Assessing the Impacts of Carbon Tax and Improved Energy Efficiency on the Construction Industry: Based on CGE Model

Abstract

1. Introduction

2. Literature Review

3. Methodology

3.1. CGE Model Specifications

3.1.1. Production Block

3.1.2. Income–Expenditure Block

3.1.3. Trade Block

3.1.4. Macroscopic-Closure and Market-Clearing Block

3.1.5. Carbon Tax Block

3.1.6. Social Welfare Block

3.2. Database and Parameters

3.3. Scenario Design

4. Results and Discussion

4.1. The Impact of Carbon Tax on the Construction Industry

4.2. The Impact of Carbon Tax on Macroeconomy

4.2.1. Macroeconomic Indicators

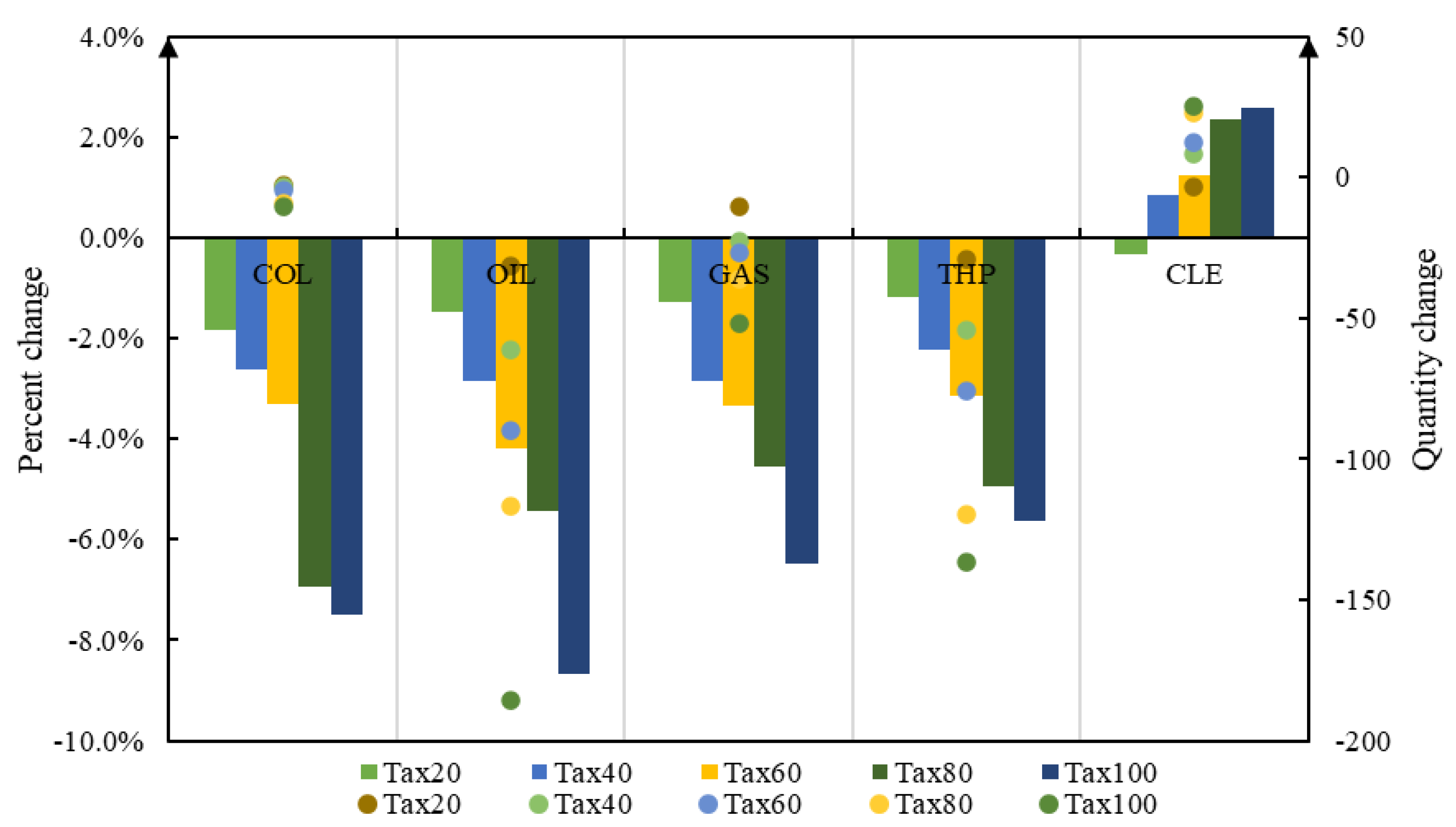

4.2.2. Energy Demand

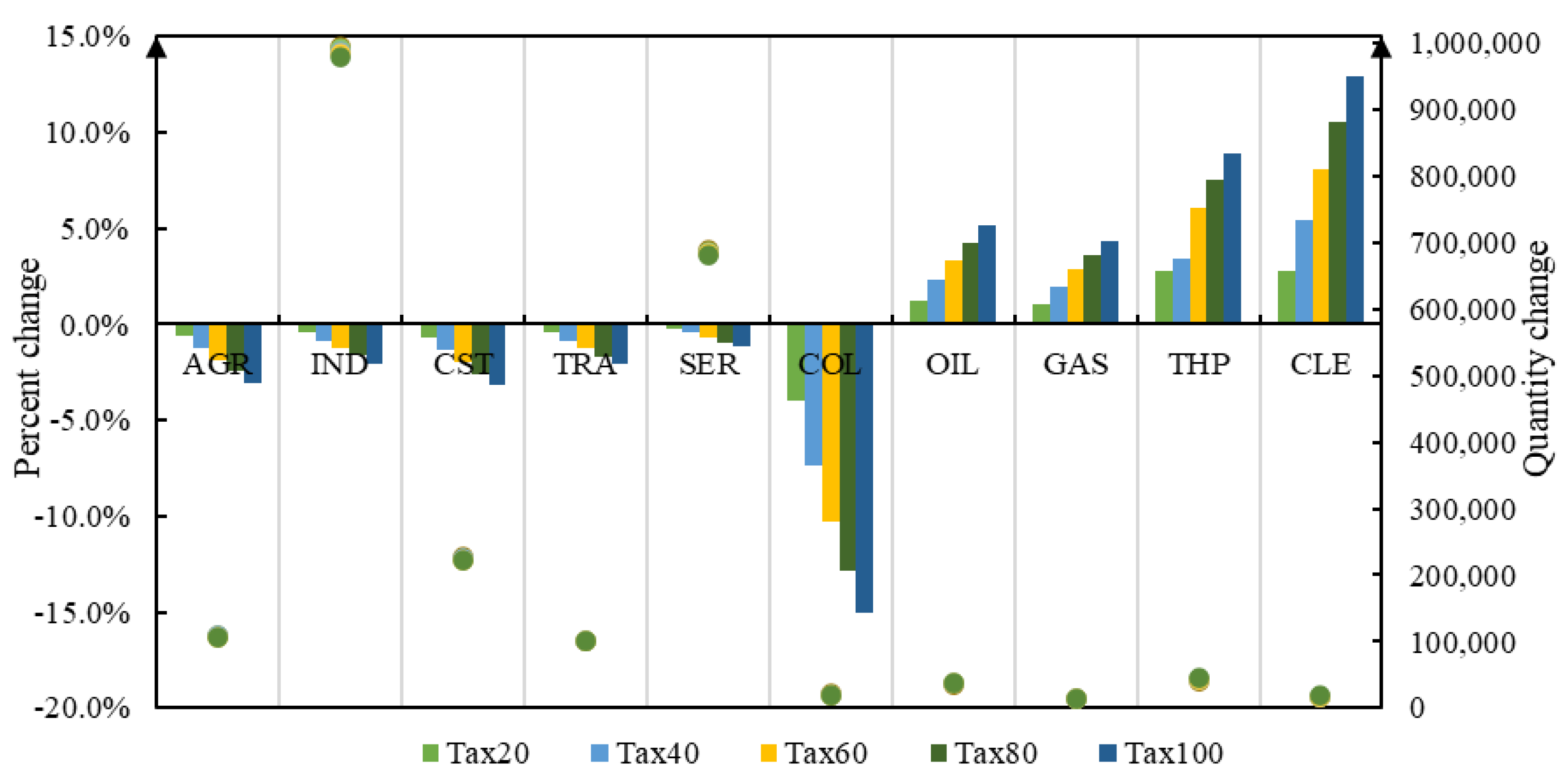

4.2.3. Sector Impacts

4.3. The Impact of Carbon Tax Revenue Recycling

4.4. The Impact of Improving Energy Efficiency

5. Conclusions and Policy Recommendations

5.1. Conclusions

5.2. Policy Recommendations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A.

Appendix A.1. Production Block

Appendix A.2. Income–Expenditure Block

Appendix A.3. Trade Block

Appendix A.4. Macroscopic-Closure and Market-Clearing Block

Appendix A.5. Carbon Tax Block

References

- Xu, G.; Wang, W. China’s Energy Consumption in Construction and Building Sectors: An Outlook to 2100. Energy 2020, 195, 117045. [Google Scholar] [CrossRef]

- Pradhan, B.K.; Ghosh, J. A Computable General Equilibrium (CGE) Assessment of Technological Progress and Carbon Pricing in India’s Green Energy Transition via Furthering Its Renewable Capacity. Energy Econ. 2022, 106, 105788. [Google Scholar] [CrossRef]

- Cheng, M.; Lu, Y.; Zhu, H.; Xiao, J. Measuring CO2 Emissions Performance of China’s Construction Industry: A Global Malmquist Index Analysis. Environ. Impact Assess. Rev. 2022, 92, 106673. [Google Scholar] [CrossRef]

- Price, L.; Khanna, N.; Zhou, N. Reinventing Fire: China-the Role of Energy EffiCiency in China’s Roadmap to 2050. Presqu’ile Giens (Hyeres Fr.) 2018, 38. [Google Scholar]

- Wang, Y.; Wang, F. Production and Emissions Reduction Decisions Considering the Differentiated Carbon Tax Regulation across New and Remanufactured Products and Consumer Preference. Urban Clim. 2021, 40, 100992. [Google Scholar] [CrossRef]

- Ding, J.; Chen, W.; Wang, W. Production and Carbon Emission Reduction Decisions for Remanufacturing Firms under Carbon Tax and Take-Back Legislation. Comput. Ind. Eng. 2020, 143, 106419. [Google Scholar] [CrossRef]

- Zepeda-Gil, C.; Natarajan, S. A Review of “Green Building” Regulations, Laws, and Standards in Latin America. Buildings 2020, 10, 188. [Google Scholar] [CrossRef]

- Luo, R.; Zhou, L.; Song, Y.; Fan, T. Evaluating the Impact of Carbon Tax Policy on Manufacturing and Remanufacturing Decisions in a Closed-Loop Supply Chain. Int. J. Prod. Econ. 2022, 245, 108408. [Google Scholar] [CrossRef]

- Luo, W.; Zhang, Y.; Gao, Y.; Liu, Y.; Shi, C.; Wang, Y. Life Cycle Carbon Cost of Buildings under Carbon Trading and Carbon Tax System in China. Sustain. Cities Soc. 2021, 66, 102509. [Google Scholar] [CrossRef]

- Levi, S. Why Hate Carbon Taxes? Machine Learning Evidence on the Roles of Personal Responsibility, Trust, Revenue Recycling, and Other Factors across 23 European Countries. Energy Res. Soc. Sci. 2021, 73, 101883. [Google Scholar] [CrossRef]

- Mardones, C. Pigouvian Taxes to Internalize Environmental Damages from Chilean Mining—A Computable General Equilibrium Analysis. J. Clean. Prod. 2022, 362, 132359. [Google Scholar] [CrossRef]

- Lin, B.; Jia, Z. The Energy, Environmental and Economic Impacts of Carbon Tax Rate and Taxation Industry: A CGE Based Study in China. Energy 2018, 159, 558–568. [Google Scholar] [CrossRef]

- He, J.; Yue, Q.; Li, Y.; Zhao, F.; Wang, H. Driving Force Analysis of Carbon Emissions in China’s Building Industry: 2000–2015. Sustain. Cities Soc. 2020, 60, 102268. [Google Scholar] [CrossRef]

- Li, B.; Han, S.; Wang, Y.; Li, J.; Wang, Y. Feasibility Assessment of the Carbon Emissions Peak in China’s Construction Industry: Factor Decomposition and Peak Forecast. Sci. Total Environ. 2020, 706, 135716. [Google Scholar] [CrossRef]

- Andersson, J.J. Carbon Taxes and CO2 Emissions: Sweden as a Case Study. Am. Econ. J. Econ. Policy 2019, 11, 1–30. [Google Scholar] [CrossRef]

- Freire-González, J.; Martinez-Sanchez, V.; Puig-Ventosa, I. Tools for a Circular Economy: Assessing Waste Taxation in a CGE Multi-Pollutant Framework. Waste Manag. 2022, 139, 50–59. [Google Scholar] [CrossRef] [PubMed]

- Feng, C.; Chang, K.; Lin, J.; Lee, T.; Lin, S. Toward Green Transition in the Post Paris Agreement Era: The Case of Taiwan. Energy Policy 2022, 165, 112996. [Google Scholar] [CrossRef]

- Matti, S.; Nässén, J.; Larsson, J. Are Fee-and-Dividend Schemes the Savior of Environmental Taxation? Analyses of How Different Revenue Use Alternatives Affect Public Support for Sweden’s Air Passenger Tax. Environ. Sci. Policy 2022, 132, 181–189. [Google Scholar] [CrossRef]

- Xu, B.; Xu, R. Assessing the Role of Environmental Regulations in Improving Energy Efficiency and Reducing CO2 Emissions: Evidence from the Logistics Industry. Environ. Impact Assess. Rev. 2022, 96, 106831. [Google Scholar] [CrossRef]

- Cheng, Y.; Sinha, A.; Ghosh, V.; Sengupta, T.; Luo, H. Carbon Tax and Energy Innovation at Crossroads of Carbon Neutrality: Designing a Sustainable Decarbonization Policy. J. Environ. Manag. 2021, 294, 112957. [Google Scholar] [CrossRef]

- Ren, S.; Hu, Y.; Zheng, J.; Wang, Y. Emissions Trading and Firm Innovation: Evidence from a Natural Experiment in China. Technol. Forecast. Soc. Chang. 2020, 155, 119989. [Google Scholar] [CrossRef]

- Yue, X.; Peng, M.Y.; Khalid, M.; Nassani, A.A.; Haffar, M.; Zaman, K. The Role of Carbon Taxes, Clean Fuels, and Renewable Energy in Promoting Sustainable Development: How Green Is Nuclear Energy? Renew. Energy 2022, 193, 167–178. [Google Scholar] [CrossRef]

- Yunzhao, L. Modelling the Role of Eco Innovation, Renewable Energy, and Environmental Taxes in Carbon Emissions Reduction in E−7 Economies: Evidence from Advance Panel Estimations. Renew. Energy 2022, 190, 309–318. [Google Scholar] [CrossRef]

- Zalejska-Jonsson, A.; Lind, H.; Hintze, S. Energy-Efficient Technologies and the Building’s Saleable Floor Area: Bust or Boost for Highly-Efficient Green Construction? Buildings 2013, 3, 570–587. [Google Scholar] [CrossRef]

- Du, H.; Chen, Z.; Zhang, Z.; Southworth, F. The Rebound Effect on Energy Efficiency Improvements in China’s Transportation Sector: A CGE Analysis. J. Manag. Sci. Eng. 2020, 5, 249–263. [Google Scholar] [CrossRef]

- Ramadhani, D.P.; Koo, Y. Comparative Analysis of Carbon Border Tax Adjustment and Domestic Carbon Tax under General Equilibrium Model: Focusing on the Indonesian Economy. J. Clean. Prod. 2022, 377, 134288. [Google Scholar] [CrossRef]

- Lin, B.; Li, X. The Effect of Carbon Tax on per Capita CO2 Emissions. Energy Policy 2011, 39, 5137–5146. [Google Scholar] [CrossRef]

- Pearce, D. The Role of Carbon Taxes in Adjusting to Global Warming. Econ. J. 1991, 101, 938. [Google Scholar] [CrossRef]

- Freeman, G.M.; Drennen, T.E.; White, A.D. Can Parked Cars and Carbon Taxes Create a Profit? The Economics of Vehicle-to-Grid Energy Storage for Peak Reduction. Energy Policy 2017, 106, 183–190. [Google Scholar] [CrossRef]

- Zhang, Y.; Qi, L.; Lin, X.; Pan, H.; Sharp, B. Synergistic Effect of Carbon ETS and Carbon Tax under China’s Peak Emission Target: A Dynamic CGE Analysis. Sci. Total Environ. 2022, 825, 154076. [Google Scholar] [CrossRef]

- Povitkina, M.; Carlsson Jagers, S.; Matti, S.; Martinsson, J. Why Are Carbon Taxes Unfair? Disentangling Public Perceptions of Fairness. Glob. Environ. Chang. 2021, 70, 102356. [Google Scholar] [CrossRef]

- Shobande, O.A.; Shodipe, O.T. Carbon Policy for the United States, China and Nigeria: An Estimated Dynamic Stochastic General Equilibrium Model. Sci. Total Environ. 2019, 697, 134130. [Google Scholar] [CrossRef] [PubMed]

- Bruvoll, A.; Larsen, B.M. Greenhouse Gas Emissions in Norway: Do Carbon Taxes Work? Energy Policy 2004, 32, 493–505. [Google Scholar] [CrossRef]

- Jiang, H.D.; Liu, L.J.; Deng, H.M. Co-Benefit Comparison of Carbon Tax, Sulfur Tax and Nitrogen Tax: The Case of China. Sustain. Prod. Consum. 2022, 29, 239–248. [Google Scholar] [CrossRef]

- Hu, H.; Dong, W.; Zhou, Q. A Comparative Study on the Environmental and Economic Effects of a Resource Tax and Carbon Tax in China: Analysis Based on the Computable General Equilibrium Model. Energy Policy 2021, 156, 112460. [Google Scholar] [CrossRef]

- Khastar, M.; Aslani, A.; Nejati, M. How Does Carbon Tax Affect Social Welfare and Emission Reduction in Finland? Energy Reports 2020, 6, 736–744. [Google Scholar] [CrossRef]

- Kula, E.; Evans, D. Dual Discounting in Cost-Benefit Analysis for Environmental Impacts. Environ. Impact Assess. Rev. 2011, 31, 180–186. [Google Scholar] [CrossRef]

- Kirchner, M.; Sommer, M.; Kratena, K.; Kletzan-Slamanig, D.; Kettner-Marx, C. CO2 Taxes, Equity and the Double Dividend—Macroeconomic Model Simulations for Austria. Energy Policy 2019, 126, 295–314. [Google Scholar] [CrossRef]

- Freire-González, J. Environmental Taxation and the Double Dividend Hypothesis in CGE Modelling Literature: A Critical Review. J. Policy Model. 2018, 40, 194–223. [Google Scholar] [CrossRef]

- Speck, S. Environmental Tax Reform and the Potential Implications of Tax Base Erosions in the Context of Emission Reduction Targets and Demographic Change. Econ. Polit. 2017, 34, 407–423. [Google Scholar] [CrossRef]

- Zhao, A.; Wang, J.; Sun, Z.; Guan, H. Environmental Taxes, Technology Innovation Quality and Firm Performance in China—A Test of Effects Based on the Porter Hypothesis. Econ. Anal. Policy 2022, 74, 309–325. [Google Scholar] [CrossRef]

- Dadzie, J.; Runeson, G.; Ding, G.; Bondinuba, F.K. Barriers to Adoption of Sustainable Technologies for Energy-Efficient Building Upgrade-Semi-Structured Interviews. Buildings 2018, 8, 57. [Google Scholar] [CrossRef]

- Du, Q.; Han, X.; Li, Y.; Li, Z.; Xia, B.; Guo, X. The Energy Rebound Effect of Residential Buildings: Evidence from Urban and Rural Areas in China. Energy Policy 2021, 153, 112235. [Google Scholar] [CrossRef]

- Dumortier, J.; Elobeid, A. Effects of a Carbon Tax in the United States on Agricultural Markets and Carbon Emissions from Land-Use Change. Land Use Policy 2021, 103, 105320. [Google Scholar] [CrossRef]

- Fu, Y.; Huang, G.; Liu, L.; Zhai, M. A Factorial CGE Model for Analyzing the Impacts of Stepped Carbon Tax on Chinese Economy and Carbon Emission. Sci. Total Environ. 2021, 759, 143512. [Google Scholar] [CrossRef]

- Wesseh, P.K.; Lin, B. Environmental Policy and ‘Double Dividend’ in a Transitional Economy. Energy Policy 2019, 134, 110947. [Google Scholar] [CrossRef]

- Carroll, D.A.; Stevens, K.A. The Short-Term Impact on Emissions and Federal Tax Revenue of a Carbon Tax in the U.S. Electricity Sector. Energy Policy 2021, 158, 112526. [Google Scholar] [CrossRef]

- Malerba, D.; Gaentzsch, A.; Ward, H. Mitigating Poverty: The Patterns of Multiple Carbon Tax and Recycling Regimes for Peru. Energy Policy 2021, 149, 111961. [Google Scholar] [CrossRef]

- Xiang, D.; Lawley, C. The Impact of British Columbia’s Carbon Tax on Residential Natural Gas Consumption. Energy Econ. 2019, 80, 206–218. [Google Scholar] [CrossRef]

- Liu, J.; Bai, J.; Deng, Y.; Chen, X.; Liu, X. Impact of Energy Structure on Carbon Emission and Economy of China in the Scenario of Carbon Taxation. Sci. Total Environ. 2021, 762, 143093. [Google Scholar] [CrossRef]

- Wing, I.S. Computable General Equilibrium Models for the Analysis of Economy–environment Interactions. Res. Tools Nat. Resour. Environ. Econ. 2011, 9, 255–306. [Google Scholar] [CrossRef]

- Guo, Z.; Li, T.; Shi, B.; Zhang, H. Economic Impacts and Carbon Emissions of Electric Vehicles Roll-out towards 2025 Goal of China: An Integrated Input-Output and Computable General Equilibrium Study. Sustain. Prod. Consum. 2022, 31, 165–174. [Google Scholar] [CrossRef]

- Weng, Y.; Chang, S.; Cai, W.; Wang, C. Exploring the Impacts of Biofuel Expansion on Land Use Change and Food Security Based on a Land Explicit CGE Model: A Case Study of China. Appl. Energy 2019, 236, 514–525. [Google Scholar] [CrossRef]

- Li, Y.; Su, B. The Impacts of Carbon Pricing on Coastal Megacities: A CGE Analysis of Singapore. J. Clean. Prod. 2017, 165, 1239–1248. [Google Scholar] [CrossRef]

- Sabine, G.; Avotra, N.; Olivia, R.; Sandrine, S. A Macroeconomic Evaluation of a Carbon Tax in Overseas Territories: A CGE Model for Reunion Island. Energy Policy 2020, 147, 111738. [Google Scholar] [CrossRef]

- Zhou, Y.; Fang, W.; Li, M.; Liu, W. Exploring the Impacts of a Low-Carbon Policy Instrument: A Case of Carbon Tax on Transportation in China. Resour. Conserv. Recycl. 2018, 139, 307–314. [Google Scholar] [CrossRef]

- Guo, Z.; Zhang, X.; Zheng, Y.; Rao, R. Exploring the Impacts of a Carbon Tax on the Chinese Economy Using a CGE Model with a Detailed Disaggregation of Energy Sectors. Energy Econ. 2014, 45, 455–462. [Google Scholar] [CrossRef]

- Shi, Q.; Ren, H.; Cai, W.; Gao, J. How to Set the Proper Level of Carbon Tax in the Context of Chinese Construction Sector? A CGE Analysis. J. Clean. Prod. 2019, 240, 117955. [Google Scholar] [CrossRef]

- Dannenberg, A.; Mennel, T.; Moslener, U. What Does Europe Pay for Clean Energy?—Review of Macroeconomic Simulation Studies. Energy Policy 2008, 36, 1318–1330. [Google Scholar] [CrossRef]

- Zhao, X.; Xue, Y.; Ding, L. Implementation of Low Carbon Industrial Symbiosis Systems under Financial Constraint and Environmental Regulations: An Evolutionary Game Approach. J. Clean. Prod. 2020, 277, 124289. [Google Scholar] [CrossRef]

- Chan, Y.; Zhao, H. Optimal carbon tax rates in a dynamic stochastic general equilibrium model with a supply chain. Econ. Model. 2022, 119, 106109. [Google Scholar] [CrossRef]

- Du, Q.; Yan, Y.; Huang, Y.; Hao, C.; Wu, J. Evolutionary Games of Low-Carbon Behaviors of Construction Stakeholders under Carbon Taxes. Int. J. Environ. Res. Public Health 2021, 18, 508. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| No. | Abbr. | Sectors | Description |

|---|---|---|---|

| 1 | AGR | Agriculture | Agriculture, forestry, animal husbandry and fishing industry |

| 2 | IND | Industry | Manufacture of metal and non-metallic ore mining, chemical, machinery products, etc. |

| 3 | CST | Construction | Building construction |

| 4 | TRA | Transportation | Transportation, warehousing and post |

| 5 | SER | Service | Culture, entertainment, health, education, information technology, service, etc. |

| 6 | COL | Coal | Mining and processing of coal |

| 7 | OIL | Oil | Extraction of petroleum |

| 8 | GAS | Gas | Extraction of natural gas |

| 9 | THP | Thermal power | Coal, gas, gasoline, diesel and other fuels generate power to generate electricity |

| 10 | CLE | Clean power | Production and supply of clean power |

| Scenarios | Description | Carbon Tax Rate (RMB/t-CO2) |

|---|---|---|

| BAU | - | - |

| Tax20 | The carbon tax rate is set as 20 RMB/t-CO2 | 20 |

| Tax40 | The carbon tax rate is set as 40 RMB/t-CO2 | 40 |

| Tax60 | The carbon tax rate is set as 60 RMB/t-CO2 | 60 |

| Tax80 | The carbon tax rate is set as 80 RMB/t-CO2 | 80 |

| Tax100 | The carbon tax rate is set as 100 RMB/t-CO2 | 100 |

| Recy1 | No tax revenue recycling, the carbon tax on construction revenue is considered a government fiscal revenue | 60 |

| Recy2 | Recycling of carbon tax revenue to households | 60 |

| Recy3 | Recycling of carbon tax revenue to households and sectoral investment | 60 |

| IEE5% | Improving energy efficiency by 5% | 60 |

| IEE10% | Improving energy efficiency by 10% | 60 |

| IEE15% | Improving energy efficiency by 15% | 60 |

| Variables | Percentage Changes from Carbon Tax Exemption (%) | ||

|---|---|---|---|

| Recy1 | Recy2 | Recy3 | |

| Energy demand | −5.233% | −4.990% | −4.245% |

| Carbon emissions | −11.141% | −10.950% | −10.759% |

| Total output | −0.951% | −0.897% | −0.842% |

| GDP | −0.948% | −0.890% | −0.833% |

| Social welfare | −0.757% | −0.497% | −0.235% |

| Variables | Percentage Changes from Improving Energy Efficiency (%) | ||

|---|---|---|---|

| IEE5% | IEE10% | IEE15% | |

| GDP | 1.922% | 3.575% | 5.010% |

| HY | 2.097% | 3.903% | 5.473% |

| HD | 1.044% | 1.952% | 2.748% |

| HS | 1.318% | 2.713% | 5.152% |

| GY | 0.245% | 0.430% | 0.572% |

| GC | −1.259% | −2.331% | −3.252% |

| GS | 0.245% | 0.430% | 0.572% |

| TINV | 2.281% | 4.249% | 5.960% |

| ENCO2 | −7.790% | −14.569% | −20.510% |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Du, Q.; Dong, Y.; Li, J.; Zhao, Y.; Bai, L. Assessing the Impacts of Carbon Tax and Improved Energy Efficiency on the Construction Industry: Based on CGE Model. Buildings 2022, 12, 2252. https://doi.org/10.3390/buildings12122252

Du Q, Dong Y, Li J, Zhao Y, Bai L. Assessing the Impacts of Carbon Tax and Improved Energy Efficiency on the Construction Industry: Based on CGE Model. Buildings. 2022; 12(12):2252. https://doi.org/10.3390/buildings12122252

Chicago/Turabian StyleDu, Qiang, Yanan Dong, Jingtao Li, Yuelin Zhao, and Libiao Bai. 2022. "Assessing the Impacts of Carbon Tax and Improved Energy Efficiency on the Construction Industry: Based on CGE Model" Buildings 12, no. 12: 2252. https://doi.org/10.3390/buildings12122252

APA StyleDu, Q., Dong, Y., Li, J., Zhao, Y., & Bai, L. (2022). Assessing the Impacts of Carbon Tax and Improved Energy Efficiency on the Construction Industry: Based on CGE Model. Buildings, 12(12), 2252. https://doi.org/10.3390/buildings12122252