Overview of Current Microgrid Policies, Incentives and Barriers in the European Union, United States and China

Abstract

:1. Introduction

- a cluster of micro sources and loads operating as a single controllable system that provides both power and heat to its local area [2].

- a group of interconnected loads and distributed energy resources within clearly defined electrical boundaries, which act as a single controllable entity with respect to the grid. A microgrid can connect and disconnect from the grid to enable it to operate in both grid-connected and islanded-modes [3].

- a combination of various distributed energy resources, operated in three different categories, namely isolated, islanded, and remote sites, which is capable of balancing captive supply and demand resources to maintain a stable service within defined boundaries [4].

- fossil fuel shortage;

- political instability in the major energy-supplying countries;

- fossil fuel power generation environmental emission which causes global warming; and

- Distributed energy resources technologies development and per unit cost reduction.

2. Microgrid Policies and Regulations

2.1. Europe

2.1.1. Policies and Directives on Renewable Energies in the EU

2013/347/EC “Trans-European Energy Infrastructure”

2009/28/EC “Renewable Energy Directive”

2001/77/EC “Renewable Energy Sources in the Internal Electricity”

2006/32/EC “Energy Efficiency and Energy Service”

2009/72/EC “Rules for Electricity Market”

2004/8/EC “Cogeneration of Energy Market”

2.2. The United States of America (USA)

2.2.1. State Policies to Support Renewable Energies

Energy Policy Act of 2005

Renewable Portfolio Standard

Energy Efficiency Resource Standard

Renewable Energy Standard

2.3. The People’s Republic of China

2.3.1. Renewable Energy Law

- More detailed explanation and clarification is provided for renewable planning and co-ordination with the overall electric power sector development and transmission, and co-ordination between central government and local (provincial) governments on national development plans. In addition, responsibilities and roles of electric utilities are elaborated in reference to grid-interconnection of renewable energy generation and definition of different classes of renewable generators (including small-scale generators with positive net power production). The law revision also addresses areas such as energy storage and smart grids.

- New provision has been made to guarantee that all renewable power generated will be purchased by electric power companies. Previously, utilities were only bound to buy if there was sufficient power demand. This has been strengthened so that utilities must buy the power in all circumstances, and can transfer it to the national grid for use elsewhere.

- The Renewable Energy law 2005 funding component, where the Ministry of Finance collected a 0.4 fen/kWh surcharge on electric power sales nation-wide, was strengthened and consolidated. Originally the fund was utilized in funds that the government used to support renewable energy projects and the costs of feed-in tariffs. However, the surcharge did not kept pace with expenditure, so the revisions allow the Ministry to supplement the renewable energy fund from general revenue.

2.3.2. Medium and Long-Term Development Plan for Renewable Energy in China

- Renewable Energy Law conscientiously implementation.

- Take up renewable energy development as a key strategic measure to attain China’s goal of establishing an environmental friendly society and sustainable development.

- Speed up the development and deployment of renewable energy and distributed generation.

- Technical progress promotion.

- Increase market competitiveness.

- Incessantly boost the share of RE and DG in China’s overall energy mix.

2.3.3. China’s 12th Five-Year Plan for Renewable Energy

- The percentage of renewable energy in energy consumption will significantly increase by 2015. Renewable energy development is key to China achieving its goal of 11.4% of primary energy consumption from non-fossil sources in 2015 and 15% in 2020.

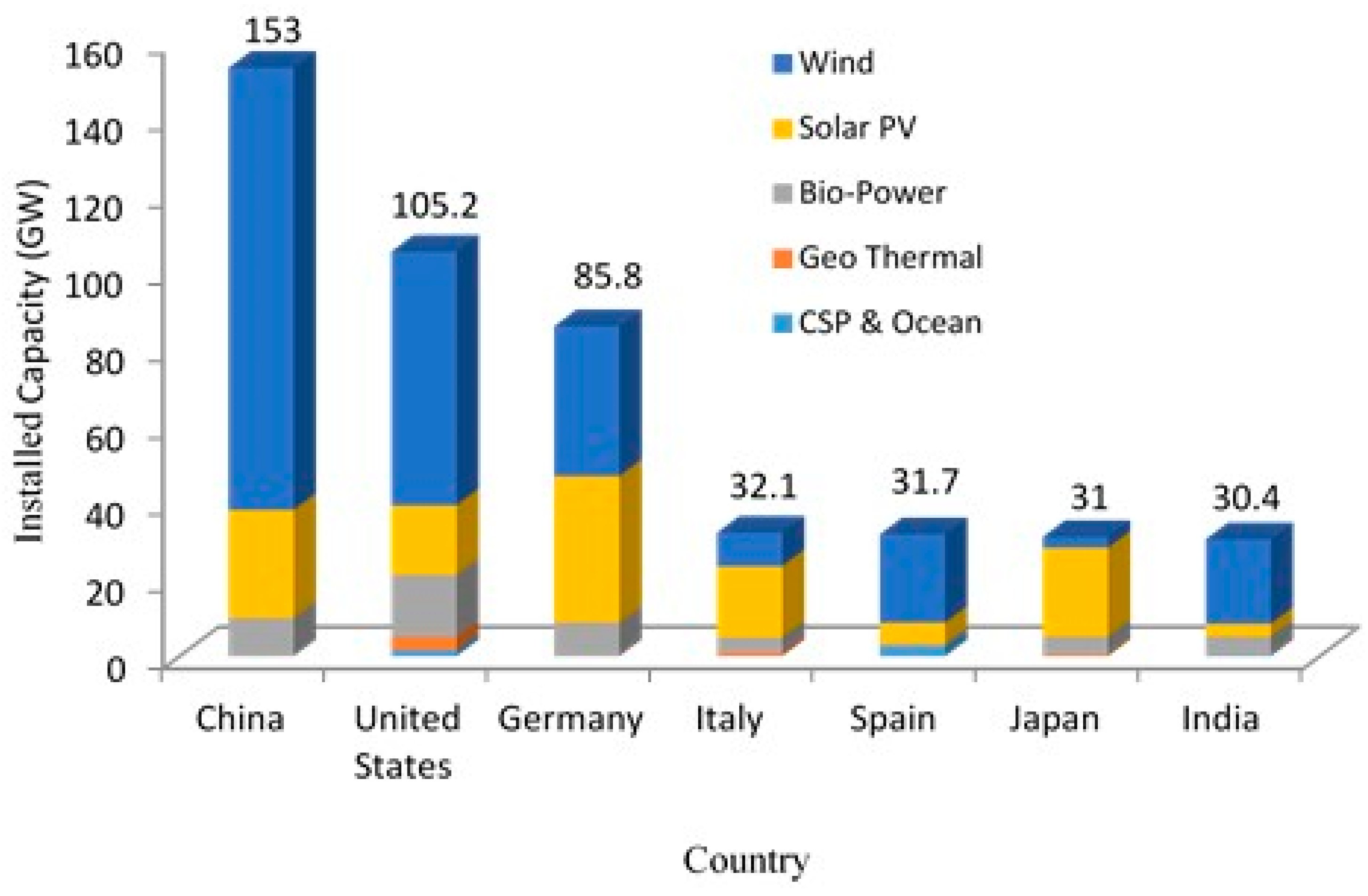

- Electricity generated from renewable energies will be an important source of China’s overall power system. During the 12th Five-Year Plan period, the installed capacity from renewable energy sources will reach 160 GW, including 70 GW from wind, 20 GW from solar PV, 61 GW from hydropower and 7.5 GW from biomass power, which accounts for more than 20% of total electricity generation by 2015.

- Renewable energy and distributed generation applications will be scaled-up. Development and deployment of grid-supporting and management systems in favor of distributed electricity generation such as solar power and wind power systems; installation of 30 new energy micro-grid demonstration projects; integrating diversified renewable energy technologies such as distributed electricity generation (solar power, etc.) and renewable energy for heating and fuel applications. Establishing 100 New-Energy City and 200 Green-Energy pilot projects and take advantage of distributed energy to supply electricity to areas where the grid cannot cover. The energy supplies of more than 50% of rural households will get access to renewable energies such as biogas, solar energy and biomass-gasification.

- Establishing sustainable and stable market demand: Sustainable and stable renewable energy market growth, expansion of renewable energy utilization, technical progress, and development of renewable energy manufacturing industries will be stimulated by means of favorable price policies, and mandated market share (MMS) policies. The MMS policies will be adopted for renewable power generation according to 12th Five Year Plan targets.

- Improve the market environment: According to the China’s Renewable Energy Law (RELaw), state utility companies are bound to purchase renewable power, and energy administrative authorities under the state council are responsible for formulating all regulations for grid connection operation and management of renewable power generation. Also state power grid companies are responsible for deployment of transmission lines for renewable power stations, thereby maximizing renewable energy resource utilization.

- Renewable power tariff and cost-sharing policies: The administrative authorities under the state council are responsible for adjusting feed-in tariff (FIT) as per China’s Renewable Energy Law and to improve the renewable energy price policy system. They will do so based on the different technical and regional characteristics of various renewable energy technologies.

- Increase fiscal input and tax incentives: In accordance with RE Law, the ministry of finance is responsible for arranging renewable energy funds. The scale of the funds will be determined according to the renewable energy development and the financial strength of the country. The state should support the renewable energy and distributed generation R&D and its deployment through preferential tax policies.

- Industry development and technology acceleration: According to the 12th Five Year Plan for education, industry development and renewable energy promotion, cooperation will be enhanced between R&D organization, educational institutions and industries for renewable energy technologies improvement and development, to produce and manufacture indigenous RE equipment and products to achieve the 2020 target, with local man-power.

2.4. Observations

- (i)

- The EU commission must remove any possible ambiguity relating to grid connection and extension and simplify the policy regulations for innovative small and medium-sized enterprises to enable better integration of RES into the utility grid, including cross-border grid connections.

- (ii)

- The USA is in a transition to a clean economy. Renewables such as solar and wind energy in particular are becoming a real part of a distributed generation power system that moves toward grid freedom from a traditional infrastructure of centralized generation. The USA utility grid has 12% renewable energy generation, of which about 10% is hydropower. That is, only about 2% of electricity comes from non-hydro renewable energy sources.A national Renewable Portfolio Standard (RPS) sets a target of 10% renewable energy generation by 2020 and 25% by 2025. This dramatic increase would be an important step toward establishing a low carbon economy and help combat global warming.Reaching the RPS set target requires grid modernization and new transmission, yet how to proceed is a contentious and difficult policy challenge. For example a project called CapX 2020 will add more than 700 miles of new transmission in Minnesota, in order to help meet the RPS. The project is encountering obstacles (including weather conditions), which reveal the difficulties scaled up renewable electricity production is likely to encounter [60,61].According to the Energy Policy Act of 2005 the Secretary of Energy is responsible for designating “any geographic area experiencing electric energy transmission capacity constraints or congestion as a national interest electric transmission corridor (NIETC)”. The law also authorizes the Federal Energy Regulatory Commission to grant permits for interstate transmission lines if a transmission developer is not able to site a line at the state level after a year or under certain other conditions.Recently renewable power generation has been supported by a number of government policies and subsidies. Federal Renewable Energy Production Tax Credit (PTC) and State Renewable Portfolio Standards (RPS) are successful recent support mechanisms. The PTC Renewable Power subsidies were created 22 years ago under the EPAct-1992. The subsidies have been extended many times, and the act was scheduled to expire on 31 December 2013.In the USA, 36 States have developed their individual State RPS and Renewable Energy Standards, for promotion and deployment of RES. The targets of these 36 RPS is to supply about 20% of total power consumed from renewable power by 2020.To avoid significant risks to the reliability of future USA Power Grids, and to achieve real-sustainable energy security and carbon reductions, the Federal Government needs to formulate a National Renewable Energy Policy (NREP) or National Clean Power Standard (CPS) to promote new energy corridors. This is especially important in view of the RPS, the increasing demand of renewables to meet new electricity demand, grid stabilization, transmission and dispatch system expansion and to facilitate renewable electricity grid connection.

- (iii)

- To expand the renewable energy share in its energy mix is a pillar of China’s vision 2020, for future energy security and its GHG reduction strategy. China is planning to inject a further 1000 GW of electricity generation into its national grid in the next 10 years, practically doubling the installed capacity of its current power plants. It is, therefore, important to enact a robust legal framework that can incentivize and manage the expansion of these renewable energy and distributed generation resources. Steps towards establishing a legal framework, like the Renewable Energy Law 2005 (amended in December 2009), 12th Five year Plan, Medium and Long-Term Development Plan for Renewable Energy and its associated implementing regulations, have played a major role in the rapid growth of China’s renewable resources in the past few years. However, the rapid growth in renewable energy, particularly solar PV and wind, is hampered, because although grid companies are bound to purchase all the power generated by renewables and interconnect the RE and DG to utility grid according to RELaw 2005, in practice this is not happening. This is because grid transmission capacity has not matched the growth rate of China’s solar and wind power plants. According to statistics from China Electricity Council and the China Wind Energy Association (WEA) only 72% (8.94 GW) of China’s total wind power capacity was connected to the grid and at the end of 2015 this had only increased to 80.2%.

3. Barriers and Challenges

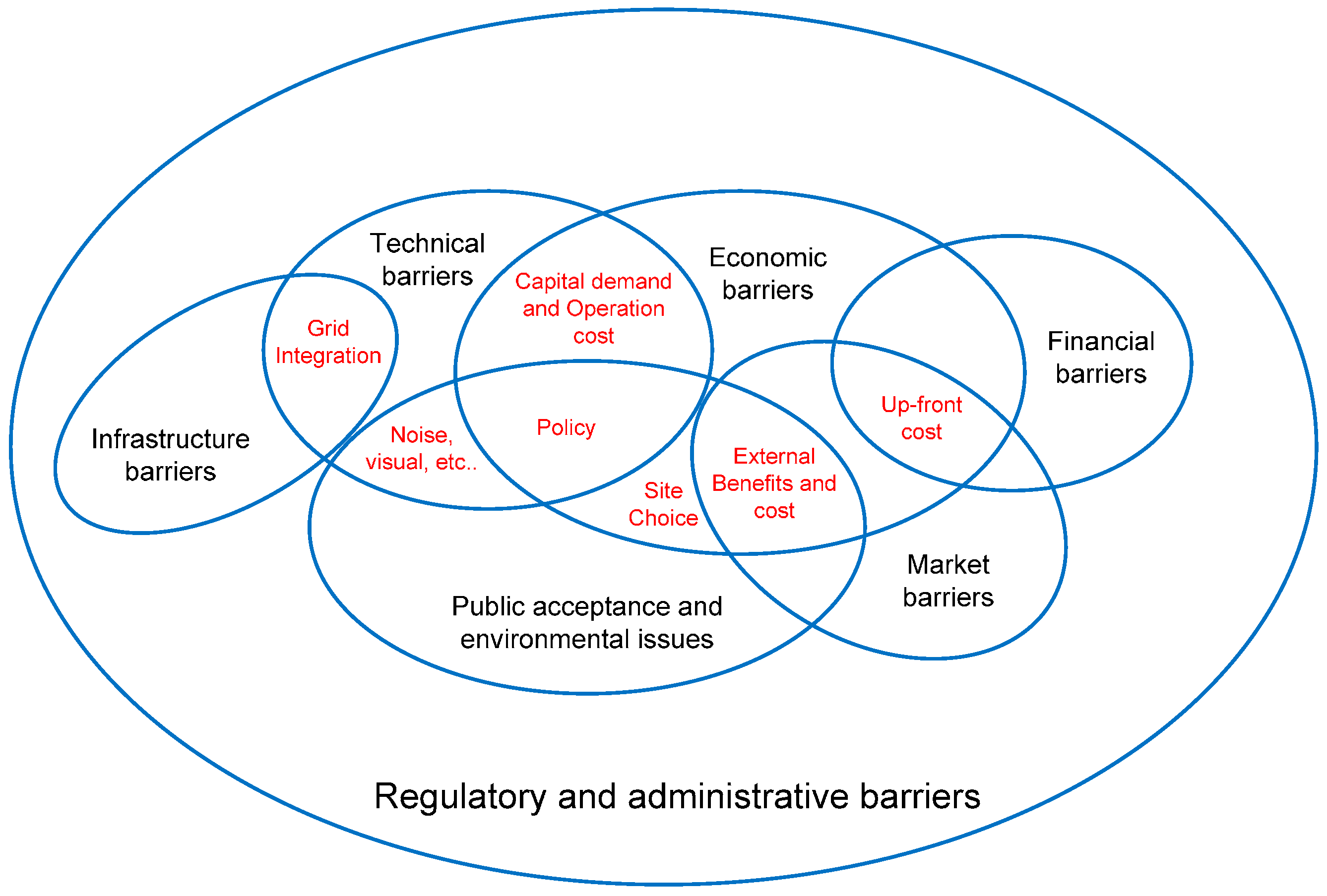

3.1. Non-Economic Barriers

- Regulatory and policy uncertainty barriers, which relate to bad policy design, or discontinuity and/or insufficient transparency of policies and legislation.

- Institutional and administrative barriers, which include the lack of strong, dedicated institutions, lack of clear responsibilities, and complicated, slow or non-transparent permitting procedures.

- Market barriers, such as inconsistent pricing structures that disadvantage renewables, asymmetrical information, market power, subsidies for fossil fuels, and the failure of costing methods to include social and environmental costs.

- Financial barriers associated with an absence of adequate funding opportunities and financing products for renewable energy.

- Infrastructure barriers that mainly center on the flexibility of the energy system, e.g., the power grid, to integrate/absorb renewable energy.

- Lack of awareness and skilled personnel relating to insufficient knowledge about the availability and performance of renewable. Plus insufficient numbers of skilled workers.

- Social acceptance and environmental barriers linked to experience with planning regulations and public acceptance of renewable energy.

3.2. Financial and Economic Issues

3.2.1. Power Purchase Agreement (PPA)

3.2.2. High Upfront Cost

- Lengthy administrative procedures for approval and permit.

- Policy instability with sudden changes and stop-and-go situations.

- Cost competitiveness and fraction.

3.2.3. Grid Connection Costs or Transmission Expansion

3.3. Regulatory Issues

3.3.1. Identifying Renewable Energy Zones

3.3.2. Distributed Generation Integration

3.3.3. Transmission Planning

4. Incentives and Benefits

4.1. Europe

4.2. USA

4.3. China

4.4. Observations and Opinion

5. Conclusions

Conflicts of Interest

References

- Soshinskaya, M.; Crijns-Graus, W.H.J.; Guerrero, J.M.; Vasquez, J.C. Microgrids: Experiences, barriers and success factors. Renew. Sustain. Energy Rev. 2014, 40, 659–672. [Google Scholar] [CrossRef]

- Lasseter, R.H. Microgrids. In Proceedings of the Power Engineering Society Winter Meeting, New York, NY, USA, 27–31 January 2002; pp. 305–308. [Google Scholar]

- US Department of Energy. Microgrid. Available online: http://www.energy.gov (accessed on 20 June 2017).

- Microgrid Institute. About Microgrids. Available online: http://www.microgridinstitute.org/about-microgrids.html (accessed on 20 June 2017).

- Ustun, T.S.; Ozansoy, C.; Zayegh, A. Recent developments in microgrids and example cases around the world—A review. Renew. Sustain. Energy Rev. 2011, 15, 4030–4041. [Google Scholar] [CrossRef]

- Colson, C.M.; Nehrir, M.H. A review of challenges to real-time power management of microgrids. In Proceedings of the Power & Energy Society General Meeting, Calgary, AB, Canada, 26–30 July 2009; pp. 1–8. [Google Scholar]

- Navigation Research. Microgrid Deployment Tracker 4Q15. Available online: http://www.navigantresearch.com/research/microgrid-deployment-tracker-4q15 (accessed on 20 June 2017).

- Zervos, A. Renewable Energy Policy Network for the 21st Century. In Renewables 2015 Global Status Report; Renewable Energy Policy Network for the 21st Century: Paris, France, 2015. [Google Scholar]

- Navigation Research. Microgrids & Distributed Renewables, 2015; Microgrids & Distributed Renewables. Available online: https://www.navigantresearch.com (accessed on 20 June 2017).

- Romankiewicz, J.; Marnay, C.; Zhou, N.; Qu, M. Lessons from international experience for China’s microgrid demonstration program. Energy Policy 2014, 67, 198–208. [Google Scholar] [CrossRef]

- Agrawal, M.; Mittal, A. Micro grid technological activities across the globe: A review. Int. J. Res. Rev. Appl. Sci. 2011, 7, 6. [Google Scholar]

- Streimikiene, D. The impact of international GHG trading regimes on penetration of new energy technologies and feasibility to implement EU Energy and Climate Package targets. Renew. Sustain. Energy Rev. 2012, 16, 2172–2177. [Google Scholar] [CrossRef]

- Office of Electricity Delivery & Energy Reliability. “GRID 2030” A National Vision For Electricity’s Second 100 Years; United States Department of Energy, Office of Electric Transmission and Distribution: Washington, DC, USA, 2003; p. 44.

- Jianfei, S.; Song, X.; Ming, Z.; Yi, W.; Yuejin, W.; Xiaoli, L.; Zhijie, W. Low-carbon development strategies for the top five power generation groups during China’s 12th Five-Year Plan period. Renew. Sustain. Energy Rev. 2014, 34, 350–360. [Google Scholar] [CrossRef]

- Yu, X.; Qu, H. The role of China’s renewable powers against climate change during the 12th Five-Year and until 2020. Renew. Sustain. Energy Rev. 2013, 22, 401–409. [Google Scholar] [CrossRef]

- Ming, Z.; Song, X.; Mingjuan, M.; Xiaoli, Z. New energy bases and sustainable development in China: A review. Renew. Sustain. Energy Rev. 2013, 20, 169–185. [Google Scholar] [CrossRef]

- Lo, K.; Wang, M.Y. Energy conservation in China’s Twelfth Five-Year Plan period: Continuation or paradigm shift? Renew. Sustain. Energy Rev. 2013, 18, 499–507. [Google Scholar] [CrossRef]

- Vandoorn, T.L.; De Kooning, J.D.M.; Meersman, B.; Vandevelde, L. Review of primary control strategies for islanded microgrids with power-electronic interfaces. Renew. Sustain. Energy Rev. 2013, 19, 613–628. [Google Scholar] [CrossRef]

- Majumder, R. Some Aspects of Stability in Microgrids. IEEE Trans. Power Syst. 2013, 28, 3243–3252. [Google Scholar] [CrossRef]

- Bhaskara, S.N.; Chowdhury, B.H. Microgrids—A review of modeling, control, protection, simulation and future potential. In Proceedings of the Power and Energy Society General Meeting, Sad Diego, CA, USA, 22–26 July 2012; pp. 1–7. [Google Scholar]

- Basak, P.; Chowdhury, S.; Halder nee Dey, S.; Chowdhury, S.P. A literature review on integration of distributed energy resources in the perspective of control, protection and stability of microgrid. Renew. Sustain. Energy Rev. 2012, 16, 5545–5556. [Google Scholar] [CrossRef]

- Salam, A.A.; Mohamed, A.; Hannan, M.A. Technical Challenges on Microgrid. ARPN J. Eng. Appl. Sci. 2008, 3, 64–69. [Google Scholar]

- L’Abbate, A.; Fulli, G.; Starr, F.; Peteves, S.D. Distributed Power Generation in Europe: Technical Issues for Further Integration; European Commission: Luxembourg, 2007. [Google Scholar]

- Sanz, J.F.; Matute, G.; Fernández, G.; Alonso, M.A.; Sanz, M. Analysis of European policies and incentives for microgrids. In Proceedings of the International Conference on Renewable Energies and Power Quality, Cordoba, Spain, 8–10 April 2014; p. 6. [Google Scholar]

- Μichalena, E.; Hills, J.M. Renewable energy issues and implementation of European energy policy: The missing generation? Energy Policy 2012, 45, 201–216. [Google Scholar] [CrossRef]

- Kitzing, L.; Mitchell, C.; Morthorst, P.E. Renewable energy policies in Europe: Converging or diverging? Energy Policy 2012, 51, 192–201. [Google Scholar] [CrossRef]

- Klessmann, C.; Held, A.; Rathmann, M.; Ragwitz, M. Status and perspectives of renewable energy policy and deployment in the European Union—What is needed to reach the 2020 targets? Energy Policy 2011, 39, 7637–7657. [Google Scholar] [CrossRef]

- Hatziargyriou, N. European Perspective on Microgrid Resilience. Available online: http://www.ieee-pes.org/presentations/gm2015/PESGM2015P-002946.pdf. (accessed on 20 June 2017).

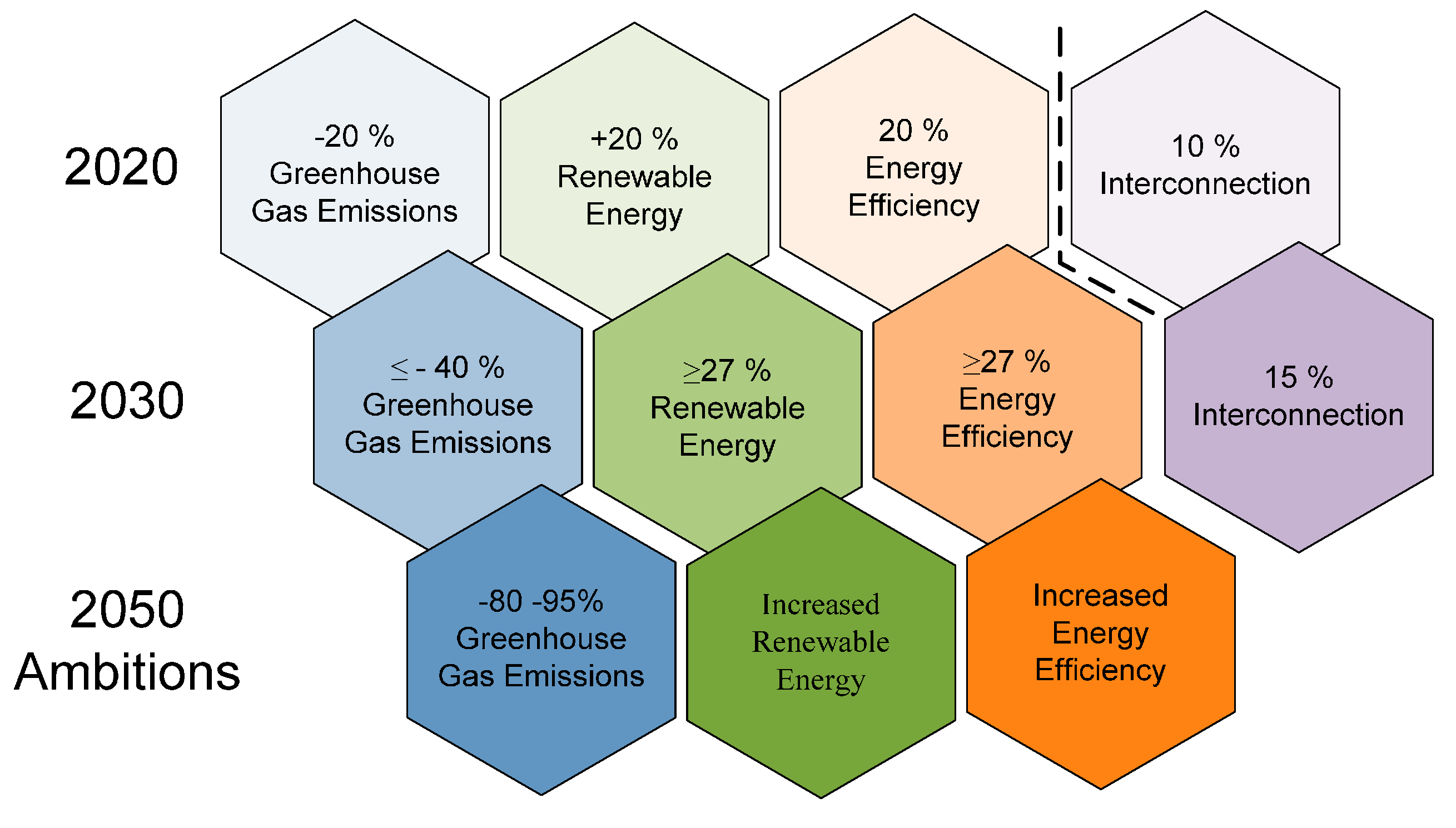

- European Commission. A Policy Framework for Climate and Energy in the Period from 2020 to 2030; The European Economic and Social Committee and the Committee of the Region: Brussels, Belgium, 2014. [Google Scholar]

- Lind, A.; Rosenberg, E.; Seljom, P.; Espegren, K.; Fidje, A.; Lindberg, K. Analysis of the EU renewable energy directive by a techno-economic optimisation model. Energy Policy 2013, 60, 364–377. [Google Scholar] [CrossRef]

- Commission, E. EU More MicroGrids. Available online: http://microgrids.eu/ (accessed on 20 June 2017).

- Braun, J.F. EU Energy Policy under the Treaty of Lisbon Rules; European Policy Institutes Network: Brussels, Belgium, 2011. [Google Scholar]

- Murat Sirin, S.; Ege, A. Overcoming problems in Turkey’s renewable energy policy: How can EU contribute? Renew. Sustain. Energy Rev. 2012, 16, 4917–4926. [Google Scholar] [CrossRef]

- European Commission. Promotion of the Use of Energy from Renewable Sources; European Commission: Brussels, Belgium, 2009. [Google Scholar]

- European Commission. Promotion of Electricity Produced from Renewable Energy Sources in the Internal Electricity Market. Off. J. Eur. Union 2001, 283, 33–40. [Google Scholar]

- European Commission. Energy end-use efficiency and energy services. Off. J. Eur. Union 2006, 114, 64–85. [Google Scholar]

- European Commission. Concerning common rules for the internal market in electricity. Off. J. Eur. Union 2009, 211, 55–93. [Google Scholar]

- European Commission. Promotion of cogeneration based on a useful heat demand in the internal energy market and amending. Off. J. Eur. Union 2004, 52, 50–60. [Google Scholar]

- Zhang, H.; Zhou, D.; Cao, J. A quantitative assessment of energy strategy evolution in China and US. Renew. Sustain. Energy Rev. 2011, 15, 886–890. [Google Scholar] [CrossRef]

- Martinot, E.; Wiser, R.; Hamrin, J. Renewable Energy Policies and Markets in the United States; Center for Resource Solutions: San Francisco, CA, USA, 2015. [Google Scholar]

- Gençer, E.; Agrawal, R. A commentary on the US policies for efficient large scale renewable energy storage systems: Focus on carbon storage cycles. Energy Policy 2016, 88, 477–484. [Google Scholar] [CrossRef]

- International Energy Agency. Energy Policies of IEA Countries: United States 2007. Available online: http://www.oecd-ilibrary.org/energy/energy-policies-of-iea-countries-united-states-2007_9789264030749-en (accessed on 20 June 2017).

- Department of Energy USA. Energy Policy Act 2005; Department of Energy USA: Washington, DC, USA, 2005.

- Lyon, T.P.; Yin, H. Why Do States Adopt Renewable Portfolio Standards?: An Empirical Investigation. Energy J. 2010, 31, 133–157. [Google Scholar] [CrossRef]

- Wang, T.; Gong, Y.; Jiang, C. A review on promoting share of renewable energy by green-trading mechanisms in power system. Renew Sustain Energy Rev. 2014, 40, 923–929. [Google Scholar] [CrossRef]

- Osmani, A.; Zhang, J.; Gonela, V.; Awudu, I. Electricity generation from renewables in the United States: Resource potential, current usage, technical status, challenges, strategies, policies, and future directions. Renew. Sustain. Energy Rev. 2013, 24, 454–472. [Google Scholar] [CrossRef]

- Research, N. Microgrid Deployment Tracker 4Q16. Available online: https://www.navigantresearch.com/research/microgrid-deployment-tracker-4q16 (accessed on 20 June 2017).

- Brennan, T.J.; Palmer, K.L. Energy Efficiency Resource Standards: Economics and Policy. Util. Policy 2012, 25, 58–68. [Google Scholar] [CrossRef]

- Solar Energy Institute. Renewable Energy Standard. Available online: http://www.seia.org/policy/renewable-energy-deployment/renewable-energy-standards (accessed on 20 June 2017).

- Ding, N.; Duan, J.; Xue, S.; Zeng, M.; Shen, J. Overall review of peaking power in China: Status quo, barriers and solutions. Renew. Sustain. Energy Rev. 2015, 42, 503–516. [Google Scholar] [CrossRef]

- Shen, J.; Luo, C. Overall review of renewable energy subsidy policies in China—Contradictions of intentions and effects. Renew. Sustain. Energy Rev. 2015, 41, 1478–1488. [Google Scholar] [CrossRef]

- Zeng, M.; Li, C.; Zhou, L. Progress and prospective on the police system of renewable energy in China. Renew. Sustain. Energy Rev. 2013, 20, 36–44. [Google Scholar] [CrossRef]

- Schuman, S.; Lin, A. China’s Renewable Energy Law and its impact on renewable power in China: Progress, challenges and recommendations for improving implementation. Energy Policy 2012, 51, 89–109. [Google Scholar] [CrossRef]

- Ministry of Commerce People’s Republic of China. Renewable Energy Law of the People’s Republic of China; MOFCOM: Beijing, China, 2009.

- Zhao, Z.-Y.; Chen, Y.-L.; Chang, R.-D. How to stimulate renewable energy power generation effectively?—China’s incentive approaches and lessons. Renew. Energy 2016, 92, 147–156. [Google Scholar] [CrossRef]

- China National Reform and Development Comission. China Renewable Energy Development Plan; NDRC: Beijing, China, 2010.

- National Development and Reform Commission. Medium and Long-Term Development Plan for Renewable Energy in China; NDRC: Beijing, China, 2007.

- Thomson, E. Introduction to special issue: Energy issues in China’s 12th Five Year Plan and beyond. Energy Policy 2014, 73, 1–3. [Google Scholar] [CrossRef]

- Hong, L.; Zhou, N.; Fridley, D.; Raczkowski, C. Assessment of China’s renewable energy contribution during the 12th Five Year Plan. Energy Policy 2013, 62, 1533–1543. [Google Scholar] [CrossRef]

- Bustamante-Cedeno, E.; Arora, S. Stochastic and minimum regret formulations for transmission network expansion planning under uncertainties. J. Oper. Res. Soc. 2008, 59, 1547–1556. [Google Scholar] [CrossRef]

- Batten, K.; Manlove, K. Identifying Hurdles to Renewable Electricity Transmission. Center for American Progress: Washington, DC, USA, 2008; Available online: http://www.americanprogress.org (accessed on 20 June 2017).

- Gruber, E.; Erge, T.; Pfafferott, J.; Ragwitz, M. Assessment and Optimisation of Renewable Energy Support Measures in the European Electricity Market; European Commission: Brussels, Belgium, 2007. [Google Scholar]

- Menanteau, P.; Finon, D.; Lamy, M.-L. Prices versus quantities: Choosing policies for promoting the development of renewable energy. Energy Policy 2003, 31, 799–812. [Google Scholar] [CrossRef]

- Haas, R.; Eichhammer, W.; Huber, C.; Langniss, O.; Lorenzoni, A.; Madlener, R.; Menanteau, P.; Morthorst, P.E.; Martins, A.; Oniszk, A.; et al. How to promote renewable energy systems successfully and effectively. Energy Policy 2004, 32, 833–839. [Google Scholar] [CrossRef]

- Pudjianto, D.; Strbac, G.; Oberbeeke, F.V.; Androutsos, A.I.; Larrabe, Z.; Saraiva, J.T. Investigation of regulatory, commercial, economic and environmental issues in microgrids. In Proceedings of the International Conference on Future Power Systems, Amsterdam, The Netherlands, 16–18 November 2005; p. 6. [Google Scholar]

- Müller, S.; Brown, A.; Ölz, S. Renewable Energy: Policy Considerations For Deploying Renewables; IEA: Paris, France, 2011. [Google Scholar]

- Barradale, M.J. Impact of public policy uncertainty on renewable energy investment: Wind power and the production tax credit. Energy Policy 2010, 38, 7698–7709. [Google Scholar] [CrossRef]

- Rohankar, N.; Jain, A.K.; Nangia, O.P.; Dwivedi, P. A study of existing solar power policy framework in India for viability of the solar projects perspective. Renew. Sustain. Energy Rev. 2016, 56, 510–518. [Google Scholar] [CrossRef]

- International Renewable Energy Agency. Rethinking Energy: Towards a New Power System; IRENA: Abu Dhabi, UAE, 2014. [Google Scholar]

- NREL. Integration of Variable Generation and Cost-Causation. Available online: http://www.nrel.gov/docs/fy12osti/56235.pdf (accessed on 20 June 2017).

- International Confederation of Energy Regulators. Renewable Energy and Distributed Generation: International Case Studies on Technical and Economic Considerations; ICER: Brussels, Belgium, 2012. [Google Scholar]

- Luckow, P.; Fagan, B.; Fields, S.; Whited, M. Technical and Institutional Barriers to the Expansion of Wind and Solar Energy; Synapse: Cambridge, MA, USA, 2015. [Google Scholar]

- Picciariello, A.; Alvehag, K.; Soder, L. State-of-art review on regulation for distributed generation integration in distribution systems. In Proceedings of the 9th International Conference on the European Energy Market (EEM), Florence, Italy, 10–12 May 2012; pp. 1–8. [Google Scholar]

- Kazmi, S.A.A.; Hasan, S.F.; Shin, D-.R. Analyzing the integration of Distributed Generation into smart grids. In Proceedings of the IEEE 10th Conference on Industrial Electronics and Applications (ICIEA), Auckland, New Zealand, 15–17 June 2015; pp. 762–766. [Google Scholar]

- Lopes, J.A.P.; Hatziargyriou, N.; Mutale, J.; Djapic, P.; Jenkins, N. Integrating distributed generation into electric power systems: A review of drivers, challenges and opportunities. Electr. Power Syst. Res. 2007, 77, 1189–1203. [Google Scholar] [CrossRef]

- De Joode, J.; Jansen, J.C.; van der Welle, A.J.; Scheepers, M.J.J. Increasing penetration of renewable and distributed electricity generation and the need for different network regulation. Energy Policy 2009, 37, 2907–2915. [Google Scholar] [CrossRef]

- Frías, P.; Gómez, T.; Cossent, R.; Rivier, J. Improvements in current European network regulation to facilitate the integration of distributed generation. Int. J. Electr. Power Energy Syst. 2009, 31, 445–451. [Google Scholar] [CrossRef]

- Ringel, M. Fostering the use of renewable energies in the European Union: The race between feed-in tariffs and green certificates. Renew. Energy 2006, 31, 1–17. [Google Scholar] [CrossRef]

- Ragwitz, M.; Winkler, J.; Klessmann, C.; Gephart, M.; Resch, G. Recent Developments of Feed-In Systems in the EU; Nature Conservation and Nuclear Safety (BMU): Bonn, Germany, 2012. [Google Scholar]

- European Comission. Renewables: Energy and Equipment Trade Developments in the EU; EC: Brussels, Belgium, 2014. [Google Scholar]

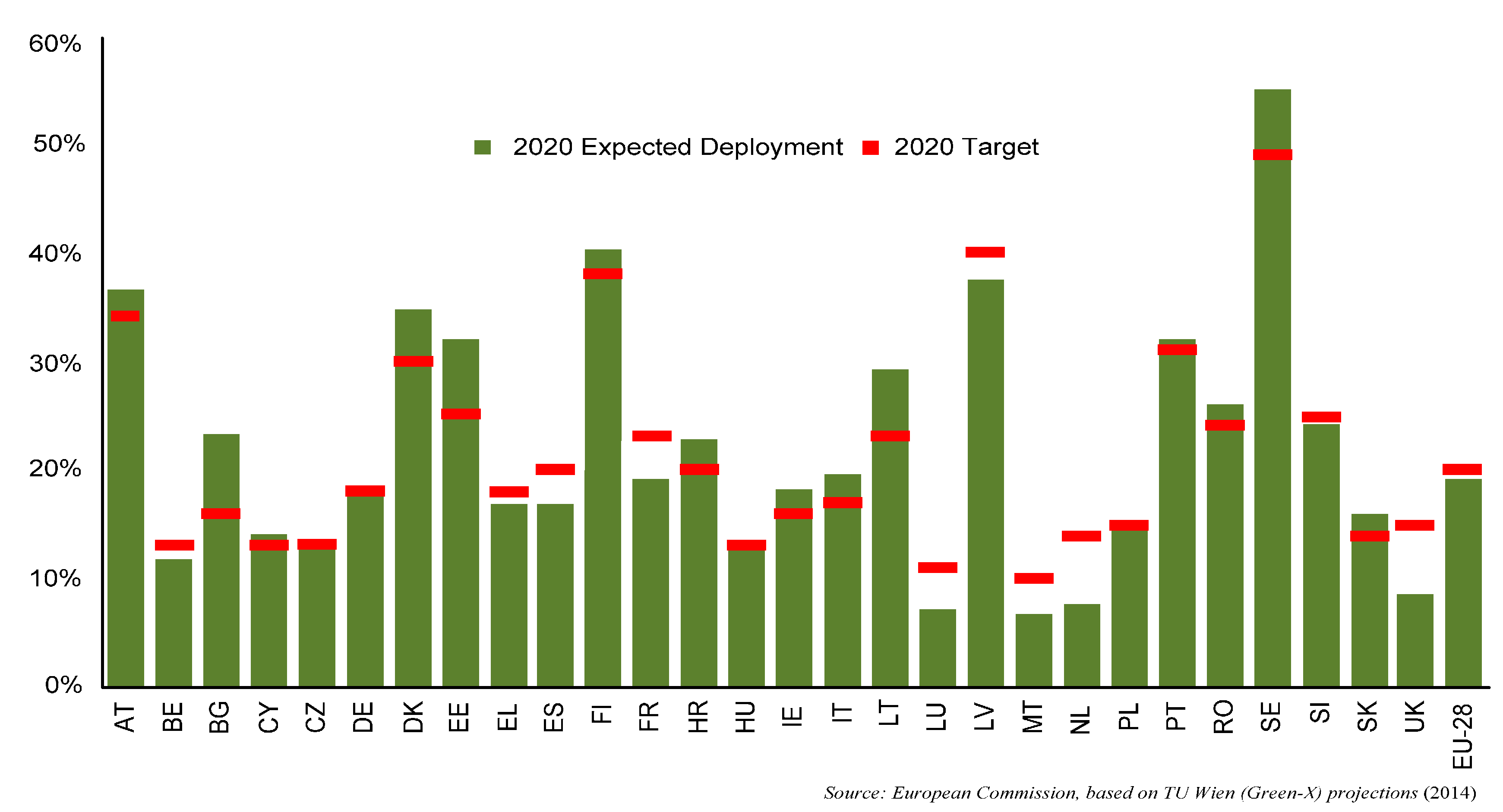

- European Forum for Renewable Energy Sources (EUFORES). EU Tracking Roadmap 2014: Keeping Track of Renewable Energy Targets Towards 2020; EUFORES: Brussels, Belgium, 2014. [Google Scholar]

- European Commission. European Commission Guidance for the Design of Renewables Support Schemes; EC: Brussels, Belgium, 2013. [Google Scholar]

- European Commission. Renewable Energy Progress Report; EC: Brussels, Belgium, 2015. [Google Scholar]

- Maehlum, M.A. What’s the Difference between Net Metering and Feed-In Tariffs? Energy Inf. Available online: http://energyinformative.org/net-metering-feed-in-tariffs-difference (accessed on 20 June 2017 ).

- Jiang, Z.; Lin, B. China’s energy demand and its characteristics in the industrialization and urbanization process. Energy Policy 2012, 49, 608–615. [Google Scholar] [CrossRef]

- U.S. Energy Information Administration (EIA). U.S. Exports of Crude Oil and Petroleum Products Have More than Doubled Since 2010. Available online: http://www.eia.gov/ (accessed on 20 June 2017).

- Qi, T.; Zhang, X.; Karplus, V.J. The energy and CO2 emissions impact of renewable energy development in China. Energy Policy 2014, 68, 60–69. [Google Scholar] [CrossRef]

- Zeng, Z.; Zhao, R.; Yang, H.; Tang, S. Policies and demonstrations of micro-grids in China: A review. Renew. Sustain. Energy Rev. 2014, 29, 701–718. [Google Scholar] [CrossRef]

- National Renewable Energy Laboratory(NREL). Renewable Energy Policy in China: Financial Incentives. Available online: http://www.nrel.gov/docs/fy04osti/36045.pdf (accessed on 20 June 2017).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Directive | Objective | Articles No. | To be Considered for Renewable Energy & Microgrid Promotion and Development |

|---|---|---|---|

| 2009/28/EC | Promotion of the use of energy from renewable sources | 7 | Promotion of electricity produced from renewable energy sources in the internal electricity market. |

| 27 | Expansion of electricity produced from renewable energy sources with public support is necessary to reach target of 20% by 2020. | ||

| 37 | Import of electricity, produced from renewable energy sources outside the Community. | ||

| 38 | To undertake joint projects with one or more third countries regarding the production of electricity from renewable energy sources. | ||

| 41 | To take into account lack of coordination between the different authorization bodies to hinder the deployment of energy from renewable sources and giving permission to construct and operate plants and associated transmission and distribution network infrastructures for the production of electricity. | ||

| 52 | Guarantee of origin issued for that a given share or quantity of energy was produced from renewable sources. | ||

| 53 | To allow the emerging consumer market for electricity generation from renewable energy sources to contribute to the construction of new installations for energy from renewable sources appropriately. | ||

| 59 | Integration of electricity produced from renewable energy sources between member countries. | ||

| 60 | Integration of electricity generated from renewable energy sources into the internal on priority basis. | ||

| 61 | To ensure transmission and distribution of electricity produced from renewable energy sources without affecting the reliability or safety of the grid system. | ||

| 62 | The costs of connecting new producers of electricity from renewable energy sources to the electricity grids should be the main objective. | ||

| 63 | Electricity producers who want to exploit the potential of energy from renewable sources in the peripheral regions of the Community, in particular in island regions and regions of low population density, should, whenever feasible, benefit from reasonable connection costs in order to ensure that they are not unfairly disadvantaged in comparison with producers situated in more central, more industrialized and more densely populated areas. | ||

| 64 | Integration of electricity from renewable energy sources into the grid according to directive 2001/77/EC. | ||

| 2006/32/EC | Energy end-use efficiency | 1 | To improve energy end-use efficiency and promotion of the production of energy from renewable energies. |

| 2 | Improve energy end-use efficiency to contribute in reduction of primary energy consumption, to mitigate CO2 and other GHGs | ||

| 3 | To improve energy end-use efficiency for cost-effective energy saving and help the community to reduce its dependence on energy imports. | ||

| 8 | To initiate energy-efficiency pilot projects. | ||

| To Be Considered for Grid Connection | |||

| 2009/72/EC | Electricity Grid Connection | 6 | To provide appropriate incentives for investing in new power generation, including in electricity from renewable energy sources. |

| 8 | To provide cross border facility for electricity generation and supply at competitive price. | ||

| 16 | Setting up of a system operator or a transmission operator that is independent from supply and generation interests should enable a vertically integrated undertaking to maintain its ownership of network assets | ||

| 27 | To encourage the modernization of distribution networks, such as through the introduction of smart grids, which should be built in a way that encourages decentralized generation and energy efficiency. | ||

| 36 | National regulatory authorities should fix or approve transmission and distribution tariffs. | ||

| To Be Considered for Energy storage and Self Consumption | |||

| 2004/8/EC | Promotes Cogeneration of Heat, energy efficiency and Security of Supply | 1 | Promote use of high efficiency cogeneration based on a useful heat demand in community with regard to saving primary energy, avoiding network losses and reducing emissions, in particular of greenhouse gases. |

| 3 | Shift towards energy efficient production plants, including combined heat and power towards a European strategy for the security of energy supply. | ||

| 5 | To increased use of cogeneration geared towards making primary energy saving. | ||

| 15 | Harmonized method directive should be established for calculation of cogeneration electricity generation | ||

| 20 | Define ‘small scale cogeneration’ comprises micro-cogeneration and distributed cogeneration units such as cogeneration units supplying isolated areas or limited residential, commercial or industrial demands. | ||

| 21 | To increase transparency for the consumer’s choice between electricity from cogeneration and electricity produced on the basis of other techniques. | ||

| 23 | To ensure increased market penetration of cogeneration in the medium term. | ||

| To Be Considered for Smart Grid Development and Integration | |||

| 2013/347/EC | Deployment of smart grids for achieving an optimal utilization | 1 | Union-wide innovation to deployment of smart grid |

| 2 | Cost effective integration of smart grid (power producer and consumer) in order to ensure an economically efficient and sustainable power system with low losses and high levels of quality, security of supply and safety | ||

| 6 | Coordination between EU member states for better deployment of smart grid | ||

| 13 | For promotion and development of smart grids, national regulatory authorities will grant the incentives on the methodology of cost benefit. | ||

| Title | Country | Year | Status |

|---|---|---|---|

| Renewable Energy Law of Poland | Poland | 2015 | In force |

| 2014 Amendment of the Renewable Energy Sources Act -EEG- | Germany | 2014 | In force |

| Act on Energy and amendments to certain acts (No. 251/2012) | Slovakia | 2013 | In force |

| Royal Decree Law on urgent measures to guarantee financial stability in the electricity system | Spain | 2013 | In force |

| Electricity Market Reform (EMR) | UK | 2013 | In force |

| National Energy Strategy | Italy | 2013 | In force |

| Energy Act 2012 | Croatia | 2012 | In force |

| Regulation on Net-metering for the Producers of Electricity for Own Needs | Denmark | 2012 | In force |

| Danish Energy Agreement for 2012-2020 | Denmark | 2012 | In force |

| Energy performance requirements for residential buildings 2012-2020 | Luxembourg | 2012 | In force |

| Act on Regulatory Office for Network Industries (Act No. 250/2012) | Slovakia | 2012 | In force |

| Law on Energy from Renewable Sources | Lithuania | 2011 | In force |

| Regulation of small power plants connation to the electricity grid (Royal Decree 1699/2011) | Spain | 2011 | In force |

| Energy White Paper 2011 | UK | 2011 | Superseded |

| Regulation on load management activity within the electricity system involving energy charging services | Spain | 2010 | Ended |

| National Renewable Energy Action Plan (NREAP) | Slovakia | 2010 | In force |

| Correction of the tariff deficit in the electricity sector (Royal Decree-Law 14/2010) | Spain | 2010 | Ended |

| Energy Concept | Germany | 2010 | In force |

| Promotion of Renewable Energy Act | Denmark | 2009 | In force |

| New regulatory framework for administrative procedures for renewable energy facilities | Spain | 2009 | In force |

| Law on establishing the promotion system of energy production from renewable energy | Romania | 2008 | In force |

| Feed-in tariffs for renewable energy | Luxembourg | 2008 | In force |

| Retailer Sustainable Commerce Agreement | France | 2008 | In force |

| Net Metering | Italy | 2008 | In force |

| Regulation on electricity market organization | Luxembourg | 2007 | In force |

| Ordinance: rights and obligations of the electricity market participants | Slovakia | 2007 | In force |

| Ordinance on Acquiring the Status of Eligible Electricity Producer | Croatia | 2007 | In force |

| Ordinance on the Use of Renewable Energy Sources and Cogeneration | Croatia | 2007 | In force |

| Regulation on the Minimum Share of Electricity Produced from RES and Cogeneration Whose Production is Incentivized | Croatia | 2007 | In force |

| Electricity Market Act 2007 | Greece | 2006 | In force |

| Energy Transition | Netherlands | 2006 | Superseded |

| Obligation for Power Purchase from Renewable Sources | Poland | 2005 | In force |

| Decree on Notification on the Origin of Electricity | Finland | 2005 | In force |

| Act on Energy and amendments (Act no. 656/2005) | Slovakia | 2005 | Superseded |

| RES promotion - Decree Implementing Directive 2001/77/EC | Italy | 2004 | Superseded |

| Reorganization of Energy Sector Regulation | Italy | 2004 | In force |

| Green Certificate Scheme—Federal | Belgium | 2003 | In force |

| Electricity Market Act 2003 | Estonia | 2003 | Superseded |

| Renewable Energy Guarantees of Origin (REGOs) | UK | 2003 | In force |

| The Electricity Law (No. 318/2003) | Romania | 2003 | Superseded |

| Renewables Obligation (RO) | UK | 2002 | In force |

| Green Electricity Act | Austria | 2002 | Superseded |

| Law on Energy | Lithuania | 2002 | In force |

| Feed-in Tariffs and Premiums | Slovenia | 2002 | In force |

| Green Certificates Scheme—Wallonia | Belgium | 2002 | In force |

| Energy Management Act (Act No. 406/2000 Coll.) | Czech Republic | 2001 | In force |

| Climate Change Levy | UK | 2001 | In force |

| Act No. 250/2012 Coll. on Regulation in Network Industries | Slovakia | 2001 | In force |

| Energy Act (Act No. 458/2000 Coll.) | Czech Republic | 2001 | In force |

| Instrument for Structural Policies for Pre-Accession (ISPA) | Hungary | 2000 | Ended |

| Access to the Grid (Renewables and CHP) | Belgium | 2000 | In force |

| Renewable Energy Sources Act | Germany | 2000 | Superseded |

| Demand Side Management to Reduce GHG Emissions—ENEL Voluntary Agreement | Italy | 2000 | Ended |

| Electricity Law 2000 | France | 2000 | In force |

| Year | Policy | |

|---|---|---|

| Era-1 | 1978 | Public Utilities Regulatory Policy Act (PURPA) enacted. |

| 1978 | Energy Tax Act provided personal income tax credits and business tax credits for renewables. | |

| 1980 | Federal R&D supporting fund for renewable energy Technologies | |

| 1980 | Windfall Profits Tax Act gave tax credits for alternative fuels production and alcohol fuel blending. | |

| Era-2 | 1992 | California delayed property tax credits for solar thermal power, which caused investment to stop. |

| 1992 | Energy Policy Act provides tax credits for ethanol fuels for vehicles. | |

| 1994 | Federal production tax credit (PTC) takes effect as part of the Energy Policy Act of 1992. | |

| 1996 | Net metering laws started to take effect in many states. | |

| 1997 | States began establishing policies for renewable portfolio standards (RPS) and public benefits funds (PBF) as part of state electricity restructuring. | |

| Era-3 | 2001 | Some states began to mandate that utilities offer green power products to their customers. |

| 2002 | Federal production tax credit (PTC) expired and was not renewed until later in the year, causing the wind industry to suffer a major downturn. This happened in 2000 also, and again in 2004. | |

| 2004 | Five new states enacted renewables portfolio standards (RPS) policies in a single year, bringing the total to 18 states plus Washington DC; public benefit funds (PBF) were operating in 15 states. | |

| 2005 | Energy Policy Act 2005 (EPAct-2005) | |

| 2007 | Energy Independence and Security Act. (EISA-2007) | |

| 2009 | American Recover and Reinvestment Act. (ARRA-2009) |

| Title | Year | Status |

|---|---|---|

| State-level Renewable Portfolio Standards (RPS) | Multiple years | In Force |

| Final Rule on Renewable Energy and Alternate Uses of Existing Facilities on the Outer Continental Shelf | 2009 | Superseded |

| Onshore Renewable Energy Development Programs | 2009 | In Force |

| Wind & Water Power Program | 2008 | In Force |

| Energy Provisions—National Defense Authorization Act for fiscal year 2009 | 2008 | Ended |

| Renewable and Energy Efficiency Portfolio Standard—Illinois | 2007 | In Force |

| Solar America Board for Codes and Standards | 2007 | In Force |

| Solar America | 2006 | Superseded |

| Renewable Portfolio Standard—Nevada | 2005 | In Force |

| Interconnection Standards for Small Generators | 2005 | In Force |

| Energy Policy Act (EPAct) | 2005 | In Force |

| Renewable Portfolio Standard—Colorado | 2004 | In Force |

| New York State Energy Plan | 2002 | In Force |

| Renewable Portfolio Standard—California | 2002 | In Force |

| Farm Security and Rural Investment Act of 2002 (Public Law 107–171) | 2002 | Superseded |

| Title | Year | Status |

|---|---|---|

| Renewable electricity generation bonus | 2013 | In Force |

| The Notice of further improvement of New Energy Demonstration implementation | 2013 | In Force |

| China Energy White Paper 2012 | 2012 | In Force |

| The Notice on New Energy Demonstration City and Industrial Park | 2012 | In Force |

| The Renewable Energy Tariff Surcharge Grant Funds Management Approach | 2012 | In Force |

| Energy saving and new energy automotive industry development plan 2012–2020 | 2012 | In Force |

| 2012 Renewable Energy Electricity feed-in tariff | 2012 | In Force |

| 12th Five Year Plan for National Strategic Emerging Industries | 2012 | In Force |

| The Twelfth Five-Year Plan for Renewable Energy | 2012 | In Force |

| Renewable Electricity Surcharge | 2009 | In Force |

| Renewable Energy Law amendments | 2009 | In Force |

| National Climate Change Program | 2007 | In Force |

| Renewable Energy Law | 2006 | In Force |

| Preferential Tax Policies for Renewable Energy | 2003 | In Force |

| Country | Incentives | ||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| FIT | Quota System | Premium | Net Metering | Tax Exemptions | |||||||||||||||||||||

| PV | Wind | Hydro | % of Quota | No. of Certificates According to Tech. | Minimum Price per Green Certificate | Amount | Cap | PV | Wind | Hydro | PV | Wind | Hydro | ||||||||||||

| PV | Wind | Hydro | PV | Wind | Hydro | PV | Wind | Hydro | PV | Wind | Hydro | PV | Wind | Hydro | |||||||||||

| Austria | AT | ✓ | ✓ | ✓ | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x |

| Belgium | BE | x | x | x | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | x | x | x | x | x | x | ✓ | ✓ | ✓ | x | x | x |

| Bulgaria | BG | ✓ | ✓ | ✓ | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x |

| Croatia | HR | ✓ | ✓ | ✓ | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x |

| Cyprus | CY | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | ✓ | x | x | x | x | x | |

| Czech Republic | CZ | ✓ | ✓ | ✓ | x | x | x | x | x | x | x | x | x | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | x | x | x | x | x | x |

| Denmark | DK | x | x | x | x | x | x | x | x | x | x | x | x | ✓ | ✓ | ✓ | x | x | x | ✓ | ✓ | ✓ | x | x | x |

| Estonia | EE | x | x | x | x | x | x | x | x | x | x | x | x | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | x | x | x | x | x | x |

| Finland | FI | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | ✓ | x | x | x | x | x | x | x | |

| France | FR | ✓ | ✓ | ✓ | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | ✓ | ✓ | ✓ |

| Germany | DE | ✓ | ✓ | ✓ | x | x | x | x | x | x | x | x | x | ✓ | ✓ | ✓ | x | x | x | x | x | x | x | x | x |

| Greece | GR | ✓ | ✓ | ✓ | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | ✓ | ✓ | x | ✓ | ✓ | ✓ |

| Hungary | HU | ✓ | ✓ | ✓ | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | ✓ | ✓ | ✓ | x | x | x |

| Ireland | IE | x | ✓ | ✓ | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | ✓ | ✓ | ✓ |

| Italy | IT | x | x | x | x | x | x | x | x | x | x | x | x | ✓ | ✓ | ✓ | ✓ | x | x | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| Latvia | LV | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | ✓ | ✓ | ✓ | x | x | x |

| Lithuania | LT | ✓ | ✓ | ✓ | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | ✓ | ✓ | ✓ |

| Luxembourg | LU | ✓ | ✓ | ✓ | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | ✓ | x | x |

| Malta | MT | ✓ | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x |

| Netherlands | NL | x | x | x | x | x | x | x | x | x | x | x | x | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| Poland | PL | x | x | x | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | x | x | x | x | x | x | x | x | x | ✓ | ✓ | ✓ |

| Portugal | PT | ✓ | ✓ | ✓ | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x |

| Romania | RO | x | x | x | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | x | x | x | x | x | x | x | x | x | x | x | x |

| Slovakia | SK | ✓ | ✓ | ✓ | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | ✓ | ✓ | ✓ |

| Slovenia | SI | ✓ | ✓ | ✓ | x | x | x | x | x | x | x | x | x | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | x | x | x | x | x | x |

| Spain | ES | x | x | x | x | x | x | x | x | x | x | x | x | ✓ | ✓ | x | x | ✓ | ✓ | x | x | x | x | x | x |

| Sweden | SE | x | x | x | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | x | x | x | x | x | ✓ | ✓ | x | x | x | x | x | x | ✓ | x |

| UK | GB | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | x | x | x | x | x | x | x | x | x | x | x | x | ✓ | x | ✓ |

| State | FIT | Net Metering | Personal Tax | Corporate Tax | Sales Tax | Property Tax | Rebates | Grants | Loan | Bonds | Performance Base Incentives |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Alabama | x | x | ✓ | x | x | x | ✓ | x | ✓ | x | ✓ |

| Alaska | x | ✓ | x | x | x | ✓ | x | ✓ | ✓ | x | ✓ |

| Arizona | x | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | x | ✓ | x | x |

| Arkansas | x | ✓ | x | x | x | x | ✓ | x | ✓ | x | x |

| California | ✓ | ✓ | x | x | ✓ | ✓ | ✓ | x | ✓ | x | ✓ |

| Colorado | x | ✓ | x | x | ✓ | ✓ | ✓ | ✓ | ✓ | x | ✓ |

| Connecticut | x | ✓ | x | x | ✓ | ✓ | ✓ | ✓ | ✓ | x | ✓ |

| Delaware | x | ✓ | x | x | x | x | ✓ | x | ✓ | x | ✓ |

| Florida | ✓ | ✓ | x | ✓ | ✓ | ✓ | ✓ | x | ✓ | x | ✓ |

| Georgia | x | ✓ | x | x | ✓ | x | ✓ | ✓ | ✓ | x | ✓ |

| Hawaii | ✓ | ✓ | ✓ | ✓ | x | ✓ | ✓ | x | ✓ | ✓ | ✓ |

| Idaho | x | ✓ | ✓ | x | x | ✓ | ✓ | ✓ | ✓ | ✓ | x |

| Illinois | x | ✓ | x | x | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| Indiana | x | ✓ | ✓ | x | ✓ | ✓ | ✓ | ✓ | ✓ | x | ✓ |

| Lowa | x | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | x | ✓ | x | ✓ |

| Kansas | x | ✓ | x | x | x | ✓ | ✓ | x | x | x | x |

| Kentucky | x | ✓ | ✓ | ✓ | ✓ | x | ✓ | ✓ | ✓ | x | ✓ |

| Louisiana | x | ✓ | ✓ | ✓ | x | ✓ | ✓ | x | ✓ | x | x |

| Maine | ✓ | ✓ | x | x | x | x | x | x | ✓ | x | ✓ |

| Maryland | x | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | x | ✓ |

| Massachusetts | x | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | x | ✓ |

| Michigan | x | ✓ | x | x | x | ✓ | ✓ | ✓ | ✓ | x | ✓ |

| Minnesota | x | ✓ | x | x | ✓ | ✓ | ✓ | ✓ | ✓ | x | ✓ |

| Mississippi | x | x | x | x | x | x | ✓ | x | ✓ | x | ✓ |

| Missouri | x | ✓ | x | ✓ | x | ✓ | ✓ | x | ✓ | x | x |

| Montana | x | ✓ | ✓ | ✓ | x | ✓ | ✓ | x | ✓ | x | x |

| Nebraska | x | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | x | ✓ | x | ✓ |

| Nevada | x | ✓ | x | x | ✓ | ✓ | ✓ | x | ✓ | x | ✓ |

| New Hampshire | x | ✓ | x | x | x | ✓ | ✓ | ✓ | ✓ | x | x |

| New Jersey | x | ✓ | x | x | ✓ | ✓ | ✓ | ✓ | ✓ | x | ✓ |

| New Mexico | x | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | x | ✓ | ✓ | ✓ |

| New York | x | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | x | ✓ | x | ✓ |

| North Carolina | x | ✓ | ✓ | ✓ | x | ✓ | ✓ | x | ✓ | x | ✓ |

| North Dakota | x | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | x | ✓ | x | x |

| Ohio | x | ✓ | x | x | ✓ | ✓ | ✓ | x | ✓ | x | ✓ |

| Oklahoma | x | ✓ | x | ✓ | x | ✓ | ✓ | x | ✓ | x | x |

| Oregon | ✓ | ✓ | ✓ | ✓ | x | ✓ | ✓ | ✓ | ✓ | x | ✓ |

| Pennsylvania | x | ✓ | x | x | x | ✓ | ✓ | ✓ | ✓ | x | ✓ |

| Rhode Island | x | ✓ | x | x | ✓ | ✓ | x | ✓ | ✓ | x | ✓ |

| South Karolina | x | ✓ | ✓ | ✓ | ✓ | x | ✓ | x | ✓ | x | ✓ |

| South Dakota | x | x | x | x | ✓ | ✓ | ✓ | x | ✓ | x | x |

| Tennessee | x | x | x | x | ✓ | ✓ | ✓ | ✓ | ✓ | x | ✓ |

| Texas | x | ✓ | x | ✓ | x | ✓ | ✓ | x | ✓ | x | ✓ |

| Utah | x | ✓ | ✓ | ✓ | ✓ | x | ✓ | x | ✓ | ✓ | x |

| Vermont | ✓ | ✓ | ✓ | x | ✓ | ✓ | ✓ | ✓ | ✓ | x | ✓ |

| Virginia | x | ✓ | ✓ | x | x | ✓ | x | x | ✓ | x | ✓ |

| Washington | x | ✓ | x | x | ✓ | x | ✓ | ✓ | ✓ | x | ✓ |

| West Virginia | x | ✓ | x | ✓ | x | ✓ | ✓ | x | x | x | x |

| Wisconsin | x | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | x | ✓ |

| Wyoming | x | ✓ | x | x | x | x | ✓ | x | ✓ | x | x |

| District of Columbia | x | ✓ | x | x | x | ✓ | x | x | ✓ | x | x |

| Palau | x | x | x | x | x | x | x | x | x | x | x |

| Guam | x | ✓ | x | x | x | x | x | x | x | x | x |

| Puerto Rico | x | ✓ | ✓ | x | ✓ | ✓ | ✓ | ✓ | x | x | x |

| Virgin Islands | x | ✓ | x | x | x | x | ✓ | x | x | x | x |

| N. Mariana Island | x | ✓ | x | x | x | x | x | x | x | x | x |

| American Samoa | x | ✓ | x | x | x | x | x | x | x | x | x |

| Policy Type (Incentive/ Subsidy) | Changes On | Type | Date of Effective | Policy Status | Target | Implementing Agency(s) | ||

|---|---|---|---|---|---|---|---|---|

| P | R | N | ||||||

| Economic Instruments, Fiscal/financial incentives, Feed-in tariffs/premiums | Offshore wind power electricity price policy | ✓ | 5 June 2014 | In force | Wind, Offshore | National Development and Reform Commission | ||

| Economic Instruments, Fiscal/financial incentives, Taxes | State Grid Corporation of China to buy distributed PV power generation electricity | ✓ | 3 June 2014 | In force | Solar PV | State Administration of taxation | ||

| Economic Instruments, Fiscal/financial incentives, Feed-in tariffs/premiums, incentives | Renewable electricity generation bonus | ✓ | 25 Sept. 2013 | In force | All RE Sources | National Development Reform Commission | ||

| Economic Instruments, Fiscal/financial incentives, Tax relief | Policy of Solar PV electricity VAT | ✓ | ✓ | 23 September 2013 | In force | Solar PV | Ministry of Finance | |

| Economic Instruments, Fiscal/financial incentives, Grants and subsidies | PV industry promotion by exert the price leverage effect | ✓ | 1 September 2013 | In force | Solar PV | National Development Reform Commission | ||

| Policy Support, Institutional creation, Economic Instruments, Fiscal/financial incentives, Grants and subsidies | Distributed power grid management procedures | ✓ | 18 July 2013 | In force | Solar PV | National Development Reform Commission | ||

| Economic Instruments, Fiscal/financial incentives, Feed-in tariffs/premiums | Solar PV Feed-in Tariff (FIT) support | ✓ | 30 August 2013 | In force | Solar PV | National Development Reform Commission | ||

| Economic Instruments, Fiscal/financial incentives, Feed-in tariffs/premiums | Renewable Energy Electricity feed-in tariff 2012 | ✓ | 12 June 2012 | In force | All RE Sources | Ministry of Finance/NDRC/NEA | ||

| Economic Instruments, Fiscal/financial incentives, Grants and subsidies | Renewable energy development fund Imposition and Management | ✓ | 1 January 2012 | In force | All RE Sources | Ministry of Finance/NDRC/NEA | ||

| Economic Instruments, Fiscal/financial incentives, Feed-in tariffs/premiums | Feed-in tariff for solar PV | ✓ | 2011 | In force | Solar PV | National Development and Reform Commission (NDRC) | ||

| Economic Instruments, Fiscal/financial incentives, Feed-in tariffs/premiums | Solar PV building Integration program | ✓ | 2010 | In force | Solar PV | Ministry of Finance | ||

| Economic Instruments, Fiscal/financial incentives, Taxes, Economic Instruments, Feed-in tariffs/premiums | Renewable Electricity Surcharge | ✓ | ✓ | 2009 (amended 2011 and 2013) | In force | All RE Sources | Ministry of Finance | |

| Policy Support, Institutional creation, Economic Instruments, Direct investment, Economic Instruments | Renewable Energy Law (amendment) | ✓ | ✓ | 2009 | In force | All RE Sources | State Council | |

| Economic Instruments, Fiscal/financial incentives, Feed-in tariffs/premiums | Onshore wind feed-in Tariff | ✓ | ✓ | 2009 | In force | Solar PV | National Development and Reform Commission (NDRC) | |

| Economic Instruments, Fiscal/financial incentives, Feed-in tariffs/premiums | Off shore wind feed-in Tariff | ✓ | ✓ | 2009 | In force | Solar PV | National Development and Reform Commission (NDRC) | |

| Policy Support, Institutional creation, Economic Instruments, Fiscal/financial incentives, Grants and subsidies | Special Fund for the Industrialization of Wind Power Equipment | ✓ | ✓ | 2007 | In force | Wind | Ministry of Finance | |

| Country | Renewable Energy Targets | Regulatory Policies | Fiscal Incentives and Public Financing | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Feed-in-Tariff/Premium Payment | Electric Utility Quota Obligation/RPS | Net Metering | Tradable REC | Tendering | Heat Obligation/Mandate | Bio Fuels Obligation/Mandate | Capital Subsidy or Rebate | Investment or Production Tax Credits | Reductions in Sales, Energy, CO2, VAT, or Other Taxes | Energy Production Payment | Public Investment, Loans or Grants | |||

| EU Member Countries | Austria | ◦ | Ra | ● | ◦ | ● | ◦ | ◦ | ||||||

| Belgium | ◦ | ● | ● | ◦ | ◦ | ◦ | ◊ a | ◦ | ◦ | ◦ | ||||

| Bulgaria | ◦ | ◦ | ◦ | ◦ | ||||||||||

| Croatia | ◦ | ◦ | ◦ | |||||||||||

| Cyprus | ◦ | ◦ | ◊ | ◦ | ◦ | R | ||||||||

| Czech Republic | ◦ | X | ◦ | ◦ | ◦ | ◦ | ◦ | |||||||

| Denmark | ◦ | ◦ | ◦ | ◦ | ◦ | ◦ | ◦ | ◦ | ◦ | R | ||||

| Estonia | ◦ | ◦ | ◦ | ◦ | ◦ | |||||||||

| Finland | ◦ | ◦ | ◦ | ◦ | ◦ | ◦ | ◦ | |||||||

| France | R | R | ◦ | R | ◦ | ◦ | R | ◦ | ◦ | |||||

| Germany | ◦ | R | ◦ | ◦ | ◦ | ◦ | ◦ | ◦ | ||||||

| Greece | ◦ | R | ◊ | ◦ | ◦ | ◦ | ◦ | ◦ | ||||||

| Hungary | ◦ | ◦ | ◦ | ◦ | ◦ | ◦ | ||||||||

| Ireland | ◦ | ◦ | ◦ | ◦ | ● | ◦ | ||||||||

| Italy | ◦ | R | ◦ | ◦ | ◦ | R | ◦ | ◦ | ◦ | ◦ | ◦ | ◦ | ||

| Latvia | ◦ | ◦ | ◊ | ◦ | ◦ | ◦ | ||||||||

| Lithuania | ◦ | R | ◦ | ◦ | ◦ | |||||||||

| Luxembourg | ◦ | ◦ | ◦ | ◦ | ||||||||||

| Malta | ◦ | ◦ | ◦ | ◦ | ◦ | |||||||||

| Netherland | ◦ | R | R | ◦ | ◦ | ◦ | ◦ | ◦ | ◦ | ◦ | ||||

| Poland | ◦ | ◦ | ◦ | R | ◦ | ◦ | ◦ | |||||||

| Portugal | R | R | ◦ | ◦ | ◦ | ◦ | X | X | ◦ | X | ||||

| Romania | ◦ | ◦ | ◦ | ◦ | ◦ | |||||||||

| Slovakia | ◦ | R | ◦ | ◦ | ◦ | ◦ | ||||||||

| Slovenia | ◦ | ◦ | ◦ | ◦ | ◦ | ◦ | ◦ | ◦ | ||||||

| Spain | ◦ | ◦ | ◦ | ◦ | ◦ | ◦ | ◦ | |||||||

| Sweden | ◦ | ◦ | ◦ | ◦ | ◦ | ◦ | ◦ | ◦ | ||||||

| UK | R | R | ◦ | ◦ | ◦ | ◦ | R | ◦ | ◦ | ◦ | ||||

| USA | R a | R a | R a | R a | ● | R | ● | R | ◦ | X | ◦ | ◦ | R | |

| China | R | R | ◦ | ◦ | ◦ | ◦ | ◦ | ◦ | ◦ | ◦ | ◦ | |||

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ali, A.; Li, W.; Hussain, R.; He, X.; Williams, B.W.; Memon, A.H. Overview of Current Microgrid Policies, Incentives and Barriers in the European Union, United States and China. Sustainability 2017, 9, 1146. https://doi.org/10.3390/su9071146

Ali A, Li W, Hussain R, He X, Williams BW, Memon AH. Overview of Current Microgrid Policies, Incentives and Barriers in the European Union, United States and China. Sustainability. 2017; 9(7):1146. https://doi.org/10.3390/su9071146

Chicago/Turabian StyleAli, Amjad, Wuhua Li, Rashid Hussain, Xiangning He, Barry W. Williams, and Abdul Hameed Memon. 2017. "Overview of Current Microgrid Policies, Incentives and Barriers in the European Union, United States and China" Sustainability 9, no. 7: 1146. https://doi.org/10.3390/su9071146

APA StyleAli, A., Li, W., Hussain, R., He, X., Williams, B. W., & Memon, A. H. (2017). Overview of Current Microgrid Policies, Incentives and Barriers in the European Union, United States and China. Sustainability, 9(7), 1146. https://doi.org/10.3390/su9071146