An Efficient Numerical Method for Pricing Double-Barrier Options on an Underlying Stock Governed by a Fractal Stochastic Process

Abstract

1. Introduction

2. Model

2.1. Preliminaries

- (i)

- a constant K, then its Jumarie fractional derivative of order α is defined by

- (ii)

- not a constant, then

2.2. Model Specification

3. Numerical Scheme

3.1. Model Discretization

3.1.1. Temporal Discretization

3.1.2. Spatial Discretization

3.2. The Full Scheme

4. Theoretical Analysis of the Scheme

4.1. Stability Analysis

4.2. Convergence of the Numerical Scheme

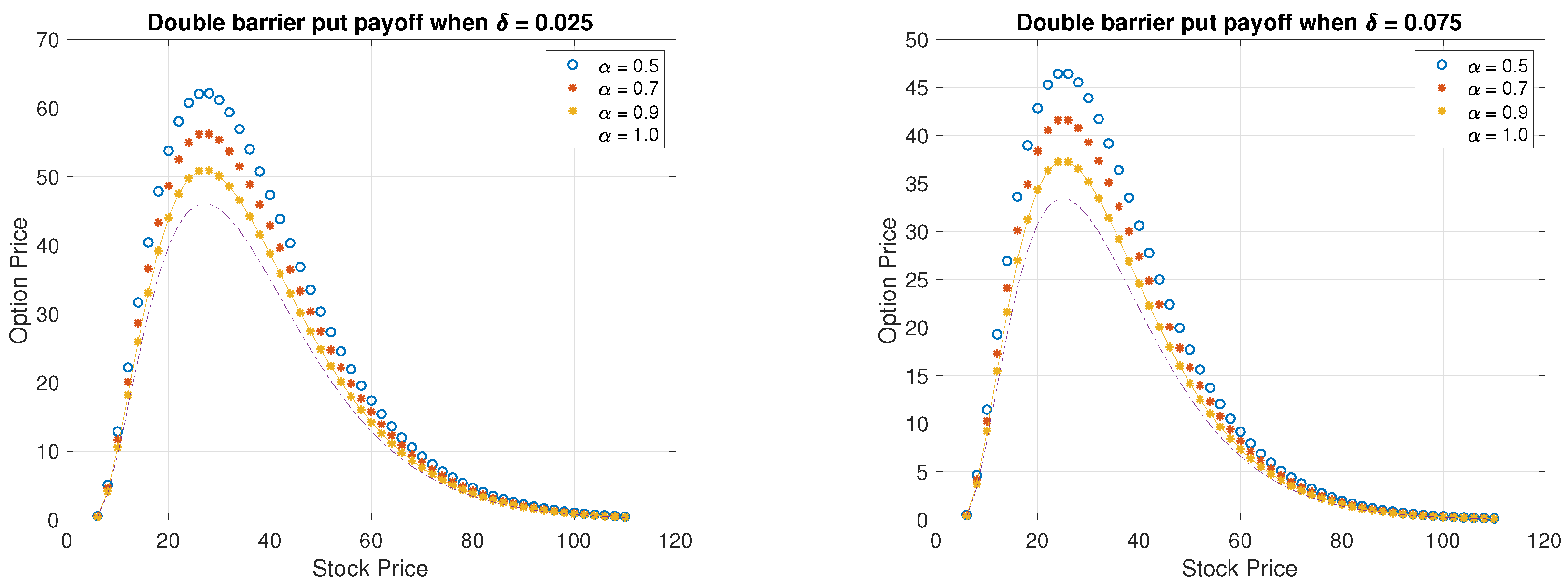

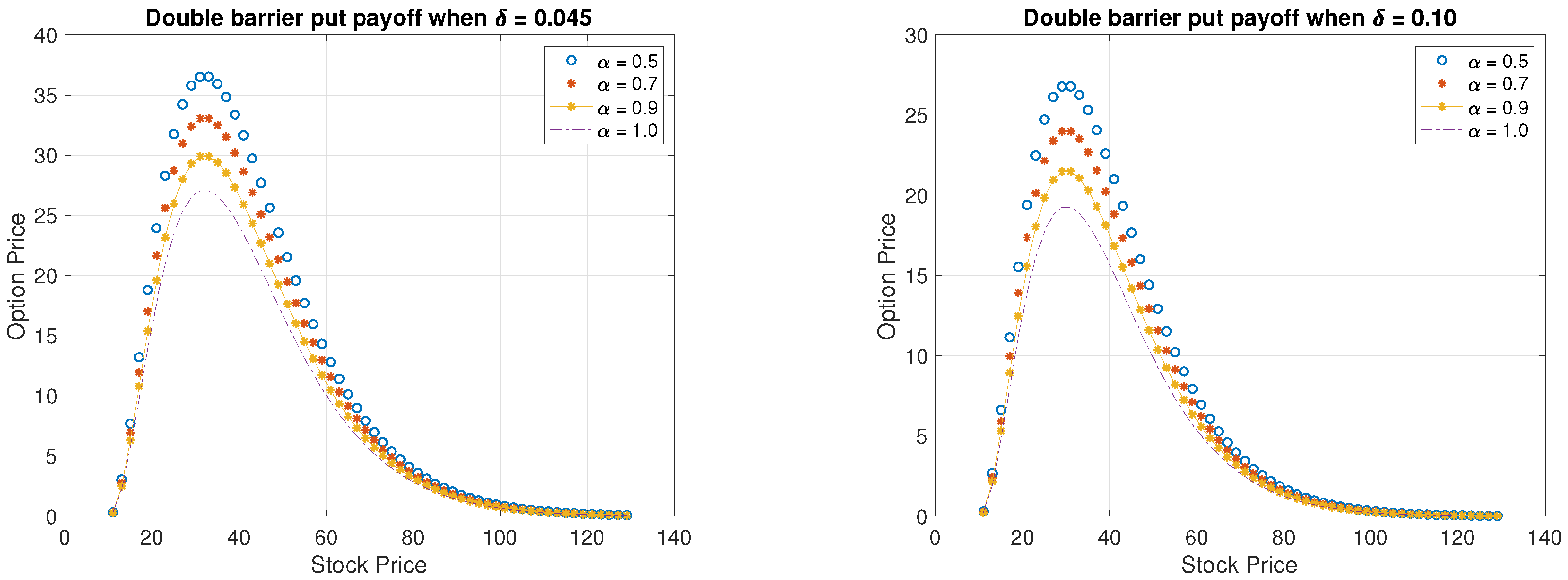

5. Numerical Results and Discussions

6. Concluding Remarks and Scope for Future Direction

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Buchen, P.; Konstandatos, O. A new approach to pricing double barrier options with arbitrary payoffs and exponential boundaries. Appl. Math. Financ. 2009, 6, 497–515. [Google Scholar] [CrossRef]

- Hull, J. Options, Futures and Other Derivatives; Pearson Prentice Hall: Upper Saddle River, NJ, USA, 2009. [Google Scholar]

- Luca, V.B.; Graziella, P.; Davide, R. A very efficient approach for pricing barrier options on an underlying described by the mixed fractional Brownian motion. Chaos Solitons Fractals 2016, 87, 240–248. [Google Scholar]

- Wilmott, P. Derivatives: The Theory and Practice of Financial Engineering; John Wiley & Sons: West Sussex, UK, 1998. [Google Scholar]

- Black, F.; Scholes, M. The pricing of options and corporate liabilities. J. Polit. Econ. 1973, 81, 637–654. [Google Scholar] [CrossRef]

- Ballerster, R.; Company, C.; Jodar, L. An efficient method for option pricing with discrete dividend payment. Comput. Math. Appl. 2008, 56, 822–835. [Google Scholar] [CrossRef]

- Kleinert, H.; Korbel, J. Option pricing beyond Black-Scholes based on double-fractional diffusion. Phys. A 2016, 449, 200–214. [Google Scholar] [CrossRef]

- Broadie, M.; Glasserman, P. A continuity correction for discrete barrier options. Math. Financ. 1997, 4, 325–348. [Google Scholar] [CrossRef]

- Ahn, D.; Gao, B.; Figlewski, S. Pricing discrete barrier options with an adaptive mesh model. Quant. Anal. Financ. Mark. 2002, 33, 296–313. [Google Scholar]

- Feng, L.; Linetsky, V. Pricing discretely monitored barrier options and defaultable bonds in levy process models: A fast Hilbert transform approach. Math. Financ. 2008, 3, 337–384. [Google Scholar] [CrossRef]

- Hsiao, Y.L.; Shen, S.Y.; Wang, A.M.L. Hybrids finite difference method for pricing tow-asst double barrier options. Math. Probl. Eng. 2015, 2015, 692695. [Google Scholar] [CrossRef]

- Jeon, J.; Kim, J.Y.; Park, C. An analytic expansion method for the valuation of double-barrier options under as stochastic volatility model. Math. Anal. Appl. 2016, 449, 207–227. [Google Scholar] [CrossRef]

- Song, S.; Wang, Y. Pricing double barrier options under a volatility regime-switching model with psychological barriers. Rev. Deriv. Res. 2017, 2, 225–280. [Google Scholar] [CrossRef]

- Bollersleva, T.; Gibson, M.; Zhoud, H. Dynamic estimation of volatility risk premia and investor risk aversion from option-implied and realized volatilities. J. Econom. 2011, 160, 235–245. [Google Scholar] [CrossRef]

- Benson, D.A.; Wheatcraft, S.W.; Meershaert, M.M. Application of a fractional advection-dispersion equation. J. Water Resour. Res. 2000, 35, 1403–1412. [Google Scholar] [CrossRef]

- Huang, G.; Huang, Q.; Zhan, H. Evidence of one-dimensional scale-dependent fractional advection-dispersion. J. Contemp. Hydrol. 2006, 85, 53–71. [Google Scholar] [CrossRef]

- Cutland, N.J.; Kopp, P.E.; Willinger, W. Stock price returns and the Joseph effect: A fractional version of the Black-Scholes model. Semin. Stoch. Anal. Random Fields Appl. 1995, 36, 327–351. [Google Scholar]

- Chang-Ming, C.; Fawang, L.; Kevin, B. Finite difference methods and a fourier analysis for the fractional reaction sub diffusion equation. Appl. Math. Comput. 2008, 2, 754–769. [Google Scholar]

- Nuugulu, S.M.; Gideon, F.; Patidar, K.C. A robust numerical solution to a time-fractional Black-Scholes equation. Adv. Differ. Equ. 2021, 2021, 123. [Google Scholar] [CrossRef]

- Nuugulu, S.M.; Gideon, F.; Patidar, K.C. A robust numerical scheme for a time-fractional Black-Scholes partial differential equation describing stock exchange dynamics. Chaos Solitons Fractals 2021, 145, 110753. [Google Scholar] [CrossRef]

- Donny, C.; Song, W. An upwind finite difference method for a nonlinear Black-Scholes equation governing European option valuation under transaction costs. Appl. Math. Comput. 2013, 219, 8811–8828. [Google Scholar]

- Liang, J.; Wang, J.; Zhang, W.; Qiu, W.; Ren, F. Option pricing of a bi-fractional Black-Scholes model with the Hurst exponent H in [1/2,1]. Appl. Math. Lett. 2010, 23, 859–863. [Google Scholar] [CrossRef]

- Meerschaert, M.M.; Tadjeran, C. Finite difference methods for two-dimensional fractional dispersion equation. J. Comput. Phys. 2006, 211, 249–261. [Google Scholar] [CrossRef]

- Murio, D.A. Implicit finite difference approximation for time fractional diffusion equations. Comput. Math. Appl. 2008, 56, 1138–1145. [Google Scholar] [CrossRef]

- Wang, H.; Wang, K.X.; Sircar, T. A direct O(N log2 N) finite difference method for fractional diffusion equations. J. Comput. Phys. 2009, 229, 8095–8104. [Google Scholar] [CrossRef]

- Bu, W.P.; Tang, Y.F.; Yang, J.Y. Galerkin finite element method for two-dimensional Riez space fractional diffusion equations. J. Comput. Phys. 2014, 267, 26–38. [Google Scholar] [CrossRef]

- Ford, N.J.; Xiao, J.Y.; Yan, Y.B. A finite element method for time fractional partial differential equations. Fract. Calc. Appl. Anal. 2011, 14, 454–474. [Google Scholar] [CrossRef]

- Jiang, Y.J.; Ma, J.T. High-order finite element methods for time-fractional partial differential equations. J. Comput. Math. 2011, 235, 3285–3290. [Google Scholar] [CrossRef]

- Canuto, C.; Hussaini, M.Y.; Quarteroni, A.; Zang, T.A. Spectral Methods: Fundamentals in Single Domains; Springer: Berlin/Heidelberg, Germany, 2006. [Google Scholar]

- Xu, C.; Lin, Y. Finite difference/spactral approximations for the time-fractional diffusion equation. J. Comput. Phys. 2007, 225, 1533–1552. [Google Scholar]

- Doha, E.H.; Bhrawy, A.H.; Ezz-Eldien, S.S. Effecient chebyshev spectral methods for solving multi-term fractional differential equations. J. Appl. Math. Model. 2011, 35, 5662–5672. [Google Scholar] [CrossRef]

- Kristoufek, L.; Vosvrda, M. Measuring capital market efficiency: Long-term memory, fractal dimension and approximate entropy. Eur. Phys. J. B 2014, 87, 162. [Google Scholar] [CrossRef]

- Sensoy, A.; Tabak, B.M. Time-varying long term memory in the European Union stock markets. Phys. A 2015, 436, 147–158. [Google Scholar] [CrossRef]

- Lahmiri, S. Long memory in international financial markets trends and short movements during the 2008 financial crisis based on variational mode decomposition and detrended fluctuation analysis. Phys. A 2015, 437, 130–138. [Google Scholar] [CrossRef]

- Panas, E. Long memory and chaotic models of prices on the London metal exchange. Resour. Policy 2001, 4, 485–490. [Google Scholar] [CrossRef]

- Acharya, V.V.; Richardson, M. Causes of the financial crisis. Crit. Rev. Found. 2009, 21, 195–210. [Google Scholar] [CrossRef]

- Jumarie, G. Merton’s model of optimal portfolio in a Black and Scholes market driven by a fractional Brownian motion with short-range dependence. Insur. Math. Econ. 2005, 37, 585–598. [Google Scholar] [CrossRef]

- Garzarelli, F.; Cristelli, M.; Pompa, G.; Zaccaria, A.; Pietronero, L. Memory effects in stock price dynamics: Evidence of technical trading. Scint. Rep. 2014, 4, 4487. [Google Scholar] [CrossRef]

- Chen, W.; Xu, X.; Zhu, S. Analytically pricing double barrier options on a time-fractional Black-Scholes equation. Comput. Math. Appl. 2015, 69, 1407–1419. [Google Scholar] [CrossRef]

- Atangana, A.; Secer, A. A note on fractional order derivatives and table of fractional derivatives of some special functions. Abstr. Appl. Anal. 2013, 2, 279681. [Google Scholar] [CrossRef]

- Jumarie, G. Modified Reimann-Liouville derivative and fractional Taylor series for non-differentiable functions, further results. Comput. Math. Appl. 2006, 51, 1367–1376. [Google Scholar] [CrossRef]

- Osler, T.J. Taylor’s series generalized for fractional derivatives and applications. SAIM-J. Math. Anal. 1971, 2, 37–47. [Google Scholar] [CrossRef]

- Jumarie, G. Stock exchange fractional dynamics defined as fractional exponential growth driven by (usual) Gaussian white noise. Application to fractional Black-Scholes equations. Insur. Math. Econ. 2008, 42, 271–287. [Google Scholar] [CrossRef]

- Jumarie, G. Derivation and solutions of some fractional Black-Scholes equations in coarse-grained space and time. Application to Merton’s optimal portfolio. Comput. Math. Appl. 2010, 59, 1142–1164. [Google Scholar] [CrossRef]

- Zhang, H.; Liu, F.; Turner, I.; Yang, Q. Numerical solution of the time fractional Black-Scholes model governing European options. Comput. Math. Appl. 2016, 71, 1772–1783. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| 0.1 | 7.1212 | 1.7901 | 4.4561 | 1.1525 | 2.9154 |

| 0.2 | 7.1336 | 1.8180 | 4.4711 | 1.1563 | 2.9250 |

| 0.3 | 7.3465 | 1.8383 | 4.5753 | 1.1827 | 2.9717 |

| 0.4 | 7.4609 | 1.9326 | 4.8371 | 1.2239 | 3.0759 |

| 0.5 | 8.1315 | 2.0213 | 5.1493 | 1.3000 | 3.2785 |

| 0.6 | 8.4515 | 2.1032 | 5.4620 | 1.3842 | 3.4915 |

| 0.7 | 9.5333 | 2.3909 | 6.1088 | 1.5478 | 3.7153 |

| 0.8 | 1.1062 | 2.5616 | 6.4925 | 1.6449 | 4.1409 |

| 0.9 | 1.2494 | 3.1452 | 7.8208 | 2.0062 | 5.0548 |

| 1.0 | 1.3815 | 3.4591 | 8.7754 | 2.2198 | 5.5953 |

| 0.1 | 1.91 | 1.95 | 1.98 | 1.99 |

| 0.2 | 1.92 | 1.96 | 1.98 | 1.99 |

| 0.3 | 1.93 | 1.96 | 1.98 | 1.99 |

| 0.4 | 1.93 | 1.96 | 1.98 | 1.99 |

| 0.5 | 1.93 | 1.97 | 1.98 | 1.99 |

| 0.6 | 1.94 | 1.97 | 1.98 | 1.99 |

| 0.7 | 1.94 | 1.97 | 1.98 | 1.99 |

| 0.8 | 1.94 | 1.97 | 1.98 | 1.99 |

| 0.9 | 1.94 | 1.97 | 1.98 | 1.99 |

| 1.0 | 1.94 | 1.97 | 1.98 | 1.99 |

| 0.1 | 6.5512 | 1.6492 | 4.1892 | 1.0597 | 2.5953 |

| 0.2 | 5.7988 | 1.4694 | 3.7170 | 9.4025 | 2.3784 |

| 0.3 | 5.2147 | 1.3191 | 3.3368 | 8.4408 | 2.1352 |

| 0.4 | 4.7443 | 1.2001 | 3.0358 | 7.6794 | 1.9426 |

| 0.5 | 4.3746 | 1.1066 | 2.7993 | 7.0810 | 1.7912 |

| 0.6 | 4.0893 | 1.0344 | 2.6167 | 6.6192 | 1.6544 |

| 0.7 | 3.8773 | 9.8080 | 2.4898 | 6.2752 | 1.5688 |

| 0.8 | 3.7318 | 9.4300 | 2.3779 | 6.0305 | 1.4980 |

| 0.9 | 3.6499 | 9.3328 | 2.4355 | 5.9979 | 1.5745 |

| 1.0 | 3.7328 | 9.2895 | 2.4246 | 5.9803 | 1.5670 |

| 0.1 | 1.95 | 1.98 | 1.99 | 1.99 |

| 0.2 | 1.96 | 1.98 | 1.99 | 1.99 |

| 0.3 | 1.96 | 1.98 | 1.99 | 1.99 |

| 0.4 | 1.96 | 1.98 | 1.99 | 2.00 |

| 0.5 | 1.97 | 1.98 | 1.99 | 2.00 |

| 0.6 | 1.97 | 1.98 | 1.99 | 2.00 |

| 0.7 | 1.97 | 1.98 | 1.99 | 2.00 |

| 0.8 | 1.97 | 1.98 | 1.99 | 2.00 |

| 0.9 | 1.97 | 1.98 | 1.99 | 2.00 |

| 1.0 | 1.97 | 1.98 | 1.99 | 2.00 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nuugulu, S.M.; Gideon, F.; Patidar, K.C. An Efficient Numerical Method for Pricing Double-Barrier Options on an Underlying Stock Governed by a Fractal Stochastic Process. Fractal Fract. 2023, 7, 389. https://doi.org/10.3390/fractalfract7050389

Nuugulu SM, Gideon F, Patidar KC. An Efficient Numerical Method for Pricing Double-Barrier Options on an Underlying Stock Governed by a Fractal Stochastic Process. Fractal and Fractional. 2023; 7(5):389. https://doi.org/10.3390/fractalfract7050389

Chicago/Turabian StyleNuugulu, Samuel Megameno, Frednard Gideon, and Kailash C. Patidar. 2023. "An Efficient Numerical Method for Pricing Double-Barrier Options on an Underlying Stock Governed by a Fractal Stochastic Process" Fractal and Fractional 7, no. 5: 389. https://doi.org/10.3390/fractalfract7050389

APA StyleNuugulu, S. M., Gideon, F., & Patidar, K. C. (2023). An Efficient Numerical Method for Pricing Double-Barrier Options on an Underlying Stock Governed by a Fractal Stochastic Process. Fractal and Fractional, 7(5), 389. https://doi.org/10.3390/fractalfract7050389