Abstract

Academic studies prior to the pandemic rather emphasized that the progression towards Industry 4.0 happened in an incremental manner. However, the extraordinary circumstances of the pandemic have led to considerable investments that were widely interpreted as a (generalized) digitalization push. However, little is known about the character of such investments and their effects. The goal of this contribution is to provide an empirically based overview of recent investment in digital technologies in six economic sectors of the German economy: mechanical engineering, chemicals, automotives, logistics, healthcare, and financial services. Based on 36 case studies and a survey at 540 companies, we investigate the following questions: 1. How much did the COVID-19 pandemic reduce existing obstacles for investments in digitalization measures? 2. Is there a universal digitalization push due to the COVID-19 pandemic that differs from the trajectory before the pandemic? The results show that the pandemic affected investment in an unequal manner. It was driven by the immediate need to sustain business operations through the virtualization of communication among employees and with external partners. However, there was less dynamism in shop-floor-related digitalization, as it was less related to epidemiological concerns and is more long-term in nature.

1. Introduction

In numerous commentaries, COVID-19 has been described as a tipping point with regard to the digital transformation of the economy and the workplace [1]. Indeed, there is little doubt that COVID-19 acted as a catalyst, as enterprises were forced to instantly move many activities online, thereby overcoming obstacles and reservations that had previously limited substantial steps towards virtual collaboration. As millions of white-collar workers were forced to work from home, it became evident that the technological foundations for remote collaboration were ready to use and that doing so would entail numerous opportunities to facilitate cooperation in the post-pandemic economy. However, remote work was not the only area in which such instantaneous innovation of business practices emerged. Restaurants, shops, public institutions, and industrial companies all had to quickly adapt to delivering goods and services especially under the condition of politically imposed contact restrictions, resorting to a number of digital tools, such as online shops and virtual customer interaction, to do so. The pandemic certainly ushered in a wave of improvisation and experimentation that helped digitalization to flourish.

“Digitalization”, however, has become a catch-all term that remains analytically shallow. According to a definition by the German business development bank KfW, digitalization can be understood as “projects for the introduction of digital technologies for the implementation or improvement of processes, products and services of a company and in contact with customers and suppliers” [2]. This definition is narrow in the sense that it only is concerned with the economic aspects that are touched by the application of digital technologies. Even so, it is a very broad definition referring to all kinds of application fields of digital—i.e., binary data processing—technologies. The term leaves open whether we deal with the introduction of industrial robots, the interaction of agents through the internet, remote communication through cloud infrastructures, the connection of devices through internet-of-things technology, or other aspects from the myriad of applications that are somehow connected to the term “digital”.

A more differentiated understanding of the recent changes in economic sectors, however, is meaningful for assessing their likely outcomes. It can be assumed that not every field of application in which digital technologies matter is affected equally. Can the pandemic even be characterized, as a recent survey concluded, as a push that is largely limited to aspects of communication, i.e., virtual interactions within and between companies ([3])? Even if we assume that the pandemic affected a broader set of digitalization themes, are there any new trends and technological fields that experienced particular investment? In particular: How do these changes relate to the fundamental assumption of a new era of digitalized manufacturing associated with the term “Industry 4.0”? These questions point to the need to go beyond linear assumptions of a comprehensive acceleration of digitalization through the pandemic. They concern the quality and the direction of the digital transformation of enterprises.

The goal of this contribution is to provide an empirically based anatomy of recent developments related to investment in digital technologies in industries, with a particular focus on so-called “Industry 4.0” technologies, by which we understand applications that take advantage of new technological possibilities through the internet of things and/or artificial intelligence. This article summarizes empirical data from six sectors of the German economy: mechanical engineering, chemicals, automotives, logistics, healthcare, and financial services. In particular, we want to answer the following questions:

- How much did the COVID-19 pandemic reduce existing obstacles to investments in digitalization measures?

- Is there a universal digitalization push due to the COVID-19 pandemic that differs from the digitalization trajectory before the pandemic?

The answers to these questions are of great relevance both at the level of theory and for practitioners. Theory-wise, they help to grasp the socio-technical realities of digitalization in the present period, i.e., the combination of technical, economic, and social factors that condition the ability of corporate actors to implement digital applications. The resulting empirically grounded assessment of current digitalization trends at companies also helps to assess the state of implementation and the scope of the so-called “Industry 4.0”, which we interpret as a narrative and a metaphor for diverse approaches related to new technological approaches based on the IoT and AI. Concrete assessments of the main trajectories of transformation in each economic sector that go beyond such narratives are important for practitioners in management, trade unions, and politics as they identify constraints, potentials, and possible fields of action.

This contribution is structured as follows: In Section 2, we discuss the state of digitalization in the German economy by introducing a pragmatist perspective that emphasizes the economic, institutional, and social conditions for progress towards “Industry 4.0”. In the third section, we provide an assessment of the pandemic as a dual crisis, i.e., a crisis in public health and the rippling effects of an economic crisis that was soon to be followed by recovery and growth. This perspective informs the empirical analysis in the sections thereafter, in which we discuss possible impacts on digitalization strategies that are related to the economic, institutional, and social fallout of the pandemic: We briefly summarize (Section 4) the qualitatively and quantitatively oriented research design and the chosen methods before (Section 5) discussing the mechanisms by which the pandemic affected the digitalization of enterprises based on an inductive analysis of material on the drivers and obstacles of digitalization from 36 company cases. In the penultimate section (Section 6), we identify and discuss the main areas of investment in digital technologies during the pandemic based on the qualitative and quantitative data from our investigation. In the discussion (Section 7), we interpret the findings as a layered progression of digitalization with investment in remote work and infrastructures at its core, complemented by the automation, digitalization, and virtualization of cognitive work, but with little activity at the level of the automation of physical processes and shop-floor-related applications. These results, as emphasized in the conclusion (Section 8), point to the need to contextualize the focus on manufacturing technologies inherent in the discourse on Industry 4.0 with a stronger consideration of the transformation of cognitive work and the associated organizational effects across different functions in enterprises.

2. Techno-Centric Narratives and Incremental Socio-Technical Change

The rapid development of a broad range of digital applications based on comprehensive methods for recording and processing data has created manifold possibilities concerning the automation, interconnection, and virtualization of processes in enterprises [4,5,6]. Beyond raising productivity, new possibilities for capturing economic value from data have resulted in the emergence of new business models through the supply of digital services and the rationalization of distribution through platforms [7,8].

In Germany, a coalition of industry associations, research institutions, and government agencies were vocal in framing certain aspects of this transformation as “Industry 4.0” and popularizing it as a stylized narrative, depicting a distinct stage of industrial development. It singled out the IoT and AI as base technologies and highlighted a bundle of digital applications that would engender leaps in productivity and enable companies to reconcile the conflicting imperatives of flexibility and productivity [9,10]. This narrative has a distinctively German flavor, emphasizing the legacy of “diversified quality production” [11] and identifying manufacturing as the main area of the digital transformation.

According to several accounts, the new industrial revolution did not live up to the initial expectations in the period preceding the pandemic. The patterns of change have been much more gradual than the narrative of Industry 4.0 would have it [12,13,14]. The diffusion of the new possibilities usually proceeds not in a revolutionary way, but rather on a pragmatic and incremental trajectory, through trial and error, as enterprises experiment with single applications from a ‘bundle of new technologies’ that mostly constitute specific modifications of existing production models, rather than a new paradigm [15]. A leading representative of the machine builders’ association (VDMA) even summarized the state of affairs in this key sector of the German economy by speaking of “ten lost years” since the initial proclamation of Industry 4.0. He emphasized that productivity growth has remained flat and said that there had been little progress in the bulk of enterprises, except for the flagship projects by technological leaders [16]. If the progress of digitalization across all sectors in the economy is concerned, the state of affairs in Germany seems to be even more critical: For an index on the levels of digitalization in Europe published by the European Commission, Germany is listed in the 18th position, with a substantial gap between it and the leading economies of Ireland, Finland, Belgium, and the Netherlands, and even behind economies such as those of the Czech Republic, Spain, and Slovenia (DESI 2020). In the period preceding the pandemic, several studies reported a slowdown in investment in digitalization at enterprises due to the then-looming recession (KfW 2021).

Gradualism is a key characteristic of any major period of socio-technical change. In fact, industrial revolutions should be thought of not as a big bang with immediate impact, but as a long-term period of accelerated innovation that involves experimentalism and micro-innovations that amount to a predominance of incremental modes of change [17,18]. However, the gap between high expectations about an imminent industrial revolution and the slow and uneven implementation of new digital technologies at enterprises puts the very essence of techno-optimist predictions into question. It warrants explanations that concern not only the state of technological innovation, but also the social processes concerning the implementation of technologies.

Existing knowledge about the barriers to digitalization processes in industrial companies is being generated from a vast pool of case studies from diverse industries and regions. Despite the high significance of the issue for practitioners and its prominence in political discourse, there have been few meta-analyses that have caused the findings to converge towards a more general understanding. In Table 1, we compare the frameworks of two available meta-studies on the subject [19,20].

Table 1.

Meta-studies on categories for barriers to digitalization in industries.

Although the framing of the findings in both studies is not identical, there is remarkable congruence among the key dimensions that affect the implementation of digital technologies. We expect that these dimensions also conditioned the implementation of digital technologies during the COVID-19 pandemic. However, we hypothesize that the malleability of these factors varies with regard to their relationship to the specific constellation brought about by the pandemic and the ability to overcome limitations within a short timeframe. In what follows, we provide a short general understanding of the effects of the COVID-19 crisis before progressing toward an empirical understanding of the drivers and obstacles in this specific context.

3. COVID-19 as a Dual Crisis

In order to identify how much and in what areas the pandemic acted as a catalyst for investment in digital technologies, we need to assess how the pandemic modified or reduced the aforementioned obstacles to the implementation of technologies. To fully grasp the impact of the pandemic, an understanding of COVID-19 as a double crisis with a health and an economic dimension is needed.

The first dimension is the health crisis, which resulted in widespread interruptions of interpersonal contacts. The immediate results of this were closures of factories, stores, and offices, disruptions in supply chains, the quick expansion of remote work, and a surge in e-commerce. COVID-19 thus demonstrated the merits of moving cognitive interactions and business transactions online wherever possible. The historic coincidence is remarkable: The sudden demand for the virtualization of social relations emerged in a situation where many of the applications that were needed to do so were already at an inflection point. An abstract possibility, therefore, became an imperative during various lockdowns and pushed the everyday use of digital applications considerably beyond the limits that had existed before. COVID-19 was also a stress test for all kinds of digital applications, including the IT infrastructure, video conferencing tools, and many other applications that facilitated the virtualization of tasks. This also convinced users that these tools could actually be applied and that they offered a broad range of options.

The second dimension of the crisis was its short-term and long-term economic impact. COVID-19 was aptly characterized as a simultaneous supply and demand shock [21]. It resulted in a deep slump in 2020 that surpassed the level of the financial crisis of 2008/2009. In Germany, the COVID-19 shock hit the economy when signs of a considerable cyclical slowdown were already widespread, and it seemed as if it could be the beginning of a major recession. These fears did not materialize, as steep recovery growth kicked in in the second half of 2020. However, the economic situation remains precarious due to the sustained fragility of supply chains, a surge in inflation, and the economic effects of the war in Ukraine with its economic and political fallout.

The macroeconomic context is of major importance for the implementation of digitalization projects. A tight macroeconomic climate can reinforce conservative investment behavior, as a return on investment is not guaranteed. Positive growth prospects, on the contrary, can lead to more confident investments with the expectation of rapid growth in a new business cycle. Historically, great economic crises and the subsequent recoveries have often resulted in shifts in the socio-technical composition of industries. They have accelerated the diffusion of base technologies in long waves of economic development [22,23], driven by new investment opportunities and Schumpeterian creative destruction. The economic effects of COVID-19 could turn out to be a cycle of economic slumps and growth of this kind. Perhaps the inflection point of “Industry 4.0” is situated in the recovery phase of COVID-19. The combination of both elements of the conjuncture—the immediate effects of the health crisis and the long-term macroeconomic effects—could result in accelerated technological adaption because there is both an awareness of new possibilities and (arguably) the economic leeway for more courageous investment behavior.

4. Research Design and Methods

The goal of our empirical study was to better understand the extent and the properties of the digitalization push during the COVID-19 pandemic. To this end, qualification and differentiation with regard to the mechanisms and the core areas of the digitalization push were needed. The rationale behind this approach was threefold. First, we found that there needs to be a more differentiated consideration of how much the pandemic acted as a driver for investments and the use of digital technologies. To what extent and in what areas did the pandemic modify the relationship between drivers of and obstacles to investment? Moreover, the theoretical reflections in Section 2 demonstrated that the obstacles to the implementation of digital technologies are manifold and include cultural, technical, organizational, economic, and regulatory dimensions. Although the pandemic certainly heightened the awareness of the importance of technological change in general, it needs to be scrutinized how much it affected the barriers with regard to each of these dimensions.

Second, the hypothesis of a universalized digitalization push leaves unspecified what technologies actually gained in weight (a byproduct of the overly vague catch-all term of ‘digitalization’). Did the pandemic, for instance, lead to equal amounts of investments in technologies for the virtualization of social interaction (e.g., video conferencing tools) and in robotics? An empirical inquiry needs to paint a differentiated picture of current events and identify the rationale for investment in each case.

Third, public debates about the impact of COVID-19 on digitalization are often based on the implicit assumption of a linear progression of events, as if the issue at stake would simply be the quantity of investment, not the characteristics of the chosen approaches. Instead, we ask about possible changes in the strategic orientations of companies, i.e., the direction of the digital transformation, and new ways to combine technology, organizations, and employees under different circumstances. It might turn out in hindsight that the pandemic will have changed the way we think and act about digitalization, as different applications and different socio-technical ways of using them have become more prominent, whereas others will have lost importance. The recent trajectory is not only about more of the same, but about choices among different options.

Methods

The empirical analysis consisted of qualitative data from 36 companies in six relevant economic sectors: automotives, mechanical engineering, chemicals, logistics, financial services, and the health sector. The choice of sectors was made according to their weight in overall employment in the German economy and their exposure to the dual effects (health-related and secondary economic effects) of the COVID-19 crisis. In each sector, a sample of 4–7 companies was chosen. The case selection aimed to include companies from relevant subsectors of each industry. We deliberately included some smaller companies and suppliers in our sample in order to account for the diversity of experiences. However, roughly two-thirds of the sample consisted of larger companies of considerable economic strength and technological sophistication. This selection strategy was chosen because we suspected a particularly significant impact of the pandemic where companies had already pursued ambitious digitalization strategies that would then be impacted or modified. However, this perspective on stronger and more advanced companies in the qualitative studies was complemented by a quantitative survey consisting of a random sample of 540 companies. The sampling strategy for this survey aimed for correspondence with the actual composition of each covered sector in terms of company size and geographical distribution. In contrast to the qualitative investigation, the quantitative sample thus contained a much larger share of SMEs [14].

The interviews for the qualitative investigation were conducted between February 2021 and March 2022. The perceptions of the impact and the further development of the pandemic were in flux during this period. We counterbalanced these contingencies by aiming to reconstruct the measures undertaken since the beginning of the pandemic in each conversation. While it was not possible to eliminate differences in perceptions and attitudes related to the unfolding of the events of the pandemic, the strategy of focusing on concrete actions taken and the reasoning behind them ensures the comparability and robustness of the recorded data.

At each company, interviews of 1–1.5 h were conducted with at least two representatives. We strove to interview representatives from management and the works council in each case in order to account for diverging perspectives from the leadership and employee representatives. Where available, we also contacted managers that were responsible for the implementation of digitalization strategies or projects, who were often denominated as “chief digitalization officers (CDOs)”. In each sector, we also led complementary interviews with industry experts in order to account for general trends in economic and technological development. In complementary interviews with start-ups and established technology providers, we also recorded the perspectives of firms that offered innovative technological solutions in each sector. The audio files of a total of 88 interviews were transcribed and analyzed by means of a qualitative content analysis. A deductively developed coding scheme that included the core categories of “economic situation”, “digitalization measures”, “relation to pandemic”, “work organization”, “quality of work”, and “geographies” was refined through the inclusion and modification of categories that were inductively derived from the analysis of interview materials. In this way, we developed a distinction among the following key categories of digitalization investment:

- Remote work and virtualization of work;

- Improvement of IT infrastructure and introduction of collaboration tools;

- Virtualization of customer/supply chain interactions;

- Virtualization/digitalization/automation of administrative work/HR functions;

- Virtualization/digitalization/automation of production processes and services;

- Digital tools for training purposes;

- Business model innovation/supply of digital services.

In what follows, we present the results of the qualitative investigation of the two questions introduced in the introduction:

- How much did the COVID-19 pandemic reduce existing obstacles to investments in digitalization measures?

- Is there a universal digitalization push due to the COVID-19 pandemic that differs from the digitalization trajectory before the pandemic?

For this sake, we first inductively collected statements on the drivers and obstacles for digitalization during the pandemic (Section 4). Subsequently, the prevalence of the aforementioned categories of digitalization investment was identified by means of a comparative analysis of the cases (Section 5). In the presentation of the material, the findings on these questions are complemented by the interpretations derived from the interview material on why investments in a certain area took place (or did not take place) (Section 5).

5. The Effects of the Pandemic on the Motivation to and Obstacles to Investment

Our inductive analysis of the qualitative data on the motivations and obstacles for investment revealed remarkable overlaps with the conceptual frameworks of [20]. In our analysis, we categorized answers that indicated some kind of relationship between the pandemic and digitalization measures, regardless of whether they acted as drivers of or barriers to investments, in order to identify its possible effects.

As Table 2 shows, the categories from the literature are largely identical with those of the inductive analysis, with two exceptions: First, the “direct factual relationship with the COVID-19 pandemic” obviously could not have played a role before the occurrence of the pandemic. As is explained in more detail below, this category addresses whether the functions of certain digital applications helped to mitigate the impact of the pandemic, for example, by helping to sustain operations under the condition of contact limitations. In so far as this has been the case, the pandemic drove investments in such technologies, while the absence of a factual relationship mostly resulted in unchanged investment behavior or, in some cases, neglect. Second, changes related to skills and HR were not mentioned as a COVID-19-related factor affecting digitalization measures during our interviews. This is remarkable, as the pandemic involved limitations in workforce mobility and aggravated labor shortages in several sectors [24]. It is conceivable that under these circumstances, shortages of skilled labor that had acted as a barrier to digitalization could not have been removed. However, in our data, there was also no evidence that the pandemic made things worse in this respect and that this put a strain on digitalization efforts.

Table 2.

Comparison of inductive categories with categories of barriers to investment in the literature.

The “environmental” category, by which Lammers et al. [20] understood factors related to a company’s environment, was framed in a more specific way in our case studies. For this category, we summarized statements that emphasized the significance of digital technologies to address customers in order to maintain sales. As will be shown, the question of whether or not a company needed to rely on the virtualization of their customer relationship in order to maintain sales turned out to be an important factor that explained the dynamic of investment in some enterprise functions.

A closer analysis of our qualitative data on the relationship between the pandemic and digitalization measures shows that it was not linear and far from universal. In fact, the relationship can be characterized as multi-faceted and often contradictory. Table 3 displays significant reasons for or against investments in digitalization measures as a reaction to the COVID-19 crisis.

Table 3.

Reasons given for investment or non-investment in digital technologies.

As became evident in all of our case studies, the direct factual relation to the COVID-19 pandemic and specific technologies were highly variable. Remote work and digital interfaces for customer interaction (websites, online shops, video calls) for many companies were indispensable means of sustaining business operations. Consequently, there was an immediate need to implement or expand technological solutions in these functions. The focus here was on means for remote communication and data exchange, which served to circumvent physical contact for health-related reasons. Conversely, in only a minority of the investigated case studies, there was investment in production-related digitalization investment. Production processes were first interrupted and then could be relaunched under safety precautions that relied on social adaptations (the modification of shift plans, hygiene and social distancing rules, etc.), not on technological solutions. Hence, it comprehensively seems that the pandemic even constituted a more difficult environment for shop-floor-related investments.

By cultural factors, we understand the mindset of the actors involved at the company level, i.e., the attitudes of management, works councils, and employees towards digitalization measures. In line with public discourse, we found a heightened awareness for the possibilities of digitalization. This was not only the overwhelming picture in our company case studies, but was also confirmed in the quantitative survey of 540 companies, in which over two-thirds of respondents confirmed an increased awareness of digitalization issues due to the COVID-19 crisis (45.0%: agree, 24.8%: partially agree). The results from the qualitative data illustrate that such perceptions mostly focused on the transition or expansion of remote work. This transition was mostly brought about in an improvised yet cooperative manner in the absence of major conflicts and, in some cases, with adherence to prior agreements between management and works councils. Cases in which works councils expressed profound concerns about remote work arrangements did exist but constituted a minority of our sample. Overall, our data confirmed that the experience of the pandemic strengthened positive attitudes towards digitalization in general. This may result in a more proactive and open stance towards future areas of investment that do not have any factual relationship with the pandemic.

Beyond these general observations—the direct factual relationship of digital applications to the COVID-19 pandemic and the mindset of the involved actors—the analysis of company cases highlights some additional criteria that affected the propensity of companies to invest in digital technologies.

The feasibility of investment often depended on factors related to a company’s environment. The absence of a mindset and habits of customers that were open to digital products and services before the pandemic had often constituted a barrier to investment. Interviewees from banks, hospitals, and outpatient care providers reported a hike in the demand for such digital offers during the pandemic due to the social distancing prescriptions, which, in turn, incentivized their institutions to expand their activities in these areas. Representatives from some mechanical engineering companies also reported that there was an increased openness on the part of customers to use tools for the remote setup and maintenance of their products. Such beneficial effects related to the mindset of customers shape most service-oriented sectors, in which interactive customer relations prevail. They are less pronounced when companies provide standardized services and products in B2B supply chains, such as in the chemical industry and in logistics. In some cases, the economic effects of the crisis even resulted in a decrease in demand for digital products and, thus, constituted a barrier to digitalization: Mech.3 (the terminology refers to Table 4, which displays an overview of the company cases), for instance, reported a decline in demand for their “digital factory” products, resulting in a delay of progress by 2–3 years, because customers were holding back investments due to economic insecurity in the first phase of the pandemic.

Table 4.

Results of the qualitative case studies.

The technological feasibility in the short term turned out to be a fundamental issue that determined the course of investment since the beginning of the pandemic. As many companies already had cloud infrastructures, software packages, and mobile hardware devices in place before the pandemic, the instantaneous implementation of services for remote communication could be provided with little friction. Moreover, companies could easily ramp up external cloud services and software options without buying hardware and going through arduous processes of setting up equipment and software solutions at their own premises (see Section 6). Other digital applications could not be spontaneously implemented, however. This, for instance, accounted for a company in our sample that, until the pandemic, had relied on their own server capacities and found it impossible to scale them up instantaneously. Similarly, investment in robotics mostly requires long-term preparation and an elaborate process of installation, which is hardly possible within a few weeks. At Auto.1, Mech.1, and Mech.3, it was emphasized that it would not be possible to spontaneously invest in tools for remote setup and maintenance; such software solutions and the corresponding equipment (data glasses) would need to be in place already in order to use them in the pandemic setting. Other digitalization projects constituted long-term efforts related to the creation of infrastructures and standards. This accounted for the introduction of healthcare information systems—a political target for roughly two decades—and the IoT-based interconnection of production equipment at industrial companies. Especially in healthcare, the pandemic certainly demonstrated the urgency of improved information systems. The implied complex processes of institutional innovation could not be solved on the spot, however.

Another factor that conditioned investment in digital technology was the amount of financial resources that a company was able to allocate to this end. In some instances, there was a considerable increase in spending. In the health sector, this was politically driven, as the government created a special fund—the so-called “hospital future fund” that was made available from the beginning of 2021. In the private sector, management mostly invested without hesitation in measures for the virtualization of communication that were considered to be low-hanging (and low-cost) fruit. Such changes also demanded organizational resources for ramping up capacities and readjusting work routines. In our quantitative survey, 52% of the enterprises that had intensified their investment in digital technologies stated that they complemented this investment with organizational changes. Among such measures was a flexibilization of working hours, an increase in cross-functional cooperation, and changes in leadership roles. The severity of the pandemic thus triggered a quest for more effective work organization, which required considerable effort. Sometimes, the obstruction of regular operations made it easier for companies to focus on organizational innovation. In Log.2, for instance, the IT department could continue to operate remotely, unlike the operative logistics division, which came to a halt in the spring of 2020. This freed up the capacities of the IT professionals, which were then used to intensify the automation of administrative tasks (robotic process automation). In contrast to such successful cases in which companies and other institutions could mobilize additional resources for digitalization projects, there was a minority of cases in which investment was cut. Mech.4 reported a freeze of (new) investments due to the insecure economic environment. The dominant picture, however, is that in most ongoing digitalization projects beyond those connected to remote work, there were few changes with regard to funding and schedules. Most company spokespersons emphasized that they had existed before the pandemic and, at most, experienced slight acceleration along with heightened interest.

Finally, some digitalization projects could benefit from ad hoc changes in regulatory circumstances. Where digital signatures had not existed before, they became accepted, thus enabling progress in paperless administration. Health insurance companies also began to accept digital signatures from customers of outpatient care units, thus facilitating the work of outpatient care providers, such as Health.6, where the need for double documentation (on paper and digitally) was eliminated. Other rules and regulations proved to be difficult to instantaneously change or could not be changed at all. In some areas of the chemical industry (such as at Chem.1), for instance, certain digital tools could not be used because of safety regulations, which is a limitation that is impossible to overcome.

The overview of the factors affecting investment or non-investment in digitalization measures during the pandemic highlights several causes for a digitalization push, but also its conditionality. Investments were most prominent where there was a strong factual relationship between the pandemic and technological change and where there was a strong conviction on behalf of the main actors in the purpose of such investments. Furthermore, the willingness of customers to accept digital offers and the ability of organizations to ramp up the available resources, as well as to loosen the regulatory context, constituted favorable circumstances for progress in digitalization. The analysis also shows that we need to distinguish between low-hanging fruits that are available with low cost and little effort (e.g., the introduction of cloud-based software packages or the broader utilization of collaboration tools) and long-term investment projects that cannot be instantaneously introduced.

6. Empirical Qualification of the Digitalization Push: Core Areas of Investment

As the prior discussion has shown, the catch-all word “digitalization” is not specific enough for a concrete analysis of recent changes in companies. “Digitalization” consists of a set of varying—not necessarily integrated—measures that affect different dimensions of an organization’s activity and require different capabilities. Quantifying the changes as “more” or “less” digitalization is not satisfactory, as this omits the particular emphasis that is given to distinct aspects of digitalization. In what follows, we provide short summaries of the most important areas of investment during the pandemic at the 36 companies in our sample while highlighting the actual relationship between the pandemic and digitalization measures.

6.1. The Transition to Remote Work

The data show that the transition to remote work affected all areas of non-location-dependent white-collar work, which also implies that it amounted to different shares of the total workforce according to the core processes of a firm. It was universal in our qualitative sample with a share of between 25 and 100 percent of workers working online (with the sole exception of a logistics division that did not have its own administration at the investigated site). In the estimation of 441 respondents in our quantitative survey, the mean average from all companies with regard to the share of employees working online roughly doubled from 15 to 29.7 percent.

There was a high degree of cooperation between management and works councils in order to make this transition possible. This afforded that works councils were prepared to chart institutionally non-regulated territories by agreeing to unprecedented work arrangements, while management cultures had to instantly change to grant more leeway for independent teamwork and to loosen (or alter) performance control. The transition was smoother when agreements that specified the rules for remote work had already been negotiated before the pandemic and high independence of teams had already been a part of the company culture. However, improvisation was needed regardless of whether such formal regulations and organizational practices had existed before. In general, a well-established co-determination routine played an important role in efficiently managing the transition without major friction. At the few companies in the sample that had more conflict-ridden industrial relations, the transition towards remote work involved more friction, as the works council suspected a deterioration of standards.

6.2. Digitalization beyond Remote Work: A Polarized Picture

While the transition towards remote work absorbed much attention and was mostly associated with the digitalization push as such by practitioners, there is evidence that the pandemic had impacts on digitalization issues beyond that. As stated before, the majority of the companies in our quantitative survey reported a generally greater awareness of digitalization options (45.0%: agree, 24.8%: partially agree). A total of 64 percent of the surveyed companies also reported additional investments in digitalization measures, with considerable effects: 33 percent of the respondents stated that the level of digitalization of their enterprise before the pandemic used to be lower than at the time of the survey in the summer of 2021. Interestingly, however, the replies also suggest that some of the measures taken were rather insular, as 63 percent of the respondents denied that it amounted to a change in the overall level of digitalization at their company.

The objectives and character of the chosen measures varied considerably depending on the peculiarities of the operations in each company (characteristics of products and services, composition of the workforce, customer relations, etc.) and the extent to which the virtualization of work was imperative for maintaining operations. Table 4 provides an overview of our qualitative findings, highlighting the differentiation according to the respective dimensions of the digital transformation.

6.3. IT Infrastructure

The challenges of rapidly scaling remote work schemes were reflected in widespread investments in IT infrastructure. These included the purchase of additional laptops and other hardware, the ramping up of server capacities (mostly externally sourced), improvements in Wi-Fi bandwidth and virtual private network (VPN) access points, and the acquisition of a range of software tools for online collaboration. Many of these possibilities had been in place before the pandemic. However, the need to instantly rely on such tools contributed to firmly establishing them in work routines and reducing uncertainties about their usability. In this sense, the pandemic proved to be a consolidation of technological developments that were already underway but had only been partially used before. The use of video conferencing software and digital collaboration tools, such as MS Teams, experienced an especially strong push beyond the boundaries of former practices. It is notable that the scaling of remote work afforded computing capacities that could barely have been provided if there was not the option of purchasing cloud computing capacities based on the infrastructure-as-a-service and software-as-a-service options that have come to dominate the market in recent years. Several companies reported that they resorted to cloud providers in order to spontaneously ramp up capacities and bandwidth. On the contrary, Mech.5 had relied on its own server capacities on premises that it reported regarding its inability to ramp these up during the pandemic. Subsequently, it canceled its plan to acquire additional self-owned server capacities in favor of sourcing them externally. In this sense, COVID-19 surely represents a tipping point for the reach and intensity of cloud computing in the business context.

6.4. Reducing Physical Contact in Services: Customer Interaction, HR Services, and Digital Learning

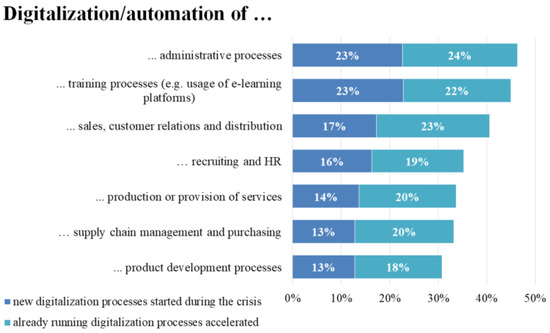

Services for customer interaction proved to be vital in mechanical engineering, healthcare, and finance, which are sectors in which regular operations rely on frequent personal interactions between firms and their customers. Such findings in the qualitative study were confirmed by our quantitative survey, which also singled out the digitalization or automation of administrative processes, training, distribution, and HR as the fields with the highest level of activity, either by launching new initiatives or by ramping up existing ones (cf. Figure 1).

Figure 1.

Core areas of investment (quantitative survey).

In mechanical engineering, remote contact with customers frequently involved the use of devices and software that could be used for interactions with the technical staff of machine providers and online manuals (Mech.1, 2, 4, 5, 6). Mech.5 introduced online services and manuals for the installment of equipment, including short videos that were distributed through the firm’s own online platform. In hospitals and care facilities, tools for virtual navigation and remote contact with patients and relatives were established (Health.1, 2, 3, 7). However, our respondents emphasized that while there had been some acceleration in the introduction of such methods, they were still only partially implemented and used. Some industrial companies (Auto.3, Chem.1, Mech.2, Mech.4) also invested in additional sales channels through digital platforms and other channels. The companies that extended techniques for virtual customer interaction had already laid the basis for doing so before the pandemic. The pandemic led to the habituation and the improvement of existing approaches in these cases, which probably amounted to establishing them permanently. As mentioned before, however, virtual customer contact through data glasses and the like is difficult to spontaneously, as it requires long-term preparation and infrastructure investment.

HR services and administrative work in general are another field that was directly related to the need to reduce physical proximity. Our quantitative survey confirmed that this constituted a major tendency, as 23 percent of the respondents said that new processes for the digitalization or automation of administrative work were newly established, and another 24 percent said that they were accelerated (46 percent said that it did not apply) (on the more specific question about the digitalization/automation of recruiting and HR, the results are as follows: newly established: 16%; accelerated: 19%; does not apply: 55%). Our qualitative investigation showed that some companies (Auto.4; Mech.6, Log.1; Health.2) established or extended the use self-service terminals for their employees, which were sometimes supported by employee apps. There was also an acceleration of initiatives for the end-to-end digitalization of administrative processes by introducing digital signatures and similar procedures (Mech.5, Log.2, 4; Health.2; Fin.2, 3). The pandemic thereby contributed to the general trend for the automation and virtualization of administrative work. This could well lead to structural changes that qualitatively transform these functions. In the long term, the changes in the media of communication could also result in a transformation of work content and the division of labor. At Mech.1, for instance, there was a geographic reshuffling of responsibilities among the HR staff. HR specialists in a particular dependency of this company were then supposed to answer requests from all employees of the entire corporation on one particular area of expertise (e.g., sickness leaves, maternity issues, etc.), instead of being generalists for employee requests from the local site only. Therefore, we suspect that the virtualization of such functions could enable structural changes ranging from adjustments of the work organization to additional possibilities for outsourcing and/or offshoring, given that no geographical co-location of such functions would be needed anymore. However, at the time of our survey, such plans were only pursued at Mech.1.

Digital technologies for supporting the training of employees were another field that, in many cases (Chem.1, 3, 4; Mech.3, 4; Health 1,2,3,6; Fin 3,4), experienced additional investment due to the need to maintain operations while avoiding direct physical contact. Some companies introduced or expanded digital learning platforms and vocational training units through video conferencing tools. Our quantitative survey confirmed the virtualization of learning processes as a major tendency. A total of 45 percent of the company representatives reported that continuous virtual training was either newly established or accelerated.

6.5. No Push for Shop-Floor-Related Investments

A striking observation at the surveyed companies concerned the absence of additional investments in the automation of physical processes. As automation can help to reduce social contacts (‘robots don’t get the flu’), it would be a likely scenario that the pandemic would also trigger investments in this field. However, this did not seem to be the case. Only five out of the 36 companies reported some additional activity with regard to shop-floor-related functions. Most companies in the automotive, chemical, mechanical engineering, and logistics industries, however, explicitly denied any correlation with the pandemic. There was a striking gap between the activities concerning remote work, IT infrastructure, and the digitalization of administrative functions and the introduction of shop-floor-related Industry 4.0 applications, which had not experienced acceleration. When companies pursued such strategic goals and projects, their pace was not greatly affected, and Auto.1 and Mech.4 even reported difficulties in pursuing them under the extraordinary circumstances of the pandemic. Industry-4.0-related applications that did experience more investments were tools for remote communication with customers for the installation of machines that were expanded at many mechanical engineering companies.

A possible explanation for the finding that there was little investment in shop-floor-related technologies is that investments in physical automation equipment need much more preparation, time and capital for their implementation than the mentioned measures for the virtualization of social interaction. They also require comprehensive adjustments of process and work organization on the shop floor, which, in many cases, had become more difficult under the conditions of the pandemic.

Moreover, the technological frontier is less permeable. As discussed in Section 2, the introduction of Industry 4.0 had progressed in a primarily incremental fashion before the pandemic. It requires long-term efforts and investment to overcome the remaining barriers to digitalization and automation, steps that often cannot be spontaneously undertaken. Most importantly, the concrete necessity to do so, apart from a general acknowledgement of the significance of digitalization strategies in general, was barely affected by the pandemic. Industry 4.0 technologies do not amount to a sweeping substitution of work to an extent that would be epidemiologically meaningful. The goal of a reduction in physical proximity out of health considerations, therefore, did not serve as a justification for automation investments in the investigated cases—especially as industrial enterprises tended to operate without major obstructions after the initial shock after the advent of the virus. Shop-floor-related digitalization projects have, thus, developed much more steadily than is the case with the dynamically developing fields of remote work, cloud computing, remote customer interaction, and the digitalization of administration and training activities.

7. Discussion

The analysis of 36 company case studies and the results from the quantitative survey in six economic sectors revealed that the pandemic affected the digitalization investments in companies in a strikingly uneven and cascaded manner. Where there was an immediate factual relationship between the pandemic and digitalization measures and where resources, technical feasibility, and the willingness of the main actors were given, the pandemic induced a push in investments. However, these conditions were not universally met, which is why there was a divergence in the digitalization patterns across our sample.

Despite this unevenness, some general tendencies could be identified as a qualification of the digitalization push in German enterprises in the six surveyed economic sectors. At its core undoubtedly lies the transition to remote work, which is not only about changes in the location of work, but also about the scaling up or addition of IT infrastructure, software applications, and new work routines. These changes seem to affect white-collar work almost universally and will continue to shape work practices after the pandemic, albeit in the form of a new synthesis between on-site and remote work. The identification of the standards and requirements that are needed in order to improve the work experience and the work–life balance of employees is of paramount importance for shaping the ‘new normal’. This strong focus of digitalization activities on enabling mobile work calls into question whether it is even appropriate to interpret the effects of the COVID-19 crisis as a general push for digitalization. Accordingly, a recent survey on the matter concluded: “The so-called corona digitalization push can therefore not be called a comprehensive one. It mainly concerns processes such as interconnected work, the information exchange within companies, and digital linkages to other companies” [25].

This alludes to a second layer of process innovation that was pursued by some (but not all) enterprises in our samples: the introduction of specific applications for the virtualization of interactions with customers and between employees. The pandemic forced enterprises and organizations in which direct personal interaction with customers was frequent (in our sample, these were especially in financial services, healthcare, and mechanical engineering) to move such communication online—a measure that had already been pursued before the pandemic, but benefitted from an increased preparedness of actors to accept options for remote consultation. In most cases that concerned the virtualization of sales channels, however, this merely amounted to an ad hoc substitution of the conventional offline practices. Prospectively, however, they could support business model innovation (e.g., if a company modifies the product that it is offering) and changes in work organization (e.g., if special departments that exclusively work remotely are defined). Measures for virtualizing collaboration also characterized several areas of administrative work and activities concerning the training of employees. Goals for introducing the ‘paperless office’ that had been pursued in the past experienced a push as well, since organizations started to tackle remaining bottlenecks through improvisation, but also by substituting inefficient practices of the past. Just as in the general education system, e-learning experienced a surge in demand, and there has been a growing proficiency and acceptance among trainers and apprentices.

In contrast with these changes that mostly concerned cognitive work routines, the digitalization of shop-floor-related functions barely experienced progress. The dominant reply by company representatives on this issue was that the pandemic had barely affected existing digitalization projects in this area. In most cases, there was no factual relationship between the automation or digitalization of manufacturing and the pandemic, since most digitalization projects in this realm did not significantly alter the density of social interactions on the shop floor and were, therefore, irrelevant in terms of health considerations. Moreover, many applications that are subsumed under the term “Industry 4.0” do not aim at reducing the labor intensity of production, but rather at improvements in the interconnection and control of production facilities. They remain relevant for industrial companies, but the pace of investment was hardly altered through the pandemic. In this sense, the pandemic cannot be interpreted as a jump start for Industry 4.0. Investments rather concerned applications beyond the realm of manufacturing and underlined that present digitalization strategies, to a great extent, concern the automation, digitalization, and virtualization of cognitive work, especially in the administrations of companies. Exceptions to this rule were some applications for the remote setup of production equipment that were extended at some mechanical engineering companies.

However, the reasons for the lack of investment in manufacturing-related issues not only had to do with a missing factual relationship to the pandemic, but also with the longer time horizons of such investments. They usually cannot be instantaneously implemented because they require complex adjustments between physical and digital processes and the implementation and alignment of infrastructures (installation of sensors, construction of digital twins, and development of appropriate data analytics). This limitation is in stark contrast with the spontaneous ramping up of software and cloud capacities, which certainly constituted a challenge for the involved actors, but was feasible under the extraordinary conditions during the pandemic [2].

This correlation between pandemic-induced investment and the time horizon of digitalization projects is confirmed by other studies on recent events. An investigation of digitalization processes at mid-sized companies (the so-called “Mittelstand”) observed a focus on short-term measures, while measures that require long-term preparations were often postponed [2]. A comprehensive monitoring effort initiated by the German Ministry of the Economy and Climate Changes similarly spoke of short-termism in investment. More comprehensive efforts with long-term effects, such as the innovation of products and business models, consequently received little attention during the pandemic [25].

8. Conclusions

This investigation departed from the question of whether the pandemic amounted to changes in the quality and the direction of the digital transformation in the investigated six sectors of the German economy. The results highlighted both continuity and a stronger focus on the automation, digitalization, and virtualization of white-collar work. On the one hand, the focus on short-termism and low-hanging fruits seemed to be in line with prior experiences. The narrative of a new industrial revolution belies the fact that the predominant mode of change had been incremental and focused on single applications with concrete returns, whereas systemic changes in processes and business models had been rather limited [12,26]. It could also be argued that changes that concern white-collar functions, i.e., the introduction of new software tools, collaboration through the cloud, and the partial automation of cognitive activities, had been a major axis of the contemporary wave of digitalization even before the pandemic. Consequently, the previously mentioned survey on digitalization activities by mid-sized companies during the pandemic concluded that neither the content nor the priorities of digitalization investment were significantly altered during the pandemic [2]. In this sense, the effects of the pandemic rather represent a discursive shift: It can be seen as a moment of reckoning that the virtualization of cognitive work and social interaction is at the core of many digitalization strategies. This suggests that the focus in the German “Industry 4.0” discourse, which is centered on manufacturing technologies, needs to be broadened in order to relate the transformation of manufacturing toward the mentioned changes in cognitive work in the service function of industrial (and non-industrial) companies.

On the other hand, the results of our study also include evidence that the pandemic constituted more than just a discursive shift and did bring new issues to the fore. At many companies, the introduction of schemes for mobile work and the intensified collaboration through the cloud, as well as virtual interactions with customers, constituted the entry into new modes of operation that implied more fluid work organization and more dense interactions. In most enterprises, some foundations for these steps were already present when the pandemic began. However, they often were of minor importance and did not amount to qualitative changes in the manner of collaboration. The shock of the pandemic induced not only a ramping up of capacities, but also a habitualization of cloud-based work routines, along with a set of new applications. The subsequent development is one in which new possibilities of virtual collaboration are constantly being explored and expanded. In this sense, our research highlights that the pandemic can be seen as the inflection point of cloud-based collaboration on a broader scale, which amounted to a major change in companies across our sample. This change certainly would have come without the pandemic, but this extraordinary event greatly affected the speed of this transformation and the subjective willingness to embrace it.

Our study highlights that a scientific understanding of the progression of digitalization and its effects requires one to differentiate among different dimensions and fields of application and to combine qualitative and quantitative methods in order to trace the digitalization trajectories in different economic sectors. Future research should extend such approaches to other economic sectors that were not covered by this study. Moreover, the digitalization approaches in different regions of the world should be systematically compared with sensitivity to institutional and cultural differences in order to uncover what could be called “varieties of digitalized capitalism”.

Author Contributions

Conceptualization, F.B.; methodology, F.B., M.K., C.G., D.W. and J.F.; investigation, F.B., C.G., D.W., J.F., M.K., L.H. and N.D.; writing—original draft preparation, F.B.; writing—review and editing, F.B., M.K., D.W., C.G. and L.H.; visualization, F.B., L.H. and N.D.; project administration, F.B. and M.K.; funding acquisition, F.B. and M.K. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by the German Ministry of Labour and Social Affairs.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Data Availability Statement

The data presented in this study are available on request from the corresponding author. The data are not publicly available due to privacy reasons.

Conflicts of Interest

The authors declare no conflict of interest.

References

- LaBerge, L.; O’Toole, C.; Schneider, J.; Smaje, K. How COVID-19 Has Pushed Companies over the Technology Tipping Point—And Transformed Business Forever; McKinsey & Company: New York, NY, USA, 2020; Available online: https://www.mckinsey.com/business-functions/strategy-and-corporate-finance/our-insights/how-covid-19-has-pushed-companies-over-the-technology-tipping-point-and-transformed-business-forever (accessed on 19 May 2023).

- KfW. KfW-Digitalisierungsbericht Mittelstand 2020. In Rückgang der Digitalisierungsaktivitäten vor Corona, Ambivalente Entwicklung Während der Krise; KfW Bankengruppe: Frankfurt am Main, Germany, 2021. [Google Scholar]

- BMWK. Digitalisierung der Wirtschaft in Deutschland. In Digitalisierungsindex 2021; BMWK: Berlin, Germany, 2022. [Google Scholar]

- Brynjolfsson, E.; McAfee, A. The Second Machine Age: Work, Progress, and Prosperity in a Time of Brilliant Technologies; W. W. Norton & Company: New York, NY, USA, 2014. [Google Scholar]

- Sturgeon, T. The “New” Digital Economy and Development; UNCTAD: Geneva, Switzerland, 2017. [Google Scholar]

- Zysman, J.; Kenney, M. The next phase in the digital revolution: Intelligent tools, platforms, growth, employment. Commun. ACM 2018, 61, 54–63. [Google Scholar] [CrossRef]

- McAfee, A.; Brynjolfsson, E. Machine, Platform, Crowd: Harnessing Our Digital Future; Norton & Company: New York, NY, USA, 2017. [Google Scholar]

- Zysman, J.; Murray, J.; Feldman, S.; Nielsen, N.C.; Kushida, K.E. Services with Everything: The ICT-Enabled Digital Transformation of Services. SSRN Electron. J. BRIE Working Paper 2011. [Google Scholar] [CrossRef]

- BMBF. Zukunftsbild “Industrie 4.0”. Bundesministerium für Bildung und Forschung. Referat IT-Systeme. 2015. Available online: https://www.plattform-i40.de/IP/Redaktion/DE/Downloads/Publikation/zukunftsbild-industrie-4-0.pdf?__blob=publicationFile&v=4 (accessed on 19 May 2023).

- Kagermann, H.; Helbig, J.; Hellinger, A.; Wahlster, W. Recommendations for Implementing the Strategic Initiative INDUSTRIE 4.0: Securing the Future of German Manufacturing Industry; Final Report of the Industrie 4.0 Working Group; Forschungsunion; Geschäftsstelle der Plattform Industrie 4.0: Berlin/Frankfurt a. M., Germany, 2013. [Google Scholar]

- Sorge, A.; Streeck, W. Diversified quality production revisited: Its contribution to German socio-economic performance over time. Socio-Econ. Rev. 2018, 16, 587–612. [Google Scholar] [CrossRef]

- Apitzsch, B.; Buss, K.-P.; Kuhlmann, M.; Weißmann, M.; Wolf, H. Arbeit in und an Digitalisierungen. Ein Resümee als Einführung. In Digitalisierung und Arbeit: Triebkräfte—Arbeitsfolgen—Regulierung; Buss, K.-P., Kuhlmann, M., Weißmann, M., Wolf, H., Apitzsch, B., Eds.; Campus Verlag: New York, NY, USA, 2021; pp. 9–39. [Google Scholar]

- Hirsch-Kreinsen, H. Industry 4.0—A Path-Dependent Innovation; Soziologisches Arbeitspapier Nr. 56/20169; Wirtschafts-und Sozialwissenschaftliche Fakultät, TU Dortmund: Dortmund, Germany, 2019; pp. 1–25. [Google Scholar]

- Krzywdzinski, M. Automation, digitalization, and changes in occupational structures in the automobile industry in Germany, Japan, and the United States: A brief history from the early 1990s until 2018. Ind. Corp. Chang. 2021, 30, 499–535. [Google Scholar] [CrossRef]

- Butollo, F.; Jürgens, U.; Krzywdzinski, M. From Lean Production to Industrie 4.0: More Autonomy for Employees? In Digitalization in Industry: Between Domination and Emancipation; Meyer, U., Schaupp, S., Seibt, D., Eds.; Springer International Publishing: Berlin/Heidelberg, Germany, 2019; pp. 61–80. [Google Scholar] [CrossRef]

- Marx, U. Maschinenbaugipfel. “Zehn verlorene Jahre”. Frankfurter Allgemeine Zeitung. Available online: https://www.faz.net/aktuell/wirtschaft/unternehmen/gipfel-zum-maschinenbau-zehn-verlorene-jahre-18379560.html (accessed on 11 October 2022).

- Heßler, M.; Thorade, N. Die Vierteilung der Vergangenheit. Eine Kritik des Begriffs Industrie 4.0. TG Tech. 2019, 86, 153–170. [Google Scholar] [CrossRef]

- Mokyr, J. Chapter 17—Long-Term Economic Growth and the History of Technology. In Handbook of Economic Growth; Aghion, P., Durlauf, S.N., Eds.; Elsevier: Amsterdam, The Netherlands, 2005; Volume 1, pp. 1113–1180. [Google Scholar] [CrossRef]

- Horváth, D.; Szabó, R.Z. Driving forces and barriers of Industry 4.0: Do multinational and small and medium-sized companies have equal opportunities? Technol. Forecast. Soc. Chang. 2019, 146, 119–132. [Google Scholar] [CrossRef]

- Lammers, T.; Tomidei, L.; Trianni, A. Towards a Novel Framework of Barriers and Drivers for Digital Transformation in Industrial Supply Chains. In Proceedings of the 2019 Portland International Conference on Management of Engineering and Technology (PICMET), Portland, OR, USA, 25–29 August 2019; pp. 1–6. [Google Scholar] [CrossRef]

- Baldwin, R.; Tomiura, E. Thinkin. ahead about the trade impact of COVID-19. In Economics in the Time of COVID-19; Baldwin, R., Weder di Mauro, B., Eds.; CEPR Press: London, UK, 2020; pp. 59–72. Available online: https://cepr.org/sites/default/files/news/COVID-19.pdf (accessed on 8 February 2021).

- Archibugi, D.; Filippetti, A.; Frenz, M. Economi. crisis and innovation: Is destruction prevailing over accumulation? Res. Policy 2013, 42, 303–314. [Google Scholar] [CrossRef]

- Louçã, F. Long Waves, the Pulsation of Modern Capitalism. In Chapters; Edward Elgar Publishing: Cheltenham, UK, 2007; Available online: https://ideas.repec.org/h/elg/eechap/2973_48.html (accessed on 8 February 2021).

- Peichl, A.; Sauer, S.; Wohlrabe, K. Fachkräftemangel in Deutschland und Europa—Historie, Status quo und was getan werden muss. Ifo Schnelld. 2022, 75, 70–75. [Google Scholar]

- DigiIndex. Digitalisierungsindex. Bundesministerium für Wirtschaft und Klimaschutz. Available online: https://www.de.digital/DIGITAL/Navigation/DE/Lagebild/Digitalisierungsindex/digitalisierungsindex.html (accessed on 11 October 2022).

- Hirsch-Kreinsen, H. Digitale Transformation von Arbeit. Entwicklungstrends und Gestaltungsansätze; Kohlhammer: Stuttgart, Germany, 2020. [Google Scholar]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).