Thermoeconomic Modeling as a Tool for Internalizing Carbon Credits into Multiproduct System Analysis

, and

, and

Abstract

1. Introduction

2. Thermoeconomic Modeling

2.1. Conventional Modeling

2.2. Inclusion of Monetary Costs of Environmental Charges

Inclusion of Carbon Credits

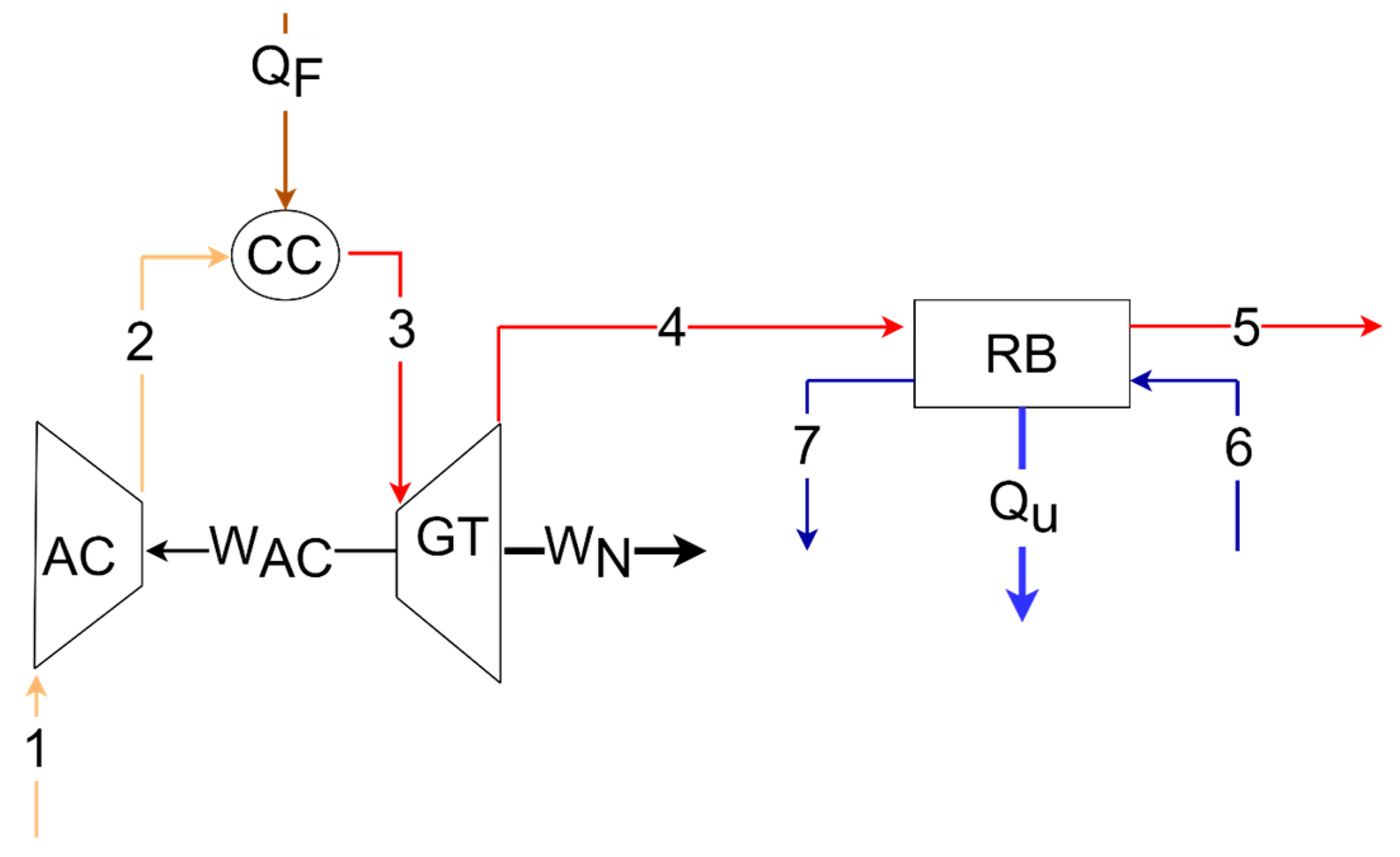

3. Case Study—Gas Turbine Cogeneration System

3.1. Thermoeconomic Models

- Process 1–2 corresponds to the compressor, with 1–2 s indicating isentropic compression.

- Process 2–3 represents the combustion chamber.

- Process 3–4 corresponds to the gas turbine, with 3–4 s denoting isentropic expansion.

- Process 4–5 corresponds to the recovery boiler.

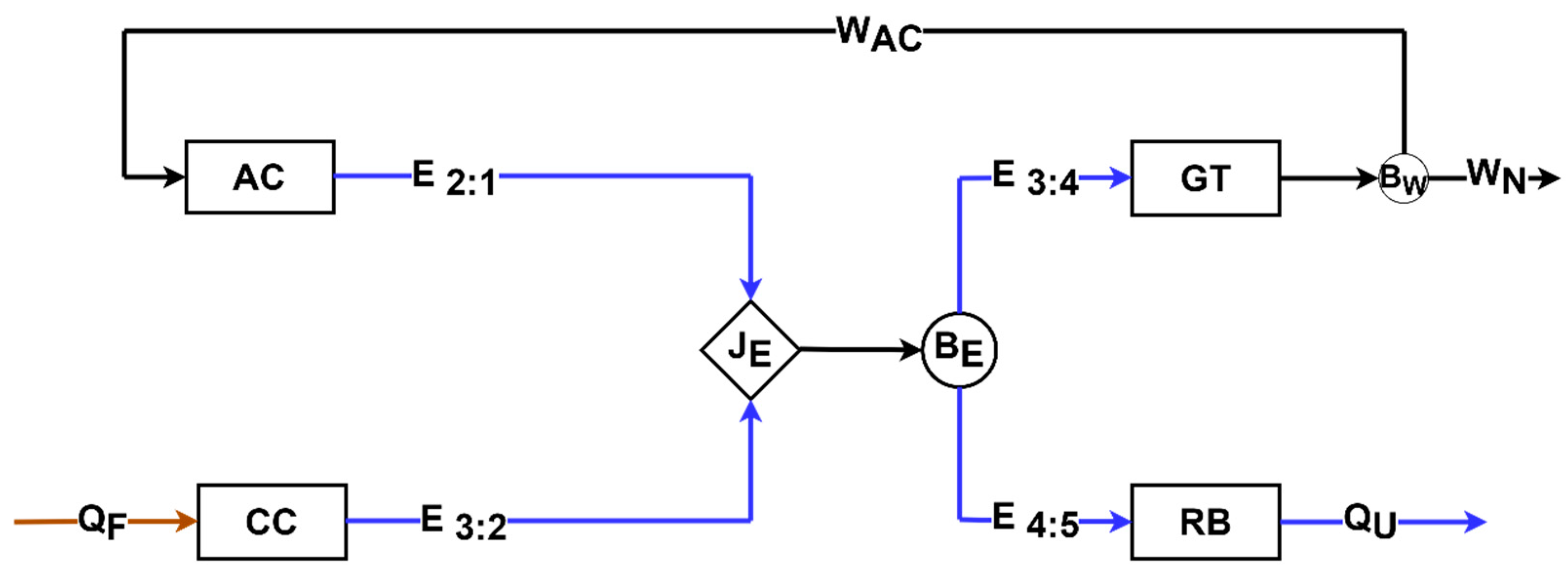

3.1.1. Productive Diagram

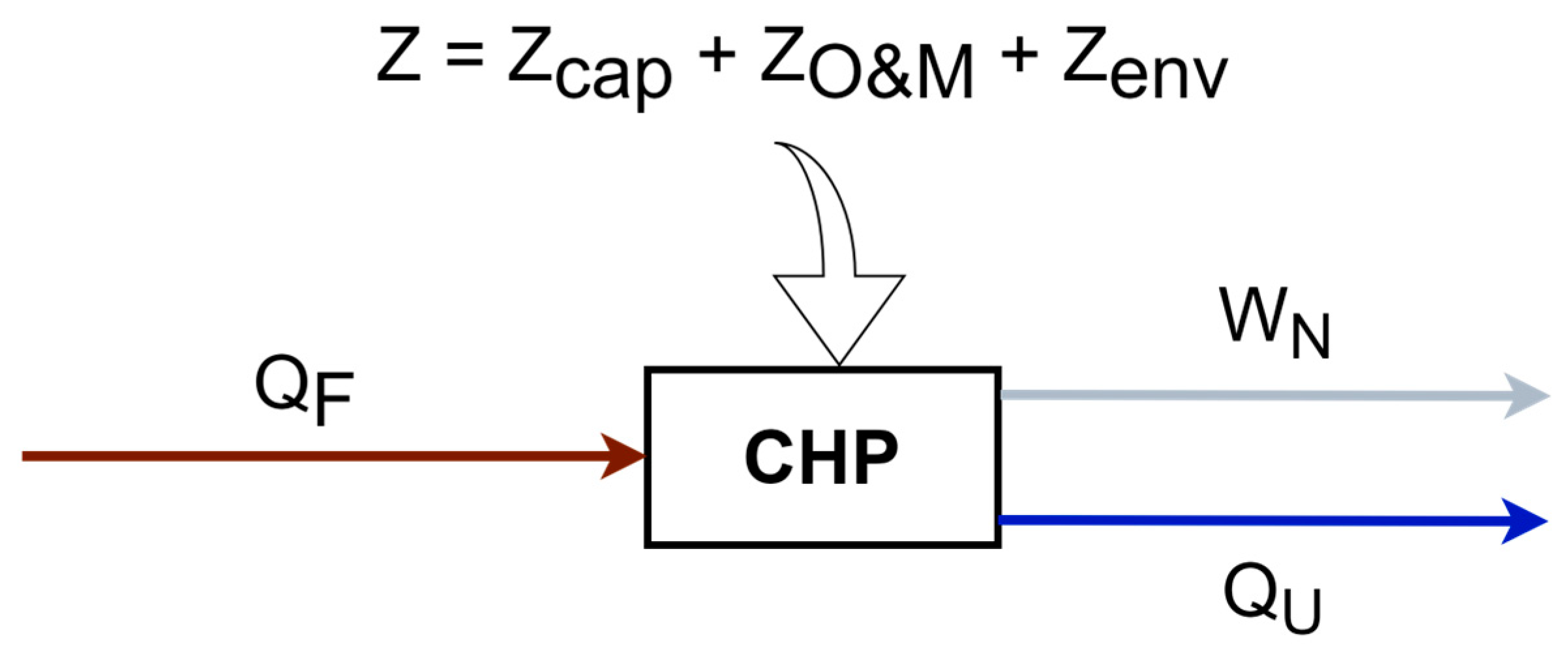

3.1.2. Monetary Cost Balance

- The environmental device (ENV) does not have any hourly costs related to capital and operations and maintenance (O&M). However, if environmental treatment equipment, which is not typically part of the physical structure of the system, is used, these costs can be considered within ;

- The expenses for licenses and permits associated with the environment are accounted for in the term;

- Similarly, the costs related to the carbon market are also accounted for through the term. When there is revenue, this term is represented as negative, and when there are expenditures, it is represented as positive.

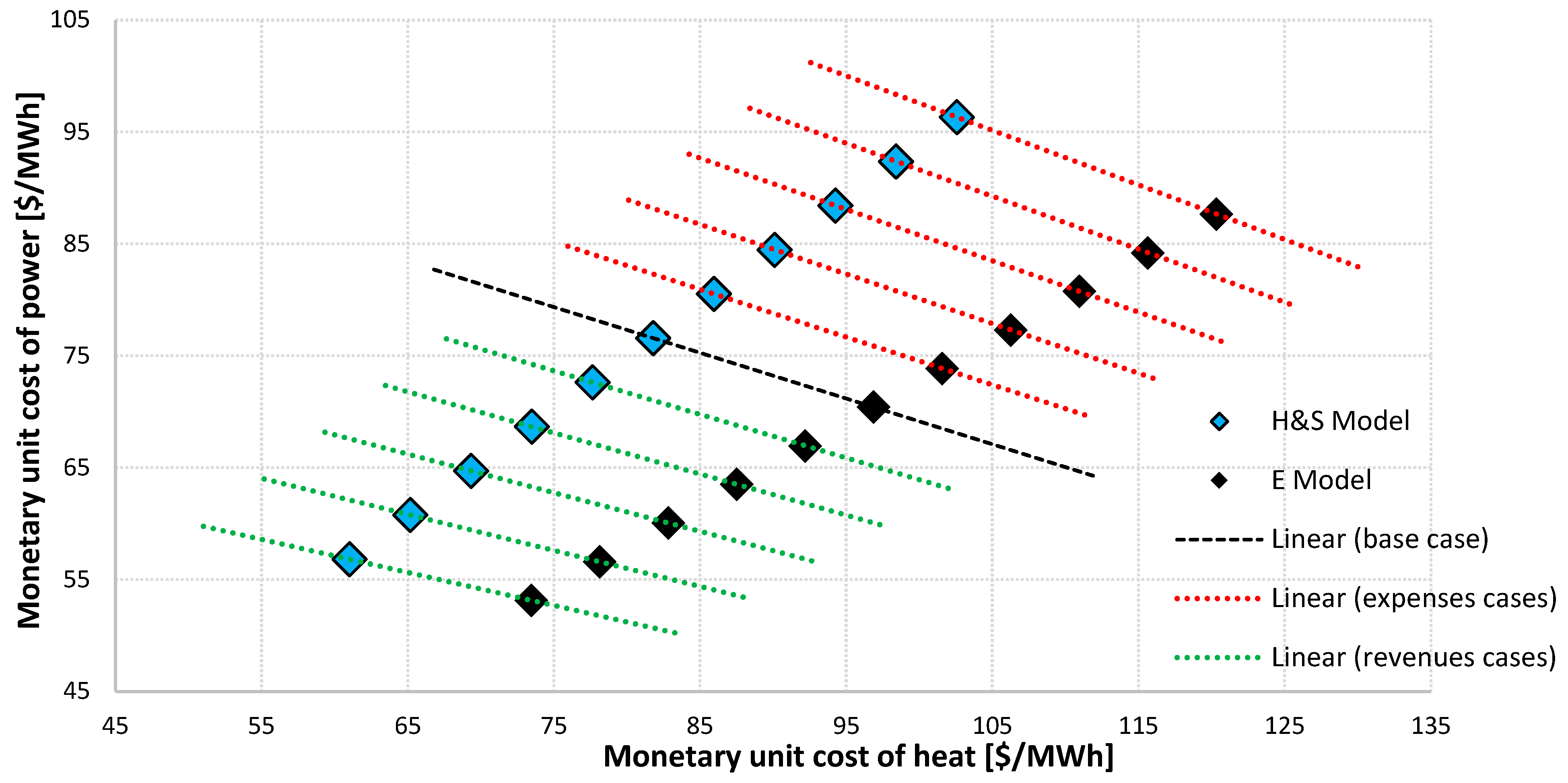

3.1.3. Results

4. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| AC | Air compressor |

| c | Monetary unit cost (USD/MWh) |

| CC | Combustion chamber |

| CCS | Carbon capture and storage |

| CEPCI | Chemical Engineering Cost Index |

| CHP | Combined heat and power |

| E | Exergy Flow (kW) |

| ENV | Environmental device |

| GHG | Greenhouse gas |

| GT | Gas turbine |

| IPCC | Intergovernmental Panel on Climate Change |

| JB | Junction–bifurcation |

| Exergetic unit cost (kW/kW) | |

| Q | Heat (exergy) (kW) |

| RB | Recovery boiler |

| W | Power (kW) |

| Y | Generic thermodynamic magnitude (kW) |

| Z | Hourly equipment cost (USD/h) |

| Greek symbols | |

| Specific CO2 emission (g/MWh) | |

| Subscripts and superscripts | |

| 0 | Reference conditions |

| CH | Chemical exergy (kW) |

| Env | Environmental |

| F | Fuel |

| H | Enthalpic flow (kW) |

| i; j | Indexes for productive components |

| in | Inlet |

| N | Net |

| out | Outlet |

| PH | Physical exergy (kW) |

| S | Entropic flow (kW) |

| U | Useful heat |

References

- IPCC. Mitigation of Climate Change. 2022. Available online: https://report.ipcc.ch/ar6wg3/pdf/IPCC_AR6_WGIII_FinalDraft_FullReport.pdf (accessed on 9 May 2022).

- IEA. CO2 Emissions from Fuel Combustion: Overview-International Energy Agency; Paris. 2020. Available online: https://www.iea.org/reports/co2-emissions-from-fuel-combustion-overview (accessed on 28 April 2023).

- Instituto E+ Transição Energética. Manual de Termos e Conceitos: Transição Energética; Rio de Janeiro/RJ—Brasil. 2020. Available online: https://emaisenergia.org/publicacao/manual-de-termos-e-conceitos-transicao-energetica/ (accessed on 12 April 2023).

- SendeCO2. Available online: https://www.sendeco2.com/es/ (accessed on 18 March 2023).

- The World Bank. State and Trends of Carbon Pricing 2022; Washington, DC. 2022. Available online: https://openknowledge.worldbank.org/entities/publication/a1abead2-de91-5992-bb7a-73d8aaaf767f (accessed on 20 March 2023).

- IPCC. AR6 Synthesis Report Climate Change 2023. 2023. Available online: https://www.ipcc.ch/report/ar6/syr/ (accessed on 19 March 2023).

- Valero, A.; Serra, L.; Uche, J. Fundamentals of Exergy Cost Accounting and Thermoeconomics. Part I: Theory. J. Energy Resour. Technol. 2006, 128, 1–8. [Google Scholar] [CrossRef]

- von Spakovsky, M.R. Application of Engineering Functional Analysis to the Analysis and Optimization of the CGAM Problem. Energy 1994, 19, 343–364. [Google Scholar] [CrossRef]

- Dincer, İ.; Rosen, M.A. Exergy: Energy, Environment, and Sustainable Development, 1st ed.; Elsevier Science: Amsterdam, The Netherlands, 2007; ISBN 9780080445298. [Google Scholar]

- Palacios-Bereche, M.C.; Palacios-Bereche, R.; Ensinas, A.V.; Gallego, A.G.; Modesto, M.; Nebra, S.A. Brazilian Sugar Cane Industry—A Survey on Future Improvements in the Process Energy Management. Energy 2022, 259, 124903. [Google Scholar] [CrossRef]

- Man, Y.; Yan, Y.; Wang, X.; Ren, J.; Xiong, Q.; He, Z. Overestimated Carbon Emission of the Pulp and Paper Industry in China. Energy 2023, 273, 127279. [Google Scholar] [CrossRef]

- Mishra, R.; Singh, R.K.; Gunasekaran, A. Adoption of Industry 4.0 Technologies for Decarbonisation in the Steel Industry: Self-Assessment Framework with Case Illustration. Ann. Oper Res. 2023. [Google Scholar] [CrossRef]

- Faria, P.R.; dos Santos, R.G.; Santos, J.J.; Barone, M.A.; Miotto, B.M. On the Allocation of Residues Cost Using Conventional and Comprehensive Thermoeconomic Diagrams. Int. J. Thermodyn. 2021, 24, 134–149. [Google Scholar] [CrossRef]

- Barone, M.A.; dos Santos, R.G.; Faria, P.R.; Lorenzoni, R.A.; Lourenço, A.B.; Santos, J.J.C.S. On the Arbitrariness and Complexity in Thermoeconomics Due to Waste Cost and Supplementary Firing Treatment. Eng. Sci. 2022, 17, 328–342. [Google Scholar] [CrossRef]

- Faria, P.R.; dos Santos, R.G.; Santos, J.J.C.S.; Barone, M.A.; Miotto, B.M.F. On the Allocation of Residues Cost in Thermoeconomics Using a Comprehensive Diagram. In Proceedings of the ECOS 2020—The 33rd International Conference on Efficiency, Cost, Optimization, Simulation and Environmental Impact of Energy Systems, Osaka, Japan, 29 June–3 July 2020; pp. 2444–2456. [Google Scholar]

- Cerqueira, S.A.A.G.; Nebra, S.A. Cost Attribution Methodologies in Cogeneration Systems. Energy Convers. Manag. 1999, 40, 1587–1597. [Google Scholar] [CrossRef]

- Modesto, M.; Nebra, S.A. Analysis of a Repowering Proposal to the Power Generation System of a Steel Mill Plant through the Exergetic Cost Method. Energy 2006, 31, 3261–3277. [Google Scholar] [CrossRef]

- Santos, R.G.; Faria, P.R.; Santos, J.J.C.S.; da Silva, J.A.M. Thermoeconomic Modeling for CO2 Allocation in Steam and Gas Turbine Cogeneration Systems. In Proceedings of the ECOS 2015—The 28th International Conference on Efficiency, Cost, Optimization, Simulation and Environmental Impact of Energy Systems, Pau, France, 29 June–3 July 2015. [Google Scholar]

- Faria, P.R.; Barone, M.A.; Santos, R.G.; Santos, J.J.C.S. The Environment as a Thermoeconomic Diagram Device for the Systematic and Automatic Waste and Environmental Cost Internalization in Thermal Systems. Renew. Sustain. Energy Rev. 2023, 171, 113011. [Google Scholar] [CrossRef]

- Faria, P.R.; Torres, C.; Santos, J.J.; Valero, A. On the Thermoeconomic Modelling of Thermal Waste Cost Allocation and Diagnosis of Malfunctions for Environmental Aspects Assessment. In Proceedings of the ECOS 2022—The 35th International Conference on Efficiency, Cost, Optimization, Simulation and Environmental Impact of Energy Systems, Copenhagen, Denmark, 3–7 July 2022. [Google Scholar]

- Fortes, A.F.C.; Carvalho, M.; da Silva, J.A.M. Environmental Impact and Cost Allocations for a Dual Product Heat Pump. Energy Convers. Manag. 2018, 173, 763–772. [Google Scholar] [CrossRef]

- Lozano, M.A.; Valero, A.; Serra, L.M. Theory of Exergetic Cost and Thermoeconomic Optimization. In Energy Systems and Ecology, Proceedings of the ENSEC’ 93: Energy Systems and Ecology: Proceedings of the International Conference: Cracow, Poland, 5–9 July 1993; Szargut, J., Kolenda, Z., Tsatsaronis, G., Ziebik, A., Eds.; University of Zaragoza: Zaragoza, Spain; Volume 1, pp. 339–350.

- Frangopoulos, C.A. Application of the Thermoeconomic Functional Approach to the CGAM Problem. Energy 1994, 19, 323–342. [Google Scholar] [CrossRef]

- Torres, C.; Valero, A.; Rangel, V.; Zaleta, A. On the Cost Formation Process of the Residues. Energy 2008, 33, 144–152. [Google Scholar] [CrossRef]

- F-Chart Software Engineering Equation Solver—EES 2017. Available online: http://www.fchart.com (accessed on 17 August 2022).

- Santos, J.J.C.S. Aplicação Da Neguentropia Na Modelagem Termoeconômica de Sistemas. Ph.D. Dissertation, Federal University of Itajubá, Itajubá, Brazil, 2009. (In Portuguese). [Google Scholar]

- Trading Economics. Available online: https://pt.tradingeconomics.com/commodity/natural-gas (accessed on 19 March 2023).

- Chemical Engineering CEPCI. Available online: https://www.chemengonline.com/category/business-economics/ (accessed on 19 March 2023).

- Valero, A.; Royo, J.; Lozano, M.A. The Characteristic Equation and Second Law Efficiency of Thermal Energy Systems. In Proceedings of the International Conference Second Law Analysis of Energy Systems: Towards the 21st Century, Rome, Italy, 5–7 July 1995; Sciubba, E., Moran, M.J., Eds.; La Sapienza: Rome, Italy, 1995; pp. 99–112. [Google Scholar]

- de Oliveira Junior, S. Exergy: Production, Cost and Renewability; Green Energy and Technology; Springer: London, UK, 2013; ISBN 978-1-4471-4164-8. [Google Scholar]

- Lazzaretto, A.; Tsatsaronis, G. SPECO: A Systematic and General Methodology for Calculating Efficiencies and Costs in Thermal Systems. Energy 2006, 31, 1257–1289. [Google Scholar] [CrossRef]

- Santos, R.G.; Faria, P.R.; Barone, M.A.; Lorenzoni, R.A.; Orozco, D.J.R.; Santos, J.J. On the Thermoeconomic Diagnosis through the Localized Physical Exergy Disaggregation for Dissipative Component Isolation. In Proceedings of the ECOS 2021—The 34th International Conference on Efficiency, Cost, Optimization, Simulation and Environmental Impact of Energy Systems, Taormina, Italy, 27 June–2 July 2021; Volume 1, pp. 450–461. [Google Scholar]

- dos Santos, R.G.; Lourenço, A.B.; Faria, P.R.; Barone, M.A.; Santos, J.J.C.S. A New Exergy Disaggregation Approach for Complexity Reduction and Dissipative Equipment Isolation in Thermoeconomics. Entropy 2022, 24, 1672. [Google Scholar] [CrossRef] [PubMed]

- Abreu, R.P.; Correia, V.H.L.; Lourenço, A.B.; Marques, A.d.S.; Carvalho, M. Thermoeconomic and Thermoenvironmental Analysis of the Chilled Water System in a Shopping Mall. Int. J. Refrig. 2022, 134, 304–311. [Google Scholar] [CrossRef]

- Santos, R.G.; Faria, P.R.; Santos, J.J.C.S.; Da Silva, J.A.M.; Donatelli, J.L.M. The Effect of the Thermodynamic Models on the Thermoeconomic Results for Cost Allocation in a Gas Turbine Cogeneration System. Rev. Eng. Térmica 2015, 14, 47. [Google Scholar] [CrossRef]

- Santos, R.G.; Lourenço, A.; Faria, P.R.; Barone, M.A.; Santos, J.J. A Comparative Study of a New Exergy Disaggregation Approach with Conventional Thermoeconomic Methodologies for Cost Allocation in an Organic Rankine Cycle Powered Vapor Compression Refrigeration System. In Proceedings of the ECOS 2022—The 35th International Conference on Efficiency, Cost, Optimization, Simulation and Environmental Impact of Energy Systems, Copenhagen, Denmark, 3–7 July 2022; pp. 1057–1068. [Google Scholar]

- Bhering Trindade, A.; Luiza Grillo Renó, M.; José Rúa Orozco, D.; Martín Martinez Reyes, A.; Aparecido Vitoriano Julio, A.; Carlos Escobar Palacio, J. Comparative Analysis of Different Cost Allocation Methodologies in LCA for Cogeneration Systems. Energy Convers. Manag. 2021, 241, 114230. [Google Scholar] [CrossRef]

- de Araújo, L.R.; Morawski, A.P.; Barone, M.A.; Donatelli, J.L.M.; Santos, J.J.C.S. On the Effects of Thermodynamic Assumptions and Thermoeconomic Approaches for Optimization and Cost Allocation in a Gas Turbine Cogeneration System. J. Braz. Soc. Mech. Sci. Eng. 2020, 42, 323–341. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Physical Flow | (kg/s) | T (°C) | P (bar) | |

|---|---|---|---|---|

| No. | Description | |||

| 1 | Air | 14.72 | 25.00 | 1.0132 |

| 2 | Air | 14.72 | 230.20 | 5.1040 |

| 3 | Gases | 14.94 | 850.00 | 4.8480 |

| 4 | Gases | 14.94 | 537.30 | 1.0207 |

| 5 | Gases | 14.94 | 151.10 | 1.0132 |

| 6 | Water | 2.487 | 60.00 | 20.400 |

| 7 | Steam | 2.487 | 212.4 | 20.000 |

| Equipment | Flow | Quantity (kW) |

|---|---|---|

| Air compressor (AC) | WAC | 3113.03 |

| Combustion chamber (CC) | QF | 11,630.96 |

| Gas turbine (GT) | WGT | 5546.50 |

| WN | 2433.47 | |

| Recovery boiler (RB) | QU | 2246.32 |

| Equipment | Z (USD/h) |

|---|---|

| Air compressor (AC) | 25.33 |

| Combustion chamber (CC) | 9.04 |

| Gas turbine (GT) | 34.37 |

| Recovery boiler (RB) | 21.71 |

| Emissions | E Model | H&S Model | Carbon Credit/Day | USD/Day | ||

|---|---|---|---|---|---|---|

| +50% | 120.33 | 87.66 | 102.57 | 96.32 | 26.7 | −2273 |

| +40% | 115.64 | 84.21 | 98.41 | 92.37 | 21.4 | −1818 |

| +30% | 110.95 | 80.76 | 94.26 | 88.42 | 16.0 | −1364 |

| +20% | 106.26 | 77.31 | 90.10 | 84.47 | 10.7 | −909 |

| +10% | 101.57 | 73.86 | 85.95 | 80.52 | 5.3 | −455 |

| Base case | 96.88 | 70.41 | 81.79 | 76.57 | 0 | 0 |

| −10% | 92.19 | 66.96 | 77.64 | 72.62 | 5.3 | 455 |

| −20% | 87.51 | 63.51 | 73.48 | 68.67 | 10.7 | 909 |

| −30% | 82.82 | 60.06 | 69.33 | 64.72 | 16.0 | 1364 |

| −40% | 78.14 | 56.6 | 65.17 | 60.77 | 21.4 | 1818 |

| −50% | 73.45 | 53.15 | 61.02 | 56.82 | 26.7 | 2273 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Santos, J.J.C.S.; Faria, P.R.d.; Chaves Belisario, I.; dos Santos, R.G.; Barone, M.A. Thermoeconomic Modeling as a Tool for Internalizing Carbon Credits into Multiproduct System Analysis. Processes 2024, 12, 705. https://doi.org/10.3390/pr12040705

Santos JJCS, Faria PRd, Chaves Belisario I, dos Santos RG, Barone MA. Thermoeconomic Modeling as a Tool for Internalizing Carbon Credits into Multiproduct System Analysis. Processes. 2024; 12(4):705. https://doi.org/10.3390/pr12040705

Chicago/Turabian StyleSantos, José Joaquim C. S., Pedro Rosseto de Faria, Igor Chaves Belisario, Rodrigo Guedes dos Santos, and Marcelo Aiolfi Barone. 2024. "Thermoeconomic Modeling as a Tool for Internalizing Carbon Credits into Multiproduct System Analysis" Processes 12, no. 4: 705. https://doi.org/10.3390/pr12040705

APA StyleSantos, J. J. C. S., Faria, P. R. d., Chaves Belisario, I., dos Santos, R. G., & Barone, M. A. (2024). Thermoeconomic Modeling as a Tool for Internalizing Carbon Credits into Multiproduct System Analysis. Processes, 12(4), 705. https://doi.org/10.3390/pr12040705