Abstract

Currently, the military actions on the territory of Ukraine require significant support from EU countries and partners in providing military and material assistance. The issue of openness and transparency of budgeting, particularly in the defence and security sector, becomes even more significant. The peak of interest in the literature on the issues of openness and transparency of budgeting appeared in 2005–2006. However, in Ukraine, which has largely continued to follow Soviet trends, this is an alarming subject. It has been brought to the forefront by the events after the full-scale invasion of the Russian Federation. One of the ways to guarantee the openness and transparency of budgeting is the development of a suitable open data system, which includes the analysis of all financial costs based on the proper methodology. Such a methodology should be founded on the concept of assessing the openness and transparency of budgeting and financial management of the defence and security sector of Ukraine at the current stage in the conditions of war and, after it, be measured quantitatively and implemented using IT. This article aims to consider the methodology of an index of openness and transparency of budgeting and financial management of the defence and security sector and to implement it in the case of Ukraine. Based on the conducted literature review, a new method to calculate the index of openness and budgeting transparency of the defence and security sector of Ukraine is built. Nine separate indicators are defined, and each of them affects the final value of the index. Some indicators have a binary form, and some have a scale, which is used to estimate their specific weight of impact. This approach makes it possible not only to monitor the openness and transparency of the defence and security sector but also to show the dynamics of the development of the phenomenon and compare it, in the future, with other countries. Based on calculations for 2008–2021, the trend of this index is shown for Ukraine, and conclusions are made regarding its further application.

1. Introduction

The history of Russia is a history of constant wars and conquests of neighbouring territories. For example, only in the 19th century this country captured the territories of modern Georgia, Azerbaijan, Armenia, Finland, Kazakhstan, Kyrgyzstan, Uzbekistan, Tajikistan, Sakhalin, Turkmenistan, Inner Mongolia, Tyva, part of Prussia, Austria, Dagestan, Amur Krai, Khabarovsk Krai, and a large part of Poland. As a rule, the capture was carried out by military means, after which puppet rulers were appointed, who “voluntarily” made the territory part of the empire. At the beginning of the 20th century, the situation was not favourable for new conquests because Russia was mainly losing territories in the first quarter of the century. In particular, Finland, Poland, Lithuania, Latvia, Estonia, part of Ukraine, and Belarus were lost. However, as early as 1934, operations to change the governments of neighbouring countries began. For example, this year, a communist government was established in Xinjiang; later, during the Second World War, the territories of modern-day Ukraine and Belarus, as well as Lithuania, Latvia, Estonia, and part of Finland were captured, and control was established over Poland, Czechoslovakia, Hungary, Albania, Yugoslavia, Romania, part of Germany, and part of Japan. The bloody world war did not stop Russia’s aggressive policy. In 1956, 1968, and 1979 Russian (i.e., Soviet) troops invaded Poland, Czechoslovakia, and Afghanistan, intending to establish the desired puppet government.

The collapse of the Soviet Union in 1991 significantly reduced the volume of the controlled territory, and a significant part of the gains of the 19th century was lost. However, since 1992, Russia has returned to its favourite business—seizing neighbouring states. The Finnish scheme remained the main one, which was tested in 1940; Saboteurs took over any settlement where a certain public republic was proclaimed, which meant the beginning of a “civil war” in which Russia intervened in various ways. In 1991–1993, Russia made a part of Georgia (South Ossetia) a puppet state; Abkhazia in 1992; a part of Moldova (the Transnistrian Republic) in 1999, and captured Ichkeria in 2008.

In 2014, Russia committed another act of aggression by seizing the Autonomous Republic of Crimea and creating a puppet entity in the Donbas of Ukraine. The non-recognition of the annexation of the territory led to an open invasion of Ukraine in 2022. Unfortunately, it must be acknowledged that no political solution guarantees Ukraine safety after the war. Even the possible accession to the EU, the status of which Ukraine received as a candidate in 2022, does not guarantee the impossibility of a repeated invasion because the aggressiveness of the northern neighbour has not decrease in any way. The war showed that even participation in various organizations would not guarantee the assistance or participation of other countries in military operations. It is obvious that the only means of protection remain to be the Ukrainian armed forces and diplomacy. It is the combination of the two that makes it possible to repel aggression and receive joint actions from allies.

Today, the armed forces of Ukraine defend the country with the help of weapons received through diplomacy. An effective army protects the people of Ukraine and strengthens Ukraine’s position in the international arena, gathering the allies in one solid alliance, revealing the opposition and alliances of Russia. For the army to be strong and staffed, effective budgeting should be developed, which will prevent corruption risks in the future or inefficient use of funds. Therefore, it is currently becoming obvious that the expected efficiency of the Ukrainian army can be drawn from the openness and transparency of budgeting.

One of the ways to guarantee the openness and transparency of budgeting is the development of an appropriate open information system, which includes the analysis of all financial costs based on the appropriate methodology. Such a methodology should be based on assessing the openness and transparency of budgeting and the financial management of Ukraine’s defence and security sector at the current stage in the conditions of the war as well, after it, which should be quantitatively measured and implemented programmatically. Considering the reporting structure of the State Treasury of Ukraine, it is best to conduct a quantitative analysis of indicators with a quarterly and annual frequency of data. It is desirable to implement an automatic system for updating and recalculating all data in the information system without human intervention to avoid corruption risks.

Such a study is aimed at determining the indicators of sustainable governance, their components and characteristics. The use of appropriate metrics provides an opportunity for the continuous monitoring and auditing of state activities in the defence sector and the introduction of a risk management system, which significantly reduces opportunities for corruption risks. The latter is very relevant for Ukraine due to its significant dependence on the supply of weapons and supplies from EU countries and the USA, which requires maximum transparency in front of partners. Any reports of non-transparent use of funds or resources may cause a significant reduction in assistance.

Thus, the purpose of this paper is to propose a concept for the methodology to assess the openness and transparency of budgeting and the financial management of the defence and security sector of Ukraine in the conditions of war and after it, which will help Ukraine meet EU membership requirements and ensure the proper use of funds for its allies. The structure of the paper conforms to the logic of its task. Based on the literature review of best practices in the field, the methodology is drawn by the authors. Then, it is implemented on the broad time series of Ukrainian statistics. The conclusion and discussion consider the possible yield of the approach to the cross-country comparisons and highlight the possible milestones of it.

2. Literature Review

To achieve the goal of the research, scientific sources considering the issues of openness and transparency of budgeting in the defence sector are critically reviewed.

The Google Trends analysis shows that the peak of interest among Internet users in budget transparency was observed in 2005–2006. The frequency of publication of Scopus articles on budget transparency proves that this issue remains quite popular among academics. In particular, the issue of budget transparency is closely linked in research with economic prosperity, sustainability at the national and local levels, the elimination of poverty, responsibility for the environment, the implementation of democratic values, the fight against corruption, effective management, and especially the effectiveness of public finances [1].

An index of budget transparency was developed in Lithuania [2] based on 20 indicators, 13 of which related to the stage of budget preparation and 7 to their implementation. Based on the analysis of the obtained index, the author concluded that the budget’s transparency level is influenced not only by economic and political factors. In particular, the author concluded that the percentage of the population living in rural areas, turnout in local elections, per capita income, and the level of intergovernmental subsidies are negatively related to the transparency of the budget, while the level of debt, on the contrary, is positively related to the level of transparency.

Military spending has broad security implications and long-term development implications. Thus, spending in the military sector requires careful analysis, taking into account important considerations related to the openness of information by government institutions, both internally and when interacting with the public. However, military spending decisions are often classified and may be based on ill-founded security policies. In the SIPRI paper (2018) [3], the level of openness of the defence budget are assessed based on the national reporting of selected African countries considering five key criteria: information availability, completeness, ease of access, reliability, and disaggregation. The study was conducted based on data from 2012 to 2017 with data from 47 African countries.

Citro et al. (2021) [4] analyse various factors that can affect the level of budget transparency. Based on the analysis of 95 countries in five periods it was indicated that increasing the efficiency of the budget system requires certain characteristics of both the government and the electoral/political systems. Therefore, reforms to these systems may limit their opacity intentions, and supervisors may be encouraged to consider political conditions that may exert pressure to make budget processes public. The results highlight the importance of the relationship between fiscal transparency and public sector reforms, particularly by influencing the political characteristics of government and the institutional rules that govern them. Thus, the war in Ukraine and the expediency of the secrecy of information can cause significant changes to both the political system and the principles of budgetary openness.

Scientists note that the process of drawing up the military budget and procurement must strictly adhere to the national practice of financial management and auditing, that is, strict adherence to the principles of public expenditure management, completeness of information, discipline in the implementation of plans, legitimacy, flexibility, predictability, competitiveness, honesty, information, transparency, constant monitoring, openness, and accountability [5].

In 2016, the foundations of initiatives and practices created to solve defence budget transparency tax issues are indicated [6]. The paper measured the transparency of the defence budget and developed a five-point scale: low, below average, average, above average, and high level. The study was conducted within the framework of the budget openness initiative, which is primarily determined through the budget openness index. The index is the most comprehensive assessment of national budget processes and budget transparency worldwide. The index includes 93 countries, which were analysed using a survey. The questionnaire contained seven questions related to defence and security.

Questions 1–3. Countries received 1 point for making each required document publicly available and 0 if they did not. The executive budget statement, the enacted budget, and the audit report are three key documents that allow the public to scrutinise their government’s spending.

Questions 4 and 5. Countries can score between 0 and 3 points, depending on the percentage of spending in the budget year that is directed toward spending on classified items related to national security and military intelligence, the level of classified spending and defence, and providing the legislature with full information for the budget year on the spending of all classified items related to national security and military intelligence.

Questions 6 and 7. Countries can score between 0 and 3, but the scores for these questions were averaged, so having an audit available to the legislature did not affect the overall score much. In particular, the issues of recruitment by the supreme control body of personnel appointed to conduct audits of central state bodies related to the security sector (military, police, and intelligence services) were analysed. The provision of the audit reports on the annual reports of the security sector (military, police, and intelligence services) and other secret programs to the legislature was also analysed.

The scores for questions 1, 2, 3, 4, and 5 and the mean for questions 6 and 7 were added together. The highest score was 12, and the worst was 0.

The rating was compiled according to this numerical rating system: 0–2—low level; 2.1–4.5—below average; 4.6–7—average; 7.1–9.5—above average; 9.6–12—high.

The results of the study indicate that approximately 14% of the countries considered in this study have a high level of openness. They primarily include developed countries with strong democratic systems. The average level is 21.5% of countries, in particular, various countries in Africa, Asia, Europe, and Latin America. The other nearly 65 per cent of countries have a low level of openness.

In the Transparency International Defence & Security Strategy 2021–2023 [7], the theory of changes of “political windows” was used, which aims to identify the problem of corruption in the defence and security sector, develop policy options to reduce the risks of corruption, and the ability to influence the political climate. This approach is consistent with recent research on how corruption control is most likely to be achieved. It also builds on current trends in broader management programming, emphasizing the adaptation of programs to current political economies or contextual analysis and the building of broad coalitions and collective action.

In the Defence Industry Influence on European Policy Agendas [8], the authors draw the main conclusions from two case studies on the impact of the defence industry on the defence and security policy in Germany and Italy. They pointed out that Germany has a rather complex system of strategic defence formation, but the reduction in the civil service and its powers has shifted too much of the responsibility on technical experts and advisers. Meanwhile, Italy lacks a comprehensive and regularly updated defence strategy, and therefore, tends to operate haphazardly rather than systematically, with a key weakness being indicated as the lack of regular budgetary spending on the security segment. The authors found that weak accidents in the security system often have a specific cause rather than all having a common cause, and the cooperation of the private and public sectors has a very beneficial effect on the protection of the state, both in the political sense and in the industrial sense. The connections between think tanks, political foundations or associations, and the political elite demonstrate their importance in shaping national security policy.

In SIPRI Insights (2022) [9], ideas are proposed for reducing the military burden after civil conflicts to ensure the recovery of the affected states. This study uses set theory techniques to find consistent ways to reduce military spending after a military conflict. In practice, this means grouping cases with similar characteristics into sets and analysing their similarities. The authors highlight two main problems faced by post-conflict countries: rebuilding the economy and the risk of a renewed conflict. A comparative analysis of the conditions for ending the conflict and the consequences of the war burden shows that peace agreements with martial law and elections are the preferred way to reduce the war burden after the end of the conflict. This is confirmed by 7 of the 11 military burden-reduction cases examined in this study. This is mostly due to the fact that such conditions solve two key problems of the post-conflict period. Democratically elected officials have more incentives to allocate funds to social goods, such as healthcare or education, rather than to the military. Economic factors, such as economic growth or debt, were not fully addressed in this paper. Admittedly, these elements may also influence decisions to reduce the military burden after a civil conflict ends.

In DCI (2020) [10] it is proposed to calculate the index of defence companies regarding the fight against corruption and corporate transparency (DCI), which evaluates the level of public commitment to the fight against corruption and transparency in the corporate policies and procedures of 134 of the world’s largest defence companies. The purpose of calculating the index is the desire to implement reforms in the defence sector, thereby reducing corruption and its influence. The calculation of the index is based on the analysis of issues from ten categories: leadership and organizational culture, internal control, employee support, conflict of interest, customer involvement, supply chain management, agents, intermediaries and joint ventures, offsets (arrangements under which the government procures the importing country obliges the supplier company of the exporting country to reinvest some share of the contract in the importing country), high-risk markets, and state-owned enterprises. Each section has several criteria questions, each of which is evaluated on a two-point scale.

3. Methodology

Based on the conducted literature review, our own method of calculating the index of openness and budgeting transparency of the defence and security sector is proposed. The principle of openness is considered here as one that allows individuals, i.e., citizens, to participate in the decision-making process [11]. The principle of openness is broader than the principle of transparency [12]. The transparency concept refers to the accessibility of information and other public administration services, while the principle of openness covers various forms of active cooperation and communication between the administration and the public [13]. In particular, the above analysis of scientific works made it possible to determine nine separate indicators, each affecting the index’s final value. Some indicators have a binary form; some have a scale by which the specific weight of the impact is assessed. Each indicator has an individual measurement scale. The list of all used indicators and their possible values is considered as follows (the case of Ukraine is taken as the example):

(1) The number of personnel in the armed forces. This is a basic indicator that directly affects the transparency of the budgeting of the defence sector (particularly in Ukraine). It has 4 ratings on a scale from 0 to 3. The essence of the indicator is that if funds for the armed forces are spent effectively, then the quality of equipment and military equipment should increase, leading to the automatization of all processes, which means that even a slight growth of the army should lead to strengthening its effectiveness and increasing defence capability.

The scale of the indicator is as follows

0—the number of employees decreased compared to the previous period;

1—has not changed;

2—increased by less than 5%;

3—increased by more than 5%.

(2) Real/planned state budget expenditures on defence. This indicator shows plans for financing the defence sector and compares them with actual ones. The stability and uniformity of funding determine the planning of investment in military objects. The lack of funding leads to the need to reuse part of the equipment and to a decrease in personnel training, which in turn reduces the effectiveness of the armed forces.

The scale is proposed as

0—actual financing is 85% or less than planned;

1—the fact is 85–90% of the plan;

2—the fact is 90–95% of the plan;

3—the fact is 95–99% of the plan;

4—the fact is equal to the plan or more.

(3) Publication of the budget declaration by the government. This indicator makes it possible to analyse and forecast the future dynamics of budgeting of the sector. In fact, crucially, it is not the publication of such a declaration but its implementation in the final budget that plays a greater role. However, this process is much more difficult to analyse and formalise, so it is better to use a binary approach for this indicator.

0—the government does not publish a budget declaration;

2—the government publishes a budget statement.

(4) Publication of the budget adopted by the government. If available, this indicator makes it possible to compare expenditures with previous periods. The public use of budget funds is one of the most important keys to effective spending and reducing corruption, so the timely publication of the budget is the basis for analysing the transparency of defence spending.

The scale is proposed as

0—the government does not publish the budget (there are any such data);

1—the government publishes only information about the adoption of the budget;

3—the government publishes the adopted budget.

(5) Publications of the audit report on the implementation of the state budget. This indicator shows the analysis of the activities of institutions responsible for compliance with the budget. It is very important that the result of the use of budget funds is periodically published, which provides an opportunity for a comprehensive analysis of such expenses and, therefore, their public discussion, expediency, and effectiveness.

The scale is proposed as

0—the report for the past period has not been published;

2—the report for the past period is published.

(6) Percentage of expenditures directed to classified expense items. This indicator demonstrates the presence of hidden additional budget information that may be related to national security. Obviously, each country has its own secret/classified projects related to defence, but the volume of funding for them should not be large because, in this case, the risk of corruption increases, which, evidently, can lead to a decrease in the efficiency of the use of funds.

The scale is proposed as

0—more than 8% is assigned to classified expense items, or this percentage is not available to the public;

1—8% or less, but more than three per cent of the costs are allocated to classified expense items;

2—3% or less, but more than one per cent of the expenditure is devoted to classified expense items;

3—1% or less of spending is allocated to classified expense items.

(7) The legislative body provides full information on the budgeting of secret/classified articles. This indicator is related to the previous one, and it indicates whether not only the amount of expenses is indicated but also their directions, which allows for the analysis of the dynamics of such expenses.

The scale is proposed as

0—no (part or all is hidden);

1—yes (everything is open).

(8) The supreme control body hires designated personnel to conduct audits of bodies related to the security sector. The indicator presents the role of audit in the expenditure related to the defence of the country. Obviously, the more control is carried out permanently, the higher the value of the indicator should be.

The scale is proposed as

0—does not hire;

1—hires, but the staffing level is a significant limitation;

2—hires, but the level of staffing is the reason for certain restrictions;

3—appointed employees work, and the staffing level generally corresponds to resources.

(9) Audit reports on the annual accounts of the security sector and other classified programs are provided to the legislature (or appropriate committee). This indicator defines the role of the parliament in analysing and monitoring spending on the defence sector in the country. The more important the role of the parliament, the more control is exercised, which means that funds are spent more transparently.

The scale is proposed as

0—no;

1—yes, but they lack important details;

2—yes, but some details are excluded;

3—yes, lawmakers are provided with detailed audit reports on the security sector and other classified programs.

The general index is calculated according to the following formula

where —an i-th indicator of the index.

Of course, the given formula can be significantly improved. For example, all indicators are taken into account with the same weight as in (1); however, the method of expert evaluations can be used to increase the weight of certain indicators. In this case, the formula will change

where is an i-th indicator of the index, is weights, where

It is also possible to change the role of different scales in the assessment. In particular, in the formula, indicators measured from 0 to 1 and from 0 to 3 have the same weight, which effectively means that the second indicator can be three times more important than the first. Perhaps it makes sense to consider the case of normalization of all scales on the interval from 0 to 1, which will indeed make the indicators comparable. In this case, Formula (1) will take the form

where is an i-th indicator of the index, is a converter that transforms any scale into a new one from 0 to 1.

In particular, if the initial scale of integers was from 0 to 3, then the new possible values would be 0, 1/3, 2/3, and 1. At the same time, the binary choice (scale from 0 to 1) does not change.

4. Results

Table 1 shows the results of the analysis of the components of the evaluation index of openness and transparency of budgeting and financial management of the defence and security sector (case of Ukraine).

Table 1.

The dynamics of the indicators of the openness of the budgeting indicators of the defence and security sector of Ukraine.

It is valuable to analyse the dynamics of the considered indicators. The first indicator, which assesses the staff size of the armed forces in the first half of the study period, showed almost no dynamics regarding the army’s increase. However, since 2014, since the beginning of the war in the east of the country, the army had to increase in numbers; accordingly, the indicator began to grow.

Meanwhile, the second defence financing indicator also reached its planned level. The process of publishing the budget declaration and the budget are often delayed, which does not give maximum values to the third and fourth indicators. It should also be noted that the audit of the state budget is not carried out permanently, which significantly reduces the index of openness. However, the parliament and its committees have a schedule of classified expense items. Additionally, in recent years, the quality of the audit of defence articles has been increasing, which is reflected in the values of Indicators 8 and 9, respectively.

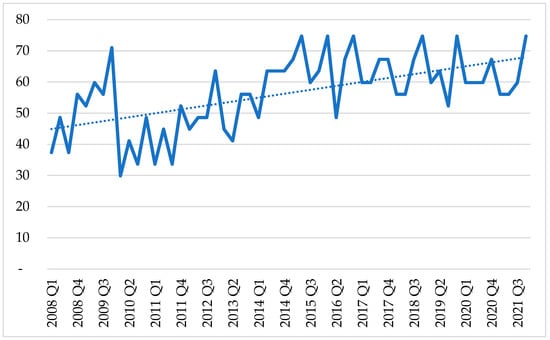

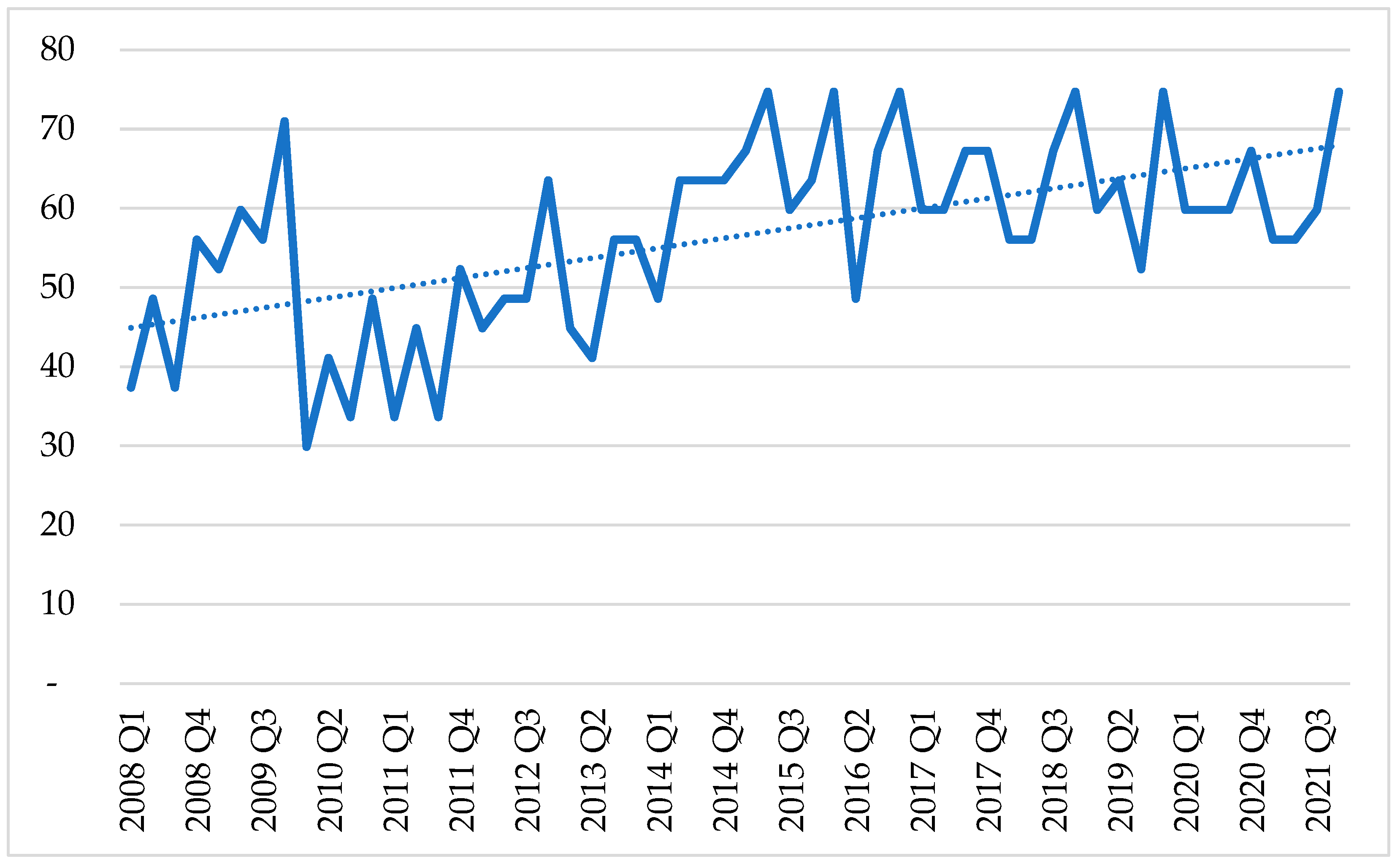

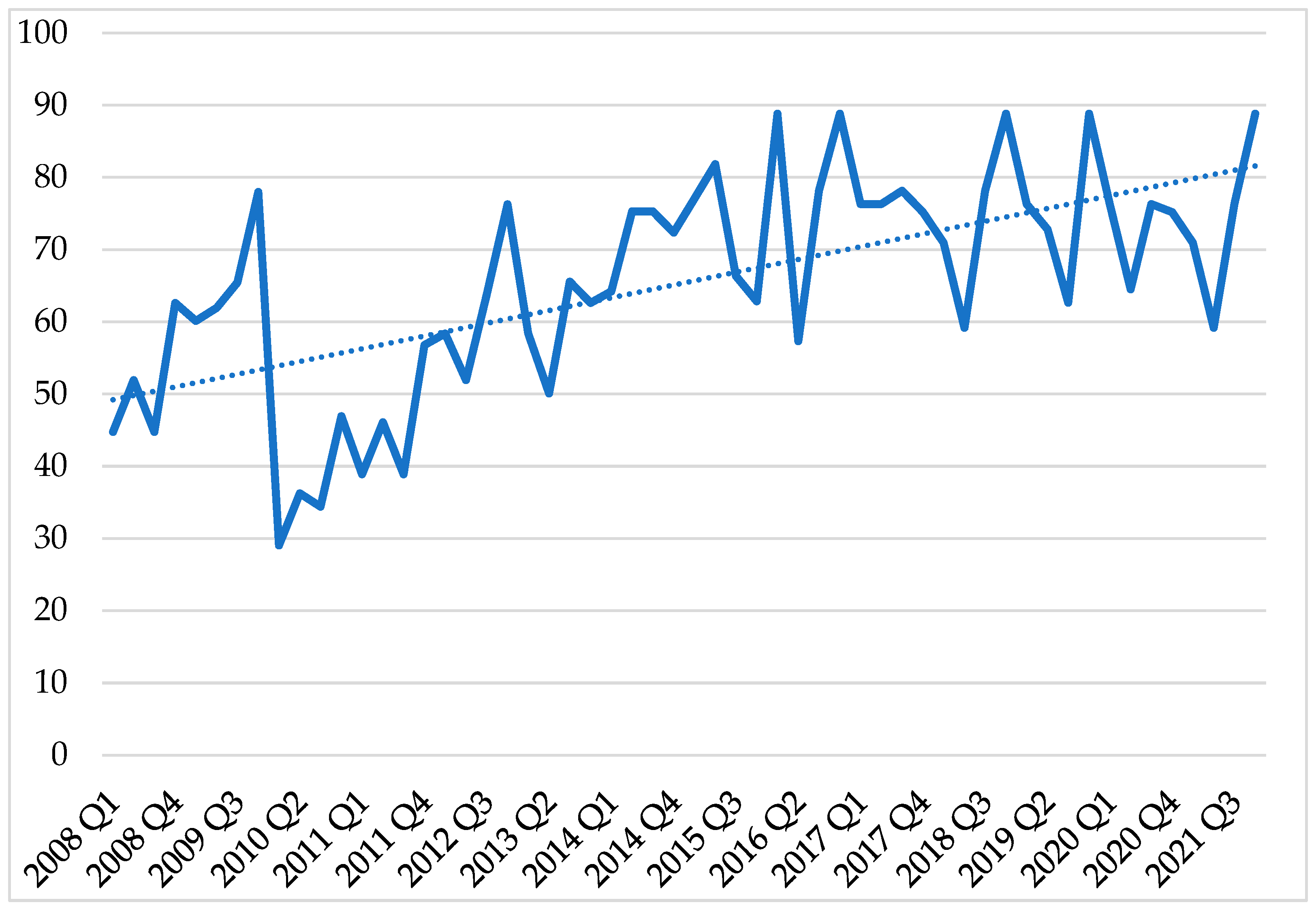

The next step of the research is to analyse the results of modelling according to the proposed methodology. Figure 1 shows the dynamics of the index, calculated according to the Formula (1), where all indicators with the same weight are taken into account. In general, there is a continuous growth of the transparency index of the openness of the budgeting of the defence and security sector of Ukraine. At the same time, the significant seasonal fluctuations of the index should be noted, which is associated with the irregularity of the publication and audit of information on the defence budget. However, the average values increased from a level of 50 in 2008 to 69 in 2021, that is, almost 1.4 times.

Figure 1.

Dynamics of the openness index of budgeting of the defence and security sector of Ukraine according to the first method. Source: compiled by the authors.

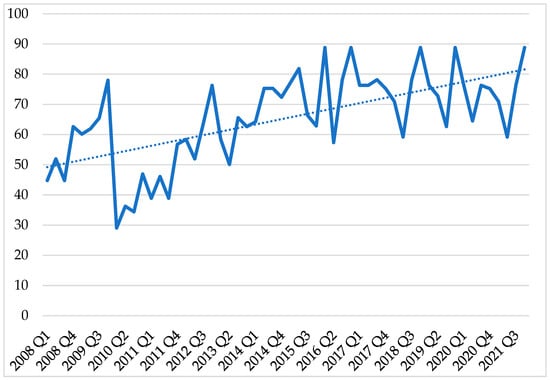

If the second approach (Formula (2)) is used, it should be used to determine the weights for calculating the index. Unfortunately, currently, only an expert way of determining such weights can be offered. The following average values of weights are determined by interviewing experts related to the field of defence (Table 2). At the same time, it should be noted that the number of interviewed experts is not sufficient to recognise these weights as relevant; however, this approach can be used to test the concept of index calculation.

Table 2.

Weights for the index of openness of budgeting of the defence and security sector of Ukraine by Formula (2).

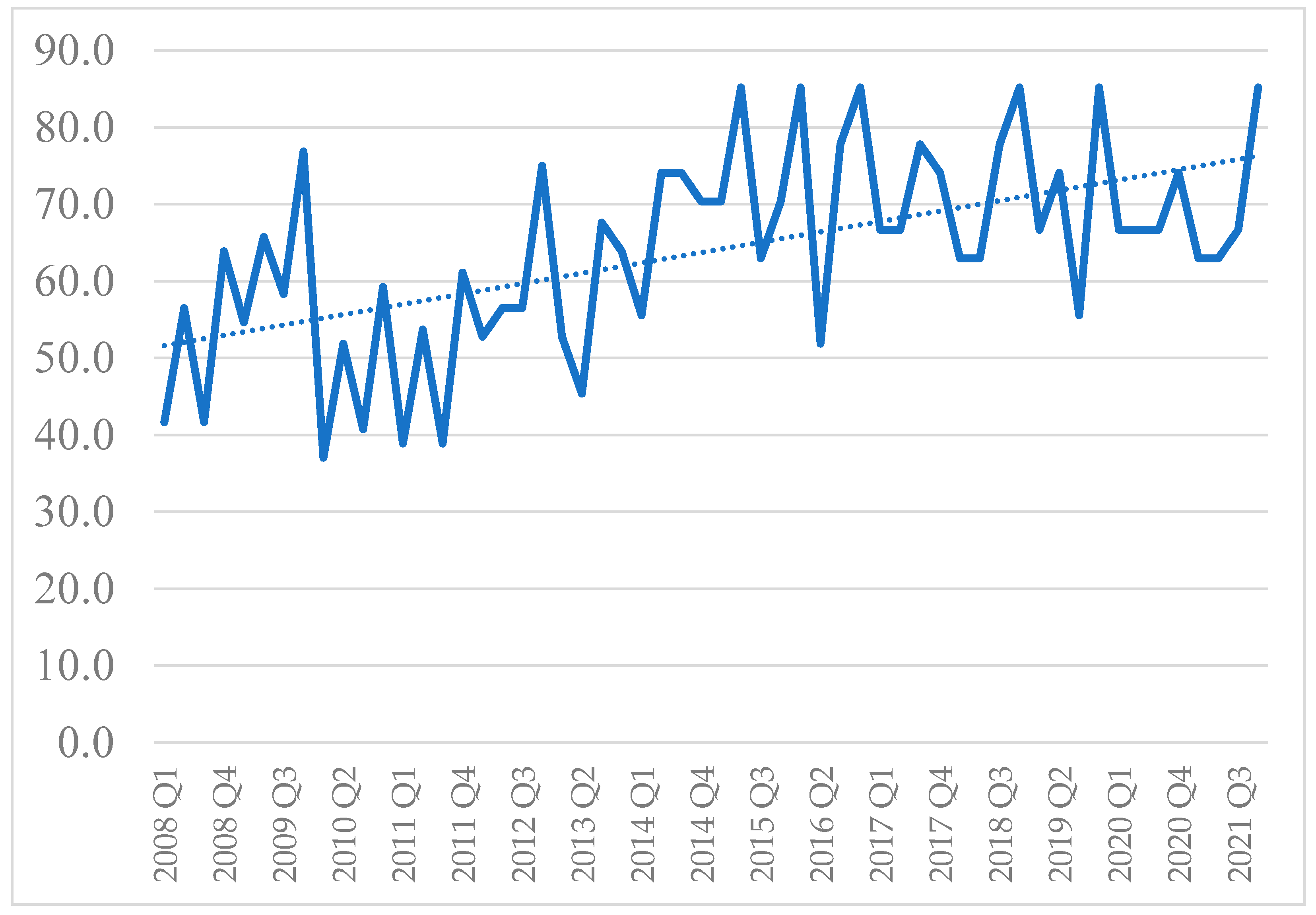

The results of the calculation of the index of openness of budgeting of the defence and security sector of Ukraine according to the second method (Formula (2)) are shown in Figure 2. It is seen that almost the same dynamics as in the first approach are followed. Although the spread of values is somewhat smaller, from 51 in 2008 to 74 in 2021, in general, the trend retains the same directionality as in the first method.

Figure 2.

Dynamics of the openness index of budgeting of the defence and security sector of Ukraine according to the second method. Source: compiled by the authors.

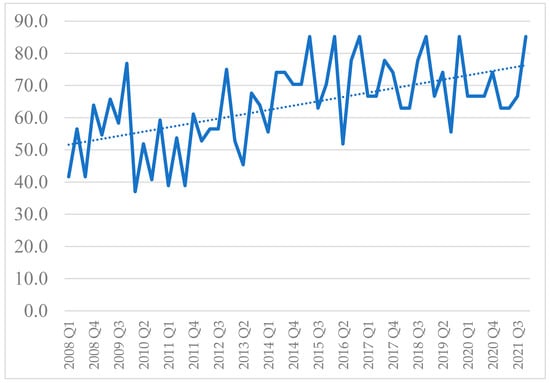

According to the third approach (Formula (3)), the results of the calculation of the openness index of budgeting of the defence and security sector of Ukraine are shown in Figure 3. The positive trend of the index is also maintained here, from 51 in 2008 to 69 in 2021.

Figure 3.

Dynamics of the openness index of budgeting of the defence and security sector of Ukraine according to the third method. Source: compiled by the authors.

Thus, all three approaches show approximately the same results, which allows us to speak about the independence of the considered methodology from the selected calculation method.

Taking into account the start of the full-scale war in 2022, the possible dynamics of this index should be determined. At the same time, the indicators will conflict. For example, the first two indicators will reach their maximum values, but the other indicators will drop significantly. This is due to the fact that during martial law, a significant part of the expenses is classified precisely for reasons of military security, which makes an audit impossible, and a timely periodic audit even more so. As a result, the index will likely return to 2008 levels or even lower during the war. However, it is already obvious that after the end of the war, its value should exceed the indicators of 2021 due to a significant demand in society for the openness and efficiency of all budgetary mechanisms.

5. Discussion

The use of the index approach is not new in the scientific literature. For example, this approach is actively used for comparing countries, as indicated by previous studies [18]. This allows avoiding nominal comparisons of countries that differ in size and power. The same situation is observed when analysing the defence and security sectors of a country. The use of nominal indicators will not be relevant precisely because of the completely different measurements of indicators and their values for specific countries. For example, certain countries may focus on nuclear security assurance, while others may focus on missile technology or the use of mainly ground forces or the navy. It is obvious that the choice is essential to determine exactly which costs will be inherent in different countries. Accordingly, each state will determine its strategic components of sustainable management, as well as how they will affect the country’s economic, military, and social development.

The analysis of scientific studies showed that openness and transparency in the field of the security complex are significantly related to several factors [19]. First, the general level of democracy of state institutions and their responsibility towards society increases the readiness to carry out reforms and the transparency of fund spending. Second, the country’s adaptation to current and future security challenges also increases transparency. In this aspect, Ukraine faces an enormous task, to carry out crucial reforms in the system of the Ministry of Defence, which will guarantee the effectiveness of the distribution of both internal funds and aid provided by allies under the conditions of war and the transition to full democracy. It should be noted that most of the aid is actually given in advance, counting on the fact that Ukraine will be able to take its place among the democratic, transparent countries of the EU and NATO, having achieved the goals of sustainable development and governance. Therefore, conducting an analysis that allows the assessment of the level of transparency of spending in the military sector is necessary at the current stage.

The introduction of a new methodology for evaluating the openness and transparency of the budgeting and financial management of the defence and security sector index allows for the analysis of the dynamics in the state. The analysis conducted until the end of 2021 showed that Ukraine is gradually but persistently increasing the level of transparency in the use of budget funds. At the beginning of 2022, military aggression was carried out against Ukraine, which forced a significant change in the level of financing of the army. Mobilization was carried out, bringing the number of military units to 1 million people, and the costs of servicemen’s salaries, treatment, and equipment provision increased significantly. For obvious reasons, part of the budget expenditure became classified since its publication could show the size of a particular military unit. However, even in such conditions, the Ukrainian society has shown that it is ready to control the Ministry of Defence and disclose certain corruption risks in some contracts. The latter led to an almost complete change in the leadership of the Ministry of Defence of Ukraine [20]. It is a reason to believe that the process of reforming both society and budgetary institutions has changed significantly. That is, the trend towards increasing the openness and transparency of expenditures will continue. Additionally, this is a prerequisite for the formation of sustainable governance in Ukraine.

6. Conclusions

A developed defence sector in each state is a guarantee of integrity, sovereignty, and independence. The world’s strong states have powerful armies, in which large sums of money are invested for their development. Ukraine’s state budget also provides valuable funding for defence spending. It is equally important that these expenditures are not only sufficient for the maintenance of the armed forces but also have a high level of openness, do not involve corruption or money laundering, and guarantee their effective use.

After analysing studies on the openness of defence budgets of enterprises and states, this paper proposes a methodology for calculating the index of openness and transparency of budgeting in the defence and security sector and tests it in the case of Ukraine. Taking into account statistical indicators from the State Treasury Service of Ukraine, the State Statistics Service of Ukraine, information from the official portal of the Verkhovna Rada of Ukraine, and expert opinions, the index was calculated quarterly from 2008 to 2021.

The results of the index indicate that the level of openness of budgeting in the defence sector of Ukraine has grown from average to above average in recent years.

Further research should focus on analysing the possible extensions of the proposed index and using additional indicators, which should increase the visibility of the obtained indicator. However, the proposed analysis has its limitations, mainly related to the availability of data that can be used for appropriate analysis. Unfortunately, large parts of the indicators related to the defence sector are either closed or there is limited access to them, and they cannot be taken into account in open scientific research. Secondly, the level of transparency in the use of budget funds changes significantly during the war, as demonstrated by the events of 2022. The technique should be improved in the case of even limited combat operations conducted.

Overall, the proposed concept can be considered as a basis for the formation of a new methodology for constructing an index of openness and transparency of budgeting and financial management of the defence and security sector of any state.

Author Contributions

Conceptualization, S.N. and A.S.; methodology, A.S.; software, A.S.; validation, S.N., A.S. and G.K.; formal analysis, A.S.; investigation, G.K.; resources, G.K.; data curation, S.N.; writing—original draft preparation, A.S.; writing—review and editing, G.K.; visualization, A.S.; supervision, S.N.; project administration, S.N.; funding acquisition, S.N. All authors have read and agreed to the published version of the manuscript.

Funding

This work was supported by Hasso Plattner Foundation through the grant LBUS-UA-RO-2023, financed by the Knowledge Transfer Center of the Lucian Blaga University of Sibiu.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data supporting reported results can be found in the list of literature links.

Acknowledgments

The authors acknowledge the support by Hasso Plattner Foundation through the grant LBUS-UA-RO-2023, and the finance by the Knowledge Transfer Center of the Lucian Blaga University of Sibiu.

Conflicts of Interest

The authors declare no conflict of interest. The funders had no role in the design of the study; in the collection, analyses, or interpretation of data; in the writing of the manuscript; or in the decision to publish the results.

References

- Molotok, I.F. Bibliometric and Trend Analysis of Budget Transparency. Bus. Ethics Leadersh. 2020, 4, 116–122. [Google Scholar] [CrossRef]

- Birskyte, L. Determinants of Budget Transparency in Lithuanian Municipalities. Public Perform. Manag. Rev. 2019, 42, 707–731. [Google Scholar] [CrossRef]

- Tian, N.; Wezeman, T.; Yun, Y. Military Expenditure Transparency in Sub-Saharan Africa. SIPRI Policy Paper 2018, No. 48. Available online: https://www.sipri.org/sites/default/files/2018-11/sipripp48.pdf (accessed on 1 February 2023).

- Citro, F.; Cuadrado-Ballesteros, B.; Bisogno, M. Explaining budget transparency through political factors. Int. Rev. Adm. Sci. 2021, 87, 115–134. [Google Scholar] [CrossRef]

- Abiodun, T.F.; Asaolu, A.A.; Ndubuisi, A.I. Defence budget and military spending on war against terror and insecurity in Nigeria: Implications for state politics, economy, and national security. Int. J. Adv. Acad. Res. (Soc. Manag. Sci.) 2020, 6, 13. [Google Scholar] [CrossRef]

- The Transparency of National Defence Budgets. Available online: https://ti-defence.org/wp-content/uploads/2016/03/2011-10_Defence_Budgets_Transparency.pdf (accessed on 15 October 2022).

- Transparency International Defence & Security Strategy 2021–2023. Available online: https://ti-defence.org/publications/strategy-2021-2023/ (accessed on 15 November 2022).

- Defence Industry Influence on European Policy Agendas. Available online: https://ti-defence.org/publications/defence-industry-influence-europe-germany-italy/ (accessed on 15 January 2023).

- Pathways for Reducing Military Spending in Post-Civil Conflict Settings. Available online: https://www.sipri.org/publications/2022/sipri-insights-peace-and-security/pathways-reducing-military-spending-post-civil-conflict-settings (accessed on 25 January 2023).

- Defence Companies Index on Anti-Corruption and Corporate Transparency 2020. Available online: https://ti-defence.org/wp-content/uploads/2021/02/DCI-2020-Methods-Paper.pdf (accessed on 25 September 2022).

- Bugaric, B. Openness and transparency in public administration: Challenges for public law. Wis. Int’l LJ 2004, 22, 483. [Google Scholar]

- Trpin, G. The process of communication between citizens and public authority bodies–a new concept of general administrative procedure. Lex Localis 2008, 6, 153–169. [Google Scholar] [CrossRef]

- Petlenko, Y.; Drozd, N. Current Framework for the Transparent Budgeting in the Defense and Security Sector of Ukraine; Publishing House “Baltija Publishing”: Riga, Latvia, 2022. [Google Scholar]

- State Treasury Service of Ukraine. Available online: https://mof.gov.ua/uk/state-treasury (accessed on 13 June 2022).

- State Statistics Service of Ukraine. Available online: http://www.ukrstat.gov.ua/ (accessed on 13 June 2022).

- Official Portal of the Verkhovna Rada of Ukraine. Available online: https://www.rada.gov.ua/ (accessed on 13 June 2022).

- Independent Anti-Corruption Commission (ICAC). Available online: https://nako.org.ua/ (accessed on 13 June 2022).

- Stavytskyy, A.; Kharlamova, G.; Komendant, O.; Andrzejczak, J.; Nakonieczny, J. Methodology for Calculating the Energy Security Index of the State: Taking into Account Modern Megatrends. Energies 2021, 14, 3621. [Google Scholar] [CrossRef]

- Liutyy, O. Management of Financial Sectors of Defence and Security of Ukraine; CP Comprint: Kyiv, Ukraine, 2022. [Google Scholar]

- Ukraine’s Defence Minister Announces Dismissal and Appointments in Defence Ministry. Available online: https://www.pravda.com.ua/eng/news/2023/02/14/7389256/ (accessed on 15 September 2022).

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).