Abstract

The ability of A-share listed companies to adhere to the digital economy and achieve long-term corporate benefits amidst an uncertain external environment through financial digital transformation remains a crucial concern for entrepreneurs and scholars. The objective of this study was to scrutinize the effect of financial digital transformation on financial performance among 2566 of China’s A-share listed companies in the hopes of providing informative recommendations for businesses that are currently undertaking or planning to undertake financial digital transformation. To investigate the mechanism by which financial performance among A-share listed companies was influenced by digital transformation, a panel data regression model was utilized. The findings suggest that, first and foremost, financial digital transformation significantly boosts corporate financial performance for A-share listed companies, and this enhancement is sustainable over time. For every 1% growth in financial digital transformation, corporate financial performance improves by 1.1%. Corporate financial performance is projected to improve by 29.8% during the next three financial years. Secondly, information symmetry and operational expenses function as intermediaries in the financial digital transformation process that affects firm financial performance. For every 1% increase in financial digital transformation, the information symmetry level of firms grows by 15.1%, while the operational cost rate declines by 0.8%. Thirdly, information disclosure and operating costs play a chained intermediary role. Every 1% increase in the level of information symmetry reduces the operating cost rate by 2.3%. Fourthly, in comparison to enterprises in eastern provinces, businesses located in central and western provinces are better positioned to improve their financial performance by undertaking a financial digital transformation.

1. Introduction

The digital economy has emerged as a fresh engine for economic growth in the context of China’s economic change. In order to support a company’s regular administration and functioning, the finance department is crucial. However, accountants of many companies have not dismissed the traditional financial management concept but still focus on the main functions of accountants: accounting and supervision. Accountancy dominated by this idea cannot escape from large workloads and a complicated process, so it has more and more difficulty adapting to modern businesses. Therefore, to the growth trend of company digital transformation, the finance department’s old operating mode has been challenging to adjust and will even have a negative impact on it [1,2,3]. Facing the above problems, companies need to recognize the significance of the financial digital transformation, and improve business information transparency [4], reduce costs, and increase efficiency through financial digital construction [5,6,7]. Financial digitization is the process of collecting, handling, and applying business data by applying digital technologies. In this process, companies can receive more comprehensive information and improve their management levels and value-creation capabilities [8]. Financial digitalization can change the internal structure, operation mode, and thinking concept of companies with digital technologies, thus establishing a data-centerd management system and realizing the transformation of financial management activities from measuring value to creating value [8,9]. Three strategies were suggested by the State-owned Assets Supervision and Administration Commission’s Notice on Accelerating the Digital Transformation of State-owned Companies, which was published in September 2020: transformations based on IT, business, and finance. Among them, financial digital transformation is the starting point of the digital transformation of central companies. Thus, it is imperative to carry out the financial digital transformation of a company that wants to complete digital transformation successfully. According to the Outline of the Fourteenth Five-Year Plan for Accounting Reform and Development issued by the Ministry of Finance, accountancy should be consistently based on digital technologies, and proactively promoting the digital transformation of accounting management and the close integration of accounting with macroeconomic management at the national level as well as corporate operation and management functions is important. Subsequently, the Accounting Informatization Development Plan (2021–2025) also pointed out that accountants need to aggressively embrace the digital era’s coming and fiercely support the growth of accounting information technology. At present, the overall objectives of China’s accounting informatization include accelerating the transformation and upgrading accounting digitization, giving accounting data its due consideration, and continually enhancing the accounting information system. Accordingly, financial digital transformation is increasingly valued by the government and companies in the tide of digital transformation.

In China, A-share companies listed on the Shanghai and Shenzhen Stock Exchanges are the backbone for China’s economic development and the active market players in the economy and take a leading position in various industries. With an absolute advantage in economic scale, these companies are superior to other types of companies in terms of financing and profitability. However, the companies listed on A-share have inefficient information transmission and communication and difficulties in management and coordination due to their large scale, their large number of staff, complex ownership, and departments [10]. In addition, as the COVID-19 fully broke out at the end of 2019, numerous employees could not go to work normally because of large-scale quarantines, which put huge pressure on the normal operation and development of companies and influenced the profitability of most A-share listed companies [11,12]. The performance report of listed companies in the first quarter of 2020 indicates that nearly two-thirds of the companies presented downward performance. In particular, in the first quarter of 2020, the net profit of the firms listed on the Shenzhen Stock Exchange fell by 22.518 to 41.507 billion yuan, a year-on-year decrease of 30.84% to 56.85% (Data source: https://www.163.com/dy/article/FAGI88V40512DU6N.html (accessed on 17 January 2023)). In terms of the difficulties in company development under the pandemic, the White Paper on the Global Digital Economy—New Hope of Recovery under the Impact of the Pandemic issued by the Chinese Academy of Communications pointed out that Chinese companies need to accelerate digital transformation based on the action of “carrying out inclusive cloud service support policies, promoting the integrated application of big data and increasing support for business intelligent transformation”. According to statistics from Zhongxingxin Cloud Service, there were above 1000 finance-sharing service centers in China by the end of 2020 (Data source: http://ztcfol.com.cn/h-nd-384.html?checkWxLogin=true (accessed on 17 January 2023)). An increasing number of A-share listed companies have gradually accepted and carried out financial digital transformation. In future developments, financial digital transformation will become a competitive advantage for companies listed on the A-share. Therefore, a question is how the A-share listed companies can reduce costs and heighten efficiency through financial digital transformation.

This study examines the process by which financial digital transformation affects the financial performance of A-share listed companies in order to respond to this issue. It does so using a panel data regression model. This study explores the relationship between financial digital transformation and corporate financial performance as well as the function of financial digital transformation in lowering operational costs and information asymmetry.

This study makes several important contributions. Firstly, while there is a plethora of literature on digital transformation [13,14,15,16], there is a dearth of quantitative analyses on financial digital transformation, with only a few case studies available [17,18]. This study addresses this gap by constructing a dictionary of financial digital transformation feature words, based on the work of Chen and Xu, Tian et al., and Wu et al. [5,19,20]. The frequency of these feature terms in the statements of A-share listed firms is then measured using text mining techniques, with the resulting text analysis results serving as the proxy variables of financial digital transformation. Secondly, while case studies have shown that financial digital transformation improves performance, the underlying mechanism is not yet clear [17]. This study seeks to address this gap by focusing on how financial digital transformation influences financial performance and by clearly proposing the intermediary effect of the information symmetry level and operating cost. Thirdly, this study provides further analysis of the relationship between the two intermediary variables and verifies that financial digitalization reduces information asymmetry, leading to a reduction in operating costs and an improvement in corporate financial performance. Thus, the effect of financial digital transformation on financial performance is further elucidated in this section of the study.

2. Literature Review

2.1. Influence of Financial Digitization on Financial Performance

Currently, most scholars have studied the relation between financial digital transformation and financial performance from a resource-based perspective. In general, the conclusions of various studies could be divided into the data value theory and the productivity paradox. The former held that the more internal and external information a company has, the better its financial performance will be [6,8,21,22,23,24], and the latter held that digital technology investment had irrelevant or insignificant influence on corporate financial performance [12].

Regarding data value theory, scholars generally believed that data were an independent factor of production. In a more complex business environment, data has a stronger ability to directly create value in three aspects of increasing revenue, saving expenditure and controlling risk, thus improving the productivity and financial performance of companies indirectly, such as business process optimization, service level improvement, and information system quality improvement. Data can create value in all aspects of a company [25]. The combination between direct and indirect procedures is what causes financial digital transformation to have a beneficial effect on financial performance. Yu et al. [26] theoretically deduced from the existing literature that digital technologies could optimize the investment and financing decisions of companies. Herala et al. [27] pointed out that the digital information and datasets of companies could be converted into more added value, and more visibility could be brought to brands by opening data, which would likely appeal to many companies. Regarding the productivity paradox, Aral and Weill [28] proposed the theoretical model of IT resources and indicated that the total IT investment composed of IT assets and IT capabilities owned by a company had a nonlinear relationship with its business performance. Kazan et al. [29] pointed out that the monopoly digital platform attempts to create unique configurations through platform layers that are challenging to replicate by tight coupling to obtain monopoly power. Hence, the smaller united digital platform could only compete with it with the collective resources of the entire company. Hajli et al. [30] pointed out that some companies benefited from IT investment but with questionable return value, and some could not gain any benefit.

As the key department of modern business management, the degree of digital transformation of the finance department will profoundly influence the overall digitalization process of a company. Financial digital transformation is based on the financial sharing service model to help companies effectively obtain internal and external information, alleviate information asymmetry, and guarantee the effectiveness of companies in managing and controlling financial information. Diamond [31] proposed that information disclosure could improve the information symmetry level and helped companies obtain more transparent and efficient information, thereby making investment and financing decisions more accurate and reducing investment and financing costs. Guo and Xu [32] found that a company’s level of digitalization had a positive link with process-based business success and a U-shaped relationship with profit-oriented financial performance after analyzing panel data from 2254 manufacturing enterprises in China from 2010 to 2020. Stefanovic et al. [33] believed that banks with a higher degree of digitalization could sell more products to existing customers, obtained more new non-bank partners, and created additional profits. According to an empirical review of how well small and medium-sized businesses have performed their digital transformation, Teng et al. [34] found that the transformation could help improve business performance. Therefore, Hypothesis 1 was proposed.

Hypothesis 1:

Corporate financial performance is positively impacted by financial digital transformation.

2.2. Information Symmetry Mediates the Link between Digital Financial Transformation and Corporate Financial Performance

The majority of the research that is currently available holds that information symmetry and financial success are positively related. From the standpoint of environmental information disclosure, Wang et al. [35] explored the intermediate impact of visibility (such as analyst coverage) and liquidity in the influence mechanism of environmental information disclosure on financial performance, concluding that disclosure positively influences financial performance. However, some scholars believed that alleviating the information symmetry level had a negative or insignificant influence on corporate financial performance. Hassel et al. [36] pointed out that companies’ environmental information disclosure had cost concern effect and value creation effect.

On the basis of building a financial sharing center, financial digital transformation involves integrating the business processes carried out by many information systems, constantly strengthening rules and standards and improving the interfacing efficiency of financial information and business information. With the advancement of corporate financial digital transformation, more and more digital technologies are being applied to financial information management so that the internal information of a company can be effectively collected, screened, applied, and transmitted at a higher rate. Meanwhile, the external market information of the company is integrated into its strategic layout and daily management in the form of high density and efficiency. Companies can make accurate investment and financing decisions, participate in market competition, and conduct strategic goal decomposition due to information flowing inside more accurately and efficiently. Hence, they are more likely to obtain better financial performance. Furthermore, according to signal transmission theory, companies will also disclose more reliable business-related information during financial digital transformation, which can transmit a signal of reliability and good reputation. Investors are more willing to invest in such companies, which helps them obtain more external financing to expand production and gain more profits. Therefore, Hypothesis 2 was proposed.

Hypothesis 2:

In the process of corporate finance digital transformation and financial performance enhancement, information symmetry functions as a helpful intermediate.

2.3. Operating Cost Mediates the Link between Digital Financial Transformation and Financial Performance

According to the business process reengineering theory [37], the reform of organizational processes brought about changes not only to business processes but also to process-related elements, such as the organizational structure, the work system, and the management system. Hammer and Champy [38] defined business process recreation and believed that it was helpful to improve the business process of a company by thoroughly redesigning and constructing the old model to break the old model under the premise that the low efficiency of the company was caused by the original prodution mode or the unreasonable management system. The key to redesigning the business process of a company is to adjust the resource structure and human resource structure and optimize the key indicators that customers care about most by improving and redesigning the business process. This greatly improves customer satisfaction with the company and ultimately improves its overall core competitiveness. Many scholars have analysed and considered process change and transformation from various dimensions after the emergence of the business process redesign theory. Grover [39] stated that five factors were indispensable during business process redesign: process, organization, management, human resources, and IT technology. The importance of digital technology in restructuring production factors was highlighted by Resca et al. [40]. Hitpass and Astudillo [41] pointed out that in the era of Industry 4.0, technologies triggered decentralised processes with stronger decision-making autonomy, thus leading to a new business process. Business process redesigning is not only a superficial improvement of the business performance of companies; more importantly, redesigning helped companies fundamentally transform from a function-centerd traditional form to a new process-centerd one, so that they have revolutionary transformation and realize the fundamental transformation of their operation and management policies.

On the one hand, financial digital transformation can help companies optimize existing business processes and achieve more effective coordination between processes and digital technologies, thereby reducing their relevant costs. Pagani and Pardo [42] pointed out that, in addition to technical iteration, company internal coordination, including the connection and reorganization of different resources of the companies, should be the key point of business digitalization. The appropriate organizational capability and a digital business plan, according to Nadeem et al. [43], were essential for a company’s digital transformation. According to Mavlutova et al. [44], digital technology was seen as the power behind the sustainable growth of finance departments. As the fourth industrial revolution began to take off, the digital transformation of the finance department is characterized by integrating digital technologies into the business process to provide new innovation opportunities, thus directly influencing its operation. Under the influence of digitalization, the data information of companies is being generated and utilized in a more complete and accurate way, with scattered personnel, businesses, and activities in the past being integrated continuously so that the transaction costs within or between companies can be lowered.

On the other hand, financial digital transformation based on digital technologies is also conducive to accelerating internal and external information exchange, and the operating cost also decreases accordingly. Verhoef et al. [45] denoted that robots could replace high-cost manpower. Tiefenbeck et al. [46] believed that technology helped to lower the cost of collecting, transmitting, processing, and storing information and that financial digitalization had reshaped social interaction and had changed people’s ability to obtain and use information. Stroumpoulis and Kopanaki [47] believed that technologies in digital transformation could boost the development of important capabilities of companies, such as reducing operating costs, achieving operational control, and monitoring and supporting ecofriendly innovation, thus increasing sustainable business performance and raising the companies’ position in the market. Companies may enhance their external environment; successfully lower information, communication, collaboration, and marketing expenses; appropriately position client expectations; and boost their dynamic competitiveness throughout the financial digital transformation process. Internally, they can improve work efficiency, update the cost calculation model, and optimize the management level in order to heighten performance. Therefore, Hypothesis 3 was proposed.

Hypothesis 3:

In the process of promoting financial performance and transforming company finances digitally, operating costs act as a negative intermediate.

2.4. Relationship between Information Symmetry and Operating Costs

A higher information symmetry level can promote a company’s management efficiency. On the one hand, companies can obtain sufficient internal and external information and thus study the development laws of the market and the timely comprehension of their production and operation, make scientific decisions in real time, improve management efficiency, and reduce operating costs according to the information. On the other hand, by improving the information symmetry level, companies can communicate with creditors proactively and reflect on the financial situation to creditors in a timely manner, which helps companies and creditors deal with creditors’ rights and debt disputes in a timely and efficient manner. Therefore, Hypothesis 4 was proposed.

Hypothesis 4:

The information symmetry level has a negative influence on operating cost.

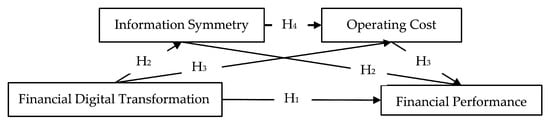

In summary, Figure 1 illustrates the technique through which this study’s construction of the financial digital transformation’s impact on financial performance works.

Figure 1.

Influence mechanism of financial digital transformation on financial performance.

3. Research Methodology

3.1. Sample Selection and Data Source

The research object of this study is China’s A-share listed companies between 2012 and 2021. The sample is first treated to guarantee the correctness of the data produced by (1) excluding the sample of companies that are categorised into ST and *ST in 2012–2021; (2) excluding the samples of companies listed after 2012; (3) excluding the sample of companies with special circumstances, incomplete data that cannot be supplemented and corrected, and serious data loss; and (4) carrying out 1% winsorization for extreme values. The indicator data used in this study are from financial reports publicly disclosed by the CNINF website and the China Stock Market and Accounting Research Database (CNINF website: http//www.cninfo.com.cn (accessed on 17 January 2023)).

3.2. Definition of Variable

Table 1 lists the explanatory, intermediate, and control variables that were used for this study.

Table 1.

Description of regression model variables.

- (1)

- Explained variables

Financial performance serves as this study’s explanatory variable. Drawing upon the work of Foster et al., Naeem et al., and Kahloul et al. [48,49,50], Tobin’s Q is selected as the measure of financial performance for the companies. This indicator offers a comprehensive way of assessing corporate financial performance.

- (2)

- Explanatory variable

The level of financial digitalization is the explanatory variable in this study. The yearly financial reports of businesses are chosen as a proxy indication of the degree of financial digitalization, and these distinctive terms connected to financial digitalization transformation are used. First, in this study, Python is used to extract text from annual financial reports of China’s A-share listing firms Second, based on the research of Chen and Xu, Wu et al., and Tian et al. [5,14,19], this study constructs a keyword dictionary of financial digital transformation (as shown in Table 2). Third, this study employs the word segmentation function of Jieba to segment the sample. Jieba is a Python-based Chinese word segmentation component that is capable of segmenting Chinese text, identifying parts of speech, extracting keywords, and supporting user-defined dictionaries. It offers three different segmentation modes: precise mode, full mode, and search engine mode. This study utilizes the precise mode. Following an examination of the annual financial report of the firm, Jieba performs word segmentation and part-of-speech tagging and retains only the words related to financial digitization that are indicated in the dictionary. Fourth, this study assesses the frequency of terms associated with financial digital transformation in the sample firms’ annual financial reports. The degree of financial digitalization indicates the degree of transformation of A-share listing firms. The degree of financial digitalization is indicated by the size of the indicator. If the indicator reads 0, the organization has not begun the shift to financial digitalization.

Table 2.

Keywords of financial digital transformation.

- (3)

- Intermediary variable

- Information symmetry levelThe information symmetry level is selected as the intermediary variable. The evaluation result of information disclosure of the Shenzhen and Shanghai Stock Exchange is selected as the proxy variable of the information symmetry level. This indicator is a rating of the information disclosure and its related normative operation of listed companies in a certain period in accordance with the information disclosure management measures, focusing on the authenticity, accuracy, timeliness, equality, and effectiveness of information disclosure, as well as the management of investor relations and information disclosure affairs. There are four grades assigned to the particular rating results: A, B, C, and D. The grades of an organization-A, B, C, and D-were rated in this study with 4, 3, 2, and 1, respectively. The larger rating result value of information disclosure indicates more transparent internal and external information transmission and a higher information symmetry level.

- Operating cost The operating cost ratio is selected as the intermediary variable. To calculate this metric, we divide operating expenses by operating income, representing the cost paid by a company for each unit of operating income.

- (4)

- Indicators of quality control

In accordance with findings from studies by Kahloul et al. and Rahman et al. [50,51], the company size, the operating income, the operating cash flow, the shareholding ratio of the largest shareholder, the nature of the property rights, the asset–liability level, and the nature of the audit report are selected as the control variables.

3.3. Panel Data Regression Model

- (1)

- Total effect model

The total effect model adopts the individual-time bidirectional fixed-effect model to validate Hypothesis 1.

In Formula (1), represents the financial performance of the ith enterprise in year t; represents the financial digital transformation; , ∑ Year, ∑ Firm, and represent control variables, time fixed effects, individual fixed effects, and residual items, respectively; and represent constant and variable regression coefficient respectively; and is the coefficient of . If is significantly positive, it indicates that there is a substantial beneficial impact on financial performance due to financial digital transformation; if is siginificantly negative, it indicates that there is a major negative impact on financial performance due to financial digital transformation.

- (2)

- Mediation effect model

The mediation effect model validates Hypotheses 2 and 3.

In Formulas (2) and (3), represents the financial performance; represents the financial digital transformation; and represents the level of information disclosure. If , and are significantly positive, the level of information symmetry plays a positive intermediary role in the effect of financial digital transformation on financial performance.

In Formulas (4) and (5), represents the level of information disclosure. If is significantly negative and is significantly positive, the operating cost plays a negative intermediary role in impediments to financial performance caused by digitization.

Further research on how publicizing information affects business expenses is needed; this study uses the individual-time bidirectional fixed-effect model to validate Hypothesis 4.

In Formula (6), represents the operating cost and is the coefficient of . If is significantly negative, information disclosure has a significant negative effect on operating cost; if is siginificantly positive, information disclosure has a significant positive effect on operating cost.

4. Research Results

4.1. Descriptive Statistics

Table 3 displays descriptive data for the indicators used in this study. The sample size of this research was 21,932, and the relevant variables had large differences. The minimum value of the financial performance (Tobin’s Q) of the A-share listed companies was 0, the maximum value was 259.1, the average value was 2.174, and the standard deviation was 3.179. This suggests a significant disparity between the financial results and the longterm success of various businesses. The average financial digital transformation (Dig) value for firms in the index was 2478, with a high variance of 2465, indicating a high degree of data dispersion. The minimum and maximum values were 0 and 10,427, indicating that some companies had not started the financial digital transformation, and some had a high degree transformation. The listed companies had remarkable differences in terms of transformation. Generally speaking, the information symmetry level (Inf) value had a mean of 2.568, with a standard deviation of 1.027, indicating that the information symmetry level of the listed companies was above the qualified level. However, the information disclosure levels of the companies varied greatly. The average value of the operating cost ratio (cost) was 72.07%, the minimum value was −15.43%, and the standard deviation was 24.89. This indicated that the companies had significant differences in terms of operating-cost ratios.

Table 3.

Descriptive statistics.

Regarding the control variables, the average value of property rights nature (Stc) was 0.401, indicating that there were fewer companies dominated by state-owned capital, and more than half of them were not state-owned companies. The average value of the asset–liability level (Deb) was 43.96%, indicating that the debt risk of the listed companies was relatively controllable. The maximum and minimum values were 90.52% and 5.58%, respectively, representing a wide disparity in the debt loads of the many corporations that are publicly traded. The average value of audit report nature (Aud) was 0.967, indicating the outstanding external supervision and management of the listed companies.

4.2. Correlation Analysis

Correlation analysis of the main variables was carried out to preliminarily understand the linear relationship between every two variables, and Table 4 displays the findings of the study. Table 4 shows that financial performance (Tobin’s Q) and digital financial transformation (Dig) have a high connection relationship. Among the intermediary variables, the correlation coefficients between financial performance (Tobin’s Q) and the information symmetry level (Inf) and between financial performance (Tobin’s Q) and operating cost (Cost) were significant at a confidence level of 99%, with correlation coefficients of 0.033 and −0.067, respectively. This indicates that listed companies can improve their financial performance by improving the information symmetry level and reducing the operating cost ratio.

Table 4.

Correlation analysis results.

4.3. Diagnostic Test

- (1)

- Multicollinearity Test

It is necessary to judge whether the explanatory variables have multicollinearity to ensure the accuracy of the model, shown in Table 5. According to the rule of thumb, there was no multicollinearity between variables.

Table 5.

Multicollinearity test results.

- (2)

- Unit root test

To test whether the data were stable, we used Fisher’s test method to test the unit root of the data used in the model. The test results indicate that all variables in this study passed the unit root test and were stationary variables without a unit root.

- (3)

- Hausman test

To verify the fixed effect and random effect and to choose between the two models, we conducted the Hausman test on the model. The results showed that p = 0.0000. Hence, the original hypothesis was rejected, and the fixed-effect model was selected.

- (4)

- F-test

To determine whether to use the mixed regression model or the fixed-effect model, we conducted an F-test on the model to verify whether the model belonged to the individual or time-fixed effect or individual-time bidirectional fixed-effect model through an F-test. The results showed that p = 0.0000, indicating that the model is the individual-time bidirectional fixed-effect model.

4.4. Regression of the Total Effect Model

The regression results of Model 1 are shown in Table 6. Controlling for variables such as company size (size), operating income (Oi), operating cash flow (Ocf), the share-holding ratio of the largest shareholder (Fir), property right nature (Stc), the asset liability level (Deb), and the audit report nature (Aud), the regression coefficient of financial digital transformation (Dig) is 0.011, which is significantly positive at a confidence level of 99%. Hence, the financial digital transformation positively influences corporate financial performance, and financial performance grows by 1.1% for every 1% increase in the degree of financial digital transformation, which verifies Hypothesis 1.

Table 6.

Effect of financial digital transformation on financial performance: principal regression.

4.5. Mediation Effect Test

4.5.1. Information Symmetry Level

The regression results of Model 2 are presented in Table 7. According to column (1)’s regression coefficient for financial digital transformation (Dig), which is 0.151 and statistically significant at the 99% level of confidence, financial digital transformation may greatly raise the degree of information symmetry in businesses. The information symmetry level grows by 15.1% for each 1% increase in the degree of financial digital transformation. In column (2), information symmetry level (Inf) and financial performance (Tobin’s Q) are significantly positively correlated at the 99% confidence level, and financial digital transformation (Dig) and financial performance (Tobin’s Q) are significantly positively correlated at the 95% confidence level. Moreover, in column (2), the regression coefficient of financial digital transformation is 0.008, which is less than 0.011 in Table 6. Therefore, this proves Hypothesis 2 because the information symmetry level acts as a positive and partial intermediate in the financial digital transformation process that influences financial performance.

Table 7.

Intermediary effect test of financial digital transformation on financial performance: information symmetry.

4.5.2. Operating Cost

The regression results of Model 3 are presented in Table 8. In column (1), the regression coefficient of financial digital transformation (Dig) was −0.008, demonstrating that the operational cost rate can be substantially reduced via financial digital transformation. The operating cost rate of companies decreases by 0.8% for every 1% increase in the degree of financial digital transformation. In column (2), the operating cost rate (cost) is significantly negatively correlated with corporate financial performance (Tobin’s Q) at a confidence level of 99%, and the financial digital transformation (Dig) is significantly positively correlated with corporate financial performance (Tobin’s Q) at a confidence level of 99%. In addition, the financial digital transformation regression coefficient in column (2) is 0.010, which is lower than the value in Table 6. Therefore, operating expenses confirm Hypothesis 3 by acting as a negative and partially intermediate factor in the financial digital transformation process that affects company financial performance.

Table 8.

Intermediary effect test of financial digital transformation on financial performance: operating cost.

Table 9 shows the influence of the information symmetry level on the operating cost rate. After controlling for the company size (size), operating income (Oi), operating cash flow (Ocf), shareholding ratio of the largest shareholder (Fir), property right nature (Stc), asset–liability level (Deb), and audit report nature (Aud), the return coefficient of information symmetry level (Inf) is −0.023, which is significantly negative at the confidence level of 99%. Hypothesis 4 is supported by the finding that for every 1% rise in information symmetry level, the operational cost rate falls by 2.3%.

Table 9.

Effect of influence disclosure on operating cost.

4.6. Endogenous Tests

To prevent endogenous issues, the two-stage least squares approach is used in this research. The endogenous test employed the data from the three financial digital transformation lag three periods (Dig lag three periods) as instrumental variables [20,52], as indicated in Table 10. After the addition of instrumental variables, the regression coefficient of financial digitalization transformation on corporate financial performance is 0.298, which is quite optimistic at the 95% level of confidence. When digital transformation in the finance department is increased by only 1%, corporate financial performance improves by 29.8%. This regression coefficient of 0.298 is greater than 0.011 in Table 10, suggesting that financial digital transformation is the reason for financial performance growth and the effect of digital financial transformation on financial results grows over time. In addition, there are some practical cases to illustrate this phenomenon. The Huawei Technology company set up a financial sharing service center in 2005. At this time, the operating profit margin was 14%. By 2008, the operating profit margin fell to 12.90%, and by 2009, the operating profit margin rose to 14.10%. In Table 10, the p value of the Anderson canon. corr. LM static, which passes the unrecognisability test, is 0.000, indicating that the instrumental variables are related to the explanatory variables, and it makes more sense to choose instrumental variables. They pass the weak instrumental variable test. The F value in the first phase of the 2SLS is 16.09, indicating that the instrumental variables selected in this study are not weak.

Table 10.

Endogenous test results.

4.7. Heterogeneity Analysis

The sample companies are divided into ones in the eastern, central, or western provinces according to their geographical locations to test the heterogeneity of the empirical results of the financial digitalization transformation of A-share listed firms influencing their corporate financial performance. This allows us to explore whether the financial digital transformation has a different influence on corporate financial performance under various conditions. Table 11 displays the outcomes of the regression analysis, in which column (1) shows the companies with headquarters from the eastern provinces of China, and column (2) shows those with headquarters from provinces in the middle and to the west. When looking at the percentage of enterprises in the eastern provinces that have undergone a financial digital transformation (Dig), the coefficient in column (1) is 0.006, which is statistically significant at the 90% level. One may be certain that the transition to digital finance (Dig) in the (2) central and western provinces in column (2) is substantial at the 99% level due to the Dig coefficient of 0.02. The results indicate that compared with the companies in eastern provinces, those in central and western provinces can improve their financial performance better through financial digital transformation. The major cause of this is the extreme commercialization of the coastal regions to the east, so the growth of financial performance brought by the financial digital transformation has a marginal diminishing effect. In contrast, companies in the central and western regions need deeper financial digital transformations to improve their financial performance.

Table 11.

Heterogeneity analysis results.

4.8. Robustness Test

To assess the robustness of the findings and assess the consistency and durability of the results, a robustness test was conducted by replacing the indicators used to assess the variables in Table 12. Building on the research of Salim and Yadav, Farza et al., Tenuta and Cam-brea, and Saridakis et al. [53,54,55,56], Tobin’s Q value was replaced by return on assets (ROA) as the explanatory variable, and panel data were once again utilized for individual-time bidirectional fixed-effect. The regression coefficient for financial digital transformation (Dig) and ROA were found to be significantly positive at a confidence level of 95%, with a coefficient of 0.012. The results of the robustness check indicate that financial digital transformation positively affects corporate financial performance.

Table 12.

Robustness check results.

5. Conclusions

China’s digital strategy places a heavy emphasis on the digitization of financial services, a cornerstone of the country’s emerging digital economy, and has played a vital role in boosting China’s economy. In this study, combined with the text mining method, the panel data regression model, and the intermediary effect test, research into the connection between financial digital transformation and corporate financial performance was conducted using data from China’s A-share listed companies. The data also allowed for the investigation of the mediating effect of the information symmetry level and operating cost. The validity of the findings was verified by means of an endogenous test and a robustness test.

5.1. Theoretical Implications

For A-share listed companies, financial digital transformation can effectively improve their financial performance permanently. First, based on a finance shared service model, financial digital transformation aims to alleviate the limitations of traditional financial management models on the development of modern companies, optimize the financial management process, change the internal employment structure, and reduce the total scale and share of labour costs of digital technologies, thus improving the operating profits of the companies. Second, during financial digital transformation, companies can effectively obtain internal and external information via the sharing platform, helping them strengthen their internal control power, realize dynamic management, absorb a large number of professional and external institutional investors, and effectively empower companies to innovate, thus improving their core business performance. Third, in the big data environment, with the help of carrying out financial innovation and transformation and establishing a big data financial system, companies can promote the transformation of financial management to a decision-support type, improve decision-making efficiency, and reduce default risk.

According to the transmission intermediary way, the information symmetry level has partial intermediary effects in the relationship between financial digital transformation and corporate financial performance; that is, financial digital transformation improves corporate financial performance by improving the information symmetry level and reducing operating costs. For the information symmetry level, on the one hand, companies should integrate digital technologies into financial information management, build a financial sharing center, integrate the business processes carried by many information systems, and constantly strengthen rules and standards. This helps them effectively collect, screen, and apply internal information; improve the communication speed between the finance department and various businesses; and enhance companies’ management efficiency. On the other hand, companies communicate with stakeholders via the financial sharing center more frequently so that external market information can be summarised into the strategic layout and daily management of companies in a high-density and efficient manner. This helps them make investment and financing decisions, formulate strategies, and participate in market competition more accurately. In addition, based on the signal transmission theory, the financial digital transformation of companies will also signal that they have a promising development prospect to attract investment so that they can obtain more external financing to expand production and gain more profits.

Regarding operating costs, the external environment can be effectively improved. Effectively overcoming regional cultural differences, language barriers, and national differences; reducing the cost of communication and cooperation between companies; facilitating communication; lowering cross-border costs; quickly collecting large user data from multiple dimensions to achieve accurate positioning and marketing to users; and reducing marketing costs are all made possible through a company’s digital transformation. Moreover, digital transformation is conducive to reducing the costs of companies moving in ground space and realizing the combination of low cost and high income. Internally, by using digital technologies, companies can optimize existing business processes; achieve more effective cross-process coordination to reduce relevant costs; generate and utilize internal data information in a more complete and accurate way; and continuously integrate personnel, businesses, and activities scattering in the past, thus reducing various internal management costs and improving corporate performance.

This study considers that the discrepancies in the geographical conditions of companies may have different effects on the improvement of corporate financial performance, to empirically examine the impact of financial digital transformation on company financial performance. The sample firms are split between the eastern and central and western regions. Compared with the companies in the eastern provinces, those in the central and western provinces can improve their financial performance better through financial digital transformation. The main reason is that marketization has reached a high level in the eastern coastal areas, so the growth of financial performance brought by financial digital transformation has a marginal diminishing effect. However, in order to boost their financial performance, enterprises in the central and western areas need to undergo a more extensive financial digital transformation.

5.2. Economic Implications

First, against the backdrop of “industry digitalization” in China, financial digital transformation possesses immense potential for future value creation among enterprises. Therefore, companies ought to endeavour to seize policy opportunities, establish reasonable transformation strategies based on their own resource conditions, and systematically promote the process of financial digital transformation to stimulate the enhancement of financial performance.

Second, companies should place a high value on the construction of data processing and analysis capabilities. In the face of the explosive growth of data, businesses require not only the ability to collect real-time data rapidly but also the ability to process and analyze such data quickly and accurately, transforming it into useful information that supports decision-making. By doing so, they can reduce the cost of obtaining effective information, improve the information transparency of the enterprise, and ultimately enhance its competitiveness.

Third, companies should place a great deal of importance on the synergy between digital technology and the original production process. In the course of financial digital transformation, the introduction of digital technology can alter the relationship between the original production processes of companies, potentially resulting in imbalanced resource allocation and wastage. Therefore, it is crucial for businesses to pay close attention to the collaboration between financial digital technology and the original production process, accelerating the integration of digital technology with the original business process, work mode, and organization mode. By doing so, they can achieve overall resource optimization across business fields and links, reducing the operating costs of the enterprise.

Fourth, companies should prioritize the digitalization of business models and production processes. Financial digital transformation can enhance the financial performance of companies by optimizing the operation mode or production process. Businesses should take into account their own unique characteristics and choose an appropriate transformation path, whether it involves the digitalization of their business model or production process, or a combination of the two, while leveraging information technology and digital innovation to amplify their impact.

5.3. Policy Recommendations

First, at present, China’s listed companies lack a clear understanding of the financial digitization construction standard. It is recommended that the financial department should take the lead in involving companies and various financial and accounting experts and develop an institutional system for data standards, data collection, data transaction, data sharing, and data security, in the construction of financial digitization. The financial department should guide companies in implementing financial digital transformation reasonably and effectively, in accordance with the system standards.

Second, financial digital transformation necessitates significant capital investment. Apart from funds generated through the company’s own finances and external financing, government departments could leverage the catalytic role of government funds, providing tax incentives, special funds, or supporting funds. Meanwhile, government departments should establish an evaluation and tracking accountability mechanism for the impact of government funds, in order to maximize the efficiency of government capital investment and usage.

Third, there is a widespread scarcity of management personnel and professionals for financial digitization in Chinese companies. As the financial digital transformation of businesses continues to develop, the corresponding demand for financial professionals with digital capabilities has risen sharply. In the future, the financial department will require more comprehensive talents who possess knowledge of both finance and technology. Therefore, the Chinese government could focus on the cultivation of financial digital professionals, building up a reserve of talented individuals in this field.

Fourth, in the context of the rapid development of the digital economy and common prosperity, it is very important to accelerate the development of the central and western regions. Most of the eastern regions are developed cities close to the coast. The capital market is mature, the talent and technology are intensive, and the financial resources are abundant. On the contrary, the financial digital transformation in the central and western regions is still at a low level, due to the shortage of funds, talents, and technology. Therefore, the government should strengthen the infrastructure construction of financial digital transformation in the central and western regions, actively promote the cooperation between the government and enterprises in the field of digitalization, encourage enterprises to develop digital technology, use financial digital transformation to improve the current situation of low production efficiency, and alleviate the imbalance of regional development to a certain extent.

5.4. Limitations and Future Directions

This study seeks to address and bridge the knowledge gap concerning the relationship between financial digital transformation and corporate financial performance, using theoretical analysis and empirical analysis. Nonetheless, there are some limitations: First, with respect to the sample data, this study only employs data from China’s A-share listed companies from 2012 to 2021 for empirical testing, but the effect of financial digital transformation on enterprises needs to be observed over a certain period. Therefore, this study may have the issue of a short analysis period, resulting in research bias. Second, regarding the mechanism, this study only considers the two intermediary effects of information symmetry level and operating cost rate. However, the effect mechanism of financial digital transformation on enterprise financial performance is complex, and there are numerous unexplored mechanisms. There are two directions for further research. First, we will gather data over a longer time span to identify the diverse and dynamic correlation between financial digital transformation and corporate financial performance. Second, we will explore additional intermediary paths through which financial digital transformation impacts corporate financial performance.

Author Contributions

Conceptualization, J.L.; data curation, Y.Z.; formal analysis, J.L. and Y.Z.; funding acquisition, J.L. and Y.Z.; investigation, Y.Z.; methodology, J.L. and K.Z.; project administration, J.L. and F.T.; software, K.Z.; supervision, J.L. and F.T.; validation, F.T.; writing—original draft, J.L.; and writing—review & editing, Y.Z. and F.T. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by the Beijing Social Science Foundation grant number 20GLC040.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data that support the findings of this study are openly available from financial reports publicly disclosed by the CNINF website and the China Stock Market and Accounting Research Database (CNINF website: http//www.cninfo.com.cn (accessed on 17 January 2023)).

Conflicts of Interest

The authors declare no conflict of interest.

References

- Kane, G.C.; Palmer, D.; Phillips, A.N.; Kiron, D.; Buckley, N. Strategy, not technology, drives digital transformation. MIT Sloan Manag. Rev. 2015, 14, 302–314. [Google Scholar]

- Kraus, S.; Durst, S.; Ferreira, J.J.; Veiga, P.; Kailer, N.; Weinmann, A. Digital transformation in business and management research: An overview of the current status quo. Int. J. Inf. Manag. 2022, 63, 102466. [Google Scholar] [CrossRef]

- Zoppelletto, A.; Orlandi, L.B.; Zardini, A.; Rossignoli, C.; Kraus, S. Organizational roles in the context of digital transformation: A micro-level perspective. J. Bus. Res. 2023, 157, 113563. [Google Scholar] [CrossRef]

- Ancillai, C.; Sabatini, A.; Gatti, M.; Perna, A. Digital technology and business model innovation: A systematic literature review and future research agenda. Technol. Forecast. Soc. Chang. 2023, 188, 122307. [Google Scholar] [CrossRef]

- Chen, Y.; Xu, J. Digital transformation and firm cost stickiness: Evidence from China. Financ. Res. Lett. 2023, 52, 103510. [Google Scholar] [CrossRef]

- Peng, Y.; Tao, C. Can digital transformation promote enterprise performance?—From the perspective of public policy and innovation. J. Innov. Knowl. 2022, 7, 100198. [Google Scholar] [CrossRef]

- Zhang, Y.; Ma, X.; Pang, J.; Xing, H.; Wang, J. The impact of digital transformation of manufacturing on corporate performance—The mediating effect of business model innovation and the moderating effect of innovation capability. Res. Int. Bus. Financ. 2023, 64, 101890. [Google Scholar] [CrossRef]

- Zeng, H.; Ran, H.; Zhou, Q.; Jin, Y.; Cheng, X. The financial effect of firm digitalization: Evidence from China. Technol. Forecast. Soc. Chang. 2022, 183, 121951. [Google Scholar] [CrossRef]

- Niu, Y.; Wen, W.; Wang, S.; Li, S. Breaking barriers to innovation: The power of digital transformation. Financ. Res. Lett. 2023, 51, 103457. [Google Scholar] [CrossRef]

- Lo, D.; Gao, L.; Lin, Y. State ownership and innovations: Lessons from the mixed-ownership reforms of China’s listed companies. Struct. Chang. Econ. Dyn. 2022, 60, 302–314. [Google Scholar] [CrossRef]

- Zhang, D.; Zheng, W. Does COVID-19 make the firms’ performance worse? Evidence from the Chinese listed companies. Econ. Anal. Policy 2022, 74, 560–570. [Google Scholar] [CrossRef] [PubMed]

- Battisti, E.; Alfiero, S.; Leonidou, E. Remote working and digital transformation during the COVID-19 pandemic: Economic–financial impacts and psychological drivers for employees. J. Bus. Res. 2022, 150, 38–50. [Google Scholar] [CrossRef]

- Gaglio, C.; Kraemer-Mbula, E.; Lorenz, E. The effects of digital transformation on innovation and productivity: Firm-level evidence of South African manufacturing micro and small enterprises. Technol. Forecast. Soc. Chang. 2022, 182, 121785. [Google Scholar] [CrossRef]

- Wu, L.; Sun, L.; Chang, Q.; Zhang, D.; Qi, P. How do digitalization capabilities enable open innovation in manufacturing enterprises? A multiple case study based on resource integration perspective. Technol. Forecast. Soc. Chang. 2022, 184, 122019. [Google Scholar] [CrossRef]

- Liu, M.; Li, C.; Wang, S.; Li, Q. Digital transformation, risk-taking, and innovation: Evidence from data on listed enterprises in China. J. Innov. Knowl. 2023, 8, 100332. [Google Scholar] [CrossRef]

- Ning, J.; Jiang, X.; Luo, J. Relationship between enterprise digitalization and green innovation: A mediated moderation model. J. Innov. Knowl. 2023, 8, 100326. [Google Scholar] [CrossRef]

- Plattfaut, R.; Borghoff, V.; Godefroid, M.; Koch, J.; Trampler, M.; Coners, A. The critical success factors for robotic process automation. Comput. Ind. 2022, 138, 103646. [Google Scholar] [CrossRef]

- Gradim, B.; Teixeira, L. Robotic Process Automation as an enabler of Industry 4.0 to eliminate the eighth waste: A study on better usage of human talent. Procedia Comput. Sci. 2022, 204, 643–651. [Google Scholar] [CrossRef]

- Tian, G.; Li, B.; Cheng, Y. Does digital transformation matter for corporate risk-taking? Financ. Res. Lett. 2022, 49, 103107. [Google Scholar] [CrossRef]

- Wu, K.; Fu, Y.; Kong, D. Does the digital transformation of enterprises affect stock price crash risk? Financ. Res. Lett. 2022, 48, 102888. [Google Scholar] [CrossRef]

- Miller, H.G.; Mork, P. From data to decisions: A value chain for big data. It Prof. 2013, 15, 57–59. [Google Scholar] [CrossRef]

- Zeng, J.; Glaister, K.W. Value creation from big data: Looking inside the black box. Strateg. Organ. 2018, 16, 105–140. [Google Scholar] [CrossRef]

- Akhtar, P.; Frynas, J.G.; Mellahi, K.; Ullah, S. Big data-savvy teams’ skills, big data-driven actions and business performance. Br. J. Manag. 2019, 30, 252–271. [Google Scholar] [CrossRef]

- Charles, I.J.; Christopher, T. Nonrivalry and the economics of data. Am. Econ. Rev. 2020, 110, 2819–2858. [Google Scholar]

- Feliciano-Cestero, M.M.; Ameen, N.; Kotabe, M.; Paul, J.; Signoret, M. Is digital transformation threatened? A systematic literature review of the factors influencing firms’ digital transformation and internationalization. J. Bus. Res. 2023, 157, 113546. [Google Scholar] [CrossRef]

- Yu, M.; Debo, L.; Kapuscinski, R. Strategic waiting for consumer-generated quality information: Dynamic pricing of new experience goods. Manag. Sci. 2016, 62, 410–435. [Google Scholar] [CrossRef]

- Herala, A.; Kokkola, J.; Kasurinen, J.; Vanhala, E. Strategy for Data: Open it or hack it? J. Theor. Appl. Electron. Commer. Res. 2019, 14, 33–46. [Google Scholar] [CrossRef]

- Aral, S.; Weill, P. IT assets, organizational capabilities, and firm performance: How resource allocations and organizational differences explain performance variation. Organ. Sci. 2007, 18, 763–780. [Google Scholar] [CrossRef]

- Kazan, E.; Tan, C.W.; Lim, E.T. Towards a framework of digital platform competition: A comparative study of monopolistic & federated mobile payment platforms. J. Theor. Appl. Electron. Commer. Res. 2016, 11, 50–64. [Google Scholar]

- Hajli, M.; Sims, J.M.; Ibragimov, V. Information technology (IT) productivity paradox in the 21st century. Int. J. Product. Perform. Manag. 2015, 64, 457–478. [Google Scholar] [CrossRef]

- Diamond, D.W. Optimal release of information by firms. J. Financ. 1985, 40, 1071–1094. [Google Scholar] [CrossRef]

- Guo, L.; Xu, L. The effects of digital transformation on firm performance: Evidence from China’s manufacturing sector. Sustainability 2021, 13, 12844. [Google Scholar] [CrossRef]

- Stefanovic, N.; Barjaktarovic, L.; Bataev, A. Digitainability and financial performance: Evidence from the Serbian banking sector. Sustainability 2021, 13, 13461. [Google Scholar] [CrossRef]

- Teng, X.; Wu, Z.; Yang, F. Research on the relationship between digital transformation and performance of SMEs. Sustainability 2022, 14, 6012. [Google Scholar] [CrossRef]

- Wang, S.; Wang, H.; Wang, J.; Yang, F. Does environmental information disclosure contribute to improve firm financial performance? An examination of the underlying mechanism. Sci. Total Environ. 2020, 714, 136855. [Google Scholar] [CrossRef]

- Hassel, L.; Nilsson, H.; Nyquist, S. The value relevance of environmental performance. Eur. Account. Rev. 2005, 14, 41–61. [Google Scholar] [CrossRef]

- Hammer, M. Reengineering work: Don’t automate, obliterate. Harv. Bus. Rev. 1990, 68, 104–112. [Google Scholar]

- Hammer, M.; Champy, J. Reengineering the corporation: A manifestor for business revolution. Bus. Horizons 1993, 36, 91. [Google Scholar] [CrossRef]

- Grover, V. Business process change: Reengineering concepts, methods and technologies. Long Range Plan. 1996, 4, 593–594. [Google Scholar] [CrossRef]

- Resca, A.; Za, S.; Spagnoletti, P. Digital platforms as sources for organizational and strategic transformation: A case study of the Midblue project. J. Theor. Appl. Electron. Commer. Res. 2013, 8, 71–84. [Google Scholar] [CrossRef]

- Hitpass, B.; Astudillo, H. Industry 4.0 challenges for business process management and electronic-commerce. J. Theor. Appl. Electron. Commer. Res. 2019, 14, 1–3. [Google Scholar] [CrossRef]

- Pagani, M.; Pardo, C. The impact of digital technology on relationships in a business network. Ind. Mark. Manag. 2017, 67, 185–192. [Google Scholar] [CrossRef]

- Nadeem, A.; Abedin, B.; Cerpa, N.; Chew, E. Digital transformation & digital business strategy in electronic commerce-The role of organizational capabilities. J. Theor. Appl. Electron. Commer. Res. 2018, 13, 1–8. [Google Scholar]

- Mavlutova, I.; Spilbergs, A.; Verdenhofs, A.; Natrins, A.; Arefjevs, I.; Volkova, T. Digital transformation as a driver of the financial sector sustainable development: An impact on financial inclusion and operational efficiency. Sustainability 2022, 15, 207. [Google Scholar] [CrossRef]

- Verhoef, P.C.; Broekhuizen, T.; Bart, Y.; Bhattacharya, A.; Dong, J.Q.; Fabian, N.; Haenlein, M. Digital transformation: A multidisciplinary reflection and research agenda. J. Bus. Res. 2021, 122, 889–901. [Google Scholar] [CrossRef]

- Tiefenbeck, V. Bring behaviour into the digital transformation. Nat. Energy 2017, 2, 17085. [Google Scholar] [CrossRef]

- Stroumpoulis, A.; Kopanaki, E. Theoretical perspectives on sustainable supply chain management and digital transformation: A literature review and a conceptual framework. Sustainability 2022, 14, 4862. [Google Scholar] [CrossRef]

- Foster, B.P.; Manikas, A.; Preece, D.; Kroes, J.R. Noteworthy diversity efforts and financial performance: Evidence from DiversityInc’s top 50. Adv. Account. 2021, 53, 100528. [Google Scholar] [CrossRef]

- Naeem, N.; Cankaya, S.; Bildik, R. Does ESG performance affect the financial performance of environmentally sensitive industries? A comparison between emerging and developed markets. Borsa Istanb. Rev. 2022, 22 (Suppl. 2), S128–S140. [Google Scholar] [CrossRef]

- Kahloul, I.; Sbai, H.; Grira, J. Does corporate social responsibility reporting improve financial performance? The moderating role of board diversity and gender composition. Q. Rev. Econ. Financ. 2022, 84, 305–314. [Google Scholar] [CrossRef]

- Rahman, M.; Faroque, A.R.; Sakka, G.; Ahmed, Z.U. The impact of negative customer engagement on market-based assets and financial performance. J. Bus. Res. 2022, 138, 422–435. [Google Scholar] [CrossRef]

- Hu, Y.; Che, D.; Wu, F.; Chang, X. Corporate maturity mismatch and enterprise digital transformation: Evidence from China. Financ. Res. Lett. 2023, 103677. [Google Scholar] [CrossRef]

- Salim, M.; Yadav, R. Capital structure and firm performance: Evidence from Malaysian listed companies. Procedia-Soc. Behav. Sci. 2012, 65, 156–166. [Google Scholar] [CrossRef]

- Farza, K.; Ftiti, Z.; Hlioui, Z.; Louhichi, W.; Omri, A. Does it pay to go green? The environmental innovation effect on corporate financial performance. J. Environ. Manag. 2021, 300, 113695. [Google Scholar] [CrossRef] [PubMed]

- Tenuta, P.; Cambrea, D.R. Corporate social responsibility and corporate financial performance: The role of executive directors in family firms. Financ. Res. Lett. 2022, 50, 103195. [Google Scholar] [CrossRef]

- Saridakis, C.; Angelidou, S.; Woodside, A.G. How historical and social aspirations reshape the relationship between corporate financial performance and corporate social responsibility. J. Bus. Res. 2023, 157, 113553. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).