Assessing the Feasibility of Global Long-Term Mitigation Scenarios

, , , ,

, , , ,

Abstract

:1. Introduction

- Constraints using newly-derived CO2 budgets from Met Office Hadley Centre;

- Model inter-comparison using population and economic growth assumptions from one of the new shared socio-economic pathways (SSP2) [3];

- Production of a database of scenarios which allows key metrics (fossil share of primary energy, electricity share of final energy, mitigation costs, CO2 sequestered) to be shown in a stepwise manner when moving between different temperature targets, different levels of delay (to 2020, to 2030) and different technology constraints. This goes further than what the IPCC 5th assessment database allows (as that focuses primarily on 2 and 2.5 °C scenarios, including a particular lack of sampling in the range 2.5–3.5 °C [4]);

- Some new technology constraint scenarios (carbon capture and storage (CCS) only available for deployment from 2050, as opposed to no CCS which has been widely explored in the IPCC’s 5th assessment, and constrained electrification of end-use sectors, which has not yet been explored).

- Lack of mitigation options;

- Binding constraints for the diffusion of technologies;

- Extremely high price signals (such as rapid increases in carbon prices).

- Mitigation costs: The latest IPCC assessment report (WGIII) [5] has costs of mitigation for “idealised implementation” scenarios (achieving a range of atmospheric GHG concentrations of between 430 and 480 ppm CO2e of 1.5%–15% of Gross Domestic Product (GDP) (median = 3%, interquartile range 2%–6%) over the period 2015–2100 (Net Present Value, discounted at 5%).

- Carbon prices: For idealised implementation scenarios, carbon prices in the 430–480 ppm scenarios rise to between $100/tCO2e and $6000/tCO2e (median = $1500tCO2e, interquartile range $1000–2000/tCO2e) by 2100 [5].

- Model solution: As noted by the IPCC 5th assessment report [5], reported ranges may contain a downward bias towards costs of mitigation and carbon prices, since they only represent results for models that solve. Model solution has been discussed as a key facet of assessing the feasibility of low-carbon pathways [6,7], although as noted in Kriegler et al. [7], feasibility is subject to different interpretations around model solution, political actions or availability of any set of technologies or actions that could meet a target.

- Implications for idled high-carbon assets: International Energy Agency (IEA) [8] estimates that a 450 ppm scenario would result in $300 billion of stranded fossil fuel assets, and more if policy lacks clarity. Johnson et al. [9] show that, in a mitigation scenario aimed at achieving a 450 ppm GHG concentration following weak policy action to 2030, there would be on average 350 GW of stranded conventional coal plants over the period 2030–2050.

- Technology deployment rates: As demonstrated by van der Zwaan et al. [10], technology deployment rates between scenarios can highlight the degree of challenge of different scenario sets, with many hundreds of GW of key supply-side technologies such as nuclear, solar PV and wind deployed in least-cost low-carbon pathways—in many cases several multiples of historical deployment rates of these technologies.

- The degree of reliance on negative emissions and other specific technologies like CCS: Numerous studies have highlighted the degree of dependence of the cost-effectiveness of low-carbon pathways on the availability of CCS [6,11], with negative emissions (combining bio-energy with CCS) a key facet of achieving low-carbon pathways [12]

- Rates of decarbonisation and energy efficiency improvements: Rates of decarbonisation in low-carbon scenarios have been used to understand the degree of challenge associated with these scenarios, with high rates of decarbonisation (beyond 3.5% per year) having been asserted as “extreme” in Den Elzen et al.’s 2010 analysis [13], but far higher rates (beyond 10% per year) included in models deemed feasible in more recent analysis by Riahi et al. [6]. Economy-wide and sector-specific energy efficiency improvements have also been analysed in a range of low-carbon scenarios [5,14].

2. Materials and Methods

- The Centro Euro-Mediterraneo sui Cambiamenti Climatici (CMCC)’s WITCH model [30].

3. Results

3.1. Overview of Results

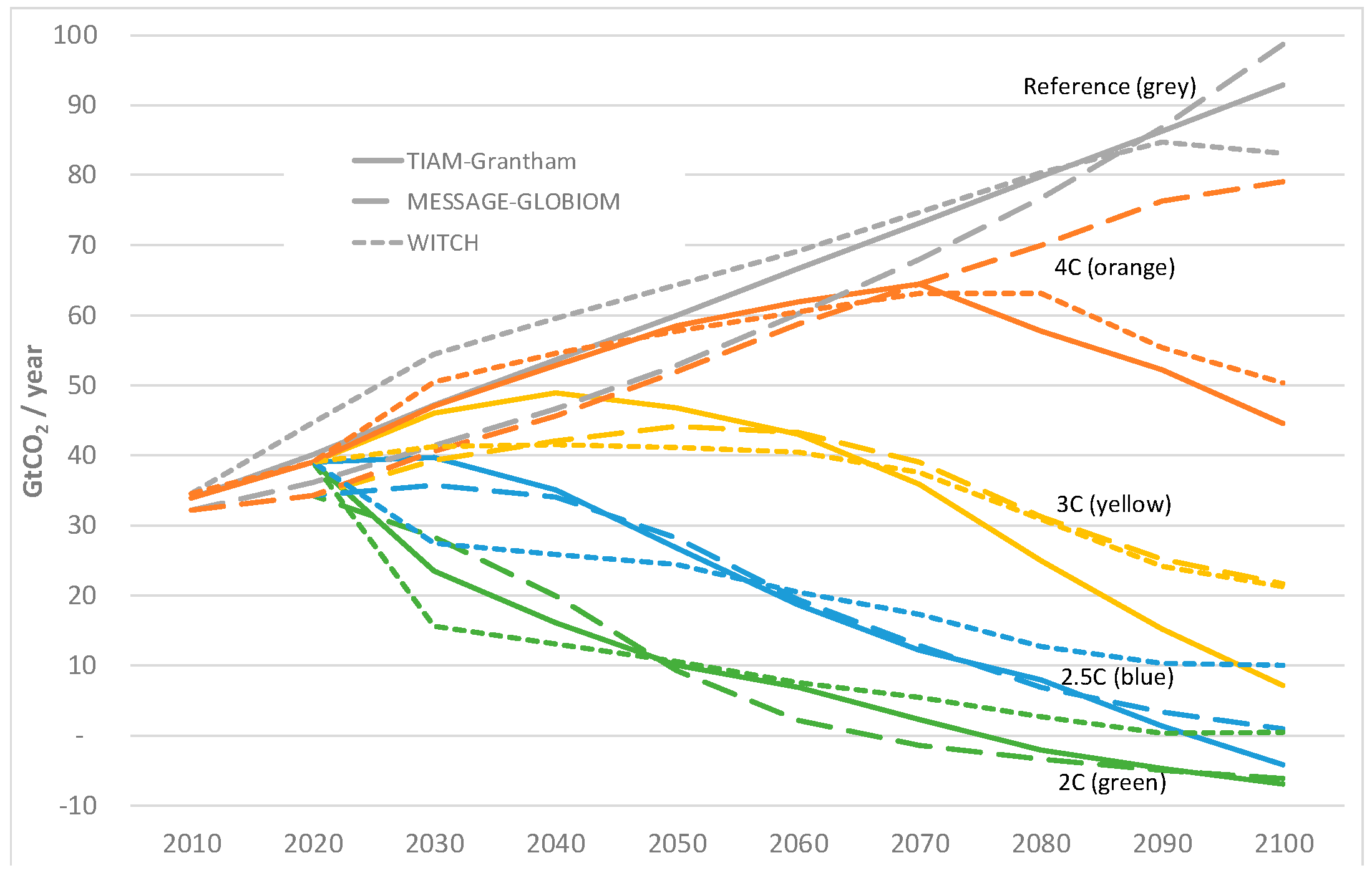

3.2. Can the Models Achieve the Different Temperature Goals?

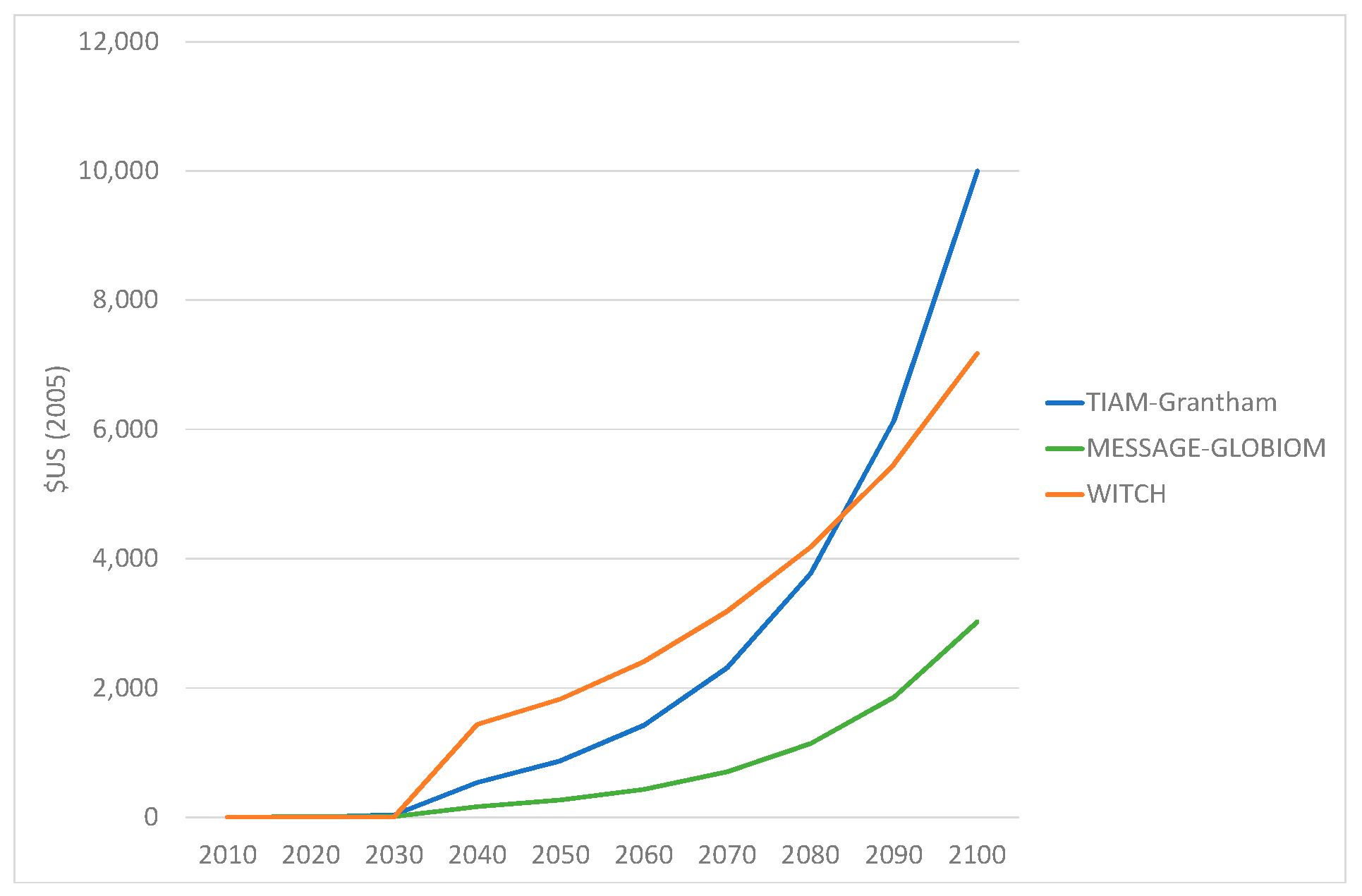

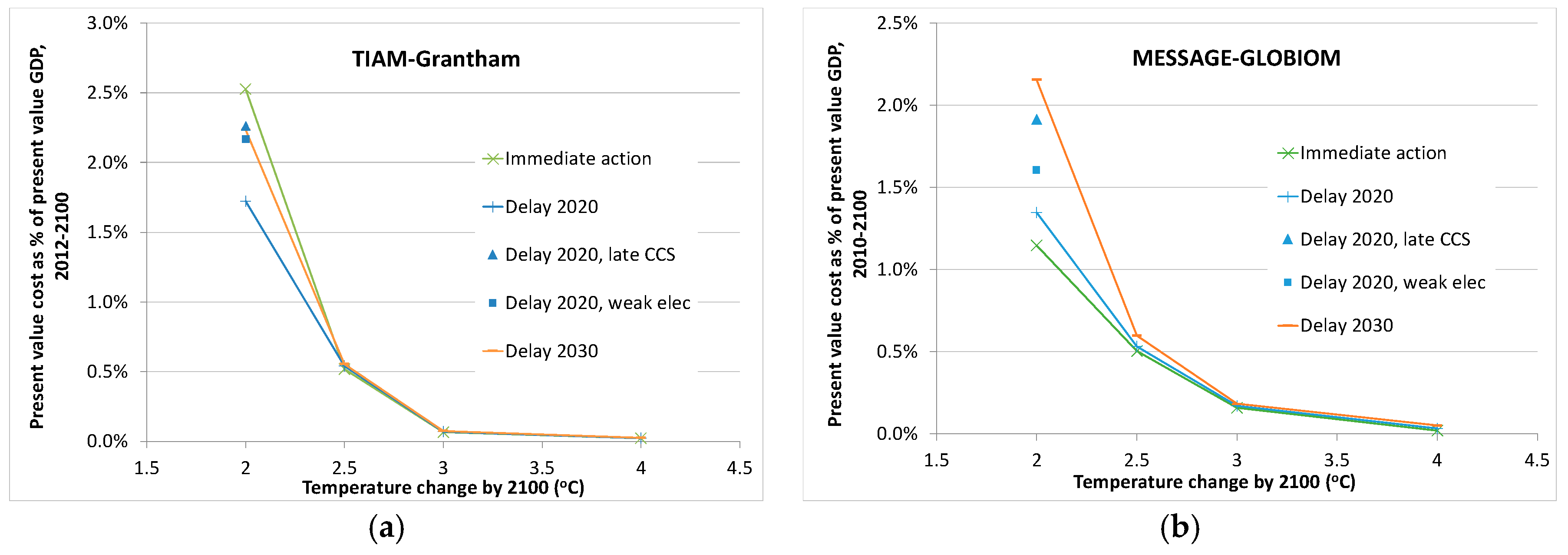

3.3. What is the Cost of Mitigation?

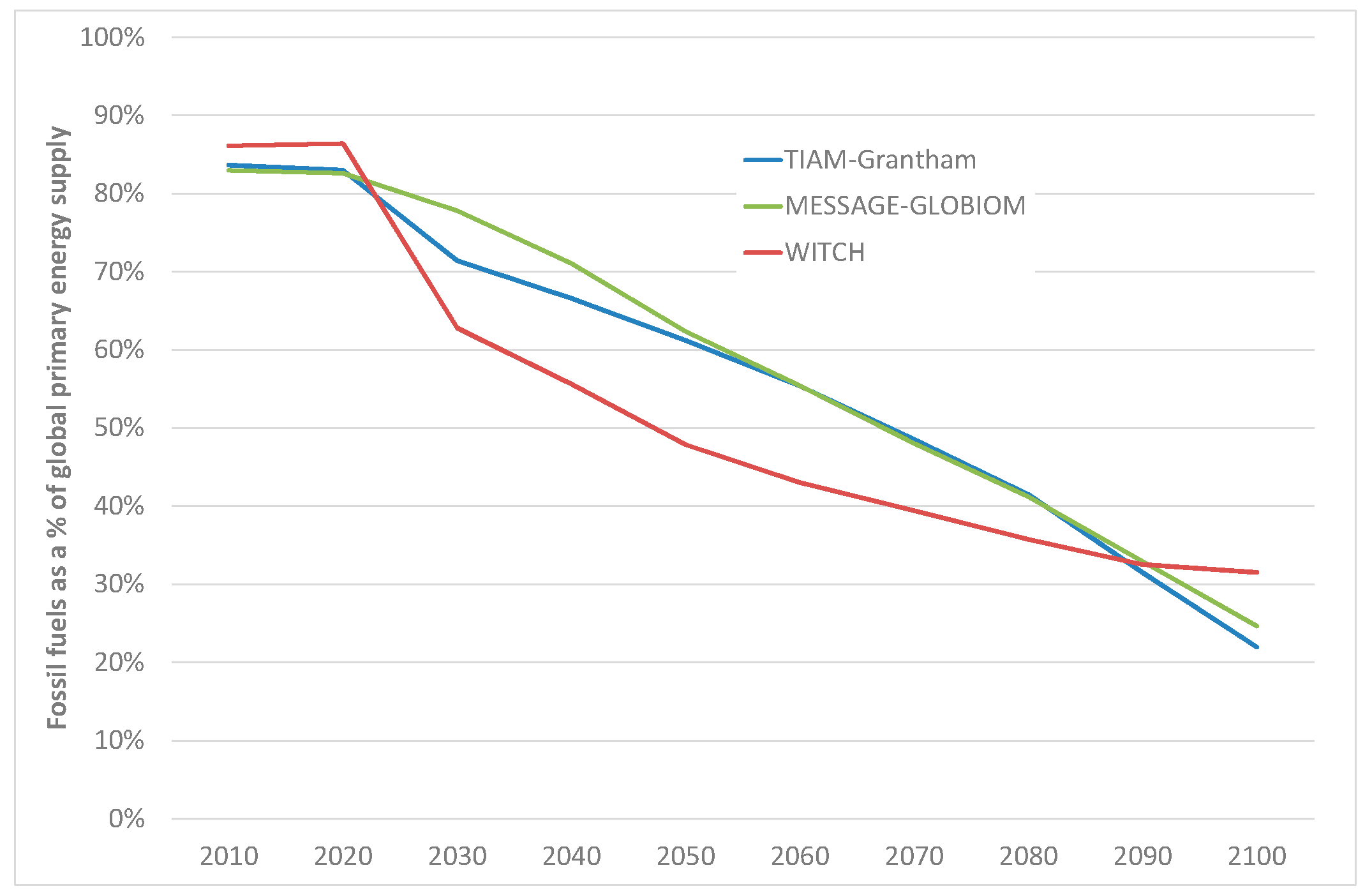

3.4. How Fast Does the Energy System Decarbonise?

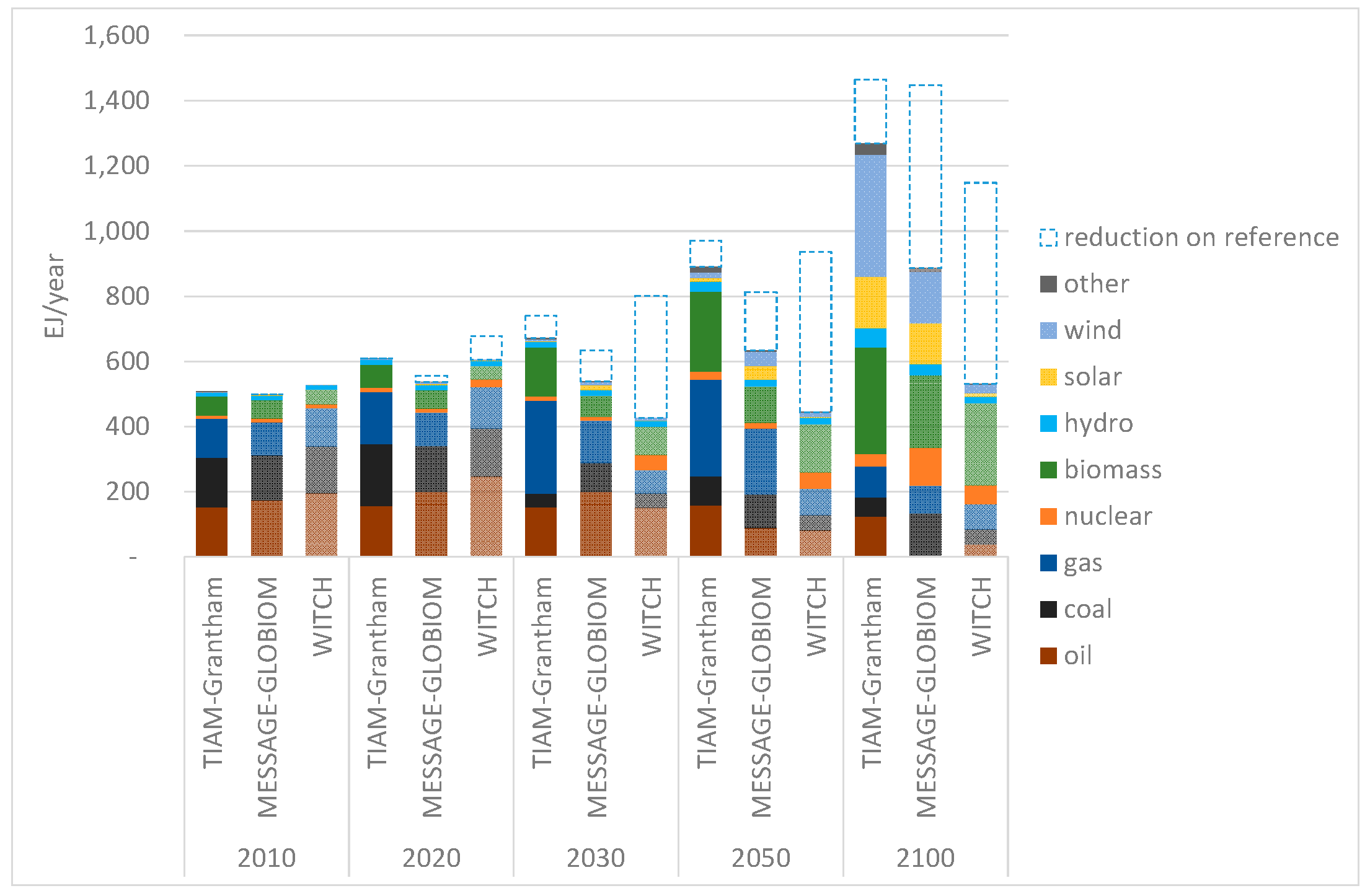

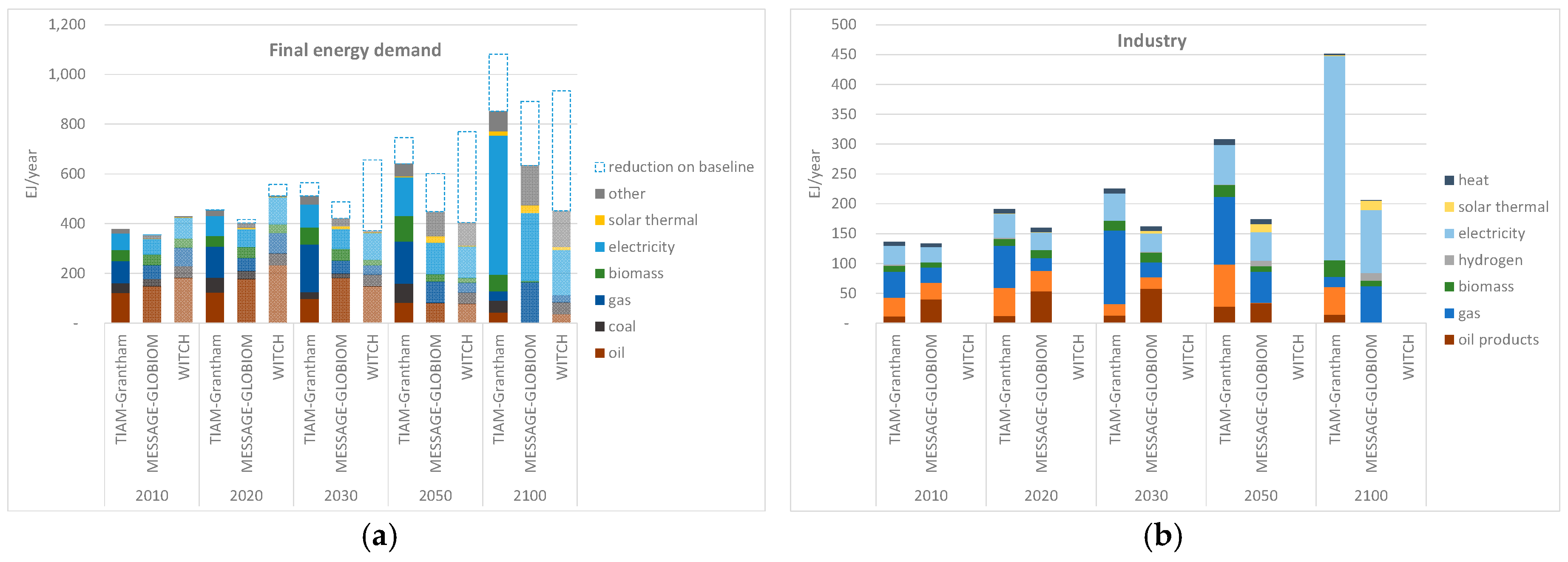

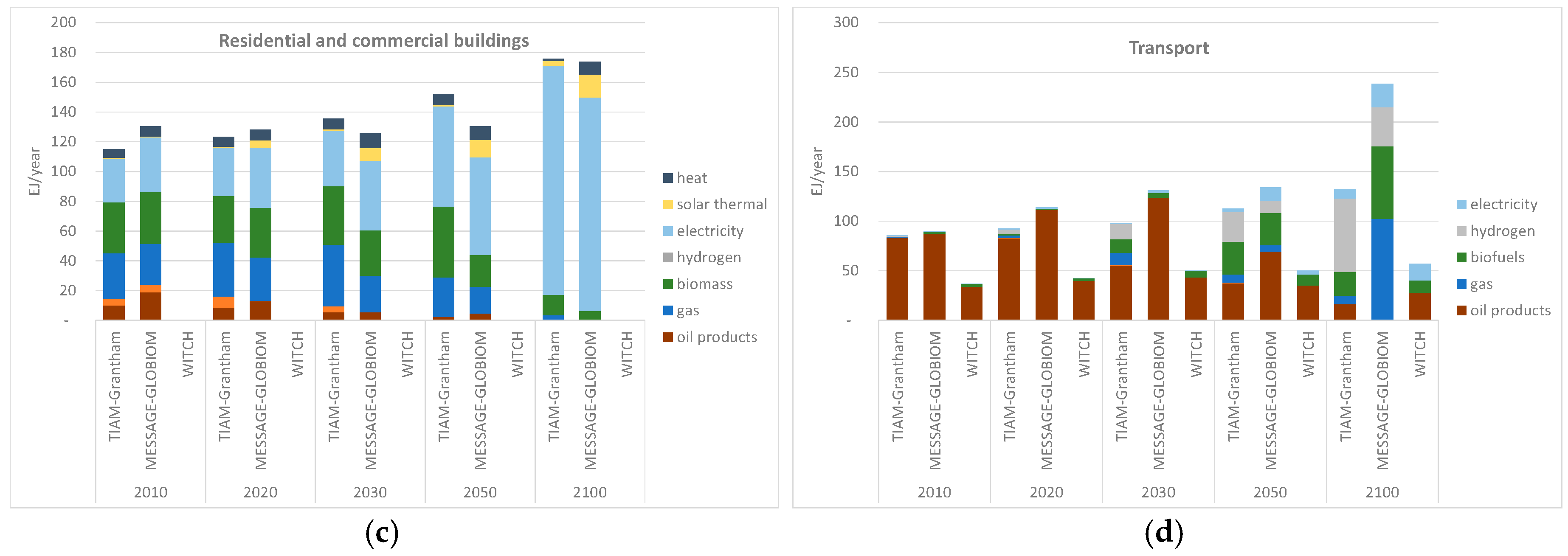

3.5. How Does the Energy System Change over the Century?

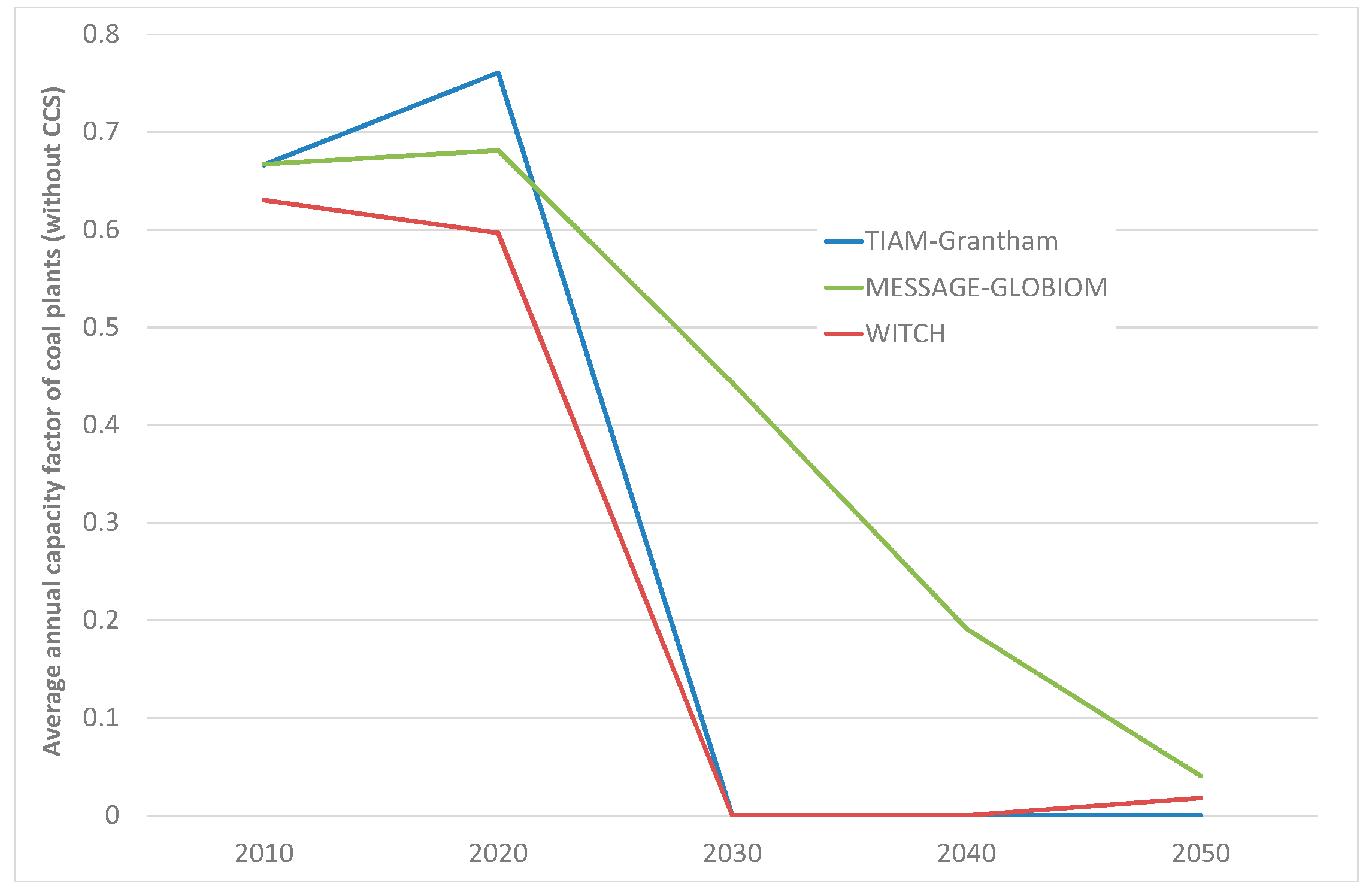

3.6. What Does Rapid Mitigation Imply for Coal-Fired Power Stations?

3.7. How Important is CO2 Capture in Achieving the Most Stringent Mitigation Scenarios?

3.8. A Matrix of Feasibility Indicators to Assess the Challenges of Different Mitigation Scenarios

4. Discussion

- Ensuring that mitigation action at a global level in line with the target begins as soon as possible, given the significant costs of delays, particularly to 2030, which implies the need for a ramping up of ambition over and above the currently submitted INDCs;

- Achieving sustained energy efficiency improvements over the course of the century and very rapid near-term improvements, which though technically feasible, would be unlikely to occur without very effective policies;

- Ensuring commercial-scale deployment of CCS is feasible as soon as technically and economically possible, such that hundreds of GW of CCS power stations can be deployed in the coming decades;

- Developing supply chains for other low-carbon technologies such as wind, biomass, solar and nuclear to ensure that hundreds of GW globally can be deployed each decade in the near future;

- Demonstrating the different aspects of BECCS technology and/or other negative emissions technologies so that global CO2 emissions can become first neutral and then net-negative in the latter half of the century;

- Increasing the penetration of electricity-using heating, transport and industrial process technologies throughout the end-use sectors;

- Managing the political economy issues that would be associated with the early idling of coal-fired power stations without CCS fitted.

Acknowledgments

Author Contributions

Conflicts of Interest

Appendix A. Regional CO2 Emissions in 2020 and 2030 for Moderate Action

- (1)

- Countries which have offered unilaterally to meet an absolute CO2 or GHG emissions reduction on a specified base year. The EU, for example, has pledged that its 2020 GHG emissions are 20% below 1990 levels by 2020. The 2020 emissions cap given such pledges is determined simply by taking the specified emissions reduction from the specified base year. In the case of the EU, unfortunately neither TIAM, WITCH nor MESSAGE represent the region distinctly, with countries spread over a Western and Eastern European region. As such, an assumption has been made that those countries in Western Europe would have a target of 25% below their 1990 value, whilst those in Eastern Europe would have a target of 5% below their 1990 level. This differentiation is in line with the effort share principles upon which the non-traded (i.e., non EU ETS) sectoral emissions target in the EU is distributed between Member States. The specific % reductions chosen follow from Croatia (an Eastern European country) having a target to achieve a 5% reduction on its 1990 emissions levels. The combination of the 25% Western European countries target with the 5% Eastern European countries target yields an average reduction across all EU28 countries of just less than 20%, so this simplified burden split is deemed an acceptable approximation.

- (2)

- Countries which have offered unilaterally to meet an emissions intensity reduction on a specified base year. This category applies to China and India, which have offered a 40% and 20% reduction on their 2005 emissions intensity respectively. The 2020 absolute emissions level under this weaker pledge is calculated by multiplying the 2005 absolute emissions level by the projected GDP growth over the period 2005–2020 (using SSP2 GDP projections) and then subtracting the specified % reduction.

- (3)

- Countries which have made a pledge based on capping emissions at a specified %age below a 2020 Business as Usual (BAU) level. Countries such as Brazil and Indonesia have made such pledges. In the case of these countries an appropriate BAU estimate is required. This has been calculated by first taking the 2005 emissions level, and then by applying a BAU emissions growth factor over the period 2005 to 2020. The latter factor has been derived from den Elzen et al. [56], which covers all GHG emissions and land use change (whereas this study is focused on energy and industrial CO2 only). Strictly speaking, the use of this factor could account for the fact that the economic growth projected in this study, using SSP2 figures, is different to that projected using den Elzen et al. [56]. However, many factors affect emissions growth, not just GDP, and so a simplifying assumption has been made to use the same factor.

- (4)

- Countries which have not made a pledge. This category applies to countries such as the USA, whose Cancun pledge is contingent on international action, and the majority of non-Annex I countries, who have stated qualitatively a series of nationally appropriate mitigation actions (NAMAs). In many cases, it makes most sense to simply not impose a cap on regions representing these countries—or combinations of these countries—in the TIAM, WITCH and MESSAGE models. However, in some cases regions represented by the models include a combination of countries form this category, and countries from other categories. In these cases a projection of BAU emissions for these countries is required, before emissions for the different countries within the region can be aggregated up to a regional estimate of 2020 emissions. As for category 3, this category of countries therefore requires an assumption of BAU emissions in 2020, and the 2005–2020 emissions growth factor derived from den Elzen et al. [56] has again been applied to 2005 emissions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country/Region | Weak Pledge | Strong Pledge |

|---|---|---|

| Australia | GHG 5% below 2000 by 2020 | GHG 25% below 2000 by 2020 |

| Belarus | Emissions 5% below 1990 by 2020 | Emissions 10% below 1990 by 2020 |

| Canada | None | GHG 17% below 2005 by 2020 |

| Croatia | Emissions 5% below 1990 by 2020 | Emissions 5% below 1990 by 2020 |

| EU | GHG 20% below 1990 by 2020 | GHG 30% below 1990 by 2020 |

| Iceland | GHG 15% below 1990 by 2020 | GHG 30% below 1990 by 2020 |

| Japan | None | GHG 25% below 1990 by 2020 |

| Kazakhstan | 15% below 1992 | GHG 25% below 1990 by 2020 |

| New Zealand | GHG 10% below 1990 by 2020 | GHG 20% below 1990 by 2020 |

| Norway | GHG 30% below 1990 by 2020 | GHG 40% below 1990 by 2020 |

| Russian Federation | GHG 15% below 1990 by 2020 | GHG 25% below 1990 by 2020 |

| Switzerland | GHG 20% below 1990 by 2020 | GHG 30% below 1990 by 2020 |

| Ukraine | GHG 15% below 1990 by 2020 | GHG 20% below 1990 by 2020 |

| USA | None | GHG 17% below 2005 by 2020 |

| Country/Region | Weak Pledge | Strong Pledge |

|---|---|---|

| Brazil | GHG 36.1% below 2020 BAU by 2020 | GHG 38.9% below 2020 BAU by 2020 |

| Chile | GHG 20% below 2020 BAU by 2020 | GHG 20% below 2020 BAU by 2020 |

| China | GHG intensity 40% below 2005 in 2020 | GHG intensity 45% below 2005 in 2020 |

| India | CO2 intensity 20% below 2005 levels in 2020 | CO2 intensity 25% below 2005 levels in 2005 |

| Indonesia | None | GHG 26% below 2020 BAU by 2020 |

| Israel | GHG 20% below 2020 BAU by 2020 | GHG 20% below 2020 BAU by 2020 |

| Mexico | None | GHG 30% below 2020 BAU by 2020 |

| Papua New Guinea | None | GHG 50% lower by 2030 |

| South Korea | GHG 30% below 2020 BAU by 2020 | GHG 30% below 2020 BAU by 2020 |

| Rep of Moldova | GHG 25% below 1990 by 2020 | GHG 25% below 1990 by 2020 |

| Singapore | None | GHG 16% below 2020 BAU by 2020 |

| South Africa | None | GHG 34% below 2020 BAU by 2020 |

| Study | 2020 Global Emissions from Fossil Fuels and Industry | 2030 Global Emissions from Fossil and Industry | Comment |

|---|---|---|---|

| This study | 38,981 | 41,422 | 2030 emissions 6% higher than 2020 |

| WEO 2013 | 34,595 (excluding industry) | 36,493 | 2030 emissions 5% higher than 2020 (Excludes cement) |

| Ampere WITCH | 39,731 | 46,406 | 2030 emissions 17% higher than 2020 |

| Ampere MESSAGE | 38,182 | 42,344 | 2030 emissions 11% higher than 2020 |

Appendix B. Capped Electrification Rates for Different Regions in Each Model

| TIAM-Grantham | MESSAGE-GLOBIOM | WITCH | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Region | IND | TRA | BUI | Region | IND | TRA | BUI | Region | IND | TRA | BUI |

| AFR | 30 | 5 | 20 | AFR | 30 | 5 | 20 | SSA | 30 | 5 | 20 |

| AUS | 40 | 5 | 60 | PAC | 40 | 5 | 60 | KOS | 40 | 5 | 60 |

| CAN | 40 | 5 | 60 | - | - | - | - | CAJ | 40 | 5 | 60 |

| CHI | 40 | 5 | 50 | CPA | 40 | 5 | 50 | CHI | 40 | 5 | 50 |

| CSA | 30 | 5 | 60 | LAC | 30 | 5 | 60 | LAM | 30 | 5 | 60 |

| EEU | 30 | 10 | 30 | CEE | 30 | 10 | 30 | EEU | 30 | 10 | 30 |

| FSU | 30 | 10 | 30 | FSU | 30 | 10 | 30 | TE | 30 | 10 | 30 |

| IN | 30 | 5 | 40 | SAS | 30 | 5 | 40 | SAS | 30 | 5 | 40 |

| JAP | 40 | 5 | 55 | - | - | - | - | - | - | - | - |

| ME | 20 | 5 | 60 | MEA | 20 | 5 | 60 | MEA | 20 | 5 | 60 |

| MEX | 40 | 5 | 40 | - | - | - | - | - | - | - | - |

| ODA | 40 | 5 | 40 | OPA | 40 | 5 | 40 | SEA | 40 | 5 | 40 |

| SKO | 40 | 5 | 40 | - | - | - | - | - | - | - | - |

| USA | 40 | 5 | 60 | NAM | 40 | 5 | 60 | USA | 40 | 5 | 60 |

| WEU | 40 | 5 | 40 | WEU | 40 | 5 | 40 | WEU | 40 | 5 | 40 |

Appendix C. Model Descriptions

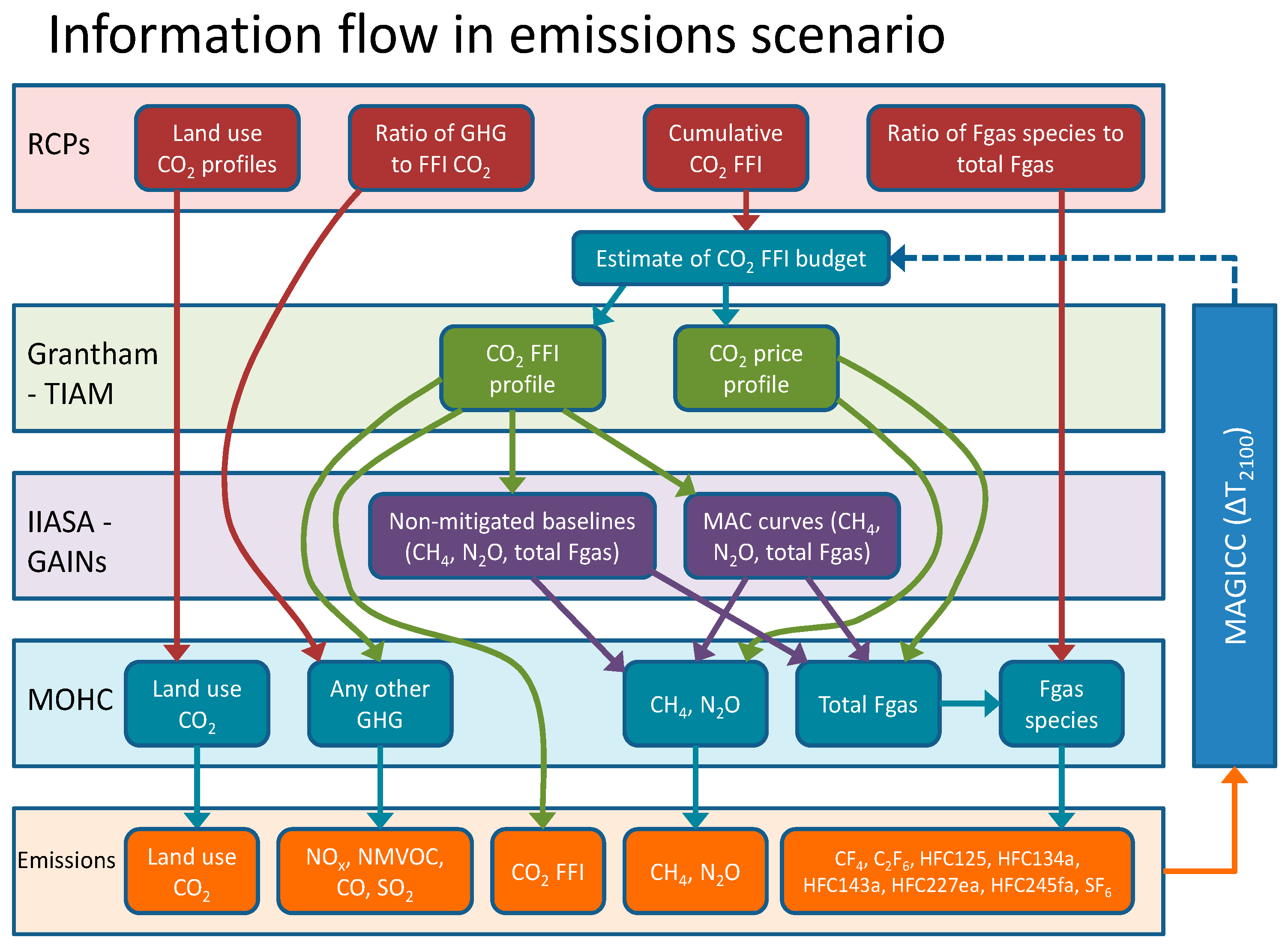

Appendix D. Deriving Temperature Goal-Consistent 21st Century CO2 Budgets and Emissions Profiles

- (1)

- Projections of global temperature change for the four RCPs is made using emissions relating to the RCPs [68]. Emissions are used rather than concentrations as this takes fuller account of uncertainty carbon cycle feedbacks. Following Bernie and Lowe [69], probabilistic projections are made using values of equilibrium climate sensitivity from models in the fifth Couple Model Inter-comparison Project (CMIP5) [70] along with uncertainty distributions of ocean mixing and carbon cycle feedbacks.

- (2)

- In each year land use emissions of CO2 are linearly interpolated from the RCPs on the basis of each RCP’s median 2100 projected temperature and the LTTG of the scenario.

- (3)

- Initial estimates of 21st century cumulative CO2 emissions from the FFI sectors are also linearly interpolated from the RCPs on the basis of future temperature projections and the scenario LTTG.

- (4)

- The cumulative CO2 FFI budget is then used to calculate emissions of CO2 from FFI, CH4, N2O and F-gases:

- (a)

- A time profile of CO2 emissions from FFI is then calculated from the cumulative CO2 FFI along with a carbon price profile;

- (b)

- The CO2 FFI emissions profile and aspects of the underlying energy system structure (in particular the fossil fuel energy mix) are then passed to GAINS to calculate non-CO2 GHG no-mitigation scenarios and corresponding marginal abatement cost (MAC) curves;

- (c)

- The CO2 FFI profile from TIAM-Grantham and the non-CO2 GHG no-mitigation scenarios and MAC curves from GAINS are then used to calculate the emissions of CH4, N2O and total F-Gas emissions, at different levels of CO2e price applied to the non-CO2 GHGs (using GWP100 values).

- (5)

- Individual F-gas emissions are then needed, but the constituent F-gases in the categories used by GAINS do not exactly match those used by MAGICC. Whilst this has a very small influence on the overall CO2e emissions, the individual gas species are needed by MAGICC. To estimate emissions of individual F-gases it is assumed that the relative emissions rate of each F-gas to the total F-gas emissions will change with time in line with the “unmitigated” RCP 8.5 scenario. Based on this assumption the emissions of each F-gas in RCP8.5 are scaled by a ratio of the total F-gas emissions from GAINS to the total F-gas emissions in the unmitigated reference scenario. So for example if the F-gas emissions from GAINS are 20% of the unmitigated F-gas emissions for that scenario, then this factor is applied to emissions of each individual F-gas from RCP8.5. This approach circumvents the issue of different gases being included in the calculation by GAINS and those needed by MAGICC. While other assumptions are possible, given the relatively small effect of differences in F-gas emissions between the RCPs, this an appropriate level of detail for the scope of the current study.

- (6)

- The emissions of non-Kyoto GHG and other gases needed by MAGICC (principally NOx, CO, NMVOC, SO2) are all based on the ratio of the emissions of each gas to the emissions of CO2 from the FFI sector in the RCPs being applied to the CO2 FFI emissions from TIAM-Grantham. For example if the CO2 FFI emissions from GAINS in a given year where 80% of the way between RCP4.5 and RCP6.0, the SO2 emissions would be the product of the CO2 FFI from TIAM-Grantham multiplied by a weighted mean of the ratio of SO2 to CO2 FFI in those two RCPs, with 4 times more weight given to the ratio from RCP6.0.

- (7)

- Projected median 2100 temperature change is then calculated and if within 0.1 °C of the original LTTG, the CO2 FFI budget is accepted, or else the CO2 budget for the scenario is re-estimated, before repeating the above procedure to re-calculate 2100 median temperature change.

References

- Intergovernmental Panel on Climate Change (IPCC). Climate Change 2014: Mitigation of Climate Change. Contribution of Working Group III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change; Edenhofer, O., Pichs-Madruga, R., Sokona, Y., Minx, J.C., Farahani, E., Kadner, S., Seyboth, K., Adler, A., Baum, I., Brunner, S., et al., Eds.; Cambridge University Press: Cambridge, UK; New York, NY, USA, 2014. [Google Scholar]

- Dessens, O.; Anandarajah, G.; Gambhir, A. Limiting global warming to 2 °C: What do the latest mitigation studies tell us about costs, technologies and other impacts? Energy Strategy Rev. 2016, 13–14, 67–76. [Google Scholar] [CrossRef]

- O’Neill, B.C.; Kriegler, E.; Riahi, K.; Ebi, K.L.; Hallegatte, S.; Carter, T.R.; Mathur, R.; van Vuuren, D.P. A new scenario framework for climate change research: The concept of shared socioeconomic pathways. Clim. Chang. 2014, 122, 387–400. [Google Scholar] [CrossRef]

- Bernie, D.; Lowe, J.A. Future Temperature Responses Based on IPCC and Other Existing Emissions Scenarios. Available online: http://avoid-net-uk.cc.ic.ac.uk/wp-content/uploads/delightful-downloads/2015/02/AVOID2_WPA-1_final_v2.pdf (accessed on 30 November 2015).

- Clarke, L.; Jiang, K.; Akimoto, K.; Babiker, M.; Blanford, G.; Fisher-Vanden, K.; Hourcade, J.C.; Krey, V.; Kriegler, E.; Löschel, A.; et al. Assessing transformation pathways. In Climate Change 2014: Mitigation of Climate Change. Contribution of Working Group III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change; Edenhofer, O., Pichs-Madruga, R., Sokona, Y., Minx, J.C., Farahani, E., Kadner, S., Seyboth, K., Adler, A., Baum, I., Brunner, S., et al., Eds.; Cambridge University Press: Cambridge, UK; New York, NY, USA, 2014. [Google Scholar]

- Riahi, K.; Kriegler, E.; Johnson, N.; Bertram, C.; den Elzen, M.G.J.; Eom, J.; Schaeffer, M.; Edmonds, J.; Isaac, M.; Krey, V.; et al. Locked into Copenhagen pledges–Implications of short-term emission targets for the cost and feasibility of long-term climate goals. Technol. Forecast. Soc. Chang. 2015, 90, 8–23. [Google Scholar] [CrossRef] [Green Version]

- Kriegler, E.; Weyant, J.P.; Blanford, G.J.; Krey, V.; Clarke, L.; Edmonds, J.; Fawcett, A.; Luderer, G.; Riahi, K.; Richels, R.; et al. The role of technology for achieving climate policy objectives: Overview of the EMF 27 study on global technology and climate policy strategies. Clim. Chang. 2014, 123, 353–367. [Google Scholar] [CrossRef] [Green Version]

- World Energy Investment Outlook 2014; International Energy Agency (IEA): Paris, France, 2014.

- Johnson, N.; Krey, V.; McCollum, D.L.; Rao, S.; Riahi, K.; Rogelj, J. Stranded on a low-carbon planet: Implications of climate policy for the phase-out of coal-based power plants. Technol. Forecast. Soc. Chang. 2015, 90, 89–102. [Google Scholar] [CrossRef]

- Van der Zwaan, B.C.C.; Rösler, H.; Kober, T.; Aboumahboub, T.; Calvin, K.V.; Gernaat, D.E.H.J.; Marangoni, G.; McCollum, D. A cross-model comparison of global long-term technology diffusion under a 2 °C climate change control target. Clim. Chang. Econ. 2013, 4, 1340013. [Google Scholar] [CrossRef]

- Krey, V.; Luderer, G.; Clarke, L.; Kriegler, E. Getting from here to there—Energy technology transformation pathways in the EMF27 scenarios. Clim. Chang. 2013, 123, 369–382. [Google Scholar] [CrossRef]

- Rose, S.K.; Kriegler, E.; Bibas, R.; Calvin, K.; Popp, A.; van Vuuren, D.P.; Weyant, J. Bioenergy in energy transformation and climate management. Clim. Chang. 2013, 123, 477–493. [Google Scholar] [CrossRef]

- Den Elzen, M.G.J.; van Vuuren, D.P.; van Vliet, J. Postponing emission reductions from 2020 to 2030 increases climate risks and long-term costs. Clim. Chang. 2010, 99, 313–320. [Google Scholar] [CrossRef]

- Riahi, K.; Dentener, F.; Gielen, D.; Grubler, A.; Jewell, J.; Klimont, Z.; Krey, V.; McCollum, D.; Pachauri, S.; Rao, S.; et al. Energy pathways for sustainable development. In Global Energy Assessment—Toward a Sustainable Future; Cambridge University Press: Cambridge, UK; New York, NY, USA; International Institute for Applied Systems Analysis (IIASA): Laxenburg, Austria, 2012; pp. 1203–1306. [Google Scholar]

- Luderer, G.; Bertram, C.; Calvin, K.; Cian, E.D.; Kriegler, E. Implications of weak near-term climate policies on long-term mitigation pathways. Clim. Chang. 2013, 136, 127–140. [Google Scholar] [CrossRef]

- Luderer, G.; Pietzcker, R.C.; Bertram, C.; Kriegler, E.; Meinshausen, M.; Edenhofer, O. Economic mitigation challenges: How further delay closes the door for achieving climate targets. Environ. Res. Lett. 2013, 8, 34033. [Google Scholar] [CrossRef]

- Von Stechow, C.; Minx, J.C.; Riahi, K.; Jewell, J.; McCollum, D.L.; Callaghan, M.W.; Bertram, C.; Luderer, G.; Baiocchi, G. 2 °C and SDGs: United they stand, divided they fall? Environ. Res. Lett. 2016, 11, 34022. [Google Scholar] [CrossRef]

- Van Sluisveld, M.A.E.; Harmsen, J.H.M.; Bauer, N.; McCollum, D.L.; Riahi, K.; Tavoni, M.; van Vuuren, D.P.; Wilson, C.; van der Zwaan, B. Comparing future patterns of energy system change in 2 °C scenarios with historically observed rates of change. Glob. Environ. Chang. 2015, 35, 436–449. [Google Scholar] [CrossRef] [Green Version]

- Kramer, G.J.; Haigh, M. No quick switch to low-carbon energy. Nature 2009, 462, 568–569. [Google Scholar] [CrossRef] [PubMed]

- Wilson, C.; Grubler, A.; Bauer, N.; Krey, V.; Riahi, K. Future capacity growth of energy technologies: Are scenarios consistent with historical evidence? Clim. Chang. 2013, 118, 381–395. [Google Scholar] [CrossRef] [Green Version]

- Iyer, G.; Hultman, N.; Eom, J.; McJeon, H.; Patel, P.; Clarke, L. Diffusion of low-carbon technologies and the feasibility of long-term climate targets. Technol. Forecast. Soc. Chang. 2015, 90, 103–118. [Google Scholar] [CrossRef]

- Napp, T.A.; Gambhir, A.; Thomas, R.; Hawkes, A.; Bernie, D.; Lowe, J.A. Exploring the Feasibility of Low-Carbon Scenarios Using Historical Energy Transitions Analysis. Available online: http://avoid-net-uk.cc.ic.ac.uk/wp-content/uploads/delightful-downloads/2015/11/Exploring-the-feasibility-of-low-carbon-scenarios-using-historical-energy-transitions-analysis-AVOID-2-WP-C3.pdf (accessed on 23 August 2016).

- The Emissions Gap Report 2014; United Nations Environment Programme (UNEP): Nairobi, Kenya, 2014.

- Adoption of the Paris Agreement; FCCC/CP/2015/L.9/Rev.1; United Nations Framework Convention on Climate Change (UNFCCC): New York, NY, USA, 2015.

- Loulou, R.; Labriet, M. ETSAP-TIAM: The TIMES integrated assessment model Part I: Model structure. Comput. Manag. Sci. 2007, 5, 7–40. [Google Scholar] [CrossRef]

- Loulou, R.; Labriet, M.; Kanudia, A. Deterministic and stochastic analysis of alternative climate targets under differentiated cooperation regimes. Energy Econ. 2009, 31, S131–S143. [Google Scholar] [CrossRef]

- Messner, S.; Strubegger, M. Model-based decision support in energy planning. Int. J. Glob. Energy Issues 1999, 12, 196–207. [Google Scholar] [CrossRef]

- Riahi, K.; Grübler, A.; Nakicenovic, N. Scenarios of long-term socio-economic and environmental development under climate stabilization. Technol. Forecast. Soc. Chang. 2007, 74, 887–935. [Google Scholar] [CrossRef]

- Havlík, P.; Valin, H.; Herrero, M.; Obersteiner, M.; Schmid, E.; Rufino, M.C.; Mosnier, A.; Thornton, P.K.; Böttcher, H.; Conant, R.T.; et al. Climate change mitigation through livestock system transitions. Proc. Natl. Acad. Sci. USA 2014, 111, 3709–3714. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Bosetti, V.; Carraro, C.; Galeotti, M.; Massetti, E.; Tavoni, M. WITCH—A World Induced Technical Change Hybrid Model; Social Science Research Network (SSRN): Rochester, NY, USA, 2006. [Google Scholar]

- Schweizer, V.J.; O’Neill, B.C. Systematic construction of global socioeconomic pathways using internally consistent element combinations. Clim. Chang. 2014, 122, 431–445. [Google Scholar] [CrossRef]

- Kanakoudis, V.; Papadopoulou, A. Allocating the cost of the carbon footprint produced along a supply chain, among the stakeholders involved. J. Water Clim. Chang. 2014, 5, 556–568. [Google Scholar] [CrossRef]

- Rogelj, J.; McCollum, D.L.; O’Neill, B.C.; Riahi, K. 2020 emissions levels required to limit warming to below 2 °C. Nat. Clim. Chang. 2013, 3, 405–412. [Google Scholar] [CrossRef]

- Sorrell, S. The Economics of Energy Efficiency: Barriers to Cost-Effective Investment; Edward Elgar Publishing Ltd.: Cheltenham, UK, 2004. [Google Scholar]

- Eom, J.; Edmonds, J.; Krey, V.; Johnson, N.; Longden, T.; Luderer, G.; Riahi, K.; van Vuuren, D.P. The impact of near-term climate policy choices on technology and emission transition pathways. Technol. Forecast. Soc. Chang. 2015, 90, 73–88. [Google Scholar] [CrossRef] [Green Version]

- Technology Roadmap: Carbon Capture and Storage; International Energy Agency (IEA): Paris, France, 2013.

- Smith, P.; Davis, S.J.; Creutzig, F.; Fuss, S.; Minx, J.; Gabrielle, B.; Kato, E.; Jackson, R.B.; Cowie, A.; Kriegler, E.; et al. Biophysical and economic limits to negative CO2 emissions. Nat. Clim. Chang. 2016, 6, 42–50. [Google Scholar] [CrossRef] [Green Version]

- Fuss, S.; Canadell, J.G.; Peters, G.P.; Tavoni, M.; Andrew, R.M.; Ciais, P.; Jackson, R.B.; Jones, C.D.; Kraxner, F.; Nakicenovic, N.; et al. Betting on negative emissions. Nat. Clim. Chang. 2014, 4, 850–853. [Google Scholar] [CrossRef] [Green Version]

- McGlashan, N.; Shah, N.; Caldecott, B.; Workman, M. High-level techno-economic assessment of negative emissions technologies. Process Saf. Environ. Prot. 2012, 90, 501–510. [Google Scholar] [CrossRef]

- Pissarides, C. Assessment of Macro Economic Transmission Mechanisms of Carbon Constraints through the UK Economy—A Report for the Committee on Climate Change. Available online: https://www.theccc.org.uk/archive/aws2/docs/Macro%20transmission%20Aug%202008.pdf (accessed on 29 October 2015).

- Gambhir, A.; Schulz, N.; Napp, T.; Tong, D.; Munuera, L.; Faist, M.; Riahi, K. A hybrid modelling approach to develop scenarios for China’s carbon dioxide emissions to 2050. Energy Policy 2013, 59, 614–632. [Google Scholar] [CrossRef]

- Gambhir, A.; Napp, T.A.; Emmott, C.J.M.; Anandarajah, G. India’s CO2 emissions pathways to 2050: Energy system, economic and fossil fuel impacts with and without carbon permit trading. Energy 2014, 77, 791–801. [Google Scholar] [CrossRef]

- Anandarajah, G.; Gambhir, A. India’s CO2 emission pathways to 2050: What role can renewables play? Appl. Energy 2014, 131, 79–86. [Google Scholar] [CrossRef]

- Clarke, L.; Edmonds, J.; Krey, V.; Richels, R.; Rose, S.; Tavoni, M. International climate policy architectures: Overview of the EMF 22 International Scenarios. Energy Econ. 2009, 31, S64–S81. [Google Scholar] [CrossRef] [Green Version]

- Smil, V. Energy Transitions: History, Requirements, Prospects; ABC-CLIO: Santa Barbara, CA, USA, 2010. [Google Scholar]

- International Institute for Applied Systems Analysis (IIASA). Global Energy Assessment; Cambridge University Press: Cambridge, UK; New York, NY, USA, 2011. [Google Scholar]

- World Energy Outlook 2014; International Energy Agency (IEA): Paris, France, 2014.

- Capital Cost for Electricity Plants; U.S. Energy Information Administration (EIA): Washington, DC, USA, 2013.

- National Renewable Energy Laboratory. Transparent Cost Database (September 2013 Update). Available online: http://www.nrel.gov/analysis/tech_cost_data.html (accessed on 18 May 2015).

- Intergovernmental Panel on Climate Change (IPCC). Special Report on Carbon Dioxide Capture and Storage: Summary for Policymakers; Cambridge University Press: Cambridge, UK; New York, NY, USA, 2005. [Google Scholar]

- Carbon Sequestration ATLAS of the United States and Canada, 3rd ed.U.S. Department of Energy’s (DOE) National Energy Technology Laboratory (NETL): Pittsburgh, PA, USA, 2010.

- Van Vuuren, D.P.; Stehfest, E.; den Elzen, M.G.J.; Kram, T.; van Vliet, J.; Deetman, S.; Isaac, M.; Goldewijk, K.K.; Hof, A.; Beltran, A.M.; et al. RCP2.6: Exploring the possibility to keep global mean temperature increase below 2 °C. Clim. Chang. 2011, 109, 95–116. [Google Scholar] [CrossRef]

- Rogelj, J.; Luderer, G.; Pietzcker, R.C.; Kriegler, E.; Schaeffer, M.; Krey, V.; Riahi, K. Energy system transformations for limiting end-of-century warming to below 1.5 °C. Nat. Clim. Chang. 2015, 5, 519–527. [Google Scholar] [CrossRef]

- Rogelj, J.; den Elzen, M.G.J.; Höhne, N.; Fransen, T.; Fekete, H.; Winkler, H.; Schaeffer, R.; Sha, F.; Riahi, K.; Meinshausen, M. Paris Agreement climate proposals need a boost to keep warming well below 2 °C. Nature 2016, 534, 631–639. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Schleussner, C. F.; Rogelj, J.; Schaeffer, M.; Lissner, T.; Licker, R.; Fischer, E.M.; Knutti, R.; Levermann, A.; Frieler, K.; Hare, W. Science and policy characteristics of the Paris Agreement temperature goal. Nat. Clim. Chang. 2016, 6, 827–835. [Google Scholar] [CrossRef]

- Den Elzen, M.G.J.; Roelfsema, M.; Hof, A.F.; Böttcher, H.; Grassi, G. Analysing the Emission Gap Between Pledged Emission Reductions under the Cancún Agreements and the 2 °C Climate Target; PBL Netherlands Environmental Assessment Agency: Bilthoven, The Netherlands, 2012. [Google Scholar]

- Compilation of Economy-Wide Emission Reduction Targets to Be Implemented by Parties Included in Annex I to the Convention; FCCC /SB/2011/INF.1/Rev.1; United Nations Framework Convention on Climate Change (UNFCCC): New York, NY, USA, 2011.

- Compilation of Information on Nationally Appropriate Mitigation Actions to Be Implemented by Parties Not Included in Annex I to the Convention; FCCC /AWGLCA/2011/INF.1; United Nations Framework Convention on Climate Change (UNFCCC): New York, NY, USA, 2011.

- World Energy Outlook 2013; International Energy Agency (IEA): Paris, France, 2013.

- Havlík, P.; Schneider, U.A.; Schmid, E.; Böttcher, H.; Fritz, S.; Skalský, R.; Aoki, K.; Cara, S.D.; Kindermann, G.; Kraxner, F.; et al. Global land-use implications of first and second generation biofuel targets. Energy Policy 2011, 39, 5690–5702. [Google Scholar] [CrossRef]

- Rao, S.; Riahi, K. The role of non-CO2 greenhouse gases in climate change mitigation: Long-term scenarios for the 21st century. Energy J. 2006, 27, 177–200. [Google Scholar] [CrossRef]

- Amann, M.; Bertok, I.; Borken-Kleefeld, J.; Cofala, J.; Heyes, C.; Höglund-Isaksson, L.; Klimont, Z.; Nguyen, B.; Posch, M.; Rafaj, P.; et al. Cost-effective control of air quality and greenhouse gases in Europe: Modeling and policy applications. Environ. Model. Softw. 2011, 26, 1489–1501. [Google Scholar] [CrossRef]

- Rafaj, P.; Rao, S.; Klimont, Z.; Kolp, P.; Schöpp, W.; Amann, M. Emissions of Air Pollutants Implied by Global Long-Term Energy Scenarios; International Institute for Applied Systems Analysis (IIASA): Laxenburg, Austria, 2010. [Google Scholar]

- Messner, S.; Schrattenholzer, L. MESSAGE–MACRO: Linking an energy supply model with a macroeconomic module and solving it iteratively. Energy 2000, 25, 267–282. [Google Scholar] [CrossRef]

- Meinshausen, M.; Raper, S.C.B.; Wigley, T.M.L. Emulating IPCC AR4 atmosphere-ocean and carbon cycle models for projecting global-mean, hemispheric and land/ocean temperatures: MAGICC 6.0. Atmos. Chem. Phys. Discuss. 2008, 8, 6153–6272. [Google Scholar] [CrossRef]

- Winiwarter, W.; Höglund-Isaksson, L.; Schöpp, W.; Tohka, A.; Wagner, F.; Amann, M. Emission mitigation potentials and costs for non-CO2 greenhouse gases in Annex-I countries according to the GAINS model. J. Integr. Environ. Sci. 2010, 7, 235–243. [Google Scholar] [CrossRef]

- Höglund-Isaksson, L.; Winiwarter, W.; Purohit, P.; Rafaj, P.; Schöpp, W.; Klimont, Z. EU low carbon roadmap 2050: Potentials and costs for mitigation of non-CO2 greenhouse gas emissions. Energy Strategy Rev. 2012, 1, 97–108. [Google Scholar] [CrossRef]

- Meinshausen, M.; Smith, S.J.; Calvin, K.; Daniel, J.S.; Kainuma, M.L.T.; Lamarque, J.F.; Matsumoto, K.; Montzka, S.A.; Raper, S.C.B.; Riahi, K.; et al. The RCP greenhouse gas concentrations and their extensions from 1765 to 2300. Clim. Chang. 2011, 109, 213–241. [Google Scholar] [CrossRef]

- Bernie, D.; Lowe, J.A. Analysis of Climate Projections from the IPCC Working Group 3 Scenario Database. Available online: https://workspace.imperial.ac.uk/grantham/Public/AVOID/AVOID2%20WPA%201%20Analysis%20of%20climate%20projections%20from%20the%20IPCC%20working%20group%203%20scenario%20database.pdf (accessed on 14 June 2016).

- Taylor, K.E.; Stouffer, R.J.; Meehl, G.A. An overview of CMIP5 and the experiment design. Bull. Am. Meteorol. Soc. 2012, 93, 485–498. [Google Scholar] [CrossRef]

- Meinshausen, M.; Meinshausen, N.; Hare, W.; Raper, S.C.B.; Frieler, K.; Knutti, R.; Frame, D.J.; Allen, M.R. Greenhouse-gas emission targets for limiting global warming to 2 °C. Nature 2009, 458, 1158–1162. [Google Scholar] [CrossRef] [PubMed]

- Allen, M.R.; Frame, D.J.; Huntingford, C.; Jones, C.D.; Lowe, J.A.; Meinshausen, M.; Meinshausen, N. Warming caused by cumulative carbon emissions towards the trillionth tonne. Nature 2009, 458, 1163–1166. [Google Scholar] [CrossRef]

- Matthews, H.D.; Gillett, N.P.; Stott, P.A.; Zickfeld, K. The proportionality of global warming to cumulative carbon emissions. Nature 2009, 459, 829–832. [Google Scholar] [CrossRef] [PubMed]

| Median Temperature Change/°C by 2100 (Relative to Pre-Industrial) | Cumulative (2000–2100) CO2 Emissions from Fossil Fuel Combustion and Industry (GtCO2) | Scenario Variants |

|---|---|---|

| 2 | 1340 | Immediate action from model base year 1 |

| Action from 2020, following moderate action | ||

| Action from 2020, following moderate action, with the introduction of CCS delayed until 2050 | ||

| Action from 2020, following moderate action, with limited potential for electricity in end-use sectors | ||

| Action from 2030, following moderate action | ||

| 2.5 | 2260 | Immediate action from model base year |

| Action from 2020, following moderate action | ||

| Action from 2030, following moderate action | ||

| 3 | 3560 | Immediate action from model base year |

| Action from 2020, following moderate action | ||

| Action from 2030, following moderate action | ||

| 4 | 5280 | Immediate action from model base year |

| Action from 2020, following moderate action | ||

| Action from 2030, following moderate action | ||

| 4.6 2 | 6000 | None |

| Model | New Nuclear | CCS | BECCS | Solar (PV and CSP) | Wind (on and offshore) | Time Step (years) | Base Year | Solution Approach |

|---|---|---|---|---|---|---|---|---|

| TIAM-Grantham [25,26] | Yes | Yes | Yes | Yes | Yes | 10 | 2012 | Inter-temporal optimisation |

| MESSAGE-GLOBIOM [14,27,28,29] | Yes | Yes | Yes | Yes | Yes | 10 | 2010 | Inter-temporal optimisation and recursive dynamic |

| WITCH [30] | Yes | Yes | Yes | Yes | Yes | 5 | 2010 | Inter-temporal optimisation |

| Indicator | Relevance | Example of Challenge |

|---|---|---|

| Does the model “solve” | Models contain a wide range of technologies and significant energy efficiency improvement capability. Lack of solution implies more ambitious technology deployment and efficiency improvements must be achieved in reality [1]. | All models provide an analytical solution for all scenarios explored, although for 2 °C scenario with global action delayed to 2030, TIAM-Grantham reaches its $10,000/tCO2 limit by 2100, indicating this is at its own model-defined feasibility limit (See Section 3.2). |

| CO2 price and rate of increase | Very high CO2 prices would imply energy services are very expensive. Very rapid decadal rises in CO2 price imply rapid adjustments to energy prices, indicating a limited availability of low-carbon technologies to provide rapid mitigation possibilities at reasonable costs. Both of these could be socially unacceptable and/or result in economic instability [33]. | For the 2 °C scenario with global action delayed to 2030, two models (TIAM-Grantham and WITCH) see decadal CO2 price increases of greater than $1,000/tCO2 (See Section 3.2). |

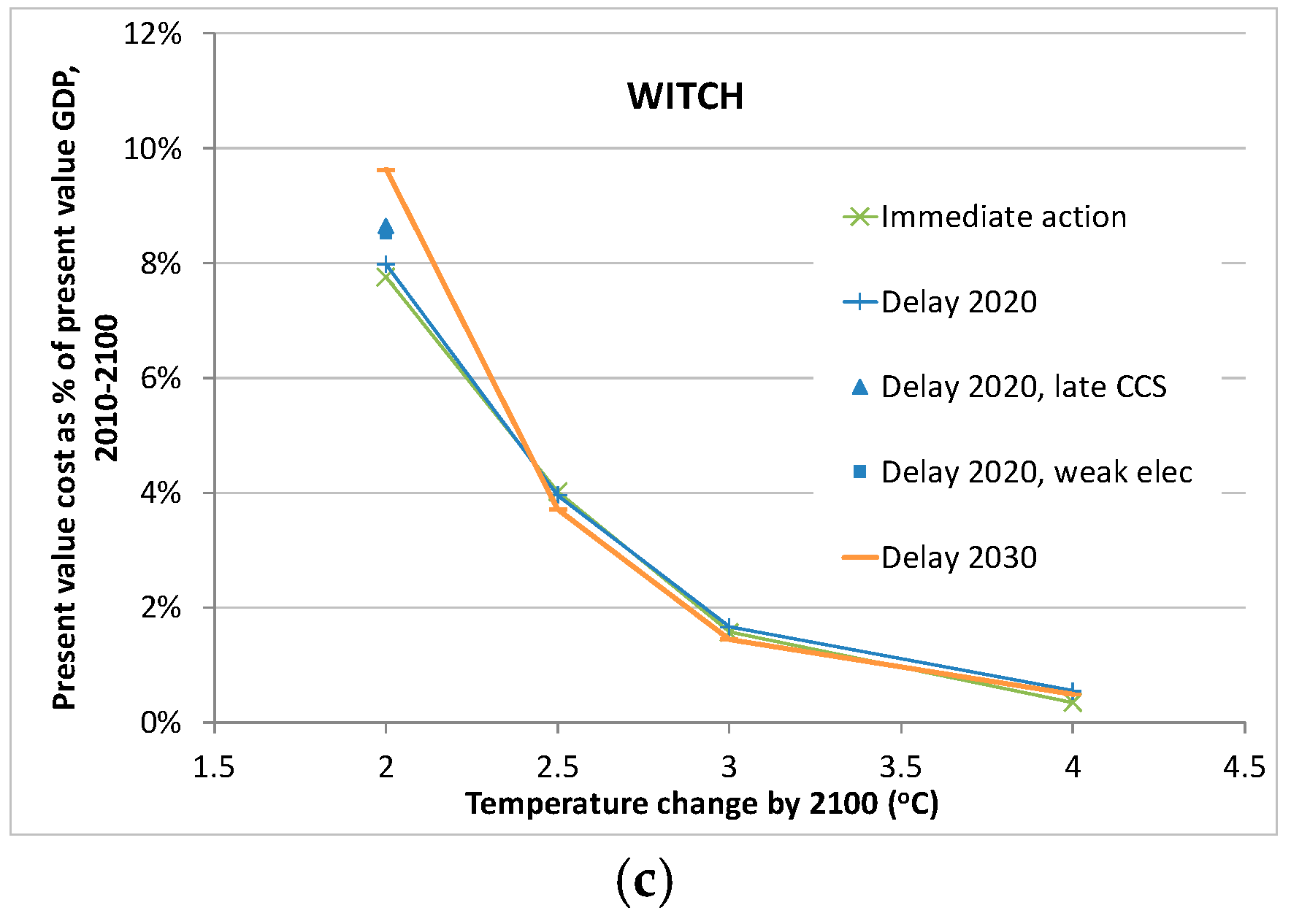

| Mitigation cost | High mitigation cost implies more expensive energy, which indicates a lack of available, reasonable cost mitigation technologies, and which is likely to lead to resistance from households and businesses. | WITCH mitigation cost for 2 °C scenario with global action delayed to 2030 costs almost 10% of 21st century GDP. This may be unacceptably high (see Section 3.3). |

| Rate of decarbonis-ation | No sustained periods of historical decarbonization globally since the beginning of the 20th century. At a country level rates of up to 3% per year during periods of policy to achieve a rapid shift away from oil [6]. | WITCH and TIAM-Grantham both show average annual CO2 reduction rates in excess of 10% per year over the decade 2030-2040, in 2 °C scenario with global action delayed to 2030 (See Section 3.4). |

| Rate of energy intensity improvements | Very rapid energy efficiency improvements across the economy would require a widespread shift to a range of technologies prone to behavioural barriers [34] and would also require avoidance of significant rebound effects [34]. | WITCH sees almost flat final energy demand globally over the 21st century in the 2 °C scenario with action delayed to 2020. This compares to a more-than-doubling of final energy demand in the reference scenario (see Section 3.4). |

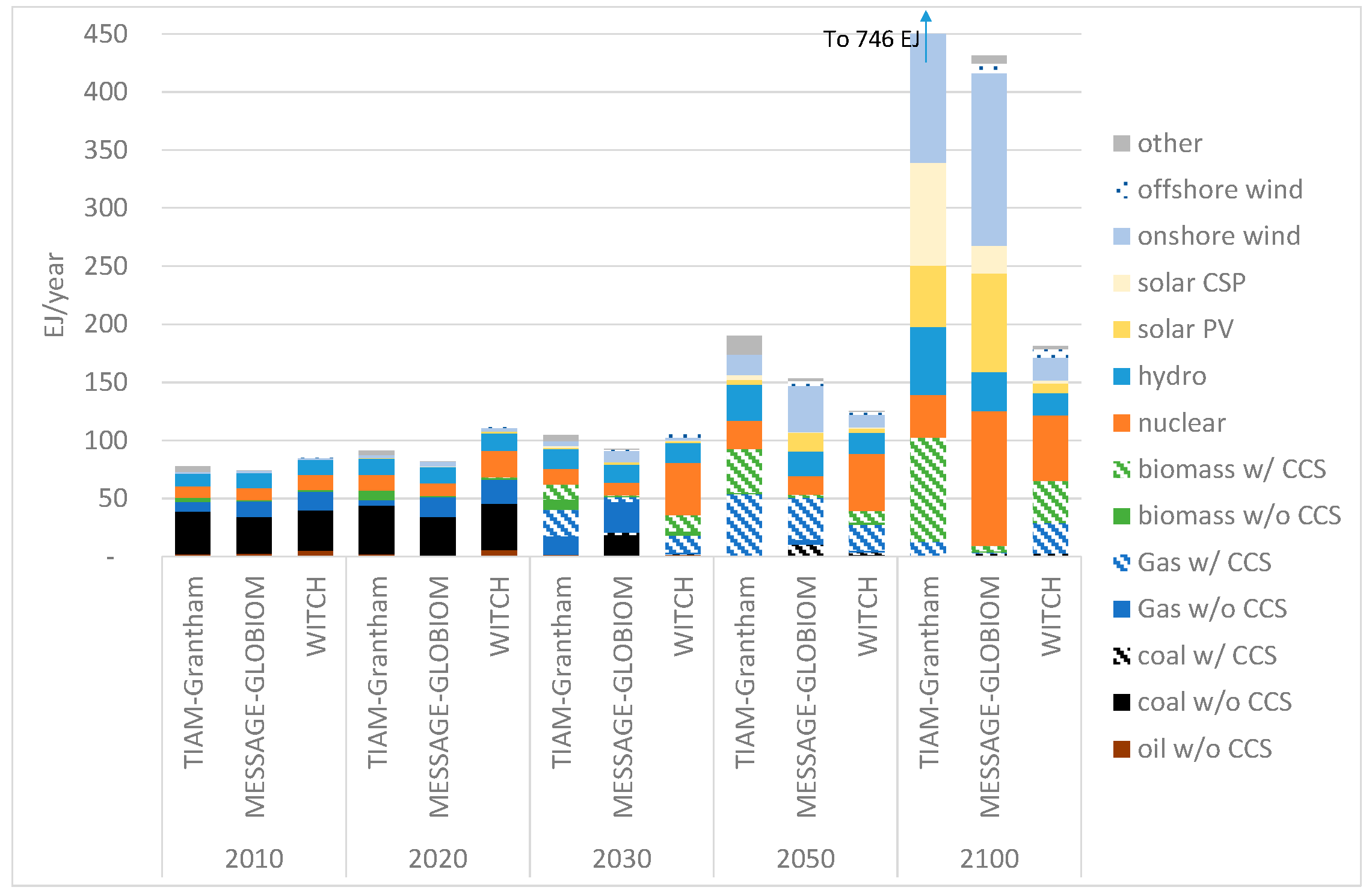

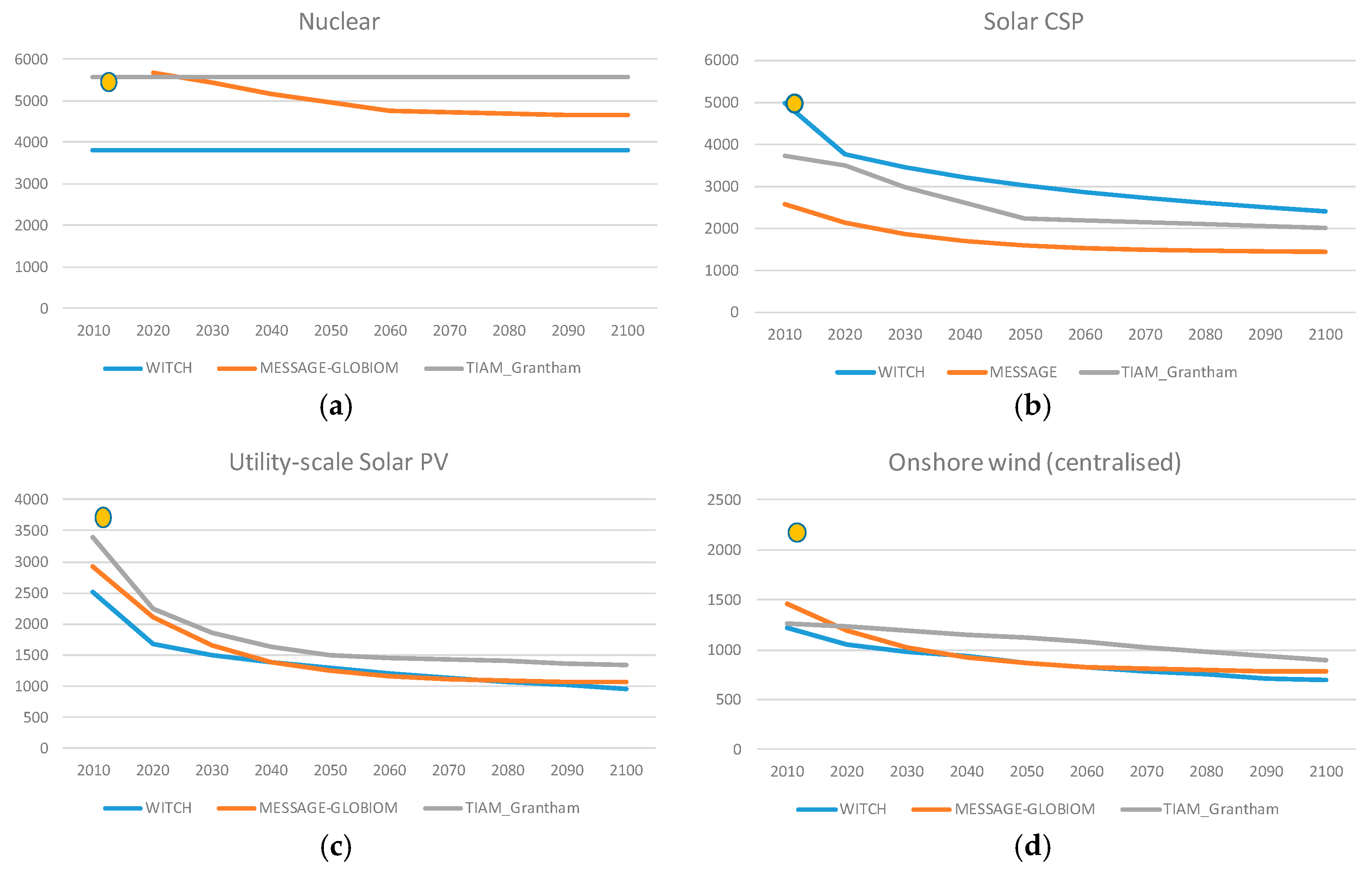

| Technology deployment rates | Significant decadal increases in particular technologies must be questioned on the grounds of real-world ability to develop and scale up supply chains and access skills and labour, and financial and material resources [10,35]. | In the 2 °C scenario with delayed action to 2020, the most striking deployment rates over the period 2020–2030 are for nuclear (830 GW in WITCH, more than twice current deployed capacity), gas with CCS (800 GW in TIAM-Grantham), biomass with CCS (520 GW in WITCH), and onshore wind (480 GW in MESSAGE-GLOBIOM, approximately current installed capacity) (See Section 3.4). |

| Idling of high-carbon assets | Early retirement (as evidenced by sustained zero capacity factors of coal plants within their lifetime) means potentially significant economic losses for coal-fired electricity generators. This will lead to resistance from utilities to idle these plants [9]. | In the 2 °C scenario with delayed action to 2030, TIAM-Grantham has 780 GW of zero capacity factor coal plants in 2040, of which 315 GW has 20 or more years of remaining life. In the 2 °C scenario with delayed action to 2020, TIAM-Grantham has 1400 GW of idle coal plant by 2030, of which almost 1200 GW has 7 years of remaining life (See Section 3.5). |

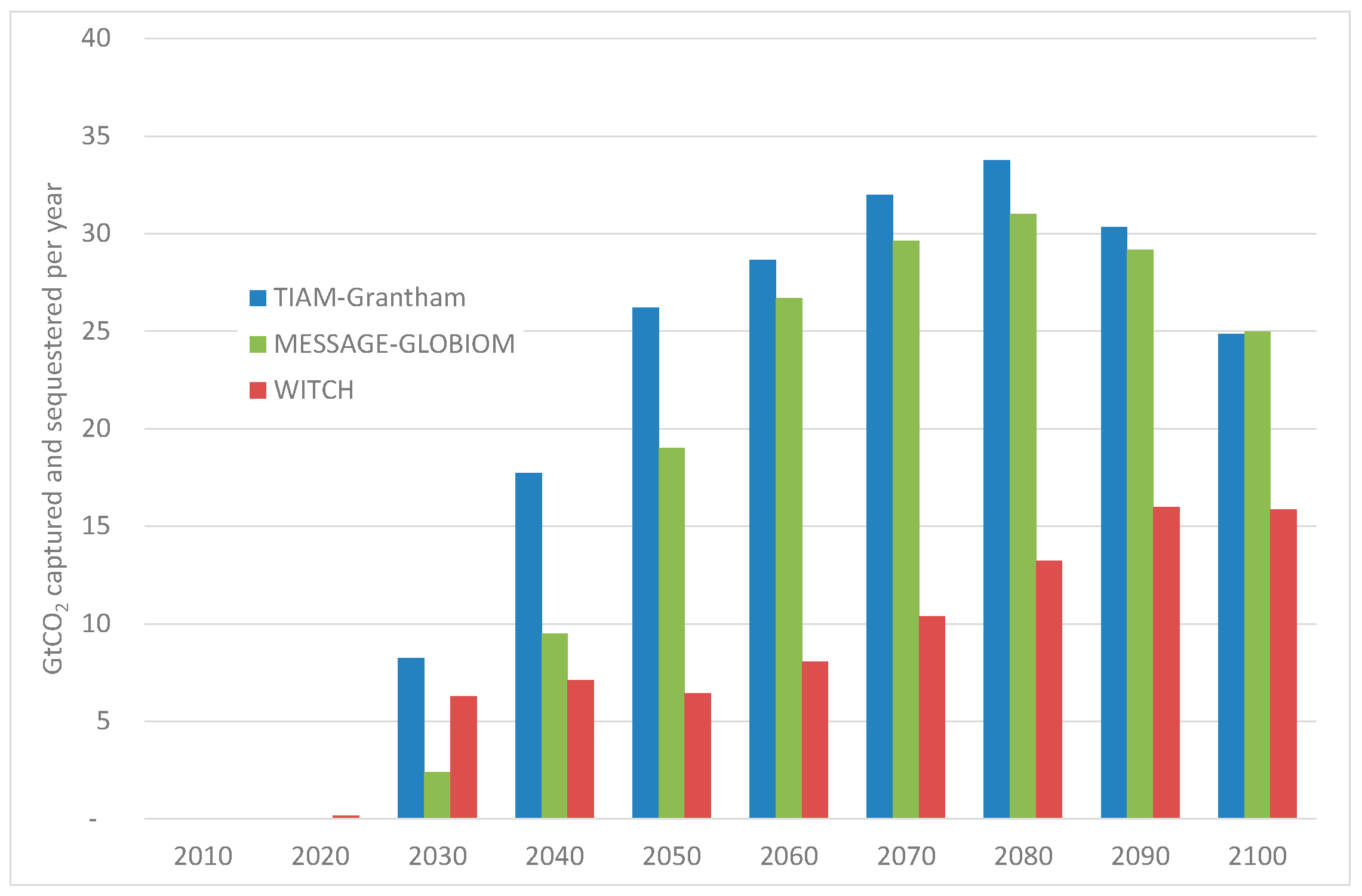

| Quantity of CO2 captured and stored | Implies successful large-scale deployment of CCS, overcoming technical, economic, legal and other barriers for CO2 transport and storage [36]. | MESSAGE-GLOBIOM and TIAM-Grantham see over 30 GtCO2/year captured by 2080 in the 2 °C scenario with delayed action to 2020 (see Section 3.6). |

| Timing of net global negative CO2 emissions | Very large-scale deployment of negative emissions technologies (e.g., BECCS) poses technical, regulatory, infrastructure, economic challenges [37,38,39]. | All three models see global CO2 emissions at negative levels by 2080 in the 2 °C scenario with delayed action to 2030 (see Section 3.6), with CCS deployed from the 2020s onwards. |

| Scenario | TIAM-Grantham | MESSAGE-GLOBIOM | WITCH |

|---|---|---|---|

| 2C immediate | −2.2% | −0.9% | −6.0% |

| 2C delay to 2020 | −5.2% | −1.9% | −8.7% |

| 2C delay to 2030 | −10.8% 1 | −6.6% | −14.2% |

| 2.5C immediate | +1.0% | +0.4% | −1.5% |

| 2.5C delay to 2020 | −0.1% | +0.4% | −3.5% |

| 2.5C delay to 2030 | −2.0% | −0.8% | −5.7% |

| 3C immediate | +2.0% | +1.0% | +1.0% |

| 3C delay to 2020 | +1.4% | +1.4% | +0.6% |

| 3C delay to 2030 | +1.1% | +0.9% | -0.2% |

| 4C immediate | +1.1% | +1.1% | +2.3% |

| 4C delay to 2020 | +1.7% | +1.7% | +2.6% |

| 4C delay to 2030 | +1.4% | +1.4% | +2.7% |

| Scenario | Technology | Growth Rate |

|---|---|---|

| 2 °C with delay to 2020 | Gas with CCS | 800 GW in 2020–2030 (TIAM-Grantham) |

| Biomass with CCS | 520 GW in 2020–2030 (WITCH) | |

| Nuclear | 830 GW in 2020–2030 (WITCH) | |

| Onshore wind | 480 GW in 2020–2030 (MESSAGE-GLOBIOM) | |

| 2 °C with delay to 2030 | Gas with CCS | 1600 GW in 2030–2040 (TIAM-Grantham) |

| Biomass with CCS | 1000 GW in 2030–2040 (TIAM-Grantham) | |

| Nuclear | 640 GW in 2030–2040 (WITCH) | |

| Onshore wind | 750 GW in 2030–2040 (MESSAGE-GLOBIOM) | |

| Solar PV | 1300 GW in 2030–2040 (TIAM-Grantham) | |

| Solar CSP | 950 GW in 2030–2040 (TIAM-Grantham) | |

| 2 °C with delay to 2020 and CCS delayed until 2050 | Gas without CCS | 780 GW in 2020–2030 (TIAM-Grantham) |

| Biomass without CCS | 480 GW in 2020–2030 (TIAM-Grantham) | |

| Nuclear | 1050 GW in 2020–2030 (WITCH) | |

| Offshore wind | 320 GW in 2020–2030 (WITCH) | |

| Solar PV | 380 GW in 2020–2030 (MESSAGE-GLOBIOM) | |

| Solar CSP | 550 GW in 2020–2030 (TIAM-Grantham) | |

| 2 °C with delay to 2020 and weak electrification | Gas with CCS | 900 GW in 2020–2030 (TIAM-Grantham) |

| Biomass with CCS | 540 GW in 2020–2030 (WITCH) | |

| Nuclear | 780 GW in 2020–2030 (WITCH) | |

| Onshore wind | 440 GW in 2020–2030 (MESSAGE-GLOBIOM) |

| Scenario | Models Solve | CO2 Prices | CO2 Rate of Change | Mitigation Cost | Idling of Coal Plant | Technology Deployment Rates (Max Across Models) | Energy Intensity Improvement | CO2 Captured | Negative Emissions | Overall |

|---|---|---|---|---|---|---|---|---|---|---|

| Delay to 2020 | All models solve | 1 model shows >$1000/tCO2 increase in CO2 price per decade (in period 2080–2100) | 2020–2030 period sees 2%–9% average annual CO2 reductions | 2 models have cost as 1.3%–1.7% of 21st century GDP. 1 model 8.0% of 21st century GDP | 2 models have 1400 GW of idle coal plant by 2030 | Over 300 GW each of nuclear, gas CCS, biomass CCS, onshore wind in 2020–2030 | 2.4%–6.8% annual fall in primary energy/unit GDP in 2020–2030 | 2 models have >30 GtCO2 captured in 2080 | 2 models see net negative emissions by 2080 | - |

| Delay to 2020, late CCS | All models solve | 1 model shows >$1000/tCO2 increase in CO2 price per decade in period 2070–2100. and CO2 price almost $10,000/tCO2 by 2100 | 2020–2030 period sees rate 2%–7% average annual CO2 reductions | 2 models have cost as 1.9%–2.3% of 21st century GDP, 1 model 8.6% of 21st century GDP | 2 models have 1400 GW of idle coal plant by 2030 | Over 300 GW each of gas, biomass, nuclear, solar (PV, CSP) and offshore wind in 2020–2030 | 3.0%–8.3% annual fall in primary energy/unit GDP in 2020–2030 | 1 model has >30 GtCO2 captured by 2060 | All models see net negative emissions by 2090 | - |

| Delay to 2020, weak electrific-ation | All models solve | 1 model shows >$1000/tCO2 increase in CO2 price per decade in period 2070–2100, and CO2 price almost $9000/tCO2 by 2100 | 2020–2030 period sees rate 2%–9% average annual CO2 reductions | 2 models have cost as 1.6%–2.2% of 21st century GDP, 1 model 8.5% of 21st century GDP | 2 models have 780–1400 GW of idle coal plant by 2030 | Over 300 GW each of gas CCS, biomass CCS, onshore wind and nuclear in 2020–2030 | 2.6%–7.1% annual fall in primary energy/unit GDP in 2020–2030 | 2 models have >30 GtCO2 captured in 2080 | 2 models see net negative emissions by 2080 | - |

| Delay to 2030 | Only two out of three models solve | All models show >$1000/tCO2 increase in CO2 price per decade in period 2090–2100. 2 models show CO2 price >$7000/tCO2 by 2100 | 2030–2040 period sees rate 7%–14% average annual CO2 reductions | 2 models have cost as 2.2% of 21st century, 1 model 9.6% of 21st century GDP | 2 models have 800 GW of idle coal plants by 2040 | Over 300 GW of gas CCS, biomass CCS, solar (PV, CSP), onshore wind and nuclear in 2030–2040 | 1.9%–8.9% annual fall in primary energy/unit GDP in 2030–2040 | 1 model has >30 GtCO2 captured by 2060 | All models see net negative emissions by 2080 | - |

| Scenario | Models Solve | CO2 Prices | CO2 Rate of Change (2020–2030) | Mitigation Cost | Idling of Coal Plant | Technology Deployment Rates (Max Across Models) | Energy Intensity Improvement | CO2 Captured | Negative Emissions | Overall |

|---|---|---|---|---|---|---|---|---|---|---|

| 2 °C | All models solve | 1 model shows >$1000/tCO2 increase in CO2 price per decade (in period 2080–2100) | 2%–9% average annual CO2 reductions | 2 models have cost as 1.3%–1.7% of 21st century GDP. 1 model 8.0% of 21st century GDP | 2 models have 1400 GW of idle coal plant by 2030 | Over 300 GW each of nuclear, gas CCS, biomass CCS, onshore wind in 2020–2030 period | 2.4%–6.8% annual fall in primary energy/unit GDP in 2020–2030 period | 2 models have >30 GtCO2/year captured in 2080 | 2 models see net negative emissions by 2080 | - |

| 2.5 °C | All models solve | CO2 price range $504–1573/t CO2 by 2100 with maximum decadal increase $607/t CO2 (TIAM-Grantham) in 2090–2100 | Between a 0.4% increase and 3.5% reduction in average annual CO2 | 2 models have cost as 0.5% of 21st century GDP, 1 model 4.0% of 21st century GDP | 1 model has reduced capacity factor equivalent to 370 GW of idle coal plant by 2030. Other models have no idling by 2030 | Over 300 GW each of gas with CCS, gas (w/out CCS), biomass and onshore wind in 2020–2030 period | 2.0%–4.5% annual fall in primary energy/unit GDP in 2020–2030 period | 2 models have >30 GtCO2/year captured by 2090 | 1 model has net negative emissions by 2100 | - |

| 3 °C | All models solve | CO2 price range $126–382/tCO2 by 2100 | 0.6%–1.4% average annual CO2 increase | 2 models have cost as 0.1%–0.2% of 21st century GDP, 1 model 1.7% of 21st century GDP | All models see no drop in coal capacity factor, so no idling, by 2030 | Over 300 GW each of gas, biomass and onshore wind in 2020–2030 period | 1.5%–2.6% annual fall in primary energy/unit GDP in 2020–2030 period | 2 models have >30 GtCO2/year captured in 2100 | No net negative emissions (lowest 2100 emissions level is 7 GtCO2) | - |

| 4 °C | All models solve | CO2 price range $16–104/tCO2 by 2100 | 1.7%–2.6% average annual CO2 increase | 2 models have cost as 0.02%–0.03% of 21st century, 1 model 0.5% of 21st century GDP | All models see no drop in coal capacity factor, so no idling, by 2030 | Over 300 GW of gas and biomass in 2020–2030 period | 1.2%–1.9% annual fall in primary energy/unit GDP in 2020–2030 period | By 2100, range of capture across models is 8–16 GtCO2/year | No net negative emissions (lowest 2100 emissions level is 45 GtCO2) | - |

| Scenario | Model Solves | CO2 Prices | CO2 Rate of Change (2020–2030) | Mitigation Cost | Idling Of Coal Plant | Technology Deployment Rates (2020–2030) | Energy Intensity Improvement | CO2 Captured | Negative Emissions | Overall |

|---|---|---|---|---|---|---|---|---|---|---|

| 1100 GtCO2 (1.85 °C) | Yes | >$1000/tCO2 increase in CO2 price per decade (in period 2070-2100) | 7.2% average annual CO2 reductions | 2.5% of 21st century GDP | 1400 GW of idle coal plant by 2030 | >1300 GW gas CCS | 2.5% annual fall in primary energy/unit GDP in 2020–2030 period | >30 GtCO2/year captured in 2060 | Net negative emissions by 2070 | - |

| >500 GW biomass CCS | ||||||||||

| 300 GW onshore wind | ||||||||||

| 1340 GtCO2 (2 °C) | Yes | >$1000/tCO2 increase in CO2 price per decade (in period 2080-2100) | 5.2% average annual CO2 reductions | 1.7% of 21st century GDP | 1400 GW of idle coal plant by 2030 | >800 GW Gas CCS | 2.4% annual fall in primary energy/unit GDP in 2020–2030 period | >30 GtCO2/year captured in 2070 | Net negative emissions by 2080 | - |

| >400 GW biomass CCS | ||||||||||

| 300 GW onshore wind |

© 2017 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC-BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gambhir, A.; Drouet, L.; McCollum, D.; Napp, T.; Bernie, D.; Hawkes, A.; Fricko, O.; Havlik, P.; Riahi, K.; Bosetti, V.; et al. Assessing the Feasibility of Global Long-Term Mitigation Scenarios. Energies 2017, 10, 89. https://doi.org/10.3390/en10010089

Gambhir A, Drouet L, McCollum D, Napp T, Bernie D, Hawkes A, Fricko O, Havlik P, Riahi K, Bosetti V, et al. Assessing the Feasibility of Global Long-Term Mitigation Scenarios. Energies. 2017; 10(1):89. https://doi.org/10.3390/en10010089

Chicago/Turabian StyleGambhir, Ajay, Laurent Drouet, David McCollum, Tamaryn Napp, Dan Bernie, Adam Hawkes, Oliver Fricko, Petr Havlik, Keywan Riahi, Valentina Bosetti, and et al. 2017. "Assessing the Feasibility of Global Long-Term Mitigation Scenarios" Energies 10, no. 1: 89. https://doi.org/10.3390/en10010089