The Bidirectional Relationship between Digital Transformation and Corporate Social Responsibility: A Legitimacy Perspective

Abstract

1. Introduction

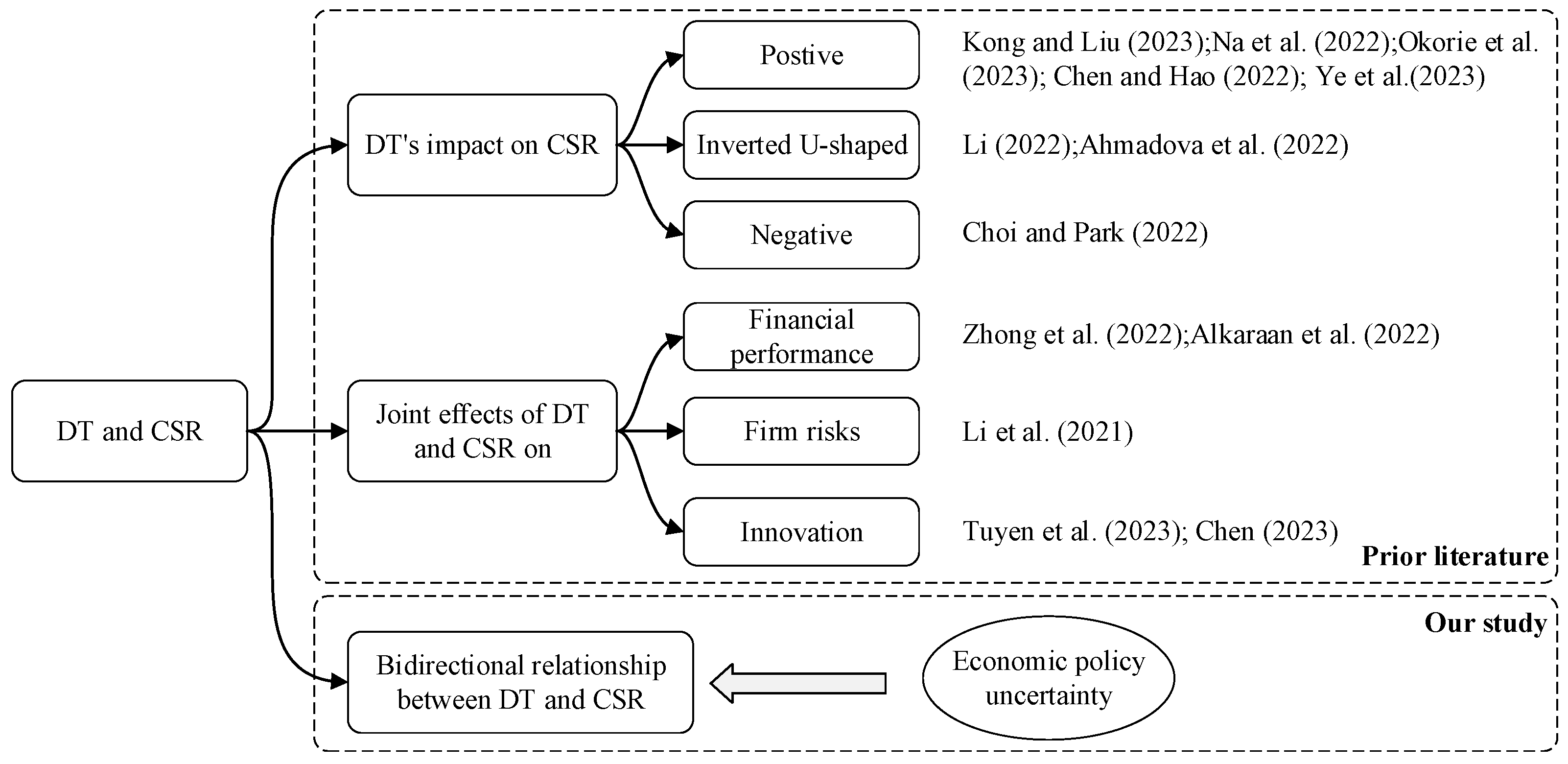

2. Related Literature and Hypothesis Development

2.1. Related Literature

2.2. Hypothesis Development

2.2.1. Legitimacy Theory

2.2.2. The Bidirectional Relationship between Digital Transformation and CSR

2.2.3. The Moderating Role of EPU

3. Empirical Design

3.1. Sample and Data

3.2. Measurements

3.2.1. Dependent and Explanatory Variables

3.2.2. Moderating Variable

3.2.3. Control Variables

3.3. Modeling and Estimation Approach

3.3.1. Modeling

3.3.2. Estimation Method

4. Results

4.1. Descriptive and Correlation Analysis

4.2. Regression Results

4.3. Robustness Checks

4.4. Addition Analysis

5. Conclusions and Discussions

5.1. Theoretical Contributions

5.2. Practical Implications

5.3. Limitations and Future Prospects

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

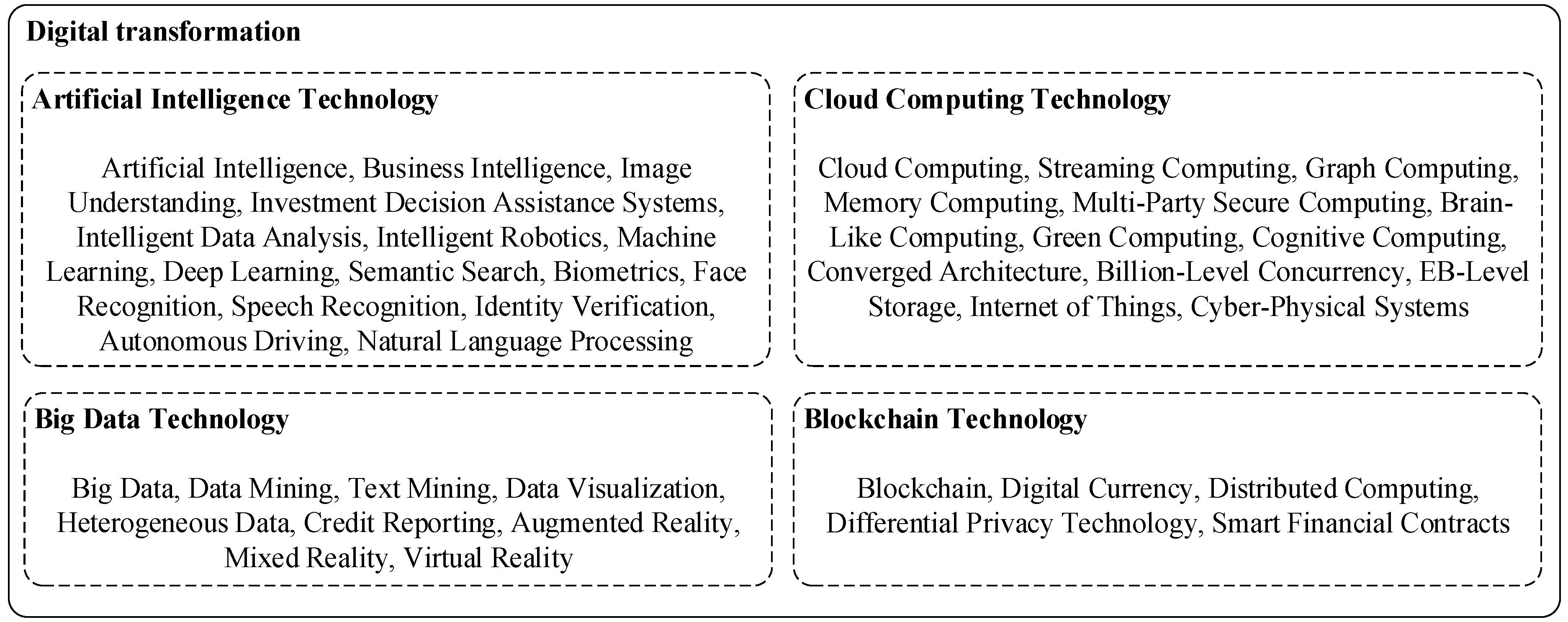

Appendix A. Feature Words for Companies’ Digital Transformation

References

- Schaltegger, S.; Hörisch, J. In Search of the Dominant Rationale in Sustainability Management: Legitimacy- or Profit-Seeking? J. Bus. Ethics 2017, 145, 259–276. [Google Scholar] [CrossRef]

- Hinings, B.; Gegenhuber, T.; Greenwood, R. Digital innovation and transformation: An institutional perspective. Inf. Organ. 2018, 28, 52–61. [Google Scholar] [CrossRef]

- Singh, S.; Sharma, M.; Dhir, S. Modeling the effects of digital transformation in Indian manufacturing industry. Technol. Soc. 2021, 67, 101763. [Google Scholar] [CrossRef]

- Manesh, M.F.; Pellegrini, M.M.; Marzi, G.; Dabic, M. Knowledge Management in the Fourth Industrial Revolution: Mapping the Literature and Scoping Future Avenues. IEEE Trans. Eng. Manag. 2021, 68, 289–300. [Google Scholar] [CrossRef]

- Sousa-Zomer, T.T.; Neely, A.; Martinez, V. Digital transforming capability and performance: A microfoundational perspective. Int. J. Oper. Prod. Man. 2020, 40, 1095–1128. [Google Scholar] [CrossRef]

- van den Broek, T.; van Veenstra, A.F. Governance of big data collaborations: How to balance regulatory compliance and disruptive innovation. Technol. Forecast. Soc. 2018, 129, 330–338. [Google Scholar] [CrossRef]

- Mittal, S.; Khan, M.A.; Purohit, J.K.; Menon, K.; Romero, D.; Wuest, T. A smart manufacturing adoption framework for SMEs. Int. J. Prod. Res. 2020, 58, 1555–1573. [Google Scholar] [CrossRef]

- Deephouse, D.L.; Suchman, M. Legitimacy in Organizational Institutionalism. Soc. Sci. Electron. Publ. 2016, 49, 77. [Google Scholar]

- Suddaby, R.; Greenwood, R. Rhetorical strategies of legitimacy. Adm. Sci. Quart. 2005, 50, 35–67. [Google Scholar] [CrossRef]

- Wang, H.; Jia, M.; Zhang, Z. Good Deeds Done in Silence: Stakeholder Management and Quiet Giving by Chinese Firms. Organ. Sci. 2021, 32, 527–908. [Google Scholar] [CrossRef]

- Xiang, Y.; Jia, M.; Zhang, Z. Hiding in the Crowd: Government Dependence on Firms, Management Costs of Political Legitimacy, and Modest Imitation. J. Bus. Ethics 2022, 176, 629–646. [Google Scholar] [CrossRef]

- Huang, G.; Ye, F.; Li, Y.; Chen, L.; Zhang, M. Corporate social responsibility and bank credit loans: Exploring the moderating effect of the institutional environment in China. Asia Pac. J. Manag. 2023, 40, 707–742. [Google Scholar] [CrossRef]

- Wang, H.; Qian, C. Corporate Philanthropy and Financial Performance: The Roles of Social Expectations and Political Access. Acad. Manag. J. 2011, 54, 1159–1181. [Google Scholar] [CrossRef]

- Liu, Z.J.; Li, W.; Hao, C.; Liu, H. Corporate environmental performance and financing constraints: An empirical study in the Chinese context. Corp. Soc. Resp. Environ. Manag. 2021, 28, 616–629. [Google Scholar] [CrossRef]

- Xu, Q.; Li, X.; Guo, F. Digital transformation and environmental performance: Evidence from Chinese resource-based enterprises. Corp. Soc. Resp. Environ. Manag. 2023, 30, 1816–1840. [Google Scholar] [CrossRef]

- Zhao, X.; Zhao, L.; Sun, X.; Xing, Y. The incentive effect of government subsidies on the digital transformation of manufacturing enterprises. Int. J. Emerg. Mark. 2023; ahead-of-print. [Google Scholar]

- Choi, H.; Park, J. Do data-driven CSR initiatives improve CSR performance? The importance of big data analytics capability. Technol. Forecast. Soc. 2022, 182, 121802. [Google Scholar] [CrossRef]

- Kong, D.; Liu, B. Digital Technology and Corporate Social Responsibility: Evidence from China. Emerg. Mark. Financ. Trade 2023, 59, 2967–2993. [Google Scholar] [CrossRef]

- Li, L. Digital transformation and sustainable performance: The moderating role of market turbulence. Ind. Market Manag. 2022, 104, 28–37. [Google Scholar] [CrossRef]

- Li, G.; Li, N.; Sethi, S.P. Does CSR Reduce Idiosyncratic Risk? Roles of Operational Efficiency and AI Innovation. Prod. Oper. Manag. 2021, 30, 2027–2045. [Google Scholar] [CrossRef]

- Tuyen, B.Q.; Phuong Anh, D.V.; Mai, N.P.; Long, T.Q. Does corporate engagement in social responsibility affect firm innovation? The mediating role of digital transformation. Int. Rev. Econ. Financ. 2023, 84, 292–303. [Google Scholar] [CrossRef]

- Zhong, X.; Chen, W.; Ren, G. The impact of corporate social irresponsibility on emerging-economy firms’ long-term performance: An explanation based on signal theory. J. Bus. Res. 2022, 144, 345–357. [Google Scholar] [CrossRef]

- Jang, S.; Kim, B.; Lee, S. Impact of corporate social (ir)responsibility on volume and valence of online employee reviews: Evidence from the tourism and hospitality industry. Tour. Manag. 2022, 91, 104501. [Google Scholar] [CrossRef]

- Akron, S.; Demir, E.; Esteban, J.M.D.; García-Gómez, C. Economic policy uncertainty and corporate investment: Evidence from the U.S. hospitality industry. Tour. Manag. 2020, 77, 104019. [Google Scholar] [CrossRef]

- Gulen, H.; Ion, M. Policy Uncertainty and Corporate Investment. Rev. Financ. Stud. 2016, 29, 523–564. [Google Scholar] [CrossRef]

- Fedorova, E.; Ledyaeva, S.; Drogovoz, P.; Nevredinov, A. Economic policy uncertainty and bankruptcy filings. Int. Rev. Financ. Anal. 2022, 82, 102174. [Google Scholar] [CrossRef]

- Suchman, M.C. Managing Legitimacy: Strategic and Institutional Approaches. Acad. Manag. Rev. 1995, 20, 571–610. [Google Scholar] [CrossRef]

- Lin, W.L.; Law, S.H.; Ho, J.A.; Sambasivan, M. The causality direction of the corporate social responsibility—Corporate financial performance Nexus: Application of Panel Vector Autoregression approach. N. Am. J. Econ. Financ. 2019, 48, 401–418. [Google Scholar] [CrossRef]

- Cheng, Z.; Masron, T.A. Economic policy uncertainty and corporate digital transformation: Evidence from China. Appl. Econ. 2023, 55, 4625–4641. [Google Scholar] [CrossRef]

- Peng, D.; Colak, G.; Shen, J. Lean against the wind: The effect of policy uncertainty on a firm’s corporate social responsibility strategy. J. Corp. Financ. 2023, 79, 102376. [Google Scholar] [CrossRef]

- Zhu, Z.; Song, T.; Huang, J.; Zhong, X. Executive Cognitive Structure, Digital Policy, and Firms’ Digital Transformation. IEEE T Eng. Manag. 2022, 71, 2579–2592. [Google Scholar] [CrossRef]

- Na, C.H.; Chen, X.; Li, X.J.; Li, Y.T.; Wang, X.L. Digital Transformation of Value Chains and CSR Performance. Sustainability 2022, 14, 10245. [Google Scholar] [CrossRef]

- Okorie, O.; Russell, J.; Cherrington, R.; Fisher, O.; Charnley, F. Digital transformation and the circular economy: Creating a competitive advantage from the transition towards Net Zero Manufacturing. Resour. Conserv. Recycl. 2023, 189, 106756. [Google Scholar] [CrossRef]

- Chen, P.; Hao, Y. Digital transformation and corporate environmental performance: The moderating role of board characteristics. Corp. Soc. Resp. Environ. Manag. 2022, 29, 1757–1767. [Google Scholar] [CrossRef]

- Ye, F.; Ouyang, Y.; Li, Y. Digital investment and environmental performance: The mediating roles of production efficiency and green innovation. Int. J. Prod. Econ. 2023, 259, 108822. [Google Scholar] [CrossRef]

- Ahmadova, G.; Delgado-Márquez, B.L.; Pedauga, L.E.; Leyva-de La Hiz, D.I. Too good to be true: The inverted U-shaped relationship between home-country digitalization and environmental performance. Ecol. Econ. 2022, 196, 107393. [Google Scholar] [CrossRef]

- Alkaraan, F.; Albitar, K.; Hussainey, K.; Venkatesh, V.G. Corporate transformation toward Industry 4.0 and financial performance: The influence of environmental, social, and governance (ESG). Technol. Forecast. Soc. 2022, 175, 121423. [Google Scholar] [CrossRef]

- Chen, W. Digital economy development, corporate social responsibility and low-carbon innovation. Corp. Soc. Resp. Environ. Manag. 2023, 30, 1664–1679. [Google Scholar] [CrossRef]

- Ilyas, M.; Mian, R.U.; Suleman, M.T. Economic policy uncertainty and firm propensity to invest in corporate social responsibility. Manag. Decis. 2022, 60, 3232–3254. [Google Scholar] [CrossRef]

- Vural-Yava, I.D. Economic policy uncertainty, stakeholder engagement, and environmental, social, and governance practices: The moderating effect of competition. Corp. Soc. Resp. Environ. Manag. 2021, 28, 82–102. [Google Scholar] [CrossRef]

- Yuan, T.; Wu, J.G.; Qin, N.; Xu, J. Being nice to stakeholders: The effect of economic policy uncertainty on corporate social responsibility. Econ. Model. 2022, 108, 105737. [Google Scholar] [CrossRef]

- Zhao, T.; Xiao, X.; Zhang, B. Economic policy uncertainty and corporate social responsibility performance: Evidence from China. Sustain. Account. Manag. Policy J. 2021, 12, 1003–1026. [Google Scholar] [CrossRef]

- Zou, H.L.; Wang, R.J.; Qi, G.Y. The Response of CSR to Economic Policy Uncertainty: Evidence from China. Sustainability 2023, 15, 12978. [Google Scholar] [CrossRef]

- Chahine, S.; Daher, M.; Saade, S. Doing good in periods of high uncertainty: Economic policy uncertainty, corporate social responsibility, and analyst forecast error. J. Financ. Stabil. 2021, 56, 100919. [Google Scholar] [CrossRef]

- Ozdemir, O.; Erkmen, E.; Han, W. EPU and financial performance in the hospitality and tourism industry: Moderating effect of CSR, institutional ownership and cash holding. Tour. Manag. 2023, 98, 104769. [Google Scholar] [CrossRef]

- Zhu, H.; Hui, K.N.; Gong, Y. Uncovering the nonmarket side of internationalization: The Belt and Road Initiative and Chinese firms’ CSR reporting quality. Asia Pac. J. Manag. 2022, 40, 1703–1731. [Google Scholar] [CrossRef]

- Saeed, A.; Baloch, M.S.; Riaz, H. Global Insights on TMT Gender Diversity in Controversial Industries: A Legitimacy Perspective. J. Bus. Ethics 2022, 179, 711–731. [Google Scholar] [CrossRef]

- Darendeli, I.S.; Hill, T.L. Uncovering the complex relationships between political risk and MNE firm legitimacy: Insights from Libya. J. Int. Bus. Stud. 2016, 47, 68–92. [Google Scholar] [CrossRef]

- Huang, H.; Shang, R.; Wang, L.; Gong, Y. Corporate social responsibility and firm value: Evidence from Chinese targeted poverty alleviation. Manag. Decis. 2022, 60, 3255–3274. [Google Scholar] [CrossRef]

- Reihlen, M.; Schlapfner, J.F.; Seeger, M.; Trittin-Ulbrich, H. Strategic Venturing as Legitimacy Creation: The Case of Sustainability. J. Manag. Stud. 2022, 59, 417–459. [Google Scholar] [CrossRef]

- Feng, Y.T.; Lai, K.H.; Zhu, Q.H. Legitimacy in operations: How sustainability certification announcements by Chinese listed enterprises influence their market value? Int. J. Prod. Econ. 2020, 224, 107563. [Google Scholar] [CrossRef]

- Meqbel, R.; Altaany, M.; Kayed, S.; Al-Omush, A. Earnings management and sustainability assurance: The moderating role of CSR committee. Corp. Soc. Resp. Environ. Manag. 2023; early view. [Google Scholar] [CrossRef]

- Marano, V.; Tashman, P.; Kostova, T. Escaping the iron cage: Liabilities of origin and CSR reporting of emerging market multinational enterprises. J. Int. Bus. Stud. 2017, 48, 386–408. [Google Scholar] [CrossRef]

- Du, S.; Vieira, E.T. Striving for Legitimacy Through Corporate Social Responsibility: Insights from Oil Companies. J. Bus. Ethics 2012, 110, 413–427. [Google Scholar] [CrossRef]

- Mangematin, V.; Sapsed, J.; Schüßler, E. Disassembly and reassembly: An introduction to the Special Issue on digital technology and creative industries. Technol. Forecast. Soc. Chang. 2014, 83, 1–9. [Google Scholar] [CrossRef]

- Xu, G.; Li, G.; Sun, P.; Peng, D. Inefficient investment and digital transformation: What is the role of financing constraints? Financ. Res. Lett. 2023, 51, 103429. [Google Scholar] [CrossRef]

- Cheng, B.; Ioannou, I.; Serafeim, G. Corporate Social Responsibility and Access to Finance. Strateg. Manag. J. 2014, 35, 1–23. [Google Scholar] [CrossRef]

- Li, S.; Lu, J.W. A Dual-Agency Model of Firm CSR in Response to Institutional Pressure: Evidence from Chinese Publicly Listed Firms. Acad. Manag. J. 2020, 63, 2004–2032. [Google Scholar] [CrossRef]

- Wang, H.L.; Jia, M.; Xiang, Y.; Lan, Y. Social Performance Feedback and Firm Communication Strategy. J. Manag. 2022, 48, 2382–2420. [Google Scholar] [CrossRef]

- Wu, K.; Fu, Y.; Kong, D. Does the digital transformation of enterprises affect stock price crash risk? Financ. Res. Lett. 2022, 48, 102888. [Google Scholar] [CrossRef]

- Davis, S.J.; Liu, D.; Sheng, X.S. Economic policy uncertainty in china since 1946: The view from mainland newspapers. Work. Paper 2019. [Google Scholar]

- Zhou, K.Z.; Gao, G.Y.; Zhao, H. State Ownership and Firm Innovation in China: An Integrated View of Institutional and Efficiency Logics. Adm. Sci. Quart. 2016, 62, 375–404. [Google Scholar] [CrossRef]

- Tian, G.; Li, B.; Cheng, Y. Does digital transformation matter for corporate risk-taking? Financ. Res. Lett. 2022, 49, 103107. [Google Scholar] [CrossRef]

- Ghose, A.; Ipeirotis, P.; Li, B. Examining the Impact of Ranking on Consumer Behavior and Search Engine Revenue. Manag. Sci. Forthcom. 2014, 60, 1632–1654. [Google Scholar] [CrossRef]

- Zhang, Y.; Chen, K. Network growth dynamics: The simultaneous interaction between network positions and research performance of collaborative organisations. Technovation 2022, 115, 102538. [Google Scholar] [CrossRef]

- Rosiello, A.; Maleki, A. A dynamic multi-sector analysis of technological catch-up: The impact of technology cycle times, knowledge base complexity and variety. Res. Policy 2021, 50, 104194. [Google Scholar] [CrossRef]

- Honjo, Y. The impact of founders’ human capital on initial capital structure: Evidence from Japan. Technovation 2021, 100, 102191. [Google Scholar] [CrossRef]

- Wooltridge, J.M. Econometrics Analysis of Cross-Section and Panel Data; The MIT Press: Cambridge, MA, USA; London, UK, 2001; Volume 1, pp. 206–209. [Google Scholar]

- Heshmati, A.; Kim, H.S. The R&D and productivity relationship of Korean listed firms. J. Prod. Anal. 2011, 36, 125–142. [Google Scholar]

- Godart, F.C.; Shipilov, A.V.; Claes, K. Making the Most of the Revolving Door: The Impact of Outward Personnel Mobility Networks on Organizational Creativity. Organ. Sci. 2013, 25, 377–400. [Google Scholar] [CrossRef]

- Jiang, K.; Du, X.; Chen, Z. Firms’ digitalization and stock price crash risk. Int. Rev. Financ. Anal. 2022, 82, 102196. [Google Scholar] [CrossRef]

- Lou, Z.; Chen, S.; Yin, W.; Zhang, C.; Yu, X. Economic policy uncertainty and firm innovation: Evidence from a risk-taking perspective. Int. Rev. Econ. Financ. 2022, 77, 78–96. [Google Scholar] [CrossRef]

- Schilling, M.A.; Phelps, C.C. Interfirm Collaboration Networks: The Impact of Large-Scale Network Structure on Firm Innovation. Manag. Sci. 2007, 53, 1113–1126. [Google Scholar] [CrossRef]

- Almeida, P.; Phene, A.; Li, S. The Influence of Ethnic Community Knowledge on Indian Inventor Innovativeness. Organ. Sci. 2014, 26, 221671228. [Google Scholar] [CrossRef]

- Vig, V. Access to Collateral and Corporate Debt Structure: Evidence from a Natural Experiment. J. Financ. 2013, 68, 881–928. [Google Scholar] [CrossRef]

- Whited, T.M.; Wu, G.J. Financial constraints risk. Rev. Financ. Stud. 2006, 19, 531–559. [Google Scholar] [CrossRef]

- Sun, S.L.; Peng, M.W.; Tan, W. Institutional relatedness behind product diversification and international diversification. Asia Pac. J. Manag. 2017, 34, 339–366. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Variable | Definition | References |

|---|---|---|

| Digital transformation | The natural logarithm of the frequency of digital transformation feature terms in the company’s annual report after adding 1 | [60] |

| CSR | The natural logarithm of CSR ratings of Chinese listed companies published by RKS | [59] |

| EPU | Annual weighted average of the China Economic Policy Uncertainty Index/100 | [61] |

| Firm size | The natural logarithm of total assets | [58] |

| Profitability | Ratio of net profit to total assets | [58] |

| Growth | Growth rate of main business income | [31] |

| Ownership concentration | Ratio of the number of shares held by the largest shareholder to the total number of shares | [31] |

| State ownership | Dummy variable, assign a value of 1 if the enterprise is a state-owned enterprise, 0 otherwise | [58] |

| Accounts receivable turnover | Ratio of net receivables to total assets | [56] |

| Book-to-market value | Ratio of book value to total market value | [30] |

| Slack resources | Ratio of cash flow to total assets | [42] |

| Analyst coverage | Total number of independent analysts issuing company earnings forecasts | [30] |

| Board size | The natural logarithm of the number of board members | [31] |

| Board independence | Ratio of the number of independent directors to the total number of board members | [14] |

| CEO duality | Dummy variable, assigned a value of 1 if the CEO and Chairman are the same person, 0 otherwise | [14] |

| GDP growth | Growth rate of GDP | [25] |

| M2 growth | Growth rate of money supply | [25] |

| GPE | Growth rate of general public expenditure | [25] |

| Industry dummies | Dummy variables set based on industry classification codes published by the China Securities Regulatory Commission | [59] |

| Variable | Min | Max | Mean | S.D. | 1 | 2 | 3 | 4 | 5 | 6 | 7 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. Digital transformation | 0.000 | 3.800 | 0.899 | 0.917 | 1 | ||||||

| 2. CSR | 3.060 | 4.376 | 3.730 | 0.266 | 0.006 | 1 | |||||

| 3. EPU | 1.039 | 4.063 | 2.458 | 1.081 | 0.168 *** | 0.023 | 1 | ||||

| 4. Firm size | 20.442 | 27.072 | 23.018 | 1.382 | −0.050 * | 0.449 *** | 0.068 *** | 1 | |||

| 5. Profitability | −0.140 | 0.246 | 0.055 | 0.054 | 0.109 *** | 0.012 | −0.041 * | −0.111 *** | 1 | ||

| 6. Growth | −0.412 | 1.937 | 0.167 | 0.320 | 0.155 *** | 0.013 | 0.052 ** | 0.024 | 0.213 *** | 1 | |

| 7. Ownership concentration | 0.071 | 0.767 | 0.357 | 0.163 | −0.236 *** | 0.143 *** | −0.104*** | 0.210 *** | 0.036 * | −0.056 *** | 1 |

| 8. State ownership | 0.000 | 1.000 | 0.492 | 0.500 | −0.130 *** | 0.129 *** | −0.097 *** | 0.283 *** | −0.149*** | −0.080 *** | 0.320 *** |

| 9. Accounts receivable turnover | 0.000 | 0.492 | 0.123 | 0.109 | 0.197 *** | −0.092 *** | 0.002 | −0.193 *** | 0.034 | 0.079 *** | −0.092 *** |

| 10. Book-to-market value | 0.112 | 6.426 | 1.032 | 1.088 | −0.153 *** | 0.237 *** | 0.055 *** | 0.667 *** | −0.334 *** | −0.016 | 0.122 *** |

| 11. Slack resources | −0.344 | 1.838 | −0.055 | 0.342 | 0.106 *** | −0.184 *** | −0.032 | −0.431 *** | 0.252 *** | −0.041 * | −0.089 *** |

| 12. Analyst coverage | 0.000 | 3.850 | 2.133 | 1.022 | 0.084 *** | 0.210 *** | −0.047 ** | 0.307 *** | 0.406*** | 0.119 *** | 0.032 |

| 13. Board size | 1.609 | 2.708 | 2.179 | 0.205 | −0.042 | 0.160 *** | −0.067 *** | 0.179 *** | −0.02 | −0.040 * | −0.004 |

| 14. Board independence | 0.333 | 0.571 | 0.379 | 0.056 | 0.043 | −0.022 | 0.022 | 0.099 *** | −0.011 | −0.018 | 0.077 *** |

| 15. CEO duality | 0.000 | 1.000 | 0.229 | 0.421 | 0.137 *** | −0.068 *** | 0.039 * | −0.099 *** | 0.088 *** | 0.066 *** | −0.108 *** |

| 16. GDP growth | 0.067 | 0.095 | 0.072 | 0.007 | −0.149 *** | −0.075 *** | −0.536 *** | −0.113 *** | 0.084 *** | −0.001 | 0.061 *** |

| 17. M2 growth | 0.081 | 0.173 | 0.121 | 0.022 | −0.201 *** | −0.041 * | −0.621 *** | −0.104 *** | 0.044 ** | −0.040 * | 0.086 *** |

| 18. GPE | 0.068 | 0.216 | 0.112 | 0.044 | −0.137 *** | −0.056 *** | −0.448 *** | −0.091 *** | 0.035 | −0.031 | 0.047 ** |

| Variable | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 | 17 | 18 |

| 8. State ownership | 1 | ||||||||||

| 9. Accounts receivable turnover | −0.123 *** | 1 | |||||||||

| 10. Book-to-market value | 0.227 *** | −0.157 *** | 1 | ||||||||

| 11. Slack resources | −0.146 *** | −0.045 ** | −0.358 *** | 1 | |||||||

| 12. Analyst coverage | −0.106 *** | 0.022 | −0.014 | −0.015 | 1 | ||||||

| 13. Board size | 0.217 *** | −0.036 * | 0.090 *** | −0.101 *** | 0.107 *** | 1 | |||||

| 14. Board independence | −0.038 * | −0.050 ** | 0.065 *** | −0.018 | 0.01 | −0.468 *** | 1 | ||||

| 15. CEO duality | −0.303 *** | 0.066 *** | −0.084 *** | 0.067 *** | 0.046 ** | −0.139 *** | 0.095 *** | 1 | |||

| 16. GDP growth | 0.046 ** | 0.023 | 0.036 * | 0.110 *** | 0.107 *** | 0.108 *** | −0.029 | −0.01 | 1 | ||

| 17. M2 growth | 0.071 *** | 0.004 | −0.049 ** | 0.084 *** | 0.062 *** | 0.089 *** | −0.026 | −0.022 | 0.705 *** | 1 | |

| 18. GPE | 0.036 * | 0.021 | −0.032 | 0.083 *** | 0.044 ** | 0.062 *** | −0.018 | 0.002 | 0.659 *** | 0.754 *** | 1 |

| Dependent Variable | CSR | |||

|---|---|---|---|---|

| Models | Model 1 | Model 2 | Model 3 | Model 4 |

| Digital transformation | 0.161 *** (0.007) | 0.163 *** (0.006) | 0.159 *** (0.007) | |

| EPU | −0.038 *** (0.007) | −0.039 *** (0.007) | ||

| Digital transformation × EPU | −0.018 *** (0.005) | |||

| Firm size | 0.104 *** (0.008) | 0.105 *** (0.007) | 0.107 *** (0.007) | 0.108 *** (0.007) |

| Profitability | 0.138 (0.139) | 0.024 (0.143) | 0.007 (0.141) | −0.002 (0.141) |

| State ownership | −0.013 (0.014) | −0.004 (0.015) | −0.007 (0.015) | −0.008 (0.015) |

| Book-to-market value | −0.012 (0.009) | −0.007 (0.007) | −0.007 (0.007) | −0.008 (0.007) |

| Slack resources | 0.011 (0.021) | 0.024 (0.016) | 0.026 (0.016) | 0.026 (0.016) |

| Analyst coverage | 0.019 ** (0.008) | 0.011 * (0.006) | 0.011 ** (0.006) | 0.012 ** (0.006) |

| Board size | 0.045 (0.036) | 0.053 (0.040) | 0.051 (0.040) | 0.050 (0.040) |

| Board independence | −0.291 ** (0.129) | −0.256 * (0.143) | −0.267 * (0.142) | −0.287 ** (0.142) |

| CEO duality | −0.020 (0.016) | −0.023 (0.017) | −0.022 (0.017) | −0.022 (0.017) |

| GDP growth | −0.299 (1.331) | 0.645 (1.446) | −1.551 (1.495) | −1.398 (1.487) |

| M2 growth | 1.147 ** (0.521) | 2.756 *** (0.583) | 3.171 *** (0.584) | 3.140 *** (0.581) |

| GPE | −0.135 (0.241) | −0.499 * (0.267) | −0.897 *** (0.276) | −0.919 *** (0.274) |

| Constant | 1.119 *** | 0.840 *** | 1.052 *** | 1.045 *** |

| (0.222) | (0.216) | (0.219) | (0.218) | |

| Industry dummies | Yes | Yes | Yes | Yes |

| Chi2 | 607.24 | 1057.55 | 1079.38 | 1095.87 |

| Observations | 1439 | 1439 | 1439 | 1439 |

| Dependent variable | Digital transformation | |||

| Models | Model 5 | Model 6 | Model 7 | Model 8 |

| CSR | 2.324 *** (0.072) | 2.308 *** (0.072) | 2.382 *** (0.076) | |

| EPU | 0.120 *** (0.026) | 0.117 *** (0.026) | ||

| CSR × EPU | 0.152 ** (0.059) | |||

| Firm size | 0.040 ** (0.017) | −0.187 *** (0.021) | −0.192 *** (0.021) | −0.193 *** (0.021) |

| Profitability | 1.071 *** (0.389) | 0.423 (0.461) | 0.473 (0.456) | 0.478 (0.457) |

| Growth | 0.244 *** (0. 064) | 0.184 *** (0.054) | 0.177 *** (0.054) | 0.173 *** (0.054) |

| Ownership concentration | −0.767 *** (0.132) | −0.391 *** (0.111) | −0.388 *** (0.111) | −0.391 *** (0.111) |

| State ownership | −0.046 (0.046) | −0.043 (0.055) | −0.034 (0.054) | −0.036 (0.054) |

| Accounts receivable turnover | 0.507 ** (0.212) | 0.496 *** (0.179) | 0.512 *** (0.179) | 0.508 *** (0.179) |

| Board size | −0.026 (0.118) | −0.138 (0.140) | −0.132 (0.139) | −0.138 (0.139) |

| Board independence | 0.455 (0.421) | 1.010 ** (0.502) | 1.041 ** (0.498) | 1.053** (0.498) |

| CEO duality | 0.015 (0.051) | 0.080 (0.061) | 0.077 (0.060) | 0.075 (0.060) |

| GDP growth | −14.445 *** (4.134) | −8.810 * (4.945) | −1.991 (5.118) | −1.981 (5.126) |

| M2 growth | −7.194 *** (1.695) | −10.250 *** (2.025) | −11.500 *** (2.025) | −11.772 *** (2.031) |

| GPE | 1.121 (0.775) | 2.131 ** (0.928) | 3.354 *** (0.956) | 3.465 *** (0.959) |

| Constant | 1.173 ** | −2.334 *** | −2.997 *** | −3.198 *** |

| (0.540) | (0.653) | (0.664) | (0.669) | |

| Industry dummies | Yes | Yes | Yes | Yes |

| Chi2 | 757.47 | 1545.57 | 1559.55 | 1576.70 |

| Observations | 1439 | 1439 | 1439 | 1439 |

| Dependent Variable | CSR | |||

|---|---|---|---|---|

| Models | Model 1 | Model 2 | Model 3 | Model 4 |

| Digital transformation | 0.842 *** (0.018) | 0.160 *** (0.007) | 0.074 *** (0.011) | 0.159 *** (0.007) |

| EPU | −0.008 (0.006) | −0.041 *** (0.008) | −0.031 *** (0.010) | −0.039 *** (0.007) |

| Digital transformation × EPU | −0.063 *** (0.015) | −0.019 *** (0.006) | −0.019 ** (0.008) | −0.018 *** (0.005) |

| Firm size | 0.094 *** (0.005) | 0.108 *** (0.007) | 0.113 *** (0.009) | 0.108 *** (0.007) |

| Profitability | 0.236 ** (0.110) | −0.001 (0.141) | −0.031 (0.168) | 0.002 (0.141) |

| State ownership | 0.020 * (0.012) | −0.008 (0.015) | −0.026 (0.018) | −0.008 (0.015) |

| Book-to-market value | −0.005 (0.004) | −0.007 (0.007) | −0.017 (0.010) | −0.008 (0.007) |

| Slack resources | −0.004 (0.010) | 0.026 (0.016) | 0.021 (0.023) | 0.026 (0.016) |

| Analyst coverage | 0.007 * (0.007) | 0.012 ** (0.006) | 0.020 ** (0.009) | 0.012 ** (0.006) |

| Board size | 0.060 ** (0.028) | 0.052 (0.039) | 0.061 (0.045) | 0.050 (0.039) |

| Board independence | −0.237 ** (0.104) | −0.281 ** (0.141) | −0.311 * (0.162) | −0.287 ** (0.142) |

| CEO duality | −0.008 (0.014) | −0.022 (0.017) | −0.011 (0.019) | −0.022 (0.017) |

| GDP growth | −2.976 *** (1.031) | −0.461 (1.458) | 4.708 ** (2.292) | −1.398 (1.487) |

| M2 growth | 0.151 (0.389) | 2.124 *** (0.583) | 0.082 (1.841) | 3.140 *** (0.581) |

| GPE | −0.027 (0.218) | −0.636 ** (0.265) | −0.411 (0.549) | −0.919 *** (0.274) |

| Constant | 1.568 *** | 1.077 *** | 0.762 *** | 3.719 *** |

| (0.151) | (0.219) | (0.270) | (0.055) | |

| Industry dummies | Yes | Yes | Yes | Yes |

| Chi2 | 3605.56 | 1091.41 | 489.17 | 1095.87 |

| Observations | 2888 | 1439 | 1031 | 1439 |

| Dependent variable | Digital transformation | |||

| Models | Model 5 | Model 6 | Model 7 | Model 8 |

| CSR | 0.578 *** (0.011) | 2.350 *** (0.075) | 1.760 *** (0.136) | 2.382 *** (0.075) |

| EPU | −0.004 (0.005) | 0.128 *** (0.028) | 0.115 *** (0.031) | 0.117 *** (0.026) |

| CSR × EPU | 0.020 ** (0.010) | 0.113 * (0.060) | 0.320*** (0.104) | 0.152 ** (0.059) |

| Firm size | −0.054 *** (0.004) | −0.191 *** (0.021) | −0.117 *** (0.024) | −0.193 *** (0.021) |

| Profitability | −0.119 (0.081) | 0.470 (0.456) | 1.285 *** (0.489) | 0.478 (0.457) |

| Growth | 0.012 (0.008) | 0.170 *** (0.054) | 0.244 *** (0.078) | 0.173 *** (0.053) |

| Ownership concentration | 0.032 * (0.016) | −0.390 *** (0.111) | −0.647 *** (0.150) | −0.391 *** (0.111) |

| State ownership | −0.011 (0.009) | −0.034 (0.054) | 0.005 (0.058) | −0.036 (0.054) |

| Accounts receivable turnover | 0.098 *** (0.029) | 0.511 *** (0.179) | 0.558 ** (0.237) | 0.508 *** (0.179) |

| Board size | −0.013 (0.022) | −0.141 (0.139) | −0.097 (0.148) | −0.138 (0.139) |

| Board independence | 0.219 *** (0.082) | 1.035 ** (0.498) | 1.110 ** (0.537) | 1.053 ** (0.498) |

| CEO duality | 0.002 (0.011) | 0.075 (0.060) | 0.028 (0.063) | 0.075 (0.060) |

| GDP growth | 2.128 *** (0.802) | −4.283 (4.995) | −18.896 ** (7.522) | −1.981 (5.126) |

| M2 growth | −0.173 (0.305) | −9.079 *** (2.031) | −4.279 (6.034) | −11.772 *** (2.031) |

| GPE | 0.057 (0.171) | 2.723 *** (0.926) | 1.723 (1.783) | 3.465 *** (0.958) |

| Constant | −1.007 *** | −3.210 *** | −2.167 *** | 0.536 *** |

| (0.108) | (0.672) | (0.778) | (0.195) | |

| Industry dummies | Yes | Yes | Yes | Yes |

| Chi2 | 3852.48 | 1560.51 | 772.41 | 1576.70 |

| Observations | 2888 | 1439 | 1031 | 1439 |

| Models | Model 1 Government Subsidies | Model 2 Cost of Debt Financing | Model 3 Financing Constraints (WW index) |

|---|---|---|---|

| CSR | 0.410 *** (0.129) | −0.010 *** (0.003) | −0.017 *** (0.005) |

| EPU | −0.091 *** (0.031) | 0.001 * (0.001) | 0.005 *** (0.001) |

| CSR × EPU | −0.076 (0.102) | −0.006 ** (0.002) | −0.008 ** (0.004) |

| Firm size | 0.841 *** (0.027) | 0.005 *** (0.001) | −0.043*** (0.001) |

| Profitability | 1.346 ** (0.552) | −0.159 *** (0.013) | −0.205 *** (0.020) |

| Growth | 0.181 ** (0.091) | 0.005 ** (0.002) | −0.013 *** (0.003) |

| Ownership concentration | −0.666 *** (0.188) | −0.001 (0.005) | −0.006 (0.006) |

| State ownership | −0.036 (0.066) | −0.006 *** (0.002) | −0.001 (0.002) |

| Board size | 0.609 *** (0.168) | 0.001 (0.004) | 0.009 (0.006) |

| Board independence | 0.857 (0.596) | 0.008 (0.014) | −0.015 (0.020) |

| CEO duality | −0.005 (0.072) | −0.001 (0.002) | −0.005 ** (0.003) |

| GDP growth | 1.401 (6.165) | 0.038 (0.148) | 0.020 (0.211) |

| M2 growth | 2.350 (2.442) | 0.061 (0.059) | −0.021 (0.089) |

| GPE | −0.796 (1.150) | −0.057 ** (0.028) | 0.019 (0.040) |

| Constant | −3.422 *** (0.829) | −0.112 *** (0.020) | −0.064 ** (0.028) |

| Industry dummies | Yes | Yes | Yes |

| R2 | 0.574 | 0.226 | 0.776 |

| F | 56.572 *** | 12.426 *** | 125.936 *** |

| Observations | 1417 | 1439 | 1236 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Huang, G.; Shen, L. The Bidirectional Relationship between Digital Transformation and Corporate Social Responsibility: A Legitimacy Perspective. Sustainability 2024, 16, 3029. https://doi.org/10.3390/su16073029

Huang G, Shen L. The Bidirectional Relationship between Digital Transformation and Corporate Social Responsibility: A Legitimacy Perspective. Sustainability. 2024; 16(7):3029. https://doi.org/10.3390/su16073029

Chicago/Turabian StyleHuang, Guangyu, and Liqiong Shen. 2024. "The Bidirectional Relationship between Digital Transformation and Corporate Social Responsibility: A Legitimacy Perspective" Sustainability 16, no. 7: 3029. https://doi.org/10.3390/su16073029

APA StyleHuang, G., & Shen, L. (2024). The Bidirectional Relationship between Digital Transformation and Corporate Social Responsibility: A Legitimacy Perspective. Sustainability, 16(7), 3029. https://doi.org/10.3390/su16073029