Relationships between Sustainable Operations and the Resilience of SMEs

1

Institute of Agricultural and Food Economics, Hungarian University of Agriculture and Life Sciences, 2100 Gödöllő, Hungary

2

Doctoral School of Economic and Regional Sciences, Hungarian University of Agriculture and Life Sciences, 2100 Gödöllő, Hungary

*

Authors to whom correspondence should be addressed.

Sustainability 2024, 16(2), 741; https://doi.org/10.3390/su16020741

Submission received: 10 November 2023

/

Revised: 12 January 2024

/

Accepted: 12 January 2024

/

Published: 15 January 2024

(This article belongs to the Special Issue Sustainable Development of Small and Medium-Sized Enterprises: Resilience, Creativity and Learning)

Abstract

:In the 21st century, the primary concerns within our society and economic framework revolve around securing a sustainable future and ensuring our future prospects. The crises witnessed in recent years have both introduced new challenges and revived existing difficulties. The crucial question emerges: can societies and economies demonstrate the resilience necessary to avert impending dangers during such circumstances? This consideration holds particular significance for small and medium-sized enterprises (SMEs) operating in the global economy. SMEs play a vital role in national economies, and their importance is even more pronounced within our national societies. Addressing threats and challenges in the SME sector proves to be more challenging due to their compact size, which lacks the protective shield against various environmental impacts enjoyed by larger enterprises with their greater size and capabilities. On the other hand, due to their smaller size, SMEs may be able to overcome these obstacles more successfully than large enterprises by using the appropriate tools and investing in opportunities. The aim of this article is to investigate to what extent environmental protection investments and other sustainability-related developments increase the resilience of SMEs. In connection with the above mentioned, it was investigated how the combination of marketing communication and sustainability goals, and how appropriate communication of sustainability, contributes to increasing the resilience of Hungarian SMEs. The analysis is based on a grouping of 266 small and medium-sized enterprises using the variables created based on the literature review and expert interviews.

1. Introduction

The pursuit of sustainability and its declaration are increasingly an external constraint for businesses (ESG). At the same time, it is also necessary to communicate the efforts made in the field of sustainability to consumers, and it is essential to choose the appropriate communication channels and tools. Growing numbers of organizations are facing increasing pressure from their stakeholders to broaden their performance reporting to encompass a more comprehensive perspective, such as triple bottom line (TBL) reporting [1,2,3,4]. This imperative is not solely an internal decision made by the organization’s management; rather, it is a response to the need for competitiveness, prompting organizations to continually reassess and potentially change their business models [5].

A study conducted by Tripopsakul and Puriwat in 2022 affirms that the environmental (E), social (S), and governance (G) aspects of ESG (environmental, social, and governance) directly impact customer engagement and brand trust [6]. The authors’ findings underscore the rationale behind current trends in ESG-integrated marketing communication strategies, aiding in determining which specific ESG categories should be emphasized and implemented to secure customer engagement and brand trust. To facilitate these concepts in a form adhering to the necessity of adapting to and defending against novel hazards, some notable examples of which are the COVID-19 pandemic and the Ukrainian war situation, the authors conducted questionnaire-based research in the Hungarian small- and medium enterprise (SME) sector. The aim of this study is to determine the intricate relationships among sustainability, integrated marketing communication, and enterprise resilience, and how they may form or reform SME practice. The main research question is the following:

Is there a connection between the use of integrated marketing communication tools and the pursuit of sustainability among Hungarian SMEs, and how does this contribute to the resilience of Hungarian SMEs?

What is the gap in our research, then? Several financial and organizational factors have been identified as barriers to the adoption of circular economy (CE) principles and practices [7,8] and to sustainability [9], showing that sustainability takes effort on the enterprise side. Yet, there is limited empirical evidence, especially regarding their impact on sustainable business performance, notably in emerging economies and among SMEs. Additionally, studies suggest the need for further research on the relationship between CSR and SMEs due to their significant contribution to the global economy [10]. To bridge this gap, this study examines the relationship between the use of integrated marketing communication (IMC) and its impact on SME sustainability in relation to enterprise resilience and performance. Performance also leads to the question of whether the enterprise is capable of protecting itself from hazardous external events. Therefore, another important question is, does the use of integrated marketing communication tools and sustainable operation affect the resilience of the SME sector during crises?

IMC, known for its cohesive information transmission and cross-channel consistency, is believed to rationalize management, boost performance, and fortify enterprises based on prior research. Its alignment with sustainable development makes it a valuable toolset. This leads us to our final research question: do a larger percentage of Hungarian SMEs considering sustainability engage in a planned marketing process?

In summary, this study addresses the lack of analysis concerning sustainable development and the implementation of IMC relations by SMEs.

2. Literature Review

At the European level and beyond, small and medium-sized enterprises (SMEs) are considered to be a key factor for growth, innovation, employment, social inclusion, and ultimately, for providing sustainability to society as a whole. The flexibility and adaptability of the SME sector are key features to overcome economic crises and are extremely relevant to the current state of the world [11]. In the era of economic globalization, SMEs are recognized as an engine of sustainable economic development in both the developed and developing world [12]. Climate change, the exponential growth of the world’s population, increased competition, the emergence of new technologies, and the pressure on natural resources all require more sustainable business operations. Therefore, business strategy must be increasingly associated with sustainability. Because sustainability has become one of the most important challenges of our time, many modern SMEs in the European Union are already integrating sustainability into their marketing strategy, communication, and all other activities [13].

The question is, how can a sustainability concept be applied to businesses? This is where the term ‘business sustainability’ comes from. Business sustainability has been defined as a company’s approach to achieving business competitiveness while applying sustainable strategies [14,15,16]. SMEs understand the significance of sustainability practice and its demands for several improvements to corporate social responsibility and marketing efforts [17]. Sustainability has played an increasingly important role in improving business management. It has contributed to driving companies to open up opportunities for increased commitment, forcing organizations to reposition their role in society and aligning individuals, firms, and communities toward common goals [18]. Sustainability has become part of many disciplines, and marketing is not an exception. The process of transitioning to sustainability marketing encompasses the combination of social and environmental factors into conventional marketing and thinking [18]. However, sustainability marketing is understudied [19].

Efforts to connect sustainability and marketing have materialized in the many forms of sustainable marketing—green marketing, sustainability marketing, environmental marketing, etc. This also shows that the two spheres of expertise have a significant intersection, which, to date, is unexplored by most enterprises, especially in the SME sector. As the specific areas of this study, integrated marketing communications and sustainability orientation were chosen. Integrated marketing communications is a more cost-efficient and thereby sustainable practice of enterprise marketing suited for mostly locally established SMEs, while sustainability orientation is mainly an entrepreneurial behavior, but as such, it is thought to be more flexibly applicable than traditional sustainability measurements. Therefore, the decision was made to evaluate these concepts, drawing heavily on the specifics of the Hungarian SME sector and the structure of SME opportunities within the Hungarian business environment.

It is important also to note that enterprise sustainability works well in large organizations; however, the literature suggests that the situation is different for SMEs. Social and environmental practices are neglected by SMEs, especially in emerging markets. The existing literature mentions that a collaborative mode of operation, government policy and facilitation, and a supporting organizational culture can positively influence SMEs’ sustainability performance, and hence, improve their financial performance [20].

Various methods exist for organizations to assess their sustainability performance [1]. Numerous studies explore the sustainability performance of organizations, emphasizing their openness to innovation as a crucial factor for continuous development [21,22]. Factors such as organizational size, the complexity of the organizational structure, and diverse processes can pose challenges to measuring organizational performance [23]. To address this challenge, organizations often consider multiple dimensions of performance, including financial performance, customer satisfaction, employee satisfaction, social performance, and environmental performance [24]. Each dimension incorporates a set of performance indicators. Some organizations utilize economic indicators such as productivity concerning resource use to gauge performance [22]. Firms, based on their resources and competencies, develop the strength to attain a competitive advantage and enhance their performance. However, the resource constraints of small and medium-sized enterprises (SMEs) raise questions about their sustainability [25]. To compete effectively against larger rivals, SMEs should prioritize intangible resources, competences, and dynamic capabilities [26]. Dynamic capabilities, distinct from ordinary ones, underscore the importance of information acquisition, utilization, and continual transformation to address environmental threats in an uncertain market [27]. This perspective is crucial for integrated marketing communication (IMC), which predominantly operates on principles derived from these factors. Less-formalized SMEs demonstrate greater flexibility in responding to environmental changes [28].

The implementation of integrated marketing communication (IMC) within an organization can be considered a dynamic capability [29,30]. Recent empirical studies from both a company and customer point of view confirm the positive effect of IMC on organizational performance [25,29,30]. As two of the IMC components, the response to market changes and message integration positively impact performance [30]. Research has also shown that using marketing communication tools improves SMEs’ innovativeness in marketing [31]. For a more direct approach to connecting with sustainability, IMC can help convey information about sustainable products, encourage thoughtful buying decisions, and raise awareness about the consequences of excessive consumption and waste. Researchers have developed a conceptual model of IMC specifically for sustainable business development. This model guides enterprises in aligning their communication strategies with sustainability goals [32]. Authors also consider how the COVID-19 pandemic forced businesses to revisit their marketing communications [33].

Smaller and less-formalized SMEs exhibit a notable ability to adapt to environmental changes more swiftly than their larger counterparts, thereby gaining an additional advantage [28,34]. Within this context, corporate social responsibility (CSR) has proven to be particularly effective in pursuing adaptive strategies while adhering to the essential principles of sustainability. However, the current state of the sector, both globally and in Hungary specifically, presents a dual perspective. SMEs offer an advantageous environment for CSR due to their versatile workforces and successful local engagement [35]. Nevertheless, a considerable number of small business owners/managers tend to perceive their social and environmental impacts as negligible [36,37]. Spence [38] characterizes SMEs as fortress enterprises, primarily focused on operational duties and somewhat detached from the broader business environment. They tend to respond reactively to urgent issues [35]. Consequently, despite their inherent advantages, most SMEs view CSR as a risky endeavor, considering it an investment with minimal financial return [39,40]. Consequently, SMEs are less inclined to make substantial investments in CSR programs, as they anticipate receiving less publicity for their socially responsible actions compared with larger corporations [41].

In general, the level of social involvement in small and medium-sized enterprises is quite low compared with large companies. One of the reasons for this disparity is the financial constraints of an SME. Sharma [42] states that one of the reasons that larger companies are more likely to invest in a CSR activity is their ability to absorb fixed costs and their ease of access to capital and other resources [35]. An SME may find it difficult to access capital for this kind of investment, while its human resources may not have the capacity to be involved in CSR initiatives due to their operational duties [35]. Many scholars through their research have found that SMEs are reluctant to invest in CSR because of the limited capital available and are more likely to invest in areas that improve the performance of their businesses, such as product marketing and advertising [35,43,44,45,46]. The relationship between the connections IMC has with CSR and with sustainability is exactly the limitations and the possibilities of countering their constraints—IMC practice is a way to cut marketing costs that is extremely suitable to the SME environment. At the same time, local involvement and a well-planned CSR profile are not only applicable to general sustainability, but are also good company for IMC, as they portray an enterprise close to the community, with clear advantages and higher possible benefits in consumer goodwill.

Finally, there is one more key issue to mention regarding sustainability and enterprise strategy—social sustainability. Its most notable factors related to enterprise are the employment of people with reduced working capability and gender equality. In this study, drawing from the specific characteristics of the Hungarian SME sector and previous expert interviews, emphasis was placed on gender equality. The gender issue is a critical concept in sustainability and entrepreneurship research [47,48]. Society needs to level its playing field constantly for all members participating in the growth and maintenance of the collective, while offering benefits on the level of the individual in relation to the benefits given by them to the collective at large. Therefore, the constraints of an older form of society with strictly defined gender constructs do not fit the modern society, where benefits can be set aside in case the person who offers them does not fit criteria that deviate from equality. This provides a point of interaction for sustainability and CSR to strengthen enterprise adaptation capability and offer resilience, not only when facing the aforementioned hazards ever present in today’s modern society, but also simply in the face of the global society and the swift changes it undergoes.

Summarizing the starting points of the research, it can be concluded that the economic sustainability of SMEs depends to a large extent on the use of IMC as a dynamic capability to adapt to the uncertain market. SMEs are reluctant to invest in CSR and are more likely to invest in business areas such as marketing and advertising. Gender equality plays an important role in sustainable development, so a related variable should be included in the analysis. All these interact with sustainability to provide a novel framework of business model conceptualization.

3. Materials and Methods

For the research, Hungarian small and medium-sized enterprises with no more than 249 employees were selected using random sampling; however, micro-enterprises with 0 or 1 employees were left out of the sample. Because the concept was to measure sustainability orientation as a fundamentally entrepreneurial attitude from the aspect of businesses, if the number of employees of the enterprise does not exceed that of the entrepreneur, then there is no significant difference between the attitude of the organization and the entrepreneur. In this case, it is not possible to match the strategic operations within the enterprise’s framework, as they will completely adhere to the entrepreneur’s values, making the difference redundant.

Due to the random sampling and the specific exception in the sample collection, there was no possible way to realize a significantly representative sample, so the final sample aimed only to mirror the structure of the Hungarian SME sector in terms of enterprise size. This was a necessary consideration to exclude extreme data distortion scenarios.

Prior to conducting the research, expert interviews were undertaken to validate the intended questions. The research employed a questionnaire survey as its methodology, utilizing a purchasable company database as the source of the base population. The data collection, carried out anonymously, occurred between December 2022 and April 2023, unfolding in two distinct stages. Initially, an online questionnaire was employed, but the response rate was modest, with barely 30 filled-in items returned in a month. Consequently, the data collection approach was adjusted, incorporating telephone inquiries to supplement and facilitate the filling process. Throughout the two stages, inquiries were made to over 500 enterprises, resulting in the recording of data from a total of 318 businesses. Notably, there were no instances of valueless fillings or significant missing data, partly attributed to the nature of the telephone inquiry. Microsoft Excel was used for data processing, and where needed, responses were standardized before analysis using the IBM SPSS statistical program package. Following the analysis, the data were presented using both the IBM SPSS statistical program package and Microsoft Excel programs.

Hypothesis 1 (H1):

According to the sustainability pillar of economic reasonableness, the sustainable part of Hungarian small and medium-sized enterprises carries out a planned marketing process in a larger percentage.

To validate this hypothesis, logistic regression was used in SPSS.

Hypothesis 2 (H2):

The use of integrated marketing communication affects the resilience of the SME sector during crises positively.

Hypothesis (H3):

The use of sustainability goals affects the resilience of the SME sector during crises positively.

To validate these hypotheses, logistic regression was used in SPSS.

Hypothesis 4 (H4):

The investigated enterprises can be divided into clearly distinguishable groups according to the variables used.

To validate this hypothesis, K-means cluster analysis was used. Interrelated variables and segments were determined via factor analysis.

According to the literature review, variables connecting to social and environmental performance were selected to segment the surveyed enterprises. Because the appropriate communication of sustainability to the stakeholders is ensured by using integrated marketing communication tools at the given enterprises, these factors were also taken into account in the segmentation. The positive economic effect of the sustainable efforts of the enterprises can be realized only in this way. As such, the use of the IMC tools belong to the economic pillar of sustainability in our concept. In terms of sustainability, we considered it important to have the gender equality variable, as this has a particularly important role in sustainable development [49], and expert interviews heavily stressed the importance of the topic in the Hungarian SME sector. Furthermore, gender equality and sustainable development can reinforce each other in powerful ways [50].

The questionnaire contained four groups of questions about the basic information of the enterprise, marketing, sustainability, and COVID-19 crises. Likert scales were used for the variables used in the cluster analysis, while the binary variables of the questionnaire were used for the logistic regression.

The research sample consists of a total of 318 enterprises that can be classified in the SME sector. The businesses included in the final sample did not refuse to answer during the survey, and they answered all the questions.

One element of the sample that determined whether the business in question is a micro-, small-, or a medium-sized enterprise was the number of employees of the enterprise. During the sampling, there were also enterprises that, due to their high added value, reached the category of small or medium-sized companies, even though based on the number of employees, they would not be a company of that size, but one category smaller. Following the rules of the European Union, those who reached the required level according to one of the conditions were classified into the higher category.

Question Q1 (the nature of your business) included in the questionnaire was included as a control question. Based on the answers, all of the business managers interviewed knew or correctly judged the size or financial statistics of their own business, showing clear competence in their place in the enterprise classification.

The other condition, which is defined by the European Union, is related to the total balance sheet or the annual income. According to total assets, 78% of enterprises were micro-enterprises, while 22% were small enterprises (which, of course, does not apply due to the number of employees). No company reached the balance sheet total, which is required to be classified as a medium-sized enterprise, so all of the 24 companies employing the most people became medium-sized enterprises based on their number of employees.

The companies were founded in the period 1999–2020. The number of businesses founded in 2010 and the number of businesses founded in 2020 are both exceptionally high. However, few surviving businesses remain that were established during the earliest period and the period of the 2008 global economic crisis.

4. Results

Does a larger percentage of Hungarian small and medium-sized enterprises that take sustainability into account carry out a planned marketing process? How does the consideration of sustainability and the use of integrated marketing communication tools during operation affect the improvement in the company’s performance? To find the answers to these questions, logistic regression was used.

4.1. Reliability of the Data Used in Logistic Regression

Reliability testing of the questionnaire questions, which were binary data without exemption and used logistic regression analysis, was performed.

- Q8. If your company applied for support from EU Budget, was it successful?

- Q9. Does your company carry out separate marketing activities?

- Q10. Does your company have a marketing manager or department?

- Q14. Does your company use integrated marketing communication tools?

- Q25. Does your business take sustainability into account in its operations?

- Q45. Has the economic result of the business improved during COVID?

4.2. Prerequisites of the Binary Regression

The logistic regression also requires the testing of multicollinearity. According to the collinearity statistics, the data are suitable for the analysis, and the VIF values are all below 2 or around 2.

4.3. Results of the First Logistic Regression

At first, the effects of the marketing tools and activities, as well as the successful applications for EU support for sustainable operation of the enterprises, were analyzed with the help of logistic regression.

As mentioned previously, the dependent variable was Q25 (Does your business take sustainability into account in its operations?)

The independent variables in this model were the following:

- Q8. If your company applied for support from EU Budget, was it successful?

- Q9. Does your company carry out separate marketing activities?

- Q10. Does your company have a marketing manager or department?

- Q14. Does your company use integrated marketing communication tools?

Results can be seen in Table 5.

As shown in Table 5, 101 cases belong to the group that do not take into consideration sustainability during their operation, and 217 cases belong to the group that do take into consideration sustainability aspects during operation, i.e., 68.2% of the sample.

Separate significance values can be seen in Table 6.

According to the Nagelkerke index, the variables explain 39.7% of the variance of the dependent variable. The index and its related values can be seen in Table 7 and Table 8.

The classification table shows that the independent variables contribute to the correct categorization of the dependent variable, because the right categorization of the data was better, with 12% according to the expected success of random categorization.

Significance values can be seen in Table 9.

The variables Q10 and Q8 are significant, and based on the Wald statistic, both variables contribute to the model. So, if a business employs a separate marketing manager or has a marketing department, it increases the chances of the business’s sustainable operation to a great extent. The separate marketing department increases this chance by more than 8 times, while the successful application for EU support increases it by more than 4 times.

4.4. Results of the Second Logistic Regression

In this part, the relations between economic performance (improvement in the economic result during the COVID-19 crisis) and the independent variables, the sustainable operation, the use of IMC tools, and the employment of a separate marketing manager, were investigated.

As mentioned previously, the dependent variable was Q45 (Has the economic result improved during COVID?). Results can be seen in Table 10.

As seen in Table 10, 26 cases belong to the group whose results did not improve as a result of the pandemic, while 292 cases belong to the group whose results improved as a result of the pandemic, i.e., 91.8% of the sample. Table 11 shows variables Q14 and Q25 are significant individually.

According to the Nagelkerke index, the three variables explain 16.6% of the variance of the dependent variable. This can be seen in Table 12.

It can be seen from the classification table that the independent variables did not contribute to the correct categorization of the dependent variable, because the ratio is 91.8%, which is the same as the expected success of random categorization. Contributions and related data can be seen in Table 13 and Table 14.

The variables Q14 and Q25 are still significant, but based on the Wald statistic, only Q14 contributes to the model. So, if a business uses the tools of integrated marketing communication, it increases the chances of the business’s results improving during the COVID-19 pandemic by six times.

4.5. Results of the Factor Analysis

The Cronbach alpha value for the variables used in the factor and cluster analyses was 0.822 for the 16 Likert scale items, where 1 meant the least true and 5 the most true.

The factor analysis ended with 266 items, i.e., 53 items were excluded from the analysis because of a lack of data (these are the businesses that answered no to the use of integrated marketing communication, so the questions regarding the use of the individual integrated marketing communication tools were not answered, thus the lack of data and unsuitability for the analysis). The KMO test was 0.882. The factor analysis finally resulted in five factors, which can be seen in Table 15.

As can be seen, the variance ratio does not increase significantly beyond five factors, which means that five factors are a statistically realistic result for the study. The rotated (Varimax) component matrix of the factors can be seen in Table 16, where the highest values by factor are highlighted.

The statements for the Likert scales in the questionnaire were the following:

- We communicate with clear, simple messages.

- We advertise with a unified message on all channels.

- We monitor consumer feedback.

- We incorporate consumer feedback into communication.

- We pay attention to the quick reaction of marketing.

- We pay attention to gender equality in the company.

- We invest in the immediate natural environment.

- We use environmentally friendly technologies and options.

- We support extensive environmental protection.

- We participate in large environmental protection systems.

- We prefer stable developments that are sure to pay off.

- We prefer longer-term returns.

- We try to buy locally as much as possible.

- We are constantly rationalizing our costs.

- Short projects are adjusted to long-term plans.

- We try to be an employee-friendly workplace.

Based on the KMO and Bartlett tests, we can say that the study is successful, and based on the factors and the variance ratio, it can be stated that the obtained factors are characteristic.

Going by the variables included in the different factors, the names of the factors are the following:

- Factor 1: the highest value was achieved by the sustainability-related variables, among which the environmental and social variables were included to the most significant extent. This factor is named social responsibility.

- Factor 2: variables focusing on long-term investments received the highest values in the factor. This factor can be called long-term development.

- Factor 3: the factor specifically focuses on communication with clear and uniform messages. This factor is the marketing messages.

- Factor 4: the factor is based in a larger part on monitoring consumer feedback and cost rationalization. The name of this factor is cost rationalization.

- Factor 5: the factor contains two variables, the incorporation of consumer feedback and the need for stable development. This factor is incorporation of consumer feedback for development.

Based on the results obtained through the factor analysis, a hierarchical cluster analysis was performed. During the hierarchical cluster analysis, Ward’s procedure was used, which allowed us to determine the ideal cluster size. Based on the standard deviation values, the Ward procedure gave the correct value, so a K-means cluster analysis was performed for three clusters. The cluster analysis gave a diversified result.

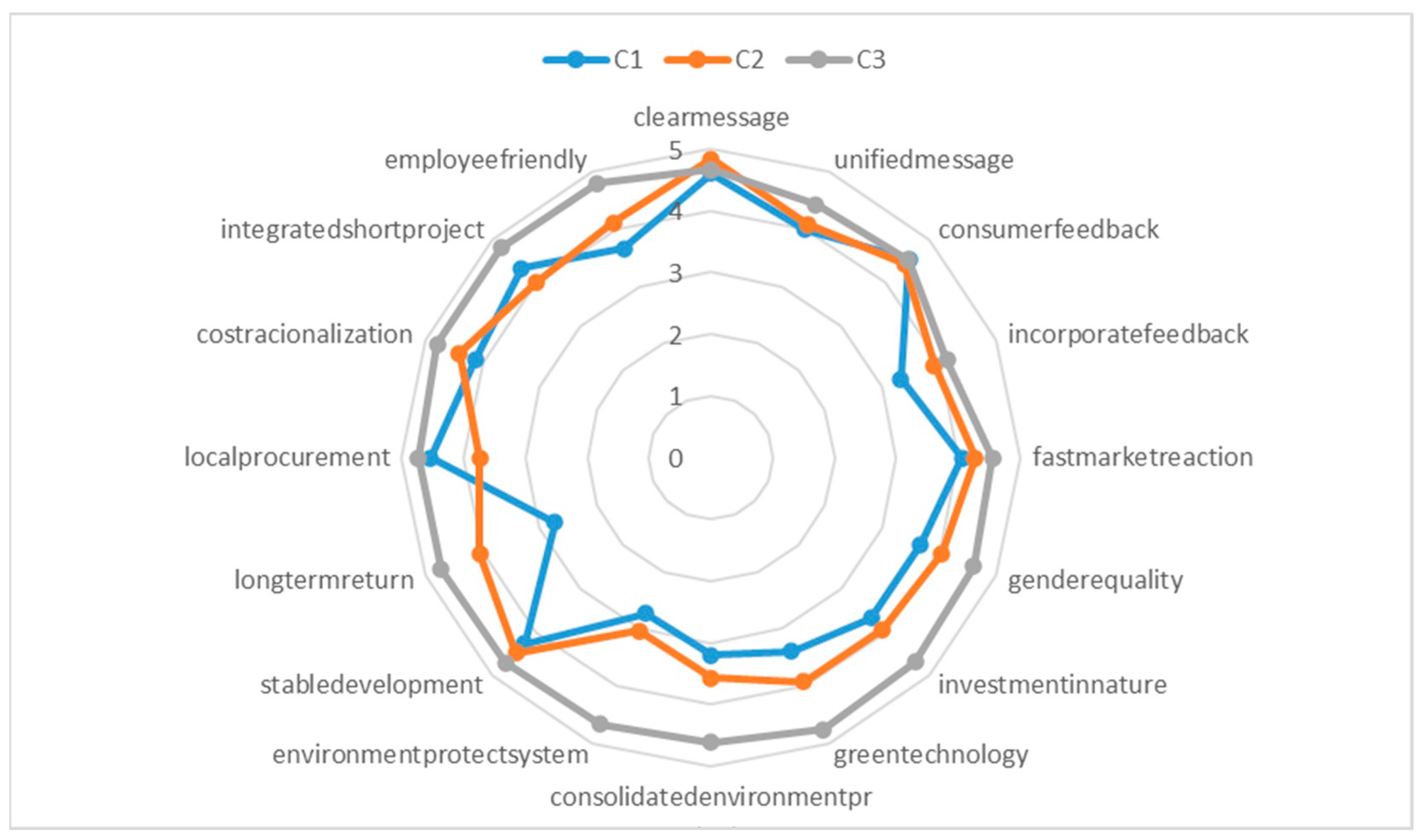

The cluster analysis resulted in three distinct groups, which are presented in Figure 1.

The C1 cluster comprises 15 members, all of which are micro-enterprises without exemption, falling within the category of fewer than 10 employees. Marketing activities are conducted by all members, except for two enterprises. Only two companies operate at the national level. These businesses demonstrate minimal incorporation of consumer feedback into their processes and lag behind the majority in establishing worker-friendly conditions. They show a reluctance toward investments promising long-term returns and do not participate in environmental protection systems. Given these characteristics, this cluster can aptly be labeled “Vegetatives”.

The C2 cluster comprises 58 members, all of which are micro-enterprises. Only eight of them do not engage in separate marketing activities, and another eight operate at the national level. Notably, these entities show a strong inclination toward using clear messages, indicating a robust integrated marketing communication strategy. They also exhibit a high preference for stable, long-term returns over immediate profit, almost reaching the highest level in this regard. Given these characteristics, the members of this cluster can be aptly labeled the “Catcher-ups”.

Cluster C3 encompasses 90 small, 24 medium-sized, and 79 micro-enterprises. While these entities predominantly engage in activities extending beyond local operations, they rely heavily on local procurement sources. Within this cluster, there are 2 international, 19 national, 9 regional, 124 county, and 39 city-level businesses. All members of this cluster are involved in marketing activities, with 134 of them utilizing integrated marketing communication tools. Given these characteristics, this cluster is appropriately named the “Sustainables”.

Analyzing the interplay between the three clusters in the context of the coronavirus pandemic and European Union subsidies reveals the following patterns. Although the clusters did not exhibit distinct differences regarding the coronavirus pandemic, the C3 cluster distinguished itself concerning the receipt of European Union subsidies. Approximately one-third of the cluster had already initiated applications for direct funding, and a quarter of the cluster—equivalent to around 80 percent of the applicants—had successfully secured these subsidies.

Balancing marketing activities that drive customer satisfaction and profit with social and environmental impact is a challenge for contemporary SMEs. Combining these areas requires strategic alignment and thoughtful use of marketing tools [51].

Leveraging digital tools and platforms is essential for businesses to remain relevant in a changing world. Corporate social responsibility (CSR) and promoting sustainability practices are integral parts of effective marketing communication [33].

5. Discussion

Throughout the various analyses, it was explored how the use of integrated marketing communications affects the sample from the Hungarian SME sector; the specifics of the sustainability orientation entrepreneurial behavior applied not to entrepreneurs, but to SMEs; and if categorization is possible and/or significant according to these factors. The main results were that the correct use of integrated marketing communications within the SME sector returned positive answers in regard to the questions of enhancing resilience in times of external hazardous scenarios and showed usability in all roles explored. In terms of the categorization, the resulting categories were distinct and relatively easily identifiable, which shows the cohesion of the cluster analysis results.

It is important to note that after making sure of the sample and the data being applicable to statistical analysis, all the questions of the research were answerable. It is essential to emphasize that these data originated from individuals within the SME sector and are entirely reliant on self-assessment and susceptible to data discrepancies. Equally crucial, however, is that the results remained coherent and consistent, displaying relatively high values during the validation analyses. This means that the SME sector within Hungary, or at least its part adhering to the specific sampling, is relatively consistent. This, on the one hand, suggests that the necessary flexibility in adapting these concepts may be lower than expected due to the high consistency of the SME management practice and philosophy in Hungary, and on the other hand, further validates the consistence of the self-evaluation of the business managers in question. Yet another important factor to note is that throughout the various analyses, theoretic implementation served to strengthen the validity of the results and research fundamentals. As virtually every analysis managed to prove, prove with limitations, or disprove the gaps highlighted earlier, we can say that the starting research fundamentals were, at the very least, reasonable.

In relation to IMC, analysis managed to prove its applicability to increasing resilience and reducing the risks of external hazard scenarios for SMEs in the sample. Also, limited relations between IMC and sustainability orientation were found via the research.

In relation to sustainability, analysis showed that there are certainly advantages for the participants of the research sample; however, there are also disadvantages. Such disadvantages go beyond the initial cost-type redundant deficiencies (redundant, as most innovative enterprises consider expenditures toward sustainability to be simple investments with a calculable return) into other factors like reach, community relations, and corporate image. However, we must take note of the fact that these are also linked to the social and economic peculiarities of the Hungarian SME sector.

Finally, the analyses were successful in validating Hypothesis 1 (According to the sustainability pillar of economic reasonableness, the sustainable part of Hungarian small and medium-sized enterprises carries out a planned marketing process in a larger percentage.); Hypothesis 2 (The use of integrated marketing communication affects the resilience of the SME sector during crises positively.); Hypothesis 3 (The use of sustainability goals affects the resilience of the SME sector during crises positively.); and Hypothesis 4 (The investigated enterprises can be divided into clearly distinguishable groups according to the variables used.). The implications of these results are that the proposed elements of sustainability orientation applied to SMEs as sustainability directives, and the use of IMC as a rationalization and CSR-functioned toolset does increase enterprise resilience and overall enterprise performance.

6. Limitations

There are three distinct limitations that need to be mentioned in regard to the research. The first is that the sample is not representative of the SME sector; thus, any form of far-reaching implications one could derive from the research results is, at the very least, strongly advised to be subject to further analysis. This also means that the research results are not ready-made to be applicable to the SME sectors of any larger units of governance, examples of which are the EU or the global SME sector. This limitation can be overcome by further testing the method of applying the sustainability orientation concept to larger organizations as a management philosophy and even more in-depth analysis of the entry variables for defining the conditions of defining sustainability orientation via input questions. The second limitation is that due to the sustainability orientation concept being fundamentally an entrepreneurial behavior pattern or a set of values/attitudes, it is fundamentally highly subject to the specifics of the entrepreneur’s personal life, nationality, and other determining factors. This limitation can be overcome by analysis into the points of enterprise management where entrepreneurs have ‘neutral’ decision-making criteria, for example, decisions involving business reasoning determined extremely strictly according to mathematical calculations and economic knowledge. After isolating the sub-processes within the organization that are more reliant on ‘the human factor’, it becomes possible to more strictly define research criteria to narrow the focus of the research. The third limitation is that all the conclusions are derived from statistically observing the possibly subjective data input according to the basic situation. This limitation is slightly special, because it is one of the more strictly unavoidable ones, and can be overcome only if a set of practical case studies is conducted (i.e., changing the given management of SMEs into one tailored to their operations based mainly on the usage of IMC, and sustainability orientation as an enterprise management philosophy). At the same time, it would be necessary to conduct measurements of performance. This, however, is very hard to implement, and strongly reliant on future research when the first two limitations are already taken out of the picture.

7. Conclusions

Sustainability is an important part of strategic business management. It can be achieved through effective marketing communications that take into account current trends.

The planned marketing activity has a positive effect on the business’s sustainable operation. The research results show that when facing external hazardous scenarios, integrated marketing communications resulted in better performance; thus, the use of the integrated marketing communication tools is a key factor in the resilience of SMEs. This stands as a significant outcome, because while the integrated marketing communications toolkit aims to enhance consumer perception and bridge the gap between consumers and the enterprise, it was not specifically designed with sustainability in mind. Nonetheless, the research reveals that beyond the anticipated economic sustainability linked to enterprises seeking profit maximization, integrated marketing communications had external effects that bolstered the toolkit’s impact, aligning with the initial assumptions.

Most of the examined companies pay attention to sustainability and declare this to consumers by using appropriate communication tools. These businesses represent sustainability potential for the economy, and economic policy should target this group. It is also interesting that the most sustainable enterprises are almost at the same level of those who neglect sustainability aspects during daily operations for most factors. Only the use and incorporation of the consumers’ feedback stand out. This can be the consequence of the fact that there are limitations in marketing communication activities of SMEs resulting from restricted finances. Furthermore, it may be related to the fact that the employees of SMEs tend to be generalists, so their marketing expertise is often limited. Hence, the research findings continued to demonstrate noteworthy significance in this particular area.

Future research must begin with strengthening the findings through a more in-depth approach and different samples. There is also the necessity of developing the concept of applying sustainability orientation to enterprises better, briefly touched upon in the research limitations. The most important factors to further develop in the research are the input criteria for applying sustainability orientation—this manifests in the questions related to it in the questionnaire and a rational categorization of these questions based on why the SME sector’s actors consider them important. This, along with the further exploration of the entrepreneur’s attitude toward these concepts, can result in the further stabilization of the concept. Matching it in follow-up research conducted on the consumer side can create a toolset specifically designed for SMEs toward empowering the main factors of marketing as a counteroffensive against threats to the enterprise and using sustainability as a pillar for resilience.

Author Contributions

Conceptualization, Z.F. and K.N.P.; methodology, K.N.P.; formal analysis, Z.F.; data curation, Z.F.; writing—original draft preparation, K.N.P.; writing—review and editing, Z.F. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

The data presented in this study are available on request from the corresponding author.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Medne, A.; Lapina, I. Sustainability and Continuous Improvement of Organization: Review of Process-Oriented Performance Indicators. J. Open Innov. Technol. Mark. Complex. 2019, 5, 49. [Google Scholar] [CrossRef]

- White, G.R.T.; James, P. Extension of Process Mapping to Identify “Green Waste”. Benchmarking Int. J. 2014, 21, 835–850. [Google Scholar] [CrossRef]

- Sherif, Z.; Sarfraz, S.; Jolly, M.; Salonitis, K. Identification of the Right Environmental KPIs for Manufacturing Operations: Towards a Continuous Sustainability Framework. Materials 2022, 15, 7690. [Google Scholar] [CrossRef]

- Bonsón, E.; Bednárová, M. CSR Reporting Practices of Eurozone Companies. Rev. Contab. 2015, 18, 182–193. [Google Scholar] [CrossRef]

- Yun, J.J.; Yigitcanlar, T. Open Innovation in Value Chain for Sustainability of Firms. Sustainability 2017, 9, 811. [Google Scholar] [CrossRef]

- Tripopsakul, S.; Puriwat, W. Understanding the Impact of ESG on Brand Trust and Customer Engagement. J. Hum. Earth Future 2022, 3, 430–440. [Google Scholar] [CrossRef]

- Mishra, R.; Singh, R.K.; Govindan, K. Barriers to the Adoption of Circular Economy Practices in Micro, Small and Medium Enterprises: Instrument Development, Measurement and Validation. J. Clean. Prod. 2022, 351, 131389. [Google Scholar] [CrossRef]

- Chowdhury, S.; Dey, P.K.; Rodríguez-Espíndola, O.; Parkes, G.; Tuyet, N.T.A.; Long, D.D.; Ha, T.P. Impact of Organisational Factors on the Circular Economy Practices and Sustainable Performance of Small and Medium-Sized Enterprises in Vietnam. J. Bus. Res. 2022, 147, 362–378. [Google Scholar] [CrossRef]

- Álvarez Jaramillo, J.; Zartha Sossa, J.W.; Orozco Mendoza, G.L. Barriers to Sustainability for Small and Medium Enterprises in the Framework of Sustainable Development—Literature Review. Bus. Strategy Environ. 2019, 28, 512–524. [Google Scholar] [CrossRef]

- Russo, I.; Confente, I.; Scarpi, D.; Hazen, B.T. From Trash to Treasure: The Impact of Consumer Perception of Bio-Waste Products in Closed-Loop Supply Chains. J. Clean. Prod. 2019, 218, 966–974. [Google Scholar] [CrossRef]

- Dumitriu, D.; Militaru, G.; Deselnicu, D.C.; Niculescu, A.; Popescu, M.A.M. Perspective Over Modern SMEs: Managing Brand Equity, Growth and Sustainability Through Digital Marketing Tools and Techniques. Sustainability 2019, 11, 2111. [Google Scholar] [CrossRef]

- Prasanna, R.; Jayasundara, J.; Naradda Gamage, S.K.; Ekanayake, E.; Rajapakshe, P.; Abeyrathne, G. Sustainability of SMEs in the Competition: A Systemic Review on Technological Challenges and SME Performance. J. Open Innov. Technol. Mark. Complex. 2019, 5, 100. [Google Scholar] [CrossRef]

- Silvius, A.J.G.; Schipper, R. Exploring the Relationship between Sustainability and Project Success—Conceptual Model and Expected Relationships. Int. J. Inf. Syst. Proj. Manag. 2022, 4, 5–22. [Google Scholar] [CrossRef]

- Al-Shaikh, M.E.; Hanaysha, J.R. A Conceptual Review on Entrepreneurial Marketing and Business Sustainability in Small and Medium Enterprises. World Dev. Sustain. 2023, 2, 100039. [Google Scholar] [CrossRef]

- Bari, N.; Chimhundu, R.; Chan, K.-C. Dynamic Capabilities to Achieve Corporate Sustainability: A Roadmap to Sustained Competitive Advantage. Sustainability 2022, 14, 1531. [Google Scholar] [CrossRef]

- Fernando, Y.; Chiappetta Jabbour, C.J.; Wah, W.-X. Pursuing Green Growth in Technology Firms through the Connections between Environmental Innovation and Sustainable Business Performance: Does Service Capability Matter? Resour. Conserv. Recycl. 2019, 141, 8–20. [Google Scholar] [CrossRef]

- Schmidt, F.; Zanini, R.; Korzenowski, A.; Schmidt Junior, R.; Xavier Do Nascimento, K. Evaluation of Sustainability Practices in Small and Medium-Sized Manufacturing Enterprises in Southern Brazil. Sustainability 2018, 10, 2460. [Google Scholar] [CrossRef]

- Khan, A.A.; Wang, M.Z.; Ehsan, S.; Nurunnabi, M.; Hashmi, M.H. Linking Sustainability-Oriented Marketing to Social Media and Web Atmospheric Cues. Sustainability 2019, 11, 2663. [Google Scholar] [CrossRef]

- McDonagh, P.; Prothero, A. Sustainability Marketing Research: Past, Present and Future. J. Mark. Manag. 2014, 30, 1186–1219. [Google Scholar] [CrossRef]

- Das, M.; Rangarajan, K.; Dutta, G. Corporate Sustainability in SMEs: An Asian Perspective. J. Asia Bus. Stud. 2020, 14, 109–138. [Google Scholar] [CrossRef]

- Roša (Rosha), A.; Lace, N. The Open Innovation Model of Coaching Interaction in Organisations for Sustainable Performance within the Life Cycle. Sustainability 2018, 10, 3516. [Google Scholar] [CrossRef]

- Danileviciene, I.; Lace, N. The Features of Economic Growth in the Case of Latvia and Lithuania. J. Open Innov. Technol. Mark. Complex. 2017, 3, 1–10. [Google Scholar] [CrossRef]

- Keeble, J.J. Using Indicators to Measure Sustainability Performance at a Corporate and Project Level. J. Bus. Ethics 2003, 44, 149–158. [Google Scholar] [CrossRef]

- Santos, J.B.; Brito, L.A.L. Toward a Subjective Measurement Model for Firm Performance. BAR Braz. Adm. Rev. 2012, 9, 95–117. [Google Scholar] [CrossRef]

- Butkouskaya, V.; Llonch-Andreu, J.; Alarcón-del-Amo, M.-C. Entrepreneurial Orientation (EO), Integrated Marketing Communications (IMC), and Performance in Small and Medium-Sized Enterprises (SMEs): Gender Gap and Inter-Country Context. Sustainability 2020, 12, 7159. [Google Scholar] [CrossRef]

- Darcy, C.; Hill, J.; McCabe, T.; McGovern, P. A Consideration of Organisational Sustainability in the SME Context: A Resource-Based View and Composite Model. Eur. J. Train. Dev. 2014, 38, 398–414. [Google Scholar] [CrossRef]

- Teece, D.J. Explicating Dynamic Capabilities: The Nature and Microfoundations of (Sustainable) Enterprise Performance. Strat. Manag. J. 2007, 28, 1319–1350. [Google Scholar] [CrossRef]

- Einwiller, S.A.; Boenigk, M. Examining the Link between Integrated Communication Management and Communication Effectiveness in Medium-Sized Enterprises. J. Mark. Commun. 2012, 18, 335–361. [Google Scholar] [CrossRef]

- Butkouskaya, V.; Llonch-Andreu, J.; Alarcón-Del-Amo, M.-D.-C. Strategic Antecedents and Organisational Consequences of IMC in Different Economy Types. J. Mark. Commun. 2021, 27, 115–136. [Google Scholar] [CrossRef]

- Butkouskaya, V.; Llonch-Andreu, J.; Alarcón-del-Amo, M.-C. Inter-Country Customer-Perspective Analysis of Strategic Antecedents and Consequences for Post-Purchase Behaviour in Integrated Marketing Communications (IMC). J. Int. Consum. Mark. 2021, 33, 68–83. [Google Scholar] [CrossRef]

- Civelek, M.; Červinka, M.; Gajdka, K.; Nétek, V. Marketing Communication Tools and Their Influence on Marketing Innovation: Evidence from Slovakian SMEs. Manag. Marketing. Chall. Knowl. Soc. 2021, 16, 210–227. [Google Scholar] [CrossRef]

- Šķiltere, D.; Bormane, S. Integrated Marketing Communication as a Business Management Tool in the Context of Sustainable Development. Open Econ. 2018, 1, 115–123. [Google Scholar] [CrossRef]

- Adeola, O.; Olaniyi, E. Marketing Communications: Embedding Sustainability Practices in a Changing World. In Marketing Communications and Brand Development in Emerging Markets Volume II; Adeola, O., Hinson, R.E., Sakkthivel, A.M., Eds.; Palgrave Studies of Marketing in Emerging Economies; Springer International Publishing: Cham, Switzerland, 2022; pp. 287–307. ISBN 978-3-030-95580-9. [Google Scholar]

- Aragón-Sánchez, A.; Sánchez-Marín, G. Strategic Orientation, Management Characteristics, and Performance: A Study of Spanish SMEs: JOURNAL OF SMALL BUSINESS MANAGEMENT. J. Small Bus. Manag. 2005, 43, 287–308. [Google Scholar] [CrossRef]

- Burlea-Schiopoiu, A.; Mihai, L.S. An Integrated Framework on the Sustainability of SMEs. Sustainability 2019, 11, 6026. [Google Scholar] [CrossRef]

- Hitchens, D.; Thankappan, S.; Trainor, M.; Clausen, J.; De Marchi, B. Environmental Performance, Competitiveness and Management of Small Businesses in Europe. Tijd. Econ. Soc. Geogr. 2005, 96, 541–557. [Google Scholar] [CrossRef]

- Mihai, L.; Burlea Schiopoiu, A.; Mihai, M. Comparison of the Leadership Styles Practiced by Romanian and Dutch SME Owners. Int. J. Organ. Leadersh. 2017, 6, 4–16. [Google Scholar] [CrossRef]

- Spence, L.J. Does Size Matter? The State of the Art in Small Business Ethics. Bus. Ethics A Eur. Rev. 1999, 8, 163–174. [Google Scholar] [CrossRef]

- Arvidsson, S. Communication of Corporate Social Responsibility: A Study of the Views of Management Teams in Large Companies. J. Bus. Ethics 2010, 96, 339–354. [Google Scholar] [CrossRef]

- Akben-Selcuk, E. Corporate Social Responsibility and Financial Performance: The Moderating Role of Ownership Concentration in Turkey. Sustainability 2019, 11, 3643. [Google Scholar] [CrossRef]

- Lee, K.; Herold, D.M.; Yu, A. Small and Medium Enterprises and Corporate Social Responsibility Practice: A Swedish Perspective. Corp. Soc. Responsib. Environ. 2016, 23, 88–99. [Google Scholar] [CrossRef]

- Sharma, S. Managerial Interpretations and Organizational Context as Predictors of Corporate Choice of Environmental Strategy. Acad. Manag. J. 2000, 43, 681–697. [Google Scholar] [CrossRef]

- Aragón-Correa, J.A.; Hurtado-Torres, N.; Sharma, S.; García-Morales, V.J. Environmental Strategy and Performance in Small Firms: A Resource-Based Perspective. J. Environ. Manag. 2008, 86, 88–103. [Google Scholar] [CrossRef] [PubMed]

- Hambrick, D.C. Speed, Stealth, and Selective Attack: How Small Firms Differ from Large Firms in Competitive Behavior. Acad. Manag. J. 1995, 38, 453–482. [Google Scholar] [CrossRef]

- Lepoutre, J.; Heene, A. Investigating the Impact of Firm Size on Small Business Social Responsibility: A Critical Review. J. Bus. Ethics 2006, 67, 257–273. [Google Scholar] [CrossRef]

- Studer, S.; Welford, R.; Hills, P. Engaging Hong Kong Businesses in Environmental Change: Drivers and Barriers. Bus. Strategy Environ. 2006, 15, 416–431. [Google Scholar] [CrossRef]

- Noguera, M.; Alvarez, C.; Urbano, D. Socio-Cultural Factors and Female Entrepreneurship. Int. Entrep. Manag. J. 2013, 9, 183–197. [Google Scholar] [CrossRef]

- Lim, S.; Envick, B.R. Gender and Entrepreneurial Orientation: A Multi-Country Study. Int. Entrep. Manag. J. 2013, 9, 465–482. [Google Scholar] [CrossRef]

- Neumayer, E.; Plümper, T. The Gendered Nature of Natural Disasters: The Impact of Catastrophic Events on the Gender Gap in Life Expectancy, 1981–2002. Ann. Assoc. Am. Geogr. 2007, 97, 551–566. [Google Scholar] [CrossRef]

- Cela, B.; Dankelman, I.; Stern, J. Bookshelf: Powerful Synergies: Gender Equality, Economic Development and Environmental Sustainability. Reprod. Health Matters 2014, 22, 197–199. [Google Scholar] [CrossRef]

- Wiścicka-Fernando, M. Sustainability Marketing Tools in Small and Medium Enterprises. In The Sustainable Marketing Concept in European SMEs; Rudawska, E., Ed.; Emerald Publishing Ltd.: Bingley, UK, 2018; pp. 81–117. ISBN 978-1-78754-039-2. [Google Scholar]

Figure 1.

Results of cluster analysis (cluster C1, C2, and C3). Source: Self-made.

{kind=link}

Table 1.

Reliability statistics for logistic regression.

| Cronbach’s Alpha | Cronbach’s Alpha Based on Standardized Items | No. of Items |

|---|---|---|

| 0.732 | 0.707 | 6 |

Source: self-made based on SPSS output.

Table 2.

Item total statistics for logistic regression.

| Scale Mean if Item Deleted | Scale Variance if Item Deleted | Corrected Item Total Correlation | Squared Multiple Correlation | Cronbach’s Alpha if Item Deleted | |

|---|---|---|---|---|---|

| Q9 | 2.98 | 1.911 | 0.591 | 0.456 | 0.660 |

| Q14 | 3.21 | 1.759 | 0.543 | 0.320 | 0.671 |

| Q25 | 3.10 | 1.898 | 0.469 | 0.352 | 0.695 |

| Q10 | 3.14 | 1.615 | 0.719 | 0.596 | 0.607 |

| Q8 | 3.63 | 2.178 | 0.373 | 0.152 | 0.719 |

| Q45 | 2.87 | 2.569 | 0.083 | 0.091 | 0.771 |

Source: self-made based on SPSS output.

Table 3.

Collinearity statistics for the first logistic regression model (dependent variable: Q25).

| Tolerance | VIF | |

|---|---|---|

| Q10 | 0.467 | 2.143 |

| Q14 | 0.700 | 1.428 |

| Q9 | 0.549 | 1.821 |

| Q8 | 0.869 | 1.151 |

Source: self-made based on SPSS output.

Table 4.

Collinearity statistics for the second logistic regression model (dependent variable: Q45).

Table 4.

Collinearity statistics for the second logistic regression model (dependent variable: Q45).

| Tolerance | VIF | |

|---|---|---|

| Q10 | 0.556 | 1.799 |

| Q14 | 0.729 | 1.372 |

| Q25 | 0.689 | 1.452 |

Source: self-made based on SPSS output.

Table 5.

Classification table of the first logistic regression.

| Observed | Predicted | ||||

| Q25 | Percentage Correct | ||||

| 0 | 1 | ||||

| Step 0 | Q25 | 0 | 0 | 101 | 0 |

| 1 | 0 | 217 | 100.0 | ||

| Overall Percentage | 68.2 | ||||

| Constant is included in the model. The cut value is 0.500. | |||||

Source: self-made based on SPSS output.

Table 6.

The separate significance of the independent variables.

| Variables Not in the Equation | |||||

|---|---|---|---|---|---|

| Score | df | Sig. | |||

| Step 0 | Variables | Q10(1) | 98.859 | 1 | <0.001 |

| Q8(1) | 21.721 | 1 | <0.001 | ||

| Q14(1) | 30.828 | 1 | <0.001 | ||

| Q9(1) | 54.623 | 1 | <0.001 | ||

| Overall Statistics | 102.260 | 4 | <0.001 | ||

Source: self-made based on SPSS output.

Table 7.

Variance explained by the independent variables.

| Step | −2 Log Likelihood | Cox and Snell R Square | Nagelkerke R Square |

|---|---|---|---|

| 1 | 291.589 a | 0.283 | 0.397 |

a Estimation terminated at iteration number 6 because parameter estimates changed by less than 0.001. Source: self-made based on SPSS output.

Table 8.

The contribution of the independent variables to the categorization of the dependent one.

| Observed | Predicted | ||||

| Q25 | Percentage Correct | ||||

| 0 | 1 | ||||

| Step 1 | Q25 | 0 | 75 | 26 | 74.3 |

| 1 | 37 | 180 | 82.9 | ||

| Overall Percentage | 80.2 | ||||

| The cut value is 0.500 | |||||

Source: self-made based on SPSS output.

Table 9.

The significance of the independent variables and their contribution to the model.

| Variables in the Equation | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| B | S.E. | Wald | df | Sig. | Exp(B) | 95% C.I. for EXP(B) | |||

| Lower | Upper | ||||||||

| Step 1 | Q10(1) | 2.174 | 0.391 | 30.850 | 1 | <0.001 | 8.791 | 4.082 | 18.931 |

| Q8(1) | 1.495 | 0.758 | 3.885 | 1 | 0.049 | 4.458 | 1.008 | 19.708 | |

| Q14(1) | 0.032 | 0.341 | 0.009 | 1 | 0.926 | 1.032 | 0.529 | 2.015 | |

| Q9(1) | 0.400 | 0.407 | 0.967 | 1 | 0.326 | 1.492 | 0.672 | 3.310 | |

| Constant | −0.899 | 0.285 | 9.930 | 1 | 0.002 | 0.407 | |||

| Variable(s) entered on step 1: Q10, Q8, Q14, Q9. | |||||||||

Source: self-made based on SPSS output.

Table 10.

Classification table of the second logistic regression.

| Observed | Predicted | ||||

| Q45 | Percentage Correct | ||||

| 0 | 1 | ||||

| Step 0 | Q45 | 0 | 0 | 26 | 0 |

| 1 | 0 | 292 | 100.0 | ||

| Overall Percentage | 91.8 | ||||

| Constant is included in the model. | |||||

| The cut value is 0.500 | |||||

Source: self-made based on SPSS output.

Table 11.

The separate significances of the independent variables.

| Variables Not in the Equation | |||||

|---|---|---|---|---|---|

| Score | df | Sig. | |||

| Step 0 | Variables | Q10(1) | 0.623 | 1 | 0.430 |

| Q14(1) | 10.627 | 1 | 0.001 | ||

| Q25(1) | 5.343 | 1 | 0.021 | ||

| Overall Statistics | 23.425 | 3 | <0.001 | ||

Source: self-made based on SPSS output.

Table 12.

Variance explained by the independent variables.

| Step | −2 Log Likelihood | Cox and Snell R Square | Nagelkerke R Square |

|---|---|---|---|

| 1 | 156.463 a | 0.071 | 0.165 |

a Estimation terminated at iteration number 6 because parameter estimates changed by less than 0.001. Source: self-made based on SPSS output.

Table 13.

The contribution of the independent variables to the categorization of the dependent one.

| Observed | Predicted | ||||

| Q45 | Percentage Correct | ||||

| 0 | 1 | ||||

| Step 1 | Q45 | 0 | 0 | 26 | 0 |

| 1 | 0 | 292 | 100.0 | ||

| Overall Percentage | 91.8 | ||||

| The cut value is 0.500 | |||||

Source: self-made based on SPSS output.

Table 14.

The significance of the independent variables and their contribution to the model.

| Variables in the Equation | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| B | S.E. | Wald | df | Sig. | Exp(B) | 95% C.I. for EXP(B) | |||

| Lower | Upper | ||||||||

| Step 1 | Q10(1) | 0.041 | 0.521 | 0.006 | 1 | 0.937 | 1.042 | 0.375 | 2.896 |

| Q14(1) | 1.815 | 0.542 | 11.196 | 1 | <0.001 | 6.139 | 2.121 | 17.772 | |

| Q25(1) | −1.947 | 0.660 | 8.707 | 1 | 0.003 | 0.143 | 0.039 | 0.520 | |

| Constant | 3.124 | 0.599 | 27.198 | 1 | <0.001 | 22.739 | |||

| Variable(s) entered on step 1: Q10, Q14, Q25. | |||||||||

Source: self-made based on SPSS output.

Table 15.

Total variance of factor analysis explained.

| Component | Total | Variance % | Cumulative % | Total | Variance % | Cumulative% |

|---|---|---|---|---|---|---|

| 1 | 4.851 | 30.319 | 30.319 | 4.851 | 30.319 | 30.319 |

| 2 | 1.641 | 10.256 | 40.575 | 1.641 | 10.256 | 40.575 |

| 3 | 1.112 | 6.950 | 47.525 | 1.112 | 6.950 | 47.525 |

| 4 | 1.070 | 6.689 | 54.215 | 1.070 | 6.689 | 54.215 |

| 5 | 1.034 | 6.464 | 60.678 | 1.034 | 6.464 | 60.678 |

| 6 | 0.810 | 5.059 | 65.738 | |||

| 7 | 0.764 | 4.777 | 70.515 | |||

| 8 | 0.749 | 4.684 | 75.199 | |||

| 9 | 0.652 | 4.075 | 79.273 | |||

| 10 | 0.599 | 3.742 | 83.016 | |||

| 11 | 0.565 | 3.531 | 86.547 | |||

| 12 | 0.501 | 3.129 | 89.675 | |||

| 13 | 0.489 | 3.056 | 92.732 | |||

| 14 | 0.421 | 2.630 | 95.362 | |||

| 15 | 0.406 | 2.538 | 97.900 | |||

| 16 | 0.336 | 2.100 | 100.000 |

Source: self-made based on SPSS output.

Table 16.

Rotated component matrix of the factor analysis.

| Variables | Component | ||||

|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | |

| Clear messages | −0.111 | 0.122 | 0.681 | −0.317 | −0.093 |

| Unified messages | 0.192 | 0.107 | 0.709 | 0.170 | 0.259 |

| Monitoring feedback | 0.121 | 0.274 | 0.275 | −0.705 | 0.142 |

| Incorporating feedback | 0.152 | −0.085 | 0.134 | 0.046 | 0.826 |

| Rapid-response marketing | 0.071 | 0.700 | 0.235 | −0.050 | −0.024 |

| Gender equality | 0.507 | 0.300 | −0.355 | −0.022 | 0.191 |

| Natural environment investment | 0.596 | 0.299 | −0.061 | −0.089 | 0.203 |

| Environmentally friendly technology | 0.739 | 0.090 | −0.043 | −0.021 | 0.113 |

| Support for comprehensive environmental protection | 0.772 | 0.157 | −0.034 | 0.120 | 0.096 |

| Large environmental protection systems | 0.776 | 0.207 | 0.057 | 0.115 | 0.073 |

| Stable development preferred | 0.016 | 0.550 | −0.122 | −0.107 | 0.523 |

| Longer return preferred | 0.489 | 0.598 | 0.010 | 0.154 | −0.082 |

| Local procurement | 0.636 | −0.029 | 0.118 | 0.017 | 0.146 |

| Cost rationalization | 0.263 | 0.280 | 0.132 | 0.701 | 0.157 |

| Integration of short projects | 0.755 | −0.088 | 0.077 | 0.053 | −0.196 |

| Employee friendliness | 0.565 | 0.443 | 0.066 | 0.302 | -0.127 |

Source: self-made based on SPSS output.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Pércsi, K.N.; Fülöp, Z. Relationships between Sustainable Operations and the Resilience of SMEs. Sustainability 2024, 16, 741. https://doi.org/10.3390/su16020741

AMA Style

Pércsi KN, Fülöp Z. Relationships between Sustainable Operations and the Resilience of SMEs. Sustainability. 2024; 16(2):741. https://doi.org/10.3390/su16020741

Chicago/Turabian StylePércsi, Kinga Nagyné, and Zsolt Fülöp. 2024. "Relationships between Sustainable Operations and the Resilience of SMEs" Sustainability 16, no. 2: 741. https://doi.org/10.3390/su16020741

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.