Ramping-Up Electro-Fuel Production

by

, ,

, ,

Ralf Peters

1,2,3,*,

Maximilian Decker

1,4,

Janos Lucian Breuer

1,4,

Remzi Can Samsun

1 and

Detlef Stolten

2,4,5

1

Institute of Energy and Climate Research—Electrochemical Process Engineering (IEK-14), Forschungszentrum Jülich GmbH, Wilhelm-Johnen-Str., 52428 Jülich, Germany

2

JARA-ENERGY, 52056 Aachen, Germany

3

Faculty of Mechanical Engineering, Synthetic Fuels, Ruhr-Universität Bochum, Universitätsstr. 150, 44801 Bochum, Germany

4

Chair for Fuel Cells, RWTH Aachen University, 52072 Aachen, Germany

5

Institute of Energy and Climate Research—Techno-Economic System Analysis (IEK-3), Forschungszentrum Jülich GmbH, Wilhelm-Johnen-Str., 52428 Jülich, Germany

*

Author to whom correspondence should be addressed.

Energies 2024, 17(8), 1928; https://doi.org/10.3390/en17081928

Submission received: 1 March 2024

/

Revised: 19 March 2024

/

Accepted: 10 April 2024

/

Published: 18 April 2024

(This article belongs to the Special Issue Advances in Powertrain Design for Greener and Sustainable Non-road Mobile Machineries)

Abstract

:Future transport systems will rely on new electrified drives utilizing batteries and hydrogen-powered fuel cells or combustion engines with sustainable fuels. These systems must complement each other and should not be viewed as competing. Properties such as efficiency, range, as well as transport and storage properties will determine their use cases. This article looks at the usability of liquid electro-fuels in freight transport and analyzes the production capacities that will be necessary through 2050 in Germany. Different scenarios with varying market shares of electro-fuels are considered. A scenario with a focus on fuel cells foresees a quantity of 220 PJ of electro-fuels, i.e., 5.1 million tons, which reduces 80% of carbon dioxide emissions in LDV and HDV transport. A further scenario achieves carbon-neutrality and leads to a demand for nearly 17 million tons of e-fuel, corresponding to 640 PJ. Considering a final production rate of 5.1 million tons of electro-fuels per year leads to maximum investment costs of around EUR 350 million/year in 2036 during the ramp-up phase. The total investment costs for synthesis plants amount to EUR 4.02 billion. A carbon-neutrality scenario requires more than a factor 3 for investment for the production facilities of electro-fuels alone.

1. Introduction

1.1. Boundary Conditions for Sustainable Transport

Vehicles newly registered from 2035 in the EU will no longer be permitted to emit CO2, with the fleet limits for passenger cars expected to fall to zero. The EU member states, amongst others, agreed on this at the EU Environment Council in June, 2023, as well as on numerous points of the Fit for 55 package [1]. With a view to future transportation using combustion engines, the aim is to ensure that vehicles which are registered from 2035 will only be powered by climate-neutral fuels (electro fuels = e-fuels). The EU Commission has agreed to make a proposal for this outside of the system of fleet limit values. According to the German federal government’s common understanding, this also applies to cars and light commercial vehicles.

For passenger road and light-duty vehicle (LDV) transport, there are very efficient technologies available in the form of battery-operated electric vehicles and those based on fuel cells using hydrogen. Within this paper, LDV transport refers to light commercial vehicles (LCV), i.e., LCV < 3.5 tones. Nevertheless, for a number of heavy-duty vehicle (HDV) applications, the only option in terms of the required range is to use a liquid energy source. This is particularly true in the aviation sector for medium- to long-range missions. With regard to heavy-duty transport, various future power train solutions for long-haul trucks were reviewed by Peters et al. [2].

Bründlinger et al. [3] reported on guidelines for a successful energy transition in 2018, considering a CO2 emissions reduction of 80%, in line with the goals at that time. The future development of road utility vehicles is of particular interest for this study, as in this sub-sector, the requirements for high payloads meet those for long ranges, which makes electrification especially difficult. This is also reflected in the studies that provide values for market developments in the form of new registration shares of alternative drive types in various truck classes, see the list in Section 1.2. Twelve scenarios with suitable data for new registration numbers by drive type were found in six of these. To enable them to be compared, the new registration forecasts for three truck classes were summarized, broken down by permissible total weight: <3.5 tons; 3.5–12 tons; and >12 tons.

It should also be noted that the scenarios presented here apply to an 80% reduction target in an intermediate stage towards climate neutrality. If this climate neutrality is to be achieved by 2045, the challenges of a possible ramp-up for electro-fuels must be overcome even more rapidly. Another effect arises from dropping sectoral targets, such as for the transport sector itself. The entirety of all sectors must meet the CO2 reduction targets now. In the intermediate stages of CO2 reduction, not all sectors will have to meet the targets in lockstep—those with higher CO2 reduction potential will be able to compensate for those with lower CO2 savings. However, there will always be sectors, such as agriculture, with fossil-related CO2 emissions that cannot be de-fossilized either by completely changing the energy conversion in the process chain through electrification or by using e-fuels. To achieve the goal of complete climate-neutrality for those applications, the Direct Air Capture (DAC) process must also be applied, enabling even negative emissions.

1.2. Scope of This Work

The origins of this study lie in a doctoral thesis of Maximilian Decker [4], which was carried out at the Research Center Jülich between 2016 and 2019. In this work, the initial goal was to reduce CO2 quantities by 80% by 2050 for duty transport in Germany. Taking into account increasing transport capacity on the one hand and analyzing the shift of propulsion systems towards electric power trains, a reliable and reasonable forecast of future liquid fuel demand is required. In the course of the research process, a 95% reduction was considered, which would have a significant impact on the fuel quantity structure. The question of the possible origin of liquid fuels in the future will also be examined as part of this work. First, the proportion of fossil-based, bio-based and electricity-based fuels is open. An ever-increasing reduction in CO2 emissions is increasing the proportion of renewable fuels.

However, valuable conclusions can also be drawn from the developed modeling approach concerning complete climate neutrality. This will be discussed in the conclusions. Finally, three research questions arose:

- How much liquid fuels are demanded in future?

- How much renewable hydrogen must be provided to synthesize these fuels?

- How should the ramp-up of sustainable fuel production be designed?

As already mentioned above, there are very efficient solutions based on electrical systems for car traffic. There are a variety of possible solutions in freight transport and liquid fuels also have their place. This work therefore focuses heavily on the truck sector. To be able to pursue the actual research questions, the following questions must be asked first:

- How much energy is demanded for duty transport in future generally?

- What proportion of vehicles run on liquid fuels?

For this reason, the results of various studies are presented in the next section.

1.3. Electrification Scenarios of Commercial Vehicles

In the wake of the recent increase in political ambitions to defossilize the transport sector, a number of studies have emerged that deal with the implementation of this goal. These studies employ different approaches, both in terms of methodology and due to different technical foci. This sub-section presents a review of the literature that relates to the future development of the transportation and fuel sectors. From a technical point of view, the main topics of these studies are partially in the field of electric transportation or fuels, or they are designed to be sector-wide. In some of the studies presented, the propagation technologies in a system and their impact in the future (system-oriented) are considered. Others look at the development prospects of a particular technology (technology-oriented). To structure the different studies, a matrix was created for the subject areas of focus, i.e., the categories of fuels, mobility sector and electromobility, and the range of study objectives, i.e., technology-oriented or cost- and system-oriented.

The following listing provides an overview of the relevant studies, within this matrix structure:

- System-focused and cost-based for fuels:

Cambridge—Fueling Europe [5],

ICCT—CO2 based SF [6],

Dena—E-Fuels [7],

WEC—PtX Roadmap [8],

Agora—SynCost [9],

IWES—Potenzial PtL Importe [10],

Öko—PtX [11],

Pietzker—Energy economic models [12],

Schnülle—PtF Sozioök [13];

- System-focused and cost-based for transportation:

FVV—RiT [14],

MKS—EEiV [15],

IFEU—TREMOD [16],

IFEU—Klimaschutzbeitrag des Verkehrs 2050 [17],

EWI—Energieszenarien [18],

UBA—Energieversorgung des Verkehrs [19];

- System-focused and cost-based for electric transportation:

Renewbility [20],

Öko—Emobil [21];

- Technology-focused for fuels:

MKS—CNG/LNG Lkw [22],

Agora—Stromspeicher für die Energiewende [23],

DLR—Alternative Kraftstoffe [24],

BMVI—Nationaler Strategierahmen Infrastruktur alt. Kraftstoffe [25],

DLR—Drop-in KS Luft [26],

FVV—Kraftstoffstudie ‘13 [27],

Prognos—Flüssige Energieträger [28],

UBA—Integration von PtG/PtL [29],

Wuppertal—PtL [30];

- Technology-focused for transportation:

Shell—Lkw [31],

Shell—Pkw [32];

- Technology-focused for electric transportation:

MKS—Brennstoffzellen-Lkw [33],

MKS—HOL Lkw [34],

Shell—Wasserstoff [35],

NOW—Antriebssysteme [36],

EMobilBW—Nullemissionsnutzfahrzeuge [37].

There are basically two approaches to creating such a scenario: top-down and bottom-up. In the top-down approach, the development of a quantity to describe the overall transport is assumed. Mostly, it concerns the transport performance in the form of passenger kilometers for passenger transport and tonne kilometers for freight transport. A country’s transport performance is also linked to developments in other sectors, so cross-sector variables such as gross domestic product (GDP), demographic change or industrial development are often used to select assumptions [38].

The forecasts of the development scenarios for the new registration structure of trucks over twelve tons (Figure 1) result in a highly heterogeneous picture. Suitable data from eleven scenarios described in six studies was found and evaluated for the class of heavy-duty trucks. Three studies each present a scenario in which there is no electrification at all in this size class. All three scenarios in the Cambridge Econometrics study show the same proportions of internal combustion and plug-in hybrid vehicles in 2050, but differ in the electrification technology used. The Cambridge Econometrics BEV (battery–electric vehicle) scenario is the only one that predicts extensive electrification (approximately 80%) by pure BEVs in this segment; all other studies connect the majority of battery drives with overhead lines for mobile power supply. Overhead lines only play a role in the heavy-duty class. Four scenarios contain new registration shares of fuel cell trucks, namely the electrification and PtG (Power-to-Gas) scenario of the dena study and the fuel cell-heavy scenarios of the studies by Cambridge Econometrics and the BMDV (Federal Ministry for Digital and Transport, formerly BMVI: Federal Ministry for Transport and Infrastructure). Three of these scenarios indicate a new registration share of fuel cell drives in the range of around 80% for 2050.

The comparison of the medium-duty truck class with permissible total masses between 3.5 t and 12 t, shown in Figure 2, shows a similarly heterogeneous picture to that of heavy-duty trucks. Suitable data from ten scenarios described in six studies was found and evaluated for the class of medium- and light duty trucks. Three of the scenarios exhibit new registrations of electrified drivetrains of 30% or less. This contrasts with four scenarios with shares of over 85%. The two scenarios from Shell’s commercial vehicle study [31] only contain values for the new registration structure for 2040. Here, it can be seen that Shell’s forecasts with regard to the sale of electric drivetrain types in this truck class are highly conservative. Furthermore, it is noticeable that fuel cell drives only play a role in the scenario in the Fraunhofer study. This scenario only covers the period up to 2030, but until then it forecasts highly optimistic electrification rates in new registrations of around 20% FCEVs and 60% BEVs.

For light commercial vehicles under 3.5 t, there is a clearer tendency towards high electrification rates for the year 2050 (Figure 3). In five of the seven scenarios that provide data for the year 2050, the proportion of electrified drives amongst new registrations is over 90%. Only the “PtL” scenario of the dena study, with a focus on the use of synthetic fuels, shows an electrified proportion of 40%. The operating behavior of light commercial vehicles is particularly user-friendly compared to battery–electric drivetrains, as the average range requirements are low at around 100 km per day in the latter case [39]. The proportion of new registrations of FCEVs in 2050 will vary between approximately 10% and 40% under the scenarios. As in the other classes, the data from the Shell study for the year 2040 is on the conservative side of the spectrum, whereas the data from the Fraunhofer study for 2030 is on the optimistic side.

How were the results in Figure 1, Figure 2 and Figure 3 achieved in these studies? A brief outline is given below.

Öko—Emobil [21]: the guidelines for future mobility were developed as part of expert workshops. Based on the future images developed in their scenario process, concrete scenarios were formulated and described in more detail based on the development of transport demand, the new registration structure, the development of efficiency at vehicle level and the development of energy demand.

Dena—E-Fuels [7]: two scenarios were taken into account based on the expectations of the European Commission how the EU28 will develop this purpose. Additionally, historical data for 1995, 2010 and 2015 were applied. An adaptation was performed that had considered occupation rates and annual driving volume per vehicle in combination with real data for the period 1995 to 2015 for fuel consumption and car registrations.

IFEU—TREMOD [16]: the trend scenario is based on assumptions about traffic development in accordance with the the 2030 Federal Transport Infrastructure Plan from the German Federal Ministry of Transport and Infrastructure (BMVI) and further assumptions for the update until 2035.

Cambridge—Fueling Europe [5]: comparable to [21], an expert panel was established to develop various reasonable technology deployment scenarios, also considering historically based diffusion rates for low-carbon technologies, as well as the range of existing projections for future technology diffusion. The panel also gave advice on the most relevant input data on mobility, vehicles, energy, infrastructure, and economy. The agreed datasets were then applied into a stock model on the European level. Each scenario includes the total amount of capital investments and the energy consumption per drive technology on an annual basis. Finally, the outputs from the stock model were fed into the macro-economic model.

Shell—Lkw [31]: for this purpose, the current trends in transport logistics for goods and people and vehicle statistics are examined and potential is more relevant technologies estimated. Conversely, with the help of goods traffic modeling and scenario technology, as well as linking important transport, energy, and environmental policy parameters, the ways in which truck and bus traffic comprehensively influences developments in Germany are considered. The most important results are provided on an annual basis.

BMVI—Nationaler Strategierahmen Infrastruktur alt. Kraftstoffe, MKS—EEiV [15,25]: the starting point for the scenarios for 2030 was the efficiency potential that is emerging as a result of technological developments in vehicle technology. Regarding average excess or reduced consumption, it was assumed that technical measures play a larger role. For technological development and scenario generation in commercial and freight transport up to 2050, the full costs for the user (total cost of ownership) were used for the use of drives in vehicles. The following effects were considered to be highly modifiable: prices for fuel and energy, the cost reduction of essential technical components, and the development of new drive technologies. The existing uncertainties were taken into account, with the foreseeable trends using differently designed scenarios. The result was three scenarios: (1) hybridization and electrification, (2) liquid natural gas (LNG) and synthetic natural gas (SNG), and (3) hydrogen and fuel cells. The scenarios were simulated using the TREMOD program.

In summary, all studies create a very inconsistent picture. Each of these studies is logical and comprehensible in its methodology. Nevertheless, they are all based on a basic idea, which varies greatly from study to study. We therefore took up the idea from the studies for the BmVI [15,25], in which different scenarios were developed. In this work, the results from such scenarios, i.e., the shares of the battery-electric, fuel cell-hydrogen and internal combustion engine drive trains, are required for the market diffusion model introduced in Section 3.4. Due to the very different results, five scenarios have been developed according to the methods in [15,25].

1.4. Approaches in the Literature

The transport studies presented in the previous section show that e-fuels need to be used in freight transport to replace fossil fuels and reduce CO2 emissions.

System analytical studies look at the interaction between energy production and energy storage. These models are often highly complex in spatial networks with high resolution and optimize the energy system with cost functions. Programs that contain elements of artificial intelligence will be used more frequently in the future. For example, Li et al. [40] reported on a comparative techno-economic analysis of large-scale renewable energy storage technologies. The main focus was a comparison between batteries and hydrogen storage. Welder et al. [41] applied a spatio-temporal optimization of a future energy system for power-to-hydrogen applications in Germany. Electro-fuels were not considered and are only a follow-up product.

Techno-economic studies such as those by Schemme et al. [42,43], Brynolf et al. [44,45], and Grahn et al. [46] show the evidence of electro-fuels in general and provide information about the costs of e-fuels and the investment costs required for such production systems. Quantity estimates for the production of electro-fuels are published by Hansson et al. [47]. They analyzed the potential for electro-fuel production in Sweden from utilized fossil and biogenic CO2 point sources. The amount of carbon available determines the amount of electro-fuel, i.e., the supply chain.

A keyword search in the literature for electro-fuel production revealed a study from Schnuelle et al. [48] that considers electro-fuels from niche to market. They made use of an agent-based modeling approach. This model is explained by a turtle model with push and pull factors. Stakeholders, such as the operators of synthesis facilities, plant designers, and suppliers belong to this grouping, in addition to stakeholder networks carrying out research projects or industrial associations. Their investments were driven by the push and pull factors. The push factors include: regulative measures from policy, societal debates regarding land use or wind power installations, and technological progress by means of improved efficiency chains and materials. Pull factors can be incentives such as subsidiaries, project funding, and tax exemptions. There is also a market pull that is driving the development towards green fuels and materials and that enables sector integration for energy storage. Finally, a vision pull considered the climate effects, national image, and supply security. The results of the present work were analyzed in comparison to this one and are described herein. To classify the results from Schnuelle et al. [48], two results should be cited here: they proposed a maximum production capacity of 3.25 GW in 2035 and production costs below 13 ct/kWh, which corresponds to 1.3 EUR/lDE and are difficult to achieve.

This work aims to bring the demand for electro-fuels and the possible supply into harmony. In the existing studies, the time course for ramping up production of electric fuels is missing, especially regarding freight transport.

2. Methods

This section discusses the methods applied for the study on vehicle stock development, fuel demand, and infrastructure ramp-up.

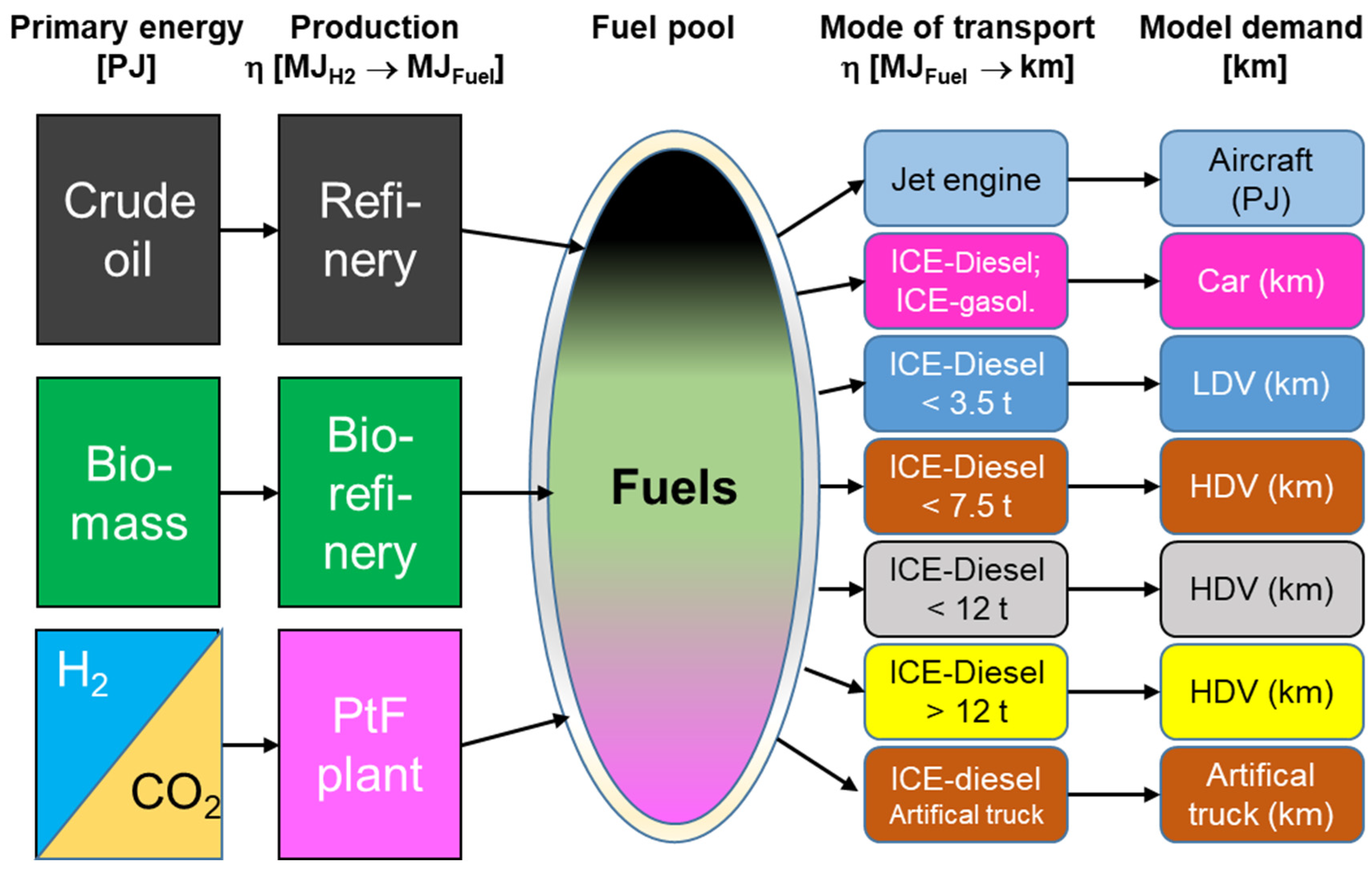

To estimate the amounts of energy required in the form of a fuel and the associated production capacities, it is necessary to formulate future forecasts for framework development in the transport sector. A set of coherent assumptions on the future development of the transport and fuel sectors is called a “scenario” in this work. Information included in such a scenario includes data from individual transport users, such as average fuel consumption, mileage, or vehicle loading, as well as sector-wide data such as total transport performance (in passenger or tonne kilometers), vehicle population, or new registrations by mode of propulsion. The relationship between these different assumptions and their compilation approaches is shown schematically in Figure 4. The bottom-up method is used in this work to create scenarios that consider the evolution of the vehicle fleet using temporal trajectories in the different weight classes for commercial light, medium and heavy commercial vehicles. The advantage of this approach is that current trend developments in specific vehicle classes can be considered in a much better way. Trends are not reflected linearly but follow a gently starting but progressive development, a fast and steep phase and a final degressive adjustment.

2.1. The S-Curve Method

The S-curve method is an approach developed by Pengg [49] for forecasting market developments. It combines Marchetti’s quantitative method, briefly described in the following text passages, and Vester’s qualitative approach. All of the concepts presented in this section can be explored in depth in Pengg’s dissertation [49]. The starting point for the applicability of the S-curve method to market forecasts is the proof of an isomorphism of biological and business systems through a description of the system dynamics according to Vester’s method. More details are reported by Decker [4] in the course of his PhD work.

2.1.1. Theoretical Background of the S-Curve Method

In brief, the following characteristics should be noted in relation to the methods of Marchetti and Vester:

- Marchetti’s method [50] applies the diffusion theory (Lotka–Volterra differential equation) to the spread of innovations. It is a one-dimensional (quantitative) method, in which development forecasts are based exclusively on past developments. On the positive side, it is highly reproducible and objective. Unfortunately, forecasts are independent of the system dynamics, i.e., of external influences. As a result, forecasts generated in this way are ambiguous without a system description and it offers no visible limits on the ability to forecast.

- Vester’s method of networked thinking [51] is used to describe and visualize complex systems and identify characteristic system dynamics by means of a qualitative system analysis method ([49], p. 207). It creates a system model that includes a description of interactions. It also offers qualitative insights into the system dynamics possible, but its conceptual models do not allow any quantitative statements.

Two example systems are used by Decker [4], in which two species or groups compete for a specific resource. In addition, the systems must be able to be viewed suitably separated from their environments. A biological and an entrepreneurial system are used as examples.

The example biological system used is described by two different yeast cell species competing for a limited amount of resources in a nutrient solution described by Vester’s method [51]. Regulatory circuits were identified for both species. In self-reinforcing control loops, the influencing variables only have a positive effect on each other. In the biological system, this applies to the relationship between “rate” and “stock”: a higher rate of proliferation causes a higher population of yeast cells, which in turn increases the rate of proliferation through a higher number of cells. Stabilizing control circuits are characterized in that a connection in the control circuit has a weakening effect. In the example, the additional stock has a positive effect on the rate, which in turn has a positive influence on the stock. However, a higher stock will negatively affect the additional stock, as the total number of yeast cells is limited. In the corporate example system used, two providers of mobile communications compete for market share in the mobile communications network. Again, both self-reinforcing and stabilizing control circuits can be identified in the system dynamics. Finally, the higher the total stock or market volume, the stronger the stabilizing control loop’s effect on the overall system, slowing down its development. For more details, see Decker [4].

It remains to describe the weighting of the control circuits: with low development (total stock of yeast cells or market volume), the self-reinforcing effects dominate the influence on the system. The higher the total stock or market volume, the stronger the stabilizing control loops effect on the overall system and slowing of development. After the comparison with the control dynamics presented above, an isomorphism (similarity of the systems) between the biological and corporate example systems is determined. From this, it is concluded that an abstract (mathematical) model for describing biological growth can also be applied to growth processes in market development. Such a growth model is embodied by the logistic function from diffusion theory. The logistic function can be formulated as an E function (see Equation (1)) and as a hyperbolic tangent function (see Equation (2)). The function, shown schematically in Figure 5, is defined by four parameters. The growth takes place from the initial value A to the final value G. At time t0 (turning point of the curve), exactly half of the growth phase is reached. The last parameter k is a measure of the slope of the curve at point t0. An alternative formulation of the slope parameter kh is used in the hyperbolic tangent form of the S-curve. The slope parameters of the different formulations can be propagated by Equation (3).

2.1.2. Application of the S-Curve Method

Building on the theory of the S-curve method, the connection and role of this method in the present study will now be outlined. The requirements for applying the S-curve method to individual growth phases are as follows:

- An innovation takes place and is accepted by the market.

- A certain market volume is identified as the saturation point.

In this work, the achievement of the national climate goals set out by the German federal government and EU are defined as a fixed goal. Furthermore, according to the objective from Section 1.2, the role of fuels as a contribution to these objectives should be analyzed analytically. With the required amount of fuels taken as the assumed necessary market volume, the S-curve method can be used to quantitatively describe the market development up to that point and thus derive consequences in terms of a fuel strategy. For this purpose, the modeling results obtained in Section 4.3 are combined in Section 3.7 with the S-curve method. Curve parameters are derived using historical data from the chemical industry, which are used for the evaluation. Furthermore, the logistical function is used in the inventory development to update current trends in the registration of commercial vehicles (i.e., as a one-dimensional quantitative method according to Marchetti [50]). It is therefore concluded that market growth phases—under the framework conditions determined by systemic analysis—can be described by the logistic function. More details can be found in Decker [4] in the course of his doctoral thesis.

2.2. The Monte Carlo Method

While the input data for the S-curve method is assembled into different cases through the scenario development, the aim of the Monte Carlo model is to combine all possible combinations of input data in one model. For this purpose, boundary conditions and model parameters are defined by probability distributions instead of fixed values. Based on the probability distribution, values for all parameters are then randomly determined and a system optimization is carried out for the dataset determined in this way. This process is repeated successively, and the model can then determine a probability distribution for the optimization results with different parameter combinations through a large number of optimization runs. Regarding the S-curve method, the system is a linear optimization problem, and the defined CO2 restrictions continue to apply as a boundary condition for the model. The probability distributions for the parameters of the system are described by gamma distributions. This distribution is defined by the three parameters lower limit xu, upper limit xo, and the value at which the probability density reaches its maximum xm. The probability density of a gamma distribution with the corresponding parameters is shown in Figure 6 as an example. The evaluation of the model results is carried out using an observed value, which constantly changes according to the statistical parameter selection. In the present case, the evaluation is carried out based on the hydrogen requirement for the production of synthetic fuels and the total requirement for these. The parameter selection, as well as the implementation and results of the Monte Carlo simulation, are presented in Section 4.4.

3. Model Development

3.1. Bottom-Up Scenario Development for National Commercial Vehicle Traffic

As already described in Section 1.2, a scenario contains a dataset of conclusive assumptions for the framework developments in the transport sector. The scenarios serve as the data basis for the system simulations carried out with the models described in this chapter. As the aim of these system simulations is to optimize the fuel supply with which the set climate targets can be achieved, it must be possible to draw conclusions regarding the CO2 emissions from the model requirement (fuel requirement).

The chain shown in Figure 4 reveals the transformation path from the scenario key figures of vehicle stock, mileage, and fuel consumption to transport performance. In the bottom-up approach, a scenario is developed from below, i.e., starting from vehicle stock. The other variables are then calculated using statistical conversion factors. When transforming the variables, the correct balance area must be observed. For example, the fuel consumption relevant to CO2 emissions cannot be directly inferred from the national total mileage. It is therefore important to adapt the conversion factors to the changing balance areas. This relationship is illustrated in Figure 7 with the distinction between the national and inland accounts. The relationship plays an important role in the conversion of the number of vehicles (balance area national) to the national CO2 emissions of the transportation sector (balance area inland).

The key figures shown in the figure are described in more detail below. An overview of the data used, and the implementation of the scenario development will be presented in the following sections.

3.1.1. Determination of Key Figures

In the next step, average mileage can be used to draw conclusions regarding the mileage of domestic vehicles from the national inventory data. When calculating domestic mileage, it must also be taken into account that a portion of this will be covered by domestic vehicles abroad and that foreign vehicles drive domestically. The mileage share of domestic vehicles abroad (national) and foreign vehicles domestically (inland) was determined using the traffic performance survey of the Federal Highway Research Institute (Bast: Bundesanstalt für Straßenwesen) [52] for 2014 and is assumed to be constant.

The national fuel consumption and the resulting CO2 emissions could be calculated from the domestic mileage determined using average consumption values. For reasons of comparability with statistical data and for the estimation of market volume, it should also be possible to convert the mileage into national fuel sales. For this purpose, factors in the refueling behavior of residents abroad and foreigners in Germany are used. These values were taken from the study by the Federal Statistical Office [53]. A surcharge for unassigned consumption [53] was added to the pure consumption. This surcharge applies, for example, to workshop trips.

3.1.2. Future Forecast Studies

The future forecasts were carried out by fitting and regressing a logistic function (S-curves) to existing data. The subsequent calculation of the spread of electric vehicles was carried out using a market diffusion model. These model elements were then implemented in a Microsoft Excel spreadsheet to expound and evaluate scenario development.

The stock figures of the Federal Motor Transport Authority (translated from German: KBA: Kraftfahrt-Bundesamt) were used as the data basis for the forecasts of the stock development [39]. The stock data is given for trucks, tractor units and buses, divided into 21 weight classes. The used KBA publication contains data from 1960 to 2017, with a new counting method having been introduced from 2008 and consistent annual data only being available from this year [39]. For commercial vehicles in all classes shown, the population development up to the year 2050 is forecast by means of an S-curve adjustment. As average data for weight classes is not available in the same level of detail as in the KBA inventory data, the classes are then summarized. Tractors and buses are not grouped according to weight class but by the type of use.

3.1.3. Electrification Rates in the Market Diffusion Model

The proliferation of electrified vehicles in the form of BEVs and FCEVs is examined by means of a market diffusion model. The model incorporates the inventory of commercial vehicle classes from year to year, considering annual replacement rates. The development of the entire portfolio was carried out using the methodology described above. The number of new registrations for each class per year was determined by considering the average service life of a vehicle. These were in turn assigned proportionally to the BEV, FCEV, and ICE drivetrain concepts. The proportion of new registrations of electric drivetrains was calculated using an S-curve development, the parameters of which were determined using the literature research presented in Figure 1, Figure 2 and Figure 3. In addition, the fuel requirement estimates of the literature scenarios (Section 3.7) were analyzed and—based on the emerging trends—lessons for the practicable introduction of alternative drivetrains and fuels were derived to develop two independent development scenarios. The model results were stock developments by drivetrain type for the commercial vehicle classes considered from 2010 to 2050 and the corresponding domestic and international mileage, as well as estimates for fuel consumption and sales. The domestic mileages by drivetrain type serve as input data for the fuel system models in Section 3.5 and Section 3.6. In a subsequent step, the annual production capacities of FCEVs and the corresponding number of vehicles on road were determined from the new registration figures. By comparing these with national targets for the use of FCEVs by 2030, the plausibility of the calculated market development was evaluated. Furthermore, the demand for hydrogen for use in FCEVs could be derived.

3.2. Validation of The Key Figure Conversion Method for the Reference Year 2010

To determine the future energy supply for transport, the framework developments in the sector must first be determined. Scenarios are used for this purpose. The description of a scenario’s content, as well as an overview of the literature scenarios, was included in Section 1.2. In this sub-chapter, a new driving performance scenario is presented using the bottom-up method described in Section 3.1. To be able to be used as a basis for determining fuel requirements, the mileage development was supplemented with two different scenarios for the development of electric transportation. The two applied electrification scenarios (PROG-FC and PROG-Mix) were based on different assumptions. As a comparison, the three reference scenarios (ICE, BAT, and FC) from the BMVI study [15], which were already included in Figure 1, Figure 2 and Figure 3, were presented. These scenarios were based on the results of the traffic integration prognosis [54] and the data of the TREMOD [12] study and reflect a neutral academic consensus as part of the mobility and fuel strategy (MFS) of the German federal government. Furthermore, the study is structured transparently, so that the interim results and assumptions used can be understood. A concluding comparison and discussion of the developed scenarios in this work and those from the literature can be found in Section 5.1. The three literature scenarios of the BMVI study, which are used as input data for the fuel supply modeling to be able to compare the influence of the different scenario approaches, are evaluated in Section 4.3 in more detail. Due to the more important role of road transport fuels, the bottom-up approach was only applied to this sub-sector. The developments of the other modes of transport were supplemented using data from the literature.

To validate the methodology presented in Section 3.1, the calculation of mileage, fuel consumption, fuel sales, CO2 emissions, and transport performance should be carried out from the inventory data for 2010 and then compared with available literature. The year 2010 was chosen as the reference year because all the literature sources used provide data for it. The only exception was the mileage survey of the Federal Highway Research Institute (bast) [52,55], which was carried out for 2014. Table A1 in the Appendix A lists the factors used in the literature. Table A2 and Table A3 show the number of vehicles as a starting point and the calculated values based on this.

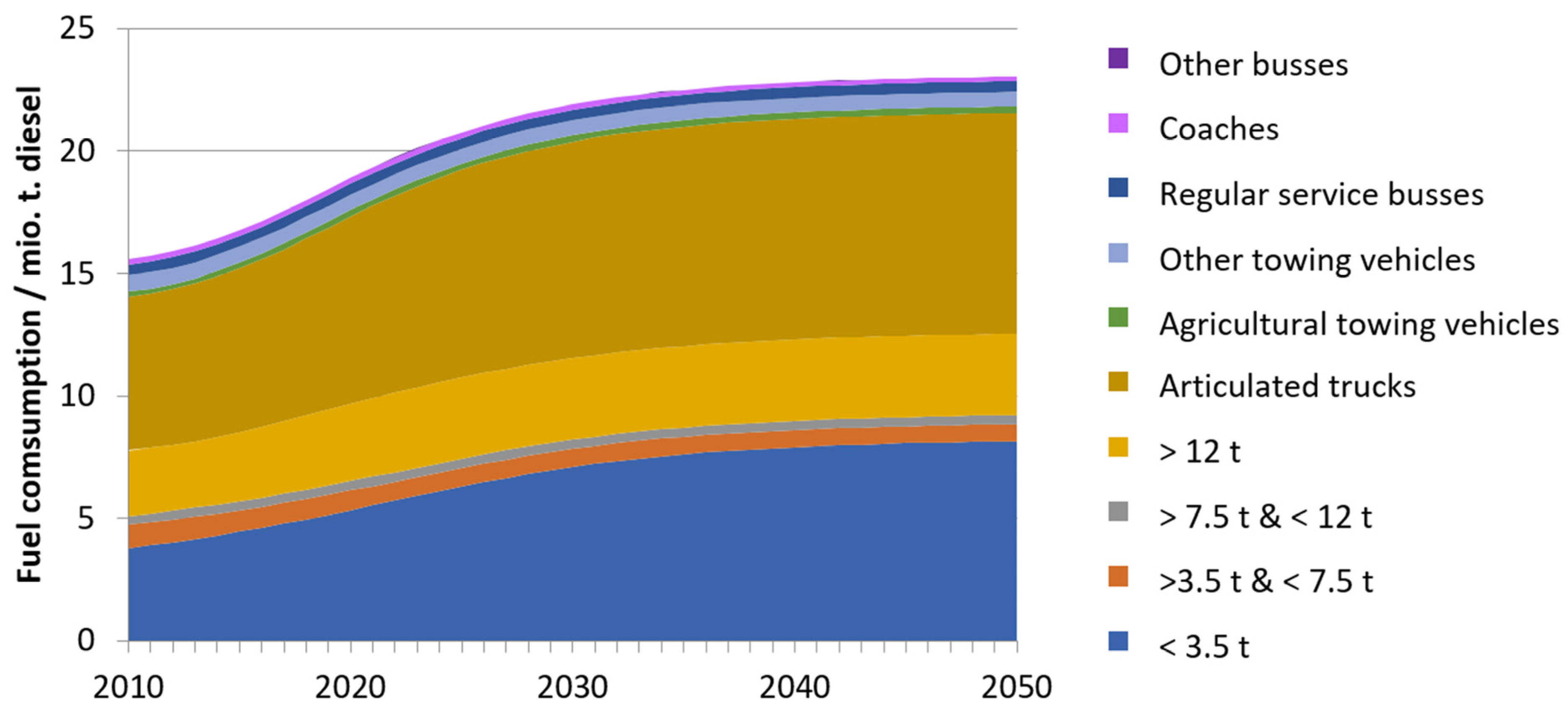

The calculated domestic mileage of 76.96 billion km exhibits good agreement with the domestic mileage from the bast mileage survey, with a deviation of approximately 10% [55]. This deviation is almost entirely due to the calculated mileage of trucks under 3.5 t. When calculating domestic mileage, a significant mileage share of 40% can be attributed to foreign vehicles in truck classes over 3.5 t. As a result, the inland mileage of 96.24 billion km is 15% higher than the national mileage. With a deviation of approximately 10%, this value also agrees well with the value from the mileage survey [7]. The value of the domestic fuel consumption based on this, including unallocated consumption, is 15.81 million tons of diesel fuel. Less the share for buses, the total fuel consumption of road freight traffic corresponds to 14.69 million t of diesel fuel, which in turn corresponds to the value of 14.7 million t from the study by the BMVI [15]. At 1.14 Mt/a, the unassigned consumption is also a relevant variable for the exact termination of the total fuel consumption and thus CO2 emissions. Based on this, the national fuel sales for heavy-duty traffic are calculated at 13.66 million t. For comparison, the MWV annual report [56] cites sales of 29.2 million t of diesel fuel for commercial and passenger vehicle traffic. Approximately half of this is used in commercial transport, which means that this value is also in the range of the literature comparison. Figure 8 shows the breakdown of stock, mileage, fuel consumption, and transport performance of commercial road traffic by weight class. A clear reversal of the majority ratio of small trucks to large ones can be seen from the key figure under consideration. Although more than 80% of the stock consists of trucks under 7.5 t, around 60% of fuel consumption in freight transport is caused by heavy-duty trucks and semi-trailers over 12 t. This shows that the vehicle market in the light commercial vehicle segment has a significantly higher volume. Due to the high mileage, however, the largest market segment in terms of fuel sales is in heavy-duty trucks.

3.3. Development Forecast Model of the Commercial Vehicle Inventory

By fitting an S-curve to the inventory data points of the KBA for the years 2008–2017, the inventory forecasts for trucks, tractor units, and buses are created by weight. The forecasts are based on the 21 weight classes listed in the KBA [39] database. Due to the limited availability of statistical data, the vehicle stocks were combined into classes according to weight or type of use for the further calculation process.

Figure 9, Figure 10 and Figure 11 show the calculated population development of the various trucks, tractor units, and buses in the combined classes. The individual subclass S-curve fittings are shown in Figures A4–A7 listed in the appendix of Decker’s PhD thesis [4]. In Figure 12, a comparison between stock data from KBA [39] for 1970–2017 and the predicted data until 2050 is shown. Important vehicle classes are LDVs in the range of gross vehicle weights between 2.801 and 3.5 tons, smaller trucks of 7.5 tons, and HDV classes of 24–26 tons and greater than 26 tons. The average deviation between stock data in the period from 2008–2017 and the model is between 0.54–0.65% for the lower weight classes, the average standard deviation is between 0.62–0.85%. For trucks with a gross vehicle weight of more than 26 tons, the error sizes are larger at 1.75% and 2.08%, respectively. To demonstrate the effectiveness of the methodology, more recent stock numbers from 2018–2022 have been added to the graphs, see Figure 12. The latest figures display the predictions for almost all classes to be in good agreement with the real figures available. However, it also shows a weakness of the method. The S-curve methodology uses a saturation effect with a maximum value to be reached during the time evolution. This is difficult to estimate, particularly for rapidly increasing stock numbers. For the HDV class larger than 26 tons, just under 58,000 vehicles were estimated to be in Germany in 2022, but in reality, there were more than 62,500. The deviation amounts to 11.7% in 2022. This could also be seen to some extent for the LDV class of up to 3.5 tons. In 2022 the deviations between real stock data and model prediction amounts to 9.9%. In this context, it is interesting to observe what impact these deviations have on fuel consumption. Using the average mileage for trucks > 26 tons and their average consumption (see Table A2), the fuel consumption for the increase in vehicles of 6536 trucks is equivalent to 3 PJ per year. Compared to a total consumption of 613 PJ (model result of this work) or 632 PJ (the literature data from BMVI [15]) according to the Table 1, this is an additional consumption of 0.49% or 0.48%. This effect is noticeably larger for the weight class between 2.8–3.5 tons at 1.8% based on the total energy consumption of all trucks but is justifiable, taking the inaccuracies of the assumptions into account.

One reason for the rapid increase in freight transport between 2017 and 2022 is the strong growth of e-commerce. Goods are distributed to the providers’ interim warehouses using HDV with higher capacity (>26 tons). The customer receives the goods via commercial delivery vehicles, including those in the vehicle class 2.8–3.5 tons. The effect was also extremely increased during the corona pandemic between 2020 and 2022. Considering the S-curve methodology, the saturation value for HDV > 26 t could be increased from 60,000 to 75,000 or 80,000 to take these effects into account. Due to the low impact of around 2% in 2022 on the fuel consumption of the entire fleet, no adjustment was made. Nevertheless, the current forecasts are more reasonable than those based on unlimited growth.

Figure 13 shows the development of all commercial vehicles, composed of the evolution of the individual vehicle classes. In addition to the commercial vehicles of <3.5 t, the others and LFZM are numerically significant. The dominant role of trucks <3.5 t and semitrailer tractors in terms of stock development and fuel consumption, conversely, will continue to be expanded. Light commercial vehicles under 3.5 t experienced a strong increase in numbers from 1.77 million in 2008 to 2.38 million units in 2017.

This is due in large part to the trend towards increased inner-city package delivery services, which was reinforced by the COVID-19 pandemic. The prognosis by adapting the curve results in a doubling of the stock figures in this weight class from 2010 to 2050. Large trucks over 12 t, which are mainly used in long-distance transport, also undergo a stock increase of 24%, to approximately 235,000 in 2050.

Conversely, the stock trends show in the market segment of so-called large vans between 3.5 t and 7.5 t a decline of 26%. The already very small market segment for trucks between 7.5 t and 12 t remains largely at a constant level, with a slight increase. The semitrailer tractors used primarily for long-distance transport have experienced a large increase in recent years, which has continued through the adjustment of the S-curve from 180,000 in 2010 to around 260,000 units. This means that semitrailer tractors remain the largest carrier of the hauling capacity. Furthermore, an increase in the number of units for agricultural and forestry tractors (LFZM) and a decrease for other tractors can be noted. However, these two tractor types only account for a small share of consumption of around 5% of the total commercial traffic. In the field of buses, the number of regular-service buses remains at a constant level of around 36,000. There are different trends in different weight classes amongst coaches, leading to a short-term increase until 2017 and then falling to around 25,000. This is due to opposite developmental tendencies in the subclasses. Other buses remain at just under 13,000.

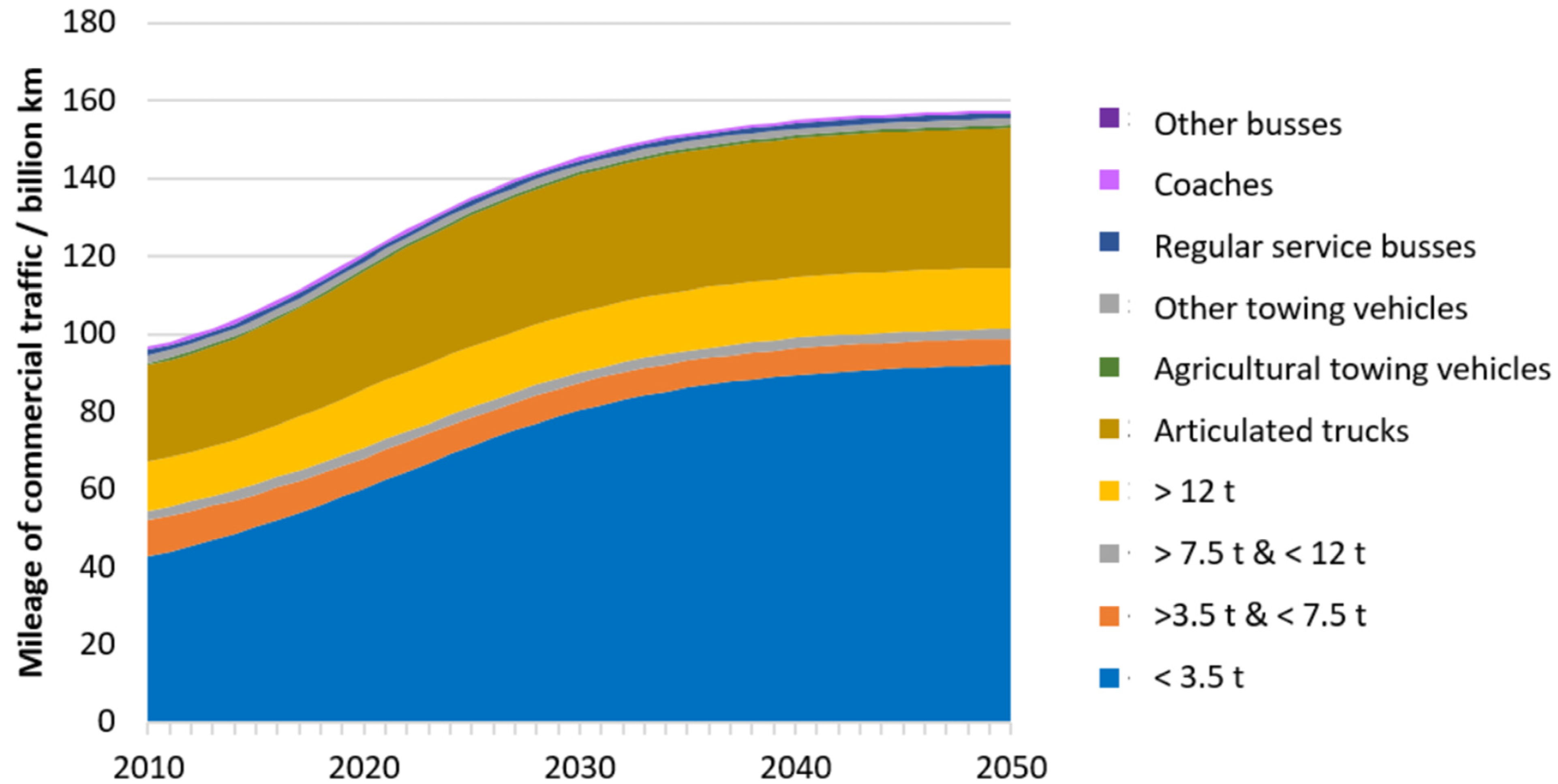

The average mileage from Table A4 in the Appendix A were used for this. The calculated total mileage is shown in Figure 14. The bottom-up method was used to calculate mileage in commercial traffic totaling 137 billion km in 2030 and 150 billion km in 2050. These values are approximately 20% higher than those of the top-down approach of the BMVI literature scenarios [15]. Based on this, transport services of 586.6 billion tkm in 2030 and 597.5 billion tkm in 2050 emerge. The calculated transport services are therefore below those of the comparison scenario (600 billion tkm in 2030 and 720 billion tkm in 2050 [15]). From these opposing tendencies of the two important indicators of mileage and transport performance, it can be concluded that the literature scenarios lead to increasing average loading factors. This is not comprehensible on the basis of current data, as the trend towards lighter and higher-quality products means that a reduction in the average load can be assumed in the future [57].

Based on the stock development and average mileage a fuel consumption can be calculated, that correspond to a business as usual scenario until 2050 solely using liquid fuels. Model parameters assumed to be frozen and remained at the 2010 level. This path should not be taken as part of a transport transition, as it either does not lead to the required reduction in CO2 emissions or requires the massive production of electro fuels. This calculation has therefore only been included graphically in the Appendix A, see Figure A1. The largest consumers in this analysis are articulated trucks with an annual requirement of 9.1 million tons in 2050, followed by commercial LDVs (<3.5 t) with 7.9 million tons and trucks (>12 t) with 3.6 million tons. Despite the large numbers, it is evident that agricultural and other tractors account for a very small proportion of fuel consumption. The total consumption of buses also accounts for only a small proportion.

3.4. Calculation of the Market Diffusion of Electrified Vehicles

The calculated stock development is complemented at this point with two electrification scenarios. The first (PROG–FC) is based on the electrification developments of the fuel cell scenario from the BMVI study [15], as this represents the scenario with the highest overall electrification rate. Furthermore, a progressive scenario (PROG–Mix) was developed, which reflects the literature scenarios through a more optimistic development of electric transportation by both BEVs and FCEVs. A concluding comparison of the scenarios is presented in Section 4.1 and Section 4.2.

3.4.1. Basic Assumptions of the Market Diffusion Model for Commercial Vehicles

As described in Section 3.1, the vehicle stock for each vehicle class is calculated by drivetrain type (BEV, FCEV, ICEV) using the market diffusion model. The basic development of the stock is given by the stock forecasts listed above. The number of new registrations is then determined by the average service life of vehicles. The annual development of the new registration structure according to drive type is again assumed in the form of an S-curve. The parameters t0 (year at mean spread), G (maximum value), and kh (degree of steepness) describe the S-curve in the hyperbolic tangent formulation from Equation (2). The assumptions of the S-curve parameters are explained in more detail below. PROG–FC: The parameters listed in Table A4 in the Appendix A for the development description of the new registration structure according to drivetrain type are based on the mileage shares of the fuel cell scenario from the BMVI study [15]. This way, the development of the mileage shares forecast in the literature scenario is projected onto the total mileage calculated in this work. The scenario is characterized by long-term, high-mileage shares of FCEVs. In contrast, the overall development of BEVs is lower, but can take a higher share in 2030 due to an earlier start of market penetration. In accordance with the development from the BMVI study [15], the steepness of the S-curves kh—as a measure of the propagation speed—is assumed to be 300 for all classes. PROG–Mix: The PROG–Mix scenario represents a progressive development with the strong implementation of electricity-based transportation. The tendencies of the literature scenarios of the BMVI [15] are taken into account: battery–electric transport can be implemented earlier, but the overall shares are lower. Fuel cell-powered transport will only take on significant market shares later, but by 2050 it will enable a higher proportion of the total electric mileage to be driven. The assumed curve parameters are listed in Appendix A (Table A5).

3.4.2. Development of Passenger Car Traffic

As with the calculation of the number of commercial vehicles, the spread of electrified drivetrains is described by an S-curve development of new registrations, which serves as an input for the market diffusion model. A linear relationship between inventory and mileage shares is assumed. The number of passenger cars in Germany was around 46.5 million vehicles in 2018 and is assumed to be constant up to 2050 in accordance with the literature studies presented (see Section 1.2). Furthermore, the total mileage of passenger car traffic for 2030 and 2050 is assumed to be 655 billion km [15] The S-curve parameters used are listed in Appendix A (Table A6).

The development of passenger car electrification in the PROG–Mix scenario is based on scenario developments from the H2 Mobility Study [58], Reuß [59], and Beneke [60]. The mileage share of ICE vehicles in 2050 should be 25%, that of BEVs 25%, and that of FCEVs 50%. As described above, the spread of electrified cars in the PROG–FC scenario is derived from the BMVI publication based on the FC scenario. The FCEV share of the car fleet here is around 40% in 2050.

3.4.3. Expansion of the Scenario for Other Modes of Transport

In the following, the scenario is completed by the other modes of transport to determine the total energy and fuel requirements of the transport sector. The developments in the modes of transport mentioned here are not extrapolated using the S-curves. In order not to neglect energy demand in the entire sector, a general demand block is defined in the optimization model.

Aviation. The fundamental difficulties in balancing CO2 emissions and fuel consumption in aviation were explained in detail by Decker [4]. There are generally three options for accounting for CO2 emissions in aviation: domestic, territorial, and international. Whereas the domestic approach only considers the emissions from flights that take off and land in Germany, the territorial one expands the balance to include the flight route shares that take place over the national air territory for flights that take off and/or land in Germany. The international approach, in turn, also includes the total route of all flights departing from Germany and is therefore in the range of kerosene sales. The territorial approach is used for further estimates of the fuel requirements, as forecast values for this approach are available in the literature. The kerosene requirement for this approach is 120 PJ in 2030 and 160 PJ in 2050 ([14], p. 56, [15], p. 18 and 116). In contrast to this is the current kerosene sales in Germany of 430 PJ [15,56] and the consumption currently balanced using the domestic flight approach of 26 PJ.

Other commercial vehicles: due to their heterogeneous usage and subordinate role in terms of energy consumption, the commercial vehicle subclasses of forestry and agricultural tractors, other tractors, and other buses were assigned to the group of other modes of transport in the optimization model. The assumed cumulative consumption of these modes of transport is 28 PJ in 2030 and 18 PJ in 2050.

Rail vehicles and ships: As rail and inland waterway transport is not considered in depth in this work, general values based on the literature are used for future fuel requirements. In accordance with the values from TREMOD [16] and the BMVI study [15], the diesel and electricity requirements for rail vehicles and ships are taken from Table A7 in the Appendix A.

3.5. Optimization of Fuel Supply Pathways

In addition, an optimization model for minimizing the primary energy consumption was set up for the calculation of the fuel supply pathways by Decker [4]. As the model does not play such a prominent role in the general statements of this article, it is only outlined in brief. The efficiency of fuel supply in the present case also corresponds to the supply costs. In a further step, another model developed by Decker [4] dealt in detail with system costs for the production of synthetic fuels. A value of 96 Mt was set as the limit for CO2 emissions by 2030. This value corresponded to a reduction of 40% against the emissions of 1990. The overall reduction targets for Germany within a stepwise reduction approach were changed in recent years. Currently, the target for CO2 emissions for 2045 is climate-neutrality. In further modeling set-ups by Decker [4], CO2 reduction scenarios of 80% and 95% were calculated. The CO2 emissions were assigned to the raw materials introduced in the sources. The transportation requirement, which must be covered by fuels via the conversion paths, were indicated by vehicle kilometers for all road vehicles, by a kerosene requirement for air traffic, and by a flat-rate requirement for the other modes of transport. The vehicles were classified by drivetrain type and, in the case of commercial traffic, also divided into weight classes. The drivetrains differ in Diesel and Otto technology, as well as methane-powered drivetrains. The distribution of the vehicle kilometers, which were provided by a specific drivetrain technology (only combustion engines), is therefore an endogenous calculation variable of the system optimization. During case analyses, fuel types in various combinations were approved to meet transportation needs. For example, the differences in the total energy requirement when using DME as an alternative diesel fuel, in contrast to a fuel supply limited to synthetic fuels in drop-in quality, can be determined. The list of case analyses for alternative fuels and their implementation and evaluation are described in detail by Decker [4].

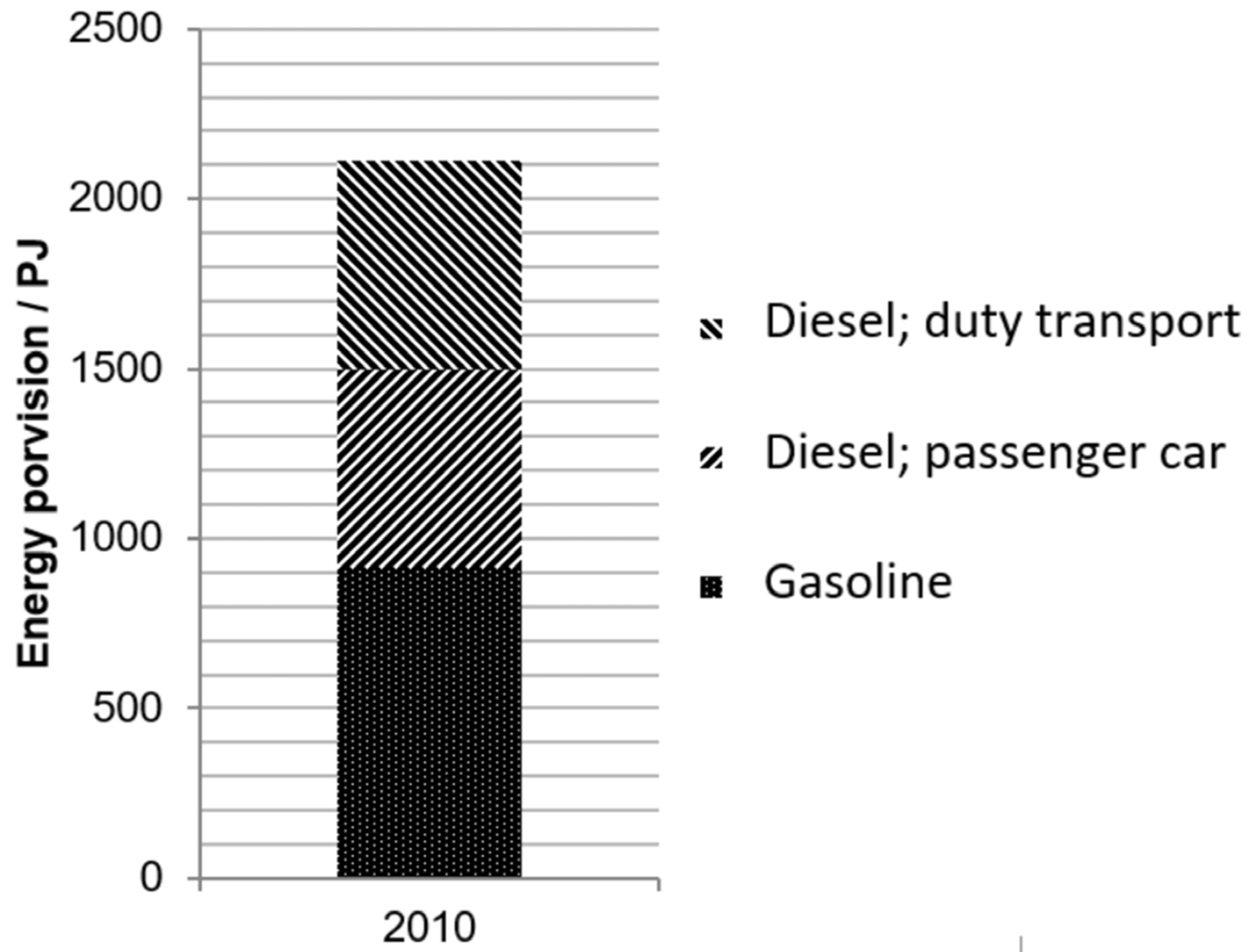

To check the model results for different fuel supply paths, the optimization model should first be run through with the boundary conditions for the year 2010. To carry out the validation, initially no restriction should be defined for the total CO2 emissions. As fossil fuels have the most efficient pathway to supply compared to alternative fuels, only these were selected for the model—as was the case with the real energy supply in 2010. The model results are presented in the form of energy supply in Figure 15.

Table 1 compares the calculated values with those from the literature. Both the fuel supply of the individual sub-sectors and the total amount show very good agreement, with deviations of less than 5%. The total CO2 emissions of the transport sector were calculated in the model by the total amount of fuel consumed. The result is a value of 154.9 Mt, which also agrees very well with the emissions reported by the BMU of 153 Mt in 2010 [61].

3.6. Sensitivity Analysis of Fuel Supply Pathways

As a next step, the sensitivity of the results was analyzed using a Monte Carlo simulation, as described in Section 2.2. For this purpose, a statistical distribution for their parameterization in a model run was defined for the following variables: costs of primary energy sources, mileages of combustion engines by vehicle class, transformers of simulation models, and maximum usable amount of biomass. The statistical distribution was defined using the lower limit value xu, the upper limit value xo, and the value at which the probability density reaches its maximum value, xm (cf. Section 2.2). The model of Decker [4] constructs a gamma distribution. In each model run, a value is determined for each of the affected parameters according to the statistical distribution and the overall system is then optimized. This process is repeated 100,000 times. Figure 16 shows the structure of the Monte Carlo model and the values used to construct the probability distributions. To be able to compare the influence of the different processes and process efficiencies the processes are summarized. This applies, for example, to the synthesis components of the PtF process, which are summarized for the Monte Carlo simulation and cover the efficiency spectrum of all possible syntheses in the distribution. In addition, the mileage as a model requirement includes the results of all scenarios considered.

All values used to set up the gamma distributions are listed in the PhD thesis by Decker (see Table A.6 in [4]). The values for the range of driving performance for calculating the fuel requirement form the maximum and minimum values from the five scenarios presented.

3.7. Derivation of Market Penetration Ramp-Up Based on Historical Data

The goal of demonstrating an implementation strategy should be complemented with the temporal development of a transformation phase. Historical data from the chemical industry is used in this chapter to provide the potential development speed of an industrial landscape for supplying transport with the identified electro-fuel requirements. In this section, the potential speed of expanding PtF production facilities is to be evaluated. As with the development of electric drivetrains in the vehicle market, the methodology of the market development forecast uses S-curves, with historical data on the production capacities of the chemical industry in Germany serving as the data basis.

According to the S-curve theory for forecasting market developments, identified market growth phases can be described with an S-curve, as per Equation (1). The course of the curve is defined by the parameters’ initial value A, end value G, turning point t0, and gradient at the turning point k. Transferred to the structure of PtF technology, the initial value for the production capacity at the beginning of the market growth phase is assumed to be zero. The assumption of the end value, which is reached after the market growth phase, is based on the results for the PtF fuel requirement from Section 3.5. This assumption is based on the fact that there is a market demand for this amount of PtF fuel. The turning point is chosen in such a way that the installed production capacity by 2020 is below that of a plant on a small industrial scale, corresponding to 30 MW or 0.02 Mt/a. The gradient at the turning point of curve k is to be determined below as the last parameter. For this purpose, historical data from the chemical industry is used to derive the parameters by fitting a curve to identified market growth phases. It is based on the assumption that the production of basic chemicals represents a comparable chemical process in a comparable branch of industry. Figure 17 shows the development of the annual production of ethylene and propylene, based on the historical data of the annual chemical industry reports [62,63,64,65,66,67,68,69,70]. The annual fuel requirement of 220 PJ or 5.1 Mt/a calculated in the reference case from Section 4.4 approximately corresponds to the value of the current ethylene production in Germany, which has been fluctuating between 4.6 Mt/a and 5.4 Mt/a in the last 15 years. It can therefore be stated that the production of the selected basic chemicals is similar to that of electro-fuels, also in terms of production volume. To derive the curve parameters, the phases of market growth from an initial level to an end one must be identified in the first step. These are recognized in the present diagram for the production of ethylene in the period from approximately 1962 to 1990 and 1987 to 2016, and for propylene from approximately 1975 to 2010.

The curve fitting (see Figure 17) was performed by minimizing the standard error on the data points (blue) of the above periods. The resulting curves are shown in red.

4. Results

4.1. Market Diffusion Model

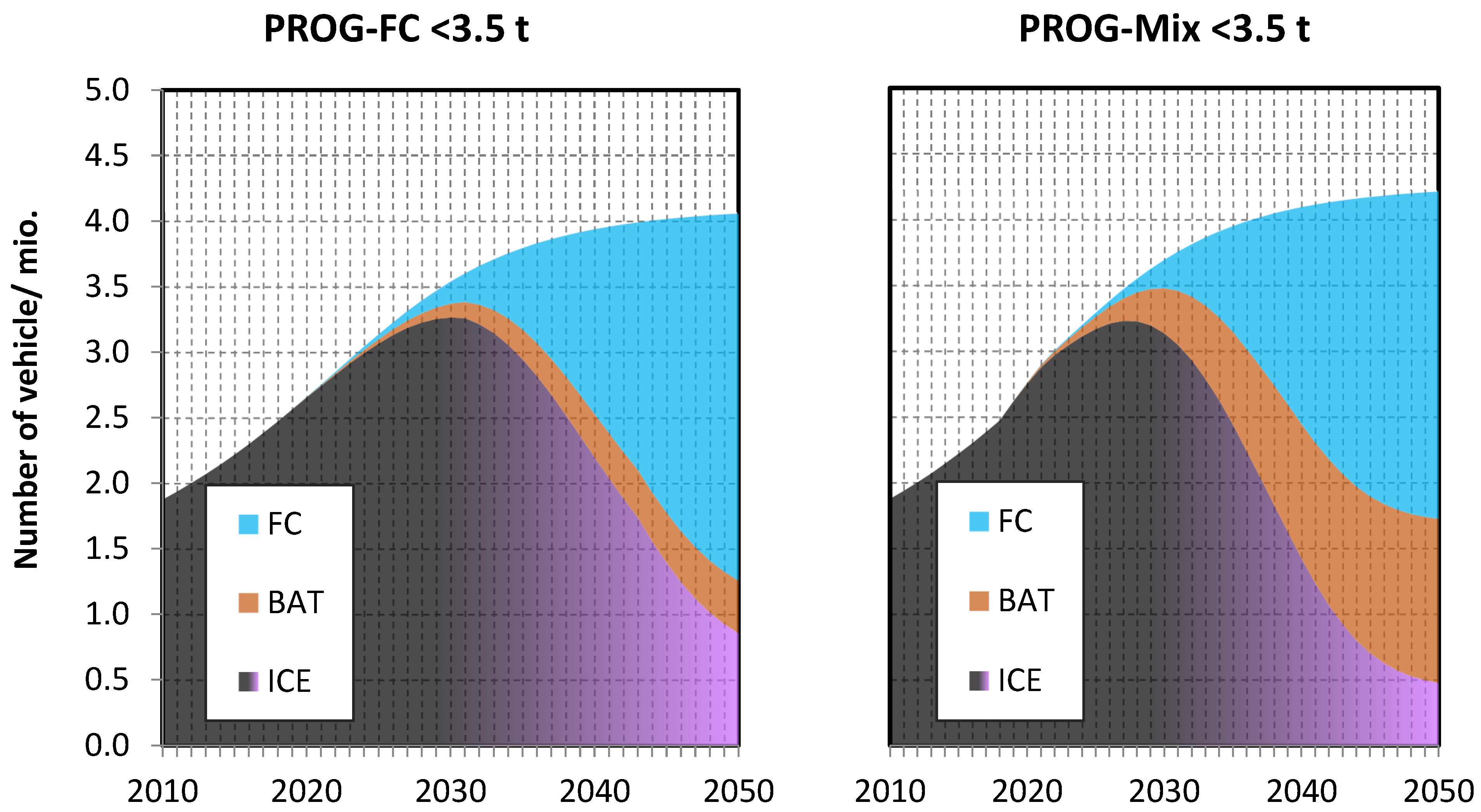

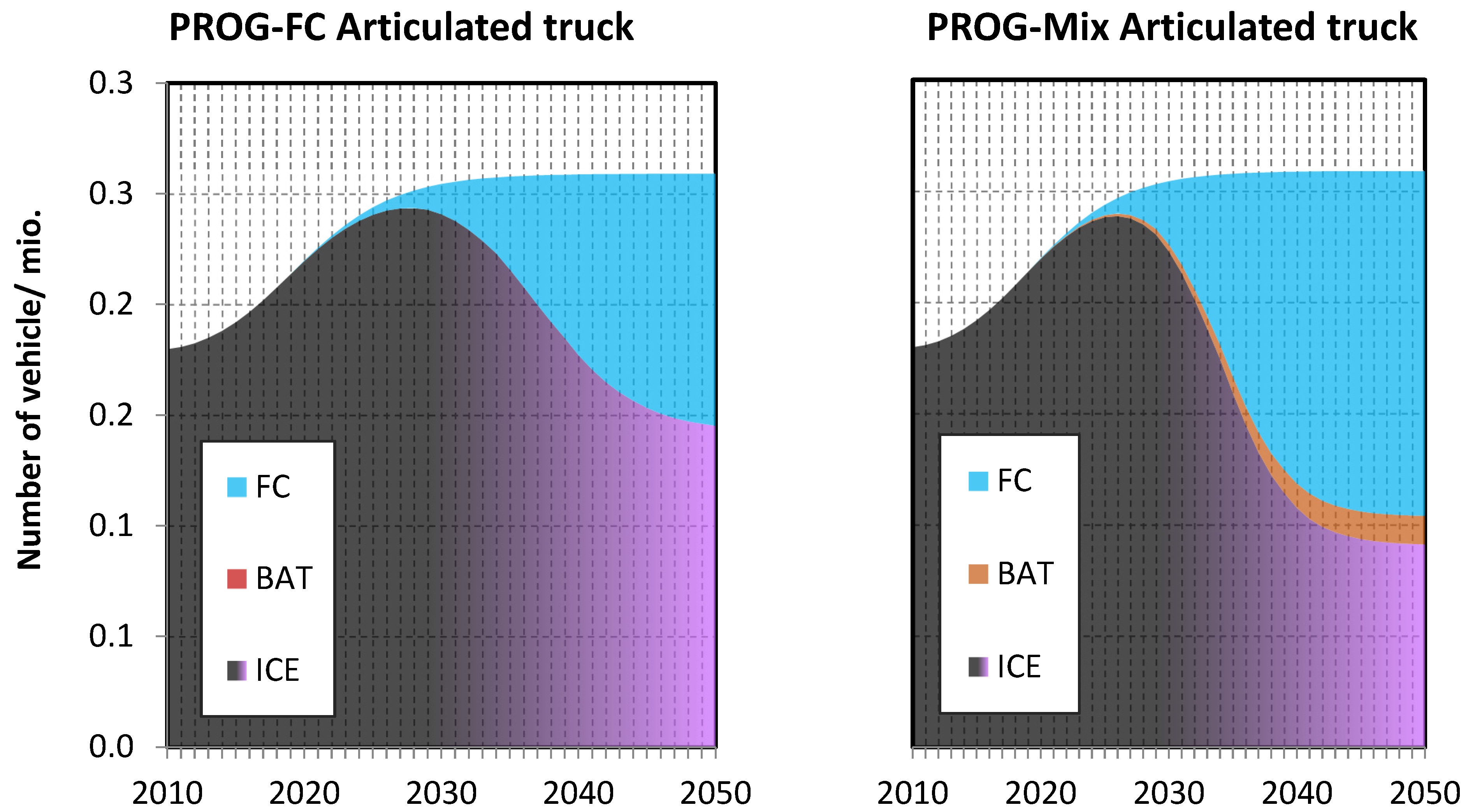

Figure 18 shows the development of the light truck (under 3.5 t) fleet and that of articulated trucks (Figure 19) for both scenarios (PROG-FC and PROG-Mix), as an example of the results output of the model. The illustrations of the remaining class developments are presented by Decker [4] in the appendix of his PhD thesis. It is important to note that the absolute stock number of vehicles in each class corresponds to the development forecast model, see Section 3.3. The market penetration of new drive technologies occurs through new vehicles, i.e., through new registrations. The number of new registrations is determined from the average service life of the vehicles. The annual development of the new registration structure by drive type is again assumed to be in the form of an S-curve.

In the case of light commercial vehicles, shown in Figure 18, a clear increase in stock numbers can be noted. In the PROG–FC scenario, the electrified parts of the stock develop somewhat more slowly than in the PROG–Mix scenario. New registration shares in 2030 are 6.4% for BEVs and 14.0% for FCEVs, and accordingly occupy 3.1% and 5.0% of the total stock.

By 2050, the share of new registrations will reach their maximum share of 10% for BEVs and 75% for FCEVs. The stock reaches a share of 10% BEVs and 68.7% FCEVs by 2050. In the PROG–Mix Scenario, BEVs will begin to make up a noticeable proportion of the stock from 2020 onwards. A few years later, sales of FCEVs will also increase. In 2030, 19.3% of newly registered vehicles will be battery-powered and 18.8% will be fuel cell-powered. This will lead to stock shares of approximately 9.2% BEVs and 5.9% FCEVs. By 2050, both new registrations and the number of light trucks will each reach a maximum of 30% BEVs and 60% FCEVs, respectively.

Due to the requirements for high loading capacities and at the same time long ranges, it is assumed that BEVs will only marginally penetrate the articulated truck market segment (see Figure 19). In the PROG–FC scenario, it is assumed there will be no penetration of BEVs in the heavy-duty truck segment. By 2050, a new registration and existing share of 45% is assumed. In 2030, the proportion of new registrations will be 8.4%, and the proportion of existing vehicles will be 5.4%. In 2024, fuel cell-powered semi-trailer tractors will, for the first time, account for one percent of the stock in the PROG–Mix scenario. In 2030, the number will be 11.2%, with 18.8% of new registrations. The maximum value of 60% by the year 2050 will also almost be reached with semi-trailer tractors.

4.2. Market Development of FCEVs in the Scenarios

In this section, the results of the scenario development are evaluated based on the stock development of FCEVs and the total mileage by drivetrain type, compared with the literature, and discussed.

For further analysis of the outlined development scenario, the corresponding development of FCEV production should be considered in terms of the new registration figures. In this way, the plausibility of the electrification scenarios can be estimated by comparing the figures with sales targets from the literature. The stock number development of FCEVs calculated using the model is shown in Figure 20a,b. For clarity, the chart is truncated at 4 million units. It can clearly be seen in the figures that the overwhelming majority of fuel cell-powered vehicles will be passenger cars.

In the PROG–FC scenario, the number of commercial FCEVs in 2030 will be over 1.5 million. This number can be compared to the other national targets of 800,000 vehicles in Japan, for example, which, with a GDP of USD 4.97 trillion and with a population of 126 million, is a country of comparable size and economic strength to Germany (whose GDP is around USD 4.0 trillion and that has a population of 83 million) is [20] very optimistic. In the PROG–Mix scenario, conversely, it is assumed that the market development of FCEV passenger cars will start later, and so the number of FCEVs in 2030 will still be less than 1 million. This reflects the goals of Japan. With around 900,000 units, the PROG–Mix scenario embodies an ambitious but realistic target for the spread of FCEVs.

4.3. Fuel Requirements under Different Development Scenarios

In the following, the models for optimizing the fuel supply pathways are applied to the future scenarios. Five different development scenarios are used to describe the boundary conditions. This includes the three literature scenarios from the BMVI study [15], as well as the two scenarios, PROG–FC and PROG–Mix, developed in Section 3.2. The demand for mileage shares for the different drive types will be compared in the next chapter. Some important cornerstones are:

- As these calculations were made from the perspective of CO2 reduction in the sense of the federal government’s official balance sheet, it is assumed that biofuels, electro- fuels, and electric transportation are fully CO2-free.

- Due to the territorial approach, the energy requirements of aviation are included in the model calculation to a limited extent.

- The use of natural gas in the transport sector is initially limited to 79 PJ/a in 2030 and 193 PJ/a in 2050 according to the electrification scenario of the BMVI study [15] and thus represents a scenario with a moderate need for infrastructural expansion. The impact of permitting alternative fuels is discussed in greater detail for this case by Decker [4] and will be published separately.

- The primary energy potential of biomass for the transport sector is 400 PJ. These are in the form of residues containing lignocellulose and can be divided into different synthesis routes by the model (see Decker [4]). The output corresponds to around 200 PJ, according to the literature research conducted regarding the biofuel potential.

Figure 21 shows the results of system optimization for the five scenarios considered in the form of energy use, broken down by final energy type and source. In this model, only drop-in quality fuels are permitted for use in the transport sector. In an analysis carried out by Decker [4], the influence of enabling different alternative fuels on the fuel distribution is also considered. Drop-in fuels are characterized by the fact that they can be mixed with conventional ones in any amount without requiring any infrastructure or vehicles to be retrofitted.

In all of the scenarios considered, electro-fuels were used as a supplement to electric transportation and biofuels in order to achieve sufficient CO2 reduction. As the required proportion of electro-fuels in the PROG–Mix scenario is very low, at 55 PJ, a further calculation was carried out with the aim of achieving a 95% (instead of an 80%) CO2 reduction. Due to the restriction on CO2 emissions and a maximum limit on biofuels, there is a certain quota of fossil fuels that must be observed. Considering the superior efficiency of the fuel supply via the fossil path, this is exhausted in all scenarios. Natural gas is advantageous compared to liquid fossil fuels due to the lower CO2 emissions related to its energy content. The maximum permissible amount of natural gas of 193 PJ is exhausted in all scenarios. In the scenario with a 95 percent CO2 reduction, the entire contingent of fossil fuels is exhausted via natural gas. The necessary quantities of liquid fuels for air, ship, and other commercial transport are covered by the bio route and electro-fuels. As the CO2 calculation in the present model is based on official regulations, no emissions from the upstream chain, such as those caused by methane slip, are included. The ICE scenario, which will increasingly rely on the use of combustion engines in the future, has by far the highest energy requirement. All scenarios assumed a biofuel capacity of 201 PJ in 2030 and 186 PJ in 2050. In 2030, the entire biofuel stock will be used for road transport, while in 2050, 123–134 PJ will be used for biojet fuel. An electro-fuel requirement of 268 PJ in 2030 and 980 PJ in 2050 was determined to meet the specified CO2 targets. These amounts of electro-fuels correspond to a hydrogen demand of 1163 PJ or approximately 10 Mt in 2050. The BAT scenario exhibits the highest electrification rates in 2030, due to a focus on battery–electric mobility. This leads to the lowest electro-fuel requirement amongst the scenarios of 139 PJ in 2030. The FCEV scenario also achieves slightly higher electro-fuel requirements of 193 PJ in 2030 compared to BEVs due to the later spread of FCEVs. The literature study by the BMVI [15] assesses the overall electrification potential. However, electrification in the FC scenario is higher than in the BAT one, which changes the picture and an electro-fuel requirement of 259 PJ (FC) contrasts with that of 404 PJ (BAT).

As the electrification of the transport sector in the PROG–FC and PROG–Mix scenarios reaches a comparatively low level in 2030, the demand for synthetic fuels is high at this point. In the PROG–Mix scenario, because fewer FCEVs are taken into account in 2030, and the demand for electro-fuels is particularly high at 240 PJ. Due to the extensive spread of electric transport by 2050, the demand for electro-fuel will drop to 221 PJ in the PROG–FC scenario and 55 PJ in the PROG–Mix one, despite the CO2 reduction targets of 80%. As the PROG–Mix scenario saves considerable amounts of CO2 solely through its high electrification rate, the possibility of pursuing more ambitious climate goals can be examined here. In a further analysis, a CO2 reduction of 95% was examined in combination with the PROG–Mix scenario. A demand for 368 PJ of electro-fuel was determined, of which 26 PJ is kerosene.

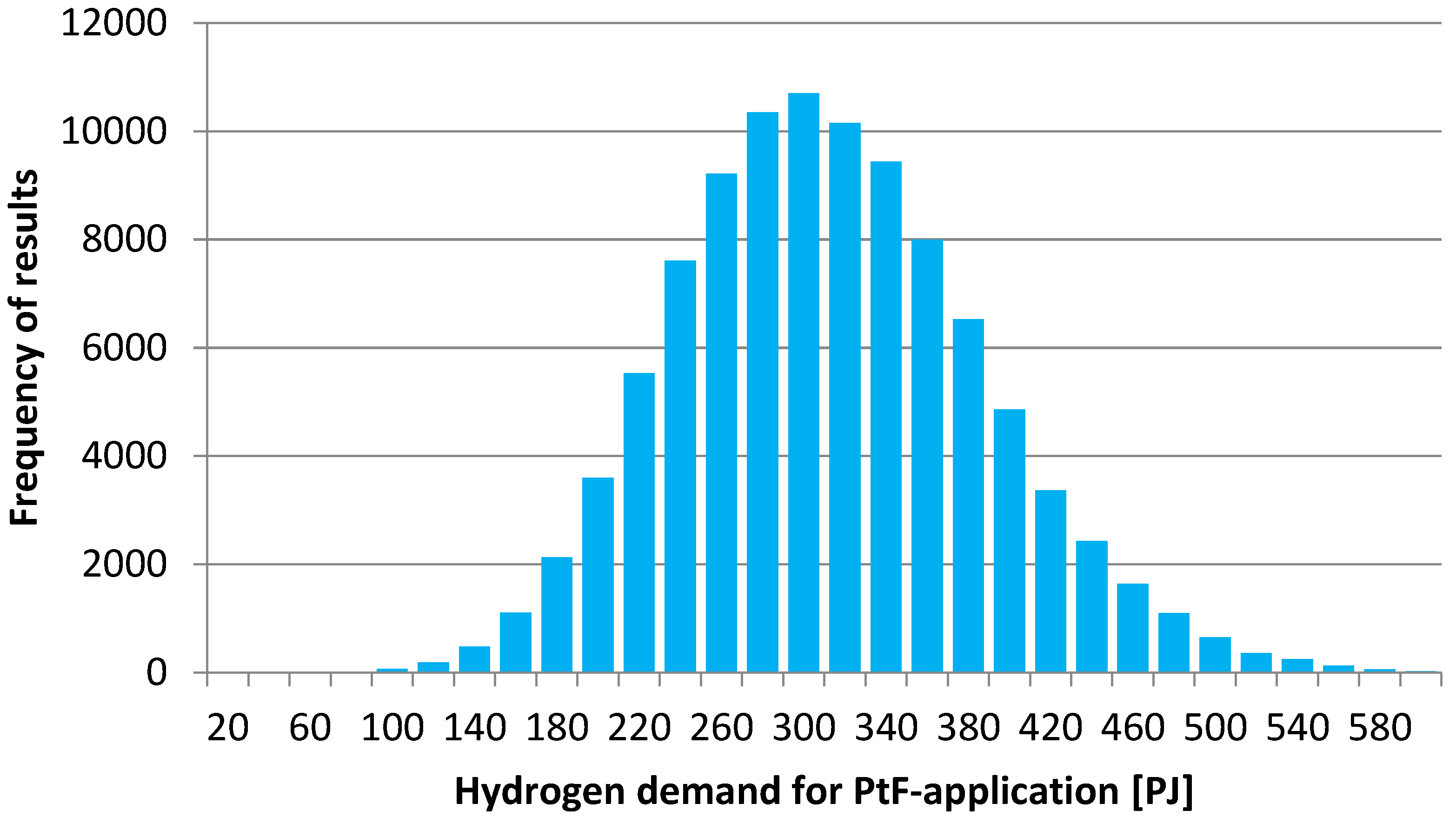

4.4. Results from the Monte Carlo Method

The evaluation of the Monte Carlo simulation was carried out using characteristic values that were calculated during the modeling. The hydrogen and fuel quantities were used here as meaningful parameters. In Figure 22 and Figure 23, the Monte Carlo simulations are evaluated based on the number of times a particular result occurred over 100,000 runs. The statistically most-frequently-occurring value of the hydrogen requirement for use in PtF technology is 300 PJ (see Figure 22), which corresponds to 2.5 million tons of hydrogen. Taking the efficiency of the comparatively less efficient FT synthesis of 74.9% as the average plant efficiency into account, this corresponds to a fuel quantity of 220 PJ, which is in line with the results from Section 4.3. In Figure 23, the simulation is evaluated based on the frequency of the results for the total demand for PtF fuels. Here, the highest occurring frequencies around the 240 PJ PtF fuel requirement point are collected.

4.5. Application of the S-Curve Method to the Development of PtF Technology

4.5.1. Ramping-Up PtF Production Capacity

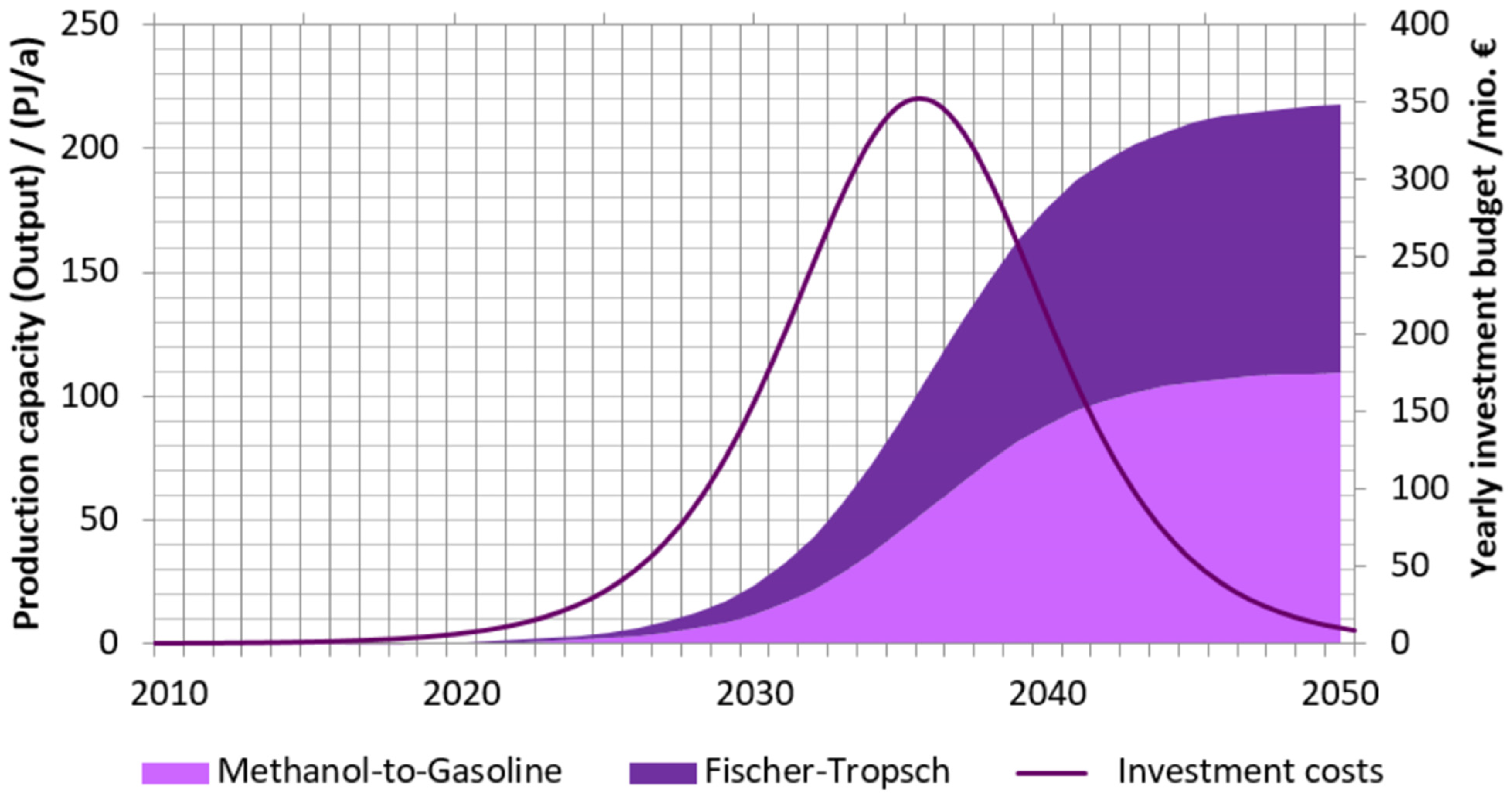

The insights derived from the previous sections regarding the expansion rate of chemical production plants are to be applied to electro-fuel production in this section. The required production capacity of the PtF plants from the reference case of 7613 MW or 5.1 Mt/a output capacity is assumed to be the target value for market saturation G. The parameter t0 was chosen so that in 2020 there was a production capacity of less than 30 MW or 0.02 Mt/a. This assumption is based on the previous definition of the smallest synthesis plant on an industrial scale.

Assuming that the construction of PtF plants begins immediately, both development speeds mean that the required production capacities can be built up by 2050. The limit at which 90% of the saturation value is achieved is reached in 2043 with a development of k = 2.85, and in 2037 with k = 2. In 2030, the S-curves reach 0.55 Mt/a (825 MW) and 1.37 Mt/a (2050 MW), corresponding to a fuel production of 24 and 59 PJ. The production capacities determined in this way remain below the calculated requirements of 217 PJ of the PROG–FC scenario and even below those of the most optimistic BEV scenario with an electro-fuel requirement of 139 PJ. One option to meet the demand for electro-fuels would be a targeted import strategy. This, in turn, could be associated with economic advantages if production were to take place in favorable regions for renewable energy production. Against this background, a decision should be made as to what proportion of PtF production ought to be implemented in Germany and to what extent imports should be used. If the production deficit is compensated for by imports in 2030, it is likely that the production capacity shown for 2050 will not be additionally built up in Germany. Despite the cost advantage of PtF production in preferred regions, it can be economically advantageous to implement a portion of the production in Germany. In Figure 24, the calculated setup of the PtF production capacity is plotted by the selected process route, together with the corresponding annual investment costs. The investment costs for the synthesis plants are taken from Decker [4] for the case with pure drop-in fuels (reference case). The more conservative gradient factor of k = 2.85 is used for the speed of market development. In 2036, these will reach a maximum of around EUR 350 million per year. The total investment costs for synthesis plants total EUR 4.02 billion.

Before the results can be compared with other studies, a few assumptions must be made. This work incorporated results from the process analyses utilized by Schemme et al. [42], which assume an annual operating time of the systems of 8000 h. A fuel production of 220 PJ annually by 2050 can be achieved through a capacity of 7.64 GW. Regarding 2035, the annual production of 100 PJ leads to a capacity of 3.47 GW. This corresponds very well with the results of Schnuelle et al. [48], with 3.25 GW in 2035 being the highest capacity. However, these production capacities are significantly lower than those calculated by Agora Energiewende [71] and Henning and Palzer [72]. Agora Energiewende reported a demand of PtF capacities of 50 GW in 2025 and 134 GW in 2050 [71]. Henning and Palzer [72] even see a capacity of 200 GW in 2050 in conjunction with a CO2 reduction of 90% to be achieved. However, these numbers must be viewed from the perspectives of 2014 and 2015, respectively. Following the values of this work capacities for electro-fuel production of 7.63 GW must be installed for 80% CO2 reduction and 22.2 GW for climate neutrality in 2045. However, these values only apply to the transport of goods with LDV and HDV. There will be additional needs to be covered by aviation, passenger car transport and the chemical industry. The values in this work are also lower because a high proportion of electrification in passenger transport was assumed. However, this may be the key to dampening the extremely high capacities of the other studies [71,72].

4.5.2. Hydrogen Demand