Green Hydrogen: Pathway to Net Zero Green House Gas Emission and Global Climate Change Mitigation

Abstract

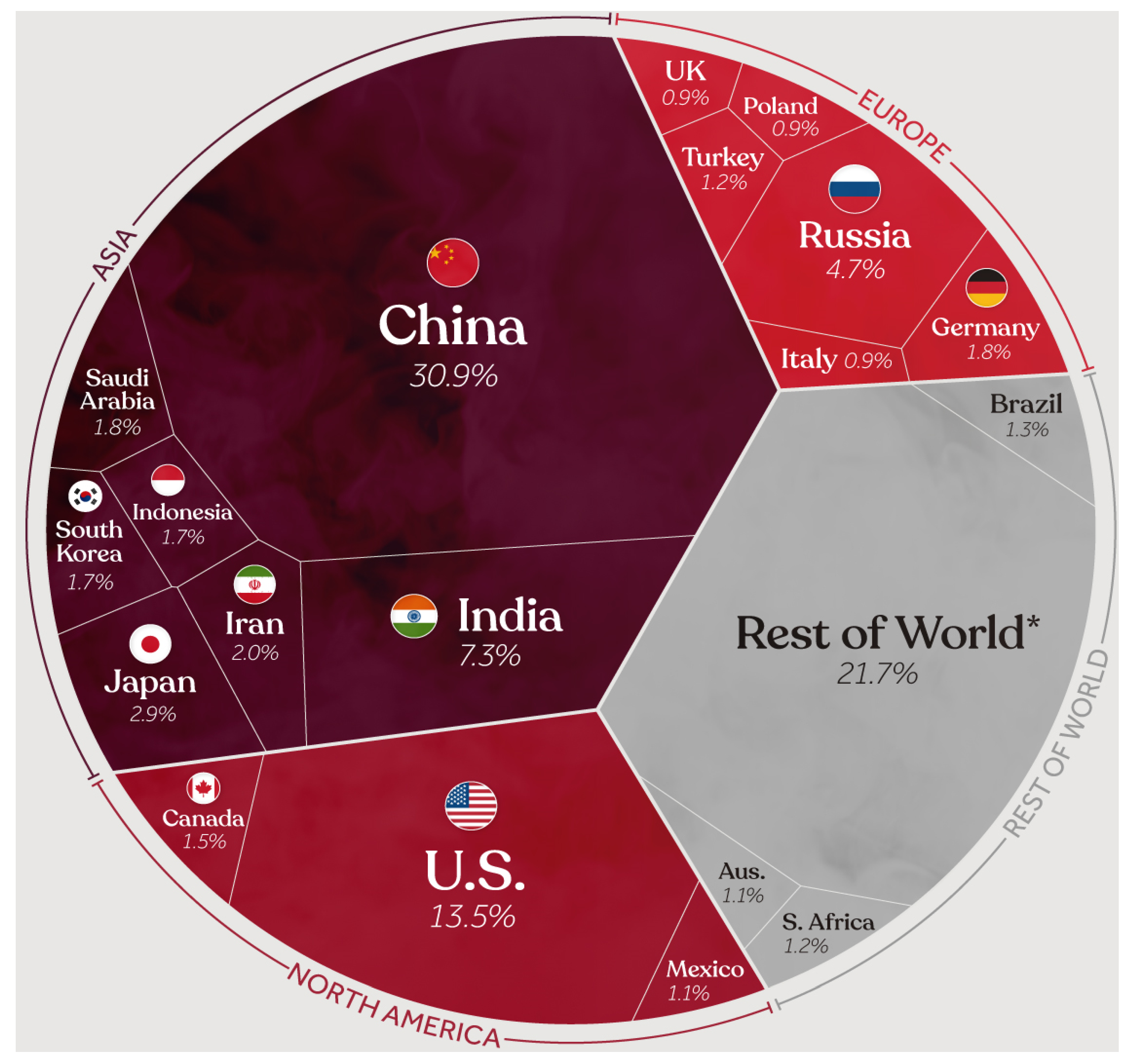

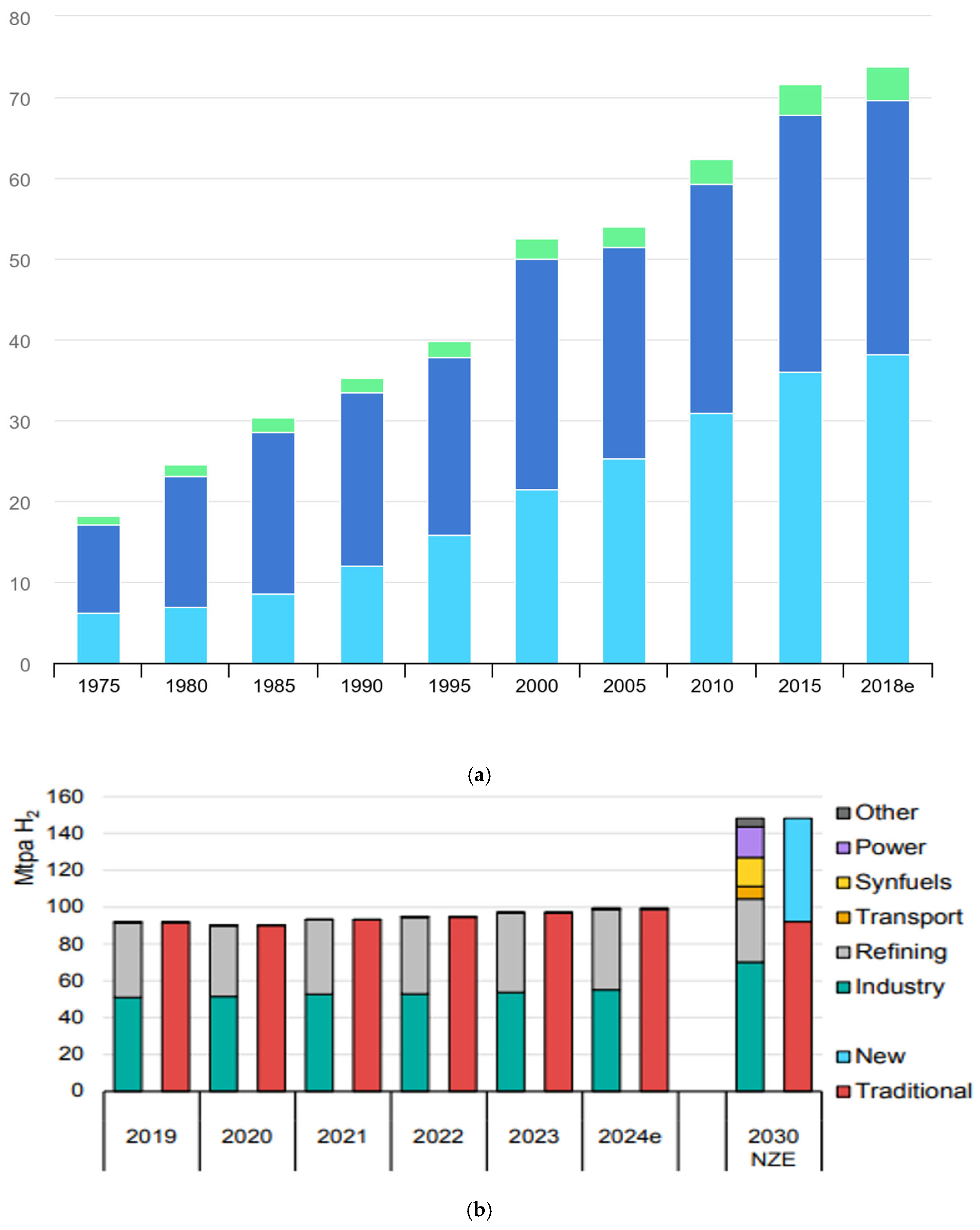

1. Introduction

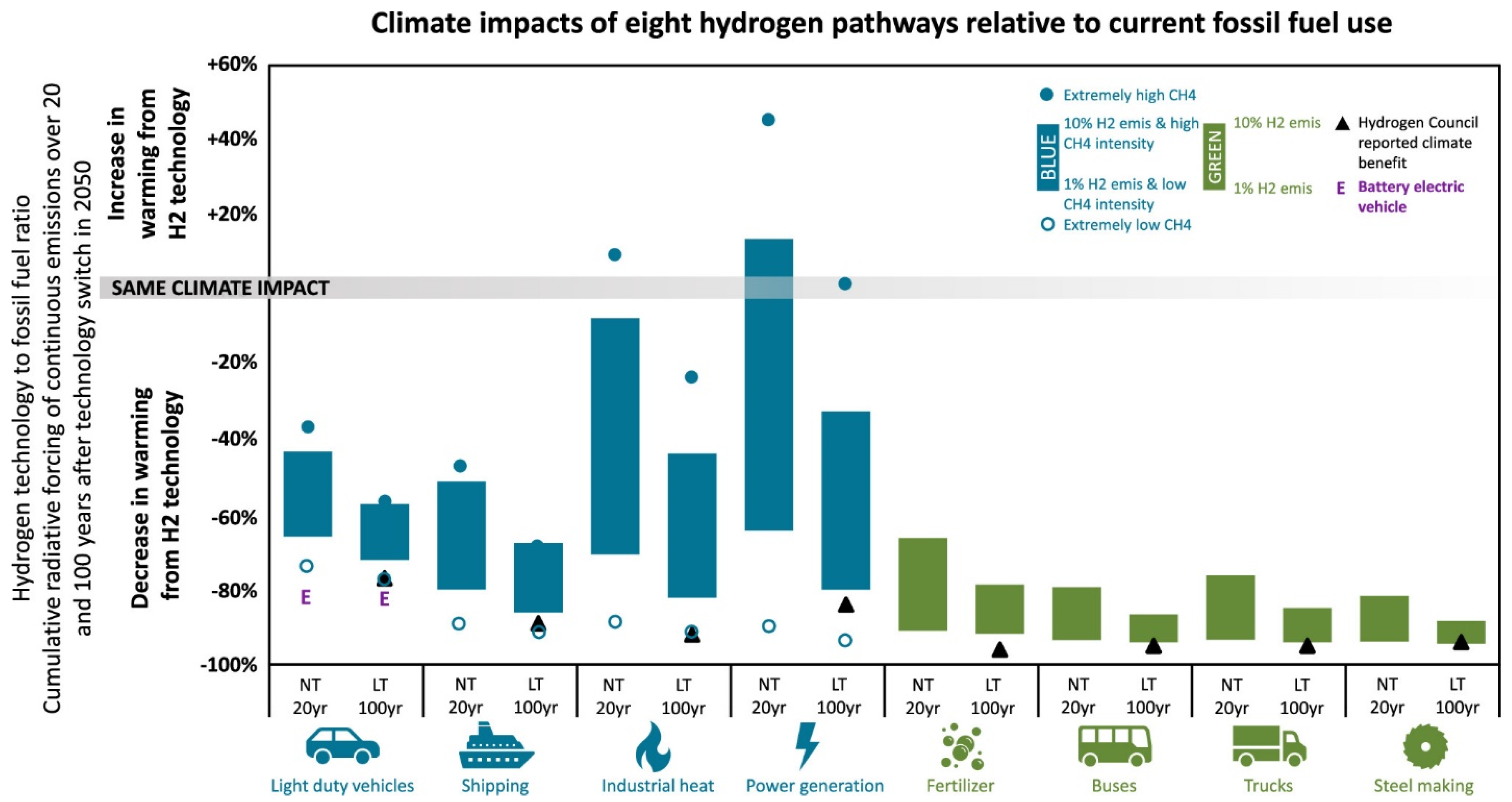

2. Potential of Green Hydrogen in Climate Change Mitigation

2.1. Green Hydrogen Presents a Viable Solution for Both Climate Change Mitigation and Cost Reduction in Sustainable Energy Systems

2.2. Case Studies of Successful Green Hydrogen Deployment

3. Green Hydrogen Production Methods

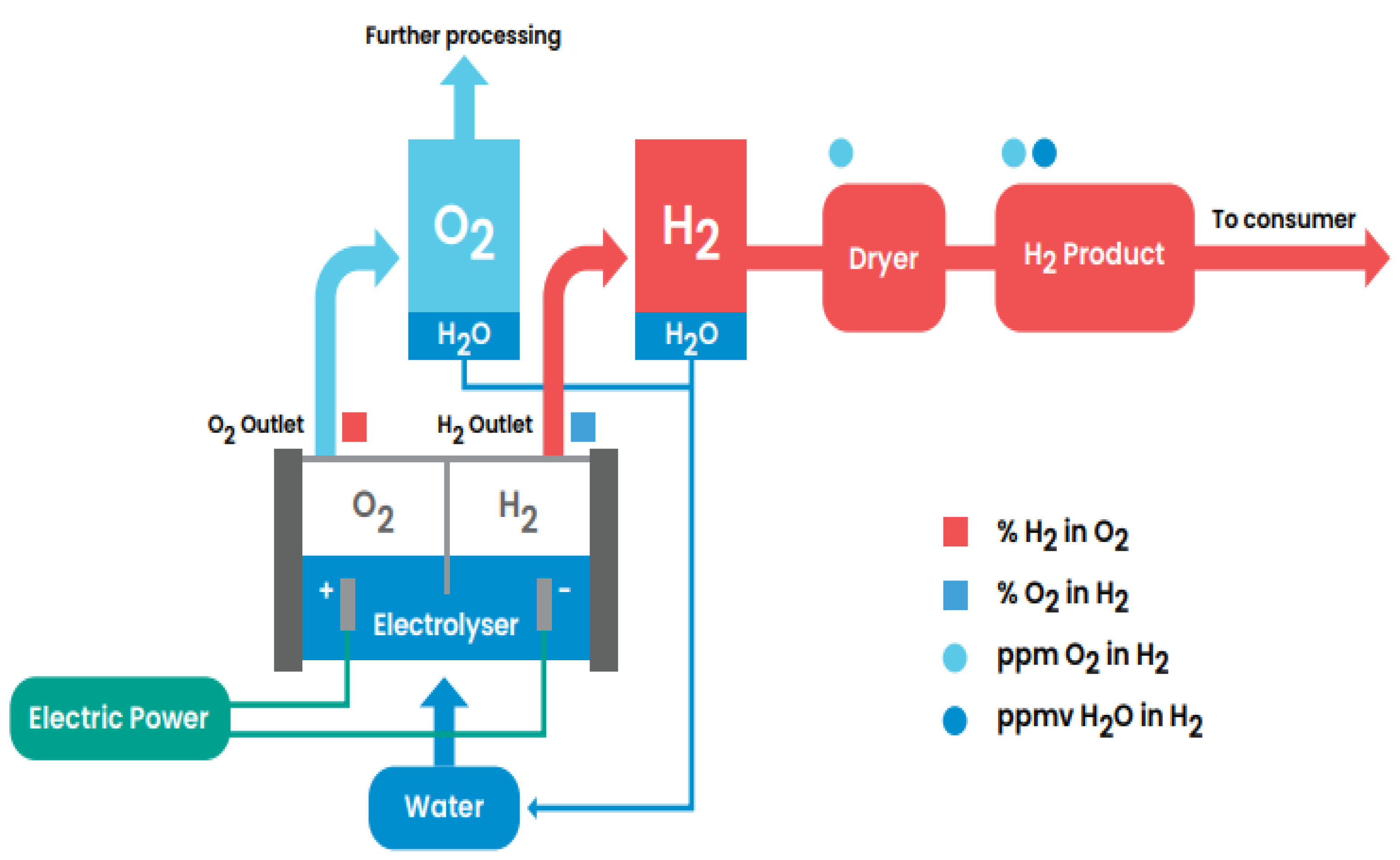

3.1. Electrolysis

3.1.1. Alkaline Electrolysis

3.1.2. Proton Membrane Electrolysis

3.1.3. High-Temperature Electrolysis

3.2. Biomass Gasification

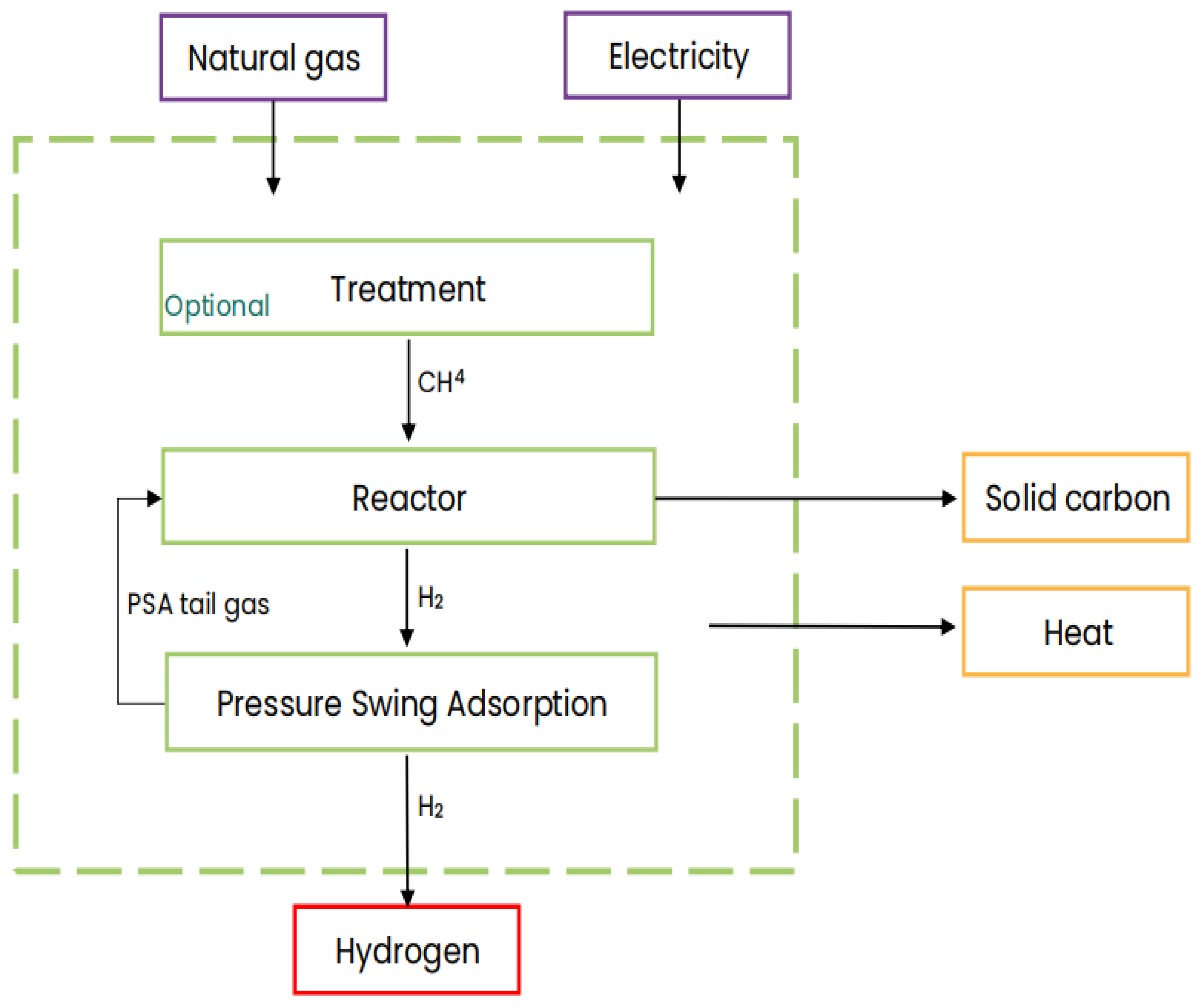

3.3. Natural Gas

4. Advantages of Green Hydrogen

4.1. Environmental Sustainability: Zero Carbon Emissions

4.2. Energy Storage Capabilities and Transportation: Balancing Renewable Energy Supply and Demand

4.3. Versatility in Applications

4.3.1. Transportation Sector

4.3.2. Industrial Sector

4.3.3. Heating

5. Challenges Facing the Adoption of Green Hydrogen

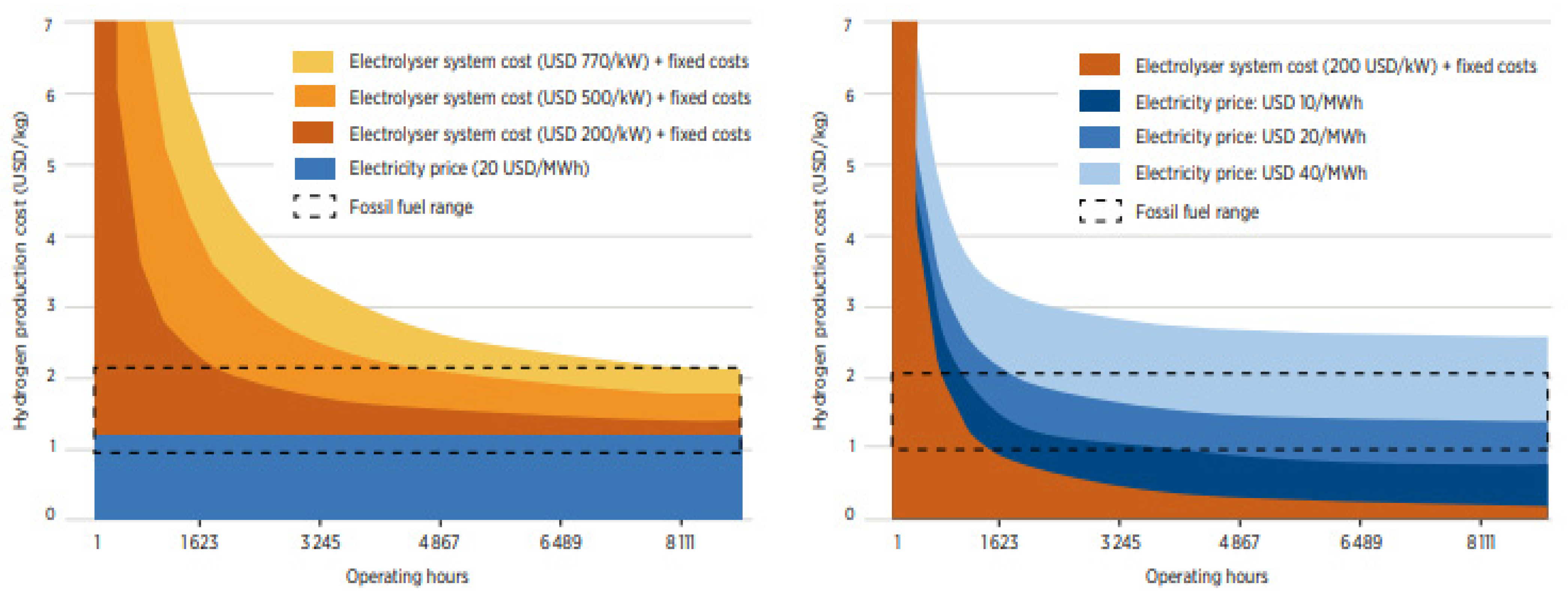

5.1. Cost Considerations: High Initial Investment and Operational Costs

5.2. Storage and Transportation Infrastructure Requirements

5.3. Technological Hurdles: Improving Electrolysis Efficiency and Reducing Equipment Costs

6. Green Hydrogen Policies and Initiatives

6.1. Government Policies and Incentives Supporting Green Hydrogen

6.1.1. The Inflation Reduction Act

6.1.2. The Infrastructure Investment and Jobs Act

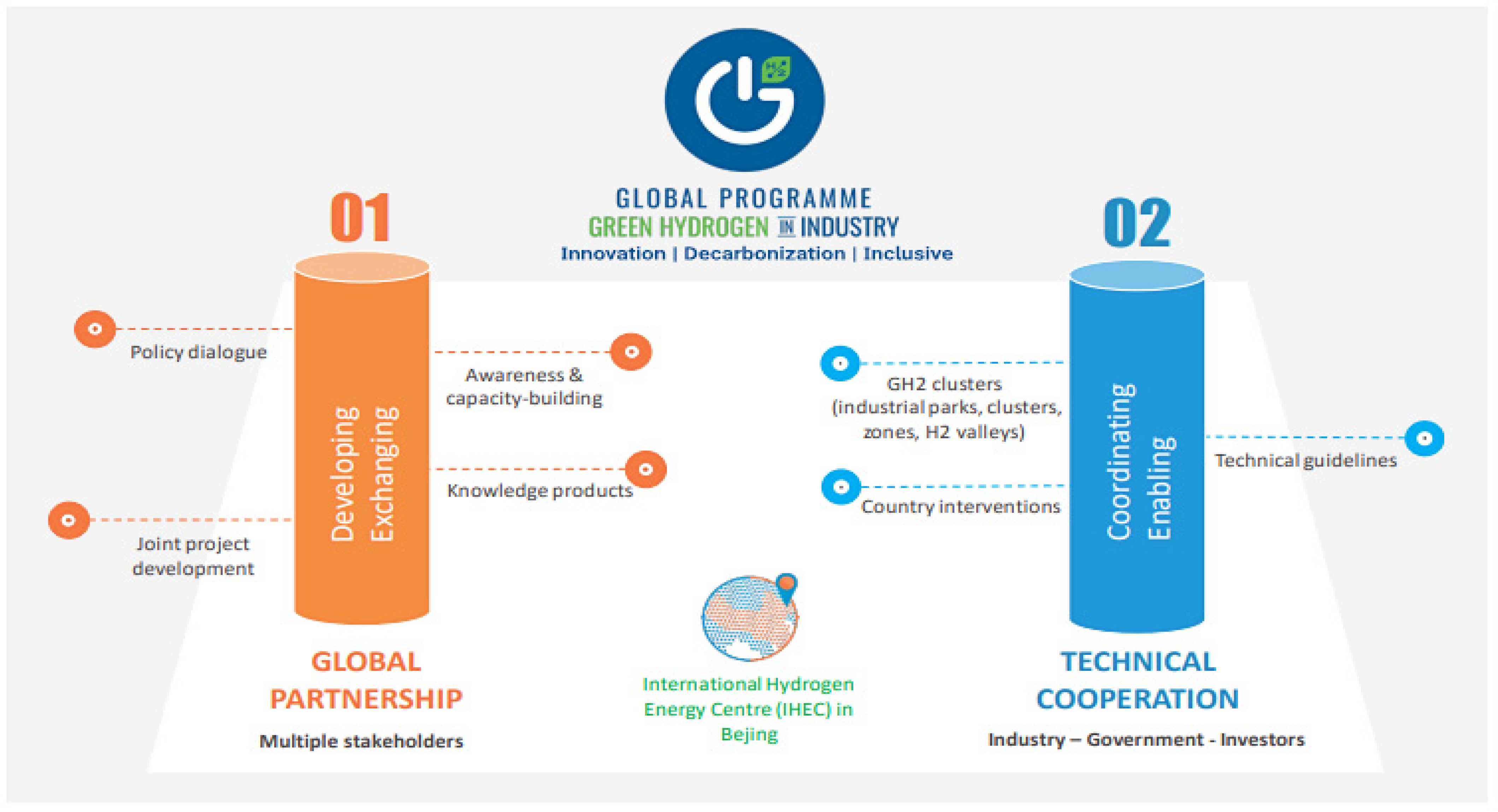

6.1.3. Industry Collaborations and Partnerships

6.2. Innovations and Research Advancements Towards Green Hydrogen Deployment

7. Future Outlook and Potential

8. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Mombekova, G.; Nurgabylov, M.; Baimbetova, A.; Keneshbayev, B.; Izatullayeva, B. The Relationship Between Energy Consumption, Population, and Economic Growth in Developing Countries. Int. J. Energy Econ. Policy 2024, 14, 368–374. [Google Scholar] [CrossRef]

- Feltrin, A.N. Energy Equality and the Challenges of Population Growth. Religions 2018, 6, 313. [Google Scholar] [CrossRef]

- Visual Capitalist. Global Carbon Atlas 2022. Available online: https://www.visualcapitalist.com/carbon-emissions-by-country-2022 (accessed on 28 March 2025).

- Olaleru, S.A.; Kirui, J.; Elegbeleye, F.; Aniyikaiye, T. Green Technology Solution to Global Climate Change Mitigation. Energy Environ. Storage J. 2021, 1, 26–41. [Google Scholar] [CrossRef]

- Elegbeleye, I.F. Studies of Interaction of Dye Molecules with TiO2 Brookite Clusters for Application in Dye-Sensitized Solar Cells. Ph.D. Thesis, University of Venda, Thohoyandou, Limpopo, South Africa, 2020. Available online: https://univendspace.univen.ac.za/handle/11602/1477 (accessed on 28 March 2025).

- Alirahmi, S.M.; Assareh, E.; Pourghassab, N.N.; Delpisheh, M.; Barelli, L.; Baldinelli, A. Green Hydrogen & Electricity Production via Geothermal-Driven Multi-Generation System: Thermo-Dynamic Modeling and Optimization. Fuel 2022, 308, 122049. [Google Scholar] [CrossRef]

- Vasseghian, Y.; Arunkumar, P.; Joo, S.W.; Gnanasekaran, L.; Kamyab, H.; Rajendran, S.; Balakrishnan, D.; Chelliapan, S.; Klemeš, J.J. Metal-Organic Framework-Enabled Pesticides Are an Emerging Tool for Sustainable Cleaner Production and Environmental Hazard Reduction. J. Clean. Prod. 2022, 373, 133966. [Google Scholar] [CrossRef]

- International Energy Agency. The Future of Hydrogen. 2019. Available online: https://www.iea.org/reports/the-future-of-hydrogen (accessed on 8 October 2024).

- Reda, B.; Elzamar, A.A.; AlFazzani, S.; Ezzat, S.M. Green Hydrogen as a Source of Renewable Energy: A Step Towards Sustainability, An Overview. Environ. Dev. Sustain. 2024, 1–21. [Google Scholar] [CrossRef]

- Hassan, Q.; Algburi, S.; Sameen, A.Z.; Salman, H.M.; Jaszczur, M. Green Hydrogen: A Pathway to a Sustainable Energy Future. Int. J. Hydrogen Energy 2024, 50, 310–333. [Google Scholar] [CrossRef]

- Osman, A.I.; Mehta, N.; Elgarahy, A.M.; Hefny, M.; Al-Hinai, A.; Al-Muhtaseb, A.A.H.; Rooney, D.W. Hydrogen Production, Storage, Utilization and Environmental Impacts: A Review. Environ. Chem. Lett. 2022, 20, 153–188. [Google Scholar] [CrossRef]

- Kartal, F.; Sezer, S.; Ozeveren, U. Investigation of steam and CO2 gasification for biochar using a circulating fluidized bed gasifier model in Aspen HYSYS. J. CO2 Util. 2022, 62, 102078. [Google Scholar] [CrossRef]

- International Energy Agency (IEA). The Future of Hydrogen: Seizing Today’s Opportunities; IEA: Paris, France, 2020. [Google Scholar]

- McKinsey & Company. Hydrogen: A Clean Fuel for the Future; McKinsey & Company: New York, NY, USA, 2022. [Google Scholar]

- International Energy Agency (IEA). The Role of Carbon Capture, Utilization, and Storage in the Hydrogen Economy; IEA: Paris, France, 2021. [Google Scholar]

- Arcos, J.M.M.; Santos, D.M. The hydrogen color spectrum: Techno-economic analysis of the available technologies for hydrogen production. Gases 2023, 3, 25–46. [Google Scholar] [CrossRef]

- Center on Global Energy Policy, Columbia University. Hydrogen Fact Sheet: Production of Low-Carbon Hydrogen. 2021. Available online: https://www.energypolicy.columbia.edu/sites/default/files/pictures/HydrogenProduction_CGEP_FactSheet_052621.pdf (accessed on 28 March 2025).

- World Economic Forum. The Many Colours of Hydrogen Explained. 2021. Available online: https://www.weforum.org/stories/2021/07/clean-energy-green-hydrogen/ (accessed on 28 March 2025).

- Xi-Liu, Y.U.E.; Qing-Xian, G.A.O. Contributions of Natural Systems and Human Activity to Greenhouse Gas Emissions. Adv. Clim. Chang. Res. 2018, 9, 243–252. [Google Scholar] [CrossRef]

- Mostefaoui, M.; Ciais, P.; McGrath, M.J.; Peylin, P.; Patra, P.K.; Ernst, Y. Greenhouse Gas Emissions and Their Trends over the Last Three Decades across Africa. Earth Syst. Sci. Data 2024, 16, 245–275. [Google Scholar] [CrossRef]

- Thapa, B.S.; Thapa, B. Green Hydrogen as a Future Multi-Disciplinary Research at Kathmandu University. J. Phys. Conf. Ser. 2020, 1608, 012020. [Google Scholar] [CrossRef]

- House of Commons Science and Technology Committee. The Role of Hydrogen in Achieving Net Zero: Fourth Report of Session 2022–23 (HC 99); UK Parliament: London, UK, 2022. [Google Scholar]

- Climateurope. What Is Climate and Climate Change? Available online: https://www.climateurope.eu/what-is-climate-and-climate-change (accessed on 8 October 2024).

- Adedeji, O.; Reuben, O.; Olatoye, O. Global Climate Change. J. Geosci. Environ. Prot. 2014, 2, 114–122. [Google Scholar] [CrossRef]

- Climate Change Information Resources, New York Metropolitan Region. Available online: https://www.earth.columbia.edu/news/2005/story03-25-05.html (accessed on 8 October 2021).

- Hydrogen Council. Hydrogen Insights 2023: An Update on the State of the Global Hydrogen Economy, with a Deep Dive into North America; Hydrogen Council: Brussels, Belgium, 2023; Available online: https://hydrogencouncil.com/wp-content/uploads/2023/05/Hydrogen-Insights-2023.pdf (accessed on 12 January 2024).

- Sun, T.; Shrestha, E.; Hamburg, S.P.; Kupers, R.; Ocko, I.B. Climate Impacts of Hydrogen and Methane Emissions Can Considerably Reduce the Climate Benefits across Key Hydrogen Use Cases and Time Scales. Environ. Sci. Technol. 2024, 58, 5299–5309. [Google Scholar] [CrossRef]

- Fasullo, J.T.; Otto-Bliesner, B.L.; Stevenson, S. ENSO’s changing influence on temperature, precipitation, and wildfire in a warming climate. Geophys. Res. Lett. 2018, 45, 9216–9225. [Google Scholar] [CrossRef]

- Hare, B.; Höhne, N.; Gütschow, J.; Schaeffer, M.; Vieweg-Mersmann, M. Climate action tracker. 2015. Available online: https://climateactiontracker.org/documents/39/CAT_2015-10-01_INDCsLowerProjectedWarming_CATUpdate.pdf (accessed on 1 October 2015).

- Hassan, Q.; Algburi, S.; Sameen, A.Z.; Salman, H.M.; Al-Jiboory, A.K. A review of green hydrogen production by renewable resources. Energy Harvest. Syst. 2024, 11, 20220127. [Google Scholar] [CrossRef]

- Baker Hughes. Water Electrolysis for Hydrogen Production; Baker Hughes: Houston, TX, USA, 2023. [Google Scholar]

- Obaideen, K.; Shehata, N.; Sayed, E.T.; Abdelkareem, M.A.; Mahmoud, M.S.; Olabi, A.G. The role of wastewater treatment in achieving sustainable development goals (SDGs) and sustainability guideline. Energy Nexus 2022, 7, 100112. [Google Scholar] [CrossRef]

- Wolfram, P.; Kyle, P.; Fuhrman, J.; O’Rourke, P.; McJeon, H. The hydrogen economy can reduce costs of climate change mitigation by up to 22%. One Earth 2024, 7, 885–895. [Google Scholar] [CrossRef]

- IRENA Coalition for Action. Decarbonising End-Use Sectors: Practical Insights on Green Hydrogen; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2021; Available online: https://www.irena.org/Publications/2021/Feb/Decarbonising-end-use-sectors-Practical-insights-on-green-hydrogen (accessed on 28 March 2025).

- Stadler Rail. Stadler Delivers North America’s First Hydrogen-Powered Passenger Train to San Bernardino County Transportation Authority. 2024. Available online: https://stadlerrail.com/hu/media/article/flirt-h2-sbcta-and-stadler-strengthen-sustainable-rail-transport-in-the-usa/1138/ (accessed on 8 April 2025).

- Plug Power. Plug Power and Olin Corporation Partner to Produce Green Hydrogen in 15 Ton Per Day Plant to Serve North America. 2022. Available online: https://www.ir.plugpower.com/press-releases/news-details/2022/Plug-Power-and-Olin-Corporation-Partner-to-Produce-Green-Hydrogen-in-15-Ton-Per-Day-Plant-to-Serve-North-America/default.aspx (accessed on 8 April 2025).

- Li, X.; Raorane, C.J.; Xia, C.; Wu, Y.; Tran, T.K.N.; Khademi, T. Latest approaches on green hydrogen as a potential source of renewable energy towards sustainable energy: Spotlighting of recent innovations, challenges, and future insights. Fuel 2023, 334, 126684. [Google Scholar] [CrossRef]

- Fernández-Arias, P.; Antón-Sancho, Á.; Lampropoulos, G.; Vergara, D. On green hydrogen generation technologies: A bibliometric review. Appl. Sci. 2024, 14, 2524. [Google Scholar] [CrossRef]

- Liu, R.T.; Xu, Z.L.; Li, F.M.; Chen, F.Y.; Yu, J.Y.; Yan, Y.; Chen, Y.; Xia, B.Y. Recent advances in proton exchange membrane water electrolysis. Chem. Soc. Rev. 2023, 52, 5652–5683. [Google Scholar] [CrossRef] [PubMed]

- Wang, L.; Pérez-Fortes, M.; Madi, H.; Diethelm, S.; Maréchal, F. Optimal design of solid-oxide electrolyzer based power-to-methane systems: A comprehensive comparison between steam electrolysis and co-electrolysis. Appl. Energy 2018, 211, 1060–1079. [Google Scholar] [CrossRef]

- Bianco, E.; Blanco, H. Green Hydrogen: A Guide to Policy Making; IRENA: Abu Dhabi, United Arab Emirates, 2020. [Google Scholar]

- Franco, A.; Giovannini, C. Recent and future advances in water electrolysis for green hydrogen generation: Critical analysis and perspectives. Sustainability 2023, 15, 16917. [Google Scholar] [CrossRef]

- Manabe, A.; Kashiwase, M.; Hashimoto, T.; Hayashida, T.; Kato, A.; Hirao, K.; Shimomura, I.; Nagashima, I. Basic Study of Alkaline Water Electrolysis. Electrochim. Acta 2013, 100, 249–256. [Google Scholar] [CrossRef]

- Rashid, M.M.; Al Mesfer, M.K.; Naseem, H.; Danish, M. Hydrogen Production by Water Electrolysis: A Review of Alkaline Water Electrolysis, PEM Water Electrolysis, and High Temperature Water Electrolysis. Int. J. Eng. Adv. Technol. 2019, 8, 81–85. [Google Scholar]

- Zhao, Y.; Zhang, L.; Li, X.; Wang, H.; Liu, Y.; Chen, J.; Li, Y.; Li, H.; Li, J.; Zhang, J. Advancements in Hydrogen Production Using Alkaline Electrolysis Systems Integrated with Renewable Energy Sources: A Review. Int. J. Hydrogen Energy 2024, 49, 5123–5140. [Google Scholar] [CrossRef]

- Shiva Kumar, S.; Himabindu, V. Hydrogen Production by PEM Water Electrolysis—A Review. Mater. Sci. Energy Technol. 2019, 2, 442–454. [Google Scholar] [CrossRef]

- Fallah Vostakola, M.; Ozcan, H.; El-Emam, R.S.; Amini Horri, B. Recent Advances in High-Temperature Steam Electrolysis with Solid Oxide Electrolysers for Green Hydrogen Production. Energies 2023, 16, 3327. [Google Scholar] [CrossRef]

- Carmo, M.; Fritz, D.L.; Mergel, J.; Stolten, D. A Comprehensive Review on PEM Water Electrolysis. Int. J. Hydrogen Energy 2013, 38, 4901–4934. [Google Scholar] [CrossRef]

- Mika, Ł.; Sztekler, K.; Bujok, T.; Boruta, P.; Radomska, E. Seawater Treatment Technologies for Hydrogen Production by Electrolysis—A Review. Energies 2024, 17, 6255. [Google Scholar] [CrossRef]

- Chen, Y.; Brandon, N.P.; Brightman, E.; Costa, R.; White, T.; Neville, T.; Kilner, J.A. High Temperature Co-Electrolysis of Steam and CO2 in an SOC Stack: Performance and Durability. Fuel Cells 2013, 13, 638–643. [Google Scholar] [CrossRef]

- Jaradat, M.; Almashaileh, S.; Bendea, C.; Juaidi, A.; Bendea, G.; Bungau, T. Green Hydrogen in Focus: A Review of Production Technologies, Policy Impact, and Market Developments. Energies 2024, 17, 3992. [Google Scholar] [CrossRef]

- Elder, R.; Cumming, D.; Mogensen, M.B. High Temperature Electrolysis. In Carbon Dioxide Utilisation: Closing the Carbon Cycle; Styring, P., Quadrelli, E.A., Armstrong, K., Eds.; Elsevier: Amsterdam, The Netherlands, 2015; pp. 183–209. [Google Scholar]

- Acar, C.; Dincer, I. Hydrogen Production. In Comprehensive Energy Systems; Dincer, I., Ed.; Elsevier: Amsterdam, The Netherlands, 2018; pp. 1–40. [Google Scholar]

- Demirbaş, A. Biomass resource facilities and biomass conversion processing for fuels and chemicals. Energy Convers. Manag. 2001, 42, 1357–1378. [Google Scholar] [CrossRef]

- Hosseini, S.E.; Wahid, M.A. Hydrogen production from renewable and sustainable energy resources: Promising green energy carrier for clean development. Renew. Sustain. Energy Rev. 2016, 57, 850–866. [Google Scholar] [CrossRef]

- Liu, S.; Zhu, J.; Chen, M.; Xin, W.; Yang, Z.; Kong, L. Hydrogen production via catalytic pyrolysis of biomass in a two-stage fixed bed reactor system. Int. J. Hydrogen Energy 2014, 39, 13128–13135. [Google Scholar] [CrossRef]

- Wang, Z.; He, T.; Qin, J.; Wu, J.; Li, J.; Zi, Z.; Liu, G.; Wu, J.; Sun, L. Gasification of biomass with oxygen-enriched air in a pilot scale two-stage gasifier. Fuel 2015, 150, 386–393. [Google Scholar] [CrossRef]

- Levin, D.B.; Pitt, L.; Love, M. Biohydrogen production: Prospects and limitations to practical application. Int. J. Hydrogen Energy 2004, 29, 173–185. [Google Scholar] [CrossRef]

- Bakenne, A.; Nuttall, W.; Kazantzis, N. Sankey-Diagram-based insights into the hydrogen economy of today. Int. J. Hydrogen Energy 2016, 41, 7744–7753. [Google Scholar] [CrossRef]

- Dunn, S. Hydrogen futures: Toward a sustainable energy system. Int. J. Hydrogen Energy 2002, 27, 235–264. [Google Scholar] [CrossRef]

- Lützkendorf, T.; Frischknecht, R. (Net-) zero-emission buildings: A typology of terms and definitions. Build. Cities 2020, 1, 1–22. [Google Scholar] [CrossRef]

- Safari, F.; Dincer, I. A review and comparative evaluation of thermochemical water splitting cycles for hydrogen production. Energy Convers. Manag. 2020, 205, 112182. [Google Scholar] [CrossRef]

- Millet, P.; Mbemba, N.; Grigoriev, S.A.; Fateev, V.N.; Aukauloo, A.; Etiévant, C. Electrochemical performances of PEM water electrolysis cells and perspectives. Int. J. Hydrogen Energy 2011, 36, 4134–4142. [Google Scholar] [CrossRef]

- Hutsol, T.; Glowacki, S.; Tryhuba, A.; Kovalenko, N.; Pustova, Z.; Rozkosz, A.; Sukmaniuk, O. Current Trends of Biohydrogen Production from Biomass—Green Hydrogen; International Visegrad Fund: Bratislava, Slovakia, 2021. [Google Scholar]

- Mirza, U.K.; Ahmad, N.; Harijan, K.; Majeed, T. A vision for hydrogen economy in Pakistan. Renew. Sustain. Energy Rev. 2009, 13, 1111–1115. [Google Scholar] [CrossRef]

- Bradhurst, D.H.; Heuer, P.M.; Stolarski, G.Z.A. Hydrogen Production and Storage. 1981. Available online: https://trid.trb.org/View/170286 (accessed on 28 March 2025).

- Abad, A.V.; Dodds, P.E. Production of Hydrogen; No. 2015; Elsevier: Amsterdam, The Netherlands, 2017; Volume 3. [Google Scholar]

- Acar, C.; Dincer, I. Comparative assessment of hydrogen production methods from renewable and non-renewable sources. Int. J. Hydrogen Energy 2014, 39, 1–12. [Google Scholar] [CrossRef]

- Krumpelt, M.; Krause, T.R.; Carter, J.D.; Kopasz, J.P.; Ahmed, S. Fuel processing for fuel cell systems in transportation and portable power applications. Catal. Today 2002, 77, 3–16. [Google Scholar] [CrossRef]

- Hydrogen Europe. Clean Hydrogen Production Pathways; Hydrogeneurope.eu Report; Hydrogen Europe: Brussels, Belgium, 2024. [Google Scholar]

- Van Rensburg, P.; Pretorius, I.S. Enzymes in winemaking: Harnessing natural catalysts for efficient biotransformations. S. Afr. J. Enol. Vitic. 2000, 21, 52–73. [Google Scholar]

- International Renewable Energy Agency (IRENA). Green Hydrogen: A Guide for Policymakers; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2020. [Google Scholar]

- Dash, S.; Singh, A.; Jose, S.; Elangovan, D.; Surapraraju, S.K.; Natarajan, S.K. Advances in green hydrogen production through alkaline water electrolysis: A comprehensive review. Int. J. Hydrogen Energy 2024, 83, 614–629. [Google Scholar] [CrossRef]

- Searcy, E.; Flynn, P. The impact of biomass availability and processing cost on optimum size and processing technology selection. Appl. Biochem. Biotechnol. 2009, 154, 92–107. [Google Scholar] [CrossRef]

- Jiang, H.; Qi, B.; Du, E.; Zhang, N.; Yang, X.; Yang, F.; Wu, Z. Modeling hydrogen supply chain in renewable electric energy system planning. IEEE Trans. Ind. Appl. 2021, 58, 2780–2791. [Google Scholar] [CrossRef]

- Hydrogen Council. Hydrogen for Net-Zero: A Pathway to Achieving the Global Climate Goals; Hydrogen Council: Brussels, Belgium, 2021; Available online: https://hydrogencouncil.com/wp-content/uploads/2021/11/Hydrogen-for-Net-Zero.pdf (accessed on 28 March 2025).

- Hydrogen Council. Hydrogen for Net Zero—A Critical Cost-Competitive Energy Vector; Hydrogen Council: Brussels, Belgium, 2021. [Google Scholar]

- Maka, A.O.; Mehmood, M. Green hydrogen energy production: Current status and potential. Clean Energy 2024, 8, 1–7. [Google Scholar] [CrossRef]

- U.S. Department of Energy. Hydrogen Storage. Available online: https://www.energy.gov/eere/fuelcells/hydrogen-storage (accessed on 28 March 2025).

- Zhang, T.; Uratani, J.; Huang, Y.; Xu, L.; Griffiths, S.; Ding, Y. Hydrogen liquefaction and storage: Recent progress and perspectives. Renew. Sustain. Energy Rev. 2023, 176, 113204. [Google Scholar] [CrossRef]

- Yue, M.; Lambert, H.; Pahon, E.; Roche, R.; Jemei, S.; Hissel, D. Hydrogen energy systems: A critical review of technologies, applications, trends and challenges. Renew. Sustain. Energy Rev. 2021, 146, 111180. [Google Scholar] [CrossRef]

- Shift2Rail. Study on the Usage of Fuel Cells and Hydrogen in the Railway Environment; Shift2Rail: Brussels, Belgium, 2021; Available online: https://rail-research.europa.eu/wp-content/uploads/2019/04/Report-2.pdf (accessed on 11 March 2025).

- Tzanetis, K.F.; Posada, J.A.; Ramirez, A. Analysis of biomass hydrothermal liquefaction and biocrude-oil upgrading for renewable jet fuel production: The impact of reaction conditions on production costs and GHG emissions performance. Renew. Energy 2017, 113, 1388–1398. [Google Scholar] [CrossRef]

- Eichman, J.; Townsend, A.; Melaina, M. Economic Assessment of Hydrogen Technologies Participating in California Electricity Markets (No. NREL/TP-5400-65856); National Renewable Energy Laboratory (NREL): Golden, CO, USA, 2016. [Google Scholar]

- Deniz, C.; Zincir, B. Environmental and economical assessment of alternative marine fuels. J. Clean. Prod. 2016, 113, 438–449. [Google Scholar] [CrossRef]

- U.S. Department of Energy. Hydrogen Use in Industry. Available online: https://www.energy.gov/eere/fuelcells/h2scale (accessed on 28 March 2025).

- European Parliament. Hydrogen in Steelmaking: A Key to Decarbonization. Available online: https://www.europarl.europa.eu/RegData/etudes/BRIE/2020/641552/EPRS_BRI(2020)641552_EN.pdf (accessed on 28 March 2025).

- Linde Group. The Role of Hydrogen in Removing Sulfur from Liquid Fuels. Available online: https://assets.linde.com/-/media/global/corporate/corporate/documents/sustainable-development/climate-change/the-role-of-hydrogen-in-removing-sulfur-from-liquid-fuels-w-disclaimer-r1.pdf (accessed on 28 March 2025).

- Maggio, G.; Nicita, A.; Squadrito, G. How the hydrogen production from RES could change energy and fuel markets: A review of recent literature. Int. J. Hydrogen Energy 2019, 44, 11371–11384. [Google Scholar] [CrossRef]

- Lebrouhi, B.E.; Djoupo, J.J.; Lamrani, B.; Benabdelaziz, K.; Kousksou, T. Global hydrogen development—A technological and geopolitical overview. Int. J. Hydrogen Energy 2022, 47, 7016–7048. [Google Scholar] [CrossRef]

- Ayodele, T.R.; Munda, J.L. Potential and economic viability of green hydrogen production by water electrolysis using wind energy resources in South Africa. Int. J. Hydrogen Energy 2019, 44, 17669–17687. [Google Scholar] [CrossRef]

- Xiang, H.; Ch, P.; Nawaz, M.A.; Chupradit, S.; Fatima, A.; Sadiq, M. Integration and economic viability of fueling the future with green hydrogen: An integration of its determinants from renewable economics. Int. J. Hydrogen Energy 2021, 46, 38145–38162. [Google Scholar] [CrossRef]

- Longden, T.; Beck, F.J.; Jotzo, F.; Andrews, R.; Prasad, M. ‘Clean’ hydrogen?—Comparing the emissions and costs of fossil fuel versus renewable electricity based hydrogen. Appl. Energy 2022, 306, 118145. [Google Scholar] [CrossRef]

- Khan, M.M.K.; Azad, A.K.; Oo, A.M.T. (Eds.) Hydrogen Energy Conversion and Management; Elsevier: Chicago, IL, USA, 2023. [Google Scholar]

- Phoumin, H.; Kimura, F.; Arima, J. Potential green hydrogen from curtailed electricity in ASEAN: The scenarios and policy implications. In Energy Sustainability and Climate Change in ASEAN; Springer: Singapore, 2021; pp. 195–216. [Google Scholar]

- Chang, Y.; Phoumin, H. Curtailed electricity surplus from renewables for hydrogen: Economic and environmental analysis. In Hydrogen Sourced from Renewables and Clean Energy: A Feasibility Study of Achieving Large-Scale Demonstration; ERIA: Jakarta, Indonesia, 2021; pp. 225–242. [Google Scholar]

- United Nations Industrial Development Organization (UNIDO). Global Programme Green Hydrogen in Industry Report 2022; United Nations Industrial Development Organization: Vienna, Austria, 2022. [Google Scholar]

- Megía, P.J.; Vizcaíno, A.J.; Calles, J.A.; Carrero, A. Hydrogen production technologies: From fossil fuels toward renewable sources. A mini review. Energy Fuels 2021, 35, 16403–16415. [Google Scholar] [CrossRef]

- Hydrogen Council. Hydrogen Insights: A Perspective on Hydrogen Investment, Market Development, and Cost Competitiveness; Hydrogen Council: Brussels, Belgium, 2021; Available online: https://hydrogencouncil.com/en/hydrogen-insights-2021 (accessed on 28 March 2025).

- European Commission. A Hydrogen Strategy for a Climate-Neutral Europe; European Commission: Brussels, Belgium, 2020; Available online: https://ec.europa.eu/energy/sites/ener/files/hydrogen_strategy.pdf (accessed on 28 March 2025).

- U.S. Department of Energy. Hydrogen Shot: Reducing the Cost of Clean Hydrogen; U.S. Department of Energy: Washington, DC, USA, 2021. Available online: https://www.energy.gov/eere/fuelcells/hydrogen-shot (accessed on 28 March 2025).

- Samsun, R.C.; Antoni, L.; Rex, M. Mobile Fuel Cell Application: Tracking Market Trends; AFC TCP: Paris, France, 2020; Available online: https://www.ieafuelcell.com/fileadmin/publications/2020_AFCTCP_Mobile_FC_Application_Tracking_Market_Trends_2020.pdf (accessed on 31 March 2025).

- Züttel, A. Hydrogen storage methods. Naturwissenschaften 2004, 91, 157–172. [Google Scholar] [CrossRef] [PubMed]

- Nguyen, T.T.; Tak, N.; Park, J.; Nahm, S.H.; Baek, U.B. Hydrogen embrittlement susceptibility of X70 pipeline steel weld under a low partial hydrogen environment. Int. J. Hydrogen Energy 2020, 45, 23739–23753. [Google Scholar] [CrossRef]

- Ahluwalia, R.K.; Wang, X. Fuel cell systems for transportation: Status and trends. J. Power Sources 2008, 177, 167–176. [Google Scholar] [CrossRef]

- Birol, F. The future of hydrogen: Seizing today’s opportunities. IEA Rep. 2019, 20, 442. [Google Scholar]

- Mikunda, T.; Sattler, C. Hydrogen Safety: Approaches, Challenges, and Solutions; Energy Central: Energy Central, CO, USA, 2024; Available online: https://energycentral.com/c/pip/hydrogen-safety-approaches-challenges-and-solutions (accessed on 11 March 2025).

- Hydrogen Infrastructure Report; Hydrogen Europe: Brussels, Belgium, 2024. Available online: https://hydrogeneurope.eu/wp-content/uploads/2024/10/2024.10_HE_.Hydrogen-Infrastructure-Report.pdf (accessed on 11 March 2025).

- U.S. Department of Energy. Hydrogen Storage Basics; U.S. Department of Energy: Washington, DC, USA, 2022. Available online: https://www.energy.gov/eere/fuelcells/hydrogen-storage-basics (accessed on 28 March 2025).

- NASA. Cryogenic Hydrogen Storage for Aerospace Applications; NASA: Washington DC, USA, 2021; Available online: https://www.iea.org/reports/ammonia-technology-roadmap (accessed on 28 March 2025).

- International Energy Agency. Ammonia as a Hydrogen Carrier: Opportunities and Challenges; International Energy Agency: Paris, France, 2022; Available online: https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2022/May/IRENA_Innovation_Outlook_Ammonia_2022.pdf (accessed on 28 March 2025).

- Fraunhofer Institute. Liquid Organic Hydrogen Carriers: A Safe and Efficient Hydrogen Transport Solution; Fraunhofer Institute: Bremen, Germany, 2023; Available online: https://www.fraunhofer.de/en/research/fraunhofer-strategic-research-fields/hydrogen-technologies/synthetic-fuels-and-hydrogen-carrier-materials.html (accessed on 28 March 2025).

- European Hydrogen Backbone. Hydrogen Pipeline Expansion Strategy; European Hydrogen Backbone: Bruxelles, Belgium, 2023; Available online: https://ehb.eu/files/downloads/EHB-2023-Implementation-Roadmap-Part-1.pdf (accessed on 28 March 2025).

- BNEF (Bloomberg New Energy Finance). Hydrogen Economy Outlook; Bloomberg New Energy Finance: London, UK, 2020. [Google Scholar]

- Vermeulen, U. Turning a hydrogen economy into reality. In Proceedings of the 28th Meeting Steering Committee IPHE, The Hague, The Netherlands, 21 November 2017. [Google Scholar]

- International Energy Agency (IEA). Global Hydrogen Review 2022; IEA: Paris, France, 2022; Available online: https://www.iea.org/reports/global-hydrogen-review-2022 (accessed on 19 August 2024).

- Australian Renewable Energy Agency (ARENA). Hydrogen Production and Market Development; Australian Renewable Energy Agency (ARENA): Canberra, Australia, 2020. Available online: https://arena.gov.au/funding/renewable-hydrogen-deployment-funding-round/ (accessed on 28 March 2025).

- Vetter, T.; Finkenrath, M. Hydrogen Production from Natural Gas Reforming: Cost and Emissions Assessment; International Energy Agency (IEA): Paris, France, 2021. [Google Scholar]

- IRENA. Green Hydrogen Cost Reduction Pathways; IRENA: Abu Dhabi, United Arab Emirates, 2021; Available online: https://www.irena.org/Publications/2021/06/Green-Hydrogen-Cost-Reduction-Pathways (accessed on 28 March 2025).

- Hydrogen Council. Hydrogen Insights: Market Trends and Cost Forecasts; Hydrogen Council: Brussels, Belgium, 2022; Available online: https://hydrogencouncil.com/en/hydrogen-insights-2022/ (accessed on 28 March 2025).

- IRENA. Green Hydrogen Cost Reduction: Scaling Up Electrolysers to Meet the 1.5 °C Climate Goal; IRENA: Abu Dhabi, United Arab Emirates, 2020; Available online: https://www.irena.org/Publications/2020/06/Green-hydrogen-cost-reduction (accessed on 28 March 2025).

- BloombergNEF. Hydrogen Economy Outlook: Key Trends and Cost Trajectories; BloombergNEF: London, UK, 2022; Available online: https://about.bnef.com/new-energy-outlook/ (accessed on 28 March 2025).

- Lantz, K.; Sower, L. Fueling a Hydrogen Boom: Federal and State Policies for Promoting Green Hydrogen. Wm. Mary Env’t L. Pol. Rev. 2023, 48, 95–116. [Google Scholar]

- Petit, J.A. Green Hydrogen’s Key Moment; Kleinman Center for Energy Policy: Philadelphia, PA, USA, 2022; Available online: https://kleinmanenergy.upenn.edu/news-insights/green-hydrogens-key-moment/ (accessed on 6 March 2025).

- Crouch, L.; Feldman, D.; Lowther, T.; Salinas, G.; Samji, O.; Yazdani, H. Inflation Reduction Act: Key Green and Blue Hydrogen and CCUS Provisions; Shearman & Sterling: New York, NY, USA, 2022; Available online: https://www.shearman.com/en/perspectives/2022/08/inflation-reduction-act-key-green-and-blue-hydrogen-and-ccus-provisions (accessed on 6 March 2025).

- Cranor, T.; Henley, G.; Kaercher, M.; Sweeney, K. Clean Hydrogen Tax Credit: Why Induced Emissions Must be Considered; The Tax Law Center at NYU Law: New York, NY, USA, 2024. [Google Scholar]

- World Bank Group. World Bank Proposes 10 GW Clean Hydrogen Initiative to Boost Adoption of Low-Carbon Energy; World Bank Group: Washington, DC, USA, 2023; Available online: https://www.worldbank.org/en/news/press-release/2023/11/17/world-bank-proposes-10-gw-clean-hydrogen-initiative-to-boost-adoption-of-low-carbon-energy (accessed on 31 March 2025).

- Organisation for Economic Co-operation and Development (OECD). Global Hydrogen Review 2023; OECD Publishing: Paris, France, 2023; Available online: https://www.oecd.org/en/publications/global-hydrogen-review-2023_cb2635f6-en.html (accessed on 31 March 2025).

- International Renewable Energy Agency (IRENA). International Co-operation to Accelerate Green Hydrogen Deployment; IRENA: Abu Dhabi, United Arab Emirates, 2023; Available online: https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2024/Apr/IRENA_CF_Green_hydrogen_deployment_2024.pdf (accessed on 31 March 2025).

- Trüby, J.; Villavicencio, M.; Brauer, J.; Ailleret, A.; Lévêque, C.; de Froidefond, M.; Chabanis, J.; Hooda, A. Assessing the Impact of Low-Carbon Hydrogen Regulation in the EU. Deloitte, 24 July 2024; 62p. Available online: https://www.agora-energiewende.org/publications/assessing-the-impact-of-low-carbon-hydrogen-regulation-in-the-eu (accessed on 23 July 2024).

- Australian Government; UK Government. Global Clean Power Alliance Finance Mission Statement; Australian Government: Barton, Australia; UK Government: Londo, UK, 2023. Available online: https://www.gov.uk/government/publications/global-clean-power-alliance-finance-mission-statement/global-clean-power-alliance-finance-mission-statement. (accessed on 31 March 2025).

- International Renewable Energy Agency (IRENA). Geopolitics of the Energy Transition: Hydrogen as a Key Player; IRENA: Abu Dhabi, United Arab Emirates, 2023; Available online: https://www.irena.org/Publications/2023/Jan/Geopolitics-of-the-Energy-Transition-Hydrogen (accessed on 31 March 2025).

- Hydrogen Council; McKinsey & Company. Global Hydrogen Flows—2023 Update; Hydrogen Council: Brussels, Belgium, 2023; Available online: https://hydrogencouncil.com/en/global-hydrogen-flows-2023-update/ (accessed on 31 March 2025).

- World Economic Forum (WEF). Hydrogen’s Star Is Rising as a Clean Energy Transition Fuel; WEF: Geneva, Switzerland, 2023; Available online: https://www.weforum.org/stories/2023/01/hydrogen-clean-energy-transition-2023/ (accessed on 31 March 2025).

- International Energy Agency (IEA). Global Hydrogen Review 2023; IEA: Paris, France, 2023; Available online: https://www.iea.org/reports/global-hydrogen-review-2023 (accessed on 31 March 2025).

- Doe, J.; Smith, A.; Lee, K. Supply Chain Resilience in Hydrogen Valleys: Addressing Challenges and Opportunities in Green Hydrogen Ecosystems. Energies 2024, 17, 409–433. [Google Scholar] [CrossRef]

- Gupta, S.; Kumar, R.; Kumar, A. Green hydrogen in India: Prioritization of its potential and viable renewable source. Int. J. Hydrogen Energy 2024, 50, 226–238. [Google Scholar] [CrossRef]

- Li, Y.; Taghizadeh-Hesary, F. The economic feasibility of green hydrogen and fuel cell electric vehicles for road transport in China. Energy Policy 2022, 160, 112703. [Google Scholar] [CrossRef]

- Liu, W.; Wan, Y.; Xiong, Y.; Gao, P. Green hydrogen standard in China: Standard and evaluation of low-carbon hydrogen, clean hydrogen, and renewable hydrogen. Int. J. Hydrogen Energy 2022, 47, 24584–24591. [Google Scholar] [CrossRef]

- Kar, S.K.; Sinha, A.S.; Bansal, R.; Shabani, B.; Harichandan, S. Overview of hydrogen economy in Australia. Wiley Interdiscip. Rev. Energy Environ. 2023, 12, e457. [Google Scholar] [CrossRef]

- AbouSeada, N.; Hatem, T.M. Climate action: Prospects of green hydrogen in Africa. Energy Rep. 2022, 8, 3873–3890. [Google Scholar] [CrossRef]

- Abad, A.V.; Dodds, P.E. Green hydrogen characterisation initiatives: Definitions, standards, guarantees of origin, and challenges. Energy Policy 2020, 138, 111300. [Google Scholar] [CrossRef]

- Chu, K.H.; Lim, J.; Mang, J.S.; Hwang, M.H. Evaluation of strategic directions for supply and demand of green hydrogen in South Korea. Int. J. Hydrogen Energy 2022, 47, 1409–1424. [Google Scholar] [CrossRef]

- Yang, B.; Yu, X.; Hou, J.; Xiang, Z. Secondary reduction strategy synthesis of Pt–Co nanoparticle catalysts towards boosting the activity of proton exchange membrane fuel cells. Particuology 2023, 79, 18–26. [Google Scholar] [CrossRef]

- Falcone, P.M.; Hiete, M.; Sapio, A. Hydrogen economy and sustainable development goals: Review and policy insights. Curr. Opin. Green Sustain. Chem. 2021, 31, 100506. [Google Scholar] [CrossRef]

- Schrotenboer, A.H.; Veenstra, A.A.; uit het Broek, M.A.; Ursavas, E. A Green Hydrogen Energy System: Optimal control strategies for integrated hydrogen storage and power generation with wind energy. Renew. Sustain. Energy Rev. 2022, 168, 112744. [Google Scholar] [CrossRef]

- Longoria, G.; Lynch, M.; Curtis, J. Green hydrogen for heating and its impact on the power system. Int. J. Hydrogen Energy 2021, 46, 26725–26740. [Google Scholar] [CrossRef]

- Sadik-Zada, E.R. Political economy of green hydrogen rollout: A global perspective. Sustainability 2021, 13, 13464. [Google Scholar] [CrossRef]

- Cheng, W.; Lee, S. How green are the national hydrogen strategies? Sustainability 2022, 14, 1930. [Google Scholar] [CrossRef]

- Collera, A.A.; Agaton, C.B. Opportunities for production and utilization of green hydrogen in the Philippines. Int. J. Energy Econ. Policy 2021, 11, 37–41. [Google Scholar] [CrossRef]

- Yu, M.; Wang, K.; Vredenburg, H. Insights into low-carbon hydrogen production methods: Green, blue and aqua hydrogen. Int. J. Hydrogen Energy 2021, 46, 21261–21273. [Google Scholar] [CrossRef]

- Dawood, F.; Anda, M.; Shafiullah, G.M. Hydrogen production for energy: An overview. Int. J. Hydrogen Energy 2020, 45, 3847–3869. [Google Scholar] [CrossRef]

- Mittal, H.; Kushwaha, O.S. Policy Implementation Roadmap, Diverse Perspectives, Challenges, and Solutions Toward Low-Carbon Hydrogen Economy. Green Low-Carbon Econ. 2024, 5, 1846. [Google Scholar] [CrossRef]

- Friedrich, M.; Zittel, W. Green Hydrogen: Energy, Technology, and Policy; Springer: Berlin/Heidelberg, Germany, 2022. [Google Scholar]

- Pingkuo, L.; Junqing, G. Comparative analysis on the development potential of green hydrogen industry in China, the United States, and the European Union. Int. J. Hydrogen Energy 2024, 84, 700–717. [Google Scholar] [CrossRef]

- Hosseini, S.E.; Wahid, M.A. Green hydrogen as a key to sustainable energy systems: A review of technologies and markets. Renew. Sustain. Energy Rev. 2023, 134, 110–119. [Google Scholar]

- Boudellal, M. Power-to-Gas: Renewable Hydrogen Economy for the Energy Transition; Walter de Gruyter GmbH & Co KG: Berlin, Germany, 2023. [Google Scholar]

- Najjar, Y.S. Hydrogen safety: The road toward green technology. Int. J. Hydrogen Energy 2013, 38, 10716–10728. [Google Scholar] [CrossRef]

- Hordvei, E.; Hummelen, S.E.; Petersen, M.; Backe, S.; Crespo del Granado, P. From policy to practice: The cost of Europe’s green hydrogen ambitions. arXiv 2024, arXiv:2406.07149. [Google Scholar] [CrossRef]

- Markus, D.; Smith, J.; Johnson, R.; Lee, H.; Tanaka, M. The Green Hydrogen Economy: A Survey of Market Opportunities and Challenges. Energy Policy 2023, 162, 112341. [Google Scholar]

- Palmer, O.; Thompson, A.; Gupta, R.; Walker, S.; Zhang, L. Long-term investment and energy procurement risk management under uncertainty for an electrolytic green hydrogen producer. Energy Econ. 2024, 45, 1010–1023. [Google Scholar] [CrossRef]

- Parra, D.; Valverde, L.; Pino, F.J.; Patel, M.K. A review on the role, cost and value of hydrogen energy systems for deep decarbonisation. Renew. Sustain. Energy Rev. 2019, 101, 279–294. [Google Scholar] [CrossRef]

- Craiut, L.; Bungau, C.; Bungau, T.; Grava, C.; Otrisal, P.; Radu, A.F. Technology Transfer, Sustainability, and Development, Worldwide and in Romania. Sustainability 2022, 14, 15728. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

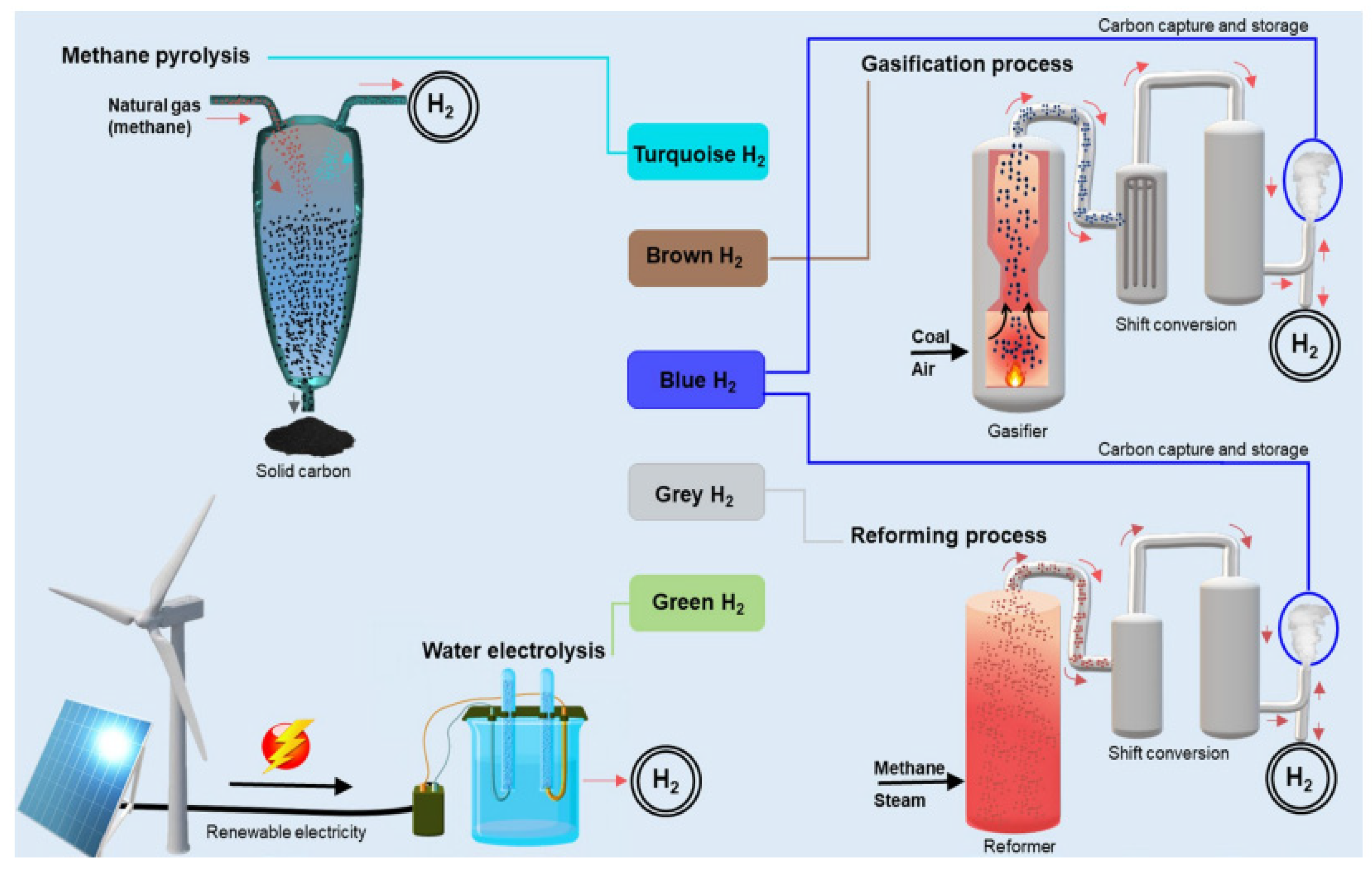

| Hydrogen Type | Production Method | Carbon Emissions | Current Market Share | Ref. |

|---|---|---|---|---|

| Grey hydrogen | Produced through steam methane reforming of natural gas without incorporating carbon capture | High CO2 emissions, as carbon is released into the atmosphere | Accounts for about 95% of global hydrogen production | [13,14] |

| Blue hydrogen | Produced from natural gas through steam methane reforming combined with carbon capture and storage. | Lower CO2 emissions compared to grey hydrogen, but not carbon-neutral | Gaining traction as carbon capture storage technology improves and fossil fuel use persists | [15] |

| Green hydrogen | Produced via electrolysis of water using renewable energy sources (solar, wind, hydropower) | Zero CO2 emissions, making it an eco-friendly option | Currently a small proportion of global hydrogen production, but expanding with renewable energy growth | [13,16] |

| Turquoise hydrogen | Made through methane pyrolysis, where methane is split without oxygen | Low CO2 emissions due to carbon capture as solid carbon black | Still in early research stages, but could expand as a cleaner alternative | [14,15] |

| Brown hydrogen | Produced from coal gasification, usually without carbon capture | Very high CO2 emissions, similar to Grey hydrogen | Represents a small and declining share of hydrogen production due to environmental concerns | [14,15] |

| Country | Net-Zero Target Year |

|---|---|

| Chile | 2050 |

| Colombia | 2050 |

| Costa Rica | 2050 |

| European Union | 2050 |

| United Kingdom | 2050 |

| Canada | 2050 |

| Germany | 2045 |

| Nepal | 2045 |

| Nigeria | 2050–2070 |

| South Korea | 2050 |

| Switzerland | 2050 |

| Thailand | 2065 |

| United States | 2050 |

| Viet Nam | 2050 |

| Argentina | 2050 |

| Australia | 2050 |

| China | 2060 |

| India | 2070 |

| Japan | 2050 |

| Kazakhstan | 2060 |

| New Zealand | 2050 |

| Russian Federation | 2060 |

| Saudi Arabia | 2060 |

| Singapore | 2050 |

| The Gambia | 2050 |

| United Arab Emirates | 2050 |

| Türkiye | 2053 |

| Bhutan | 2050 |

| Brazil | 2050 |

| Ethiopia | 2050 |

| Indonesia | 2060 |

| Morocco | 2030 |

| Peru | 2050 |

| South Africa | 2050 |

| Egypt | No signified target |

| Iran | No signified target |

| Kenya | No signified target |

| Mexico | No signified target |

| Norway | No signified target |

| Philippines | No signified target |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Elegbeleye, I.; Oguntona, O.; Elegbeleye, F. Green Hydrogen: Pathway to Net Zero Green House Gas Emission and Global Climate Change Mitigation. Hydrogen 2025, 6, 29. https://doi.org/10.3390/hydrogen6020029

Elegbeleye I, Oguntona O, Elegbeleye F. Green Hydrogen: Pathway to Net Zero Green House Gas Emission and Global Climate Change Mitigation. Hydrogen. 2025; 6(2):29. https://doi.org/10.3390/hydrogen6020029

Chicago/Turabian StyleElegbeleye, Ife, Olusegun Oguntona, and Femi Elegbeleye. 2025. "Green Hydrogen: Pathway to Net Zero Green House Gas Emission and Global Climate Change Mitigation" Hydrogen 6, no. 2: 29. https://doi.org/10.3390/hydrogen6020029

APA StyleElegbeleye, I., Oguntona, O., & Elegbeleye, F. (2025). Green Hydrogen: Pathway to Net Zero Green House Gas Emission and Global Climate Change Mitigation. Hydrogen, 6(2), 29. https://doi.org/10.3390/hydrogen6020029