Multi-Objective Portfolio Optimization Using a Quantum Annealer

Abstract

:1. Introduction

- Balancing Risk and Return: Multi-objective optimization allows investors to find a balance between risk and return that suits their risk appetite and investment goals. This is not just about maximizing returns; it is about achieving the best trade-off between risk and return that aligns with an investor’s preferences.

- Diversification: Effective portfolio management involves diversifying investments across different assets to reduce risk. Multi-objective optimization helps identify diverse combinations of assets that can potentially provide higher returns, while managing risk through diversification.

- Handling Trade-offs: Multi-objective optimization helps investors explicitly address trade-offs between conflicting objectives. For instance, an investor might be willing to accept slightly lower returns in exchange for significantly lower risk. Multi-objective optimization can quantify these trade-offs and help in making informed decisions.

- Tailored Solutions: Different investors have different preferences and constraints. Multi-objective optimization allows for the creation of personalized portfolios that align with an individual investor’s specific goals and constraints.

- Market Uncertainty: Financial markets are inherently uncertain and subject to volatility. By considering multiple objectives, investors can design portfolios that are robust and adaptable to changing market conditions.

- Flexible Decision-Making: Multi-objective optimization provides a range of possible solutions, known as the Pareto frontier or Pareto front. This set of solutions represents different combinations of risk and return that an investor can choose from based on their preferences.

- Stress Testing: Multi-objective optimization enables investors to stress test their portfolios by examining how different market scenarios impact the trade-off between risk and return. This helps in assessing the resilience of a portfolio under adverse conditions.

- Long-Term Planning: Portfolio optimization is not a one-time task; it requires continuous monitoring and adjustment. Multi-objective optimization aids in making informed decisions when rebalancing portfolios over time, considering changing market dynamics and investor preferences.

2. Quantum Annealing and QUBO Formulation

3. Problem Description

3.1. Basic Problem

3.2. Our Financial Case

- The decision variables are now denoted by

4. Classical Convex Optimization

| Algorithm 1: Classical Convex Optimization |

|

5. Reformulation to QUBO

6. Experimental Set-Up and Results

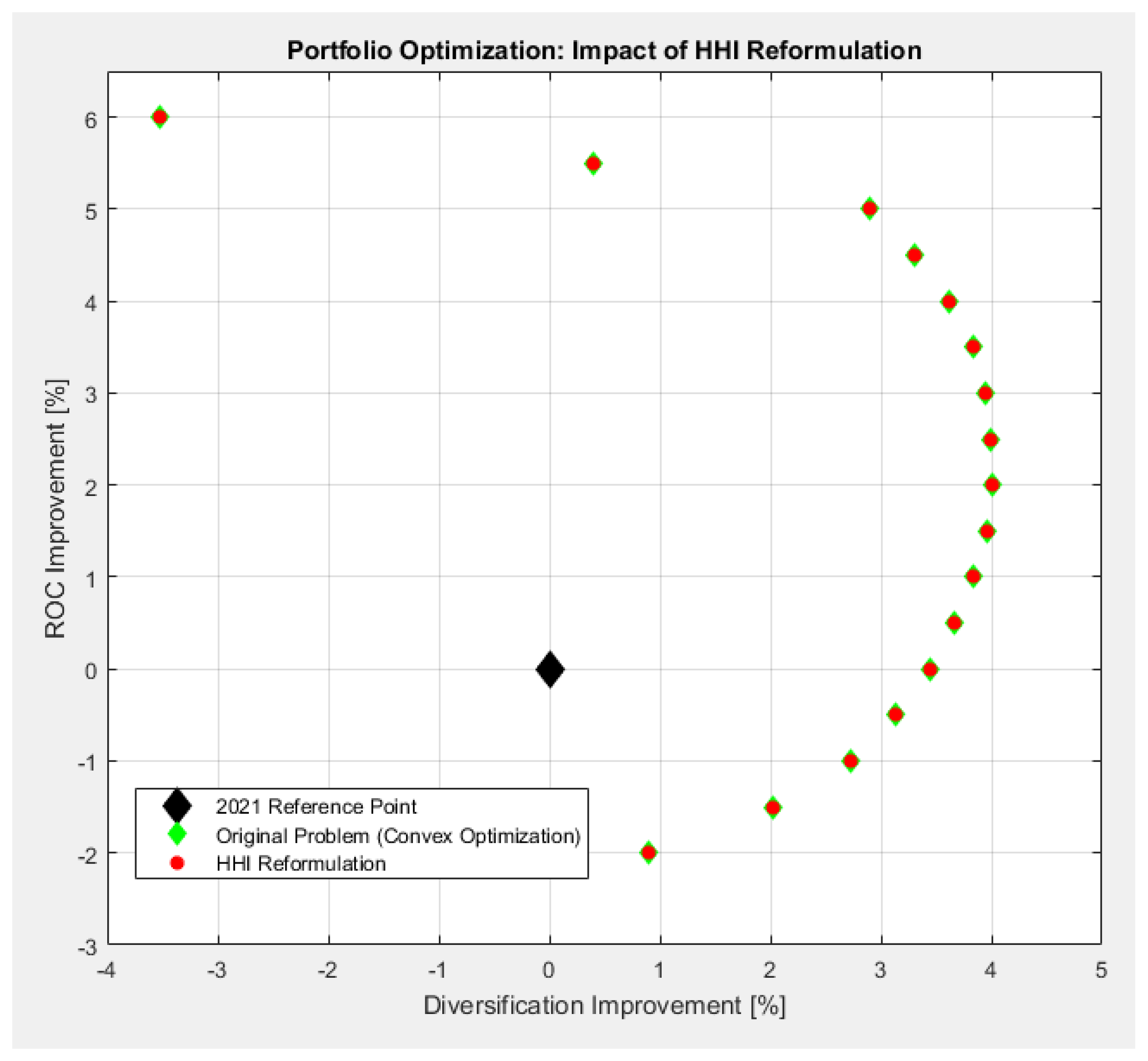

6.1. Classical Approach: Convex Optimization

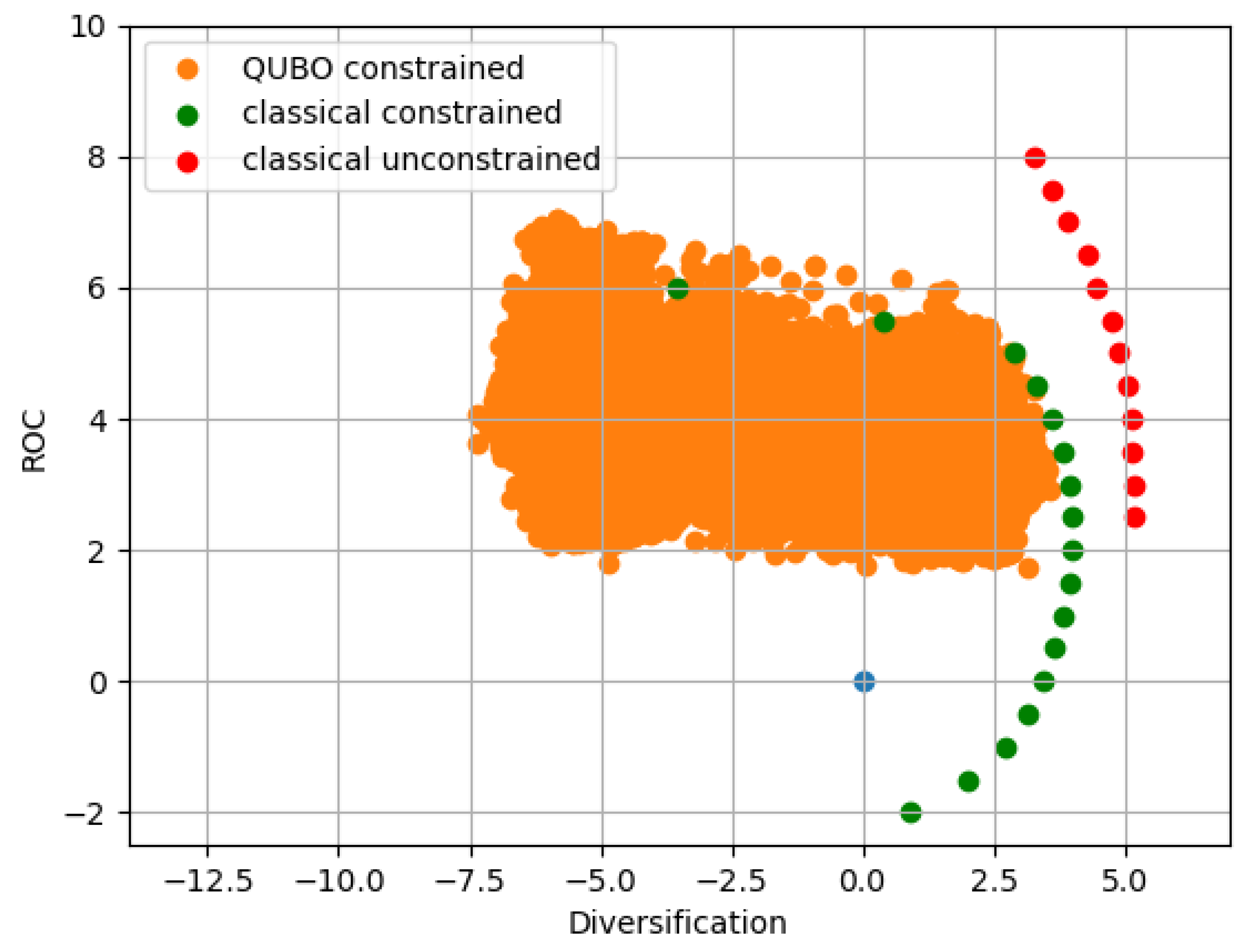

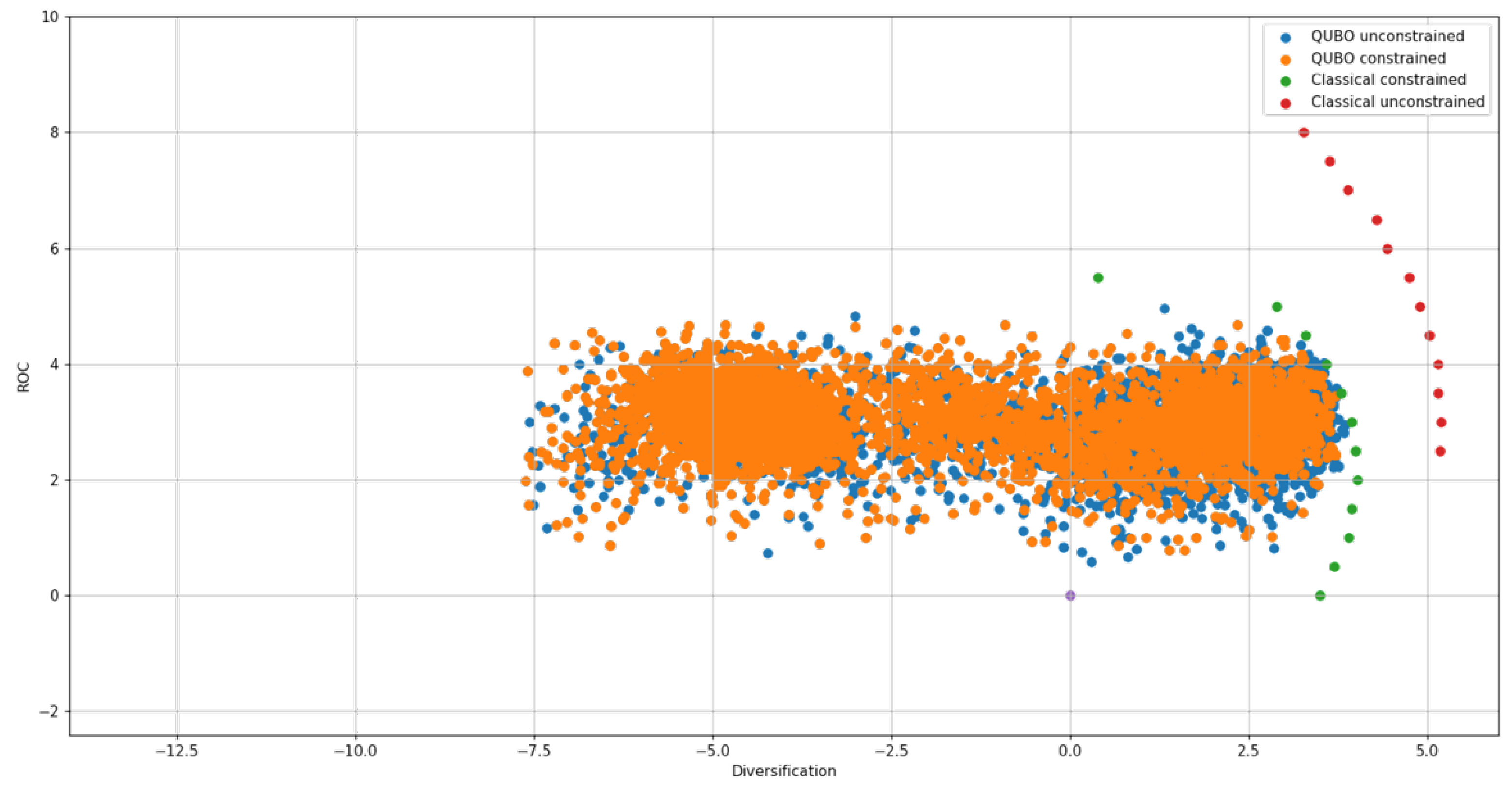

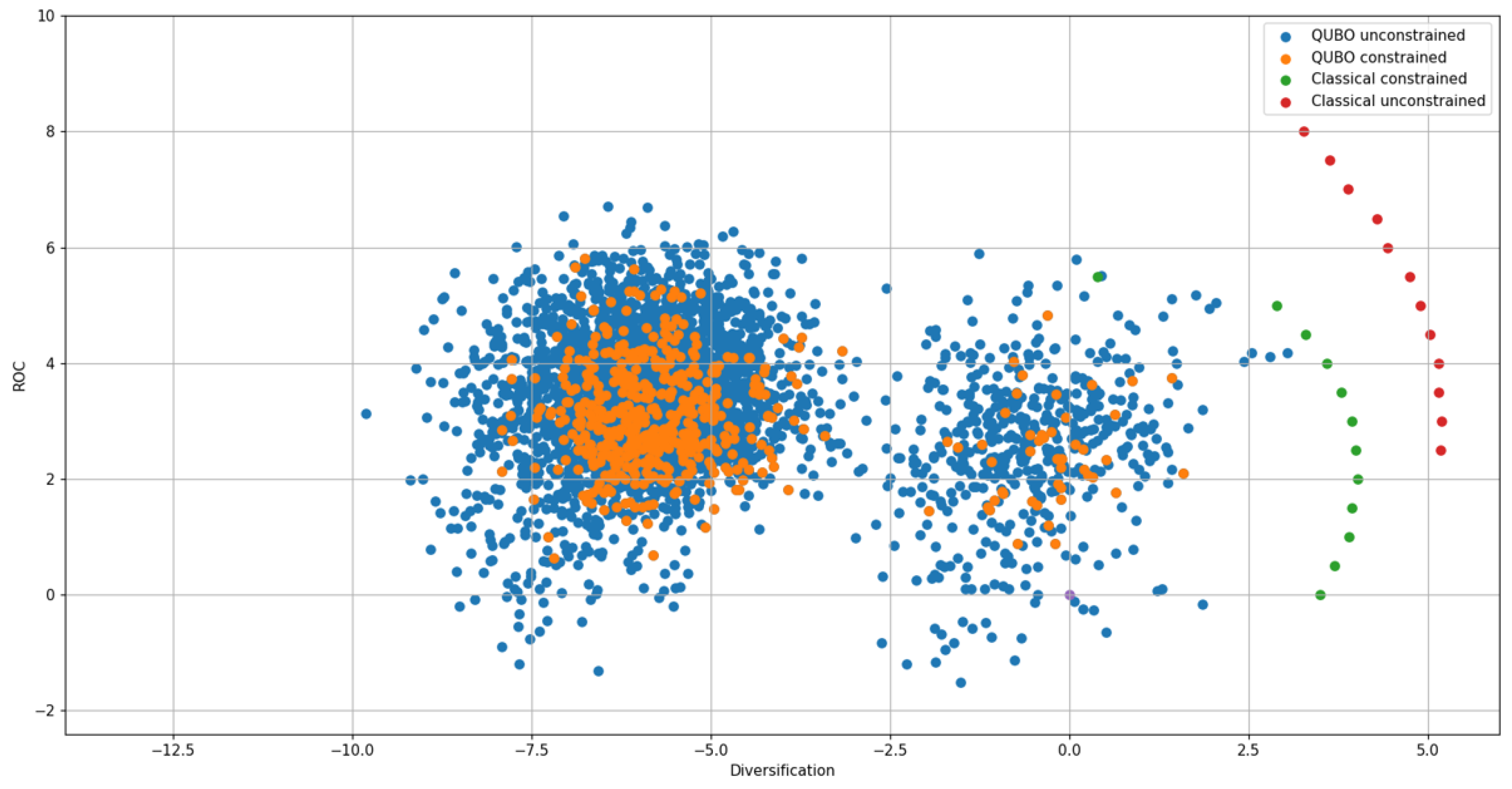

6.2. Results

6.3. Results

7. Conclusions and Further Research

- Recommendations for further research:

- Refinement of QUBO Formulations: We recommend further refinement of the QUBO formulations to better capture the nuances of the portfolio optimization problem. Fine-tuning penalty and preference parameters, especially in the second QUBO formulation, could lead to improved results.

- Exploration of Alternative Quantum Algorithms: While quantum annealing has been shown to be promising, it might be worthwhile to explore other quantum algorithms, such as QAOA, for portfolio optimization. Comparative studies could help determine the most effective approach.

- Quantum Computing Hardware Development: As quantum computing hardware continues to advance, we recommend staying up to date with developments from leading companies like Google, IBM, and D-Wave. Newer, more powerful quantum computers may provide even better solutions for portfolio optimization.

- Integration with Traditional Portfolio Management: Quantum computing can be used in conjunction with traditional portfolio management techniques. We recommend exploring hybrid approaches that leverage the strengths of both classical and quantum computing to enhance portfolio management strategies.

- Validation on Diverse Datasets: It is crucial to validate the quantum computing solutions on diverse datasets and real-world scenarios, to ensure their robustness and practical applicability. Additionally, investigating the scalability of quantum solutions for larger portfolios is essential.

- Continuous Monitoring and Improvement: Portfolio management is an ongoing process, and quantum solutions should be continuously monitored and improved to adapt to changing market dynamics and investor preferences.

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Abbreviations

| HHI | Herfindahl–Hirschman index (HHI) |

| IQP | Integer quadratic programming |

| QAOA | Quantum approximate optimization algorithm |

| QUBO | Quadratic unconstrained binary optimization problem |

| ROC | Return on capital |

References

- Markowitz, H. Harry Markowitz: Selected Works; World Scientific: Singapore, 2009; Volume 1. [Google Scholar]

- Radulescu, M.; Radulescu, C.Z. A Multi-objective Approach to Multi-period: Portfolio Optimization with Transaction Costs. In Financial Decision Aid Using Multiple Criteria; Springer: Cham, Switzerland, 2018; pp. 93–112. [Google Scholar]

- Xidonas, P.; Mavrotas, G.; Hassapis, C.; Zopounidis, C. Robust multiobjective portfolio optimization: A minimax regret approach. Eur. J. Oper. Res. 2017, 262, 299–305. [Google Scholar] [CrossRef]

- Skaf, J.; Boyd, S. Multi-Period Portfolio Optimization with Constraints and Transaction Costs. Working Manuscript. 2009. Available online: https://web.stanford.edu/~boyd/papers/pdf/dyn_port_opt.pdf (accessed on 20 March 2024).

- Liagkouras, K.; Metaxiotis, K. Multi-period mean–variance fuzzy portfolio optimization model with transaction costs. Eng. Appl. Artif. Intell. 2018, 67, 260–269. [Google Scholar] [CrossRef]

- Fulga, C.; Stanojević, B. Single period portfolio optimization with fuzzy transaction costs. In Proceedings of the 20th International Conference EURO Mini Conference “Continuous Optimization and Knowledge-Based Technologies”, EurOPT 2008, Neringa, Lithuania, 20–23 May 2008; Vilnius Gediminas Technical University: Vilnius, Lithuania, 2008. [Google Scholar]

- Pang, T.; Hussain, A. A stochastic portfolio optimization model with complete memory. Stoch. Anal. Appl. 2017, 35, 742–766. [Google Scholar] [CrossRef]

- Pang, T.; Varga, K. Portfolio Optimization for Assets with Stochastic Yields and Stochastic Volatility. J. Optim. Theory Appl. 2019, 182, 691–729. [Google Scholar] [CrossRef]

- Del Pia, A.; Dey, S.S.; Molinaro, M. Mixed-integer quadratic programming is in NP. Math. Program. 2017, 162, 225–240. [Google Scholar]

- Garey, M.R.; Johnson, D.S. Computers and Intractability; Freeman: San Francisco, CA, USA, 1979; Volume 174. [Google Scholar]

- Li, D.; Sun, X.; Gu, S.; Gao, J.; Liu, C. Polynomially solvable cases of binary quadratic programs. In Optimization and Optimal Control; Springer: New York, NY, USA, 2010; pp. 199–225. [Google Scholar]

- Poli, R.; Kennedy, J.; Blackwell, T. Particle swarm optimization: An overview. Swarm Intell. 2007, 1, 33–57. [Google Scholar] [CrossRef]

- Grefenstette, J.J. Genetic algorithms and machine learning. In Proceedings of the Sixth Annual Conference on Computational Learning Theory, Santa Cruz, CA, USA, 26–28 July 1993; pp. 3–4. [Google Scholar]

- Angus, D.; Woodward, C. Multiple objective ant colony optimisation. Swarm Intell. 2009, 3, 69–85. [Google Scholar] [CrossRef]

- Kirkpatrick, S.; Gelatt, C.D., Jr.; Vecchi, M.P. Optimization by simulated annealing. Science 1983, 220, 671–680. [Google Scholar] [CrossRef]

- Zanjirdar, M. Overview of Portfolio Optimization Models. Adv. Math. Financ. Appl. 2020, 5, 1–16. [Google Scholar]

- Ronagh, P.; Woods, B.; Iranmanesh, E. Solving constrained quadratic binary problems via quantum adiabatic evolution. Quantum Inf. Comput. 2016, 16, 1029–1047. [Google Scholar] [CrossRef]

- McGeoch, C.C. Adiabatic quantum computation and quantum annealing: Theory and practice. Synth. Lect. Quantum Comput. 2014, 5, 1–93. [Google Scholar]

- Farhi, E.; Harrow, A.W. Quantum supremacy through the quantum approximate optimization algorithm. arXiv 2016, arXiv:1602.07674. [Google Scholar]

- Neumann, N.; Phillipson, F.; Versluis, R. Machine learning in the quantum era. Digit. Welt 2019, 3, 24–29. [Google Scholar] [CrossRef]

- Möller, M.; Vuik, C. On the impact of quantum computing technology on future developments in high-performance scientific computing. Ethics Inf. Technol. 2017, 19, 253–269. [Google Scholar] [CrossRef]

- Gemeinhardt, F.G. Quantum Computing: A Foresight on Applications, Impacts and Opportunities of Strategic Relevance. Ph.D. Thesis, Universität Linz, Linz, Austria, 2020. [Google Scholar]

- Resch, S.; Karpuzcu, U.R. Quantum computing: An overview across the system stack. arXiv 2019, arXiv:1905.07240. [Google Scholar]

- Piattini, M.; Peterssen, G.; Pérez-Castillo, R.; Oliver, J.L.H.; Serrano, M.A.; González, G.J.H.; de Guzmán, I.G.R.; Paradela, C.A.; Polo, M.; Murina, E.; et al. The Talavera Manifesto for Quantum Software Engineering and Programming. In Proceedings of the QANSWER, Talavera, Spain, 12–18 February 2020; pp. 1–5. [Google Scholar]

- Van den Brink, R.; Phillipson, F.; Neumann, N.M. Vision on next level quantum software tooling. In Proceedings of the Computation Tools, Venice, Italy, 5–9 May 2019. [Google Scholar]

- Neumann, N.M.P.; van der Schoot, W.; Sijpesteijn, T. Quantum Cloud Computing from a User Perspective. In Proceedings of the International Conference on Innovations for Community Services, Bamberg, Germany, 11–13 September 2023; Springer: Cham, Switzerland, 2023; pp. 236–249. [Google Scholar]

- Orus, R.; Mugel, S.; Lizaso, E. Quantum computing for finance: Overview and prospects. Rev. Phys. 2019, 4, 100028. [Google Scholar] [CrossRef]

- Elsokkary, N.; Khan, F.S.; La Torre, D.; Humble, T.S.; Gottlieb, J. Financial Portfolio Management Using D-Wave Quantum Optimizer: The Case of Abu Dhabi Securities Exchange; Technical report; Oak Ridge National Lab. (ORNL): Oak Ridge, TN, USA, 2017. [Google Scholar]

- Venturelli, D.; Kondratyev, A. Reverse quantum annealing approach to portfolio optimization problems. Quantum Mach. Intell. 2019, 1, 17–30. [Google Scholar] [CrossRef]

- Marzec, M. Portfolio optimization: Applications in quantum computing. In Handbook of High-Frequency Trading and Modeling in Finance; Wiley: Hoboken, NJ, USA, 2016; pp. 73–106. [Google Scholar]

- Cohen, J.; Khan, A.; Alexander, C. Portfolio Optimization of 40 Stocks Using the D-Wave Quantum Annealer. arXiv 2020, arXiv:2007.01430. [Google Scholar]

- Cohen, J.; Khan, A.; Alexander, C. Portfolio Optimization of 60 Stocks Using Classical and Quantum Algorithms. arXiv 2020, arXiv:2007.08669. [Google Scholar]

- Kaushik, N.; Raj, A.; Srivastava, M.; Ansari, M.S.; Pushpalatha, M.; Gayathri, M.; Kavisankar, L.; Deshpande, S.; Venkatraman, R. Financial Portfolio Optimization: A QAOA and VQE Formulation for Sharpe Ratio Maximization. In Proceedings of the 2023 6th International Conference on Recent Trends in Advance Computing (ICRTAC), Chennai, India, 14–15 December 2023; IEEE: Piscataway, NJ, USA, 2023; pp. 575–581. [Google Scholar]

- Phillipson, F.; Bhatia, H.S. Portfolio optimisation using the D-Wave quantum annealer. In Proceedings of the International Conference on Computational Science, Krakow, Poland, 16–18 June 2021; Springer: Cham, Switzerland, 2021; pp. 45–59. [Google Scholar]

- Sakuler, W.; Oberreuter, J.M.; Aiolfi, R.; Asproni, L.; Roman, B.; Schiefer, J. A real world test of Portfolio Optimizationwith Quantum Annealing. arXiv 2024, arXiv:2303.12601. [Google Scholar]

- George, B.; Loo, J.; Jie, W. Novel multi-objective optimisation for maintenance activities of floating production storage and offloading facilities. Appl. Ocean. Res. 2023, 130, 103440. [Google Scholar] [CrossRef]

- Afshari, H.; Tosarkani, B.M.; Jaber, M.Y.; Searcy, C. The effect of environmental and social value objectives on optimal design in industrial energy symbiosis: A multi-objective approach. Resour. Conserv. Recycl. 2020, 158, 104825. [Google Scholar] [CrossRef]

- Lucas, A. Ising formulations of many NP problems. Front. Phys. 2014, 2, 5. [Google Scholar] [CrossRef]

- Glover, F.; Kochenberger, G.; Hennig, R.; Du, Y. Quantum Bridge Analytics I: A tutorial on formulating and using QUBO models. Ann. Oper. Res. 2019, 17, 335–371. [Google Scholar] [CrossRef]

- Domino, K.; Koniorczyk, M.; Krawiec, K.; Jałowiecki, K.; Deffner, S.; Gardas, B. Quantum annealing in the NISQ era: Railway conflict management. Entropy 2023, 25, 191. [Google Scholar] [CrossRef]

- Neukart, F.; Compostella, G.; Seidel, C.; Von Dollen, D.; Yarkoni, S.; Parney, B. Traffic flow optimization using a quantum annealer. Front. ICT 2017, 4, 29. [Google Scholar] [CrossRef]

- Phillipson, F.; Chiscop, I. Multimodal container planning: A QUBO formulation and implementation on a quantum annealer. In Proceedings of the International Conference on Computational Science, Krakow, Poland, 16–18 June 2021; Springer: Cham, Switzerland, 2021; pp. 30–44. [Google Scholar]

- Chiscop, I.; Nauta, J.; Veerman, B.; Phillipson, F. A hybrid solution method for the multi-service location set covering problem. In Proceedings of the Computational Science–ICCS 2020: 20th International Conference, Amsterdam, The Netherlands, 3–5 June 2020; Proceedings, Part VI 20. Springer: Berlin/Heidelberg, Germany, 2020; pp. 531–545. [Google Scholar]

- Phillipson, F. Quantum Computing in Telecommunication—A Survey. Mathematics 2023, 11, 3423. [Google Scholar] [CrossRef]

- Lin, M.M.; Shu, Y.C.; Lu, B.Z.; Fang, P.S. Nurse Scheduling Problem via PyQUBO. arXiv 2023, arXiv:2302.09459. [Google Scholar]

- Nazareth, D.P.; Spaans, J.D. First application of quantum annealing to IMRT beamlet intensity optimization. Phys. Med. Biol. 2015, 60, 4137. [Google Scholar] [CrossRef]

- Rhoades, S.A. The Herfindahl-Hirschman Index. Fed. Res. Bull. 1993, 79, 188. [Google Scholar]

- Lobo, M.; Fazel, M.; Boyd, S. Portfolio Optimization with Linear and Fixed Transaction Costs. Ann. Oper. Res. 2007, 152, 341–365. [Google Scholar] [CrossRef]

- Boyd, S.; Busseti, E.; Diamond, S.; Kahn, R.N.; Kwangmoo, K.; Nystrup, P.; Speth, J. Multi-Period Trading via Convex Optimization. Found. Trends Optim. 2017, 3, 1–76. [Google Scholar] [CrossRef]

- Boyd, S.; El Ghaoui, L.; Feron, E.; Venkataramanan, B. Linear Matrix Inequalities in System and Control Theory; Soc. for Industrial and Applied Mathematics (SIAM): Philadelphia, PA, USA, 1994. [Google Scholar]

- Boyd, S.; Vandenberghe, L. Convex Optimization; Cambridge University Press: Cambridge, UK, 2004. [Google Scholar]

- Nesterov, Y.; Nemirovskii, A. Interior-Point Polynomial Methods in Convex Programming; Soc. for Industrial and Applied Mathematics (SIAM): Philadelphia, PA, USA, 1994. [Google Scholar]

- Sturm, J.F. Using SeDuMi 1.02, a Matlab Toolbox for Optimization over Symmetric Cones. Optim. Methods Softw. 1999, 11–12, 625–653. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Description | Notation |

|---|---|

| Outstanding amount in 2021 per asset (€) | |

| Return (i.e., income) in 2021 per asset (€) | |

| Regulatory capital in 2021 per asset (€) | |

| Lower bound outstanding amount in 2030 per asset (€) | |

| Upper bound outstanding amount in 2030 per asset (€) | |

| Emission intensity total reduction in 2030 (fixed) | 24% |

| Emission intensity in 2021 per asset (kg CO2e/€) |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Aguilera, E.; de Jong, J.; Phillipson, F.; Taamallah, S.; Vos, M. Multi-Objective Portfolio Optimization Using a Quantum Annealer. Mathematics 2024, 12, 1291. https://doi.org/10.3390/math12091291

Aguilera E, de Jong J, Phillipson F, Taamallah S, Vos M. Multi-Objective Portfolio Optimization Using a Quantum Annealer. Mathematics. 2024; 12(9):1291. https://doi.org/10.3390/math12091291

Chicago/Turabian StyleAguilera, Esteban, Jins de Jong, Frank Phillipson, Skander Taamallah, and Mischa Vos. 2024. "Multi-Objective Portfolio Optimization Using a Quantum Annealer" Mathematics 12, no. 9: 1291. https://doi.org/10.3390/math12091291