Economic Policy Uncertainty and Commercial Property Performance: An In-Depth Analysis of Rents and Capital Values

Abstract

1. Introduction

2. Literature Review

2.1. Property Investment Decision-Making

2.2. The Threat of Rising Uncertainty on Property Performance

2.3. Uncertainty and Commercial Property Performance: Market Implications

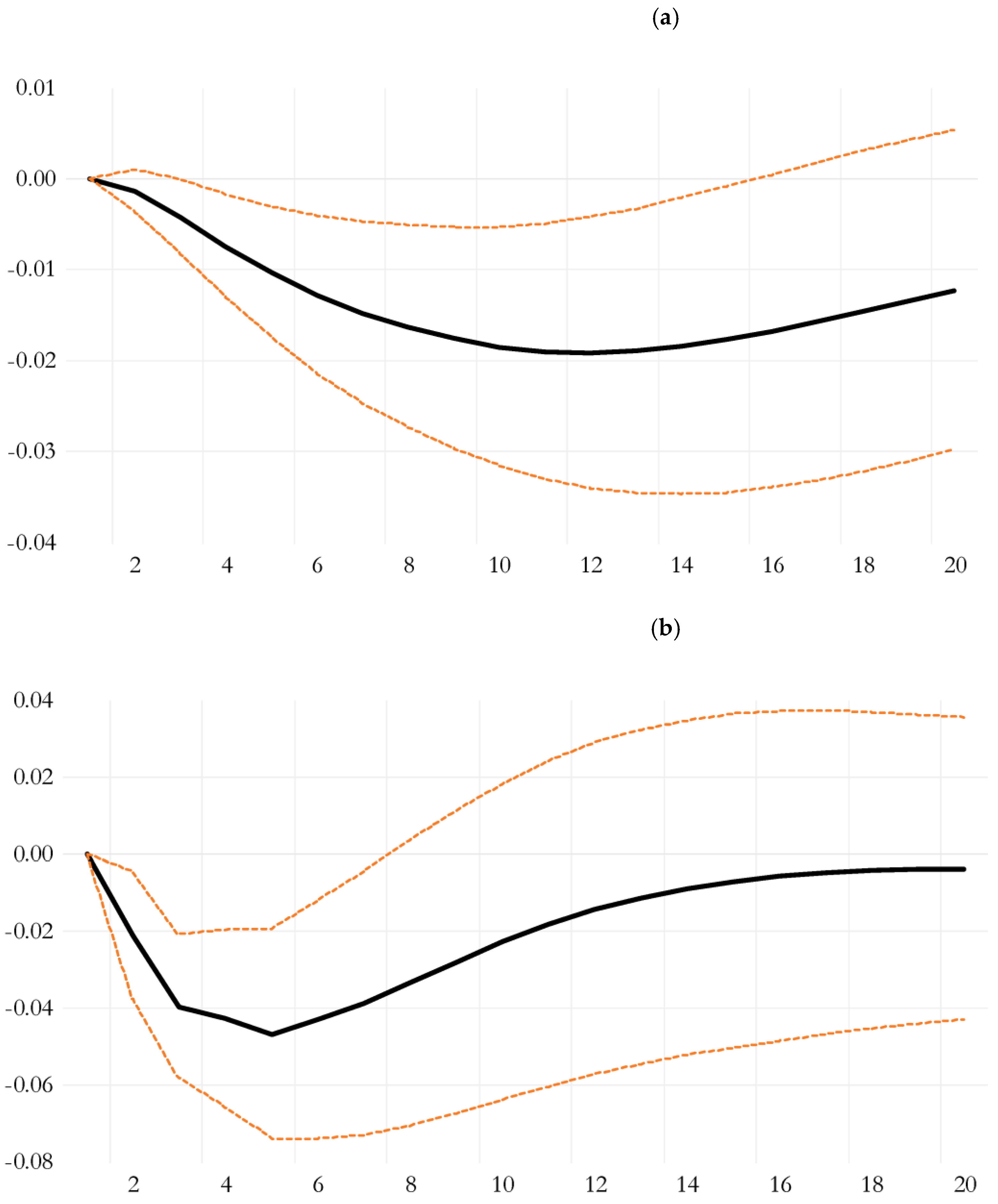

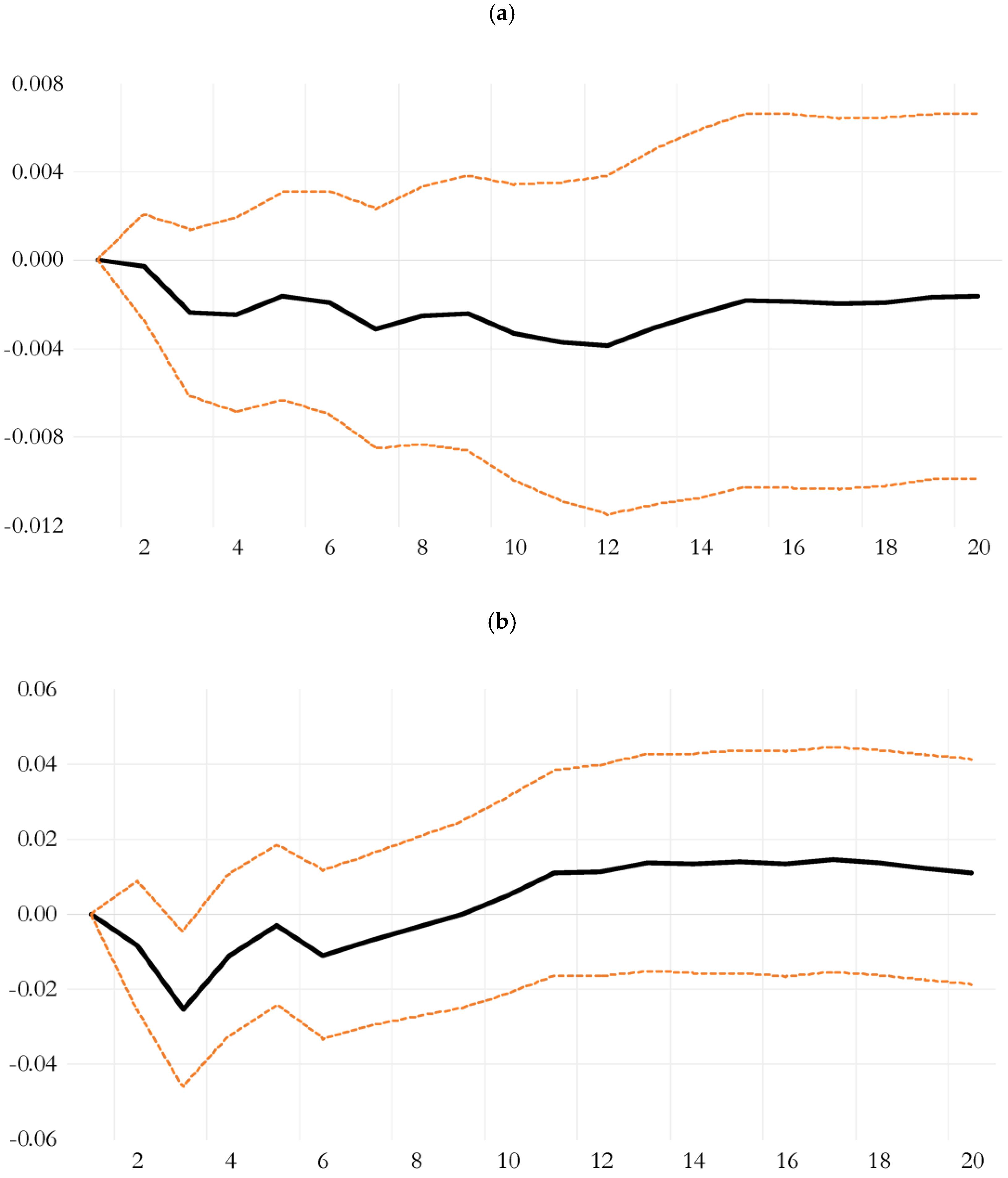

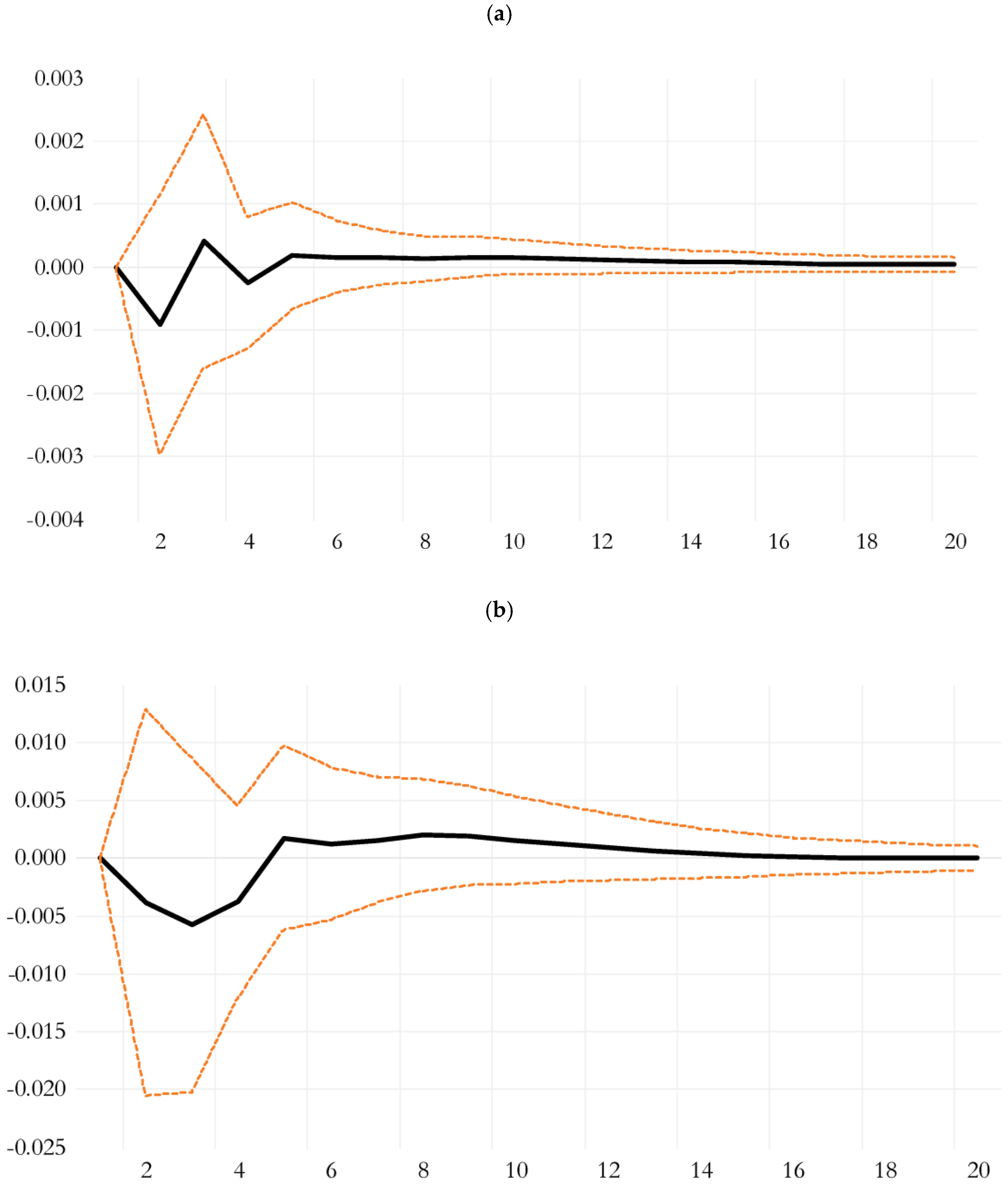

3. Results and Discussion

3.1. Impact of Uncertainty in the Office Sector

3.2. Impact of Uncertainty in the Retail Sector

3.3. Impact of Uncertainty in the Industrial Sector

4. Materials and Methods

4.1. Data

4.2. VAR Model

5. Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

Appendix B

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Off_rent | Off_cap | Ret_rent | Ret_cap | Ind_rent | Ind_cap | |

|---|---|---|---|---|---|---|

| Lag | ||||||

| 1 | 0.006 | 0.116 | 0.268 | 0.161 * | 0.002 | 0.040 |

| 2 | 0.706 * | 0.313 * | 0.143 * | 0.037 | 0.019 | 0.509 * |

| 3 | 0.669 | 0.000 | 0.005 | 0.001 | 0.003 | 0.004 |

| 4 | 0.062 | 0.213 | 0.372 | 0.270 | 0.364 * | 0.183 |

Appendix C

| Variance Decomposition of Office Rents | Variance Decomposition of Office Capital Values | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Period | S.E. | Off_rent | EPU | CPI | GDP | UNEM | HP | Period | S.E. | Off_cap | EPU | CPI | GDP | UNEM | HP |

| 1 | 0.010 | 100.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 1 | 0.072 | 100.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| 2 | 0.019 | 98.186 | 1.538 | 0.103 | 0.038 | 0.133 | 0.001 | 2 | 0.089 | 92.166 | 5.784 | 0.689 | 0.491 | 0.067 | 0.802 |

| 3 | 0.027 | 93.103 | 6.150 | 0.248 | 0.211 | 0.271 | 0.017 | 3 | 0.109 | 78.654 | 14.373 | 4.175 | 0.329 | 0.140 | 2.329 |

| 4 | 0.035 | 86.622 | 11.710 | 0.467 | 0.673 | 0.352 | 0.175 | 4 | 0.127 | 66.016 | 20.522 | 8.033 | 0.252 | 0.829 | 4.348 |

| 5 | 0.043 | 79.664 | 17.244 | 0.831 | 1.218 | 0.380 | 0.663 | 5 | 0.146 | 54.250 | 24.528 | 12.751 | 0.385 | 1.915 | 6.171 |

| 6 | 0.050 | 72.892 | 22.132 | 1.366 | 1.626 | 0.360 | 1.624 | 6 | 0.166 | 44.902 | 25.709 | 17.517 | 0.932 | 3.292 | 7.648 |

| 7 | 0.057 | 66.429 | 26.236 | 2.074 | 1.861 | 0.311 | 3.089 | 7 | 0.184 | 37.811 | 25.334 | 21.822 | 1.656 | 4.676 | 8.701 |

| 8 | 0.064 | 60.295 | 29.556 | 2.987 | 1.932 | 0.255 | 4.975 | 8 | 0.201 | 32.402 | 24.130 | 25.758 | 2.457 | 5.891 | 9.362 |

| 9 | 0.070 | 54.561 | 32.108 | 4.127 | 1.871 | 0.212 | 7.121 | 9 | 0.218 | 28.258 | 22.573 | 29.318 | 3.243 | 6.897 | 9.712 |

| 10 | 0.076 | 49.299 | 33.947 | 5.495 | 1.723 | 0.204 | 9.332 | 10 | 0.233 | 25.052 | 20.966 | 32.524 | 3.939 | 7.689 | 9.830 |

| 11 | 0.082 | 44.565 | 35.161 | 7.070 | 1.535 | 0.245 | 11.424 | 11 | 0.247 | 22.537 | 19.453 | 35.417 | 4.522 | 8.287 | 9.786 |

| 12 | 0.088 | 40.390 | 35.857 | 8.055 | 1.350 | 0.345 | 13.252 | 12 | 0.259 | 20.536 | 18.097 | 38.021 | 4.989 | 8.724 | 9.634 |

| 13 | 0.093 | 36.773 | 36.155 | 10.638 | 1.199 | 0.504 | 14.732 | 13 | 0.271 | 18.925 | 16.918 | 40.360 | 5.348 | 9.032 | 9.418 |

| 14 | 0.098 | 33.687 | 36.168 | 12.498 | 1.097 | 0.714 | 15.836 | 14 | 0.281 | 17.615 | 15.908 | 42.453 | 5.615 | 9.241 | 9.168 |

| 15 | 0.103 | 31.090 | 35.999 | 14.321 | 1.047 | 0.959 | 16.584 | 15 | 0.291 | 16.537 | 15.053 | 44.321 | 5.805 | 9.376 | 8.907 |

| 16 | 0.108 | 28.929 | 35.730 | 16.049 | 1.043 | 1.224 | 17.025 | 16 | 0.300 | 15.645 | 14.333 | 45.979 | 5.936 | 9.458 | 8.649 |

| 17 | 0.112 | 27.150 | 35.426 | 17.641 | 1.072 | 1.490 | 17.221 | 17 | 0.308 | 14.900 | 13.728 | 47.446 | 6.021 | 9.502 | 8.403 |

| 18 | 0.116 | 25.699 | 35.131 | 19.069 | 1.119 | 1.744 | 17.238 | 18 | 0.315 | 14.273 | 13.222 | 48.738 | 6.073 | 9.521 | 8.174 |

| 19 | 0.119 | 24.528 | 34.873 | 20.318 | 1.173 | 1.975 | 17.133 | 19 | 0.321 | 13.744 | 12.799 | 49.870 | 6.099 | 9.522 | 7.965 |

| 20 | 0.122 | 23.592 | 34.667 | 21.385 | 1.224 | 2.176 | 16.957 | 20 | 0.327 | 13.294 | 12.447 | 50.859 | 6.109 | 9.513 | 7.777 |

Appendix D

| Variance Decomposition of Retail Rents | Variance Decomposition of Retail Capital Values | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Period | S.E. | Ret_rent | EPU | CPI | GDP | UNEM | HP | Period | S.E. | Ret_cap | EPU | CPI | GDP | UNEM | HP |

| 1 | 0.008 | 100.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 1 | 0.075 | 100.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| 2 | 0.015 | 93.130 | 0.205 | 2.582 | 2.550 | 1.460 | 0.073 | 2 | 0.092 | 96.576 | 1.337 | 0.098 | 0.948 | 0.162 | 0.879 |

| 3 | 0.021 | 87.340 | 1.069 | 4.237 | 4.217 | 3.069 | 0.067 | 3 | 0.106 | 92.018 | 4.544 | 0.647 | 0.847 | 0.122 | 1.823 |

| 4 | 0.026 | 82.792 | 1.836 | 5.512 | 5.851 | 3.963 | 0.045 | 4 | 0.116 | 88.814 | 6.194 | 1.053 | 0.748 | 0.215 | 2.976 |

| 5 | 0.030 | 79.259 | 2.700 | 6.215 | 7.252 | 4.493 | 0.082 | 5 | 0.125 | 84.882 | 7.788 | 2.098 | 0.780 | 0.441 | 4.011 |

| 6 | 0.034 | 76.714 | 3.526 | 6.596 | 8.146 | 4.823 | 0.196 | 6 | 0.132 | 81.149 | 8.391 | 3.508 | 1.172 | 0.866 | 4.914 |

| 7 | 0.037 | 74.725 | 4.246 | 6.881 | 8.744 | 5.034 | 0.372 | 7 | 0.139 | 77.971 | 8.367 | 4.857 | 1.758 | 1.420 | 5.628 |

| 8 | 0.040 | 73.033 | 4.887 | 7.107 | 9.189 | 5.197 | 0.587 | 8 | 0.145 | 75.248 | 8.001 | 6.126 | 2.513 | 2.009 | 6.103 |

| 9 | 0.043 | 71.539 | 5.464 | 7.288 | 9.546 | 5.341 | 0.822 | 9 | 0.150 | 72.969 | 7.514 | 7.199 | 3.376 | 2.584 | 6.359 |

| 10 | 0.046 | 70.186 | 5.991 | 7.434 | 9.859 | 5.471 | 1.058 | 10 | 0.155 | 71.125 | 7.053 | 8.033 | 4.254 | 3.103 | 6.431 |

| 11 | 0.048 | 68.950 | 6.482 | 7.545 | 10.146 | 5.591 | 1.286 | 11 | 0.159 | 69.676 | 6.681 | 8.638 | 5.093 | 3.545 | 6.367 |

| 12 | 0.050 | 67.825 | 6.944 | 7.624 | 10.411 | 5.699 | 1.498 | 12 | 0.163 | 68.581 | 6.404 | 9.041 | 5.857 | 3.904 | 6.213 |

| 13 | 0.052 | 66.806 | 7.380 | 7.676 | 10.655 | 5.795 | 1.688 | 13 | 0.167 | 67.798 | 6.205 | 9.277 | 6.524 | 4.183 | 6.012 |

| 14 | 0.005 | 65.888 | 7.794 | 7.707 | 10.878 | 5.879 | 1.855 | 14 | 0.171 | 67.281 | 6.054 | 9.387 | 7.089 | 4.393 | 5.796 |

| 15 | 0.056 | 65.065 | 8.185 | 7.720 | 11.080 | 5.952 | 1.998 | 15 | 0.174 | 66.979 | 5.929 | 9.405 | 7.554 | 4.546 | 5.587 |

| 16 | 0.057 | 64.332 | 8.554 | 7.720 | 11.262 | 6.013 | 2.118 | 16 | 0.177 | 66.848 | 5.812 | 9.360 | 7.928 | 4.651 | 5.401 |

| 17 | 0.058 | 63.681 | 8.902 | 7.710 | 11.425 | 6.065 | 2.217 | 17 | 0.180 | 66.841 | 5.695 | 9.275 | 8.224 | 4.721 | 5.245 |

| 18 | 0.059 | 63.107 | 9.227 | 7.692 | 11.570 | 6.107 | 2.297 | 18 | 0.182 | 66.922 | 5.577 | 9.165 | 8.452 | 4.763 | 5.121 |

| 19 | 0.060 | 62.602 | 9.529 | 7.669 | 11.697 | 6.142 | 2.360 | 19 | 0.184 | 67.057 | 5.460 | 9.043 | 8.625 | 4.784 | 5.031 |

| 20 | 0.061 | 62.160 | 9.809 | 7.643 | 11.808 | 6.170 | 2.410 | 20 | 0.186 | 67.221 | 5.347 | 8.917 | 8.754 | 4.791 | 4.970 |

Appendix E

| Variance Decomposition of Industrial Rents | Variance Decomposition of Industrial Capital Values | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Period | S.E. | Ind_rent | EPU | CPI | GDP | UNEM | HP | Period | S.E. | Ind_cap | EPU | CPI | GDP | UNEM | HP |

| 1 | 0.009 | 100.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 1 | 0.072 | 100.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| 2 | 0.015 | 96.849 | 0.433 | 1.468 | 0.783 | 0.002 | 0.465 | 2 | 0.095 | 95.016 | 0.331 | 3.179 | 0.128 | 0.006 | 1.341 |

| 3 | 0.022 | 90.071 | 0.963 | 4.017 | 3.025 | 0.359 | 1.566 | 3 | 0.116 | 90.382 | 0.944 | 5.027 | 0.136 | 0.552 | 2.959 |

| 4 | 0.030 | 82.108 | 1.745 | 6.410 | 5.361 | 1.226 | 3.150 | 4 | 0.132 | 83.228 | 1.570 | 9.178 | 0.185 | 1.460 | 4.379 |

| 5 | 0.037 | 74.359 | 2.566 | 8.190 | 7.673 | 2.187 | 5.024 | 5 | 0.157 | 75.473 | 1.731 | 13.431 | 0.750 | 2.913 | 5.701 |

| 6 | 0.045 | 67.764 | 3.464 | 9.067 | 9.659 | 2.965 | 7.082 | 6 | 0.175 | 68.321 | 1.693 | 17.073 | 1.489 | 4.536 | 6.887 |

| 7 | 0.052 | 62.611 | 4.384 | 9.209 | 11.036 | 3.439 | 9.321 | 7 | 0.192 | 61.808 | 1.558 | 20.274 | 2.411 | 6.044 | 7.905 |

| 8 | 0.058 | 58.628 | 5.267 | 8.909 | 11.829 | 3.627 | 11.740 | 8 | 0.207 | 56.142 | 1.383 | 22.902 | 3.388 | 7.383 | 8.802 |

| 9 | 0.064 | 55.504 | 6.082 | 8.372 | 12.126 | 3.606 | 14.311 | 9 | 0.221 | 51.371 | 1.224 | 25.008 | 4.285 | 8.509 | 9.603 |

| 10 | 0.068 | 52.986 | 6.800 | 7.743 | 12.037 | 3.452 | 16.982 | 10 | 0.233 | 47.382 | 1.104 | 26.699 | 5.081 | 9.418 | 10.316 |

| 11 | 0.072 | 50.885 | 7.400 | 7.121 | 11.685 | 3.232 | 19.677 | 11 | 0.243 | 44.066 | 1.032 | 28.043 | 5.767 | 10.139 | 10.952 |

| 12 | 0.075 | 49.073 | 7.871 | 6.570 | 11.179 | 3.002 | 22.306 | 12 | 0.252 | 41.323 | 1.009 | 29.107 | 6.340 | 10.703 | 11.518 |

| 13 | 0.078 | 47.468 | 8.208 | 6.130 | 10.618 | 2.802 | 24.775 | 13 | 0.260 | 39.055 | 1.031 | 29.947 | 6.812 | 11.136 | 12.020 |

| 14 | 0.080 | 46.019 | 8.418 | 5.819 | 10.083 | 2.661 | 27.000 | 14 | 0.267 | 37.180 | 1.089 | 30.607 | 7.198 | 11.464 | 12.461 |

| 15 | 0.082 | 44.701 | 8.515 | 5.638 | 9.630 | 2.593 | 28.923 | 15 | 0.273 | 35.630 | 1.177 | 31.125 | 7.510 | 11.711 | 12.847 |

| 16 | 0.084 | 43.504 | 8.520 | 5.571 | 9.295 | 2.600 | 30.510 | 16 | 0.278 | 34.349 | 1.286 | 31.529 | 7.761 | 11.893 | 13.183 |

| 17 | 0.085 | 42.427 | 8.459 | 5.591 | 9.087 | 2.671 | 31.765 | 17 | 0.283 | 33.288 | 1.408 | 31.844 | 7.961 | 12.026 | 13.473 |

| 18 | 0.086 | 41.475 | 8.355 | 5.668 | 8.995 | 2.791 | 32.716 | 18 | 0.287 | 32.410 | 1.538 | 32.088 | 8.122 | 12.121 | 13.722 |

| 19 | 0.087 | 40.651 | 8.233 | 5.771 | 8.995 | 2.938 | 33.411 | 19 | 0.290 | 31.682 | 1.670 | 32.276 | 8.249 | 12.187 | 13.936 |

| 20 | 0.088 | 39.959 | 8.108 | 5.876 | 9.057 | 3.094 | 33.906 | 20 | 0.293 | 31.078 | 1.800 | 32.422 | 8.350 | 12.233 | 14.118 |

References

- Abdallah, Mohamad Hussein Ismail, Hussein Hassan Al-Tamimi, and Andi Duqi. 2020. Real estate investors’ behaviour. Qualitative Research in Financial Markets 13: 82–98. [Google Scholar] [CrossRef]

- Ahir, Hites, Nicholas Bloom, and Davide Furceri. 2022. The World Uncertainty Index. Available online: http://www.policyuncertainty.com/wui_quarterly.html (accessed on 3 April 2024).

- Akinsomi, Omokolade, and Nikiwe Mkhabela. 2016. The Drivers of Direct Commercial Real Estate Returns: Evidence from South Africa. Paper presented the 16th African Real Estate Society (AfRES) Annual Conference—Sustainable Multi-Sectoral Real Estate Development in Emerging Economies, Addis-Ababa, Ethiopia. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2846088 (accessed on 3 April 2024).

- Allan, Roddy, Ervi Liusman, Teddy Lu, and Desmond Tsang. 2021. The COVID-19 Pandemic and Commercial Property Rent Dynamics. Journal of Risk and Financial Management 14: 360. [Google Scholar] [CrossRef]

- Andre, Christophe, Lumengo Bonga-Bonga, Rangan Gupta, and John W. Muteba Mwamba. 2017. Economic Policy Uncertainty, US Real Housing Returns and Their Volatility: A Nonparametric Approach. Journal of Real Estate Research 39: 493–513. [Google Scholar] [CrossRef]

- Antonakakis, Nikolaos, Rangan Gupta, and Christophe Andre. 2015. Dynamic co-movements between economic policy uncertainty and housing market returns. Journal of Real Estate Portfolio Management 21: 53–60. [Google Scholar] [CrossRef]

- Baker, Scott R., Nicholas Bloom, and Steven J. Davis. 2016. Measuring economic policy uncertainty. Quarterly Journal of Economics 131: 1593–636. [Google Scholar] [CrossRef]

- Baum, Andrew. 2009. Commercial Real Estate Investment, 2nd ed. London: Routledge. [Google Scholar]

- Bird, Ron, and Danny Yeung. 2012. How do investors react under uncertainty? Pacific Basin Finance Journal 20: 310–27. [Google Scholar] [CrossRef]

- Bitterman, Alex, and Daniel Baldwin Hess. 2021. Going dark: The post-pandemic transformation of the metropolitan retail landscape. In Town Planning Review. 92 vols. Issue 3. Liverpool: Liverpool University Press, pp. 385–93. [Google Scholar] [CrossRef]

- Bloom, Nicholas. 2009. The Impact of Uncertainty Shocks. Econometrica 77: 623–85. [Google Scholar] [CrossRef]

- Bloom, Nicholas, Hites Ahir, and Davide Furceri. 2022. Visualizing the Rise of Global Economic Uncertainty. Havard Business Review. Available online: https://hbr.org/2022/09/visualizing-the-rise-of-global-economic-uncertainty (accessed on 12 April 2024).

- Bond, Shaun A., and Soosung Hwang. 2007. Smoothing, nonsynchronous appraisal and cross-sectional aggregation in real estate price indices. Real Estate Economics 35: 349–82. [Google Scholar] [CrossRef]

- Bond, Shaun A., Soosung Hwang, and Gianluca Marcato. 2012. Commercial Real Estate Returns: An Anatomy of Smoothing in Asset and Index Returns. Real Estate Economics 40: 637–61. [Google Scholar] [CrossRef]

- Carrière-Swallow, Yan, and Luis Felipe Céspedes. 2013. The impact of uncertainty shocks in emerging economies. Journal of International Economics 90: 316–25. [Google Scholar] [CrossRef]

- Carson, Selma, Anupam Nanda, Sotirios Thanos, Eero Valtonen, and Yishuang Xu. 2021. Imagining a post-COVID-19 world of real estate. In Town Planning Review. 92 vols. Issue 3. Liverpool: Liverpool University Press, pp. 371–76. [Google Scholar] [CrossRef]

- CBRE Research. 2021. Asia Pacific Real Estate Market Outlook|Australia|Retail—Restart the Uneven Recovery. Available online: https://www.cbre.com.au/insights/books/australia-real-estate-market-outlook-2021 (accessed on 3 April 2024).

- CBRE Research. 2022. Industrial and Logistics Figures: Australia’s Industrial and Logistics Vacancy Dips to 0.8% as Rental Growth Reaches Double Digits. Available online: https://www.cbre.com.au/insights/reports/australia-industrial-logistics-vacancy-report-h1-2022 (accessed on 3 April 2024).

- Che, Jihyun, Jae Seung Lee, and Saehoon Kim. 2023. How has COVID-19 impacted the economic resilience of retail clusters? Examining the difference between neighborhood-level and district-level retail clusters. Cities 140: 104457. [Google Scholar] [CrossRef] [PubMed]

- Chmielewska, Aneta, Jerzy Adamiczka, and Michał Romanowski. 2020. Genetic Algorithm as Automated Valuation Model Component in Real Estate Investment Decisions System. Real Estate Management and Valuation 28: 1–14. [Google Scholar] [CrossRef]

- Chong, Fennee. 2023. Housing Price and Interest Rate Hike: A Tale of Five Cities in Australia. Journal of Risk and Financial Management 16: 61. [Google Scholar] [CrossRef]

- Christiaens, Nathan, and Jeroen Macharis. 2021. The Impact of COVID-19 on Stock Market Performance Worldwide. Master’s thesis, Ghent University, Ghent, Belgium. Available online: https://libstore.ugent.be/fulltxt/RUG01/003/010/090/RUG01-003010090_2021_0001_AC.pdf (accessed on 23 March 2024).

- Clayton, Jim, David C. Ling, and Andy Naranjo. 2009. Commercial real estate valuation: Fundamentals versus investor sentiment. Journal of Real Estate Finance and Economics 38: 5–37. [Google Scholar] [CrossRef]

- Clayton, Jim, David Geltner, and Stanley W. Hamilton. 2001. Smoothing in commercial property valuations: Evidence from individual appraisals. Real Estate Economics 29: 337–60. [Google Scholar] [CrossRef]

- Eichholtz, Piet M. A., Martin Hoesli, Bryan D. MacGregor, and Nanda Nanthakumaran. 1995. Real estate portfolio diversification by property type and region. Journal of Property Finance 6: 39–59. [Google Scholar] [CrossRef]

- Gabauer, David, and Rangan Gupta. 2020. Spillovers across macroeconomic, financial and real estate uncertainties: A time-varying approach. Structural Change and Economic Dynamics 52: 167–73. [Google Scholar] [CrossRef]

- Geltner, David. 1993. Estimating Market Values from Appraised Values without Assuming an Efficient Market. The Journal of Real Estate Research 8: 325–45. [Google Scholar] [CrossRef]

- Gholipour, Hassan F. 2019. The effects of economic policy and political uncertainties on economic activities. Research in International Business and Finance 48: 210–18. [Google Scholar] [CrossRef]

- Gholipour, Hassan F., Amir Arjomandi, Mohammad Reza Farzanegan, and Sharon Yam. 2022. Global and local economic uncertainties and office vacancy in Australia: A sub-class analysis. Applied Economics 54: 5393–411. [Google Scholar] [CrossRef]

- Gholipour, Hassan F., Reza Tajaddini, Mohammad Reza Farzanegan, and Sharon Yam. 2021. Responses of REITs index and commercial property prices to economic uncertainties: A VAR analysis. Research in International Business and Finance 58: 101457. [Google Scholar] [CrossRef]

- Hargitay, Stephen. E., and Shi-Ming Yu. 1993. Property Investment Decisions: A Quantitative Approach, 1st ed. London: Routledge. [Google Scholar]

- Heinig, Steffen, and Anupam Nanda. 2018. Measuring sentiment in real estate—A comparison study. Journal of Property Investment and Finance 36: 248–58. [Google Scholar] [CrossRef]

- Hoesli, Martin, and Elias Oikarinen. 2016. Are public and private asset returns and risks the same? Evidence from real estate data. Journal of Real Estate Portfolio Management 22: 179–98. [Google Scholar] [CrossRef]

- Hoskins, Nicholas, David Higgins, and Richard Cardew. 2004. Macroeconomic Variables and Real Estate Returns: An International Comparison. The Appraisal Journal 72: 163. [Google Scholar]

- IMF. 2022. World Economic Outlook; War Sets Back the Global Recovery. Washington, DC: International Monetary Fund. Available online: https://www.imf.org/-/media/Files/Publications/WEO/2022/April/English/text.ashx (accessed on 1 April 2024).

- Jackson, Cath, and Allison Orr. 2019. Investment decision-making under economic policy uncertainty. Journal of Property Research 36: 153–85. [Google Scholar] [CrossRef]

- JLL. 2023. Investor Sentiment Barometer 2023: Investors are Responding to Macro Headwinds by Pivoting Their Strategies and Focusing on Selected Sectors. Available online: https://www.jll.com.au/en/trends-and-insights/research/investor-sentiment-barometer (accessed on 15 April 2024).

- Johansen, Søren. 1995. Likelihood-Based Inference in Cointegrated Vector Autoregressive Models. Oxford: Oxford University Press. [Google Scholar]

- Knight, Frank Hyneman. 1921. Risk, Uncertainty, and Profit. Edited by Schaffner Hart and Houghton Mifflin Marx. Boston: Houghton Mifflin. [Google Scholar]

- Lan, Ting. 2019. Intrinsic bubbles and Granger causality in the Hong Kong residential property market. Frontiers of Business Research in China 13: 17. [Google Scholar] [CrossRef]

- Lang, Elmar, Ferdinand Mager, and Kerstin Hennig. 2022. Uncertainty and commercial real estate excess returns in European markets. Journal of Property Research 39: 321–37. [Google Scholar] [CrossRef]

- Lashgari, Yasaman S., and Sina Shahab. 2022. The Impact of the COVID-19 Pandemic on Retail in City Centres. Sustainability 14: 11463. [Google Scholar] [CrossRef]

- Lee, Chyi Lin. 2008. Volatility Spillover in Australian Commercial Property. Pacific Rim Property Research Journal 14: 434–77. [Google Scholar]

- Lee, Chyi Lin, Simon Stevenson, and Hyunbum Cho. 2022. Listed real estate futures trading, market efficiency, and direct real estate linkages: International evidence. Journal of International Money and Finance 127: 102693. [Google Scholar] [CrossRef]

- Lieser, Karsten, and Alexander Peter Groh. 2014. The Determinants of International Commercial Real Estate Investment. Journal of Real Estate Finance and Economics 48: 611–59. [Google Scholar] [CrossRef]

- Ling, David C., Andy Naranjo, and Benjamin Scheick. 2010. Investor Sentiment and Asset Pricing in Public and Private Markets. Paper presented at the 46th Annual American Real Estate and Urban Economics Association (AREUEA) Conference, 29 November 2010. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1717110 (accessed on 15 April 2024).

- Ling, David C., and Andy Naranjo. 1997. Economic Risk Factors and Commercial Real Estate Returns. Journal of Real Estate Finance and Economics 15: 283–307. [Google Scholar] [CrossRef]

- Ling, David C., Chongyu Wang, and Tingyu Zhou. 2020. A first look at the impact of COVID-19 on commercial real estate prices: Asset-level evidence. Review of Asset Pricing Studies 10: 669–704. [Google Scholar] [CrossRef]

- Marcato, Gianluca, and Anupam Nanda. 2016. Information Content and Forecasting Ability of Sentiment Indicators: Case of Real Estate Market. Journal of Real Estate Research 38: 165–204. [Google Scholar] [CrossRef]

- McDonald, Robert, and Daniel Siegel. 1986. The value of waiting to invest. Quarterly Journal of Economics 101: 707–27. [Google Scholar] [CrossRef]

- Meinen, Philipp, and Oke Roehe. 2017. On measuring uncertainty and its impact on investment: Cross-country evidence from the euro area. European Economic Review 92: 161–79. [Google Scholar] [CrossRef]

- Milcheva, Stanimira. 2022. Volatility and the Cross-Section of Real Estate Equity Returns during COVID-19. Journal of Real Estate Finance and Economics 65: 293–320. [Google Scholar] [CrossRef]

- Moore, Angus. 2017. Measuring Economic Uncertainty and Its Effects. Economic Record 93: 550–75. [Google Scholar] [CrossRef]

- MSCI. 2023. The Property Council of Australia/MSCI Australia Annual Property Index (Unfrozen) Published Quarterly (AUD). Available online: www.msci.com (accessed on 1 March 2024).

- Nanda, Anupam, Yishuang Xu, and Fangchen Zhang. 2021. How would the COVID-19 pandemic reshape retail real estate and high streets through acceleration of E-commerce and digitalization? Journal of Urban Management 10: 110–24. [Google Scholar] [CrossRef]

- Nayar, Nandkumar, Mckay Price, and Ke Shen. 2023. Macroeconomic Uncertainty and Predictability of Real Estate Returns: The Impact of Asset Liquidity. Bethlehem: Perella Department of Finance, College of Business, Lehigh University. [Google Scholar] [CrossRef]

- Newell, Graeme, and Hsu Wen Peng. 2006. The Significance of Emerging Property Sectors in Property Portfolios. Pacific Rim Property Research Journal 12: 177–97. [Google Scholar] [CrossRef]

- Newell, Graeme, and Muhammad Jufri Marzuki. 2023. The impact of the COVID-19 crisis on global real estate capital flows. Journal of Property Investment and Finance 41: 553–73. [Google Scholar] [CrossRef]

- Nguyen, Canh Phuc, and Gabriel S. Lee. 2021. Uncertainty, financial development, and FDI inflows: Global evidence. Economic Modelling 99: 105473. [Google Scholar] [CrossRef]

- Pesaran, Hashem H, and Yongcheol Shin. 1998. Generalized impulse response analysis in linear multivariate models. Economics Letters 58: 17–29. [Google Scholar] [CrossRef]

- Property Council of Australia. 2023. Property Council of Australia; The Data Room. Available online: https://www.propertycouncil.com.au/news-research/overview/the-data-room (accessed on 3 March 2024).

- Quan, Daniel C., and John M. Quigley. 1989. Inferring an Investment Return Series for Real Estate from Observations on Sales. Real Estate Economics 17: 218–30. [Google Scholar] [CrossRef]

- RBA. 2023. Cash Rate Target|RBA. Cash Rate Target. Available online: https://www.rba.gov.au/statistics/cash-rate/ (accessed on 3 March 2024).

- Roberts, Claire, and John Henneberry. 2007. Exploring office investment decision-making in different European contexts. Journal of Property Investment and Finance 25: 289–305. [Google Scholar] [CrossRef]

- Sah, Paul, Paul Gallimore, and John Sherwood Clements. 2010. Experience and real estate investment decision-making: A process-tracing investigation. Journal of Property Research 27: 207–19. [Google Scholar] [CrossRef]

- Schätz, Alexander, and Steffen Sebastian. 2009. The links between property and the economy—Evidence from the British and German markets. Journal of Property Research 26: 171–91. [Google Scholar] [CrossRef]

- Sims, Christopher A. 1980. Macroeconomics and Reality. Econometrica: Journal of the Economic Society 48: 1–48. [Google Scholar] [CrossRef]

- Stock, James H., and Mark W. Watson. 2001. Vector Autoregressions. Journal of Economic Perspectives 15: 101–15. [Google Scholar] [CrossRef]

- Tsolacos, Sotiris, Yi Wu, and Samuel Duah. 2018. The Joint Dynamics of European Office Yields. Available online: https://ideas.repec.org/p/arz/wpaper/eres2018_273.html (accessed on 23 November 2023).

- Wang, Sen, Yanni Zeng, Jiaying Yao, and Hao Zhang. 2020. Economic policy uncertainty, monetary policy, and housing price in China. Journal of Applied Economics 23: 235–52. [Google Scholar] [CrossRef]

- Wu, Ji, Jing Zhang, Shiyu Zhang, and Liping Zou. 2020. The economic policy uncertainty and firm investment in Australia. Applied Economics 52: 3354–78. [Google Scholar] [CrossRef]

| Variable | Description | Source |

|---|---|---|

| Off_Rent | Prime office net face rents | CBRE Research |

| Off_Cap | Prime office capital values | |

| Ret_Rent | Regional retail net face rents | |

| Ret_Cap | Regional retail capital values | |

| Ind_Rent | Super-prime industrial net face rents | |

| Ind_Cap | Super-prime industrial capital values | |

| EPU | Economic policy uncertainty index (Australia) | Economic policy uncertainty www.policyuncertainty.com (accessed on 8 April 2024) |

| CPI | Consumer price index (quarterly % change) | Australia Bureau of Statistics |

| GDP | Gross domestic product (quarterly % change) | |

| UNEM | Unemployment rate (expressed in %) | |

| HP | Real house price index, deflated by CPI |

| Statistics | Normality | ADF Test | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Variable | Mean | Median | Min | Max | Std. Dev. | Skew. | Kurt. | JB-Stat | Prob. | Lags | Level |

| Off_rent | 6.430 | 6.487 | 6.017 | 6.796 | 0.245 | −0.376 | −1.078 | 6.144 ** | 0.014 | 3 | I (0) |

| Off_cap | 9.225 | 9.215 | 8.558 | 9.890 | 0.401 | −0.053 | −1.147 | 4.782 * | 0.063 | 3 | I (0) |

| Ret_rent | 7.260 | 7.295 | 6.906 | 7.404 | 0.144 | −1.075 | 0.107 | 16.413 *** | 0.026 | 1 | I (0) |

| Ret_cap | 10.108 | 10.153 | 9.580 | 10.484 | 0.215 | −0.960 | 0.513 | 13.758 *** | 0.085 | 0 | I (0) |

| Ind_rent | 4.615 | 4.667 | 4.317 | 4.909 | 0.143 | −0.964 | −0.068 | 13.756 *** | 0.024 | 0 | I (1) |

| Ind_cap | 7.314 | 7.298 | 6.652 | 8.224 | 0.351 | 0.375 | −0.006 | 1.853 | 0.000 | 0 | I (1) |

| EPU | 4.533 | 4.581 | 3.338 | 5.743 | 0.542 | −0.156 | −0.243 | 0.665 | 0.013 | 1 | I (0) |

| CPI | 2.603 | 2.500 | −0.300 | 7.300 | 1.258 | 1.243 | 2.676 | 51.026 *** | 0.004 | 3 | I (1) |

| GDP | 0.708 | 0.700 | −6.700 | 3.900 | 1.096 | −3.152 | 25.419 | 2132.99 *** | 0.001 | 3 | I (0) |

| UNEM | 5.403 | 5.391 | 3.486 | 6.962 | 0.739 | −0.128 | 0.106 | 0.226 | 0.079 | 1 | I (0) |

| HP | 4.580 | 4.573 | 4.061 | 4.955 | 0.199 | −0.322 | −0.157 | 1.153 | 0.022 | 3 | I (0) |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ahiadu, A.A.; Abidoye, R.B.; Yiu, T.W. Economic Policy Uncertainty and Commercial Property Performance: An In-Depth Analysis of Rents and Capital Values. Int. J. Financial Stud. 2024, 12, 71. https://doi.org/10.3390/ijfs12030071

Ahiadu AA, Abidoye RB, Yiu TW. Economic Policy Uncertainty and Commercial Property Performance: An In-Depth Analysis of Rents and Capital Values. International Journal of Financial Studies. 2024; 12(3):71. https://doi.org/10.3390/ijfs12030071

Chicago/Turabian StyleAhiadu, Albert Agbeko, Rotimi Boluwatife Abidoye, and Tak Wing Yiu. 2024. "Economic Policy Uncertainty and Commercial Property Performance: An In-Depth Analysis of Rents and Capital Values" International Journal of Financial Studies 12, no. 3: 71. https://doi.org/10.3390/ijfs12030071

APA StyleAhiadu, A. A., Abidoye, R. B., & Yiu, T. W. (2024). Economic Policy Uncertainty and Commercial Property Performance: An In-Depth Analysis of Rents and Capital Values. International Journal of Financial Studies, 12(3), 71. https://doi.org/10.3390/ijfs12030071