The Leaders, the Laggers, and the “Vulnerables”

Abstract

:1. Introduction

- First, we examine the lead-lag effect reported by Lo and MacKinlay (1990) between large and small capitalization financial index returns. To obtain the two indexes, we divide the financial institutions based on their market capitalization into top ones that are the largest until reaching the top 50th percentile of market capitalization and the remaining bottom ones, repeating this procedure on a weekly basis over the pre- and post-financial crisis period of 2007. We choose to use market capitalization (market cap), as it is widely used to create a context for judging company financial performance and business outlook. Larger cap tend to have more broadly diversified business structures than smaller firms. This may give them more stable business performance from year-to-year, with relatively less variable earnings and revenue streams. As a result, large companies may have less volatile share prices than smaller firms in many circumstances. Large companies generally have also tended to be the least sensitive to economic headwinds. Smaller companies, on the other hand, tend to have a tighter business focus. They may have the potential for more rapid revenue and profit growth, but this potential is often more variable. As a result, small-company shares may be, on average, more volatile and more sensitive to macroeconomic shifts than the shares of larger companies.

- Second, we form a large and a small cap portfolio of the stocks that remained as index constituents in every rebalance (named “survived” large and small cap stocks), and we test whether the lead-lag effect is sustained within the systemic risk measures of those. For this purpose, we use a non-directional systemic risk measure, which does not take size into account upon its construction. This allows us to control for the contemporaneous size effect that results from the systemic risk measure specification. Thus, we use the bivariate marginal expected shortfall (MES) systemic risk measure of Acharya et al. (2017) to estimate the risk exposure of an individual institution to the market.

- Third, we test if the size impact holds upon taking into consideration the financial system structure. The use of network analysis gives insightful information about important players in terms of network connectivity. For this purpose, we use two alternatives of MES that take the interconnectedness relations into account: the network based MES (NetMES), which extends MES by taking multivariate dependencies into its estimation; and the Bayesian NetMES, which further accounts for the network model uncertainty.

2. Data and Market Indices

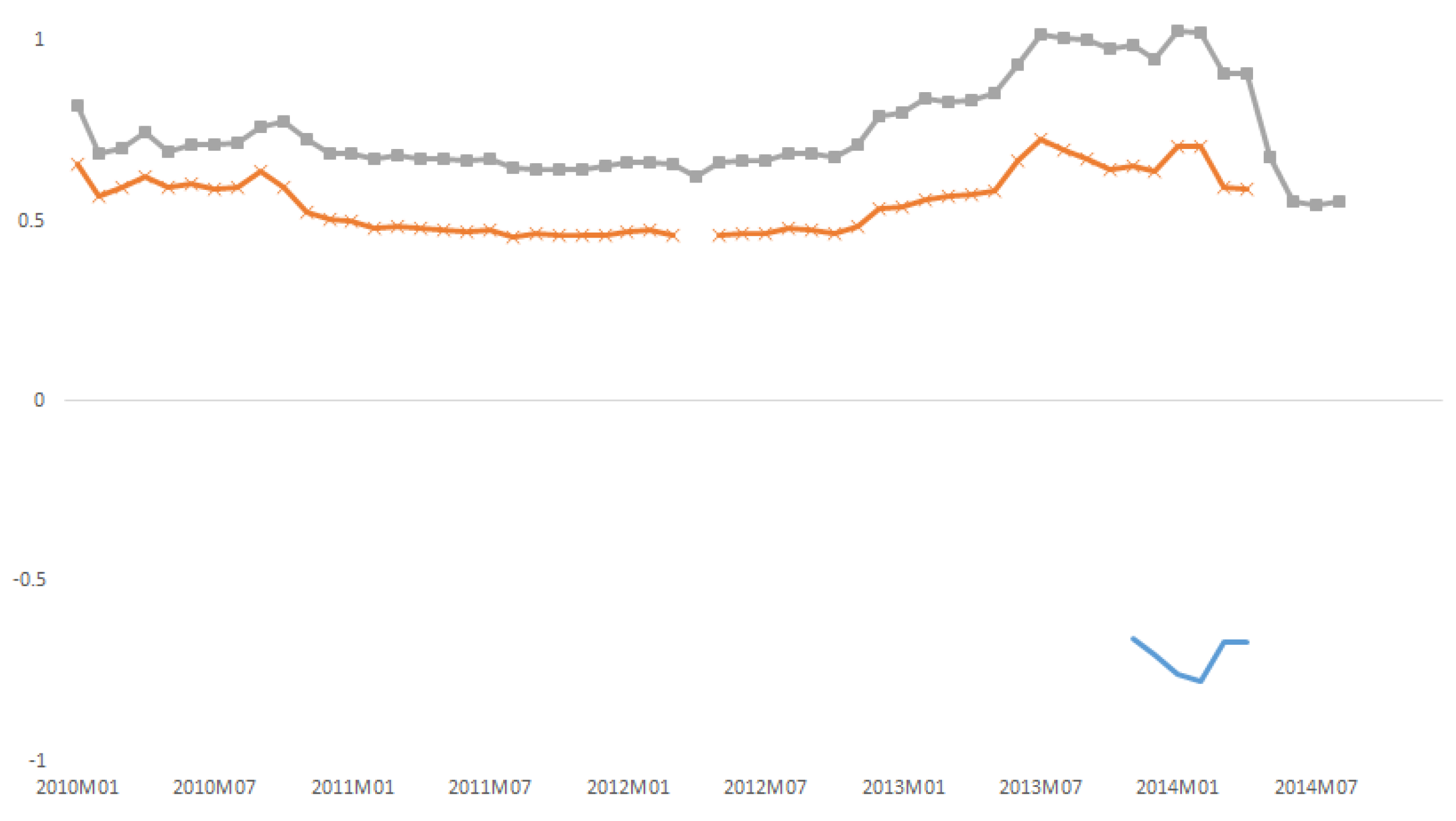

3. Lead-Lag Effect

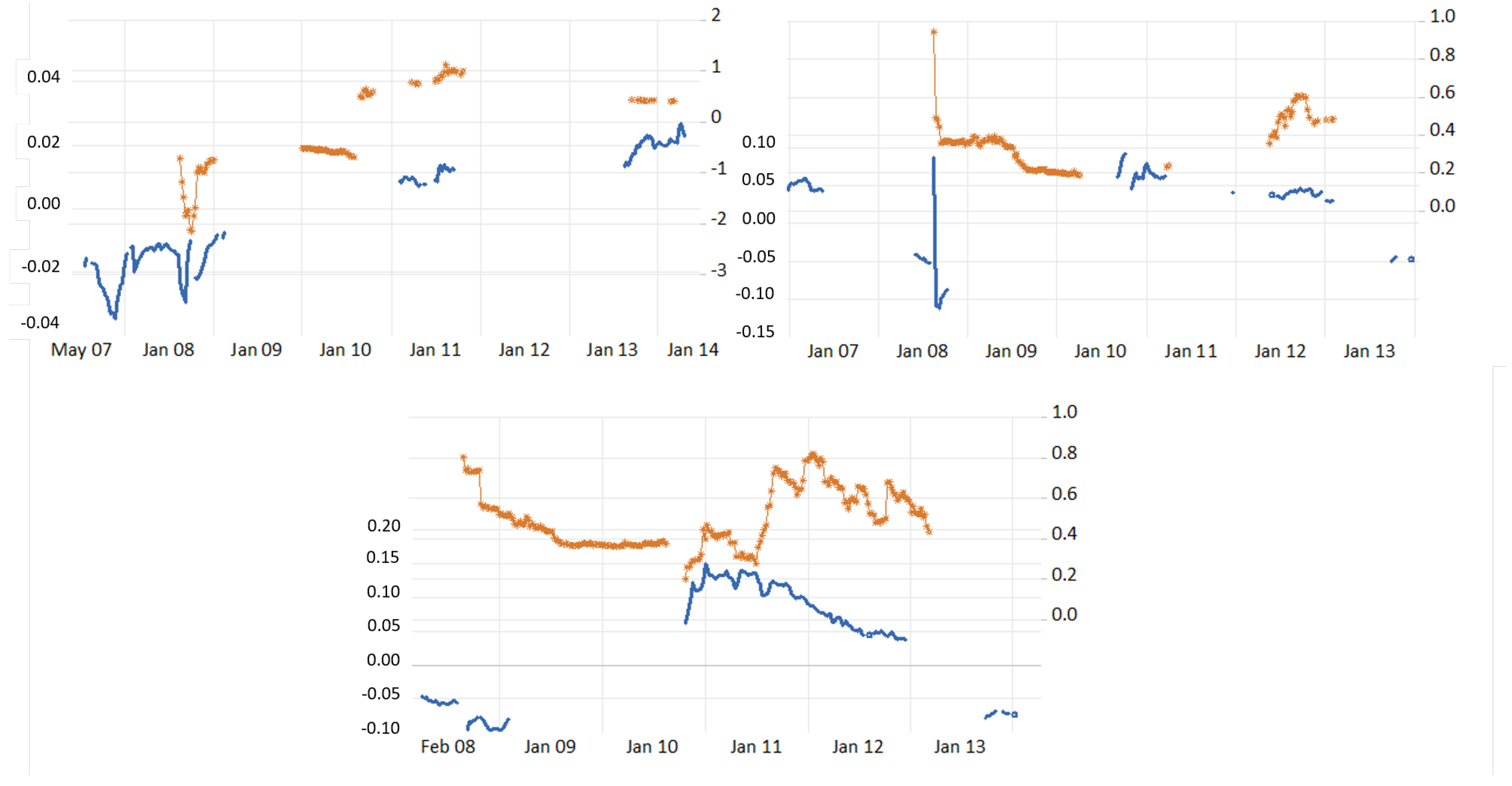

4. Systemic Risk and Network Measures

4.1. Marginal Expected Shortfall

4.2. Network Marginal Expected Shortfall

4.3. Bayesian Network Marginal Expected Shortfall

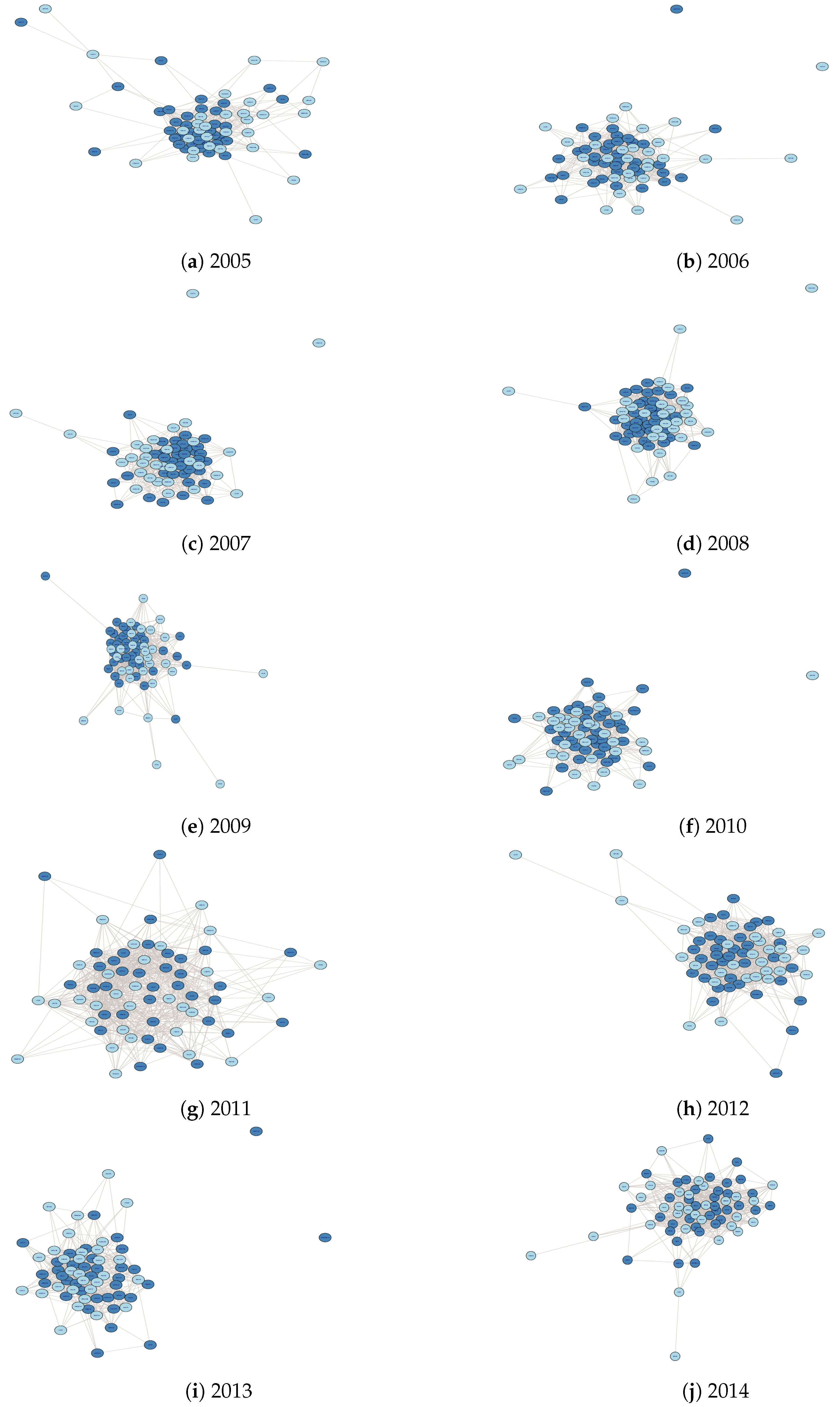

4.4. Centrality Measures

5. Findings and Discussion

- In the United States, Legg Mason Inc. (LM.US) was one of the institutional investors that bore a huge loss when Bear Stearns collapsed, as the group held 11% of Bear Stearns, making the group the bank’s biggest shareholder. Legg Mason was also ranked among the most important institutions by Acharya et al. (2017), as well as Goldman Sachs, TD Ameritrade, and New York Community Bancorp for the period June 2006–June 2007 that the authors examined.

- In France, two prominent French financial institutions were among the most massively hit by the fear of contingent liabilities: Natixis, France’s fourth largest bank, also assumed systemically important, had announced a €1.2 billion write-down of exposure to bad U.S. mortgage debt. Natixis, a publicly-listed corporate and investment banking firm jointly controlled by Caisses d’ Epargne (the French Savings Banks group) and Banques Populaires, and Dexia, a French-Belgian bank specializing in the financing of municipalities. In both cases, the problems were related to their investments in bond insurers in the United States: CDC IXIS Financial Guaranty (CIFG) in the case of Natixis and Financial Security Assurance (FSA) in the case of Dexia12.

- In Germany, an investment-banking arm of Deutsche Bank deeply involved in toxic securities was found systemic by all measures. By some estimates, German banks at the outset of the crisis had an average ratio of debt to net worth of 52 to one compared with 12 to one in the U.S. Indeed, the U.S. Federal Reserve helped Deutsche Bank with $290 billion in mortgage securities.

- In South Africa, Investec Bank was systemically important by all the measures. Indeed, the British government was forced to act by injecting liquidity into financial markets through various schemes including a 50 billion Credit Guarantee Scheme in October 2008, in which Investec Bank was eligible to participate.

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Sector: Financials. Industry Group: Banks | |

|---|---|

| Industry | Sub-industry |

| Banks | Diversified Banks (abbrev. DB) (e.g., Citigroup Inc. (U.S.), Bank of America Corp (U.S.), JPMorgan Chase & Co (U.S.), Wells Fargo & Co (U.S.), Banco Santander SA (Spain)) |

| Large, geographically diverse banks with a national footprint whose revenues are derived primarily from conventional banking operations, have significant business activity in retail banking and small and medium corporate lending, and provide a diverse range of financial services. Excludes banks classified in the Regional Banks and Thrifts & Mortgage Finance sub-industries. Also excludes investment banks classified in the Investment Banking & Brokerage Sub-industry. | |

| Regional Banks (abbrev. RB) (e.g., SunTrust Banks Inc. (U.S.), BB&T Corp (U.S.), PNC Financial Services Group Inc/The (U.S.), Regions Financial Corp (U.S.), Fifth Third Bancorp (U.S.), M&T Bank Corp (U.S.)) | |

| Commercial banks whose businesses are derived primarily from conventional banking operations and have significant business activity in retail banking and small and medium corporate lending. Regional banks tend to operate in limited geographic regions. Excludes companies classified in the Diversified Banks and Thrifts & Mortgage Banks sub-industries. Also excludes investment banks classified in the Investment Banking & Brokerage sub-industry. | |

| Thrifts & Mortgage Finance | Thrifts & Mortgage Finance (abbrev. TMF) (e.g., Federal National Mortgage Association (U.S.), Federal Home Loan Mortgage Corp (U.S.), Housing Development Finance Corp Ltd. (India), MGIC Investment Corp (U.S.), New York Community Bancorp Inc. (U.S.)) |

| Financial institutions providing mortgage and mortgage related services. These include financial institutions whose assets are primarily mortgage related, savings & loans, mortgage lending institutions, building societies and companies providing insurance to mortgage banks. | |

| Capital Markets | Asset Management & Custody Banks (abbrev. AMC) (e.g., Bank of New York Mellon Corp/The (U.S.) Franklin Resources Inc. (U.S.), State Street Corp (U.S.), Brookfield Asset Management Inc. (Canada), T Rowe Price Group Inc. (U.S.) Man Group PLC (U.K.)) |

| Financial institutions primarily engaged in investment management and/or related custody and securities fee based services. Includes companies operating mutual funds, closed-end funds and unit investment trusts. Excludes banks and other financial institutions primarily involved in commercial lending, investment banking, brokerage and other specialized financial activities. | |

| Investment Banking & Brokerage (abbrev. IBB) (e.g., Goldman Sachs Group Inc/The (U.S.), Morgan Stanley (U.S.), Nomura Holdings Inc. (Japan) Charles Schwab Corp/The (U.S.), Daiwa Securities Group Inc. (Japan)) | |

| Financial institutions primarily engaged in investment banking & brokerage services, including equity and debt underwriting, mergers and acquisitions, securities lending and advisory services. Excludes banks and other financial institutions primarily involved in commercial lending, asset management and specialized financial activities. | |

| Diversified Capital Markets (abbrev. DCM) (e.g., UBS Group AG (Switzerland), Deutsche Bank AG (Germany), Credit Suisse Group AG (Switzerland), Natixis SA (France), Macquarie Group Ltd. (Australia)) | |

| Financial institutions primarily engaged in diversified capital markets activities, including a significant presence in at least two of the following area: large/major corporate lending, investment banking, brokerage and asset management. Excludes less diversified companies classified in the Asset Management & Custody Banks or Investment Banking & Brokerage sub-industries. Also excludes companies classified in the Banks or Insurance industry groups or the Consumer Finance Sub-industry. | |

| Mean | Median | Maximum | Minimum | Std.Dev. | Skewness | Kurtosis | Jarque-Bera | Prob. | |

|---|---|---|---|---|---|---|---|---|---|

| LCR | 0.0046 | 0.0127 | 0.2243 | −0.2128 | 0.0527 | −0.3325 | 7.4896 | 102.9966 | 0.0000 |

| SCR | 0.0076 | 0.0138 | 0.1793 | −0.1778 | 0.0449 | −0.3497 | 6.8502 | 76.57078 | 0.0000 |

| Pairwise Granger Causality Tests | |||||||||

| Null Hypothesis | F-Statistic | Prob. | |||||||

| SCR does not Granger cause LCR | 1.3653 | 0.2450 | |||||||

| LCR does not Granger cause SCR | 6.1030 | 0.0149 | |||||||

| Panel A: Financial Leverage of Large-Cap Survived Financial Institutions (Average Per Period) | |||||

|---|---|---|---|---|---|

| Sub-industry | 1/1/2005–12/31/2006 | 1/1/2007–12/31/2008 | 1/1/2009–12/31/2010 | 1/1/2011–12/31/2012 | 1/1/2013–12/31/2014 |

| Asset Management & Custody Banks (AMC) | 1.44 | 1.82 | 1.77 | 1.49 | 1.41 |

| Diversified Banks (DB) | 2.80 | 3.75 | 5.67 | 6.23 | 4.68 |

| Diversified Capital Markets (DCM) | 2.65 | 3.77 | 3.76 | 4.04 | 4.24 |

| Investment Banking & Brokerage (IBB) | 3.34 | 4.13 | 4.97 | 7.13 | 5.51 |

| Regional Banks (RB) | 1.81 | 2.28 | 2.92 | 2.58 | 2.36 |

| Thrifts & Mortgage Finance (TMF) | 5.75 | 20.64 | 144.54 | 382.19 | 82.07 |

| Panel B: Market Capitalization of Large-Cap Survived Financial Institutions (Total Per Period. Numbers in Billion U.S. Dollars) | |||||

| Sub-industry | 1/1/2005–12/31/2006 | 1/1/2007–12/31/2008 | 1/1/2009–12/31/2010 | 1/1/2011–12/31/2012 | 1/1/2013–12/31/2014 |

| Asset Management & Custody Banks (AMC) | 212,536 | 271,262 | 197,192 | 219,003 | 289,875 |

| Diversified Banks (DB) | 2,092,360 | 2,278,660 | 1,944,820 | 2,231,659 | 2,941,330 |

| Diversified Capital Markets (DCM) | 88,566 | 109,625 | 77,923 | 77,553 | 95,089 |

| Investment Banking & Brokerage (IBB) | 210,996 | 216,106 | 174,965 | 151,316 | 219,165 |

| Regional Banks (RB) | 342,808 | 300,445 | 228,424 | 257,018 | 322,905 |

| Thrifts & Mortgage Finance (TMF) | 125,271 | 90,002 | 36,084 | 37,321 | 67,174 |

| Panel C: Financial Leverage of Small-Cap Survived Financial Institutions Per Sub-Industry(Average Per Period) | |||||

| Sub-industry | 1/1/2005–12/31/2006 | 1/1/2007–12/31/2008 | 1/1/2009–12/31/2010 | 1/1/2011–12/31/2012 | 1/1/2013–12/31/2014 |

| Asset Management & Custody Banks (AMC) | 2.16 | 2.43 | 2.61 | 1.78 | 1.60 |

| Diversified Banks (DB) | 5.09 | 8.14 | 11.71 | 7.82 | 6.89 |

| Investment Banking & Brokerage (IBB) | 1.48 | 1.78 | 1.78 | 3.13 | 4.02 |

| Regional Banks (RB) | 1.78 | 2.31 | 3.54 | 2.99 | 2.23 |

| Thrifts & Mortgage Finance (TMF) | 5.36 | 27.92 | 56.08 | 23.04 | 10.45 |

| Panel D: Market Capitalization of Small-Cap Survived Financial Institutions(Total Per Period. Numbers in Billion U.S. Dollars) | |||||

| Sub-industry | 1/1/2005–12/31/2006 | 1/1/2007–12/31/2008 | 1/1/2009–12/31/2010 | 1/1/2011–12/31/2012 | 1/1/2013–12/31/2014 |

| Asset Management & Custody Banks (AMC) | 4634 | 5834 | 3727 | 3794 | 4039 |

| Diversified Banks (DB) | 4034 | 6734 | 6180 | 5345 | 5331 |

| Diversified Capital Markets (DCM) | 2077 | 2440 | 857 | 680 | 600 |

| Investment Banking & Brokerage (IBB) | 5857 | 7802 | 6015 | 5250 | 5904 |

| Regional Banks (RB) | 19,721 | 17,564 | 11,918 | 13,117 | 16,876 |

| Thrifts & Mortgage Finance (TMF) | 3468 | 2506 | 1690 | 1988 | 2632 |

| Industry | Closeness | Industry | Degree | Industry | Eigenvector Centrality | Industry | Betweenness % | |||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2005 | SANTGRU.CI | L.AM | 0.005181 | LM.US | L.AM | 14 | OCFC.US | S.TMF | 0.178653 | OCFC.US | S.TMF | 0.048558 |

| LM.US | L.AM | 0.004975 | SANTGRU.CI | L.AM | 12 | PGR.SJ | S.AMC | 0.177352 | ALBAV.FH | S.DB | 0.047278 | |

| MLP.GR | L.AM | 0.004608 | MLP.GR | L.AM | 6 | SANTGRU.CI | L.AM | 0.174771 | IMH.US | S.TMF | 0.037376 | |

| VONN.SW | L.AM | 0.003922 | 8616.JP | L.IBB | 4 | FSBK.US | S.RB | 0.173471 | 8614.JP | S.IBB | 0.035849 | |

| CAF.FP | L.RB | 0.003861 | BPI.PM | L.DB | 4 | SCB.TB | L.DB | 0.171668 | 8616.JP | L.IBB | 0.034817 | |

| CHFC.US | L.RB | 0.003861 | KN.FP | L.DCM | 4 | MQG.AU | L.DCM | 0.170623 | GKG.SP | S.RCS | 0.032493 | |

| 2006 | 8595.JP | L.AM | 0.005102 | LM.US | L.AM | 13 | TPEIR.GA | L.DB | 0.181499 | GKG.SP | S.RCS | 0.052294 |

| LM.US | L.AM | 0.005051 | MLP.GR | L.AM | 9 | CRAP.FP | L.RB | 0.180081 | FSBK.US | S.RB | 0.051185 | |

| MLP.GR | L.AM | 0.004762 | VPBN.SW | L.AM | 6 | CAF.FP | L.RB | 0.169709 | KNK.MK | S.IBB | 0.035955 | |

| VONN.SW | L.AM | 0.004065 | 8601.JP | L.IBB | 6 | PGR.SJ | S.AMC | 0.168861 | CAF.FP | L.RB | 0.029135 | |

| BAC.US | L.DB | 0.003906 | ITG.US | L.IBB | 5 | SECH.KK | S.DCM | 0.167201 | IMH.US | S.TMF | 0.026233 | |

| SANTGRU.CI | L.AM | 0.003876 | 8595.JP | L.AM | 4 | 8616.JP | L.IBB | 0.164756 | CHIB.PM | L.DB | 0.025356 | |

| 2007 | MLP.GR | L.AM | 0.005291 | 8595.JP | L.AM | 14 | MTG.US | L.TMF | 0.172005 | TMB.TB | L.DB | 0.055944 |

| 8595.JP | L.AM | 0.005181 | SANTGRU.CI | L.AM | 9 | FCBC.US | S.RB | 0.171019 | CNS.TB | S.IBB | 0.042395 | |

| SANTGRU.CI | L.AM | 0.004831 | VPBN.SW | L.AM | 7 | CFFN.US | L.TMF | 0.165398 | OPY.US | S.IBB | 0.034206 | |

| LM.US | L.AM | 0.004082 | MLP.GR | L.AM | 6 | CHIB.PM | L.DB | 0.165047 | DXIL.IT | S.DB | 0.033959 | |

| BPSO.IM | L.DB | 0.004082 | LM.US | L.AM | 5 | 165.HK | L.DCM | 0.164251 | AMTD.US | L.IBB | 0.030148 | |

| VPBN.SW | L.AM | 0.003984 | TMB.TB | L.DB | 5 | SBCF.US | S.RB | 0.162894 | BPSO.IM | L.DB | 0.027496 | |

| 2008 | SANTGRU.CI | L.AM | 0.00578 | SANTGRU.CI | L.AM | 12 | GSDHO.TI | S.DB | 0.140767 | 626.HK | L.RB | 0.078572 |

| MLP.GR | L.AM | 0.004975 | ALBK.ID | L.DB | 10 | GKG.SP | S.RCS | 0.139739 | MLP.GR | L.AM | 0.043968 | |

| ALBK.ID | L.DB | 0.004739 | VPBN.SW | L.AM | 9 | NYCB.US | L.TMF | 0.138752 | GKG.SP | S.RCS | 0.043732 | |

| HB.CY | L.DB | 0.004484 | ALPHA.GA | L.DB | 6 | MTG.US | L.TMF | 0.138549 | GSDHO.TI | S.DB | 0.041172 | |

| INL.SJ | L.DCM | 0.004329 | INL.SJ | L.DCM | 5 | PGR.SJ | S.AMC | 0.138138 | EFS.GR | S.AMC | 0.036526 | |

| 8601.JP | L.IBB | 0.004329 | 8601.JP | L.IBB | 5 | SANTGRU.CI | L.AM | 0.138068 | KN.FP | L.DCM | 0.032975 | |

| 2009 | VPBN.SW | L.AM | 0.005435 | VPBN.SW | L.AM | 16 | 626.HK | L.RB | 0.142476 | 626.HK | L.RB | 0.020224 |

| LM.US | L.AM | 0.004505 | 8595.JP | L.AM | 7 | OPY.US | S.IBB | 0.141236 | OPY.US | S.IBB | 0.017514 | |

| BAC.US | L.DB | 0.004464 | SWEDA.SS | L.DB | 7 | TRST.US | L.TMF | 0.141071 | TRST.US | L.TMF | 0.018687 | |

| BAP.US | L.DB | 0.004464 | BAC.US | L.DB | 5 | NYCB.US | L.TMF | 0.140346 | NYCB.US | L.TMF | 0.013479 | |

| 8595.JP | L.AM | 0.004167 | ITG.US | L.IBB | 5 | MQG.AU | L.DCM | 0.140346 | MQG.AU | L.DCM | 0.013479 | |

| INL.SJ | L.DCM | 0.004032 | AIRE.SW | S.AMC | 5 | KA.NA | S.AMC | 0.14023 | KA.NA | S.AMC | 0.013905 | |

| 2010 | 8595.JP | L.AM | 0.005587 | 8595.JP | L.AM | 10 | AF.US | L.TMF | 0.174098 | AF.US | L.TMF | 0.021152 |

| SANTGRU.CI | L.AM | 0.005128 | VPBN.SW | L.AM | 8 | FBAK.US | L.RB | 0.170886 | FBAK.US | L.RB | 0.027655 | |

| VPBN.SW | L.AM | 0.004695 | SANTGRU.CI | L.AM | 7 | INL.SJ | L.DCM | 0.170254 | INL.SJ | L.DCM | 0.026623 | |

| ALPHA.GA | L.DB | 0.004255 | ALPHA.GA | L.DB | 6 | NYCB.US | L.TMF | 0.169919 | NYCB.US | L.TMF | 0.016441 | |

| DBK.GR | L.DCM | 0.004219 | 8616.JP | L.IBB | 6 | 165.HK | L.DCM | 0.158964 | 165.HK | L.DCM | 0.025424 | |

| LM.US | L.AM | 0.004219 | LM.US | L.AM | 5 | KN.FP | L.DCM | 0.158697 | KN.FP | L.DCM | 0.010844 | |

| 2011 | LM.US | L.AM | 0.005525 | LM.US | L.AM | 10 | 6800.KS | L.DCM | 0.152724 | CAF.FP | L.RB | 0.094042 |

| SANTGRU.CI | L.AM | 0.004651 | MLP.GR | L.AM | 8 | CAF.FP | L.RB | 0.152315 | PAG.LN | L.TMF | 0.051556 | |

| 8595.JP | L.AM | 0.004566 | VPBN.SW | L.AM | 7 | VONN.SW | L.AM | 0.151866 | OCFC.US | S.TMF | 0.043034 | |

| VPBN.SW | L.AM | 0.004405 | 8595.JP | L.AM | 6 | OCFC.US | S.TMF | 0.151594 | SNBC.US | S.RB | 0.035732 | |

| BAC.US | L.DB | 0.004329 | SANTGRU.CI | L.AM | 5 | PAG.LN | L.TMF | 0.151027 | ALBAV.FH | S.DB | 0.033062 | |

| ALPHA.GA | L.DB | 0.004115 | 8616.JP | L.IBB | 5 | BPOP.US | L.RB | 0.150388 | VPBN.SW | L.AM | 0.030576 | |

| 2012 | LM.US | L.AM | 0.005525 | LM.US | L.AM | 19 | KN.FP | L.DCM | 0.167036 | NYCB.US | L.TMF | 0.06052 |

| 8595.JP | L.AM | 0.004975 | KN.FP | L.DCM | 6 | 165.HK | L.DCM | 0.167036 | ALPHA.GA | L.DB | 0.042107 | |

| SANTGRU.CI | L.AM | 0.004292 | PAG.LN | L.TMF | 6 | AF.US | L.TMF | 0.165888 | FDEF.US | S.TMF | 0.041178 | |

| VPBN.SW | L.AM | 0.004219 | 8595.JP | L.AM | 5 | TRST.US | L.TMF | 0.164555 | GKG.SP | S.RCS | 0.036114 | |

| VONN.SW | L.AM | 0.004219 | SANTGRU.CI | L.AM | 5 | INL.SJ | L.DCM | 0.164464 | SANTGRU.CI | L.AM | 0.035323 | |

| MB.IM | L.DB | 0.004115 | MB.IM | L.DB | 4 | SNBC.US | S.RB | 0.16297 | 8595.JP | L.AM | 0.028406 | |

| 2013 | LM.US | L.AM | 0.00578 | SANTGRU.CI | L.AM | 10 | SPOG.NO | S.DB | 0.176911 | 8601.JP | L.IBB | 0.050827 |

| SANTGRU.CI | L.AM | 0.005128 | LM.US | L.AM | 9 | MTG.US | L.TMF | 0.175996 | TRST.US | L.TMF | 0.047171 | |

| MLP.GR | L.AM | 0.005076 | MLP.GR | L.AM | 7 | ADC.GR | S.AMC | 0.170295 | 8614.JP | S.IBB | 0.045854 | |

| 165.HK | L.DCM | 0.004367 | DBK.GR | L.DCM | 7 | SNV.US | L.RB | 0.170002 | LD.FP | L.DB | 0.036833 | |

| 666.HK | S.AMC | 0.004292 | TPEIR.GA | L.DB | 6 | 8625.JP | S.IBB | 0.16952 | KN.FP | L.DCM | 0.031443 | |

| VPBN.SW | L.AM | 0.004219 | 165.HK | L.DCM | 5 | 666.HK | S.AMC | 0.167537 | 6005.TT | L.IBB | 0.030302 | |

| 2014 | 8595.JP | L.AM | 0.005618 | 8595.JP | L.AM | 10 | 8616.JP | L.IBB | 0.190897 | MTG.US | L.TMF | 0.050147 |

| SANTGRU.CI | L.AM | 0.005102 | LM.US | L.AM | 9 | 8601.JP | L.IBB | 0.187831 | NASB.US | S.TMF | 0.045331 | |

| LM.US | L.AM | 0.00495 | SANTGRU.CI | L.AM | 7 | SGC.KK | S.DCM | 0.184773 | 8625.JP | S.IBB | 0.040566 | |

| VPBN.SW | L.AM | 0.004202 | VPBN.SW | L.AM | 7 | INL.SJ | L.DCM | 0.180898 | 626.HK | L.RB | 0.033206 | |

| BCE.MC | L.DB | 0.004202 | VONN.SW | L.AM | 7 | GS.US | L.IBB | 0.175884 | SVEG.NO | S.DB | 0.032992 | |

| DBK.GR | L.DCM | 0.004167 | BAC.US | L.DB | 6 | ALMUTAHE.KK | L.DB | 0.173706 | OPY.US | S.IBB | 0.031155 |

| Industry | Closeness | Industry | Node Degree | Industry | Eigenvector Centrality | Industry | Betweenness % | |||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2005 | LM.US | L.AMC | 0.00565 | 8595.JP | L.AMC | 11 | MQG.AU | L.DCM | 0.18481 | PAG.LN | L.TMF | 0.08888 |

| 8595.JP | L.AMC | 0.00541 | LM.US | L.AMC | 8 | KN.FP | L.DCM | 0.18021 | CAY.LN | S.IBB | 0.06871 | |

| VONN.SW | L.AMC | 0.00465 | VONN.SW | L.AMC | 5 | SANTGRU.CI | L.AMC | 0.17996 | CFFN.US | L.TMF | 0.05712 | |

| RHBC.MK | L.DB | 0.00444 | ALBK.ID | L.DB | 5 | 8601.JP | L.IBB | 0.17986 | ALPHA.GA | L.DB | 0.05152 | |

| FII.US | L.AMC | 0.00437 | BGCP.US | L.IBB | 5 | OCFC.US | S.TMF | 0.17947 | SNV.US | L.RB | 0.04891 | |

| ALBK.ID | L.DB | 0.00437 | PAG.LN | L.TMF | 5 | FMBI.US | L.RB | 0.17833 | 6800.KS | L.DCM | 0.03544 | |

| 2006 | LM.US | L.AMC | 0.00532 | LM.US | L.AMC | 9 | 8595.JP | L.AMC | 0.21323 | DBK.GR | L.DCM | 0.05677 |

| ADN.LN | L.AMC | 0.00500 | ADN.LN | L.AMC | 9 | BCBB.BG | S.DB | 0.18794 | 8616.JP | L.IBB | 0.04787 | |

| 8595.JP | L.AMC | 0.00459 | VONN.SW | L.AMC | 8 | FMBI.US | L.RB | 0.18423 | turn.US | S.AMC | 0.03986 | |

| SANTGRU.CI | L.AMC | 0.00420 | HB.CY | L.DB | 7 | 6800.KS | L.DCM | 0.18017 | CFFN.US | L.TMF | 0.03901 | |

| BNII.IJ | L.DB | 0.00413 | 8616.JP | L.IBB | 5 | BSF.US | S.TMF | 0.17666 | BCBB.BG | S.DB | 0.03863 | |

| HB.CY | L.DB | 0.00407 | BPOP.US | L.RB | 4 | PRO.IM | S.IBB | 0.17000 | 8614.JP | S.IBB | 0.03312 | |

| 2007 | LM.US | L.AMC | 0.00552 | BNII.IJ | L.DB | 11 | PAG.LN | L.TMF | 0.19450 | OCFC.US | S.TMF | 0.07308 |

| SANTGRU.CI | L.AMC | 0.00493 | LM.US | L.AMC | 7 | BSF.US | S.TMF | 0.18938 | turn.US | S.AMC | 0.04301 | |

| VONN.SW | L.AMC | 0.00478 | VPBN.SW | L.AMC | 6 | BIM.IM | L.IBB | 0.18883 | DBK.GR | L.DCM | 0.03838 | |

| BNII.IJ | L.DB | 0.00474 | SANTGRU.CI | L.AMC | 5 | TRST.US | L.TMF | 0.18745 | PRO.IM | S.IBB | 0.03820 | |

| ADN.LN | L.AMC | 0.00422 | ADN.LN | L.AMC | 5 | MQG.AU | L.DCM | 0.18658 | BGCP.US | L.IBB | 0.03497 | |

| INL.SJ | L.DCM | 0.00412 | BIM.IM | L.IBB | 5 | 165.HK | L.DCM | 0.18517 | CIMB.MK | L.DB | 0.03384 | |

| 2008 | LM.US | L.AMC | 0.00488 | LM.US | L.AMC | 8 | SANTGRU.CI | L.AMC | 0.18377 | VONN.SW | L.AMC | 0.05474 |

| 8595.JP | L.AMC | 0.00474 | KN.FP | L.DCM | 7 | NYCB.US | L.TMF | 0.17727 | CFFN.US | L.TMF | 0.05473 | |

| BC.SW | L.DB | 0.00429 | BC.SW | L.DB | 6 | MQG.AU | L.DCM | 0.17473 | FMCC.US | L.TMF | 0.05193 | |

| VONN.SW | L.AMC | 0.00422 | VONN.SW | L.AMC | 6 | PRO.IM | S.IBB | 0.17240 | KN.FP | L.DCM | 0.03658 | |

| BNII.IJ | L.DB | 0.00386 | BNII.IJ | L.DB | 6 | INL.SJ | L.DCM | 0.17126 | SVEG.NO | S.DB | 0.03565 | |

| RAT.LN | L.AMC | 0.00386 | RHBC.MK | L.DB | 6 | BSF.US | S.TMF | 0.16836 | ASP.TB | S.IBB | 0.03523 | |

| 2009 | SANTGRU.CI | L.AMC | 0.00397 | KBC.BB | L.DB | 7 | 6800.KS | L.DCM | 0.17504 | BGCP.US | L.IBB | 0.05660 |

| 8595.JP | L.AMC | 0.00394 | BC.SW | L.DB | 6 | NYCB.US | L.TMF | 0.17484 | FMBI.US | L.RB | 0.05599 | |

| BC.SW | L.DB | 0.00385 | HB.CY | L.DB | 6 | TRST.US | L.TMF | 0.17296 | 8616.JP | L.IBB | 0.04728 | |

| LM.US | L.AMC | 0.00355 | 8616.JP | L.IBB | 6 | CIMB.MK | L.DB | 0.17213 | 8543.JP | L.RB | 0.04667 | |

| CIMB.MK | L.DB | 0.00352 | SANTGRU.CI | L.AMC | 5 | OPY.US | S.IBB | 0.17158 | SCB.CN | S.TMF | 0.03621 | |

| VPBN.SW | L.AMC | 0.00338 | VONN.SW | L.AMC | 5 | 8595.JP | L.AMC | 0.17122 | 8614.JP | S.IBB | 0.03620 | |

| 2010 | 8595.JP | L.AMC | 0.00746 | 8595.JP | L.AMC | 21 | SBCF.US | S.RB | 0.20901 | UMBF.US | L.RB | 0.04446 |

| HB.CY | L.DB | 0.00538 | 8601.JP | L.IBB | 5 | BIM.IM | L.IBB | 0.20752 | BPOP.US | L.RB | 0.04340 | |

| SANTGRU.CI | L.AMC | 0.00538 | HB.CY | L.DB | 4 | PROV.US | S.TMF | 0.20503 | NYCB.US | L.TMF | 0.04130 | |

| 8601.JP | L.IBB | 0.00532 | LM.US | L.AMC | 4 | MTG.US | L.TMF | 0.20125 | OPY.US | S.IBB | 0.04088 | |

| LM.US | L.AMC | 0.00532 | AMTD.US | L.IBB | 4 | HB.CY | L.DB | 0.19200 | 21080.KS | S.AMC | 0.04041 | |

| VPBN.SW | L.AMC | 0.00532 | VPBN.SW | L.AMC | 3 | COB.US | S.RB | 0.18107 | HB.CY | L.DB | 0.03626 | |

| 2011 | 8595.JP | L.AMC | 0.00595 | 8595.JP | L.AMC | 17 | NYCB.US | L.TMF | 0.19414 | fusb.US | S.RB | 0.05917 |

| VONN.SW | L.AMC | 0.00556 | VONN.SW | L.AMC | 5 | CIMB.MK | L.DB | 0.18736 | GRLA.DC | S.RB | 0.04212 | |

| BNII.IJ | L.DB | 0.00463 | BNII.IJ | L.DB | 5 | BPOP.US | L.RB | 0.18640 | BIM.IM | L.IBB | 0.03264 | |

| ADN.LN | L.AMC | 0.00463 | ADN.LN | L.AMC | 4 | GRLA.DC | S.RB | 0.18410 | DBAN.GR | S.AMC | 0.03170 | |

| LM.US | L.AMC | 0.00442 | LM.US | L.AMC | 4 | OPY.US | S.IBB | 0.18175 | BPOP.US | L.RB | 0.03066 | |

| DBK.GR | L.DCM | 0.00442 | INL.SJ | L.DCM | 4 | MTG.US | L.TMF | 0.17993 | KBC.BB | L.DB | 0.02907 | |

| 2012 | VONN.SW | L.AMC | 0.00559 | VONN.SW | L.AMC | 14 | MQG.AU | L.DCM | 0.19355 | BPOP.US | L.RB | 0.05108 |

| 8595.JP | L.AMC | 0.00498 | BNII.IJ | L.DB | 6 | ASP.TB | S.IBB | 0.19056 | CAY.LN | S.IBB | 0.04924 | |

| BNII.IJ | L.DB | 0.00452 | 8595.JP | L.AMC | 5 | KN.FP | L.DCM | 0.19051 | 165.HK | L.DCM | 0.04543 | |

| ALPHA.GA | L.DB | 0.00433 | KBC.BB | L.DB | 5 | SCB.CN | S.TMF | 0.18788 | BGCP.US | L.IBB | 0.04254 | |

| SANTGRU.CI | L.AMC | 0.00422 | CIMB.MK | L.DB | 4 | INL.SJ | L.DCM | 0.18722 | HB.CY | L.DB | 0.03695 | |

| CIMB.MK | L.DB | 0.00422 | 165.HK | L.DCM | 4 | CIMB.MK | L.DB | 0.18647 | CIMB.MK | L.DB | 0.03101 | |

| 2013 | LM.US | L.AMC | 0.00498 | LM.US | L.AMC | 8 | COB.US | S.RB | 0.21207 | NBKE.EY | S.DB | 0.04629 |

| HB.CY | L.DB | 0.00457 | HB.CY | L.DB | 8 | MTG.US | L.TMF | 0.20954 | 21080.KS | S.AMC | 0.04582 | |

| 8595.JP | L.AMC | 0.00441 | 8595.JP | L.AMC | 6 | BIM.IM | L.IBB | 0.20328 | BIM.IM | L.IBB | 0.04438 | |

| ADN.LN | L.AMC | 0.00405 | BNII.IJ | L.DB | 6 | 21080.KS | S.AMC | 0.19951 | COB.US | S.RB | 0.04286 | |

| DBK.GR | L.DCM | 0.00395 | ADN.LN | L.AMC | 4 | 8625.JP | S.IBB | 0.19386 | 8543.JP | L.RB | 0.03941 | |

| VPBN.SW | L.AMC | 0.00386 | VPBN.SW | L.AMC | 4 | SNV.US | L.RB | 0.19106 | 8616.JP | L.IBB | 0.03316 | |

| 2014 | 8595.JP | L.AMC | 0.00658 | 8595.JP | L.AMC | 15 | ASP.TB | S.IBB | 0.21532 | SAHA.GR | S.AMC | 0.05481 |

| VONN.SW | L.AMC | 0.00641 | VONN.SW | L.AMC | 11 | PRO.IM | S.IBB | 0.20648 | BGCP.US | L.IBB | 0.05294 | |

| SANTGRU.CI | L.AMC | 0.00505 | MTG.US | L.TMF | 5 | INL.SJ | L.DCM | 0.19970 | ASP.TB | S.IBB | 0.04377 | |

| DBK.GR | L.DCM | 0.00481 | FII.US | L.AMC | 5 | 165.HK | L.DCM | 0.19798 | LD.FP | S.TMF | 0.03818 | |

| MTG.US | L.TMF | 0.00481 | DBK.GR | L.DCM | 4 | FMBI.US | L.RB | 0.19687 | PAG.LN | L.TMF | 0.03757 | |

| KN.FP | L.DCM | 0.00481 | KN.FP | L.DCM | 4 | GRLA.DC | S.RB | 0.19351 | BCBB.BG | S.DB | 0.03618 |

| Industry | Closeness | Industry | Node Degree | Industry | Eigenvector Centrality | Industry | Betweenness % | |||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2005 | 8595.JP | L.AMC | 0.005319 | LM.US | L.AMC | 11 | MQG.AU | L.DCM | 0.184416 | BCBB.BG | S.DB | 0.081837 |

| VONN.SW | L.AMC | 0.005102 | 8595.JP | L.AMC | 11 | BIM.IM | L.IBB | 0.181143 | CAF.FP | L.RB | 0.071296 | |

| BAP.US | L.DB | 0.004587 | SBIN.IN | L.DB | 6 | OCFC.US | S.TMF | 0.179697 | PAG.LN | L.TMF | 0.061393 | |

| LM.US | L.AMC | 0.004425 | DBK.GR | L.DCM | 6 | OPY.US | S.IBB | 0.179587 | CAY.LN | S.IBB | 0.038407 | |

| SBIN.IN | L.DB | 0.004132 | 6800.KS | L.DCM | 6 | KN.FP | L.DCM | 0.179040 | 21080.KS | S.AMC | 0.036663 | |

| HB.CY | L.DB | 0.004098 | HB.CY | L.DB | 4 | SANTGRU.CI | L.AMC | 0.178505 | CFFN.US | L.TMF | 0.035094 | |

| 2006 | VONN.SW | L.AMC | 0.006452 | VONN.SW | L.AMC | 14 | BCBB.BG | S.DB | 0.195170 | BCBB.BG | S.DB | 0.073190 |

| RAT.LN | L.AMC | 0.005780 | RAT.LN | L.AMC | 11 | 165.HK | L.DCM | 0.192246 | DBK.GR | L.DCM | 0.050477 | |

| 8595.JP | L.AMC | 0.005348 | LM.US | L.AMC | 6 | DBK.GR | L.DCM | 0.185441 | 8616.JP | L.IBB | 0.046745 | |

| 8543.JP | L.RB | 0.004785 | 8595.JP | L.AMC | 6 | NASB.US | S.TMF | 0.183326 | 8543.JP | L.RB | 0.039037 | |

| BAP.US | L.DB | 0.004739 | SANTGRU.CI | L.AMC | 5 | 6800.KS | L.DCM | 0.182559 | 8614.JP | S.IBB | 0.038075 | |

| SBIN.IN | L.DB | 0.004608 | 8543.JP | L.RB | 5 | 8595.JP | L.AMC | 0.180163 | PAG.LN | L.TMF | 0.037034 | |

| 2007 | ADN.LN | L.AMC | 0.004808 | CHIB.PM | L.DB | 9 | BSF.US | S.TMF | 0.189265 | OCFC.US | S.TMF | 0.069634 |

| LM.US | L.AMC | 0.004762 | RHBC.MK | L.DB | 8 | TRST.US | L.TMF | 0.187098 | BGCP.US | L.IBB | 0.062759 | |

| CHIB.PM | L.DB | 0.004505 | RAT.LN | L.AMC | 7 | BIM.IM | L.IBB | 0.184806 | turn.US | S.AMC | 0.043719 | |

| RAT.LN | L.AMC | 0.004425 | VONN.SW | L.AMC | 4 | 165.HK | L.DCM | 0.184042 | DBK.GR | L.DCM | 0.039933 | |

| 165.HK | L.DCM | 0.003788 | LM.US | L.AMC | 4 | MQG.AU | L.DCM | 0.183710 | PRO.IM | S.IBB | 0.032516 | |

| VONN.SW | L.AMC | 0.003759 | ADN.LN | L.AMC | 4 | PAG.LN | L.TMF | 0.181808 | PGR.SJ | S.AMC | 0.031952 | |

| 2008 | SANTGRU.CI | L.AMC | 0.005780 | BAP.US | L.DB | 9 | NYCB.US | L.TMF | 0.177473 | CFFN.US | L.TMF | 0.070379 |

| RAT.LN | L.AMC | 0.005348 | 8616.JP | L.IBB | 9 | MQG.AU | L.DCM | 0.176199 | VONN.SW | L.AMC | 0.050911 | |

| LM.US | L.AMC | 0.004785 | RAT.LN | L.AMC | 8 | INL.SJ | L.DCM | 0.175540 | FMCC.US | L.TMF | 0.049563 | |

| 8616.JP | L.IBB | 0.004739 | LM.US | L.AMC | 7 | LASP.DC | S.DB | 0.174415 | KN.FP | L.DCM | 0.037231 | |

| BAP.US | L.DB | 0.004405 | SANTGRU.CI | L.AMC | 5 | OCFC.US | S.TMF | 0.174060 | LASP.DC | S.DB | 0.033454 | |

| VPBN.SW | L.AMC | 0.004367 | ALPHA.GA | L.DB | 4 | PRO.IM | S.IBB | 0.173592 | 8614.JP | S.IBB | 0.031573 | |

| 2009 | LM.US | L.AMC | 0.006369 | LM.US | L.AMC | 13 | OPY.US | S.IBB | 0.176723 | UMBF.US | L.RB | 0.047378 |

| 8595.JP | L.AMC | 0.005464 | 8595.JP | L.AMC | 8 | 8595.JP | L.AMC | 0.175862 | SANTGRU.CI | L.AMC | 0.044767 | |

| VONN.SW | L.AMC | 0.005076 | VONN.SW | L.AMC | 7 | NYCB.US | L.TMF | 0.174494 | KN.FP | L.DCM | 0.043701 | |

| INL.SJ | L.DCM | 0.004831 | INL.SJ | L.DCM | 6 | 6800.KS | L.DCM | 0.172134 | BCBB.BG | S.DB | 0.042210 | |

| KN.FP | L.DCM | 0.004651 | VPBN.SW | L.AMC | 4 | TRST.US | L.TMF | 0.171775 | GRLA.DC | S.RB | 0.040354 | |

| 6800.KS | L.DCM | 0.004651 | RAT.LN | L.AMC | 3 | MQG.AU | L.DCM | 0.171251 | FMBI.US | L.RB | 0.033752 | |

| 2010 | VONN.SW | L.AMC | 0.005263 | VONN.SW | L.AMC | 10 | BIM.IM | L.IBB | 0.200952 | OPY.US | S.IBB | 0.087552 |

| LM.US | L.AMC | 0.005000 | BNII.IJ | L.DB | 8 | SBCF.US | S.RB | 0.200207 | SANTGRU.CI | L.AMC | 0.052690 | |

| 8595.JP | L.AMC | 0.004587 | LM.US | L.AMC | 6 | PROV.US | S.TMF | 0.200207 | NYCB.US | L.TMF | 0.047267 | |

| HB.CY | L.DB | 0.004505 | HB.CY | L.DB | 6 | MTG.US | L.TMF | 0.195417 | LM.US | L.AMC | 0.039902 | |

| RAT.LN | L.AMC | 0.004032 | 8595.JP | L.AMC | 5 | BAP.US | L.DB | 0.193931 | OCFC.US | S.TMF | 0.039587 | |

| 8543.JP | L.RB | 0.004032 | BIM.IM | L.IBB | 5 | HB.CY | L.DB | 0.183587 | BAP.US | L.DB | 0.037286 | |

| 2011 | VONN.SW | L.AMC | 0.006024 | VONN.SW | L.AMC | 13 | NYCB.US | L.TMF | 0.188460 | DBAN.GR | S.AMC | 0.046681 |

| C.US | L.AMC | 0.005319 | C.US | L.AMC | 9 | CIMB.MK | L.DB | 0.182926 | BIM.IM | L.IBB | 0.043714 | |

| LM.US | L.AMC | 0.005155 | CHIB.PM | L.DB | 6 | KN.FP | L.DCM | 0.180730 | PGR.SJ | S.AMC | 0.039625 | |

| FII.US | L.AMC | 0.004545 | LM.US | L.AMC | 5 | MTG.US | L.TMF | 0.176983 | CACB.US | S.RB | 0.037534 | |

| CIMB.MK | L.DB | 0.004505 | RAT.LN | L.AMC | 5 | BSF.US | S.TMF | 0.176903 | FMBI.US | L.RB | 0.032418 | |

| 6800.KS | L.DCM | 0.004464 | INL.SJ | L.DCM | 5 | BPOP.US | L.RB | 0.176642 | ALPHA.GA | L.DB | 0.030919 | |

| 2012 | 8595.JP | L.AMC | 0.006173 | 8595.JP | L.AMC | 13 | KN.FP | L.DCM | 0.198168 | BAP.US | L.DB | 0.052362 |

| VONN.SW | L.AMC | 0.005155 | VONN.SW | L.AMC | 6 | INL.SJ | L.DCM | 0.193101 | CAY.LN | S.IBB | 0.048778 | |

| DBK.GR | L.DCM | 0.005051 | RAT.LN | L.AMC | 6 | MQG.AU | L.DCM | 0.189807 | INL.SJ | L.DCM | 0.047073 | |

| RAT.LN | L.AMC | 0.004950 | CHIB.PM | L.DB | 6 | TRST.US | L.TMF | 0.187221 | BPOP.US | L.RB | 0.045089 | |

| BNII.IJ | L.DB | 0.004587 | DBK.GR | L.DCM | 6 | 165.HK | L.DCM | 0.180399 | BGCP.US | L.IBB | 0.043087 | |

| LM.US | L.AMC | 0.004464 | KN.FP | L.DCM | 6 | ALPHA.GA | L.DB | 0.174612 | HB.CY | L.DB | 0.039755 | |

| 2013 | LM.US | L.AMC | 0.005587 | LM.US | L.AMC | 10 | MTG.US | L.TMF | 0.211206 | BCBB.BG | S.DB | 0.050632 |

| VONN.SW | L.AMC | 0.005291 | ALPHA.GA | L.DB | 8 | SNV.US | L.RB | 0.199877 | SCB.TB | L.DB | 0.047976 | |

| ALPHA.GA | L.DB | 0.004831 | SANTGRU.CI | L.AMC | 6 | BIM.IM | L.IBB | 0.199045 | NBKE.EY | S.DB | 0.039395 | |

| SANTGRU.CI | L.AMC | 0.004525 | 165.HK | L.DCM | 5 | BYLK.US | S.RB | 0.193692 | 21080.KS | S.AMC | 0.038239 | |

| 165.HK | L.DCM | 0.004405 | MTG.US | L.TMF | 5 | 21080.KS | S.AMC | 0.190409 | BIM.IM | L.IBB | 0.037467 | |

| DBK.GR | L.DCM | 0.004255 | VONN.SW | L.AMC | 4 | 8614.JP | S.IBB | 0.187220 | BSF.US | S.TMF | 0.034415 | |

| 2014 | VONN.SW | L.AMC | 0.004808 | VONN.SW | L.AMC | 7 | PRO.IM | S.IBB | 0.208298 | BGCP.US | L.IBB | 0.048682 |

| 8595.JP | L.AMC | 0.004505 | RAT.LN | L.AMC | 6 | CFFI.US | S.RB | 0.205214 | NYCB.US | L.TMF | 0.040771 | |

| SANTGRU.CI | L.AMC | 0.004274 | SANTGRU.CI | L.AMC | 5 | INL.SJ | L.DCM | 0.203851 | LD.FP | S.TMF | 0.040653 | |

| CHIB.PM | L.DB | 0.004098 | BAP.US | L.DB | 5 | PGR.SJ | S.AMC | 0.198631 | PGR.SJ | S.AMC | 0.038840 | |

| FII.US | L.AMC | 0.003906 | SBIN.IN | L.DB | 5 | BYLK.US | S.RB | 0.192585 | BCBB.BG | S.DB | 0.035816 | |

| 8616.JP | L.IBB | 0.003817 | 8595.JP | L.AMC | 4 | 165.HK | L.DCM | 0.192335 | ALPHA.GA | L.DB | 0.032856 |

References

- Abedifar, Pejman, Paolo Giudici, and Shatha Qamhieh Hashem. 2017. Heterogeneous market structure and systemic risk: Evidence from dual banking systems. Journal of Financial Stability 33: 96–119. [Google Scholar] [CrossRef] [Green Version]

- Acharya, Viral, Robert Engle, and Matthew Richardson. 2012. Capital shortfall: A new approach to ranking and regulating systemic risks. American Economic Review 102: 59–64. [Google Scholar] [CrossRef] [Green Version]

- Acharya, Viral V., Lasse H. Pedersen, Thomas Philippon, and Matthew Richardson. 2017. Measuring systemic risk. The Review of Financial Studies 30: 2–47. [Google Scholar] [CrossRef]

- Adrian, Tobias, and Markus K. Brunnermeier. 2016. CoVaR. American Economic Review 106: 1705–41. [Google Scholar] [CrossRef]

- Ahelegbey, Daniel Felix, Monica Billio, and Roberto Casarin. 2016. Bayesian graphical models for structural vector autoregressive processes. Journal of Applied Econometrics 31: 357–86. [Google Scholar] [CrossRef] [Green Version]

- Allen, Franklin, Ana Babus, and Elena Carletti. 2012. Asset commonality, debt maturity and systemic risk. Journal of Financial Economics 104: 519–34. [Google Scholar] [CrossRef]

- Allen, Franklin, and Anthony M Santomero. 2001. What do financial intermediaries do? Journal of Banking & Finance 25: 271–94. [Google Scholar] [CrossRef] [Green Version]

- Amini, Hamed, Rama Cont, and Andreea Minca. 2016. Resilience to contagion in financial networks. Mathematical Finance 26: 329–65. [Google Scholar] [CrossRef] [Green Version]

- Arakelian, Veni, Paolo Giudici, and Shatha Qamhieh. 2019. Online Supplementary Material for “The Leaders, the Laggers and the Vulnerables”. Available online: https://www.researchgate.net/publication/332781875_Online_Supplementary_Material_for_The_Leaders_the_Laggers_and_the_Vulnerables (accessed on 11 March 2020).

- Artzner, Philippe, Freddy Delbaen, Jean-Marc Eber, and David Heath. 1999. Coherent measures of risk. Mathematical Finance 9: 203–28. [Google Scholar] [CrossRef]

- Avdjiev, Stefan, Paolo Giudici, and Alessandro Spelta. 2019. Measuring contagion risk in international banking. Journal of Financial Stability 42: 36–51. [Google Scholar] [CrossRef] [Green Version]

- Bartram, Söhnke M., Gregory W. Brown, and John E. Hund. 2007. Estimating systemic risk in the international financial system. Journal of Financial Economics 86: 835–69. [Google Scholar] [CrossRef] [Green Version]

- Battiston, Stefano, Domenico Delli Gatti, Mauro Gallegati, Bruce Greenwald, and Joseph E. Stiglitz. 2012. Liaisons dangereuses: Increasing connectivity, risk sharing, and systemic risk. Journal of Economic Dynamics & Control 36: 1121–41. [Google Scholar] [CrossRef] [Green Version]

- Battiston, Stefano, Michelangelo Puliga, Rahul Kaushik, Paolo Tasca, and Guido Caldarelli. 2012. Debtrank: Too central to fail? financial networks, the fed and systemic risk. Scientific Reports 2: 541. [Google Scholar] [CrossRef] [Green Version]

- Benoit, Sylvain, Gilbert Colletaz, Christophe Hurlin, and Christophe Pérignon. 2013. A Theoretical and Empirical Comparison of Systemic Risk Measures. HEC Paris Research Paper No. FIN-2014-1030. Jouy-en-Josas: HEC Paris. [Google Scholar]

- Benoit, Sylvain, Jean-Edouard Colliard, Christophe Hurlin, and Christophe Pérignon. 2017. Where the risks lie: A survey on systemic risk. Review of Finance 21: 109–52. [Google Scholar] [CrossRef]

- Benoit, Sylvain, Christophe Hurlin, and Christophe Pérignon. 2019. Pitfalls in systemic-risk scoring. Journal of Financial Intermediation 38: 19–44. [Google Scholar] [CrossRef]

- Berger, Allen N., and Christa H. S. Bouwman. 2009. Bank liquidity creation. Review of Financial Studies 22: 3779–837. [Google Scholar] [CrossRef] [Green Version]

- Bhattacharya, Sudipto, and Anjan V. Thakor. 1993. Contemporary banking theory. Journal of Financial Intermediation 3: 2–50. [Google Scholar] [CrossRef]

- Billio, Monica, Mila Getmansky, Andrew W. Lo, and Loriana Pelizzon. 2012. Econometric measures of connectedness and systemic risk in the finance and insurance sectors. Journal of Financial Economics 104: 535–59. [Google Scholar] [CrossRef]

- Brewer, Elijah, and Ann Marie Klingenhagen. 2010. Be careful what you wish for: The stock market reactions to bailing out large financial institutions. Journal of Financial Regulation and Compliance 18: 56–69. [Google Scholar] [CrossRef]

- Brownlees, Christian T., and Robert F. Engle. 2012. Volatility, Correlation and Tails for Systemic Risk Measurement. Working Paper. NYU. [Google Scholar]

- Brownlees, Christian T., and Robert F. Engle. 2017. SRISK: A Conditional Capital Shortfall Measure of Systemic Risk. The Review of Financial Studies 30: 48–79. [Google Scholar] [CrossRef]

- Brunnermeier, Markus K., and Patrick Cheridito. 2019. Measuring and allocating systemic risk. Risks 7: 46. [Google Scholar] [CrossRef] [Green Version]

- Calabrese, Raffaella, and Paolo Giudici. 2015. Estimating bank default with generalised extreme value regression models. Journal of the Operational Research Society 66: 1783–92. [Google Scholar] [CrossRef] [Green Version]

- Caporale, Guglielmo Maria, Andrea Cipollini, and Nicola Spagnolo. 2005. Testing for contagion: A conditional correlation analysis. Journal of Empirical Finance 12: 476–89. [Google Scholar] [CrossRef]

- Chiang, Thomas C., Bang Nam Jeon, and Huimin Li. 2007. Dynamic correlation analysis of financial contagion: Evidence from Asian markets. Journal of International Money and Finance 26: 1206–28. [Google Scholar] [CrossRef]

- Chowdhury, Biplob, Mardi Dungey, Moses Kangogo, Mohammad Abu Sayeed, and Vladimir Volkov. 2019. The changing network of financial market linkages: The asian experience. International Review of Financial Analysis 64: 71–92. [Google Scholar] [CrossRef] [Green Version]

- Danielsson, Jon, Kevin R. James, Marcela Valenzuela, and Ilknur Zer. 2016. Model risk of risk models. Journal of Financial Stability 23: 79–91. [Google Scholar] [CrossRef] [Green Version]

- Dawid, A. Philip, and Steffen L. Lauritzen. 1993. Hyper Markov laws in the statistical analysis of decomposable graphical models. Ann. Statist. 21: 1272–317. [Google Scholar] [CrossRef]

- DeMiguel, Victor, Francisco J. Nogales, and Raman Uppal. 2014. Stock return serial dependence and out-of-sample portfolio performance. The Review of Financial Studies 27: 1031–73. [Google Scholar] [CrossRef]

- Diebold, Francis, and Kamil Yilmaz. 2014. On the Network Topology of Variance Decompositions: Measuring the Connectedness of Financial Firms. Journal of Econometrics 182: 119–34. [Google Scholar] [CrossRef] [Green Version]

- Ding, Dong, and Robin C. Sickles. 2018. Frontier efficiency, capital structure, and portfolio risk: An empirical analysis of u.s. banks. BRQ Business Research Quarterly 21: 262–77. [Google Scholar] [CrossRef]

- Eisenberg, Larry, and Thomas H. Noe. 2001. Systemic risk in financial systems. Management Science 47: 236–49. [Google Scholar] [CrossRef]

- Elliott, Matthew, Benjamin Golub, and Matthew O. Jackson. 2014. Financial Networks and Contagion. American Economic Review 104: 3115–53. [Google Scholar] [CrossRef] [Green Version]

- Engle, Robert. 2002. Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models. Journal of Business & Economic Statistics 20: 339–50. [Google Scholar] [CrossRef]

- Engle, Robert, and Kevin Sheppard. 2001. Theoretical and Empirical Properties of Dynamic Conditional Correlation Multivariate GARCH. NBER Working Paper No. w8554. Cambridge: National Bureau of Economic Research. [Google Scholar] [CrossRef]

- Engle, Robert F. 2012. Dynamic conditional beta. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Farhi, Emmanuel, and Jean Tirole. 2012. Collective moral hazard, maturity mismatch, and systemic bailouts. American Economic Review 102: 60–93. [Google Scholar] [CrossRef] [Green Version]

- Gennaioli, Nicola, Andrei Shliefer, and Robert W. Vishny. 2013. A model of shadow banking. Journal of Finance 68: 1331–63. [Google Scholar] [CrossRef] [Green Version]

- Giudici, Paolo, and Peter J. Green. 1999. Decomposable graphical gaussian model determination. Biometrika 86: 785–801. [Google Scholar] [CrossRef] [Green Version]

- Giudici, Paolo, and Alessandro Spelta. 2016. Graphical network models for international financial flows. Journal of Business & Economic Statistics 34: 128–38. [Google Scholar] [CrossRef]

- Gofman, Michael. 2017. Efficiency and stability of a financial architecture with too-interconnected-to-fail institutions. Journal of Financial Economics 124: 113–46. [Google Scholar] [CrossRef]

- Hashem, Shatha Qamhieh, and Paolo Giudici. 2016. NetMES: A network based marginal expected shortfall measure. The Journal of Network Theory in Finance 2: 1–36. [Google Scholar] [CrossRef]

- Heiberger, Raphael H. 2014. Stock network stability in times of crisis. Physica A: Statistical Mechanics and Its Applications 393: 376–81. [Google Scholar] [CrossRef]

- Hou, Kewei. 2007. Industry information diffusion and the lead-lag effect in stock returns. Review of Financial Studies 20: 1113–38. [Google Scholar] [CrossRef]

- Idier, Julien, Gildas Lamé, and Jean-Stéphane Mésonnier. 2014. How useful is the marginal expected shortfall for the measurement of systemic exposure. Journal of Banking & Finance 47: 134–46. [Google Scholar] [CrossRef] [Green Version]

- Kashyap, Anil K., Raghuram Rajan, and Jeremy C. Stein. 2002. Banks as liquidity providers: An explanation for the coexistence of lending and deposit-taking. The Journal of Finance 57: 33–74. [Google Scholar] [CrossRef] [Green Version]

- Kinnunen, Jyri. 2017. Dynamic cross-autocorrelation in stock returns. Journal of Empirical Finance 40: 162–73. [Google Scholar] [CrossRef]

- Laeven, Luc, Lev Ratnovski, and Hui Tong. 2016. Bank size, capital, and systemic risk: Some international evidence. Journal of Banking & Finance 69: S25–S34. [Google Scholar] [CrossRef]

- Laopodis, Nikiforos T. 2016. Industry returns, market returns and economic fundamentals: Evidence for the united states. Economic Modelling 53: 89–106. [Google Scholar] [CrossRef]

- Lauritzen, Steffen L. 1996. Graphical Models. Oxford Statistical Science Series; Oxford: Clarendon Press. [Google Scholar]

- Lehar, Alfred. 2005. Measuring systemic risk: A risk management approach. Journal of Banking & Finance 29: 2577–603. [Google Scholar] [CrossRef] [Green Version]

- Lo, Andrew W., and A. Craig MacKinlay. 1990. When are contrarian profits due to stock market overreaction? Review of Financial Studies 3: 175–205. [Google Scholar] [CrossRef]

- Malevergne, Yannick, and Didier Sornette, eds. 2006. Extreme Financial Risks: From Dependence to Risk Management. Berlin and Heidelberg: Springer. [Google Scholar] [CrossRef]

- Markowitz, Harry. 1952. Portfolio selection: Efficient diversification of investments. The Journal of Finance 7: 77–91. [Google Scholar] [CrossRef]

- Minoiu, Camelia, and Javier A. Reyes. 2013. A network analysis of global banking: 1978–2010. Journal of Financial Stability 9: 168–84. [Google Scholar] [CrossRef]

- Qin, Xiao, and Chen Zhou. 2013. Systemic Risk Allocation for Systems with a Small Number of Banks. DNB Working Papers No. 378. Amsterdam: Netherlands Central Bank, Research Department. [Google Scholar]

- Roll, Richard. 1992. Industrial structure and the comparative behavior of international stock market indices. The Journal of Finance 47: 3–41. [Google Scholar] [CrossRef]

- Sandoval, Leonidas, and Italo De Paula Franca. 2012. Correlation of financial markets in times of crisis. Physica A: Statistical Mechanics and its Applications 391: 187–208. [Google Scholar] [CrossRef] [Green Version]

- Santomero, Anthony M. 1984. Modeling the banking firm: A survey. Journal of Money, Credit and Banking 16: 576–602. [Google Scholar] [CrossRef]

- Shleifer, Andrei, and Robert W. Vishny. 2010. Unstable banking. Journal of Financial Economics 97: 306–18. [Google Scholar] [CrossRef] [Green Version]

- Soramaki, Kimmo, and Samantha Cook. 2013. Sinkrank: An algorithm for identifying systemically important banks in payment systems. Open-Assessment E-Journal 7: 1–27. [Google Scholar] [CrossRef] [Green Version]

- Tarashev, Nikola, Claudio Borio, and Kostas Tsatsaronis. 2010. Attributing Systemic Risk to Individual Institutions. Bank for International Settlements Working Papers 308. Basel: Bank for International Settlements. [Google Scholar]

- Terraza, Virginie. 2015. The Effect of Bank Size on Risk Ratios: Implications of Banks’ Performance. Procedia Economics and Finance 30: 903–9. [Google Scholar] [CrossRef] [Green Version]

- Volcker, Paul. 2012. Unfinished business in financial reform. International Finance 15: 125–35. [Google Scholar] [CrossRef]

- Wagner, Wolf. 2010. Diversification at financial institutions and systemic crises. Journal of Financial Intermediation 19: 373–86. [Google Scholar] [CrossRef] [Green Version]

- Whittaker, Joe. 2009. Graphical Models in Applied Multivariate Statistics. Wiley Series in Probability and Mathematical Statistics; Chichester: John Wiley and Sons. [Google Scholar]

- Xu, Qifa, Mengting Li, Cuixia Jiang, and Yaoyao He. 2019. Interconnectedness and systemic risk network of chinese financial institutions: A LASSO-CoVaR approach. Physica A: Statistical Mechanics and its Applications 534: 122173. [Google Scholar] [CrossRef]

| 1. | The literature is vast. We refer to some papers that can navigate the reader who is interested in the literature of financial intermediation and the related topics, e.g., Santomero (1984), Bhattacharya and Thakor (1993), Allen and Santomero (2001), and Berger and Bouwman (2009). |

| 2. | The literature is vast. Among others, see Eisenberg and Noe (2001), Lehar (2005), Bartram et al. (2007), and Gofman (2017). |

| 3. | The homogeneity could be empowered by the tendency of financial institutions to hold the market portfolio as inclined by the modern portfolio theory Markowitz (1952) and by the deregulation following the Second Banking Directive of 1989 and the Gramm-Leach-Bliley Act (1999) (https://www.govinfo.gov/content/pkg/PLAW-106publ102/pdf/PLAW-106publ102.pdf) in Europe and the US. |

| 4. | For example, the Deutsche Boerse AG German Stock Index, DAX, is composed of 30 selected German blue-chip stocks, while the Russell 1000 Index is composed of the largest 1000 companies of Russell 3000, representing the universe of the large capitalization stocks from which most active money managers typically select. |

| 5. | Appendix ATable A1 contains the definitions of the groups according to GICS obtained from https://www.msci.com/gics and some examples. |

| 6. | Furthermore, considering that the Cholesky decomposition of the variance-covariance matrix is See, Benoit et al. (2013). |

| 7. | For details of the proof, see Benoit et al. (2013). |

| 8. | For brevity, we use the terms “large cap” and “small cap” instead of the terms “large cap survived financial institutions” and “small cap survived financial institutions”. |

| 9. | See Table A3. We estimated the financial leverage as the ratio of the sum of short and long term debt and market capitalization, divided by market capitalization. |

| 10. | We acknowledge the fact that the systemic risk measures did not identify simultaneously a financial institution as a top SIFI, as it was addressed by some papers in the literature, e.g., Danielsson et al. (2016), Benoit et al. (2013). |

| 11. | We selected the top six financial institutions from both the large and the small cap groups. |

| 12. | The state coordinated restructuring of Natixis precipitated the merger of its two parent groups to form the newly branded B.P.C.E. group in February 2009. In August 2009, the French investment bank Natixis said that its partially state-owned parent company would guarantee about €35 billion in toxic assets on its books, in what amounted to a government-engineered reinforcement of its troubled finances. B.P.C.E., which held 70% of Natixis, guaranteed the loans, equivalent to $50 billion, in exchange for fees of €48 million a year. The parent took on the risk for 85% of the assets, with Natixis holding the remaining 15%. Natixis reported a second-quarter loss of 883 million euros. While that was down from a loss of more than €1 billion for the same period last year, it marked the fifth straight losing quarter for Natixis, which continued to write down its monoline bond insurance portfolio, asset-backed securities, and collateralized debt obligations underpinned by subprime mortgages. |

| Financial Institution | Sub-Industry | Country | |

|---|---|---|---|

| Legg Mason Inc. | AMC | UNITED STATES | 3 |

| Jafco Co Ltd. | AMC | JAPAN | 3 |

| Santander Chile Holding SA | AMC | CHILE | 3 |

| VP Bank AG | AMC | LIECHTENSTEIN | 3 |

| Vontobel Holding AG | AMC | SWITZERLAND | 3 |

| Alpha Bank AE | DB | GREECE | 3 |

| Hellenic Bank PCL | DB | CYPRUS | 3 |

| Credicorp Ltd. | DB | PERU | 3 |

| Natixis SA | DCM | FRANCE | 3 |

| China Everbright Ltd. | DCM | HONG KONG | 3 |

| Investec Ltd. | DCM | SOUTH AFRICA | 3 |

| Macquarie Group Ltd. | DCM | AUSTRALIA | 3 |

| Mirae Asset Daewoo Co Ltd. | DCM | SOUTH KOREA | 3 |

| Deutsche Bank AG | DCM | GERMANY | 3 |

| Tokai Tokyo Financial Holdings Inc. | IBB | JAPAN | 3 |

| Goldman Sachs Group Inc/The, TD Ameritrade Holding Corp | IBB | UNITED STATES | 3 |

| Daiwa Securities Group Inc. | IBB | JAPAN | 3 |

| Caisse Regionale de Credit Agricole Mutuel de Paris et d’Ile-de-France | RB | FRANCE | 3 |

| Paragon Banking Group PLC | TMF | GREAT BRITAIN | 3 |

| MGIC Investment Corp, TrustCo Bank Corp NY, New York Community Bancorp Inc, Capitol Federal Financial Inc. | TMF | UNITED STATES | 3 |

| MLP SE | AMC | GERMANY | 2 |

| Allied Irish Banks PLC | DB | IRELAND | 2 |

| China Banking Corp | DB | PHILIPPINES | 2 |

| Swedbank AB | DB | SWEDEN | 2 |

| Investment Technology Group Inc. | IBB | UNITED STATES | 2 |

| Capital Securities Corp | IBB | TAIWAN | 2 |

| Caisse Regionale de Credit Agricole Mutuel Alpes Provence | RB | FRANCE | 2 |

| Oldenburgische Landesbank AG | RB | GERMANY | 2 |

| Public Financial Holdings Ltd. | RB | HONG KONG | 2 |

| Daishi Bank Ltd/The, Nishi-Nippon City Bank Ltd/The | RB | JAPAN | 2 |

| Federal Home Loan Mortgage Corp | TMF | UNITED STATES | 2 |

| Federated Investors Inc. | AMC | UNITED STATES | 2 |

| Rathbone Brothers PLC | AMC | GREAT BRITAIN | 2 |

| RHB Capital Bhd | DB | MALAYSIA | 2 |

| Bank Maybank Indonesia Tbk PT | DB | INDONESIA | 2 |

| CIMB Group Holdings Bhd | DB | MALAYSIA | 2 |

| Bank Cler AG | DB | SWITZERLAND | 2 |

| KB Securities Co Ltd. | IBB | SOUTH KOREA | 2 |

| Minato Bank Ltd/The | RB | JAPAN | 2 |

| Popular Inc. | RB | PUERTO RICO | 2 |

| First Midwest Bancorp Inc/IL, Synovus Financial Corp, UMB Financial Corp, 1st Source Corp | RB | UNITED STATES | 2 |

| Bank of America Corp | DB | UNITED STATES | 1 |

| Scotiabank Peru SAA | DB | PERU | 1 |

| TMB Bank PCL | DB | THAILAND | 1 |

| Mediobanca Banca di Credito Finanziario SpA | DB | ITALY | 1 |

| AFFIN Holdings Bhd | DB | MALAYSIA | 1 |

| BMCE Bank | DB | MOROCCO | 1 |

| Astoria Financial Corp | TMF | UNITED STATES | 1 |

| Aberdeen Asset Management PLC | AMC | GREAT BRITAIN | 1 |

| KBC Group NV | DB | BELGIUM | 1 |

| State Bank of India | DB | INDIA | 1 |

| BGC Partners Inc. | IBB | UNITED STATES | 1 |

| Marusan Securities Co Ltd. | IBB | JAPAN | 1 |

| BB&T Corp | RB | UNITED STATES | 1 |

| Piraeus Bank SA | DB | GREECE | 1 |

| Financial Institution | Sub-Industry | Country | |

|---|---|---|---|

| 180 Degree Capital Corp | AMC | UNITED STATES | 3 |

| Effecten-Spiegel AG, Deutsche Beteiligungs AG | AMC | GERMANY | 3 |

| FDG Kinetic Ltd. | AMC | HONG KONG | 3 |

| GSD Holding AS | DB | TURKEY | 3 |

| Bank Ochrony Srodowiska SA | DB | POLAND | 3 |

| Alandsbanken Abp | DB | FINLAND | 3 |

| Barclays Bank of Botswana Ltd. | DB | BOTSWANA | 3 |

| Oppenheimer Holdings Inc. | IBB | UNITED STATES | 3 |

| Banca Profilo SpA | IBB | ITALY | 3 |

| Charles Stanley Group PLC | IBB | GREAT BRITAIN | 3 |

| Toyo Securities Co Ltd. | IBB | JAPAN | 3 |

| Banestes SA Banco do Estado do Espirito Santo | RB | BRAZIL | 3 |

| Seacoast Banking Corp of Florida, FNCB Bancorp Inc. | RB | UNITED STATES | 3 |

| Locindus SA | TMF | FRANCE | 3 |

| Federal Agricultural Mortgage Corp, NASB Financial Inc, OceanFirst Financial Corp, Provident Financial Holdings Inc. | TMF | UNITED STATES | 3 |

| Street Capital Group Inc. | TMF | CANADA | 3 |

| Bear State Financial Inc. | TMF | UNITED STATES | 3 |

| Peregrine Holdings Ltd. | AMC | SOUTH AFRICA | 2 |

| Sparebanken Vest | DB | NORWAY | 2 |

| Asia Plus Group Holdings PCL | IBB | THAILAND | 2 |

| First United Corp, CommunityOne Bancorp | RB | UNITED STATES | 2 |

| Atinum Investment Co Ltd. | AMC | SOUTH KOREA | 2 |

| National Bank of Kuwait-Egypt SAE | DB | EGYPT | 2 |

| Lan & Spar Bank | DB | DENMARK | 2 |

| Berliner Effektengesellschaft AG | IBB | GERMANY | 2 |

| GronlandsBANKEN A/S | RB | GREENLAND | 2 |

| Capital City Bank Group Inc, Baylake Corp | RB | UNITED STATES | 2 |

| SHK Hong Kong Industries Ltd. | AMC | HONG KONG | 1 |

| KAS Bank NV | AMC | NETHERLANDS | 1 |

| Airesis SA | AMC | SWITZERLAND | 1 |

| Norvestia Oyj | AMC | FINLAND | 1 |

| Sparebanken Ost | DB | NORWAY | 1 |

| Takagi Securities Co Ltd. | IBB | JAPAN | 1 |

| Cie Financiere Tradition SA | IBB | SWITZERLAND | 1 |

| South China Financial Holdings Ltd. | IBB | HONG KONG | 1 |

| Bryn Mawr Bank Corp, Cascade Bancorp, Commercial National Financial Corp/PA, Peoples Financial Corp/MS, C&F Financial Corp, Independent Bank Corp/MI, First Community Bancshares Inc/VA, First South Bancorp Inc/NC, Financial Institutions Inc, Heritage Commerce Corp, HopFed Bancorp Inc, MainSource Financial Group Inc, Pacific Continental Corp, Sun Bancorp Inc/NJ | RB | UNITED STATES | 1 |

| Tsukuba Bank Ltd. | RB | JAPAN | 1 |

| Sachsenmilch AG | AMC | GERMANY | 1 |

| Peapack Gladstone Financial Corp | RB | UNITED STATES | 1 |

| First US Bancshares Inc. | UNITED STATES | 1 | |

| KAF-Seagroatt & Campbell Bhd | IBB | MALAYSIA | 1 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Arakelian, V.; Qamhieh Hashem, S. The Leaders, the Laggers, and the “Vulnerables”. Risks 2020, 8, 26. https://doi.org/10.3390/risks8010026

Arakelian V, Qamhieh Hashem S. The Leaders, the Laggers, and the “Vulnerables”. Risks. 2020; 8(1):26. https://doi.org/10.3390/risks8010026

Chicago/Turabian StyleArakelian, Veni, and Shatha Qamhieh Hashem. 2020. "The Leaders, the Laggers, and the “Vulnerables”" Risks 8, no. 1: 26. https://doi.org/10.3390/risks8010026

APA StyleArakelian, V., & Qamhieh Hashem, S. (2020). The Leaders, the Laggers, and the “Vulnerables”. Risks, 8(1), 26. https://doi.org/10.3390/risks8010026