The Role of Employee Empowerment in Supporting Accounting Information Systems Outcomes: A Mediated Model

Abstract

1. Introduction

- What is the relationship between employee empowerment and AIS outcomes?

- How can management awareness mediate the relationship between employee empowerment and AIS outcomes?

- Identify the impact of employee empowerment on AIS outcomes.

- Realize the role of managerial awareness in enhancing AIS outcomes.

- Highlight the interconnectedness between employee empowerment, AIS outcomes, and managerial awareness.

2. Literature Review

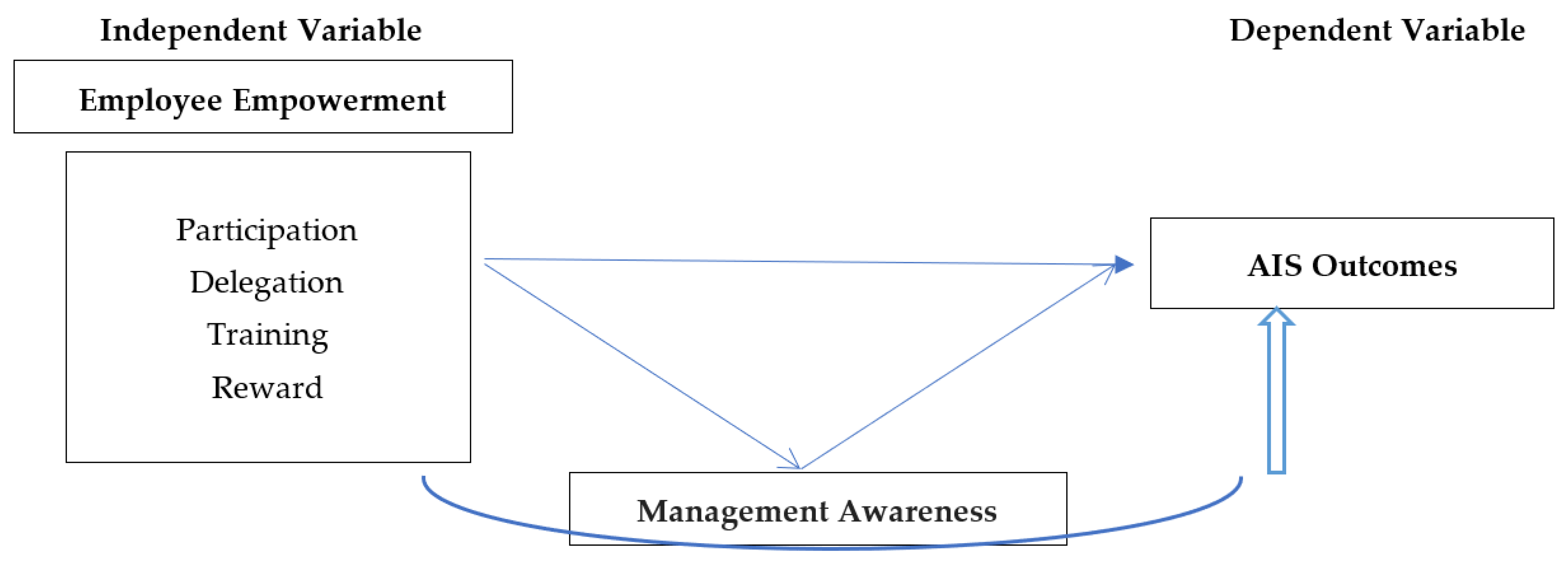

2.1. Employee Empowerment

2.1.1. Participation

2.1.2. Delegation

2.1.3. Training

2.1.4. Reward

2.2. AIS Outcomes

2.3. Management Awareness

3. Hypotheses Development

4. Methods

4.1. Methodological Approach

4.2. Study Tool

4.3. Population and Sample

4.4. Data Screening and Analysis

- Mean and standard deviation.

- Frequencies and percentages.

5. Results and Discussion

5.1. Demographic Results

5.2. Questionnaire Analysis

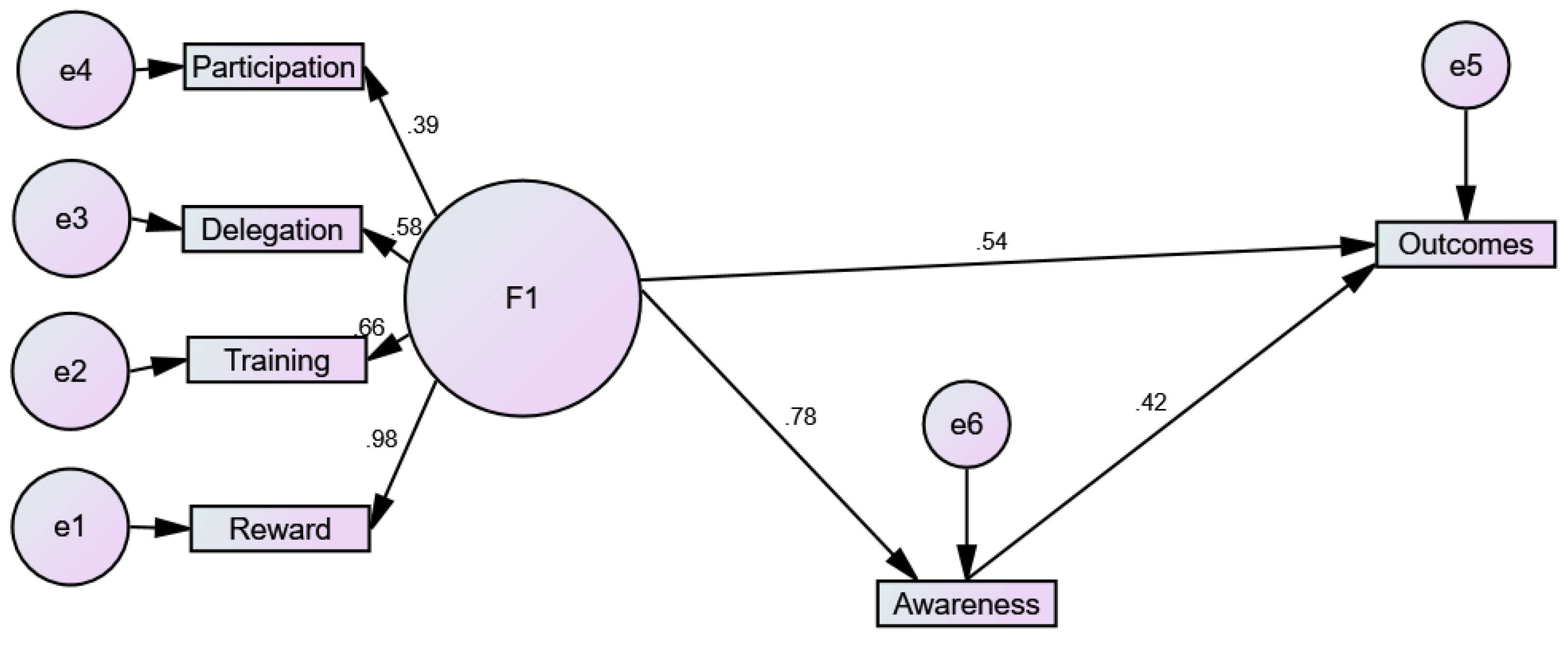

5.3. Hypotheses Testing

6. Discussion

- H (1). Employee empowerment has a significant impact on management awareness.

- H (2). Management awareness has a significant impact on AIS outcomes.

- H (3). Employee empowerment has a significant impact on AIS outcomes.

- H (4). Management awareness mediates the relationship between employee empowerment and AIS outcomes.

6.1. Employee Empowerment Positively Influences AIS Outcomes

6.2. Managerial Awareness Mediates the Relationship between Employee Empowerment and AIS Outcomes

7. Conclusions

8. Theoretical Contribution

- Employee empowerment: This study contributes to the existing literature on employee empowerment by examining its role in supporting AIS outcomes in the banking sector. It provides empirical evidence on the impact of employee empowerment on AIS outcomes.

- AIS outcomes: The study also contributes to the AIS literature by examining the outcomes of AIS. It identifies the key factors that affect AIS outcomes and provides insights into how employee empowerment can improve these outcomes.

- Mediating influence of higher management awareness: The study also contributes to the literature on the mediating influence of higher management awareness. It provides evidence that higher management awareness plays a critical role in mediating the relationship between employee empowerment and AIS outcomes.

- Banking sector: The study focuses specifically on the banking sector, which is an important industry in most economies; it provides insights into how employee empowerment can be used to improve AIS outcomes in the banking sector.

9. Limitations of Study

10. Recommendations

- Utilize integrated cloud-based systems to increase the availability of information and reduce the need for manual data entry.

- Automate key tasks wherever possible to save time and create greater accuracy.

- Balance the security and accessibility of data so that important systems and data are protected but can still be accessed by appropriate staff and systems.

- Take advantage of interactive features for reporting and analysis.

- Implement strong audit trails to help track changes and identify potential problems.

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Haapamäki, E.; Sihvonen, J. Cybersecurity in accounting research. Manag. Audit. J. 2019, 34, 808–834. [Google Scholar] [CrossRef]

- Nguyen, H.; Nguyen, A. Determinants of accounting information systemsAIS quality: Empirical evidence from Vietnam. Accounting 2020, 6, 185–198. [Google Scholar] [CrossRef]

- Ahmad, M.A.; Al-Shbiel, S.O. The effect of accounting information system on organizational performance in Jordanian industrial SMEs: The mediating role of knowledge management. Int. J. Bus. Soc. Sci. 2019, 10, 99–104. [Google Scholar] [CrossRef]

- Haleem, A.H.; Kevin, L.L.T. Impact of user competency on accounting information system success: Banking sectors in Sri Lanka. Int. J. Econ. Financ. Issues 2018, 8, 167. [Google Scholar] [CrossRef]

- Chen, Y.; Long, X. The Empowerment and Subversion of Information Technology to Accounting Information System. In Proceedings of the 2022 3rd International Conference on E-commerce and Internet Technology (ECIT 2022), Zhangjiajie, China, 4–6 March 2022; pp. 384–392. [Google Scholar] [CrossRef]

- Astuty, W.; Pratama, I.; Basir, I.; Harahap, J.P.R. Does Enterprise Resource Planning Lead to The Quality of The Management Accounting Information System. Pol. J. Manag. Stud. 2022, 25, 93–107. [Google Scholar] [CrossRef]

- Sivagnanasundaram, J.; Goonetillake, J.; Buhary, R.; Dharmawardhana, T.; Weerakkody, R.; Gunapala, R.; Ginige, A. Digitally-Enabled Crop Disorder Management Process Based on Farmer Empowerment for Improved Outcomes: A Case Study from Sri Lanka. Sustainability 2021, 13, 7823. [Google Scholar] [CrossRef]

- Abuzaid, A. Employees’ empowerment and its role in achieving strategic success: A practical study on Jordanian insurance companies. Jordan J. Bus. Adm. 2018, 14, 641–660. [Google Scholar]

- Lassoued, K.; Awad, A.; Guirat, R. The impact of managerial empowerment on problem solving and decision making skills: The case of Abu Dhabi University. Manag. Sci. Lett. 2020, 10, 769–780. [Google Scholar] [CrossRef]

- Andi Kele, A.T. Employee Empowerment in Luxury Hotels in East Malaysia. Ph.D. Thesis, The University of Waikato, Hamilton, New Zealand, 2020. [Google Scholar]

- Nicholls, A. A general theory of social impact accounting: Materiality, uncertainty and empowerment. J. Soc. Entrep. 2018, 9, 132–153. [Google Scholar] [CrossRef]

- Al-Hattami, H.M.; Kabra, J.D. The influence of accounting information system on management control effectiveness: The perspective of SMEs in Yemen. Inf. Dev. 2022. [Google Scholar] [CrossRef]

- Raharjono, M.A.A.; Dharmadiaksa, I.B. The Effect of Incentives and Employee Empowerment on the Effectiveness of Accounting Information SystemsAIS. Am. J. Humanit. Soc. Sci. Res. (AJHSSR) 2021, 5, 149–153. [Google Scholar]

- Al Maani, A.I.; Al Adwan, A.; Areiqat, A.Y.; Zamil, A.M.; Salameh, A.A. Level of administrative empowerment at private institution and its impact on institutional performance: A case study. Entrep. Sustain. Issues 2020, 8, 500. [Google Scholar] [CrossRef] [PubMed]

- Vu, H.M. Employee empowerment and empowering leadership: A literature review. Technium 2020, 2, 20–28. [Google Scholar] [CrossRef]

- Ghasempour Ganji, S.F.; Johnson, L.W.; Babazadeh Sorkhan, V.; Banejad, B. The effect of employee empowerment, organizational support, and ethical climate on turnover intention: The mediating role of job satisfaction. Iran. J. Manag. Stud. 2021, 14, 311–329. [Google Scholar]

- Obiekwe, O.; Zeb-Obipi, I.; Ejo-Orusa, H. Employee involvement in organizations: Benefits, challenges and implications. Manag. Hum. Resour. Res. J. 2019, 8, 1–11. [Google Scholar]

- Zaraket, W.; Garios, R.; Malek, L.A. The impact of employee empowerment on the organizational commitment. Int. J. Hum. Resour. Stud. 2018, 8, 284–299. [Google Scholar] [CrossRef]

- Hewagama, G.; Boxall, P.; Cheung, G.; Hutchison, A. Service recovery through empowerment? HRM, employee performance and job satisfaction in hotels. Int. J. Hosp. Manag. 2019, 81, 73–82. [Google Scholar] [CrossRef]

- Turkmenoglu, M.A. Investigating benefits and drawbacks of employee empowerment in the sector of hospitality: A review. Int. Res. J. Bus. Stud. 2019, 12, 1–13. [Google Scholar] [CrossRef]

- Natrajan, N.S.; Sanjeev, R.; Singh, S.K. Achieving job performance from empowerment through the mediation of employee engagement: An empirical study. Indep. J. Manag. Prod. 2019, 10, 1094–1105. [Google Scholar] [CrossRef]

- Irakoze, E.; David, K.G. Linking Motivation to Employees’ Performance: The Mediation of Commitment and Moderation of Delegation Authority. Int. Bus. Res. 2019, 12. [Google Scholar] [CrossRef]

- Bani-Melhem, S.; Quratulain, S.; Al-Hawari, M.A. Customer incivility and frontline employees’ revenge intentions: Interaction effects of employee empowerment and turnover intentions. J. Hosp. Mark. Manag. 2020, 29, 450–470. [Google Scholar] [CrossRef]

- Philip, K.; Arrowsmith, J. The limits to employee involvement? Employee participation without HRM in a small not-for-profit organisation. Pers. Rev. 2020, 50, 401–419. [Google Scholar] [CrossRef]

- Sandi, H.; Yunita, N.A.; Heikal, M.; Ilham, R.N.; Sinta, I. Relationship Between Budget Participation, Job Characteristics, Emotional Intelligence and Work Motivation As Mediator Variables to Strengthening User Power Performance: An Emperical Evidence From Indonesia Government. Morfai J. 2021, 1, 36–48. [Google Scholar] [CrossRef]

- Baird, K.; Tung, A.; Su, S. Employee empowerment, performance appraisal quality and performance. J. Manag. Control. 2020, 31, 451–474. [Google Scholar] [CrossRef]

- Seaton, F.S. Empowering teachers to implement a growth mindset. Educ. Psychol. Pract. 2018, 34, 41–57. [Google Scholar] [CrossRef]

- Nwachukwu, C.; Chládková, H.; Agboga, R.S.; Vu, H.M. Religiosity, employee empowerment and employee engagement: An empirical analysis. Int. J. Sociol. Soc. Policy 2021, 41, 1195–1209. [Google Scholar] [CrossRef]

- Andika, R.; Darmanto, S. The effect of employee empowerment and intrinsic motivation on organizational commitment and employee performance. J. Apl. Manaj. 2020, 18, 241–251. [Google Scholar] [CrossRef]

- Motamarri, S.; Akter, S.; Yanamandram, V. Frontline employee empowerment: Scale development and validation using Confirmatory Composite Analysis. Int. J. Inf. Manag. 2020, 54, 102177. [Google Scholar] [CrossRef]

- Murray, W.C.; Holmes, M.R. Impacts of employee empowerment and organizational commitment on workforce sustainability. Sustainability 2021, 13, 3163. [Google Scholar] [CrossRef]

- AlKahtani, N.; Iqbal, S.; Sohail, M.; Sheraz, F.; Jahan, S.; Anwar, B.; Haider, S. Impact of employee empowerment on organizational commitment through job satisfaction in four and five stars hotel industry. Manag. Sci. Lett. 2021, 11, 813–822. [Google Scholar] [CrossRef]

- Al-Okaily, A.; Al-Okaily, M.; Shiyyab, F.; Masadah, W. Accounting information system effectiveness from an organizational perspective. Manag. Sci. Lett. 2020, 10, 3991–4000. [Google Scholar] [CrossRef]

- Arif, D.; Yucha, N.; Setiawan, S.; Oktarina, D.; Martah, V. Applications of goods mutation control form in accounting information system: A case study in sumber indah perkasa manufacturing, Indonesia. J. Asian Financ. Econ. Bus. 2020, 7, 419–424. [Google Scholar] [CrossRef]

- Jasim, Y.A.; Raewf, M.B. Information technology’s impact on the accounting system. Cihan Univ.-Erbil J. Humanit. Soc. Sci. 2020, 4, 50–57. [Google Scholar] [CrossRef]

- HA, V.D. Impact of organizational culture on the accounting information system and operational performance of small and medium sized enterprises in Ho Chi Minh City. J. Asian Financ. Econ. Bus. 2020, 7, 301–308. [Google Scholar] [CrossRef]

- Qatawneh, A. The influence of data mining on Accounting Information System Performance: A mediating role of Information Technology Infrastructure. J. Gov. Regul. 2022, 11, 141–151. [Google Scholar] [CrossRef]

- Alshirah, M.; Lutfi, A.; Alshirah, A.; Saad, M.; Ibrahim, N.M.E.S.; Mohammed, F. Influences of the environmental factors on the intention to adopt cloud based accounting information system among SMEs in Jordan. Accounting 2021, 7, 645–654. [Google Scholar] [CrossRef]

- Lutfi, A. Factors Influencing the Continuance Intention to Use Accounting Information System in Jordanian SMEs from the Perspectives of UTAUT: Top Management Support and Self-Efficacy as Predictor Factors. Economies 2022, 10, 75. [Google Scholar] [CrossRef]

- Sarwar, M.I.; Iqbal, M.W.; Alyas, T.; Namoun, A.; Alrehaili, A.; Tufail, A.; Tabassum, N. Data vaults for blockchain-empowered accounting information systems. IEEE Access 2021, 9, 117306–117324. [Google Scholar] [CrossRef]

- Al-Ibbini, O.A. The critical success factors influencing the quality of accounting information systemsAIS and the expected performance. Int. J. Econ. Financ. 2017, 9, 162. [Google Scholar] [CrossRef]

- Amoush, A.; Saleh, I.; Khayata, K.; Al-Shalabi, F. The Impact of Accounting Information SystemsAIS Success on Professional Skepticism Empirical study at Auditing Offices in Jordan. Int. Res. J. Appl. Financ. 2018, 9, 46–66. [Google Scholar]

- Yuan, Z.; Hou, L.; Zhou, Z.; Sun, Y. The impact of accounting information quality on corporate labor investment efficiency: Evidence from China. J. Syst. Sci. Syst. Eng. 2022, 31, 594–618. [Google Scholar] [CrossRef]

- Ahad, T.; Busch, P.; Blount, Y.; Picoto, W. Mobile phone-based information systems for empowerment: Opportunities for ready-made garment industries. J. Glob. Inf. Technol. Manag. 2021, 24, 57–85. [Google Scholar] [CrossRef]

- Al-Okaily, M.; Alkhwaldi, A.F.; Abdulmuhsin, A.A.; Alqudah, H.; Al-Okaily, A. Cloud-based accounting information systemsAIS usage and its impact on Jordanian SMEs’ performance: The post-COVID-19 perspective. J. Financ. Report. Account. 2022; ahead-of-print. [Google Scholar] [CrossRef]

- Khalid, B.; Kot, M. The impact of accounting information systems on performance management in the banking sector. IBIMA Bus. Rev. 2021, 2021, 578902. [Google Scholar] [CrossRef]

- Latifah, L.; Setiawan, D.; Aryani, Y.A.; Rahmawati, R. Business strategy–MSMEs’ performance relationship: Innovation and accounting information system as mediators. J. Small Bus. Enterp. Dev. 2021, 28, 1–21. [Google Scholar] [CrossRef]

- Qatawneh, A.M.; Kasasbeh, H. Role of Accounting Information SystemsAIS (AIS) Applications on Increasing SMES Corporate Social Responsibility (CSR) During COVID-19. In Digital Economy, Business Analytics, and Big Data Analytics Applications; Studies in Computational Intelligence; Yaseen, S.G., Ed.; Springer: Cham, Switzerland, 2022; Volume 1010. [Google Scholar] [CrossRef]

- Elmets, C.A.; Leonardi, C.L.; Davis, D.M.; Gelfand, J.M.; Lichten, J.; Mehta, N.N.; Armstrong, A.; Connor, C.; Cordoro, K.M.; Menter, A. Joint AAD-NPF guidelines of care for the management and treatment of psoriasis with awareness and attention to comorbidities. J. Am. Acad. Dermatol. 2019, 80, 1073–1113. [Google Scholar] [CrossRef]

- Todaro, N.M.; Testa, F.; Daddi, T.; Iraldo, F. The influence of managers’ awareness of climate change, perceived climate risk exposure and risk tolerance on the adoption of corporate responses to climate change. Bus. Strategy Environ. 2021, 30, 1232–1248. [Google Scholar] [CrossRef]

- Wolff, C.E.; Jarodzka, H.; Boshuizen, H. Classroom management scripts: A theoretical model contrasting expert and novice teachers’ knowledge and awareness of classroom events. Educ. Psychol. Rev. 2021, 33, 131–148. [Google Scholar] [CrossRef]

- Saad, A.; Zahid, S.M.; Muhammad, U.B. Role of awareness in strengthening the relationship between stakeholder management and project success in the construction industry of Pakistan. Int. J. Constr. Manag. 2020, 22, 1884–1893. [Google Scholar] [CrossRef]

- Benoit, K.; Watanabe, K.; Wang, H.; Nulty, P.; Obeng, A.; Müller, S.; Matsuo, A. quanteda: An R package for the quantitative analysis of textual data. J. Open Source Softw. 2018, 3, 774. [Google Scholar] [CrossRef]

- Zakrzewska-Bielawska, A. The relationship between managers’ network awareness and the relational strategic orientation of their firms: Findings from interviews with Polish managers. Sustainability 2018, 10, 2691. [Google Scholar] [CrossRef]

- Thomas, G.; van Heinsbergen, M.; van der Heijden, J.; Slooter, G.; Konsten, J.; Maaskant, S. Awareness and management of low anterior resection syndrome: A Dutch national survey among colorectal surgeons and specialized nurses. Eur. J. Surg. Oncol. 2019, 45, 174–179. [Google Scholar] [CrossRef] [PubMed]

- Glezeva, N.; Chisale, M.; McDonald, K.; Ledwidge, M.; Gallagher, J.; Watson, C.J. Diabetes and complications of the heart in Sub-Saharan Africa: An urgent need for improved awareness, diagnostics and management. Diabetes Res. Clin. Pract. 2018, 137, 10–19. [Google Scholar] [CrossRef] [PubMed]

- Cao, C.; Tong, X.; Chen, Y.; Zhang, Y. How top management’s environmental awareness affect corporate green competitive advantage: Evidence from China. Kybernetes 2021, 51, 1250–1279. [Google Scholar] [CrossRef]

- Al-Okaily, M. Assessing the effectiveness of accounting information systems in the era of COVID-19 pandemic. VINE J. Inf. Knowl. Manag. Syst. 2021; ahead-of-print. [Google Scholar] [CrossRef]

- Mohapatra, M.; Mishra, S. The employee empowerment as a key factor defining organizational performance in emerging market. Int. J. Bus. Insights Transform. 2018, 12, 48–52. [Google Scholar]

- Rastogi, R.A.; Sharma, T. Quantitative analysis of drainage basin characteristics. J. Soil Water Conserv. India 2022, 26, 18–25. [Google Scholar]

- Ribeiro, J.P.; Barbosa-Povoa, A. Supply Chain Resilience: Definitions and quantitative modelling approaches–A literature review. Comput. Ind. Eng. 2018, 115, 109–122. [Google Scholar] [CrossRef]

- Jiang, Y.; Liu, J. Definitions of pseudocapacitive materials: A brief review. Energy Environ. Mater. 2019, 2, 30–37. [Google Scholar] [CrossRef]

- Al-Ababneh, M.M. Linking ontology, epistemology and research methodology. Sci. Philos. 2020, 8, 75–91. [Google Scholar]

- Dewaele, J.M. The vital need for ontological, epistemological and methodological diversity in applied linguistics. In Voices and Practices in Applied Linguistics: Diversifying a Discipline; White Rose University Press: New York, NY, USA, 2019; pp. 71–88. [Google Scholar] [CrossRef]

- Lutfi, A.; Al-Okaily, M.; Alsyouf, A.; Alsaad, A.; Taamneh, A. The impact of AIS usage on AIS effectiveness among Jordanian SMEs: A multi-group analysis of the role of firm size. Glob. Bus. Rev. 2020. [Google Scholar] [CrossRef]

- Uher, J. Quantitative data from rating scales: An epistemological and methodological enquiry. Front. Psychol. 2018, 9, 2599. [Google Scholar] [CrossRef]

- Tripp, A.M.; Hughes, M.M. Methods, methodologies and epistemologies in the study of gender and politics. Eur. J. Politics Gend. 2018, 1, 241–257. [Google Scholar] [CrossRef]

- Boparai, J.K.; Singh, S.; Kathuria, P. How to design and validate a questionnaire: A guide. Curr. Clin. Pharmacol. 2018, 13, 210–215. [Google Scholar] [CrossRef] [PubMed]

- Brace, I. Questionnaire Design: How to Plan, Structure and Write Survey Material for Effective Market Research; Kogan Page Publishers: London, UK, 2018. [Google Scholar]

- Krosnick, J.A. Questionnaire design. In The Palgrave Handbook of Survey Research; Palgrave Macmillan: Cham, Switzerland, 2018; pp. 439–455. [Google Scholar] [CrossRef]

- Majid, U. Research fundamentals: Study design, population, and sample size. Undergrad. Res. Nat. Clin. Sci. Technol. J. 2018, 2, 1–7. [Google Scholar] [CrossRef]

- Wang, X.; Cheng, Z. Cross-sectional studies: Strengths, weaknesses, and recommendations. Chest 2020, 158, S65–S71. [Google Scholar] [CrossRef] [PubMed]

- Şahin, M.; Aybek, E. Jamovi: An easy to use statistical software for the social scientists. Int. J. Assess. Tools Educ. 2019, 6, 670–692. [Google Scholar] [CrossRef]

- Jakobsen, T.G.; Mehmetoglu, M. Applied statistics using Stata: A guide for the social sciences. In Applied Statistics Using Stata; Sage: Newcastle upon Tyne, UK, 2022; pp. 1–100. [Google Scholar]

- Vuong, Q.H.; La, V.P.; Vuong, T.T.; Ho, M.T.; Nguyen, H.K.T.; Nguyen, V.H.; Pham, H.H.; Ho, M.T. An open database of productivity in Vietnam’s social sciences and humanities for public use. Sci. Data 2018, 5, 180188. [Google Scholar] [CrossRef]

- Sekaran, U.; Bougie, R. Research Methods for Business: A Skill-Building Approach, 7th ed.; John Wiley & Sons: Haddington, UK, 2016. [Google Scholar]

- Miles, J.; Shevlin, M. Effects of sample size, model specification and factor loadings on the GFI in confirmatory factor analysis. Personal. Individ. Differ. 1998, 25, 85–90. [Google Scholar] [CrossRef]

- Tabachnick, B.G.; Fidell, L.S. Using Multivariate Statistics, 5th ed.; Allyn and Bacon: New York, NY, USA, 2007. [Google Scholar]

- MacCallum, R.C.; Browne, M.W.; Sugawara, H.M. Power Analysis and Determination of Sample Size for Covariance Structure Modeling. Psychol. Methods 1996, 1, 130–149. [Google Scholar] [CrossRef]

- Hu, L.T.; Bentler, P.M. Cutoff Criteria for Fit Indexes in Covariance Structure Analysis: Conventional Criteria Versus New Alternatives. Struct. Equ. Model. 1999, 6, 1–55. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Variable | # of Statements |

|---|---|

| Employee Empowerment | 5 |

| Participation | 5 |

| Delegation | 5 |

| Training | 5 |

| Reward | 4 |

| AIS Outcomes | 5 |

| Management Awareness | 6 |

| Variable | Alpha |

|---|---|

| Participation | 0.89 |

| Delegation | 0.895 |

| Training | 0.884 |

| Reward | 0.896 |

| Management Awareness | 0.903 |

| AIS Outcomes | 0.897 |

| f | % | |

|---|---|---|

| Gender | ||

| Male | 62 | 63.9 |

| Female | 35 | 36.1 |

| Age | ||

| 25–30 | 18 | 18.6 |

| 31–36 | 40 | 41.2 |

| 37–42 | 26 | 26.8 |

| +43 | 13 | 13.4 |

| Education | ||

| BA | 77 | 79.4 |

| MA | 17 | 17.5 |

| PhD | 3 | 3.1 |

| Job | ||

| Financial Manager | 18 | 18.6 |

| Accounting Manager | 22 | 22.7 |

| Financial Facilities Manger | 57 | 58.8 |

| Total | 97 | 100.0 |

| Statement | Mean | Std. Deviation |

|---|---|---|

| employees are engaged in every decision making | 3.59 | 1.37 |

| participation takes place according to job description | 3.54 | 1.26 |

| employees’ recommendations are taken into consideration | 3.46 | 1.16 |

| employees are exposed to all new measures all the time | 3.49 | 1.16 |

| employees are informed in all updates that takes place on AIS | 3.44 | 1.12 |

| Participation | 3.51 | 1.01 |

| All employees are delegated to take decision according to their position | 3.30 | 1.17 |

| leaders delegate a lot of tasks in order to save time and efforts | 3.21 | 0.97 |

| employees are able to access AIS platforms according to their job description | 3.18 | 0.92 |

| delegations are done with clear instructions | 3.30 | 0.94 |

| employees have the ability to take decision based on their | 3.46 | 0.95 |

| Delegation | 3.29 | 0.83 |

| ongoing orientations are done to employees on using AIS | 3.36 | 0.98 |

| Leaders are always available for directions | 3.38 | 0.99 |

| AIS applications are always up to date for employees | 3.40 | 0.96 |

| any errors or mistakes are taken seriously for not being repeated again | 3.15 | 1.18 |

| training courses and seminars on AIS applications are always available | 3.16 | 1.20 |

| Training | 3.29 | 0.89 |

| employees are rewarded based on their performance | 3.54 | 1.16 |

| lack of mistakes and errors make is always appreciated by the management | 3.48 | 1.07 |

| employees are always appreciated and rewarded for their job development | 3.39 | 1.11 |

| Employees’ ability to reach certain goals is always rewarded | 3.36 | 1.01 |

| Reward | 3.44 | 0.95 |

| employees’ empowerment developed the level of AIS outcomes | 3.58 | 0.94 |

| AIS outcomes are always up to date an shared to employees based on their tasks | 3.35 | 0.94 |

| with empowerment employees are more engaged and developed in managing AIS | 3.27 | 1.20 |

| AIS outcomes are more reliable and credible | 3.28 | 1.12 |

| Decision making is more attainable when it comes to AIS outcomes | 3.47 | 1.07 |

| AIS Outcomes | 3.39 | 0.89 |

| the management is aware of empowerment influence on AIS outcomes | 3.23 | 1.02 |

| Management makes sure that all employees get the needed orientation on AIS applications | 3.35 | 0.94 |

| Management supports leadership in empowerment efforts | 3.43 | 1.15 |

| Management appreciate the influence of empowerment on AIS outcomes | 3.41 | 1.09 |

| Management is aware that empowerment develops the relationship between leadership and employees | 3.60 | 1.01 |

| the management makes sure that all employees are aware of their role in AIS applications | 3.35 | 0.98 |

| Management Awareness | 3.40 | 0.85 |

| Indicator | AGFI | GFI | RMSEA | CFI | NFI | |

|---|---|---|---|---|---|---|

| Value Recommended | >0.8 | <5 | >0.90 | ≤0.10 | >0.9 | >0.9 |

| References | [77] | [78] | [77] | [79] | [80] | [80] |

| Value of Model | 0.83 | 4.781 | 0.935 | 0.069 | 0.919 | 0.922 |

| Direct Impact | Indirect Impact | Total Impact | C.R. | p | Result | |||

|---|---|---|---|---|---|---|---|---|

| Awareness | <--- | Employee Empowerment | 0.78 | 0.78 | 10.184 | *** | accept | |

| Outcomes | <--- | Awareness | 0.423 | 0.423 | 4.875 | *** | accept | |

| Outcomes | <--- | Employee Empowerment | 0.54 | 0.33 | 0.87 | 5.577 | *** | accept |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Qatawneh, A.M. The Role of Employee Empowerment in Supporting Accounting Information Systems Outcomes: A Mediated Model. Sustainability 2023, 15, 7155. https://doi.org/10.3390/su15097155

Qatawneh AM. The Role of Employee Empowerment in Supporting Accounting Information Systems Outcomes: A Mediated Model. Sustainability. 2023; 15(9):7155. https://doi.org/10.3390/su15097155

Chicago/Turabian StyleQatawneh, Adel M. 2023. "The Role of Employee Empowerment in Supporting Accounting Information Systems Outcomes: A Mediated Model" Sustainability 15, no. 9: 7155. https://doi.org/10.3390/su15097155

APA StyleQatawneh, A. M. (2023). The Role of Employee Empowerment in Supporting Accounting Information Systems Outcomes: A Mediated Model. Sustainability, 15(9), 7155. https://doi.org/10.3390/su15097155