Increasing Income Generation: The Role of Staff Participation and Awareness

Abstract

:1. Introduction

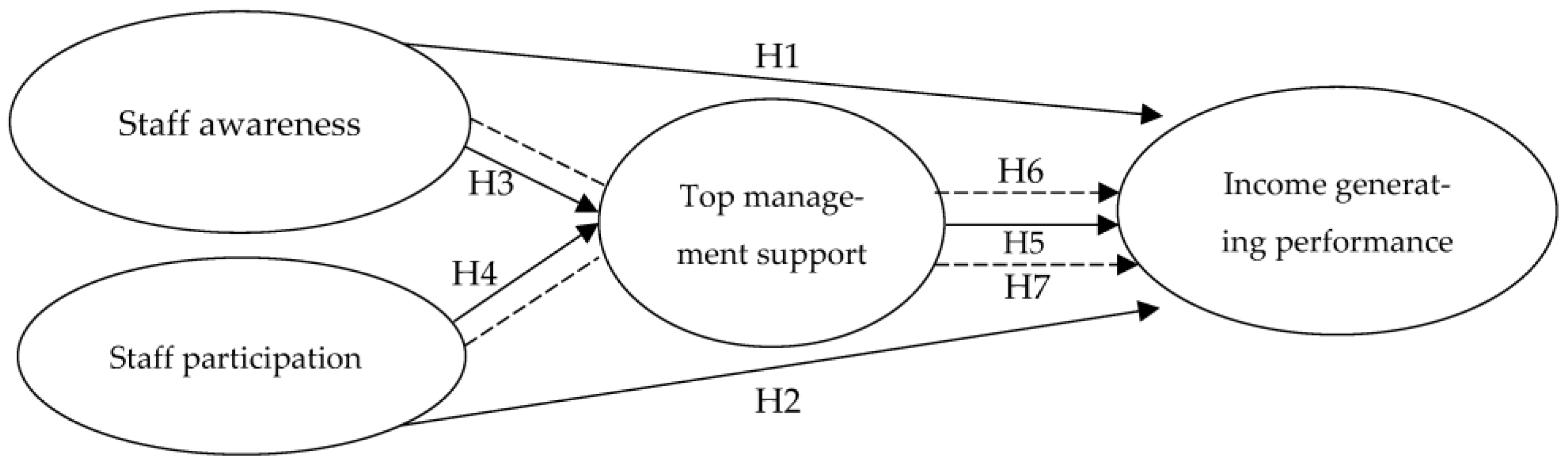

2. Literature Review and Research Hypotheses Development

2.1. Resources Dependence Theory

2.2. Staff Awareness

2.3. Staff Participation

2.4. Top Management Support

3. Methods

3.1. Research Design

3.2. Population and Research Sample

3.3. Research Variables

3.4. Data Collection and Analysis Methods

4. Results and Discussion

4.1. Results

4.1.1. Measurement Model

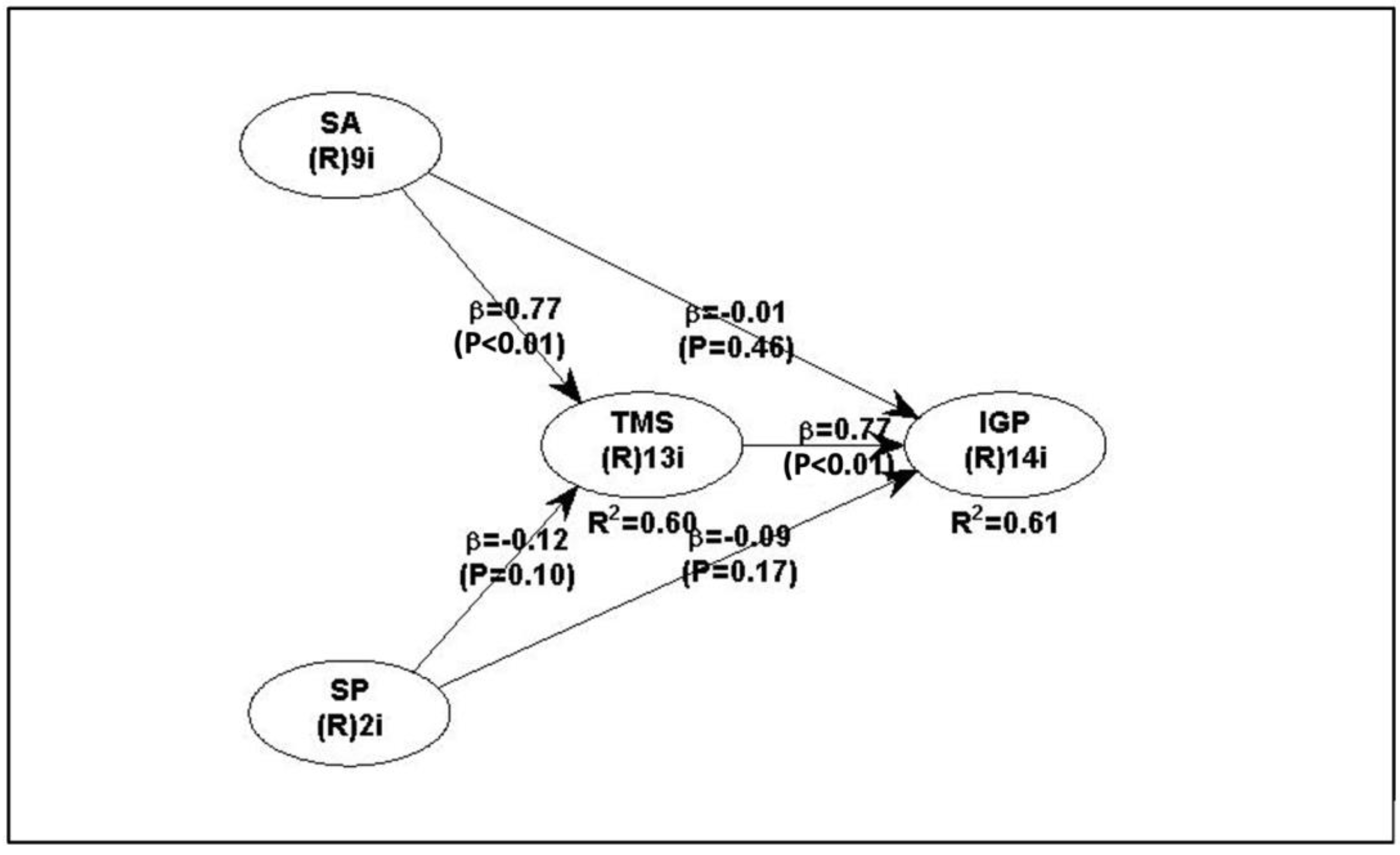

4.1.2. Hypotheses Testing

4.2. Discussion

4.2.1. Staff Awareness Influences on Income-Generating Performance

4.2.2. Staff Participation Influences on Income-Generating Performance

4.2.3. Staff Awareness Influences Top Management Support

4.2.4. Staff Participation Influences Top Management Support

4.2.5. Top Management Support Influences on Income-Generating Performance

4.2.6. Top Management Mediate the Staff Awareness of Income-Generating Performance

4.2.7. Top Management Support Mediate the Staff Participation in Income-Generating Performance

5. Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Adan, S. M., and P. Keiyoro. 2017. Factors Influencing the Implementation of Income Generating Projects in Public Secondary Schools in Isiolo North Sub County, Kenya. International Academic Journal of Information Sciences and Project Management 2: 558–73. [Google Scholar]

- Ahmed, R., and N. Azmi bin Mohamed. 2017. Development and validation of an instrument for multidimensional top management support. International Journal of Productivity and Performance Management 66: 873–95. [Google Scholar] [CrossRef]

- Aldrich, H. 1976. Resource dependence and in terorganiza tional relations: Local employment service offices and social services sector organizations. Administration & Society 7: 419–54. [Google Scholar]

- Arqawi, S. M., A. A. Al Hila, S. S. A. Naser, and M. J. Al Shobaki. 2018. The Degree of Employee Awareness of the Reality of Excellence in Performance at the Technical University of Palestine (Kadoorei). International Journal of Academic Management Science Research (IJAMSR) 2: 27–40. [Google Scholar]

- Bailey, C., A. Madden, K. Alfes, and L. Fletcher. 2017. The Meaning, Antecedents and Outcomes of Employee Engagement: A Narrative Synthesis. International Journal of Management Reviews 19: 31–53. [Google Scholar] [CrossRef] [Green Version]

- Benn, S., S. T. T. Teo, and A. Martin. 2015. Employee participation and engagement in working for the environment. Personnel Review 44: 492–510. [Google Scholar] [CrossRef]

- Bhatti, K., and S. Nawab. 2011. Effect of Direct Participation on Organizational Commitment. International Journal of Business and Social Science 2: 15–23. [Google Scholar]

- Brown, K. W., and R. M. Ryan. 2003. The Benefits of Being Present: Mindfulness and Its Role in Psychological Well-Being. Journal of Personality and Social Psychology 84: 822–48. [Google Scholar] [CrossRef] [Green Version]

- Cai, Y., and Y. Mehari. 2015. The Use of Institutional Theory in Higher Education Research. Theory and Method in Higher Education Research 1: 1–25. [Google Scholar] [CrossRef]

- Chang, K., S. Max, and J. Celse. 2021. Employee’s lying behavior and the role of self-awareness. International Journal of Organizational Analysis 30: 1538–53. [Google Scholar] [CrossRef]

- Chukwuemeka, S. O. 2020. Employee Participation in Decision Making and Organizational Performance in Public Organization Anambra State, Nigeria. International Journal of Business & Law Research 8: 79–88. [Google Scholar]

- Daft, R. L. 2010. The Executive and the Elephant: A Leader’s Guide for Building Inner Excellence. New York: John Wiley & Sons. [Google Scholar]

- Dane, E. 2011. Paying attention to mindfulness and its effects on task performance in the workplace. Journal of Management 37: 997–1018. [Google Scholar] [CrossRef]

- Dane, E., and B. J. Brummel. 2013. Examining workplace mindfulness and its relations to job performance and turnover intention. Human Relations 67: 105–28. [Google Scholar] [CrossRef]

- de Bakker, K., A. Boonstra, and H. Wortmann. 2010. Does risk management contribute to IT project success? A meta-analysis of empirical evidence. International Journal of Project Management 28: 493–503. [Google Scholar] [CrossRef]

- DiMaggio, P. J., and W. W. Powell. 1983. The Iron Cage Revisited: Institutional Isomorphism in Organizational Fields. American Sociological Review 48: 147–60. [Google Scholar] [CrossRef]

- Garg, N., and B. Lal. 2015. Exploring the Linkage between Awareness and Perception of High-performance Work Practices with Employee Well-being at Workplace: A New Dimension for HRM. Jindal Journal of Business Research 4: 81–100. [Google Scholar] [CrossRef]

- Glomb, T. M., M. K. Duffy, J. E. Bono, and T. Yang. 2011. Mindfulness at work. In Research in Personnel and Human Resources Management. Bingley: Emerald Group Publishing Ltd., vol. 30. [Google Scholar] [CrossRef]

- Grizzle, G. A., and C. D. Pettijohn. 2002. Implementing performance-based program budgeting: A system-dynamics perspective. Public Administration Review 62: 51–62. [Google Scholar] [CrossRef]

- Groen, B. A. C., M. J. F. Wouters, and C. P. M. Wilderom. 2017. Employee participation, performance metrics, and job performance: A survey study based on self-determination theory. Management Accounting Research 36: 51–66. [Google Scholar] [CrossRef]

- Henseler, J., C. M. Ringle, and M. Sarstedt. 2015. A New Criterion for Assesing Discriminant Validity in Variance-based Structural Equation Modeling. Journal of the Academy of Marketing Science 43: 115–35. [Google Scholar] [CrossRef] [Green Version]

- Hillman, A. J., M. C. Withers, and B. J. Collins. 2009. Resource Dependence Theory: A Review. Journal of Management 35: 1404–27. [Google Scholar] [CrossRef] [Green Version]

- Huy, Q. N. 2001. In praise of middle managers. Harvard Business Review 79: 72–79. [Google Scholar] [PubMed]

- Hyland, P. K., R. A. Lee, and M. J. Mills. 2015. Mindfulness at work: A new approach to improving individual and organizational performance. Industrial and Organizational Psychology 8: 576–602. [Google Scholar] [CrossRef] [Green Version]

- Iravo, D. mike. 2014. Effects of Emmployee Participation in Decision Making. International Journal of Advanced Research in Management and Social Sciences 3: 131–42. [Google Scholar]

- Irawanto, D. W. 2015. Employee participation in decision-making: Evidence from a state-owned enterprise in indonesia. Management 20: 159–72. [Google Scholar]

- Kezar, A., and C. Sam. 2013. Institutionalizing Equitable Policies and Practices for Contingent Faculty. The Journal of Higher Education 84: 56–87. [Google Scholar] [CrossRef]

- Khalid, K., and S. Nawab. 2018. Employee Participation and Employee Retention in View of Compensation. SAGE Open, 8. [Google Scholar] [CrossRef]

- Kiamba, C. 2004. Privately Sponsored Students and Other Income-Generating Activities at the University of Nairobi. Journal of Higher Education in Africa 2: 53–73. [Google Scholar]

- King, E., and J. M. Haar. 2017. Mindfulness and job performance: A study of Australian leaders. Asia Pacific Journal of Human Resources 55: 298–319. [Google Scholar] [CrossRef]

- Kipkoech, C. S. 2018. Determinants Of Implementation Of Income Generating Projects In Public Secondary Schools In Konoin District, Bomet County, Kenya. IOSR Journal of Business and Management (IOSR-JBM) 20: 64–68. [Google Scholar] [CrossRef]

- Lam, M., M. O. Donnell, and D. Robertson. 2015. Achieving employee commitment for continous improvement initiatives. International Journal of Operations & Production Management 35: 201–15. [Google Scholar] [CrossRef]

- Li, Wuwei, and S. N. Tobias. 2022. Assessing the Contributions of Top Management Team on Organization Performance in Tourism Industry, Tanzania. International Journal of Managerial Studies and Research 10: 8–15. [Google Scholar]

- Liu, L., and L. Gao. 2021. Financing university sustainability initiatives in China: Actors and processes. International Journal of Sustainability in Higher Education 22: 44–58. [Google Scholar] [CrossRef]

- Lunani, A. M. 2014. Selected Factors Influencing Principals’ Management of Income Generating Activities in Public Secondary Schools of Mumias District, Kenya. Doctoral dissertation, Moi University, Eldoret, Kenya. [Google Scholar]

- Mahmud, A., A. Nuryatin, and N. Susilowati. 2022. Investigation of Income Generating Activity in Higher Education: A Case Study at Indonesia Public University. International Journal of Evaluation and Research in Education (IJERE) 11: 303–12. [Google Scholar] [CrossRef]

- Mikulas, W. L. 2011. Mindfulness: Significant Common Confusions. Mindfulness 2: 1–7. [Google Scholar] [CrossRef]

- Miranda, A. T., and E. R. Celestino. 2016. The income-generating projects of a government academic institution in the Philippines The case of the University of Eastern Philippines. Asia Pacific Journal of Innovation and Entrepreneurship 10: 5–16. [Google Scholar] [CrossRef]

- Nyamwega, H. N. 2016. An Evaluation of Income Generating Projects in Public Secondary Schools in Nairobi County. International Journal of African and Asian Studies 21: 6–16. [Google Scholar]

- Oluwatayo, A., A. P. Opoko, and I. C. Ezema. 2017. Employee Participation in Decision—Making in architectural firms. Urbanism Architecture Constructions 8: 193–206. [Google Scholar]

- Pautz, H. 2014. Income generation in public libraries: Potentials and pitfalls. Library Review 63: 560–73. [Google Scholar] [CrossRef]

- Pratolo, S., H. Sofyani, and M. Anwar. 2020. Performance-based budgeting implementation in higher education institutions: Determinants and impact on quality. Cogent Business & Management 7: 1786315. [Google Scholar]

- Reb, J., J. Narayanan, and S. Chaturvedi. 2014. Leading Mindfully: Two Studies on the Influence of Supervisor Trait Mindfulness on Employee Well-Being and Performance. Mindfulness 5: 36–45. [Google Scholar] [CrossRef]

- Rigolizzo, M., and Z. Zhu. 2020. Motivating reflection habits and raising employee awareness of learning. Evidence-Based HRM 8: 161–75. [Google Scholar] [CrossRef]

- Ritter, B. A. 2006. Can business ethics be trained? A study of the ethical decision-making process in business students. Journal of Business Ethics 68: 153–64. [Google Scholar] [CrossRef]

- Ruedy, N. E., and M. E. Schweitzer. 2010. In the Moment: The Effect of Mindfulness on Ethical Decision Making. Journal of Business Ethics 95: 73–87. [Google Scholar] [CrossRef]

- Safitri, A. E. 2019. Pengaruh Stres Kerja Terhadap Produktivitas Kerja Karyawan pada PT.Telkom Witel Bekasi. Jurnal Ilmiah MEA (Manajemen, Ekonomi, Dan Akuntansi) 3: 170–80. [Google Scholar] [CrossRef]

- Salvato, C. 2009. Capabilities Unveiled: The Role of Ordinary Activities in the Evolution of Product Development Processes. Organization Science 20: 384–409. [Google Scholar] [CrossRef]

- Shillingi, V. 2017. The Influence of Top Management and OrganisationResources on Implimentation of Strategic Plans in Public Sector. International Journal of Academic Research in Business and Social Sciences 7: 101–24. [Google Scholar]

- Siswanto, Ely, M. Djumahir, K. Sonhadji, and M. Idrus. 2013. Good University Income Generating Governance in Indonesia: Agency Theory Perspective. International Journal of Learning and Development 3: 67. [Google Scholar] [CrossRef] [Green Version]

- Slovin, E. 1960. Slovin’s Formula for Sampling Technique. Available online: https://prudencexd.weebly.com/ (accessed on 7 September 2022).

- Small, C., and C. Lew. 2019. Mindfulness, Moral Reasoning and Responsibility: Towards Virtue in Ethical Decision-Making. Journal of Business Ethics 169: 103–17. [Google Scholar] [CrossRef]

- Strauss, G. 2006. Worker Participation—Some Under-Considered Issues. Industrial Relations 45: 778–803. [Google Scholar] [CrossRef]

- Tchapchet, E. T., C. G. Iwu, and C. Allen-Ile. 2014. Employee participation and productivity in a South African university. Implications for human resource management. Problems and Perspectives in Management 12: 293–304. [Google Scholar]

- Towett, S. M., I. Naibei, and W. Rop. 2019. Effect of Financial Control Mechanisms on Performance of Income Generating Units in Selected Public Universities in Kenya. International Journal of Current Aspects 3: 286–304. [Google Scholar] [CrossRef]

- Turner, L. A., and A. J. Angulo. 2018. Risky Business: An Integrated Institutional Theory for Understanding High-Risk Decision Making in Higher Education. Harvard Educational Review 88: 53–80. [Google Scholar] [CrossRef]

- Uribetxebarria, U., A. Garmendia, and U. Elorza. 2021. Does employee participation matter? An empirical study on the effects of participation on well-being and organizational performance. Central European Journal of Operations Research 29: 1397–425. [Google Scholar] [CrossRef]

- van der Westhuizen, D. W., G. Pacheco, and D. J. Webber. 2012. Culture, participative decision making and job satisfaction. International Journal of Human Resource Management 23: 2661–79. [Google Scholar] [CrossRef]

- Weick, K. E., and K. M. Sutcliffe. 2006. Mindfulness and the quality of organizational attention. Organization Science 17: 514–24. [Google Scholar] [CrossRef]

- Yu, C., Y. Wang, T. Li, and C. Lin. 2022. Do top management teams’ expectations and support drive management innovation in small and medium-sized enterprises? Journal of Business Research 142: 88–99. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Construct | AVE | Cronbach’s Alpha | Composite Reliability |

|---|---|---|---|

| Staff Awareness | 0.599 | 0.916 | 0.930 |

| Staff Participation | 0.762 | 0.728 | 0.865 |

| Top Management Support | 0.691 | 0.963 | 0.967 |

| Income-Generating Performance | 0.732 | 0.972 | 0.967 |

| Staff Awareness | Staff Participation | Top Management Support | Income-Generating Performance | |

|---|---|---|---|---|

| Staff Awareness | 0.774 | |||

| Staff Participation | 0.066 | 0.873 | ||

| Top Management Support | 0.764 | −0.084 | 0.832 | |

| Income-Generating Performance | 0.595 | −0.086 | 0.785 | 0.855 |

| Staff Awareness | Staff Participation | Top Management Support | Income-Generating Performance | |

|---|---|---|---|---|

| Staff Awareness | - | |||

| Staff Participation | 0.138 | - | ||

| Top Management Support | 0.820 | 0.119 | - | |

| Income-Generating Performance | 0.812 | 0.162 | 0.633 | - |

| No | Model Fit and Quality Indices | Fit Criteria | Results | Notes |

|---|---|---|---|---|

| 1. | Average Path Coefficient (APC) | p = 0.002 | 0.335 p < 0.001 | Accepted |

| 2. | Average R-squared (ARS) | p < 0.001 | 0.624 p < 0.001 | Accepted |

| 3. | Average adjusted R-squared (AARS) | p < 0.001 | 0.616 p < 0.001 | Accepted |

| 4. | Average block VIF (AVIF) | Accepted if ≤5, ideally ≤ 3.3 | 1.629 | Ideal |

| 5. | Average full collinearity VIF (AFVIF) | Accepted if ≤5, ideally ≤ 3.3 | 2.617 | Accepted |

| 6. | Tenenhaus GoF (GoF) | small ≥ 0.1, medium ≥ 0.25, large ≥ 0.36 | 0.722 | Large, Accepted |

| 7. | Sympson’s Paradox Ratio (SPR) | Accepted if ≥0.7, ideally = 1 | 1.000 | Accepted |

| 8. | R-squared Contribution Ratio (RSCR) | Accepted if ≥0.9, ideally = 1 | 1.000 | Accepted |

| 9. | Statistical Suppression Ratio (SSR) | Accepted if ≥0.7 | 1.000 | Accepted |

| 10. | Nonlinear Bivariate Causality Direction Ratio (NLBCDR) | Accepted if ≥0.7 | 1.000 | Accepted |

| Hypothesis | Relationship between Variables | Path Coeff. | p-Values | Notes | ||

|---|---|---|---|---|---|---|

| Explanatory Variable | > | Responded Variable | ||||

| H1 | Staff Awareness (SA) | > | Income-Generating Performance (IGP) | −0.01 | 0.46 | Rejected |

| H2 | Staff Participation (SP) | > | Income-Generating Performance (IGP) | −0.09 | 0.17 | Rejected |

| H3 | Staff Awareness (SA) | > | Top Management Support (TMS) | 0.77 | <0.01 | Accepted |

| H4 | Staff Participation (SP) | > | Top Management Support (TMS) | −0.13 | 0.10 | Rejected |

| H5 | Top Management Support (TMS) | > | Income-Generating Performance (IGP) | 0.77 | <0.01 | Accepted |

| Hypothesis | Relationship between Variables | Path Coeff. | p-Values | Notes | ||||

|---|---|---|---|---|---|---|---|---|

| Explanatory Variable | > | Intervening Variable | > | Response Variable | ||||

| H6 | Staff Awareness (SA) | > | Top Management Support (TMS) | > | Income-Generating Performance (IGP) | 0.595 | <0.01 | Accepted |

| H7 | Staff Participation (SP) | > | Top Management Support (TMS) | > | Income-Generating Performance (IGP) | −0.094 | 0.078 | Rejected |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mahmud, A.; Susilowati, N.; Anisykurlillah, I.; Sari, P.N. Increasing Income Generation: The Role of Staff Participation and Awareness. Int. J. Financial Stud. 2023, 11, 25. https://doi.org/10.3390/ijfs11010025

Mahmud A, Susilowati N, Anisykurlillah I, Sari PN. Increasing Income Generation: The Role of Staff Participation and Awareness. International Journal of Financial Studies. 2023; 11(1):25. https://doi.org/10.3390/ijfs11010025

Chicago/Turabian StyleMahmud, Amir, Nurdian Susilowati, Indah Anisykurlillah, and Puji Novita Sari. 2023. "Increasing Income Generation: The Role of Staff Participation and Awareness" International Journal of Financial Studies 11, no. 1: 25. https://doi.org/10.3390/ijfs11010025

APA StyleMahmud, A., Susilowati, N., Anisykurlillah, I., & Sari, P. N. (2023). Increasing Income Generation: The Role of Staff Participation and Awareness. International Journal of Financial Studies, 11(1), 25. https://doi.org/10.3390/ijfs11010025