Does Investor Sentiment Drive Corporate Green Innovation: Evidence from China

Abstract

1. Introduction

2. Literature Review and Hypothesis Development

2.1. Literature Review

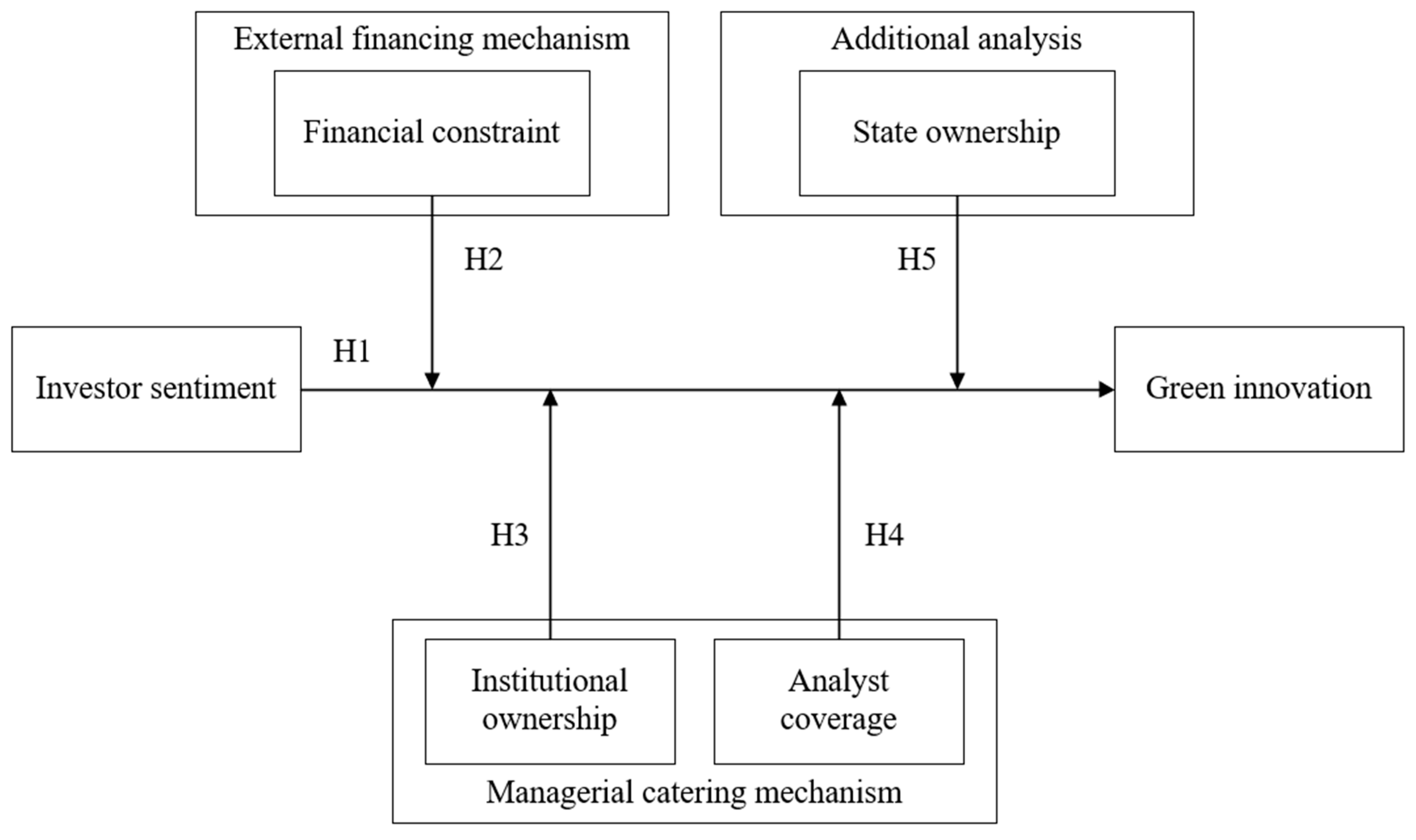

2.2. Investor Sentiment and Corporate Green Innovation

2.3. Potential Mechanism

2.3.1. External Financing Channel

2.3.2. Managerial Catering Channel

2.4. State Ownership

3. Research Design

3.1. Sample and Data

3.2. Measurement of Variables

3.2.1. Dependent Variable

3.2.2. Independent Variable

3.2.3. Moderating Variable

3.2.4. Control Variable

3.3. Empirical Model

4. Empirical Analysis

4.1. Descriptive Statistics

4.2. Baseline Regression Result

4.3. Moderating Effect

5. Robustness Test

5.1. Instrumental Variable

5.2. Propensity Score Matching

5.3. Re-Measuring the Green Innovation and the Investor Sentiment

5.4. Replace the Regression Model

5.5. Distinguish Patent Types

6. Conclusions and Discussion

6.1. Conclusions

- (1)

- The optimistic investor sentiment exerts a positive influence on firm green innovation. This conclusion’s robustness has been confirmed through a variety of tests.

- (2)

- Mechanistic analysis shows that investor sentiment propels corporate green innovation via external financing and managerial catering channels. Positive investor sentiment facilitates access to the financial capital required for green innovation and aids companies in surmounting fiscal constraints associated with these endeavors. During periods of high sentiment, green innovation satisfies investors’ pursuit of high-risk but high-return projects, prompting managers to cater to these preferences and bolstering firms’ resolve to pursue green innovation. Both institutional ownership and analyst coverage can amplify the positive impact of investor sentiment on corporate green innovation. Institutional investors prioritise long-term returns and corporate environmental performance, while analyst coverage can increase firms’ information transparency and lessen the information asymmetry that exists between investors and managers. Together, these two external governance mechanisms can increase managerial pressure and incentives to pursue green innovation.

- (3)

- Additional investigation has shown that the relationship between investor sentiment and green innovation is favourably moderated by state ownership. One explanation might be that SOEs have political incentives to support green development policies and are key players in driving green innovation. Because of this, SOEs need to invest a lot of money, especially in equity, to strengthen their capacity for green innovation. Positive investor mood offers SOEs a chance to advance environmental conservation objectives, reduce equity costs, and lessen the diluting effect of issuing shares on national ownership.

6.2. Theoretical Contribution

6.3. Practical Implication

6.4. Limitation and Further Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Amore, M.D.; Bennedsen, M.; Larsen, B.; Rosenbaum, P. CEO education and corporate environmental footprint. J. Environ. Econ. Manag. 2019, 94, 254–273. [Google Scholar] [CrossRef]

- Abid, N.; Ceci, F.; Ahmad, F.; Aftab, J. Financial development and green innovation, the ultimate solutions to an environmentally sustainable society: Evidence from leading economies. J. Clean. Prod. 2022, 369, 133223. [Google Scholar] [CrossRef]

- Aftab, J.; Abid, N.; Sarwar, H.; Veneziani, M. Environmental ethics, green innovation, and sustainable performance: Exploring the role of environmental leadership and environmental strategy. J. Clean. Prod. 2022, 378, 134639. [Google Scholar] [CrossRef]

- Sierzchula, W.; Nemet, G. Using patents and prototypes for preliminary evaluation of technology-forcing policies: Lessons from California’s Zero Emission Vehicle regulations. Technol. Forecast. Soc. Chang. 2015, 100, 213–224. [Google Scholar] [CrossRef]

- Dangelico, R.M.; Pujari, D.; Pontrandolfo, P. Green product innovation in manufacturing firms: A sustainability-oriented dynamic capability perspective. Bus. Strategy Environ. 2017, 26, 490–506. [Google Scholar] [CrossRef]

- Mrkajic, B.; Murtinu, S.; Scalera, V.G. Is green the new gold? Venture capital and green entrepreneurship. Small Bus. Econ. 2019, 52, 929–950. [Google Scholar] [CrossRef]

- Etzkowitz, H.; Leydesdorff, L. The endless transition: A “triple helix” of university-industry-government relations: Introduction. Minerva 1998, 36, 203–208. [Google Scholar] [CrossRef]

- Stein, J. Rational Capital Budgeting in an Irrational World. J. Bus. 1996, 69, 429–455. [Google Scholar] [CrossRef]

- Baker, M.; Wurgler, J. Market Timing and Capital Structure. J. Financ. 2002, 57, 1–32. [Google Scholar] [CrossRef]

- Polk, C.; Sapienza, P. The Stock Market and Corporate Investment: A Test of Catering Theory. Rev. Financ. Stud. 2009, 22, 187–217. [Google Scholar] [CrossRef]

- Dang, T.V.; Xu, Z. Market sentiment and innovation activities. J. Financ. Quant. Anal. 2018, 53, 1135–1161. [Google Scholar] [CrossRef]

- Shen, H.; Zheng, S.; Xiong, H.; Tang, W.; Silverman, H. Stock market mispricing and firm innovation based on path analysis. Econ. Model. 2021, 95, 330–343. [Google Scholar] [CrossRef]

- Rennings, K. Redefining innovation—Eco-innovation research and the contribution from ecological economics. Ecol. Econ. 2000, 32, 319–332. [Google Scholar] [CrossRef]

- Baker, M.; Stein, J.C.; Wurgler, J. When does the Market Matter? Stock Prices and the Investment of Equity-Dependent Firms. Q. J. Econ. 2003, 118, 969–1005. [Google Scholar] [CrossRef]

- Hua, G.; Zhou, S.; Zhang, S.; Wang, J. Industry policy, investor sentiment, and cross-industry capital flow: Evidence from Chinese listed companies’ cross-industry M&As. Res. Int. Bus. Financ. 2020, 53, 101221. [Google Scholar]

- Naughton, J.P.; Wang, C.; Yeung, I. Investor sentiment for corporate social performance. Account. Rev. 2019, 94, 401–420. [Google Scholar] [CrossRef]

- Dyck, A.; Lins, K.V.; Roth, L.; Wagner, H.F. Do institutional investors drive corporate social responsibility? International evidence. J. Financ. Econ. 2019, 131, 693–714. [Google Scholar] [CrossRef]

- Bekkum, S.V.; Han, S.; Pennings, E. Buy Smart, Time Smart: Are Takeovers Driven by Growth Opportunities or Mispricing? Financ. Manag. 2011, 40, 911–940. [Google Scholar] [CrossRef]

- D’Angelo, V.; Cappa, F.; Peruffo, E. Green manufacturing for sustainable development: The positive effects of green activities, green investments, and non-green products on economic performance. Bus. Strategy Environ. 2023, 32, 1900–1913. [Google Scholar] [CrossRef]

- Tang, M.; Walsh, G.; Lerner, D.; Fitza, M.A.; Li, Q. Green innovation, managerial concern and firm performance: An empirical study. Bus. Strategy Environ. 2018, 27, 39–51. [Google Scholar] [CrossRef]

- Qiu, L.; Jie, X.; Wang, Y.; Zhao, M. Green product innovation, green dynamic capability, and competitive advantage: Evidence from Chinese manufacturing enterprises. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 146–165. [Google Scholar] [CrossRef]

- Sarwar, H.; Aftab, J.; Ishaq, M.I. Achieving business competitiveness through corporate social responsibility and dynamic capabilities: An empirical evidence from emerging economy. J. Clean. Prod. 2023, 386, 135820. [Google Scholar] [CrossRef]

- Lee, K.H.; Min, B. Green R&D for eco-innovation and its impact on carbon emissions and firm performance. J. Clean. Prod. 2015, 108, 534–542. [Google Scholar]

- Dangelico, R.M. Green product innovation: Where we are and where we are going. Bus. Strategy Environ. 2016, 25, 560–576. [Google Scholar] [CrossRef]

- Wang, M.; Li, Y.; Li, M. Will carbon tax affect the strategy and performance of low-carbon technology sharing between enterprises? J. Clean. Prod. 2019, 210, 724–737. [Google Scholar] [CrossRef]

- Wang, C.; Nie, P.; Peng, D.; Li, Z.H. Green insurance subsidy for promoting clean production innovation. J. Clean. Prod. 2017, 148, 111–117. [Google Scholar] [CrossRef]

- Qi, G.; Jia, Y.; Zou, H. Is institutional pressure the mother of green innovation? Examining the moderating effect of absorptive capacity. J. Clean. Prod. 2021, 278, 123957. [Google Scholar] [CrossRef]

- Qi, G.; Zou, H.; Xie, X. Governmental inspection and green innovation: Examining the role of environmental capability and institutional development. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 1774–1785. [Google Scholar] [CrossRef]

- Liu, Y.; Wang, A.; Wu, Y. Environmental regulation and green innovation: Evidence from China’s new environmental protection law. J. Clean. Prod. 2021, 297, 126698. [Google Scholar] [CrossRef]

- Liao, Z.; Weng, C.; Shen, C. Can public surveillance promote corporate environmental innovation? The mediating role of environmental law enforcement. Sustain. Dev. 2020, 28, 1519–1527. [Google Scholar] [CrossRef]

- Zhang, F.; Zhu, L. Enhancing corporate sustainable development: Stakeholder pressures, organizational learning, and green innovation. Bus. Strategy Environ. 2019, 28, 1012–1026. [Google Scholar] [CrossRef]

- Wang, H.; Khan, M.A.S.; Anwar, F.; Shahzad, F.; Adu, D.; Murad, M. Green innovation practices and its impacts on environmental and organizational performance. Front. Psychol. 2021, 11, 553625. [Google Scholar] [CrossRef] [PubMed]

- Song, M.; Yang, M.X.; Zeng, K.J.; Feng, W. Green knowledge sharing, stakeholder pressure, absorptive capacity, and green innovation: Evidence from Chinese manufacturing firms. Bus. Strategy Environ. 2020, 29, 1517–1531. [Google Scholar] [CrossRef]

- Zhang, C.; Jin, S. How Does an Environmental Information Disclosure of a Buyer’s Enterprise Affect Green Technological Innovations of Sellers’ Enterprise? Int. J. Environ. Res. Public Health 2022, 19, 14715. [Google Scholar] [CrossRef]

- Hu, G.; Wang, X.; Wang, Y. Can the green credit policy stimulate green innovation in heavily polluting enterprises? Evidence from a quasi-natural experiment in China. Energy Econ. 2021, 98, 105134. [Google Scholar] [CrossRef]

- Han, S.; Zhang, Z.; Yang, S. Green Finance and Corporate Green Innovation: Based on China’s Green Finance Reform and Innovation Pilot Policy. J. Environ. Public Health 2022, 2022, 1833377. [Google Scholar] [CrossRef] [PubMed]

- Zeng, Q.; Tong, Y.; Yang, Y. Can green finance promote green technology innovation in enterprises: Empirical evidence from China. Environ. Sci. Pollut. Res. 2023, 30, 87628–87644. [Google Scholar] [CrossRef]

- Albort-Morant, G.; Leal-Millán, A.; Cepeda-Carrion, G.; Henseler, J. Developing green innovation performance by fostering of organizational knowledge and coopetitive relations. Rev. Manag. Sci. 2018, 12, 499–517. [Google Scholar] [CrossRef]

- Arfi, W.B.; Hikkerova, L.; Sahut, J.M. External knowledge sources, green innovation and performance. Technol. Forecast. Soc. Change 2018, 129, 210–220. [Google Scholar] [CrossRef]

- Pan, X.; Chen, X.; Sinha, P.; Dong, N. Are firms with state ownership greener? An institutional complexity view. Bus. Strategy Environ. 2020, 29, 197–211. [Google Scholar] [CrossRef]

- Iguchi, H.; Katayama, H.; Yamanoi, J. CEOs’ religiosity and corporate green initiatives. Small Bus. Econ. 2022, 58, 497–522. [Google Scholar] [CrossRef]

- Ren, S.; Wang, Y.; Hu, Y.; Yan, J. CEO hometown identity and firm green innovation. Bus. Strategy Environ. 2021, 30, 756–774. [Google Scholar] [CrossRef]

- Horbach, J.; Jacob, J. The relevance of personal characteristics and gender diversity for (eco-) innovation activities at the firm-level: Results from a linked employer–employee database in Germany. Bus. Strategy Environ. 2018, 27, 924–934. [Google Scholar] [CrossRef]

- Soewarno, N.; Tjahjadi, B.; Fithrianti, F. Green innovation strategy and green innovation: The roles of green organizational identity and environmental organizational legitimacy. Manag. Decis. 2019, 57, 3061–3078. [Google Scholar] [CrossRef]

- Wang, C.H. How organizational green culture influences green performance and competitive advantage: The mediating role of green innovation. J. Manuf. Technol. Manag. 2019, 30, 666–683. [Google Scholar] [CrossRef]

- Sharma, S.; Prakash, G.; Kumar, A.; Mussada, E.K.; Antony, J.; Luthra, S. Analysing the relationship of adaption of green culture, innovation, green performance for achieving sustainability: Mediating role of employee commitment. J. Clean. Prod. 2021, 303, 127039. [Google Scholar] [CrossRef]

- Amore, M.D.; Bennedsen, M. Corporate governance and green innovation. J. Environ. Econ. Manag. 2016, 75, 54–72. [Google Scholar] [CrossRef]

- Usman, M.; Javed, M.; Yin, J. Board internationalization and green innovation. Econ. Lett. 2020, 197, 109625. [Google Scholar] [CrossRef] [PubMed]

- Yu, C.H.; Wu, X.; Zhang, D.; Chen, S.; Zhao, J. Demand for green finance: Resolving financing constraints on green innovation in China. Energy Policy 2021, 153, 112255. [Google Scholar] [CrossRef]

- Xiang, X.; Liu, C.; Yang, M. Who is financing corporate green innovation? Int. Rev. Econ. Financ. 2022, 78, 321–337. [Google Scholar] [CrossRef]

- Li, X.; Shao, X.; Chang, T.; Albu, L.L. Does digital finance promote the green innovation of China’s listed companies? Energy Econ. 2022, 114, 106254. [Google Scholar] [CrossRef]

- Lin, B.; Ma, R. How does digital finance influence green technology innovation in China? Evidence from the financing constraints perspective. J. Environ. Manag. 2022, 320, 115833. [Google Scholar] [CrossRef] [PubMed]

- Sha, Y.; Zhang, P.; Wang, Y.; Xu, Y. Capital market opening and green innovation—Evidence from Shanghai-Hong Kong stock connect and the Shenzhen-Hong Kong stock connect. Energy Econ. 2022, 111, 106048. [Google Scholar] [CrossRef]

- Zhang, Y.; Zhang, J.; Cheng, Z. Stock market liberalization and corporate green innovation: Evidence from China. Int. J. Environ. Res. Public Health 2021, 18, 3412. [Google Scholar] [CrossRef] [PubMed]

- Takalo, S.K.; Tooranloo, H.S. Green innovation: A systematic literature review. J. Clean. Prod. 2021, 279, 122474. [Google Scholar] [CrossRef]

- Noailly, J.; Smeets, R. Directing technical change from fossil-fuel to renewable energy innovation: An application using firm-level patent data. J. Environ. Econ. Manag. 2015, 72, 15–37. [Google Scholar] [CrossRef]

- Li, D.; Zhao, Y.; Zhang, L.; Chen, X.; Cao, C. Impact of quality management on green innovation. J. Clean. Prod. 2018, 170, 462–470. [Google Scholar] [CrossRef]

- Elliott, W.B.; Koëter-Kant, J.; Warr, R.S. Market Timing and the Debt–equity Choice. J. Financ. Intermediation 2008, 17, 175–197. [Google Scholar] [CrossRef]

- Chen, Y.S. The driver of green innovation and green image–green core competence. J. Bus. Ethics 2008, 81, 531–543. [Google Scholar] [CrossRef]

- Hillestad, T.; Xie, C. Haugland S A. Innovative corporate social responsibility: The founder’s role in creating a trustworthy corporate brand through “green innovation”. J. Prod. Brand Manag. 2010, 19, 440–451. [Google Scholar] [CrossRef]

- Chiou, T.Y.; Chan, H.K.; Lettice, F.; Chung, S.H. The influence of greening the suppliers and green innovation on environmental performance and competitive advantage in Taiwan. Transp. Res. Part E Logist. Transp. Rev. 2011, 47, 822–836. [Google Scholar] [CrossRef]

- Huang, J.W.; Li, Y.H. Green innovation and performance: The view of organizational capability and social reciprocity. J. Bus. Ethics 2017, 145, 309–324. [Google Scholar] [CrossRef]

- Przychodzen, J.; Przychodzen, W. Relationships between eco-innovation and financial performance–evidence from publicly traded companies in Poland and Hungary. J. Clean. Prod. 2015, 90, 253–263. [Google Scholar] [CrossRef]

- García-Sánchez, I.M.; Gallego-Álvarez, I.; Zafra-Gómez, J.L. Do the ecoinnovation and ecodesign strategies generate value added in munificent environments? Bus. Strategy Environ. 2020, 29, 1021–1033. [Google Scholar] [CrossRef]

- Sparkes, R.; Cowton, C.J. The maturing of socially responsible investment: A review of the developing link with corporate social responsibility. J. Bus. Ethics 2004, 52, 45–57. [Google Scholar] [CrossRef]

- Rezende, L.A.; Bansi, A.C.; Alves, M.F.R.; Galina, S.V.R. Take your time: Examining when green innovation affects financial performance in multinationals. J. Clean. Prod. 2019, 233, 993–1003. [Google Scholar] [CrossRef]

- Luo, X.; Wang, H.; Raithel, S.; Zheng, Q. Corporate social performance, analyst stock recommendations, and firm future returns. Strateg. Manag. J. 2015, 36, 123–136. [Google Scholar] [CrossRef]

- Aghion, P.; Van Reenen, J.; Zingales, L. Innovation and institutional ownership. Am. Econ. Rev. 2013, 103, 277–304. [Google Scholar] [CrossRef]

- Yang, Z.; Su, D.; Xu, S.; Han, X. Institutional investors and corporate green innovation: Evidence from China. Pac. Econ. Rev. 2023, 1–37. [Google Scholar] [CrossRef]

- Fiorillo, P.; Meles, A.; Mustilli, M.; Salerno, D. How does the financial market influence firms’ Green innovation? The role of equity analysts. J. Int. Financ. Manag. Account. 2022, 33, 428–458. [Google Scholar] [CrossRef]

- Ivković, Z.; Jegadeesh, N. The timing and value of forecast and recommendation revisions. J. Financ. Econ. 2004, 73, 433–463. [Google Scholar] [CrossRef]

- Lui, D.; Markov, S.; Tamayo, A. What makes a stock risky? Evidence from sell-side analysts’ risk ratings. J. Account. Res. 2007, 45, 629–665. [Google Scholar] [CrossRef]

- Asquith, P.; Mikhail, M.B.; Au, A.S. Information content of equity analyst reports. J. Financ. Econ. 2005, 75, 245–282. [Google Scholar] [CrossRef]

- Mola, S.; Rau, P.R.; Khorana, A. Is there life after the complete loss of analyst coverage? Account. Rev. 2013, 88, 667–705. [Google Scholar] [CrossRef]

- Berrone, P.; Fosfuri, A.; Gelabert, L.; Gomez-Mejia, L.R. Necessity as the mother of ‘green’inventions: Institutional pressures and environmental innovations. Strateg. Manag. J. 2013, 34, 891–909. [Google Scholar] [CrossRef]

- Li, J.; Xia, J.; Shapiro, D.; Lin, Z. Institutional compatibility and the internationalization of Chinese SOEs: The moderating role of home subnational institutions. J. World Bus. 2018, 53, 641–652. [Google Scholar] [CrossRef]

- Xia, J.; Ma, X.; Lu, J.W.; Yiu, D.W. Outward foreign direct investment by emerging market firms: A resource dependence logic. Strateg. Manag. J. 2014, 35, 1343–1363. [Google Scholar] [CrossRef]

- Meyer, K.E.; Peng, M.W. Theoretical foundations of emerging economy business research. J. Int. Bus. Stud. 2016, 47, 3–22. [Google Scholar] [CrossRef]

- Lin, J.Y.; Cai, F.; Li, Z. Competition, policy burdens, and state-owned enterprise reform. Am. Econ. Rev. 1998, 88, 422–427. [Google Scholar]

- Song, Z.; Storesletten, K.; Zilibotti, F. Growing Like China. Am. Econ. Rev. 2011, 101, 196–233. [Google Scholar] [CrossRef]

- Zhou, K.Z.; Gao, G.Y.; Zhao, H. State ownership and firm innovation in China: An integrated view of institutional and efficiency logics. Adm. Sci. Q. 2017, 62, 375–404. [Google Scholar] [CrossRef]

- Chen, V.Z.; Li, J.; Shapiro, D.M.; Zhang, X. Ownership structure and innovation: An emerging market perspective. Asia Pac. J. Manag. 2014, 31, 1–24. [Google Scholar] [CrossRef]

- Luo, X.R.; Wang, D.; Zhang, J. Whose call to answer: Institutional complexity and firms’ CSR reporting. Acad. Manag. J. 2017, 60, 321–344. [Google Scholar] [CrossRef]

- Fang, V.W.; Tian, X.; Tice, S. Does stock liquidity enhance or impede firm innovation? J. Financ. 2014, 69, 2085–2125. [Google Scholar] [CrossRef]

- Rhodes-Kropf, M.; Robinson, D.T.; Viswanathan, S. Valuation waves and merger activity: The empirical evidence. J. Financ. Econ. 2005, 77, 561–603. [Google Scholar] [CrossRef]

- Hadlock, C.J.; Pierce, J.R. New evidence on measuring financial constraints: Moving beyond the KZ index. Rev. Financ. Stud. 2010, 23, 1909–1940. [Google Scholar] [CrossRef]

- To, T.Y.; Navone, M.; Wu, E. Analyst coverage and the quality of corporate investment decisions. J. Corp. Financ. 2018, 51, 164–181. [Google Scholar] [CrossRef]

- Liu, X. Managerial myopia and firm green innovation: Based on text analysis and machine learning. Front. Psychol. 2022, 13, 911335. [Google Scholar] [CrossRef] [PubMed]

- Li, H.; Qian, Z.; Wang, S.; Wang, J.; Wang, Q. Do green concerns promote corporate green innovation? Evidence from Chinese stock exchange interactive platforms. Manag. Decis. Econ. 2023, 44, 1786–1801. [Google Scholar] [CrossRef]

- Zhao, J.; Qu, J.; Wei, J.; Yin, H.; Xi, X. The effects of institutional investors on firms’ green innovation. J. Prod. Innov. Manag. 2023, 40, 195–230. [Google Scholar] [CrossRef]

- Saunders, E.M. Stock prices and Wall Street weather. Am. Econ. Rev. 1993, 83, 1337–1345. [Google Scholar]

- Hirshleifer, D.; Shumway, T. Good day sunshine: Stock returns and the weather. J. Financ. 2003, 58, 1009–1032. [Google Scholar] [CrossRef]

- Baker, M.; Wurgler, J. Investor Sentiment and the Cross-Section of Stock Returns. J. Financ. 2006, 61, 1645–1680. [Google Scholar] [CrossRef]

- Campello, M.; Graham, J.R. Do stock prices influence corporate decisions? Evidence from the technology bubble. J. Financ. Econ. 2013, 107, 89–110. [Google Scholar] [CrossRef]

- Fu, J.; Wu, X.; Liu, Y.; Chen, R. Firm-specific investor sentiment and stock price crash risk. Financ. Res. Lett. 2021, 38, 101442. [Google Scholar] [CrossRef]

- Badertscher, B.A.; Shanthikumar, D.M.; Teoh, S.H. Private Firm Investment and Public Peer Misvaluation. Account. Rev. 2019, 94, 31–60. [Google Scholar] [CrossRef]

{kind=link}

| Variable | Symbol | Definition |

|---|---|---|

| Green innovation | Green | Logarithm of one plus the number of green patent applications in that year that are ultimately granted |

| Investor sentiment | IS | Stock mispricing obtained by decomposing the market-book ratio |

| Financial constraints | FC | SA index, SA= −0.737 × Size + 0.043 × Size2 − 0.04 × Age |

| Institutional ownership | IO | Shares held by institutional investors/Total shares |

| Analyst coverage | AC | Logarithm of one plus the number of analysts following a firm in a year |

| State ownership | SOE | If the firm is a SOE, SOE equals 1; otherwise, SOE equals 0. |

| Size | Size | Logarithm of total assets |

| Age | Age | Logarithm of firm age |

| Leverage | Lev | Total liabilities/total assets |

| Profitability | ROA | Net profits/total assets |

| Growth | Grow | Revenue growth rate |

| Asset structure | Fix | Net fixed assets/total assets |

| Cash flow | CF | Operating cash flow/total assets |

| Ownership concentration | Top | The largest shareholder’s shares/total shares |

| Independence of the board | ID | Number of independent directors/number of directors |

| Variable | Mean | SD | Min | Median | Max |

|---|---|---|---|---|---|

| Green | 0.686 | 1.037 | 0 | 0 | 4.263 |

| IS | 0.043 | 0.394 | −0.728 | 0.003 | 1.210 |

| FC | −3.733 | 0.241 | −4.317 | −3.740 | −3.086 |

| IO | 0.408 | 0.249 | 0 | 0.424 | 0.896 |

| AC | 1.496 | 1.153 | 0 | 1.386 | 3.714 |

| SOE | 0.413 | 0.492 | 0 | 0 | 1 |

| Size | 22.08 | 1.289 | 19.48 | 21.92 | 26.02 |

| Age | 2.317 | 0.646 | 1.099 | 2.398 | 3.258 |

| Lev | 0.444 | 0.213 | 0.053 | 0.439 | 0.929 |

| ROA | 0.035 | 0.059 | −0.248 | 0.034 | 0.191 |

| Grow | 0.214 | 0.563 | −0.594 | 0.116 | 4.070 |

| Fix | 0.225 | 0.168 | 0.002 | 0.190 | 0.719 |

| CF | 0.041 | 0.073 | −0.191 | 0.041 | 0.245 |

| Top | 0.350 | 0.149 | 0.091 | 0.330 | 0.750 |

| ID | 0.374 | 0.053 | 0.333 | 0.333 | 0.571 |

| (1) | (2) | (3) | |

|---|---|---|---|

| Green | Green | Green | |

| IS | 0.182 *** | 0.171 *** | 0.127 *** |

| (0.016) | (0.015) | (0.017) | |

| Size | 0.338 *** | 0.344 *** | |

| (0.007) | (0.006) | ||

| Age | −0.250 *** | −0.115 *** | |

| (0.012) | (0.011) | ||

| Lev | 0.064 * | 0.134 *** | |

| (0.035) | (0.034) | ||

| ROA | 0.192 * | 0.721 *** | |

| (0.108) | (0.106) | ||

| Grow | −0.016 | −0.004 | |

| (0.011) | (0.010) | ||

| Fix | −0.115 *** | −0.133 *** | |

| (0.040) | (0.041) | ||

| CF | −0.209 ** | −0.036 | |

| (0.088) | (0.078) | ||

| Top | −0.382 *** | −0.152 *** | |

| (0.047) | (0.042) | ||

| ID | 0.202 | −0.071 | |

| (0.126) | (0.110) | ||

| SOE | 0.008 | 0.069 *** | |

| (0.015) | (0.014) | ||

| _cons | 0.678 *** | −6.158 *** | −6.973 *** |

| (0.007) | (0.147) | (0.137) | |

| Ind | No | No | Yes |

| Year | No | No | Yes |

| N | 23,002 | 23,002 | 23,002 |

| R * | 0.005 | 0.159 | 0.343 |

| Financial Constraint | Institutional Ownership | Analyst Coverage | State Ownership | |

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| Green | Green | Green | Green | |

| IS | 0.087 *** | 0.131 *** | 0.098 *** | 0.085 *** |

| (0.016) | (0.017) | (0.017) | (0.019) | |

| IS × FC | 0.285 *** | |||

| (0.059) | ||||

| IS × IO | 0.117 ** | |||

| (0.058) | ||||

| IS × AC | 0.029 ** | |||

| (0.013) | ||||

| IS × SOE | 0.121 *** | |||

| (0.030) | ||||

| Size | 0.332 *** | 0.345 *** | 0.305 *** | 0.342 *** |

| (0.006) | (0.006) | (0.007) | (0.006) | |

| Age | −0.041 *** | −0.112 *** | −0.089 *** | −0.112 *** |

| (0.012) | (0.011) | (0.011) | (0.011) | |

| Lev | 0.157 *** | 0.134 *** | 0.169 *** | 0.134 *** |

| (0.034) | (0.034) | (0.034) | (0.034) | |

| ROA | 0.872 *** | 0.731 *** | 0.370 *** | 0.745 *** |

| (0.105) | (0.105) | (0.107) | (0.105) | |

| Grow | −0.002 | −0.004 | −0.002 | −0.004 |

| (0.010) | (0.010) | (0.010) | (0.010) | |

| Fix | −0.157 *** | −0.131 *** | −0.126 *** | −0.128 *** |

| (0.041) | (0.041) | (0.041) | (0.041) | |

| CF | −0.047 | −0.033 | −0.116 | −0.031 |

| (0.078) | (0.079) | (0.079) | (0.079) | |

| Top | −0.174 *** | −0.128 *** | −0.118 *** | −0.150 *** |

| (0.042) | (0.045) | (0.042) | (0.042) | |

| ID | −0.162 | −0.082 | −0.045 | −0.067 |

| (0.109) | (0.110) | (0.110) | (0.110) | |

| SOE | 0.068 *** | 0.073 *** | 0.080 *** | 0.066 *** |

| (0.014) | (0.014) | (0.014) | (0.014) | |

| FC | 0.400 *** | |||

| (0.032) | ||||

| IO | −0.040 | |||

| (0.028) | ||||

| AC | 0.069 *** | |||

| (0.006) | ||||

| _cons | −5.436 *** | −6.993 *** | −6.348 *** | −6.937 *** |

| (0.163) | (0.140) | (0.151) | (0.137) | |

| Ind | Yes | Yes | Yes | Yes |

| Year | Yes | Yes | Yes | Yes |

| N | 23,002 | 23,002 | 23,002 | 23,002 |

| R * | 0.349 | 0.343 | 0.346 | 0.343 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | |

|---|---|---|---|---|---|---|---|---|---|

| Green | Green | Green | Green | Green | Green | GreenN | GreenI | GreenU | |

| IS | 0.120 *** | 0.125 *** | 0.186 *** | 0.108 *** | 0.027 *** | 0.086 ** | 0.100 ** | 0.148 *** | 0.080 *** |

| (0.022) | (0.023) | (0.017) | (0.016) | (0.009) | (0.039) | (0.044) | (0.011) | (0.015) | |

| Size | 0.342 *** | 0.341 *** | 0.334 *** | 0.334 *** | 0.341 *** | 0.704 *** | 0.790 *** | 0.200 *** | 0.289 *** |

| (0.007) | (0.009) | (0.007) | (0.006) | (0.006) | (0.013) | (0.015) | (0.005) | (0.006) | |

| Age | −0.140 *** | −0.094 *** | −0.149 *** | −0.086 *** | −0.114 *** | −0.339 *** | −0.291 *** | −0.051 *** | −0.100 *** |

| (0.013) | (0.015) | (0.013) | (0.010) | (0.011) | (0.025) | (0.028) | (0.007) | (0.010) | |

| Lev | 0.127 *** | 0.108 ** | 0.166 *** | 0.104 *** | 0.157 *** | 0.243 *** | 0.351 *** | −0.069 *** | 0.190 *** |

| (0.036) | (0.046) | (0.035) | (0.032) | (0.034) | (0.087) | (0.094) | (0.021) | (0.031) | |

| ROA | 0.786 *** | 0.757 *** | 0.948 *** | 0.292 *** | 0.815 *** | 2.222 *** | 2.190 *** | 0.119 * | 0.632 *** |

| (0.109) | (0.148) | (0.125) | (0.102) | (0.105) | (0.296) | (0.326) | (0.063) | (0.097) | |

| Grow | −0.009 | 0.002 | −0.019 * | −0.033 *** | 0.001 | −0.003 | −0.041 | −0.013 ** | −0.002 |

| (0.010) | (0.014) | (0.010) | (0.009) | (0.010) | (0.024) | (0.029) | (0.006) | (0.009) | |

| Fix | −0.107 ** | −0.085 | −0.121 *** | −0.116 *** | −0.163 *** | −0.323 *** | 0.009 | −0.158 *** | −0.051 |

| (0.043) | (0.057) | (0.043) | (0.039) | (0.041) | (0.103) | (0.117) | (0.026) | (0.038) | |

| CF | −0.039 | 0.025 | 0.094 | −0.019 | −0.023 | −0.304 | 0.037 | 0.156 *** | −0.128 * |

| (0.082) | (0.108) | (0.081) | (0.076) | (0.078) | (0.210) | (0.240) | (0.048) | (0.072) | |

| Top | −0.133 *** | −0.132 ** | −0.143 *** | −0.112 *** | −0.138 *** | −0.326 *** | −0.450 *** | −0.072 *** | −0.104 *** |

| (0.044) | (0.059) | (0.043) | (0.040) | (0.042) | (0.095) | (0.105) | (0.028) | (0.038) | |

| ID | −0.074 | 0.032 | 0.067 | −0.067 | −0.018 | −0.611 ** | 0.155 | 0.303 *** | −0.088 |

| (0.116) | (0.153) | (0.118) | (0.104) | (0.110) | (0.239) | (0.257) | (0.075) | (0.101) | |

| SOE | 0.076 *** | 0.057 *** | 0.069 *** | 0.047 *** | 0.064 *** | 0.161 *** | 0.038 | 0.082 *** | 0.034 *** |

| (0.015) | (0.020) | (0.015) | (0.014) | (0.014) | (0.033) | (0.036) | (0.009) | (0.013) | |

| _cons | −6.886 *** | −7.021 *** | −6.715 *** | −6.860 *** | −6.526 *** | −15.816 *** | −17.520 *** | −4.095 *** | −5.985 *** |

| (0.145) | (0.188) | (0.145) | (0.132) | (0.155) | (0.290) | (0.327) | (0.106) | (0.127) | |

| Ind | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Year | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| N | 20,978 | 12,097 | 21,432 | 23,002 | 23,002 | 23,002 | 23,002 | 23,002 | 23,002 |

| R * | 0.349 | 0.350 | 0.340 | 0.344 | 0.341 | 0.162 | 0.111 | 0.246 | 0.334 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Dong, L.; Zhang, X.; Chen, J. Does Investor Sentiment Drive Corporate Green Innovation: Evidence from China. Sustainability 2024, 16, 3220. https://doi.org/10.3390/su16083220

Dong L, Zhang X, Chen J. Does Investor Sentiment Drive Corporate Green Innovation: Evidence from China. Sustainability. 2024; 16(8):3220. https://doi.org/10.3390/su16083220

Chicago/Turabian StyleDong, Li, Xin Zhang, and Jinlong Chen. 2024. "Does Investor Sentiment Drive Corporate Green Innovation: Evidence from China" Sustainability 16, no. 8: 3220. https://doi.org/10.3390/su16083220

APA StyleDong, L., Zhang, X., & Chen, J. (2024). Does Investor Sentiment Drive Corporate Green Innovation: Evidence from China. Sustainability, 16(8), 3220. https://doi.org/10.3390/su16083220