A Survey on Empirical Findings about Spillovers in Cryptocurrency Markets

Laboratory of Economic Policy and Strategic Planning, Department of Economics, University of Thessaly, 28th October 78 Street, P.C. 38333 Volos, Greece

J. Risk Financial Manag. 2019, 12(4), 170; https://doi.org/10.3390/jrfm12040170

Submission received: 14 October 2019

/

Revised: 9 November 2019

/

Accepted: 11 November 2019

/

Published: 12 November 2019

(This article belongs to the Special Issue Recent Developments in Cryptocurrency Markets: Co-movements, Spillovers and Forecasting)

Abstract

:This paper provides a systematic survey on return and volatility spillovers of cryptocurrencies based on the empirical results of relevant academic literature. Evidence reveals that Bitcoin is the most influential among digital coins mainly as a transmitter toward digital currencies but also as a receiver of spillovers from virtual currencies and alternative assets. Ethereum, Litecoin, and Ripple present the most significant interlinkages with Bitcoin. Return spillovers are more pronounced but volatility spillovers often present a bi-directional character. Volatility shock transmission is detected among Bitcoin and national currencies, while economic policy uncertainty is not influential. This survey provides useful guidance in the hotly-debated issue of reform and decentralization of financial systems.

1. Introduction

With the emergence of a large number of cryptocurrencies since the bull market of 2017, a heated debate has ensued over whether Bitcoin could preserve its leading role in the markets of digital coins. Studying transactions by virtual currencies considerably enriches academic work on monetary economics and provides useful feedback for policymakers, academics, investors, and the economic press. More specifically, the examination of interconnection and spillovers among these innovative forms of liquidity epitomizes a critical facet of international finance and generates fundamental ramifications for trading.

A number of important academic research contributions have taken place regarding cryptocurrencies. Earlier papers have been focusing on the characteristics (Selgin 2015; Böhme et al. 2015; Ammous 2018), volatility measurement (Katsiampa 2017, 2019a, 2019b; Chaim and Laurini 2018; Beneki et al. 2019; Kyriazis et al. 2019), and inefficiency in the markets of digital coins (Urquhart 2016; Nadarajah and Chu 2017; Bariviera 2017). Another strand of papers have centered their interest on speculation and hedging properties in virtual currency markets (Dyhrberg 2016; Bouri et al. 2017; Fang et al. 2019) while others investigate liquidity characteristics of cryptocurrencies (Wei 2018; Kyriazis and Prassa 2019). Extant empirical testing generally tends to focus on high-capitalization cryptocurrencies in order to ascertain whether coins such as Ethereum, Ripple, Litecoin, or Stellar could substitute Bitcoin regarding investors’ preferences in a noteworthy extent. Moreover, two integrated surveys have been conducted that provide the overall views of digital currency characteristics (Corbet et al. 2019; Kyriazis 2019).

The exceptionally high levels of volatility embedded in cryptocurrencies have brought to the forth an ongoing discussion related to the possibility of creation of stablecoins, that is coins tied to well-established assets such as the US dollar and whether they could replace Bitcoin in international transactions. The Facebook—planned to be—stablecoin “Libra” has sparked increasing interest among investors, academics, and legislative institutions as has been considered to be the workhorse toward a fully-decentralized digital payment system. Despite claims about rivalry between Libra and Bitcoin, the announcement about creation of the former has aroused even more vivid interest in cryptocurrencies.

If one looks at the existing literature, it is easily observable that not a large number of academic papers have been devoted to studying spillover influences among digital currencies. Existing empirical work mainly investigates the linkages among virtual coins of primary importance but also econometric estimations take place about impacts on smaller-cap currencies. In stark contrast to the bulk of relevant research, spillovers among digital currencies are considered to be one of the most fundamental axes for casting light in cryptocurrency markets and gaining insight into the use of innovative forms of money for the purposes of consumption and investments.

This survey paper abstains from mingling up with co-movements between virtual coins and concentrates on the preponderant issue of spillover impacts in their returns and volatilities. In order to elaborate on the findings brought to the surface by this strand of the literature, we dwell on all the eleven empirical studies that practically form the base of this systematic survey. Exploring spillover interconnectedness and providing a roadmap for further relevant research across digital currencies serves as a motivation for this paper.

The remainder of this study proceeds as follows. Section 2 provides a review of the methodologies adopted for detecting spillovers in cryptocurrency markets. Section 3 provides the literature for return and volatility spillovers among cryptocurrencies. In Section 4, spillovers among digital currencies and other assets are also presented and economic implications are analyzed. Finally, Section 5 summarizes the findings and conclusions. Figure A1, Figure A2, Figure A3, Figure A4, Figure A5, Figure A6, Figure A7, Figure A8 and Figure A9 in the Appendix A display an integrated overview of special characteristics regarding the studies under scrutiny.

2. Methodologies about Studying Spillover Effects in Cryptocurrency and Other Financial Markets

A number of advanced econometric techniques have been employed in order to investigate the interconnectedness among financial assets. Vector autoregressive (VAR) schemes based on Diebold and Yilmaz (2009) and forecast error variance decomposition (FEVD) based on Diebold and Yilmaz (2012) as in Gillaizeau et al. (2019) are employed. They define that “spillovers” is the fraction of the H-step ahead error variances in forecasting x_i arising from shocks to x_j, for i ≠ j. Moreover, apart from classical VAR, structural vector autoregressive (SVAR) schemes have been adopted in order to examine Granger causality among financial assets by Luu Duc Huynh (2019). Additionally, least absolute shrinkage and selection operator (LASSO)-VAR techniques have been adopted by Yi et al. (2018). Moreover, the multivariate quantile conditional autoregressive value-at-risk (MVQM-CAViaR) model constitutes a VAR extension to quantile models. This has been employed by Wang et al. (2018) in order to investigate spillover impacts from economic policy uncertainty to Bitcoin.

Autoregressive conditional heteroskedasticity (ARCH) methodologies and especially the exponential GARCH (EGARCH) and the Glosten-Jagannathan-Runkle (GJR)-GARCH specifications have been employed for capturing volatilities and leverage effects as in Bouri et al. (2018). Correlation is also investigated by dynamic conditional correlations (DCC)-GARCH and asymmetric DCC-GARCH methods. Baba-Engle-Kraft-Kroner (BEKK) combined with GARCH specifications have been used for the measurement of spillovers as in Katsiampa (2019a). The BEKK structure enables the interaction of the conditional variances and covariances of a significant number of time series. Thereby, volatility transmission impacts can be identified. In a similar vein, the VAR-BEKK-asymmetric GARCH methodology has been adopted in order to examine the return, volatility, and shock spillovers between financial assets. This model takes into consideration the asymmetries of negative shocks on conditional variance as in Symitsi and Chalvatzis (2018). Alternative specifications based on the combination of VAR and GARCH schemes have been employed in Bouri et al. (2018) in the form of smooth-transition VAR combined with bivariate GARCH-M (STVAR-BTGARCH-M) specifications. Integrated GARCH (IGARCH) methodologies combined with dynamic conditional correlations have been adopted by Kumar and Anandarao (2019).

Moreover, classical Pearson correlation estimations have been employed for measuring the interlinkages as in Luu Duc Huynh (2019). In a different vein, in order to detect the direction of volatility spillovers not only parametric but also non-parametric tests have been used. The wavelet multiple correlation (WMC) is a multivariate time-scale method used for tracing interconnectedness. Moreover, the autoregressive distributed lag (ARDL) methodology has been employed for the same purposes by Ciaian and Rajcaniova (2018).

3. Studies about Spillovers among Cryptocurrency Markets

Spillovers among digital currencies have aroused interest in academics, policymakers and investors, and the financial press and have resulted in an embryonic but increasing and very interesting array of publications in highly-respected journals. This has provided an impetus to literature about cryptocurrency spillovers and has led to further sophistication of estimation methodologies.

To be more precise, Katsiampa et al. (2019) employed three pairwise bivariate models in order to look into the conditional volatility dynamics as well as the interconnectedness and conditional correlations among the Bitcoin-Ethereum, Bitcoin-Litecoin and Ethereum-Litecoin currency prices. These specifications are based on the Baba-Engle-Kraft-Kroner (BEKK) methodology. Evidence is provided that the historical shocks and volatility of each digital currency are very influential regarding its conditional covariance. Moreover, they reveal that shock transmission is bi-directional concerning the pair Bitcoin–Ethereum as well as the pair Bitcoin–Litecoin. Nevertheless, outcomes indicate that there is only uni-directional spillover of shocks from Ethereum toward Litecoin. As regards volatility spillovers, bi-directional effects are detected between each one of the three pairs under scrutiny. Overall, empirical results support that the cryptocurrency markets take steps toward higher integration. Furthermore, Koutmos (2018) investigates interdependencies among 18 digital currencies of major importance. The methodology adopted is based on vector autoregressive (VAR) schemes and variance decomposition as well as the construction of a spillover index. Furthermore, generalized autoregressive conditional heteroskedasticity (GARCH) methodologies are employed for robustness checks. Decomposition of return and volatility shocks provides evidence that Bitcoin is the most important cryptocurrency as a generator of return and volatility spillovers toward other high-capitalization virtual currencies. Outcomes reveal that the intensity of these spillovers has been increasing in a steady pace as time passes. Furthermore, it is found that major news triggers higher spillovers. Emphasis is paid on the higher level of contagion risk among cryptocurrency markets because of the growing of interdependence among the digital currencies. This is accompanied by a higher level of uncertainty in such markets because of the fluctuations of spillovers throughout time.

In a somewhat similar vein, Kumar and Anandarao (2019) look into the dynamics of volatility spillovers concerning the returns of Bitcoin, Ethereum, Ripple, and Litecoin. The methodology they employ is the integrated generalized autoregressive conditional heteroskedasticity—dynamic conditional correlations (IGARCH(1,1)—DCC(1,1)) specification. Outcomes from GARCH estimations reveal the existence of significant volatility spillovers from Bitcoin to Ethereum and Litecoin. Moreover, estimations based on conditional correlations provide evidence of modest co-movement behavior among returns of digital currencies. They also show that volatility co-movement is weak during earlier years but more intense since the bullish trend in the markets of virtual currencies. It should be noted that the wavelet cross-spectra adopted for examination confirm the findings by DCC methodologies. Overall, there is evidence that Bitcoin is the most prominent and influential among cryptocurrencies. Moreover, Luu Duc Huynh (2019) examines spillover risks among markets of digital currencies by employing a number of methodologies. Pearson correlations, vector autoregressive (VAR) and structural vector autoregressive (SVAR) causality as well as Student’s—t copulas are adopted in order to detect the interdependency among Bitcoin, Ethereum, Ripple, Litecoin, and Stellar. Findings indicate that Bitcoin is not found to receive or to exert any spillover impacts regarding the rest of the coins investigated.

By following a different methodology, Omane-Adjepong and Alagidede (2019) used wavelet-based methodologies as well as parametric and non-parametric tests in order to investigate market coherences and the causal nexus regarding volatility among Bitcoin, BitShares, Litecoin, Stellar, Ripple, Monero, and Dash. The maximum overlap discrete wavelet transform (MODWT) is used to obtain wavelet coefficients and the wavelet multiple correlation (WMC) is estimated. Furthermore, the generalized autoregressive conditional heteroskedasticity GARCH(1,1) and the Glosten-Jagannathan-Runkle generalized autoregressive conditional heteroskedasticity GJR-GARCH(1,1) specifications are employed for measuring conditional volatility. Moreover, conventional Granger causality tests are adopted in vector autoregressive (VAR) frameworks. Econometric estimations reveal that there is weak to modest level of connectedness concerning all the currencies examined. Bitcoin and Ripple are found to be the most influential ones. There is evidence that the most tightly-interconnected pairs are: Dash-Ripple, Monero-Ripple, and Dash-Stellar. Results reveal the non-homogeneous directions of connectedness as a significant number of pairs exhibit (non)linear feedback nexus or shock transmissions of only one direction. During longer-term investments, more intense linkages are detected between pairs. It is emphasized that the linkages and causality as regards volatility depend in a large extent on trading scales and the proxy for market volatility.

When it comes to Zięba et al. (2019), they examined interdependencies between log-returns of digital currencies by employing the minimum spanning tree (MST) methodology as well as vector autoregressive (VAR) models that are based on clusters formed by the MST results. Evidence reveals that despite Bitcoin’s dominance in the cryptocurrency markets, shocks in Bitcoin’s market value are not transmitted into shocks in other digital currencies. Furthermore, the reverse transmission procedure does not hold. Somewhat surprisingly, Litecoin and Dogecoin are found to be more influential as regards spillovers toward other virtual coins. Moreover, powerful links are traced in the group of the Bitcoin, Monero and Dash currencies. The same holds regarding the group of Dogecoin, Ripple, Stellar, and BitShares.

4. Studies about Spillovers between Cryptocurrency Markets and Markets of Other Assets or Economic Conditions

Investigation about spillovers related to digital currencies has surpassed the limits of cryptocurrency markets. Thereby, a respectable number of prestigious academic studies have shed light on interconnectedness between virtual coins and traditional assets, such as stocks or currencies. It should be noted that also research into the influence between economic policy uncertainty and digital currencies has been carried out.

More specifically, Bouri et al. (2018) investigate return and volatility spillovers between Bitcoin and stocks, commodities, currencies and bonds in bearish and bullish conditions in markets. They employ a bivariate generalized autoregressive conditional heteroskedasticity (BTGARCH) specification to model volatility as well as the smooth transition vector autoregressive (STVAR) scheme in order to capture the changes between market conditions (STVAR-BTGARCH-M). Moreover, the Glosten-Jagannathan-Runkle generalized autoregressive conditional heteroskedasticity (GJR-GARCH) methodology is used for estimations. Results reveal that spillover impacts between Bitcoin and the other assets are subject to time and market conditions and that the linkage is more powerful concerning returns rather than volatility. Spillovers are found to be asymmetric and there is evidence that Bitcoin is most often the receiver rather than the giver of volatility effects. It is argued that the size effect of spillovers varies according to market conditions. Moreover, Symitsi and Chalvatzis (2018) adopt an asymmetric multivariate vector autoregressive- generalized autoregressive conditional heteroskedasticity based on the Baba-Engle-Kraft-Kroner (VAR-BEKK-AGARCH) specification in order to look into spillover impacts between Bitcoin and energy and technology companies. Empirical outcomes provide evidence that energy and technology stocks generate significant return spillovers toward Bitcoin. When it comes to volatility, results reveal that technology companies trigger short-run volatility spillovers toward Bitcoin whereas energy companies are responsible for long-run volatility spillovers toward this dominant currency. It is found that bi-directional asymmetric shock spillovers take place between Bitcoin and equity indices while dynamic correlation between them is weak.

Trabelsi (2018) examines whether there is connectedness among markets of virtual currencies and across the Bitcoin index (BPI) and popular assets such as currencies, equity market indices, gold and Brent oil. The spillover index by Diebold and Yilmaz (2012) and Baruník and Křehlík (2018) is employed along with the spectral representation of variance decomposition in networks, in order to measure the linkages. Findings document that no significant spillover impacts exist between the market of digital currencies and the markets of traditional assets. As regards Gillaizeau et al. (2019), they examine outward and inward volatility spillovers in cross-market Bitcoin prices by following the generalized variance decomposition procedure by Diebold and Yilmaz (2012) and frequency domain analysis. Exchange rates of Bitcoin in relation to USD, AUD, CAD, EUR, and the GBP are under scrutiny. The Parkinson’s high-low historical volatility (HL-HV) measure and the Garman-Glass measure are employed for measuring volatility. Evidence reveals that volatility shocks to the BTC/EUR and BTC/USD exchange rates are also found to be influential. Furthermore, there is evidence that the BTC/EUR market of currency values is the most sensitive to uncertainty about the other exchange rates and the BTC/USD follows whereas the BTC/GBP is both very weakly influenced and influential. It is argued that the BTC/CAD and BTC/EUR markets are net receivers of volatility while BTC/USD constitutes a net provider as regards negative net volatility. Overall, approximately 15% to 20% of the forecast error variance in volatility of each rate can be explained by the other rates. Results about return spillovers are in accordance with those about volatility spillovers. It is argued that investor sentiment and uncertainty strengthen volatility.

By adopting an alternative view, Wang et al. (2018) look into the risk spillover impacts from economic policy uncertainty (EPU) to Bitcoin by employing a multivariate quantile model, the Granger causality risk test and a conditional autoregressive value-at-risk framework ((MVQM-CAViaR(1,1)). The US EPU index, the equity market uncertainty index, and the VIX index are used as proxies for EPU. Econometric estimations provide evidence that the risk spillover effect from EPU to Bitcoin is not significant and that the value-at-risk of Bitcoin is influenced by the values of this measure and volatility at past times. Results are robust to estimations at different quantiles and time-lags, data frequency, the 2013 Bitcoin price crash event and contemporaneous or instantaneous correlations.

Evidence by primary studies indicates that Bitcoin is an influential giver of spillover effects toward cryptocurrency markets but is also a receiver of spillover impacts from high-capitalization digital coins and more traditional assets, such as leading stocks, currencies, and commodities. This gives credence to arguments that Bitcoin remains dominant in the markets of digital currencies but is mainly affected and not affects the global economic factors, such as traditional assets, major news and economic policy uncertainty. These findings support the integration of digital currencies—especially Bitcoin—into global financial markets, but reveal that large steps toward digitalization in payment systems have to take place in order for Bitcoin to become the centerpiece of the financial system in international markets.

Table 1 provides an overview of the variables examined, frequency of data and the time period investigated in primary papers of this survey. Moreover, the data source, the methodologies employed, and the conclusions about spillover effects are laid out.

5. Conclusions

This paper provides an integrated survey of empirical research on return and volatility spillovers across cryptocurrency markets. Results about interconnectedness among digital coins are predicated by a spectrum of methodologies. Econometric outcomes cast light on whether herding behavior exists in digital currency markets and whether the prevalence of new coins by initial coin offerings (ICOs) could dampen the domineering influence of Bitcoin on virtual currency markets. The aim of this systematic survey is to shed light on unknown aspects about spillovers among innovative forms of liquidity and help investors decide whether trading with virtual currencies constitutes an idea worth pondering in a wider context of financial digitalization.

This survey builds on the nascent but proliferating literature on spillovers among high-capitalization cryptocurrencies as well as papers concerning the nexus of popular digital currencies with less liquid ones. Influences with traditional assets such as currencies, stocks, gold, and oil are also examined in primary studies and also measurements of linkages with indices of uncertainty take place. An integrated overview of the methodologies adopted, the quality of data employed and the economic underpinnings of outcomes is provided.

More specifically, it is revealed that Bitcoin remains the dominant cryptocurrency and is the most influential giver as concerning virtual coins and receiver of spillover impacts as regards high-capitalization cryptocurrencies and other assets. Currencies such as Ethereum, Litecoin, and Ripple are found to be in tight relation to Bitcoin mainly as receivers of its spillovers. There is evidence that return spillovers are more pronounced but volatility spillovers present more often a bi-directional character.

Overall, results indicate the existence of a potential for a sustainable spillover behavior in the digital currency markets with Bitcoin remaining the cornerstone in the perpetuation of this phenomenon. The interconnectedness of virtual coins with traditional assets could enable portfolio managers to mitigate risk by forming diversified portfolios with optimal proportions of assets. Spillover impacts are indicative of the cryptocurrency markets making steps toward higher integration in global financial markets.

This study can serve as a roadmap for academic researchers, policymakers, and regulatory institutions, investors, and the economic press for achieving an in-depth understanding of the interconnectedness among these highly-speculative forms of trading. Potential avenues for future research in the field of virtual currencies should include the thorough investigation of co-movements across returns and volatility of cryptocurrencies and of how this affects the investor behavior in the markets of digital currencies and stablecoins.

Funding

This research received no external funding.

Acknowledgments

This paper is part of the author’s post-doctoral research. The author is grateful to Stephanos Papadamou for useful guidance regarding this paper and his overall help in his post-doctoral research.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

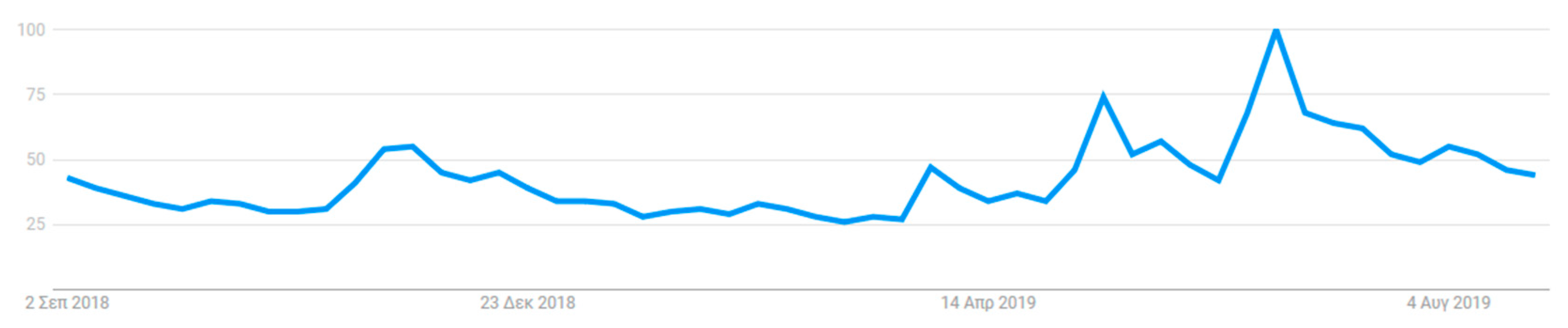

Figure A1.

Google trends for “Bitcoin” in a global level (source: https://trends.google.com).

Figure A1.

Google trends for “Bitcoin” in a global level (source: https://trends.google.com).

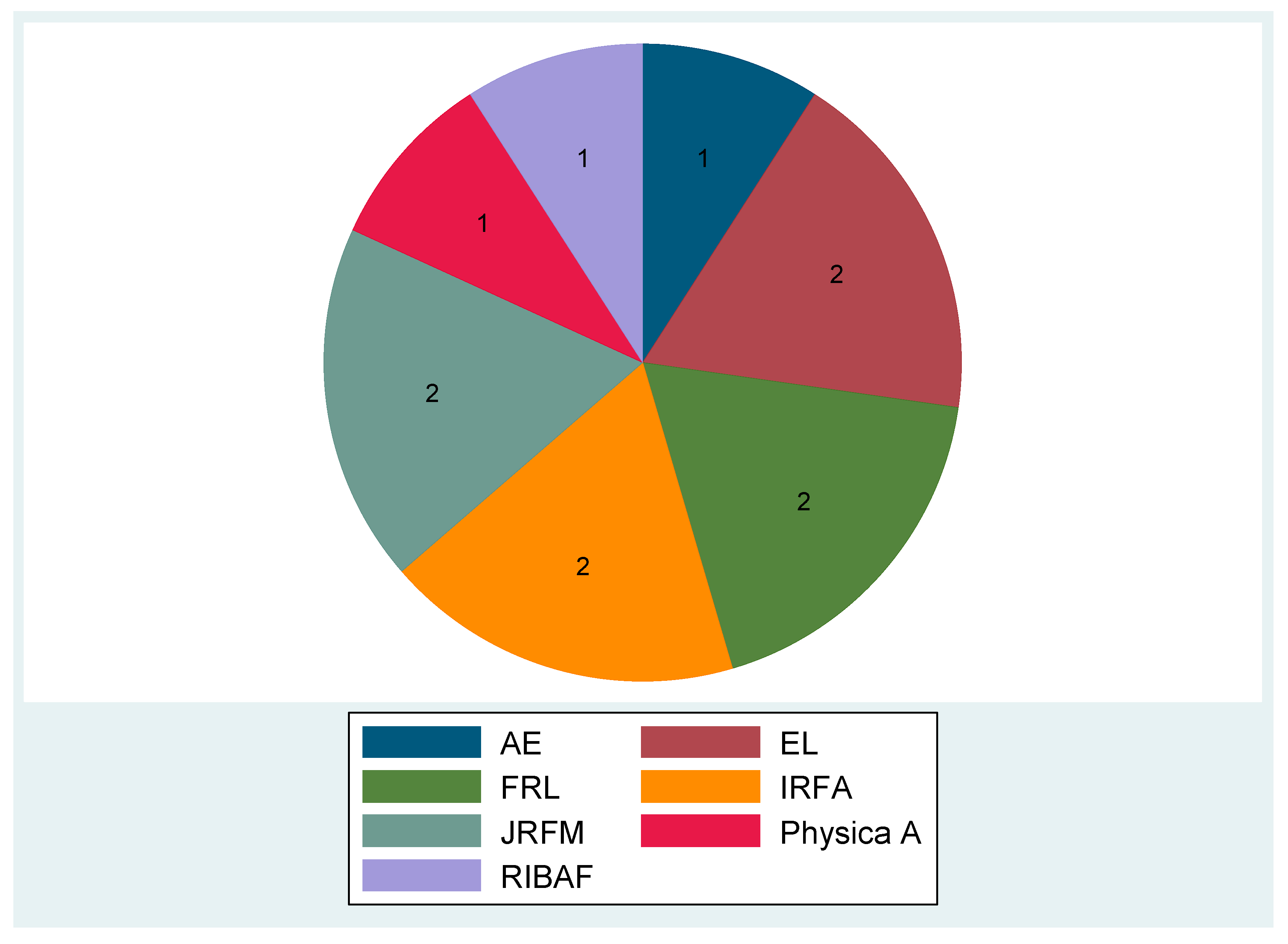

Figure A2.

Frequency of articles published in journals (extracted on: 30 August 2019). Notes: AE, EL, FRL, IRFA, JRFM, Physica A, and RIBAF stand for Applied Economics, Economics Letters, Finance Research Letters, International Review of Financial Analysis, Journal of Risk and Financial Management, Physica A: Statistical Mechanics and its Applications, and Research in International Business and Finance, respectively.

Figure A2.

Frequency of articles published in journals (extracted on: 30 August 2019). Notes: AE, EL, FRL, IRFA, JRFM, Physica A, and RIBAF stand for Applied Economics, Economics Letters, Finance Research Letters, International Review of Financial Analysis, Journal of Risk and Financial Management, Physica A: Statistical Mechanics and its Applications, and Research in International Business and Finance, respectively.

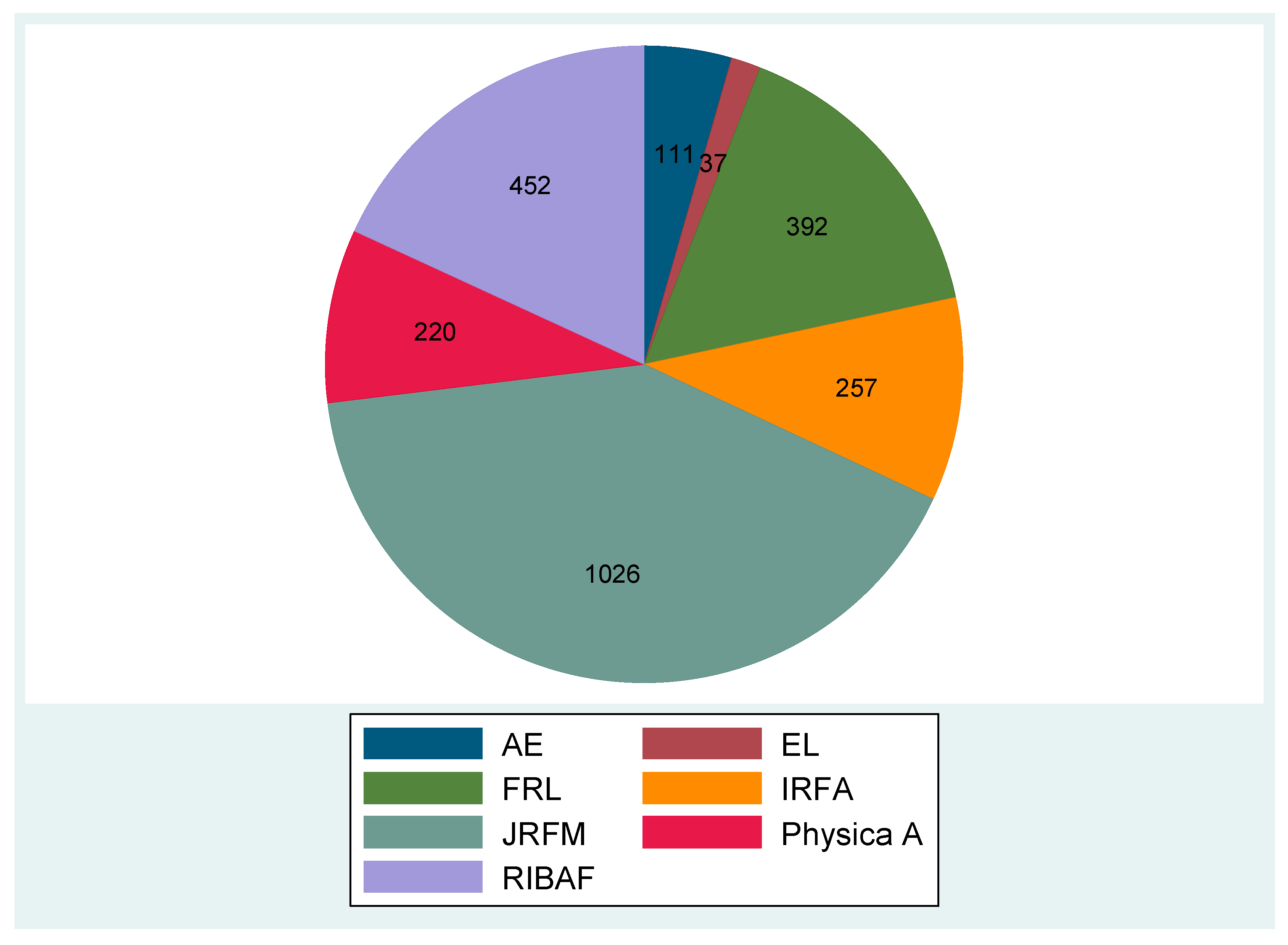

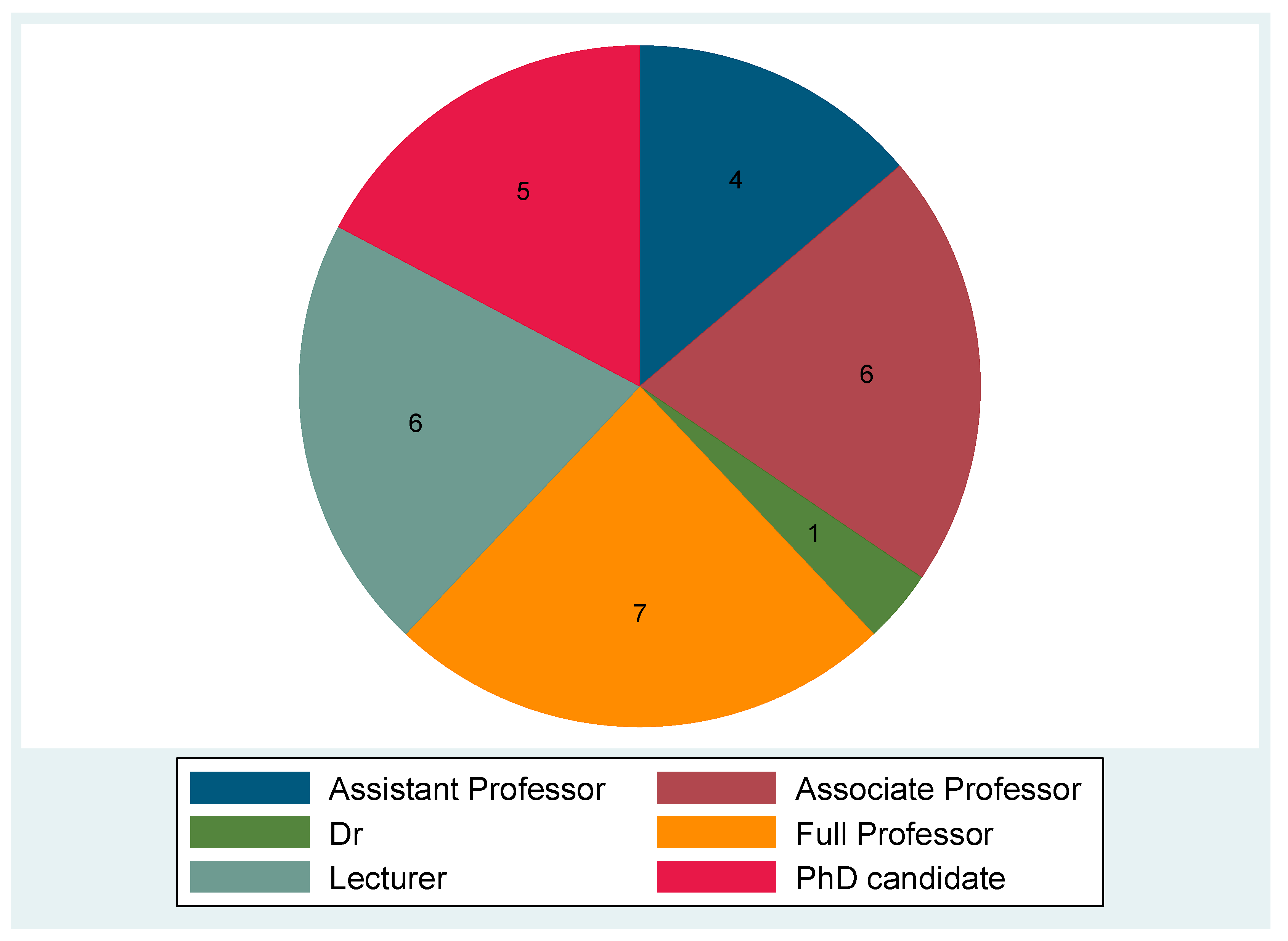

Figure A3.

H-index scores for each journal (extracted on: 30 August 2019).

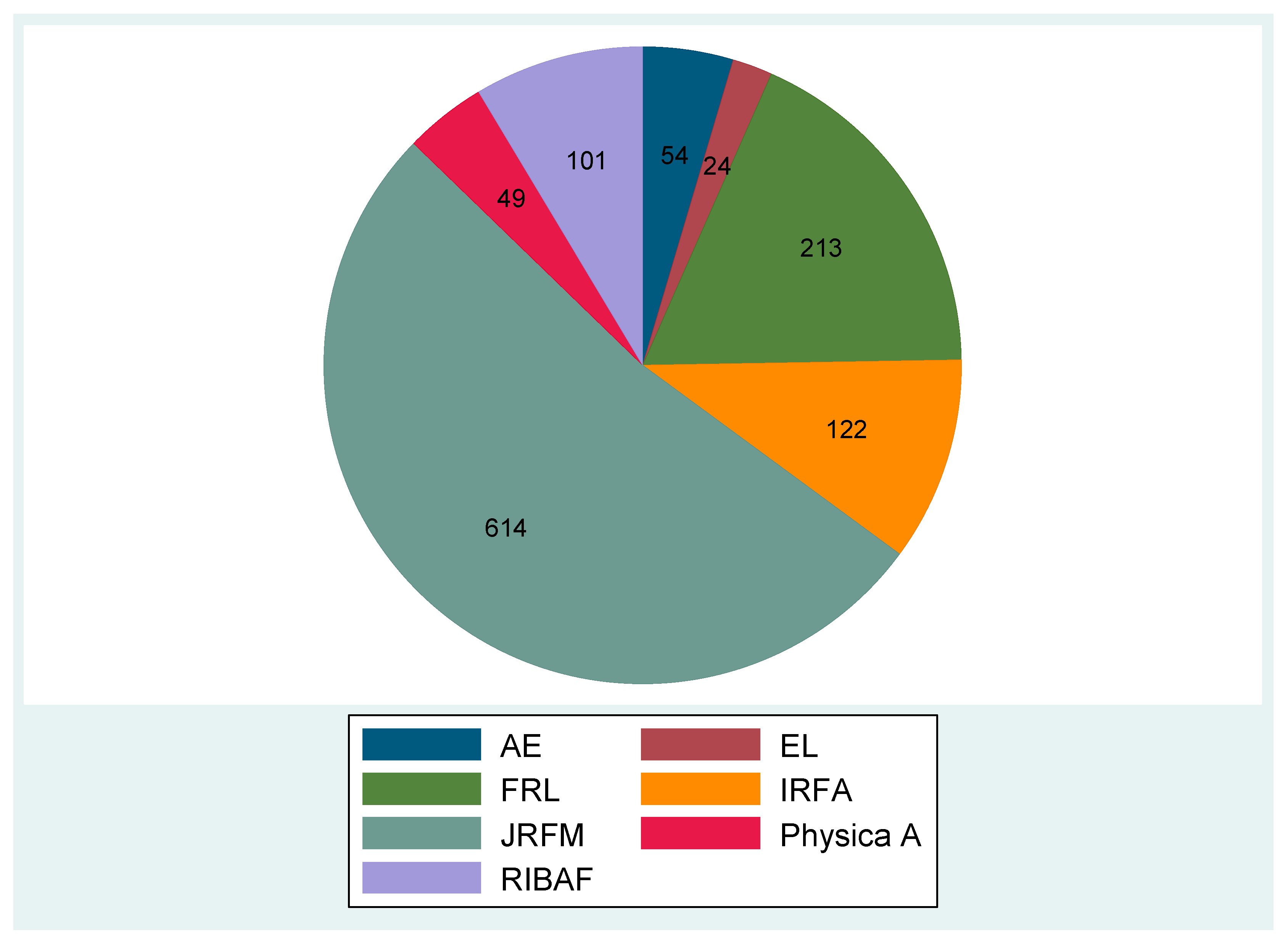

Figure A4.

Average abstract views concerning each journal (extracted on: 30 August 2019).

Figure A5.

Average downloads concerning each journal (extracted on: 30 August 2019).

Figure A6.

Citations per academic paper (extracted on: 30 August 2019).

Figure A7.

Number of references used by academic papers (extracted on: 30 August 2019).

Figure A8.

Country location of universities where authors about cryptocurrency spillovers are employed (information extracted on: 30 August 2019).

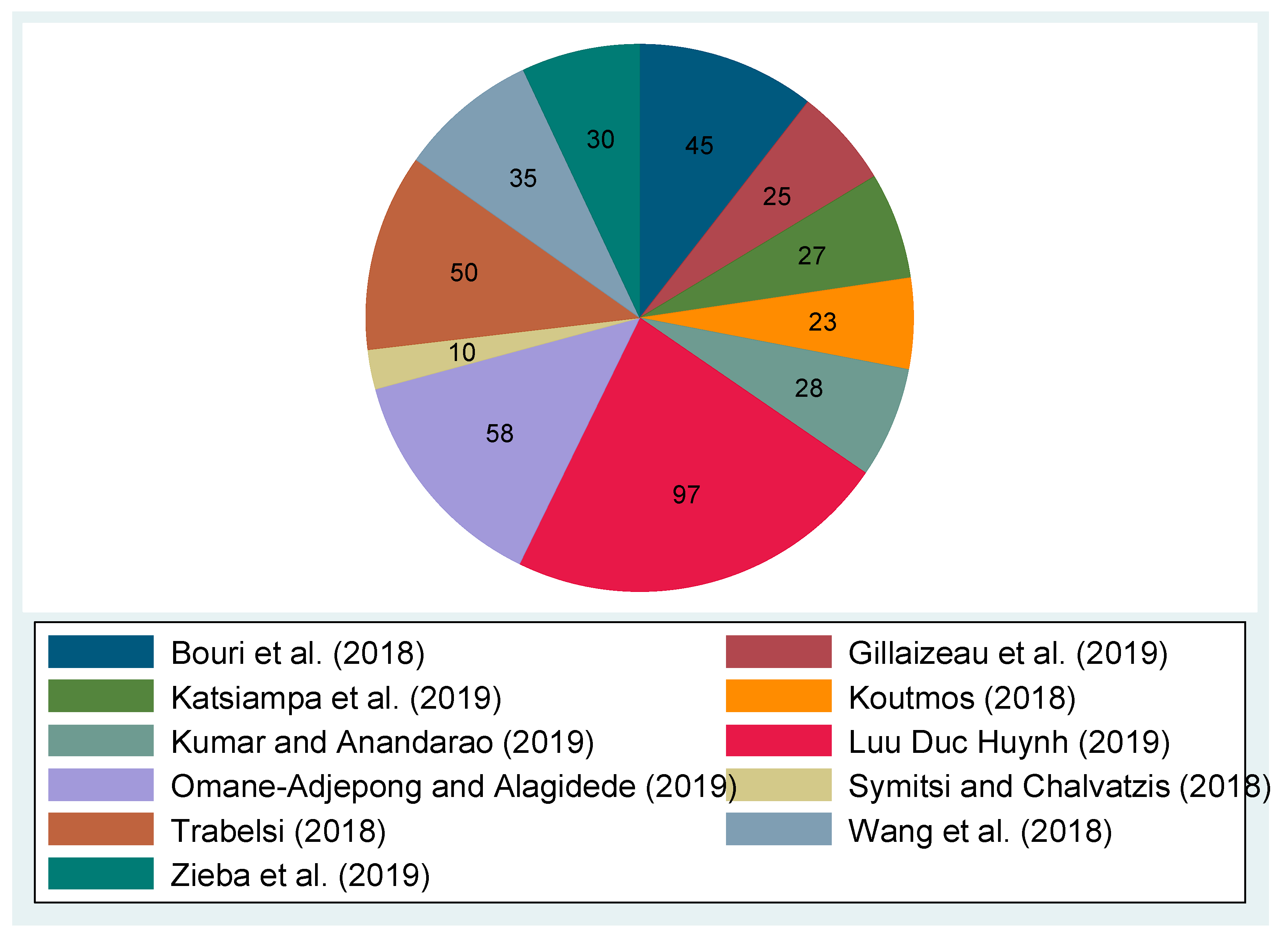

Figure A8.

Country location of universities where authors about cryptocurrency spillovers are employed (information extracted on: 30 August 2019).

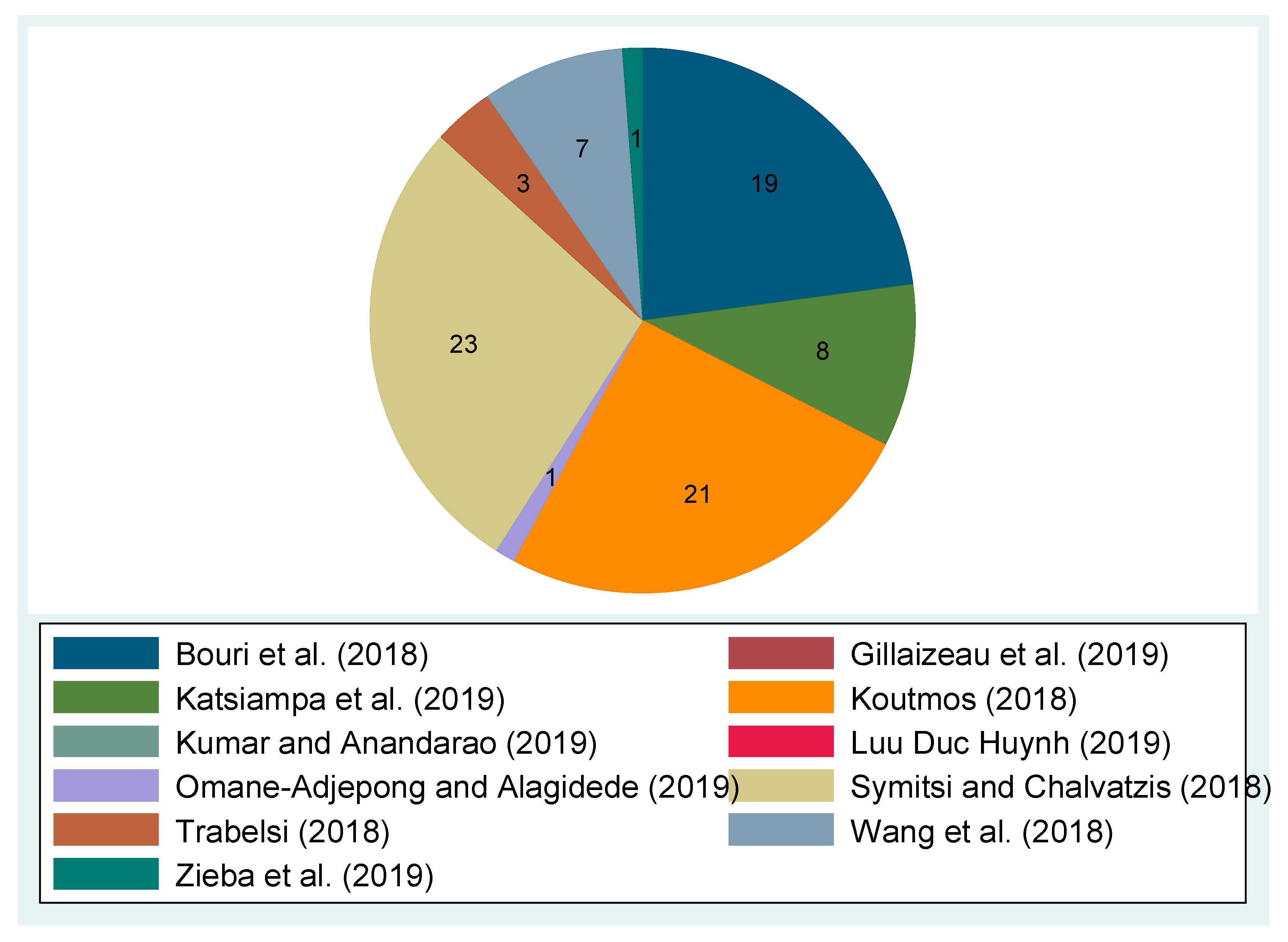

Figure A9.

Academic ranks of researchers about spillover effects in cryptocurrency markets (information extracted on: 30 August 2019).

Figure A9.

Academic ranks of researchers about spillover effects in cryptocurrency markets (information extracted on: 30 August 2019).

References

- Ammous, Saifedean. 2018. Can cryptocurrencies fulfil the functions of money? The Quarterly Review of Economics and Finance 70: 38–51. [Google Scholar] [CrossRef]

- Baker, Scott R., Nicholas Bloom, and Steven J. Davis. 2016. Measuring economic policy uncertainty. The Quarterly Journal of Economics 131: 1593–636. [Google Scholar] [CrossRef]

- Bariviera, Aurelio F. 2017. The inefficiency of Bitcoin revisited: A dynamic approach. Economics Letters 161: 1–4. [Google Scholar] [CrossRef]

- Baruník, Jozef, and Tomáš Křehlík. 2018. Measuring the frequency dynamics of financial connectedness and systemic risk. Journal of Financial Econometrics 16: 271–96. [Google Scholar] [CrossRef]

- Beneki, Christina, Alexandros Koulis, Nikolaos A. Kyriazis, and Stephanos Papadamou. 2019. Investigating volatility transmission and hedging properties between Bitcoin and Ethereum. Research in International Business and Finance 48: 219–27. [Google Scholar] [CrossRef]

- Böhme, Rainer, Nicolas Christin, Benjamin Edelman, and Tyler Moore. 2015. Bitcoin: Economics, technology, and governance. Journal of Economic Perspectives 29: 213–38. [Google Scholar] [CrossRef]

- Bollerslev, Tim. 1986. Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics 31: 307–27. [Google Scholar] [CrossRef]

- Bouri, Elie, Peter Molnár, Georges Azzi, David Roubaud, and Lars Ivar Hagfors. 2017. On the hedge and safe haven properties of Bitcoin: Is it really more than a diversifier? Finance Research Letters 20: 192–98. [Google Scholar] [CrossRef]

- Bouri, Elie, Mahamitra Das, Rangan Gupta, and David Roubaud. 2018. Spillovers between Bitcoin and other assets during bear and bull markets. Applied Economics 50: 5935–49. [Google Scholar] [CrossRef]

- Chaim, Pedro, and Márcio P. Laurini. 2018. Volatility and return jumps in bitcoin. Economics Letters 173: 158–63. [Google Scholar] [CrossRef]

- Ciaian, Pavel, and Miroslava Rajcaniova. 2018. Virtual relationships: Short-and long-run evidence from BitCoin and altcoin markets. Journal of International Financial Markets, Institutions and Money 52: 173–95. [Google Scholar] [CrossRef]

- Corbet, Shaen, Brian Lucey, Andrew Urquhart, and Larisa Yarovaya. 2019. Cryptocurrencies as a financial asset: A systematic analysis. International Review of Financial Analysis 62: 182–99. [Google Scholar] [CrossRef]

- Diebold, Francis X., and Kamil Yilmaz. 2009. Measuring financial asset return and volatility spillovers, with application to global equity markets. The Economic Journal 119: 158–71. [Google Scholar] [CrossRef]

- Diebold, Francis X., and Kamil Yilmaz. 2012. Better to give than to receive: Predictive directional measurement of volatility spillovers. International Journal of Forecasting 28: 57–66. [Google Scholar] [CrossRef]

- Dyhrberg, Anne Haubo. 2016. Hedging capabilities of bitcoin. Is it the virtual gold? Finance Research Letters 16: 139–44. [Google Scholar] [CrossRef]

- Engle, Robert F. 1982. Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica: Journal of the Econometric Society 50: 987–1007. [Google Scholar] [CrossRef]

- Engle, Robert F., and Kenneth F. Kroner. 1995. Multivariate simultaneous generalized ARCH. Econometric Theory 11: 122–50. [Google Scholar] [CrossRef]

- Engle, Robert F., and Simone Manganelli. 2004. CAViaR: Conditional autoregressive value at risk by regression quantiles. Journal of Business & Economic Statistics 22: 367–81. [Google Scholar]

- Engle, Robert F., and Tim Bollerslev. 1986. Modelling the persistence of conditional variances. Econometric Reviews 5: 1–50. [Google Scholar] [CrossRef]

- Engle, Robert. 2002. Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models. Journal of Business & Economic Statistics 20: 339–50. [Google Scholar]

- Fang, Libing, Elie Bouri, Rangan Gupta, and David Roubaud. 2019. Does global economic uncertainty matter for the volatility and hedging effectiveness of Bitcoin? International Review of Financial Analysis 61: 29–36. [Google Scholar] [CrossRef]

- Garman, Mark B., and Michael J. Klass. 1980. On the estimation of security price volatilities from historical data. Journal of Business 53: 67–78. [Google Scholar] [CrossRef]

- Gillaizeau, Marc, Ranadeva Jayasekera, Ahmad Maaitah, Tapas Mishra, Mamata Parhi, and Evgeniia Volokitina. 2019. Giver and the receiver: Understanding spillover effects and predictive power in cross-market Bitcoin prices. International Review of Financial Analysis 63: 86–104. [Google Scholar] [CrossRef]

- Glosten, Lawrence R., Ravi Jagannathan, and David E. Runkle. 1993. On the relation between the expected value and the volatility of the nominal excess return on stocks. The Journal of Finance 48: 1779–801. [Google Scholar] [CrossRef]

- Granger, Clive W. 1969. Investigating causal relations by econometric models and cross-spectral methods. Econometrica: Journal of the Econometric Society 37: 424–38. [Google Scholar] [CrossRef]

- Katsiampa, Paraskevi, Shaen Corbet, and Brian Lucey. 2019. Volatility spillover effects in leading cryptocurrencies: A BEKK-MGARCH analysis. Finance Research Letters 29: 68–74. [Google Scholar] [CrossRef]

- Katsiampa, Paraskevi. 2017. Volatility estimation for Bitcoin: A comparison of GARCH models. Economics Letters 158: 3–6. [Google Scholar] [CrossRef]

- Katsiampa, Paraskevi. 2019a. Volatility co-movement between Bitcoin and Ether. Finance Research Letters 30: 221–27. [Google Scholar] [CrossRef]

- Katsiampa, Paraskevi. 2019b. An empirical investigation of volatility dynamics in the cryptocurrency market. Research in International Business and Finance 50: 322–35. [Google Scholar] [CrossRef]

- Koutmos, Dimitrios. 2018. Return and volatility spillovers among cryptocurrencies. Economics Letters 173: 122–27. [Google Scholar] [CrossRef]

- Kumar, Anoop S., and Suvvari Anandarao. 2019. Volatility spillover in crypto-currency markets: Some evidences from GARCH and wavelet analysis. Physica A: Statistical Mechanics and its Applications 524: 448–58. [Google Scholar] [CrossRef]

- Kundu, Srikanta, and Nityananda Sarkar. 2016. Return and volatility interdependences in up and down markets across developed and emerging countries. Research in International Business and Finance 36: 297–311. [Google Scholar] [CrossRef]

- Kyriazis, Nikolaos A. 2019. A survey on efficiency and profitable trading opportunities in cryptocurrency markets. Journal of Risk and Financial Management 12: 67. [Google Scholar] [CrossRef] [Green Version]

- Kyriazis, Νikolaos A., and Paraskevi Prassa. 2019. Which Cryptocurrencies Are Mostly Traded in Distressed Times? Journal of Risk and Financial Management 12: 135. [Google Scholar] [CrossRef] [Green Version]

- Kyriazis, Νikolaos A., Kalliopi Daskalou, Marios Arampatzis, Paraskevi Prassa, and Evangelia Papaioannou. 2019. Estimating the volatility of cryptocurrencies during bearish markets by employing GARCH models. Heliyon 5: e02239. [Google Scholar] [CrossRef] [PubMed]

- Luu Duc Huynh, Toan. 2019. Spillover Risks on Cryptocurrency Markets: A Look from VAR-SVAR Granger Causality and Student’st Copulas. Journal of Risk and Financial Management 12: 52. [Google Scholar] [CrossRef] [Green Version]

- Mantegna, Rosario N. 1999. Hierarchical structure in financial markets. The European Physical Journal B-Condensed Matter and Complex Systems 11: 193–97. [Google Scholar] [CrossRef] [Green Version]

- Mantegna, Rosario N., and H. Eugene Stanley. 1999. Introduction to Econophysics: Correlations and Complexity in Finance. Cambridge: Cambridge University Press. [Google Scholar]

- McAleer, Michael, Suhejla Hoti, and Felix Chan. 2009. Structure and asymptotic theory for multivariate asymmetric conditional volatility. Econometric Reviews 28: 422–40. [Google Scholar] [CrossRef]

- Nadarajah, Saralees, and Jeffrey Chu. 2017. On the inefficiency of Bitcoin. Economics Letters 150: 6–9. [Google Scholar] [CrossRef] [Green Version]

- Omane-Adjepong, Maurice, and Imhotep Paul Alagidede. 2019. Multiresolution analysis and spillovers of major cryptocurrency markets. Research in International Business and Finance 49: 191–206. [Google Scholar] [CrossRef]

- Parkinson, Michael. 1980. The extreme value method for estimating the variance of the rate of return. Journal of Business 53: 61–65. [Google Scholar] [CrossRef]

- Pesaran, H. Hashem, and Yongcheol Shin. 1998. Generalized impulse response analysis in linear multivariate models. Economics Letters 58: 17–29. [Google Scholar] [CrossRef]

- Selgin, George. 2015. Synthetic commodity money. Journal of Financial Stability 17: 92–99. [Google Scholar] [CrossRef]

- Symitsi, Efthymia, and Konstantinos J. Chalvatzis. 2018. Return, volatility and shock spillovers of Bitcoin with energy and technology companies. Economics Letters 170: 127–30. [Google Scholar] [CrossRef] [Green Version]

- Trabelsi, Nader. 2018. Are There Any Volatility Spill-Over Effects among Cryptocurrencies and Widely Traded Asset Classes? Journal of Risk and Financial Management 11: 66. [Google Scholar] [CrossRef] [Green Version]

- Urquhart, Andrew. 2016. The inefficiency of Bitcoin. Economics Letters 148: 80–82. [Google Scholar] [CrossRef]

- Wang, Gang Jin, Chi Xie, Danyan Wen, and Longfeng Zhao. 2018. When Bitcoin meets economic policy uncertainty (EPU): Measuring risk spillover effect from EPU to Bitcoin. Finance Research Letters. [Google Scholar] [CrossRef]

- Wei, Wang Chun. 2018. Liquidity and market efficiency in cryptocurrencies. Economics Letters 168: 21–24. [Google Scholar] [CrossRef]

- White, Halbert, Tae-Hwan Kim, and Simone Manganelli. 2015. VAR for VaR: Measuring tail dependence using multivariate regression quantiles. Journal of Econometrics 187: 169–88. [Google Scholar] [CrossRef] [Green Version]

- Yi, Shuyue, Zishuang Xu, and Gang-Jin Wang. 2018. Volatility connectedness in the cryptocurrency market: Is Bitcoin a dominant cryptocurrency? International Review of Financial Analysis 60: 98–114. [Google Scholar] [CrossRef]

- Zięba, Damian, Ryszard Kokoszczyński, and Katarzyna Śledziewska. 2019. Shock transmission in the cryptocurrency market. Is Bitcoin the most influential? International Review of Financial Analysis 64: 102–25. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Overview of studies investigated.

| Authors | Variables Examined | Frequency of Data | Time Period Examined | Data Source | Methodology | Conclusions about Spillovers |

|---|---|---|---|---|---|---|

| Bouri et al. (2018) | Bitcoin MSCI World MSCI Emerging Markets MASCI China SP SGCI Commodity SP SGCI energy Gold US dollar index US 10-year Treasury yields | Daily | 19 July 2010–31 October 2017 | Coindesk Datastream | STVAR-BTGARCH-M as in Kundu and Sarkar (2016) GJR-GARCH by Glosten et al. (1993) DCC-GARCH by Engle (2002) | Asymmetric spillovers. Bitcoin is usually the receiver. Return spillovers higher than volatility spillovers. |

| Gillaizeau et al. (2019) | BTC/USD BTC/AUD BTC/CAD BTC/EUR BTC/GBP EPU | Daily | 12 March 2013–31 January 2018 | www.bitcoincharts.com Mt.Gox Bitstamp LocalBitcoins | Generalized variance decomposition (GVD) approach by Diebold and Yilmaz (2012) in VAR models Parkinson’s high-low historical volatility (HL-HV) model by Parkinson (1980) Garman-Klass measure for volatility by Garman and Klass (1980) | BTC/USD has high predictive power BTC/EUR is net receiver of volatility spillovers |

| Katsiampa et al. (2019) | Bitcoin Ethereum Litecoin | Daily | 7 August 2015 to 10 July 2018 | Coinmarketcap.com | BEKK-MGARCH model by Engle and Kroner (1995) | Bi-directional spillover effects between Bitcoin-Ethereum and between Bitcoin-Litecoin; Uni-directional shock spillover from Ethereum to Litecoin; Bi-directional volatility spillover between all three pairs |

| Koutmos (2018) | Bitcoin Ethereum Ripple Litecoin Dash Stellar NEM Monero Tether Bytecoin BitShares Verge Dogecoin DigiByte MaidSafeCoin MonaCoin ReddCoin Emercoin | Daily | 7 August 2015–17 July 2018 | Coinmarketcap.com | GARCH methodologies by Engle (1982) and Bollerslev (1986) Random rotations by Diebold and Yilmaz (2009) Generalized decomposition in VAR models by Pesaran and Shin (1998) | Bitcoin is the dominant contributor of return and volatility spillovers; Steady increase of spillovers over time; Spikes in spillovers during major events |

| Kumar and Anandarao (2019) | Bitcoin Ethereum Ripple Litecoin | Daily | 15 August 2015–18 January 2018 | Coinmarketcap.com | IGARCH(1,1)—DCC GARCH(1,1) by Engle and Bollerslev (1986) and Engle (2002) Wavelet cross spectra | Significant volatility spillover from Bitcoin to Ethereum and Litecoin |

| Luu Duc Huynh (2019) | Bitcoin Ethereum Ripple Litecoin Stellar | Daily | 8 September 2015–4 January 2019 | - | Pearson correlation VAR-SVAR causality t-Student’s copulas (Gaussian, Student’s-t) | Bitcoin is receiver of spillovers; Ethereum is not affected |

| Omane-Adjepong and Alagidede (2019) | Bitcoin BitShares Litecoin Stellar Ripple Monero Dash | Daily | 8 May 2014–12 February 2018 | Coinmarketcap.com | Maximum Overlap Discrete Wavelet Transform (MODWT) Granger causality (Granger 1969) in a VAR system GARCH GJR-GARCH by Glosten et al. (1993) | (Non)linear feedback linkages or unidirectional transmission of shocks Bitcoin and Ethereum most influential |

| Symitsi and Chalvatzis (2018) | Bitcoin SP Global Clean Energy Index (SPGCE) MSCI World Energy Index (MSCIWE) MSCI World Information Technology Index (MSCIWIT) | Daily | 22 August 2011–15 February 2018 | Datastream | VAR(1)-BEKK-AGARCH model by McAleer et al. (2009) | Significant return spillovers from energy and technology stocks to Bitcoin Short-run volatility spillovers from technology companies and long-run towards energy companies. Bi-directional asymmetric character |

| Trabelsi (2018) | Bitcoin Ethereum Ripple Litecoin Bitcoin Price Index SP500 NASDAQ FTSE100 HangSeng Nikkei225 EUR/USD GBP/USD USD/JPY USD/CHF USD/CAD Gold Brent futures contracts | Daily | 7 October 2010–8 February 2018 | Coindesk - | Spillover index approach by Diebold and Yilmaz (2009) FEVD by Diebold and Yilmaz (2012) and Baruník and Křehlík (2018) | No significant spillover effects |

| Wang et al. (2018) | Bitcoin US EPU index Equity market uncertainty index VIX index | Daily | 18 July 2010–31 May 2018 | www.policyuncertainty.com by Baker et al. (2016) Coindesk | MVQM-CAViaR model based on White et al. (2015) and Engle and Manganelli (2004) | Negligible risk spillover impact from EPU to Bitcoin |

| Zięba et al. (2019) | Pura Emercoin Verge LEOcoin Nexus NewYorkCoin MonetaryUnion Dimecoin I.O.Coin Groestlcoin Energycoin NeosCoin Cloakcoin Ubiq BitBay ECC Mooncoin Monacoin FedoraCoin BitSend Crown CasinoCoin Tether BitCNY Mintcoin Siacoin Boolberry Monero Aeon PotCoin Viacoin FlorinCoin Burst MaidSafeCoin Ethereum Clams DigitalNote NavCoin ByteCoin Omni ReddCoin Stealthcoin Blocknet Bean.Cash Dash FoldingCoin GridCoin Myriad Einstenium OKCash FairCoin WhiteCoin SolarCoin RubyCoin Gulden Feathercoin Diamond Unobtanium DNotes NEM GameCredits DigiByte Counterparty Syscoin VeriCoin BitcoinDark Primecoin Dogecoin BlackCoin Vertcoin Nxt Stellar Ripple BitShares Namecoin Peercoin Litecoin Bitcoin | Daily | 01 September 2015–19 December 2016 20 December 2016–02 May 2018 | Coinmarketcap.com | Minimum-spanning tree (MST) by Mantegna (1999) and Mantegna and Stanley (1999) VAR models and causality by Granger (1969) | No significant spillover effects towards or from Bitcoin. Linkages among Bitcoin, Monero, and Dash. Also interconnectedness among Dogecoin, Ripple, Stellar, and BitShares |

© 2019 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Kyriazis, N.A. A Survey on Empirical Findings about Spillovers in Cryptocurrency Markets. J. Risk Financial Manag. 2019, 12, 170. https://doi.org/10.3390/jrfm12040170

AMA Style

Kyriazis NA. A Survey on Empirical Findings about Spillovers in Cryptocurrency Markets. Journal of Risk and Financial Management. 2019; 12(4):170. https://doi.org/10.3390/jrfm12040170

Chicago/Turabian StyleKyriazis, Nikolaos A. 2019. "A Survey on Empirical Findings about Spillovers in Cryptocurrency Markets" Journal of Risk and Financial Management 12, no. 4: 170. https://doi.org/10.3390/jrfm12040170