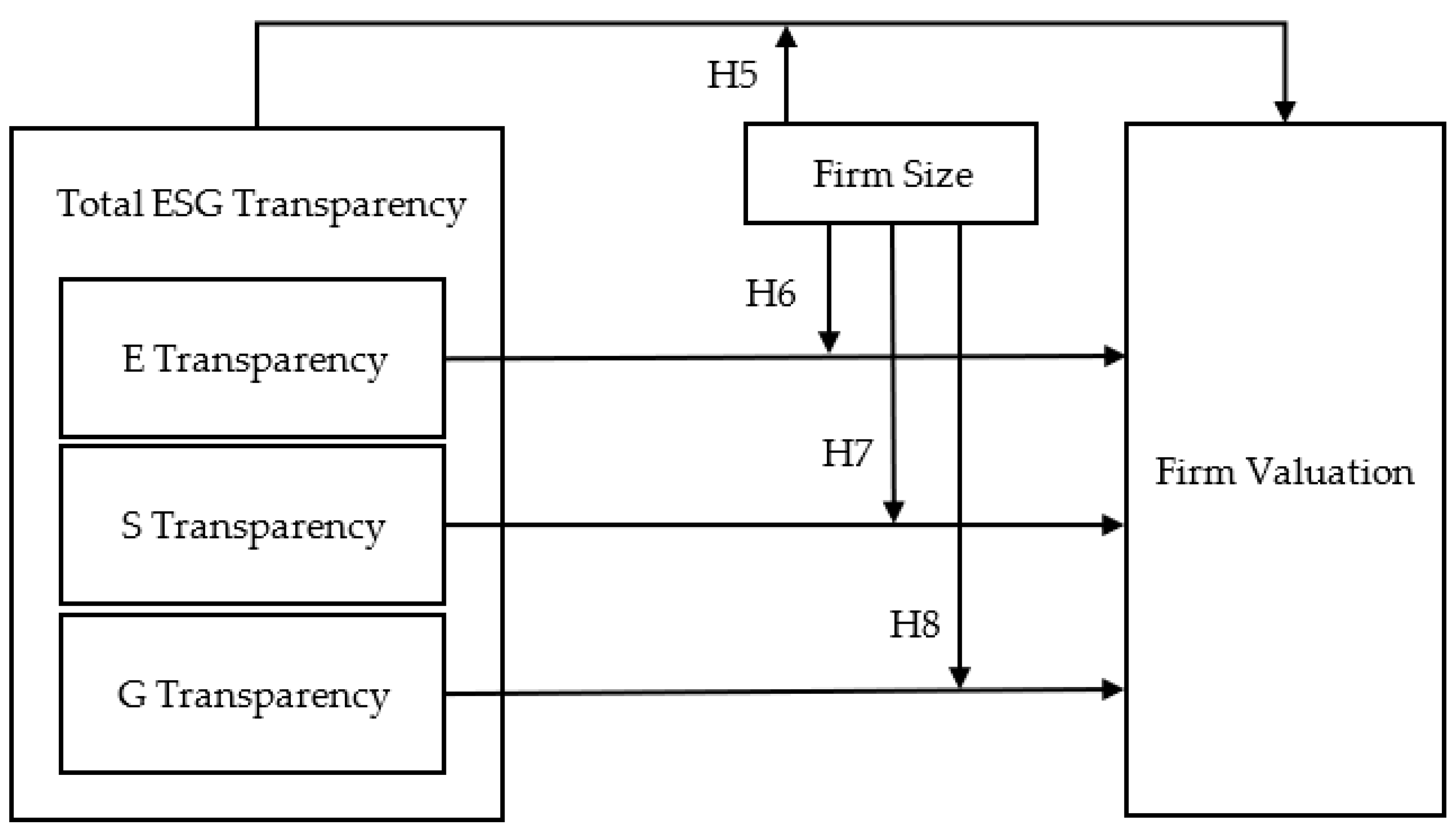

Figure 2 summarizes the conceptual framework for the moderating role of firm size on the relationship between transparency and firm valuation in hypotheses 5 to 8.

Figure 2.

Conceptual framework for the moderating role of firm size.

4. Research Methodology

This section describes the methods adopted for designing the research, including the data sources and variables used for conducting the model tests to investigate the hypotheses developed in Section 3.

4.1. Methodology

This study adopts a deductive approach to test the eight hypotheses that (i) examine the direct relationships that total ESG, environmental, social, and governance transparency have with firm valuation and (ii) understand the moderating role of firm size on the direct relationships that total ESG, environmental, social, and governance transparency have with firm valuation. The paper then evaluates the findings for the hypotheses.

The hypotheses are formulated by defining the measures used for each construct shown in Table 1. The construct of ESG transparency will be defined by the ESG disclosure scores in ZSL’s SPOTT 2021 assessment. Overall ESG transparency will be defined by the total score, while environmental, social, and governance transparency are defined by environmental (E), social (S), and governance (G) scores, respectively. The construct of firm size as moderator will be defined by revenue, or assets in the robustness test, while firm valuation is defined by P/E.

Table 1.

Mapping constructs to measures.

The investigation will be a cross-sectional study of 36 palm oil companies, which compares four categories of ESG disclosure scores—total score, and independent E, S, and G scores—to isolate netting effects from other scores. Subsequently, the study will explore if firm size (revenue or assets) plays a moderating role by strengthening the relationship between ESG scores and P/E. To test the hypotheses, a multiple regression analysis was performed using the analysis of variance (ANOVA) test via Microsoft Excel based on the ordinary least squares regression method.

4.2. Data

ESG disclosure scores were retrieved from the total, E, S, and G scores in the SPOTT assessment of 100 palm oil companies released in November 2021. SPOTT is a relevant framework because it has a niche focus on commodity producers, processors, and traders, and assesses public disclosure of their organization, policies, and practices towards ESG issues [89]. These companies are closer to the upstream supply chain with greater exposure and control over plantation activities that dominate the ESG issues highlighted earlier. SPOTT is a reliable tool for measuring ESG transparency because its index values are measured against a comprehensive indicator framework, which was formulated through in-depth consultation with SPOTT’s companies and users, and it has stabilized over the years since its inception in 2014 [93]. SPOTT is also versatile, as it provides access to both broad and detailed information of companies with a disaggregation of variables such as market capitalization, landbank, and company engagement [93]. This provides an opportunity to assess trends across different factors. Referencing the SPOTT assessment will respond to Tey and Brindal (2020) [37], who acknowledged RSPO certification was exclusive to larger companies and called for a more easily understood and accepted ESG framework. The SPOTT assessment framework addresses this by going beyond the requirements of certification to assess ESG performance, having attained a point of maturity [93], making it more inclusive towards smaller companies. The framework also responds to Godfrey and Hatch’s (2007) [106] call for more industry-specific criteria that increase the relevance of criteria for the sector.

The SPOTT 2021 palm oil assessment adopts a comprehensive framework with 182 ESG indicators across 10 categories, developed with consideration of the UN SDGs [89]. Table 2 presents the 10 categories and the corresponding number of ESG indicators for each category. These categories include themes that are tailored to the palm oil sector, such as traceability, deforestation, certification, and labor rights. Among the total of 182 indicators, an indicator can fulfil two or all three categories of E, S, and G. Thus, there are 136 E indicators, 120 S indicators, and 52 G indicators. For each indicator, points of 0 to 1 are assigned, where 0 is given for no disclosure, a partial point (e.g., 0.5 or 0.01 to 0.99) can be given for partial disclosure, and 1 point for clear disclosure (e.g., 100% traceability). The scores are then converted to percentages ranging from 0 to 100, where higher scores are associated with more transparent disclosure.

Table 2.

Categories and indicators in the SPOTT 2021 palm oil assessment.

Companies’ financial data were sourced from Thomson Reuters, a professional platform for financial data. Data were sourced based on the latest available in July 2022, to account for a lagged effect within a year of SPOTT’s score release. Fiscal year-end numbers and reported currencies for revenue and assets were also verified on companies’ annual reports and websites to ensure accuracy. As palm oil companies are listed across multiple stock exchanges globally, financial data were reflected in different reporting currencies. For standardization, numbers were converted to USD based on exchange rates in Xe.com, which is an established platform for global exchange rates. The dates of exchange rates used for conversion were based on the latest fiscal year reporting date (for assets and revenue) and share price closing date (for market capitalization), where applicable.

4.3. Sample

The sample aims to represent the global population of publicly listed palm oil companies with a score from the SPOTT assessment. The reason for scoping publicly listed companies is because their data are more easily accessible to the wider group of public investors who can make investment decisions that contribute to enabling sustainable production. Among SPOTT’s 2021 assessment of 100 companies, 45 companies were publicly listed. Due to missing financial data on Thomson Reuters (e.g., delisted, restructured), 9 companies were omitted from the study. This narrowed the final sample to 36 companies listed in Appendix A. They include dominant players in Southeast Asia such as Wilmar International, Sime Darby Plantation, IOI Corporation, Kuala Lumpur Kepong Bhd, QL Resources Bhd, Golden Agri-Resources Ltd., and FGV Holdings. Other global players such as Itochu Corporation, Archer-Daniels-Midland Co, Bunge Ltd., and AAK AB listed in Japan, New York, and Sweden are also included. Of the 36 companies, at least 31 have operations in Indonesia and Malaysia, and 29 of them (including subsidiaries) are RSPO members. This sample size is larger than the sample sizes in some of the earlier studies conducted. The sample also provides a global representation of palm oil companies, as opposed to earlier studies that mostly focused on companies in Indonesia and Malaysia only.

4.4. Variables

With the sample size of 36 companies, three independent variables are considered to align with the norms of regression analysis by having at least 10 observations per variable [135] to avoid overfitting. The first four hypotheses will have one direct and two control variables to examine the direct relationship, while the remaining four will have a direct, interactive, and control variable to examine the interactive relationship.

The direct variables of ESG disclosure scores are the total, E, S, and G scores which are used to assess the direct relationships in hypotheses 1 to 4. They are also used to assess the interactive relationships in hypotheses 5 to 8.

To test the direct relationship in hypotheses 1 to 4, two control variables for firm size are used—market capitalization and revenue. In this study, the natural logarithm is applied to both attributes to reduce skewness.

To test the interactive relationship in hypotheses 5 to 8, one interactive variable and one control variable are used. The interactive variable considers firm size as a moderator where total revenue is multiplied by the sustainability score. It assesses if firm size moderates the relationship between ESG scores and the P/E ratio. Meanwhile, the control variable retains the natural logarithm of market capitalization.

In all hypotheses, the dependent variable references the P/E ratio as a measure for firm valuation that is commonly used by investors. This is based on the share price divided by the normalized annual earnings per share. Normalized earnings exclude unusual expenses or revenue that are not typical of the companies’ main businesses.

For robustness, each test is replicated by replacing the revenue with assets as the firm size proxy in the control variable for hypotheses 1 to 4, and in the interactive variable for hypotheses 5 to 8.

Table 3 summarizes the description of each variable.

Table 3.

Variable description.

To evaluate the impact of ESG transparency on firm valuation of palm oil companies, the equation for the direct relationship is as follows:

where:

P/Ei,t = β0 + β1ESGi,t-1 + β2Control(FSi,t-1) + β3Control(MC)i,t + εi

- P/Ei,t is the valuation of company i at time t

- ESGi,t-1 is a measure of the total, E, S, or G disclosure score of the company i at time t-1

- Control(FS)i,t-1 is the control variable of firm size (revenue or assets) at time t-1

- Control(MC)i,t is the control variable of market capitalization at time t

- εi is the error term.

To evaluate the moderating role of firm size on the relationship between ESG transparency and firm valuation of palm oil companies, the equation for including the interaction effect is as follows:

where:

P/Ei,t = β0 + β1ESGi,t-1 + β2(ESGi,t-1×FSi,t-1) + β3Control(MC)i,t + εi

- P/Ei,t is the valuation of company i at time t

- ESGi,t-1 is a measure of the total, E, S, or G disclosure score of the company i at time t-1

- ESGi,t-1×FSi,t-1 is a measure of interaction between the disclosure score (total, E, S, or G) of company i at time t-1, multiplied by the firm size (revenue or assets) of the company i at time t-1

- Control(MC)i,t is the control variable of market capitalization at time t

- εi is the error term.

4.5. Model Tests

To conduct an ordinary least squares regression, eight model tests are run. For each of the four independent direct variables (total, E, S, G Score), two tests are run. One tests for the direct relationship, and the other for the interaction effect. In all tests, the same control (market capitalization) and independent variable (P/E) are used. Table 4 presents the difference in variables used across each model.

Table 4.

Model description.

5. Results and Analysis

This section examines the data through descriptive statistics, correlation analysis, and the regression results of the study, which analyzes whether the hypotheses in question can be accepted or rejected.

5.1. Descriptive Statistics

Table 5 presents the summary statistics for the 36 publicly listed palm oil companies in this study. The P/E ratio averages 10.150 with a range from 3.85 to 58.57, which indicates that firms can be significantly undervalued or overvalued relative to one another. The total scores range from 8.1 to 91.30 with an average of 61.4. This average is higher than the average of 42.8 from the original list of 100 companies which included private companies, hinting that publicly listed companies are more inclined to engage in more ESG transparency to meet additional requirements of public exchanges. The individual E, S, and G scores average 56.293, 63.066, and 56.153, respectively, suggesting that each component does not differ too much from the average total score, although the S score is the closest.

Table 5.

Descriptive statistics.

5.2. Correlation Analysis

Table 6 presents the correlation coefficients for the variables used in this paper. At first glance, the direct variables total, E, S, and G scores are negatively correlated with P/E, with E having the highest correlation. Firm size variables of revenue and assets are weakly negatively correlated with P/E, while market capitalization has a positive correlation with P/E. In their natural logarithm form, revenue, assets, and market capitalization are all positively correlated with P/E and disclosure scores. As interactive variables, when the score is multiplied by revenue or assets, the correlation is negative. Among the direct variables, E, S, and G scores are highly correlated with the total score above 0.9, suggesting that netting effects from each score are minimal. E and S have higher correlations with the total score above 0.99, while G has a lower correlation of 0.95, implying that E and S scores could have more influence over the total scores than G scores.

Table 6.

Correlation matrix.

5.3. Regression Results

Table 7 summarizes the results of the eight model tests. It reports the estimated coefficients, standard errors, and significance levels.

Table 7.

Regression results for 36 palm oil companies.

5.3.1. Direct Effect of ESG Transparency on Firm Valuation

In models 1, 2, 3, and 4, the regression results of the total, E, S, G score variable respectively are negatively significant at a 1% significance level. This indicates a negative relationship where companies with higher total, E, S and G scores reflect lower P/E ratios. H1a, H2a, H3a, H4a are rejected while H1b, H2b. H3b. H4b are accepted at a 99% confidence interval.

5.3.2. Firm Size Moderates the Effect of ESG Transparency on Firm Valuation

In models 5 and 7, the regression results of the interactive variable using firm size multiplied by the total scores and S scores respectively are negatively significant at a 1% significance level. This means that firm size strengthens the negative effect of the total score and S score on P/E. H5a and H7a are rejected while H5b and H7b, are accepted at a 99% confidence interval.

Similarly, in models 6 and 8, the regression results of the interactive variable using firm size multiplied by the E scores and G scores respectively are negatively significant at a 5% significance level. This means that firm size strengthens the negative effect of the E score and G score on P/E. H6a and H8a are rejected while H6b and H8b are accepted at a 95% confidence interval.

A robustness test was performed by replacing revenue with assets as a control variable in models 1r to 4r, and as an interactive variable in models 5r to 8r, which is summarized in Table 8. The reproduced regression results in Table 9 reiterate that overall relationships across direct and interactive variables are all negatively significant at a 5% significance level in models 1r to 8r. When revenue is used, the direct negative relationships are stronger at a 1% significance in models 1 to 4. The interaction effects are also stronger at a 1% significance when revenue is multiplied by total and social scores (models 5 and 7, respectively). In the robustness test, the adjusted R-squared parameters are smaller when assets are used for testing the interaction effect. Models 5, 6, 7, and 8 hence explain a larger proportion of the variance of P/E by the interaction effect of firm size when compared to models 5r, 6r, 7r, and 8r, respectively. Nonetheless, the robustness test provides consistent results that the direct and interactive relationships hold at a 5% significance level.

Table 8.

Model description for robustness test.

Table 9.

Regression results for robustness test of 36 palm oil companies.

The results in the first four models affirm the negative effect of total ESG, environmental, social, and governance transparency on firm valuation.

Table 10 summarizes the results of the direct relationship, which accepts the first four hypotheses that favor a negative relationship and rejects those that favor a positive relationship.

Table 10.

Result summary for the direct relationship.

Expanding on the direct relationship, the results confirm that firm size acts as a moderator in strengthening the negative effect that total ESG, environmental, social, and governance transparency have on firm valuation.

Table 11 summarizes the moderating role of firm size, which accepts the last four hypotheses in favor of strengthening the negative effect.

Table 11.

Result summary for the moderating role of firm size.

6. Discussion

This section evaluates the results to verify how they align with findings from the literature review and conceptual development. It then provides recommendations for various stakeholder groups and describes the limitations of the study, which can have implications for future research.

6.1. Interpretation

6.1.1. Direct Relationship

The results of the first four models reflect that total, environmental, social, and governance scores are all negatively significantly correlated with P/E in the palm oil sector. These findings differ from Almeyda and Darmansyah (2019), Abdullah, Hamzah, Ali, Tseng, and Brander, (2020), Orlitzky, Schmidt, and Rynes (2003), and Velte (2017) [26,28,29,105], who found that individual components of E, S, or G were more determinant in influencing financial indicators. The results also counter Nofsingera, Sulaeman, and Varma (2019) [94] regarding the possibility of netting effects and Lam, Zhang, and Chien’s (2018) [27] mix of positive and negative relationships. Instead, the netting effects of individual E, S, and G scores are considered minimal and less heterogeneous. The results show that all three ESG factors in the palm oil sector are strongly linked with one another and must be considered holistically. This aligns with the correlation matrix in Table 6, which showed a strong positive relationship between total, environmental, social, and governance scores. The 182 indicators in Table 2 also reflected that some indicators overlap with one another. For example, attaining 100% traceability not only enhances transparency and ensures good governance, but it mitigates environmental issues associated with deforestation and social issues such as land use conflicts. Initiatives such as companies’ NDPE policies and RSPO certifications collectively aim to address environmental issues such as deforestation and peatland management, social issues such as exploitation, human conflicts, and smallholder inclusion, and governance issues such as weak transparency and traceability.