Global Transportation Demand Development with Impacts on the Energy Demand and Greenhouse Gas Emissions in a Climate-Constrained World

Abstract

:

1. Introduction

2. Methods and Data

2.1. Transportation Demand Data

2.1.1. The Role of Gross Domestic Product (GDP) and Population in Transportation Demand Projections

2.1.2. Road and Rail Transportation Activity

2.1.3. Marine Transportation Activity

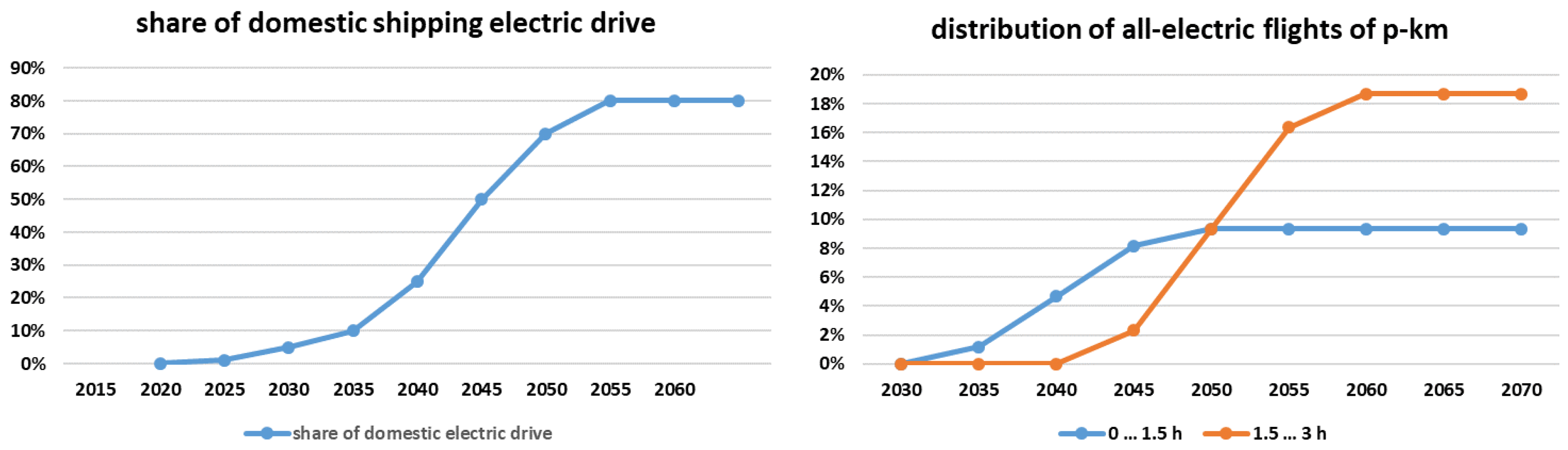

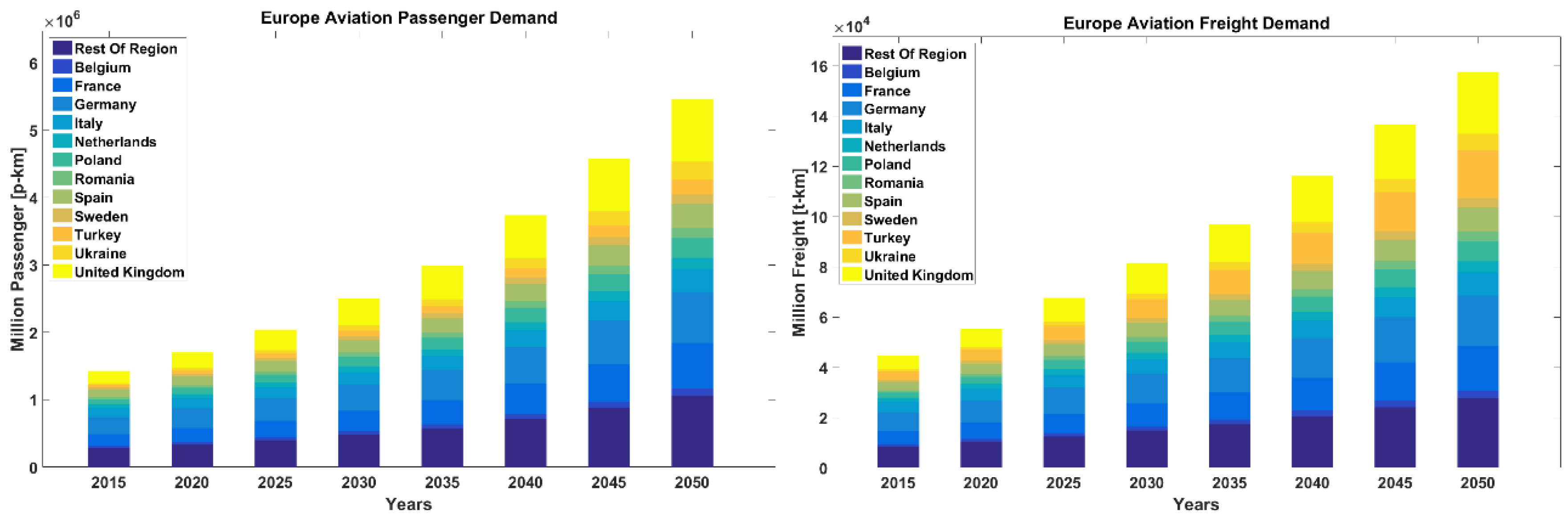

2.1.4. Aviation Transportation Activity

2.2. Specific Energy Demand

2.2.1. Road Specific Energy Demand

2.2.2. Rail Specific Energy Demand

2.2.3. Marine Specific Energy Demand

2.2.4. Aviation Specific Energy Demand

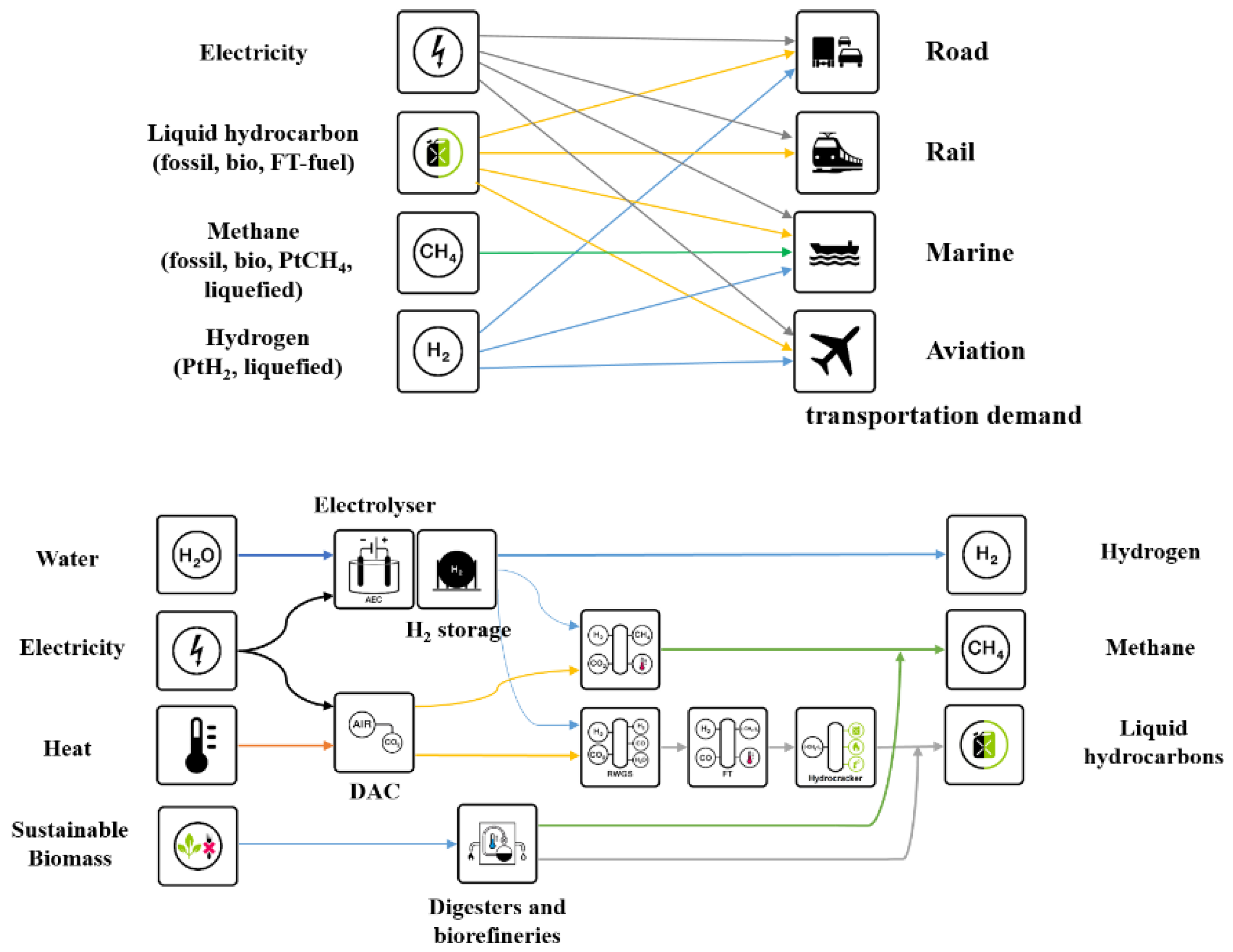

2.3. Fuel-Share Distribution of Transport Modes

- Road: electricity, hydrogen, liquid fuels (liquid hydrocarbons)

- Rail: electricity, liquid fuels (liquid hydrocarbons)

- Marine: electricity, hydrogen, methane, liquid fuels (liquid hydrocarbons)

- Aviation: electricity, hydrogen, liquid fuels (liquid hydrocarbons)

2.4. Capital Expenditures, Operational Expenditures, and Lifetimes for Road Vehicles

2.4.1. Capital Expenditures

2.4.2. Operational Expenditures

2.4.3. Lifetime

2.4.4. Annual Kilometers for the Road Segment

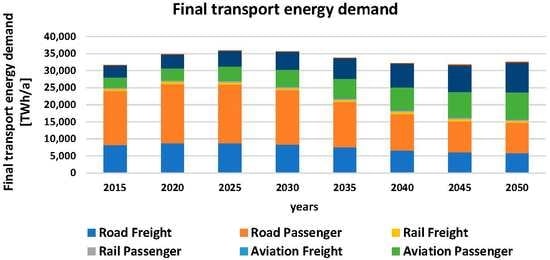

2.5. Global Final Energy Demand in the Transport Sector

2.6. GHG Emissions from the Transport Sector

2.7. Primary Energy Demand and Well-to-Wheel Efficiency

3. Results

3.1. Global, Regional, and Country Level Transportation Demand

3.2. Specific Energy Demand, Road LCOM, and Shares of Vehicle and Fuel Types

3.2.1. Specific Energy Demand

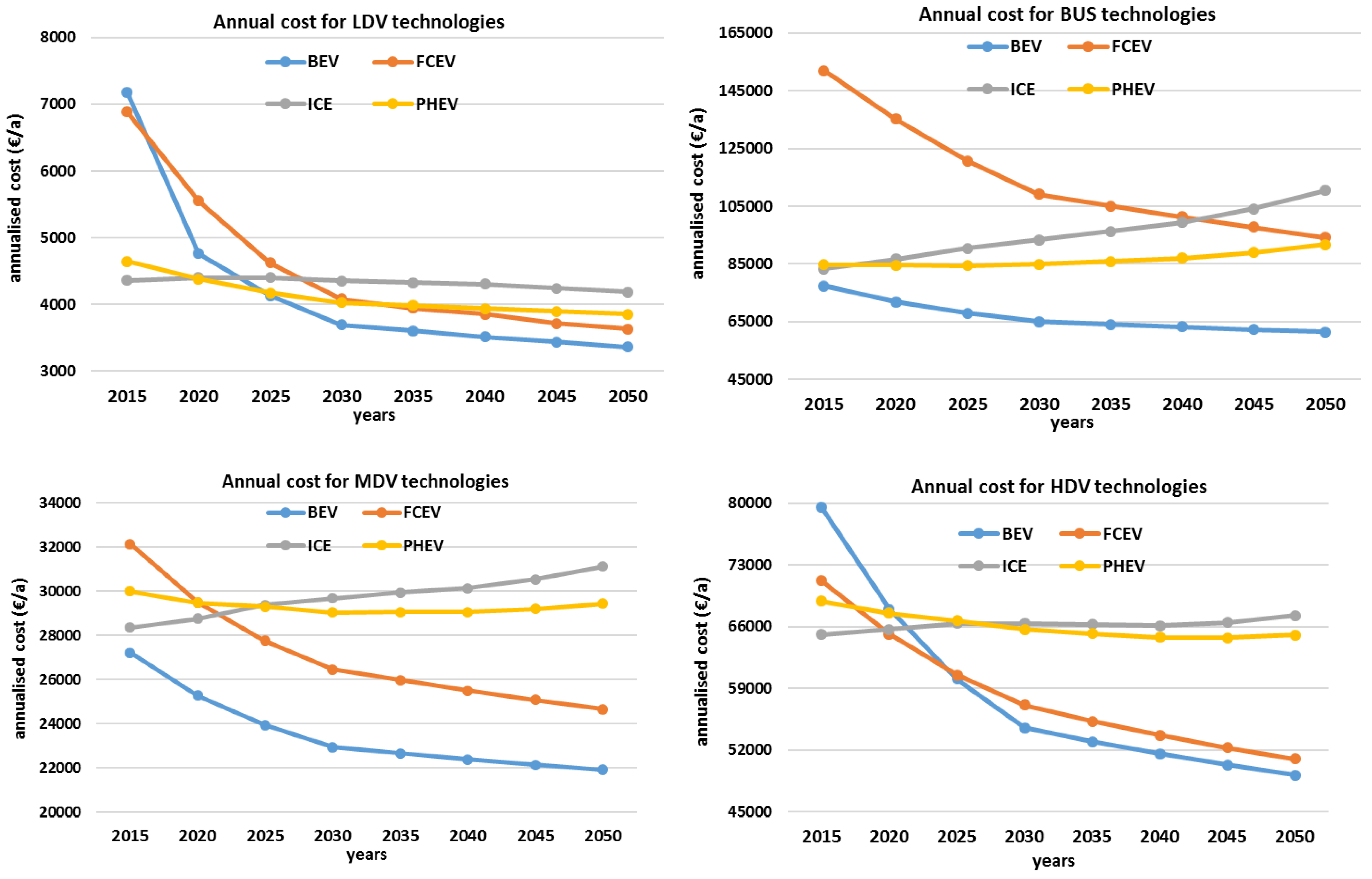

3.2.2. Road LCOM

3.2.3. Vehicles and Fuel Type Shares

3.3. Global Final Energy Demand for the Transport Sector

3.4. Total GHG Emissions in the Transport Sector

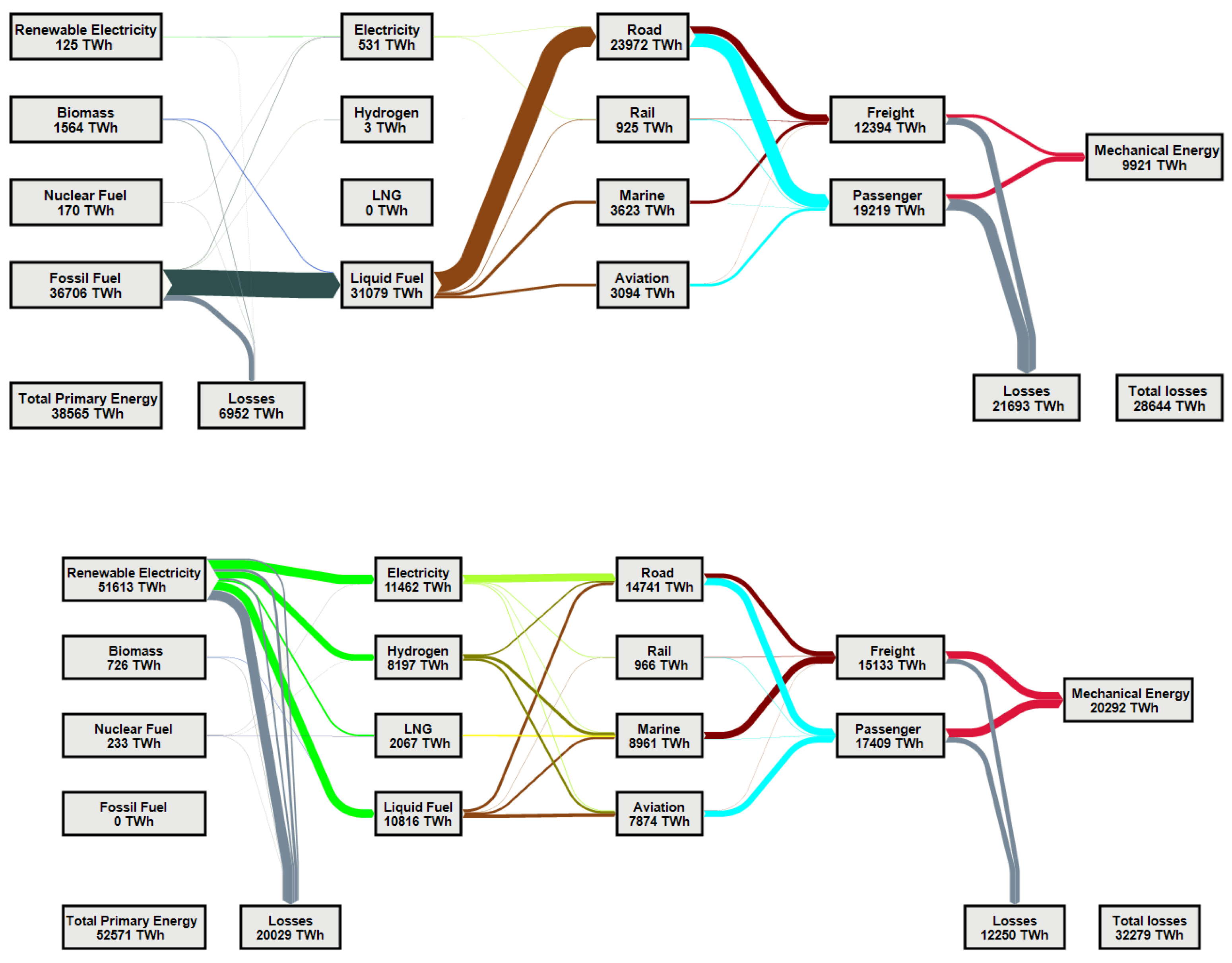

3.5. Primary Energy Demand and Well-to-Wheel Efficiency

4. Discussion

4.1. Data Analysis

4.2. Comparison to Other Results

4.3. Outlook and Further Investigations

5. Conclusions

Supplementary Materials

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Abbreviations

| BEV | battery-electric vehicle |

| BUS | buses |

| COP | conference of parties |

| CAGR | compound annual growth rate |

| Capex | capital expenditure |

| eq | equivalence |

| € | euro |

| FCET | fuel-cell electric truck |

| FCEV | fuel-cell electric vehicle |

| GHG | greenhouse gas |

| GDP | growth domestic product |

| HEV | hybrid electric vehicle |

| HHDT | heavy heavy-duty truck |

| HDV | heavy-duty vehicle |

| ICE | internal combustion engine |

| ICAO | International Civil Aviation Organization |

| ICCT | International Council on Clean Transportation |

| IPCC | Intergovernmental Panel on Climate Change |

| IMO | International Marine Organization |

| GR | growth rate |

| LDV | light duty vehicles |

| LCOM | levelized cost of mobility |

| LHDT | light heavy-duty truck |

| LH2 | liquid hydrogen |

| LNG | liquefied natural gas |

| MDV | medium duty vehicle |

| MHDT | medium heavy-duty truck |

| NG | natural gas |

| Opex | operational expenditure |

| PHEV | plug-in hybrid electric vehicle |

| p-km | passenger kilometer |

| RP-km | revenue passenger kilometers |

| PtG | power-to-gas |

| PtL | power-to-liquids |

| SMR | steam methane reforming |

| t-km | ton kilometers |

| t-mi | ton-miles |

| TTW | Tank-to-Wheel |

| TWh | Terawatt hour |

| UF | utility factor |

| UNCTAD | United Nation Conference on Traded and Development |

| WTW | Well-to-Wheel |

| WTT | Well-to-Tank |

| WTG | Well-to-Grid |

| WACC | weighted average cost of capital |

| 2W | two wheelers |

| 3W | three wheelers |

| Subcripts | |

| el | Electric units |

| th | Thermal units |

| H2 | Hydrogen units |

| CH4 | Methane units |

| DME | Dimethyl ether units |

References

- International Energy Agency (IEA). World Energy Outlook 2017; International Energy Agency: Paris, France, 2017. [Google Scholar]

- United Nations Framework Convention on Climate Change (UNFCCC). Adaptation of the Paris Agreement, COP21. United Nations Framework Convention on Climate Change: Paris, France, 2015. Available online: https://unfccc.int/resource/docs/2015/cop21/eng/l09r01.pdf (accessed on 13 August 2016).

- ExxonMobil. 2017 Outlook for Energy: A View to 2040. ExxonMobil: Irvine, CA, USA, 2017. Available online: https://cdn.exxonmobil.com/~/media/global/files/outlook-for-energy/2017/2017-outlook-for-energy.pdf (accessed on 5 February 2018).

- International Transport Forum (ITF). ITF Transport Outlook 2019; International Transport Forum: Paris, France, 2019; Available online: http://doi.org/10.1787/25202367 (accessed on 23 March 2019).

- Hua, J.; Wu, Y.H.; Jin, F.P. Prospects for renewable energy for seaborne transportation—Taiwan example. Renew. Energy 2008, 33, 1056–1063. [Google Scholar] [CrossRef]

- Creutzig, F. Evolving narratives of low-carbon futures in transportation. Transp. Rev. 2015, 36, 341–360. [Google Scholar] [CrossRef]

- Baronti, F.; Chow, M.Y.; Ma, C.; Rahimi-Eichi, H.; Saletti, R. E-transportation: The role of embedded systems in electric energy transfer from grid to vehicle. EURASIP J. Embed. Syst. 2016, 2016, 11. [Google Scholar] [CrossRef]

- Royal Belgian Council of Applied Science. Hydrogen as an Energy Carrier. Royal Belgian Council of Applied Science: Belgium, 2006. Available online: http://www.kvab.be/sites/default/rest/blobs/1125/tw_BACAS_hydrogen_as_an_energy_carrier.pdf (accessed on 11 July 2017).

- International Energy Agency (IEA). Global EV Outlook 2018. Towards Cross-Model Electrification; International Energy Agency: Paris, France, 2018. [Google Scholar]

- German Aerospace Center. Development of the Car Fleet in EU28+2 to Achieve the Paris Agreement Target to Limit Global Warming to 1.5 °C. Cologne, Germany, 2018. Available online: https://www.greenpeace.de/sites/www.greenpeace.de/files/publications/20180907_gp_eucarfleet_1.5.pdf (accessed on 5 June 2019).

- International Energy Agency (IEA). Hybrid and Electric Vehicles, IA-HEV, The Electric Drive Delivers; International Energy Agency: Paris, France, 2015. [Google Scholar]

- Liu, H.; MA, J.; Tong, G.; Zheng, Z.; Yao, M. Investigation on the potential of high efficiency for internal combustion engines. Energies 2018, 11, 513. [Google Scholar] [CrossRef]

- Transport and Environment. Don’t Breathe Here, Beware the Invisible Killer; Transport and Environment: Brussels, Belgium, 2015. Available online: https://www.transportenvironment.org/sites/te/files/publications/Dont_Breathe_Here_exec_summary_FINAL.pdf (accessed on 15 August 2018).

- International Energy Agency (IEA). Energy and Air Pollution; World Energy Outlook: Paris, France, 2016. [Google Scholar]

- Singer, M. Consumer Views on Plug-in Electric Vehicles-National Benchmark Report; National Renewable Energy Laboratory (NREL): Golden, CO, USA, 2016. Available online: https://www.nrel.gov/docs/fy17osti/67107.pdf (accessed on 11 August 2017).

- Zhang, Q.; Ou, X.; Yan, X.; Zhang, X. Electric vehicle market penetration and impacts on energy consumption and CO2 emissions in the future: Beijing case. Energies 2017, 10, 228. [Google Scholar] [CrossRef]

- Plötz, P.; Funke, S. Real-World Fuel Economy and CO2 Emissions of Plug-in Hybrid Electric Vehicles; Fraunhofer Institute for Systems and Innovation Research: Karlsruhe, Germany, 2015; Available online: https://www.isi.fraunhofer.de/content/dam/isi/dokumente/sustainability-innovation/2015/WP01-2015_Real-world-fuel-economy-and-CO2-emissions-of-PHEV_Ploetz-Funke-Jochem-Patrick.pdf (accessed on 9 March 2017).

- Varga, B.; Sagoian, A.; Mariasiu, F. Prediction of electric vehicle range: A comprehensive review of current issues and challenges. Energies 2019, 12, 946. [Google Scholar] [CrossRef]

- Hummel, P. Evidence Lab Electric Car Teardown—Disruption Ahead? UBS: Zurich, Switzerland, 2017. Available online: https://neo.ubs.com/shared/d1wkuDlEbYPjF/ (accessed on 29 February 2018).

- Schmidt, B. Tesla Extends Range to Near 600 km, Says New Batteries Will Last 1.6 Million Kms. 2019. Available online: https://thedriven.io/2019/04/24/tesla-extends-range-to-near-600km-says-new-batteries-will-last-1-6-million-kms/ (accessed on 12 April 2018).

- Emadi, A. Transportation 2. IEEE Power Energy Mag. 2011, 9, 18–29. [Google Scholar] [CrossRef]

- Un-Noor, F.; Padmanaban, S.; Mihet-popa, L.; Mollah, M.; Hossain, E. A Comprehensive Study of Key Electric (EV) Components, Technologies, Challenges, Impacts, and Future Direction of Development. Energies 2017, 10, 1217. [Google Scholar] [CrossRef]

- Kurtz, J.; Sprik, S.; Saur, G.; Onorato, S. On-Road Fuel Cell Electric Vehicles Evaluation: Overview. National Renewable Energy Laboratory (NREL): Golden, CO, USA, 2018. Available online: https://www.nrel.gov/docs/fy19osti/73009.pdf (accessed on 3 March 2019).

- FuelCellToday. Fuel Cell Electric Vehicles: The Road Ahead. FuelCellToday: London, UK, 2013. Available online: http://www.fuelcelltoday.com/media/1711108/fuel_cell_electric_vehicles_-_the_road_ahead_v3.pdf (accessed on 13 June 2016).

- Lee, D.; Elgowainy, A.; Kotz, A.; Vijayagopal, R. Marcinkoski. Life-cycle implications of hydrogen fuel cell electric vehicle technology for medium- and heavy-duty trucks. J. Power Sour. 2018, 393, 217–229. [Google Scholar] [CrossRef]

- Lipman, T.; Elke, M.; Lidicker, J. Hydrogen fuel cell electric vehicle performance and user-response assessment: Results of an extended driver study. Int. J. Hydrog. Energy 2018, 43, 12442–12454. [Google Scholar] [CrossRef]

- Kaa, G.V.D.; Scholtan, D.; Rezaei, J.; Milcharm, C. The battle between battery and fuel cell powered electric vehicle: A BWM approach. Energies 2017, 10, 1707. [Google Scholar] [CrossRef]

- Transport and Environment. Electric Surge: Carmakers’ Electric Car Plans Across Europe 2019–2025; Transport and Environment: Brussels, Belgium, 2019; Available online: https://www.transportenvironment.org/sites/te/files/publications/2019_07_TE_electric_cars_report_final.pdf (accessed on 10 November 2018).

- DNV. GL. Energy Transition Outlook 2019, A Global and Regional Forecast to 2050; London, UK. Available online: https://eto.dnvgl.com/2019#ETO2019-top (accessed on 12 September 2019).

- Schmitt, B. German Auto Industry Battles Over the Electric Future. 2019. Available online: https://www.thedrive.com/tech/27841/german-auto-industry-battles-over-the-electric-future (accessed on 30 May 2019).

- International Energy Agency (IEA). Railway Handbook 2017. Energy Consumption and CO2 Emissions, Focus on Passenger Rail Services; International Energy Agency: Paris, France, 2017. [Google Scholar]

- International Union of Railways (UCI). Technologies and Potential Development for Energy Efficiency and CO2 Reductions in Rail Systems; International Union of Railways: Paris, France, 2016; Available online: https://uic.org/IMG/pdf/_27_technologies_and_potential_developments_for_energy_efficiency_and_co2_reductions_in_rail_systems._uic_in_colaboration.pdf (accessed on 19 April 2018).

- International Energy Agency (IEA). The Future of Rail Opportunities for Energy and The Environment; International Energy Agency (IEA): Paris, France, 2019. [Google Scholar]

- Greenpeace. Energy [r] Evolution. A Sustainable World Energy Outlook 2015, 100% Renewable Energy for All; Greenpeace. Energy [r] Evolution: Amsterdam, The Netherlands, 2015; Available online: https://www.greenpeace.de/sites/www.greenpeace.de/files/publications/greenpeace_energy-revolution_erneuerbare_2050_20150921.pdf (accessed on 12 April 2018).

- Petzinger, J. The World’s First Hydrogen-Powered Train Hits the Tracks in Germany. 2018. Available online: https://qz.com/1392287/the-worlds-first-hydrogen-powered-train-hits-the-tracks-in-germany/ (accessed on 23 December 2018).

- Horvath, S.; Fasihi, M.; Breyer, C. Techno-economic analysis of a decarbonized shipping sector: Technology suggestions for a fleet in 2030 and 2040. Energy Convers. Manag. 2018, 164, 230–241. [Google Scholar] [CrossRef]

- Grenzeback, L.R.; Brown, A.; Fischer, M.J.; Hutson, N.; Lamm, C.R.; Pei, Y.L.; Vimmerstedt, L.; Vyas, A.D.; Winebrake, J.J. Freight Transportation Demand: Energy-Efficient Scenarios for a Low-Carbon Future; Transportation Energy Future Series; DOE/GO-102013-3711; Cambridge Systematics, Inc.: Cambridge, UK; National Renewable Energy Laboratory: Golden, CO, USA; U.S. Department of Energy: Washington, DC, USA, 2013; 82. Available online: https://www.nrel.gov/docs/fy13osti/55641.pdf (accessed on 19 May 2017).

- International Transport Forum (ITF). Reducing Shipping Greenhouse Gas Emissions: Lessons from Port-Based Incentives; International Transport Forum: Paris, France, 2018; Available online: https://www.itf-oecd.org/sites/default/files/docs/reducing-shipping-greenhouse-gas-emissions.pdf (accessed on 23 December 2018).

- Bakhtov, A. Alternative Fuels for Shipping in the Baltic Sea Region (HELCOM 2019). Available online: http://www.helcom.fi/Lists/Publications/HELCOM-EnviSUM-Alternative-fuels-for-shipping.pdf (accessed on 12 April 2018).

- Raucci, C. The Potential of Hydrogen to Fuel International Shipping. UCL Energy Institute. Ph.D. Thesis, University College London, London, UK, February 2017. Available online: http://discovery.ucl.ac.uk/1539941/1/PhD%20Thesis%20Carlo%20Raucci%20Final.pdf (accessed on 2 May 2018).

- Jafarzadeh, S.; Schjolberg, I. Operational profiles ships in Norwegian water: An activity-based approach to assess the benefits of hybrid and electric propulsion. Transp. Res. Part D 2018, 65, 500–523. [Google Scholar] [CrossRef]

- Yu, J.; Vob, S.; Tang, G. Strategy development for retrofitting ships for implementing shore side electricity. Transp. Res. Part D 2019, 74, 201–213. [Google Scholar] [CrossRef]

- Lim, C.; Park, B.; Lee, J.; Kim, E.S.; Shin, S. Electric power consumption predictive modeling of an electric propulsion ship considering the marine environment. Int. J. Nav. Archit. Ocean Eng. 2019, 11, 765–781. [Google Scholar] [CrossRef]

- Kanellos, F.; Moghaddam, A.A.; Guerrero, J.M. A cost-effective and emission-aware power management system for ships with integrated full electric propulsion. Electr. Power Syst. Res. 2017, 150, 63–75. [Google Scholar] [CrossRef] [Green Version]

- Moore, R. World’s Most Powerful All-Electric Ferry to Enter Operations. 2019. Available online: https://www.rivieramm.com/news-content-hub/worldrsquos-most-powerful-all-electric-ferry-to-enter-operations-55117 (accessed on 28 June 2018).

- International Air Transport Association (IATA). IATA 2015 Report on Alternative Fuels; International Air Transport Association: Geneva, Switzerland, 2015; Available online: https://www.iata.org/publications/Documents/2015-report-alternative-fuels.pdf (accessed on 16 July 2017).

- Han, H.; Yu, J.; Kim, W. An electric airplane: Assessing the effect of travelers’ perceived risk, attitude, and new product knowledge. J. Air Transp. Manag. 2019, 78, 33–42. [Google Scholar] [CrossRef]

- Kadyk, T.; Winnefeld, C.; Hanke-Rauschenbach, R.; Krewer, U. Analysis and Design of Fuel Cell Systems for Aviation. Energies 2018, 11, 375. [Google Scholar] [CrossRef]

- German Environment Agency (UBA). Power-To-Liquids. Potential and Perspectives for the Future Supply of Renewable Aviation Fuel; German Environment Agency (UBA): Berlin, Germany, 2016. Available online: http://www.lbst.de/news/2016_docs/161005_uba_hintergrund_ptl_barrierrefrei.pdf (accessed on 12 July 2018).

- Baroutaji, A.; Wilberforce, T.; Ramadan, M.; Olabi, A.G. Comprehensive investigation on hydrogen and fuel cell technology in the aviation and aerospace sectors. Renew. Sustain. Energy Rev. 2019, 106, 31–40. [Google Scholar] [CrossRef] [Green Version]

- Fireman, H.; Arbor, A. Designing All Electric Ships. Ninth International Marine Design Conference 2006, University of Michigan, Department USA. NA&ME, Designing All Electric Ships, IMDC’06, 16 May 2006, NAVSEA. Available online: https://pdfs.semanticscholar.org/presentation/1291/50a6ce6311ca5cf489f48081d249f0a87f5c.pdf (accessed on 28 June 2018).

- The Guardian. Norway Aims for All Short-Haul Flights to Be 100% Electric by 2040. The Guardian: London, UK, 2018; Available online: https://www.theguardian.com/world/2018/jan/18/norway-aims-for-all-short-haul-flights-to-be-100-electric-by-2040 (accessed on 17 March 2018).

- Reimers, J.O. Introduction of Electric Aviation in Norway. Green Future: Norway, 2018. Available online: https://avinor.no/contentassets/c29b7a7ec1164e5d8f7500f8fef810cc/introduction-of-electric-aircraft-in-norway.pdf (accessed on 12 May 2017).

- Hepperle, M. Electric Flight—Potential and Limitation. NATO, OTAN, German Aerospace Center Sto-MP-AVT-209. Available online: https://www.mh-aerotools.de/company/paper_14/MP-AVT-209-09.pdf (accessed on 11 February 2018).

- Colbertaldo, P.; Guandalini, G.; Campanari, S. Modelling the integrated power and transport energy system: The role of power-to-gas and hydrogen in long-term scenarios for Italy. Energy 2018, 154, 592–601. [Google Scholar] [CrossRef]

- Bellocchi, S.; Falco, M.D.; Gambini, M.; Manno, M.; Stilo, T.; Vellini, M. Opportunities for power-to-Gas and Power-to-liquid in CO2-reduced energy scenarios: The Italian case. Energy 2019, 175, 847–861. [Google Scholar] [CrossRef]

- Child, M.; Koskinen, O.; Linnanen, L.; Breyer, C. Sustainability guardrails for energy scenarios of the global energy transition. Renew. Sustain. Energy Rev. 2018, 91, 321–334. [Google Scholar] [CrossRef]

- Kahn Ribeiro, S.; Kobayashi, S.; Beuthe, M.; Gasca, J.; Greene, D.; Lee, D.S.; Muromachi, Y.; Newton, P.J.; Plotkin, S.; Sperling, D.; et al. Transport and its infrastructure. In Climate Change 2007: Mitigation; Contribution of Working Group III to the Fourth Assessment Report of the Intergovernmental Panel on Climate Change; Cambridge University Press: Cambridge, UK, 2007. [Google Scholar]

- Royal Automobile Club Foundation. Travel Demand and its Causes. Motoring towards 2050-Roads and Reality. Royal Automobile Club Foundation: London, UK, 2008. Available online: https://www.racfoundation.org/assets/rac_foundation/content/downloadables/roads%20and%20reality%20-%20bayliss%20-%20travel%20demand%20and%20its%20causes%20-%20150708%20-%20background%20paper%203.pdf (accessed on 12 March 2017).

- Fang, B.; Han, X. Relating Transportation To GDP: Concepts, Measures, and Data; MacroSys Research and Technology. MacroSys: Washington, DC, USA. Available online: http://www.e-ajd.net/source-pdf/nouveau/ajd-41-fang-han-4-december-2000.pdf (accessed on 16 March 2018).

- Garcia, C.; Levy, S.; Limäo, S.; Kupfer, F. Correlation Between Transport Intensity and GDP in European Regions: A New Approach, 8th Swiss Transport Research Conference, Monte Verit/Ascona. 2008. Available online: http://www.strc.ch/2008/2008_Garcia_Levy_Limao_Kupfer_TransportIntensity_GDP.pdf (accessed on 14 May 2017).

- United Nations, Department of Economic and Social Affairs, Population Division. World Population Prospects: The 2015 Revision, Key Findings and Advance Tables. Working Paper No. ESA/P/WP.241. New York. Available online: https://population.un.org/wpp/DataQuery/ (accessed on 24 December 2017).

- Toktarova, A.; Gruber, L.; Hlusiak, M.; Bogdanov, D.; Breyer, C. Long term load projection in high resolution for all countries globally. Int. J. Electr. Power Energy Syst. 2019, 111, 160–181. [Google Scholar] [CrossRef]

- International Council on Clean Transportation (ICCT). Global Transportation Roadmap; International Council on Clean Transportation: Washington, DC, USA, 2012; Available online: www.theicct.org/transportation-roadmap (accessed on 26 July 2016).

- International Marine Organization (IMO). Third IMO Greenhouse Gas Study 2014; International Marine Organization: Suffolk, UK, 2014; Available online: http://www.imo.org/en/OurWork/Environment/PollutionPrevention/AirPollution/Documents/Third%20Greenhouse%20Gas%20Study/GHG3%20Executive%20Summary%20and%20Report.pdf (accessed on 25 October 2017).

- Fasihi, M.; Bogdanov, D.; Breyer, C. Techno-economic assessment of power-to-liquid (PtL) fuels production and global trading based on Hybrid PV-Wind power plants. Energy Procedia 2016, 99, 243–268. [Google Scholar] [CrossRef]

- Fasihi, M.; Bogdanov, D.; Breyer, C. Long-term hydrocarbon trade options for the Maghreb region and Europe—renewable energy based synthetic fuels for a net zero emissions world. Sustainability 2016, 9, 306. [Google Scholar] [CrossRef]

- Heuser, P.M.; Ryberg, D.S.; Grube, T.; Robinius, M.; Stolten, D. Techno-economic analysis of a potential energy trading link between Patagonia and Japan based on CO2 free hydrogen. Int. J. Hydrog. Energy 2019, 44, 12733–12747. [Google Scholar] [CrossRef]

- The Intergovernmental Panel on Climate Change (IPCC). IPCC 5th Assessment report: Working Group III—Mitigation of Climate Change. Geneva, Switzerland, 2014. Available online: http://www.ipcc.ch/ (accessed on 10 November 2017).

- European Commission (EC). EU Transport in Figures, Statistical Pocketbook 2012. European Commission: Brussels, Belgium, 2012. Available online: https://ec.europa.eu/transport/sites/transport/files/facts-fundings/statistics/doc/2012/pocketbook2012.pdf (accessed on 22 March 2016).

- International Civil Aviation Organization (ICAO). Appendix 1. Tables Relating to the World of Air Transport in 2015; International Civil Aviation Organization: Montreal, QC, Canada, 2015; Available online: https://www.icao.int/annual-report-2015/Documents/Appendix_1_en.pdf (accessed on 13 April 2017).

- International Civil Aviation Organization (ICAO). Committee on Aviation Environmental Protection (CAEP), Agenda Item 3: Forecasting and Economic Analysis Support Group (FESG); International Civil Aviation Organization: Lima, Peru, 2008; Available online: http://s3.amazonaws.com/zanran_storage/www.icao.int/ContentPages/108603156.pdf (accessed on 26 March 2018).

- Heywood, J.; Mackenzie, D. On the Road Toward 2050: Potential for Sustainable Reductions in Light-Duty Vehicles Energy Use and Greenhouse Gas Emissions. Available online: http://web.mit.edu/sloan-auto-lab/research/beforeh2/files/On-the-Road-toward-2050.pdf (accessed on 18 June 2017).

- Plötz, P.; Funke, S.A.; Jochem, P. Emprirical fuel consumption and CO2 emissions of plug-in hybrid electric vehicles. J. Ind. Ecol. 2017, 22, 4. [Google Scholar] [CrossRef]

- Mendes, M.; Duarte, G.; Baptista, P. Introducing specific power to bicycle and motorcycles: Application to electric mobility. Transp. Res. Part C Emerg. Technol. 2015, 51, 120–135. [Google Scholar] [CrossRef]

- CIVITAS. Cleaner and Smarter Transport in Cities. Smart Choices for Cities. Policy Note, Clean Buses for City, CIVITAS: Belgium, 2013. Available online: http://civitas.eu/sites/default/files/civ_pol-an_web.pdf (accessed on 9 January 2018).

- Transportation Research Center—University of Vermont (UVM TRC). Plug-in Hybrid Electric Vehicle Research Project: Phase II Report. Available online: http://www.greenmtn.edu/wordpress/wp-content/uploads/phev-final-report-april2010.pdf (accessed on 15 April 2018).

- Boer, E.D.; Aarnink, S. Zero Emissions Trucks, An Overview of State-Of-The-Art Technologies and Their potential. DLR, D-70569. Available online: https://www.theicct.org/sites/default/files/publications/CE_Delft_4841_Zero_emissions_trucks_Def.pdf (accessed on 1 July 2017).

- Fulton, L.; Eads, G. IEA/SMP Model Documentation and Reference Case Projection. Paris, France, 2004. Available online: http://www.libralato.co.uk/docs/SMP%20model%20guidance%202004.pdf (accessed on 16 March 2018).

- Schäfer, A.; Dray, L.; Andersson, E.; Ben-Akiva, M.E.; Berg, M.; Boulouchos, K.; Dietrich, P.; Fröidh, O.; Graham, W.; Kok, R.; et al. TOSCA Project Final Report: Description of the Main S&T Results/Foregrounds. California, 2011. TOSCA, EC FP7 Project. Available online: http://www.transport-research.info/sites/default/files/project/documents/20120406_000154_97382_TOSCA_FinalReport.pdf (accessed on 14 May 2017).

- DNV GL. Fuels & Fuel Converters (Future). Maritime Academy. NTNU, Norwegian University of Science and Technology: Trondheim, Norway. Available online: https://www.ntnu.edu/documents/20587845/1266707380/01_Fuels.pdf/1073c862-2354-4ccf-9732-0906380f601e (accessed on 3 December 2017).

- Becken, S. Tourism and Oil, Preparing for the Challenge; Channel View Publications; Tourism Essential: Bristol, UK, 2015. [Google Scholar]

- Air, B.P. Handbook of Products. Air BP Ltd.: London, UK, 2000. Available online: https://web.archive.org/web/20110608075828/http://www.bp.com/liveassets/bp_internet/aviation/air_bp/STAGING/local_assets/downloads_pdfs/a/air_bp_products_handbook_04004_1.pdf (accessed on 2 May 2018).

- Mueller, J.K.; Bensmann, A.; Bensmann, B. Design Considerations for the Electrical Power Supply of Future Civil Aircraft with Active High-Lift Systems. Energies 2018, 11, 179. [Google Scholar] [CrossRef]

- Parfomak, P.W.; Frittelli, J.; Lattanzio, R.K.; Patner, M. LNG as a Marine Fuel: Prospects and Policy. Congressional Research Service: Washington, DC, USA, 2019. Available online: https://fas.org/sgp/crs/misc/R45488.pdf (accessed on 19 October 2017).

- Misyris, G.S.; Marinopoulos, A.; Doukas, D.I.; Tengner, T.; Labridis, D.P. On battery state estimation algorithms for electric ship applications. Electr. Power Syst. Res. 2017, 151, 115–124. [Google Scholar] [CrossRef]

- National Post. Norway is Building Some of the World’s first Battery-Powered Ferries. Will They Lead the Way in Cutting Maritime Pollution? Toronto, Ontario, 2018. Available online: https://nationalpost.com/news/world/will-new-electric-ferries-lead-the-way-in-cutting-maritime-pollution (accessed on 18 September 2018).

- Newsweek. World’s First Electric Ships Now Sailing in China-and Hauling Coal. USA, 2017. Available online: https://www.newsweek.com/worlds-first-electric-ship-now-sailing-china-and-hauling-coal-740015 (accessed on 28 April 2018).

- International Council on Clean Transportation (ICCT). Greenhouse Gas Emissions from Global Shipping, International Council on Clean Transportation, 2013–2015; International Council on Clean Transportation: Washington, DC, USA, 2017; Available online: https://www.theicct.org/sites/default/files/publications/Global-shipping-GHG-emissions-2013-2015_ICCT-Report_17102017_vF.pdf (accessed on 21 January 2018).

- Jacobson, M.Z.; Delucchi, M.A.; Bauer, Z.A.; Goodman, S.C.; Chapman, W.E.; Cameron, M.A.; Bozonnat, C.; Chobadi, L.; Clonts, H.A.; Enevoldsen, P.; et al. 100% Clean and Renewable Wind, Water, and Sunlight All-Sector Energy Roadmaps for 139 Countries of the World. Joule 2017, 1, 1–14. [Google Scholar] [CrossRef]

- Wilkerson, J.; Jacobson, M.Z.; Malwitz, A.; Wayson, R.; Naiman, A.D.; Lele, S.K.; Balasubramanian, S.; Fleming, G. Analysis of emission data from global commercial aviation: 2004 and 2006. Atmos. Chem. Phys. 2010, 10, 6391–6408. [Google Scholar] [CrossRef] [Green Version]

- Hagedorn, G.; Kalmus, P.; Mann, M.; Vicca, S.; Berge, J.V.D.; Van Ypersele, J.-P.; Bourg, D.; Rotmans, J.; Kaaronen, R.; Rahmstorf, S.; et al. Concerns of young protesters are justified. Science 2019, 364, 139–140. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Hagedorn, G.; Loew, T.; Seneviratne, S.I.; Lucht, W.; Beck, M.-L.; Hesse, J.; Knutti, R.; Quaschning, V.; Schleimer, J.-H.; Mattauch, L.; et al. The concerns of the young protesters are justified: A statement by scientists for future concerning the protests for more climate protection. GAIA 2019, 28, 79–87. [Google Scholar] [CrossRef]

- Thomson, R. EasyJet CEO Johan Lundgren: Electric Planes within 10 years—Electrical Propulsion Reduces Environmental Footprint, Point of Views. Roland Berger: London, UK, 2018. Available online: https://www.rolandberger.com/en/Point-of-View/easyJet-CEO-Johan-Lundgren-Electric-planes-within-10-years.html (accessed on 20 September 2019).

- Bogdanov, D.; Farfan, J.; Sadovskaia, K.; Aghahosseini, A.; Child, M.; Gulagi, A.; Oyewo, A.S.; Barbosa, L.D.S.N.S.; Breyer, C. Radical transformation pathway towards sustainable electricity via evolutionary steps. Nat. Commun. 2019, 10, 1077. [Google Scholar] [CrossRef]

- Vliet, O.; Brouwer, A.S.; Kuramochi, T.; Brok, M.V.D.; Faaij, A. Energy use, cost and CO2 emissions of electric cars. J. Power Sources 2010, 196, 2298–2310. [Google Scholar] [CrossRef]

- Curry, C. Lithium-Ion Battery Cost and Market. Lithium-Ion Battery Cost and Market. Squeezed Margins Seek Technology Improvements & New Business Models. Bloomberg New Energy Finance: New York, NY, USA, 2017. Available online: https://data.bloomberglp.com/bnef/sites/14/2017/07/BNEF-Lithium-ion-battery-costs-and-market.pdf (accessed on 12 July 2018).

- Nguyen, T.; Ward, J. Life-Cycle Costs of Mid-Size Light-Duty Vehicles, Program Record (Office of Vehicle Technologies & Fuel Cell Technologies). Washington, DC, USA, 2013. Available online: https://www.hydrogen.energy.gov/pdfs/13006_ldv_life_cycle_costs.pdf (accessed on 11 March 2018).

- Bubeck, S.; Tomaschek, J.; Fahl, U. Perspective of electric mobility: Total cost of ownership of electric vehicles in Germany. Transp. Policy 2016, 50, 63–77. [Google Scholar] [CrossRef]

- Lajunen, A.; Lipman, T. Lifecycle cost assessment and carbon dioxide emissions of diesel natural gas, hybrid electric, fuel cell hybrid and electric transit buses. Energy 2016, 106, 329–342. [Google Scholar] [CrossRef]

- Lajunen, A. Evaluation of battery requirements for hybrid and electric city buses. World Electr. Veh. J. 2012, 5, 340–349. [Google Scholar] [CrossRef]

- Yeon, L.D.; Thomas, V.M. Parametric modeling approach for economic and environmentally life cycle assessment of medium-duty truck electrification. J. Clean. Prod. 2017, 142, 3300–3321. [Google Scholar] [CrossRef]

- Lee, A.H.; Kim, N.W.; Jeong, J.R.; Park, Y.I.; Cha, A.W. Component sizing and engine optimal operation line analysis for a plug-in hybrid electric transit bus. J. Clean. Prod. 2013, 14, 459–469. [Google Scholar] [CrossRef]

- Kast, J.; Vijayagopal, R.; Gangloff, J.J.; Marcinkoski, J. Clean commercial transportation: Medium and heavy duty fuel cell electric trucks. Int. J. Hydrog. Energy 2017, 42, 4508–4517. [Google Scholar] [CrossRef] [Green Version]

- Laitila, J.; Asikainen, A.; Ranta, T. Cost analysis of transporting forest chips and forest industry by-product with large truck-trailers in Finland. Biomass Bioenergy 2016, 90, 252–261. [Google Scholar] [CrossRef]

- Ars Technica. Tesla Announce Truck Prices Lower than Experts Predicted. 2017. Available online: https://arstechnica.com/cars/2017/11/teslas-expected-truck-prices-are-much-lower-than-experts-predicted/ (accessed on 24 October 2017).

- DMV.ORG. Average Car Insurance Rates. USA. Available online: https://www.dmv.org/insurance/average-car-insurance-rates.php (accessed on 17 November 2017).

- EZ-EV. Electric Cars vs. Gas Cars: Comparing Maintenance & Battery Costs. Available online: https://ez-ev.com/tips/electric-cars-vs-gas-maintenance-battery-cost (accessed on 25 February 2018).

- Trusted Choice. How Much Does Commercial Vehicle Insurance Cost? USA. Available online: https://www.trustedchoice.com/commercial-vehicle-insurance/compare-coverage/rate-cost/ (accessed on 13 May 2018).

- Trusted Choice. Commercial Truck Insurance Light, Medium, Heavy & Extra Heavy. USA. Available online: https://truckinsurance.mobi/ (accessed on 26 March 2017).

- Bento, A.; Roth, K.; Zou, Y. Vehicle Lifetime Trend and Scrappage Behavior in the U.S. Used Car Market. Energy J. Int. Assoc. Energy Econ. 2016, 39. [Google Scholar] [CrossRef]

- Dun, C.; Horton, G.; Kollamthodi, S. Improvements to the Definition of Lifetime Mileage of Light Duty Vehicles. Ricardo-AEA: London, UK, 2015. Available online: https://ec.europa.eu/clima/sites/clima/files/transport/vehicles/docs/ldv_mileage_improvement_en.pdf (accessed on 24 August 2018).

- Guenther, C.; Schott, B.; Hennings, W.; Waldowski, P.; Danzer, A.M. Model-based investigation of electric vehicle aging by means of vehicle-to-grid scenario simulations. J. Power Sour. 2013, 239, 604–610. [Google Scholar] [CrossRef]

- Laver, R.; Schneck, D.; Skorupski, D.; Brady, S.; Cham, L. Useful Life of Transit Buses and Vans; Report No. FTA VA-26-7229-07.1; U.S. Department of Transportation Federal Transit Administration: Washington, DC, USA, 2007. Available online: https://www.transitwiki.org/TransitWiki/images/6/64/Useful_Life_of_Buses.pdf (accessed on 23 September 2017).

- Vilppo, O.; Markkula, J. Feasibility of electric buses in public transport. World Electr. Veh. J. 2015, 7, 357–365. [Google Scholar] [CrossRef]

- Norregaard, K.; Johsen, B.; Gravesen, C.H. Battery Degradation in Electric Buses. Danish Technological Institute: Taastrup, Denmark, 2016; Available online: https://www.trafikstyrelsen.dk/~/media/Dokumenter/06%20Kollektiv%20trafik/Forsogsordningen/2013/Elbusser/Battery%20degradation%20in%20electric%20buses%20-%20final.pdf (accessed on 12 March 2018).

- Martinez-Laserna, E.; Herrera, V.; Gandiaga, I.; Milo, A.; Sarasketa-Zabala, E.; Gaztañaga, H. Li-Ion battery lifetime Model’s influence on the economic assessment of a hybrid electric bus’s operation. World Electr. Veh. J. 2018, 9, 28. [Google Scholar] [CrossRef]

- Weinert, J.; Ogden, J.; Sperling, D.; Burke, A. The future of electric two-wheelers and electric vehicle in China. Energy Policy 2008, 36, 2544–2555. [Google Scholar] [CrossRef]

- European Environment Agency (EEA). Average Age of the Vehicle Fleet. European Environment Agency: Copenhagen, Denmark, 2016; Available online: https://www.eea.europa.eu/data-and-maps/indicators/average-age-of-the-vehicle-fleet/average-age-of-the-vehicle-8 (accessed on 5 August 2018).

- International Panel on Climate Change (IPCC). Energy. 1996 IPCC. Guidelines for National Greenhouse Gas Inventories: Reference Manual, Chapter 1 Energy. Italy. Available online: https://www.ipcc-nggip.iges.or.jp/public/2006gl/ (accessed on 18 January 2017).

- Rahman, M.M.; Canter, C.; Kumar, A. Well-to-wheel life cycle assessment of transportation fuels derived from different North American conventional crudes. Appl. Energy 2015, 156, 159–173. [Google Scholar] [CrossRef]

- Wang, M.; Han, J.; Dunn, J.B.; Cai, H.; Elgowainy, A. Well-to-wheels energy use and greenhouse gas emissions of ethanol from corn, sugarcane and cellulosic biomass for US use. Environ. Res. Lett. 2012, 7, 045905. [Google Scholar] [CrossRef]

- Nylund, N.O.; Koponen, K. Fuel and Technology Alternatives for Buses: Overall Energy Efficiency and EMISSION performance. VTT Technology: Espoo, Finland, 2012; Available online: https://www.vtt.fi/inf/pdf/technology/2012/T46.pdf (accessed on 11 June 2018).

- Renewable Energy Policy Network for the 21st Century (REN21), Renewables 2018 Global Status Report. REN21: Paris, France. Available online: https://www.renewable-ei.org/pdfdownload/activities/S1_Arthouros%20Zervos.pdf (accessed on 21 July 2018).

- Delgado, O.; Muncrief, R. Assessment of Heavy-Duty Natural Gas Vehicle Emissions: Implications and Policy Recommendations. White Paper; International Council on Clean Transportation (ICCT): Washington, DC, USA, 2015; Available online: https://www.theicct.org/sites/default/files/publications/ICCT_NG-HDV-emissions-assessmnt_20150730.pdf (accessed on 24 March 2018).

- Fasihi, M.; Breyer, C. Baseload electricity and hydrogen supply based on hybrid PV-Wind power plants. J. Clean. Prod. 2020, 243, 118466. [Google Scholar] [CrossRef]

- Elgowainy, A.; Dai, Q.; Han, J.; Wang, M. Life Cycle Analysis of Emerging Hydrogen Production Technologies. Annual Progress Report; Argonne National Laboratory, 2016. Available online: https://www.hydrogen.energy.gov/pdfs/progress16/ix_5_elgowainy_2016.pdf (accessed on 27 July 2018).

- Schuller, O. Greenhouse Gas Intensity of Natural Gas. Think Step AG: Germany, 2017. SOL 16-043.1. Available online: http://gasnam.es/wp-content/uploads/2017/11/NGVA-thinkstep_GHG_Intensity_of_NG_Final_Report_v1.0.pdf (accessed on 14 September 2017).

- Skone, T.J. Life Cycle Greenhouse Gas Perspective on Exporting Liquefied Natural Gas from the United States. NETL, National Energy Technology Laboratory: USA, 2014. Available online: https://www.energy.gov/sites/prod/files/2014/05/f16/Life%20Cycle%20GHG%20Perspective%20Report.pdf (accessed on 19 November 2017).

- Sadovskaia, K.; Bogdanov, D.; Honkapuro, S.; Breyer, C. Power transmission and distribution losses—A model based on available empirical data and future for all countries globally. Electr. Power Energy Syst. 2019, 107, 98–109. [Google Scholar] [CrossRef]

- European Commission. Well-To-Wheels Analysis of Future Automotive Fuels and Powertrains in the European Context. Well-To-Tank Report Version4. Luxembourg. 2013. Available online: https://ec.europa.eu/jrc/en/publication/eur-scientific-and-technical-research-reports/tank-wheels-report-version-4a-well-wheels-analysis-future-automotive-fuels-and-powertrains (accessed on 8 November 2017).

- Dehaghani, E.S. Well-To-Wheels Energy Efficiency Analysis of Plug-in Electric Vehicles Including Varying Charging Regimes. M.Sc. Thesis, Concordia University, Montreal, QC, Canada, 2013. Available online: https://pdfs.semanticscholar.org/20bb/5e329521fde98163b406c2f44951f5dbed99.pdf (accessed on 28 November 2017).

- Fasihi, M.; Bogdanov, D.; Breyer, C. Overview on PtX Options Studied in NCE and Their Global Potential Based on Hybrid PV-Wind Power Plants. Presentation. Neo-Carbon Energy Seminar: Lappeenranta, Finland, 2017. Available online: http://www.neocarbonenergy.fi/wp-content/uploads/2016/02/13_Fasihi.pdf (accessed on 11 May 2018).

- Prieur, P.; Fareau, D.; Vinot, S. Well to Tank Technology Pathways and Carbon Balance. Luxembourg, 2009. Available online: http://s3.amazonaws.com/zanran_storage/www.roads2hy.com/ContentPages/2498021066.pdf (accessed on 1 November 2017).

- Wang, M.; Elgowainy, A. Well-To-Wheels GHG Emissions of Natural Gas Use in Transportation: CNGVs, LNGVs, EVs, and FCVs. Washington, DC, USA, 2014. Available online: https://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=1&cad=rja&uact=8&ved=2ahUKEwie35zmio3kAhXtiIsKHU_IAhwQFjAAegQIAhAC&url=https%3A%2F%2Fgreet.es.anl.gov%2Ffiles%2FEERE-LCA-NG&usg=AOvVaw3aBA3Xrrz_O4NhNXbFZkqy (accessed on 8 December 2017).

- Organisation for Economic Co-Operation and Development—Food and Agriculture (OECD-FAO). Agricultural Outlook; Dataset; FAO: Rome, Italy; OECD: Paris, France, 2016; Available online: https://www.oecd-ilibrary.org/agriculture-and-food/data/oecd-agriculture-statistics_agr-data-en (accessed on 9 May 2017).

- Washing, E.M.; Pulugurtha, S. Well-To-Wheel analysis of electric and hydrogen light rail. J. Public Transp. 2015, 18, 74–88. [Google Scholar] [CrossRef]

- Serpa, D. Tank to Wheel Efficiency. After Oil EV, 2011. Available online: http://www.afteroilev.com/Pub/EFF_Tank_to_Wheel.pdf (accessed on 8 November 2018).

- Auto Tech Review. Making Sense of Two-Wheeler Fuel Efficiencies. Auto Tech Review: New Delhi, 2016. Available online: https://autotechreview.com/technology/tech-update/making-sense-of-two-wheeler-fuel-efficiencies (accessed on 14 March 2018).

- Schwertner, M.; Weidmann, U. Comparison of Well-to_wheel efficiencies for different drivetrain configurations of transit buses. Transp. Res. Rec. J. Transp. Res. Board 2016, 2539, 55–64. [Google Scholar] [CrossRef]

- Thiruvengadam, A.; Pradhan, S.; Besch, M.; Carder, D. Heavy-Duty Vehicle Design Engine Efficiency Evaluation and Energy Audit. CAFEE, Center for Alternative Fuels, Engines and Emissions; West Virginia University: Morgantown, WV, USA, 2014; Available online: https://theicct.org/sites/default/files/publications/HDV_engine-efficiency-eval_WVU-rpt_oct2014.pdf (accessed on 1 May 2018).

- Gruber, C.; Wurster, R. Hydrogen-Fueled Buses: The Bavarian Fuel Cell Bus Project. MAN Nutzfahrzeuge, Munich; L-B-Systemtechnik, Ottobrunn. Available online: http://ieahydrogen.org/pdfs/Case-Studies/bavarian_proj.aspx (accessed on 19 May 2018).

- Hoffrichter, A. Hydrogen as an Energy Carrier for Railway Traction. Ph.D. Dissertation, University of Birmingham, Birmingham, UK, 2013. Available online: https://etheses.bham.ac.uk/id/eprint/4345/9/Hoffrichter13PhD1.pdf (accessed on 15 April 2018).

- Vodovozov, V.; Lehtla, T. Power Accounting for Ship Electric Propulsion. Closing Conference of Doctoral School of Energy and Geotechnology II, Pärnu, Estonia. 2015. Available online: https://pdfs.semanticscholar.org/6663/89cd6ba20958fb5e92e46d78683f66fecf89.pdf (accessed on 19 April 2017).

- Breyer, C.; Khalili, S.; Bogdanov, D. Solar Photovoltaic Capacity Demand for a fully sustainable Transport Sector—How to fulfill the Paris Agreement by 2050. Prog. Photovolt. Res. Appl. 2018, 1–12. [Google Scholar] [CrossRef]

- Du, J.; Li, F.; Li, J.; Wu, X.; Song, Z.; Zou, Y. Evaluating the technological evolution of battery electric buses: China as a case. Energy 2019, 176, 309–319. [Google Scholar] [CrossRef]

- Transport and Environment. Electric Buses Arrive on Time. Market Place, Economy, Technology, Environmental and Policy Perspectives for Fully Electric Buses in the UE. Transport and Environment: Brussels, Belgium, 2018. Available online: https://www.transportenvironment.org/sites/te/files/publications/Electric%20buses%20arrive%20on%20time.pdf (accessed on 1 May 2019).

- Zart, N. 100% Electric Bus Fleet for Shenzhen (Population 11.9 Million) by End of 2017. Clean Technica: El Cerrito, CA, USA, 2017; Available online: https://cleantechnica.com/2017/11/12/100-electric-bus-fleet-shenzhen-pop-11-9-million-end-2017/ (accessed on 22 May 2017).

- Creutzig, F.; McGlynn, E.; Minx, J.; Edenhofer, O. Climate policies for road transport revisited (I): Evaluation of the current framework. Energy Policy 2011, 39, 2396–2406. [Google Scholar] [CrossRef]

- Creutzig, F.; Jochem, P.; Edelenbosch, O.Y.; Mattauch, L.; Vuuren, D.P.V.; Mccollum, D.; Minx, J.C. Transport: A roadblock to climate change mitigation? Science 2015, 350, 911–912. [Google Scholar] [CrossRef] [Green Version]

- Keiner, D.; Ram, M.; Barbosa, L.D.S.; Bogdanov, D.; Breyer, C. Cost optimal self-consumption of PV prosumers with stationary batteries, heat pumps, thermal energy storage and electric vehicle across the world up to 2050. Sol. Energy 2019, 185, 406–423. [Google Scholar] [CrossRef]

- Keiner, D.; Breyer, C.; Sterner, M. Cost and self-consumption optimized residential PV prosumer system in Germany covering residential electricity, heat and mobility demand. Int. J. Sustain. Energy Plan. Manag. 2019, 21, 35–58. [Google Scholar] [CrossRef]

- Robinius, M.; Linßen, J.; Grube, T.; Reuß, M.; Stenzel, P.; Syranidis, K.; Kuckertz, P.; Stolten, D. Comparative Analysis of Infrastructures: Hydrogen Fueling and Electric Charging of Vehicles. Forschungszentrum Jülich: Jülich, Germany, 2018. Available online: https://content.h2.live/wp-content/uploads/2018/01/Energie-und-Umwelt_408_Robinius-final.pdf (accessed on 17 July 2018).

- Hoekstra, A. The understanding potential of battery electric vehicles to reduce emissions. Joule 2019, 3, 1404–1414. [Google Scholar] [CrossRef]

- Breyer, C.; Koskinen, O.; Blechinger, P. Profitable climate mitigation: The case of greenhouse gas emission reduction benefits enabled by solar photovoltaic systems. Renew. Sustain. Energy Rev. 2015, 49, 610–628. [Google Scholar] [CrossRef]

- Creutzig, F.; Ravindranath, N.H.; Berndes, G.; Bolwig, S.; Bright, R.; Cherubini, F.; Chum, H.; Corbera, E.; Delucchi, M.; Faaij, A.; et al. Bioenergy and climate change mitigation: An assessment. Glob. Change Biol. Bioenergy 2015, 7, 916–944. [Google Scholar] [CrossRef]

- Ram, M.; Bogdanov, D.; Aghahosseini, A.; Gulagi, A.; Oyewo, A.S.; Child, M.; Caldera, U.; Sadovskaia, K.; Farfan, J.; Barbosa, L.S.N.S.; et al. Global Energy System Based on 100% Renewable Energy—Power, Heat, Transport and Desalination Sectors. Lappeenranta University of Technology and Energy Watch Group: Lappeenranta, Finland; Berlin, Germany, 2019; Available online: http://energywatchgroup.org/wp-content/uploads/EWG_LUT_100RE_All_Sectors_Global_Report_2019.pdf (accessed on 12 July 2019).

- Lund, M.T.; Aamaas, B.; Berntsen, T.; Bock, L.; Burkhardt, U.; Fuglestvedt, J.S.; Shine, K.P. Emission metrics for quantifying regional climate impacts of aviation. Earth Syst. Dyn. 2017, 8, 547–563. [Google Scholar] [CrossRef] [Green Version]

- Burkhardt, U.; Bock, L.; Bier, A. Mitigating the contrail cirrus climate impact by reducing aircraft soot number emissions. NPJ Clim. Atmos. Sci. 2018, 1, 37. [Google Scholar] [CrossRef]

- Breyer, C.; Fasihi, M.; Bajamundi, C.; Creutzig, F. Direct air capture of CO2—A key technology for ambitious climate change mitigation. Joule 2019, 3, 2053–2057. [Google Scholar] [CrossRef]

- Fuss, S.; Lamb, W.F.; Callaghan, M.W.; Hilaire, J.; Creutzig, F.; Amann, T.; Beringer, T.; Garcia, W.D.O.; Hartmann, J.; Khanna, T.; et al. Negative emissions—Part 2: Costs, potentials and side effects. Environ. Res. Lett. 2018, 13, 063002. [Google Scholar] [CrossRef]

- Vartiainen, E.; Masson, G.; Breyer, C.; Moser, D.; Medina, E.R. Impact of Weighted Average Cost of Capital, Capital Expenditure and Other Parameters on Future Utility-Scale PV Levelised Cost of Electricity. Prog. Photovolt. Res. Appl. 2019, in press. [Google Scholar] [CrossRef]

- Haegel, N.M.; Atwater, H.; Barnes, T.; Breyer, C.; Burrell, A.; Chiang, Y.M.; De Wolf, S.; Dimmler, B.; Feldman, D.; Glunz, S.; et al. Terawatt-scale photovoltaics: Transform global energy. Science 2019, 364, 836–838. [Google Scholar] [CrossRef] [Green Version]

- International Energy Agency (IEA). World Energy Outlook 2015; International Energy Agency: Paris, France, 2015. [Google Scholar]

- Bloomberg New Energy Finance. New Energy Outlook 2015. Long-Term Projections of the Global Energy Sector. BNEF: London, 2015. Available online: Catskillcitizens.org/learnmore/BNEF-NEO2015_Executive-summary.pdf (accessed on 19 March 2018).

- Hansen, K.; Breyer, C.; Lund, H. Status and perspectives on 100% renewable energy systems. Energy 2019, 175, 471–480. [Google Scholar] [CrossRef]

- García-Olivares, A.; Sole, J.; Osychenko, O. Transportation in a 100% renewable energy system. Energy Convers. Manag. 2018, 158, 266–285. [Google Scholar] [CrossRef]

- Brown, T.W.; Bischof-Niemz, T.; Blok, K.; Breyer, C.; Lund, H.; Mathiesen, B.V. Response to ‘Burden of proof: A comprehensive review of the feasibility of 100% renewable-electricity systems’. Renew. Sustain. Energy Rev. 2018, 92, 834–847. [Google Scholar] [CrossRef]

- Teske, S. Achieving the Paris Climate Agreement Goals, Global and Regional 100% Renewable Energy Scenarios with Non-Energy GHG Pathways for +1.5 °C and +2 °C; Springer: Basel, Switzerland, 2019. [Google Scholar]

- Jacobson, M.Z.; Delucchi, M.A.; Cameron, M.A.; Mathiesen, B.V. Matching demand with supply at low cost in 139 countries among 20 world regions with 100% intermittent wind, water, and sunlight (WWS) for all purposes. Renew. Energy 2018, 123, 236–248. [Google Scholar] [CrossRef]

- Löffler, K.; Hainsch, K.; Burandt, T.; Oei, P.Y.; Kemfert, C.; Hirschhausen, C.V. Designing a model for the Global energy system-GENeSYS-MOD: An Application of the Open-Source energy modeling system (OSeMOSYS). Energies 2017, 10, 1468. [Google Scholar] [CrossRef]

- Pursiheimo, E.; Holttinen, H.; Koljonen, T. Inter-sectoral effects of high renewable energy share in global energy system. Renew. Energy 2019, 136, 1119–1129. [Google Scholar] [CrossRef]

- World Wildlife Fund (WWF). The Energy Report 100% Renewable Energy by 2050; World Wildlife Fund (WWF): Washington, DC, USA, 2011. Available online: https://www.google.com/search?client=firefoxbe&q=World+Wildlife+Fund+%28WWF%29.+The+energy+report+100%25+renewable+energy+by+2050.+2011%2C+Washington+DC%2C+USA.+Available+online%3A (accessed on 19 May 2018).

- Deng, Y.Y.; Blok, K.; Der Leun, K.V. Transition to a fully sustainable global energy system. Energy Strategy Rev. 2012, 1, 109–121. [Google Scholar] [CrossRef]

- World Energy Council. World Energy Scenarios 2019. Exploring Innovation Pathways to 2040; World Energy Council: London, UK, 2019. Available online: https://www.worldenergy.org/assets/downloads/European_Scenarios_FINAL_for_website.pdf (accessed on 10 September 2019).

- International Energy Agency (IEA). World Energy Outlook 2018; International Energy Agency: Paris, France, 2018. [Google Scholar]

- Luderer, G.; Vrontisi, Z.; Bertram, C.; Edelenbosch, O.Y.; Pietzcker, R.C.; Rogelj, J.; De Boer, H.S.; Drouet, L.; Emmerling, J.; Fricko, O.; et al. Residual fossil CO2 emissions in 1.5–2 °C pathway. Nat. Clim. Change 2018, 8, 626–633. [Google Scholar] [CrossRef]

- Shell International B.V. Sky Scenario. The Hague, The Netherlands, 2018. Available online: https://www.shell.com/energy-and-innovation/the-energy-future/scenarios/shell-scenario-sky.html (accessed on 20 August 2019).

- BP Energy Outlook. BP Energy Economics: UK, 2019. Available online: https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/energy-economics/energy-outlook/bp-energy-outlook-2019.pdf (accessed on 8 March 2018).

- Energy Information Administration (EIA). Global Transportation Energy Consumption: Examination of Scenarios to 2040 Using ITEDD. Energy Information Administration: Washington, DC, USA, 2017. Available online: https://www.eia.gov/analysis/studies/transportation/scenarios/pdf/globaltransportation.pdf (accessed on 12 May 2018).

- Breyer, C.; Tsupari, E.; Tikka, V.; Vainikka, P. Power-to-Gas as an Emerging profitable business through creating an integrated value chain. Energy Procedia 2015, 73, 182–189. [Google Scholar] [CrossRef]

- Child, M.; Nordling, A.; Breyer, C. The impacts of high V2G participation in a 100% renewable Åland energy system. Energies 2018, 11, 2206. [Google Scholar] [CrossRef]

- Meschede, H.; Child, M.; Breyer, C. Assessment of sustainable energy system configuration for a small Canary island in 2030. Energy Convers. Manag. 2018, 165, 363–372. [Google Scholar] [CrossRef]

- Mathiesen, B.V.; Lund, H.; Connolly, D.; Wenzel, H.; Østergaard, P.A.; Möller, B.; Nielsen, S.; Ridjan, I.; Karnøe, P.; Sperling, K.; et al. Smart energy systems for coherent 100% renewable energy and transport solutions. Appl. Energy 2015, 145, 139–154. [Google Scholar] [CrossRef]

- Brown, T.; Schäfer, M.; Greiner, M. Sectoral interactions as carbon dioxide emissions approach zero in a Highly-Renewable European energy system. Energies 2019, 12, 1032. [Google Scholar] [CrossRef]

- Gulagi, A.; Bogdanov, D.; Fasihi, M.; Breyer, C. Can Australia power the energy-hungry Asia with renewable energy? Sustainability 2017, 9, 233. [Google Scholar] [CrossRef]

- Junne, T.; Wulff, N.; Breyer, C.; Naegler, T. Critical materials in global low carbon energy scenarios: The case of dysprosium, neodymium, lithium and cobalt. 2019; submitted. [Google Scholar]

- Greim, P.; Solomon, A.A.; Breyer, C. Availability of lithium for the global transition towards renewable based energy supply with focus on power and mobility. 2019; submitted. [Google Scholar]

- Grandell, L.; Lehtilä, A.; Kivinen, M.; Koljonen, T.; Kihlman, S. Role of critical metals in the future markets of clean energy technologies. Renew. Energy 2016, 95, 53–62. [Google Scholar] [CrossRef]

- Altermatt, P.P.; Chen, Y.; Feng, Z. Riding the workhorse of the industry: PERC. Photovolt. Int. 2018, 41, 46–54. [Google Scholar]

- Köntges, M.; Jung, V. Al/Ni: V/Ag metal stacks as rear-side metallization for crystalline silicon solar cells. Prog. Photovolt. Res. Appl. 2012, 21, 876–883. [Google Scholar] [CrossRef]

- Hsiao, P.-C.; Song, N.; Wang, X.; Shen, X.; Phua, B.; Colwell, J.; Romer, U.; Johnston, B.; Lim, S.; Shengzhao, Y.; et al. 266-nm ps laser ablation for copper-plated p-type selective emitter PERC silicon solar cells. IEE J. Photovolt. 2018, 8, 4. [Google Scholar] [CrossRef]

- International Renewable Energy Agency (IRENA). Renewable Energy and Jobs. Abu Dhabi, United Arab Emirates, 2019. Available online: https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2019/Jun/IRENA_RE_Jobs_2019-report.pdf (accessed on 1 May 2018).

- Manish, R.; Aghahosseini, A.; Breyer, C. Job creation during the global energy transition towards 100% renewable power system by 2050. Tech. Forecast. Soc. Chang. 2019. [Google Scholar] [CrossRef]

- Intergovernmental Panel on Climate Change (IPCC). Global Warming of 1.5 °C; Intergovernmental Panel on Climate Change (IPCC): Geneva, Switzerland, 2018. Available online: https://report.ipcc.ch/sr15/pdf/sr15_spm_final.pdf (accessed on 6 April 2018).

- Pahle, M.; Burtraw, D.; Flachsland, C.; Kelsey, N.; Biber, E.; Meckling, J.; Edenhofer, O.; Zysman, J. Sequencing to ratchet up climate policy stringency. Nat. Clim. Change 2018, 8, 861–867. [Google Scholar] [CrossRef]

- Breyer, C.; Heinonen, S.; Ruotsalainen, J. New consciousness: A societal and energetic vision for rebalancing humankind within the limits of planet earth. Technol. Forecast. Soc. Change 2017, 114, 7–15. [Google Scholar] [CrossRef]

- Smith, C.J.; Forster, P.M.; Allen, M.; Fuglestvedt, J.; Miller, R.J.; Rogelj, J.; Zickfeld, K. Current fossil fuel infrastructure does not yet commit us to 1.5°C warming. Nat. Commun. 2019, 10, 101. [Google Scholar] [CrossRef] [PubMed]

- Kalkuhl, M.; Steckel, J.; Edenhofer, O. All or nothing: Climate policy when assets can become stranded. J. Environ. Econ. Manag. 2019, in press. [Google Scholar] [CrossRef]

- Cabon Tracker Initiative. 2020 Vision: Why You Should See Peak Fossil Fuels Coming. London, 2018. Available online: https://www.carbontracker.org/reports/2020-vision-why-you-should-see-the-fossil-fuel-peak-coming/ (accessed on 20 September 2019).

- Geels, F.W.; Sovacool, B.K.; Schwanen, T.; Sorrell, S. The Socio-Technical Dynamics of Low-Carbon Transitions. Joule 2017, 1, 463–479. [Google Scholar] [CrossRef] [Green Version]

- Geels, F.W. Regime resistance against low-carbon energy transitions: Introducing politics and power in the multi-level perspective. Theory Cult. Soc. 2014, 31, 21–40. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Vehicle | Unit | 2015 | 2020 | 2025 | 2030 | 2035 | 2040 | 2045 | 2050 |

|---|---|---|---|---|---|---|---|---|---|

| LDV | b p-km | 23,137 | 27,482 | 31,438 | 36,145 | 41,356 | 47,458 | 54,535 | 62,942 |

| 2W/3W | b p-km | 4370 | 5606 | 6634 | 7750 | 8780 | 10,164 | 12,067 | 15,232 |

| BUS | b p-km | 18,619 | 21,653 | 24,235 | 27,240 | 30,440 | 34,295 | 38,684 | 42,498 |

| MDV | b t-km | 2919 | 3433 | 3894 | 4438 | 5065 | 5835 | 6694 | 7617 |

| HDV | b t-km | 9787 | 11,398 | 12,889 | 14,628 | 16,601 | 19,021 | 21,691 | 24,539 |

| Transport Modes | Unit | 2015 | 2020 | 2025 | 2030 | 2035 | 2040 | 2045 | 2050 |

|---|---|---|---|---|---|---|---|---|---|

| Road Passenger | b p-km | 46,104 | 54,713 | 62,247 | 71,100 | 80,546 | 91,899 | 105,297 | 120,739 |

| Road Freight | b t-km | 12,708 | 14,832 | 16,783 | 19,066 | 21,665 | 24,856 | 28,385 | 32,156 |

| Rail Passenger | b p-km | 3821 | 4573 | 5171 | 5792 | 6280 | 6854 | 7504 | 8193 |

| Rail Freight | b t-km | 11,141 | 12,302 | 13,333 | 14,520 | 15,898 | 17,591 | 19,566 | 21,857 |

| Transport Modes | Unit | 2015 | 2020 | 2025 | 2030 | 2035 | 2040 | 2045 | 2050 |

|---|---|---|---|---|---|---|---|---|---|

| Marine Passenger | b p-km | 126 | 151 | 185 | 226 | 278 | 340 | 411 | 491 |

| Marine Freight | b t-km | 83,961 | 98,980 | 116,550 | 137,402 | 162,472 | 192,967 | 230,438 | 276,879 |

| Transport Modes | Unit | 2015 | 2020 | 2025 | 2030 | 2035 | 2040 | 2045 | 2050 |

|---|---|---|---|---|---|---|---|---|---|

| Aviation Passenger | b p-km | 5629 | 6866 | 8335 | 10,665 | 13,131 | 17,024 | 21,520 | 26,363 |

| Aviation Freight | b t-km | 198 | 264 | 354 | 473 | 634 | 863 | 1157 | 1514 |

| Vehicle | Item | Unit | Reference |

|---|---|---|---|

| LDV | Energy consumption | kWh/100 km | [73] |

| Load factor | passengers per vehicle | [34,64] | |

| 2W/3W | Energy consumption | kWh/100 km | [9,75] |

| Load factor | passengers per vehicle | [64] | |

| BUS | Energy consumption | kWh/km | [76] |

| Load factor | passengers per vehicle | [1] | |

| MDV | Energy consumption | kWh/km | [34,78,79] |

| Load factor | ton per vehicle | [64] | |

| HDV | Energy consumption | kWh/km | [34,78,79] |

| Load factor | ton per vehicle | [64] |

| Modes | Item | Unit | Reference |

|---|---|---|---|

| Rail | Specific energy demand | MJel/p-km | [80] |

| Specific energy demand | MJel/t-km | [80] | |

| Marine | Bunker fuel consumption | kilo ton | [65] |

| Calorific value | kJ/g | [81] | |

| Efficiency | % | [36,51] | |

| Specific energy demand | MJth/p-km | [82] | |

| Specific energy demand | MJth/t-km | [82] | |

| Aviation | Calorific value | MJth/kg | [83] |

| Efficiency | % | [84] | |

| Specific energy demand | MJth/p-km | [83,84] | |

| Specific energy demand | MJth/t-km | [83,84] |

| Vehicle | Item | Unit | Reference |

|---|---|---|---|

| LDV | Vehicle price | € | [96] |

| Battery/hydrogen price | €/kWh | [19,97,98,99] | |

| BUS | Vehicle price | € | [100] |

| Battery/hydrogen price | €/kWh | [100,101] | |

| MDV | Vehicle price | € | [102] |

| Battery/hydrogen price | €/kWh | [104] | |

| HDV | Vehicle price | € | [105] |

| Battery/hydrogen price | €/kWh | [104,106] | |

| All types | Insurance | €/vehicle | [107,109,110] |

| Maintenance | €/vehicle | [19,100,108] |

| Vehicle | Unit | 2015–2050 | Reference |

|---|---|---|---|

| LDV | years | 15 | [111,112] |

| 2W/3W | years | 10 | [9] |

| BUS | years | 15 | [114] |

| MDV | years | 15 | [119] |

| HDV | years | 16 | [114,119] |

| Vehicle Type | Unit | 2015–2050 | Reference |

|---|---|---|---|

| LDV BEV | years | 10 | [113] |

| LDV PHEV | years | 10 | [113] |

| 2W/3W BEV | years | 9 | [9] |

| BUS BEV | years | 9 | [101] |

| BUS PHEV | years | 6 | [101] |

| MDV BEV | years | 10 | [113] |

| MDV PHEV | years | 5 | [113] |

| HDV BEV | years | 10 | [113] |

| HDV PHEV | years | 5 | [113] |

| Vehicle Type | Unit | 2015 | 2020 | 2025 | 2030 | 2035 | 2040 | 2045 | 2050 |

|---|---|---|---|---|---|---|---|---|---|

| LDV | km/a | 14,603 | 14,004 | 13,357 | 12,993 | 12,728 | 12,468 | 12,217 | 11,971 |

| 2W/3W | km/a | 7224 | 7380 | 7453 | 7494 | 7435 | 7427 | 7480 | 7702 |

| BUS | km/a | 64,744 | 67,178 | 68,854 | 70,810 | 72,610 | 74,503 | 76,293 | 77,465 |

| MDV | km/a | 25,389 | 26,154 | 26,631 | 27,140 | 27,601 | 28,058 | 28,416 | 28,655 |

| HDV | km/a | 54,541 | 53,521 | 52,941 | 52,582 | 52,188 | 51,747 | 51,312 | 50,866 |

| Fuel | Method | Unit | 2015 | 2020 | 2025 | 2030 | 2035 | 2040 | 2045 | 2050 |

|---|---|---|---|---|---|---|---|---|---|---|

| Electricity | TTW | gCO2eq/kWhel | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Hydrogen | TTW | gCO2eq/kWhH2 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| LNG | TTW | gCO2eq/kWhCH4 | 237 | 237 | 237 | 230 | 194 | 135 | 54 | 0 |

| Liquid fuel | TTW | gCO2eq/kWhth | 266 | 266 | 266 | 258 | 218 | 151 | 71 | 10 |

| Electricity | WTW | gCO2eq/kWhel | 513 | 373 | 140 | 47 | 15 | 6 | 2 | 0 |

| Hydrogen | WTW | gCO2eq/kWhH2 | 389 | 395 | 334 | 223 | 148 | 65 | 21 | 0 |

| LNG | WTW | gCO2eq/kWhCH4 | 300 | 300 | 300 | 294 | 251 | 176 | 71 | 0 |

| Liquid fuel | WTW | gCO2eq/kWhth | 368 | 366 | 366 | 358 | 305 | 211 | 96 | 8 |

| Primary Input | Conversion | Final Energy Fuel |

|---|---|---|

| Fossil fuels | Refinery | liquid hydrocarbons, diesel, gasoline |

| Fossil fuels | Power plants (coal, gas, oil) | electricity |

| Fossil fuels | Steam methane reforming | hydrogen |

| Nuclear fuels | Nuclear power plant | electricity |

| Electricity | Fischer-Tropsch | liquid hydrocarbons |

| Electricity | Electrolysis | hydrogen |

| Hydrogen | Methanation | methane |

| Methane | Liquefaction | LNG |

| Biomass | Biorefinery | biofuels, liquid hydrocarbons, biodiesel, bioethanol |

| Primary Origination | Fuel Type | WTT Efficiency | 2015 | 2020 | 2025 | 2030 | 2035 | 2040 | 2045 | 2050 |

|---|---|---|---|---|---|---|---|---|---|---|

| Fossil | Diesel [131,132] | % | 83 | 84 | 85 | 85 | 86 | 87 | 87 | 88 |

| Fossil | Gasoline [131,132] | % | 85 | 86 | 86 | 87 | 88 | 88 | 89 | 90 |

| Fossil | Liquid Hydrocarbons | % | 84 | 85 | 85 | 86 | 87 | 87 | 88 | 89 |

| RE | Liquid Hydrocarbons [133] | % | n/a | n/a | n/a | 53 | 53 | 53 | 53 | 53 |

| Fossil | Electricity [95] | % | 44 | 46 | 47 | 48 | 47 | 46 | 46 | 0 |

| Nuclear | Electricity [95] | % | 33 | 33 | 33 | 33 | 37 | 37 | 37 | 38 |

| RE | Electricity [95] | % | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 |

| Fossil | Hydrogen [134] | % | 85 | 85 | 85 | 85 | 85 | 85 | 85 | 85 |

| RE | Hydrogen [95] | % | 84 | 84 | 84 | 84 | 84 | 84 | 84 | 84 |

| Fossil | LNG [135] | % | 85 | 85 | 85 | 85 | 85 | 85 | 85 | 85 |

| RE | LNG [135] | % | 57 | 57 | 57 | 57 | 57 | 57 | 57 | 57 |

| Corn | Bioethanol [131] | % | 61 | 61 | 61 | 61 | 61 | 61 | 61 | 61 |

| Sugarcane | Bioethanol [131] | % | 48 | 48 | 48 | 48 | 48 | 48 | 48 | 48 |

| Palm | Biodiesel [131] | % | 80 | 80 | 80 | 80 | 80 | 80 | 80 | 80 |

| Biomass | Liquid Hydrocarbons | % | 60 | 60 | 60 | 60 | 60 | 60 | 60 | 60 |

| Final Energy Fuel | Input | Contribution Share | 2015 | 2020 | 2025 | 2030 | 2035 | 2040 | 2045 | 2050 |

|---|---|---|---|---|---|---|---|---|---|---|

| Electricity | Fossil | % | 68 | 50 | 19 | 7 | 2 | 1 | 0 | 0 |

| Nuclear | % | 10 | 10 | 7 | 4 | 2 | 1 | 1 | 0 | |

| Renewable | % | 22 | 40 | 74 | 89 | 96 | 98 | 99 | 100 | |

| Hydrogen | Fossil | % | 100 | 90 | 75 | 50 | 35 | 15 | 5 | 0 |

| Electricity | % | 0 | 10 | 25 | 50 | 65 | 85 | 95 | 100 | |

| LNG | Fossil | % | 100 | 100 | 100 | 97 | 82 | 57 | 23 | 0 |

| Electricity | % | 0 | 0 | 0 | 3 | 18 | 43 | 77 | 100 | |

| Liquid hydrocarbons | Biofuel | % | 3 | 4 | 4 | 4 | 4 | 4 | 4 | 4 |

| FT fuels | % | 0 | 0 | 0 | 3 | 18 | 43 | 73 | 96 | |

| Fossil | % | 97 | 96 | 96 | 93 | 78 | 53 | 23 | 0 |

| Vehicle | Type | TTW Efficiency | 2015 | 2020 | 2025 | 2030 | 2035 | 2040 | 2045 | 2050 |

|---|---|---|---|---|---|---|---|---|---|---|

| LDV | ICE [137] | % | 20 | 22 | 24 | 26 | 26 | 27 | 27 | 28 |

| BEV [138] | % | 74 | 77 | 81 | 84 | 86 | 87 | 89 | 91 | |

| PHEV—ICE | % | 20 | 22 | 24 | 26 | 26 | 27 | 27 | 28 | |

| PHEV—EV | % | 74 | 77 | 81 | 84 | 86 | 87 | 89 | 91 | |

| FCEV [131] | % | 30 | 34 | 39 | 43 | 45 | 47 | 48 | 50 | |

| 2W/3W [139] | ICE | % | 12 | 13 | 14 | 16 | 16 | 16 | 16 | 17 |

| BEV | % | 44 | 46 | 48 | 50 | 51 | 52 | 53 | 54 | |

| BUS [140] | ICE | % | 33 | 33 | 34 | 35 | 35 | 36 | 36 | 37 |

| BEV | % | 73 | 76 | 79 | 83 | 85 | 86 | 88 | 90 | |

| PHEV—ICE | % | 33 | 33 | 34 | 35 | 35 | 36 | 36 | 37 | |

| PHEV—EV | % | 73 | 76 | 79 | 83 | 85 | 86 | 88 | 90 | |

| FCEV | % | 44 | 46 | 48 | 50 | 52 | 54 | 56 | 58 | |

| MDV | ICE [141] | % | 32 | 32 | 33 | 33 | 34 | 34 | 35 | 35 |

| BEV [142] | % | 73 | 76 | 79 | 83 | 85 | 86 | 88 | 90 | |

| PHEV—ICE | % | 32 | 32 | 33 | 33 | 34 | 34 | 35 | 35 | |

| PHEV—EV | % | 73 | 76 | 79 | 83 | 85 | 86 | 88 | 90 | |

| FCEV [142] | % | 45 | 47 | 49 | 51 | 53 | 55 | 57 | 59 | |

| HDV | ICE [141] | % | 41 | 42 | 43 | 43 | 44 | 45 | 45 | 46 |

| BEV [142] | % | 73 | 76 | 79 | 83 | 85 | 86 | 88 | 90 | |

| PHEV—ICE | % | 41 | 42 | 43 | 43 | 44 | 45 | 45 | 46 | |

| PHEV—EV | % | 73 | 76 | 79 | 83 | 85 | 86 | 88 | 90 | |

| FCEV [142] | % | 45 | 47 | 49 | 51 | 53 | 55 | 57 | 59 |

| Modes | Type | TTW Efficiency | 2015 | 2020 | 2025 | 2030 | 2035 | 2040 | 2045 | 2050 |

|---|---|---|---|---|---|---|---|---|---|---|

| Rail, trains [143] | Electric | % | 76 | 77 | 78 | 79 | 80 | 81 | 82 | 83 |

| Diesel | % | 31 | 33 | 34 | 35 | 36 | 36 | 37 | 37 | |

| Marine, ships [36,144] | Electric | % | 62 | 63 | 64 | 64 | 65 | 66 | 67 | 68 |

| Hydrogen | % | 45 | 48 | 51 | 54 | 56 | 57 | 59 | 60 | |

| LNG | % | 45 | 46 | 48 | 49 | 50 | 50 | 51 | 51 | |

| Diesel | % | 42 | 43 | 45 | 46 | 47 | 47 | 48 | 48 | |

| Aviation, airplanes [54] | Electric | % | 73 | 74 | 75 | 76 | 77 | 78 | 79 | 81 |

| Hydrogen | % | 44 | 46 | 47 | 49 | 50 | 52 | 54 | 55 | |

| Jet fuel | % | 39 | 40 | 41 | 42 | 43 | 44 | 44 | 45 |

| Vehicle | Type | Unit | 2015 | 2020 | 2025 | 2030 | 2035 | 2040 | 2045 | 2050 |

|---|---|---|---|---|---|---|---|---|---|---|

| LDV | ICE | kWhth/p-km | 0.485 | 0.456 | 0.413 | 0.368 | 0.336 | 0.308 | 0.260 | 0.211 |

| BEV | kWhel/p-km | 0.113 | 0.101 | 0.089 | 0.078 | 0.072 | 0.067 | 0.061 | 0.055 | |

| PHEV | kWhth/p-km | 0.145 | 0.114 | 0.091 | 0.081 | 0.074 | 0.068 | 0.057 | 0.046 | |

| PHEV | kWhel/p-km | 0.079 | 0.075 | 0.069 | 0.061 | 0.056 | 0.052 | 0.048 | 0.043 | |

| FCEV | kWhH2/p-km | 0.172 | 0.164 | 0.136 | 0.130 | 0.119 | 0.118 | 0.097 | 0.091 | |

| 2W/3W | ICE | kWhth/p-km | 0.126 | 0.126 | 0.126 | 0.126 | 0.125 | 0.125 | 0.125 | 0.125 |

| BEV | kWhel/p-km | 0.044 | 0.044 | 0.044 | 0.044 | 0.044 | 0.044 | 0.044 | 0.044 | |

| BUS | ICE | kWhth/p-km | 0.233 | 0.224 | 0.210 | 0.210 | 0.205 | 0.199 | 0.193 | 0.189 |

| BEV | kWhel/p-km | 0.107 | 0.101 | 0.095 | 0.091 | 0.087 | 0.083 | 0.079 | 0.076 | |

| PHEV | kWhth/p-km | 0.116 | 0.112 | 0.105 | 0.105 | 0.102 | 0.100 | 0.097 | 0.095 | |

| PHEV | kWhel/p-km | 0.053 | 0.050 | 0.048 | 0.045 | 0.043 | 0.041 | 0.039 | 0.038 | |

| FCEV | kWhH2/p-km | 0.178 | 0.166 | 0.156 | 0.147 | 0.139 | 0.132 | 0.124 | 0.118 | |

| MDV | ICE | kWhth/t-km | 1.334 | 1.229 | 1.132 | 1.043 | 0.961 | 0.885 | 0.815 | 0.751 |

| BEV | kWhel/t-km | 0.549 | 0.479 | 0.419 | 0.367 | 0.333 | 0.302 | 0.275 | 0.251 | |

| PHEV | kWhth/t-km | 0.801 | 0.737 | 0.679 | 0.626 | 0.576 | 0.531 | 0.489 | 0.450 | |

| PHEV | kWhel/t-km | 0.220 | 0.191 | 0.168 | 0.147 | 0.133 | 0.121 | 0.110 | 0.101 | |

| FCEV | kWhH2/t-km | 0.801 | 0.737 | 0.679 | 0.626 | 0.576 | 0.531 | 0.489 | 0.450 | |

| HDV | ICE | kWhth/t-km | 0.445 | 0.403 | 0.365 | 0.330 | 0.299 | 0.271 | 0.246 | 0.222 |

| BEV | kWhel/t-km | 0.237 | 0.207 | 0.181 | 0.159 | 0.144 | 0.130 | 0.119 | 0.108 | |

| PHEV | kWhth/t-km | 0.311 | 0.282 | 0.255 | 0.231 | 0.210 | 0.190 | 0.172 | 0.156 | |

| PHEV | kWhel/t-km | 0.071 | 0.062 | 0.054 | 0.048 | 0.043 | 0.039 | 0.036 | 0.032 | |

| FCEV | kWhH2/t-km | 0.267 | 0.242 | 0.219 | 0.198 | 0.180 | 0.163 | 0.147 | 0.133 |

| Modes | Type | Unit | 2015 | 2020 | 2025 | 2030 | 2035 | 2040 | 2045 | 2050 |

|---|---|---|---|---|---|---|---|---|---|---|

| Rail | Electricity | kWhel/p-km | 0.068 | 0.065 | 0.063 | 0.060 | 0.058 | 0.055 | 0.053 | 0.050 |

| Diesel | kWhth/p-km | 0.105 | 0.104 | 0.102 | 0.101 | 0.099 | 0.097 | 0.096 | 0.094 | |

| Electricity | kWhel/t-km | 0.034 | 0.032 | 0.030 | 0.028 | 0.026 | 0.024 | 0.022 | 0.019 | |

| Diesel | kWhth/t-km | 0.065 | 0.063 | 0.060 | 0.058 | 0.056 | 0.054 | 0.052 | 0.050 | |

| Marine | Electricity | kWhel/p-km | 0.315 | 0.319 | 0.323 | 0.325 | 0.325 | 0.325 | 0.325 | 0.325 |

| Diesel | kWhth/p-km | 0.680 | 0.657 | 0.634 | 0.612 | 0.605 | 0.599 | 0.592 | 0.586 | |

| LNG | kWhCH4/p-km | 0.680 | 0.657 | 0.634 | 0.612 | 0.605 | 0.599 | 0.592 | 0.586 | |

| Hydrogen | kWhH2/p-km | n/a | n/a | n/a | 0.566 | 0.521 | 0.484 | 0.472 | 0.461 | |

| Electricity | kWhel/t-km | 0.019 | 0.020 | 0.020 | 0.020 | 0.020 | 0.020 | 0.020 | 0.020 | |

| Diesel | kWhth/t-km | 0.042 | 0.041 | 0.039 | 0.038 | 0.037 | 0.037 | 0.037 | 0.036 | |

| LNG | kWhCH4/t-km | 0.042 | 0.041 | 0.039 | 0.038 | 0.037 | 0.037 | 0.037 | 0.036 | |

| Hydrogen | kWhH2/t-km | n/a | n/a | n/a | 0.035 | 0.032 | 0.030 | 0.029 | 0.029 | |

| Aviation | Electricity | kWhel/p-km | 0.204 | 0.194 | 0.184 | 0.175 | 0.166 | 0.157 | 0.149 | 0.141 |

| Jet fuel | kWhth/p-km | 0.545 | 0.517 | 0.490 | 0.465 | 0.442 | 0.419 | 0.398 | 0.377 | |

| Hydrogen | kWhH2/p-km | 0.392 | 0.372 | 0.353 | 0.335 | 0.318 | 0.302 | 0.286 | 0.271 | |

| Electricity | kWhel/t-km | 0.053 | 0.050 | 0.048 | 0.045 | 0.043 | 0.041 | 0.039 | 0.037 | |

| Jet fuel | kWhth/t-km | 0.142 | 0.134 | 0.128 | 0.121 | 0.115 | 0.109 | 0.104 | 0.098 | |

| Hydrogen | kWhH2/t-km | 0.102 | 0.097 | 0.092 | 0.087 | 0.083 | 0.079 | 0.075 | 0.071 |

| Vehicle | Type | Unit | 2015 | 2020 | 2025 | 2030 | 2035 | 2040 | 2045 | 2050 |

|---|---|---|---|---|---|---|---|---|---|---|

| LDV | ICE | €/unit | 20,260 | 20,260 | 20,260 | 20,260 | 20,260 | 20,260 | 20,260 | 20,260 |

| BEV | €/unit | 50,070 | 30,126 | 25,805 | 22,850 | 22,279 | 21,756 | 21,279 | 20,843 | |

| PHEV | €/unit | 25,466 | 23,874 | 22,593 | 21,679 | 21,510 | 21,296 | 21,153 | 20,974 | |

| FCEV | €/unit | 46,396 | 35,144 | 28,199 | 23,896 | 23,199 | 22,572 | 22,006 | 21,496 | |

| BUS | ICE | €/unit | 225,000 | 225,000 | 225,000 | 225,000 | 225,000 | 225,000 | 225,000 | 225,000 |

| BEV | €/unit | 289,735 | 254,988 | 230,663 | 213,534 | 210,143 | 207,020 | 204,142 | 201,489 | |

| PHEV | €/unit | 255,089 | 242,750 | 233,279 | 225,952 | 224,403 | 222,946 | 221,573 | 220,280 | |

| FCEV | €/unit | 742,500 | 612,085 | 511,172 | 433,088 | 413,592 | 395,519 | 378,765 | 363,234 | |

| MDV | ICE | €/unit | 78,950 | 78,950 | 78,950 | 78,950 | 78,950 | 78,950 | 78,950 | 78,950 |

| BEV | €/unit | 102,177 | 89,739 | 81,039 | 74,918 | 73,707 | 72,592 | 71,565 | 70,618 | |

| PHEV | €/unit | 89,458 | 85,136 | 81,813 | 79,237 | 78,692 | 78,179 | 77,695 | 77,240 | |

| FCEV | €/unit | 111,138 | 92,009 | 80,203 | 72,888 | 71,703 | 70,637 | 69,676 | 68,808 | |

| HDV | ICE | €/unit | 152,000 | 152,000 | 152,000 | 152,000 | 152,000 | 152,000 | 152,000 | 152,000 |

| BEV | €/unit | 337,364 | 265,925 | 217,695 | 185,132 | 178,896 | 173,219 | 168,051 | 163,343 | |

| PHEV | €/unit | 172,922 | 164,376 | 157,833 | 152,784 | 151,718 | 150,715 | 149,772 | 148,883 | |

| FCEV | €/unit | 189,358 | 161,228 | 143,866 | 133,108 | 131,365 | 129,797 | 128,384 | 127,108 |

| Vehicle | Type | Unit | 2015 | 2020 | 2025 | 2030 | 2035 | 2040 | 2045 | 2050 |

|---|---|---|---|---|---|---|---|---|---|---|

| LDV | ICE | €/year | 1207 | 1207 | 1207 | 1207 | 1207 | 1207 | 1207 | 1207 |

| BEV | €/year | 898 | 898 | 898 | 898 | 898 | 898 | 898 | 898 | |

| PHEV | €/year | 1318 | 1318 | 1318 | 1318 | 1318 | 1318 | 1318 | 1318 | |

| FCEV | €/year | 1053 | 1053 | 1053 | 1053 | 1053 | 1053 | 1053 | 1053 | |

| BUS | ICE | €/year | 36,983 | 36,983 | 36,983 | 36,983 | 36,983 | 36,983 | 36,983 | 36,983 |

| BEV | €/year | 30,775 | 30,775 | 30,775 | 30,775 | 30,775 | 30,775 | 30,775 | 30,775 | |

| PHEV | €/year | 39,212 | 39,212 | 39,212 | 39,212 | 39,212 | 39,212 | 39,212 | 39,212 | |

| FCEV | €/year | 33,879 | 33,879 | 33,879 | 33,879 | 33,879 | 33,879 | 33,879 | 33,879 | |

| MDV | ICE | €/year | 15,461 | 15,461 | 15,461 | 15,461 | 15,461 | 15,461 | 15,461 | 15,461 |

| BEV | €/year | 13,098 | 13,098 | 13,098 | 13,098 | 13,098 | 13,098 | 13,098 | 13,098 | |

| PHEV | €/year | 16,310 | 16,310 | 16,310 | 16,310 | 16,310 | 16,310 | 16,310 | 16,310 | |

| FCEV | €/year | 14,280 | 14,280 | 14,280 | 14,280 | 14,280 | 14,280 | 14,280 | 14,280 | |

| HDV | ICE | €/year | 33,468 | 33,468 | 33,468 | 33,468 | 33,468 | 33,468 | 33,468 | 33,468 |

| BEV | €/year | 27,260 | 27,260 | 27,260 | 27,260 | 27,260 | 27,260 | 27,260 | 27,260 | |

| PHEV | €/year | 35,697 | 35,697 | 35,697 | 35,697 | 35,697 | 35,697 | 35,697 | 35,697 | |

| FCEV | €/year | 30,364 | 30,364 | 30,364 | 30,364 | 30,364 | 30,364 | 30,364 | 30,364 |

| Quantity | Unit | 2015 | 2020 | 2025 | 2030 | 2035 | 2040 | 2045 | 2050 |

|---|---|---|---|---|---|---|---|---|---|

| Electricity price excluding distribution | €/kWhel | 0.070 | 0.067 | 0.063 | 0.060 | 0.057 | 0.054 | 0.052 | 0.049 |

| Electricity price including distribution | €/kWhel | 0.093 | 0.088 | 0.084 | 0.080 | 0.076 | 0.072 | 0.069 | 0.065 |

| Fuel price excluding distribution | €/kWhth | 0.070 | 0.075 | 0.081 | 0.088 | 0.094 | 0.102 | 0.109 | 0.118 |

| Fuel price including distribution | €/kWhth | 0.079 | 0.085 | 0.092 | 0.099 | 0.106 | 0.115 | 0.123 | 0.133 |

| Hydrogen price excluding distribution | €/kWhH2 | 0.139 | 0.130 | 0.120 | 0.110 | 0.104 | 0.099 | 0.094 | 0.089 |

| Hydrogen price including distribution | €/kWhH2 | 0.181 | 0.170 | 0.156 | 0.144 | 0.137 | 0.130 | 0.123 | 0.117 |

| CO2 price | €/t | 9.000 | 28.00 | 52.00 | 61.00 | 68.00 | 75.00 | 100.00 | 150.00 |

| Fuel price | €/l | 0.700 | 0.750 | 0.812 | 0.875 | 0.943 | 1.016 | 1.094 | 1.179 |

| Vehicle | Type | Unit | 2015 | 2020 | 2025 | 2030 | 2035 | 2040 | 2045 | 2050 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| LDV | ICE | E | €/km | 0.062 | 0.064 | 0.063 | 0.061 | 0.060 | 0.060 | 0.055 | 0.049 |

| GHG | €/km | 0.002 | 0.006 | 0.009 | 0.010 | 0.008 | 0.006 | 0.003 | 0.001 | ||

| BEV | E | €/km | 0.017 | 0.015 | 0.012 | 0.010 | 0.009 | 0.008 | 0.007 | 0.006 | |

| GHG | €/km | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| PHEV | E | €/km | 0.030 | 0.027 | 0.024 | 0.022 | 0.020 | 0.019 | 0.018 | 0.016 | |

| GHG | €/km | 0.001 | 0.001 | 0.002 | 0.002 | 0.002 | 0.001 | 0.001 | 0.000 | ||

| FCEV | E | €/km | 0.050 | 0.046 | 0.035 | 0.031 | 0.027 | 0.026 | 0.020 | 0.018 | |

| GHG | €/km | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| BUS | ICE | E | €/km | 0.323 | 0.342 | 0.363 | 0.384 | 0.407 | 0.431 | 0.457 | 0.484 |

| GHG | €/km | 0.010 | 0.030 | 0.055 | 0.061 | 0.057 | 0.043 | 0.026 | 0.006 | ||

| BEV | E | €/km | 0.174 | 0.160 | 0.146 | 0.134 | 0.123 | 0.113 | 0.104 | 0.095 | |

| GHG | €/km | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| PHEV | E | €/km | 0.248 | 0.251 | 0.249 | 0.259 | 0.265 | 0.272 | 0.280 | 0.289 | |

| GHG | €/km | 0.005 | 0.015 | 0.026 | 0.031 | 0.028 | 0.021 | 0.013 | 0.003 | ||

| FCEV | E | €/km | 0.566 | 0.507 | 0.446 | 0.392 | 0.355 | 0.322 | 0.291 | 0.264 | |

| GHG | €/km | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| MDV | ICE | E | €/km | 0.179 | 0.183 | 0.185 | 0.187 | 0.189 | 0.192 | 0.194 | 0.194 |

| GHG | €/km | 0.002 | 0.006 | 0.010 | 0.010 | 0.009 | 0.006 | 0.004 | 0.001 | ||

| BEV | E | €/km | 0.087 | 0.074 | 0.063 | 0.053 | 0.047 | 0.041 | 0.036 | 0.032 | |

| GHG | €/km | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| PHEV | E | €/km | 0.142 | 0.139 | 0.136 | 0.134 | 0.132 | 0.132 | 0.131 | 0.129 | |

| GHG | €/km | 0.003 | 0.010 | 0.017 | 0.018 | 0.016 | 0.011 | 0.007 | 0.001 | ||

| FCEV | E | €/km | 0.247 | 0.219 | 0.189 | 0.164 | 0.146 | 0.130 | 0.116 | 0.102 | |

| GHG | €/km | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| HDV | ICE | E | €/km | 0.277 | 0.277 | 0.276 | 0.275 | 0.273 | 0.272 | 0.271 | 0.268 |

| GHG | €/km | 0.004 | 0.012 | 0.021 | 0.021 | 0.018 | 0.013 | 0.008 | 0.001 | ||

| BEV | E | €/km | 0.174 | 0.148 | 0.125 | 0.107 | 0.094 | 0.083 | 0.073 | 0.064 | |

| GHG | €/km | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| PHEV | E | €/km | 0.246 | 0.238 | 0.231 | 0.224 | 0.220 | 0.215 | 0.211 | 0.207 | |

| GHG | €/km | 0.006 | 0.017 | 0.029 | 0.031 | 0.027 | 0.019 | 0.011 | 0.002 | ||

| FCEV | E | €/km | 0.382 | 0.332 | 0.282 | 0.241 | 0.211 | 0.185 | 0.162 | 0.141 | |

| GHG | €/km | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| Vehicle | Type | Unit | 2015 | 2020 | 2025 | 2030 | 2035 | 2040 | 2045 | 2050 |

|---|---|---|---|---|---|---|---|---|---|---|

| LDV | ICE | €/km | 0.299 | 0.314 | 0.329 | 0.335 | 0.340 | 0.345 | 0.347 | 0.350 |

| BEV | €/km | 0.491 | 0.340 | 0.309 | 0.285 | 0.283 | 0.282 | 0.281 | 0.281 | |

| PHEV | €/km | 0.318 | 0.313 | 0.312 | 0.310 | 0.313 | 0.316 | 0.319 | 0.322 | |

| FCEV | €/km | 0.471 | 0.396 | 0.346 | 0.314 | 0.310 | 0.309 | 0.304 | 0.303 | |

| BUS | ICE | €/km | 1.286 | 1.291 | 1.314 | 1.319 | 1.326 | 1.335 | 1.364 | 1.426 |

| BEV | €/km | 1.196 | 1.070 | 0.986 | 0.918 | 0.881 | 0.847 | 0.815 | 0.793 | |

| PHEV | €/km | 1.310 | 1.258 | 1.225 | 1.200 | 1.183 | 1.168 | 1.166 | 1.184 | |

| FCEV | €/km | 2.348 | 2.012 | 1.753 | 1.542 | 1.447 | 1.359 | 1.280 | 1.216 | |

| MDV | ICE | €/km | 1.240 | 1.233 | 1.193 | 1.169 | 1.144 | 1.132 | 1.125 | 1.128 |

| BEV | €/km | 1.190 | 1.083 | 0.973 | 0.904 | 0.866 | 0.841 | 0.816 | 0.794 | |

| PHEV | €/km | 1.312 | 1.263 | 1.190 | 1.144 | 1.111 | 1.091 | 1.075 | 1.067 | |

| FCEV | €/km | 1.405 | 1.263 | 1.127 | 1.042 | 0.993 | 0.957 | 0.923 | 0.893 | |

| HDV | ICE | €/km | 1.194 | 1.227 | 1.254 | 1.263 | 1.270 | 1.278 | 1.295 | 1.323 |

| BEV | €/km | 1.458 | 1.271 | 1.134 | 1.037 | 1.015 | 0.996 | 0.980 | 0.967 | |

| PHEV | €/km | 1.263 | 1.261 | 1.259 | 1.249 | 1.250 | 1.252 | 1.262 | 1.279 | |

| FCEV | €/km | 1.306 | 1.218 | 1.143 | 1.086 | 1.059 | 1.037 | 1.018 | 1.002 |

| Vehicle | Type | Unit | 2015 | 2020 | 2025 | 2030 | 2035 | 2040 | 2045 | 2050 |

|---|---|---|---|---|---|---|---|---|---|---|