1. Introduction

Accounting information comparability is regarded as a distinctive quality among other qualitative aspects of financial data that improve a company’s mechanisms (

Choi and Suh 2019). It has drawn interest from theoretical and technical perspectives due to the numerous advantages it provides to stakeholders and investors (

Luo et al. 2020). There is a replacement effect between earnings and cash flow measures that is favorably correlated with the compensation weight of earnings and negatively correlated with the weight of earnings (

Thakkar and Chaudhari 2021). As seen by the extensive volume of specialist literature, the theory discussed in the following pages, the efficient market hypothesis (EMH), is highly contentious and of particular interest to financial economists, educators, and researchers (

Kong and So 2023). Despite numerous attempts to uncover the truth about the EMH, no definitive answer has yet been found. Consequently, stock prices reflect a timely and effective response to information. However, due to the complexity of human nature and the inherent game properties of financial markets, financial chaos such as excessive stock price volatility, total earnings announcements, and surplus drift have occurred frequently in capital markets, leading scholars to challenge the assumptions made by modern financial theory.

The implementation of the International Financial Reporting Standards for high-quality accounting information, which guarantees financial stability and economic efficiency in the globalized market, has been promoted by numerous nations, global professional organizations, and trade associations. The goal of adopting international accounting standards is to raise the level of financial reporting quality in order to boost users’ confidence in financial statements when making decisions and to make financial statements more comparable across various organizations and nations (

Shahid et al. 2022). High-quality accounting information can assist shareholders and investors in making better decisions by overcoming information asymmetry. Accounting information informs the capital market about a company’s financial status and business performance. However, not all publicly traded corporations’ accounting information is of unquestionable quality. Financial fraud has been more frequently reported in the press in recent years (

Liang et al. 2022). For investors and financial markets around the world, the COVID-19 pandemic breakout has brought up previously unheard-of difficulties. The pandemic’s uncertainty and information overload have had a severe influence on investors’ attention spans and their capacity to comprehend sophisticated financial information. Accounting information comparability becomes crucial in such a situation for investors to make wise investment decisions (

Olayinka 2022).

The challenges within the Chinese stock market not only influence investor decisions but also hold significant implications for market health. Against this background, we aim to address the following questions:

Question (1): Can limited investor attention impact stock returns in China?

Question (2): To what extent does investor attention impact the stock returns of the capital market in China?

Question (3): Does the relationship between investor attention and stock returns vary depending on accounting information comparability?

To tackle the above questions, this study employs the following theoretical foundations to investigate the Chinese stock market. Firstly, the information asymmetry theory explores the impact of information availability on market efficiency, revealing mechanisms behind trading behavior and stock valuation (

Akerlof 1970;

Kyle 1985). Secondly, the limited attention theory elucidates the challenges faced by individual Chinese investors in information acquisition, especially under subjective market sentiments and media influence, resulting in their limited attention (

Simon 1955;

Mullainathan and Thaler 2000). The accounting information comparability theory plays a crucial role in the Chinese market, acting as a positive regulator in an environment with non-standardized information disclosure. It reduces investors’ information search costs and enhances information understanding (

Lang et al. 2019). The herd behavior theory explains how, in the face of information uncertainty, investors collectively focus on specific stocks, influencing market dynamics (

Bikhchandani et al. 1992). In the context of the Chinese market, herd effects are more pronounced, as investors are more susceptible to others’ behavior, resulting in excessive attention to certain stocks. Lastly, signal transmission theory emphasizes the strategic use of accounting information in the Chinese market, particularly considering comparability, to attract investors (

Spence 1973;

Lambert et al. 2011).

This paper investigates the impact of individual investor attention on current stock returns, examining the moderating effect of accounting information comparability, providing essential insights into the Chinese market and suggesting meaningful improvements. We use monthly data from a comprehensive sample of Chinese A-shares for listed companies on the main board market of the Shanghai Securities Exchange from 2017 to 2021. Subsequently, we employ statistical analysis and multiple regression methods, supplemented by robustness tests, to validate the applicability of the theoretical framework. Regression analysis reveals a statistically significant positive relationship between current investor attention and monthly stock returns, along with a significant negative correlation between lagged investor attention and current monthly stock returns. Moreover, our findings indicate that accounting information comparability partially moderates the outlined relationships. To ensure the robustness of our results, we employ the instrumental variables method and quantify the core dependent variable using monthly stock returns that account for reinvested cash dividends to check the robustness.

Compared with the existing literature, the main contributions of our study are as follows. (a) Enhanced positive influence and mitigation of adverse effects: In contrast to earlier scholars concentrating on the impact of accounting information comparability on stock prices, we advance the discourse by underscoring the dual role of comparability within the realm of limited investor attention. Accounting information comparability not only enhances the positive influence of current investor attention on stock returns but also mitigates the adverse effects of delayed attention. (b) In-depth exploration of investor attention’s impact on stock returns: Departing from the focus on how investor attention affects stock returns, we delve into the underlying reasons behind this impact. The argument is that heightened investor attention in the current period positively influences stock returns. However, in line with the limited attention theory and signaling theory, information distortion during subsequent dissemination leads to investor overreaction and a subsequent decline in stock prices. (c) Innovative use of accounting information comparability as a moderating variable: This study introduces accounting information comparability as a novel moderating variable to scrutinize the impact of investor concerns on stock returns. Companies with high comparability of accounting information effectively reduce costs associated with information search, understanding, and dissemination distortion. This innovative approach captures the intricate process through which investor attention influences stock returns.

The remainder of this paper is organized as follows.

Section 2 includes a literature review and theoretical deductions, followed by the formulation of research hypotheses in

Section 3. Additionally,

Section 4 presents the methodology, including data collection and the empirical research design.

Section 5 provides a detailed exposition of our empirical test analysis. The final section offers our conclusions and their implications.

5. Empirical Results and Discussion

This section is divided into two main subsections. Firstly, descriptive statistics, stationary tests, and correlation analyses are performed on the cleaned data in

Section 4. Second, based on this, a fixed-effects regression model is applied to regress investor attention on monthly current stock returns. Additionally, we examine the moderating impact of accounting information comparability through both multiple regression analysis and robustness tests.

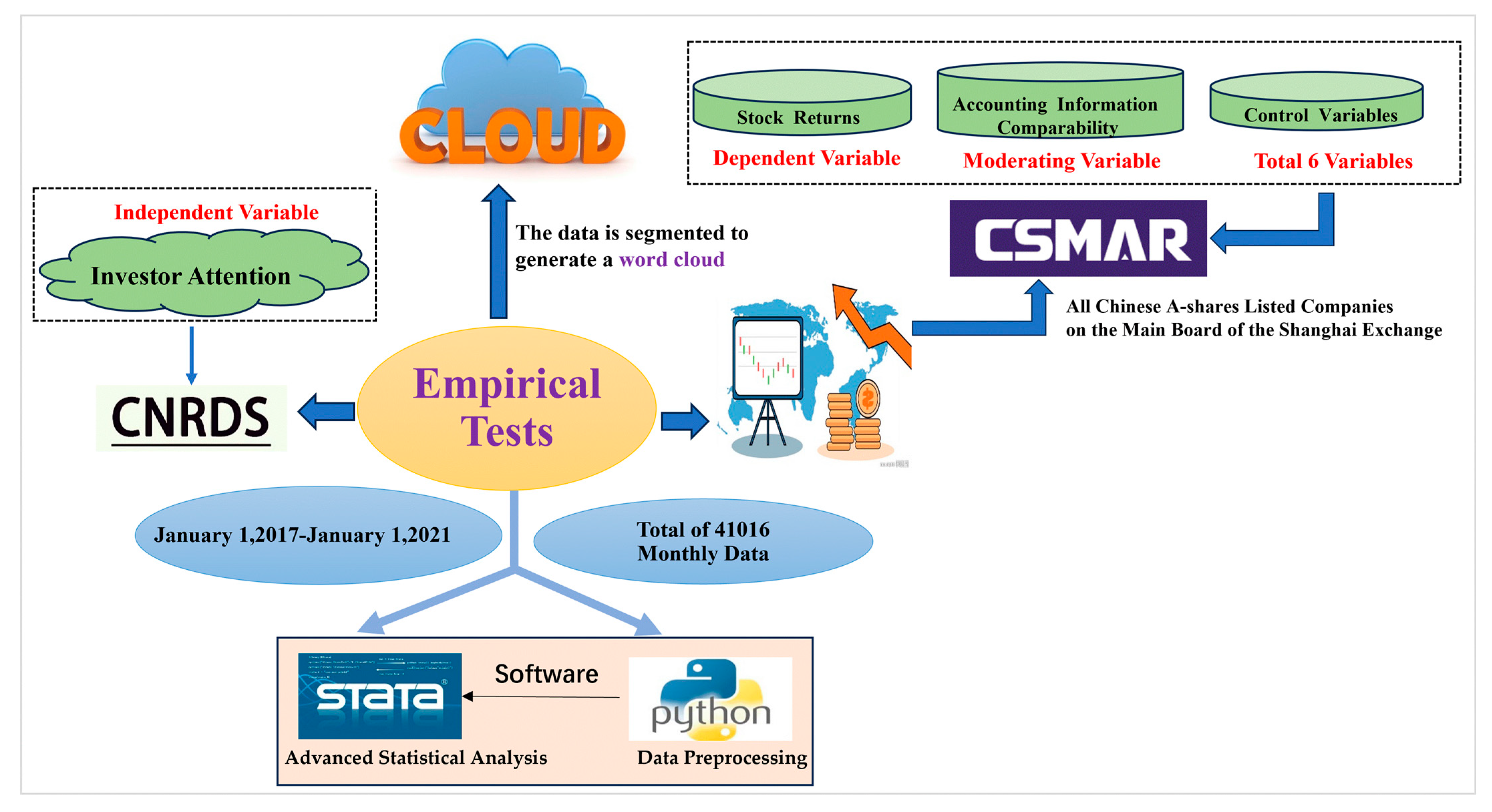

Figure 3 visually presents the workflow of the empirical tests.

5.1. Descriptive Statistics

In this study, we conducted an analysis on a dataset that included 1021 companies selected from the period between 1 January 2017, and 1 January 2021, focusing on the Shanghai Stock Exchange (SSE) main board A-shares market as our research sample, resulting in a total of 41,016 valid data points.

Table 3 presents the descriptive statistics for the entire dataset.

5.1.1. Dependent Variable of Monthly Stock Returns

As depicted in

Table 3, the monthly stock return indicator exhibits a range from a minimum of −58% to a maximum of 249.6%, demonstrating a significant standard deviation. In addition, the mean value of the monthly stock return indicator is 1%, indicating that investors have the potential to realize positive returns in the stock market. However, these returns are relatively modest and do not match the scale of China’s economic development, leaving substantial room for further growth and development.

5.1.2. Independent Variable of Investor Attention

As shown in

Table 3, the composite index of investor attention presents a range from a minimum value of 0 to a maximum value of 15.315, with a mean value of 10.101. This variation suggests that investor attention is not uniform across different stocks, suggesting the existence of a phenomenon commonly referred to as the “herding effect”. In this context, stocks with more visibility tend to garner more attention, often irrespective of their intrinsic value. This observation aligns with the prevailing dynamics of the Chinese stock market, characterized by a tendency to speculate on specific sectors, chase hot topics, and pursuit rising up and abandoned down.

5.1.3. Moderating Variable of Accounting Information Comparability

As illustrated in

Table 3, the mean value of accounting information comparability of the sample companies is −0.015 and the median value is −0.013, which indicates that the sample is more evenly distributed and there is no significant left or right bias. Another point to note is that accounting information comparability is a positive indicator, with larger values indicating stronger comparability. Descriptively, the minimum value for accounting information comparability is −0.161, the maximum value is −0.002, and the standard deviation is 0.011. Considering the effect of the dimension, this result indicates the presence of variations in accounting information comparability between different sample companies.

5.2. Stationary Test

Our dataset consists of an extensive panel of data exhibiting time-series characteristics. The temporal nature of this dataset introduces the possibility of non-random sampling, thereby necessitating an initial stationarity test to guard against spurious regression. We employ the Fisher panel unit root test to examine the stationarity of all variables.

In columns (2) and (3) of

Table 4, notably high Chi-squared statistics and a

p-value of 0 were observed for each variable, indicating the rejection of the unit root hypothesis at a 1% significance level. These results confirm the stationarity of all variables, including “Return”, “Inattention”, “Mc”, “Lev”, “Roe”, “Cashflow”, “BM”, and “Growth”. This confirmation enhances the dataset’s reliability, establishing a robust foundation for subsequent empirical analyses.

5.3. Correlation Analysis

Before conducting regression analysis, this study undertakes a correlation analysis for two primary objectives: 1. to establish an initial understanding of the relationship between the independent variables and the dependent variables without considering other variables; and 2. to test the presence of multicollinearity.

The results are presented in

Table 5 and can be summarized as follows. Column (1) indicates that the regression coefficient between the current investor attention and current stock returns was 0.073 at the 1% confidence level. Conversely, investor attention with a one-period lag and a two-period lag shows a significant negative correlation with stock returns in the current period, with a coefficient of −0.049, also passing the 1% confidence level test. These results align with the hypothesis of this paper. Column (2) shows the highest coefficient observed is 0.577. and all the absolute values of the Pearson correlation coefficients are below 0.8, indicating that the model does not exhibit significant substantial multicollinearity among the variables.

However, the Pearson correlation coefficient between the control variable, monthly circulating market value of individual stocks (MC), and investor attention surpasses 0.5 in magnitude. To improve the reliability of the findings, a subsequent variance inflation factor (VIF) test is conducted. In this test, if VIF exceeds 10, it indicates a severe collinearity issue, while VIF exceeding 5 indicates a moderate collinearity problem (

Cheng et al. 2020). The results of this test are displayed in

Table 6. Column 2 indicates that the maximum VIF value of the variable is 1.66 and the mean value is 1.34. All the VIF values are less than 5. Therefore, the independent variable does not cause multicollinearity problems.

5.4. Multiple Linear Regression Analysis

Based on the previous correlation analysis, we have gained a preliminary understanding of the relationships among the main variables. Our hypotheses have received initial validation. Building upon this foundation, this research employs a fixed-effects model to conduct regression analysis of the relationships between the variables. This choice is made for the following reasons: in contrast to the random effects model, the fixed-effects model consistently yields stable estimates; and the variables used do not include any time-invariant variables, thereby ensuring that the fixed-effects model does not omit any critical variables.

5.4.1. Baseline Regression

First, to test the effect of current investor attention on stock returns as hypothesized in Hypothesis 1, we conducted a regression analysis using Model 8 on the sample data. The regression results are presented in

Table 7 (1). The below table shows that after adding control variables and controlling for industry and monthly fixed effects, the coefficient of Inattention

is calculated to be 0.041, exhibiting a positive sign and passing the significance test at the 1% level. This result proves that stocks with greater investor attention during the current period exhibit higher monthly stock returns, thereby validating Hypothesis 1. In other words, increased investor attention to a stock lowers the search costs for investors, reduces their cognitive demands, and makes the stock more attractive for investment. This results in a positive pressure to buy, consequently leading to higher stock returns.

- 2.

Lagged Investor Attention and Current Stock Returns

Through the above analysis, we find that greater investor attention correlates with increased stock returns, However, whether this attention-driven buying phenomenon is enduring necessitates further investigation. To test the effect of lagged investor attention on current period stock returns in Hypothesis 2, we conducted a regression analysis using models 9 and 10 on the sample data. The regression results are presented in

Table 7 (2) and (3).

After adding the control variables and controlling for industry and monthly fixed effects, column (2) shows that the coefficient for Inattention (−1) is −0.083, while column (3) presents that the coefficient for Inattention (−2) is −0.069, both of which passes the significance test at the 1% level. This indicates that stocks receiving significant investor attention experience a subsequent decrease in stock returns, Furthermore, this reversal effect persists for at least two periods. Additionally, the absolute value of the Inattention (−1) coefficient is 0.083, and the absolute value of the Inattention (−2) coefficient is 0.069, suggesting that as the number of periods increases, the strength of the reversal effect diminishes.

In summary, Hypothesis 2 is validated, indicating an inverse relationship between lagged investor attention and current stock returns. The more attention a stock receives in the current period, the greater the likelihood of a return reversal in the subsequent period.

5.4.2. Moderating Effect Regression of Accounting Information Comparability

The above analysis demonstrates that the increase in stock returns due to increased investor attention is not sustainable, Investor attention lagged by one to two periods is inversely related to stock returns. The reason for this phenomenon is that stocks that receive investor attention in the current period can reduce investors’ information search costs and lessen the consumption of investors’ attention, consequently triggering investors’ buying behavior. Such increases are driven by factors unrelated to fundamentals, making them unsustainable, and ultimately leading to stock price reversals caused by overreactions resulting from distorted information received by investors.

Moreover, increased accounting information comparability enhances greater accessibility and comprehensibility of information. As a result, it is less susceptible to distortion and imposes a reduced burden on investors’ attention. Then how does accounting information comparability serve as a moderating factor? To explore this question, this study brings the sample data into models 11, 12, and 13 for regression analysis. The specific regression results are shown in

Table 8.

From

Table 8 (1), the coefficient β3 of the cross-product term between

Inattentioni,t, and

acci,t is 0.283, which passes the significance test at the 1% level, even after accounting for control variables and industry and monthly fixed effects. This result suggests that higher accounting information comparability amplifies the positive influence of current investor attention on current stock returns. This finding is also consistent with common sense. People naturally direct greater attention towards information that is straightforward, easily comprehensible, and readily comparable, as opposed to complex data.

Additionally, it is noteworthy that the regression results indicate a positive coefficient for accounting information comparability, which remains significant at the 1% level. This signifies that the format of accounting information, characterized by its ease of comprehension and comparability, can influence stock returns independently of its content. This finding underscores the potential for regulatory authorities to craft policies and incentives encouraging companies to simplify their financial statements. Hypothesis 3 is hereby confirmed.

As shown in

Table 8 (2), after adding control variables and controlling for industry and monthly fixed effects, the coefficient

η3 of the cross-product term between

Inattentioni,t−1, and

acci,t is 0.249, which passes the significance test at the 1% level. Furthermore, in column (3) of

Table 8, the coefficient

of the cross-product term between

Inattentioni,t−2, and

acci,t is 0.182, which passes the significance test at the 10% level. In other words, the higher the comparability of accounting information, the less effort is required to comprehend the information, making it easier for investors to understand the information itself without being influenced by distorted details. Consequently, the overreactions caused by distorted details are suppressed.

The coefficient of the cross-product term between Inattentioni,t−2, and acci,t is positive, but insignificant. This suggests that the inverse effect of lagged investor attention on stock returns weakens over time, and the moderating effect of accounting information comparability becomes less important. This observation serves as a reminder that policymakers should not solely focus on the quality of annual reports for listed companies, as the positive moderating effect of accounting information comparability is time-sensitive. In practice, semiannual, quarterly, and monthly reports are essential sources of information for investors to understand a company’s operation and stock valuation and deserve equal attention. Hypothesis 4 is substantiated.

5.5. Robustness Tests

To ensure the robustness of the research conclusions, the following robustness tests are carried out.

5.5.1. Alternative Dependent Variables

Recognizing that the selection of variable measurement methods can potentially influence the final regression results, this study employs a requantified measurement of the dependent variable, accounting for the reinvestment of cash dividends, denoted as “returns 1”. The specific calculation method is as follows:

represents the comparable price of the daily closing price of stock on the last trading day of month considering the reinvestment of cash dividends.

signifies the comparable cost of the daily closing price of stock on the last trading day of month , also considering reinvestment of cash dividends.

The regression results are presented in

Table 9. A subsequent regression analysis was conducted using the new measure of stock returns, which resulted in minimal changes in the coefficients among the main variables. This reaffirms the robustness of the regression results.

Column (1) of

Table 9 indicates a significant positive relationship at the 1% level between current investor attention and stock returns, with a coefficient of 0.046, thus validating hypothesis 1. In addition, from

Table 9 (2) and (3), the regression results also indicate that lagged one-period investor attention and lagged two-period investor attention continue to exhibit a significant negative correlation with current stock returns at the 1% level, with coefficients of −0.079 and −0.066, respectively, thereby supporting Hypothesis 2.

- 2.

Moderating Effect Regression of Accounting Information Comparability

From

Table 9 (1), the regression result for the cross-product term involving current investor attention and accounting information comparability with stock returns is 0.283, which remains significantly positive at the 1% level, indicating that high accounting information comparability reinforces the positive association between current investor attention and stock returns, thereby validating Hypothesis 3.

According to column (2) in

Table 9, lagged one-period investor attention and the cross-product term of accounting information comparability regressed on current stock returns yield a coefficient of 0.249, which remains significantly positively correlated at the 1% level. Furthermore, column (3) in

Table 9 shows that the cross-product term involving lagged two-period investor attention and accounting information comparability produces a regression coefficient of 0.182, showing a significant positive correlation at the 10% confidence level. This proves that high accounting information comparability mitigates the negative correlation between lagged investor attention and current stock returns, thereby confirming Hypothesis 4.

5.5.2. Instrumental Variable (IV) Method

Potential issues must be addressed, including the possibility of independent variables and core independent variables acting as causal or omitted variables (

Frankel et al. 2022). Firstly, we indicate that investors’ attention can significantly influence stock returns. However, it is essential to consider the reciprocal effect, where high stock returns can attract investors’ attention, potentially leading to a two-way causality problem. Secondly, the realm of factors impacting stock returns is extensive, and the selected control variables do not encompass them all, potentially resulting in omitted variables. To address these concerns and enhance the robustness of the findings, we employ the first-order difference of the core independent variables as an instrumental variable to test the baseline regression outcomes.

Since the number of instrumental variables equals the number of endogenous independent variables, there is no problem of over-identification. The specific test results are shown in

Table 10. First, in the underidentification test, the

p-values of the core independent variables

Inattentioni,t,

Inattentioni,t−1,

Inattentioni,t−2 are all 0, which is less than the critical value of 0.05, leading to the firm rejection of the original hypothesis. Second, in the weak identification test, Wald F values for

Inattentioni,t,

Inattentioni,t−1, and

Inattentioni,t−2 are 6846.204, 6260.734, and 6580.861, respectively. These values significantly exceed the 10% threshold value of 16.38, indicating the absence of a weak instrumental variable problem.

The preceding discussion demonstrates the reasonableness of the instrumental variables used in this paper. Based on these instruments, the regression analysis for the underlying hypotheses is conducted with Inattention IV as the core independent variable, which is brought into models 8, 9, and 10. The specific regression results are shown in

Table 11.

From

Table 11 (1), the coefficient between Inattention IV and stock return is 0.407, signifying a positive relationship and passing the significance test at the 1% level, thereby validating Hypothesis 1. Moving to

Table 11 (2), the coefficient between Inattention (−1) IV and stock return is −0.051, indicating a negative association and passing the significance test at the 1% level, confirming the validity of Hypothesis 2. Furthermore,

Table 11 (3) displays a coefficient of −0.047 for the connection between Inattention (−2) IV and stock return, reflecting a negative relationship and passing the significance test at the 1% level, also validating Hypothesis 2. These findings align with the baseline regression results, confirming their robustness even after employing the instrumental variables method to mitigate endogeneity problems resulting from factors such as reciprocal causality or omitted variables.

6. Conclusions

In contrast to most previous studies that indirectly quantify investor attention indicators, we directly quantify investor attention using an internet search index. This approach allows for a more direct exploration of how fluctuations in investor attention influence stock returns and how the relationship evolves over time. Additionally, we quantify accounting information comparability using a rolling regression of individual stock returns and accounting earnings for company and to quantify accounting information comparability and investigate its moderating role.

Drawing on theories related to information asymmetry, signal transmission, herd behavior, and the limited attention theory, this study utilizes a comprehensive sample of all A-share stocks listed on the main board of the Shanghai Stock Exchange during the period from 2017 to 2021. The dataset comprises 41,016 valid data points, which are empirically analyzed to assess the influence of investor attention on stock returns, as well as the moderating effect of accounting information comparability. This study shows several key findings. First of all, current investor attention exhibits a positive correlation with current stock returns. In other words, stocks attracting higher investor attention in the current period tend to yield higher returns. This is attributed to the limited attention span of investors, resulting in lower search costs for stocks that capture investor attention, ultimately leading to increased stock returns. Lagged investor attention is negatively related to current stock returns. In other words, the higher the lagged investor’s attention, the greater the reversal in current-period returns for the stock. This is because the information is distorted in the process of dissemination, and investors are influenced by the distorted information to overreact to their investment behavior later on. This momentum buying behavior caused by the distorted information leads to a stock premium that lacks fundamental support and ultimately leads to a stock price reversal later on. Concurrently, high accounting information comparability strengthens the positive correlation between current investor attention and current stock returns while weakening the negative correlation between lagged investor attention and current stock returns. Highly comparable accounting information can effectively increase the informational value embedded in stock prices, consequently diminishing the cognitive costs associated with information comprehension for investors. When the target company exhibits a high degree of comparability, greater accessibility to information tends to attract more investor attention. Finally, highly comparable accounting information can effectively reduce the irrational bias caused by investors’ comprehension difficulties, thereby reducing the irrational fluctuations in stock prices resulting from investors mistaking distorted information for reliable insights.

{kind=link}

{kind=link}

{kind=link}