A Generative Adversarial Network for Financial Advisor Recruitment in Smart Crowdsourcing Platforms

Abstract

:1. Introduction

- We develop a smart crowdsourcing approach to leverage the process of financial advisors recruitment.

- We combine the concept of crowdsourcing and artificial intelligence to optimize the recruitment of financial advisors and hence, enhance the portfolio’s performances.

- We extrapolate the investor–advisors recruitment process into an image processing process where we employ GAN to generate financial advisors’ profiles based on the investors’ profiles.

- We perform a many-to-many matching to solve an ILP task while maximize the commutative return of the investors and hence, financial advisors.

2. Crowdsourcing-Based System Components

2.1. Financial Advisors’ Profiles

2.2. Investors’ Profiles

2.3. Crowdsourcing Server

3. Proposed Recruitment Framework

3.1. Financial Advisors’ Signature Encoding

3.2. Financial Advisors’ Signatures Generation (FASG) Phase

- is the discriminator’s estimate of the probability that a real financial advisor signature f is real.

- is the expected value over all real data instances f.

- is the generator’s output given an investor profile i.

- is the discriminator’s estimate of the probability that a generated financial advisor signature is real.

- is the expected value over all generated fake instances .

3.2.1. The Discriminator

3.2.2. The Generator

3.3. Advisor to Investor (AIM) Matching Phase

4. Results and Discussions

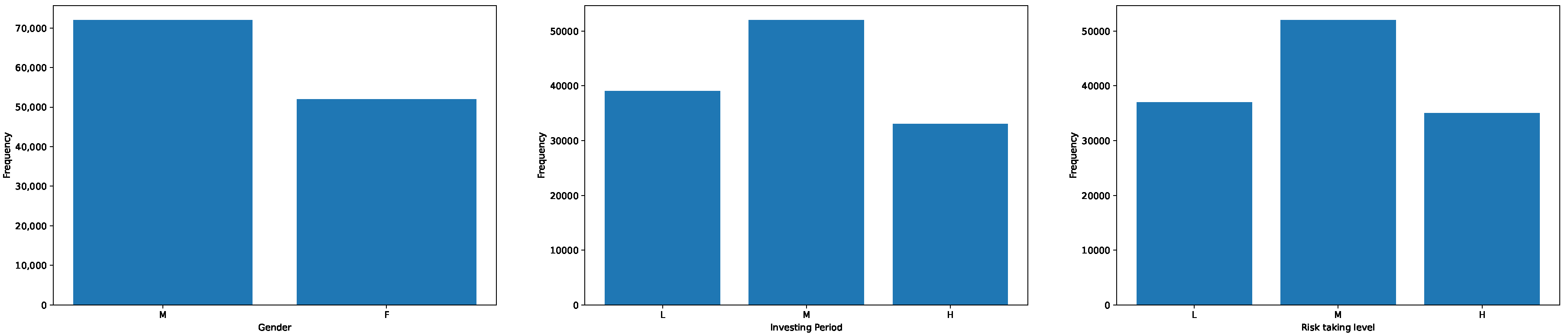

4.1. Investigated Data Sets

- AdvisorBN: Boolean variable indicating if the financial advisor is registered or not, i.e., if he/she has a business number or not.

- License: categorical variable identifying the license name of the financial advisors.

- LicenceBN: Boolean variable indicating if a business number is associated to the license.

- LicenceCtrl: numerical variable counting the number of company(ies) or people who control the licensee’s business.

- NumberDiplomas: numerical variable counting the number of diplomas received by the financial advisors.

- Experience: numerical variable counting the number of experience years of the financial advisors.

- Restrictions: categorical variable identifying the areas that the financial advisor is restricted from giving advice on.

- Capacity: numerical variable counting the total number of concurrent investors each advisor can host.

4.2. Generative Adversarial Networks’ Training Process

- Gradient boosting regressor [63] is a well-known machine learning approach for tabular datasets. It builds an ensemble of shallow and weak successive trees to make decisions. GBR is powerful enough to detect any nonlinear relationship between a model target and features, and it is powerful enough to deal with missing values, outliers, and large cardinality categorical values on your features without requiring any extra treatment.

- Artificial Neural Networks (ANNs) [64] are biologically inspired computational networks that are typically based on biological neural networks that form the structure of the human brain. Similar to how neurons in the human brain are interconnected, neurons in artificial neural networks are linked to each other in various layers of the networks. These neurons are referred to as nodes.

4.3. Financial Advisors Clustering and Matching Results

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Elton, E.J.; Gruber, M.J.; Brown, S.J.; Goetzmann, W.N. Modern Portfolio Theory and Investment Analysis; John Wiley & Sons: Hoboken, NJ, USA, 2009. [Google Scholar]

- Haugen, R.A.; Haugen, R.A. Modern Investment Theory; Prentice Hall: Upper Saddle River, NJ, USA, 2001; Volume 5. [Google Scholar]

- Dimmock, S.G.; Wang, N.; Yang, J. The Endowment Model and Modern Portfolio Theory; Technical Report; National Bureau of Economic Research: Cambridge, MA, USA, 2019. [Google Scholar]

- Markowitz, H. Portfolio Selection. J. Financ. 1952, 7, 77–91. [Google Scholar]

- Martin, R.A. PyPortfolioOpt: Portfolio optimization in Python. J. Open Source Softw. 2021, 6, 3066. [Google Scholar] [CrossRef]

- Ghasemi Saghand, P.; Haider, Z.; Charkhgard, H.; Eaton, M.; Martin, J.; Yurek, S.; Udell, B.J. SiteOpt: An open-source R-package for site selection and portfolio optimization. Ecography 2021, 44, 1678–1685. [Google Scholar] [CrossRef]

- Bessler, W.; Opfer, H.; Wolff, D. Multi-asset portfolio optimization and out-of-sample performance: An evaluation of Black–Litterman, mean-variance, and naïve diversification approaches. Eur. J. Financ. 2017, 23, 1–30. [Google Scholar] [CrossRef]

- Imbs, J.; Wacziarg, R. Stages of diversification. Am. Econ. Rev. 2003, 93, 63–86. [Google Scholar] [CrossRef]

- Goetzmann, W.N.; Kumar, A. Equity portfolio diversification. Rev. Financ. 2008, 12, 433–463. [Google Scholar] [CrossRef]

- French, K.R.; Poterba, J.M. Investor Diversification and International Equity Markets; Technical Report; National Bureau of Economic Research: Cambridge, MA, USA, 1991. [Google Scholar]

- Rubinstein, M. Markowitz’s “portfolio selection”: A fifty-year retrospective. J. Financ. 2002, 57, 1041–1045. [Google Scholar] [CrossRef]

- Feldman, K. Portfolio Selection, Efficient Diversification of Investments. By Harry M. Markowitz (Basil Blackwell, 1991)£ 25.00. J. Inst. Actuar. 1992, 119, 165–166. [Google Scholar] [CrossRef]

- Levy, H.; Sarnat, M. International diversification of investment portfolios. Am. Econ. Rev. 1970, 60, 668–675. [Google Scholar]

- Zhang, Y.; Zhao, P.; Wu, Q.; Li, B.; Huang, J.; Tan, M. Cost-Sensitive Portfolio Selection via Deep Reinforcement Learning. IEEE Trans. Knowl. Data Eng. 2022, 34, 236–248. [Google Scholar] [CrossRef]

- Samuelson, P.A. Efficient portfolio selection for Pareto-Lévy investments. J. Financ. Quant. Anal. 1967, 107–122. [Google Scholar] [CrossRef]

- Bakar, N.A.; Rosbi, S. Robust Statistical Portfolio Investment in Modern Portfolio Theory: A Case Study of Two Stocks Combination in Kuala Lumpur Stock Exchange. Int. J. Eng. Adv. Technol. 2019. [CrossRef]

- Ramadhiani, R.; Yan, M.; Hertono, G.F.; Handari, B.D. Implementation of e-New Local Search based Multiobjective Optimization Algorithm and Multiobjective Co-variance based Artificial Bee Colony Algorithm in Stocks Portfolio Optimization Problem. In Proceedings of the 2018 2nd International Conference on Informatics and Computational Sciences (ICICoS), Semarang, Indonesia, 30–31 October 2018. [Google Scholar] [CrossRef]

- Chu-Xin, J.; Wan-Yi, C.; Shu-Jing, Y. Robust Portfolio Selection Based on Optimization Methods. In Proceedings of the 2018 37th Chinese Control Conference (CCC), Wuhan, China, 25–27 July 2018. [Google Scholar]

- Kulian, V.; Yunkova, O.; Korobova, M. Digital Optimization of Portfolio with Market Restrictions. In Proceedings of the 2019 IEEE International Conference on Advanced Trends in Information Theory (ATIT) Kyiv, Ukraine, Ukraine, 18–20 December 2019. [Google Scholar] [CrossRef]

- Dai, Y. Portfolio Optimization with Upper Bounds Under a l∞ Risk Measure. In Proceedings of the 2019 16th International Conference on Service Systems and Service Management (ICSSSM), Shenzhen, China, 13–15 July 2019. [Google Scholar] [CrossRef]

- Huang, S.H.; Miao, Y.H.; Hsiao, Y.T. Novel Deep Reinforcement Algorithm with Adaptive Sampling Strategy for Continuous Portfolio Optimization. IEEE Access 2021, 9, 77371–77385. [Google Scholar] [CrossRef]

- Chou, Y.H.; Jiang, Y.C.; Kuo, S.Y. Portfolio Optimization in Both Long and Short Selling Trading Using Trend Ratios and Quantum-Inspired Evolutionary Algorithms. IEEE Access 2021, 9, 152115–152130. [Google Scholar] [CrossRef]

- Belanche, D.; Casaló, L.V.; Flavián, C. Artificial Intelligence in FinTech: Understanding robo-advisors adoption among customers. Ind. Manag. Data Syst. 2019, 119, 1411–1430. [Google Scholar] [CrossRef]

- Jung, D.; Dorner, V.; Weinhardt, C.; Pusmaz, H. Designing a robo-advisor for risk-averse, low-budget consumers. Electron. Mark. 2018, 28, 367–380. [Google Scholar] [CrossRef]

- Fisch, J.E.; Laboure, M.; Turner, J.A. The Emergence of the Robo-Advisor. In Pension Research Council Working Paper; 2018; Available online: https://pensionresearchcouncil.wharton.upenn.edu/wp-content/uploads/2018/12/WP-2018-12-Fisch-et-al.pdf (accessed on 25 September 2022).

- Leow, E.K.W.; Nguyen, B.P.; Chua, M.C.H. Robo-advisor using genetic algorithm and BERT sentiments from tweets for hybrid portfolio optimisation. Expert Syst. Appl. 2021, 179, 115060. [Google Scholar] [CrossRef]

- Brabham, D.C.; Ribisl, K.M.; Kirchner, T.R.; Bernhardt, J.M. Crowdsourcing applications for public health. Am. J. Prev. Med. 2014, 46, 179–187. [Google Scholar] [CrossRef] [PubMed]

- Wan, X.; Ghazzai, H.; Massoud, Y. Mobile Crowdsourcing for Intelligent Transportation Systems: Real-Time Navigation in Urban Areas. IEEE Access 2019, 7, 136995–137009. [Google Scholar] [CrossRef]

- Yuen, M.; King, I.; Leung, K. A Survey of Crowdsourcing Systems. In Proceedings of the 2011 IEEE Third International Conference on Privacy, Security, Risk and Trust and 2011 IEEE Third International Conference on Social Computing, Boston, MA, USA, 9–11 October 2011. [Google Scholar] [CrossRef]

- Mao, K.; Capra, L.; Harman, M.; Jia, Y. A survey of the use of crowdsourcing in software engineering. J. Syst. Softw. 2017, 126, 57–84. [Google Scholar] [CrossRef]

- Lucic, M.C.; Wan, X.; Ghazzai, H.; Massoud, Y. Leveraging Intelligent Transportation Systems and Smart Vehicles Using Crowdsourcing: An Overview. Smart Cities 2020, 3, 341–361. [Google Scholar] [CrossRef]

- Khanfor, A.; Hamrouni, A.; Ghazzai, H.; Yang, Y.; Massoud, Y. A Trustworthy Recruitment Process for Spatial Mobile Crowdsourcing in Large-scale Social IoT. In Proceedings of the 2020 IEEE Technology Engineering Management Conference (TEMSCON), Novi, MI, USA, 3–6 June 2020. [Google Scholar] [CrossRef]

- Tong, Y.; Zhou, Z.; Zeng, Y.; Chen, L.; Shahabi, C. Spatial crowdsourcing: A survey. VLDB J. 2020, 29, 217–250. [Google Scholar] [CrossRef]

- Tahmasebian, F.; Xiong, L.; Sotoodeh, M.; Sunderam, V. Crowdsourcing under data poisoning attacks: A comparative study. In IFIP Annual Conference on Data and Applications Security and Privacy; Springer: Cham, Switzerland, 2020. [Google Scholar]

- Kappel, T. Ex Ante Crowdfunding and the Recording Industry: A Model for the U.S. Loyola Los Angeles Entertain. Law Rev. 2009, 29, 375. [Google Scholar]

- Howe, J. Crowdsourcing: Why the Power of the Crowd Is Driving the Future of Business, 1st ed.; Crown Publishing Group: New York, NY, USA, 2008. [Google Scholar]

- Schwienbacher, A.; Larralde, B. Crowdfunding of Small Entrepreneurial Ventures. In The Oxford Handbook of Entrepreneurial Finance; Oxford University Press: Oxford, UK, 2010. [Google Scholar]

- Hentzen, J.K.; Hoffmann, A.; Dolan, R.; Pala, E. Artificial intelligence in customer-facing financial services: A systematic literature review and agenda for future research. Int. J. Bank Mark. 2022, 40, 1299–1336. [Google Scholar] [CrossRef]

- Northey, G.; Hunter, V.; Mulcahy, R.; Choong, K.; Mehmet, M. Man vs machine: How artificial intelligence in banking influences consumer belief in financial advice. Int. J. Bank Mark. 2022, 40, 1182–1199. [Google Scholar] [CrossRef]

- Zhang, L.; Pentina, I.; Fan, Y. Who do you choose? Comparing perceptions of human vs robo-advisor in the context of financial services. J. Serv. Mark. 2021, 35, 634–646. [Google Scholar] [CrossRef]

- Wang, J.; Zhou, M.; Guo, X.; Qi, L. Multiperiod Asset Allocation Considering Dynamic Loss Aversion Behavior of Investors. IEEE Trans. Comput. Soc. Syst. 2019, 6, 73–81. [Google Scholar] [CrossRef]

- Naik, M.J.; Albuquerque, A.L. Hybrid optimization search-based ensemble model for portfolio optimization and return prediction in business investment. Prog. Artif. Intell. 2022. [Google Scholar] [CrossRef]

- Yan, W.; Wang, H.; Zuo, M.; Li, H.; Zhang, Q.; Lu, Q.; Zhao, C.; Wang, S. A Deep Machine Learning-Based Assistive Decision System for Intelligent Load Allocation under Unknown Credit Status. Comput. Intell. Neurosci. 2022, 2022, 5932554. [Google Scholar] [CrossRef]

- Raby, H.; Ghazzai, H.; Hichem, B.; Massoud, Y. Financial Advisor Recruitment: A Smart Crowdsourcing-assisted Approach. IEEE Trans. Comput. Soc. Syst. 2020, 8, 682–688. [Google Scholar]

- Deng, Y.; Bao, F.; Kong, Y.; Ren, Z.; Dai, Q. Deep Direct Reinforcement Learning for Financial Signal Representation and Trading. IEEE Trans. Neural Netw. Learn. Syst. 2017, 28, 653–664. [Google Scholar] [CrossRef] [PubMed]

- Mitzenmacher, M. A brief history of generative models for power law and lognormal distributions. Internet Math. 2004, 1, 226–251. [Google Scholar] [CrossRef]

- Salakhutdinov, R. Learning deep generative models. Annu. Rev. Stat. Its Appl. 2015, 2, 361–385. [Google Scholar] [CrossRef]

- Jaakkola, T.; Haussler, D. Exploiting generative models in discriminative classifiers. Adv. Neural Inf. Process. Syst. 1999, 11. [Google Scholar]

- Kingma, D.P.; Mohamed, S.; Rezende, D.J.; Welling, M. Semi-supervised learning with deep generative models. Adv. Neural Inf. Process. Syst. 2014, 27. [Google Scholar] [CrossRef]

- Rezende, D.J.; Mohamed, S.; Wierstra, D. Stochastic backpropagation and approximate inference in deep generative models. arXiv 2014, arXiv:1401.4082. [Google Scholar]

- Goodfellow, I.; Pouget-Abadie, J.; Mirza, M.; Xu, B.; Warde-Farley, D.; Ozair, S.; Courville, A.; Bengio, Y. Generative Adversarial Nets. In Advances in Neural Information Processing Systems; Ghahramani, Z., Welling, M., Cortes, C., Lawrence, N.D., Weinberger, K.Q., Eds.; Curran Associates, Inc.: Red Hook, NY, USA, 2014; Volume 27, pp. 2672–2680. [Google Scholar]

- Goodfellow, I.J. NIPS 2016 Tutorial: Generative Adversarial Networks. CoRR 2017, arXiv:1701.00160. [Google Scholar]

- Radford, A.; Metz, L.; Chintala, S. Unsupervised Representation Learning with Deep Convolutional Generative Adversarial Networks. arXiv 2016, arXiv:cs.LG/1511.06434. [Google Scholar]

- Jabbar, A.; Li, X.; Omar, B. A Survey on Generative Adversarial Networks: Variants, Applications, and Training. arXiv 2020, arXiv:cs.CV/2006.05132. [Google Scholar] [CrossRef]

- Pan, Z.; Yu, W.; Yi, X.; Khan, A.; Yuan, F.; Zheng, Y. Recent Progress on Generative Adversarial Networks (GANs): A Survey. IEEE Access 2019, 7, 36322–36333. [Google Scholar] [CrossRef]

- Pan, Z.; Yu, W.; Wang, B.; Xie, H.; Sheng, V.S.; Lei, J.; Kwong, S. Loss Functions of Generative Adversarial Networks (GANs): Opportunities and Challenges. IEEE Trans. Emerg. Top. Comput. Intell. 2020, 4, 500–522. [Google Scholar] [CrossRef]

- Ghosh, B.; Dutta, I.K.; Totaro, M.; Bayoumi, M. A Survey on the Progression and Performance of Generative Adversarial Networks. In Proceedings of the 2020 11th International Conference on Computing, Communication and Networking Technologies (ICCCNT), Kharagpur, India, 1–3 July 2020. [Google Scholar] [CrossRef]

- Zhang, K.; Zhong, G.; Dong, J.; Wang, S.; Wang, Y. Stock Market Prediction Based on Generative Adversarial Network. Procedia Comput. Sci. 2019, 147, 400–406. [Google Scholar] [CrossRef]

- Larkin, K.G. Structural Similarity Index SSIMplified: Is there really a simpler concept at the heart of image quality measurement? arXiv 2015, arXiv:1503.06680. [Google Scholar]

- Wang, Z.; Bovik, A.C.; Sheikh, H.R.; Simoncelli, E.P. Image quality assessment: From error visibility to structural similarity. IEEE Trans. Image Process. 2004, 13, 600–612. [Google Scholar] [CrossRef]

- Erpek, T.; Sagduyu, Y.E.; Shi, Y. Deep Learning for Launching and Mitigating Wireless Jamming Attacks. IEEE Trans. Cogn. Commun. Netw. 2019, 5, 2–14. [Google Scholar] [CrossRef]

- Hodge, J.A.; Mishra, K.V.; Zaghloul, A.I. RF Metasurface Array Design Using Deep Convolutional Generative Adversarial Networks. In Proceedings of the 2019 IEEE International Symposium on Phased Array System & Technology (PAST), Waltham, MA, USA, 15–18 October 2019. [Google Scholar] [CrossRef]

- Prettenhofer, P.; Louppe, G. Gradient boosted regression trees in scikit-learn. PyData 2014, 2014. Available online: https://hdl.handle.net/2268/163521 (accessed on 24 February 2014).

- Wang, S.C. Artificial neural network. In Interdisciplinary Computing in Java Programming; Springer: Berlin/Heidelberg, Germany, 2003; pp. 81–100. [Google Scholar]

- Hamrouni, A.; Ghazzai, H.; Massoud, Y. Many-to-Many Recruitment and Scheduling in Spatial Mobile Crowdsourcing. IEEE Access 2020, 8, 48707–48719. [Google Scholar] [CrossRef]

- Mendoza, M.L.Z.; Antonio, R. Bipartite Graph. In Encyclopedia of Systems Biology; Springer: New York, NY, USA, 2013; pp. 147–148. [Google Scholar]

- Colannino, J.; Damian, M.; Hurtado, F.; Langerman, S.; Meijer, H.; Ramaswami, S.; Souvaine, D.; Toussaint, G. Efficient Many-To-Many Point Matching in One Dimension. Graphs Comb. 2007, 23, 169–178. [Google Scholar] [CrossRef]

- Krishnaswamy, S. Maximum Matching in a Partially Matched Bipartite Graph and Its Applications. In Proceedings of the 2010 2nd International Conference on Computational Intelligence, Communication Systems and Networks, Liverpool, UK, 28–30 July 2010. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Algorithm | Mean | St. Dev. |

|---|---|---|

| Proposed GANs | 0.841 | 0.214 |

| ANNs | 0.755 | 0.291 |

| Gradient Boosting Regressor | 0.674 | 0.385 |

| Technique | Random | Budget | ML | Proposed |

|---|---|---|---|---|

| Average ER (%) | 4.06 | 7.12 | 10.51 | 12.78 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hamadi, R.; Ghazzai, H.; Massoud, Y. A Generative Adversarial Network for Financial Advisor Recruitment in Smart Crowdsourcing Platforms. Appl. Sci. 2022, 12, 9830. https://doi.org/10.3390/app12199830

Hamadi R, Ghazzai H, Massoud Y. A Generative Adversarial Network for Financial Advisor Recruitment in Smart Crowdsourcing Platforms. Applied Sciences. 2022; 12(19):9830. https://doi.org/10.3390/app12199830

Chicago/Turabian StyleHamadi, Raby, Hakim Ghazzai, and Yehia Massoud. 2022. "A Generative Adversarial Network for Financial Advisor Recruitment in Smart Crowdsourcing Platforms" Applied Sciences 12, no. 19: 9830. https://doi.org/10.3390/app12199830