Abstract

This study examines risk factors in mergers and acquisitions (M&As) identified in the recent literature, addressing the following question: “What risk factors associated with M&A transactions are discussed in the recent academic literature?” A semi-systematic literature review was conducted using a comprehensive search strategy with targeted keywords related to M&A risks. Papers from 2020 to 2024 were selected based on quality and relevance, with detailed review of abstracts and titles. Co-occurrence analysis using VOSviewer software (version 1.6.20) was applied to categorize key themes. The review of 118 papers identified four main risk categories: information asymmetry; performance and corporate reputation; litigation and investor protection; and geopolitical factors. Findings reveal complex interdependencies among these risks, highlighting the need for a holistic approach to risk management. Corporate social responsibility (CSR) is crucial for mitigating risks, improving transparency, and enhancing reputation. This study offers recommendations for better financial disclosures, robust environmental, social and governance strategies, and the integration of digital finance technologies as blockchain in M&A activity. Future research should include longitudinal studies on M&A risk dynamics, case studies on corporate governance, advanced valuation methods, and comparative analyses across regions and industries, focusing on emerging technologies like AI and blockchain.

1. Introduction

Mergers and acquisitions (M&As) are prevalent strategies used by companies to achieve corporate restructuring and financial growth. M&As involve the consolidation of two or more previously independent organizations into a single entity. Specifically, a merger is the combination of two companies into one, while an acquisition involves one company purchasing another. These operations integrate all aspects of the involved businesses, including their brand equity, assets, and liabilities. This comprehensive integration aims to enhance operational efficiency, expand market reach, and create synergies between the combined entities (Piesse et al. 2022).

M&A operations have a profound impact on the business landscape, reflected in their substantial economic footprint. Over the past four years, a total of 195,981 M&A deals have been executed, collectively generating an economic impact of EUR 10.936 trillion (IMAA—Institute for Mergers, Acquisitions, and Alliances 2024). This vast volume underscores the pivotal role of M&A activities in reshaping industries, driving corporate growth, and enhancing market efficiency.

Trends in the M&A landscape are facing a shift. Recent political scenarios have profoundly impacted mergers and acquisitions by introducing a range of challenges and opportunities that have reshaped strategic priorities. Geopolitical tensions, trade policies, and regulatory changes have created an increasingly complex environment for M&A activity (Shen et al. 2021). More recently, events like Russia’s invasion of Ukraine, US–China tensions, and ongoing conflicts in the Middle East are driving heightened political risk (Darbyshire et al. 2024). Financial institutions are hiring political experts and creating dedicated geopolitical advisory units to navigate these risks. Despite this, financial markets have shown resilience, with stock indexes reaching record highs and limited immediate impact from geopolitical shocks (PricewaterhouseCoopers 2024). This shift is causing investors to seek greater geopolitical insights and adapt their strategies accordingly.

These political factors, coupled with the rise of emergent technologies (Florackis et al. 2022) and a heightened emphasis on sustainability and corporate social responsibility (CSR) (Tampakoudis and Anagnostopoulou 2020), have compelled companies to navigate a more volatile market. In the evolving M&A landscape, sustainability and technology are pivotal drivers. Companies are increasingly pursuing acquisitions to enhance their environmental, social, and governance (ESG) credentials, comply with stricter regulations, and integrate advanced technologies like AI and digital platforms. This strategic focus on sustainability and technology helps firms accelerate growth, adapt to market shifts, and meet the demands of a tech-savvy, environmentally conscious consumer base.

On these grounds, this paper seeks to address the critical research question: “What are the primary risk factors associated with mergers and acquisitions discussed in the recent literature?” This paper aims to analyze what the recent academic literature has discussed on the risks associated with mergers and acquisitions. Therefore, the review seeks to identify prevailing themes and concerns, and establish a foundation for future research.

A semi-systematic literature review is used to examine risks in mergers and acquisitions. Unlike comprehensive reviews that cover all published studies, this approach integrates diverse perspectives and identifies key themes without aiming to catalog every study (Snyder 2019). It focuses on addressing specific research questions by combining various viewpoints for a thorough overview. This study employs the semi-systematic review method to map the research landscape, highlight major M&A risk factors, and find gaps in the literature. This review, covering studies from 2020 to 2024 sourced from the Web of Science Core Collection database, involved selecting 118 relevant papers through abstracts and keywords and identifying key themes using co-occurrence analysis with VOSviewer software. The analysis of these themes aims to provide insights into current academic evidence and suggest gaps in the literature.

This analysis identifies four key M&A risk areas: (1) information asymmetry and emerging technologies, (2) performance and corporate reputation, (3) litigation, and (4) geopolitical factors. It highlights the interconnected nature of these risks, showing how litigation is linked to political and informational factors. The findings stress the need for a holistic approach to risk management and emphasize the role of CSR in mitigating risks by enhancing corporate reputation and improving transparency and disclosure.

The rest of this study unfolds as follows: Section 2 provides an overview of the process of M&A operations and the key aspects in each stage. The methodological approach is developed in Section 3. Section 4 identifies the key findings of the literature review. Ultimately, Section 5 discuss the key points found in this analysis, providing directions for future research.

2. Conceptual Background

This section establishes a foundational understanding of M&A processes through the lens of various theoretical frameworks, crucial for identifying risks in M&A operations, as highlighted in the recent literature.

2.1. The M&A Process

The merger and acquisition process is inherently complex and unfolds through a series of sequential stages. According to DePamphilis (2018), the M&A process is structured into ten distinct stages. These stages can be categorized into three overarching phases based on their role in the transaction timeline: planning and targeting, deal structuring and closing, and post-merger stages.

2.1.1. Acquisition Planning and Targeting

The planning phase involves preliminary activities and strategic groundwork crucial for setting the stage for an acquisition. Initially, acquiring companies formulate a business plan that is supported by an acquisition plan. Additionally, the plan addresses the financing strategy to safeguard the financial stability of the acquiring firm and incorporates an integration plan to manage post-merger challenges effectively (DePamphilis 2018).

In the pre-deal stage of M&As, senior management establishes financial parameters that guide target selection, drawing on resources such as internal cash flow, equity, and debt markets (Ott 2020). While financial theory suggests that funding can be secured if the acquisition meets its cost of capital, managerial risk tolerance often dictates the actual financial commitment (Hemrajani et al. 2023). The target selection process relies heavily on information sources, with challenges arising particularly for privately owned firms due to fragmented data (Welch et al. 2020). Key criteria include market size, profitability, and regulatory environment, with both financial and nonfinancial objectives reflecting the risks and strategic motivations of the acquisition.

Within this phase, evaluating synergies is essential for selecting appropriate acquisition targets by assessing the potential value that the merger could generate (Feldman and Hernandez 2022). Synergies can enhance operational efficiencies, reduce costs, increase revenues, and provide competitive advantages that are not achievable independently. The accuracy of this assessment is crucial, as misjudging synergies cannot be fully mitigated during post-merger integration, even with effective management (Bauer and Friesl 2024).

Risks considered in the preliminary stages of an M&A are mainly three (DePamphilis 2018). Operating risks, which concern the acquirer’s ability to manage a company, particularly if the target operates outside the acquirer’s core business; financial risk, which involves assessing the ability to leverage the acquisition without compromising financial ratios critical for maintaining a credit rating and understanding investor tolerance for potential earnings per share dilution; and lastly, overpayment risk refers to the potential long-term impact growth rates if the acquisition price exceeds the economic value of the target.

The intensity of these risks is determined by two main aspects: contextual factors and information asymmetry (Welch et al. 2020), as valuation of target firms influences the terms of negotiation in posterior stages. Contextual factors, such as the industry or culture the acquirer is familiar with, determine the selection of targets. According to Pan et al. (2020), firm managers with a higher degree of uncertainty avoidance, influenced by their cultural heritage, are significantly less likely to engage in mergers and acquisitions and tend to select acquisition targets in familiar industries and with fewer post-merger integration challenges. Concurrently, information asymmetry affects targeting valuation and selection, as target firms with limited access to information are more overvalued compared to those with better information access (Li 2020).

Companies mitigate these risks by selecting targets similar to their previous acquisitions or those targeted by industry peers (Welch et al. 2020), as well as increasing analyst coverage on target firms to refine valuation outcomes. Additionally, companies use investor protection mechanisms such as representations and warranties, contractual assertions made by the seller about the target’s condition, such as the accuracy of financial statements (Even-Tov et al. 2022).

2.1.2. Deal Structuring and Closing

Deal structuring is a key phase in mergers and acquisitions, focusing on negotiating and finalizing the terms of the transaction to align the goals of both parties. This phase involves setting initial negotiating positions, assessing risks, and addressing potential conflicts related to payment structures and legal and financial considerations. Key components include selecting the acquisition vehicle, determining post-closing organizational structure, and establishing payment methods, provisions, and tax implications (DePamphilis 2018).

To analyze risks, acquirer companies perform due diligence. This involves reviewing the information available for the acquired company to assess the levels of risk present in the operation and implement them in the post-merger integration planning. According to (Wangerin 2019), the process typically unfolds in three phases: preliminary due diligence, where publicly available information is reviewed; detailed due diligence, which involves a deeper examination of financial records, operational details, and legal matters; and final due diligence, focusing on verifying all aspects before concluding the transaction.

Risks present in this phase are mainly related to the correct identification of post-merger risk factors, as well as overvaluation risk (Welch et al. 2020). These risks are affected by the availability of information and the price of the deal. To mitigate such risks, due diligence duration tends to increase directly in proportion to the price of the deal, but inversely regarding the availability of information (Daley et al. 2024). However, there is a relationship between due diligence duration and the probability of a deal failure, such that a longer duration increases the probability of fail. In this regard, good dealers aim to complete transactions swiftly, typically within six months, to reduce the risk of information leaks and uncertainty among stakeholders (DePamphilis 2018).

Research shows that the main factor mitigating overvaluation and identification risks is the integration of technological advances over the due diligence process (Florackis et al. 2022; Gu et al. 2022). Technological advances have reduced overvaluation risks by enhancing the accuracy and transparency of financial reporting and compliance processes (Gu et al. 2022). However, this shift to digital processes introduces significant cyber risks, including potential data breaches and unauthorized access. Ensuring the security of sensitive information in this virtual environment requires the implementation of stringent cybersecurity measures to mitigate these risks and maintain the integrity of the due diligence process (Florackis et al. 2022).

2.1.3. Post-Merger Performance and Control

In the final stage of the M&A process, firms execute post-merger integration and evaluation. Integration focuses on merging the acquired company with the acquiring organization, addressing alignment, system integration, and cultural harmonization to realize synergies and efficiencies (DePamphilis 2018). Following this, the evaluation phase assesses the acquisition’s performance against its initial goals by analyzing financial outcomes, operational effectiveness, and strategic benefits. In this stage, achieving synergies is essential for realizing the value from the merger or acquisition. Evidence of synergies includes observable outcomes such as increased revenues, reduced costs, and improved operational efficiencies that exceed the individual performance of the firms (Feldman and Hernandez 2022). Additionally, positive abnormal stock returns and enhanced accounting profits following the merger can signal that synergies are being effectively realized.

Hence, significant risks include litigation and market reaction risks. Litigation risks arise from the performance measures established during the deal phase, such as EBITDA or net sales, which are used to track and verify the target’s performance. If these measures are informative yet subjective, disputes over performance assessments may occur, leading to potential litigation if former shareholders suspect manipulation (Huang et al. 2023). Additionally, the clarity and verifiability of these metrics are crucial for the accurate valuation of earnouts (Battauz et al. 2021), contractual provisions in M&A agreements that tie a portion of the purchase price to the future performance of the acquired business. Poorly defined measures can result in conflicts between buyers and sellers over payments and overall performance satisfaction (Dahlen et al. 2024). Market reaction risks involve the potential for the market to overvalue or undervalue synergies and the firm, which can ultimately affect the success of the M&A (Song et al. 2021).

To mitigate these risks, firms implement tighter controls when assessing performance (Dahlen et al. 2024) and attempt to reduce information asymmetry. One effective strategy is cross-listing, which enhances transparency and aligns performance metrics with more stringent market standards, thereby reducing the likelihood of disputes and ensuring more accurate market assessments of the deal’s value (Huang et al. 2023; Song et al. 2021).

Table 1 summarizes the M&A process, the risks associated with each phase, and mitigation strategies used by firms, according to the literature:

Table 1.

Phases, associated risks, and mitigation strategies in the M&A process, according to the literature. Source: Author.

3. Methodology

The present article employs a literature review as the methodology for research. A literature review is a research method that involves systematically collecting, analyzing, and synthesizing existing studies on a specific topic to build a comprehensive understanding of the subject. A literature review is essential for integrating findings from various studies, which enables researchers to address research questions with a depth and breadth that single studies alone cannot achieve (Page et al. 2021; Snyder 2019). This method provides a solid foundation for advancing knowledge and facilitating theory development.

On these grounds, a semi-systematic review approach has been employed to synthesize the existing literature on the topic. Unlike comprehensive reviews that aim to encompass all published works, a semi-systematic review focuses on integrating diverse perspectives rather than exhaustively covering every study. As Snyder (2019) stated, this approach is particularly valuable when the goal is to combine various viewpoints and provide a comprehensive overview of a specific issue or research problem.

The semi-systematic review involves a structured approach to selecting and analyzing relevant studies to map the research field, synthesize current knowledge, and lay the groundwork for future research (Snyder 2019). This method aligns well with the main objective of this study: to identify and discuss the risk factors associated with merger and acquisition transactions as presented in the recent academic literature.

3.1. Database and Searching Strategy

The literature used in this review was extracted from the Web of Science (WoS) database. This database serves as an efficient and reliable source of academic research. A research strategy was developed to refine the literature considered for review.

The time frame selected for this review, spanning from 2020 to 2024, was chosen to include recent research that reflects current methodologies, theoretical advancements, and trends in mergers and acquisitions. Although there may be publication delays, this period encompasses the most recent academic discourse and evolving perspectives on M&A risks. By focusing on recent publications, we aim to capture how contemporary scholars are interpreting and responding to M&A risks in light of the most current economic, political, and technological environments.

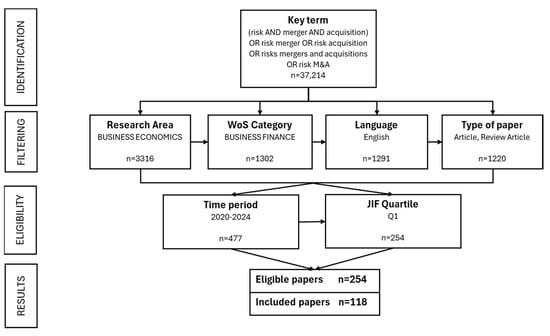

Initial filtering (Figure 1) was made by narrowing to the specific timeframe and key terms related to the topic: risks in mergers and acquisitions. The search yielded a total of 478 papers that fit into the search terms. Subsequent filtering was made using the impact factor of the journals (JIF) from which articles were published, as a proxy for paper quality (Mingers and Yang 2017). From this, a total of 254 papers were eligible for this review.

Figure 1.

Analysis filtering, adapted from Page et al. (2021).

3.2. Data Refining and Analysis

A final filtering was guided by analyzing author keywords to assess the validity of studies that passed earlier filters, ensuring only relevant papers on M&A risks were included. Initially, abstracts and contents of papers were reviewed to confirm their relevance. Abstracts, providing concise summaries of research, allowed for a quick assessment of each paper’s focus. Papers that did not include the key terms, used them in unrelated contexts, or were thematically irrelevant were manually excluded to ensure the final selection focused specifically on M&A risks.

A total of 118 papers were included in this review. For these papers’ keywords, a co-occurrence analysis was performed to identify thematic areas in the M&A risks literature. The subsequent section of this paper delves into the primary themes identified in the literature concerning risks associated with mergers and acquisitions. This analysis synthesizes the key topics and issues explored across various studies, highlighting the predominant concerns and findings related to M&A risks.

4. Findings

This section offers a detailed overview of the principal themes found within the reviewed literature regarding risks in mergers and acquisitions.

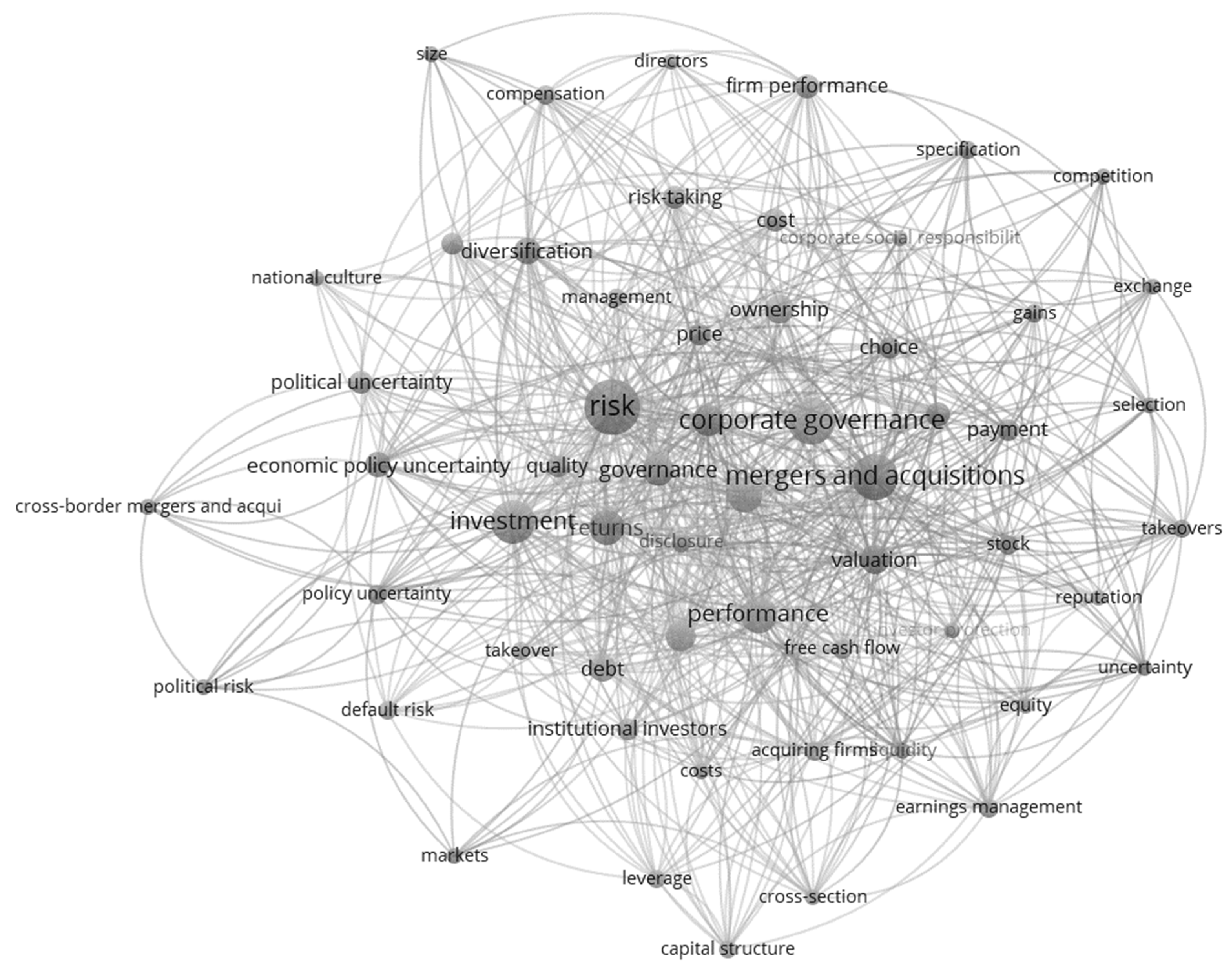

4.1. Keyword Co-Occurrence Analysis

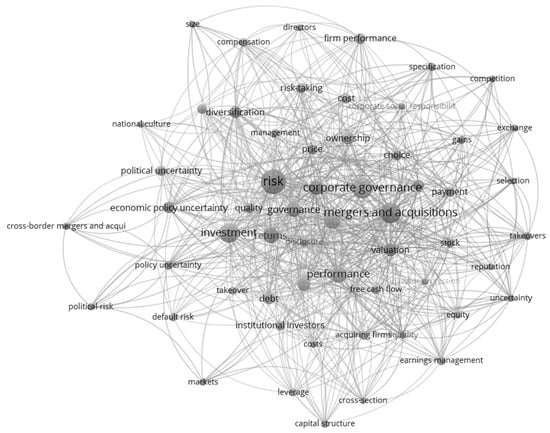

A keyword co-occurrence analysis was performed using VOSviewer version 1.6.20 to identify thematic areas to focus on the review (Figure 2).

Figure 2.

Co-occurrence author keywords projection in VOSviewer. Source: Authors.

This approach involves examining the frequency with which keywords appear together in the literature to identify significant patterns and relationships. We applied a threshold criterion of an occurrence count of four, meaning that only keywords appearing at least four times in the reviewed texts were considered for further analysis. Out of an initial pool of 699 keywords, 58 keywords met this threshold and were included in the final analysis. A total of four clusters were identified, from which a review of each was conducted. Table 2 summarizes each cluster and the key terms in order of most to least occurrence.

Table 2.

Clusters, key terms, and main themes of the co-occurrence analysis. Source: Authors.

Clusters can be classified into four main themes regarding risks in M&A operations. The first main theme is related to performance and reputational risks, with key terms such as “corporate governance”, “performance”, “corporate social responsibility (CSR)”, and “reputation” directly related to performance and reputational risks. Second is the theme of information asymmetry risks, with the terms “information”, “information asymmetry”, “uncertainty”, and elements associated with information asymmetry risks such as “valuation”, “payment”, “gains”, or “price”. The third main theme is investor protection with the key terms “investment”, “investor protection”, or “cost” and associated terms such as “firm performance”, “risk taking”, “compensation”, and “disclosure”. The final theme revolves around geopolitical risks, with the terms “economic policy uncertainty”, “policy uncertainty”, “cross-border mergers and acquisitions”, and related terms such as “diversification”, “markets”, or “size”.

The subsequent subsections offer a comprehensive analysis of each identified theme. For each theme, the discussion includes a definition of risks, the associated impacts, and mitigation strategies, all derived from the studies incorporated into the analysis.

4.2. Geopolitical Risks

Geopolitical risks refer to the potential threats and uncertainties that arise from political instability and conflicts on a global scale, influencing economic and financial systems. First highlighted in the International Monetary Fund’s 2014 reports, GPR has become increasingly significant with events like the COVID-19 pandemic, military coups, regional conflicts, and rising terrorism (Shen et al. 2021). Political risks have become more pronounced in recent years due to heightened uncertainty stemming from key elections and political events, where contrasting policy agendas on critical issues have intensified concerns about future economic stability (Choi et al. 2022). These risks shape the macro conditions of a financial market, impacting government policies, investor confidence, and firm behaviors (Ott 2020).

Political risks can lead to uncertainty in firm valuations by reducing market attractiveness and increasing information asymmetry. When national economic policies are highly uncertain, firms tend to take precautions by reducing investments, hiring, and M&A transactions (Jeon et al. 2022). Elevated geopolitical risks often result in weaker regulatory enforcement and less transparent economic transactions, which fuels investor disagreement and complicates decision-making, increasing risks of litigation (Du and Zhang 2024). In such environments, there is often an increase in information asymmetry, where relevant financial and operational data may not be as readily available or reliable (Makrychoriti and Pyrgiotakis 2024).

Geopolitical risks have a pronounced impact on cross-border mergers and acquisitions, influencing not only the strategic considerations but also the structural and operational aspects of these transactions (Shen et al. 2021). The presence of geopolitical risks primarily influences the direction and volume of cross-border M&A activities. The increase in geopolitical risks heightens the probability of scenarios that could significantly negatively impact investors’ wealth. Such scenarios range from sudden regulatory changes to economic sanctions, or even the expropriation of assets (Du and Zhang 2024). As a result, investors may become more risk-averse and hesitant to commit capital to the home country, perceiving it as an unstable or unreliable market (Zhang et al. 2021). Consequently, the number of inbound M&A transactions tends to decline, as foreign investors seek safer, more stable environments for their investments (Ahsan et al. 2024). In the context of outbound mergers, the response by domestic corporations is observed to be inverse. Contrasting to the decline in inbound M&A transactions during periods of heightened geopolitical risks, outbound M&A activity from such countries often faces an increase (Paudyal et al. 2021). In summary, the increase in geopolitical risks has a direct relation on outbound M&As and an inverse relation on inbound or domestic M&As (Li et al. 2021)

These risks impact other aspects of M&As as well, such as competition, costs, and the structure of deals. Research has shown that differences in formal institutions between the acquirer and target countries can significantly influence the level of competition for M&A deals (Ahsan et al. 2024). Specifically, variations in regulatory frameworks, transparency, and the enforcement of legal protections can either attract or deter potential acquirers (Balachandran et al. 2020; Du and Zhang 2024). The presence of clear regulations and reliable legal systems reduces uncertainties, thereby increasing the attractiveness of the target market to a broader range of investors.

Conversely, high political risks lead to increased equity costs as investors demand higher returns to compensate for the volatility and uncertainty, deterring cross-border acquisitions. This results in higher premiums for target firms to offset the perceived risks, creating a geopolitical risk premium that affects both the valuation and cost of acquisitions (Paudyal et al. 2021). However, the literature indicates that the overall effects of geopolitical risks are multifaceted. While geopolitical risks in home countries can have negative implications, they simultaneously create incentives for outbound mergers and acquisitions (Li et al. 2021).

The literature shows that firms employ several mechanisms to mitigate the impact of these risks. Geographical diversification through acquisitions is a widely used strategy to manage risks and reduce exposure to domestic uncertainties (Ahsan et al. 2024). By investing in foreign markets, firms can mitigate the policy uncertainties present in their home countries, effectively using outbound M&A activities as a hedging mechanism against domestic geopolitical risks (Paudyal et al. 2021). As noted by Argimón and Rodríguez-Moreno (2022), firms with operations spread across multiple regions are better able to handle geopolitical risks by minimizing the impact of political instability in any single location. In high-risk environments, companies may adopt more aggressive long-term investment strategies, such as mergers and acquisitions, to capitalize on potential synergies (Shen et al. 2021). Additionally, firms with a significant number of equity analysts and reports often increase their diversification efforts during periods of high economic policy uncertainty (EPU), which helps mitigate associated risks and improve overall performance (Hoang et al. 2021).

Managers may adjust financial policies, such as reducing dividends or increasing voluntary disclosures, to enhance transparency (Jeon et al. 2022). However, these measures can have mixed effects, as increased disclosures might heighten information asymmetry and lead to agency issues, especially if managers withhold unfavorable information when firm valuation is challenging (Makrychoriti and Pyrgiotakis 2024). Institutional investors play a vital role in this process by actively participating in corporate governance, influencing decisions on executive compensation, corporate payouts, mergers, and financial leverage. Their involvement helps reduce information asymmetry and lowers geopolitical risks by facilitating better information production (Choi et al. 2022).

Research shows as well that ESG factors can become a mitigating factor for political risk. For instance, to manage political and reputational risks, banks often enhance their ESG scores during periods of high economic policy uncertainty by increasing their commitment to environmental, social, and governance practices (Alam et al. 2024). This strategic response aims to strengthen stakeholder relationships and improve public image, thereby mitigating the potential negative impacts of political instability and economic unpredictability and reinforcing corporate social responsibility. Additionally, political donations and CSR initiatives can help neutralize the adverse effects of political exposure and risk (Choi et al. 2022).

Table 3 summarizes what has been discussed in the literature reviewed regarding geopolitical risks:

Table 3.

Review on geopolitical risks. Source: Author.

4.3. Information Asymmetry Risks

Information asymmetry refers to the differences in information held by stock market investors and the managers of an acquiring firm. These disparities can significantly impact the outcome of a transaction, influencing elements such as pricing, interests, and other related factors (Song et al. 2021). In economic transactions, the information available to the parties involved is often unequal, which can lead to imbalances in decision-making and negotiation. In the context of M&As, information asymmetry is particularly pertinent when firms from different industries merge. The distinct knowledge each firm has about its respective industry can create challenges in integrating their operations. This divergence in industry-specific expertise and techniques may complicate the process of merging activities, potentially impeding the achievement of the synergies typically expected from an M&A transaction (Huang and Xie 2023). Additionally, if the market’s assessment is incomplete at the time of the M&A announcement, the acquirer’s management may miss out on valuable insights from market prices regarding the deal’s synergy potential and its likelihood of completion (Barbopoulos et al. 2020).

Information asymmetry in economic transactions arises from several key factors. These include the hierarchical structure of infrastructural organizations, potential miscommunication within dealership chains, disparities in information among agents, the impact of electronic and automated trading tools, political uncertainties (Makrychoriti and Pyrgiotakis 2024), and temporal heterogeneity (Swem 2022) in market activities. These elements create risks by leading to imbalances in information between parties involved in a transaction. Table 4 summarizes each source of these risks (Ranaldo and Somogyi 2021).

Table 4.

Sources of information asymmetry, adapted from (Ranaldo and Somogyi 2021).

Asymmetry significantly affects various aspects of the operation, particularly the alignment between initial stock market reactions to M&A announcements and subsequent post-M&A performance. While a positive alignment between market reactions and post-acquisition outcomes is generally expected, this alignment is predicted to weaken in the presence of high information asymmetry (Buehlmaier and Zechner 2020). This is often attributed to the target company’s opacity to investors or the acquirer’s operation in a less-developed financial market with a weak information environment. As a result, one party may hold a privileged position due to access to more precise information, creating a disparity and weakening the other party’s position.

Research indicates that companies with higher information asymmetry are more likely to engage in M&A transactions and tend to generate higher excess returns. This phenomenon also influences their financing preferences; such companies typically prefer internal financing over external sources and encounter more significant financial constraints compared to firms with lower information asymmetry. Additionally, firms with high information asymmetry and financial constraints often benefit more from M&A transactions, ultimately achieving greater excess returns (Ranaldo and Somogyi 2021).

One of the key aspects influenced by information asymmetry is the valuation of firms. Information asymmetry often results in misvaluation, where the target firm may be overvalued due to the unequal distribution of information between the involved parties (Welch et al. 2020). This misvaluation is particularly evident in firms with low analyst coverage, as the lack of extensive external analysis and oversight leads to greater discrepancies in valuation. In contrast, firms that are followed by a large number of analysts tend to be less overvalued, as the extensive scrutiny and broader availability of information help reduce the effects of information asymmetry, leading to a more accurate assessment of the firm’s true value (Li 2020).

To mitigate these risks, firms typically employ several measures. These measures include conducting rigorous due diligence to ensure comprehensive and transparent disclosure of pertinent information by all parties involved. The involvement of neutral third parties, such as auditors, legal experts, and independent consultants, is also crucial for providing essential oversight and identifying and addressing any potential abuses or discrepancies related to information asymmetry. Furthermore, firms that find themselves in a weaker informational position should develop a robust corporate governance body and risk management plan to proactively address and mitigate potential issues arising from information asymmetry (Balachandran et al. 2020).

The advent of digital finance has significantly influenced mergers and acquisitions (M&As) by altering the dynamics of information asymmetry. M&A transactions are inherently complex and fraught with risks, necessitating robust support from both internal and external factors for successful outcomes. The integration of digital technology with financial services, known as digital finance, has improved financial operations’ efficiency and made financial information more transparent and accessible, thereby reducing information opacity (Peng et al. 2024; Xue 2024). Companies implementing technologies such as blockchain are able to mitigate the risks associated with information asymmetry in M&A transactions, thereby potentially improving the overall effectiveness and success rates of these complex investment activities.

Studies suggest that digital finance is positively correlated with enterprise M&A activities, with a more pronounced effect during the growth and maturity stages of a company’s development. In these phases, firms seek to expand investments to capture market share, and digital finance can enhance financial services, thereby supporting more informed and strategic M&A decisions. Consequently, this improved access to financial data is expected to positively influence enterprise performance through M&As (Peng et al. 2024). However, the widespread adoption of digital platforms can also exacerbate information asymmetry. While digital finance provides access to vast amounts of data, this can create a disparity if one party is less equipped to manage or utilize the information effectively. Thus, despite the overall potential for digital finance to reduce information asymmetry by increasing transparency, it can simultaneously create new imbalances if the involved parties have unequal access to or control over digital resources (Huang and Xie 2023).

Political institutions mitigate information asymmetry through the implementation and enforcement of regulations, including disclosure requirements and reporting standards, which compel firms to provide accurate and comprehensive information to stakeholders (Liu et al. 2024). CSR reporting further addresses information asymmetry by offering detailed and transparent information, thereby narrowing the gap between management and investors (Hickman 2019). Regulatory bodies are essential in this process, as they mandate CSR disclosures and other reporting requirements to enhance transparency and reduce information imbalances.

Table 5 summarizes information asymmetry risks:

Table 5.

Information asymmetry risk literature review. Source: Author.

The existing literature examines the impact of knowledge spillovers on firm behavior in the M&A market, suggesting that these spillovers may drive M&A activity at the industry level and influence vertical mergers linked by product connections. Further investigation is needed to understand the trade-offs between acquiring new knowledge through M&A and internalizing it through increased research and development and innovation, as well as the conditions that favor one approach over the other (Huang and Xie 2023). Cybersecurity is another critical area for future research, given its increasing importance due to rapid technological advancements and emerging risks. Recent studies propose a transparent and implementable measure for assessing cybersecurity risks in firms, enabling systematic analysis of these risks and their impact on firm value, corporate policies, and operations, thereby identifying new research opportunities (Florackis et al. 2022).

On these grounds, future research on knowledge spillovers in M&A and cybersecurity risks can benefit from qualitative research and longitudinal studies. Qualitative methods, such as case studies and interviews, can provide deep insights into how firms manage knowledge acquisition and cybersecurity threats in practice, offering detailed understanding of specific strategies and challenges. Longitudinal studies can track changes and impacts over time, revealing long-term effects of knowledge spillovers and cybersecurity practices on firm performance and strategy. These approaches together help in understanding dynamic processes and evolving responses in these critical areas.

4.4. Investor Protection and Litigation Risks

Investor protection encompasses the available mechanisms to address potential disagreements and protect their position in financial operations. More specifically, litigation risks refer to the potential for legal challenges that a firm may face, including disputes arising from shareholder lawsuits, regulatory non-compliance, or contractual disagreements (Wang and Zhang 2024). Shareholder litigation risk involves the threat of legal action by shareholders against a company’s management or board, especially in the context of mergers and acquisitions. Litigation risks are particularly high in industries such as technology, service, pharmaceutical/chemical, and financial due to their complex regulatory environments and frequent disputes over intellectual property, contracts, and compliance (Dahlen et al. 2024).

This type of risk is significant as it influences to a great extent a firm’s decisions regarding external growth strategies, such as M&As and alliances (Huang et al. 2023). Legal challenges in M&As can arise from allegations of breaches of fiduciary duty, inadequate disclosures, or other conflicts, potentially impacting the strategic choices and financial outcomes of the transactions.

Litigation risks in M&As often emerge due to information asymmetries. Although initial information may be equally accessible to both the buyer and the seller, disputes can arise later. One source of risk is the potential mistrust of the accounting reports provided by the buyer, as sellers may suspect that these figures have been manipulated through earnings management to decrease the earnout payment. Another risk arises when the target company’s performance does not meet expectations; in such cases, sellers may struggle to determine whether the underperformance is due to inadequate effort by the buyer in managing the business or if it reflects the sellers’ own overestimation of the company’s future profitability (Huang et al. 2023). These factors contribute to the potential for legal disputes in earnout agreements.

Additionally, litigation risks often emerge in unstable political environments where regulatory unpredictability and policy shifts create conditions conducive to disputes. Political instability can exacerbate these risks by fostering an environment where legal protections and enforcement mechanisms are inconsistent or unreliable (Du and Zhang 2024). Consequently, patterns of litigation can serve as a barometer for assessing a country’s political stability and investment climate, providing valuable insights into how political risks translate into legal challenges.

One of the major sources of litigation risks are earnouts. Earnouts are contractual provisions in mergers and acquisitions where the purchase price is partly contingent on the future performance of the target company. Litigation risks arise from the reliance on accounting figures to determine performance metrics, which can be subject to earnings management and manipulation. The inherent subjectivity and flexibility in accounting practices can create discrepancies between the reported and actual performance of the target company. These difficulties in performance verification, coupled with potential disputes over the accuracy of reported metrics, can lead to legal action if the former shareholders believe that the acquirer has not adhered to the earnout terms or has misrepresented performance (Dahlen et al. 2024).

Shareholder lawsuits can impose significant costs on managers and their companies, both financially and reputationally. These legal challenges can result in direct monetary losses and damage to the company’s public image. Additionally, directors may face personal social embarrassment from being involved in such litigation. Due to these risks, managers might become more risk averse and cautious in their decision-making (Huang et al. 2023). Consequently, the threat of shareholder lawsuits can influence managers to pursue less risky strategies, as they seek to mitigate the potential for legal and reputational damage. Studies suggest that these concerns can distort managers’ incentives, reducing their inclination to engage in high-risk projects (Dong and Doukas 2021).

Litigation risks impact both the volume and the means of payment in M&As. When litigation risks are high, they can reduce the overall volume of M&A deals as firms become more cautious and selective about potential transactions. Companies may shy away from complex or contentious deals, such as those involving high-tech industries or high-value targets, due to the increased likelihood of disputes and legal challenges (Dahlen et al. 2024). Regarding the means of payment, managers may structure deals with lower contingent payments or incorporating more conservative earnout provisions. These measures are designed to mitigate the potential for future performance-related disputes and the associated legal expenses. This approach parallels the strategy observed in initial public offerings (IPOs), where underpricing is employed as a safeguard against litigation risks.

Litigation risks affect valuation as well. According to Imperatore et al. (2024), when the risk of litigation is high, firms may lower their valuations to mitigate disputes over transaction prices, which often occur when shareholders perceive the price as inadequate. To avoid such litigation, valuations may be adjusted downward, aligning the takeover price with the upper end of what is considered fair to the shareholders.

Companies mitigate litigation risks in mergers and acquisitions through several key mechanisms. They often accumulate substantial cash reserves to cover potential legal costs and settlements, ensuring operational stability amidst unforeseen expenses (Klitzka et al. 2022). Additionally, firms may incorporate specific contractual terms, such as indemnity clauses and arbitration provisions, to manage and limit legal exposure (Wilson 2020). Indemnity clauses can allocate the risk of certain liabilities to one party, protecting the other from unforeseen legal issues arising post-deal. Arbitration provisions, on the other hand, provide a framework for resolving disputes outside of traditional court proceedings, which can be faster and less costly. Furthermore, firms might seek specialized insurance products, such as litigation risk insurance, to provide additional financial protection against potential legal disputes (DePamphilis 2018; Even-Tov et al. 2022).

CSR and corporate governance can serve as mitigators of litigation risks, especially in the context of earnout agreements. Research indicates that firms with robust enterprise risk management frameworks are more inclined to engage in CSR activities, which can help reduce litigation risks improving transparency and stakeholder trust (Kuo et al. 2021). When a firm actively practices CSR, it demonstrates a commitment to ethical business practices and transparency, which helps build trust with stakeholders, including shareholders, employees, and regulators. This trust reduces the likelihood of disputes and litigation, as stakeholders are more likely to believe that the company is acting in good faith and adhering to fair practices. Moreover, robust corporate governance structures ensure that the firm’s management is accountable and that there are mechanisms in place to address and resolve potential conflicts.

Table 6 summarizes the definition, sources, effects, and mitigation strategies of litigation risks.

Table 6.

Litigation risks according to the literature. Source: Author.

Future research in litigation risks and deal valuations should address several key areas according to the recent literature. First, there is a need to refine valuation methods for earnouts, moving beyond basic option-pricing models to more sophisticated approaches that account for the complex nature of these contracts (Dahlen et al. 2024). Additionally, Future research in litigation risks and M&A activity should focus on the underexplored impact of regulatory and technological advances on these domains (Gu et al. 2022). Case studies of recent regulatory reforms and technological advancements can provide insights into their concrete effects on litigation risks.

4.5. Performance and Reputational Risks

Reputational risks refer to the potential negative consequences that a company may face due to damage to its corporate reputation. Corporate reputation is a fundamental and multifaceted concept that encompasses the public image and perception of a company by its stakeholders, including customers, investors, employees, and the general public (Maung et al. 2020). It is shaped by a company’s internal and external actions, encompassing intangible aspects such as ethics, morality, honesty, and overall corporate image. The management and measurement of corporate reputation are crucial, as it represents a vital source of value for the company. A strong reputation can confer significant competitive advantages in a market characterized by increasingly homogeneous products and services. Reputational risks, therefore, involve any threats to a company’s credibility and ethical behavior, including its commitment to corporate social responsibility and environmental, social, and governance criteria (D’Souza et al. 2024). ESG criteria are crucial for guiding companies towards sustainability while optimizing long-term financial performance. By adopting ESG principles, companies not only comply with future regulations and mitigate risks but also showcase their commitment to sustainability and corporate ethics. The integration of ESG practices is becoming a fundamental aspect of business strategy and culture across various industries.

Corporate reputation has become increasingly critical in today’s business environment due to the rise of advanced technologies and heightened transparency. Mandas et al. (2024) note that new tools now integrate numerical and textual data, providing comprehensive indexes that make it easier for stakeholders to assess a company’s non-financial performance. Additionally, Boone and Uysal (2020) emphasize that reputational risks are less susceptible to information asymmetry, as environmental rankings and reputational changes are quickly and widely disseminated through media, allowing stakeholders to react promptly.

Stemming from reputation, business credibility refers to a company’s ability to inspire confidence among its consumers regarding the quality and reliability of its products or services. This credibility is established through consistently meeting customer expectations and ensuring complete satisfaction (Tampakoudis and Anagnostopoulou 2020). It is an invaluable asset for any company aiming to maintain a strong reputation and attract and retain customers. To build and sustain credibility, a company must consistently deliver on its promises, provide high-quality products and services, maintain transparency, implement corporate social responsibility practices, and offer excellent customer service.

In the context of M&A, reputation risks impact several aspects of operations. Firstly, the presence of such risks significantly affects the likelihood of firms engaging in M&A activities, as firms with poor environmental reputations or past social irresponsibility incidents are less likely to be acquirers or targets. This is due to the fact that negative reputations are persistent and difficult to change, making such firms unattractive for M&As (Boone and Uysal 2020). Acquiring a company with a poor reputation can result in financial losses and damage to the acquirer’s own standing, as reputational risks from social irresponsibility incidents can be transferred from the acquirer to the merged firm (D’Souza et al. 2024).

Moreover, a firm’s ethical behavior and reputation are particularly important in M&A transactions due to the additional complexities, information asymmetry, and heightened risks associated with these deals. Firms with high CSR activities, especially those with poor governance, are more likely to use cash instead of stock for acquisitions, reflecting concerns about overvaluation and reputational risks tied to their social responsibility actions (Vo et al. 2024). Note that increasing CSR efforts without tacking the specific sources of reputational risk might worsen the negative impact of carbon risk (Bose et al. 2021), particularly under stringent carbon regulations. Investors often react adversely to high carbon emissions from CSR-focused firms, especially in countries with stringent environmental protections.

Reputational risks do not only affect the firm’s investment attractiveness but also the conditions of deals. Research shows that acquiring firms with high levels of corporate social responsibility tend to prefer cash payments over stock payments, particularly when they have poor corporate governance (Vo et al. 2024). This preference likely stems from the need to manage reputational risks and avoid overvaluation associated with excessive CSR activities. When governance is weak, firms may opt for cash to signal financial strength and reduce the potential negative impact on shareholder value that could arise from issuing potentially overvalued stock. Furthermore, the time frame of deal completion is affected as well. Firms are generally less likely to pursue acquisitions after experiencing an environmental or social incident, as such incidents can damage their reputation and increase the perceived risks of further expansion. However, this reluctance to acquire is influenced by the cost of delaying the acquisition. If delaying the deal could result in significant financial or strategic losses, firms might still proceed with the acquisition despite the reputational damage, weighing the costs of delay against the potential risks (D’Souza et al. 2024).

To mitigate reputational risks, companies may use diverse strategies. On one hand, firms can deliberately leverage dual holders, individuals or entities that hold both equity and debt in a firm (Nguyen et al. 2023). Dual holders benefit from both cash flow and control rights, allowing them to enforce greater oversight and accountability. By aligning their interests with the firm’s performance and ensuring rigorous managerial monitoring, dual holders can effectively address agency problems and enhance the firm’s overall governance structure. On the other hand, firms can strengthen their governance structures to ensure that CSR activities are balanced and well-managed. Enhancing governance through increased disclosure requirements helps mitigate potential reputational risks. In countries with strong political institutions, stricter disclosure requirements are usually enforced, reducing agency conflicts and minimizing the risk of reputational damage (Balachandran et al. 2020).

A prevention strategy followed by acquirer companies is to search for targets with similar reputation (Boone and Uysal 2020). By aligning with targets that share comparable CSR values and face similar reputational challenges, acquirers can leverage their existing knowledge and strategies to address these concerns. This familiarity allows the acquiring firm to more seamlessly integrate the target company, align policies, and manage potential risks associated with the merger.

Companies are increasingly adopting comprehensive strategies to integrate ESG principles into their organizational culture. These strategies include establishing a dedicated CSR committee, and fostering a CSR-focused culture further boosts competitive advantage and efficiency in M&A transactions (Li et al. 2023). Additionally, improving financial reporting quality and stakeholder orientation enhances firm value and reduces acquisition premiums for cross-border deals by better managing reputational risks and achieving successful M&A outcomes (Maung et al. 2020; Ni 2020). Leadership plays a crucial role, as a strong commitment from top executives is essential for driving the ESG agenda forward. Confident CEOs who actively engage in CSR initiatives and hold significant shares in their firms are more likely to drive robust CSR activities (Kuo et al. 2021). Their strong commitment reduces the impact of overall risks on CSR efforts, aligns personal and corporate interests, and enhances the effectiveness of CSR practices. Effective corporate governance further supports this convergence of CSR practices, ensuring that CSR efforts are integrated into the firm’s strategy.

Table 7 summarizes academic discussion regarding reputational risks.

Table 7.

Reputational risk management according to the literature. Source: Author.

The recent literature underscores the necessity for in-depth research into how reputational risks affect post-merger performance. A pertinent area of investigation is whether the transfer of reputation from the acquired to the acquiring firm influences market performance or operational outcomes following the acquisition (Maung et al. 2020). Additionally, future research could delve into how market-imposed sanctions, such as increased acquisition costs, function as deterrents against environmental and social violations. Specifically, it should examine the impact of financial penalties on corporate behavior and decision-making in response to failing to meet ESG standards. Studying how such sanctions influence the attractiveness of firms in M&A transactions could shed light on the broader role of regulators on corporate strategy and sustainability (Bose et al. 2021).

4.6. Aggregate Analysis of Key Areas

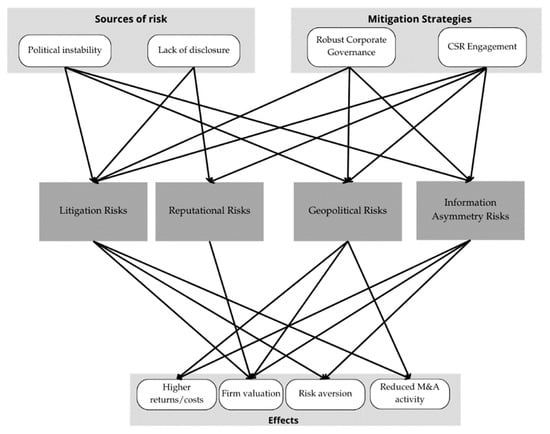

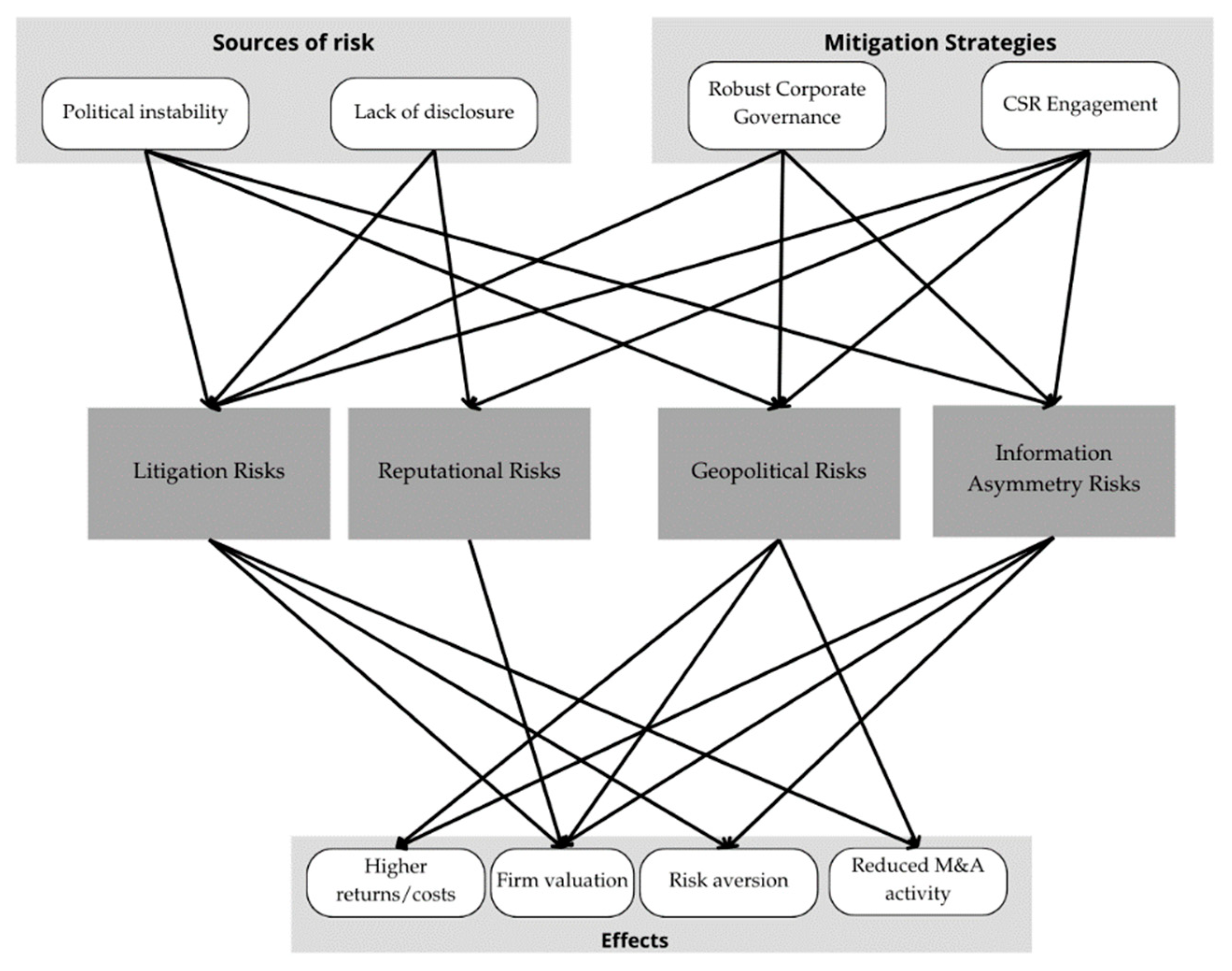

The analysis of various risk types reveals a complex web of interconnectedness that highlights the multifaceted nature of risk management in contemporary business environments, especially in the context of M&As. Based on the reviewed literature, these risks are connected in terms of the sources of risk, the impacts on M&A aspects, or the mitigation strategies followed by companies. Figure 3 addresses the main relationships depicted in the literature in an aggregated way.

Figure 3.

Risk relationships by source, mitigation strategy, and effect. Source: author.

In terms of sources, political uncertainty is presented as a common main source for geopolitical (Du and Zhang 2024; Paudyal et al. 2021), litigation (Huang et al. 2023; Dahlen et al. 2024), and information asymmetry risks (Makrychoriti and Pyrgiotakis 2024; Ranaldo and Somogyi 2021). Policymakers play a major role in mitigating these risks through the enforcement of laws. For instance, political institutions can shape regulatory frameworks, thereby affecting the likelihood and nature of litigation (Ahsan et al. 2024). Similarly, information asymmetry, concerning the unequal distribution of information among parties, can be exacerbated or mitigated by political conditions, impacting the transparency and trustworthiness of M&A transactions (Ranaldo and Somogyi 2021). Reputational risks are highly affected by transparency and disclosure (Vo et al. 2024; Balachandran et al. 2020; D’Souza et al. 2024). Therefore, the role of political actors in enabling a favorable setting for M&A transactions is crucial.

The main aspect of M&As that is affected by risks is valuation. Geopolitical risks, such as political instability and regulatory shifts, create valuation uncertainty and hinder cross-border transactions by increasing complexity and costs (Jeon et al. 2022; Makrychoriti and Pyrgiotakis 2024; Shen et al. 2021). Information asymmetry risks lead to greater M&A engagement but can also result in misvaluation of targets due to discrepancies between market perceptions and actual firm performance (Buehlmaier and Zechner 2020; Welch et al. 2020). Litigation risks, including shareholder lawsuits and regulatory non-compliance, contribute to reduced M&A volume and downward adjustments in firm valuations as firms become cautious about potential legal challenges (Dong and Doukas 2021; Imperatore et al. 2024). Reputational risks impact investment attractiveness and can lead to financial losses for acquirers by diminishing the perceived value of target companies (Boone and Uysal 2020; Bose et al. 2021).

In terms of mitigation strategies, the literature focuses on solid corporate governance as a mitigator. By enhancing ESG scores and adopting robust governance frameworks, firms can better navigate geopolitical uncertainties and political instability, thus reducing valuation uncertainty and attracting stable investments (Ahsan et al. 2024; Choi et al. 2022). Comprehensive risk management and transparency address information risks, ensuring accurate valuations and smoother M&A integration (Balachandran et al. 2020). Strengthening governance structures and risk management practices also help manage litigation risks by ensuring compliance and reducing potential legal challenges (Klitzka et al. 2022). Furthermore, improved disclosure and ESG strategies mitigate reputational risks by safeguarding the company’s image and attracting investment (Nguyen et al. 2023).

Rapid advancement of digital technologies has amplified these interconnections. Digital innovations not only increase the speed and complexity of transactions but also introduce new dimensions of risk, such as cybersecurity concerns and data privacy issues, which can further complicate the assessment and management of traditional risks (Florackis et al. 2022). The disruption brought by new technologies generally contributes to reducing risks associated with information asymmetry. Advanced tools for information management can significantly impact both the valuation of companies and the equitable access to information by the target and acquiring firms, enhancing transparency. The recent literature has demonstrated that decreasing information asymmetry can mitigate litigation risks, as it reduces the necessity for extensive contracts aimed at strengthening the position of the acquiring firm (Dahlen et al. 2024).

In conclusion, this analysis reveals that geopolitical, information, litigation, and reputational risks are deeply interconnected and collectively impact M&A valuations. Political uncertainty influences these risks, highlighting the importance of robust corporate governance. Effective governance, through enhanced ESG practices and transparency, mitigates these risks, improves valuation accuracy, and fosters a stable investment climate.

5. Conclusions and Future Directions

The current study provides a comprehensive analysis of the risk factors associated with mergers and acquisitions, as explored in the recent academic literature. Utilizing a semi-systematic review of articles sourced from the Web of Science database on M&A risks, this study elucidates key findings. The analysis identifies four primary thematic areas of risk: (1) risks related to information asymmetry and the impact of emerging technologies; (2) issues concerning sustainability and corporate reputation; (3) litigation risks; and (4) risks emerging from the contemporary geopolitical landscape. Each theme is reviewed to provide a definition for each risk, the impacts of such, and mitigation strategies followed by companies.

The review of the literature reveals a significant main point: the interconnectedness of risks associated with M&As. The analysis demonstrates that litigation risk is intricately linked to political factors and information asymmetry, with each element influencing the others in a series of interdependencies regarding the sources of risk, the aspects of M&As that are affected, and mitigators. Thus, this elucidates how the contemporary M&A landscape is characterized by a heightened level of risk interdependence, requiring a more holistic and integrated approach to risk assessment and management. Additionally, findings highlight the importance of CSR for risk mitigation. Ultimately, effective CSR initiatives can lead to more stable and resilient M&A outcomes by fostering a positive corporate image and aligning business practices with broader societal expectations.

This study contributes to the field of M&A risk management by providing aggregated analysis of relevant risks in M&A operations based on the recent literature. It highlights the need for integrated risk management strategies and robust governance frameworks to navigate the complexities of modern M&A transactions effectively.

Practical implications are diverse. For practitioners, it offers actionable insights on risk mitigation strategies. Efforts should be put into enhancing financial disclosure, developing robust ESG strategies, and strengthening corporate governance frameworks. Focus should also be placed on increasing institutional shareholder participation and leveraging dual holders. Implementing digital finance technologies such as blockchain can further strengthen risk management efforts. For policymakers, they should enforce stringent transparency and disclosure requirements and mandate robust legal and compliance standards. Additionally, they should incentivize firms to integrate ESG strategies and CSR practices by implementing penalties for non-compliance, which will further reduce risks associated with M&A transactions.

The authors acknowledge that a limitation of this study is the use of filters that focused primarily on business and finance literature in the WoS database, which may have excluded relevant studies from related disciplines, such as economics. Additionally, the chosen time frame might have missed significant contemporary developments in the field. Future reviews could address these limitations by incorporating other databases, include a broader range of disciplines, and extending the time frame to include more recent and relevant studies.

Future research should adopt longitudinal studies to track the evolving interconnectedness of M&A risks over time and conduct detailed case studies on corporate governance to identify best practices in managing these risks. Developing advanced valuation methods that integrate multiple risk factors and exploring the impact of emerging technologies, such as artificial intelligence and blockchain, on M&A risk dynamics are also crucial (Gu et al. 2022). Additionally, comparative analyses across different regions and industries will help identify diverse risk management strategies and trends.

Author Contributions

Conceptualization, M.G.-N., V.B.-R., J.M.R.-J. and R.F.-L.; methodology, M.G.-N., V.B.-R., J.M.R.-J. and R.F.-L.; formal analysis, M.G.-N., V.B.-R., J.M.R.-J. and R.F.-L.; investigation, M.G.-N., V.B.-R., J.M.R.-J. and R.F.-L.; writing—original draft preparation, M.G.-N., V.B.-R., J.M.R.-J. and R.F.-L.; writing—review and editing, M.G.-N., V.B.-R., J.M.R.-J. and R.F.-L. All authors have read and agreed to the published version of the manuscript.

Funding

This publication has been co-funded by the Consejería de Universidad, Investigación e Innovación de la Junta de Andalucía, within the framework of the research project SUBV. ProyExcel_00353 Call 2021. We also acknowledge the financial contribution of the research group of PAIDI SEJ-111 Universidad Pablo de Olavide- Junta de Andalucía.

Data Availability Statement

Data are available from authors upon reasonable request.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Ahsan, Faisal Mohammad, Manish Popli, and Vikas Kumar. 2024. Formal institutions and cross-border mergers and acquisitions: A systematic literature review and research agenda. International Business Review 33: 102306. [Google Scholar] [CrossRef]

- Alam, Ahmed W., M. Kabir Hassan, and Hasanul Banna. 2024. An empirical investigation of banks’ sustainability performance under economic policy uncertainty. Journal of Sustainable Finance and Investment 2024: 2309499. [Google Scholar] [CrossRef]

- Argimón, Isabel, and María Rodríguez-Moreno. 2022. Risk and control in complex banking groups. Journal of Banking and Finance 134: 106038. [Google Scholar] [CrossRef]

- Balachandran, Balasingham, Huu Nhan Duong, Hoang Luong, and Lily Nguyen. 2020. Does takeover activity affect stock price crash risk? Evidence from international M&A laws. Journal of Corporate Finance 64: 101697. [Google Scholar] [CrossRef]

- Barbopoulos, Leonidas G., Samer Adra, and Anthony Saunders. 2020. Macroeconomic News and Acquirer Returns in M&As: The Impact of Investor Alertness. Journal of Corporate Finance 64: 101583. [Google Scholar] [CrossRef]

- Battauz, Anna, Stefano Gatti, Annalisa Prencipe, and Luca Viarengo. 2021. Earnouts: The real value of disagreement in mergers and acquisitions. European Financial Management 27: 981–1024. [Google Scholar] [CrossRef]

- Bauer, Florian, and Martin Friesl. 2024. Synergy Evaluation in Mergers and Acquisitions: An Attention-Based View. Journal of Management Studies 61: 37–68. [Google Scholar] [CrossRef]

- Boone, Audra, and Vahap B. Uysal. 2020. Reputational concerns in the market for corporate control. Journal of Corporate Finance 61: 101399. [Google Scholar] [CrossRef]

- Bose, Sudipta, Kristina Minnick, and Syed Shams. 2021. Does carbon risk matter for corporate acquisition decisions? Journal of Corporate Finance 70: 102058. [Google Scholar] [CrossRef]

- Buehlmaier, Matthias M. M., and Josef Zechner. 2020. Financial Media, Price Discovery, and Merger Arbitrage. Review of Finance 25: rfaa037. [Google Scholar] [CrossRef]

- Choi, Wonseok, Chune Young Chung, and Kainan Wang. 2022. Firm-level political risk and corporate investment. Finance Research Letters 46: 102307. [Google Scholar] [CrossRef]

- Dahlen, Niklas, Alexander Lahmann, and Maximilian Schreiter. 2024. Panacea for M&A dealmaking? Investor perceptions of earnouts. Finance Research Letters 60: 104850. [Google Scholar] [CrossRef]

- Daley, Brendan, Thomas Geelen, and Brett Green. 2024. Due Diligence. The Journal of Finance 79: 2115–61. [Google Scholar] [CrossRef]

- Darbyshire, Madison, Nicholas Megaw, and James Fontanella-Khan. 2024. How the investment world is trying to navigate geopolitics. Financial Times. July 5. Available online: https://www.ft.com/content/23ce295d-bf65-47fd-bebd-808b5a7bcab5 (accessed on 4 August 2024).

- DePamphilis, Donald M. 2018. Mergers, Acquisitions, and Other Restructuring Activities: An Integrated Approach to Process, Tools, Cases and Solutions, 9th ed. Amsterdam and New York: Elsevier and Academic Press. [Google Scholar]

- Dong, Feng, and John Doukas. 2021. The effect of managers on M&As. Journal of Corporate Finance 68: 101934. [Google Scholar] [CrossRef]

- D’Souza, Reagan, Choy Yeing (Chloe) Ho, and Joey W. Yang. 2024. The cost of corporate social irresponsibility for acquirers. Journal of Banking and Finance 162: 107132. [Google Scholar] [CrossRef]

- Du, Julan, and Yifei Zhang. 2024. ISDS disputes, adjudication and cross-border M&As. Journal of Corporate Finance 87: 102594. [Google Scholar] [CrossRef]

- Even-Tov, Omri, James Ryans, and Steven Davidoff Solomon. 2022. Representations and warranties insurance in mergers and acquisitions. Review of Accounting Studies 29: 423–50. [Google Scholar] [CrossRef]

- Feldman, Emilie R., and Exequiel Hernandez. 2022. Synergy in Mergers and Acquisitions: Typology, Life Cycles, and Value. Academy of Management Review 47: 549–78. [Google Scholar] [CrossRef]

- Florackis, Chris, Christodoulos Louca, Roni Michaely, and Michael Weber. 2022. Cybersecurity Risk. The Review of Financial Studies 36: 351–407. [Google Scholar] [CrossRef]

- Gu, Ming, Dongxu Li, and Xiaoran Ni. 2022. Too much to learn? The (un)intended consequences of RegTech development on mergers and acquisitions. Journal of Corporate Finance 76: 102276. [Google Scholar] [CrossRef]

- Hemrajani, Pragati, Muskan Khan, and Rahul Dhiman. 2023. Financial risk tolerance: A review and research agenda. European Management Journal 41: 1119–33. [Google Scholar] [CrossRef]

- Hickman, L. Emily. 2019. Information Asymmetry in CSR Reporting: Publicly-Traded versus Privately-Held Firms. Sustainability Accounting, Management and Policy Journal 11: 207–32. [Google Scholar] [CrossRef]

- Hoang, Khanh, Cuong Nguyen, and Hailiang Zhang. 2021. How does economic policy uncertainty affect corporate diversification? International Review of Economics and Finance 72: 254–69. [Google Scholar] [CrossRef]

- Huang, Chenchen, Neslihan Ozkan, and Fangming Xu. 2023. Shareholder Litigation Risk and Firms’ Choice of External Growth. Journal of Financial and Quantitative Analysis 58: 574–614. [Google Scholar] [CrossRef]

- Huang, Jingong, and Taojun Xie. 2023. Technology centrality, bilateral knowledge spillovers and mergers and acquisitions. Journal of Corporate Finance 79: 102366. [Google Scholar] [CrossRef]

- IMAA—Institute for Mergers, Acquisitions, and Alliances. 2024. M&A Statistics: Transactions and Activity by Year. M&A Trends|IMAA. Available online: https://imaa-institute.org/mergers-and-acquisitions-statistics/ (accessed on 27 July 2024).

- Imperatore, Claudia, Gabriel Pündrich, Rodrigo S. Verdi, and Benjamin P. Yost. 2024. Litigation risk and strategic M&A valuations. Journal of Accounting and Economics 78: 101671. [Google Scholar] [CrossRef]

- Jeon, Chunmi, Seongjae Mun, and Seung Hun Han. 2022. Firm-level political risk, liquidity management, and managerial attributes. International Review of Financial Analysis 83: 102285. [Google Scholar] [CrossRef]

- Klitzka, Michael, Jianan He, and Dirk Schiereck. 2022. The rationality of M&A targets in the choice of payment methods. Review of Managerial Science 16: 933–67. [Google Scholar] [CrossRef]

- Kuo, Ya-Fen, Yi-Mien Lin, and Hsiu-Fang Chien. 2021. Corporate social responsibility, enterprise risk management, and real earnings management: Evidence from managerial confidence. Finance Research Letters 41: 101805. [Google Scholar] [CrossRef]

- Li, Fengchun, Ting Liang, and Hailian Zhang. 2021. Does economic policy uncertainty affect cross-border M&As?—A data analysis based on Chinese multinational enterprises. International Review of Financial Analysis 73: 101631. [Google Scholar] [CrossRef]

- Li, Hong-yan, Ruiqing He, and Qiang Fu. 2023. Does corporate social responsibility affect the performance of cross-border M&A of emerging market multinationals? Finance Research Letters 58: 104320. [Google Scholar] [CrossRef]

- Li, Keming. 2020. Does Information Asymmetry Impede Market Efficiency? Evidence from Analyst Coverage. Journal of Banking and Finance 118: 105856. [Google Scholar] [CrossRef]

- Liu, Tingting, Tao Shu, Erin Towery, and Jasmine Wang. 2024. The Role of External Regulators in Mergers and Acquisitions: Evidence from SEC Comment Letters. Review of Accounting Studies 29: 451–92. [Google Scholar] [CrossRef]

- Makrychoriti, Panagiota, and Emmanouil G. Pyrgiotakis. 2024. Firm-level political risk and stock price crashes. Journal of Financial Stability 74: 101303. [Google Scholar] [CrossRef]

- Mandas, Marco, Oumaima Lahmar, Luca Piras, and Riccardo De Lisa. 2024. ESG Reputational Risk and Market Valuation: Evidence from the European Banking Industry. Research in International Business and Finance 69: 102286. [Google Scholar] [CrossRef]

- Maung, Min, Craig Wilson, and Weisu Yu. 2020. Does reputation risk matter? Evidence from cross-border mergers and acquisitions. Journal of International Financial Markets, Institutions and Money 66: 101204. [Google Scholar] [CrossRef]

- Mingers, John, and Liying Yang. 2017. Evaluating journal quality: A review of journal citation indicators and ranking in business and management. European Journal of Operational Research 257: 323–37. [Google Scholar] [CrossRef]

- Nguyen, Hien T., Hieu V. Phan, and Hong Vo. 2023. Agency problems and corporate social responsibility: Evidence from shareholder-creditor mergers. International Review of Financial Analysis 90: 102937. [Google Scholar] [CrossRef]

- Ni, Xiaoran. 2020. Does stakeholder orientation matter for earnings management: Evidence from non-shareholder constituency statutes. Journal of Corporate Finance 62: 101606. [Google Scholar] [CrossRef]

- Ott, Christian. 2020. The risks of mergers and acquisitions—Analyzing the incentives for risk reporting in Item 1A of 10-K filings. Journal of Business Research 106: 158–81. [Google Scholar] [CrossRef]

- Page, Matthew J., Joanne E. McKenzie, Patrick M. Bossuyt, Isabelle Boutron, Tammy C. Hoffmann, Cynthia D. Mulrow, Larissa Shamseer, Jennifer M. Tetzlaff, Elie A. Akl, Sue E. Brennan, and et al. 2021. The PRISMA 2020 statement: An updated guideline for reporting systematic reviews. Systematic Reviews 10: 89. [Google Scholar] [CrossRef] [PubMed]

- Pan, Yihui, Stephan Siegel, and Tracy Yue Wang. 2020. The Cultural Origin of CEOs’ Attitudes toward Uncertainty: Evidence from Corporate Acquisitions. The Review of Financial Studies 33: 2977–3030. [Google Scholar] [CrossRef]

- Paudyal, Krishna, Chandra Thapa, Santosh Koirala, and Sulaiman Aldhawyan. 2021. Economic policy uncertainty and cross-border mergers and acquisitions. Journal of Financial Stability 56: 100926. [Google Scholar] [CrossRef]

- Peng, Zhen, Fan Bai, and Feng Zhao. 2024. Digital finance, life cycle, and enterprise mergers and acquisitions. Finance Research Letters 67: 105784. [Google Scholar] [CrossRef]

- Piesse, Jenifer, Cheng-Few Lee, Lin Lin, and Hsien-Chang Kuo. 2022. Merger and Acquisition: Definitions, Motives, and Market Responses. In Encyclopedia of Finance. Berlin and Heidelberg: Springer. [Google Scholar]

- PricewaterhouseCoopers. 2024. Global M&A Industry Trends: 2024 Mid-Year Outlook. PwC. Available online: https://www.pwc.com/gx/en/services/deals/trends.html (accessed on 26 August 2024).

- Ranaldo, Angelo, and Fabricius Somogyi. 2021. Asymmetric information risk in FX markets. Journal of Financial Economics 140: 391–411. [Google Scholar] [CrossRef]

- Shen, Huayu, Yue Liang, Hanwen Li, Jie Liu, and Guangxi Lu. 2021. Does geopolitical risk promote mergers and acquisitions of listed companies in energy and electric power industries. Energy Economics 95: 105115. [Google Scholar] [CrossRef]

- Snyder, Hannah. 2019. Literature review as a research methodology: An overview and guidelines. Journal of Business Research 104: 333–39. [Google Scholar] [CrossRef]

- Song, Sangcheol, Yuping Zeng, and Bing Zhou. 2021. Information asymmetry, cross-listing, and post-M&A performance. Journal of Business Research 122: 447–57. [Google Scholar] [CrossRef]

- Souissi, Yasmine, Ferdaws Ezzi, and Anis Jarboui. 2024. Blockchain Adoption and Financial Distress: Mediating Role of Information Asymmetry. Journal of the Knowledge Economy 15: 3903–26. [Google Scholar] [CrossRef]

- Swem, Nathan. 2022. Information in Financial Markets: Who Gets It First? Journal of Banking & Finance 140: 106488. [Google Scholar] [CrossRef]

- Tampakoudis, Ioannis, and Evgenia Anagnostopoulou. 2020. The effect of mergers and acquisitions on environmental, social and governance performance and market value: Evidence from EU acquirers. Business Strategy and the Environment 29: 1865–75. [Google Scholar] [CrossRef]

- Vo, Hong, Hien T. Nguyen, and Hieu V. Phan. 2024. Corporate social responsibility and the choice of payment method in mergers and acquisitions. International Review of Financial Analysis 94: 103241. [Google Scholar] [CrossRef]

- Wang, Muyun, and Ying Zhang. 2024. Excess goodwill and enterprise litigation risk. Finance Research Letters 67: 105819. [Google Scholar] [CrossRef]

- Wangerin, D. 2019. M&A Due Diligence, Post-Acquisition Performance, and Financial Reporting for Business Combinations. Contemporary Accounting Research 36: 2344–78. [Google Scholar] [CrossRef]

- Welch, Xena, Stevo Pavićević, Thomas Keil, and Tomi Laamanen. 2020. The Pre-Deal Phase of Mergers and Acquisitions: A Review and Research Agenda. Journal of Management 46: 843–78. [Google Scholar] [CrossRef]