Nonlinear Impact of Corporate Financialization on Sustainable Development Ability: Evidence from Listed Companies in China

Abstract

1. Introduction

2. Theoretical Analysis and Hypothesis Proposal

2.1. Corporate Sustainable Development

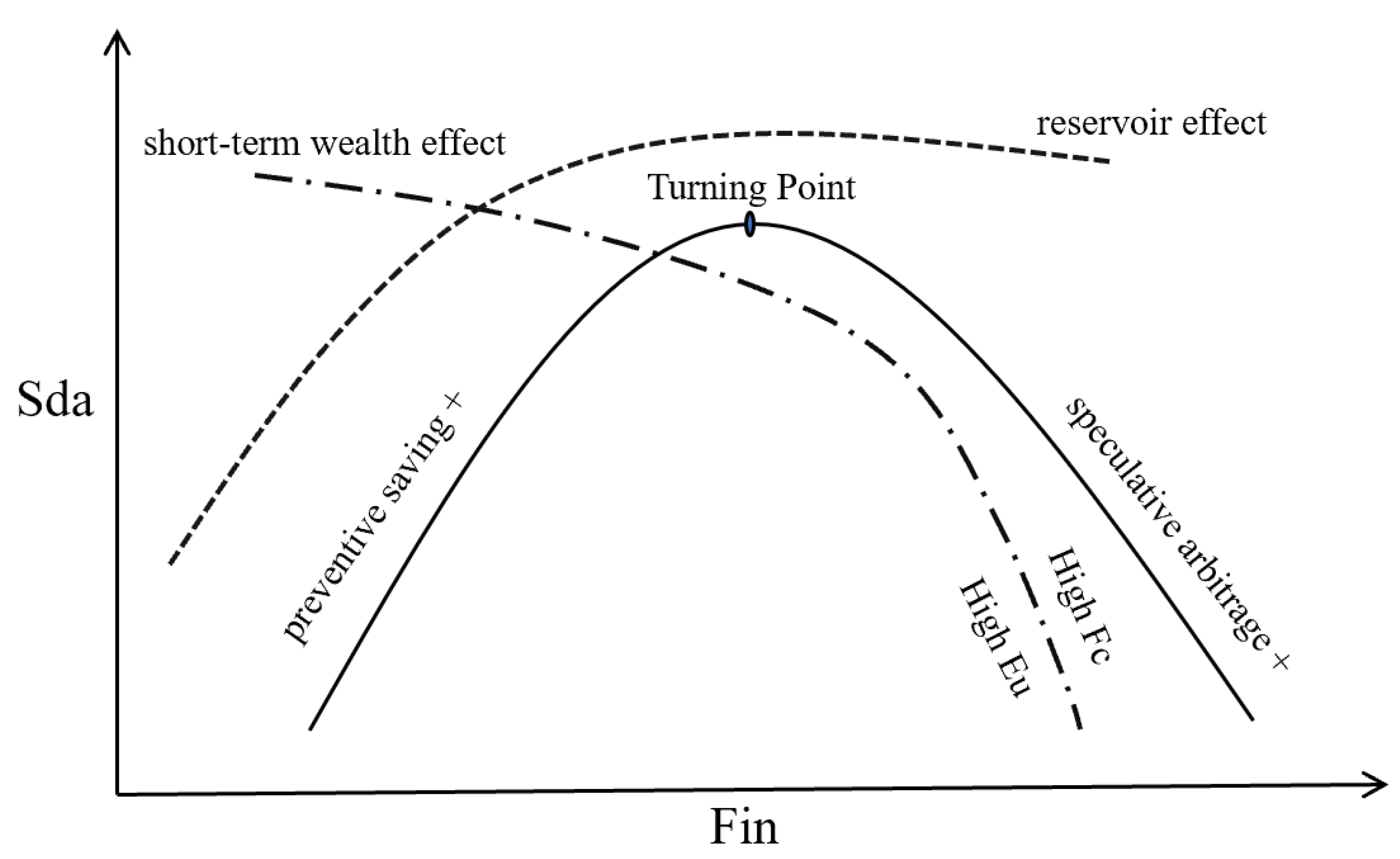

2.2. Corporate Financialization and Sustainable Development Ability

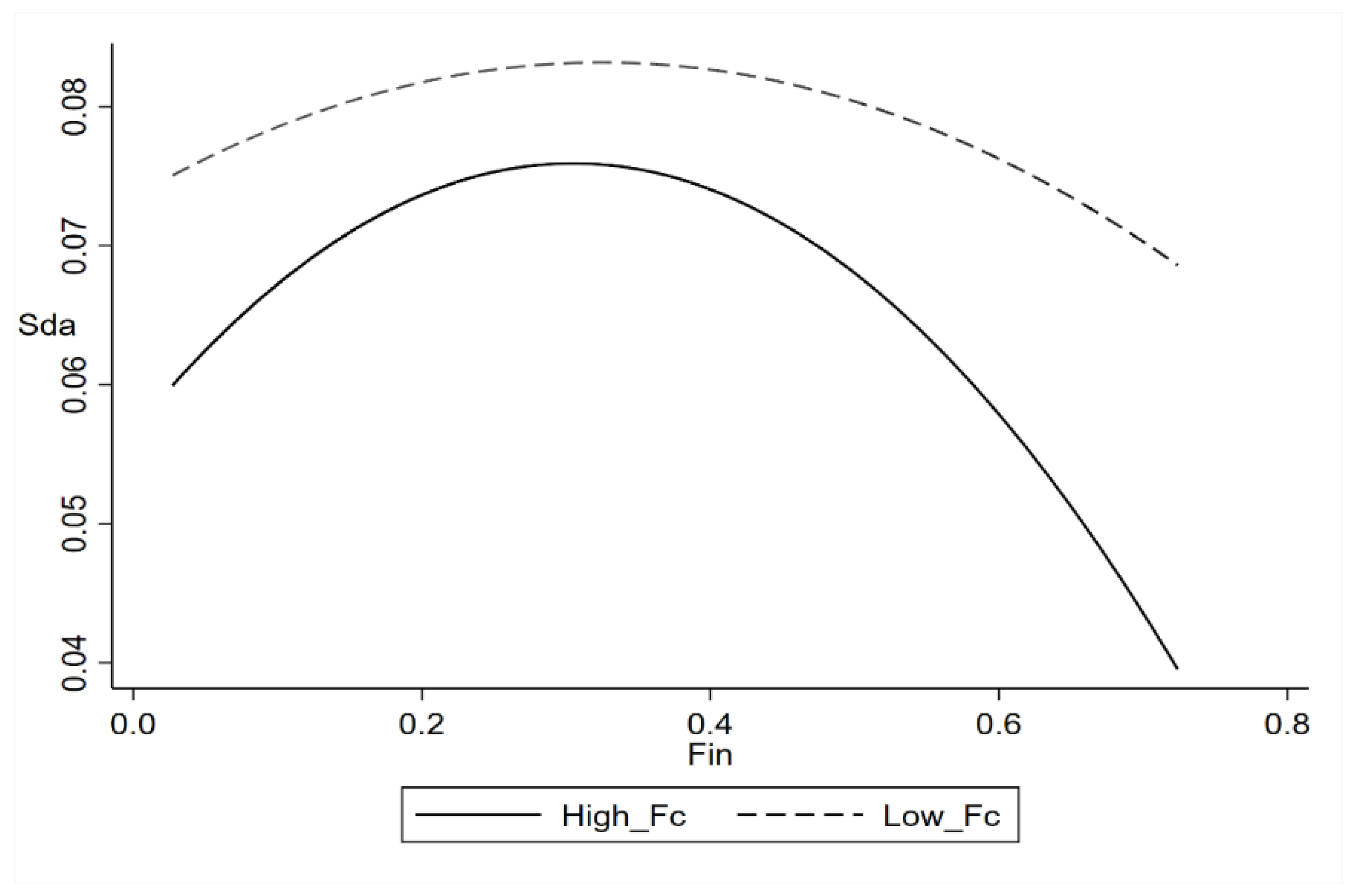

2.3. The Moderating Role of Financing Constraints

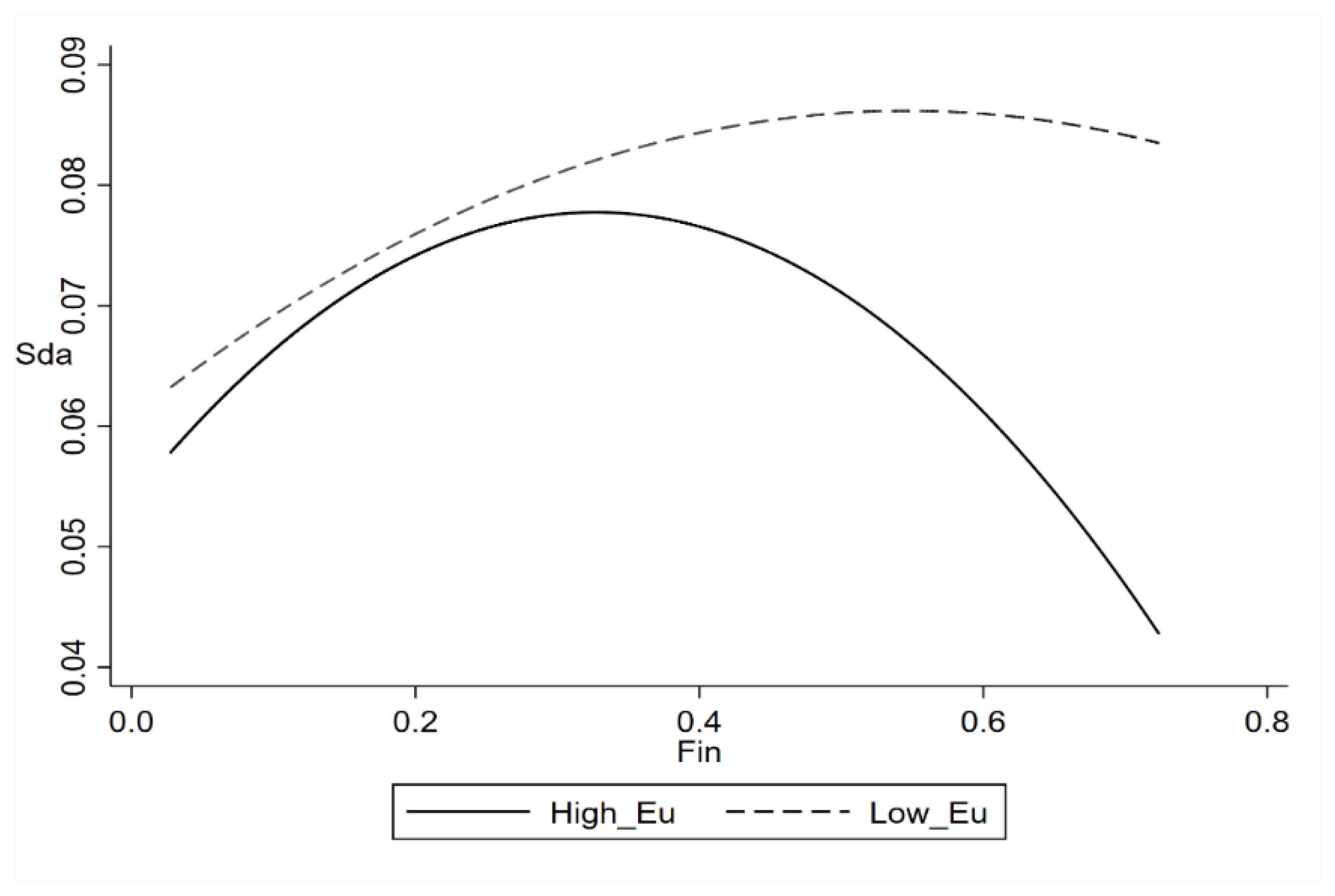

2.4. The Moderating Role of Environmental Uncertainty

3. Study Design

3.1. Sample Selection and Data Sources

3.2. Variable Selection and Description

3.2.1. Dependent Variable

3.2.2. Independent Variable

3.2.3. Moderating Variables

3.2.4. Control Variables

3.3. Model Design

4. Empirical Test for Hypothesis 1

4.1. Descriptive Statistics and Correlations

4.2. Empirical Results

4.3. Robustness Test

4.3.1. Replacing Dependent Variable

4.3.2. Replacing Independent Variable

4.3.3. Sub-Sample Regression

4.3.4. Addressing Endogeneity

5. Moderating Effects

5.1. Nonlinear Moderating Effect Test

5.2. Results and Analysis

6. Further Study

6.1. Transmission Mechanism Analysis

6.2. Heterogeneity Analysis of the Term Structure

7. Conclusions and Recommendations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Liao, Y.; Qiu, X.; Wu, A.; Sun, Q.; Shen, H.; Li, P. Assessing the impact of green innovation on corporate sustainable development. Front. Energy Res. 2022, 9, 800848. [Google Scholar] [CrossRef]

- Demir, F. Financial liberalization, private investment and portfolio choice: Financialization of real sectors in emerging markets. J. Dev. Econ. 2009, 88, 314–324. [Google Scholar] [CrossRef]

- Gong, C.M.; Gong, P.; Jiang, M. Corporate financialization and investment efficiency: Evidence from China. Pac. Basin Financ. J. 2023, 79, 102045. [Google Scholar] [CrossRef]

- Jin, X.M.; Mai, Y.; Cheung, A.W.K. Corporate financialization and fixed investment rate: Evidence from China. Financ. Res. Lett. 2022, 48, 102898. [Google Scholar] [CrossRef]

- Yu, W.; Zhan, Q.; Ameer, W.; Li, L.; Tarczyński, W.; Mentel, U. Effects of Heterogeneity of Financialization on Firm Innovation: Evidence in Context of Energy Transition in Lens of Research and Development. Front. Energy Res. 2022, 10, 930974. [Google Scholar] [CrossRef]

- Xie, Z.; Du, J.; Wu, Y. Does financialization of non-financial corporations promote the persistence of innovation: Evidence from A-share listed manufacturing corporations in China. Eurasian Bus. Rev. 2022, 12, 229–250. [Google Scholar] [CrossRef]

- Liu, L.; He, J. Does financialization affect firm’R&D investment? Evidence from China. Financ. Res. Lett. 2023, 58, 104311. [Google Scholar]

- Lin, Z.; Li, S. Financialization, Earnings Management and Investment Efficiency. In Proceedings of the Fourteenth International Conference on Management Science and Engineering Management: Volume 1, Chisinau, Moldova, 30 July–2 August 2020; Springer International Publishing: Berlin/Heidelberg, Germany, 2020; pp. 130–141. [Google Scholar]

- Wang, H.; Wang, Q.; Sheng, X. Does corporate financialization have a non-linear impact on sustainable total factor productivity? Perspectives of cash holdings and technical innovation. Sustainability 2021, 13, 2533. [Google Scholar] [CrossRef]

- Lyu, Y.; Zhang, J.; Qing, X.; Bai, Y. The influence of non-financial enterprises’ financialization on total factor productivity of enterprises: Promotion or inhibition? Int. J. Financ. Econ. 2023, 1, 15. [Google Scholar] [CrossRef]

- Tori, D.; Onaran, Ö. Financialization, financial development and investment. Evidence from European non-financial corporations. Soc. Econ. Rev. 2020, 18, 681–718. [Google Scholar] [CrossRef]

- Leng, T.; Liu, Y.; Xiao, Y.; Hou, C. Does firm financialization affect optimal real investment decisions? Evidence from China. Pac. Basin Financ. J. 2023, 79, 101970. [Google Scholar] [CrossRef]

- Xu, S.; Guo, L. Financialization and corporate performance in China: Promotion or inhibition? Abacus 2023, 59, 776–817. [Google Scholar] [CrossRef]

- Deng, M.; Fang, X.; Lyu, Q.; Luo, W. How does corporate financialization affect operational risk? Evidence from Chinese listed companies. Econ. Res. Ekon. Istraživanja 2023, 1–21. [Google Scholar] [CrossRef]

- Zhang, S.; Yin, X.; Xu, L.; Li, Z.; Kong, D. Effect of environmental, social, and governance performance on corporate financialization: Evidence from China. Sustainability 2022, 14, 10712. [Google Scholar] [CrossRef]

- Zhu, G.P.; Gui, H.F.; Peng, T.; Jiang, C.H. Corporate tax avoidance and corporate financialization: The moderating effect of managerial myopia. Manag. Decis. Econ. 2023, 44, 459–472. [Google Scholar] [CrossRef]

- Cupertino, S.; Consolandi, C.; Vercelli, A. Corporate social performance, financialization, and real investment in US manufacturing firms. Sustainability 2019, 11, 1836. [Google Scholar] [CrossRef]

- Orhangazi, Ö. Financialisation and capital accumulation in the non-financial corporate sector: A theoretical and empirical investigation on the US economy: 1973–2003. Camb. Econ. 2008, 32, 863–886. [Google Scholar] [CrossRef]

- Xu, X.; Xuan, C. A study on the motivation of financialization in emerging markets: The case of Chinese nonfinancial corporations. Int. Rev. Econ. Financ. 2021, 72, 606–623. [Google Scholar] [CrossRef]

- Haans, R.F.J.; Pieters, C.; He, Z.L. Thinking about U: Theorizing and testing U-and inverted U-shaped relationships in strategy research. Strateg. Manag. J. 2016, 37, 1177–1195. [Google Scholar] [CrossRef]

- Higgins, R.C. Sustainable growth under inflation. Financ. Manag. 1981, 10, 36–40. [Google Scholar] [CrossRef]

- Schmidheiny, S. Changing Course: A Global Business Perspective on Development and the Environment; MIT Press: Cambridge, MA, USA, 1992. [Google Scholar]

- Dyllick, T.; Hockerts, K. Beyond the business case for corporate sustainability. Bus. Strategy Environ. 2002, 11, 130–141. [Google Scholar] [CrossRef]

- Gao, P.; Wang, X.; Wang, H.; Cheng, C. A correction to the entropy weight coefficient method by Shen et al. for accessing urban sustainability [Cities 42 (2015) 186–194]. Cities 2020, 103, 102742. [Google Scholar] [CrossRef]

- Rehman, M.H.; Chang, V.; Batool, A.; Wah, T.Y. Big data reduction framework for value creation in sustainable enterprises. Int. J. Inf. Manag. 2016, 36, 917–928. [Google Scholar] [CrossRef]

- Anbarasan, P.; Sushil. Stakeholder engagement in sustainable enterprise: Evolving a conceptual framework, and a case study of ITC. Bus. Strategy Environ. 2018, 27, 282–299. [Google Scholar] [CrossRef]

- Boscoianu, M.; Prelipcean, G.; Lupan, M. Innovation enterprise as a vehicle for sustainable development–A general framework for the design of typical strategies based on enterprise systems engineering, dynamic capabilities, and option thinking. J. Clea. Produ. 2018, 172, 3498–3507. [Google Scholar] [CrossRef]

- Wu, L.; Qing, C.; Jin, S. Environmental protection and sustainable development of enterprises in China: The moderating role of media attention. Front. Environ. Sci. 2022, 10, 966479. [Google Scholar] [CrossRef]

- Li, S.; Gao, D.; Hui, X. Corporate governance, agency costs, and corporate sustainable development: A mediating effect analysis. Discret. Dyn. Nat. Soc. 2021, 2021, 5558175. [Google Scholar] [CrossRef]

- Wang, J.; Mao, N. Does financialization of non-financial corporations promote or prohibit corporate risk-taking? Emerg. Mark. Financ. Trade 2022, 58, 1913–1924. [Google Scholar] [CrossRef]

- Baud, C.; Durand, C. Financialization, globalization and the making of profits by leading retailers. Socio-Econ. Rev. 2012, 10, 241–266. [Google Scholar] [CrossRef]

- Xu, M.; Albitar, K.; Li, Z. Does corporate financialization affect EVA? Early evidence from China. Green Financ. 2020, 2, 392–408. [Google Scholar] [CrossRef]

- Arcand, J.L.; Berkes, E.; Panizza, U. Too much finance? J. Econ. Growth 2015, 20, 105–148. [Google Scholar] [CrossRef]

- Tori, D.; Onaran, O. The effects of financialization on investment: Evidence from firm-level data for the UK. Camb. J. Econ. 2018, 42, 1393–1416. [Google Scholar] [CrossRef]

- Clarke, T. The impact of financialisation on international corporate governance: The role of agency theory and maximising shareholder value. Law Financ. Mark. Rev. 2014, 8, 39–51. [Google Scholar] [CrossRef]

- Su, K.; Liu, H. Financialization of manufacturing companies and corporate innovation: Lessons from an emerging economy. Manag. Decis. Econ. 2021, 42, 863–875. [Google Scholar] [CrossRef]

- Wang, J.; Zhu, Z.; Huang, X. Stock bubbles under sudden public crises: A perspective from the excessive financialization of firms. Financ. Res. Lett. 2023, 57, 104189. [Google Scholar] [CrossRef]

- Yan, X.; Wang, X.; Liu, S. A U-shaped relationship between real financialization and financial risk: Evidence from a single threshold model. Financ. Res. Lett. 2023, 56, 104017. [Google Scholar] [CrossRef]

- Ayyagari, M.; Demirgüç-Kunt, A.; Maksimovic, V. How important are financing constraints? The role of finance in the business environment. World Bank Econ. Rev. 2008, 22, 483–516. [Google Scholar] [CrossRef]

- Campello, M.; Graham, J.R.; Harvey, C.R. The real effects of financial constraints: Evidence from a financial crisis. J. Financ. Econ. 2010, 97, 470–487. [Google Scholar] [CrossRef]

- Deng, L.; Zhao, Y. Investment lag, financially constraints and company value—Evidence from China. Emerg. Mark. Financ. Trade 2022, 58, 3034–3047. [Google Scholar] [CrossRef]

- Tadesse, S. Financial architecture and economic performance: International evidence. J. Financ. Intermediation 2002, 11, 429–454. [Google Scholar] [CrossRef]

- Aalbers, M. The Financialization of Home and the Mortgage Market Crisis. Compet. Change 2008, 12, 148–166. [Google Scholar]

- Han, X.; Hsu, S.; Li, J.; An, R. Economic policy uncertainty, non-financial enterprises’ shadow banking activities and stock price crash risk. Emerg. Mark. Rev. 2023, 54, 101003. [Google Scholar] [CrossRef]

- Tao, L.; Chen, L.; Li, K. Corporate financialization, financing constraints, and environmental investment. Sustainability 2021, 13, 14040. [Google Scholar] [CrossRef]

- Broome, T.; Moore, W.; Alleyne, P. Financing constraints and the R&D decision in the Caribbean. Entrep. Reg. Dev. 2018, 30, 964–986. [Google Scholar]

- Haider, Z.A.; Liu, M.; Wang, Y.; Zhang, Y. Government ownership, financial constraint, corruption, and corporate performance: International evidence. J. Int. Financ. Mark. Inst. Money 2018, 53, 76–93. [Google Scholar] [CrossRef]

- Uzkurt, C.; Kumar, R.; Kimzan, H.S.; Sert, H. The impact of environmental uncertainty dimensions on organisational innovativeness: An empirical study on SMEs. Int. J. Innov. Manag. 2012, 16, 1–23. [Google Scholar] [CrossRef]

- Tversky, A.; Kahneman, D. Advances in prospect theory: Cumulative representation of uncertainty. J. Risk Uncertain. 1992, 5, 297–323. [Google Scholar] [CrossRef]

- Su, Z.; Xie, E.; Peng, J. Impacts of environmental uncertainty and firms’ capabilities on R&D investment: Evidence from China. Innovation 2010, 12, 269–282. [Google Scholar]

- Van Vo, L.; Le, H.T.T. Strategic growth option, uncertainty, and R&D investment. Int. Rev. Financ. Anal. 2017, 51, 16–24. [Google Scholar]

- Zhang, Y.; Zhuo, C.; Deng, F. Policy uncertainty, financialization and enterprise technological innovation: A way forward towards economic development. Front. Environ. Sci. 2022, 10, 905505. [Google Scholar] [CrossRef]

- Barraza, S.; Civelli, A. Economic policy uncertainty and the supply of business loans. J. Bank. Financ. 2020, 121, 105983. [Google Scholar] [CrossRef]

- Waisman, M.; Ye, P.; Zhu, Y. The effect of political uncertainty on the cost of corporate debt. J. Financ. Stab. 2015, 16, 106–117. [Google Scholar] [CrossRef]

- Younge, K.A.; Tong, T.W. Competitive pressure on the rate and scope of innovation. J. Econ. Behav. Organ. 2018, 150, 162–181. [Google Scholar] [CrossRef]

- Fonseka, M.M.; Ramos, C.G.; Tian, G. The most appropriate sustainable growth rate model for managers and researchers. J. Appl. Bus. Res. (JABR) 2012, 28, 481–500. [Google Scholar] [CrossRef]

- Wen, H.; Jiang, L. The challenges of maturity mismatch in investment and financing for sustainable development of carbon-intensive enterprises. Environ. Sci. Pollut. Res. 2023, 30, 99541–99560. [Google Scholar] [CrossRef] [PubMed]

- Zhang, C.; Zheng, N. Monetary policy and financial investments of nonfinancial firms: New evidence from China. China Econ. Rev. 2020, 60, 101420. [Google Scholar] [CrossRef]

- Gao, Y.; Wang, Z.; Wang, K.; Zhang, R.; Lu, Y. Effect of big data on enterprise financialization: Evidence from China’s SMEs. Technol. Soc. 2023, 75, 102351. [Google Scholar] [CrossRef]

- Kaplan, S.N.; Zingales, L. Do investment-cash flow sensitivities provide useful measures of financing constraints. Q. J. Econ. 1997, 112, 169–215. [Google Scholar] [CrossRef]

- Bai, X.; Han, J.; Ma, Y.; Zhang, W. ESG performance, institutional investors’ preference and financing constraints: Empirical evidence from China. Borsa Istanb. Rev. 2022, 22, S157–S168. [Google Scholar] [CrossRef]

- Ghosh, D.; Olsen, L. Environmental uncertainty and managers’ use of discretionary accruals. Account. Organ. Soc. 2009, 34, 188–205. [Google Scholar] [CrossRef]

- Li, K.; Xia, B.; Chen, Y.; Ding, N.; Wang, J. Environmental uncertainty, financing constraints and corporate investment: Evidence from China. Pac. Basin Financ. J. 2021, 70, 101665. [Google Scholar] [CrossRef]

- Lind, J.T.; Mehlum, H. With or without U? The appropriate test for a U-shaped relationship. Oxf. Bull. Econ. Stat. 2010, 72, 109–118. [Google Scholar] [CrossRef]

- Chen, Y.; Sun, R. Corporate financialization and the long-term use of short-term debt: Evidence from China. Finance Res. Lett. 2023, 58, 104602. [Google Scholar] [CrossRef]

- Lewbel, A. Constructing instruments for regressions with measurement error when no additional data are available, with an application to patents and R&D. Econometric 1997, 65, 1201–1213. [Google Scholar]

- Jin, G.; Yu, B.; Shen, K. Domestic trade and energy productivity in China: An inverted U-shaped relationship. Energy Econ. 2021, 97, 105234. [Google Scholar] [CrossRef]

- Zhao, Y.; Su, K. Economic policy uncertainty and corporate financialization: Evidence from China. Int. Rev. Financ. Anal. 2022, 82, 102182. [Google Scholar] [CrossRef]

- Yang, F.; Li, X. Corporate Financialization, ESG Performance and Sustainability Development: Evidence from Chinese-Listed Companies. Sustainability 2023, 15, 2978. [Google Scholar] [CrossRef]

- Zhang, Y.; Zhang, H.; Yang, L.; Xu, P. Managerial ownership and corporate financialization. Financ. Res. Lett. 2023, 58, 104682. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Type | Name | Symbol | Definition |

|---|---|---|---|

| Dependent Variable | Sustainable Development Ability | Sda | Net profit margin on sales × retention ratio × (1 + equity ratio) ÷ [1/turnover of total capital − net profit margin on sales × retention ratio × (1 + equity ratio)] |

| Independent Variable | Corporate Financialization | Fin | Financial assets/total assets |

| Moderating Variables | Financing Constraint | Fc | Dummy variable of financing constraint degree |

| Environmental Uncertainty | Eu | Dummy variables of environmental uncertainty after industry adjustment | |

| Control Variables | Corporate Size | Size | Ln (total assets) |

| Corporate Age | Age | Ln (current year − establishment year + 1) | |

| Corporate Growth | Growth | Increase rate of main business revenue | |

| Ownership Concentration | Shrcr | Percentage of shares held by the top ten shareholders | |

| Executive Compensation | Pay | Sum of top three executives’ compensation/total executive compensation | |

| Asset–Liability Ratio | Lev | Total liabilities/total assets | |

| Management Expense Ratio | Expen | Management expense/operating revenue |

| Variable | N | Mean | SD | Median | Min | Max |

|---|---|---|---|---|---|---|

| Sda | 13,278 | 0.0714 | 0.0648 | 0.0551 | −0.0177 | 0.3440 |

| Fin | 13,278 | 0.2270 | 0.1492 | 0.1871 | 0.0272 | 0.7239 |

| Age | 13,278 | 2.8532 | 0.3746 | 2.9444 | 1.6094 | 3.4657 |

| Size | 13,278 | 22.5584 | 1.3198 | 22.3896 | 20.2088 | 26.4828 |

| Lev | 13,278 | 0.4223 | 0.1921 | 0.4258 | 0.0505 | 0.8254 |

| Shrcr | 13,278 | 56.8325 | 15.3193 | 56.9531 | 23.6761 | 90.5819 |

| Growth | 13,278 | 0.1778 | 0.3144 | 0.1220 | −0.3799 | 1.8956 |

| Expen | 13,278 | 0.0819 | 0.0583 | 0.0688 | 0.0079 | 0.3206 |

| Pay | 13,278 | 0.4613 | 0.1342 | 0.4413 | 0.2283 | 0.8827 |

| Sda | Fin | Age | Size | Lev | Growth | Expen | Pay | Shrcr | Fc | Eu | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Sda | 1 | ||||||||||

| Fin | 0.021 ** | 1 | |||||||||

| Age | −0.023 *** | −0.148 *** | 1 | ||||||||

| Size | 0.110 *** | −0.283 *** | 0.256 *** | 1 | |||||||

| Lev | 0.096 *** | −0.411 *** | 0.222 *** | 0.526 *** | 1 | ||||||

| Growth | 0.247 *** | 0.006 | −0.122 *** | 0.001 | 0.036 *** | 1 | |||||

| Expen | −0.114 *** | 0.231 *** | −0.177 *** | −0.393 *** | −0.409 *** | −0.066 *** | 1 | ||||

| Pay | 0.01 | 0.098 *** | 0.097 *** | −0.158 *** | −0.097 *** | 0.015 * | −0.009 | 1 | |||

| Shrcr | 0.081 *** | 0.068 *** | −0.245 *** | 0.224 *** | −0.007 | 0.104 *** | −0.103 *** | −0.030 *** | 1 | ||

| Fc | −0.068 *** | −0.325 *** | 0.017 * | 0.089 *** | 0.495 *** | −0.002 | −0.125 *** | −0.048 *** | −0.084 *** | 1 | |

| Eu | 0.0001 | 0.097 *** | −0.156 *** | −0.089 *** | −0.071 *** | 0.217 *** | 0.048 *** | 0.040 *** | 0.103 *** | 0.023 *** | 1 |

| (1) | (2) | (3) | |

|---|---|---|---|

| Sda | Sda | Sda | |

| Fin | 0.1195 *** | 0.1243 *** | 0.1393 *** |

| (5.1587) | (5.4941) | (7.2871) | |

| Fin2 | −0.1735 *** | −0.2105 *** | −0.1998 *** |

| (−5.2530) | (−6.5439) | (−6.7804) | |

| Age | 0.008664 ** | ||

| (2.0172) | |||

| Size | 0.008158 *** | ||

| (5.9861) | |||

| Lev | 0.008474 | ||

| (0.8600) | |||

| Growth | 0.04369 *** | ||

| (12.9853) | |||

| Expen | −0.07555 *** | ||

| (−3.3865) | |||

| Pay | 0.01655 * | ||

| (1.8055) | |||

| Shrcr | 0.00009516 | ||

| (1.3761) | |||

| Year | No | Yes | Yes |

| Industry | No | Yes | Yes |

| _cons | 0.05705 *** | 0.05870 *** | −0.1725 *** |

| (19.1159) | (19.4679) | (−4.8227) | |

| N | 13,278 | 13,278 | 13,278 |

| R2 | 0.006463 | 0.07548 | 0.1568 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| TFP_LP | Sda | Sda | Sda | Sda | Sda | |

| Fin1 | 0.1524 *** | |||||

| (8.3886) | ||||||

| Fin12 | −0.2245 *** | |||||

| (−7.3702) | ||||||

| Fin | 1.9472 *** | 0.1450 *** | 0.1181 *** | |||

| (11.5945) | (5.0103) | (6.4710) | ||||

| Fin2 | −2.4304 *** | −0.2153 *** | −0.1390 *** | |||

| (−7.2129) | (−4.3985) | (−4.6020) | ||||

| L.Fin | 0.1140 *** | 0.1123 *** | ||||

| (5.6932) | (5.5864) | |||||

| L.Fin2 | −0.1585 *** | −0.1478 *** | ||||

| (−5.3447) | (−5.0045) | |||||

| Control Variables | Yes | Yes | Yes | Yes | Yes | Yes |

| Year | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry | Yes | Yes | Yes | Yes | Yes | Yes |

| _cons | −4.3418 *** | −0.1728 *** | −0.2248 *** | −0.1804 *** | −0.1878 *** | −0.1250 *** |

| (−10.8613) | (−4.8757) | (−5.1317) | (−5.7715) | (−5.3377) | (−3.6217) | |

| N | 13,005 | 13,278 | 8463 | 10,960 | 11,529 | 11,529 |

| R2 | 0.8235 | 0.1580 | 0.1614 | 0.1488 | 0.1543 | 0.1261 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Fin | Fin2 | F.Sda | Fin | Fin2 | F.Sda | |

| IV1, the first stage | the second stage | IV2, the first stage | the second stage | |||

| Fin | 0.6661 ** | 0.1394 *** | ||||

| (1.98) | (6.55) | |||||

| Fin2 | −0.9987 * | −0.1800 *** | ||||

| (−1.91) | (−6.63) | |||||

| IV1 | −18.37 *** | −12.005 *** | 14.447 *** | 9.059 *** | ||

| (−4.13) | (−4.77) | (101.50) | (154.80) | |||

| IV2 | 0.3392 *** | 0.1794 *** | −93.936 *** | −47.344 *** | ||

| (8.37) | (6.87) | (−71.88) | (−88.15) | |||

| Control Variables | Yes | Yes | Yes | Yes | Yes | Yes |

| Year | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry | Yes | Yes | Yes | Yes | Yes | Yes |

| N | 12,114 | 12,114 | 12,114 | 12,114 | 12,114 | 12,114 |

| F-statistics | 19.62 | 19.48 | 60.14 | 3190.62 | 3836.73 | 72.88 |

| (1) | (2) | |

|---|---|---|

| Sda | Sda | |

| Fin | 0.05959 * | 0.09315 *** |

| (1.8865) | (3.4749) | |

| Fin2 | −0.09167 ** | −0.08526 * |

| (−2.1724) | (−1.8180) | |

| Fin × Fc | 0.06678 * | |

| (1.7375) | ||

| Fin2 × Fc | −0.1156 ** | |

| (−2.4029) | ||

| Fc | −0.01684 *** | |

| (−6.0913) | ||

| Fin × Eu | 0.05219 * | |

| (1.9147) | ||

| Fin2 × Eu | −0.1370 *** | |

| (−2.6557) | ||

| Eu | −0.006741 *** | |

| (−4.1594) | ||

| Control Variables | Yes | Yes |

| Year | Yes | Yes |

| Industry | Yes | Yes |

| N | 13,278 | 13,278 |

| R2 | 0.1675 | 0.1603 |

| (1) | (2) | (3) | |

|---|---|---|---|

| Sda | Cash | Sda | |

| Cash | 0.3274 *** | ||

| (13.2817) | |||

| Fin | 0.1393 *** | 0.03970 *** | 0.1146 *** |

| (7.2871) | (3.6530) | (6.6053) | |

| Fin2 | −0.1998 *** | −0.1811 *** | |

| (−6.7804) | (−6.9767) | ||

| Control Variables | Yes | Yes | Yes |

| Year | Yes | Yes | Yes |

| Industry | Yes | Yes | Yes |

| _cons | −0.1725 *** | −0.0931 *** | −0.1406 *** |

| (−4.8227) | (−3.0330) | (−4.3742) | |

| N | 13,278 | 13,278 | 13,278 |

| R2 | 0.1568 | 0.1565 | 0.2428 |

| (1) | (2) | (3) | |

|---|---|---|---|

| Sda | Main | Sda | |

| Main | −0.01541 *** | ||

| (−15.1021) | |||

| Fin | 0.1393 *** | 0.1770 ** | 0.1435 *** |

| (7.2871) | (2.0230) | (7.8882) | |

| Fin2 | −0.1998 *** | −0.2021 *** | |

| (−6.7804) | (−7.0539) | ||

| Control Variables | Yes | Yes | Yes |

| Year | Yes | Yes | Yes |

| Industry | Yes | Yes | Yes |

| _cons | −0.1725 *** | −0.2001 | −0.1757 *** |

| (−4.8227) | (−0.9279) | (−5.0216) | |

| N | 13,278 | 13,278 | 13,278 |

| R2 | 0.1568 | 0.08237 | 0.1760 |

| (1) | (2) | |

|---|---|---|

| Sda | Sda | |

| SFin | 0.1603 *** | |

| (7.9224) | ||

| SFin2 | −0.2422 *** | |

| (−6.7947) | ||

| LFin | 0.004137 | |

| (0.0915) | ||

| LFin2 | −0.06461 | |

| (−0.3951) | ||

| Control Variables | Yes | Yes |

| Year | Yes | Yes |

| Industry | Yes | Yes |

| _cons | −0.1743 *** | −0.1551 *** |

| (−4.9279) | (−3.9800) | |

| N | 13,278 | 13,278 |

| R2 | 0.1591 | 0.1495 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, S.; Nie, B.; Huang, X. Nonlinear Impact of Corporate Financialization on Sustainable Development Ability: Evidence from Listed Companies in China. Sustainability 2024, 16, 3402. https://doi.org/10.3390/su16083402

Chen S, Nie B, Huang X. Nonlinear Impact of Corporate Financialization on Sustainable Development Ability: Evidence from Listed Companies in China. Sustainability. 2024; 16(8):3402. https://doi.org/10.3390/su16083402

Chicago/Turabian StyleChen, Shuanglian, Benhuan Nie, and Xiaohua Huang. 2024. "Nonlinear Impact of Corporate Financialization on Sustainable Development Ability: Evidence from Listed Companies in China" Sustainability 16, no. 8: 3402. https://doi.org/10.3390/su16083402

APA StyleChen, S., Nie, B., & Huang, X. (2024). Nonlinear Impact of Corporate Financialization on Sustainable Development Ability: Evidence from Listed Companies in China. Sustainability, 16(8), 3402. https://doi.org/10.3390/su16083402