Analysis of Trends in Mortgage Lending in the Agricultural Sector of Ukraine

,

,  ,

,

Abstract

:1. Introduction

2. Materials and Methods

- Model the problem as a hierarchy containing the goal of decision making, alternatives for achieving it, and criteria for evaluating alternatives.

- Establish priorities among the elements of the hierarchy, making a number of judgments based on a pairwise comparison of the elements.

- Synthesize (combine) these judgments to obtain a set of common priorities for the hierarchy. Check the consistency of judgments.

- Approach the final decision based on the results of this process.

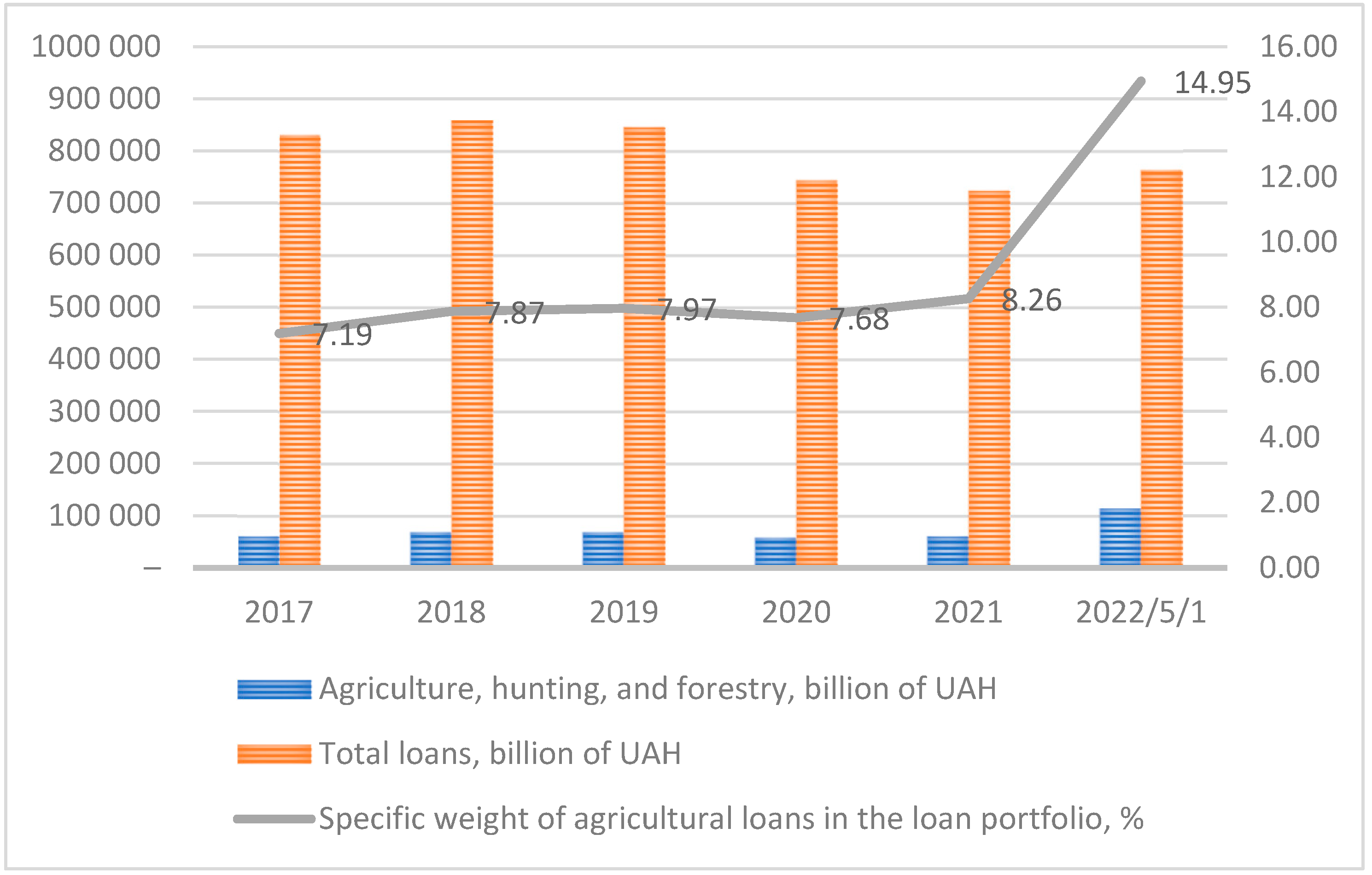

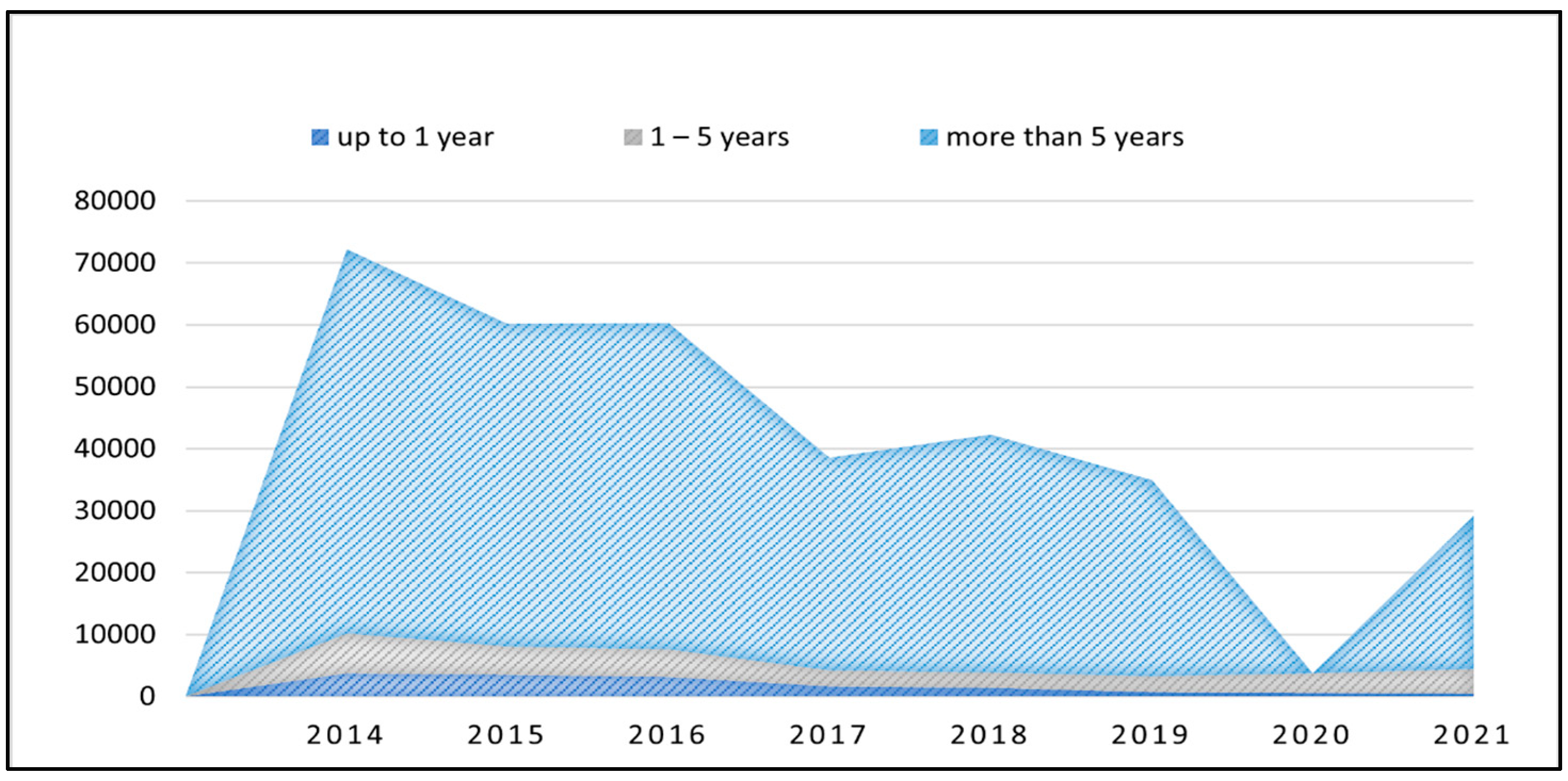

3. Data Analysis

4. Results

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Aggeek. 2020. Platforma AgriAnalytica Sproshchuie Dostup Fermeriv do Finansuvannia. November 16. Available online: https://aggeek.net/ru-blog/platforma-agrianalytica-sproschue-dostup-fermeriv-do-finansuvannya (accessed on 15 January 2023).

- Agribusiness Today. 2020. Ahrarna Ipoteka: Fermery, Banky y Derzhava u Poshukakh Spilnoho Znamennyka. December 1. Available online: http://agro-business.com.ua/agro/ekspertna-dumka/item/19693 (accessed on 25 January 2023).

- Agropolit. 2017. Land Reform of the New EU Member States Is the Experience of Poland. March 16. Available online: https://agropolit.com/spetsproekty/254-zemelna-reforma-novih-krayin-chleniv-yes-dosvid-polschi (accessed on 1 February 2023).

- Aleinikova, Olena V., Oleksandr I. Datsii, Iryna I. Kalina, Anastasiia A. Zavgorodnia, Yuliia O. Yeremenko, and Vitalii S. Nitsenko. 2023. Digital technologies as a reason and tool for dynamic transformation of territory marketing. Naukovyi Visnyk Natsionalnoho Hirnychoho Universytetu 1: 154–59. [Google Scholar] [CrossRef]

- Aleskerova, Yuliia, Oksana Radchenko, and Volodymyr Todosiichuk. 2018. Credit aspects of state support development of agricultural sector of ukraine. Economy, Finances, Management: Topical Issues of Science and Practical Activity 11: 84–94. [Google Scholar]

- Alessandrini, Pietro, Luca Papi, and Alberto Zazzaro. 2003. Banks, regions and development. PSL Quarterly Review 56: 23–55. [Google Scholar] [CrossRef]

- Bakhur, Nadiia. 2020. The influence of the institutional environment on development of investment activity in the agricultural sector of the economy. University Economic Bulletin 46: 7–20. [Google Scholar] [CrossRef]

- Balanovska, Tetiana, Olga Gogulya, Krystyna Dramaretska, Volodymyr Voskolupov, and Viktoriia Holik. 2021. Using Marketing Management to Ensure Competitiveness of Agricultural Enterprises. Agricultural and Resource Economics: International Scientific E-Journal 7: 142–61. [Google Scholar] [CrossRef]

- Berazneva, Julia, and David R. Lee. 2013. Lee Explaining the African food riots of 2007–2008: An empirical analysis. Food Policy 39: 28–39. [Google Scholar] [CrossRef]

- BMEL. 2020. Bundesministerium für Ernährung und Landwirtschaft. Von Besondere Ernte- und Qualitätsermittlung (BEE) 2019. Available online: https://www.bmel.de/SharedDocs/Downloads/DE/Broschueren/besondere (accessed on 21 January 2023).

- de Sousa Nóia Júnior, Rogério, Frank Ewert, Heidi Webber, Pierre Martre, Thomas W. Hertel, Martin K. van Ittersum, and Senthold Asseng. 2022. Senthold Asseng, Needed global wheat stock and crop management in response to the war in Ukraine. Global Food Security 35: 100662. [Google Scholar] [CrossRef]

- Dvigun, Alla, Oleksandr Datsii, Nataliia Levchenko, Ganna Shyshkanova, and Ruslan Dmytrenko. 2022. Rational Use of Fresh Water as a Guarantee of Agribusiness Development in the Context of the Exacerbated Climate Crisis. Science and Innovation 18: 85–99. [Google Scholar] [CrossRef]

- Dziamulych, Mykola, Tetiana Shmatkovska, Antonina Gordiichuk, Myroslava Kupyra, and Tetiana Korobchuk. 2020. Estimating peasant farms income and the standard of living of a rural population based on multi-factorial econometric modeling: A case study of Ukraine. Scientific Papers. Management, Economic Engineering in Agriculture and Rural Development 20: 199–206. Available online: https://managementjournal.usamv.ro/pdf/vol.20_1/Art27.pdf (accessed on 20 January 2023).

- European Fund for Southeast Europe. 2019. Potential for Agricultural Finance in Ukraine. Available online: http://www.efse.lu (accessed on 25 January 2023).

- Fenyves, Veronika, Tibor Tarnóczi, and Kinga Zsidó. 2015. Financial Performance Evaluation of agricultural enterprises with DEA Method. Procedia Economics and Finance 32: 423–31. [Google Scholar] [CrossRef]

- Guk, Olga, Hanna Mokhonko, and Lina Shenderivska. 2021. Investment trends in Ukraine. Economics and Society, 29. [Google Scholar] [CrossRef]

- IFC. 2019. International Finance Corporation. Von Tomorrow’s Harvests Fund Today’s Investments in Ukrainian Farms. Available online: https://www.ifc.org/wps/wcm/connect/news_ext_content/ifc_ (accessed on 15 January 2023).

- Jansson, Kristina Hedman, Chelsey Jo Huisman, Carl Johan Lagerkvist, and Ewa Rabinowicz. 2013. Agricultural Credit Market Institutions A Comparison of Selected European Countries. Factor Markets Working Paper 33: 30. Available online: https://www.ceps.eu/wp-content/uploads/2013/01/FM%20WP33%20Credit%20Market%20Institutions.pdfhttp://ageconsearch.umn.edu/ (accessed on 23 January 2023).

- JSC CB Privatbank. 2022. Ipotechni kredyty. Ofitsiinyi sait. Available online: https://privatbank.ua/ (accessed on 15 January 2023).

- JSC Credit Agricole Bank. 2022. Ipotechni kredyty. Ofitsiinyi sait. Available online: https://credit-agricole.ua (accessed on 15 January 2023).

- JSC Kredobank. 2022. Ipotechni kredyty. Ofitsiinyi sait. Available online: https://kredobank.com.ua (accessed on 15 January 2023).

- JSC Raiffeisen Bank Aval. 2022. Ipotechni kredyty. Ofitsiinyi sait. Available online: https://www.aval.ua (accessed on 15 January 2023).

- JSC Ukreximbank. 2022. Ipotechni kredyty. Ofitsiinyi sait. Available online: https://www.eximb.com (accessed on 15 January 2023).

- JSC Ukrsibbank. 2022. Ipotechni kredyty. Ofitsiinyi sait. Available online: https://my.ukrsibbank.com/ (accessed on 15 January 2023).

- Kharchuk, Svitlana. 2020. State of investment activity of enterprises of Ukraine in conditions of economic instability. Ekonomika ta derzhava 1: 66–72. [Google Scholar] [CrossRef]

- Kolesnik, Ya. V. 2016. Statistical approaches to the evaluation of business reputation of banks. Ukraine statistics 4: 27–32. [Google Scholar]

- Kramar, Iryna, Olena Panukhnyk, and Nataliia Marynenko. 2015. Trends of foreign direct investment in Ukrainian economy. Actual Problems of Economics 170: 76–82. [Google Scholar]

- Kucher, Lesia, Anatolii Kucher, Hanna Morozova, and Yulia Pashchenko. 2022. Development of circular agricultural economy: Potential sources of financing innovative projects. Agricultural and Resource Economics: International Scientific E-Journal 8: 206–27. [Google Scholar] [CrossRef]

- Kvasha, Serhii, Liubov Pankratova, Viktor Koval, and Rima Tamošiūnienė. 2019. Illicit financial flows in export operations with agricultural products. Intelellectual Economics 13: 195–209. [Google Scholar] [CrossRef]

- Lehkostup, Ihor, and Nataliia Sainchuk. 2022. Current state of investment activity in Ukraine: Domestic and international aspects. Economics and Society, 46. [Google Scholar] [CrossRef]

- Lemishko, Olena, and Natalie Shevchenko. 2021. Lending in the agricultural sector of Ukraine: Challenges and solutions. Economic Annals 192: 74–87. [Google Scholar] [CrossRef]

- Loiko, Valeryia, and Tatiana Bashkyrtseva. 2018. Innovations as a Power of Banking Activity. European Scientific Journal of Economic and Financial Innovation 1: 67–76. [Google Scholar] [CrossRef]

- Marqués-Pérez, Inmaculada, Inmaculada Guaita-Pradas, and José-Luis Pérez-Salas. 2017. Discounting in agro-industrial complex. A methodological proposal for risk premium. Spanish Journal of Agricultural Research 15: e0105. [Google Scholar] [CrossRef]

- Mihaylenko, O., and N. Krasnikova. 2020. Influence of foreign investments on the development of the economy of Ukraine under the conditions of globalization. Efektyvna ekonomika, 7. [Google Scholar] [CrossRef]

- Minfin. 2022. Reitynh stiikosti bankiv za pidsumkamy 2 kvartalu 2022. October 1. Available online: https://minfin.com.ua/ua/banks/rating/ (accessed on 18 January 2023).

- Ministry of Agrarian Policy and Food of Ukraine. 2021. Derzhpidtrymka -2021. Available online: https://minagro.gov.ua/news/derzhpidtrimka-2021-uryad-vidnoviv-pidtrimku-subyektiv-gospodaryuvannya-apk (accessed on 24 January 2023).

- Miuller, Viktoriia. 2020. Analiz finansuvannia silskoho hospodarstva v Ukraini. Ahropolitychnyi zvit. Kyiv, Ukraine. Available online: https://www.apd-ukraine.de/images/2020/APD_Berichte_2020/11_Landwirtschaftsfinanzierungen/Bericht_Mueller_Landwirtschaftsfinanz_APD_UKR.pdfhttps://www.apd-ukraine.de/images/2020 (accessed on 26 January 2023).

- Mohd Thas Thaker, Hassanudin, Ahmad Khaliq Khaliq, K Chandra Sakaran Sakaran, and Mohamed Asmy Mohd Thas Thaker Mohd Thas Thaker. 2020. A discourse on the potential of crowdfunding and Islamic finance in the agricultural sector of East Java, Indonesia. Jurnal Ekonomi & Keuangan Islam 6: 10–23. [Google Scholar] [CrossRef]

- National Bank of Ukraine. 2022. Monetary Statistics. Loans Provided by Deposit-Taking Corporations. Statistical Bulletin. Available online: https://bank.gov.ua (accessed on 15 January 2023).

- Nehoda, Yuliia, Olena Zharikova, and Tetyana Grebenyuk. 2022. Mortgage lending market: Problems and development prospects. Political Science and Security Studies Journal 3: 26–37. [Google Scholar] [CrossRef]

- Nickerson, David. 2022. Credit Risk, Regulatory Costs and Lending Discrimination in Efficient Residential Mortgage Markets. Journal of Risk and Financial Management 15: 197. [Google Scholar] [CrossRef]

- Nitsenko, Vitalii. 2020. Mismanagement in Ukraine. Problems of Management in the 21st Century 15: 4–8. [Google Scholar] [CrossRef]

- Nitsenko, Vitalii S., and Valerii I. Havrysh. 2016. Enhancing the stability of a vertically integrated agro-industrial companies in the conditions of uncertainty. Actual Problems of Economics 10: 167–72. [Google Scholar]

- Perevozova, I. V., O. H. Bodnarchuk, O. I. Bodnarchuk, and A. S. Politova. 2019. Normative and Legal Aspects Of Banking Regulation And Ensuring The Reliability Of Banking System Of Ukraine. Financial and Credit Activity Problems of Theory and Practice 1: 26–35. [Google Scholar] [CrossRef]

- Perez, Ines. 2013. Climate Change and Rising Food Prices Heightened Arab Spring. Scientific American. Available online: https://www.scientificamerican.com/article/climate-change-and-rising-food-prices-heightened-arab-spring/ (accessed on 23 January 2023).

- Saaty, Thomas L. 1990. Multicriteria decision making—The analytic hierarchy process. European Journal of Operational Research 48: 9–26. [Google Scholar] [CrossRef]

- Sallach, David L. 1972. Systems Analysis and Sociological Theory. Sociological Focus 5: 54–60. [Google Scholar] [CrossRef]

- Samotoenkova, Olena. 2019. An investment activeity of Ukraine: Trends and prospects. Efektyvna Ekonomika 5. [Google Scholar] [CrossRef]

- Sarkis, Joe. 2007. Preparing Your Data for DEA. In Modeling Data Irregularities and Structural Complexities in Data Envelopment Analysis. Edited by Joe Zhu and Wade D. Cook. Boston: Springer, pp. 305–20. [Google Scholar] [CrossRef]

- Schierhorn, Von Florian, Daniel Müller, and Max Hofmann. 2018. Der Klimawandel gefährdet den boomenden Getreidesektor in der Ukraine. Ukraine-Analysen 210: 2–6. [Google Scholar] [CrossRef]

- Seven, Unal, and Semih Tumen. 2020. Agricultural Credits and Agricultural Productivity: Cross-Country Evidence von Agricultural Credits and Agricultural Productivity: Cross-Country Evidence Seite 4. GLO Discussion Paper No. 439. Essen: Global Labor Organization (GLO). Available online: https://poseidon01.ssrn.com/delivery.php?ID (accessed on 20 January 2023).

- Shevchenko, Liliia. 2019. Economic methods for managing foreign investments in Ukrainian economy. Entrepreneurship and Innovation 10: 9–16. [Google Scholar] [CrossRef]

- Sirant, Myroslava, Liliia Yarmol, Oksana Baik, Iryna Andrusiak, and Nataliia Stetsyuk. 2022. State policy of Ukraine in the sphere of environmental protection in the context of european integration. Naukovyi Visnyk Natsionalnoho Hirnychoho Universytetu 2: 107–11. [Google Scholar] [CrossRef]

- Sodoma, Ruslana, Oksana Agres, Olha Havryliuk, and Kateryna Melnyk. 2019. Mortgage lending in the agricultural economy: Opportunities and risks. Financial and Credit Activity. Problems of Theory and Practice 1: 225–33. [Google Scholar] [CrossRef]

- Storozhuk, Vitaly, Syman Jurk, and Volker Sasse. 2019. APD: Der Agrarsektor der Ukraine und Deutschlands: Fakten und Kommentare. Available online: https://www.apd-ukraine.de/images/2019/Fact_sheets_2019/factsheets_deu_6._Ausgabe_DEU.pdfhttps://www.apd (accessed on 20 January 2023).

- Studinska, Galina, and Viachesla Prosov. 2020. Assessment of the level of Ukrainian mortgage market development. University Economic Bulletin 46: 160–69. [Google Scholar] [CrossRef]

- Tretiak, A. M., V. M. Tretiak, and A. S. Polishchuk. 2021. Peculiarities of estimating the cost of agricultural land use in land mortgageOsoblyvosti otsinky vartosti silskohospodarskoho zemlekorystuvannia v zemelnii ipotetsi. Ahrosvit 7–8: 10–16. [Google Scholar] [CrossRef]

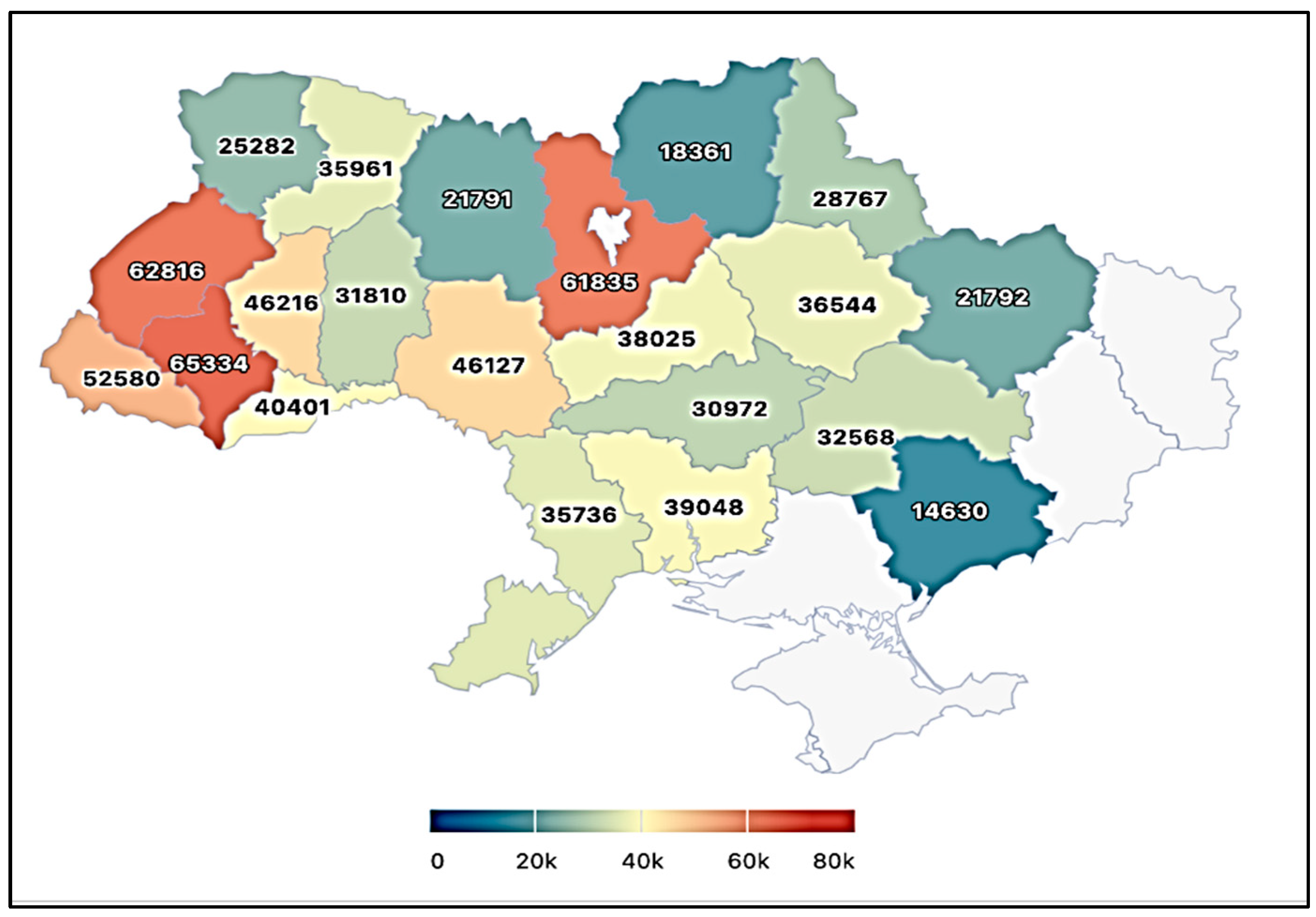

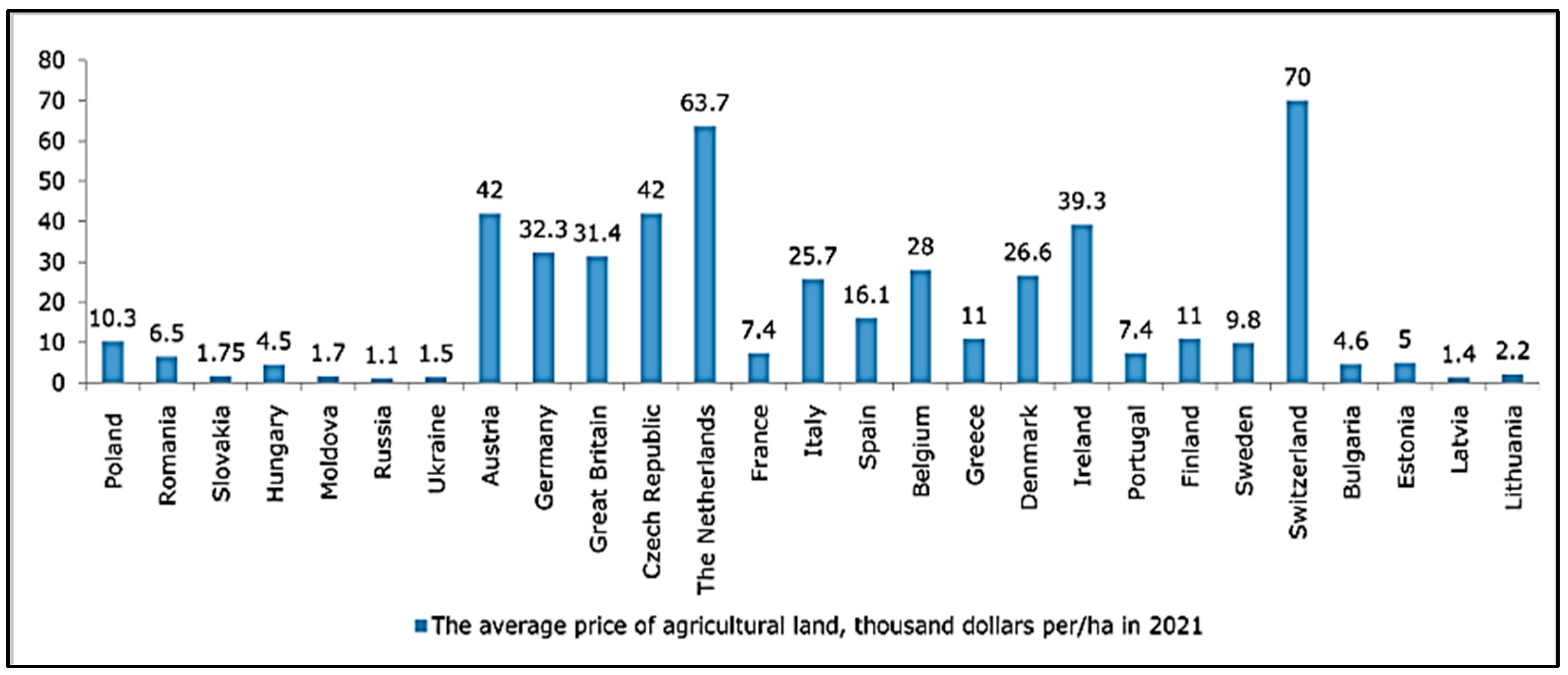

- UNIAN. 2022. Information Agency. Rynok zemli v umovakh viiny: Skilky koshtuie hektar u riznykh rehionakh Ukrainy (infohrafika). November 7. Available online: https://www.unian.ua/economics/agro/skilki-koshtuye-gektar-zemli-v-ukrajini-infografika-po-oblastyah-12037563.html (accessed on 15 January 2023).

- Van Mol, Christof, and Helga de Valk. 2016. Migration and Immigrants in Europe: A Historical and Demographic Perspective. In Integration Processes and Policies in Europe. IMISCOE Research Series. Edited by Blanca Garcés-Mascareñas and Rinus Penninx. Cham: Springer, pp. 31–55. [Google Scholar] [CrossRef]

- Verkhovna Rada of Ukraine. 2002. Land Code of Ukraine. The Official Bulletin of the Verkhovna Rada of Ukraine 3–4: 27. [Google Scholar]

- Verkhovna Rada of Ukraine. 2021. Pro Fond chastkovoho harantuvannia kredytiv u silskomu hospodarstvi. No. 1865-IX. Law of Ukraine. Available online: https://zakon.rada.gov.ua/laws/show/1865-20#Text (accessed on 15 January 2023).

- Westercamp, Christine, Miryam Nouri, and André Oertel. 2015. Agricultural Credit: Assessing the Use of Interest Rate Subsidies. AFD Sustainable Development Department, 165. Available online: https://www.afd.fr/sites/afd/files/imported-files/29-VA-A-Savoir.pdf (accessed on 25 January 2023).

- Wigier, Marek, Barbara Wieliczko, and Jozsef Forgarasi. 2014. Impact of Investment Support on Hungarian and Polish Agriculture. Paper prepared at the 142nd EAAE Seminar Growing Success? Agriculture and Rural Development in an Enlarged EU, Budapest, Hungary, May 29–30. [Google Scholar] [CrossRef]

- Yazliuk, Borys, Olena Dombrovska, and Andriy Butov. 2020. Analysis of Factors Affecting the Development of Mortgage Relations in Ukraine. Ukrainian Journal of Applied Economics 5: 70–79. [Google Scholar] [CrossRef]

- Zaverbnyj, Andrii. 2021. Problems and prospects of investment support of Ukrainian enterprises under European integration conditions. Management and Entrepreneurship in Ukraine: Stages of Formation and Development Problems 3: 153–60. [Google Scholar] [CrossRef]

- Zayed, Nurul Mohammad, Isse Sudi Mohamed, Khan Mohammad Anwarul Islam, Iryna Perevozova, Vitalii Nitsenko, and Olena Morozova. 2022. Factors Influencing the Financial Situation and Management of Small and Medium Enterprises. Journal of Risk and Financial Management 15: 554. [Google Scholar] [CrossRef]

- Zharikova, Olena, and Kateryna Cherkesenko. 2021. Integration of banks and insurance companies activities in Ukraine. Journal of Scientific Papers «Social Development and Security» 11: 42–57. [Google Scholar] [CrossRef]

- Zharikova, Olena, and Oksana Pashchenko. 2018. Increasing the competitiveness of Ukrainian dairy products in line with European standards. International Journal of Scientific and Technological Research 4: 435–41. Available online: https://www.iiste.org/Journals/index.php/JSTR/article/view/45486/46970/ (accessed on 14 January 2023).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Criteria | Units of Measurement | Alternatives | ||

|---|---|---|---|---|

| K1 | Position in the rating of banks | Rating estimate | A1 | Bank 1 |

| K2 | Bank reputation | Points | A2 | Bank 2 |

| K3 | Lending limit | UAH | A3 | Bank 3 |

| K4 | Lending period | Months | A4 | Bank 4 |

| K5 | Interest rates | % | ||

| K6 | The convenience of using bank services | Rating estimate | ||

| Name of State Support | Amount of Funds Received, UAH | Number of Recipients |

|---|---|---|

| 2019 | ||

| State support for the livestock industry | 2,433,576,120 | 1179 |

| State support of the hops, berries, and orchards industry | 397,878,900 | 210 |

| Provision of loans to farms | 225,083,000 | 595 |

| Financial support in the agricultural sector by making loans cheaper | 449,872,336 | 966 |

| Financial support for the development of farming | 420,446,654 | 5944 |

| Financial support for agricultural producers | 640,793,815 | 4315 |

| 2020 | ||

| Financial support for the development of farming | 65,566,900 | 176 |

| Financial support for agricultural producers | 3,965,818,473 | 11,538 |

| 2021 | ||

| Financial support for the development of farming | 50,000,000 | 127 |

| Financial support for agricultural producers | 4,662,394,874 | 11,198 |

| Bank | Type of Loan Product | Lending Limit | Lending Term | Interest Rate % |

|---|---|---|---|---|

| JSC Raiffeisen Bank Aval | Overdraft | UAH 4,500,000 | 36 months | 18.45–20.45% |

| Credit line | UAH 37,000,000 | 18 months | 13–14% | |

| Partnership programs | UAH 37,300,000 | 60 months | up to 14.5% | |

| Investment loan for the purchase of agricultural machinery and equipment | UAH 37,300,000 | 60 months | 18.5–20.0% | |

| JSC UkrSybbank | Current activity of agricultural business | UAH 5,000,000 | 12 months | Up to 8.5% |

| Agrocredit “Investing” | Advance payment from 30% | Up to 60 months fixed assets, Up to 36 months corporate rights | Hryvnia—from 11.40% US dollar—from 5.95% Euro—from 5.20% | |

| JSC Ukreximbank | Agrocredit “Investing” | Advance payment from 30% | Real estate, corporate rights—up to 60 months Other purposes—up to 36 months | Hryvnia—from 11.40% US dollar—from 5.95% Euro—from 5.20% |

| Agrocredit “Agricultural machinery” | 15% and more—for new agricultural machinery 20% and more—for other agricultural machinery | New agricultural machinery—up to 7 years Other agricultural machinery—up to 5 years | Hryvnia—from 11.40% US dollar—from 5.95% Euro—from 5.20% | |

| JSC “Credit Agricole Bank” | Lending for business development | Up to 75%—collateral property—object of lending Up to 90% other property | Up to 60 months—fixed assets | Hryvnia—15% US dollar—6.5% Euro—5.5% |

| Financing the purchase of agricultural machinery (equipment) | X | Up to 60 months—fixed assets | Hryvnia—15% US dollar—6.5% Euro—5.5% | |

| JSC CB “Pryvatbank” | Credit line “Agroseason” | From UAH 500,000 | 36 months | 17% per annum |

| Loan for the purchase of fixed assets | From UAH 100,000 | 1–3 years | UIRD + 7% per annum or from 0% per annum | |

| Leasing of agricultural machinery | From UAH 300,000 to 5 million | 5 years | From 0.01% per annum | |

| JSC “Kredobank” | Agricultural machinery for small- and medium-sized businesses | Unlimited, advance payment from 10% | Up to 60 months | Hryvnia—13.75% US dollar—6.0% Euro—4.5% |

| Agricultural investment | Unlimited, advance payment from 30% | Up to 84 months | Hryvnia—13.75% US dollar—6.0% Euro—4.5% |

| Priority Vectors | Global Priority (GP) | ||||||

|---|---|---|---|---|---|---|---|

| K1 | K2 | K3 | K4 | K5 | K6 | ||

| 0.444 | 0.027 | 0.100 | 0.049 | 0.152 | 0.228 | ||

| Bank 1 | 0.355 | 0.143 | 0.085 | 0.110 | 0.424 | 0.085 | 0.259 |

| Bank 2 | 0.067 | 0.046 | 0.291 | 0.037 | 0.103 | 0.290 | 0.144 |

| Bank 3 | 0.534 | 0.669 | 0.042 | 0.427 | 0.050 | 0.042 | 0.297 |

| Bank 4 | 0.044 | 0.143 | 0.582 | 0.427 | 0.424 | 0.582 | 0.300 |

| Total | 1.00 | ||||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Perevozova, I.; Malynka, O.; Nitsenko, V.; Kryshtal, H.; Kostiuk, V.; Mishchenko, V. Analysis of Trends in Mortgage Lending in the Agricultural Sector of Ukraine. J. Risk Financial Manag. 2023, 16, 255. https://doi.org/10.3390/jrfm16050255

Perevozova I, Malynka O, Nitsenko V, Kryshtal H, Kostiuk V, Mishchenko V. Analysis of Trends in Mortgage Lending in the Agricultural Sector of Ukraine. Journal of Risk and Financial Management. 2023; 16(5):255. https://doi.org/10.3390/jrfm16050255

Chicago/Turabian StylePerevozova, Iryna, Oksana Malynka, Vitalii Nitsenko, Halyna Kryshtal, Viktoriia Kostiuk, and Vitaliia Mishchenko. 2023. "Analysis of Trends in Mortgage Lending in the Agricultural Sector of Ukraine" Journal of Risk and Financial Management 16, no. 5: 255. https://doi.org/10.3390/jrfm16050255