Can ESG Stocks Be a Safe Haven during Global Crises? Evidence from the COVID-19 Pandemic and the Russia-Ukraine War with Time-Frequency Wavelet Analysis

,

,  ,

,

Abstract

:1. Introduction

2. Literature Review

- I.

- Do investments in ESG promote a superiority related to other investment choices? A theoretical approach

- II.

- ESG investments in times of crises

- III.

- Hypothesis Testing

- Is any kind of interdependence observed between each MSCI ESG index examined and all specific individual commodities indices and fear index?

- In case of interrelation between the variables being examined, which variable seems to affect the other more and in which direction (in-phase or out of phase)?

- Which is the band width and the time period extension during which this impact is more intense and robust in case of interdependencies between variables?

- Are any differences observed in the outcome related to the two periods of crises being examined (health vs. energy crisis)?

- Which can be considered as the most important safe heaven investment spots for potential investors?

3. Data and Methodology

3.1. Data and Variables

- MSCI Emerging Markets ESG Leaders Index (MSCI ESG EM): This index is a capitalization-weighted index that includes specific large and mid-capitalization stocks from 24 emerging markets that meet ESG criteria compared to their industry peers.

- MSCI ACWI ESG Leaders Index (MSCI ESG ACWI): This index is a capitalization-weighted index that includes specific large and mid-capitalization stocks from 23 developed and 24 emerging markets that meet ESG criteria compared to their industry peers.

- MSCI Europe ESG Leaders Index (MSCI ESG Europe): This index is a capitalization-weighted index that includes specific large and mid-capitalization stocks from 15 developed markets that meet high ESG criteria compared to their industry peers.

- MSCI KLD 400 Social Index (MSCI KLD): This index is a capitalization-weighted index that includes specific large and mid-capitalization stocks from 400 U.S. companies that have the highest ESG ratings in the stock market.

- MSCI North America ESG Leaders Index (MSCI ESG NA): This index includes large and mid-cap stocks from the U.S. and Canada, reflecting an investment strategy with a strong ESG profile.

- Chicago Board Options Exchange Volatility Index (VIX): This index represents the market’s expectations for upcoming price fluctuations of the S&P 500 Index.

- U.S. Economic Policy Uncertainty Index (EPU): This index quantifies media coverage of policy-related economic uncertainty.

- S&P GSCI Crude Oil Index (S&P Crude Oil): This index is a reliable benchmark for investment performance in the crude oil market.

- Refinitiv/Core Commodity CRB(R) Index (Commodity Index): This pricing index serves as a benchmark for investment in commodities.

- Natural Gas Futures (Natural Gas): This continuous contract includes front-month futures of Natural Gas futures listed on the New York Mercantile Exchange.

3.2. Methodology

4. Empirical Results

4.1. Descriptive Statistics

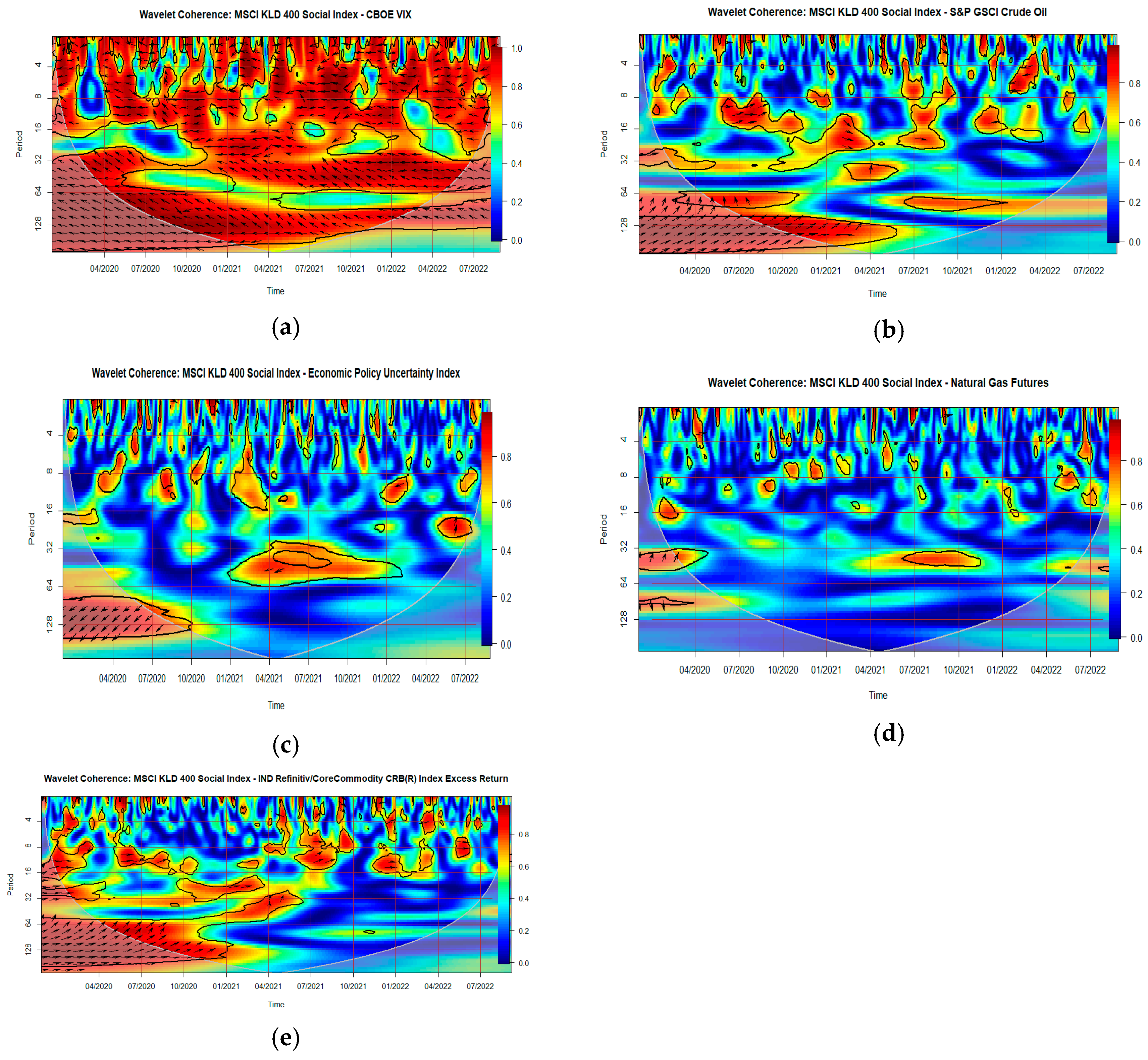

4.2. Empirical Results

5. Conclusions and Further Implications

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Aevoae, George Marian, Alin Marius Andrieș, Steven Ongena, and Nicu Sprincean. 2023. ESG and systemic risk. Applied Economics 55: 3085–109. [Google Scholar] [CrossRef]

- Albuquerque, Rui, Yrjo Koskinen, Shuai Yang, and Chendi Zhang. 2020. Resiliency of Environmental and Social Stocks: An Analysis of the Exogenous COVID-19 Market Crash. The Review of Corporate Finance Studies 9: 593–621. [Google Scholar] [CrossRef]

- Alessandrini, Fabio, and Eric Jondeau. 2020. ESG investing: From sin stocks to smart beta. The Journal of Portfolio Management 46: 75–94. [Google Scholar] [CrossRef]

- Alinaitwe, Grace, and Olvar Bergland. 2024. Assessing the Relationship between Fuel and Charcoal Prices in Uganda. Economies 12: 46. [Google Scholar] [CrossRef]

- Alshehhi, Ali, Haitham Nobanee, and Nilesh Khare. 2018. The Impact of Sustainability Practices on Corporate Financial Performance: Literature Trends and Future Research Potential. Sustainability 10: 494. [Google Scholar] [CrossRef]

- Ashraf, Dawood, Muhammad Suhail Rizwan, and Ghufran Ahmad. 2020. Islamic equity investments and the COVID-19 pandemic. Pacific-Basin Finance Journal 73: 101765. [Google Scholar] [CrossRef]

- Auer, Benjamin R. 2016. Do Socially Responsible Investment Policies Add or Destroy European Stock Portfolio Value? Journal of Business Ethics 135: 381–97. [Google Scholar] [CrossRef]

- Barth, Florian, Benjamin Hübel, and Hendrik Scholz. 2022. ESG and corporate credit spreads. The Journal of Risk Finance 23: 169–90. [Google Scholar] [CrossRef]

- Basdekis, Charalampos. 2023. The Impact of ESG Investments on Capital Markets, Economies and Firms’ Performance. New York: Crimson Publishers, vol. 14. [Google Scholar] [CrossRef]

- Basdekis, Charalampos, Apostolos Christopoulos, Ioannis Katsampoxakis, and Vasileios Nastas. 2022. The Impact of the Ukrainian War on Stock and Energy Markets: A Wavelet Coherence Analysis. Energies 15: 8174. [Google Scholar] [CrossRef]

- Basdekis, Charalampos, Ioannis Katsampoxakis, and Konstantinos Anathreptakis. 2023. Women’s Participation in Firms’ Management and Their Impact on Financial Performance: Pre-COVID-19 and COVID-19 Period Evidence. Sustainability 15: 8686. [Google Scholar] [CrossRef]

- Batista, Alamo Alexandre da Silva, and Antonio Carlos de Francisco. 2018. Organizational Sustainability Practices: A Study of the Firms Listed by the Corporate Sustainability Index. Sustainability 10: 226. [Google Scholar] [CrossRef]

- Bauer, Rob, and Paul Smeets. 2015. Social identification and investment decisions. Journal of Economic Behavior & Organization 117: 121–34. [Google Scholar] [CrossRef]

- Baur, Dirk G., and Lai T. Hoang. 2021. A crypto safe haven against Bitcoin. Finance Research Letters 38: 101431. [Google Scholar] [CrossRef]

- Bloomberg Intelligence: “ESG May Surpass $41 Trillion Assets in 2022, But Not Without Challenges, Finds Bloomberg Intelligence”. 2023. Available online: https://www.bloomberg.com/company/press/esg-may-surpass-41-trillion-assets-in-2022-but-not-without-challenges-finds-bloomberg-intelligence/ (accessed on 5 September 2023).

- Bouri, Elie, Syed Jawad Hussain Shahzad, David Roubaud, Ladislav Kristoufek, and Brian Lucey. 2020. Bitcoin, gold, and commodities as safe havens for stocks: New insight through wavelet analysis. The Quarterly Review of Economics and Finance 77: 156–64. [Google Scholar] [CrossRef]

- Broadstock, David C., Kalok Chan, Louis T. W. Cheng, and Xiaowei Wang. 2020. The role of ESG performance during times of financial crisis: Evidence from COVID-19 in China. Finance Research Letters 38: 101716. [Google Scholar] [CrossRef] [PubMed]

- Brzeszczyński, Janusz, and Graham McIntosh. 2014. Performance of Portfolios Composed of British SRI Stocks. Journal of Business Ethics 120: 335–62. [Google Scholar] [CrossRef]

- Cagli, Efe C. Caglar, Pinar Evrim Mandaci, and Dilvin Taşkın. 2023. Environmental, social, and governance (ESG) investing and commodities: Dynamic connectedness and risk management strategies. Sustainability Accounting, Management and Policy Journal 14: 1052–74. [Google Scholar] [CrossRef]

- Capelle-Blancard, Gunther, and Aurélien Petit. 2019. Every Little Helps? ESG News and Stock Market Reaction. Journal of Business Ethics 157: 543–65. [Google Scholar] [CrossRef]

- Charlo, Maria J., Ismael Moya, and Ana M. Muñoz. 2015. Sustainable Development and Corporate Financial Performance: A Study Based on the FTSE4Good IBEX Index. Business Strategy and the Environment 24: 277–88. [Google Scholar] [CrossRef]

- Chen, Hong-Yi, and Sharon S. Yang. 2020. Do Investors exaggerate corporate ESG information? Evidence of the ESG momentum effect in the Taiwanese market. Pacific-Basin Finance Journal 63: 101407. [Google Scholar] [CrossRef]

- Christopoulos, Apostolos G., Petros Kalantonis, Ioannis Katsampoxakis, and Konstantinos Vergos. 2021. COVID-19 and the Energy Price Volatility. Energies 14: 6496. [Google Scholar] [CrossRef]

- Cunha, Felipe Arias Fogliano de Souza, Erick Meira de Oliveira, Renato J. Orsato, Marcelo Cabus Klotzle, Fernando Luiz Cyrino Oliveira, and Rodrigo Goyannes Gusmão Caiado. 2020. Can sustainable investments outperform traditional benchmarks? Evidence from global stock markets. Business Strategy and the Environment 29: 682–97. [Google Scholar] [CrossRef]

- De la Torre, Oscar, Evaristo Galeana, and Dora Aguilasocho. 2016. The use of the sustainable investment against the broad market one. A first test in the Mexican stock market. European Research on Management and Business Economics 22: 117–23. [Google Scholar] [CrossRef]

- Dhaliwal, Dan S., Oliver Zhen Li, Albert Tsang, and Yong George Yang. 2011. Voluntary Nonfinancial Disclosure and the Cost of Equity Capital: The Initiation of Corporate Social Responsibility Reporting. The Accounting Review 86: 59–100. [Google Scholar] [CrossRef]

- Díaz, Violeta, Denada Ibrushi, and Jialin Zhao. 2021. Reconsidering systematic factors during the COVID-19 pandemic—The rising importance of ESG. Finance Research Letters 38: 101870. [Google Scholar] [CrossRef]

- Engelhardt, Nils, Jens Ekkenga, and Peter Posch. 2021. ESG Ratings and Stock Performance during the COVID-19 Crisis. Sustainability 13: 7133. [Google Scholar] [CrossRef]

- Fassas, Athanasios P. 2020. Risk aversion connectedness in developed and emerging equity markets before and after the COVID-19 pandemic. Heliyon 6: e05715. [Google Scholar] [CrossRef]

- Fatemi, Ali, Martin Glaum, and Stefanie Kaiser. 2018. ESG performance and firm value: The moderating role of disclosure. Global Finance Journal 38: 45–64. [Google Scholar] [CrossRef]

- Ferriani, Fabrizio, and Filippo Natoli. 2020. ESG risks in times of COVID-19. Applied Economics Letters 28: 1537–41. [Google Scholar] [CrossRef]

- Filbeck, Greg, Eric Robbins, and Xin Zhao. 2022. Social capital during the coronavirus pandemic: The value of corporate benevolence. Applied Economics 54: 1460–72. [Google Scholar] [CrossRef]

- Gao, Yang, Yangyang Li, and Yaojun Wang. 2021. Risk spillover and network connectedness analysis of China’s green bond and financial markets: Evidence from financial events of 2015–20. The North American Journal of Economics and Finance 57: 101386. [Google Scholar] [CrossRef]

- Gao, Yang, Yangyang Li, Chengjie Zhao, and Yaojun Wang. 2022. Risk spillover analysis across worldwide ESG stock markets: New evidence from the frequency-domain. The North American Journal of Economics and Finance 59: 101619. [Google Scholar] [CrossRef]

- Gehricke, Sebastian A., Xinfeng Ruan, and Jin E. Zhang. 2023. Doing well while doing good: ESG ratings and corporate bond returns. Applied Economics 56: 1916–34. [Google Scholar] [CrossRef]

- Giglio, Stefano, Matteo Maggiori, Johannes Stroebel, and Stephen Utkus. 2021. Five Facts about Beliefs and Portfolios. American Economic Review 111: 1481–522. [Google Scholar] [CrossRef]

- Global Sustainability Investment Alliance. 2018. Available online: https://www.gsi-alliance.org/wp-content/uploads/2019/03/GSIR_Review2018.3.28.pdf (accessed on 24 July 2023).

- Gong, Xiao-Li, Xi-Hua Liu, Xiong Xiong, and Wei Zhang. 2019. Financial systemic risk measurement based on causal network connectedness analysis. International Review of Economics & Finance 64: 290–307. [Google Scholar] [CrossRef]

- Goodell, John W., and Stephane Goutte. 2020. Co-movement of COVID-19 and Bitcoin: Evidence from wavelet coherence analysis. Finance Research Letters 38: 101625. [Google Scholar] [CrossRef] [PubMed]

- Grinsted, Aslak, John C. Moore, and Svetlana Jevrejeva. 2004. Application of the cross wavelet transform and wavelet coherence to geophysical time series. Nonlinear Processes in Geophysics 11: 561–66. [Google Scholar] [CrossRef]

- Gubareva, Mariya, and Maria Rosa Borges. 2016. Typology for Flight-toquality Episodes and Downside Risk Measurement. Applied Economics 48: 835–53. [Google Scholar] [CrossRef]

- Hassan, M. Kabir, Hadrian Geri Djajadikerta, Tonmoy Choudhury, and Muhammad Kamran. 2021. Safe havens in Islamic financial markets: COVID-19 versus GFC. Global Finance Journal 54: 100643. [Google Scholar] [CrossRef]

- Ioannou, Ioannis, and George Serafeim. 2015. The impact of corporate social responsibility on investment recommendations: Analysts’ perceptions and shifting institutional logics. Strategic Management Journal 36: 1053–81. [Google Scholar] [CrossRef]

- Jain, Mansi, Gagan Deep Sharma, and Mrinalini Srivastava. 2019. Can Sustainable Investment Yield Better Financial Returns: A Comparative Study of ESG Indices and MSCI Indices. Risks 7: 15. [Google Scholar] [CrossRef]

- Ji, Qiang, Dayong Zhang, and Yuqian Zhao. 2020. Searching for safe-haven assets during the COVID-19 pandemic. International Review of Financial Analysis 71: 101526. [Google Scholar] [CrossRef]

- Karamti, Chiraz, and Olfa Belhassine. 2022. COVID-19 pandemic waves and global financial markets: Evidence from wavelet coherence analysis. Finance Research Letters 45: 102136. [Google Scholar] [CrossRef] [PubMed]

- Katsampoxakis, Ioannis. 2021. ECB’s unconventional monetary policy and spillover effects between sovereign and bank credit risk. EuroMed Journal of Business 17: 218–45. [Google Scholar] [CrossRef]

- Katsampoxakis, Ioannis, Apostolos Christopoulos, Petros Kalantonis, and Vasileios Nastas. 2022. Crude Oil Price Shocks and European Stock Markets during the COVID-19 Period. Energies 15: 4090. [Google Scholar] [CrossRef]

- Kenourgios, Dimitris, and Dimitrios Dimitriou. 2015. Contagion of the Global Financial Crisis and the real economy: A regional analysis. Economic Modelling 44: 283–93. [Google Scholar] [CrossRef]

- Kenourgios, Dimitrios, Zaghum Umar, and Paraskevi Lemonidi. 2020. On the effect of credit rating announcements on sovereign bonds: International evidence. International Economics 163: 58–71. [Google Scholar] [CrossRef]

- Krüger, Philipp. 2015. Corporate goodness and shareholder wealth. Journal of Financial Economics 115: 304–29. [Google Scholar] [CrossRef]

- La Torre, Mario, Annarita Trotta, Helen Chiappini, and Alessandro Rizzello. 2019. Business Models for Sustainable Finance: The Case Study of Social Impact Bonds. Sustainability 11: 1887. [Google Scholar] [CrossRef]

- Lassala, Carlos, Andreea Apetrei, and Juan Sapena. 2017. Sustainability Matter and Financial Performance of Companies. Sustainability 9: 1498. [Google Scholar] [CrossRef]

- Leite, Paulo, and Maria Céu Cortez. 2015. Performance of European socially responsible funds during market crises: Evidence from France. International Review of Financial Analysis 40: 132–41. [Google Scholar] [CrossRef]

- Li, Yiwei, Mengfeng Gong, Xiu-Ye Zhang, and Lenny Koh. 2018. The impact of environmental, social, and governance disclosure on firm value: The role of CEO power. The British Accounting Review 50: 60–75. [Google Scholar] [CrossRef]

- Liket, Kellie, and Karen Maas. 2016. Strategic Philanthropy: Corporate Measurement of Philanthropic Impacts as a Requirement for a “Happy Marriage” of Business and Society. Business & Society 55: 889–921. [Google Scholar] [CrossRef]

- Lööf, Hans, Maziar Sahamkhadam, and Andreas Stephan. 2022. Is Corporate Social Responsibility investing a free lunch? The relationship between ESG, tail risk, and upside potential of stocks before and during the COVID-19 crisis. Finance Research Letters 46: 102499. [Google Scholar] [CrossRef] [PubMed]

- Mariana, Christy Dwita, Irwan Adi Ekaputra, and Zaäfri Ananto Husodo. 2021. Are Bitcoin and Ethereum safe-havens for stocks during the COVID-19 pandemic? Finance Research Letters 38: 101798. [Google Scholar] [CrossRef]

- Marti, Carmen Pilar, M. Rosa Rovira-Val, and Lisa G. J. Drescher. 2015. Are Firms that Contribute to Sustainable Development Better Financially? Corporate Social Responsibility and Environmental Management 22: 305–19. [Google Scholar] [CrossRef]

- Miralles-Quiros, Maria del Mar, Jose Luis Miralles-Quiros, and Irene Guia Arraiano. 2017. Sustainable Development, Sustainability Leadership and Firm Valuation: Differences across Europe. Business Strategy and the Environment 26: 1014–28. [Google Scholar] [CrossRef]

- Morea, Donato, Fabiomassimo Mango, Mavie Cardi, Cosimo Paccione, and Lucilla Bittucci. 2022. Circular Economy Impact Analysis on Stock Performances: An Empirical Comparison with the Euro Stoxx 50® ESG Index. Sustainability 14: 843. [Google Scholar] [CrossRef]

- Morning Star: “Can ESG Investments Outperform the Market?”. 2023. Available online: https://www.morningstar.com/views/blog/esg/esg-performance-morningstar-indexes (accessed on 10 August 2023).

- Naughton, James P., Clare Wang, and Ira Yeung. 2019. Investor Sentiment for Corporate Social Performance. The Accounting Review 94: 401–20. [Google Scholar] [CrossRef]

- Ortas, Eduardo, Isabel Gallego-Alvarez, and Igor Álvarez Etxeberria. 2015. Financial Factors Influencing the Quality of Corporate Social Responsibility and Environmental Management Disclosure: A Quantile Regression Approach. Corporate Social Responsibility and Environmental Management 22: 362–80. [Google Scholar] [CrossRef]

- Papathanasiou, Spyros, Dimitrios Vasiliou, Anastasios Magoutas, and Drosos Koutsokostas. 2021. Do hedge and merger arbitrage funds actually hedge? A time-varying volatility spillover approach. Finance Research Letters 44: 102088. [Google Scholar] [CrossRef]

- Rajnoha, Rastislav, Petra Lesníková, and Antonín Korauš. 2016. From Financial Measures to Strategic Performance Measurement System and Corporate Sustainability: Empirical Evidence from Slovakia. Economics & Sociology 9: 134–52. [Google Scholar] [CrossRef]

- Rajnoha, Rastislav, Petra Lesníková, and Vladimír Krajčík. 2017. Influence of business performance measurement systems and corporate sustainability concept to overal business performance: “save the planet and keep your performance”. E+M Ekonomie a Management 20: 111–28. [Google Scholar] [CrossRef]

- Rehman, Mobeen Ur, and Xuan Vinh Vo. 2020. Cryptocurrencies and precious metals: A closer look from diversification perspective. Resources Policy 66: 101652. [Google Scholar] [CrossRef]

- Riaz, Yasir, Choudhry Tanveer Shehzad, and Zaghum Umar. 2019. Pro-cyclical effect of sovereign rating changes on stock returns: A fact or factoid? Applied Economics 51: 1588–601. [Google Scholar] [CrossRef]

- Riedl, Arno, and Paul Smeets. 2017. Why Do Investors Hold Socially Responsible Mutual Funds? The Journal of Finance 72: 2505–50. [Google Scholar] [CrossRef]

- Rubbaniy, Ghulame, Ali Awais Khalid, and Aristeidis Samitas. 2021. Are Cryptos Safe-Haven Assets during COVID-19? Evidence from Wavelet Coherence Analysis. Emerging Markets Finance and Trade 57: 1741–56. [Google Scholar] [CrossRef]

- Rubbaniy, Ghulame, Ali Awais Khalid, Muhammad Faisal Rizwan, and Shoaib Ali. 2022. Are ESG stocks safe-haven during COVID-19? Studies in Economics and Finance 39: 239–55. [Google Scholar] [CrossRef]

- Samitas, Aristeidis, Spyros Papathanasiou, and Drosos Koutsokostas. 2021. The connectedness between Sukuk and conventional bond markets and the implications for investors. International Journal of Islamic and Middle Eastern Finance and Management 14: 928–49. [Google Scholar] [CrossRef]

- Shaik, Muneer, and Mohd Ziaur Rehman. 2023. The Dynamic Volatility Connectedness of Major Environmental, Social, and Governance (ESG) Stock Indices: Evidence Based on DCC-GARCH Model. Asia-Pacific Financial Markets 30: 231–46. [Google Scholar] [CrossRef]

- Singh, Amanjot. 2020. COVID-19 and safer investment bets. Finance Research Letters 36: 101729. [Google Scholar] [CrossRef] [PubMed]

- Thanh, Quang Phung. 2022. Economic effects of green bond market development in Asian economies. The Journal of Risk Finance 23: 480–97. [Google Scholar] [CrossRef]

- Torrence, Christopher, and Gilbert P. Compo. 1998. A practical guide to wavelet analysis. Bulletin of the American Meteorological Society 79: 61–78. [Google Scholar] [CrossRef]

- Torrence, Christopher, and Peter J. Webster. 1999. Interdecadal changes in the ENSO–monsoon system. Journal of Climate 12: 2679–90. [Google Scholar] [CrossRef]

- Umar, Zaghum, and Mariya Gubareva. 2021. The relationship between the COVID-19 media coverage and the Environmental, Social and Governance leaders equity volatility: A time-frequency wavelet analysis. Applied Economics 53: 3193–206. [Google Scholar] [CrossRef]

- Umar, Zaghum, and Tahir Suleman. 2017. Asymmetric Return and Volatility Transmission in Conventional and Islamic Equities. Risks 5: 22. [Google Scholar] [CrossRef]

- Umar, Zaghum, Dimitris Kenourgios, and Sypros Papathanasiou. 2020. The static and dynamic connectedness of environmental, social, and governance investments: International evidence. Economic Modelling 93: 112–24. [Google Scholar] [CrossRef] [PubMed]

- Umar, Zaghum, Mariya Gubareva, Dang Khoa Tran, and Tamara Teplova. 2021. Impact of the COVID-19 induced panic on the Environmental, Social and Governance leaders equity volatility: A time-frequency analysis. Research in International Business and Finance 58: 101493. [Google Scholar] [CrossRef] [PubMed]

- Urquhart, Andrew, and Hanxiong Zhang. 2019. Is Bitcoin a hedge or safe haven for currencies? An intraday analysis. International Review of Financial Analysis 63: 49–57. [Google Scholar] [CrossRef]

- Vives, Antonio, and Baljit Wadhwa. 2012. Sustainability indices in emerging markets: Impact on responsible practices and financial market de-velopment. Journal of Sustainable Finance and Investment 2: 318–37. [Google Scholar] [CrossRef]

- Wang, Ze, Xiangyun Gao, Haizhong An, Renwu Tang, and Qingru Sun. 2020. Identifying influential energy stocks based on spillover network. International Review of Financial Analysis 68: 101277. [Google Scholar] [CrossRef]

- Yarovaya, Larisa, Ahmed H. Elsayed, and Shawkat Hammoudeh. 2021. Determinants of Spillovers between Islamic and Conventional Financial Markets: Exploring the Safe Haven Assets during the COVID-19 Pandemic. Finance Research Letters 43: 101979. [Google Scholar] [CrossRef]

- Yousaf, Imran, Elie Bouri, Shoaib Ali, and Nehme Azoury. 2021. Gold against Asian Stock Markets during the COVID-19 Outbreak. Journal of Risk and Financial Management 14: 186. [Google Scholar] [CrossRef]

- Zhang, Weiping, Xintian Zhuang, Jian Wang, and Yang Lu. 2020. Connectedness and systemic risk spillovers analysis of Chinese sectors based on tail risk network. The North American Journal of Economics and Finance 54: 101248. [Google Scholar] [CrossRef]

- Zheng, Guang-Wen, Abu Bakkar Siddik, Mohammad Masukujjaman, and Nazneen Fatema. 2021. Factors Affecting the Sustainability Performance of Financial Institutions in Bangladesh: The Role of Green Finance. Sustainability 13: 10165. [Google Scholar] [CrossRef]

- Zhu, Wenzhong, Jiajia Yang, Han Lv, and Meier Zhuang. 2021. Pandemic Uncertainty and Socially Responsible Investments. Frontiers in Public Health 9: 661482. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| MSCI ESG ACWI | MSCI ESG EM | MSCI ESG Europe | MSCI KLD | MSCI ESG NA | VIX | Natural Gas | Commodity Index | S&P Crude Oil | EPU | |

|---|---|---|---|---|---|---|---|---|---|---|

| Mean | 2231.02 | 2064.77 | 91.54 | 1476.00 | 383.86 | 24.74 | 3.78 | 205.09 | 309.38 | 192.42 |

| Median | 2290.43 | 2078.80 | 91.84 | 1498.35 | 392.61 | 22.92 | 2.97 | 200.04 | 292.98 | 147.99 |

| Maximum | 2709.68 | 2600.34 | 108.18 | 1868.09 | 485.04 | 82.69 | 9.68 | 329.59 | 581.80 | 807.66 |

| Minimum | 1323.34 | 1302.83 | 58.58 | 841.54 | 217.00 | 12.10 | 1.48 | 106.29 | 76.70 | 22.25 |

| Std. Dev. | 315.88 | 287.43 | 11.15 | 236.11 | 62.30 | 9.22 | 1.99 | 57.62 | 123.59 | 124.52 |

| Skewness | −0.51 | −0.34 | −0.47 | −0.35 | −0.35 | 2.49 | 1.09 | 0.48 | 0.39 | 1.66 |

| Kurtosis | 2.38 | 2.18 | 2.55 | 2.19 | 2.11 | 12.49 | 3.34 | 2.11 | 2.02 | 5.89 |

| Jarque-Bera | 40.25 | 31.70 | 30.18 | 32.18 | 36.14 | 3195.50 | 136.76 | 41.86 | 43.39 | 539.39 |

| p-value | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Katsampoxakis, I.; Xanthopoulos, S.; Basdekis, C.; Christopoulos, A.G. Can ESG Stocks Be a Safe Haven during Global Crises? Evidence from the COVID-19 Pandemic and the Russia-Ukraine War with Time-Frequency Wavelet Analysis. Economies 2024, 12, 89. https://doi.org/10.3390/economies12040089

Katsampoxakis I, Xanthopoulos S, Basdekis C, Christopoulos AG. Can ESG Stocks Be a Safe Haven during Global Crises? Evidence from the COVID-19 Pandemic and the Russia-Ukraine War with Time-Frequency Wavelet Analysis. Economies. 2024; 12(4):89. https://doi.org/10.3390/economies12040089

Chicago/Turabian StyleKatsampoxakis, Ioannis, Stylianos Xanthopoulos, Charalampos Basdekis, and Apostolos G. Christopoulos. 2024. "Can ESG Stocks Be a Safe Haven during Global Crises? Evidence from the COVID-19 Pandemic and the Russia-Ukraine War with Time-Frequency Wavelet Analysis" Economies 12, no. 4: 89. https://doi.org/10.3390/economies12040089

APA StyleKatsampoxakis, I., Xanthopoulos, S., Basdekis, C., & Christopoulos, A. G. (2024). Can ESG Stocks Be a Safe Haven during Global Crises? Evidence from the COVID-19 Pandemic and the Russia-Ukraine War with Time-Frequency Wavelet Analysis. Economies, 12(4), 89. https://doi.org/10.3390/economies12040089