Abstract

Contrary to the conventional viewpoint that “high housing price promotes industrial upgrading”, this study finds that increasingly high housing prices are a pivotal factor that obstructs industrial value chain upgrading. Based on city-level data, micro-level data for Chinese industrial enterprises, and data for listed Chinese enterprises, this study examines the impacts of urban housing prices on value chain upgrading. We find that soaring housing prices in China since 2004 stunted industrial value chain upgrading, as indicated by the value-added rate. When housing prices increase by 100%, the enterprise value-added rate decreases by 12.4%. Intermediary mechanism analysis shows that housing price increases lead to innovation input suppression effects and resource misallocation effects, which in turn obstruct industrial value chain upgrading. Further analysis demonstrates that the impacts of housing price increases on industrial value chain upgrading, presenting an inverted-U shape, are varied in terms of time and region. Enterprises’ value chain upgrading also showcases different degrees of sensitivity to housing price increases, due to their respective features. The conclusions of this study carry significant policy implications for the sound development of the real estate market and industrial upgrading in China, as well as in developing countries at large.

1. Introduction

Since the 1990s, vertical specialization featured by separation of production processes in different locations has promoted global value chain (GVC) specialization, which has brought unprecedented development opportunities for developing countries. During that process, China tapped into its labor cost and policy advantages that followed its reforms and opening-up. Due to international relocation of industries on a large scale, products “made in China” have been increasingly embedded into the GVC. However, China’s manufacturing industry is still at the medium or low end of the GVC. It is large in scale, but weak in terms of core competitiveness. Due to the lack of high-end factors, such as core technologies and brands, China’s manufacturing industry is experiencing hardship in moving up the value chain. In another words, China is facing the severe issue of low-end lock-in. Apparently, low-end lock-in of the manufacturing industry runs counter to the current goal of high-quality economic development in China, which is an issue facing all developing countries. Such issues also impose vital impacts on developing countries’ engagement in global climate change governance. Suffering from low-end lock-in in their manufacturing industries, developing countries tend to be “conservative” in setting their goals for carbon emission peaks and carbon neutrality.

In terms of the factors influencing developing countries’ value chain upgrading, there are internal reasons, such as factor endowment and external constraints on industrial development. Developing countries are subject to factor endowment in the early stages of development; they specialize in labor-intensive industries and low-end processing in high-end industries. Taking the supply chain Apple Inc. as an example, China manufactures or assembles the vast majority of Apple’s electronic products, but claims less than 2% of the value added (Kraemer et al., 2011) [1], which is much lower than that of the other processing procedures in the Apple industrial chain. By examining the role of factor input in industrial upgrading at both the industry and enterprise levels, Yang and Huang (2014) [2] argued that technological innovation and the simultaneous increase in materials and human capital—in particular, the accumulation of human capital—help in realizing manufacturing upgrading in China. Moreover, research by Poon (2004) [3] demonstrated that technological level and marketing capability are important indications of competitiveness, which are also the key factors in driving enterprises to enter capital-intensive and technology-intensive sectors. Qu et al., (2020) [4] believed that China’s manufacturing industry needs to switch from factor-driven and investment-driven development to innovation-driven growth. Efforts should be made in original innovation and basic research. In-depth cooperation with multinationals should be promoted in R&D, brand design, marketing channels, etc., to move up the GVC and stop being held as a “captive” at the low end.

With respect to external conditions, factors affecting manufacturing upgrading or GVC elevation include the service level of the manufacturing industry (Neely, 2008; Kastalli & Looy, 2003; Crozet & Milet, 2017) [5,6,7], the presence of multinational firms (Saliola & Zanfei, 2008) [8], and industrial policy (Cheng & Kwan, 2000; Wang, 2013) [9,10], among others. It is worth noting that the prosperity and rapid expansion of the real estate industry may also influence manufacturing upgrading and GVC elevation. In fact, when China’s GVC participation rate showcased a substantial increase, housing prices in China also skyrocketed. The annual increase in average housing prices from 2000 to 2013 in China was 8.69%. The increase in 35 Chinese medium and large cities from 2004 to 2013 was as high as 11.65%. Surging housing prices attract wide attention from academia. Recent years have witnessed the emergence of a series of studies on the impacts of housing prices’ on economic activities, including their impacts on consumer spending (Kishor, 2007; Dong et al., 2017) [11,12], investment risk (Gang et al., 2021) [13], labor flow (Laamanen, 2013) [14], resource allocation efficiency (Zhou et al., 2020) [15], economic growth (Collyns & Senhadji, 2003; Hui et al., 2007; Miller et al., 2011) [16,17,18], credit constraints (Corradin and Popov, 2015) [19], etc.

It is also worth mentioning that current research on the impacts of housing prices on manufacturing upgrading has not reached a consensus. Some scholars believe that increases in housing prices can significantly promote industrial upgrading. For example, research by Rong and Ni (2020) [20] and Gan (2007) [21] revealed that housing price increases boost capital appreciation for property-owning enterprises, which enhances their external financing capacity. This means that such enterprises are able to obtain additional investments for technological innovation and enterprise upgrading. Helpman (1998) [22] maintained that housing prices affect the relative utility of labor, and thus suppress the clustering of labor in a region. In addition, Foote (2016) [23] demonstrated that housing price increases exert positive wealth effects and negative lock-in effects on the migration decisions of home-owning laborers. To put it differently, high housing prices suppress labor inflow (Rabe & Taylor, 2012) [24] and elevate salary levels and enterprise production costs, delivering crowd-out effects on low added-value and labor-intensive industries in a region (Liang et al., 2016) [25]. However, for technology-intensive enterprises that are insensitive to housing prices, rent costs, and labor costs, employees continue to cluster in the region. As a result, enterprises in such a region gradually climb up the value chain and ultimately realize industrial upgrading through industrial restructuring (Cai, 2021) [26]. However, and conversely, other researchers have found that housing price increases stunt industrial upgrading. Housing price increases generate high-return investment opportunities in the real estate industry. Capital in the manufacturing industry will be drawn into the real estate industry. When enterprises invest in the real estate industry, their input in R&D and innovation invariably decreases, which prevents technological innovation and exerts negative impacts in industrial upgrading (Rong et al., 2016) [27]. Sun and Tang (2021) [28] also found that housing price increases significantly suppress the upgrading of the industrial mix in local and neighboring regions by distorting capital, inhibiting consumption, crowding out labor, and other means. The above research on the relation between housing prices and industrial upgrading employs a three-sector structure to indicate industrial upgrading in a region. Such an inaccurate measure may be the reason for the contradictory conclusions among current studies. As Zhou et al. (2018) [29] pointed out, the changes in a three-sector structure mainly reflect the evolution of the industrial structure over time, instead of industrial upgrading. Such a measurement fails to display the internal messages of manufacturing industry. Enterprise upgrading and industrial upgrading are, in essence, added-value increases for products (Pietrobelli & Rabellotti, 2006) [30], which are displayed by the transition from producing low value-added products to producing high value-added products, coupled with enterprise status elevation in the product chain or the product value chain (Gereffi, 1999) [31].

Based on the above literature review, the current research on the effect of housing price increases on manufacturing upgrading presents several gaps to fill. First, research on the impact of housing prices on enterprise upgrading is, in China and the world at large, inadequate, especially empirical research on the impact of housing prices on industrial upgrading at a micro level. Second, due to the inadequacy in micro-level research, current macro-level research is conducted by measuring industrial upgrading on the basis of shares in a certain type of industry. The results may be biased, as neither the value-added of products nor the elevation of value chain status is taken into account. Third, in terms of the impact mechanism, the cross-region flow of labor is interpreted as the intermediary mechanism through which housing prices affect industrial structural upgrading. The micro-level mechanism of the impact of housing prices on enterprise-upgrading is neglected. To fill these gaps, this study employs micro-level data of Chinese enterprises, unravels the impact of housing prices on industrial upgrading from the perspective of value chain on an empirical basis, and explores the micro-level mechanism through which housing prices affect industrial upgrading. Compared with current research, this study makes its contribution in the following three ways: first, in terms of the research angle, this study examines the impact of housing prices on industrial upgrading from the perspective of the enterprise value chain on an empirical basis for the first time; second, in terms of research sample, this study selects industrial enterprises from Chinese industrial and listed-enterprises databases from 2001 to 2013 as samples, which is a breakthrough compared with previous research based on the three-sector industrial structure; third, in terms of research content, unlike previous research focusing on the impacts of housing prices on industrial structural transformation, this study concentrates on the impact of housing prices on upgrading within an industry, reveals the intermediary mechanism through which housing prices affect industrial upgrading, and explores the heterogeneous impact of housing prices on enterprise upgrading.

2. Theoretical Analysis and Hypothesis

2.1. Empirical Facts in Relation to the Value-Added Rate and Housing Prices

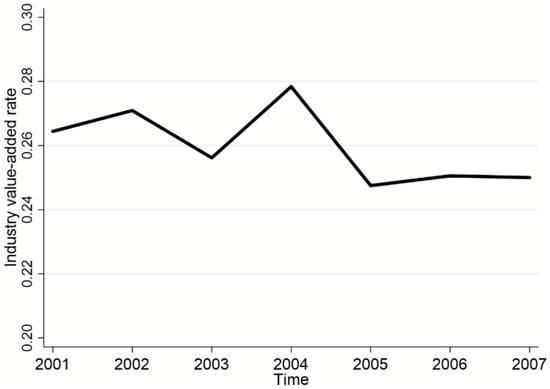

Industrial upgrading refers to industrial transformation from low value-added and low-technology status to high value-added and high-technology status (Pietrobelli & Rabellotti, 2006; Azadegan & Wagner, 2011; Su et al., 2017) [30,32,33]. After nearly four decades of development, China is now equipped with a solid industrial foundation. However, China is still at the low end on the GVC and is facing tremendous pressure in promoting industrial upgrading, as indicated by the industry value-added rate. From a lateral perspective, a huge divide between China and developed countries can be found in terms of the industry value-added rate. China’s industry value-added rate is below 30%, while that of the developed countries is normally over 35%. The value-added rate in the United States and Germany exceeds 40% (Huang, 2014) [34]. From a longitudinal perspective, China’s industry value-added rate showcases a downward trend in fluctuation. There was a structural downturn in 2014 (Figure 1).

Figure 1.

Industry value-added rate in 35 Chinese medium or large cities, 2001–2007.

Researchers explain the low industry value-added rate in China on the basis of the division of labor in the GVC. They believe China is “captive” to and “oppressed” within the GVC. Chinese enterprises have been locked in low-cost manufacturing for a long time and have developed paths that are dependent on technologies (Qu et al., 2020) [4]. When China’s manufacturing industry is fully embedded into the GVC, manufacturing upgrading—as indicated by value-added rate—will be directly affected by the international division of labor. The receipt of industries that relocate from other parts of the world, and/or increasing the input in intermediate products, lowers to some extent the value-added rate of China (Xia & Zhang, 2015) [35]. Apart from the impact of the division of labor in the GVC, China’s industrial upgrading is dependent on factor endowment changes (Su et al., 2017; Wang & Yang, 2020) [33,36]. However, enterprises’ factor input and their participation in the division of labor in the GVC remained stable over time and they did not experience structural changes in 2004. Therefore, these factors are not the reasons for the structural changes in value-added rate of China.

Since industrial upgrading is the evolution from the low value-added end to the high value-added end, we can identify factors obstructing China’s manufacturing upgrading, other than the division of labor in the GVC and factor endowment, as long as the factor resulting in the structural changes in the value-added rate is found. Based on this, what could be the factor suppressing China’s manufacturing upgrading? Real estate industry expansion and rapid housing price increases driven by the government may be important reasons.

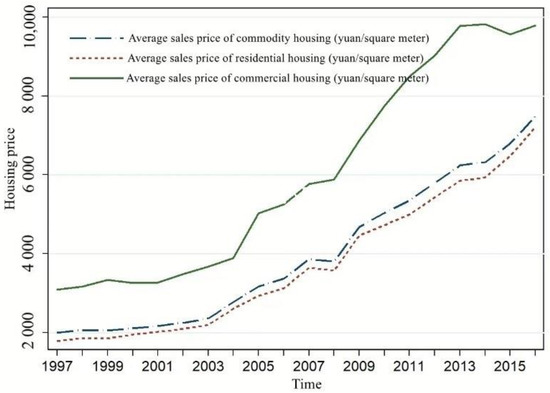

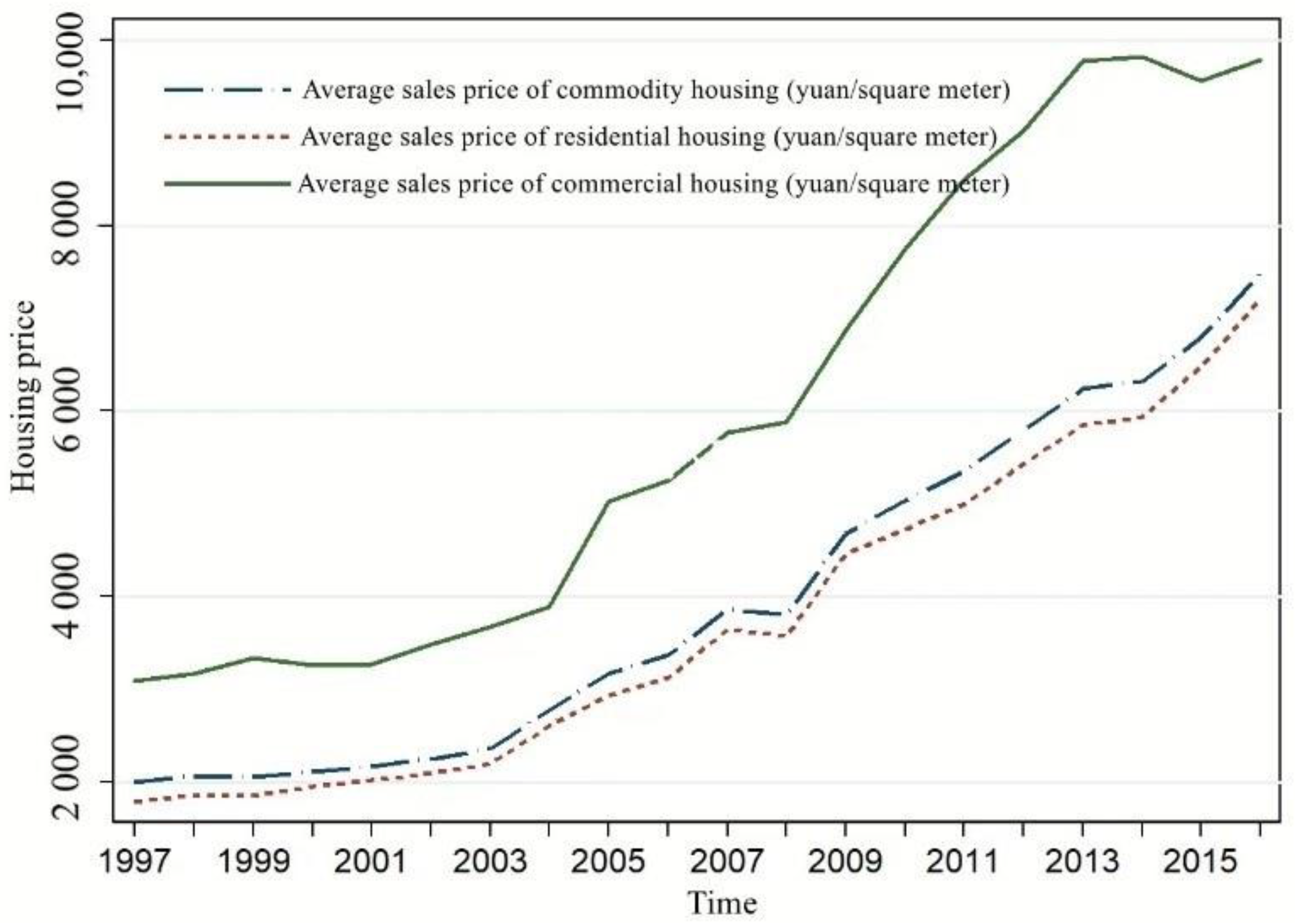

Even though China started all-round market-based housing reform in 1998, that reform did not directly lead to housing price increases. Figure 2 shows that 2004 witnessed rapid housing price increases in China. Commercial housing, in particular, experienced rapid increases in 2005. In fact, commodity housing price increases in China were only 14.3% from 1998 to 2003, with an annual average increase rate of 2.7%. Starting in 2004, commodity housing prices began to surge, increasing by 169% from 2004 to 2010 with an annual average increase of 8.6%. This indicates that housing prices skyrocketed, while the industry value-added rate plummeted. Based on this empirical fact, we believe there is a causal relation, instead of a coincidence, between the decline in the industry value-added rate and the rapid increase in housing prices around 2004.

Figure 2.

Average sales price of commodity housing, 1997–2016.

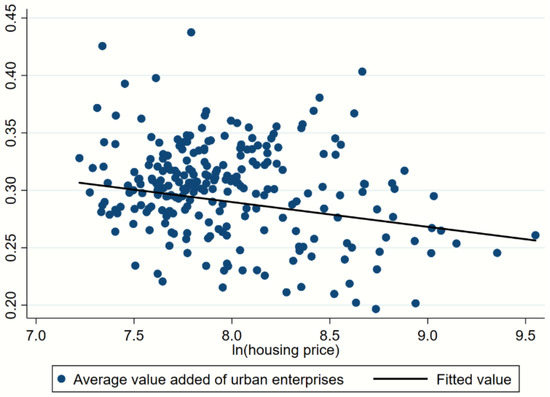

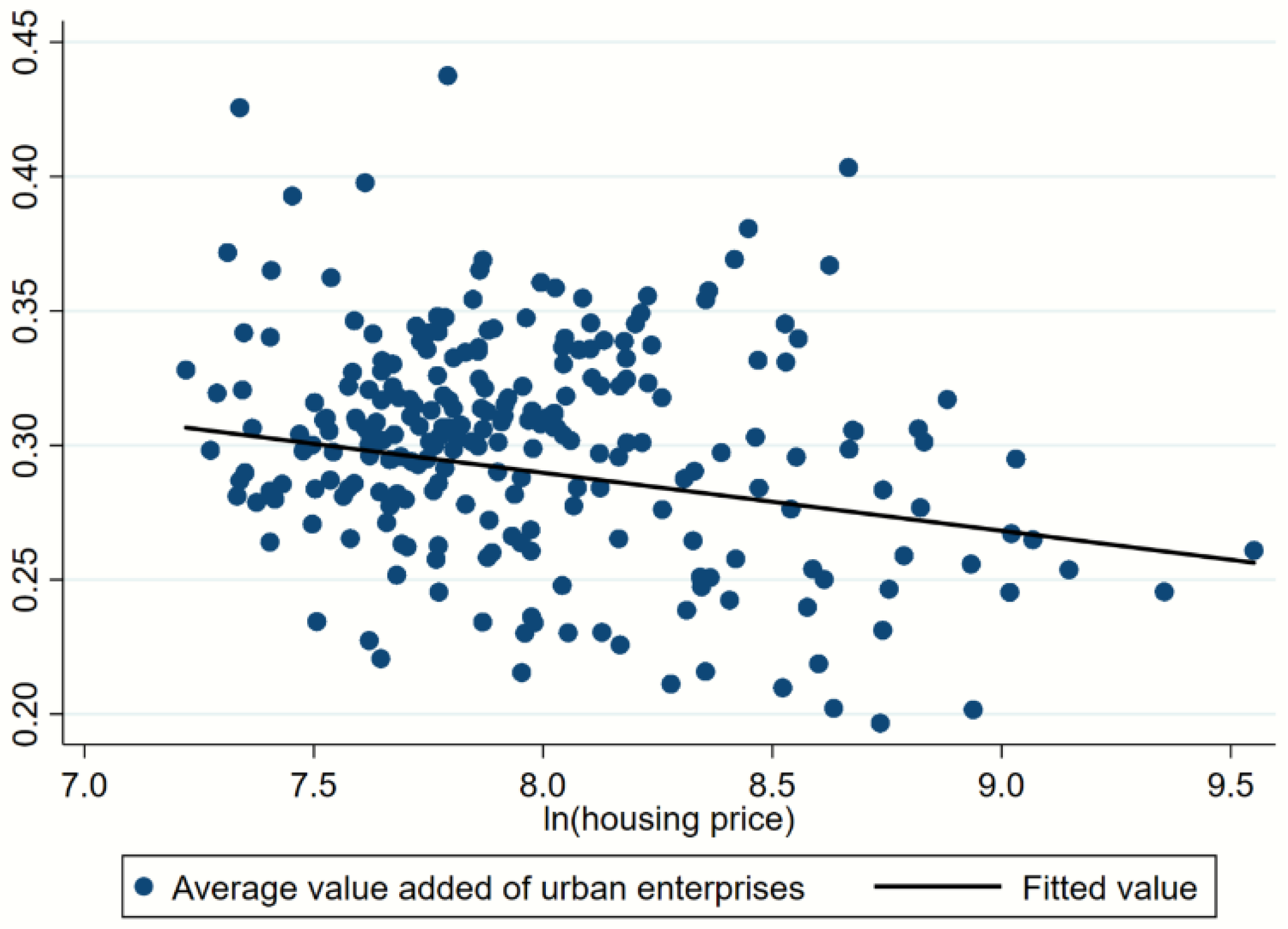

To further investigate the correlation between housing prices and the industry value-added rate, we sketched a scatter diagram of housing prices (logarithm) and the industry value-added rate of 35 Chinese medium and large cities from 2001 to 2007 (Figure 3). The scatter diagram showcases an evident negative correlation between the average industry value-added rate and housing prices.

Figure 3.

Enterprise average value-added rate and housing prices.

2.2. Impact Mechanism of Urban Housing Price Increases on Value Chain Upgrading

How do increases in housing prices affect industrial chain upgrading? From the perspective of production, technological input and resource allocation efficiency determine value added. Therefore, this study explores the impact mechanism through which an increase in urban housing prices affects value chain upgrading, from the angles of innovation input and resource allocation.

(1) Suppression effects of housing price increases on innovation input. According to the bubble theory, a real estate bubble exerts both a positive and negative effect on enterprises’ innovation input; that is, a credit easing effect and a crowd-out effect (Miao and Wang, 2014) [37]. On the one hand, high housing prices resulting from real estate bubble-led resources, such as the land and housing owned by enterprises, to appreciate, which mitigates the enterprises’ collateral constraints and promotes investment and R&D input by enterprises (Gan, 2007; Chaney et al., 2012) [21,38]. On the other hand, a real estate bubble crowds out resources, because it encourages enterprises to invest more capital into the real estate market, which is irrelevant to their key business (Campello et al., 2010) [39], causing such enterprises to reduce their investments and R&D in their key business. Bank loans are vital sources of enterprises’ input in R&D. When housing prices surge, a real estate sector bubble can lead to more bank loans, crowding credit out of industry enterprises (Bleck and Liu, 2018) [40]. Due to financing constraints, the innovation input of industry enterprises is suppressed. As far as China is concerned, the “crowd-out effect” of housing price increases on innovation input is prominent. Chen et al. (2015) [41] demonstrated, based on the empirical analysis of listed enterprises from 1998 to 2012, that the “crowd-out effect” of housing price increases overshadows their credit-easing effects on innovation input. Based on empirical research on major Chinese cities, Miao and Wang (2014) [37] found that housing price changes suppressed R&D intensity in non-real estate enterprises.

(2) Resource misallocation effects of housing price increases. Hsieh and Klenow (2009) [42] found that improvement in resource allocation in China can increase industrial output by 110%. If the resource allocation efficiency in China can reach the same level as that of the United States, China’s total factor productivity (TFP) can increase from 30% to 50%. This demonstrates the vital significance of resource allocation on China’s industrial upgrading and value chain elevation. Excessive housing price increases cause profits in real estate-related industries to soar, which further widens the profit gap between industry enterprises and real estate enterprises. Such massive interests drive industry enterprises to channel resources to the real estate sector, where higher profits can be gained. However, productivity in the real estate industry and related industries is much lower than that of the industry sector. When resources are relocated from high-productivity enterprises to low-productivity ones, resource allocation efficiency and overall industrial productivity decrease. Such misallocation hinders the driving force for industrial upgrading within a country. The research of Bai and Xu (2018) [43] revealed that the distorted development of the real estate market in China, beginning in 2004, was a vital reason for capital misallocation, where capital flocks out of the real economy and swarms into the real estate industry. In addition, soaring housing prices in cities exert negative impacts on the allocation of innovative talents, which are the integral factor for enterprises to move up the value chain from the lower end. The clustering of innovative talents helps in realizing a cluster economy and industrial upgrading. As housing prices increase, hindrances—such as decreases in incomes caused by uncertainty—propels innovative talents to diffuse instead of clustering, which suppresses industrial upgrading. Zhang et al., (2017) [44] found, based on data from the China Labor-force Dynamic Survey, that the suppression effect of high housing prices is stronger on highly skilled labor.

Based on the above analysis, this study proposes the following hypothesis: housing prices exert negative impacts on enterprises’ value chain elevation. Its innovation input suppression effects and resource misallocation effects serve as the intermediary mechanisms. In addition, considering the huge differences in housing prices in various regions, the impact of housing prices on the value chain elevation of enterprises may, accordingly, be different in different regions.

3. Materials and Methods

3.1. Econometric Model

As enterprises are major players in an economic system, the impacts of housing prices on the upgrading of the industrial value chain are delivered by affecting an enterprise’s status in the value chain. Compared with high-level data from an industry or a region, enterprise-level data reveal the micro-level mechanism through which housing prices affect the value chain. Therefore, this study selects micro data at the enterprise level as samples and makes an estimation based on the following equation.

where i, j, k, and t represent enterprise, industry, city, and year, respectively (same below). is the indicator showcasing the value chain elevation of enterprises. denotes urban housing prices. is the control variable set at the enterprise level, while is the control variable set at the city level. is the random error. denotes enterprises’ status change in value chain over urban housing prices, which reflects the impact of housing price levels on the value added of enterprises. , , and are the constant term, coefficient of enterprise-level control variables, and coefficient of city-level control variables, respectively. , , and represent enterprise, industry, and time effects, respectively.

3.2. Variable Selection and Description

Dependent variable. This study uses the value-added rate—that is, the ratio of the value added of an industrial enterprise to its total output—as a measure of its industrial chain elevation.

Independent variable. The average sales price of commodity housing in the city where an enterprise is located is the core independent variable, which is calculated by dividing commodity housing sales revenue by the total of the commodity housing sold.

Control variables. One set of control variables includes the characteristics of enterprises, including the following: capital input, denoted by the proxy variable net fixed assets; labor input, denoted by the number of employees in the survey year; intermediary product input; enterprise age and the square of enterprise age; enterprise size, denoted by the logarithm of total assets; stakeholding by the state (which is rendered as 1 if the state holds stocks in the enterprise and 0 otherwise); stakeholding by foreign investors (which is 1 if over 25% of the paid-up capital is from foreign investor, and 0 otherwise); and export condition (which is 1 if the enterprise’s export exceeds nil, and 0 otherwise). The other set of control variables includes the characteristics of cities, including per capita GDP, share of the secondary industry, share of the tertiary industry, and foreign direct investment (FDI).

3.3. Data Source

The enterprise-level data used in this study came from two datasets. One was the database of the National Bureau of Statistics of China for industrial enterprises with an annual sales revenue of over five million yuan. This database contains basic and financial information of all stated-owned enterprises and non-SOEs with an annual sales revenue of over five million yuan. These enterprises contribute 85% of the industrial output in China and represent the overall situation of industrial enterprises in China. Industrial enterprises in China are mainly located in provincial capitals and central cities. Rising housing prices are more common in medium and large cities. Therefore, this study selected industrial enterprises located in 35 Chinese medium or large cities as research samples The 35 medium or large cities are identified by the National Bureau of Statistics of China as the major cities in China. Available online: http://data.stats.gov.cn/easyquery.htm?cn=E0105, (accessed on 11 November 2021). After excluding abnormal samples and deleting enterprises with only one year of data, we obtained unbalanced panel data with over 470,000 samples spanning a period of two to seven years. This paper mainly used these data to examine the impact and intermediate mechanism of urban housing prices on value chain upgrading.

The other data focus on the enterprises listed on the A share of the Shanghai Stock Exchange or the Shenzhen Stock Exchange. A total of 1413 manufacturing enterprises were adopted as the research samples and their data are from China Stock Market & Accounting Research Database, which provides basic information about enterprises, such as their operation status and their financial indicators. Samples from 2010 to 2013 were used to avoid any potential influence of the 2008–2009 global financial crisis on enterprise upgrading. It is worth noting that data on housing prices in cities of listed enterprises after 2013 are not available, because the China Statistical Yearbook for Regional Economy is no longer published. We also winsorized enterprise-level data at 1% in each tail. This paper mainly used these data to perform a robust analysis.

Corresponding city-level data was derived from the China Statistical Yearbook for Regional Economy, the China City Statistical Yearbook, and the database of the National Bureau of Statistics of China. Table 1 presents the model variables and the statistical descriptions.

Table 1.

Descriptive statistics of model variables.

3.4. Endogeneity and Instrumental Variable

Logically, there may be an endogeneity issue in the relationship between housing prices in a city and the value-added rate of enterprises. First, there may be a reverse causal relationship between the value-added rate of enterprises and housing prices, which ultimately results in engodegenity. Cities with high value-added rates among enterprises are often from regions with relatively high levels of economic development and factor endowment. In these cities, housing demand is met by increasing salaries at enterprises, which causes housing prices to increase. Therefore, the existence of a reverse causal relationship leads to an underestimation of OLS coefficients. Second, the endogeneity of housing prices impacts on the value-added rate of enterprises may be due to potentially neglected variables. This study considered a series of variables related to city-level and enterprise-level characteristics and employed time, enterprise, and industry-fixed effects to mitigate the impacts of unobservable factors. However, in theory, there may still be omitted variables that affect enterprise upgrading. Therefore, if the impact of unobservable factors were not controlled, the estimate results of the OLS would be biased.

This study mitigated potential endogeneity through instrumental variables to lower the biases of estimate results. The underlying logic was to find an exogenous variable that could only affect the value-added rate through housing prices as the instrumental variable. Referring to the practice of Liang et al. (2016) [25], this study selected per capita area of land supply as the instrumental variable for urban housing prices. The main reason for that choice was that the per capita area of land supply, as the instrumental variable for urban housing prices, satisfies two premises. First, the area of land supply directly affects urban housing prices in China (Du and Peiser, 2014; Shen et al., 2018) [45,46]. Second, the per capita area of land supply does not affect the value-added rate of enterprises through channels other than housing prices. With no direct link with industrial enterprises, the per capital area of land supply is mainly influenced by local government and by the real estate market. However, it may affect the value-added rate of urban industrial enterprises by promoting economic development. Considering such a possibility, this study considered per capita GDP, share of the secondary industry, and share of the tertiary industry in the regression model. After such treatments, the per capita area of land supply could hardly affect housing prices through unobservable factors, thus satisfying the second premise. Based on the above analysis, the per capita area of land supply was a suitable instrumental variable for urban housing prices. Furthermore, this study employed, based on the OLS regression model, a two-stage least square (2SLS) for coefficient estimation of the econometric model. The per capita area of land supply was obtained by dividing the area of urban land supply by the total urban population. The area of urban land supply was derived from the China Statistical Yearbook for Land Resources, while the urban population data were from the China City Statistical Yearbook for the relevant years.

4. Results and Discussion

4.1. Benchmark and Robustness Test

Table 2 reports the overall regression results on the relationship between urban housing prices and the value-added rate of enterprises. Column (1) exhibits the simple regression results of fixed effects. The regression coefficient of housing prices indicates that the higher the housing prices, the lower the value-added rate of enterprises. A 100% increase in urban housing price leads to a 1.174% decrease in the value-added rate of enterprises. In column (2), enterprise-level control variables are introduced. The regression results show that the coefficients of housing price remain negative. A 100% increase in housing prices results in a 4.21% decline in the value-added rate of enterprises. City-level control variables are introduced to column (3), where the coefficients of housing prices are still negative at a statistically significant level, showcasing housing prices’ significant and negative impacts on enterprises’ value-added rate. Columns (4) to (6) in Table 2 display 2SLS estimate results on the instrumental variable. Table 3 presents the results of the first stage. First-stage regression results in each column of Table 3 show a high degree of negative correlation between the instrumental variable (the per capita area of land supply) and urban housing prices at the 1% significance level, with or without control variables. This means that housing prices in regions with a higher per capita area of land supply are lower, which is in line with the theoretical analysis on the premise of the use of the instrumental variable, previously stated. The regression results of 2SLS, from columns (4) to (6), indicate a significantly negative relationship between urban housing prices and the value-added rate of industrial enterprises. The estimate coefficient is larger than that of OLS, demonstrating possible endogeneity. Therefore, we took the estimate results from 2SLS for analysis of control variables. In summary, through the instrumental variables, we further confirmed that an increase in housing prices is one of the key factors leading to a decline in enterprises’ value-added rates.

Table 2.

The basic regression result of housing prices and the enterprise added-value rate.

Table 3.

Regression results of the first stage of instrumental variables.

In terms of other control variables, the regression coefficients of capital and labor were positive at a statistically significant level, demonstrating the promoting effects of capital and investment input on enterprises’ value-added rate. The regression coefficients of intermediary product input were significantly negative, revealing that increases in outsourced products or services led enterprises’ value-added rates to decline. The relation between enterprise age and value-added rate turned on an inverted-U shape. Young enterprises were more dynamic, with a stronger driving force for upgrading, while older enterprises showed weaker strength in upgrading. Enterprise size was positively correlated to enterprises’ value-added rate, showcasing the effects of economy of scale on enterprise upgrading. The impact on enterprise upgrading of government subsidy and stockholding by foreign investors was not statistically significant. The value-added rate of export enterprises was higher, because export enterprises harness foreign market to acquire higher product value added. Per capita GDP, FDI, share of a secondary industry, and share of a tertiary industry delivered positive impacts on enterprises’ value-added rate at a statistically significant level, demonstrating the promoting effects of urban economic development level, utilization degree of foreign capital, industrialization level, and service level on enterprise upgrading.

To ensure the robustness of our conclusion, we replaced overall housing prices with urban residential housing prices for regression. OLS and 2SLS were employed for econometric analysis on the relationship between urban housing prices and the value-added rate of enterprises to verify the robustness of the conclusion. Table 4 shows the regression results for the relationship between urban residential housing price and the value-added rate of enterprises. Based on the regression results in Table 4, urban housing prices in general suppress enterprise upgrading, as indicated by the value-added rate. However, due to regional differences in housing prices, the inverted-U impacts of housing prices on enterprise upgrading still exist. Such robustness analysis offers empirical support for the conclusions of this study.

Table 4.

Regression results of urban housing prices and the enterprise added-value rate.

Due to data availability for industrial enterprises, the above analysis only examined the impacts of housing prices on industrial value chain upgrading during the early period of housing increases (2005–2007). The results showed that relatively high housing prices exert evidently negative impacts on the upgrading of Chinese industrial enterprises. To ensure that the conclusions drawn in this study are universal, we employed data for 1413 listed manufacturing enterprises from 2010 to 2013 to investigate the relationship between housing prices and the value chain upgrading of the listed enterprises. The regression results in Table 5 demonstrate that housing prices deliver negative impacts on the value-added rate of listed enterprises at the 10% significance level. The impacts of housing prices on the value-added rate of enterprises remained significantly negative, irrespective of the enterprise characteristics variables. This illustrates that urban housing price increases impose significantly negative impacts on the value chain upgrading of enterprises, which once again verifies the reliability of the conclusion.

Table 5.

Regression results of urban housing prices and the value-added rate of listed enterprises.

4.2. Period-Based Test on Relation between Urban Housing Prices and Enterprises’ Value-Added Rate

Urban housing prices in China remained stable until 2004, after which they started to soar. The overall obstructing effects of urban housing prices on enterprise upgrading became prominent after 2004, before which the effects may have been trivial. Therefore, we regarded the year 2004 as the break point and divided samples into two groups for tests. The regression results are shown in Table 6. For regression results on samples before 2004, the coefficients of housing price in column (5) were positive at a statistically significant level. The coefficients became negative but were statistically insignificant when we introduced city-level control variables in column (6). This demonstrated that the obstructing effects of housing prices on enterprise upgrading was not significant on a whole before 2004. Housing prices may even have promoted enterprise upgrading by promoting urban economic development. However, in terms of the estimate results of OLS and 2SLS in 2004 and afterwards, the coefficients of urban housing prices were negative at the 1% significance level, showcasing the robust obstructing effects of housing prices on enterprise upgrading after 2004.

Table 6.

Temporal regression results of housing prices and the enterprise added-value rate.

4.3. Analysis of Influential Mechanism

The empirical results in section 4 demonstrated that urban housing price increases since 2004 exerted obstructing effects on the value chain upgrading of industrial enterprises in general. According to the theoretical analysis on impact mechanisms in this study, surging urban housing prices stunted value chain upgrading by urban industrial enterprises through innovation suppression effects and resource misallocation effects. In this section, we verify the existence of the intermediary mechanism, i.e., housing prices’ suppression effects and resource misallocation effects on the R&D input of industrial enterprises. As the R&D input value of many enterprises is zero, this study used the dummy variable of R&D to measure enterprises’ innovation input level. If the regression coefficient of the impacts of housing prices on R&D input is negative, it shows that housing prices lower an enterprise’s motivation in R&D input. We utilized TFP to measure resource allocation efficiency. If the negative impacts of urban housing prices on enterprise TFP were identified, it meant that housing prices generated resource misallocation effects. TFP data for enterprises were estimated by the LP method, and the logarithm of TFP was adopted in the regression. As key information, such as R&D input, is missing in data before 2004, we excluded that information in the regression analysis. That is, this section only adopts samples from 2005 to 2007.

According to the test method of Baron and Kenny (1986) [47], the procedure for the mechanism test is as follows: (1) regress urban housing prices with enterprise R&D input and enterprise TFP, respectively. If the regression coefficient is significant, it shows that urban housing prices deliver impacts on enterprise R&D input and enterprise TFP; (2) regress the value-added rate of enterprises with enterprise R&D input and enterprise TFP, respectively. If the regression coefficient is significant, it shows that enterprise R&D input and TFP exert influences on value-added rate of enterprises; (3) when the above two results hold, regress housing prices, enterprise R&D input, and enterprise TFP with the value-added rate of enterprises simultaneously. If the regression coefficient of urban housing prices declines or becomes insignificant, it shows that urban housing prices affect the value-added rate of enterprises through the intermediary variable, partly or completely.

Following the above test procedure, we established the empirical model as follows:

Step one: verify whether urban housing prices affect enterprise innovation and TFP.

Step two: verify whether enterprise innovation and TFP affect the value-added rate of enterprises.

Step three: put enterprise innovation, TFP, and urban housing prices into the model simultaneously.

Table 7 exhibits the test results of the intermediary mechanism model, where columns (1) to (3) are test results of the suppression effects on R&D input and columns (4) to (6) are the test results of resource misallocation effects. First, we shed light on the test results of the suppression effects on R&D input. The step-one results demonstrated that housing prices significantly lower enterprises’ motivation in R&D input. Enterprises from cities with higher housing prices showed lower possibilities in R&D input. The coefficient was significant at the 1% level. The step-two regression results revealed enterprises’ R&D input significantly increased enterprises’ value-added rate, which was significant at the 1% level. This shows enterprises’ R&D input is beneficial to value chain upgrading of enterprises. The step-three regression results showed that when housing prices and R&D input were added simultaneously, the impact coefficient of housing prices on enterprises’ value-added rate was −0.0092, which represented a large degree of decline compared with a housing price regression coefficient of −0.0389 when R&D input was not added into regression. The significance level also dropped. This demonstrated that urban housing price increases since 2004 resulted in evident suppression effects on innovation input, which obstructed enterprise upgrading. As for the test results of resource misallocation effects, the step-one regression results showed that housing prices significantly lowered enterprises’ TFP. Enterprises from cities with higher housing prices indicated lower TFP, whose coefficient was significant at the 1% level. The step-two regression results indicated that enterprises’ TFP significantly increased the value-added rate of enterprises at the 1% significance level, meaning that improvement of enterprises’ TFP promoted enterprise upgrading. The step-three regression results revealed that when housing prices and TFP were added into the regression simultaneously, the impact coefficient of housing prices on enterprises’ value-added rate became statistically insignificant. This demonstrated that urban housing price increases since 2004 resulted in obvious resource misallocation, which obstructed enterprise upgrading. Column (7) of Table 7 displays the regression results on the value-added rate when R&D input, TFP, housing prices, and other control variables were added. The impact coefficient of both R&D input and TFP on enterprises’ value-added rate was positive at the 1% significance level. The impact coefficient of housing prices on value-added rate of enterprises also became statistically insignificant. These results verified that housing price increases obstruct enterprise upgrading through innovation suppression effects and resource misallocation effects.

Table 7.

Test results of intermediate mechanism.

5. Conclusions

This study employed data for industrial enterprises in 35 Chinese medium or large cities from 2001 to 2007 and data of 1413 listed enterprises to investigate the impacts of urban housing prices on the value chain upgrading of such enterprises. In addition, this study explored the intermediary mechanism, the non-linear characteristics, and the heterogeneity of the impacts of housing prices on enterprises’ value chain upgrading. The empirical results demonstrate the following:

(1) In general, housing prices deliver significant obstructing effects on value chain upgrading of Chinese industrial enterprises. When the per capita area of land supply is adopted as the instrumental variable for housing prices, housing prices still significantly suppress enterprises’ value chain upgrading. However, there are differences in the impacts of housing prices on enterprises’ value upgrading, in terms of time. From 2005 to 2007, 100% increases in housing prices led enterprises’ value-added rate to decrease by 12.4%.

(2) Analysis on the intermediary mechanism showed that soaring housing prices since 2004 obstructed enterprises’ value chain upgrading, through innovation suppression effects and resource misallocation effects.

(3) Due to the huge differences in housing prices in various regions, the impacts of housing prices on enterprises’ value chain upgrading also indicated region-based variance. Further analysis indicated that urban housing prices delivered non-linear and inverted-U impacts on enterprise upgrading. The tipping housing price was 3720 yuan/m2. Furthermore, the impacts of housing prices on the value chain upgrading of industrial enterprises are heterogeneous, in terms of ownership, size, export, and subsidy.

(4) Test results based on listed enterprises revealed that the value chain upgrading of listed manufacturing enterprises is also subject to the obstructing effects of urban housing price increases. When overall housing prices were replaced by residential housing prices for robustness checks, the results showed that housing prices still suppressed enterprises’ value chain upgrading.

The conclusions drawn in this study carry rich policy implications.

(1) The government and the relevant department(s) should pay attention to the negative impacts of surging housing prices on industrial upgrading and the development of the real economy. Driving housing price increases for industrial upgrading and growth of the real economy, a practice exercised by some cities, is detrimental. In the long term, as it will only lead to economic issues such as a low level of innovation, resource misallocation, lock-in in low-end industries, and a sluggish growth driver. Therefore, the establishment of a long-term and effective mechanism for stable housing prices and curbing rapid housing price increases is of great significance for economic structural adjustment, industrial transformation and upgrading, and economic growth.

(2) Efforts should be made to promote market-based reform for the real estate market. High housing prices deliver innovation input suppression effects and resource misallocation effects on industrial enterprises. On the one hand, housing prices should be kept at a stable range in the long term to avoid a decline in investment in R&D and in the main business of enterprises. Meanwhile, the government should encourage enterprises to increase innovation input through fiscal and taxation policies, to create a favorable atmosphere for technological innovation. On the other hand, market-based reform for interest rates and factors should accelerate. The government should eliminate the distortion in the factor market and promote financial institutional reform to lower the degree of resource misallocation. For example, market-based measures such as a property tax can be adopted to avoid the overflow of capital into the real estate sector.

(3) City-specific real estate policies should be implemented. The impacts of housing prices on enterprises’ value chain upgrading are varied in different cities. There is no one-size-fits-all policy for all cities. For a city where housing prices surpass the threshold and start to negatively affect enterprise-upgrading, comprehensive regulations on housing prices are beneficial to industrial upgrading in the city. Central and western Chinese cities, where housing prices are relatively low, are weaker in industrial foundation and lack geographical advantages compared with eastern seaboard cities. Such cities should remain on guard against the negative impacts of housing price increases on industrial upgrading. However, viewed from the other perspective, the relatively low housing prices in central and western Chinese cities are advantages. By offering premium public services and infrastructures, these cities can accommodate industries relocated from eastern China and realize industrial upgrading.

It is worth stating that it is still possible to generalize valuable information from the results even though the data are almost 10 years old. First, although some changes may have taken place in markets, cities, and enterprises during this period, the interaction between real estate and manufacturing has not changed in nature. In recent years, the Chinese government has successively issued many regulatory policies to promote the healthy development of the real estate market and the transformation and upgrading of the manufacturing industry. Therefore, balancing the relationship between real estate and the manufacturing industry is still a hot topic in China’s political and academic circles at this stage. Second, although the research data are old, the research conclusions still have important reference value for the healthy development of China’s real estate market and for realizing the upgrading of the manufacturing industry and high-quality economic development. Moreover, our research conclusions have certain enlightenment significance for some developing countries that are in the primary stages of industrialization.

Author Contributions

Conceptualization, Y.Y., X.Z., S.Z. and Y.L.; methodology, Y.Y. and X.Z.; software, Y.Y. and X.Z.; validation, S.Z.; formal analysis, Y.Y. and X.Z.; investigation, S.Z.; resources, Y.Y. and X.Z.; data curation, Y.Y. and X.Z.; writing—original draft preparation, Y.Y., X.Z. and S.Z.; writing—review and editing, Y.Y.; visualization, X.Z.; supervision, S.Z.; project administration, Y.L.; funding acquisition, Y.L. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by the National Social Science Foundation of China (17ZDA046), the Research Foundation of Education Bureau of Hunan Province (19B198), and the Natural Science Foundation of Hunan Province of China (2021JJ40215).

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data presented in this study are available on request from the corresponding author.

Acknowledgments

The authors are particularly grateful to all researchers for providing data support for this study.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Kraemer, K.L.; Linden, G.; Dedrick, J. Capturing Value in Global Networks: Apple’s Ipad and Iphone. Available online: http://economiadeservicos.com/wp-content/uploads/2017/04/value_ipad_iphone.pdf (accessed on 10 July 2021).

- Gaoju, Y.; Xianhai, H. Internal Drivers and the Specialization Status of Under-developed Countries: Evidence from China’s High-tech Industry. Soc. Sci. China 2014, 35, 106–121. [Google Scholar] [CrossRef]

- Poon, T.S. Beyond the Global Production Networks: A Case of Further Upgrading of Taiwan's Information Technology Industry. Int. J. Technol. Glob. 2004, 1, 130–144. [Google Scholar] [CrossRef]

- Qu, C.; Shao, J.; Cheng, Z. Can Embedding in Global Value Chain Drive Green Growth in China’s Manufacturing Industry? J. Clean. Prod. 2020, 268, 121962. [Google Scholar] [CrossRef]

- Neely, A. Exploring the Financial Consequences of the Servitization of Manufacturing. Oper. Manag. Res. 2008, 1, 103–118. [Google Scholar] [CrossRef] [Green Version]

- Kastalli, I.V.; Van looy, B. Servitization: Disentangling the Impact of Service Business Model Innovation on Manufacturing Firm Performance. J. Oper. Manag. 2013, 31, 169–180. [Google Scholar] [CrossRef] [Green Version]

- Crozet, M.; Milet, E. Should Everybody Be in Services? The Effect of Servitization on Manufacturing Firm Performance. J. Econ. Manag. Strategy 2017, 26, 820–841. [Google Scholar] [CrossRef]

- Saliola, F.; Zanfei, A. Multinational Firms, Global Value Chains and the Organization of Knowledge Transfer. Res. Policy 2009, 38, 369–381. [Google Scholar] [CrossRef]

- Cheng, L.K.; Kwan, Y.K. What Are the Determinants of the Location of Foreign Direct Investment? The Chinese Experience. J. Int. Econ. 2000, 51, 379–400. [Google Scholar] [CrossRef]

- Wang, J. The Economic Impact of Special Economic Zones: Evidence from Chinese Municipalities. J. Dev. Econ. 2013, 101, 133–147. [Google Scholar] [CrossRef]

- Kishor, N.K. Does Consumption Respond More to Housing Wealth Than to Financial Market Wealth? If So, Why? J. Real Estate Financ. Econ. 2007, 35, 427–448. [Google Scholar] [CrossRef]

- Dong, Z.; Hui, E.C.; Jia, S. How Does Housing Price Affect Consumption in China: Wealth Effect or Substitution Effect? Cities 2017, 64, 1–8. [Google Scholar] [CrossRef]

- Gang, J.; Peng, L.; Zhang, J. Are Pricier Houses Less Risky? Evidence from China. J. Real Estate Financ. Econ. 2021, 63, 662–677. [Google Scholar] [CrossRef]

- Laamanen, J. Home-ownership and the Labour Market: Evidence from Rental Housing Market Deregulation. Labour Econ. 2017, 48, 157–167. [Google Scholar] [CrossRef] [Green Version]

- Zhou, H.; Wang, Y.; Gao, L.; Wu, H. How Housing Price Fluctuation Affects Resource Allocation: Evidence from China. Emerg. Mark. Financ. Trade 2020, 56, 3084–3094. [Google Scholar] [CrossRef]

- Collyns, C.; Senhadji, A. Lending Booms, Real Estate Bubbles, and the Asian Crisis. In Asset Price Bubbles: The Implication for Monetary, Regulatory and International Policies; Mit Press: Cambridge, UK; London, UK, 2003; pp. 25–101. [Google Scholar]

- Hui, E.C.; Yue, S. Housing Price Bubbles in Hong Kong, Beijing and Shanghai: A Comparative Study. J. Real Estate Financ. Econ. 2006, 33, 299–327. [Google Scholar] [CrossRef]

- Miller, N.; Peng, L.; Sklarz, M. House Prices and Economic Growth. J. Real Estate Financ. Econ. 2011, 42, 522–541. [Google Scholar] [CrossRef]

- Corradin, S.; Popov, A. House Prices, Home Equity Borrowing, and Entrepreneurship. Rev. Financ. Stud. 2015, 28, 2399–2428. [Google Scholar] [CrossRef] [Green Version]

- Rong, Z.; Ni, J. How Do Housing Cycles Influence Listed Firms’ R&d Investment: Evidence from the Collateral Channel. Econ. Innov. New Technol. 2020, 29, 287–312. [Google Scholar]

- Gan, J. Collateral, Debt Capacity, and Corporate Investment: Evidence from a Natural Experiment. J. Financ. Econ. 2007, 85, 709–734. [Google Scholar] [CrossRef] [Green Version]

- Helpman, E. The Size of Regions In’topics in Public Economics: Theoretical and Applied Analysis; Cambridge University Press: Cambridge, UK, 1998. [Google Scholar]

- Foote, A. The Effects of Negative House Price Changes on Migration: Evidence Across Us Housing Downturns. Reg. Sci. Urban Econ. 2016, 60, 292–299. [Google Scholar] [CrossRef]

- Rabe, B.; Taylor, M.P. Differences in Opportunities? Wage, Employment and House-price Effects on Migration. Oxf. Bull. Econ. Stat. 2012, 74, 831–855. [Google Scholar] [CrossRef]

- Liang, W.; Lu, M.; Zhang, H. Housing Prices Raise Wages: Estimating the Unexpected Effects of Land Supply Regulation in China. J. Hous. Econ. 2016, 33, 70–81. [Google Scholar] [CrossRef]

- Shukai, C. An Analysis of the “direct Effect” and “indirect Effect” of Urban Housing Prices on the Upgrading of Industrial Structure—Based on Data of 285 Cities. In Journal of Physics: Conference Series; Iop Publishing: Bristol, UK, 2021; p. 12017. [Google Scholar]

- Rong, Z.; Wang, W.; Gong, Q. Housing Price Appreciation, Investment Opportunity, and Firm Innovation: Evidence from China. J. Hous. Econ. 2016, 33, 34–58. [Google Scholar] [CrossRef]

- Sun, C.; Tang, Y.F. Urban house price fluctuation and industrial structure adjustment:empirical evidence from the spatial spill-over horizon. J. Shanxi Univ. (Philos. Soc. Sci. Ed.) 2021, 43, 68–82. (In Chinese) [Google Scholar]

- Zhou, M.; Lu, Y.; Du, Y.; Yao, X. Special Economic Zones and Region Manufacturing Upgrading. China Ind. Econ. 2018, 3, 62–79. (In Chinese) [Google Scholar]

- Pietrobelli, C.; Rabellotti, R. Upgrading to Compete Global Value Chains, Clusters, and Smes in Latin America. Rev. Adm. Contemp. 2009, 13, 522–523. [Google Scholar]

- Gereffi, G. International Trade and Industrial Upgrading in the Apparel Commodity Chain. J. Int. Econ. 1999, 48, 37–70. [Google Scholar] [CrossRef]

- Azadegan, A.; Wagner, S.M. Industrial Upgrading, Exploitative Innovations and Explorative Innovations. Int. J. Prod. Econ. 2011, 130, 54–65. [Google Scholar] [CrossRef]

- Su, H.; Zheng, L.; Mou, Y.F. Factor Endowment and China's Manufacturing Industry Upgrading: An Analysis Based on WIOD and China Industrial Enterprise Database. Manag. World 2017, 4, 70–79. (In Chinese) [Google Scholar]

- Huang, Q.H. “The New Normal”, the Late Stage of Industrialization and the New Power of Industrial Growth. China Ind. Econ. 2014, 10, 5–19. (In Chinese) [Google Scholar]

- Xia, M.; Zhang, H.X. The Change of Value-added and Value-added Rate of Transnational Production and Trade—Theoretical Analysis of Value-added Rate Based on Input-output Framework. Manag. World 2015, 2, 32–44. (In Chinese) [Google Scholar]

- Jianmin, W.; Li, Y. Does Factor Endowment Allocation Improve Technological Innovation Performance? An Empirical Study on the Yangtze River Delta Region. Sci. Total Environ. 2020, 716, 137107. [Google Scholar] [CrossRef] [PubMed]

- Miao, J.; Wang, P. Sectoral bubbles, misallocation, and endogenous growth. J. Math. Econ. 2014, 53, 153–163. [Google Scholar] [CrossRef]

- Chaney, T.; Sraer, D.; Thesmar, D. The Collateral Channel: How Real Estate Shocks Affect Corporate Investment. Am. Econ. Rev. 2012, 102, 2381–2409. [Google Scholar] [CrossRef] [Green Version]

- Campello, M.; Graham, J.R.; Harvey, C.R. The Real Effects of Financial Constraints: Evidence from a Financial Crisis. J. Financ. Econ. 2010, 97, 470–487. [Google Scholar] [CrossRef] [Green Version]

- Bleck, A.; Liu, X. Credit Expansion and Credit Misallocation. J. Monet. Econ. 2018, 94, 27–40. [Google Scholar] [CrossRef]

- Chen, T.; Liu, L.X.; Zhou, L.A. The Crowding-out Effects of Real Estate Shocks—Evidence from China; Social Science Electronic Publishing: Rochester, NY, USA, 2015; pp. 1–39. [Google Scholar]

- Hsieh, C.T.; Klenow, P.J. Misallocation and Manufacturing TFP in China and India. Q. J. Econ. 2009, 124, 1403–1448. [Google Scholar] [CrossRef] [Green Version]

- Bai, P.W.; Xu, J. Capital Stock and the Rate of Return to Capital in the Three Industries and the Convergence Hypothesis in China: 1978–2013. China Econ. Q. 2018, 17, 1171–1206. (In Chinese) [Google Scholar]

- Zhang, L.; He, J.; Ma, R.H. How Housing Price Affects Labor Migration? Econ. Res. J. 2017, 52, 155–170. (In Chinese) [Google Scholar]

- Du, J.; Peiser, R.B. Land supply, pricing and local governments' land hoarding in China. Reg. Sci. Urban Econ. 2014, 48, 180–189. [Google Scholar] [CrossRef]

- Shen, X.; Huang, X.; Li, H.; Li, Y.; Zhao, X. Exploring the relationship between urban land supply and housing stock: Evidence from 35 cities in China. Habitat Int. 2018, 77, 80–89. [Google Scholar] [CrossRef]

- Baron, R.M.; Kenny, D.A. The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. J. Personal. Soc. Psychol. 1986, 51, 1173–1182. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).