Information Technology Governance and Corporate Boards’ Relationship with Companies’ Performance and Earnings Management: A Longitudinal Approach

Abstract

:1. Introduction

2. Literature Review and Hypotheses Development

2.1. Theoretical Framework

2.2. CG/ITG Mechanisms, Financial Performance, and Earnings Management

2.3. Board ITG Mechanisms and Board Characteristics

2.4. Board-Level ITG and Firm Performance

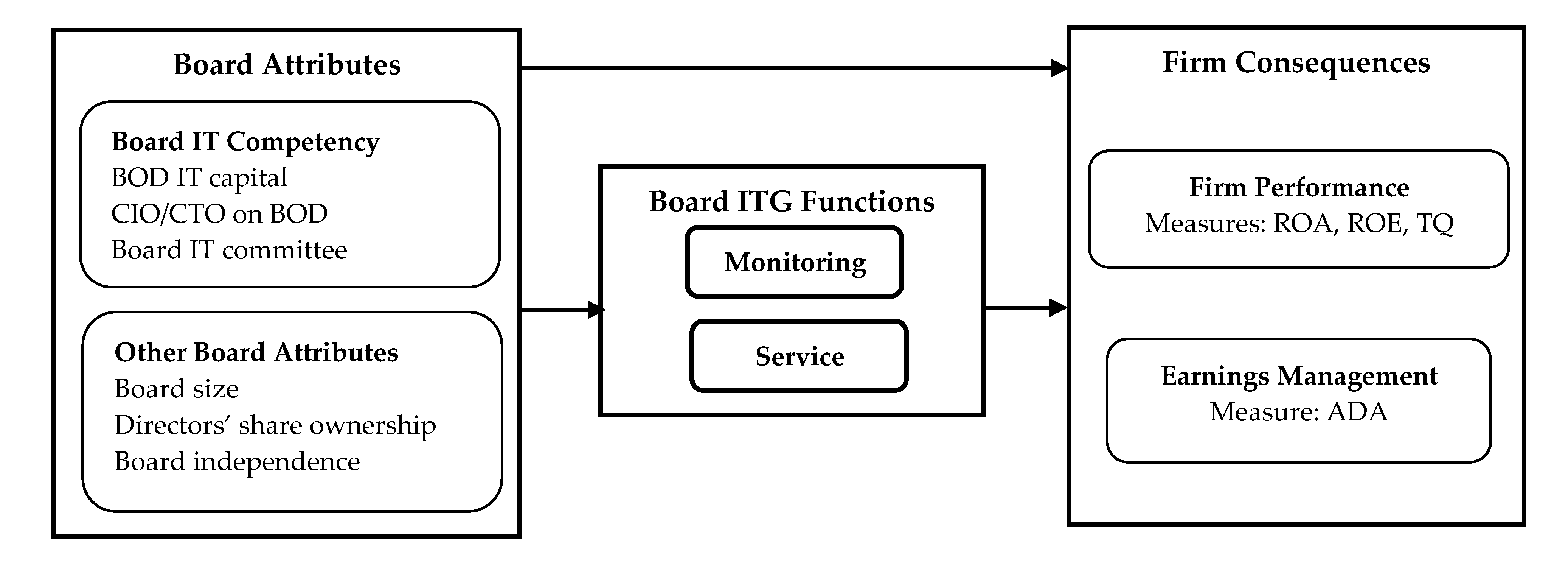

2.5. Hypotheses and Theoretical Model

3. Methodology

3.1. Data and Sample Selection

3.2. Variables and Measures

3.2.1. Dependent Variables

- ROAit = return on assets of the firm i for the year t;

- ROEit = return on equity of the firm i for the year t;

- TQit = Tobin’s Q of the firm i for the year t;

- BITCit = ratio of directors with IT capital on the board of the firm i for the year t;

- CITBit = CIO/CTO named as executive officer on the board of the firm i for the year t;

- ITCMit = number of board-level IT committees in the existence of the firm i for the year t;

- BSIZit = number of directors on the board of the firm i for the year t;

- DOWNit = percentage of shares owned by executive directors of the firm i for the year t;

- BINDit = percentage of independent directors on the board of the firm i for the year t;

- CSIZit = logarithm of the total assets of the firm i for the year t;

- FLEVit = total liabilities divided by total assets of the firm i for the year t; and

- εit = error term.

- TAit = total accruals for firm i in the year t;

- Ait−1 = net total assets for firm i in the year t−1;

- ∆REVit= change in revenue for firm i from the year t−1 to the year t;

- ∆ARit = change in accounts receivable for firm i from the year t−1 to the year t;

- PPEit = plant and equipment for firm i in the year t;

- εit = error term for firm i in the year t; and

- β1 and β2 = company-specific estimates.

- EXAt = earnings before extraordinary and abnormal items in year t; and

- OCFt = operating cash flow in year t.

- TAit = total accruals for firm i in the year t;

- Ait−1 = net total assets for firm i in the year t−1;

- ∆REVit= change in revenue for firm i from the year t−1 to the year t;

- ∆ARit = change in accounts receivable for firm i from the year t−1 to the year t;

- PPEit = plant and equipment for firm i in the year t;

- β0, β1, and β2 = company-specific estimates; and

- εit = error term for firm i in the year t.

- ADAit is EM measured using the modified Jones model [118];

- BITCit = ratio of directors with IT capital on the board of the firm i for the year t;

- CITBit = CIO/CTO named as executive officer on the board of the firm i for the year t;

- ITCMit = number of board-level IT committees in the existence of the firm i for the year t;

- BSIZit = number of directors on the board of the firm i for the year t;

- DOWNit = percentage of shares owned by executive directors of the firm i for the year t;

- BINDit = percentage of independent directors on the board of the firm i for the year t;

- CSIZit = logarithm of the total assets of the firm i for the year t;

- FLEVit = total liabilities divided by total assets of the firm i for the year t; and

- εit = error term.

3.2.2. Independent and Control Variables

4. Results and Discussion

4.1. Descriptive Statistics and Correlation Analysis

4.2. Empirical Results and Discussion

4.2.1. Multivariate Regression Results and Discussion

4.2.2. Robustness Analysis

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Ali, S.; Green, P. Effective Information Technology (IT) Governance Mechanisms: An IT Outsourcing Perspective. Inf. Syst. Front. 2012, 14, 179–193. [Google Scholar] [CrossRef]

- Sandulli, F.D.; Fernández-Menéndez, J.; Rodríguez-Duarte, A.; López-Sánchez, J.I. The Productivity Payoff of Information Technology in Multimarket SMEs. Small Bus. Econ. 2012, 39, 99–117. [Google Scholar] [CrossRef]

- Lazic, M. IT Governance and Business Performance—A Resource Based Analysis. In Proceedings of the Pacific Asia Conference on Information Systems (PACIS 2011), Brisbane, QLD, Australia, 7–11 July 2011. [Google Scholar]

- Hamdan, A.; Khamis, R.; Anasweh, M.; Al-Hashimi, M.; Razzaque, A. IT Governance and Firm Performance: Empirical Study From Saudi Arabia. SAGE Open 2019, 9, 178–194. [Google Scholar] [CrossRef] [Green Version]

- De Haes, S.; Van Grembergen, W. An Exploratory Study into IT Governance Implementations and Its Impact on Business/IT Alignment. Inf. Syst. Manag. 2009, 26, 123–137. [Google Scholar] [CrossRef]

- Lan, L.L.; Heracleous, L. Rethinking Agency Theory: The View from Law. Acad. Manag. Rev. 2010, 35, 294–314. [Google Scholar] [CrossRef] [Green Version]

- Dechow, P.M.; Hutton, A.P.; Kim, J.H.; Sloan, R.G. Detecting Earnings Management: A New Approach. J. Account. Res. 2012, 50, 275–334. [Google Scholar] [CrossRef]

- Juiz, C.; Duhamel, F.; Gutiérrez-Martínez, I.; Luna-Reyes, L.F. IT Managers’ Framing of IT Governance Roles and Responsibilities in Ibero-American Higher Education Institutions. Informatics 2022, 9, 68. [Google Scholar] [CrossRef]

- Li, C.; Lim, J.-H.; Wang, Q. Internal and External Influences on IT Control Governance. Int. J. Account. Inf. Syst. 2007, 8, 225–239. [Google Scholar] [CrossRef]

- ITGI. IT Control Objectives for Sarbanes-Oxley: The Role of IT in the Design, Implementation of Internal Control Over Financial Reporting; IT Governance Institute: Rolling Meadows, IL, USA, 2006. [Google Scholar]

- Weill, P.; Ross, J. IT Governance: How Top Performers Manage IT Decision Rights for Superior Results; Harvard Business School Press: Boston, MA, USA, 2004. [Google Scholar]

- Turel, O.; Liu, P.; Bart, C. Board-Level Information Technology Governance Effects on Organizational Performance: The Roles of Strategic Alignment and Authoritarian Governance Style. Inf. Syst. Manag. 2017, 34, 117–136. [Google Scholar] [CrossRef]

- Lunardi, G.L.; Becker, J.L.; Maçada, A.C.G.; Dolci, P.C. The Impact of Adopting IT Governance on Financial Performance: An Empirical Analysis among Brazilian Firms. Int. J. Account. Inf. Syst. 2014, 15, 66–81. [Google Scholar] [CrossRef]

- Estrada, C.F. Aligning Information Technology Within the Framework of Corporate Governance to Increase Corporate Value. Int. J. Manag. Inf. Syst. 2010, 14, 13–18. [Google Scholar] [CrossRef]

- Robertson, C.; Al-AlSheikh, S.; Al-Kahtani, A. An Analysis of Perceptions of Western Corporate Governance Principles in Saudi Arabia. Int. J. Public Adm. 2012, 35, 402–409. [Google Scholar] [CrossRef]

- Dawson, G.S.; Denford, J.S.; Williams, C.K.; Preston, D.; Desouza, K.C. An Examination of Effective IT Governance in the Public Sector Using the Legal View of Agency Theory. J. Manag. Inf. Syst. 2016, 33, 1180–1208. [Google Scholar] [CrossRef]

- Singh, H.P.; Agrawal, A.; Kaurav, R.P.S.; Kowitsthienchai, V. Prospects, Potential and Future of E-Governance in India and Thailand in Globalized Era. In Proceedings of the Second International Conference on Interdisciplinary Research and Development, Bangkok, Thailand, 31 May–2 June 2012; Interdisciplinary Network of the Royal Institute of Thailand: Bangkok, Thailand, 2012; pp. 1–4. [Google Scholar]

- Albassam, B.A. Does Saudi Arabia’s Economy Benefit from Foreign Investments? Benchmarking An Int. J. 2015, 22, 1214–1228. [Google Scholar] [CrossRef]

- Elage, A.; Mard, Y. Corporate Governance Code and Earnings Management: The French Case. Account. Audit. Control 2018, 24, 113–147. [Google Scholar]

- Benaroch, M.; Chernobai, A. Operational IT Failures, IT Value Destruction, and Board-Level IT Governance Changes. MIS Q. 2017, 41, 729–762. [Google Scholar] [CrossRef]

- Joshi, A.; Benitez, J.; Huygh, T.; Ruiz, L.; De Haes, S. Impact of IT Governance Process Capability on Business Performance: Theory and Empirical Evidence. Decis. Support Syst. 2022, 153, 113668. [Google Scholar] [CrossRef]

- Peng, M.W. Institutional Transitions and Strategic Choices. Acad. Manag. Rev. 2003, 28, 275–296. [Google Scholar] [CrossRef]

- Wu, M.; Coleman, M.; Bawuah, J. The Predictive Power of K-Nearest Neighbor (KNN): The Effect of Corporate Governance Mechanisms on Earnings Management. SAGE Open 2020, 10, 2158244020949537. [Google Scholar] [CrossRef]

- Zang, Z.; Zhu, Q.; Mogorrón-Guerrero, H. How Does R & D Investment Affect the Financial Performance of Cultural and Creative Enterprises? The Moderating Effect of Actual Controller. Sustainability 2019, 11, 297. [Google Scholar] [CrossRef] [Green Version]

- Al-Shattarat, B.; Hussainey, K.; Al-Shattarat, W. The Impact of Abnormal Real Earnings Management to Meet Earnings Benchmarks on Future Operating Performance. Int. Rev. Financ. Anal. 2022, 81, 101264. [Google Scholar] [CrossRef] [Green Version]

- Singh, H.P.; Alhamad, I.A. A Data Mining Approach to Predict Key Factors Impacting University Students Dropout in a Least Developed Economy. Arch. Bus. Res. 2022, 10, 48–59. [Google Scholar] [CrossRef]

- Singh, H.P.; Alhamad, I.A. A Novel Categorization of Key Predictive Factors Impacting Hotels’ Online Ratings: A Case of Makkah. Sustainability 2022, 14, 16588. [Google Scholar] [CrossRef]

- Wraikat, M.M. Information Technology Governance Role in Enhancing Performance: A Case Study on Jordan Public Sector. In Proceedings of the World Congress on Engineering and Computer Science, San Francisco, CA, USA, 20–22 October 2010; International Association of Engineers: San Francisco, CA, USA, 2010; pp. 1–6. [Google Scholar]

- Dutot, V.; Bergeron, F.; Calabrò, A. The Impact of Family Harmony on Family SMEs’ Performance: The Mediating Role of Information Technologies. J. Fam. Bus. Manag. 2022, 12, 1131–1151. [Google Scholar] [CrossRef]

- Khatib, S.F.A.; Abdullah, D.F.; Elamer, A.; Hazaea, S.A. The Development of Corporate Governance Literature in Malaysia: A Systematic Literature Review and Research Agenda. Corp. Gov. Int. J. Bus. Soc. 2022, 22, 1026–1053. [Google Scholar] [CrossRef]

- Menshawy, I.M.; Basiruddin, R.; Mohdali, R.; Qahatan, N. Board Information Technology Governance Mechanisms and Firm Performance among Iraqi Medium-Sized Enterprises: Do IT Capabilities Matter? J. Risk Financ. Manag. 2022, 15, 72. [Google Scholar] [CrossRef]

- Gajdosikova, D.; Valaskova, K.; Durana, P. Earnings Management and Corporate Performance in the Scope of Firm-Specific Features. J. Risk Financ. Manag. 2022, 15, 426. [Google Scholar] [CrossRef]

- Chakroun, S.; Ben Amar, A.; Ben Amar, A. Earnings Management, Financial Performance and the Moderating Effect of Corporate Social Responsibility: Evidence from France. Manag. Res. Rev. 2022, 45, 331–362. [Google Scholar] [CrossRef]

- Singh, H.P.; Alhulail, H.N. Predicting Student-Teachers Dropout Risk and Early Identification: A Four-Step Logistic Regression Approach. IEEE Access 2022, 10, 6470–6482. [Google Scholar] [CrossRef]

- Singh, H.P.; Singh, A.; Alam, F.; Agrawal, V. Impact of Sustainable Development Goals on Economic Growth in Saudi Arabia: Role of Education and Training. Sustainability 2022, 14, 14119. [Google Scholar] [CrossRef]

- Singh, A.; Singh, H.P.; Alam, F.; Agrawal, V. Role of Education, Training, and E-Learning in Sustainable Employment Generation and Social Empowerment in Saudi Arabia. Sustainability 2022, 14, 8822. [Google Scholar] [CrossRef]

- Alam, F.; Singh, H.P.; Singh, A. Economic Growth in Saudi Arabia through Sectoral Reallocation of Government Expenditures. SAGE Open 2022, 12, 215824402211271. [Google Scholar] [CrossRef]

- Dalwai, T.A.R.; Basiruddin, R.; Abdul Rasid, S.Z. A Critical Review of Relationship between Corporate Governance and Firm Performance: GCC Banking Sector Perspective. Corp. Gov. 2015, 15, 18–30. [Google Scholar] [CrossRef]

- Fama, E.F.; Jensen, M.C. Separation of Ownership and Control. J. Law Econ. 1983, 26, 301–325. [Google Scholar] [CrossRef]

- Ahmed, K.; Henry, D. Accounting Conservatism and Voluntary Corporate Governance Mechanisms by Australian Firms. Account. Financ. 2012, 52, 631–662. [Google Scholar] [CrossRef]

- Jensen, M.C.; Meckling, W.H. Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Kothari, S.P.; Leone, A.J.; Wasley, C.E. Performance Matched Discretionary Accrual Measures. J. Account. Econ. 2005, 39, 163–197. [Google Scholar] [CrossRef]

- Leggett, D.; Parsons, L.M.; Reitenga, A.L. Real Earnings Management and Subsequent Operating Performance. IUP J. Oper. Manag. 2016, 15, 7–32. [Google Scholar] [CrossRef]

- Al-ahdal, W.M.; Hashim, H.A. Impact of Audit Committee Characteristics and External Audit Quality on Firm Performance: Evidence from India. Corp. Gov. Int. J. Bus. Soc. 2022, 22, 424–445. [Google Scholar] [CrossRef]

- So, I.G.; Haron, H.; Gui, A.; Princes, E.; Sari, S.A. Sustainability Reporting Disclosure in Islamic Corporates: Do Human Governance, Corporate Governance, and IT Usage Matter? Sustainability 2021, 13, 13023. [Google Scholar] [CrossRef]

- Ho, J.L.Y.; Wu, A.; Xu, S.X. Corporate Governance and Returns on Information Technology Investment: Evidence from an Emerging Market. Strateg. Manag. J. 2011, 32, 595–623. [Google Scholar] [CrossRef]

- Matta, M.; Cavusoglu, H.; Benbasat, I. Understanding the Board’s Involvement in Information Technology Governance. Inf. Syst. Manag. 2022, 127–147. [Google Scholar] [CrossRef]

- Priyadarsini, A.; Kumar, A. A Literature Review on IT Governance Using Systematicity and Transparency Framework. Digit. Policy, Regul. Gov. 2022, 24, 309–328. [Google Scholar] [CrossRef]

- Muhammad, J.S.; Miah, S.J.; Isa, A.M.; Samsudin, A.Z.H. Investigating Importance and Key Factors for Information Governance Implementation in Nigerian Universities. Educ. Inf. Technol. 2022, 27, 5551–5571. [Google Scholar] [CrossRef]

- Jewer, J.; McKay, K.N. Antecedents and Consequences of Board IT Governance: Institutional and Strategic Choice Perspectives. J. Assoc. Inf. Syst. 2012, 13, 581–617. [Google Scholar] [CrossRef] [Green Version]

- Wu, J.-H.; Lin, L.-M.; Rai, A.; Chen, Y.-C. How Health Care Delivery Organizations Can Exploit EHealth Innovations: An Integrated Absorptive Capacity and IT Governance Explanation. Int. J. Inf. Manag. 2022, 65, 102508. [Google Scholar] [CrossRef]

- Da Cunha, P.R.; Piccoli, M.R. Influence of Board Interlocking on Earnings Management. Rev. Contab. Finanças 2017, 28, 179–196. [Google Scholar] [CrossRef] [Green Version]

- Hillman, A.J.; Dalziel, T. Boards of Directors and Firm Performance: Integrating Agency and Resource Dependence Perspectives. Acad. Manag. Rev. 2003, 28, 383–396. [Google Scholar] [CrossRef]

- Khamees, B.A. Information Technology Governance and Bank Performance: A Situational Approach. Int. J. Financ. Stud. 2023, 11, 44. [Google Scholar] [CrossRef]

- Nolan, R.L.; McFarlan, F.W. Information Technology and the Board of Directors. Harv. Bus. Rev. 2005, 83, 96–106. [Google Scholar]

- Islam, M.S.; Stafford, T. Board-Level Security Expertise Information Technology (IT) Integration and Cybersecurity/Security: The Security Savviness of Board of Directors Emergent Research Forum Paper. In Proceedings of the Twenty-third Americas Conference on Information Systems, Boston, MA, USA, 10–12 August 2017; pp. 1–5. [Google Scholar]

- Andriole, S.J. Boards of Directors and Technology Governance: The Surprising State of Th Practice. Commun. Assoc. Inf. Syst. 2009, 24, 373–394. [Google Scholar] [CrossRef]

- Farooq, M.; Noor, A.; Ali, S. Corporate Governance and Firm Performance: Empirical Evidence from Pakistan. Corp. Gov. Int. J. Bus. Soc. 2022, 22, 42–66. [Google Scholar] [CrossRef]

- Davis, J.H.; Schoorman, F.D.; Donaldson, L. Toward A Stewardship Theory of Management. Acad. Manag. Rev. 1997, 22, 20–47. [Google Scholar] [CrossRef]

- Donaldson, L.; Davis, J.H. Stewardship Theory or Agency Theory: CEO Governance and Shareholder Returns. Aust. J. Manag. 1991, 16, 49–64. [Google Scholar] [CrossRef] [Green Version]

- Wen, M. Corporate Governance and Firm Performance. China Boom Discontents 2005, 10, 484–489. [Google Scholar] [CrossRef]

- Leventis, S.; Dimitropoulos, P. The Role of Corporate Governance in Earnings Management: Experience from US Banks. J. Appl. Account. Res. 2012, 13, 161–177. [Google Scholar] [CrossRef]

- Anglin, P.; Edelstein, R.; Gao, Y.; Tsang, D. What Is the Relationship Between REIT Governance and Earnings Management? J. Real Estate Financ. Econ. 2013, 47, 538–563. [Google Scholar] [CrossRef]

- Elghuweel, M.I.; Ntim, C.G.; Opong, K.K.; Avison, L. Corporate Governance, Islamic Governance and Earnings Management in Oman: A New Empirical Insights from a Behavioural Theoretical Framework. J. Account. Emerg. Econ. 2017, 7, 190–224. [Google Scholar] [CrossRef] [Green Version]

- Kwon, S.S.; Wang, H.; Nasreen, T. The Impact of Technology and Regulatory Changes on the Relationship between a Firm’s External Governance Index and Its Financial Performance and Earnings Management. J. Forensic Investig. Account. 2015, 7, 178–223. [Google Scholar] [CrossRef]

- Hamdan, A.; Ahmed, E. The Impact of Corporate Governance on Firm Performance: Evidence from Bahrain Bourse. Int. Manag. Rev. 2015, 11, 21–37. [Google Scholar]

- Al-Ghamdi, M.; Rhodes, M. Family Ownership, Corporate Governance and Performance: Evidence from Saudi Arabia. Int. J. Econ. Financ. 2015, 7, 78–89. [Google Scholar] [CrossRef] [Green Version]

- Sami, H.; Wang, J.; Zhou, H. Corporate Governance and Operating Performance of Chinese Listed Firms. J. Int. Account. Audit. Tax. 2011, 20, 106–114. [Google Scholar] [CrossRef]

- Safari, M.; Mirshekary, S.; Wise, V. Compliance with Corporate Governance Principles: Australian Evidence. Australas. Account. Bus. Financ. J. 2015, 9, 3–19. [Google Scholar] [CrossRef]

- Ria, R. Determinant Factors of Corporate Governance on Company Performance: Mediating Role of Capital Structure. Sustainability 2023, 15, 2309. [Google Scholar] [CrossRef]

- Liang, T.-P.; Chiu, Y.-C.; Wu, S.P.J.; Straub, D. The Impact of IT Governance on Organizational Performance. In Proceedings of the 17th Americas Conference on Information Systems (AMCIS 2011), Detroit, MI, USA, 4–8 August 2011; Association for Information Systems: Detroit, MI, USA, 2011. [Google Scholar]

- Shapiro, D.; Tang, Y.; Wang, M.; Zhang, W. The Effects of Corporate Governance and Ownership on the Innovation Performance of Chinese SMEs. J. Chinese Econ. Bus. Stud. 2015, 13, 311–335. [Google Scholar] [CrossRef]

- Hussainey, K.; Al-Najjar, B. Understanding the Determinants of RiskMetrics/ISS Ratings of the Quality of UK Companies’ Corporate Governance Practice. Can. J. Adm. Sci. Rev. Can. Sci. l’Administration 2012, 29, 366–377. [Google Scholar] [CrossRef] [Green Version]

- Capurro, R.; Fiorentino, R.; Galeotti, R.M.; Garzella, S. The Impact of Digitalization and Sustainability on Governance Structures and Corporate Communication: A Cross-Industry and Cross-Country Approach. Sustainability 2023, 15, 2064. [Google Scholar] [CrossRef]

- Mohd Noor, N.; Rasli, A.; Abdul Rashid, M.A.; Mubarak, M.F.; Abas, I.H. Ranking of Corporate Governance Dimensions: A Delphi Study. Adm. Sci. 2022, 12, 173. [Google Scholar] [CrossRef]

- Christensen, J.; Kent, P.; Routledge, J.; Stewart, J. Do Corporate Governance Recommendations Improve the Performance and Accountability of Small Listed Companies? Account. Financ. 2015, 55, 133–164. [Google Scholar] [CrossRef]

- Haes, S.D.; Joshi, A.; Huygh, T.; Jansen, S. Exploring How Corporate Governance Codes Address IT Governance. ISACA J. 2017, 4, 1–7. [Google Scholar]

- Raghupathi, W. Corporate Governance of IT. Commun. ACM 2007, 50, 94–99. [Google Scholar] [CrossRef]

- Mohamed, N.; Kaur a/p Gian Singh, J. A Conceptual Framework for Information Technology Governance Effectiveness in Private Organizations. Inf. Manag. Comput. Secur. 2012, 20, 88–106. [Google Scholar] [CrossRef]

- Scheeren, A.W.; Fontes-Filho, J.R.; Tavares, E. Impacts of a Relationship Model on Informational Technology Governance: An Analysis of Managerial Perceptions in Brazil. J. Inf. Syst. Technol. Manag. 2013, 10, 621–642. [Google Scholar] [CrossRef] [Green Version]

- Ghani, E.K.; Azemi, N.A.H.; Puspitasari, E. The Effect of Information Asymmetry and Environmental Uncertainty on Earnings Management Practices among Malaysian Technology-Based Firms. Int. J. Acad. Res. Econ. Manag. Sci. 2017, 6, 178–194. [Google Scholar] [CrossRef] [Green Version]

- Parent, M.; Reich, B.H. Governing Information Technology Risk. Calif. Manag. Rev. 2009, 51, 134–152. [Google Scholar] [CrossRef]

- Wilkin, C.L.; Chenhall, R.H. A Review of IT Governance: A Taxonomy to Inform Accounting Information Systems. J. Inf. Syst. 2010, 24, 107–146. [Google Scholar] [CrossRef]

- Haislip, J.Z.; Masli, A.; Richardson, V.J.; Sanchez, J.M. Repairing Organizational Legitimacy Following Information Technology (IT) Material Weaknesses: Executive Turnover, IT Expertise, and IT System Upgrades. J. Inf. Syst. 2016, 30, 41–70. [Google Scholar] [CrossRef]

- Saudi Arabia Corporate Governance Regulations. Corporate Governance Regulations in the Kingdom of Saudi Arabia; Capital Market Authority: Riyadh, Saudi Arabia, 2022. [Google Scholar]

- Chen, J.J.; Zhang, H. The Impact of the Corporate Governance Code on Earnings Management—Evidence from Chinese Listed Companies. Eur. Financ. Manag. 2014, 20, 596–632. [Google Scholar] [CrossRef]

- Héroux, S.; Fortin, A. Exploring the Influence of Executive Management Diversity on IT Governance. J. Inf. Syst. Technol. Manag. 2017, 14, 401–429. [Google Scholar] [CrossRef] [Green Version]

- Wong, Y.C.; Bajuri, N.H. Corporate Governance: Board Structure, Information Technology and CSR Reporting. J. Teknol. 2013, 64, 109–113. [Google Scholar] [CrossRef] [Green Version]

- Karimi, J.; Bhattacherjee, A.; Gupta, Y.P.; Somers, T.M. The Effects of MIS Steering Committees on Information Technology Management Sophistication. J. Manag. Inf. Syst. 2000, 17, 207–230. [Google Scholar] [CrossRef]

- Weill, P.; Ross, J.W. A Matrixed Approach to Designing IT Governance. Sloan Manag. Rev. 2005, 46, 26–34. [Google Scholar]

- Higgs, J.L.; Pinsker, R.E.; Smith, T.J.; Young, G.R. The Relationship between Board-Level Technology Committees and Reported Security Breaches. J. Inf. Syst. 2016, 30, 79–98. [Google Scholar] [CrossRef]

- Chakravarty, A.; Grewal, R.; Sambamurthy, V. Information Technology Competencies, Organizational Agility, and Firm Performance: Enabling and Facilitating Roles. Inf. Syst. Res. 2013, 24, 976–997. [Google Scholar] [CrossRef]

- Ghasemaghaei, M.; Ebrahimi, S.; Hassanein, K. Data Analytics Competency for Improving Firm Decision Making Performance. J. Strateg. Inf. Syst. 2018, 27, 101–113. [Google Scholar] [CrossRef]

- Kobelsky, K.W.; Richardson, V.J.; Smith, R.E.; Zmud, R.W. Determinants and Consequences of Firm Information Technology Budgets. Account. Rev. 2008, 83, 957–995. [Google Scholar] [CrossRef]

- Henderson, B.C.; Kobelsky, K.; Richardson, V.; Smith, R.E. The Relevance of Information Technology Expenditures. J. Inf. Syst. 2010, 24, 39–77. [Google Scholar] [CrossRef]

- Chau, D.C.K.; Ngai, E.W.T.; Gerow, J.E.; Thatcher, J.B. The Effects of Business-IT Strategic Alignment and IT Governance on Firm Performance: A Moderated Polynomial Regression Analysis. MIS Q. 2020, 44, 1679–1703. [Google Scholar] [CrossRef]

- Al-Thuneibat, A.A.; Al-Angari, H.A.; Al-Saad, S.A. The Effect of Corporate Governance Mechanisms on Earnings Management: Evidence from Saudi Arabia. Rev. Int. Bus. Strateg. 2016, 26, 2–32. [Google Scholar] [CrossRef]

- Widharto, P.; Suhatman, Z.; Aji, R.F. Measurement of Information Technology Governance Capability Level: A Case Study of PT Bank BBS. TELKOMNIKA Telecommun. Comput. Electron. Control. 2022, 20, 296. [Google Scholar] [CrossRef]

- Ilmudeen, A. Information Technology (IT) Governance and IT Capability to Realize Firm Performance: Enabling Role of Agility and Innovative Capability. Benchmarking Int. J. 2022, 29, 1137–1161. [Google Scholar] [CrossRef]

- Solana-González, P.; Vanti, A.A.; García Lorenzo, M.M.; Bello Pérez, R.E. Data Mining to Assess Organizational Transparency across Technology Processes: An Approach from IT Governance and Knowledge Management. Sustainability 2021, 13, 10130. [Google Scholar] [CrossRef]

- Liu, Y.; Lee, Y.; Chen, A.N.K. How IT Wisdom Affects Firm Performance: An Empirical Investigation of 15-Year US Panel Data. Decis. Support Syst. 2020, 133, 113300. [Google Scholar] [CrossRef]

- Florackis, C. Agency Costs and Corporate Governance Mechanisms: Evidence for UK Firms. Int. J. Manag. Financ. 2008, 4, 37–59. [Google Scholar] [CrossRef] [Green Version]

- Carr, N.G. IT Doesn’t Matter. Harv. Bus. Rev. 2003, 81, 41–49. [Google Scholar] [CrossRef]

- Kaur, J.; Mohamed, N.; Ahlan, A.R. Modeling the Impact of Information Technology Governance Effectiveness Using Partial Least Square. In Proceedings of the 2012 International Conference on Statistics in Science, Business and Engineering (ICSSBE), Langkawi, Malaysia, 10–12 September 2012; IEEE: Langkawi, Malaysia, 2012; pp. 1–5. [Google Scholar]

- Boritz, E.; Lim, J.-H. Impact of Top Management’s IT Knowledge and IT Governance Mechanisms on Financial Performance. In Proceedings of the 28th International Conference on Information Systems (ICIS), Montreal, QC, Canada, 9–12 December 2007; Association for Information Systems: Montreal, QC, Canada, 2007; pp. 1–16. [Google Scholar]

- Hamdan, B. Examining the Antecedents of Sarbanes-Oxley Section 404 IT Control Weaknesses: An Empirical Study. In Proceedings of the Thirty Second International Conference on Information Systems, Shanghai, China, 4–7 December 2011; Association for Information Systems: Shanghai, China, 2011; pp. 1–14. [Google Scholar]

- Preston, D.S.; Chen, D.; Leidner, D.E. Examining the Antecedents and Consequences of CIO Strategic Decision-Making Authority: An Empirical Study. Decis. Sci. 2008, 39, 605–642. [Google Scholar] [CrossRef]

- Grada, M.S. Longitudinal Approach to the Study of Corporate Governance Code and Earnings Management Relationship: The Case of Saudi Arabia. J. Account. Emerg. Econ. 2022, 12, 615–644. [Google Scholar] [CrossRef]

- Becht, M.; Bolton, P.; Röell, A. Corporate Governance and Control. In Handbook of the Economics of Finance; Constantinides, G.M., Harris, M., Stulz, R.M., Eds.; Elsevier: Amsterdam, The Netherlands, 2003; pp. 1–109. ISBN 978-0-444-51362-5. [Google Scholar]

- Carney, M. Corporate Governance and Competitive Advantage in Family–Controlled Firms. Entrep. Theory Pract. 2005, 29, 249–265. [Google Scholar] [CrossRef]

- Jacoby, G.; Liu, M.; Wang, Y.; Wu, Z.; Zhang, Y. Corporate Governance, External Control, and Environmental Information Transparency: Evidence from Emerging Markets. J. Int. Financ. Mark. Inst. Money 2019, 58, 269–283. [Google Scholar] [CrossRef]

- Peasnell, K.V.; Pope, P.F.; Young, S. Board Monitoring and Earnings Management: Do Outside Directors Influence Abnormal Accruals? J. Bus. Financ. Account. 2005, 32, 1311–1346. [Google Scholar] [CrossRef]

- El-Chaarani, H.; Abraham, R.; Khalife, D.; Salameh-Ayanian, M. Corporate Governance Effects on Bank Profits in Gulf Cooperation Council Countries during the Pandemic. Int. J. Financ. Stud. 2023, 11, 36. [Google Scholar] [CrossRef]

- Al-Matari, E.M.; Al-Swidi, A.K.; Fadzil, F.H.B. The Measurements of Firm Performance’s Dimensions. Asian J. Financ. Account. 2014, 6, 24. [Google Scholar] [CrossRef]

- Cordeiro da Cunha Araújo, R.; André Veras Machado, M. Book-to-Market Ratio, Return on Equity and Brazilian Stock Returns. RAUSP Manag. J. 2018, 53, 324–344. [Google Scholar] [CrossRef]

- Wernerfelt, B.; Montgomery, C.A. Tobin’s q and the Importance of Focus in Firm Performance. Am. Econ. Rev. 1988, 78, 246–250. [Google Scholar]

- Bharadwaj, A.S.; Bharadwaj, S.G.; Konsynski, B.R. Information Technology Effects on Firm Performance as Measured by Tobin’s Q. Manag. Sci. 1999, 45, 1008–1024. [Google Scholar] [CrossRef]

- Dechow, P.; Sloan, R.; Sweeney, A. Detecting Earnings Management. Account. Rev. 1995, 70, 193–225. [Google Scholar]

- Al-Bassam, W.M.; Ntim, C.G.; Opong, K.K.; Downs, Y. Corporate Boards and Ownership Structure as Antecedents of Corporate Governance Disclosure in Saudi Arabian Publicly Listed Corporations. Bus. Soc. 2018, 57, 335–377. [Google Scholar] [CrossRef]

- Saona, P.; Muro, L.; Alvarado, M. How Do the Ownership Structure and Board of Directors’ Features Impact Earnings Management? The Spanish Case. J. Int. Financ. Manag. Account. 2020, 31, 98–133. [Google Scholar] [CrossRef] [Green Version]

- Cohen, D.A.; Zarowin, P. Accrual-Based and Real Earnings Management Activities around Seasoned Equity Offerings. J. Account. Econ. 2010, 50, 2–19. [Google Scholar] [CrossRef] [Green Version]

- Outa, E.R.; Eisenberg, P.; Ozili, P.K. The Impact of Corporate Governance Code on Earnings Management in Listed Non-Financial Firms. J. Account. Emerg. Econ. 2017, 7, 428–444. [Google Scholar] [CrossRef]

- Bernerth, J.B.; Aguinis, H. A Critical Review and Best-Practice Recommendations for Control Variable Usage. Pers. Psychol. 2016, 69, 229–283. [Google Scholar] [CrossRef]

- Prasastine, S.A.; Yulianto, A. Good Corporate Governance and Leverage Control Variables at Agency Cost: Non Financial Companies in Indonesia. Manag. Anal. J. 2022, 11, 227–239. [Google Scholar]

- Naiker, V.; Navissi, F.; Sridharan, V. The Agency Cost Effects of Unionization on Firm Value. J. Manag. Account. Res. 2008, 20, 133–152. [Google Scholar] [CrossRef]

- Buallay, A.; Hamdan, A.; Zureigat, Q. Corporate Governance and Firm Performance: Evidence from Saudi Arabia. Australas. Account. Bus. Financ. J. 2017, 11, 78–98. [Google Scholar] [CrossRef] [Green Version]

- Bendig, D.; Wagner, R.; Jung, C.; Nüesch, S. When and Why Technology Leadership Enters the C-Suite: An Antecedents Perspective on CIO Presence. J. Strateg. Inf. Syst. 2022, 31, 101705. [Google Scholar] [CrossRef]

- Schober, P.; Boer, C.; Schwarte, L.A. Correlation Coefficients. Anesth. Analg. 2018, 126, 1763–1768. [Google Scholar] [CrossRef]

- Ratner, B. The Correlation Coefficient: Its Values Range between +1/−1, or Do They? J. Targeting Meas. Anal. Mark. 2009, 17, 139–142. [Google Scholar] [CrossRef] [Green Version]

- Coles, J.; Daniel, N.; Naveen, L. Boards: Does One Size Fit All? J. Financ. Econ. 2008, 87, 329–356. [Google Scholar] [CrossRef] [Green Version]

- Vassalou, M.; Xing, Y. Default Risk in Equity Returns. J. Financ. 2004, 59, 831–868. [Google Scholar] [CrossRef]

- Hair, J.F.; Ringle, C.M.; Sarstedt, M. PLS-SEM: Indeed a Silver Bullet. J. Mark. Theory Pract. 2011, 19, 139–152. [Google Scholar] [CrossRef]

- Hair, J.F.; Hult, G.T.M.; Ringle, C.M.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM); Thousand, O., Ed.; SAGE Publications: Thousand Oaks, CA, USA, 2016. [Google Scholar]

- Gujarati, D.N.; Porter, D.C. Basic Econometrics, 5th ed.; McGraw-Hill Irwin: New York, NY, USA, 2009. [Google Scholar]

- Halunga, A.G.; Orme, C.D.; Yamagata, T. A Heteroskedasticity Robust Breusch–Pagan Test for Contemporaneous Correlation in Dynamic Panel Data Models. J. Econom. 2017, 198, 209–230. [Google Scholar] [CrossRef] [Green Version]

- Bhimavarapu, V.M.; Rastogi, S.; Abraham, R. The Influence of Transparency and Disclosure on the Valuation of Banks in India: The Moderating Effect of Environmental, Social, and Governance Variables, Shareholder Activism, and Market Power. J. Risk Financ. Manag. 2022, 15, 612. [Google Scholar] [CrossRef]

- Habbash, M.; Alghamdi, S. Audit Quality and Earnings Management in Less Developed Economies: The Case of Saudi Arabia. J. Manag. Gov. 2017, 21, 351–373. [Google Scholar] [CrossRef]

- Abdallah, A.A.-N.; Ismail, A.K. Corporate Governance Practices, Ownership Structure, and Corporate Performance in the GCC Countries. J. Int. Financ. Mark. Inst. Money 2017, 46, 98–115. [Google Scholar] [CrossRef]

- Jabbouri, I. Determinants of Corporate Dividend Policy in Emerging Markets: Evidence from MENA Stock Markets. Res. Int. Bus. Financ. 2016, 37, 283–298. [Google Scholar] [CrossRef]

- Al-Najjar, B.; Clark, E. Corporate Governance and Cash Holdings in MENA: Evidence from Internal and External Governance Practices. Res. Int. Bus. Financ. 2017, 39, 1–12. [Google Scholar] [CrossRef] [Green Version]

- Bellemare, M.F.; Masaki, T.; Pepinsky, T.B. Lagged Explanatory Variables and the Estimation of Causal Effect. J. Polit. 2017, 79, 949–963. [Google Scholar] [CrossRef]

- Brüderl, J.; Ludwig, V. Fixed-Effects Panel Regression. In The SAGE Handbook of Regression Analysis and Causal Inference; Best, H., Wolf, C., Eds.; SAGE Publications Ltd: London, UK, 2014; pp. 327–358. [Google Scholar]

- Wintoki, M.B.; Linck, J.S.; Netter, J.M. Endogeneity and the Dynamics of Internal Corporate Governance. J. Financ. Econ. 2012, 105, 581–606. [Google Scholar] [CrossRef]

- Jackling, B.; Johl, S. Board Structure and Firm Performance: Evidence from India’s Top Companies. Corp. Gov. An Int. Rev. 2009, 17, 492–509. [Google Scholar] [CrossRef]

{kind=link}

| Sector | Sample | Percentage (%) | Total Observations |

|---|---|---|---|

| Petrochemicals | 11 | 7.14 | 1287 |

| Retail | 14 | 9.09 | 1638 |

| Cement | 12 | 7.79 | 1404 |

| Agriculture and Food | 14 | 9.09 | 1638 |

| Telecom and IT | 4 | 2.60 | 468 |

| Energy and Utilities | 2 | 1.30 | 234 |

| Hotels and Tourism | 4 | 2.60 | 468 |

| Industrial Investment | 13 | 8.44 | 1521 |

| Building Construction | 15 | 9.74 | 1755 |

| Multi-investment | 7 | 4.55 | 819 |

| Transport | 5 | 3.25 | 585 |

| Real Estate Development | 8 | 5.19 | 936 |

| Media and Publishing | 3 | 1.95 | 351 |

| Healthcare Services | 6 | 3.90 | 702 |

| Consumer Durables and Apparel | 9 | 5.84 | 1053 |

| Commercial and Professional Services | 7 | 4.55 | 819 |

| Metals and Mining | 10 | 6.49 | 1170 |

| Capital Goods | 10 | 6.49 | 1170 |

| Total | 154 | 100 | 18,018 |

| Variable | Definition/Measurement |

|---|---|

| Dependent Variables | |

| Firm Performance | |

| Return on Asset (ROA) (Operational) | Operating income divided by total assets at the start of the year |

| Return on Equity (ROE) (Financial) | Net income divided by total equity at the start of the year |

| Tobin’s Q (TQ) (Market-based) | The ratio of the market value of an asset to its replacement cost |

| Transparency | |

| Earnings management (ADA) | Total accruals less non-discretionary accruals |

| Independent Variables | |

| Board IT Competence | |

| Board IT Capital (BITC) | The ratio of directors with IT capital |

| CIO/CTO on Board (CITB) | 1 if CIO/CTO is an executive member of the board, 0 otherwise |

| IT Committee (ITCM) | 1 if the board IT committee exists, 0 otherwise |

| Other Corporate Governance | |

| Board size (BSIZ) | Total number of BOD members |

| Director (Exe.) ownership (DOWN) | Percentage of shares held by executive directors |

| Board independence (BIND) | Percentage of independent directors on the BOD |

| Control Variables | |

| Company Size (CSIZ) | The logarithm of the company’s total assets |

| Financial leverage (FLEV) | The ratio of total debt to total assets |

| Variables | Mean | Min | Max | Std. Dev. | Coefficient of Variation |

|---|---|---|---|---|---|

| Dependent Variables | |||||

| ROA | 0.061 | −0.118 | 0.138 | 0.073 | 1.197 |

| ROE | 0.097 | −0.238 | 0.161 | 0.123 | 1.268 |

| Tobin’s Q (TQ) | 1.971 | 0.021 | 2.024 | 0.594 | 0.301 |

| ADA | 0.148 | 0.117 | 0.199 | 0.029 | 0.196 |

| Independent Variables | |||||

| Board IT Capital (BITC) | 0.169 | 0 | 0.202 | 0.046 | 0.272 |

| CIO/CTO on Board (CITB) | 0.095 | 0 | 1 | 0.275 | 2.895 |

| IT Committee (ITCM) | 0.077 | 0 | 1 | 0.287 | 3.727 |

| Board size (BSIZ) | 9.588 | 6 | 12 | 1.548 | 0.161 |

| Director (Exe.) ownership (DOWN) | 0.214 | 0.005 | 0.398 | 0.097 | 0.453 |

| Board independence (BIND) | 0.694 | 0.379 | 0.806 | 0.115 | 0.166 |

| Control Variables | |||||

| Company Size (CSIZ) | 14.396 | 2.556 | 18.581 | 4.089 | 0.284 |

| Financial leverage (FLEV) | 0.091 | 0.012 | 0.592 | 0.169 | 1.857 |

| ROA | ROE | TQ | ADA | BITC | CITB | ITCM | BSIZ | DOWN | BIND | CSIZ | FLEV | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ROA | 1 | |||||||||||

| ROE | 0.269 *** | 1 | ||||||||||

| TQ | 0.281 * | 0.331 | 1 | |||||||||

| ADA | 0.369 | −0.343 *** | 0.261 | 1 | ||||||||

| BITC | 0.201 | 0.349 | 0.334 ** | 0.352 * | 1 | |||||||

| CITB | 0.276 *** | 0.297 | 0.294 | 0.335 ** | 0.432 | 1 | ||||||

| ITCM | 0.303 ** | 0.328 | 0.273 | −0.316 | 0.357 *** | 0.368 *** | 1 | |||||

| BSIZ | 0.364 | 0.367 *** | 0.358 *** | 0.354 | 0.422 | 0.359 | 0.329 *** | 1 | ||||

| DOWN | 0.342 | 0.385 | 0.318 | 0.359 ** | 0.372 ** | 0.381 | 0.386 * | 0.418 | 1 | |||

| BIND | 0.379 | 0.345 | 0.315 | 0.291 | 0.388 ** | 0.347 *** | 0.372 * | 0.385 | 0.275 | 1 | ||

| CSIZ | 0.378 *** | 0.376 | 0.374 | 0.361 *** | 0.377 ** | 0.365 | 0.228 *** | 0.338 ** | 0.346 ** | 0.379 | 1 | |

| FLEV | −0.335 | 0.355 *** | 0.384 * | 0.327 | 0.386 | 0.353 ** | 0.375 ** | −0.425 ** | 0.365 | 0.368 * | 0.293 | 1 |

| Variables | Multicollinearity (VIF Test) | Heteroscedasticity (Breusch–Pagan and Koenker Test) |

|---|---|---|

| ROA | 3.692 | 0.038 |

| ROE | 2.516 | 0.025 |

| Tobin’s Q (TQ) | 2.952 | 0.018 |

| Earnings Management (ADA) | 3.696 | 0.008 |

| Board IT Capital (BITC) | 2.208 | 0.006 |

| CIO/CTO on Board (CITB) | 2.409 | 0.035 |

| IT Committee (ITCM) | 2.016 | 0.033 |

| Board Size (BSIZ) | 3.598 | 0.007 |

| Director (Exe.) Ownership (DOWN) | 3.062 | 0.029 |

| Board Independence (BIND) | 2.656 | 0.029 |

| Company Size (CSIZ) | 1.785 | 0.009 |

| Financial Leverage (FLEV) | 2.935 | 0.024 |

| Model 1 (ROA) | Model 2 (ROE) | Model 3 (TQ) | Model 4 (ADA) | |||||

|---|---|---|---|---|---|---|---|---|

| Variable | β | T-Stat (Std. Error) | β | T-Stat (Std. Error) | β | T-Stat (Std. Error) | β | T-Stat (Std. Error) |

| Board IT Competency Variables | ||||||||

| BITC | 2.626 | 2.167 ** (1.212) | 1.986 | 1.544 (1.286) | 2.227 | 1.621 (1.374) | 2.347 | 1.648 (1.424) |

| CITB | 2.284 | 2.628 *** (0.869) | 1.467 | 1.591 (0.922) | 1.782 | 1.633 (1.091) | 2.046 | 1.626 (1.258) |

| ITCM | 1.112 | 2.079 ** (0.535) | 1.845 | 1.616 (1.142) | 1.474 | 1.362 (1.082) | −2.173 | −2.046 (1.062) ** |

| Other Corporate Governance Variables | ||||||||

| BSIZ | −1.816 | −1.633 (1.112) | 0.994 | 1.511 (0.658) | 1.312 | 1.944 * (0.675) | 2.143 | 2.079 ** (1.031) |

| DOWN | −1.104 | −1.612 (0.685) | −0.976 | −1.307 (0.747) | 1.992 | 1.004 (1.985) | 2.197 | 1.775 * (1.238) |

| BIND | 2.098 | 1.597 (1.314) | 1.108 | 1.554 (0.713) | 0.913 | 1.545 (0.591) | −2.184 | −1.631 (1.339) |

| Control Variables | ||||||||

| CSIZ | −1.906 | −1.459 (1.306) | 1.418 | 1.507 (0.941) | −2.246 | −1.614 (1.392) | 2.285 | 1.578 (1.448) |

| FLEV | −1.693 | −1.647 (1.028) | 1.979 | 1.539 (1.286) | −1.405 | −1.471 (0.955) | 2.292 | 1.546 (1.483) |

| R2 | 0.463 | 0.342 | 0.332 | 0.325 | ||||

| Adjusted R2 | 0.446 | 0.331 | 0.324 | 0.316 | ||||

| p-value | 0.035 ** | 0.139 | 0.112 | 0.103 | ||||

| No. of firms | 154 | 154 | 154 | 154 | ||||

| Observations | 18,018 | 18,018 | 18,018 | 18,018 | ||||

| Model 5 (ROA) | Model 6 (ROE) | Model 7 (TQ) | Model 8 (ADA) | |||||

|---|---|---|---|---|---|---|---|---|

| Variable | β | T-Stat (Std. Error) | β | T-Stat (Std. Error) | β | T-Stat (Std. Error) | β | T-Stat (Std. Error) |

| Board IT Competency Variables | ||||||||

| BITC | 2.705 | 2.197 ** (1.231) | 2.104 | 1.571 (1.339) | 2.581 | 1.638 (1.576) | 2.658 | 1.639 (1.622) |

| CITB | 2.326 | 2.667 *** (0.872) | 1.795 | 1.601 (1.121) | 1.965 | 1.648 (1.192) | 2.085 | 1.647 (1.266) |

| ITCM | 1.184 | 2.122 ** (0.558) | 1.964 | 1.635 (1.201) | 1.643 | 1.408 (1.167) | −2.396 | −2.064 ** (1.161) |

| Other Corporate Governance Variables | ||||||||

| BSIZ | −1.877 | −1.649 (1.138) | 1.152 | 1.532 (0.752) | 1.562 | 1.948 * (0.802) | 2.291 | 2.108 (1.087) |

| DOWN | −1.098 | −1.596 (0.688) | −0.948 | −1.331 (0.712) | 2.183 | 1.031 (2.118) | 2.289 | 1.787 (1.281) |

| BIND | 2.183 | 1.625 (1.343) | 1.205 | 1.592 (0.757) | 1.105 | 1.572 (0.703) | −2.072 | −1.641 (1.263) |

| Control Variables | ||||||||

| CSIZ | −1.883 | −1.489 (1.265) | 1.463 | 1.519 (0.963) | −2.297 | −1.626 (1.413) | 2.302 | 1.586 (1.451) |

| FLEV | −1.725 | −1.648 (1.047) | 1.991 | 1.546 (1.288) | −1.482 | −1.481 (1.001) | 2.298 | 1.554 (1.479) |

| R2 | 0.468 | 0.351 | 0.345 | 0.339 | ||||

| Adjusted R2 | 0.449 | 0.339 | 0.334 | 0.326 | ||||

| p-value | 0.032 ** | 0.142 | 0.117 | 0.108 | ||||

| No. of firms | 154 | 154 | 154 | 154 | ||||

| Observations | 18,018 | 18,018 | 18,018 | 18,018 | ||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Singh, H.P.; Alhulail, H.N. Information Technology Governance and Corporate Boards’ Relationship with Companies’ Performance and Earnings Management: A Longitudinal Approach. Sustainability 2023, 15, 6492. https://doi.org/10.3390/su15086492

Singh HP, Alhulail HN. Information Technology Governance and Corporate Boards’ Relationship with Companies’ Performance and Earnings Management: A Longitudinal Approach. Sustainability. 2023; 15(8):6492. https://doi.org/10.3390/su15086492

Chicago/Turabian StyleSingh, Harman Preet, and Hilal Nafil Alhulail. 2023. "Information Technology Governance and Corporate Boards’ Relationship with Companies’ Performance and Earnings Management: A Longitudinal Approach" Sustainability 15, no. 8: 6492. https://doi.org/10.3390/su15086492