1. Introduction

The traditional economic model that relies on resource endowment is gradually being watered down with the implementation of an innovation-driven strategy. Economic growth fueled by technological innovation is more competitive and sustainable. However, financial issues that stymie the development of technological innovation are common in innovation activities, such as insufficient financial support and information asymmetry caused by the inadequate development of traditional financial markets [

1]. As a result, it is critical to improve financial support services to foster technological innovation [

2,

3].

Digital technology innovation in the financial sector has led to the emergence of digital inclusive finance [

4], an emerging financial service model [

5] and a key guarantee for the sustainable advancement of technological innovation [

6]. It provides new financial services such as mobile payment, credit, insurance, and financing by utilizing the new generation of information digital technology [

7], and frees financial businesses from the constraints of “people” and “physical departments”. In order to better match the target customer groups and improve the efficiency of capital allocation [

8,

9], it also broadens the scope and use-depth of finance, enhances user experience and access to finance [

10], and removes barriers that traditional finance faces when supporting innovative activities. We should strengthen the development of digital finance and improve the contribution of innovation to economic growth [

11]. Therefore, it is crucial to research how to encourage sustainable economic development through the coordinated development of digital finance and technological innovation.

According to the existing literature, digital finance is thought to be capable of assisting technological innovation departments [

12,

13,

14] in resolving financial issues due to its broad coverage, low cost, and high inclusiveness [

12,

15]. However, there are few explanations for how technological innovation has affected digital finance. This study asserts that the relationship between digital finance and technological innovation is more than just digital finance’s unilateral influence on technological innovation; technological innovation can provide technical support and create financial demand for digital finance. Digital finance and technological innovation should be mutually supportive and spiraling in development. There is a long-term equilibrium relationship between finance and technological innovation [

16], and enterprise financialization and innovation have a dynamic relationship [

17]. Therefore, in contrast to earlier researchers who only looked at the one-way effect of digital finance on technological innovation, the main focus of this paper is on the coupling and synergy between digital finance and technological innovation.

Based on the above analysis, this article proposes Hypothesis 1:

Hypothesis 1. Digital finance promotes technological innovation, and technological innovation also promotes digital finance. The relationship between the two is symbiotic, interdependent, and mutually coupled.

From the standpoint of regional development, the various resource endowments in various regions will result in varying development levels, creating an unbalanced but closely connected spatial pattern. Friedmann [

18] used the “core–periphery” theory to explain regional economic development’s spatial relevance. He believes that the different development speeds of different regions will lead to a widening gap and form a spatial pattern, with the faster-developing areas as the core and the slower-developing areas as the periphery. The two types of regions are closely related to each other: the core regions concentrate the important elements needed for development to achieve industrial clusters and have an impact on the peripheral regions through the trickle-down effect; the marginal regions rely on the core regions to make progress. In 1991, Krugman [

19] further revealed that the main factor of the “core–periphery theory” is the endogenous comparative advantage of each region: the core region generally has more material and human capital, which drives the development of the peripheral areas via the radiation effect. In terms of the spatial relationship of the coupling coordination between digital finance and technological innovation, building a network in different regions to form a cross-regional collaborative innovation model can reduce potential risks [

20], promote the digital flow of financial resources, and stimulate more innovative output [

21]. On the one hand, the interaction and coupling of financial institutions and innovation departments within the region can raise the level of digital finance and technological innovation; on the other hand, the spatial connection and spillover effect caused by the movement of elements between regions can further couple and coordinate digital finance and technological innovation. In light of this, this paper contends that the coordinated development of digital finance and technological innovation exhibits a spatial correlation.

Therefore, we propose Hypothesis 2:

Hypothesis 2. There is a spatial correlation of the coupling coordination network between digital finance and technological innovation among different regions.

This study employs the SNA method to investigate the spatial correlation network of coupling coordination between digital finance and technological innovation, providing a new perspective and empirical evidence for comprehending the spatial effects of sustainable economic growth. We gain a deeper comprehension of how the coupling coordination development has evolved over time and across different regions through this study. This paper also identifies key regions that play an important role in the coupling coordinated growth of digital finance and technological innovation, assisting policymakers to promote coordinated regional development. In addition, this article can serve as a resource for other developing nations with backgrounds and growth rates comparable to China. Therefore, studying the coupling between digital finance and technological innovation has important value.

This study is organized into six sections to explore the collaborative development relationship between digital finance and technological innovation.

Section 2 details the literature review.

Section 3 introduces and explains the research method and data source.

Section 4 contains an in-depth discussion of the coupling coordination degrees in Chinese provinces.

Section 5 analyzes the spatial network characteristics of the coupling coordination. The final section summarizes the key conclusions. This study is of great significance for accelerating the transformation of innovation momentum and strengthening financial services to the real economy.

2. Literature Review

- (1)

Research on the influence of digital finance on technological innovation

The relationship between digital finance and technological innovation has been a topic of much discussion and research in recent years. The existing literature has theoretically proved that digital finance can promote technological innovation. Digital finance services such as mobile payments can drive innovation by simplifying loan approval, which improves the access of small businesses to credit and drives innovation [

22]. Digital construction can assist enterprises in deeply integrating resources to stimulate open innovation [

23], and digital finance can guide the flow of social funds to promote the upgrading of high-tech industries, which can provide good technology spillover conditions for technological innovation and improve the level of regional technological innovation [

12]. Meanwhile, digital finance can alleviate the financing difficulties of innovative enterprises and provide funds for innovative activities to improve the efficiency of capital allocation, easing the financing constraints of innovative enterprises [

24,

25]. Lin B et al. [

26] also used financing constraints as intermediary variables to conclude that digital finance can promote green innovation by alleviating financing constraints. Some scholars have studied the transmission mechanism of digital finance to technological innovation. For example, Zhao Hongyan et al. [

27] empirically studied the significant role of digital finance in promoting collaborative innovation and sorted out the transmission mechanisms of credit scale, social consumption, and industrial upgrading. Jinhui Zhu et al. [

28] concluded that the impact mechanisms of digital financial inclusion to promote agricultural enterprises’ technological innovation include enterprise digitization, financing constraints, and market efficiency. Digital finance can also influence technological innovation by promoting residents’ wage income [

29], generating income effects [

30], improving consumer credit [

31], stimulating consumer demand [

32,

33], and other factors. Furthermore, digital finance can stimulate green technology innovation [

34,

35]. Guangqin Li [

36] examined the direct role and spatial spillover effect of the digital economy in improving the efficiency of industrial green innovation. In addition, Wenrong Pan et al. [

37] demonstrated the non-linear relationship between the digital economy and innovation.

- (2)

Research on the influence of technological innovation on digital finance

There are few relevant documents on the impact of technological innovation on digital finance. This paper summarizes the relevant arguments on the impact of technological innovation on the digital economy. Lin Liang and Yan Li [

38] concluded the impact of the regional innovation ecosystem on the digital economy, proving the positive spatial spillover effect of regional innovation on the digital economy. Xiaohui Chen et al. [

39] analyzed the role of fintech on the digital economy and its internal impact mechanism based on the CRITIC method, believing that fintech can accelerate the development of China’s digital economy by promoting technological innovation.

- (3)

Research on coupling coordination

There have been few studies on the interactive coupling relationship between digital finance and technological innovation. Zou Xinyue and Wang Wang [

2] used the spatial simultaneous model to empirically study the interaction between digital finance and technological innovation. Most scholars chose to adopt the coupling coordination degree (CCD) model to measure the coupling coordinated development relationship between digital finance and technological innovation; the degree of coupling coordination between digital finance and technological innovation in China was relatively low but increasing steadily, and the distribution characteristics are high in the southeast and low in the northwest [

2,

40,

41]. LV Jianglin [

41] studied the coordinated development level of digital inclusive finance and real economy by using the Dagum Gini coefficient, kernel density estimation, and standard deviation ellipse. They also concluded that while the overall level was still low, the eastern region was higher than the midwestern regions, and the regional difference was gradually decreasing. In addition, some scholars used the CCD model to study other coupling coordination relationships: the coupling coordination of digital economy and green technology innovation [

42]; technological innovation and green development [

43]; tourism development and resource environment carrying capacity [

44]; data elements and green development [

45]; digitalization and energy storage innovation [

46]; and so on.

According to this review of the literature, scholars generally believe that digital finance plays a positive role in promoting technological innovation. However, research on the relationship between digital finance and technological innovation primarily focuses on the unilateral influence of digital finance on technological innovation, with little research on the impact of technological innovation on digital finance. This paper holds that the relationship between digital finance and technological innovation should be complementary and interdependent, and that studying the coordinated development of the two is beneficial to economic sustainability and the conversion of economic momentum. In addition, there is a lack of in-depth analysis of the spatial correlation between digital finance and technological innovation in China. Therefore, the main contributions of this paper are as follows: Create a technological innovation index system and calculate the technological innovation development index of each region. Next, assess the coupling degree and coupling coordination degree of digital finance and technological innovation, and analyze the time series characteristics, spatial differences, as well as the space–time evolution characteristics of the coupling coordination. Finally, investigate the spatial correlation and spatial spillover characteristics of the coupling coordination between digital finance and technological innovation.

3. Research and Design

Technological innovation is the first driving force behind development and the key to achieving high-quality economic development. Innovation activities require financial support, but traditional financial systems constrain the development of innovation. Digital finance can alleviate the financial challenges faced by technological innovation. Studying the coordinated relationship between digital finance and technological innovation can deeply explore the driving role of digital finance in technological innovation, as well as the support of technological innovation in the field of digital finance.

To begin with, the entropy weight method is applied to compute the technological innovation development index. Subsequently, the CCD model is adopted to measure the coupling coordination degree of digital finance and technological innovation. Following this, we utilize the improved gravity model to determine the spatial correlation distance matrix, and then based on this matrix, we conduct a social network analysis of the coupling coordination between digital finance and technological innovation.

3.1. Technological Innovation Index

Scholars often use the number of patents to measure the ability of technological innovation, but this paper constructs an indicator system of technological innovation and calculates the index by entropy method. The index system is presented in

Table 1, selecting indicators from the input and output dimensions [

40]. The digital inclusive financial index [

47] was published by the Digital Financial Research Center of Peking University. The study selects the panel data of 31 provinces and cities in China from 2011 to 2020 as the research sample; the data are obtained from the WIND database and the China Science and Technology Statistical Yearbook.

- 2.

Dimensionless processing

Considering the dimensions of the data are different, it is necessary to standardize the data to eliminate the dimension influence. The indicators in this paper are all positive, so the following formula is carried out to preprocess the data:

where

and

represent the maximum and minimum of index j respectively. To avoid the influence of the 0 on the subsequent calculation, the standardized data are processed as follows:

0.00001.

- 3

Entropy method

This study performs the entropy method to determine the weight of each indicator in the evaluation system of the technological innovation index. The method calculates the final weight by using the difference degree of each index, which is more objective because it can avoid subjective bias. The main steps are as follows:

① The weight of each index in the system :

(m represents the number of samples for each index);

② The entropy value of index j: ;

③ The difference coefficient of index j: ;

④ The weight of index , for which the formula is:, (1, 2, …n); and

⑤ The comprehensive evaluation value: .

3.2. The Coupling Coordination Degree Model

To study the system interactions between digital finance and technological innovation, the research refers to the concept of “coupling” in physics and constructs a corresponding coupling model to measure the coupling degree between the digital financial system and the technological innovation system. The coupling model is as follows [

41,

43]:

where

and

denote the development level of digital finance and technological innovation, respectively.

C represents the coupling degree, which ranges from 0 to 1; the higher the coupling degree

C is, the smaller the deviation between the two systems. However, the coupling degree model has the phenomenon of “pseudo-evaluation”. In the initial development stage, if the level of digital finance and technological innovation is relatively low and similar, the coupling degree may also have a higher score. At the same time, the model cannot reveal the coordination degree between the two systems. In order to avoid misjudgment and obtain the benign coupling coordination level of the two systems, this paper introduces the coupling coordination degree (CCD) model as follows:

where

D denotes the coupling coordination degree,

C represents the coupling degree,

T represents the coordination evaluation index of the two subsystems,

and

are the contributions of the two subsystems, and

. Considering the equal status of the two subsystems,

0.5.

There is no completely unified criterion for the division of coupling degree and coupling coordination degree at present. Referring to the existing research and the research objective, the evaluation standards of

C and

D are in

Table 2 in the subsections below.

3.3. Spatial Correlation Intensity

This paper chooses the improved gravity model [

48,

49] to depict the spatial correlation distance of the coupling coordination development between digital finance and technological innovation:

where

denotes the spatial correlation strength between region i and region

j;

denotes the gravitational constant, reflecting the contribution rate of region i to the coupling coordination between region i and region j;

and

represent the resident population of the two regions at year-end;

and

represent the gross domestic product (GDP); and

represent the coupling coordination quality of digital finance and technological innovation. Furthermore,

is the geographical distance between the provincial capitals of i and j (calculated by ArcGIS software based on the projection data of provincial administrative regions);

and

represent the per capita GDP; and

is the economic distance between region

i and

j, which is calculated from the geographical distance and per capita GDP.

After calculation, this paper obtains the spatial gravity matrix of the coupling coordinated development in various provinces, and uses the mean value as the threshold to transform the matrix into an asymmetric 0–1 matrix.

3.4. Social Network Analysis

To study the structural characteristics as well as the role and status of each province in the network, this study applies the SNA method [

50,

51,

52,

53] to establish the spatial association network. The social network analysis (SNA) method is an interdisciplinary approach that was first used in sociology; it was also later used in the fields of business and economics [

54]. The SNA method employs graph theory and algebra to examine network relationships. It enables quantitative analysis of spatial relationships and provides empirical tools for testing theoretical hypotheses. By constructing a spatial correlation network, SNA can effectively reveal the interregional characteristics of coupling between digital finance and technological innovation.

In the case of the coupling coordination of digital finance and technological innovation across various provinces in China, there exists a spatial correlation that can be explored using SNA. Each province is represented as a node in the network, and the connections between nodes denote network associations between provinces. The first step is to gather spatial data, such as network nodes (provinces) and their connections (spatial coupling associations calculated by the improved gravity mode). Following that, we can use UCINET software to perform overall network analysis and individual network analysis, while the UCINET NetDra module is used to create a spatial correlation network diagram of the coupling coordination. Finally, we can also use the CONCOR method in UCINET to conduct a block model analysis.

3.4.1. Overall Network Analysis

To analyze the overall network structure characteristics, this study calculates three indicators, including network density, network hierarchy, and network efficiency [

55]. Firstly, the overall network density is used to measure the correlation strength between the network subjects, the high network density represents the spatial relationship between the subjects is close, and vice versa.

Secondly, the overall network hierarchy is used to describe the hierarchical structure of the network. If the network hierarchy is lower, there would be fewer edge nodes and the network correlations would be strengthened. Finally, the network efficiency is used to measure the connection efficiency of the network. That is, the number of redundant connections in the network. The lower the network efficiency is, the more redundant connections in the network are, and the more stable the network structure is; on the contrary, the greater the network efficiency, the weaker the connection between the agents, and the weaker the stability of the network structure.

3.4.2. Individual Network Analysis

The nodes at the center of the social network have a great influence on other individuals. In order to know the status and function of each province in the whole network, it is necessary to analyze the centrality of the individual network, using centrality indicators to measure connectivity, intermediation, and accessibility [

56]. The measurement indicators mainly include degree centrality, closeness centrality, and betweenness centrality:

① Degree centrality: This represents the influence of the network subject. The larger the value is, the closer this subject is to the center in the network, and the more connections it makes to other subjects.

② Closeness centrality: This indicates the sum of the shortest distance between a subject and another subject. The larger the indicator, the closer the relationship between the subject and other individuals.

③ Betweenness centrality: This is mainly used to measure the impact of one province on other provinces. The larger the index, the greater the intermediary role of the subject in the network.

3.4.3. Block Model Analysis

After analyzing the overall network and individual network, this paper uses the block model to conduct block clustering research. The regions with similar characteristics are classified into one block. Clearing the function of each block and studying the relationship between each block is important. In the spatial correlation network of coupling coordination between digital finance and technological innovation, the block model divides all provinces into four plate types: agent plate, main inflow plate, main outflow plate, and bidirectional spillover plate. The agent plate generally plays the role of bridge in the network, which is mainly associated with other plate members. The main inflow plate receives the relationships from the external plate, which is significantly higher in number than the other plate overflow relations it sends; this plate also receives the relationships sent by the members in its plate. The main outflow plate is opposite to the main inflow plate, as this plate receives few connections from the external plates; the relationships overflowing to the outer plate are more than that from the external plates, and this plate sends connections to the internal plate. The bidirectional spillover plate not only spills relations to the external plate, but also sends out relations to the internal plate.

5. Spatial Association Network Analysis

This chapter will use the matrix formed by the spatial correlation intensity to study the spatial correlation network of the coupling coordination by social network analysis.

5.1. Overall Network Characteristics

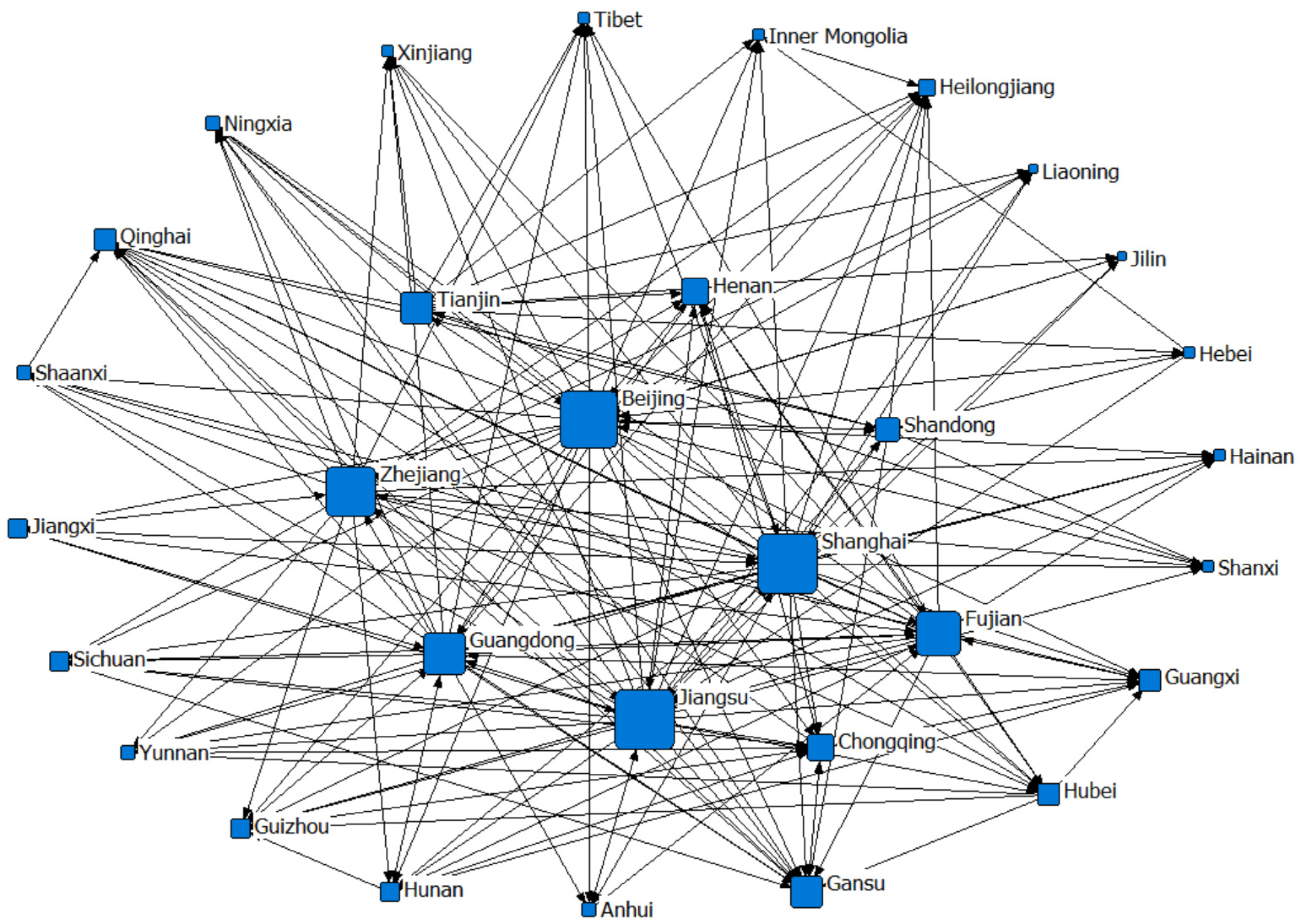

A province represents a node in the association network. The NetDra module of UCINET software is used to create the spatial correlation network diagram of the coupling coordination between digital finance and technological innovation, which is used to depict the network structure of digital finance and technological innovation coupling coordination in China over time. This paper takes 31 provinces as the spatial network nodes and takes the spatial correlation intensity between provinces as the connection line, as shown in

Figure 5 and

Figure 6, using the years 2011 and 2020 as examples.

In the above image, it can be seen that the network lines in 2020 were denser than those in 2011, which indicates that the spatial relationship of coupling coordination of digital finance and innovation in China was becoming closer over time, and there was no isolated province. Second, the size of the icon was used to represent the strength of a region’s ties to other regions. We discover that the provinces at the network’s core were primarily the more developed eastern coastal provinces of Beijing, Shanghai, Jiangsu, Zhejiang, and Guangdong. These provinces were closely connected to other provinces. The provinces at the network’s edges were primarily the less developed regions of the midwest and northeast.

This study also measured the overall density, number of ties, network hierarchy, and network efficiency of the network in accordance with the spatial correlation matrix of the coupling coordination of digital finance and technological innovation. In

Figure 7 and

Figure 8, the corresponding change trend diagram is drawn.

Figure 7 depicts the overall network density and the number of ties from 2011 to 2020. We can see that while both almost exhibit an increasing trend, the spatial correlation was closer with more network ties, and network stability was greater with higher network density. It is important to note that while the number of ties among 31 nodes increased in 2020 compared to previous years, it was still only 209, when the maximum number of relationships among 31 nodes should be 930, which indicates that the network was still in its infancy, the overall level of correlation was still low, and the coupling coordination relationships among provinces need to be further strengthened. However, based on the current development and steady growth trend, the spatial association network will have more relationships in the future.

Figure 8 depicts the trend of network hierarchy and network efficiency from 2011 to 2020; the two indicators showed a fluctuating downward trend overall. The degree of network hierarchy decreased from 0.57 in 2011 to 0.50 in 2020, indicating that the network structure was developing more closely, the correlation intensity was enhanced, and the spatial synergy was stronger. At the same time, the network efficiency fell from 0.75 to 0.67, indicating that an increase in network connections made the connections of network individuals stronger.

5.2. Individual Network Characteristics

The degree centrality, closeness centrality, and betweenness centrality of 31 provinces are measured using UCINET in this paper in order to analyze the role of each province in the coupling coordinating spatial network of digital finance and technological innovation. The results for 2011 and 2020 are listed in

Table 6.

Individual centrality is classified as outdegree centrality or indegree centrality. The number of network relations actively sent by a central subject to other cooperative subjects is the outdegree, and the number of network relations sent by other cooperators is the indegree. As shown in the table above, Shanghai, Jiangsu, and Beijing are among the top three in terms of outdegree, indicating that the eastern developed areas act as central actors in the associated networks and have a greater impact on other provinces. Inner Mongolia, Qinghai, Tibet, Xinjiang, Heilongjiang, and other western and northeastern regions have the lowest outdegree and thus have little influence on other regions.

The data in the preceding table are drawn in a radar chart to more intuitively observe the individual centrality of the network, as shown in

Figure 9. Between 2011 and 2020, the provinces with the highest centrality are Shanghai, Jiangsu, Beijing, Zhejiang, Guangdong, and Tianjin. The majority of them are eastern coastal provinces in the core of the network, which have more connections to other regions. They play the role of an intermediary bridge, making each province complement and promote each other in the coupling coordinated development of digital finance and technological innovation.

5.3. Block Model Analysis

This section will use the CONCOR method in UCINET to analyze the block model based on the data in 2020 in accordance with the spatial gravity matrix generated by the improved gravity model. The spatial relationship of coupling coordination in 31 regions was divided into four sectors: agent, main inflow, main outflow, and bidirectional spillover plates, and the network relationships between plates are shown in

Table 7. In 2020, the total number of ties in 31 provinces was 209, of which the number of ties among members within the plate was 36, and the number of cross-board connections was 173. There is a substantial spatial spillover effect.

The role of the plate is divided according to the plate spillover relationship in the preceding table, and

Figure 10 is drawn. There are 11 relationships that overflow to other plates from block II, while block II receives up to 103 relationships from other plates. Plate II is thus the “main inflow plate”, which includes Tibet, Xinjiang, Qinghai, Gansu, Ningxia, Yunnan, Guizhou, Sichuan, Chongqing, Guangxi, Jiangxi, Shaanxi, Hubei, Hunan, Heilongjiang, and Hainan, primarily in the western and central underdeveloped regions. On the contrary, plate III overflows 64 relations to other sectors and accepts 13 relations from other plates. Because the number of relationships overflowing to other plates is significantly greater than that of the number of relationships accepted, plate III is the “main outflow plate,” including developed eastern regions such as Beijing, Jiangsu, and Tianjin. The number of relationships in which plate I overflows to other plates, 24, is close to the number of relationships in which plate I accepts other plates, 36, indicating that this plate acts as an “intermediary” with other plates and belongs to the “agent plate,” which includes Hebei, Shandong, Shanxi, Anhui, Henan, Liaoning, Jilin, and Inner Mongolia. Plate IV in the spatial network relationship spills over to other plates as well as its own plate, making it a “bidirectional spillover plate”; this plate includes Zhejiang, Shanghai, Guangdong, and Fujian, which are developed areas on the eastern coast.

The actual internal relations of plates I, III, and IV are all smaller than their expected internal relations among the four blocks. Only in module II does the actual internal relation exceed the expected internal relations.

This paper calculates the density matrix and image matrix of the four plates in order to further investigate the role of the four plates in the network and whether there is a spatial spillover relationship between the plates. According to the previous calculation of the overall network relationship, the overall network density of the coupling coordination of digital finance and technological innovation in 2020 is 0.225. If the density of a plate is greater than the overall network density, the plate is said to have a spillover trend, and if it is less than 0.225, it does not exist. As shown in

Table 8, the image matrix is obtained by transforming the density matrix, assigning 0.225 as the critical value, assigning 1 if it is greater than this value, and taking 0 if it is less than this value.

From the perspective of the intra-plate relationship, there is a spillover effect in plate III and plate IV, while there is no spillover effect in plate I and plate II, that is, there is a significant spatial network correlation between Beijing, Tianjin, Shanghai, Guangdong, Zhejiang, Jiangsu, and other eastern cities. From the perspective of the spillover relationship between plates, plate III has a spillover relationship with plates I, II, and IV, and plate IV has a spillover relationship with plates I and II, indicating that the more developed cities in the east have significant spillover effects in the process of coupling and coordinated development of digital finance and technological innovation, which will promote the coordinated development of central and western cities.

7. Discussion

7.1. Contributions

This paper has several significant contributions in the current sustainable economic development context.

Firstly, technological innovation is a key driver of economic growth, and this paper constructs the evaluation system of technological innovation and calculates the technological innovation development index by entropy method, providing a comprehensive assessment of the technological innovation level of different regions and a reference for future research.

Secondly, this study measures the coupling degree and coupling coordination degree between digital finance and technological innovation, and analyzes the time series characteristics, spatial differences, as well as space–time evolution characteristics of the coupling coordination. This provides a better understanding of how the coupling coordination development has evolved over time and across different regions.

Thirdly, the SNA method is adopted to investigate the spillover characteristics of the spatial association network of the coupling coordination between digital finance and technological innovation. Few papers have explored the coupling coordination between digital finance and technological innovation from a spatial network perspective, and this paper expands the research perspective and fills the research gap in the spatial network analysis, providing insights into the spatial characteristics of the coupling coordination and enriching the research paradigm in this field, and it is of great significance for policy-making and practical applications for regional development.

In summary, this research is one of the first to establish a spatial association network between digital finance and technological innovation, providing various insights into sustainable coordinated development and serving as a reference for future research. This paper may also have implications for other developing countries and regions facing similar challenges.

7.2. Limitations and Future Research

There are several limitations to the research discussed in this paper:

- (1)

Data source and quality: This study may experience problems with data quality, such as sample bias and limitations in data collection tools, as a result of the small sample size and constrained data collection techniques. To improve the quality of the research data, future studies can use a wider range of city data samples and more effective data analysis techniques.

- (2)

Research scope: This study only considers the impact of digital finance and technological innovation, ignoring other important factors because the number of variables is restricted by the coupling coordination degree (CCD) model. Future research could introduce an empirical regression model and add other, more comprehensive factors that can affect sustainable economic development as control variables.

- (3)

Research region: This study only focuses on a specific region in China and may not be directly generalizable to other regions or countries. Future research can expand the sample size by replicating the study in different countries and regions to confirm the generalizability of the findings. These findings can be compared with similar studies conducted in other regions or countries to identify similarities or differences in the results.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}