Abstract

The high-quality development of energy is the basis for and premise of achieving the high-quality development of the economy, and energy enterprises, as the main body of the microeconomy, are the “carrier” of its success. The national strategy of dual carbon and energy security requires energy enterprises to achieve sustainable development. In the context of global sustainable development, ESG is an evaluation technology that comprehensively measures the environmental sustainability, social value and governance ability of enterprises and improves the sustainable development ability of enterprises by focusing on the non-financial performance of enterprises and the co-creation and sharing of stakeholder value. As an important energy producer and consumer, China has not yet established an ESG evaluation system for energy enterprises that is in line with international standards and national conditions. Therefore, this paper constructs an ESG evaluation model framework of energy enterprises and studies the high-quality development performance evaluation of energy enterprises under the sustainable development strategy from the two dimensions of theoretical enrichment and empirical analysis. The model framework includes a factor structure model, performance evaluation index system, index weight model and performance evaluation model. First, integrating the new development concept and the safe development concept, the ESG connotation of China’s energy enterprises was defined by localization. Second, using the Delphi method, an ESG evaluation system with 3 sub-target layers, 14 criteria layers and 40 index layers was constructed. Third, the weights of each index in the ESG evaluation system were established by using an AHP–entropy combination weighting method. Fourth, based on the statistical data of 2021, 79 key pollutant energy enterprises listed in China were selected. The TOPSIS method was used to establish an evaluation model to empirically evaluate the comprehensive level of ESG and the performance of the E, S and G dimensions of the sample companies, and the evaluation results were analyzed. The results show that the weight ratio of E, S and G is relatively balanced; and the weight of social responsibility ranks first at the target level, environmental response ranks first at the criterion level and energy supply guarantee ranks first at the index level. The overall ESG performance of the sample companies is average, and the G performance is not ideal. The ESG synthesis and the performance of all dimensions are significantly polarized, and the development of different dimensions of E, S and G is mostly unbalanced and uncoordinated. The results demonstrate the following: (1) Using the Delphi method, the ESG structural dimension model of energy enterprises is constructed by selecting evaluation indicators reflecting the concepts of innovation, coordination, green, open, sharing and safety, which enriches the connotation and extension theory of ESG. (2) The AHP–entropy combination weighting method model can scientifically obtain the weights of indicators at each level in the ESG evaluation system. (3) The proposed ESG evaluation index system can effectively measure the high-quality development level of energy enterprises. This research can provide regulatory authorities with sustainable development policy suggestions for strengthening the top-level design of ESG; building an ESG-healthy ecosystem; and integrating ESG investment with energy security, carbon-neutral goals and corporate strategies to promote the high-quality development of enterprises.

1. Introduction

The world is currently undergoing the third energy transition for sustainable development [1]. Countries are striving to achieve the long-term goals set by the Paris Agreement to limit the global temperature increase to no more than 2 °C (above the pre-industrial level) by the end of the 21st century, strive to control it within 1.5 °C, and achieve net zero greenhouse gas emissions in the second half of the 21st century.

The International Energy Agency (IEA) released the world’s first “Energy Sector Roadmap to 2050 Net Zero Emissions” report in 2021, pointing out that the energy industry produces about three-quarters of the world’s greenhouse gases. As the world’s largest energy producer, consumer and carbon emitter [2], China has made a solemn commitment to “dual carbon” and the long-term goals of the Paris Agreement that requires a profound transformation of its energy economic system.

At the same time, the Russia–Ukraine conflict and other major changes not seen in a century have also made us more aware that we must attach great importance to national energy security. China is the world’s largest oil importer and natural gas importer, with its dependence on foreign oil and gas reaching 71.2% and 40.5% respectively, in 2022. The spatial mismatch between the international energy consumption center and the energy supply area and the increasingly complex geopolitical environment have brought challenges to China’s energy security.

ESG (Environmental Social Governance) was first proposed by the UN Global Compact’s “Who Cares Wins” report in June 2004 [3], and its origin is “ethical investment” or “socially responsible investment” [4]. Developed on the basis of corporate social responsibility theory [5,6] and sustainable development theory [7], it is an evaluation technology that comprehensively measures corporate environmental sustainability, social value and governance ability [6]. The core idea of ESG is highly compatible with the new development concept and has become an important reference system for measuring the sustainable and high-quality development of enterprises.

Governments, organizations and institutions have adopted various means to promote the development of ESG. In December 2019, the European Union implemented the European Green Deal and the “Fit for 55” energy and climate package to address climate change; ESG reporting initiatives such as the Global Reporting Initiative and non-profit organizations also have an impact on the disclosure of energy companies [8]. Energy is one of the most sensitive sectors in terms of ESG measures and related regulations [9]. In terms of the increasing number of investors moving away from traditional investment paradigms to investments based on ESG accountability principles, the energy sector is also the most affected [10].

The report of the 20th National Congress of the Communist Party of China pointed out that high-quality development is the primary task of comprehensively building socialist modernization. Therefore, the goal of high-quality development is the phased goal of the Sustainable Development Goal in China’s new era. As the lifeblood of the national economy, energy is vital to the national economy, people’s livelihood and national security. High-quality energy development is related to the establishment of a new development pattern and is a key element of building a great modern socialist country in all respects. The Chinese energy enterprises are shouldering many important responsibilities, such as holding the energy rice bowl and implementing the goal of peak carbon emissions and carbon neutrality. For them, there is an urgent need to apply ESG to energy enterprises; ESG is no longer the optional question, but the required question.

However, China has not yet established an ESG evaluation system for energy enterprises. At present, Chinese energy enterprises have the bottleneck problem of one-sided emphasis on the environmental responsibility of the dual-carbon target while ignoring the social responsibility of energy supply assurance, or excessive demand for the social responsibility of energy security, resulting in environmental damage. In addition, the problems of irregular corporate governance and low development quality are prominent. The sustainable development level of energy enterprises still has great room for improvement, which requires the government, energy enterprises and relevant departments to build an ESG evaluation system to jointly manage the sustainable development of the energy industry.

In fact, the international ESG evaluation developed earlier, and it started relatively late in China, so it is not appropriate to apply it directly. For example, in February 2023, FTSE Russell reported a score of only 2.5 points (out of 5 points) for China Shenhua, a leading listed energy enterprise in China, while companies higher than 3.3 points can be included in its index products. The existing ESG evaluation system mostly follows the investment concept and rating framework recognized by Western developed countries, which cannot effectively measure the ESG performance of China’s energy enterprises, let alone prompt its high-quality development. Therefore, it is necessary to conduct empirical research on the ESG evaluation of Chinese energy enterprises in the context of high-quality development.

In order to establish an ESG evaluation system for Chinese energy enterprises that is consistent with international transition and national conditions, solve the contradiction between green transformation and energy security, vigorously promote the application of ESG in energy enterprises, and promote the improvement of sustainable development ability of energy enterprises, in this paper, we constructed an ESG evaluation system for Chinese energy enterprises, so as to scientifically evaluate their sustainable development level. We defined the connotation of ESG of Chinese energy enterprises. Then, we used the Delphi method to build an ESG evaluation index system from the concepts of innovation, coordination, green, open, sharing and safety. At the same time, to solve the problem of ESG-related data of energy enterprises not being easy to obtain accurately, an AHP–entropy combination weighting model was introduced to determine the weights of ESG evaluation indicators. Finally, based on the ESG theory, AHP–entropy Combination Weighting method and TOPSIS model, the ESG evaluation model framework of Chinese energy enterprises from the perspective of sustainable development was constructed.

Firstly, the ESG connotation of Chinese energy enterprises was defined on the basis of integrating the new development concept and the safe development concept. On this basis, the ESG structural dimension model was constructed by using the Delphi method and combining the development characteristics of Chinese energy enterprises, and an ESG evaluation index system of Chinese energy enterprises with 40 specific indices was established. Secondly, the weighting model of the ESG evaluation index of Chinese energy enterprises was constructed by using an AHP–entropy combination weighting method. Thirdly, the ESG evaluation model of Chinese energy enterprises was constructed based on the TOPSIS model. Fourthly, 79 key pollutant energy listed enterprises were taken as sample enterprises to evaluate their overall ESG performance and the performance levels of E, S and G dimensions in 2021. From the perspective of sustainable development, the scientific and rational ESG evaluation system of Chinese energy enterprises was confirmed.

Compared with the existing research, the two contributions of this paper are as follows: (1) Firstly, from the perspective of theoretical enrichment, based on the goal of high-quality development, following the new development concept and safe development concept, we innovatively interpreted the definition of ESG for Chinese energy enterprises and enriched the connotation and extension of ESG. On this basis, we selected evaluation indicators reflecting the concepts of innovation, coordination, green, open, sharing and safety at the target level, criterion level and indicator level. The setting of indicators fully considered the special nature of state-owned property rights accounting for the vast majority of Chinese energy enterprises and the dual-carbon goal requirements of achieving both energy security and low-carbon development. This was the first time an innovative ESG evaluation index system was built for Chinese energy enterprises, filling the gap of there being no ESG evaluation system for Chinese energy enterprises and providing theoretical support for realizing the sustainable development of energy enterprises. It was conducive to solving the contradiction between green development and the energy supply guarantee of Chinese energy enterprises. (2) Secondly, from the perspective of empirical analysis, for the first time, we comprehensively applied an AHP–entropy combination weighting method and the TOPSIS model to construct an ESG performance evaluation system for Chinese energy enterprises. We innovatively constructed an ESG multi-criteria decision-making (MCDM) model framework and established the performance evaluation index system on the basis of the Delphi method, index weight model on the basis of the AHP–entropy combination weighting method and performance evaluation model on the basis of the TOPSIS method. (i) The Delphi method is a feedback anonymous correspondence method, which can avoid some possible shortcomings of group decision-making controlled by some people. We adopted it to establish an ESG evaluation index system, which can ensure the scientific and reliable setting of specific indicators. (ii) The AHP is a multi-objective decision-making method that hierarchizes and quantifies the decision-making process according to the laws of thinking and psychology, and the result is subjective. The entropy method refers to a mathematical method used to judge the degree of dispersion of a certain index, which is not subjective. We innovatively combined two methods, systematically combined qualitative and quantitative decision-making, overcame the limitation that may lead to insufficient scientific results when they are used alone, and made the index weights and evaluation results more objective and in line with the actual situation of Chinese energy enterprises. (iii) TOPSIS, as an effective method in multi-objective decision-making analysis, evaluates the relative advantages and disadvantages of existing objects. We applied the TOPSIS method in ESG comprehensive evaluation and E, S and G single-dimensional evaluation of Chinese energy enterprises, which can achieve the purpose of quickly and effectively measuring the sustainable development level of Chinese energy enterprises.

The remainder of this paper is arranged as follows: Section 2 is devoted to a literature review on ESG connotation, ESG evaluation and empirical research on ESG evaluation. Section 3 defines the ESG connotation of Chinese energy enterprises by integrating high-quality development, the new development concept and the safe development concept. Section 4 constructs an ESG evaluation index system and structural dimension model based on the Delphi method. Section 5 validates and empirically analyzes the ESG evaluation system based on the AHP–entropy combination weighting method and TOPSIS model. Section 6 presents research conclusions, the originality of the research, managerial recommendations, limitations and further research ideas.

2. Literature Review

2.1. ESG Connotation

The definition of ESG is inconclusive. Foreign scholars focus on its interpretation from a theoretical perspective. Based on institutional theory and legitimacy theory, Baldini et al. (2018) [11] and Drempetic et al. (2020) [12] believed that ESG disclosure is an enterprise’s response to the pressure of stakeholders’ concern in environmental, social and governance aspects to meet their expectations and is an evaluation tool for sustainable development performance results. Galbreath (2013) [13] combined institutional theory with strategic choice, arguing that ESG performance improvement is not only a passive response to external institutional pressure, but also the result of active internal strategic choice. Branco et al. (2008) [14] combined institutional theory with resource-based theory and argued that ESG is a strategy for enterprises to develop valuable intangible assets (resources and capabilities) to gain competitive advantages. Based on social derivative theory, Parfitt (2020) [15] argued that ESG is a way to translate responsible investing into political action.

Domestic scholars define ESG more from the perspective of methodology. Huang Shizhong (2021) [7] believed that ESG is a new methodology for evaluating the sustainable development of enterprises. Cao Qun et al. (2019) [16] argued that ESG is a core element in measuring corporate sustainability and ethical dimensions and an extension of corporate social responsibility. Li Jinglin et al. (2021) [17] believed that ESG is an effective means for enterprises to achieve high-quality and sustainable development, and a new concept of how environment, society and governance can achieve sustainable development in enterprises.

2.2. ESG Evaluation

The concept of ESG has attracted wide attention since it was put forward. In particular, ESG evaluation results have a direct or indirect impact on investor preferences [18], and a large number of investors incorporate ESG evaluation results into portfolio selection criteria [18,19]. However, Widyawati (2021) [20] and Berg et al. (2022) [21] found that the correlation of ESG rating results of mainstream foreign rating agencies was low. Huber et al. (2017) [22] believed that third-party reporting, rating methods and coverage vary widely among providers, leading to that result. Sahin et al. (2022) [23] believed that it is related to the failure to take into account factors such as unpublished and potential new ESG disclosure information.

As domestic rating agencies directly use foreign ready-made ESG system frameworks and indicators [24,25,26], differences in ESG evaluation results also exist in the domestic market. Wang Kai et al. (2022) [24] found that the average correlation coefficient of ESG rating results of the China Securities Index, Shangdao Ronggreen Index and Social Investment Union Index was only 0.26.

Chatterji et al. (2016) [27] believed that the data of FTSE4Good and six other rating agencies had a weak correlation, which led to the failure to guarantee the quality of ESG ratings, suggesting that the results of academic research based on ESG evaluation systems should be re-evaluated. Christensen et al. (2022) [28] found that the greater the ESG divergence among rating agencies, the lower the possibility of issuing external financing. Avramov et al. (2022) [29] argued that ESG rating uncertainty affects investor demand and reduces the economic welfare of ESG-sensitive agents, thereby affecting sustainable investment. Drempetic et al. (2020) [12] found that Thomson Reuters ASSET4 ESG ratings do not properly measure sustainability performance and do not channel funds to more sustainable companies, which is detrimental to climate change mitigation and the achievement of sustainable development goals.

2.3. Empirical Research on ESG Evaluation

In recent years, more and more academic studies in the fields of management, economics, finance and investment have relied on ESG evaluation results to demonstrate the positive [30,31], negative [14,32], uncorrelated [33,34], nonlinear [35] and mixed relationships [36] between ESG performance and financial performance of enterprises. And there has been empirical research in ESG preference and asset price [37], ESG disclosure and “greenwashing” behavior [38], ESG rating and green innovation quantity and quality [39], ESG performance and credit rating [40], bond default [41], energy enterprise credit default probability [42] and other fields. Changhong Zhao et al. (2018) [43], Su Chang et al. (2022) [26] and Suli Hao et al. (2022) [44] carried out empirical studies on the ESG evaluation of environmentally sensitive and resource-based enterprises such as electric power, heavy polluting manufacturing and coal, respectively (Table 1).

Table 1.

Literature review summary.

There are limitations in the existing studies. First, most of them discuss the connotation of ESG from the theoretical level in a general sense, lack in-depth discussion in the specific context of different countries and industries and fail to combine the high-quality development goals of China in the new era. Second, the ESG evaluation system has not taken into account the overall situation of China’s economic and social development, and the indicators lack differentiation consideration. Most rating agencies regard the details of evaluation methods as commercial secrets, and the evaluation process is still a “black box” with a low correlation of evaluation results [45], Therefore, the validity and applicability of the conclusions of the research conducted on this basis are doubtful. Third, there are more empirical studies on the relationship between ESG and corporate financial performance based on evaluation results, while there are few empirical studies on ESG evaluation itself, and even fewer involving energy enterprises.

3. ESG Connotation of China’s Energy Enterprises

Determining how to clarify the ESG connotation is the basic premise of establishing an ESG evaluation system for energy enterprises in China. ESG is an important tool for measuring high-quality economic development. High-quality development is the goal and task of China’s modernization construction, and the new development concept is the guiding principle of China’s modernization construction. In the face of risks and challenges in the modernization process, it is more important to emphasize the concept of safe development [46]. Therefore, high-quality development, the new development concept and the safe development concept constitute the basic elements of ESG connotation.

In addition, the connotation of ESG varies according to the nature of the industry and the concerns at the environmental, social and governance levels [47]. The white paper “China’s Energy Development in the New Era” clearly states that China’s energy development in the new era must unswervingly follow the new path of high-quality development; adhere to the new development concepts of innovation, coordination, green, open and sharing; and constantly improve the quality and security of energy supply.

This paper interprets the connotation of ESG of China’s energy enterprises as follows: enterprises follow the concept of innovation, coordination, green, open, sharing and safety in order to achieve high-quality development goals and maximize the behavior or performance of creating value for stakeholders in terms of environment, society and governance.

4. Construction of ESG Evaluation System

According to the connotation of Chinese energy enterprises’ ESG, evaluation indices reflecting the concepts of innovation, coordination, green, openness, sharing and safety are selected at the target layer, criterion layer and index layer, and an ESG evaluation index system is constructed to measure the high-quality development level of energy enterprises in our country.

4.1. Target Layer and Criterion Layer Construction

Referring to the general practice of mainstream rating agencies at home and abroad, the target layer is first divided into three dimensions, namely environmental responsibility (E), social responsibility (S) and governance responsibility (G), and then the expert consultation method and literature analysis method are adopted to construct the criterion layer.

4.1.1. Environmental Responsibility Dimension

With reference to the pressure–state–response (PSR) conceptual model proposed by the Organization for Economic Cooperation and Development (OECD) and the United Nations Environment Programme (UNEP) [48], the dynamic criterion system of “Environmental Press (EP), Environmental State (ES) and Environmental Response (ER)” is constructed.

4.1.2. Social Responsibility Dimension

Based on the theory of social responsibility, according to the classification of stakeholders, the staff, investors, government, shareholders and society criterion layers are set up.

4.1.3. Governance Responsibility Dimension

Based on the practices of Bai Chongen et al. (2005) [49] and Jiang Yan et al. (2009) [50], the governance level of equity structure, board governance level, executive compensation level, information disclosure level and holding governance level with Chinese characteristics and enterprise Party organization governance are taken as the criterion layer [49,50].

4.2. Index Layer Construction

Firstly, based on the connotation of ESG of Chinese energy enterprises, ESG primary indicators are formed. The E dimension basically covers the key environmental indicators in the Environmental, Social and Governance Reporting Guidelines. In the S dimension, representative indicators that are most directly related to stakeholders are selected. For example, the operating cash ratio that was proposed by the State-owned Assets Supervision and Administration Commission of the State Council in 2023 is used to measure the central enterprise of quality of shareholders’ returns. In the G dimension, referring to Bai Chongen et al. (2005) [49], Jiang Yan et al. (2009) [50], Zhang Huili et al. (2012) [51], Qiu Muyuan et al. (2019) [52], Li Jinglin et al. (2021) [17] and Zhang Zenglian et al. (2022) [53], eight indices including the share ratio of the largest shareholder, the share ratio of the second to the tenth shareholder, whether there is a parent company, the proportion of independent directors, whether the general manager and chairman are held by the same person, the share ratio of the senior executives, whether the enterprise is cross-listed in B or H shares and the property rights nature are included in the evaluation indicators.

Secondly, 15 experts with ESG theoretical and practical experience were invited to discuss the primary indicators. The experts suggested that, in the E dimension, under the “environmental response” criteria, the intensity of R&D investment and the number of authorized patents should be increased, considering innovation as the driving force for energy enterprises’ transformation. In the S dimension, the index of international energy cooperation is increased based on the importance of energy cooperation such as the Belt and Road Initiative. In the G dimension, considering that 81% of Chinese key pollutant energy listed enterprises are state-owned, the index of Party organization participation in governance is increased, and the “two-way entry” degree is used to measure the degree of enterprise Party organization participation in governance with reference to Liu Xuexin et al. (2022) [54].

Finally, the Delphi method was used to conduct expert evaluation and consultation, and an ESG comprehensive evaluation system was established, which included 3 sub-target layers, 14 criteria layers and 40 index layers, as shown in Table 2 (weight is in parentheses, “+” represents positive indicators and “−” represents negative indicators).

Table 2.

ESG evaluation index system for energy enterprises in China.

5. Empirical Research on ESG Evaluation of Chinese Energy Enterprises

5.1. Sample Selection and Data Source

According to the Ministry of Environmental Protection’s Environmental Information Disclosure Guidelines for Listed Companies, the Ministry of Ecological Environmental Protection’s Measures for the Administration of Legal Disclosure of Corporate Environmental Information in 2022, and the China Securities Regulatory Commission’s Guidance on Industry Classification of Listed Companies and the Results of Industry Classification of Listed Companies in the third quarter of 2021 and selecting the coal mining and washing industry (B06), oil and gas mining industry (B07), oil processing, coking and nuclear fuel processing industry (C25), electricity and heat production and supply industry (D44) and gas production and supply industry (D45) as energy industries, 164 energy listed companies were initially obtained.

On 28 June 2021, the China Securities Regulatory Commission revised and issued Announcement No. 15, “Information Disclosure Content and Format Standards for Publicly Issued Securities Companies No. 2”, and Announcement No. 16, “Information Disclosure Content and Format Standards for Publicly Issued Securities Companies No. 3”, requiring improvements in the chapter on corporate governance and the chapter on environmental and social responsibility in the annual report disclosure of listed companies that from 2021 onwards. On 31 December 2021, the Ministry of Ecology and Environment issued the “Corporate Environmental Information Disclosure Format Guidelines in accordance with the Law” to clarify that key pollutant discharge enterprises must disclose key environmental information. Excluding ST, *ST companies and newly listed enterprises in 2021, a total of 94 companies were included in the list of key pollutant discharge enterprises published by the local ecological and environmental protection department. Considering the availability of data, after sample screening, companies with incomplete data and missing values were excluded, and the data of 79 listed energy companies listed in key pollutant discharge enterprises in 2021 were finally selected as research samples in this paper.

Information disclosure evaluation data comes from the Wind database. The number of patents, operating cash ratio and corporate governance data are from the CSMAR database. Other data are derived from social responsibility reports, annual reports or sustainability reports, which are available through the cninf website and the stock exchange website.

5.2. Evaluation Method and Procedure

5.2.1. Methods of Quantification and Standardization of Indicators

For the quantitative processing of qualitative indicators, if the relevant indicators are not described in the company’s annual report, CSR or ESG report, a value of 0 is assigned, a value of 1 is assigned if there is a qualitative description, and a value of 2 is assigned if there is both qualitative and quantitative description. After that, all qualitative and quantitative indicators are treated according to the deviation standardization method:

and are the standardized scores and raw data of the jth index of the ith evaluation object, respectively.

5.2.2. AHP–Entropy Combination Weighting

The entropy method is a mathematical method for calculating the weight of each index by judging the degree of dispersion of each index. It relies on quantitative data, and the result is objective but can easily contradict reality. The Analytic Hierarchy Process (AHP) is a qualitative and quantitative analysis method that relies on expert experience and knowledge, and the results are subjective but reasonable. Combining the advantages and disadvantages of the two methods, this paper uses an AHP–entropy combination weighting method to determine weights. Firstly, the Delphi method and Analytic Hierarchy Process are applied, and yaahp 12.8 software is used to calculate the weight (). Secondly, the entropy method is used to calculate the weight according to the discrete distribution characteristics of the index data. The specific steps are as follows:

Step 1: Establish the standardized data matrix of each index. In order to ensure that all data are meaningful, the standardized data are translated as a whole, , so that the original data are retained to the maximum extent, and = 0.0001 is adopted in this paper.

Step 2: Measure the characteristic proportion of the object to be evaluated :

Step 3: Calculate entropy and difference coefficient :

Step 4: Calculate the weight of item j evaluation index, and the weight obtained by entropy method is marked as :

Finally, the weight coefficient is selected to control the weight , obtained by the two methods, and the comprehensive weight is obtained:

Referring to the study of Su Chang et al. (2022) [26], the selection coefficient is 0.5. The final comprehensive weights of indicators are shown in Table 2.

5.2.3. Comprehensive Evaluation Based on TOPSIS Model

The TOPSIS method is a method for sorting by detecting the distance between a limited number of evaluation objects to the optimal solution and the worst solution, and it is used to evaluate the relative advantages and disadvantages of existing objects. It can be used to carry out comprehensive evaluation and local evaluation and is an effective method for multi-objective decision analysis.

After the weights of each index in the ESG evaluation system are obtained, the TOPSIS method is used to evaluate the comprehensive level of ESG and the performance of the E, S and G dimensions of the sample companies.

(1) Construct the weighted normalized matrix :

(2) Determine the optimal solution and the worst solution :

(3) Calculate Euclidean distance , :

(4) Calculate relative proximity :

5.3. Empirical Research Results and Analysis

5.3.1. Index Weight Analysis

In the three target layers E, S and G, the weight ratio of each dimension is fairly balanced, and the difference is not significant. The ranking from high to low is social responsibility 0.3664, environmental responsibility 0.3334 and governance responsibility 0.3002, which is in line with the goal of balanced development in the three dimensions of E, S and G, among which the weight of social responsibility is the largest, indicating that China’s energy enterprises place more importance on the performance of social responsibility compared with other dimensions of goals.

(1) Criterion layer: The environmental response weight is the largest, at 0.1827, which is consistent with China’s commitment of “striving to achieve carbon peak before 2030 and carbon neutral before 2060” and the “Action Plan for carbon Peak before 2030”, “insisting on standing first and breaking later, ensuring national energy security and economic development as the bottom line, and promoting the smooth transition of low-carbon energy transition. Steadily and orderly, Step by step to promote the carbon Peaking action to ensure safe carbon reduction” and “on the complete, accurate and comprehensive implementation of the new development concept to do a good job of carbon peaking carbon neutral work”. “With energy green and low-carbon development as the key, unswervingly take the ecological priority, green and low-carbon high-quality development road, Ensure the realization of carbon peak and carbon neutrality on schedule” and the overall requirements of the Party’s 20th National Congress report “Actively and steadily promote carbon peak carbon neutrality” are consistent.

(2) Index layer: The energy guarantee weight is 0.0540, ranking first, which is consistent with the “14th Five-Year Plan for Modern Energy System” “Building a modern energy system on the premise of ensuring security, constantly enhancing risk response capabilities, ensuring national energy security, and coordinating promotion of energy supply security and low-carbon transformation”. “Strengthen security capacity building in key areas, ensure the security of food, energy resources, important industrial chain and supply chain” and “energy rice bowl must be in their own hands” and “energy development in the new era must first ensure energy security” in line with the security development concept.

Under the goal of environmental responsibility, the R&D investment intensity and the number of authorized patents have the largest weights, 0.0446 and 0.0341, respectively, coinciding with the Guiding Opinions on Accelerating the Establishment of a sound Green low-carbon Circular Development Economic System which proposed that “the ‘dual-carbon’ goal must rely on scientific and technological innovation and policy innovation. By building a clean, low-carbon, safe and efficient energy system and a green economy system”.

Under the goal of social responsibility, the weight of the international energy cooperation index is 0.0515, ranking second, which is consistent with the new energy security strategy of “comprehensively strengthening international cooperation and realizing energy security under open conditions” in the “four revolutions and one cooperation” and the requirements of continuously deepening the opening-up of the energy field. The weights of rural revitalization and charitable donations are 0.0370 and 0.0200. Consolidating the effective connection between poverty alleviation achievements and rural revitalization has become one of the contents of energy enterprises’ social responsibility, narrowing the gap between urban and rural areas in energy infrastructure and service level, increasing the effectiveness of energy to benefit the people, and promoting more and better benefits of energy development results for the masses of the people. Strengthening the security of energy demand in the field of people’s livelihood, providing strong energy security for realizing people’s yearning for a better life, is also an important embodiment of improving the development and sharing level of energy enterprises and practicing the concept of “coordination”.

(3) Under the goal of governance responsibility, the governance weight of enterprise Party organizations is the largest, at 0.0621, which is consistent with the reform requirements of state-owned enterprises to strengthen the party’s leadership, improve corporate governance and establish a modern enterprise system.

5.3.2. Results Analysis

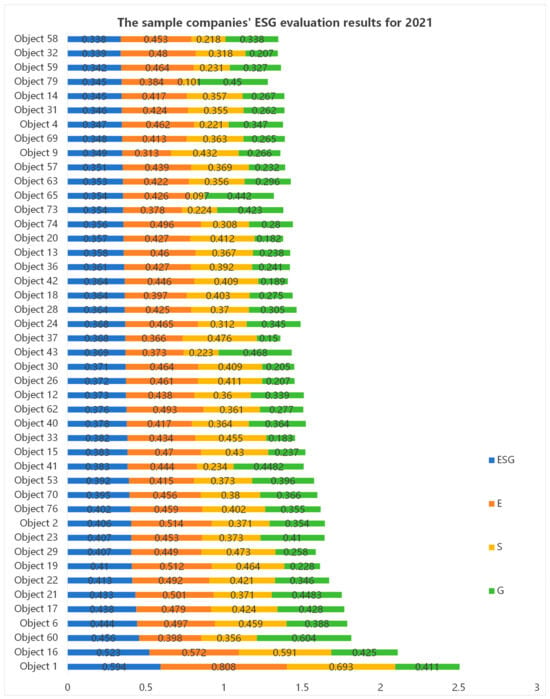

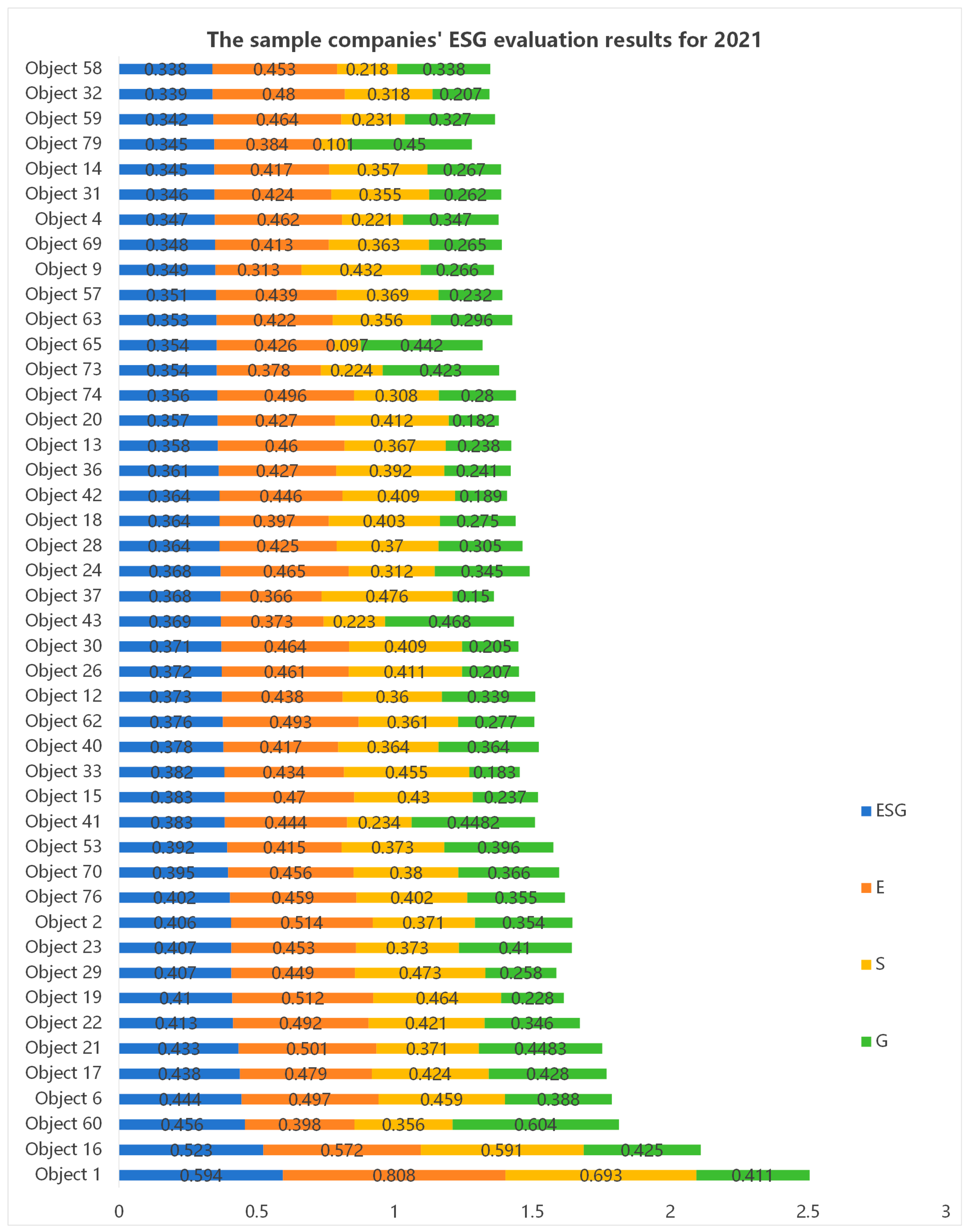

According to the data in Table 3, the average ESG score of the sample companies is 0.347 points, and only 38 companies exceed the average score, indicating that the ESG comprehensive performance of the key pollutant discharge energy enterprises is average and needs to be further improved. From the three dimensions of E, S and G, the average score of E is relatively high, at 0.428 points. From the distribution of the sample companies, it can be seen that only 35 companies exceed the average score, and the E performance of most companies is lower than the average level. The mean value of G performance is the lowest among the three dimensions, at 0.295 points, indicating that the overall performance of the key pollutant energy industry in G is not ideal.

(1) From the perspective of the ESG performance of a single sample company, the ESG of sample company 1, sample company 16 and sample company 60 ranked in the top three (Figure 1), with good overall performance; sample company 39 ranked last in the overall ESG ranking, and its scores in E, S and G were at a low level, ranking 76, 56 and 79, respectively.

(2) According to the evaluation results of the three dimensions of E, S and G of sample companies, the E and S rankings of sample companies 1 and 16, which ranked first and second in ESG overall, were consistent with the ESG comprehensive ranking. Although the G ranking was slightly behind, the overall ranking was still high, and the overall performance was stable, but starting from sample company 60, which ranked third in ESG overall ranking, the performance of different dimensions of E, S and G was uneven. G ranks first, but E and S performed poorly, ranking 59th and 37th, respectively. Similarly, G of sample company 43 ranked second, but E ranked 67th and S ranked 58th; S of sample company 37 ranked third, but E ranked 69th and G ranked 77th (third from the bottom). On the whole, the overall ESG performance of the sample companies was average; the comprehensive performance of ESG and the performance of all dimensions were significantly polarized; and the development of different dimensions of E, S and G was mostly unbalanced and uncoordinated.

Figure 1.

Top 45 sample companies’ ESG evaluation results for 2021.

Figure 1.

Top 45 sample companies’ ESG evaluation results for 2021.

Table 3.

The sample companies’ ESG evaluation results for 2021.

Table 3.

The sample companies’ ESG evaluation results for 2021.

| Evaluation Object | ESG | E | S | G | ||||

|---|---|---|---|---|---|---|---|---|

| Relative Proximity | Ranking | Relative Proximity | Ranking | Relative Proximity | Ranking | Relative Proximity | Ranking | |

| Object 1 | 0.594 | 1 | 0.808 | 1 | 0.693 | 1 | 0.411 | 10 |

| Object 16 | 0.523 | 2 | 0.572 | 2 | 0.591 | 2 | 0.425 | 8 |

| Object 60 | 0.456 | 3 | 0.398 | 59 | 0.356 | 37 | 0.604 | 1 |

| Object 6 | 0.444 | 4 | 0.497 | 6 | 0.459 | 6 | 0.388 | 13 |

| Object 17 | 0.438 | 5 | 0.479 | 11 | 0.424 | 10 | 0.428 | 7 |

| Object 21 | 0.433 | 6 | 0.501 | 5 | 0.371 | 23 | 0.4483 | 4 |

| Object 22 | 0.413 | 7 | 0.492 | 9 | 0.421 | 11 | 0.346 | 24 |

| Object 19 | 0.410 | 8 | 0.512 | 4 | 0.464 | 5 | 0.228 | 59 |

| Object 29 | 0.407 | 9 | 0.449 | 27 | 0.473 | 4 | 0.258 | 50 |

| Object 23 | 0.407 | 10 | 0.453 | 24 | 0.373 | 22 | 0.410 | 11 |

| Object 2 | 0.406 | 11 | 0.514 | 3 | 0.371 | 24 | 0.354 | 19 |

| Object 76 | 0.402 | 12 | 0.459 | 20 | 0.402 | 18 | 0.355 | 18 |

| Object 70 | 0.395 | 13 | 0.456 | 22 | 0.380 | 20 | 0.366 | 16 |

| Object 53 | 0.392 | 14 | 0.415 | 50 | 0.373 | 21 | 0.396 | 12 |

| Object 41 | 0.383 | 15 | 0.444 | 30 | 0.234 | 50 | 0.4482 | 5 |

| Object 15 | 0.383 | 16 | 0.470 | 12 | 0.430 | 9 | 0.237 | 57 |

| Object 33 | 0.382 | 17 | 0.434 | 33 | 0.455 | 7 | 0.183 | 70 |

| Object 40 | 0.378 | 18 | 0.417 | 47 | 0.364 | 28 | 0.364 | 17 |

| Object 62 | 0.376 | 19 | 0.493 | 8 | 0.361 | 30 | 0.277 | 41 |

| Object 12 | 0.373 | 20 | 0.438 | 32 | 0.360 | 33 | 0.339 | 28 |

| Object 26 | 0.372 | 21 | 0.461 | 18 | 0.411 | 14 | 0.207 | 63 |

| Object 30 | 0.371 | 22 | 0.464 | 15 | 0.409 | 16 | 0.205 | 65 |

| Object 43 | 0.369 | 23 | 0.373 | 67 | 0.223 | 58 | 0.468 | 2 |

| Object 37 | 0.368 | 24 | 0.366 | 69 | 0.476 | 3 | 0.150 | 77 |

| Object 24 | 0.368 | 25 | 0.465 | 13 | 0.312 | 41 | 0.345 | 25 |

| Object 28 | 0.364 | 26 | 0.425 | 42 | 0.370 | 25 | 0.305 | 35 |

| Object 18 | 0.364 | 27 | 0.397 | 61 | 0.403 | 17 | 0.275 | 42 |

| Object 42 | 0.364 | 28 | 0.446 | 29 | 0.409 | 15 | 0.189 | 68 |

| Object 36 | 0.361 | 29 | 0.427 | 35 | 0.392 | 19 | 0.241 | 54 |

| Object 13 | 0.358 | 30 | 0.460 | 19 | 0.367 | 27 | 0.238 | 55 |

| Object 20 | 0.357 | 31 | 0.427 | 36 | 0.412 | 13 | 0.182 | 71 |

| Object 74 | 0.356 | 32 | 0.496 | 7 | 0.308 | 43 | 0.280 | 40 |

| Object 73 | 0.354 | 33 | 0.378 | 66 | 0.224 | 54 | 0.423 | 9 |

| Object 65 | 0.354 | 34 | 0.426 | 39 | 0.097 | 77 | 0.442 | 6 |

| Object 63 | 0.353 | 35 | 0.422 | 46 | 0.356 | 35 | 0.296 | 37 |

| Object 57 | 0.351 | 36 | 0.439 | 31 | 0.369 | 26 | 0.232 | 58 |

| Object 9 | 0.349 | 37 | 0.313 | 77 | 0.432 | 8 | 0.266 | 46 |

| Object 69 | 0.348 | 38 | 0.413 | 51 | 0.363 | 29 | 0.265 | 47 |

| Object 4 | 0.347 | 39 | 0.462 | 17 | 0.221 | 59 | 0.347 | 22 |

| Object 31 | 0.346 | 40 | 0.424 | 43 | 0.355 | 38 | 0.262 | 48 |

| Object 14 | 0.345 | 41 | 0.417 | 48 | 0.357 | 34 | 0.267 | 45 |

| Object 79 | 0.345 | 42 | 0.384 | 64 | 0.101 | 73 | 0.450 | 3 |

| Object 59 | 0.342 | 43 | 0.464 | 14 | 0.231 | 51 | 0.327 | 34 |

| Object 32 | 0.339 | 44 | 0.480 | 10 | 0.318 | 40 | 0.207 | 64 |

| Object 58 | 0.338 | 45 | 0.453 | 23 | 0.218 | 61 | 0.338 | 29 |

| Object 34 | 0.337 | 46 | 0.411 | 52 | 0.361 | 31 | 0.216 | 60 |

| Object 35 | 0.335 | 47 | 0.360 | 70 | 0.353 | 39 | 0.289 | 38 |

| Object 11 | 0.332 | 48 | 0.410 | 53 | 0.361 | 32 | 0.200 | 66 |

| Object 64 | 0.332 | 49 | 0.394 | 62 | 0.356 | 36 | 0.238 | 56 |

| Object 25 | 0.331 | 50 | 0.309 | 78 | 0.417 | 12 | 0.192 | 67 |

| Object 77 | 0.328 | 51 | 0.371 | 68 | 0.237 | 49 | 0.373 | 15 |

| Object 47 | 0.328 | 52 | 0.426 | 38 | 0.139 | 66 | 0.379 | 14 |

| Object 72 | 0.324 | 53 | 0.416 | 49 | 0.228 | 53 | 0.328 | 33 |

| Object 66 | 0.311 | 54 | 0.386 | 63 | 0.215 | 62 | 0.339 | 27 |

| Object 49 | 0.311 | 55 | 0.426 | 41 | 0.092 | 79 | 0.353 | 20 |

| Object 3 | 0.310 | 56 | 0.348 | 73 | 0.223 | 57 | 0.347 | 23 |

| Object 5 | 0.310 | 57 | 0.399 | 58 | 0.143 | 65 | 0.352 | 21 |

| Object 45 | 0.309 | 58 | 0.431 | 34 | 0.221 | 60 | 0.288 | 39 |

| Object 68 | 0.308 | 59 | 0.447 | 28 | 0.270 | 45 | 0.183 | 69 |

| Object 51 | 0.307 | 60 | 0.408 | 54 | 0.264 | 46 | 0.251 | 52 |

| Object 8 | 0.302 | 61 | 0.404 | 56 | 0.305 | 44 | 0.178 | 73 |

| Object 48 | 0.301 | 62 | 0.450 | 26 | 0.098 | 75 | 0.296 | 36 |

| Object 50 | 0.301 | 63 | 0.407 | 55 | 0.097 | 76 | 0.340 | 26 |

| Object 67 | 0.299 | 64 | 0.457 | 21 | 0.224 | 55 | 0.181 | 72 |

| Object 56 | 0.298 | 65 | 0.424 | 44 | 0.241 | 48 | 0.214 | 61 |

| Object 61 | 0.296 | 66 | 0.451 | 25 | 0.134 | 69 | 0.269 | 44 |

| Object 38 | 0.295 | 67 | 0.354 | 72 | 0.310 | 42 | 0.213 | 62 |

| Object 55 | 0.294 | 68 | 0.463 | 16 | 0.121 | 71 | 0.241 | 53 |

| Object 46 | 0.292 | 69 | 0.286 | 79 | 0.249 | 47 | 0.330 | 31 |

| Object 54 | 0.286 | 70 | 0.426 | 40 | 0.230 | 52 | 0.162 | 75 |

| Object 44 | 0.285 | 71 | 0.348 | 74 | 0.135 | 68 | 0.334 | 30 |

| Object 71 | 0.280 | 72 | 0.340 | 75 | 0.138 | 67 | 0.329 | 32 |

| Object 7 | 0.279 | 73 | 0.423 | 45 | 0.095 | 78 | 0.273 | 43 |

| Object 52 | 0.276 | 74 | 0.358 | 71 | 0.210 | 63 | 0.261 | 49 |

| Object 10 | 0.266 | 75 | 0.384 | 65 | 0.154 | 64 | 0.256 | 51 |

| Object 75 | 0.252 | 76 | 0.426 | 37 | 0.100 | 74 | 0.157 | 76 |

| Object 78 | 0.250 | 77 | 0.398 | 60 | 0.125 | 70 | 0.177 | 74 |

| Object 27 | 0.236 | 78 | 0.404 | 57 | 0.103 | 72 | 0.134 | 78 |

| Object 39 | 0.226 | 79 | 0.313 | 76 | 0.224 | 56 | 0.129 | 79 |

| 0.347 | 0.428 | 0.300 | 0.295 | |||||

6. Conclusions and Related Recommendations

6.1. Main Conclusions

In order to improve the sustainable development ability of Chinese energy enterprises and solve the contradiction between low-carbon development and energy security of energy enterprises, an empirical study on ESG evaluation of Chinese energy enterprises was carried out, and the conclusions of this paper were as follows:

Firstly, based on the theory of sustainable development, the new development concept and the concept of safe development were integrated to reasonably interpret the definition of ESG for Chinese energy enterprises and enrich the connotation and extension of ESG. On this basis, using the Delphi method, starting from the three dimensions of environment, society and governance, 40 specific indicators reflecting the concepts of innovation, coordination, green, open, sharing and security were selected to build an ESG structural dimension model. This index system is scientific, objective and feasible, reflecting the reality that China’s energy enterprises, under the characteristics of “rich coal, poor oil and less gas” energy resource endowment, must not only bear the social responsibility of producing coal and coal power to ensure energy security, but also bear the environmental responsibility of innovation-driven realization of the two-carbon goal.

Secondly, in terms of model and method, combining the advantages and disadvantages of the AHP method and entropy method, the weight model of the ESG evaluation index of Chinese energy enterprises was constructed by using an AHP–entropy combination weighting method. The model can scientifically determine the weights of the target layer, criterion layer and indicator layer in the ESG evaluation system, and the weight results are consistent with China’s current policy of ensuring national energy security as the bottom line and steadily promoting carbon peak, which is conducive to the realization of sustainable development goals for Chinese energy enterprises.

Thirdly, after obtaining the weights of each index in the ESG evaluation system, the ESG evaluation model of Chinese energy enterprises was constructed with the TOPSIS method. Seventy-nine key pollutant energy listed enterprises were taken as sample enterprises to evaluate their ESG comprehensive level and the performance of E, S and G in 2021. The results showed that the overall ESG performance of the sample companies was average, and the performance of G was not ideal. There was significant polarization in ESG synthesis and in all dimensions. Most of the different dimensions of E, S and G developed unevenly and were uncoordinated. The empirical results are consistent with the actual situation of the sample enterprises. The ESG evaluation system can measure the sustainable development level of Chinese energy enterprises scientifically and reasonably.

6.2. Policy Implications

The first recommendation is to strengthen the top-level design of ESG and build a healthy ecosystem of ESG. The state should improve the legal system of ESG information disclosure supervision of listed companies as soon as possible. The regulatory authorities should learn from the mainstream ESG information disclosure norms at home and abroad, combine the actual situation of China, and establish a graded and classified ESG information disclosure system and information supervision and related error correction system according to the industry, scale and risk exposure degree; formulate normative guidelines for information disclosure with Chinese characteristics; formulate an industry-specific ESG information disclosure index system; establish a mandatory ESG information disclosure system for the energy sector; promote full coverage of ESG disclosure subjects; prevent “greenwashing” behavior of selective disclosure; establish environmental disclosure indicators in line with international GRI standards, which not only disclose carbon emissions but also subdivide carbon emissions into direct emissions, indirect emissions and other indirect emissions; and disclose the data of the past three years to improve the vertical comparability of information disclosure and strengthen ESG-oriented information disclosure.

The regulatory authorities should give play to the leading role of the government and reward enterprises with high-quality ESG information disclosure and good ESG performance with government subsidies, green credit concessions, tax deductions and other rewards; establish a negative list of enterprises with poor ESG performance and poor ESG information disclosure evaluation; guide banks to reduce the loan amount or increase the loan restriction; increase the cost of enterprises with poor ESG performance; and increase the punishment for false ESG information disclosure.

CSRC, stock exchanges, AMAC and other relevant capital market departments should guide and supervise the ESG behavior of enterprises. The natural resources department should incorporate the ESG principle into the green mine identification standard; carry out green mine construction and ecological governance; and play the role of carbon compensation, carbon reduction and carbon sequestration. Third-party institutions and auditing institutions should be encouraged to review ESG information disclosure; for example, Petrochina hired Price Waterhouse Coopers Zhongtian accounting firm to independently verify its 2022 ESG performance indicators to ensure the reliability of indicators. The regulatory authorities should give full play to the role of media supervision and reputation mechanism and supervise enterprise ESG information disclosure and its responsibility performance.

The regulatory authorities should strengthen data sharing between environmental protection departments, marketing departments and third-party evaluation departments and improve the quality and efficiency of cross-departmental data collection. Energy enterprises should integrate various information systems by means of data technology through independent innovation or the establishment of an innovation consortium; strengthen carbon asset management such as carbon verification; improve the professional ability to collect, sort and process complex environmental indicators; establish an authoritative and comprehensive shared cloud platform; establish a big data model for ESG risk early warning, risk prevention and control and processing; realize an intelligent ESG database; promote the standardization and informatization of ESG management; and promote the digital transformation of enterprise ESG management.

Secondly, ESG investments should be combined with national energy security and carbon neutrality goals to promote safe and green development. The People’s Bank of China, the National Development and Reform Commission, the China Securities Regulatory Commission and other departments should guide and improve the landing policies and information disclosure of green bond support projects and support the development of green investment projects in the form of green bonds by using ESG investment concepts to guide the investment transformation of high-energy energy industries. The National Development and Reform Commission and the People’s Bank of China should further increase financial support for coal power enterprises based on coal-based national conditions; promote cooperation with key energy resource countries; deepen the “Belt and Road” energy cooperation partnership; improve energy supply security capacity at the same time as green finance as the energy industry carbon neutral implementation path, with the green industry fund guidance role and sustainable finance financing support; and promote the implementation of low-carbon clean utilization of high-carbon energy project cooperation. Financial institutions should improve the ESG risk management system and incorporate the ESG performance of energy enterprises into the credit-granting process. Large institutional investors should play a demonstration effect, develop ESG-themed diversified investment products, enrich and innovate green securities financial products and services, take the initiative to follow the green index and force energy companies to improve ESG performance by exercising shareholder voting rights.

Finally, the ESG concept should be integrated with corporate strategy to promote the modernization of corporate governance capabilities. Energy enterprises should take the initiative to “embrace” ESG, integrate ESG into their development strategies, implement ESG concepts from top to bottom, improve ESG governance structure and operating mechanisms, and establish ESG target management and performance appraisal mechanisms. In particular, energy enterprises should formulate medium- and long-term environmental governance goals and improve carbon emission control levels. The state should formulate laws and regulations to clarify the relationship between enterprise Party organizations and decision-making management and other governance subjects, and enterprises should clarify the boundaries of powers and responsibilities of each governance subject in the articles of association, implement the management functions and powers of the board of directors as the highest decision-making body of ESG, amend the Governance Rules for Listed Companies, add an ESG management professional committee to the board of directors, increase the proportion of external directors with ESG management background, improve the quality of ESG investment decisions of the board of directors, strengthen ESG special training, integrate ESG into the whole process of enterprise operation, study low-carbon development paths, research and develop carbon capture and utilization technology, reduce carbon footprint, and promote clean and efficient utilization of the whole energy industry chain. By using the information dissemination function of media, analysts and other channels, we can reduce the information asymmetry between enterprises and external stakeholders, improve ESG performance and actively respond to institutional pressure and stakeholder demands to gain competitive advantages, achieve green transformation and enable high-quality development.

6.3. Limitations and Further Research Ideas

(1) Because China has not developed an industry-specific ESG information disclosure index system, the environmental and social information disclosure of Chinese energy enterprises is not standardized and detailed. Therefore, considering the availability of data, the selection of some evaluation indicators is not specific and accurate enough.

(2) Since the China Securities Regulatory Commission has required listed companies to add an environmental chapter to their annual reports since 28 June 2021, and the Ministry of Ecology and Environment has made it clear on 31 December 2021 that key pollutant discharge units are required to disclose key environmental information, while other energy enterprises are required to disclose environmental information voluntarily, considering the difficulty in obtaining environmental data, the research sample in this paper is limited to the enterprises listed in the list of key polluters published by the Ministry of Ecological and Environmental Protection. Horizontally, the ESG level of all Chinese energy enterprises cannot be comprehensively evaluated. Vertically, it is not possible to compare the ESG performance of Chinese energy enterprises before 2021.

(3) Based on the interpretation of the connotation of ESG in Chinese energy enterprises, this paper carries out an empirical study on ESG evaluation. However, this study mainly reflects the level and status of sustainable development of enterprises. To achieve sustainable development goals, energy enterprises ultimately need to rely on the endogenous driving force of enterprise ESG, and this study does not carry out in-depth research on ESG driving mechanisms.

(4) According to the ESG information disclosure guidelines with Chinese characteristics and accurate indicators formulated by China in the future, at the same time, the ESG evaluation index system will be more refined by building a data-sharing platform and digital transformation of enterprise ESG management, so as to more accurately improve the sustainable development ability of energy enterprises.

(5) As China establishes a mandatory ESG information disclosure system in the energy sector and promotes full coverage of ESG disclosure subjects in the future, horizontal and vertical comparative studies on ESG of energy enterprises can be carried out comprehensively among energy enterprises.

(6) In order to explore the driving mechanism for energy enterprises to practice ESG, in the future, ESG evaluation results will be used as explanatory variables to perform a vertical empirical analysis of the relationship between ESG performance and enterprise value of energy enterprises and the action path, which will have deeper significance for promoting high-quality development.

Author Contributions

Writing—review & editing, X.X.; Supervision, H.Z. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data are contained within the article.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Fan, Y.; Yi, B.W. The law, driving mechanism and China’s path of energy transformation. Manag. World 2021, 37, 95–105. [Google Scholar]

- Zhang, X.L.; Zhang, D.; Yu, R.X. Design theory and practice of national carbon market with Chinese characteristics. Manag. World 2021, 37, 80–95. [Google Scholar]

- Wal, T. Financiers Put Social Teeth into Money Decisions, at Hearing on New Global Finance Framework[EB/OL].[5/20]. Available online: https://www.unglobalcompact.org/news/1761-04-08-2015 (accessed on 26 May 2024).

- Michelson, G.; Wailes, N.; Van Der Laan, S.; Frost, G. Ethical investment Processes and Outcomes. J. Bus. Ethics 2004, 52, 1–10. [Google Scholar] [CrossRef]

- Liu, B.; Lu, J.R.; Ju, T. Formalism or materialism: A study of green innovation under the soft regulation of ESG rating. Nankai Bus. Rev. 2023, 26, 16–26. [Google Scholar]

- Leins, S. ‘Responsible investment’: ESG and the post-crisis ethical order. Econ. Soc. 2020, 49, 71–91. [Google Scholar] [CrossRef]

- Huang, S.Z. Three theoretical pillars underpin ESG. Financ. Account. Mon. 2021, 19, 3–10. [Google Scholar]

- Baran, M.; Kuźniarska, A.; Makieła, Z.J.; Sławik, A.; Stuss, M.M. Does ESG Reporting Relate to Corporate Financial Performance in the Context of the Energy Sector Transformation? Evidence from Poland. Energies 2022, 15, 477. [Google Scholar] [CrossRef]

- Chodnicka-Jaworska, P. Environmental, Social, and Governance Impact on Energy Sector Default Risk—Long-Term Issuer Credit Ratings Perspective. Front. Energy Res. 2022, 10, 817679. [Google Scholar] [CrossRef]

- Zainullin, S.; Zainullina, O. Scientific review digitalization of corporate culture as a factor influencing ESG investment in the energy sector. Int. Rev. 2021, 130–136. [Google Scholar] [CrossRef]

- Baldini, M.; Maso, L.D.; Liberatore, G.; Mazzi, F.; Terzani, S. Role of Country- and Firm-Level Determinants in Environmental, Social, and Governance Disclosure. J. Bus. Ethics 2018, 150, 79–98. [Google Scholar] [CrossRef]

- Drempetic, S.; Klein, C.; Zwergel, B. The Influence of Firm Size on the ESG Score: Corporate Sustainability Ratings Under Review. J. Bus. Ethics 2020, 167, 333–360. [Google Scholar] [CrossRef]

- Galbreath, J. ESG in Focus: The Australian Evidence. J. Bus. Ethics 2013, 118, 529–541. [Google Scholar] [CrossRef]

- Branco, M.C.; Rodrigues, L.L. Factors Influencing Social Responsibility Disclosure by Portuguese Companies. J. Bus. Ethics 2008, 83, 685–701. [Google Scholar] [CrossRef]

- Parfitt, C. ESG Integration Treats Ethics as Risk, but Whose Ethics and Whose Risk? Responsible Investment in the Context of Precarity and Risk-Shifting. Crit. Sociol. 2020, 46, 573–587. [Google Scholar] [CrossRef]

- Cao, Q.; Xu, Q. Research on the construction of financial “environmental, Social and Governance” (ESG) system. Financ. Regul. Res. 2019, 4, 95–111. [Google Scholar]

- Li, J.L.; Yang, Z.; Chen, J. The mechanism of ESG promoting firm performance: Based on the perspective of firm innovation. Sci. Sci. Manag. S.& T 2021, 42, 71–89. [Google Scholar]

- Pedersen, L.H.; Fitzgibbons, S.; Pomorski, L. Responsible investing: The ESG-efficient frontier. J. Financ. Econ. 2021, 142, 572–597. [Google Scholar] [CrossRef]

- Hill, R.P.; Ainscough, T.; Shank, T.; Manullang, D. Corporate Social Responsibility and Socially Responsible Investing: A Global Perspective. J. Bus. Ethics 2007, 70, 165–174. [Google Scholar] [CrossRef]

- Widyawati, L. Measurement concerns and agreement of environmental social governance ratings. Account. Financ. 2021, 61, 1589–1623. [Google Scholar] [CrossRef]

- Berg, F.; Kölbel, J.F.; Rigobon, R. Aggregate Confusion: The Divergence of ESG Ratings. Rev. Financ. 2022, 26, 1315–1344. [Google Scholar] [CrossRef]

- Huber, B.M.; Comstock, M. ESG reports and ratings: What they are, why they matter? Corp. Gov. Advis. 2017, 25, 1–12. [Google Scholar]

- Sahin, Ö.; Bax, K.; Czado, C.; Paterlini, S. Environmental, Social, Governance scores and the Missing pillar—Why does missing information matter? Corp. Soc. Responsib. Environ. Manag. 2022, 29, 1782–1798. [Google Scholar] [CrossRef]

- Wang, K.; Zhang, Z.W. Current situation, comparison and outlook of ESG rating at home and abroad. Financ. Account. Mon. 2022, 2, 137–143. [Google Scholar]

- Chen, N.; Sun, F. The comparison of ESG system development at home and abroad and the suggestion of constructing ESG system in China. Dev. Res. 2019, 3, 59–64. [Google Scholar]

- Su, C.; Chen, C. Research on ESG evaluation system of listed companies under the new development concept—A case study of listed companies in heavy pollution manufacturing industry. Financ. Account. Mon. 2022, 6, 155–160. [Google Scholar]

- Chatterji, A.K.; Durand, R.; Levine, D.I.; Touboul, S. Do ratings of firms converge? Implications for managers, investors and strategy researchers. Strateg. Manag. J. 2016, 37, 1597–1614. [Google Scholar] [CrossRef]

- Christensen, D.M.; Serafeim, G.; Sikochi, A. Why is Corporate Virtue in the Eye of The Beholder? The Case of ESG Ratings. Account. Rev. 2022, 97, 147–175. [Google Scholar] [CrossRef]

- Avramov, D.; Cheng, S.; Lioui, A.; Tarelli, A. Sustainable investing with ESG rating uncertainty. J. Financ. Econ. 2022, 145, 642–664. [Google Scholar] [CrossRef]

- Friede, G.; Busch, T.; Bassen, A. ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. J. Sustain. Financ. Invest. 2015, 5, 210–233. [Google Scholar] [CrossRef]

- Velte, P. Does ESG performance have an impact on financial performance? Evidence from Germany. J. Glob. Responsib. 2017, 8, 169–178. [Google Scholar] [CrossRef]

- Duque-Grisales, E.; Aguilera-Caracuel, J. Environmental, Social and Governance (ESG) Scores and Financial Performance of Multilatinas: Moderating Effects of Geographic International Diversification and Financial Slack. J. Bus. Ethics 2021, 168, 315–334. [Google Scholar] [CrossRef]

- Atan, R.; Alam, M.M.; Said, J.; Zamri, M. The impacts of environmental, social, and governance factors on firm performance: Panel study of Malaysian companies. Manag. Environ. Qual. Int. J. 2018, 29, 182–194. [Google Scholar] [CrossRef]

- Galema, R.; Plantinga, A.; Scholtens, B. The stocks at stake: Return and risk in socially responsible investment. J. Bank. Financ. 2008, 32, 2646–2654. [Google Scholar] [CrossRef]

- Xie, J.; Nozawa, W.; Yagi, M.; Fujii, H.; Managi, S. Do environmental, social, and governance activities improve corporate financial performance? Bus. Strategy Environ. 2019, 28, 286–300. [Google Scholar] [CrossRef]

- Shaikh, I. Environmental, Social, and Governance (ESG) Practice and Firm Performance: An International Evidence. J. Bus. Econ. Manag. 2022, 23, 218–237. [Google Scholar] [CrossRef]

- Pastor, L.; Stambaugh, R.F.; Taylor, L.A. Sustainable investing in equilibrium. J. Financ. Econ. 2021, 142, 550–571. [Google Scholar] [CrossRef]

- Zhang, D. Are firms motivated to greenwash by financial constraints? Evidence from global firms’ data. J. Int. Financ. Manag. Account. 2022, 33, 459–479. [Google Scholar] [CrossRef]

- Tan, Y.; Zhu, Z. The effect of ESG rating events on corporate green innovation in China: The mediating role of financial constraints and managers’ environmental awareness. Technol. Soc. 2022, 68, 101906. [Google Scholar] [CrossRef]

- Kim, S.; Li, Z.F. Understanding the Impact of ESG Practices in Corporate Finance. Sustainability 2021, 13, 3746. [Google Scholar] [CrossRef]

- Li, P.; Zhou, R.; Xiong, Y. Can ESG Performance Affect Bond Default Rate? Evidence from China. Sustainability 2020, 12, 2954. [Google Scholar] [CrossRef]

- Aslan, A.; Poppe, L.; Posch, P. Are Sustainable Companies More Likely to Default? Evidence from the Dynamics between Credit and ESG Ratings. Sustainability 2021, 13, 8568. [Google Scholar] [CrossRef]

- Zhao, C.; Guo, Y.; Yuan, J.; Wu, M.; Li, D.; Zhou, Y.; Kang, J. ESG and Corporate Financial Performance: Empirical Evidence from China’s Listed Power Generation Companies. Sustainability 2018, 10, 2607. [Google Scholar] [CrossRef]

- Hao, S.; Ren, C.; Zhang, L. Research on Performance Evaluation of Coal Enterprises Based on Grounded Theory, Entropy Method and Cloud Model from the Perspective of ESG. Sustainability 2022, 14, 11526. [Google Scholar] [CrossRef]

- Shen, H.T.; Li, S.Y.; Lin, H.H. Rethinking the value relevance of ESG ratings: A risk-based perspective. Financ. Account. Mon. 2022, 1–9. [Google Scholar] [CrossRef]

- Huang, Q.H. New concept of development: A systematic theory of development. Econ. Perspect. 2022, 8, 13–24. [Google Scholar]

- Zhang, H. Theoretical basis, research status and future prospect of ESG responsible investment. Financ. Account. Mon. 2022, 933, 143–150. [Google Scholar]

- Hammond, A.; Adriaanse, A.; Rodenburg, E.; Bryant, D.; Woodward, R. Environmental Indicators: A Systematic Approach to Measuring and Reporting on Environmental Policy Performance in the Context of Sustainable Development; World Resource Institute: Washington, DC, USA, 1995. [Google Scholar]

- Bai, C.E.; Liu, Q.; Lu, Z.; Song, M.; Zhang, J.X. An empirical study on the governance structure of Chinese listed companies. Econ. Res. J. 2005, 2, 81–91. [Google Scholar]

- Jiang, Y.; Lu, Z.F. Corporate governance and equity financing cost: A study on governance effects of single and comprehensive mechanisms. J. Quant. Tech. Econ. 2009, 26, 60–75. [Google Scholar]

- Zhang, H.L.; Lu, Z.F. Cash distribution, corporate governance and overinvestment: An investigation of cash holdings of listed companies and their subsidiaries in China. Manag. World 2012, 141–150. [Google Scholar] [CrossRef]

- Qiu, M.; Yin, H. ESG performance and financing cost of enterprises in the context of ecological civilization construction. J. Quant. Tech. Econ. 2019, 36, 108–123. [Google Scholar]

- Zhang, Z.L.; Deng, W.Y.Y. Study on the effect and path of local government debt on corporate ESG. Mod. Econ. Res. 2022, 10–21. [Google Scholar]

- Liu, X.X.; Li, H.Y.; Kong, X.X. Study on the influence of Party organization governance on ESG performance of enterprises. Collect. Essays Financ. Econ. 2022, 38, 100–112. [Google Scholar]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).