Abstract

Space-time panel data widely exist in many research fields such as economics, management, geography and environmental science. It is of interest to study the relationship between response variable and regressors which come from above fields by establishing regression models. This paper introduces a new fixed effects partially linear varying coefficient panel data regression model with nonseparable space-time filters. On the basis of approximating the varying coefficient functions with a powerful B-spline method, the profile quasi-maximum likelihood estimators of parameters and varying coefficient functions are constructed. Under some regular conditions, we derive their consistency and asymptotic normality. Monte Carlo simulation shows that our estimates have good finite performance and ignoring spatial and serial correlations may lead to inefficiency of estimates. Finally, the driving forces of Chinese resident consumption rate are studied using our estimation method.

Keywords:

partially linear varying coefficient panel data regression model; profile quasi-maximum likelihood estimation; nonseparable space-time filters; asymptotic property; Monte Carlo simulation MSC:

62F10; 62F12; 62G05; 62G20; 62P20

1. Introduction

A space-time panel dataset is one sample collected from a number of spatial units over time periods (Li et al. [1]). Such datasets widely exist in economics, management, geography, environmental science and other research fields. How to effectively analyze space-time panel datasets and construct space-time panel data regression models has great theoretical and empirical significance. The space-time panel data regression models are a natural extension of panel data regression models. In the early 19th century, “regression” was first mentioned in the works of Legendre and Gauss. Later, at the turn of the 19th and 20th centuries, Galton and Pearson conceptualized regression, there were a number of regression models for analyzing panel data and exploring the association between dependent variable and regressors (Hsiao [2]; Baltagi [3]; Porter et al. [4]; Zamanzade [5]; Imai and Kim [6]). Among them, parametric panel data regression models have been widely used to study linear influence of regressors. Since the 1990s, nonparametric methods have been gradually applied into regression analysis (Fan and Gijbels [7]; Luo et al. [8]; Ullah et al. [9]; Dai et al. [10]), Li and Stengos [11] first proposed nonparametric panel data regression models to explore nonlinear influence of regressors. However, such models have their drawbacks. Parametric panel data regression models need to be precisely pre-specified, misspecified model forms can lead to inconsistent estimates as well as incorrect policy prescriptions. Although nonparametric panel data regression models are useful whenever we are not certain what the correct functional forms are, they may face the “curse of dimensionality” when the dimension of regressors is higher (Fan and Gijbels [7]), namely, the estimation accuracy decreases rapidly with the number of regressors increasing. Therefore, scholars proposed a number of non/semiparametric panel data regression models with a dimension reduction function to more flexibly overcome the “curse of dimensionality” encountered in practice, for example, partially linear additive panel data regression model, partially linear single-index panel data regression model and partially linear varying coefficient panel data regression model. In recent years, a series of their estimation methods have been also developed, including profile least squares estimation (Baltagi et al. [12]; Chen et al. [13]; Huang et al. [14]; Yong et al. [15]; Zhou et al. [16]; Zhang and Shen [17]), profile quasi-maximum likelihood estimation (Li et al. [18]; Su and Ullah [19]; Wu et al. [20]; Hu [21]), generalized method of moment estimation (GMM) (Tran and Tsionas [22]; Su and Ullah [23]), and others (Liu and Zhuang [24]).

All those modeling techniques and corresponding statistical inference methods for the above-mentioned semiparametric panel data regression models need the assumption that there is no correlation among the individuals or time periods. Elhorst [25] pointed out that two problems hampering the modeling of space-time panel data are serial correlation between the observations on each spatial unit over time and spatial correlation between the observations on the spatial units at each point in time. Furthermore, Baltagi et al. [12] mentioned that ignoring the serial correlation in the errors will result in consistent, but inefficient estimates of the regression coefficients and biased standard errors. Therefore, some scholars added nonseparable space-time filters, that is, space-time error correlation are modeled jointly, or separable space-time filters, that is, space-time error correlation are modeled independently from one another, under the framework of semi/parametric panel data regression models. The estimation, testing and empirical analysis of these models have been studied in recent years. Baltagi et al. [26] derived joint and conditional Lagrange Multiplier (LM) and Likelihood Ratio (LR) test statistics of random effects parametric panel regression model with separable space-time correlations and presented their small sample performance using Monte Carlo experiments. Elhorst [25] constructed a random effects parametric panel regression model with nonseparable space-time filters and presented its maximum likelihood estimation. Parent and LeSage [27] explored the Markov Chain Monte Carlo method of random effects parametric panel regression model with separable space-time filters—both Monte Carlo simulation and an application were used to illustrate the method. Lee and Yu [28] investigated quasi-maximum likelihood estimation for fixed effects parametric panel regression model with separable or nonseparable space-time filters, which might be spatially stable or unstable. They also derived consistency and asymptotic normality of the estimators under some regular conditions. Bai et al. [29] proposed a random effects partially linear varying coefficient panel model with separable space-time filters and derived consistency and asymptotic normality of weighted semiparametric least squares estimators. Zhao et al. [30] constructed weighted semiparametric least squares estimators and generalized F-type test statistic for random effects partially linear single-index panel model with separable space-time filters. They also derived the asymptotic properties of estimators and the asymptotic distribution of F-type test statistic. Li et al. [1] studied profile quasi-maximum likelihood estimation and generalized F-type test of random effects partially linear nonparametric panel model with separable space-time filters and obtained the consistency and asymptotic normality of parametric and nonparametric estimators as well as asymptotic distribution of generalized F-type test statistic. Monte Carlo simulation and Indonesian rice farming data were used to illustrate their methods.

To the best of our knowledge, there are no non/semiparametric spatiotemporal econometric models that study both fixed effects and nonseparable space-time filters in the existing literature. In this paper, we attempt to propose a fixed effects partially linear varying coefficient panel data regression model (PLVCPDRM) with nonseparable spacetime filters. It can simultaneously capture the linear and nonlinear effects of regressors, spatial and serial correlations of error structure, and individual fixed effects. Our aim is to construct profile quasi-maximum likelihood estimators (PQMLE) of this model and systematically study their asymptotic properties and finite sample performance. Furthermore, the proposed estimation method is illustrated by using a real dataset.

The rest of this paper is organized as follows: Section 2 presents a fixed effects PLVCPDRM with nonseparable space-time filters and its PQMLEs. Section 3 lays out some regular assumptions and asymptotic properties. Section 4 reports simulation results for examining the finite sample performance of the proposed estimators. Section 5 shows the empirical study for illustrating the proposed methodology. Conclusions are summarized in Section 6. Appendix A presents a lemma and proofs of the main theorems.

2. Model and Estimation

Consider a fixed effects PLVCPDRM with nonseparable space-time filters:

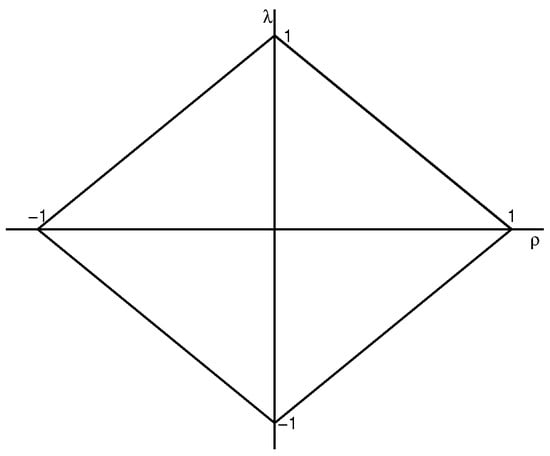

where , are observations of a response variable, ; , , and are observations of p-dimensional and q-dimensional exogenous regressors, respectively; is a regression coefficient vector of , is an unknown univariate varying coefficient function vector, are smoothing functions of u, u is an intermediate univariate variable; are fixed effects satisfying for identification purpose; W is an row-normalized non-negative spatial weights matrix with zero diagonals; is an vector of disturbance term, is an vector of random error term which is assumed to be . In order to keep the stationarity of the model (1)–(2), serial correlation coefficient and spatial correlation coefficient should belong to parameter space (Elhorst [25]; Lee and Yu [28]), see Figure 1.

Figure 1.

The parameter space of and .

For the model (1)–(2), it is necessary to identify an appropriate estimation method to obtain estimators of the unknown parameter vector and varying coefficient functions .

Before proceeding to the estimation procedure, the fitting problem of the varying coefficient functions needs to be solved priority. Polynomial spline method is efficient in function approximation and numerical computation. Polynomial splines are piecewise polynomials with the polynomial pieces joining together smoothly at a set of interior knot points (see De Boor [31]; Huang and Shen [32]; Zou and Zhu [33]). B-spline is a special form of polynomial spline. Considering that the B-spline basis has better numerical properties than other basis functions, we use the B-spline method to approximate the varying coefficient functions in the model (1). To be precise, let , and be a partition of interval . Using the as knots, we have normalized B-spline basis function of order that forms a basis function for the linear spline space on . Denote B-spline basis function , we can approximate by some spline function in : , where is an unknown spline coefficient vector. Thus, the model (1) can be written as

where , , and

is a matrix, .

For any vector , denote as the first order difference. By first difference of the model (2)–(3) to eliminate the fixed effects, we have

Note that is observable for , can’t be observed. Let , , , , and is an identity matrix. The Equation (5) can be rewritten as for all t. With backward substitution, we have , where . By denoting and

the matrix form of the Equation (5) can be simply expressed as , . As , where

and , we can obtain with

Note that the only unknown element of is . In order to obtain determinant and inverse of , we define a confirmable block matrix (Hsiao et al [34]; Lee and Yu [28]) as

From straight calculation, we know that

Thus, the determinant and the inverse . Therefore, the quasi-log-likelihood function can be written as

where , , , , with

as the first order difference transformation matrix of dimension .

Motivated by Su and Jin [35], we obtain PQMLEs of parameter vector and varying coefficient functions by the following the two-step estimation procedure:

Step 1: Assuming the parameter is known, the initial estimators of can be obtained by maximizing quasi-log-likelihood function (6):

Step 2: With the estimated , and , PQMLE of can be obtained by maximizing the concentrated quasi-log-likelihood function of :

The final estimator of is given by . With the estimated , update

and , we can obtain the final PQMLEs as

where I is an identity matrix of dimension , . Then, the estimator of the nonparametric function can be written as

3. Asymptotic Properties

To derive the asymptotic properties of the estimators, we first introduce some regular assumptions. For clear exposition, denote , and as the true parameter vector of , and , respectively, and as the true varying coefficient function vector of .

Assumption 1.

(i) The sequences , and are nonstochastic, and they have bounded support set on , and respectively. In addition, forms a sequence of designs such that they are analogous to a positive and bounded “design density“ (Su and Jin [35]).

(ii) For any bounded continuous function , it holds that

(iii) The parameter in a neighborhood of satisfies , where is a positive constant.

Assumption 2.

The disturbances are with zero mean, variance and for some .

Assumption 3.

(i) For every K, the smallest eigenvalue of and are bounded away from zero uniformly in K.

(ii) There is a sequence of constants satisfying such that as .

(iii) For any -th continuously differentiable bounded function satisfying the normalization of , there exist some such that as and as .

Assumption 4.

(i) W is a row-normalized and prespecified spatial weights matrix.

(ii) Row and column sums of W in absolute value are uniformly bounded (i.e., UB).

(iii) is invertible for all , where is compact and the true parameter is in the interior of . Additionally, is UB for .

Assumption 5.

(i) is UB, where and .

(ii) is UB.

(iii) The limit of the information matrix (A4) in Appendix A is nonsingular.

(iv) is nonsingular.

Assumption 6.

for , where is defined in (A1).

Remark 1.

The fixed bounded design in Assumption 1 is typically assumed in spatial econometric literature, see Kelejian and Prucha [36], Kelejian and Prucha [37], Su and Jin [35] and Cheng and Chen [38]. Assumption 1 (ii) parallels Assumption 1 of Su and Jin [35] and Assumption 2.1 (iv) of Hu et al. [39]. It means that if are with the density , the Equation (9) holds with probability 1. Assumption 2 presents regularity assumptions for error terms . Assumption 3 is a set of mild conditions on the B-spline method (see Newey [40]; Hu et al. [39]; Yong et al. [15]; Zhang [41]). Assumption 3(i) ensures that and are asymptotically nonsingular, which parallels Assumption 3 of Zhang [41] and Assumption 2(i) of Newey [40]. Newey [40] gave some primitive conditions for power series and splines such that Assumption 3(ii)–(iii) hold. In addition, Assumption 3(iii) is the counterpart assumption in the kernel method. Assumption 4 provides the basic features of the spatial weight matrix. The uniform boundedness of W and limits the spatial correlation to a manageable degree in Assumptions 4(ii)–(iii). Assumption 5(i) is the absolute summability condition and row/column sum boundedness condition for disturbances, which will play an important role for the proofs of asymptotic properties. To prove the absolute summability of , a sufficient condition is for any matrix norm (see Corollary 5.6.16 in Horn and Johnson [42]) that satisfies . When , exists and can be defined as . Under the condition that the inverse of the variance matrix of is UB for and , Assumption 5(ii) can be certified. Assumption 5(iii)–(iv) is used for establishing the uniqueness identification and asymptotic normality of the proposed estimators. Assumption 6 specifies an identification condition for the estimators of parameters when Assumption 5(iv) is not satisfied.

In order to prove consistency of the parametric estimators, we need to obtain the expected value function for the quasi-log-likelihood function (6) divided by the effective sample size . The relationship between and (the first block of N in e are not exactly the original and all the entries are i.i.d. under normality) would be used frequently, where

and . Thus, and under the normality of disturbances. Split into four block matrices, one of which is . Utilizing the formula for inversion of a block matrix, we have that

Define , then

However, when are not normally distributed, elements in are uncorrelated but not necessarily independent of each other even though they are independent with (). Consider the case that the process starts at a finite past period, such as . Denote , which includes the original disturbances vectors, we have , where

is UB. Under non-normality, we can obtain

To show the consistency of , we follow Lee [43] by identifying based upon the maximum value of and showing the uniform convergence of to zero, consistency of follows.

Theorem 1.

Suppose Assumptions 1–6 hold, is globally identifiable and is consistent with .

Theorem 2.

Theorem 3.

Suppose Assumptions 1–5 hold, we have

Remark 2.

The term essentially corresponds to a variance term and to a bias term. When K is chosen as so that these two terms go to zero at the same rate, which occurs when K goes to infinity at the same rate as (and the side condition is satisfied), the convergence rate will be .

Theorem 4.

Suppose Assumptions 1–5 hold, as simultaneously, we have

where , , is an identity matrix of dimension K.

4. Simulation Studies

In this section, we report the results of Monte Carlo simulation experiments to examine the finite sample performance of the proposed estimation method. In order to illustrate the estimation accuracy of parameters, we use the sample mean (Mean), the sample standard deviation (SD) and the root mean square error (RMSE) as the evaluation criteria. Here,

where is the simulation times, are the parametric estimates of each simulation and is the true value. For the nonparametric estimates, we consider the mean absolute deviation error (MADE) as the evaluation criterion which is defined as

where are Q fixed grid points at support set of u.

Example 1.

The first example is to evaluate the performance of the estimation procedure. Consider the following data-generated processes:

where , , , , , the link functions and , . As in Su [44], the spatial weighting matrix is set to the Rook weight matrix. Sample size is and . For each case, we ran 500 simulations. The R software was used.

Table 1 summarizes Means, Medians, SDs and RMSEs for parametric estimates of and when the true values of spatial correlation coefficient and serial correlation coefficient are set as and , respectively. Table 2 and Table 3 give the median and SD of MADE values of and at 20 fixed grid points in all cases, respectively. We have the following finds: (1) The estimates of are close to true values for all cases; (2) SDs and RMSEs for are fairly small for all cases; (3) For fixed T(or N), as N(or T) increased, the SDs and RMSEs for estimates of all parameters decrease; (4) The SDs and Medians for 500 MADEs of and at 20 fixed grid points decrease as T or N is increased. Based on these findings, we conclude that the estimates of all parameters and varying coefficient functions are fairly close to their true values, and the deviations decrease with increasing of sample size. Overall, our proposed estimators for the model (12) perform well in finite sample cases.

Table 1.

Simulation results of parametric estimates and .

Table 2.

The Medians and SDs of MADE values for .

Table 3.

The Medians and SDs of MADE values for .

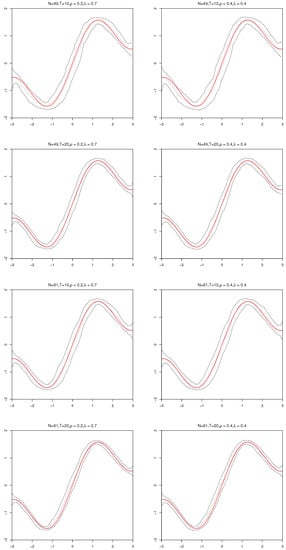

Figure 2 and Figure 3 present the fitting results and 95% confidence intervals of and under (or 81) and (or 20), where the short dashed curves in black are the average fits over 500 simulations by PQMLE, the solid curves in red are the true values of nonparametric functions and the two long dashed curves in black are the corresponding 95% confidence bands. We can see that the short dashed curve is close to the solid curve, and the confidence bandwidth gradually becomes narrow with the increase of the sample size. They indicate that the nonparametric estimation procedure is feasible in the case of small samples.

Figure 2.

The fitting results and 95% confidence intervals of in the model (12).

Figure 3.

The fitting results and 95% confidence intervals of in the model (12).

Example 2.

The second example is used to show that misspecification for the model (12) will lead to inconsistent parameter estimates. Here are the three most likely misspecified models, which ignore the spatial correlation, serial correlation and spatio-temporal correlations in the model (12), respectively:

where all variables in the above models are the same as the model (12). No loss of generality, we only study the case that and . Additionally, we set , and . The experimental results are presented in Table 4.

Table 4 lists the Means, Medians, SDs, RMSEs and MRs of parameter estimates in the models (12)–(15), where MR is the growth rate of RMSE on the basis of that in the model (12). From Table 4, we can see that: (1) The Means and Medians for the estimates of all parameters in the model (12) are closer to true values as sample size increases. However, it is easy to see that the Means and Medians of , , , and in the models (13)–(15) do not converge with the increasing of N, indicating that they are not stable. (2) The SDs and RMSEs of almost all parameter estimators in the models (13)–(15) are larger than that in the model (12). In particular, the SDs and RMSEs of do not decrease with the increasing of sample size. (3) MRs of most parameter estimators are greater than 0% and increase with the increasing of sample size, especially for , and . In addition, MRs of in the models (13) and (14) are less than 0%, which again indicates that the estimator of is unstable. It can be concluded that model misspecification would result in inconsistent parameter estimators. It further indicates that our proposed model is more effective and reliable.

5. Real Data Analysis

In this section, we employ the proposed model and its estimation method to study the driving forces of Chinese resident consumption rate. This dataset was collected on 1 August 2022) from the China Statistical Yearbook (http://www.stats.gov.cn/sj/ndsj/) for 2008 to 2020 and covers 30 provincial administrative regions (except Tibet, Taiwan, Hong Kong and Macau). Based on the research results drawn by Ding and Chen [45] and Ding [46], let be response variable and , , , and be regressors. There is no doubt that per capita disposable income has an important impact on the resident consumption rate. Therefore, we assume that the impacts of the above regressors on resident consumption rate may be realized through per capita disposable income and is selected as their intermediate variable. The definitions of these variables and their meanings are given in Table 5.

Table 5.

Variable definitions and their meanings.

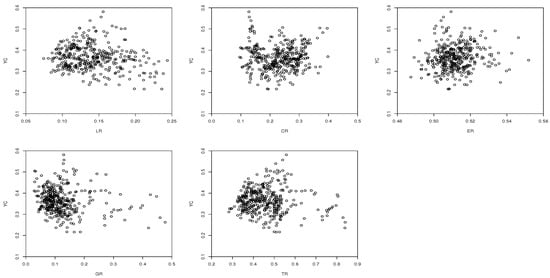

Firstly, Table 6 and Figure 4 show the descriptive statistics of the response variable, five regressors and intermediate variable. From observing Table 6, we can draw the conclusion that , , , , and are steady, as well as concluding that has a small fluctuation range. In addition, Figure 4 presents the scatter plots between versus each regressor (, , , and ). It can be found that the regressor has a linear effect on the response variable . The rest of the regressors have nonlinear effects on the response variable .

Table 6.

The descriptive statistics of the response variable, five regressors and intermediate variable.

Figure 4.

Scatter plots of the response variable versus five regressors, respectively.

Based on the above comprehensive analysis, the study on driving forces of Chinese resident consumption rate can be analyzed by establishing the following PLVCPDRM with nonseparable space-time filters:

where is a normalized spatial weight matrix calculated by the Euclidean distance in the light of the longitude and latitude coordinates of any two provinces.

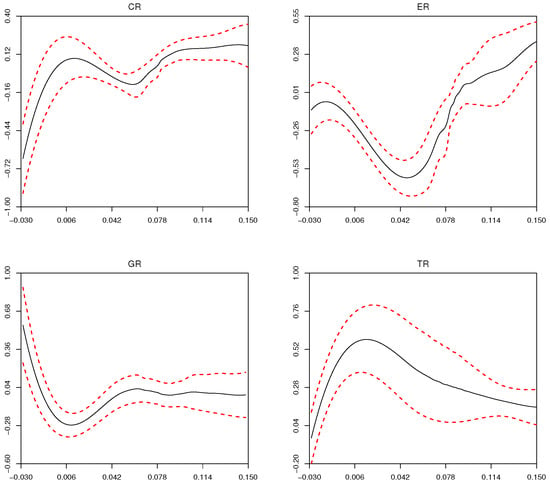

Table 7 reports the estimation results of parameters in the model (16). It can be seen that and are significant. Namely, it indicates that there exist strong and positive spatial and serial correlations among the disturbance terms in the model (16). Furthermore, is significant, which means that the linear effect of on the resident consumption rate is negative. Figure 5 shows the varying coefficient effects of , , and to and their confidence intervals. It can be seen that , , and have obvious nonlinear effects on resident consumption rate with .

Table 7.

Estimation results of parameters in the model (16).

Figure 5.

Varying coefficient effects of , , and to and their confidence intervals, respectively.

6. Concluding Remarks

In order to sufficiently use the information of spatial and serial correlations in the disturbances when modeling space-time data by regression models, we propose a fixed effects PLVCPDRM with nonseparable space-time filters. It can not only simultaneously capture non/linear effects of regressors and space-time correlations of error structure, but also overcome the “curse of dimensionality” in multivariate nonparametric regression models.

In this paper, the PQMLEs of unknown parameters and varying coefficient functions for this model are constructed. Under the regular assumptions, we prove that the estimators satisfy consistency and asymptotic normality. Monte Carlo simulations show that the proposed estimators have good finite sample performances. In addition, ignoring spatial and serial correlations in errors of the model would result in inconsistent and inefficient estimators. Finally, a Chinese resident consumption rate dataset is used to illustrate our estimation method.

This paper mainly focuses on the estimation of a fixed effects PLVCPDRM with nonseparable space-time filters. In the future, we may study the methods of variable selection, Bayesian estimation and quantile regression for the proposed model in our paper; we can also use the proposed method to study similar semiparametric panel data regression models with space-time filters.

Author Contributions

Formal analysis, B.L. and S.L.; Methodology, B.L. and J.C.; Software and writing—original draft, B.L.; Supervision, writing—review and editing and funding acquisition, J.C.; Data curation, S.L. All authors have read and agreed to the published version of manuscript.

Funding

This work is supported by National Social Science Fund of China (22BTJ024) and Natural Science Foundation of Fujian Province (2020J01170, 2022J01193).

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Acknowledgments

The authors are deeply grateful to the editors and anonymous referees for their careful reading and insightful comments. The comments led us to significantly improve the paper.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

To prove the theoretical results, the following facts and lemma will be used frequently in the sequel.

Fact 1: If and are matrices that are uniformly bounded in row sums (resp., column sums), then is also uniformly bounded in row sums (resp., column sums).

Fact 2: If is uniformly bounded in row sums (resp., column sums) and is a conformable matrix whose elements are uniformly , then so are the elements of (resp. .

The above two Facts can be found in Su and Jin [35].

Lemma A1.

Under Assumptions 1–3, we have that

- (i)

- .

- (ii)

- .

Proof.

(i) See the proof of Theorem 1 in Newey [40] (pp. 161–162); (ii) It follows from Assumption 3(i) by similar proof of (i). □

Proof of Theorem 1.

Substituting into the quasi-log-likelihood function (6), we have that

where

In order to prove that uniformly for , it is sufficient to prove that uniformly for according to that is deterministic by Assumption 4, where , . For case , as , we have that

By using Lemma 7 in Yu et al. [47], we have that uniformly for when T is fixed due to the explicit forms of , and which are UB from Assumption 4. For case , similarly, as and are UB, using Lemma 8 in Yu et al. [47], we have that when T is fixed.

To prove that is uniformly equicontinuous, we just need to investigate and according to that . It is easy to know that

It is obvious that is uniformly equicontinuous for and , so is . Furthermore, we know that

by . With the explicit form of , is uniformly equicontinuous for and . Thus, is uniformly equicontinuous for and . For , we find that is a linear quadratic form of parameters and , and a function of . Thus, it is uniformly equicontinuous for .

To prove identification uniqueness of , note that

where

and

Consider an auxiliary nonseparable space-time disturbance process: , where its quasi-log-likelihood function is

According to the information inequality for the auxiliary nonseparable space-time disturbance process, we know that for any and . Additionally, is a quadratic function of and with a negative semidefinite matrix given . We can find that identification uniqueness of and would be possible when

is nonsingular given any value of in Assumption 5 (iv), then for any and . In addition, when

for in Assumption 6 is satisfied, the identification uniqueness of and is obtained. This completes the proof. □

Proof of Theorem 2.

Denote and . According to the Taylor expansion of the first-order condition from maximizing the quasi-log-likelihood function

we have

where lies between and and converges to in probability by Theorem 1. The proof is completed if we can show that

and

To prove that (A2)–(A4) hold, we need to compute the following scores under the non-normality of errors:

Defining

and for any square matrix , we can obtain the expected Hessian matrix

which is a symmetric matrix.

According to the above results, it is not hard to obtain that

where is related to the third and fourth moments of . The expression of is as follows

where

and is the column vector formed by diagonal elements of a square matrix .

Proof of Theorem 3.

Note that is consistent with in Theorem 1, from the Equation (7), it holds that

where . Consider the first term of the last equation in (A7), let be the indicator function for the smallest eigenvalue of and being greater than . Then, . By Assumption 3, Lemma A1 and Fact 2, we have that

For the second term of last equation in (A7), note that by Assumption 3 (iii), then

For the third term of the last equation in (A7), it suffices to prove

by and . According to the Markov inequality, it follows that .

By Assumption 3, (A11) and Theorem 2, it is easy to obtain that

□

Proof of Theorem 4.

According to (A7), we have

Denote , we know

For any fixed point , as , applying the central limit theorem, we can obtain that

where . This completes the proof of Theorem 4. □

References

- Li, S.; Chen, J.; Li, B. Estimation and testing of random effects semiparametric regression model with separable space-time filters. Fractal Fract. 2022, 6, 735. [Google Scholar] [CrossRef]

- Hsiao, C. Benefits and limitations of panel data. Economet. Rev. 1985, 4, 121–174. [Google Scholar] [CrossRef]

- Baltagi, B.H. Panel data methods. In Handbook of Applied Economic Statistics; CRC Press: Boca Raton, FL, USA, 1998; pp. 311–323. [Google Scholar]

- Porter, C.O.; Outlaw, R.; Gale, J.P.; Cho, T.S. The use of online panel data in management research: A review and recommendations. J. Manag. 2019, 45, 319–344. [Google Scholar] [CrossRef]

- Zamanzade, E. EDF-based tests of exponentiality in pair ranked set sampling. Stat. Pap. 2019, 60, 2141–2159. [Google Scholar] [CrossRef]

- Imai, K.; Kim, I.S. On the use of two-way fixed effects regression models for causal inference with panel data. Polit. Anal. 2021, 29, 405–415. [Google Scholar] [CrossRef]

- Fan, J.; Gijbels, I. Local Polynomial Modelling and Its Applications; Chapman and Hall: London, UK, 1996. [Google Scholar]

- Luo, G.; Wu, M.; Pang, Z. Empirical likelihood inference for the semiparametric varying-coefficient spatial autoregressive model. J. Syst. Sci. Complex. 2021, 34, 2310–2333. [Google Scholar] [CrossRef]

- Ullah, A.; Wang, T.; Yao, W. Semiparametric partially linear varying coefficient modal regression. J. Econom. 2022. [Google Scholar] [CrossRef]

- Dai, X.; Li, S.; Jin, L.; Tian, M. Quantile regression for partially linear varying coefficient spatial autoregressive models. Commun. Stat-Simul. 2022, 1–16. [Google Scholar] [CrossRef]

- Li, Q.; Stengos, T. Semiparametric estimation of partially linear panel data models. J. Econom. 1996, 71, 389–397. [Google Scholar] [CrossRef]

- Baltagi, B.H.; Li, D. Series estimation of partially linear panel data models with fixed effects. Ann. Econ. Financ. 2002, 3, 103–116. [Google Scholar]

- Chen, J.; Gao, J.; Li, D. Estimation in partially linear single-index panel data models with fixed effects. J. Bus. Econ. Stat. 2013, 31, 315–330. [Google Scholar] [CrossRef]

- Huang, B.; Sun, Y.; Wang, S. Estimation of partially linear panel data models with cross-sectional dependence. J. Syst. Sci. Complex. 2021, 34, 2219–2230. [Google Scholar] [CrossRef]

- Yong, A.; Cheng, H.; Dong, L. Semiparametric estimation of partially linear varying coefficient panel data models. Adv. Econom. 2016, 36, 47–65. [Google Scholar]

- Zhou, B.; You, J.; Xu, Q.; Chen, G. Weighted profile least squares estimation for a panel data varying-coefficient partially linear model. Chin. Ann. Math. B 2010, 31, 247–272. [Google Scholar] [CrossRef]

- Zhang, Y.; Shen, D. Estimation of semi-parametric varying-coefficient spatial panel data models with random-effects. J. Stat. Plan. Infer. 2015, 159, 64–80. [Google Scholar] [CrossRef]

- Li, S.; Chen, J.; Chen, D. PQMLE of a partially linear varying coefficient spatial autoregressive panel model with random effects. Symmetry 2021, 13, 2057. [Google Scholar] [CrossRef]

- Su, L.; Ullah, A. Profile likelihood estimation of partially linear panel data models with fixed effects. Econ. Lett. 2006, 92, 75–81. [Google Scholar] [CrossRef]

- Wu, Q.; Luo, X.; Li, Y. Partially linear varying-coefficient panel data models with fixed effects. Far East J. Theor. Stat. 2008, 25, 229–238. [Google Scholar]

- Hu, X. Estimation in a semi-varying coefficient model for panel data with fixed effects. J. Syst. Sci. Complex. 2014, 27, 594–604. [Google Scholar] [CrossRef]

- Tran, K.C.; Tsionas, E.G. Local GMM estimation of semiparametric panel data with smooth coefficient models. Economet. Rev. 2009, 29, 39–61. [Google Scholar] [CrossRef]

- Su, L.; Ullah, A. Nonparametric and semiparametric panel econometric models: Estimation and testing. In Handbook of Empirical Economics and Finance; CRC Press: Boca Raton, FL, USA, 2011; pp. 455–497. [Google Scholar]

- Liu, Y.; Zhuang, X. Shrinkage estimation of semi-parametric spatial autoregressive panel data model with fixed effects. Stat. Probabil. Lett. 2023, 194, 109746. [Google Scholar] [CrossRef]

- Elhorst, J.P. Serial and spatial error correlation. Econ. Lett. 2008, 99, 422–424. [Google Scholar] [CrossRef]

- Baltagi, B.H.; Song, S.H.; Jung, B.C.; Koh, W. Testing for serial correlation, spatial autocorrelation and random effects using panel data. J. Econ. 2007, 140, 5–51. [Google Scholar] [CrossRef]

- Parent, O.; LeSage, J.P. A space-time filter for panel data models containing random effects. Comput. Stat. Data Anal. 2011, 55, 475–490. [Google Scholar] [CrossRef]

- Lee, L.; Yu, J. Estimation of fixed effects panel regression models with separable and nonseparable space-time filters. J. Econ. 2015, 184, 174–192. [Google Scholar] [CrossRef]

- Bai, Y.; Hu, J.; You, J. Panel data partially linear varying-coefficient model with both spatially and time-wise correlated errors. Stat. Sin. 2015, 35, 275–294. [Google Scholar] [CrossRef]

- Zhao, J.Q.; Zhao, Y.; Lin, J.; Miao, Z.; Khaled, W. Estimation and testing for panel data partially linear single-index models with errors correlated in space and time. Random Matrices Theory Appl. 2020, 9, 2150005. [Google Scholar] [CrossRef]

- De Boor, C. A Practical Guide to Splines; Springer: New York, NY, USA, 1978. [Google Scholar]

- Huang, J.Z.; Shen, H. Functional coefficient regression models for non-linear time series: A polynomial spline approach. Scand. J. Stat. 2004, 31, 515–534. [Google Scholar] [CrossRef]

- Zou, Q.; Zhu, Z. M-estimators for single-index model using B-spline. Metrika 2014, 77, 225–246. [Google Scholar] [CrossRef]

- Hsiao, C.; Pesaran, H.; Tahmiscioglu, K. Maximum likelihood estimation of fixed effects dynamic panel data models covering short time periods. J. Econ. 2002, 109, 107–150. [Google Scholar] [CrossRef]

- Su, L.; Jin, S. Profile quasi-maximum likelihood estimation of partially linear spatial autoregressive models. J. Econ. 2010, 157, 18–33. [Google Scholar] [CrossRef]

- Kelejian, H.H.; Prucha, I.R. A generalized spatial two-stage least squares procedure for estimation a spatial autoregressive model with autoregressive disturbances. J. Real Estate Financ. Econ. 1998, 17, 99–121. [Google Scholar] [CrossRef]

- Kelejian, H.H.; Prucha, I.R. A generalized moments estimator for the autoregressive parameter in a spatial model. Int. ECcon. Rev. 1999, 40, 509–533. [Google Scholar] [CrossRef]

- Cheng, S.; Chen, J. Estimation of partially linear single-index spatial autoregressive model. Stat. Pap. 2021, 62, 495–531. [Google Scholar] [CrossRef]

- Hu, J.; Liu, F.; You, J. Panel data partially linear model with fixed effects, spatial autoregressive error components and unspecified intertemporal correlation. J. Multivar. Anal. 2014, 130, 64–89. [Google Scholar] [CrossRef]

- Newey, W.K. Convergence rates and asymptotic normality for series estimators. J. Econ. 1997, 79, 147–168. [Google Scholar] [CrossRef]

- Zhang, Y. Estimation of partially specified spatial panel data models with random-effects and spatially correlated error components. Commun. Stat.-Theory Methods 2017, 46, 1056–1079. [Google Scholar] [CrossRef]

- Horn, R.; Johnson, C. Matrix Algebra; Cambridge University Press: Cambridge, UK, 1985. [Google Scholar]

- Lee, L. Asymptotic distributions of quasi-maximum likelihood estimators for spatial econometric models. Econometrica 2004, 72, 1899–1925. [Google Scholar] [CrossRef]

- Su, L. Semiparametric GMM estimation of spatial autoregressive models. J. Econ. 2012, 167, 543–560. [Google Scholar] [CrossRef]

- Ding, F.; Chen, J. Fast efficient estimators of partially linear varying coefficient panel model with fixed effects. Chin. J. Appl. Probab. Statist. 2019, 36, 11. [Google Scholar]

- Ding, F. Penalized empirical likelihood estimation for partially linear single index panel model with fixed effects. Chin. J. Appl. Probab. Statist. 2019, 35, 573–593. [Google Scholar]

- Yu, J.; De Jong, R.; Lee, L. Quasi-maximum likelihood estimators for spatial dynamic panel data with fixed effects when both n and T are large. J. Econ. 2008, 146, 118–134. [Google Scholar] [CrossRef]

- Kelejian, H.H.; Prucha, I.R. On the asymptotic distribution of the Moran I test statistic with applications. J. Econ. 2001, 104, 219–257. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).