Digital Banks in Brazil: Struggling to Reach the Breakeven Point or a New Evolution Wave?

Abstract

:1. Introduction

- Convenience: customers can access banking services anytime and anywhere through their smartphones or computers without having to visit a physical bank branch;

- Lower fees: digital banks often have lower overhead costs compared to traditional banks, allowing them to offer lower fees and better rates on deposits and loans;

- Enhanced security: digital banks often use advanced security measures to protect customer data and prevent fraud, such as two-factor authentication and biometric authentication;

- Personalized services: digital banks can use customer data and artificial intelligence to provide personalized financial advice and tailored banking services.

- Lower costs: digital banks can operate with lower overhead costs than traditional banks, allowing them to offer competitive pricing on products and services;

- Agile operations: digital banks can quickly adapt to changes in the market and customer needs by leveraging technology and data analytics;

- Scalability: digital banks can expand their customer base quickly and efficiently by leveraging digital channels;

- Enhanced customer experience: digital banks can offer a seamless and personalized customer experience by leveraging technology and data analytics.

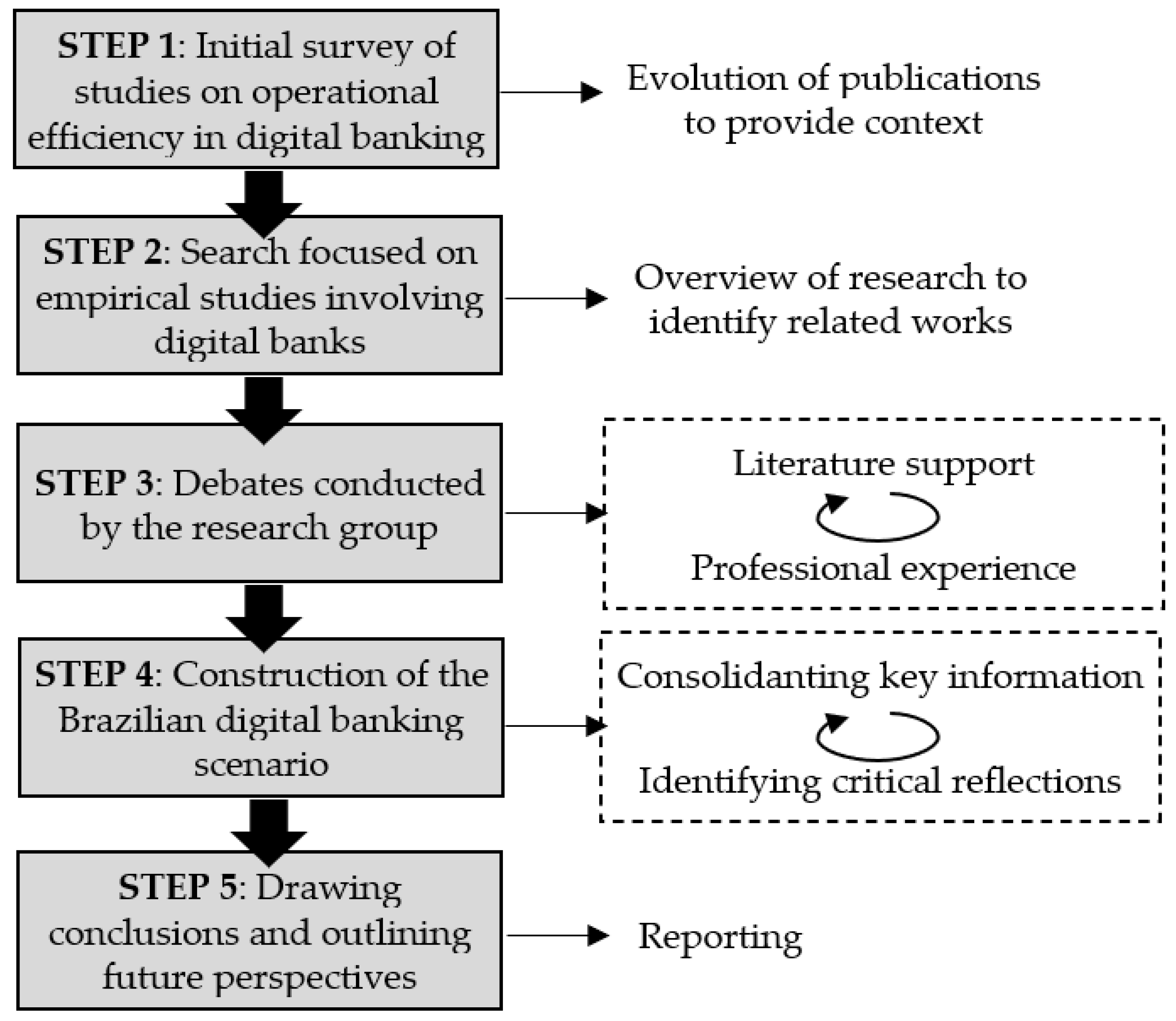

2. Methodological Approach

3. Overview of Research on Digital Banks

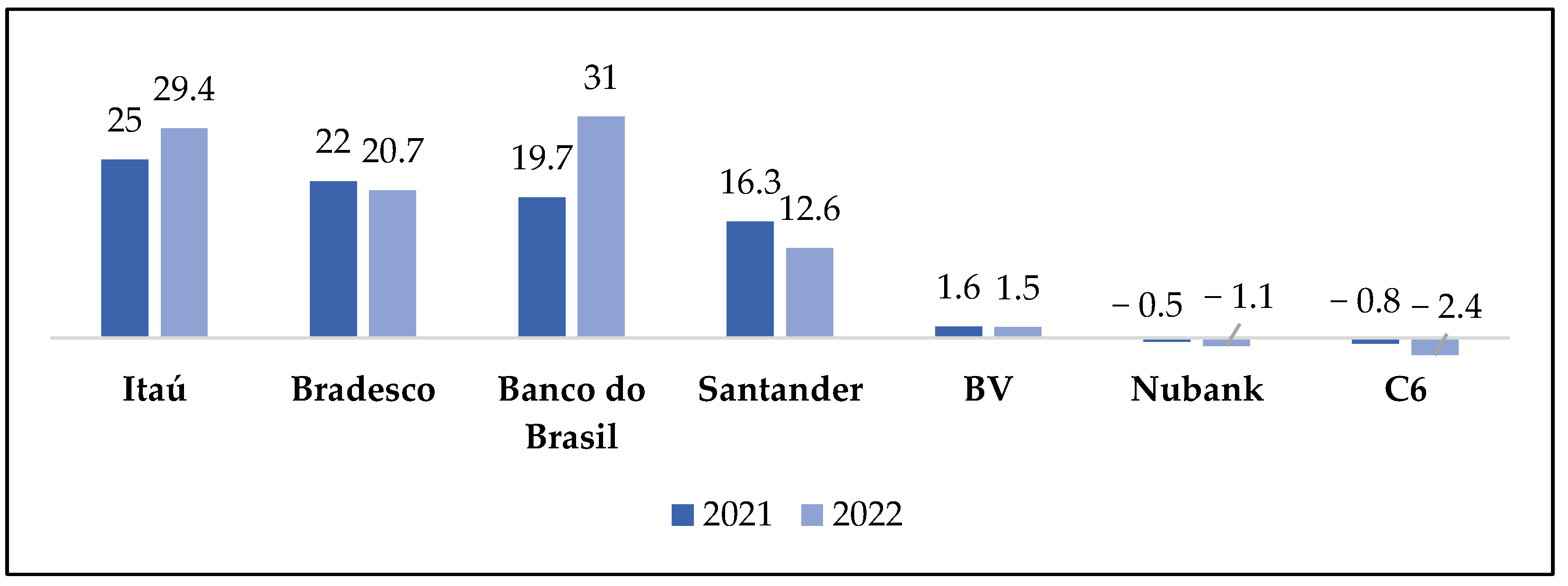

4. Portrait and Reflections on Digital Banks in the Brazilian Scenario

- i

- Customer Acquisition Cost (CAC): Measures how much it costs the digital bank to acquire a new customer. A low CAC indicates that the digital bank is effective at attracting new customers.

- ii

- Customer Retention Rate: Measures the proportion of customers who continue to use the digital bank’s services over time. A high retention rate indicates that customers are satisfied with the services provided by the digital bank.

- iii

- Net Promoter Score (NPS): Measures a customer’s likelihood of recommending the digital bank’s services to others. A high NPS indicates that customers are satisfied with the services provided by the digital bank and are likely to recommend it to others.

- iv

- Average Revenue Per User (ARPU): Measures the average revenue generated by each customer over time. A high ARPU indicates that the digital bank is generating a substantial amount of revenue per customer.

- v

- Cost-to-Income Ratio: Measures the cost efficiency of the digital bank by comparing the operating costs to the revenue generated. A low cost-to-income ratio indicates that the digital bank is effective at generating revenue while incurring few operating expenses.

- vi

- Digital Engagement Metrics: Measures customers’ engagement with the digital bank’s digital channels, such as the mobile app or website. These metrics may involve logins, transactions, and time spent on digital channels.

5. Conclusions and Future Perspectives

- Digital operational efficiency for banks: investigate how operational efficiency can be effectively measured, taking into account the actual impact of digital transformation initiatives and investments on banking operations;

- Digital banks’ attraction to customers: analyze the primary factors that influence customers’ adoption of digital banks and their continued engagement with these institutions;

- Leveraging digital financial services in the retail industry: evaluate the benefits and challenges associated with implementing the new digital business model that integrates financial services with the retail industry.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Kadyan, S.; Bhasin, N.K.; Sharma, M. Fintech: Review of theoretical perspectives and exploring challenges to trust building and retention in improving online digital bank marketing. Transnatl. Mark. J. 2022, 10, 579–592. [Google Scholar] [CrossRef]

- Indriasari, E.; Prabowo, H.; Lumban Gaol, F.; Purwandari, B. Intelligent digital banking technology and architecture. Int. J. Interact. Mob. Technol. 2022, 16, 98–117. [Google Scholar] [CrossRef]

- Aysan, A.F.; Nanaeva, Z. Fintech as a financial disruptor: A bibliometric analysis. FinTech 2022, 1, 412–433. [Google Scholar] [CrossRef]

- Sharma, S.; Sharma, R.; Kayal, G.; Kaur, J. Digital banking: A meta-analysis approach. Indian J. Mark. 2022, 52, 41. [Google Scholar] [CrossRef]

- Moghni, H.; Nassehifar, V.; Nategh, T. Designing model for quality servicesin digital banking. J. Crit. Rev. 2020, 7, 679–690. [Google Scholar] [CrossRef]

- Chauhan, S.; Akhtar, A.; Gupta, A. Customer experience in digital banking: A review and future research directions. Int. J. Qual. Serv. Sci. 2022, 14, 311–348. [Google Scholar] [CrossRef]

- Vincenzo, Y.; Jayadi, R. Important factors that affect customer satisfaction with digital banks in Indonesia. J. Theor. Appl. Inf. Technol. 2023, 101, 1341–1352. [Google Scholar]

- Harb, A.; Thoumy, M.; Yazbeck, M. Customer satisfaction with digital banking channels in times of uncertainty. Banks Bank Syst. 2022, 17, 27–37. [Google Scholar] [CrossRef]

- Meher, B.K.; Hawaldar, I.T.; Mohapatra, L.; Spulbar, C.; Birau, R.; Rebegea, C. The impact of digital banking on the growth of micro, small and medium enterprises (MSMES) in India: A case study. Bus. Theory Pract. 2021, 22, 18–28. [Google Scholar] [CrossRef]

- Lv, S.; Du, Y.; Liu, Y. How do Fintechs impact banks’ profitability?—An empirical study based on banks in China. FinTech 2022, 1, 155–163. [Google Scholar] [CrossRef]

- Yuspin, W.; Wardiono, K.; Nurrahman, A.; Budiono, A. Personal data protection law in digital banking governance in Indonesia. Stud. Iurid. Lub. 2023, 32, 99–130. [Google Scholar] [CrossRef]

- Al-Alawi, A.I.; Al-Khaja, N.A.; Mehrotra, A.A. Women in cybersecurity: A study of the digital banking sector in Bahrain. J. Int. Womens Stud. 2023, 25, 21. [Google Scholar]

- Saif, M.A.M.; Hussin, N.; Husin, M.M.; Alwadain, A.; Chakraborty, A. Determinants of the intention to adopt digital-only banks in Malaysia: The extension of environmental concern. Sustainability 2022, 14, 11043. [Google Scholar] [CrossRef]

- De Carvalho, A.C.P.; Christino, J.; Cardozo, E. Digital bank accounts and digital credit cards: Extending UTAUT2 to FinTech’s services in Brazil. Int. J. Serv. Oper. Manag. 2021, 1, 1. [Google Scholar] [CrossRef]

- Dos Santos, A.A.; Ponchio, M.C. Functional, psychological and emotional barriers and the resistance to the use of digital banking services. Innov. Manag. Rev. 2021, 18, 331–348. [Google Scholar] [CrossRef]

- Karim, Y.; Hasan, R. Taming the digital bandits: An analysis of digital bank heists and a system for detecting fake messages in electronic funds transfer. In National Cyber Summit (NCS) Research Track 2020; Springer: Berlin/Heidelberg, Germany, 2021; pp. 193–210. [Google Scholar]

- Cnaan, R.A.; Scott, M.L.; Heist, H.D.; Moodithaya, M.S. Financial Inclusion in the Digital Banking Age: Lessons from Rural India. J. Soc. Policy 2021, 52, 520–541. [Google Scholar] [CrossRef]

- Guerra-Leal, E.M.; Arredondo-Trapero, F.G.; Vázquez-Parra, J.C. Financial inclusion and digital banking on an emergent economy. Rev. Behav. Financ. 2023, 15, 257–272. [Google Scholar] [CrossRef]

- Syed, A.A.; Kamal, M.A.; Ullah, A.; Grima, S. An Asymmetric analysis of the influence that economic policy uncertainty, institutional quality, and corruption level have on India’s digital banking services and banking stability. Sustainability 2022, 14, 3238. [Google Scholar] [CrossRef]

- Husseini, S.A.; Fam, S.-F. Integrating TQM practices and knowledge management to enhance Malaysian digital banking. Opcion 2019, 35, 2899–2921. [Google Scholar]

- Musyaffi, A.M.; Johari, R.J.; Rosnidah, I.; Respati, D.K.; Wolor, C.W.; Yusuf, M. Understanding digital banking adoption during post-coronavirus pandemic: An integration of technology readiness and technology acceptance model. TEM J. 2022, 11, 683–694. [Google Scholar] [CrossRef]

- Shaikh, I.; Anwar, M. Digital bank transactions and performance of the Indian banking sector. Appl. Econ. 2023, 55, 839–852. [Google Scholar] [CrossRef]

- Kangwa, D.; Mwale, J.T.; Shaikh, J.M. The social production of financial inclusion of generation Z in digital banking ecosystems. Australas. Account. Bus. Financ. J. 2021, 15, 95–118. [Google Scholar] [CrossRef]

- Anholon, R.; Silva, D.; Souza Pinto, J.; Rampasso, I.S.; Domingos, M.L.C.; Dias, J.H.O. COVID-19 and the administrative concepts neglected: Reflections for leaders to enhance organizational development. Kybernetes 2021, 50, 1654–1660. [Google Scholar] [CrossRef]

- Cazeri, G.T.; Anholon, R.; Santa-Eulalia, L.A.; Rampasso, I.S. Potential COVID-19 impacts on the transition to Industry 4.0 in the Brazilian manufacturing sector. Kybernetes 2022, 51, 2233–2239. [Google Scholar] [CrossRef]

- Sigahi, T.F.A.C.; Rampasso, I.S.; Anholon, R.; Sznelwar, L.I. Classical Paradigms versus complexity thinking in engineering education: An essential discussion in the education for sustainable development. Int. J. Sustain. High. Educ. 2023, 24, 179–192. [Google Scholar] [CrossRef]

- Moher, D. Preferred reporting items for systematic reviews and meta-analyses: The PRISMA statement. Ann. Intern. Med. 2009, 151, 264. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Ashenafi, B.B.; Dong, Y. Financial inclusion, fintech, and income inequality in Africa. FinTech 2022, 1, 376–387. [Google Scholar] [CrossRef]

- Hassan, A.; El-Aziz, R.A.B.D.; Hamza, M. The Exclusion of people with visual disabilities from digital banking services in the digitalization era. IBIMA Bus. Rev. 2020, 2020, 1–15. [Google Scholar] [CrossRef]

- Bankuoru Egala, S.; Boateng, D.; Aboagye Mensah, S. To leave or retain? An interplay between quality digital banking services and customer satisfaction. Int. J. Bank Mark. 2021, 39, 1420–1445. [Google Scholar] [CrossRef]

- Ahiabenu, K. A comparative study of the design frameworks of the Ghanaian and Nigerian central banks’ digital currencies (CBDC). FinTech 2022, 1, 235–249. [Google Scholar] [CrossRef]

- Rohatgi, S.; Gera, N.; Nayak, K. Has digital banking usage reshaped economic empowerment of urban women? J. Manag. Gov. 2023, 1–21. [Google Scholar] [CrossRef]

- Bansal, N.; Pareek, N.; Nigam, A. The impact of customer’s training of digital banking services on its acceptability by customers’ in India. Int. J. Bus. Glob. 2022, 30, 207–231. [Google Scholar] [CrossRef]

- Kaur, B.; Kiran, S.; Grima, S.; Rupeika-Apoga, R. Digital banking in Northern India: The risks on customer satisfaction. Risks 2021, 9, 209. [Google Scholar] [CrossRef]

- Ilankumaran, G. Payment system indicators of digital banking ecosystem in India. Int. J. Sci. Technol. Res. 2019, 8, 3397–3400. [Google Scholar]

- Gandasari, R.A.; Mauritsius, T. A study on the effect of gamification components on customer loyalty toward a digital bank. J. Theor. Appl. Inf. Technol. 2023, 101, 2304–2313. [Google Scholar]

- Indriyarti, E.R.; Christian, M.; Yulita, H.; Aryati, T.; Arsjah, R.J. Digital bank channel distribution: Predictors of usage attitudes in Jakarta’s gen Z. J. Distrib. Sci. 2023, 21, 21–34. [Google Scholar] [CrossRef]

- Andrian, B.; Simanungkalit, T.; Budi, I.; Wicaksono, A.F. Sentiment analysis on customer satisfaction of digital banking in Indonesia. Int. J. Adv. Comput. Sci. Appl. 2022, 13, 466–473. [Google Scholar] [CrossRef]

- Amidjaya, P.G.; Widagdo, A.K. Sustainability reporting in Indonesian listed banks. J. Appl. Account. Res. 2019, 21, 231–247. [Google Scholar] [CrossRef]

- Mufarih, M.; Jayadi, R.; Sugandi, Y. Factors influencing customers to use digital banking application in Yogyakarta, Indonesia. J. Asian Financ. Econ. Bus. 2020, 7, 897–908. [Google Scholar] [CrossRef]

- Meliala, J.S.; Sinansari, P. Improving the intensity of sales through digital banking: The case of Indonesian banking behaviour. Pertanika J. Soc. Sci. Humanit. 2020, 28, 359–367. [Google Scholar]

- Unal, I.M.; Aysan, A.F. Fintech, digitalization, and blockchain in Islamic finance: Retrospective investigation. FinTech 2022, 1, 388–398. [Google Scholar] [CrossRef]

- Levy, S. Brand bank attachment to loyalty in digital banking services: Mediated by psychological engagement with service platforms and moderated by platform types. Int. J. Bank Mark. 2022, 40, 679–700. [Google Scholar] [CrossRef]

- Shin, J.W. Mediating effect of satisfaction in the relationship between customer experience and intention to reuse digital banks in Korea. Soc. Behav. Pers. 2021, 49, 1–18. [Google Scholar] [CrossRef]

- Ghani, E.K.; Ali, M.M.; Musa, M.N.R.; Omonov, A.A. The effect of perceived usefulness, reliability, and COVID-19 pandemic on digital banking effectiveness: Analysis using technology acceptance model. Sustainability 2022, 14, 11248. [Google Scholar] [CrossRef]

- Latif, K.A.; Mahmood, N.H.N.; Ali, N.R.M. Exploring sustainable human resource management change in the context of digital banking. J. Environ. Treat. Technol. 2020, 8, 779–786. [Google Scholar]

- Aidonojie, P.A.; Ikubanni, O.O.; Okuonghae, N. The prospects, challenges, and legal issues of digital banking in Nigeria. Cogito 2022, 14, 186–209. [Google Scholar]

- Ananda, S.; Devesh, S.; Al Lawati, A.M. What factors drive the adoption of digital banking? An empirical study from the perspective of omani retail banking. J. Financ. Serv. Mark. 2020, 25, 14–24. [Google Scholar] [CrossRef]

- Shaikh, I.M.; Amin, H.; Noordin, K.; Shaikh, J.M. Islamic bank customers’ adoption of digital banking services: Extending diffusion theory of innovation. J. Islam. Monet. Econ. Financ. 2023, 9, 57–70. [Google Scholar] [CrossRef]

- Martínez-Navalón, J.-G.; Fernández-Fernández, M.; Alberto, F.P. Does Privacy and ease of use influence user trust in digital banking applications in Spain and Portugal? Int. Entrep. Manag. J. 2023, 19, 781–803. [Google Scholar] [CrossRef]

- Larsson, A.; Viitaoja, Y. Building customer loyalty in digital banking: A study of bank staff’s perspectives on the challenges of digital CRM and loyalty. Int. J. Bank Mark. 2017, 35, 858–877. [Google Scholar] [CrossRef]

- Özen, E.; Eren Yıldırım, A. How digital banking affects greenhouse gas emissions in Turkey? An empirical investigation. Stat. Stat. Econ. J. 2023, 103, 101–112. [Google Scholar] [CrossRef]

- Yıldırım, A.C.; Erdil, E. The effect of Covid-19 on digital banking explored under business model approach. Qual. Res. Financ. Mark. 2023; ahead of print. [Google Scholar] [CrossRef]

- Prokopenko, O.; Zholamanova, M.; Mazurenko, V.; Kozlianchenko, O.; Muravskyi, O. Improving customer relations in the banking sector of Ukraine through the development of priority digital banking products and services: Evidence from Poland. Banks Bank Syst. 2022, 17, 12–26. [Google Scholar] [CrossRef]

- Washington, P.B.; Rehman, S.U.; Lee, E. Nexus between regulatory sandbox and performance of digital banks—A study on UK digital banks. J. Risk Financ. Manag. 2022, 15, 610. [Google Scholar] [CrossRef]

- Nguyen, N.T.H.; Kim-Duc, N.; Freiburghaus, T.L. Effect of digital banking-related customer experience on banks’ financial performance during Covid-19: A perspective from Vietnam. J. Asia Bus. Stud. 2022, 16, 200–222. [Google Scholar] [CrossRef]

- Nguyen, T.T.; Nguyen, H.T.; Mai, H.T.; Tran, T.T.M. Determinants of digital banking services in Vietnam: Applying Utaut2 model. Asian Econ. Financ. Rev. 2020, 10, 680–697. [Google Scholar] [CrossRef]

- Nguyen, O.T. Factors affecting the intention to use digital banking in Vietnam. J. Asian Financ. Econ. Bus. 2020, 7, 303–310. [Google Scholar] [CrossRef]

- Nguyen, D.N.; Nguyen, D.D.; Van Nguyen, D. Distribution information safety and factors affecting the intention to use digital banking in Vietnam. J. Distrib. Sci. 2020, 18, 83–91. [Google Scholar] [CrossRef]

- Wadesango, N. The impact of digital banking services on performance of commercial banks. J. Manag. Inf. Decis. Sci. 2020, 23, 343–353. [Google Scholar]

- Aziz, M.R.A.; Jali, M.Z.; Noor, M.N.M.; Sulaiman, S.; Harun, M.S.; Mustafar, M.Z.I. Bibliometric analysis of literatures on digital banking and financial inclusion between 2014–2020. Libr. Philos. Pract. 2021, 2021, 1–31. [Google Scholar]

- C6 Results Report. 2023. Available online: https://www.c6bank.com.br/documentos#relatorio-anual (accessed on 20 June 2023).

- Itaú Results Report. 2023. Available online: https://www.itau.com.br/relacoes-com-investidores/resultados-e-relatorios/central-de-resultados/ (accessed on 20 June 2023).

- Bradesco Results Report. 2023. Available online: https://www.bradescori.com.br/informacoes-ao-mercado/central-de-resultados/ (accessed on 20 June 2023).

- Banco do Brasil Results Report. 2023. Available online: https://ri.bb.com.br/informacoes-financeiras/central-de-resultados/ (accessed on 20 June 2023).

- Santander Results Report. 2023. Available online: https://www.santander.com.br/ri/relatorios (accessed on 20 June 2023).

- BV Results Report. 2023. Available online: https://ri.bv.com.br/informacoes-aos-investidores/central-de-resultados/ (accessed on 20 June 2023).

- Nubank Results Report. 2023. Available online: https://www.investidores.nu/financas/central-de-resultados/ (accessed on 20 June 2023).

- Del Vecchio, P.; Secundo, G.; Garzoni, A. Phygital Technologies and environments for breakthrough innovation in customers’ and citizens’ journey. A critical literature review and future agenda. Technol. Forecast. Soc. Change 2023, 189, 122342. [Google Scholar] [CrossRef]

- Santosh, K. Phygital banking—A game changer in Indian banking sector. Int. J. Innov. Technol. Explor. Eng. 2019, 8, 289–292. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Selection Process | Action | Documents |

|---|---|---|

| Initial search | Search for documents with “digital bank*” in the title | 171 |

| Filter 1 | Applying databases filter (document type): only articles and reviews | 95 |

| Filter 2 | Applying databases filter (language): only English | 95 |

| Filter 3 | Reading title, abstracts, and keywords to assess suitability for the study’s scope | 88 |

| Filter 4 | Reading methods and results section to search for empirical evidence | 66 |

| Final sample | Reading full text to map the research topic, sampla, and context | 46 |

| Research Topic | Sample/Data | Context | Reference |

|---|---|---|---|

| Impact of financial inclusion and fintechs on income inequality | Data from 39 African countries | Africa | [28] |

| Gender perspective of cybersecurity in the digital banking sector | 50 participants from cybersecurity, engineering, and top management in banks | Bahrain | [12] |

| Resistance to the use of digital banking services | 202 customers | Brazil | [15] |

| Impact of fintechs on banks’ profitability | Industrial and Commercial Bank of China (the most representative bank in China, according to the authors) | China | [10] |

| Exclusion of people with visual disabilities from digital banking services | Not informed | Egypt | [29] |

| Influence of economic policy uncertainty, institutional quality, and corruption level on the growth of digital financial services | N/A | General | [19] |

| Impact of quality digital banking services delivered during the COVID-19 pandemic on customers’ satisfaction and retention intentions | 395 responses | Ghana | [30] |

| Central bank digital currency | CBDC design documents | Ghana and Nigeria | [31] |

| Impact of digital banking usage on women’s economic empowerment | 286 women | India | [32] |

| Impact of digital bank transactions on the performance of banks | 32 public and private banks | India | [22] |

| Impact of customer’s training of digital banking services on its acceptability by customers | 402 training schedules | India | [33] |

| Intensity of the risk factors that influence customer satisfaction for digitalized banking services and products | 222 customers | India | [34] |

| Financial inclusion in the digital banking age | 3159 participants from rural villages | India | [17] |

| Impact of digital banking on the growth of micro, small, and medium enterprises | 454 companies | India | [9] |

| Payment system indicators of digital banking ecosystem | N/A | India | [35] |

| Gamification implementation for digital banks | 158 users | Indonesia | [36] |

| Factors influencing customer satisfaction in digital banks | 408 respondents | Indonesia | [7] |

| Personal data protection in the context of digital banks | N/A | Indonesia | [11] |

| Predictors of usage attitudes related to digital bank channel distribution | 616 university students | Indonesia | [37] |

| Sentiment analysis on customer satisfaction of digital banking | 34,605 tweets related to three digital banks | Indonesia | [38] |

| Relationship between digital banking and intention to produce sustainability report | 155 observations | Indonesia | [39] |

| Factors influencing customers to use digital banking application | 300 respondents | Indonesia | [40] |

| Intensity of sales through digital banking | 78 banks | Indonesia | [41] |

| Technology readiness and technology acceptance in digital banking | 422 respondents from the millenial generation | Indonesia/Malaysia | [21] |

| Banks’ digitalization, blockchain, and crypto assets | 100 articles | Islamic banks | [42] |

| Customer emotional experience generated during digital banking service delivery | 502 participants | Israel | [43] |

| Customer experience of digital banking | 247 digital bank users | Korea | [44] |

| Effect of perceived usefulness, banking system reliability, and COVID-19 pandemic on the digital banking effectiveness | 228 clients | Malaysia | [45] |

| Sustainable human resource management change in the context of digital banking | 4 business leaders, 7 human resources professionals, and 3 high potential talents | Malaysia | [46] |

| Integrating Total Quality Management practices and knowledge management in digital banks | 100 employees the executive management team level | Malaysia | [20] |

| Financial inclusion through digital banking | 12,446 households | Mexico | [18] |

| Legal issues concerning digital banking | 306 respondents | Nigeria | [47] |

| Factors influencing the adoption of digital banking by retail banking customers | 200 customers | Omani | [48] |

| Factors that drive non-users of digital banking services | 208 customers | Pakistan | [49] |

| Impact of privacy, ease of use, and trust in digital banking | 320 participants | Portugal and Spain | [50] |

| Customer loyalty in digital banking | 10 bank managers | Sweden | [51] |

| Impact of digital banking on greenhouse gas emissions | 36 banks | Turkey | [52] |

| Impacts of COVID-19 on the progression of digitalization of banks | 4 vice presidents and 3 digital bank managers | Turkey | [53] |

| Improvement in the relations with clients in the banking sector | 50 respondents from Ukraine and 50 respondents from Poland | Ukraine and Poland | [54] |

| Digital banks’ adoption of a regulatory sandbox to foster innovation in financial sectors | 24 challenger banks | United Kingdom | [55] |

| Effect of digital banking-related customer experience on banks’ financial performance during COVID-19 | 456 customers of 20 Vietnamese commercial banks | Vietnam | [56] |

| Determinants of consumers’ behavioral intention to adopt or use digital banking | 241 participants | Vietnam | [57] |

| Factors affecting the intention to use digital banking | 201 customers | Vietnam | [58] |

| Information safety and factors affecting the intention to use digital banking | 329 customers | Vietnam | [59] |

| Effect of digital banking on financial performance of commercial banks | Not informed | Zimbabwe | [60] |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bueno, L.A.; Sigahi, T.F.A.C.; Anholon, R. Digital Banks in Brazil: Struggling to Reach the Breakeven Point or a New Evolution Wave? FinTech 2023, 2, 374-387. https://doi.org/10.3390/fintech2030021

Bueno LA, Sigahi TFAC, Anholon R. Digital Banks in Brazil: Struggling to Reach the Breakeven Point or a New Evolution Wave? FinTech. 2023; 2(3):374-387. https://doi.org/10.3390/fintech2030021

Chicago/Turabian StyleBueno, Luiz Antonio, Tiago F. A. C. Sigahi, and Rosley Anholon. 2023. "Digital Banks in Brazil: Struggling to Reach the Breakeven Point or a New Evolution Wave?" FinTech 2, no. 3: 374-387. https://doi.org/10.3390/fintech2030021