Financial Risk Disclosure and Financial Attributes among Publicly Traded Manufacturing Companies: Evidence from Bangladesh

Abstract

:1. Introduction

2. Legal Framework for Risk Disclosure in Bangladesh

3. Literature Review

4. Theoretical Framework

5. Hypothesis Development

5.1. Firm Size and Level of Financial Risk Disclosure

5.2. Firm Performance and Level of Financial Risk Disclosure

5.3. Corporate Financial Leverage and Level of Financial Risk Disclosure

5.4. Liquidity and Level of Financial Risk Disclosure

5.5. Industry Type and Level of Financial Risk Disclosure

5.6. Auditor Type and Level of Financial Risk Disclosure

6. Methodology

6.1. Sample

6.2. Method of Analysis

6.3. Financial Risk Category Selection

6.4. Item Selection for Financial Risk Description

6.5. Financial Risk Disclosure Index

6.6. Measurement of Variables

6.7. Model Development

7. Results and Discussion

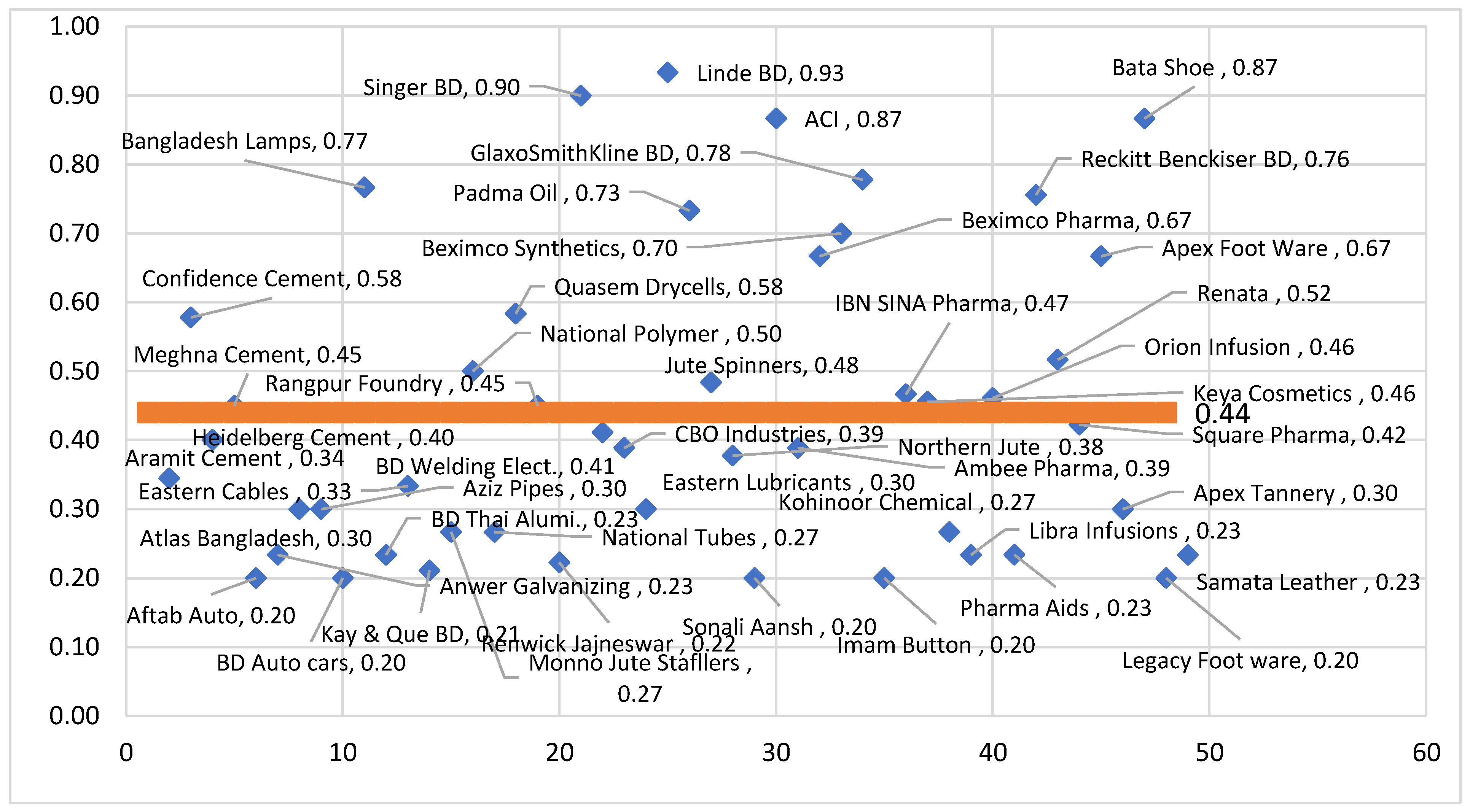

7.1. Aggregated Disclosure Index of Financial Risks

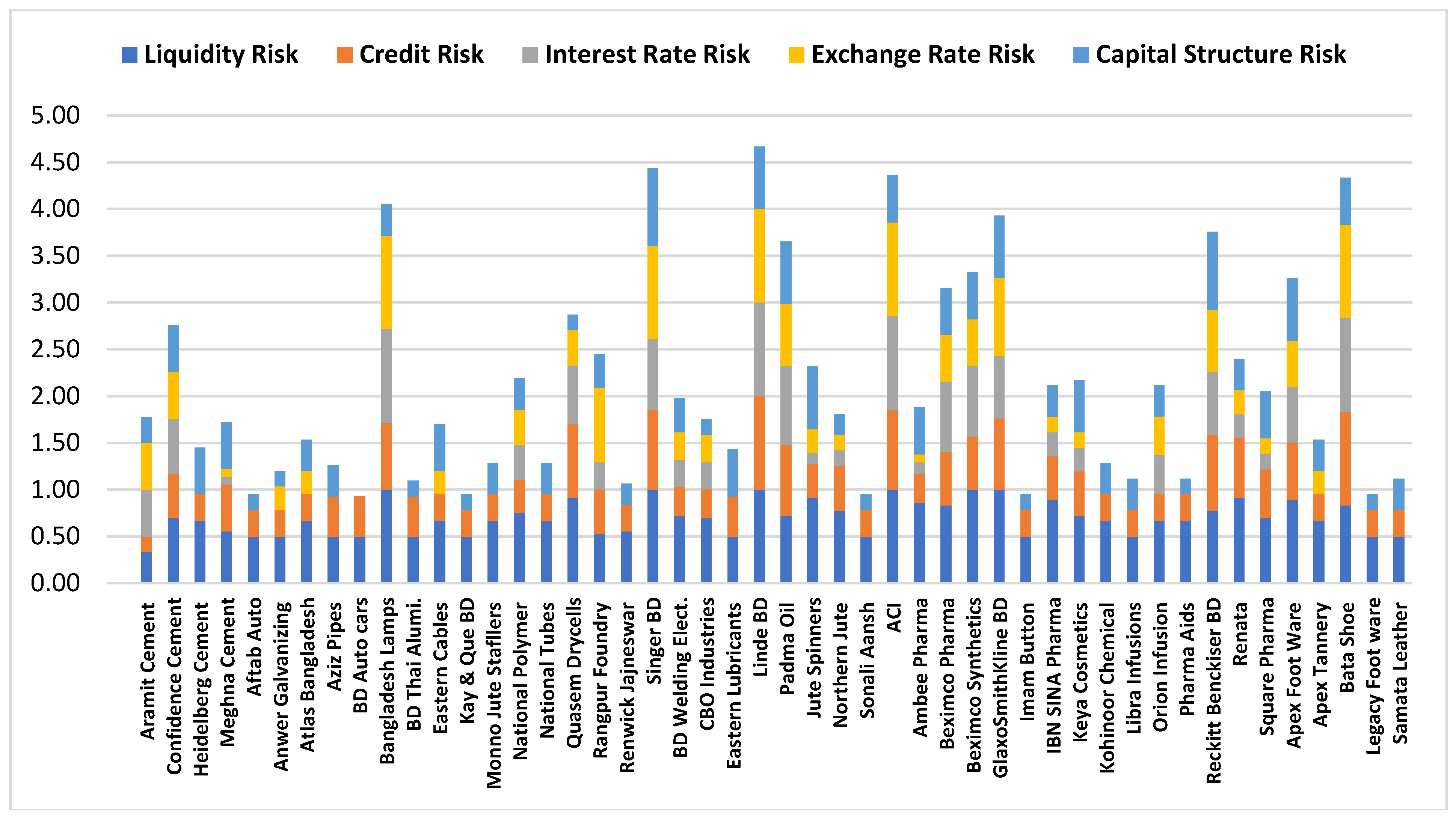

7.2. Specific Disclosure Indices of Financial Risks: Analysis of Level

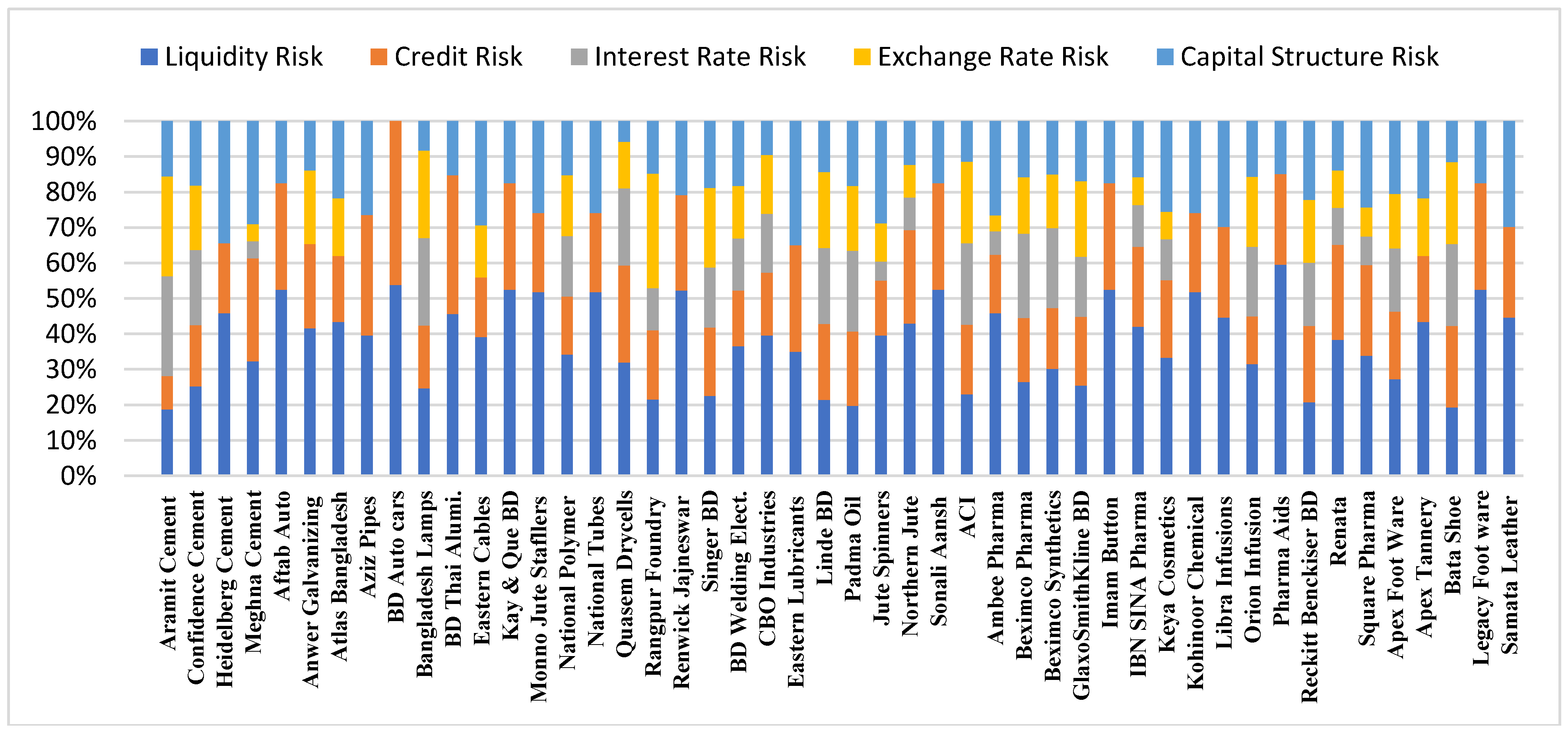

7.3. Specific Disclosure Indices of Financial Risks: Analysis of Composition

7.4. Univariate Analysis

7.5. Multivariate Analysis

8. Conclusions and Limitations

Author Contributions

Funding

Conflicts of Interest

References

- Abraham, Santhosh, and Paul Cox. 2007. Analyzing the determinants of narrative risk information in UK FTSE 100 annual reports. British Accounting Review 39: 227–48. [Google Scholar] [CrossRef]

- Akhtaruddin, Md. 2005. Corporate mandatory disclosure practices in Bangladesh. International Journal Accounting 40: 399–422. [Google Scholar] [CrossRef]

- Akhtaruddin, Mohamed, and Mahmud Hossain. 2008. Investment opportunity set, ownership control and voluntary disclosures in Malaysia. JOAAG 3: 25–39. [Google Scholar]

- Aliabadi, Sara, Alireza Dorestani, and Zabihollah Rezaee. 2013. Integration of Enterprise Risk management into Corporate Governance. International Journal of Management Accounting Research 3: 31–46. [Google Scholar]

- Al-Mulhem, Adnan Abdullah. 1997. An Empirical Investigation of the Level of Financial Disclosure by Saudi Arabian Corporations. Doctoral dissertation, University of Hull, Hull, UK. [Google Scholar]

- Alsaeed, Khalid. 2006. The association between firm-specific characteristics and disclosure: The case of Saudi Arabia. Managerial Auditing Journal 21: 476–96. [Google Scholar] [CrossRef]

- Amran, Azlan, and Roszaini Haniffa. 2011. Evidence in development of sustainability reporting: A case of a developing country. Business Strategy and the Environment 3: 141–56. [Google Scholar] [CrossRef]

- Amran, Azlan, Abdul Manaf Rosli Bin, and Bin Che Haat Mohd Hassan. 2008. Risk reporting: An exploratory study on risk management disclosure in Malaysian annual reports. Managerial Auditing Journal 24: 39–57. [Google Scholar] [CrossRef]

- Barako, Dulacha G., Phil Hancock, and H. Y. Izan. 2006. Factors influencing voluntary corporate disclosure by Kenyan companies. Corporate Governance: An International Review 14: 107–25. [Google Scholar] [CrossRef]

- Beasley, Mark, Don Pagach, and Richard Warr. 2008. Information conveyed in hiring announcement of senior executives overseeing enterprise-wide risk management process. Journal of Accounting, Auditing and Finance 23: 311–32. [Google Scholar] [CrossRef]

- Beretta, Sergio, and Saverio Bozzolan. 2004. A framework for the analysis of firm risk communication. The International Journal of Accounting 39: 265–88. [Google Scholar] [CrossRef]

- Brammer, Stephen, and Stephen Pavelin. 2008. Factors influencing the quality of corporate environmental disclosure. Business Strategy and the Environment 17: 120–36. [Google Scholar] [CrossRef]

- Bujaki, Merridee, and Bruce J. McConomy. 2002. Corporate governance: Factors influencing voluntary disclosure by publicly traded Canadian firms. Accounting Perspectives 1: 105–39. [Google Scholar] [CrossRef]

- Chalmers, Keryn, and Jayne M. Godfrey. 2004. Reputation costs: The impetus for voluntary derivative financial instrument reporting. Accounting Organizations and Society 29: 95–125. [Google Scholar] [CrossRef]

- Connelly, Brian L., S. Trevis Certo, R. Duane Ireland, and Christopher R. Reutzel. 2011. Signaling theory: A review and assessment. Journal of Management 37: 39–67. [Google Scholar] [CrossRef]

- Core, John E. 2001. A review of the empirical disclosure literature: Discussion. Journal of Accounting and Economics 31: 441–56. [Google Scholar] [CrossRef]

- Das, Sumon, Rob Dixon, and Amir Michael. 2015. Corporate mandatory reporting: A longitudinal investigation of listed companies in Bangladesh. Global Review of Accounting and Finance 6: 64–85. [Google Scholar] [CrossRef]

- Deumes, Rogier, and W. Robert Knechel. 2008. Economic incentives for voluntary reporting on internal risk management and control systems. Auditing: A Journal of Practice & Theory 27: 35–66. [Google Scholar]

- Dobler, Michael. 2005. National and international developments in risk reporting: May the German Accounting Standard 5 lead the way internationally. German Law Journal 6: 1191–200. [Google Scholar]

- (DOF) Dodd–Frank Wall Street Reform and Consumer Protection Act. 2010. 111th Congress Public Law 203; Washington, DC: Government Printing Office. Available online: http://www.gpo.gov/fdsys/pkg/PLAW-111publ203/html/PLAW-111publ203.htm (accessed on 16 June 2018).

- Ferguson, Michael J., Kevin C. K. Lam, and Grace Meina Lee. 2002. Voluntary disclosure by state-owned enterprises listed on the stock exchange of Hong Kong. Journal of International Financial Management & Accounting 13: 125–52. [Google Scholar]

- Financial Reporting Act (FRA). 2015. The Bangladesh National Parliament. Available online: http://www.icmab.org.bd/images/stories/journal/2015/Nov-Dec/6.Opinions%20%20Comments.pdf (accessed on 16 June 2018).

- Haniffa, Ros M., and Terry E. Cooke. 2002. Culture, corporate governance and disclosure in Malaysian corporations. Abacus 38: 317–49. [Google Scholar] [CrossRef]

- Hasan, Tanweer, Waresul Karim, and Shakil Quayes. 2008. Regulatory change and the quality of compliance to mandatory disclosure requirements: Evidence from Bangladesh. Research in Accounting Regulation 20: 193–203. [Google Scholar] [CrossRef]

- Hasan, Md. Shamimul, Syed Zabid Hossain, and Robert J. Swieringa. 2013. Corporate governance and financial disclosures: Bangladesh perspective. Corporate Governance 4: 109–19. [Google Scholar]

- Healy, Paul M., and Krishna G. Palepu. 2001. Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. Journal of Accounting and Economics 31: 405–40. [Google Scholar] [CrossRef]

- Hossain, Mohammed, and Peter J. Taylor. 2007. The empirical evidence of the voluntary information disclosure in the annual reports of banking companies: The case of Bangladesh. Corporate Ownership and Control 4: 111–25. [Google Scholar] [CrossRef]

- Inchausti, Begoña Giner. 1997. The influence of company characteristics and accounting regulation on information disclosed by Spanish firms. European Accounting Review 6: 45–68. [Google Scholar] [CrossRef]

- Kabir, M. Humayun, Divesh Sharma, Md Ainul Islam, and Amirus Salat. 2011. Big 4 auditor affiliation and accruals quality in Bangladesh. Managerial Auditing Journal 26: 161–81. [Google Scholar] [CrossRef]

- Kamal Hassan, Mostafa. 2009. UAE corporations-specific characteristics and level of risk disclosure. Managerial Auditing Journal 24: 668–87. [Google Scholar] [CrossRef]

- Khlifi, Foued, and Abdelfettah Bouri. 2010. Corporate Disclosure and Firm Characteristics: A Puzzling Relationship. Journal of Accounting, Business & Management 17: 62–89. [Google Scholar]

- Konishi, Noriyuki, and Md Mohobbot Ali. 2007. Risk reporting of Japanese companies and its association with corporate characteristics. International Journal of Accounting, Auditing and Performance Evaluation 4: 263–85. [Google Scholar] [CrossRef]

- Lajili, Kaouthar, and Daniel Zéghal. 2005. A content analysis of risk management disclosures in Canada annual reports. Canada Journal of Administrative Science 22: 125–42. [Google Scholar] [CrossRef]

- Linsley, Philip M., and Michael J. Lawrence. 2007. Risk reporting by the largest UK companies: Readability and lack of obfuscation. Accounting, Auditing & Accountability Journal 20: 620–27. [Google Scholar]

- Linsley, Philip M., and Philip J. Shrives. 2006. Risk reporting: A study of risk disclosures in the annual reports of UK companies. The British Accounting Review 38: 387–404. [Google Scholar] [CrossRef]

- Lombardi, Rosa, Daniela Coluccia, Giuseppe Russo, and Silvia Solimene. 2016. Exploring financial risks from corporate disclosure: Evidence from Italian listed companies. Journal of the Knowledge Economy 7: 309–27. [Google Scholar] [CrossRef]

- Lopes, Patrícia Teixeira, and Lúcia Lima Rodrigues. 2007. Accounting for financial instruments: An analysis of the determinants of disclosure in the Portuguese stock exchange. The International Journal of Accounting 42: 25–56. [Google Scholar] [CrossRef]

- Magness, Vanessa. 2006. Strategic posture, financial performance and environmental disclosure: An empirical test of legitimacy theory. Accounting, Auditing & Accountability Journal 19: 540–63. [Google Scholar]

- Miihkinen, Antti. 2010. What drives quality of firm risk disclosure? The impact of a national disclosure standard and reporting incentives under IFRS. The International Journal of Accounting 47: 437–68. [Google Scholar] [CrossRef]

- Milne, Markus J. 2002. Positive accounting theory, political costs and social disclosure analyses: A critical look. Critical Perspectives on Accounting 13: 369–95. [Google Scholar] [CrossRef]

- Nandi, Sunil, and Santanu Kumar Ghosh. 2013. Corporate governance attributes, firm characteristics and the level of corporate disclosure: Evidence from the Indian listed firms. Decision Science Letters 2: 45–58. [Google Scholar] [CrossRef] [Green Version]

- Naser, Kamal, Khalid Al-Khatib, and Yusuf Karbhari. 2002. Empirical evidence on the depth of corporate information disclosure in developing countries: The case of Jordan. International Journal of Commerce and Management 12: 122–55. [Google Scholar] [CrossRef]

- Ng, Anthony C., and Zabihollah Rezaee. 2015. Business sustainability performance and cost of equity capital. Journal of Corporate Finance 34: 128–49. [Google Scholar] [CrossRef]

- Oliveira, Jonas, Lúcia Lima Rodrigues, and Russell Craig. 2011a. Risk-related disclosures by non-finance companies: Portuguese practices and disclosure characteristics. Managerial Auditing Journal 26: 817–39. [Google Scholar] [CrossRef] [Green Version]

- Oliveira, Jonas, Lúcia Lima Rodrigues, and Russell Craig. 2011b. Voluntary risk reporting to enhance institutional and organizational legitimacy: Evidence from Portuguese banks. Journal of Financial Regulation and Compliance 19: 271–89. [Google Scholar] [CrossRef] [Green Version]

- Pagach, Donald, and Richard Warr. 2007. An Empirical Investigation of the Characteristics of Firms Adopting Enterprise Risk Management. Working Paper, College of Management, North Carolina State University, Raleigh, NC, USA. [Google Scholar]

- Poskitt, Russell. 2005. Disclosure regulation and information risk. Accounting and Finance 45: 457–77. [Google Scholar] [CrossRef]

- Reverte, Carmelo. 2009. Determinants of corporate social responsibility disclosure ratings by Spanish listed firms. Journal of Business Ethics 88: 351–66. [Google Scholar] [CrossRef]

- Rezaee, Zabihollah. 2016. Business sustainability research: A theoretical and integrated perspective. Journal of Accounting Literature 36: 48–64. [Google Scholar] [CrossRef]

- Schuster, Peter, and Vincent O’Connell. 2006. The trend toward voluntary corporate disclosures. Management Accounting Quarterly 7: 1–9. [Google Scholar]

- Verrecchia, Robert E. 1983. Discretionary disclosure. Journal of Accounting and Economics 5: 179–94. [Google Scholar] [CrossRef]

- Wallace, R. S. Olusegun, and Kamal Naser. 1995. Firm-specific determinants of the comprehensiveness of mandatory disclosure in the corporate annual reports of firms listed on the stock exchange of Hong Kong. Journal of Accounting and Public Policy 14: 311–68. [Google Scholar] [CrossRef]

- Wang, Kun, O. Sewon, and M. Cathy Claiborne. 2008. Determinants and consequences of voluntary disclosure in an emerging market: Evidence from China. Journal of International Accounting, Auditing and Taxation 17: 14–30. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Category of FR | No. | Disclosure Identifier |

|---|---|---|

| Liquidity Risk | 1 | Definition or motivation |

| 2 | Classification of debts by type and maturity | |

| 3 | Comparison with previous years | |

| 4 | Quantitative data on available cash or cash equivalents | |

| 5 | Company’s approach toward managing liquidity | |

| 6 | Current ratio and quick ratio | |

| Credit Risk | 1 | Definition or motivation |

| 2 | Quantitative or qualitative data on exposure to credit risk | |

| 3 | Classification of customers’ obligations in terms of their creditworthiness (rating) | |

| 4 | Aging schedule of accounts receivable | |

| 5 | Comparison with previous years | |

| 6 | Alternative credit classification (by activity, geographical area, others) | |

| 7 | Notes on the concentration of credit | |

| Interest Rate Risk | 1 | Definition or motivation |

| 2 | Classification of debt by interest rate (fixed/variable) | |

| 3 | Sensitivity analysis | |

| 4 | Information on derivative hedging instruments | |

| Currency Risk | 1 | Definition or motivation |

| 2 | Detail of items in foreign currencies | |

| 3 | Comparison with previous years | |

| 4 | Sensitivity analysis | |

| Capital Structure Risk | 1 | Company’s ability to continue as a going concern |

| 2 | Leverage ratios | |

| 3 | Capital expenditure forecast (quantitative and qualitative) | |

| 4 | Forecast of growth capacity (both qualitative and quantitative) | |

| 5 | Capital expenditure commitment | |

| 6 | Long term credit rating | |

| General | 1 | Financial risk management policy |

| 2 | Information on responsibility for establishment and oversight of the risk management framework | |

| 3 | Review of risk management policies, procedures and systems To reflect changes in market conditions and the company’s activities |

| Name of Variables | Type of Variables | Proxies | Acronyms | Measurement |

|---|---|---|---|---|

| Financial Risk Disclosure | Dependent | Financial Risk Disclosure Index | FRDI | Ratio of score obtained by a company and maximum possible score |

| Firm Specific Characteristics | Independent | Firm Size | FS | Logarithm of Total Assets |

| Financial Performance | ROA | EBIT/Total Assets | ||

| Corporate Financial leverage | FL | Total Liabilities/Total Assets | ||

| Liquidity | LIQD | Current Assets/Current Liabilities | ||

| Industry Type (Dummy) | IT | 1 or 0 | ||

| Auditor Type (Dummy) | AT | 1 or 0 |

| Variables | FRDI | DR | ROA | FS | LIQD | AT | CEM | ENG | FP | Jute | PC | TAN |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| FRDI | 1 | |||||||||||

| DR | −0.07 | 1 | ||||||||||

| ROA | 0.38 ** | −0.28 ** | 1 | |||||||||

| FS | 0.52 ** | −0.29 ** | 0.25 ** | 1 | ||||||||

| LIQD | 0.07 | −0.51 ** | 0.22 ** | 0.19 ** | 1 | |||||||

| AT | 0.65 ** | −0.001 | 0.47 ** | 0.49 ** | 0.09 | 1 | ||||||

| CEM | 0.000 | 0.024 | 0.07 | 0.19 ** | −0.07 | 0.03 | 1 | |||||

| ENG | −0.21 ** | 0.01 | −0.12 * | −0.23 ** | 0.12 * | −0.25 ** | −0.21 ** | 1 | ||||

| FP | 0.16 ** | −0.02 | 0.06 | 0.06 | −0.03 | 0.16 ** | −0.10 | −0.24 ** | 1 | |||

| Jute | −0.07 | 0.20 ** | −0.10 | 0.03 | −0.20 ** | −0.07 | 0.73 ** | −0.29 ** | −0.14 * | 1 | ||

| PC | 0.14 * | −0.09 | 0.18 ** | 0.28 ** | −0.17 ** | 0.11 | 0.37 ** | −0.57 ** | −0.28 ** | 0.15 * | 1 | |

| TAN | 0.01 | −0.03 | 0.07 | 0.13 * | 0.18 ** | 0.15 * | 0.63 ** | −0.34 ** | −0.16 ** | 0.41 ** | 0.05 | 1 |

| Model | Unstandardized Coefficients | Standardized Coefficients | t-Value | Sig. | |

|---|---|---|---|---|---|

| B | Std. Error | Beta | |||

| Constant | 0.036 | 0.076 | 0.478 | 0.633 | |

| Firm Size | 0.042 | 0.008 | 0.290 | 5.241 *** | 0.000 |

| Financial performance | 0.306 | 0.138 | 0.116 | 2.212 ** | 0.028 |

| Financial Leverage | 0.030 | 0.046 | 0.036 | 0.651 | 0.516 |

| Liquidity | −0.003 | 0.012 | −0.013 | −0.233 | 0.816 |

| Cement Industrial Sector | −0.073 | 0.076 | −0.085 | −0.969 | 0.333 |

| Fuel and Power Industrial Sector | 0.049 | 0.038 | 0.063 | 1.298 * | 0.195 |

| Jute Industrial Sector | 0.030 | 0.046 | 0.045 | 0.656 | 0.513 |

| Pharmaceuticals and Chemical Industrial Sector | 0.016 | 0.027 | 0.033 | 0.596 | 0.552 |

| Tannery Industrial Sector | −0.033 | 0.038 | −0.054 | −0.855 | 0.393 |

| Type of Audit Firm | 0.263 | 0.035 | 0.449 | 7.590 *** | 0.000 |

| Adj. R2 | 0.473 | ||||

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Dey, R.K.; Hossain, S.Z.; Rezaee, Z. Financial Risk Disclosure and Financial Attributes among Publicly Traded Manufacturing Companies: Evidence from Bangladesh. J. Risk Financial Manag. 2018, 11, 50. https://doi.org/10.3390/jrfm11030050

Dey RK, Hossain SZ, Rezaee Z. Financial Risk Disclosure and Financial Attributes among Publicly Traded Manufacturing Companies: Evidence from Bangladesh. Journal of Risk and Financial Management. 2018; 11(3):50. https://doi.org/10.3390/jrfm11030050

Chicago/Turabian StyleDey, Ripon Kumar, Syed Zabid Hossain, and Zabihollah Rezaee. 2018. "Financial Risk Disclosure and Financial Attributes among Publicly Traded Manufacturing Companies: Evidence from Bangladesh" Journal of Risk and Financial Management 11, no. 3: 50. https://doi.org/10.3390/jrfm11030050