1. Introduction

Researchers [

1,

2] and policymakers [

3,

4] are becoming more and more interested in sustainable innovation and its connection with organizational performance. Moreover, stakeholders are becoming increasingly aware of sustainability in international business activities. It is, therefore, crucial to develop sustainable innovation to gain access to international marketplaces [

5,

6]. Sustainable innovation can be understood as “innovation that improves sustainability performance, where such performance includes ecological, economic, and social criteria” [

7] (p. 2). Several researchers suggest that sustainable innovation is a basic requirement to enhance international business activities [

8]. However, much remains to be studied about the mechanisms that facilitate and enhance this relationship [

9,

10]. To this regard, Boons

et al. [

7] (p. 2) state that “while there is a considerable amount of knowledge on what drives sustainable innovation at the firm level, we know less about how sustainable innovations can be realized and how win-win business situations can be created for those involved while actually enabling sustainability at the level of production and consumption systems”. Our study addresses this latter issue by analyzing the interaction of Management Accounting and Control Systems (MACS), sustainable innovation, and international performance.

Previous researchers have argued that MACS can influence the success of innovative companies in terms of organizational performance [

11,

12]. MACS can be defined as a “set of procedures and processes that managers use in order to provide valuable information in decision-making, planning, monitoring and evaluating and, ultimately, to ensure the achievement of their goals and the goals of their organizations” [

12] (p. 394). Chenhall and Langfield-Smith [

13] classified the MACS tools as either contemporary or traditional according to the different characteristics and outcomes. Contemporary MACS, such as balanced scorecard or benchmarking, are tools directed to the external environment rather than the internal organization. They not only use financial indicators but also non-financial indicators. These tools offer a comprehensive approach for controlling internal processes (manufacturing, distribution, customer services, delivery,

etc.) within the organizational strategy framework [

13] while traditional MACS, such as cost accounting or budgetary systems, are focused on operative and internal control. Furthermore, the information provided by the latter to implement recently-developed new manufacturing processes is less useful [

13]. This leads us to propose the following research question: “Are MACS one of the organizational mechanisms that facilitate the appropriation of the potential benefits of sustainable innovations in terms of international performance?”

This study aims to extend our understanding on the connection between sustainability practices and organizational performance [

14,

15,

16]. To this end it draws on accounting, sustainability, and innovation literature, and it postulates that only contemporary MACS are likely to moderate the relationship between sustainable innovation and internationalization. The contribution of this paper is two-fold. Firstly, it sheds more light on the underlying mechanisms that explain the relationship between sustainable innovations and organizational performance. Previous literature recognized that the existence of certain contingent factors could explain the somewhat ambiguous link between these two variables [

14]. However, to the best of our knowledge, no study to date has considered MACS a potential moderating variable. Secondly, this study also contributes to control literature by providing empirical evidence on the influence of traditional and contemporary MACS in supporting the success of sustainable production innovations. Despite the fact that the influence of control tools is likely to be different “depending on the degree to which particular strategies are emphasized” [

13] (p. 245), previous studies in control literature fail to consider the specific managerial issues behind sustainable innovation strategies. Furthermore, previous works limited the analysis to a single control tool (e.g., Dunk [

17]) or a specific use of MACS (e.g., Bisbe and Otley [

18] and Lopez-Valeiras

et al. [

19]).

The empirical study was carried out in the Spanish and Portuguese agrifood industry, which ranks in a top position for its contribution to GDP. Food industry is also a strategic sector in both of these countries because of its decisive impact on rural development. Agribusiness has been confronting challenges coming from the increasing awareness of worldwide stakeholders concerning the sustainability of their activities [

5]. In order to address this issue, organizations within this sector need to innovate in production processes from a sustainable point of view. Data were collected through surveys gathered from senior managers of 123 established firms. Respondents were asked to evaluate the degree of development of sustainable innovation in their companies. MACS were measured as an overall technique that comprises four individual control systems widely used in practice (traditional MACS: cost accounting and budget systems; contemporary MACS: balanced scorecard and benchmarking). Internationalization was measured through the presence of the company in international markets. Results suggest that MACS positively moderate the relationship between sustainable production and internationalization only when contemporary tools are implemented. Traditional MACS appear to have no significant moderating effect.

The remainder of this paper is structured as follows. The next section briefly reviews the literature and the subsequent section develops the hypothesis. The methodology section describes the empirical study. The results section shows the findings of the empirical analysis using a structural equation modeling. Finally, theoretical contributions, practical implications, limitations, and insights for future research are presented in the conclusions section.

3. Hypothesis Development

The development of innovations in general or sustainable production processes in particular, does not necessary guarantee a direct impact on organizational performance [

43,

44]. Commercialization has been generally considered as the last key step in the innovation process, and it need to be properly managed [

45]. Therefore, at this point there is a need for managerial tools that allow a firm to better exploit and appropriate the potential benefits from sustainable production [

46]. Specifically, a better understanding on the features, meanings and benefits of the innovative sustainable process is needed. It is also needed to understand the competitive environment [

13].

According to the above discussion, organizations must align their strategies to include aspects related to innovation and marketing capabilities [

47,

48]. Maletič

et al. [

14] argued the potential synergies between sustainable innovation and MACS. From a sustainable innovation perspective, MACS allow the company to identify the stakeholders and their needs, measuring the progress towards organizational goals, and helping managers to “understand the current situation and the key issues they must address” [

14] (p. 186).

In this regard, sustainable production innovations allow firms to follow a differentiation strategy [

26]. Among other strategic priorities, differentiation strategy focuses on offering specialized product features that are valuable for costumers [

26]. To implement these strategies successfully, organizations need to have an accurate vision about the current competitive situation to persuade costumers about the features of the sustainable products [

49]. Nowadays, retailers and costumers demand relevant information on sustainability of products [

50]. This allows organizations to obtain valuable and timely feedback about the evolution of those key features (e.g., customer service or distribution) [

13]. Therefore market orientation becomes a key capability for new product introduction [

51]. Thus, benchmarking may play a significant role in responding to this need by supporting organizational learning. Benchmarking is a contemporary tool that facilitates managers to develop competitive analysis and to evaluate their competitive position in order to know how better satisfy customers. The objective of benchmarking is to learn from the experience of other successful firms. This information facilitates managers to understand what customers value and demand, and present the product/service in a way that addresses the existing gap [

52,

53]. Therefore, benchmarking provides a clear focus for the new product marketing strategies.

Balanced scorecard is a tool connected with benchmarking that provides a balanced focus of financial (e.g., profits and returns) and non-financial indicators (e.g., customer satisfaction or production wastes) [

38] that supports the implementation of differentiation strategies. That is, balanced scorecard is a control tool that operationalizes and translates the strategy to all the agents within the company, providing them with procedures and cues to develop strategic priorities.

Contrarily, traditional MACS, as cost accounting and budgets, are unlikely to support product differentiation strategies [

13]. Those tools are internally oriented and mainly emphasize on controlling costs. Thus, the information that traditional MACS provide does not generally suit the complex and diverse environment that involves a product differentiation strategy [

13]. Therefore, we formulate the following hypothesis:

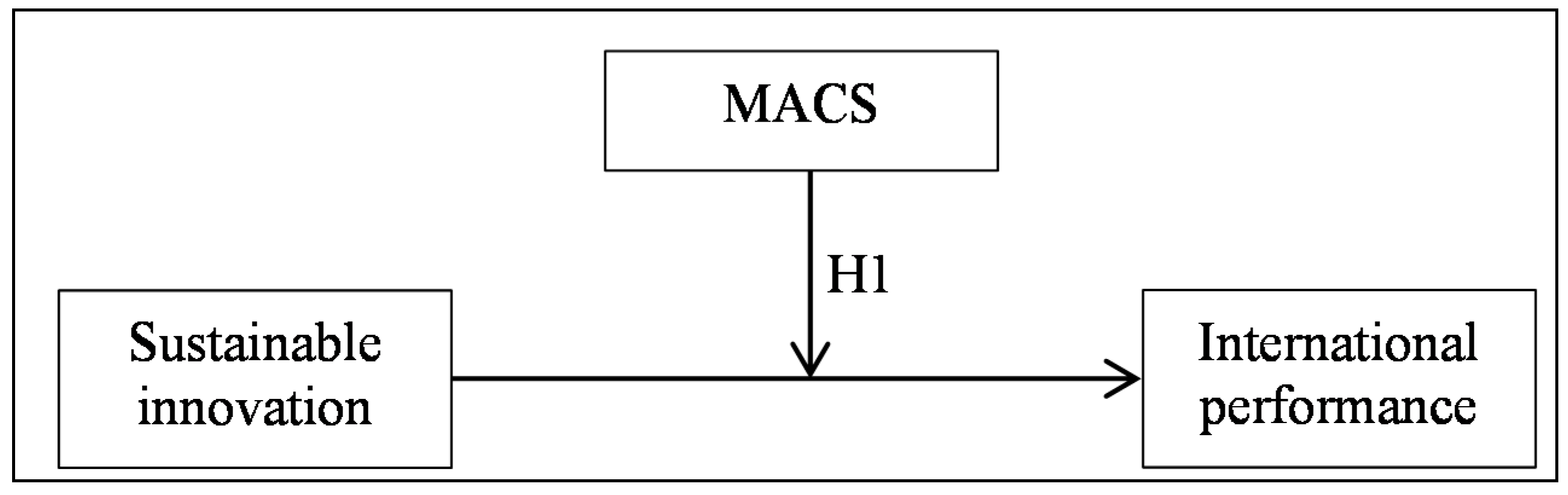

H1:

Contemporary MACS are more likely to have a positive moderator effect than traditional MACS on the relationship between sustainable production innovations and internationalization.

Our research model is displayed in

Figure 1.

Figure 1.

Research model.

Figure 1.

Research model.

5. Empirical Results

We used SmartPLS v.3 software to obtain partial least squares (PLS) estimates for both the measurement and structural parameters. The PLS technique is very suitable for small samples, and it places minimum requirements on measurement levels [

56]. By following Hulland [

57], our PLS model was analyzed in two stages. The first involved the assessment of the reliability and validity of the measurement model and the second involved the assessment of the structural model.

The model of the current research includes multiplicative interaction terms, which are developed following the procedure outlined in Chin

et al. [

58]. With the objective of minimizing the degree of multicollinearity, all items reflecting the predictor and moderator constructs were standardized.

5.1. Measurement Model: Assessing Psychometric Properties

To analyze the measurement model, we used composite scale reliability and average variance extracted (AVE). The composite scale reliability ranged between 0.685 and 0.857. The AVE ranged from 0.510 to 0.752 and thus exceeded the 0.5 cut-off value [

54]. To examine convergent validity, we checked the factor loadings of the measures on their respective constructs.

Table 3 shows the PLS analysis results, which confirmed the proposed constructs. Items were loaded on their respective latent variable at greater than 0.7, except in two cases. One item loading was lower than 0.7 but greater than 0.6, and another one was lower than 0.7 but greater than 0.5, which was acceptable.

Table 3.

Psychometric properties of measures.

Table 3.

Psychometric properties of measures.

| | Standardized Loadings | Composite Reliability | Average Variance Extracted | Cronbach Alpha |

|---|

| Sustainable innovation | | 0.685 | 0.510 | 0.690 |

| SI1. Eco-efficient and biodegradable materials | 0.674 | | | |

| SI2. Reclamation of subproducts and waste | 0.859 | | | |

| SI3. Local biological resources | 0.565 | | | |

| SI4. New equipment | 0.598 | | | |

| Traditional MACS | | 0.857 | 0.752 | 0.707 |

| TMACS1. Cost accounting | 0.766 | | | |

| TMACS2. Budget system | 0.957 | | | |

| Contemporary MACS | | 0.840 | 0.724 | 0.618 |

| CMACS1. Balanced Scorecard | 0.854 | | | |

| CMACS2. Benchmarking | 0.847 | | | |

Discriminant validity was analyzed by comparing the AVE of each construct and the variance shared between such constructs and other constructs in the model.

Table 4 displays the correlations between different constructs in the lower left off-diagonal element of the matrix, and the square root of AVE along the diagonal. The diagonal elements are significantly greater than the off-diagonal elements in the corresponding rows and columns. Results on

Table 4 show support for discriminant validity.

Table 4.

Discriminant validity coefficients.

Table 4.

Discriminant validity coefficients.

| | Sustainable Innovation | Traditional MACS | Contemporary MACS | Internationalization |

|---|

| Sustainable innovation | 0.628 | - | - | - |

| Traditional MACS | 0.395 *** | 0.867 | - | - |

| Contemporary MACS | 0.382 *** | 0.469 *** | 0.851 | - |

| Internationalization | 0.285 *** | 0.346 *** | 0.329 *** | N/A |

5.2. Structural Model

The second step in the PLS analysis is the estimation of the specified structural equations. PLS does not make any assumption about data distribution. Thus, the statistical significance of analyzed paths is examined by non-parametric techniques. We used a bootstrapping procedure with 500 resamples. The structural model was tested in three stages, independently, for traditional and contemporary MACS: (1) Main effect of sustainable innovation on Internationalization; (2) Effect of MACS on Internationalization; and (3) Interaction effect. To determine the exploratory power of the structural model, we analyzed the R-square adjusted values of the dependent variable.

The results in

Table 5 and

Table 6 indicated a significant path between Sustainable innovation and Internationalization (β = 0.285,

p < 0.10). Furthermore, the results supported our hypothesis since there was a positive and significant interaction effect of Contemporary MACS on the relationship between Sustainable innovation and Internationalization (β = 0.193,

p < 0.05). The interaction effect of Traditional MACS on the relationship between Sustainability and Internationalization was not significant.

Table 5.

PLS structural model results: path coefficients and R2. Traditional MACS model.

Table 5.

PLS structural model results: path coefficients and R2. Traditional MACS model.

| Paths | Traditional MACS |

|---|

| | Stage I | Stage II | Stage III |

|---|

| Sustainable innovation → Internationalization | 0.285 * | 0.190 * | 0.164 |

| Traditional MACS → Internationalization | | 0.278 *** | 0.273 *** |

| Sustainable innovation x Traditional MACS → Internationalization | | | 0.127 |

| R2 adjusted | 0.101 | 0.168 | 0.189 |

Table 6.

PLS structural model results: path coefficients and R2. Contemporary MACS model.

Table 6.

PLS structural model results: path coefficients and R2. Contemporary MACS model.

| Paths | Contemporary MACS |

|---|

| | Stage I | Stage II | Stage III |

|---|

| Sustainable innovation → Internationalization | 0.285 * | 0.203 * | 0.188 * |

| Contemporary MACS → Internationalization | | 0.252 *** | 0.205 ** |

| Sustainable innovation x Contemporary MACS → Internationalization | | | 0.193 ** |

| R2 adjusted | 0.101 | 0.170 | 0.199 |

6. Conclusions

The relationship between corporate sustainability and organizational performance has been widely studied in last decades. However, literature reveals inconclusive results and there is still a lack of empirical research on the nature of this relationship. Consistently, with recent calls for in-depth studies in this field [

14,

24,

59], our paper analyzed the relationship between sustainable innovation and international performance at organizational level. It also analyzed the potential interaction of MACS in such relationship. In particular, we postulated that MACS types (contemporary

vs. traditional) have different moderating effects on the relationship between sustainable innovation and international performance. We expected a stronger moderator effect of contemporary MACS than traditional MACS. Our results supported our expectations, by showing a positive moderating effect of Balanced Scorecard and benchmarking controls (

i.e., contemporary MACS).

These findings extend existing management accounting and sustainability literature. Firstly, results are in line with previous research, suggesting that companies that follow differentiation strategies may benefit from the use of contemporary MACS [

13]. Specifically, MACS with similar features of contemporary types of control are able to enhance the impact of innovation developments into organizational performance [

17,

18]. Secondly, from a sustainability perspective, our paper confirms the existence of critical organizational capabilities that may be displayed in order to enhance the impact of sustainable innovations into organizational performance [

7]. In this line, Maletic

et al. [

14] (p. 186) suggested that sustainable innovations should be complemented with “the capability of an organization to measure and manage the interaction among business, society and the environment”. Similarly, Boons

et al. [

7] recommend building a shared project vision and creating broad and reflexive learning processes in order to make successful market introduction. In this line, this paper makes it clear that contemporary MACS play a central role in actively guiding the linkage between sustainable innovation and customer. The use of this tool supports the necessary systemic perspective on marketing [

7] that facilitates the introduction of sustainable innovations into international markets.

This paper has several limitations. Firstly, it used a general conceptualization of sustainable innovation. Future research may use more in-depth conceptualizations that allow the gaining of greater insight about the relationship between sustainable innovations, MACS and organizational performance. As Maletič

et al. [

14] suggested, the exploration

vs. exploitation sustainable innovations paradox should be empirically developed. Furthermore, as with many other studies in management accounting literature, this paper only considered a limited number of MACS tools. This limitation implies that results should be interpreted with care. Future research could analyze empirically the dynamics of MACS in the relationship between sustainable innovation and organizational performance.

{kind=link}