1. Introduction

ESG has emerged as a significant area of concern in both theoretical and practical circles in recent years. This is particularly evident amidst the uncertainties brought about by the COVID-19 pandemic, climate change, and other related factors. ESG has gradually gained prominence, surpassing the heat surrounding corporate social responsibility (CSR), and has become a “new blue ocean” for academic research. This response addresses numerous societal issues and represents the amalgamation and advancement of the principles of “ethical investment”, “socially responsible investment”, and “sustainable development” spanning the period from the 1950s to the 1990s. Subsequently, significant advancements have been made in the field of ESG, including the development of specialized organizations such as the Climate Disclosure Standards Board (CDSB), Sustainable Development Accounting Board (SASB), Value Reporting Foundation (VRF), and International Sustainable Development Standards Board (ISSB). ESG has emerged as one of the three criteria used by the world community to assess the sustainable development capability of economic organizations. ESG places greater emphasis on the disclosure of non-financial information in comparison to CSR. Companies that actively implement ESG principles take into account non-financial metrics alongside financial indicators like profit and growth. These non-financial indicators pertain to the environmental, social, and governance aspects of the company. Consequently, ESG can effectively encourage businesses to invest in the maximization of social value rather than their interests. Current studies on corporate ESG are primarily centered on the financial outcomes of ESG performance, including its influence on corporate performance [

1,

2], managerial behavior [

3], firm value [

4,

5], and stock returns [

6,

7,

8]. Nevertheless, there has been limited scholarly investigation into the impact of the ESG performance of companies within the same industry on target companies.

Enhancing the company’s green innovation potential is of significant importance within the framework of sustainable development. Green innovation refers to the creation of new ideas and technologies that aim to decrease resource usage, minimize pollution, enhance the availability of ecological technology, and encourage the shift towards a sustainable economy and lifestyle [

9]. In contrast to typical innovation behaviors, GTI (green technology innovation) can not only diminish environmental pollution and enhance the company’s environmental governance capabilities but also significantly enhance the company’s fundamental competitiveness [

10], thereby achieving a mutually beneficial outcome of economic growth and environmental protection [

11]. Nevertheless, given the extended duration for returns and the elevated risk associated with GTI, organizations require substantial external assistance to execute GTI initiatives [

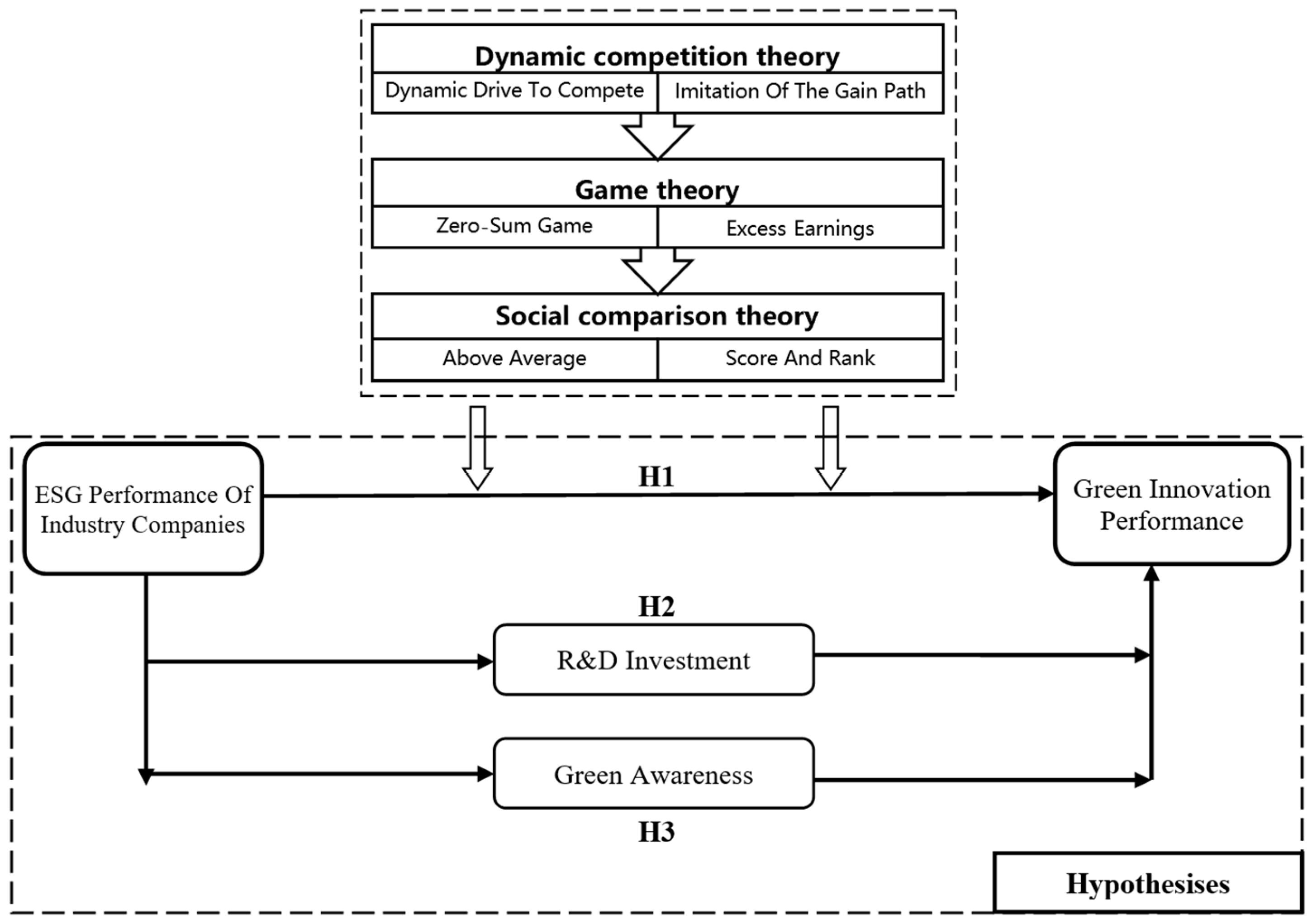

12]. Consequently, it becomes crucial to investigate the elements that influence corporate green innovation. Objectively speaking, there are relationships such as games, comparisons, and competition between companies in the same industry. Therefore, driven by interests, companies in the same industry may generate spillover effects based on the above relationships. On the one hand, there is consistency among companies in the industry in terms of business conditions and corporate characteristics. As a result, the market, social, regulatory, and other pressures faced by the firms will force them to form an atmosphere of mutual imitation. On the other hand, the gaming and competitive relationship of firms in the industry will contribute to the stimulation and radiation of decision making among firms. Therefore, based on the above research gaps, this paper investigates whether the better ESG performance of companies in the same industry will have a spillover effect on the green innovation behavior of target companies. What is the transmission mechanism of this spillover effect? This is the question that needs to be answered in this paper.

This study examines the influence of a company’s ESG performance on its green technology innovation behavior within the same industry. It analyzes the ESG scores and green patent data of A-share listed companies in Shanghai and Shenzhen from 2010 to 2020. The study also investigates how the relationship between ESG performance and green technology innovation varies under different circumstances, such as ownership nature, scale difference, external supervision, industrial pollution, and environmental regulation intensity. In addition, the improvement of ESG performance in the industry primarily promotes the green innovation activities of the target enterprises through an increase in R&D investment and green awareness. The results indicate that the green innovation performance of target companies is positively influenced by the ESG performance of companies in the same industry, with the strongest promotion effect occurring in the environmental dimension (E). Ultimately, this study concludes that the impact of peer enterprises’ ESG performance on corporate green innovation activities is particularly pronounced in non-state-owned enterprises, small enterprises, enterprises with higher levels of external attention, enterprises in non-highly polluting industries, and enterprises subject to stronger external environmental supervision.

The primary incremental contributions of this study are as follows. Firstly, it broadens the existing studies on the spillover impact of corporate ESG conduct. This paper takes a different approach compared to previous research by examining the spillover effect of a company’s ESG behavior, analyzing the decision-making relevance among companies in a group, and investigating the influence mechanism of corporate ESG performance on GTI through R&D investment and green awareness. It rectifies the deficiencies of the current research and broadens the scope of investigation regarding the “theoretical black box” associated with the organization’s GTI. Secondly, it enhances the existing literature on the company’s green innovation behavior by examining the correlation between ESG performance and the company’s green innovation performance through theoretical research. The majority of the current research concentrates on analyzing the influence of political capital [

13], legitimacy pressure, and corporate profitability [

14] on the performance of green innovation. This study examines the “ESG performance of companies in the same industry—green innovation behavior” topic, contributing to the research on the factors that influence companies’ GTI behavior from a macro industry perspective in the context of “dual carbon”. Thirdly, this paper examines the practical aspect by analyzing the variation in ESG performance among firms within the same industry. Specifically, it explores how distinct company attributes—including ownership, size, analyst focus, and environmental regulation intensity—impact the ability of firms to innovate green technology. It offers more precise recommendations for achieving the “dual carbon” objective. This paper contributes to the existing theoretical research on the spillover effect of ESG performance of listed companies within the same industry and offers empirical evidence supporting the role of ESG behavior in promoting green innovation output.

The remaining sections of this paper are organized as follows.

Section 2 presents a literature review;

Section 3 offers a literature review and research hypotheses;

Section 4 describes the research methodology, encompassing models, variables, and data;

Section 5 conducts an analysis of empirical results, including benchmark regression, the robustness test, mediating effect regression, and heterogeneous effect regression;

Section 6 gives the article’s conclusion along with some suggestions.

4. Research Design

4.1. Data Collection and Data Sources

This study focuses on publicly traded businesses in the Shanghai and Shenzhen stock exchanges, namely those listed on the A-share market, throughout the period from 2011 to 2020. A total of 27,725 samples were collected for research purposes. The following measures were taken to process the data to ensure the correctness and reliability of the study findings in this publication:

Since the accounting standards of financial companies are different from those of general companies, the sample of financial companies is excluded.

Since there are anomalies in the data of some companies, the sample of companies with missing data is excluded.

When listed companies in China have behaviors of non-compliance and continuous losses, these companies are labeled with symbols such as ST, *ST, and so on. In order to enhance the reliability of the study’s conclusions, these abnormal company samples are excluded.

All continuous variables were winsorized at the 1% and 99% quantile to prevent the impact of extreme values.

ESG performance data from Bloomberg’s ESG disclosure score were utilized in this study to generate rating findings. Additionally, green patent data and other financial information were sourced from the CSMAR database. Furthermore, Stata software (version 17.0) was employed in this work for the purpose of data analysis and processing.

4.2. Data Collection and Data Sources

4.2.1. Dependent Variable: Green Innovation Activity (PAT)

The process of innovation is intricate. The potential for innovation was assessed using three indicators employed in this study to gauge a company’s green innovation behavior. The quality of green innovation patents (PAT_QUA) was determined by taking the natural logarithm of the combined number of citations received by green invention patents, utility model patents, and design patents of listed enterprises in the T year and then adding 1 to the result. The number of green innovation patents (PAT_NUM) was calculated as the natural logarithm of the number of green invention patents awarded by the listed company in the T year, increased by 1. The green innovation activity (PAT) was quantified as the logarithm of the sum of the quality (PAT_QUA) and quantity (PAT_NUM) of green innovation, increased by 1.

4.2.2. Independent Variable: Average ESG Score of The Same Industry (ESG_SCORE)

The ESG rating published in the Bloomberg database was used in this study as a proxy variable for assessing the ESG performance of SG. The Bloomberg ESG disclosure score comprises sub-dimension scores for environmental (E), social (S), and governance (G) factors, ranging from 0 to 100. Higher scores indicate superior ESG performance. More precisely, the average ESG rating of other firms in the same industry (ESG_SCORE) obtained from the Bloomberg database, excluding our own company, was used in this study as the explanatory variable.

4.2.3. Intermediary Variable: R&D Investment (Inv), Green Awareness (Green)

The data on the company’s R&D investment and green awareness were obtained from the CSMAR database. Existing literature and R&D costs divided by total assets were utilized in this study to quantify the R&D investment intensity (Inv) of firms. This work assessed corporate green awareness by considering many dimensions and determining the cumulative scores of numerous indicators as a proxy variable for corporate green behavior (Green). Specific dimensions are placed in the

Appendix A.

4.2.4. Control Variables

A series of economic characteristic indicators were chosen in this study as control variables to account for other factors that may influence the company’s green innovation based on the available research literature. The aim of this study was to analyze and regulate various financial and governance characteristics of a company, including its size (Size), asset/liability ratio (Lev), return on total assets (ROA), growth rate of main business income (Growth), size of the board of directors (Boardsize), size of independent directors (Indepsize), shareholding ratio of the top ten shareholders (Top10), shareholding ratio of the management (Mstock), executive compensation (Mincome), violation (Break), state-owned company (SOE) status, audit complexity (Big10), profit and loss (Loss), and audit risk (AO). Furthermore, the model incorporates year- and industry-fixed effects and accounts for clustering at the business level when adjusting the standard errors.

The specific definitions of the relevant variables are shown in

Table 1.

4.3. Model Specification

Since the explanatory and interpretive variables in this paper are continuous variables and the research data are company-year panel data, this paper adopts the following OLS regression model to empirically test the impact of ESG performance of listed companies on corporate green innovation behavior. Specifically, the research model of this paper is constructed as follows:

To assess the mediation influence of corporate green awareness (Green) and R&D investment (Inv) between ESG performance and corporate green innovation behavior of companies in the same industry, we developed the following model:

PATi,t represents the proxy variable for the company’s green innovation behaviors, namely encompassing green innovation activity, green innovation quality, and green innovation quantity. ESG refers to the environmental, social, and governance performance of companies operating within the same industry. The term “” includes the promotion of environmental consciousness and the allocation of resources towards research and development. The term “” refers to the variable that is used to control or influence the outcome of an experiment or study. The symbol “” represents the industry fixed effect, whereas “” represents the year fixed effect. The variable “” denotes distinct years, while “” represents the random error term. Furthermore, cluster adjustment at the firm level was implemented in this work to mitigate the influence of the aggregation effect on the regression outcomes and ensure the strength and dependability of the study. In the robustness test section, this paper re-runs the regression using two-stage regression (2SLS), lagging the explanatory variables, continuous variables without shrinking tails, fixed-effects modeling, adding more control variables, excluding the effect of public health events, and replacing the explanatory variables and the explained variables, in order to overcome the endogeneity problem of this paper and to enhance the reliability of the results.

6. Conclusions and Implications

6.1. Conclusions and Discussion

This study utilized dynamic competition theory, game theory, social comparison theory, resource base theory, and competitive strategy theory to examine and verify the spillover effects of companies’ ESG performance within the same industry. Additionally, it investigated the impact of these spillover effects on the green innovation performance of target companies. Furthermore, the study explored the mediating role of companies’ R&D investment and green awareness in this relationship. This research further analyzed the green innovation effect of ESG performance on various sub-scores. It also examined the heterogeneity of the green innovation effect of ESG performance from various property rights, sizes, levels of external monitoring, industries, and environmental regulations. The findings of this paper are based on the Chinese institutional context, which provides empirical evidence not only for the Chinese institutional environment on the one hand, but also can provide lessons for other developing countries. The findings of the research are as follows.

Firstly, the benchmark regression findings of this research (

Table 3) indicate that when the ESG performance of publicly traded firms in the same industry improves, the target company will allocate greater attention towards enhancing its own ESG performance due to competitive pressure and above-average incentives. ESG promotes the idea of environmentally friendly conservation and enhances social accountability. Green innovation refers to the company’s efforts to modify its goods, technology, and manufacturing methods with the aim of safeguarding the environment. Hence, in order to enhance ESG performance, the firm should prioritize the advancement of green innovation initiatives and implement tangible measures by committing resources to foster its own green innovation performance.

Secondly, further analysis of this study (

Table 6) reveals that the environmental (E) and social (S) performance of the average level of listed companies in the same industry can have a positive impact on the green innovation performance of the target companies. Notably, the impact of corporate environmental (E) performance is more pronounced and statistically significant in this regard. Nevertheless, the effectiveness of corporate governance (G) has a negative impact on the firm’s green innovation behavior. A company that actively embraces environmental responsibility will enhance its investment in environmental management and innovation in environmental technology. This will not only drive green technology innovation but also confer a competitive edge to the company in the realm of green innovation. Active corporate social responsibility entails the company receiving recognition from stakeholders and gaining a competitive advantage in terms of reputation. It also helps address the issue of information asymmetry with stakeholders and promotes the advancement of green technology research, development, and innovation. When companies take on the duty of stakeholders, the need for environmental management and environmentally friendly technology can directly encourage them to engage in research and development for green innovation. This, in turn, leads to an increased emphasis on and investment in green innovation practices. Once a satisfactory level of corporate governance performance is achieved, managers may develop a myopic inclination, prioritizing management inputs to optimize the organizational structure and enhance the system while being reluctant to allocate additional funds towards green research and development. This hinders the progress of green innovation performance to some extent and diminishes or decelerates green innovation activities.

Thirdly, based on the results of the mediation mechanism test (

Table 7), this study comes to the conclusion that improving a company’s ESG performance makes it easier to share non-financial information with outside stakeholders, evens out the distribution of information, promotes a responsible and positive corporate image, and leads to higher-quality investment from outside the company. Consequently, the firm may acquire additional cash to allocate towards technological research and development. This will facilitate the advancement of green technology and enhance production efficiency, ultimately leading to improved performance in the company’s green innovation output. This creates a positive feedback loop of green innovation called “input–output.” According to the findings of the mediation mechanism test in this study (

Table 8), it can be concluded that in order to enhance their ESG performance and achieve sustainable development, target firms within the same industry should adopt a range of environmentally friendly strategies and integrate green awareness into all aspects of their operations. When the leadership, administration, and workers at all levels of an organization possess a robust understanding and commitment to environmental sustainability, organizations will prioritize internal initiatives for green innovation and actively promote research and development in this area. Consequently, this will lead to enhanced performance in green innovation.

Lastly, according to the analysis of diversity in this research (

Table 9,

Table 10,

Table 11,

Table 12 and

Table 13), it is observed that non-state-owned companies, in comparison to state-owned companies, have weaker connections with the government, encounter more intense competition in the market, experience greater limitations in obtaining financial resources, and possess greater motivations to engage in green technological innovation endeavors with the aim of enhancing their corporate competitiveness. Small firms, in contrast to large firms, have limited internal financial strength and turnover capacity, resulting in weaker external access to green innovation information and resources. Consequently, small firms have a greater need to enhance their ESG performance in order to attract the attention of investment entities and financial institutions. As a result, the impact of ESG performance on green innovation performance is more pronounced for small firms. As the focus from external analysts increases, the firm’s management conduct is subjected to more rigorous scrutiny. This compels the corporation to govern its own behavior and engage in green innovation initiatives more actively. The ESG performance of companies in heavily polluting industries has a lesser impact on the investment enthusiasm of stakeholders, who generally believe that improving environmental performance is the inherent responsibility of such companies. Conversely, the production and operation activities of publicly traded companies in non-heavily polluting industries are more consistent with the principles of green and sustainable development. Consequently, stakeholders are more attentive to the disclosed ESG information pertaining to such companies. Environmental rules have enhanced the oversight and control of local governments in environmental matters, compelling firms to fulfill obligatory environmental criteria solely by means of heightened technical research and development and ongoing green technology innovation.

6.2. Inspiration and Suggestions

In order to encourage the overall improvement of green innovation performance of companies in the same industry, government regulatory agencies should establish and improve the ESG information disclosure system and reward and punishment system to guide companies in various industries to support each other, encourage benign competition, and stimulate the implementation of green innovation behavior. Increased support from government functional departments for businesses with excellent ESG performance is needed. Examples of this support include integrating ESG evaluation into procurement policies and encouraging financial institutions to offer credit support, tax relief, financial subsidies, and other benefits. By assisting businesses in lowering the cost of environmental protection and green innovation, these departments will help the industry perform better overall in terms of green innovation. Businesses should also be encouraged and directed to conform more closely with the ESG standards of the top businesses in the same sector, use the spillover effect’s transmission mechanism to establish a variety of demonstration businesses, use the power of example to persuade other businesses in the same sector to follow suit, fully utilize the spillover effect’s positive incentive role, and support businesses in their ongoing efforts to develop competitive advantages through green innovation. Subsequently, the ecological, sustainable, and low-carbon progress of Chinese enterprises as a whole must be encouraged.

In addition to considering a company’s production and operations, investors should also factor environmental and social responsibility into the evaluation process when selecting investment targets. This will force the company to reorient its green innovation strategy system and fulfill its environmental and social obligations. Investors should keep up with external supervision intelligence and urge companies to prioritize ESG concepts. The amount of money should also be considered to boost long-term investment returns and environmental benefits. Investors and investment institutions should raise their own awareness of ESG issues when making investments and push businesses to implement green innovation, inspiring a variety of market participants to get involved in the development of green, low-carbon, and recycling projects.

Companies should create ESG and green innovation strategies, incorporate green ESG concepts into their daily operations, company strategies, and culture, and apply these concepts to management systems at all levels. This is especially important for listed businesses in high-pollution industries and those with less external oversight. Additionally, businesses should pay more attention to the development of ESG, raise awareness of their obligations under ESG, and encourage the methodical advancement of green innovation. Businesses should also improve their corporate governance, make ESG and green innovation decisions that are more scientific and logical, invest more in management and R&D, and set aside a range of resources, such as money and people, for related activities. They could look at the number of patents on green innovation and the ESG practices of companies in the same industry and figure out how to make more ethical and environmentally friendly decisions. This would help businesses quickly adjust to changing environmental conditions, forge hard-to-replicate competitive advantages, and start down the path of long-term, excellent green development.

6.3. Research Limitations and Future Prospects

This paper innovatively investigates the spillover effect of ESG performance of companies in the same industry based on the data of Chinese listed companies. However, the study still has the following limitations. On the one hand, the ESG performance of listed companies is made by third-party intermediaries. Therefore, the ESG performance made by different organizations is divergent, and whether this divergence affects the results of this paper is yet to be tested. In the future, we can focus on the role of ESG divergence in spillover effects. On the other hand, the research data in this paper are based on the Chinese institutional context. Therefore, whether the conclusions of this paper hold in developed countries is yet to be tested. Therefore, future research can be conducted based on the data of listed companies in Europe, the United States, and other regions to verify the generalizability of this paper’s conclusions.

{kind=link}