Abstract

This study aimed to investigate the relationship between intellectual capital (human capital, relational capital, and structural capital) and sustainable competitive advantage, and the relationship between sustainable competitive advantage and organizational performance. The sample used was 308 SMEs located in Denpasar, Bali Province, Indonesia. Data were collected using a questionnaire that was sent directly to the CEO of the SMEs. Data were analyzed using SEM-PLS with WarpPLS 8.0. The findings show that there is a significant positive relationship between each dimension of intellectual capital (human capital, relational capital, and structural capital) and sustainable competitive advantage. Sustainable competitive advantage is also significantly and positively related to organizational performance. This study contributes to the understanding of intellectual capital in the value creation process of SMEs in developing countries. This study also enriches the previously developed conceptualization of intellectual capital by proposing intellectual capital as an important variable underlying the sustainability practices of companies, which allows them to achieve superior performances.

1. Introduction

Today, business organizations worldwide are competing to achieve a sustainable competitive advantage. In this regard, intellectual capital is perceived as one of the most valuable organizational resources that enables sustainable development (Gross-Gołacka et al. 2020). All dimensions of intellectual capital—human capital, relational capital, and structural capital—are a source of innovation, and new activities provide an effective sustainable competitive position (Duodu and Rowlinson 2019). Moreover, in a volatile market, the sustainable competitive position of business organizations is strongly influenced by their intellectual capital (Lu et al. 2021).

For small and medium enterprises (SMEs), intellectual capital dimensions are an important driver for technological innovation, which, in turn, spurs innovative performance and a sustainable competitive position (Agostini et al. 2017). Developing a sustainable business is challenging for SMEs in developing countries. In contrast, the high costs of procurement of tangible resources, due to financial limitations, prompt business organizations in developing countries to prefer intangible resources, particularly intellectual capital in order to spur competitiveness and performance (Lu et al. 2021). Thus, sustainable competitive advantage is no longer rooted in tangible resources and financial capital, but the effective channeling of unique intellectual resources (Balaji and Makhija 2001).

In several developing countries, SMEs contribute to economic empowerment in the form of job creation and the social welfare of the majority of the population, especially for those who do not have access to formal jobs in the public sector (Agyei 2018). In Indonesia, SMEs are the most important pillars of the economy. The Coordinating Ministry of Economic Affairs of the Republic of Indonesia (2021) noted that the number of SMEs in 2021 reached 64.2 million, with a contribution to the Gross Domestic Product of 61.07% (8573.89 trillion rupiah). The contribution of SMEs to the Indonesian economy includes the ability to absorb 97% of the total workforce and collect up to 60.4% of the total investment. However, bankruptcy and failure remain a problem for SMEs worldwide, especially in less developed economies (Kücher et al. 2020).

According to resource-based theory (RBT), firm resources, especially intangible ones, are more likely to contribute to firms achieving and maintaining superior performance when combined or integrated (Barney 1991). From the intellectual capital-based view (ICV), competitive advantage takes the form of resource characteristics that allow a company to outperform competitors in the same industry (Reed et al. 2006). Both of these became the theoretical motivation for conducting this study. Another motivation for conducting this research was that empirically, even though SMEs have a large influence on the global economy, attention to SMEs in the study of intellectual capital is still limited (Marzo and Scarpino 2016). The concept and nature of intellectual capital have been widely studied, but a common understanding of the role of intellectual capital in achieving a sustainable competitive advantage in organizations, with the changing environment and world economic situation, is still lacking (Lentjushenkova et al. 2019). Business organizations’ awareness of the importance of intellectual capital for their development is still low because of the intangible characteristics of intellectual capital, and the many elements it comprises (Gross-Gołacka et al. 2020).

Several researchers have examined the relationship between intellectual capital and sustainability issues, such as Chaudhry and Chaudhry (2022), who examine the effect of green intellectual capital on sustainable economic excellence in manufacturing companies in Pakistan; Lu et al. (2021), who examined the effect of intellectual capital on sustainable competitive advantage in terms of differentiation strategy and cost leadership strategy in Chinese and Pakistani companies; Mukherjee and Sen (2019), who examined the effect of intellectual capital on sustainable growth in Indian firms; and Xu and Wang (2018), who examined the relationship between intellectual capital and the sustainable growth of manufacturing companies in Korea. Other researchers have also conducted research on the relationship between sustainable competitive advantage and organizational performance, such as Patrisia et al. (2022), Khan et al. (2019), and Guimarães et al. (2017). Even so, it is difficult to find research that examines intellectual capital as an antecedent of sustainable competitive advantage, and that examines the impact of sustainable competitive advantage on organizational performance in a comprehensive research model.

Therefore, this research seeks to build an empirical model of organizational performance by considering the role of intellectual capital and sustainable competitive advantage. This is the novelty of this research. In addition, this study focuses on the context of SMEs, which have received less attention in the intellectual capital domain compared to larger organizations. The research questions to be answered in this study are: (a) Does intellectual capital (human capital, relational capital, and structural capital) relate to sustainable competitive advantage? (b) Does sustainable competitive advantage relate to organizational performance? Therefore, the purpose of this study is to investigate the relationship between intellectual capital (human capital, relational capital, and structural capital) and sustainable competitive advantage, and the relationship between sustainable competitive advantage and organizational performance.

Some of the contributions of this study are as follows: firstly, this study focuses on SMEs in developing countries, namely Indonesia, so that the findings enrich the understanding of intellectual capital in the value creation process in developing countries. Secondly, this study examines the impact of sustainable competitive advantage on organizational performance, which can increase the understanding that sustainable competitive advantage must be translated into organizational performance, to the extent that organizational performance is higher than competitors. Thirdly, this study also extends the previous studies by proposing intellectual capital as an important variable underlying the sustainability practices of companies for superior performances. Finally, the results of this study support the RBT and the ICV.

2. Literature Review

2.1. An Overview of the Resource-Based View and ICV

Organizations ensure their sustainability by making effective use of their available resources. The resource-based view (RBV) and ICV are frameworks that can explain resources from the perspective of competitive advantage. In this study, both are used to explain the achievement of organizational performance through sustainable competitive advantage, which is obtained from intellectual capital in business operations.

Barney (1991) proposed the main concept of the RBV, which is considered to be one of the most influential ideas in the RBV (Foss and Knudsen 2003). Barney (1991) examines the relationship between firm resources and sustainable competitive advantage. The results show that sustainable competitive advantage comes from exploiting internal strengths, and by responding to environmental opportunities while neutralizing external threats and avoiding internal weaknesses. After 20 years of development, Barney et al. (2011) stated that the RBV was mature enough to be called a theory, and renamed the RBV as RBT, which is widely recognized as one of the most prominent and powerful theories for describing, explaining, and predicting organizational relationships.

The RBT broadly defines resources—including all tangible and intangible assets, organizational processes, knowledge, capabilities, and other sources of potential competitive advantage (Lavie 2006)—that can be used to understand and implement value-creation strategies. Barney (1991) suggested that to create a sustainable competitive advantage, resources must be valuable, scarce, inimitable, and strategically unmatched. According to the RBT, when integrated, organizational resources—especially intangible resources—are highly likely to ensure that the organization achieves and maintains a superior performance (Grant 1996). Intangible knowledge has been described as intellectual capital.

The emergence of intellectual capital encourages the emergence of the ICV proposed by Reed et al. (2006). According to Reed et al. (2006) the ICV is a mid-range theory because it represents one specific aspect of the more general RBV; in this case the ICV is narrower because it only considers three resources that have been linked theoretically to a company’s competitive advantage. The ICV only deals with knowledge created and stored in the three capital components, i.e., in humans (human capital), social relations (social capital), and information technology systems and processes (organizational capital) (Edvinsson and Malone 1997; Wright et al. 2001). Furthermore, the ICV defines competitive advantage in terms of the characteristics of the resources that enable a business organization to outperform its competitors.

Previous researchers, such as Sveiby (1997), Bontis (1998), Jelčić (2007), and Bruggen et al. (2009), have developed a taxonomy of intellectual capital. According to them, intellectual capital is a form of knowledge, intelligence, and brain power activity that uses knowledge to create value and includes human, relational, and structural capital. Human capital reflects the knowledge, competence, and brain power of employees. Relationships with customers, suppliers, distributors, and other groups, in the form of strength, loyalty, and satisfaction, comprise relational capital. In contrast, structural capital refers to an organizational system, practice, and process.

2.2. Intellectual Capital and Sustainable Competitive Advantage

A sustainable competitive advantage will be achieved by a company if it is able to perform better than its competitors. A sustainable competitive advantage is an advantage in which the company can achieve or improve its competitive position in the market in the long term (Papula and Volná 2013). According to the RBT, sustainable competitive advantage is achieved by continuing to develop existing resources and by creating new firm resources and capabilities in response to rapidly changing market conditions. The main source of thriving companies in today’s economy is intangible resources, which are referred to as intellectual capital—human capital, relational capital, and structural capital.

In the context of the RBT, human capital can be a source of sustainable competitive advantage (Coff and Kryscynski 2011), but only when the isolation mechanism can prevent employees from passing on their valuable knowledge and skills to competing organizations (Barney 1991). As business organizations need human resources to facilitate the achievement of their goals (Burhan et al. 2017), their value increases when the intellect of their employees is highly developed (Lentjushenkova et al. 2019). Hashim (2012) highlighted that the skills, knowledge, and competence of employees are vital for SMEs not only to acquire new technologies and knowledge, but also to survive in a globalized world. Additionally, the knowledge, values, skills, and experience of employees have a significant impact on the social and environmental sustainability of SMEs, and this intellectual capital can be used to achieve competitive advantage, to promote innovation regarding social and environmental practices, and to protect SMEs from their competitors (Loucks et al. 2010).

Sustainable competitive advantage is achieved by implementing sustainable competitive advantage strategies supported by quality human capital. Human capital is an important source of competitive advantage because of its ability to interact with other sources and internal skills, knowledge, and experience while dealing with the diverse nature of problems and other forms of organizational innovation (Lu et al. 2021). Chaudhry and Chaudhry (2022) found a significant positive relationship between human capital and corporate sustainability. Human capital is a positive predictor of agility strategy, quality strategy, and cost strategy (Santa et al. 2022). Khan et al. (2022) found that the social sustainability and economic sustainability of companies increase with the increasing managerial ability of the CEO in the company.

Dyer and Singh (1998) indicate that relational capital is a strong predictor of competitive advantage. As relational capital allows the exchange of information between stakeholders and the organization, it provides organizations with the information to meet stakeholder expectations and needs. Moreover, knowledge sharing between stakeholders and organizations is necessary to support sustainable organizational practices (Matinaro et al. 2019). Omar et al. (2017), Xu and Wang (2018), and Chaudhry and Chaudhry (2022) report that relational capital is significantly and positively related to the sustainability of business organizations.

Organizations with strong structural capital have a culture that motivates employees to try to learn new information (Florin et al. 2003). However, organizations with poor procedures and systems are less likely to reach their full potential (Widener 2006). Therefore, policies and structures instituted by organizations play an important role in implementing and achieving sustainability (Yusliza et al. 2020). The findings of De Pablos (2004) suggest that structural capital is an important element in predicting the competitive advantage of an organization. Similar findings are shown by Dimitrakaki (2022), demonstrating that a strong level of learning and development of organizational knowledge tends to be positively related to achieving competitive advantage.

Based on the description above, the following hypotheses are formulated:

H1.

Human capital is positively related to sustainable competitive advantage.

H2.

Relational capital is positively related to sustainable competitive advantage.

H3.

Structural capital is positively related to sustainable competitive advantage.

2.3. Sustainable Competitive Advantage and Organizational Performance

In the context of practice, sustainable competitive advantage should translate into higher performance in comparison to competitors (Guimarães et al. 2017), which is conventionally measured by, for example, market share and profitability—the measures of financial performance (Fahy 2000). However, there is a need to include non-financial measures to evaluate organizational performance, as financial measures alone are not sufficient (Chenhall and Langfield-Smith 2007).

According to the RBT, company resources, including all assets, capabilities, organizational processes, company attributes, information, and knowledge, owned and/or managed by the organization enable it to develop and implement strategies that increase efficiency and effectiveness, and to ensure that its performance is superior. Reports indicate a significant positive relationship between sustainable competitive advantage and organizational performance (Elijah and Millicent 2018). Guimarães et al. (2017) suggest that the construct of sustainable competitive advantage is an important antecedent of organizational performance, as it highlights the fundamental attributes of organizations that are required to achieve positive economic consequences. Patrisia et al. (2022) found a significant positive effect of competitive advantage on business performance.

Based on these description above, the following hypothesis is formulated:

H4.

Sustainable competitive advantage is positively related to organizational performance.

3. Methodology

The positivism paradigm used in this research is to seek the interconnection of social phenomena, namely the practice of intellectual capital in SMEs in developing countries, especially Indonesia, in order to produce a general causal law so that an event can be controlled and predicted. This study used a sample of SMEs located in Denpasar, Bali province, Indonesia. Based on data from the Denpasar City Communication Informatics and Statistics Office (2022), there were 1348 SMEs in Denpasar, which included South Denpasar, East Denpasar, West Denpasar, and North Denpasar. The sample size of 308 SMEs was determined using the sample size determination formula (Yamane 1973):

where n is the sample size, N is the population, and e is the tolerable error.

A simple, random sampling technique was used, with the sample selection procedure using a lottery without returns until 308 SMEs were selected. Data were collected from CEOs of SMEs, who represented organizations as respondents, using questionnaires that were directly sent to the respondents.

The questionnaire was accompanied by a cover letter that explained the purpose of the study and guaranteed data confidentiality. Two weeks after sending out the questionnaires, responses began to be received. Of the 308 questionnaires sent, 105 were filled in and received (response rate: 34.09%). However, only 99 were filled out completely by the respondents and were used in this study (usable response rate: 32.14%).

Non-response bias test was conducted to determine whether the characteristics of the respondents who returned filled-in questionnaires were different from those of respondents who did not return them (non-response). In this study, respondents who returned answers to the questionnaire after the specified time were considered to represent the answers of non-response respondents. The results of the independent sample t-test (Table 1) show that the t-value at equal variance was −0.158, with a p-value of 0.875 (>0.05). Therefore, there is no difference in scores between the returning and non-returning questionnaire groups, indicating that there was no non-response bias. Most of the participants in this study are males (66.66%), had been employed for >5 years (75.75%), and have bachelor’s degrees as their highest qualification (80.19%).

Table 1.

Non-response bias results.

Measurements of intellectual capital, including human, relational, and structural capital, and organizational performance are adapted from Wang et al. (2014). Human and relational capital are measured by five items, whereas structural capital is measured by seven items, and organizational performance is measured by 11 items. Sustainable competitive advantage is measured using a tool adopted from Guimarães et al. (2017) consisting of six items. All measurements are based on a five-point Likert scale, ranging from 1 (strongly disagree) to 5 (strongly agree).

Table 2 summarizes the descriptive statistics of the research variables, which include the minimum and maximum values (theoretical and actual), mean, and standard deviation. The mean value indicates that the responses of the participants to the research variables were similar. Respondents answer that they agree to the variable items of human capital (HC), relational capital (RC), sustainable competitive advantage (SCA), and organizational performance (OP), which are indicated by the mean values of 4.15, 4.18, 4.28, and 4.38, respectively. Similarly, the mean value of the structural capital (SC) variable is 3.69, which is close to 4.00, indicating that the respondents agree with these variable items.

Table 2.

Descriptive statistics of variable studied.

The research hypothesis is tested using variance-based structural equation modeling (SEM-PLS), which is able to test several dependent and independent variables simultaneously and works efficiently with small sample sizes and complex models. This study uses WarpPLS software (ver. 8.0).

4. Results

4.1. Measurement Model Analysis

The reliability is measured based on composite reliability and Cronbach’s alpha. Fornell and Larcker (1981) and Nunnally (1978) suggested reliability requirements in the form of composite reliability and Cronbach’s alpha values >0.70. Table 3 illustrates that the reliability of the research instruments for all constructs is fulfilled because it attains the minimum reliability requirements.

Table 3.

Reliability and convergent validity.

Construct validity is determined using convergent and discriminant validities. Convergent validity is based on the loading value of each indicator and the average variance extracted (AVE). Table 4 indicates that all indicators are significant and exhibit a loading value >0.60. The minimum loading value of 0.60 is important because it shows that this measure contributes to at least 60% of the variance of the underlying latent variable (Chin 1998). According to Fornell and Larcker (1981), the eligible AVE criterion is valued at >0.50. The AVE value for all research constructs suggests that these criteria are met (Table 3). Therefore, the convergent validity for the reflective construct of this research is fulfilled.

Table 4.

Combined loading and cross-loading results.

Discriminant validity in this study is tested by cross-loading. The value of loading to another construct (cross-loading) is expected to be lower than that of the construct. The cross-loading results in Table 4 reveal that the discriminant validity criteria are met. For example, the HC1 indicator exhibits a greater loading to the HC construct of 0.795 compared to cross-loading to other constructs (RC, SC, SCA, OP), which shows lower values compared to the HC construct. The same applies to the loading value of other indicators (bold and brackets) to other constructs.

4.2. Structural Model Analysis

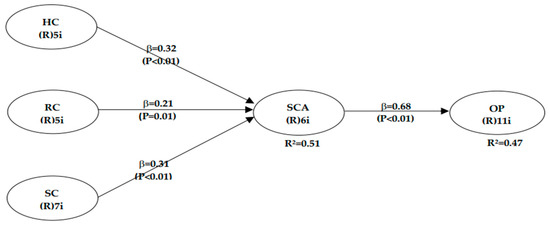

The full-model test shows a significant positive relationship (β = 0.317; p < 0.001) between human capital and sustainable competitive advantage. There is a significant positive relationship between relational capital and sustainable competitive advantage (β = 0.215; p = 0.013), as well as structural capital and sustainable competitive advantage (β = 0.311; p < 0.001). Therefore, H1, H2, and H3 are confirmed.

Table 5 suggests a significant positive relationship between sustainable competitive advantage and organizational performance (β = 0.683; p < 0.001). Thus, the results of the full-model test support H4.

Table 5.

PLS results for full model.

The coefficient of determination in this study uses the R2 value. The R2 value of the sustainable competitive advantage construct is 0.515 (Table 5, Figure 1), indicating that the variance of sustainable competitive advantage could be explained, by 51.5%, by the variance of intellectual capital—human capital, relational capital, and structural capital. The R2 value of the organizational performance construct is 0.466, suggesting that the variance of organizational performance could be explained by the variance of intellectual capital—human capital, relational capital, and structural capital—and sustainable competitive advantage of 46.6% (Table 1, Figure 1).

Figure 1.

PLS results. Note: HC: Human Capital, RC: Relational Capital, SC: Structural Capital, SCA: Sustainable Competitive Advantage, OP: Organizational Performance.

An effect size test is conducted to determine the practical significance and estimate the extent to which the statistical findings of this study corroborate with the population.

According to Kock (2014), there are three categories of effect size: weak (0.02), medium (0.15), and large (0.35). Table 6 summarizes the largest effect size test value, which exhibits a sustainable competitive advantage on organizational performance (0.466). This value is included in the large effect size category, which means that from a practical perspective, sustainable competitive advantage has an important role in driving organizational performance.

Table 6.

Effect size test results.

5. Discussion

The findings of this study indicate that intangible resources—in this case, intellectual capital—benefit sustainable competitive advantage and organizational performance. Intellectual capital is an intangible resource that works towards achieving sustainable competitive advantage and higher organizational performance (Kianto et al. 2014). This study succeeded in confirming H1, H2, and H3, by proving that the three dimensions of intellectual capital are significantly and positively related to sustainable competitive advantage. The better the quality of intellectual capital owned, the more sustainable competitive advantages can be achieved by SMEs. Employees of SMEs in Denpasar are creative, experienced, and often develop new ideas and knowledge, all of which help companies to explore market opportunities and defend against environmental threats by increasing revenues and/or reducing expenses. Furthermore, the training provided by the company strengthens the professional skills of the employees. These main resources for the company are difficult to obtain or imitate by competitors and cannot be easily substituted. This finding is consistent with that of Mukherjee and Sen (2019), who claim that intellectual capital is a significant driver of sustainable growth in developing companies. In addition, the results of this study are also in line with the findings of Lu et al. (2021), who show that in Pakistan and China, human capital exhibited a positive and significant effect on sustainable competitive advantage. The findings of this study also support Chaudhry and Chaudhry (2022), who found that human capital has a significant positive effect on sustainable competitive advantage in manufacturing companies certified to ISO 14001 in Pakistan.

The significantly positive relationship between relational capital and sustainable competitive advantage reveals that the exploration of market opportunities or the company’s efforts to defend itself from environmental threats resulted from intense communication and effective collaboration to identify and solve problems. The achievement of sustainable competitive advantage is also supported by interactions with stakeholders, including customers and strategic partners, which are always well maintained by the company. De Castro et al. (2004) insist that relational capital contributes to creating reputational value for the company and is considered an open system that is in dialogue with the external environment and interested parties. This finding is also supported by that of Xu and Wang (2018), who conclude that relational capital significantly contributes to the growth of corporate sustainability in Korea. The findings of this study suggest that intellectual capital plays an important role for companies, and helps them to survive in the long term in a dynamic market (Bontis et al. 2018) by using a strategy that is different from their competitors (Lu et al. 2021). The findings of this study also support Chaudhry and Chaudhry (2022), who found relational capital to have a significant positive effect on sustainable competitive advantage.

This study confirms that SMEs with efficient operating procedures have a flexible and comfortable culture and atmosphere, and can rapidly respond to changes, making it difficult for competitors to imitate their products and services. The systems and procedures of the companies that support innovation encourage companies to adhere to environmental sustainability by using key resources in the production process and product development. Emphasis on investment in the development of new markets has also encouraged companies to be responsible while using their main resources, particularly economically, to provide goods and services to the community. The findings of this study support the claim (Chen 2008) that structural capital provides a competitive advantage to firms in China. In addition to China, the role of structural capital in sustainable competitive advantage, other strategic advantages, and cost leadership strategies has also been reported for companies in Pakistan (Lu et al. 2021). The findings of this study imply that companies investing in intangible resources (Khan et al. 2019) and their organizational culture (Jardon and Martínez-Cobas 2019) can gain sustainable competitive advantage. Indeed, adequate investment in the dimensions of intellectual capital is an important factor for the strategic position of a business (Kong and Ramia 2010).

Confirmation of H1, H2, and H3 of this research, as described above, shows the importance of intellectual capital as a creator of productivity, competitiveness, and the long-term sustainability of an organization (Singh et al. 2019). These findings support the ICV, which identifies that intellectual capital is a key production factor that can ensure a sustainable competitive advantage for companies. Intellectual capital has an inevitable role to play in the value creation process and is a significant determinant of a company’s market success (Radjenović and Krstić 2017). In a rapidly changing environment, companies achieve and maintain their competitive advantage by mobilizing and profitably exploiting intellectual resources.

This study has also proven that sustainable competitive advantage has a significant positive relationship with organizational performance, so that H3 is accepted. These findings support the RBV, which illustrates that a company’s superior performance is contributed to by a combination and integration of resources. Increasing the value of the company increases its competitive advantage, which leads to an increase in company performance. The company’s ability to face sustainability challenges determined its profits and market viability (de Villiers and Sharma 2020). Therefore, the construct of sustainable competitive advantage is an important antecedent of organizational performance because sustainable competitive advantage is a basic attribute needed by organizations to achieve positive economic consequences (Guimarães et al. 2017). Moreover, the company’s ability to explore market opportunities and its main resources, which are difficult to obtain, replace, or imitate by competitors, make the rate of return on investment and assets, as well as the rate of return on sales, of the company better than those of its main competitors. This also has an impact on obtaining higher profits and sales growth, compared to its competitors. The company’s commitment to the welfare of employees, society, and the environment, as well as responsibly using key resources in economic, ethical, and philanthropic aspects, shows that the company is responsive and exhibits good quality development. This finding emphasizes that intellectual capital can play a strategic role in social relationships to achieve the set mission or raison d’être and fulfill the interest of local communities, people, or social groups by performing commercial activities (Bontis et al. 2018). The results of this study are similar to those of Saeidi et al. (2015), Walsh and Dodds (2017), Khan et al. (2019), and Dimitrakaki (2022) who find a significant positive relationship between sustainable competitive advantage and organizational performance.

6. Conclusions

This study investigates the relationship between each dimension of intellectual capital and sustainable competitive advantage and highlights the importance of the relationship between sustainable competitive advantage and organizational performance, all of which are found to be significantly and positively related. These findings indicate that human capital plays a significant role as an important intangible resource in building a sustainable competitive advantage. The findings of this study also show empirical evidence that relational capital is a determinant in creating a sustainable competitive advantage. These findings indicate that the influence of relational capital cannot be underestimated in creating a sustainable competitive advantage. The results of this study also provide empirical evidence that structural capital is a significant predictor in supporting the construction of a sustainable competitive advantage.

These results contribute to the fact that the significant role of structural capital cannot be ignored in influencing sustainable competitive advantage. Furthermore, the empirical evidence of this research is demonstrated by the significant effect of sustainable competitive advantage on increasing organizational performance. Likewise, if sustainable competitive advantage increases, then organizational performance will also increase. Therefore, human capital, relational capital, and structural capital play an important role in achieving sustainable competitive advantage, which ultimately results in increased organizational performance. This finding enriches the understanding of intellectual capital in the value creation process of SMEs in developing countries. In addition, it also enhances the understanding of sustainable competitive advantage’s translation into organizational performance.

The findings of this study provide theoretical implications supporting the RBT and ICV by asserting that intangible resources—in this case, intellectual capital—benefit sustainable competitive advantage and organizational performance. This has implications for academics and researchers who must explore the role of intellectual capital more deeply so that the theory of intellectual capital can be further developed. The methodological implication of this research is that it can provide information, description, and comparison for further studies that wish to discuss similar topics, but with different conditions of research subjects, research variables, and research periods.

The practical implication of this research is that it is recommended that SME owners continue to develop and maintain their intellectual capital through investment in workforce recruitment and selection, workforce training and development, collaboration with stakeholders, organizational learning, and others. SMEs must allocate more investment to intangible resources, especially intellectual capital, in order to have strategic resources that are valuable, scarce, inimitable, and strategically unmatched, so as to be able to create competitive advantage and produce organizational performance that exceeds their competitors.

To be able to generalize the results of this study, further studies must include a large sample size. Subsequent research can also examine the direct relationship of intellectual capital with organizational performance, as well as the role of sustainable competitive advantage as a mediator. Further investigation is also required to analyze organizational performance using its components—operational and financial performance.

Author Contributions

Conceptualization, P.D.A., L.K.D., and A.C.; methodology, P.D.A., L.K.D., and A.C.; software, P.D.A.; validation, P.D.A., L.K.D., and A.C.; formal analysis, P.D.A.; investigation, P.D.A., L.K.D., and A.C.; resources, P.D.A., L.K.D., and A.C.; data curation, P.D.A.; writing—original draft preparation, P.D.A., L.K.D., and A.C.; writing—review and editing, P.D.A., L.K.D., and A.C.; visualization, P.D.A.; supervision, P.D.A.; project administration, P.D.A., L.K.D., and A.C.; funding acquisition, P.D.A., L.K.D., and A.C. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by the Ministry of Education, Culture, Research and Technology of the Republic of Indonesia, grant number 160/E5/PG.02.00.PT/2022, 0967/LL8/Ak.04/2022, 731/UNWAR/LEMLIT/PD-13/2022, and the APC was funded by the Ministry of Education, Culture, Research and Technology of the Republic of Indonesia.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Acknowledgments

The authors would like to thank the Ministry of Education, Culture, Research and Technology of the Republic of Indonesia.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Agostini, Lara, Anna Nosella, and Roberto Filippini. 2017. Does Intellectual Capital Allow Improving Innovation Performance. Journal of Intellectual Capital 18: 400–18. [Google Scholar] [CrossRef]

- Agyei, Samuel Kwaku. 2018. Culture, Financial Literacy, and SME Performance in Ghana. Cogent Economics and Finance 6: 1–16. [Google Scholar] [CrossRef]

- Balaji, Y., and M. Makhija. 2001. The Knowledge Imperative. Special Advertising Supplement, March 15. [Google Scholar]

- Barney, Jay B. 1991. Firm Resources and Sustained Competitive Advantage. Advances in Strategic Management 17: 203–27. [Google Scholar] [CrossRef]

- Barney, Jay B., David J. Ketchen, and Mike Wright. 2011. The Future of Resource-Based Theory: Revitalization or Decline? Journal of Management 37: 1299–315. [Google Scholar] [CrossRef]

- Bontis, Nick, Massimo Ciambotti, Federica Palazzi, and Francesca Sgro. 2018. Intellectual Capital and Financial Performance in Social Cooperative Enterprises. Journal of Intellectual Capital 19: 712–31. [Google Scholar] [CrossRef]

- Bontis, Nick. 1998. Intellectual Capital: An Exploratory Study That Develops Measures and Models. Management Decision 36: 63–76. [Google Scholar] [CrossRef]

- Bruggen, Alexander, Philip Vergauwen, and Mai Dao. 2009. Determinants of Intellectual Capital Disclosure: Evidence from Australia. Management Decision 47: 233–45. [Google Scholar] [CrossRef]

- Burhan, Nik Ahmad Sufian, Razli Che Razak, Fauzilah Salleh, and María Elena Labastida Tovar. 2017. The Higher Intelligence of the ‘Creative Minority’ Provides the Infrastructure for Entrepreneurial Innovation. Intelligence 65: 93–106. [Google Scholar] [CrossRef]

- Chaudhry, Naveed Iqbal, and Muhammad Amir Chaudhry. 2022. Green Intellectual Capital and Corporate Economic Sustainability: The Mediating Role of Financial Condition. Pakistan Journal of Commerce and Social Science 16: 257–78. [Google Scholar]

- Chen, Yu-Shan. 2008. The Positive Effect of Green Intellectual Capital on Competitive Advantages of Firms. Journal of Business Ethics 77: 271–86. [Google Scholar] [CrossRef]

- Chenhall, Robert H., and Kim Langfield-Smith. 2007. Multiple Perspectives of Performance Measuresr. European Management Journal 25: 266–82. [Google Scholar] [CrossRef]

- Chin, Wynne W. 1998. The Partial Least Squares Approach for Structural Equation Modeling. In Modern Methods for Business Research, 295–358. London: Lawrence Erlbaum Associates. [Google Scholar]

- Coff, Russell, and David Kryscynski. 2011. Drilling for Micro-Foundations of Human Capital-Based Competitive Advantages. Journal of Management 37: 1429–43. [Google Scholar] [CrossRef]

- Coordinating Ministry of Economic Affairs of the Republic of Indonesia. 2021. Siaran Pers HM.4.6/103/SET.M.EKON.3/05/2021. UMKM Menjadi Pilar Penting Dalam Perekonomian Indonesia. Available online: https://ekon.go.id/publikasi/detail/2969/umkm-menjadi-pilar-penting-dalam-perekonomian-indonesia (accessed on 5 January 2022).

- De Castro, Gregorio Martín, Pedro López Sáez, and José Emilio Navas López. 2004. The Role of Corporate Reputation in Developing Relational Capital. Journal of Intellectual Capital 5: 575–85. [Google Scholar] [CrossRef]

- De Pablos, Patricia Ordóñez. 2004. The Nurture of Knowledge-Based Resources through the Design of an Architecture of Human Resource Management Systems: Implications for Strategic Management. International Journal of Technology Management 27: 533–43. [Google Scholar] [CrossRef]

- Denpasar City Communication Informatics and Statistics Office. 2022. Denpasar City MSME Data. Available online: https://bankdata.denpasarkota.go.id/?page=Data-Detail&language=id&domian=bankdata.denpasarkota.go.id&data_id=1606876170 (accessed on 1 April 2022).

- Dimitrakaki, Ioanna. 2022. Organizational Knowledge as a Source of Competitive Advantage-Amazon Case Study. London Journal of Research in Management and Business 22: 27–37. [Google Scholar]

- Duodu, Bismark, and Steve Rowlinson. 2019. Intellectual Capital for Exploratory and Exploitative Innovation. Exploring Linear and Quadratic Effects in Construction Contractor Firms. Journal of Intellectual Capital 20: 382–405. [Google Scholar] [CrossRef]

- Dyer, Jeffrey H., and Harbir Singh. 1998. Relational View: Cooperative Strategy and Sources of Interorganizational Competitive Advantage. Academy of Management Review 23: 660–79. [Google Scholar] [CrossRef]

- Edvinsson, Leif, and Michael S. Malone. 1997. Intellectual Capital: Realising Your Company’s True Value by Finding Its Hidden Brainpowe. New York, NY: Harper Collins. [Google Scholar]

- Elijah, Asante Boakye, and Adu-Damoah Millicent. 2018. The Impact of a Sustainable Competitive Advantage on a Firm’s Performance: Empirical Evidence from Coca-Cola Ghana Limited. Global Journal of Human Resource Management 6: 30–46. [Google Scholar]

- Fahy, John. 2000. The Resource-Based View of the Firm: Some Stumbling-Blocks on the Road to Understanding Sustainable Competitive Advantage. Journal of European Industrial Training 24: 94–104. [Google Scholar] [CrossRef]

- Florin, Juan, Michael Lubatkin, and William Schulze. 2003. A Social Capital Model of New Venture Performance. Academy of Management Journal 46: 374–84. [Google Scholar] [CrossRef]

- Fornell, Claes, and David F. Larcker. 1981. Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. Journal of Marketing Research XVIII: 39–50. [Google Scholar] [CrossRef]

- Foss, Nicolai J., and Thorbjørn Knudsen. 2003. The Resource-Based Tangle: Towards a Sustainable Explanation of Competitive Advantage. Managerial and Decision Economics 24: 291–307. [Google Scholar] [CrossRef]

- Grant, Robert M. 1996. Toward a Knowledge-Based Theory of the Firm. Strategic Management Journal 17: 109–22. [Google Scholar] [CrossRef]

- Gross-Gołacka, Elwira, Marta Kusterka-Jefmanska, and Bartłomiej Jefmanski. 2020. Can Elements of Intellectual Capital Improve Business Sustainability? The Perspective of Managers of SMEs in Poland. Sustainability 12: 1545. [Google Scholar] [CrossRef]

- Guimarães, Julio Cesar Ferro de, Eliana Andréa Severo, and César Ricardo Maia de Vasconcelos. 2017. Sustainable Competitive Advantage: A Survey of Companies in Southern Brazil. Brazilian Business Review 14: 352–67. [Google Scholar] [CrossRef]

- Hashim, Fariza. 2012. Challenges for the Internationalization of SMEs and the Role of Government: The Case of Malaysia. Journal of International Business and Economy 13: 97–122. [Google Scholar] [CrossRef]

- Jardon, Carlos M., and Xavier Martínez-Cobas. 2019. Leadership and Organizational Culture in the Sustainability of Subsistence Small Businesses: An Intellectual Capital Based View. Sustainability 11: 3491. [Google Scholar] [CrossRef]

- Jelčić, Karmen. 2007. Intellectual Capital: Handbook of IC Management in Companies. Available online: http:www2.hgk.hr/hrdc/IC_Management-Handbook.pdf (accessed on 6 March 2021).

- Khan, Muhammad Kaleem, R. M. Ammar Zahid, Khuram Shahzad, Muhammad Jameel Hussain, and Mbwana Mohamed Kitendo. 2022. Role of Managerial Ability in Environmental, Social, and Economics Sustainability: An Empirical Evidence from China. Journal of Environmental and Public Health 2022: 1–11. [Google Scholar] [CrossRef]

- Khan, Sher Zaman, Qing Yang, and Abdul Waheed. 2019. Investment in Intangible Resources and Capabilities Spurs Sustainable Competitive Advantage and Firm Performance. Corporate Social Responsibility and Environmental Management 26: 285–95. [Google Scholar] [CrossRef]

- Kianto, Aino, Paavo Ritala, John Christopher Spender, and Mika Vanhala. 2014. The Interaction of Intellectual Capital Assets and Knowledge Management Practices in Organizational Value Creation. Journal of Intellectual Capital 15: 362–75. [Google Scholar] [CrossRef]

- Kock, Ned. 2014. Advanced Mediating Effects Tests, Multi-Group Analyses, and Measurement Model Assessments in PLS-Based SEM. International Journal of E-Collaboration 10: 1–13. [Google Scholar] [CrossRef]

- Kong, Eric, and Gaby Ramia. 2010. A Qualitative Analysis of Intellectual Capital in Social Service Non-Profit Organisations: A Theory–Practice Divide. Journal of Management & Organization 16: 656–76. [Google Scholar] [CrossRef]

- Kücher, Alexander, Stefan Mayr, Christine Mitter, Christine Duller, and Birgit Feldbauer-Durstmüller. 2020. Firm Age Dynamics and Causes of Corporate Bankruptcy: Age Dependent Explanations for Business Failure. Review of Managerial Science 14: 633–61. [Google Scholar] [CrossRef]

- Lavie, Dovev. 2006. The Competitive Advantage of Interconnected Firms: An Extension of the Resource-Based View. Academy of Management 31: 638–58. [Google Scholar] [CrossRef]

- Lentjushenkova, Oksana, Vita Zarina, and Jelena Titko. 2019. Disclosure of Intellectual Capital in Financial Reports: Case of Latvia. Oeconomia Copernicana 10: 341–57. [Google Scholar] [CrossRef]

- Loucks, Elizabeth Stubblefield, Martin L. Martens, and Charles H. Cho. 2010. Engaging Small-and Medium-Sized Businesses in Sustainability. Sustainability Accounting, Management and Policy Journal 1: 178–200. [Google Scholar] [CrossRef]

- Lu, Yuqiu, Guowei Li, Zhe Luo, Muhammad Anwar, and Yunju Zhang. 2021. Does Intellectual Capital Spur Sustainable Competitive Advantage and Sustainable Growth?: A Study of Chinese and Pakistani Firms. SAGE Open 11: 1–18. [Google Scholar] [CrossRef]

- Marzo, Giuseppe, and Elena Scarpino. 2016. Exploring Intellectual Capital Management in SMEs: An in-Depth Italian Case Study. Journal of Intellectual Capital 17: 27–51. [Google Scholar] [CrossRef]

- Matinaro, Ville, Yang Liu, Tzong Ru (Jiun Shen) Lee, and Jurgen Poesche. 2019. Extracting Key Factors for Sustainable Development of Enterprises: Case Study of SMEs in Taiwan. Journal of Cleaner Production 209: 1152–69. [Google Scholar] [CrossRef]

- Mukherjee, Tutun, and Som Sankar Sen. 2019. Intellectual Capital and Corporate Sustainable Growth: The Indian Evidence. Journal of Business Economics and Environmental Studies 9: 5–15. [Google Scholar] [CrossRef]

- Nunnally, Jum C. 1978. Psychometric Theory. New York: McGraw-Hill. [Google Scholar]

- Omar, Muhamad Khalil, Yusmazida Mohd Yusoff, and Maliza Delima Kamarul Zaman. 2017. The Role of Green Intellectual Capital on Business Sustainability. World Applied Sciences Journal 35: 2558–63. [Google Scholar]

- Papula, Ján, and Jana Volná. 2013. Core Competence for Sustainable Competitive Advantage. Multidisciplinary Academic Research 2013: 1–7. Available online: http://www.mac-prague.com/ (accessed on 3 March 2019).

- Patrisia, Dina, Muthia Roza Linda, and Abror Abror. 2022. Creation of Competitive Advantage in Improving the Business Performance of Banking Companies. Jurnal Siasat Bisnis 26: 121–37. [Google Scholar] [CrossRef]

- Radjenović, Tamara, and Bojan Krstić. 2017. Intellectual Capital as the Source of Competitive Advantage: The Resource-Based View. Facta Universitatis, Series: Economics and Organization 14: 127–37. [Google Scholar] [CrossRef]

- Reed, Kira Kristal, Michael Lubatkin, and Narasimhan Srinivasan. 2006. Proposing and Testing an Intellectual Capital-Based View of the Firm. Journal of Management Studies 43: 867–93. [Google Scholar] [CrossRef]

- Saeidi, Sayedeh Parastoo, Saudah Sofian, Parvaneh Saeidi, Sayyedeh Parisa Saeidi, and Seyyed Alireza Saaeidi. 2015. How Does Corporate Social Responsibility Contribute to Firm Financial Performance? The Mediating Role of Competitive Advantage, Reputation, and Customer Satisfaction. Journal of Business Research 68: 341–50. [Google Scholar] [CrossRef]

- Santa, Ricardo, Mario Ferrer, Thomas Tegethoff, and Annibal Scavarda. 2022. An Investigation of the Impact of Human Capital and Supply Chain Competitive Drivers on Firm Performance in a Developing Country. PLoS ONE 17: e0274592. [Google Scholar] [CrossRef]

- Singh, Sanjay Kumar, Jin Chen, Manlio Del Giudice, and Abdul Nasser El-Kassar. 2019. Environmental Ethics, Environmental Performance, and Competitive Advantage: Role of Environmental Training. Technological Forecasting and Social Change 146: 203–11. [Google Scholar] [CrossRef]

- Sveiby, Karl Erik. 1997. The New Organizational Wealth. Managing & Measuring Knowledge-Based Assets. San Fransisco: Berrett-Koehler. [Google Scholar]

- de Villiers, Charl, and Umesh Sharma. 2020. A Critical Reflection on the Future of Financial, Intellectual Capital, Sustainability and Integrated Reporting. Critical Perspectives on Accounting 70: 101999. [Google Scholar] [CrossRef]

- Walsh, Philip R., and Rachel Dodds. 2017. Measuring the Choice of Environmental Sustainability Strategies in Creating a Competitive Advantage. Business Strategy and the Environment 26: 672–87. [Google Scholar] [CrossRef]

- Wang, Zhining, Nianxin Wang, and Huigang Liang. 2014. Knowledge Sharing, Intellectual Capital and Firm Performance. Management Decision 52: 230–58. [Google Scholar] [CrossRef]

- Widener, Sally K. 2006. Human Capital, Pay Structure, and the Use of Performance Measures in Bonus Compensation. Management Accounting Research 17: 198–221. [Google Scholar] [CrossRef]

- Wright, Patrick M., Benjamin B. Dunford, and Scott A. Snell. 2001. Human Resources and the Resource Based View of the Firm. Journal of Management 27: 701–21. [Google Scholar] [CrossRef]

- Xu, Jian, and Binghan Wang. 2018. Intellectual Capital, Financial Performance and Companies’ Sustainable Growth: Evidence from the Korean Manufacturing Industry. Sustainability 10: 4651. [Google Scholar] [CrossRef]

- Yamane, Taro. 1973. Statistics. An Introductory Analysis. New York: Harper & Row, Publishers. [Google Scholar]

- Yusliza, Mohd Yusoff, Jing Yi Yong, M. Imran Tanveer, T. Ramayah, Juhari Noor Faezah, and Zikri Muhammad. 2020. A Structural Model of the Impact of Green Intellectual Capital on Sustainable Performance. Journal of Cleaner Production 249: 119334. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).