An Investigation of the Influence of the Worldwide Governance and Competitiveness on Accounting Fraud Cases: A Cross-Country Perspective

Abstract

1. Introduction

2. Theoretical Background

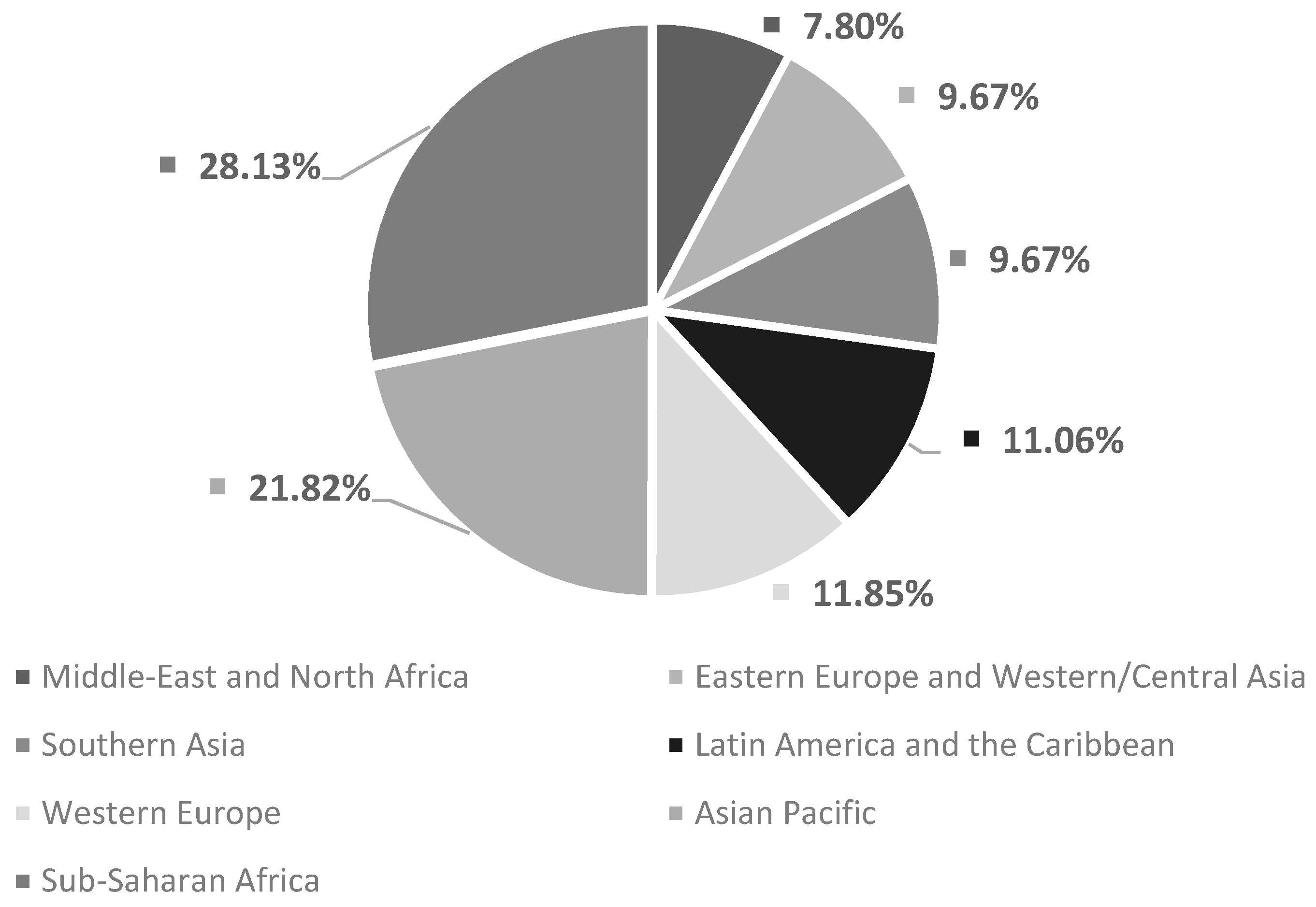

3. Data and Methodologies

4. Results and Discussion

5. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

Appendix A

{kind=link}

| Independent Variables | COC | GOE | POS | REQ | RLW | VOA | ln(GDP) | ln(GCI) |

|---|---|---|---|---|---|---|---|---|

| COF | 1.000 | |||||||

| GOE | −0.702 | 1.000 | ||||||

| POS | −0.497 | 0.106 | 1.000 | |||||

| REQ | 0.109 | −0.441 | 0.091 | 1.000 | ||||

| RLW | −0.092 | −0.052 | −0.248 | −0.547 | 1.000 | |||

| VOA | −0.812 | 0.561 | 0.686 | 0.017 | −0.304 | 1.000 | ||

| ln(GDP) | 0.282 | −0.098 | −0.339 | −0.259 | 0.280 | −0.225 | 1.000 | |

| ln(GCI) | −0.805 | 0.432 | 0.762 | 0.051 | −0.166 | 0.764 | −0.511 | 1.000 |

References

- Lerner, K.L.; Lerner, B.W. World of Forensic Science; Thomson/Gale: Farmington Hills, MI, USA, 2006; ISBN 1414402953. [Google Scholar]

- Garner, B.A.; Black, H.C. Black’s Law Dictionary; Thomson/West: Egon, MN, USA, 2004; ISBN 978-0-31-415199-5. [Google Scholar]

- Association of Certified Fraud Examiners (ACFE). Report to the Nations Detection: On Occupational Fraud and Abuse; ACFE: Austin, TX, USA, 2016. [Google Scholar]

- Dorminey, J.W.; Fleming, A.S.; Kranacher, M.-J.; Riley, R.A. Beyond the Fraud Triangle. CPA J. 2010, 80, 41–54. [Google Scholar]

- Hoti, S.; McAleer, M.; Pauwels, L.L. Modelling Environmental Risk. Environ. Model. Software 2005, 20, 1289–1298. [Google Scholar] [CrossRef]

- Vaughan, D. The Dark Side of Organizations: Mistake, Misconduct, and Disaster. Annu. Rev. Sociol. 1999, 25, 271–305. [Google Scholar] [CrossRef]

- Rutherford, M. Institutional Economics: Then and Now. J. Econ. Perspect. 2001, 15, 173–194. [Google Scholar] [CrossRef]

- North, D.C. Economic Performance through Time. Am. Econ. Rev. 1994, 84, 359–368. [Google Scholar] [CrossRef]

- North, D.C. Institutions, Ideology, and Economic Performance. Cato J. 1991, 11, 477–496. [Google Scholar]

- Weingast, B.R. The Economic Role of Political Institutions: Market-Preserving Federalism and Economic Development. J. Law Econ. Organ. 1995, 11, 1–31. [Google Scholar] [CrossRef]

- Turvey, B.E. Forensic Fraud : Evaluating Law Enforcement and Forensic Science Cultures in the Context of Examiner Misconduct; Academic Press: Cambridge, MA, USA, 2013; ISBN 0124080731. [Google Scholar]

- Sutherland, E.H.; Locke, J. Twenty Thousand Homeless Men: A Study of Unemployed Men in the Chicago Shelters; Arno Press: New York, NY, USA, 1936. [Google Scholar]

- Clinard, M.B.; Cressey, D.R. Other People’s Money: A Study in the Social Psychology of Embezzlement. Am. Sociol. Rev. 1954, 19, 362. [Google Scholar] [CrossRef]

- Wolfe, D.T.; Hermanson, D.R. The Fraud Diamond: Considering the Four Elements of Fraud. CPA J. 2004, 74, 38–42. [Google Scholar]

- Albrecht, W.S.; Albrecht, C.; Albrecht, C.C. Current Trends in Fraud and its Detection. Inf. Secur. J. Glob. Perspect. 2008, 17, 2–12. [Google Scholar] [CrossRef]

- Free, C. Looking through the fraud triangle: A review and call for new directions. Meditari Account. Res. 2015, 23, 175–196. [Google Scholar] [CrossRef]

- Morales, J.; Gendron, Y.; Guénin-Paracini, H. The construction of the risky individual and vigilant organization: A genealogy of the fraud triangle. Account. Organ. Soc. 2014, 39, 170–194. [Google Scholar] [CrossRef]

- Cieslewicz, J.K. The Fraud Model in International Contexts: A Call to Include Societal-Level Influences in the Model. J. Forencic Investig. Account. 2012, 4, 214–254. [Google Scholar]

- Lokanan, M.E. Challenges to the fraud triangle: Questions on its usefulness. Account. Forum 2015, 39, 201–224. [Google Scholar] [CrossRef]

- Krambia-Kapardis, M. Financial Crisis, Fraud, and Corruption. In Corporate Fraud and Corruption; Palgrave Macmillan US: New York, NY, USA, 2016; pp. 5–38. [Google Scholar]

- Hayek, F. The Constitution of Liberty: The Definitve Edition; University of Chicago Press: Chicago, IL, USA, 1960; ISBN 978-0-22-632084-7. [Google Scholar]

- Williamson, O.E. The New Institutional Economics: Taking Stock, Looking Ahead. J. Econ. Lit. 2000, 38, 595–613. [Google Scholar] [CrossRef]

- Williamson, C.R. Informal institutions rule: Institutional arrangements and economic performance. Public Choice 2009, 139, 371–387. [Google Scholar] [CrossRef]

- Boettke, P.J.; Coyne, C.J.; Leeson, P.T. Institutional Stickiness and the New Development Economics. Am. J. Econ. Sociol. 2008, 67, 331–358. [Google Scholar] [CrossRef]

- Long, J.S.; Ervin, L.H. Using Heteroscedasticity Consistent Standard Errors in the Linear Regression Model. Am. Stat. 2000, 54, 217–224. [Google Scholar] [CrossRef]

- The World Bank Worldwide Governance Indicators Data. Available online: https://data.worldbank.org/data-catalog/worldwide-governance-indicators (accessed on 3 January 2018).

- Kaufmann, D.; Kraay, A.; Mastruzzi, M. The Worldwide Governance Indicators: Methodology and Analytical Issues; Policy Research Working Paper Series 5430; The World Bank: Washington, DC, USA, 2010. [Google Scholar]

- Penn World Table (PWT) 9.0. Available online: https://www.rug.nl/ggdc/productivity/pwt/ (accessed on 3 January 2018).

- Feenstra, R.C.; Inklaar, R.; Timmer, M.P. The Next Generation of the Penn World Table. Am. Econ. Rev. 2015, 105, 3150–3182. [Google Scholar] [CrossRef]

- The World Bank Global Competitiveness Index. Available online: https://tcdata360.worldbank.org/indicators/gci?country=HUN&indicator=631&viz=line_chart&years=2007,2016 (accessed on 4 January 2018).

- Strickland, J. Predictive Analytics Using R; LULU COM: Morrisville, NC, USA, 2014; ISBN 978-1-31-284101-7. [Google Scholar]

- Feng, C.; Wang, H.; Lu, N.; Chen, T.; He, H.; Lu, Y.; Tu, X.M. Log-transformation and its implications for data analysis. Shanghai Arch. Psychiatry 2014, 26, 105–109. [Google Scholar] [CrossRef] [PubMed]

- Podobnik, B.; Horvatić, D.; Kenett, D.Y.; Stanley, H.E. The competitiveness versus the wealth of a country. Sci. Rep. 2012, 2, 678. [Google Scholar] [CrossRef] [PubMed]

- Mo, P.H. Corruption and Economic Growth. J. Comp. Econ. 2001, 29, 66–79. [Google Scholar] [CrossRef]

- Ulman, S.-R. Corruption and National Competitiveness in Different Stages of Country Development. Procedia Econ. Financ. 2013, 6, 150–160. [Google Scholar] [CrossRef]

- La Porta, R.; Lopez-de-Silanes, F.; Shleifer, A.; Vishny, R.W. Law and Finance. J. Political Econ. 1998, 106, 1113–1155. [Google Scholar] [CrossRef]

- Kimbro, M.B. A Cross-Country Empirical Investigation of Corruption and its Relationship to Economic, Cultural, and Monitoring Institutions: An Examination of the Role of Accounting and Financial Statements Quality. J. Account. Audit. Financ. 2002, 17, 325–350. [Google Scholar] [CrossRef]

- Arndt, C.; Oman, C. The Politics of Governance Ratings; MGSoG: Maastricht, The Netherlands, 2008. [Google Scholar]

- Thomas, M.A. What Do the Worldwide Governance Indicators Measure? Eur. J. Dev. Res. 2010, 22, 31–54. [Google Scholar] [CrossRef]

- Langbein, L.; Knack, S. The Worldwide Governance Indicators: Six, One, or None? J. Dev. Stud. 2010, 46, 350–370. [Google Scholar] [CrossRef]

- Tálas, D.; Rózsa, A. Financial competitiveness analysis in the Hungarian dairy industry. Compet. Rev. 2015, 25, 426–447. [Google Scholar] [CrossRef]

- Brodbeck, F.C.; Frese, M.; Akerblom, S.; Audia, G.; Bakacsi, G.; Bendova, H.; Bodega, D.; Bodur, M.; Booth, S.; Brenk, K.; et al. Cultural variation of leadership prototypes across 22 European countries. J. Occup. Organ. Psychol. 2000, 73, 1–29. [Google Scholar] [CrossRef]

- Oláh, J.; Bai, A.; Karmazin, G.; Balogh, P.; Popp, J. The Role Played by Trust and Its Effect on the Competiveness of Logistics Service Providers in Hungary. Sustainability 2017, 9, 2303. [Google Scholar] [CrossRef]

- Singleton, T.; Singleton, A.J. Fraud Auditing and Forensic Accounting; Wiley: Hoboken, NJ, USA, 2010; ISBN 978-0-47-056413-4. [Google Scholar]

- European Comission. Protection of the European Union’s Financial Interests—Fight against Fraud—2015 Annual Report; European Comission: Brussels, Belgium, 2015. [Google Scholar]

- European Commission. Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee, the Committee of the Regions and the European Investment Bank—On the Comission Anti-Fraud Strategy; European Comission: Brussels, Belgium, 2015. [Google Scholar]

- Williams, T. Role of Management, Corporate Governance, and Sarbanes-Oxley in Fraud: A Focus on the Precious Metals Industry; Springer: Singapore, 2018; pp. 391–409. [Google Scholar]

- Hamilton, A.; Hammer, C. Can We Measure the Power of the Grabbing Hand? A Comparative Analysis of Different Indicators of Corruption; Policy Research Working Paper; The World Bank: Washington, DC, USA, 2017. [Google Scholar]

- Máté, D.; Sadaf, R.; Tarnóczi, T.; Fenyves, V. Fraud Detection by Testing the Conformity to Benford’s Law in the Case of Wholesale Enterprises. Pol. J. Manag. Stud. 2017, 16, 115–126. [Google Scholar] [CrossRef]

| Variables/Statistics | ln(fraud) | COC | GOE | POS | REQ | RLW | VOA | ln(GDP) | ln(GCI) |

|---|---|---|---|---|---|---|---|---|---|

| Mean | 1.433 | 0.162 | 0.355 | −0.059 | 0.346 | 0.293 | 0.13 | 12.554 | 1.483 |

| Median | 1.386 | −0.138 | 0.193 | 0.009 | 0.345 | 0.037 | 0.147 | 12.761 | 1.478 |

| Minimum | 0.000 | −1.549 | −1.567 | −2.757 | −1.899 | −1.433 | −1.800 | 8.338 | 1.099 |

| Maximum | 6.471 | 2.270 | 2.194 | 1.453 | 2.231 | 2.121 | 1.740 | 16.659 | 1.741 |

| S. deviation | 1.218 | 1.064 | 0.969 | 0.955 | 0.965 | 1.029 | 0.974 | 1.712 | 0.147 |

| C.V. | 0.850 | 6.558 | 2.730 | 16.127 | 2.793 | 3.515 | 9.434 | 0.136 | 0.099 |

| Skewness | 1.070 | 0.574 | 0.130 | −0.567 | −0.041 | 0.333 | 9.274 | 0.026 | −0.165 |

| Ex. kurtosis | 1.936 | −0.889 | −1.041 | −0.171 | −0.797 | −1.122 | −1.084 | −0.448 | −0.670 |

| Shapiro-Wilk test for normality | |||||||||

| W | 0.907 *** | 0.921 *** | 0.962 *** | 0.957 *** | 0.978 *** | 0.932 *** | 0.961 *** | 0.988 *** | 0.972 *** |

| Test for multivariate normality | |||||||||

| Doornik-Hansen (χ2) = 1956.778 *** | |||||||||

| Independent Variables | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 | Model 7 | Model 8 |

|---|---|---|---|---|---|---|---|---|

| Constant | 1.129 | 1.210 | −4.542 | −3.375 | −0.449 | −0.536 | −5.798 | −3.127 |

| 8.415 *** | 9.66 *** | −5.608 *** | −4.456 | −1.850* | −2.352 * | −8.699 *** | −2.553 ** | |

| COC | −0.549 | −0.756 | −0.663 | −0.497 | ||||

| 0.456 | −1.968 * | −1,654 | −1.9920 * | |||||

| GOE | 0.995 | 0.631 | -0.298 | 1.252 | 1.079 | |||

| 2.201 ** | 3.027 *** | −0.298 | 3.230 *** | 3.903 *** | ||||

| POS | −0.550 | −0.654 | 0.080 | −0.498 | 0.344 | |||

| −2.593 ** | −2.933 *** | 0.142 | −2.962 *** | −2.544 ** | ||||

| REQ | −0.523 | 0.149 | −0.305 | |||||

| −1.434 | 0.436 | −1.127 | ||||||

| RLW | 0.660 | 0.687 | 0.315 | |||||

| 1.130 | 1.438 | 0.664 | ||||||

| VOA | 0.021 | 0.019 | 0.017 | 0.017 | 0.016 | 0.046 | ||

| 4.654 *** | 5.668 *** | 4.275 *** | 6.680 *** | 3.815 *** | 3.593 *** | |||

| ln(GDP) | 0.464 | 0.376 | 0.464 | |||||

| 6.735 *** | 6.063 *** | 8.879 *** | ||||||

| ln(GCI) | 1.855 | |||||||

| 2.553 ** | ||||||||

| English | 1.910 | 1.954 | 2.026 | 2.439 | ||||

| 6.007 *** | 5.406 *** | 9.354 *** | 6.947 *** | |||||

| French | 1.215 | 2.02553 | 1.242 | 1.617 | ||||

| 4.335 *** | 5.289 *** | 6.934 *** | 6.372 *** | |||||

| German | 1.378 | 1.425 | 0.940 | 1.626 | ||||

| 3.362 *** | 3.544 *** | 2.253 ** | 4.652 *** | |||||

| Observation | 89 | 89 | 89 | 89 | 67 | 67 | 66 | 63 |

| Adjusted R2 | 0.826 | 0.793 | 0.891 | 0.861 | 0.983 | 0.981 | 0.680 | 0.665 |

| F-test | 70.67 *** | 113.41 *** | 102.66 *** | 287.28 *** | 451.61 *** | 486.36 *** | 35.56 *** | 31.88 *** |

| Independent Variables | Model 9 | Model 10 | Model 11 | Model 12 | Model 13 | Model 14 |

|---|---|---|---|---|---|---|

| Constant | 1.221 | 2.221 | −0.402 | –2.661 | –5.292 | |

| 10.27 *** | 10.27 *** | −0.942 | −2.335 ** | −4.209 *** | ||

| COC | −0.097 | −0.917 | -0.925 | |||

| −0.2800 | −2.675 *** | −3.253 *** | ||||

| GOE | 0.346 | 1.035 | 1.533 | 1.551 | ||

| 0.804 | 5.654 *** | 3.161 *** | 4.589 *** | |||

| POS | −0.631 | −0.641 | −0.955 | −0.842 | ||

| −3.986 *** | −4.922 *** | −5.348 *** | −4.666 *** | |||

| REQ | 0.190 | −0.212 | ||||

| 0.363 | −0.558 | |||||

| RLW | 0.190 | −0.212 | ||||

| 0.363 | 0.903 | |||||

| VOA | −0.004 | 0.681 | 0.612 | |||

| −0.026 | 3.279 *** | 3.363 *** | ||||

| ln(GCI) | 3.029 | 3.674 | ||||

| 3.863 *** | 4.986 *** | |||||

| English | 1.941 | 1.132 | 2.239 | |||

| 4.132 *** | 3.462 *** | 5.450 *** | ||||

| French | 1.328 | 0.542 | 1.562 | |||

| 2.816 *** | 1.187 ** | 4.482 *** | ||||

| German | 0.742 | 0.963 | ||||

| 0.127 | 3.686 *** | |||||

| Observation | 102 | 102 | 74 | 74 | 95 | 70 |

| Adjusted R2 | 0.195 | 0.231 | 0.563 | 0.421 | 0.138 | 0.372 |

| F-test | 5.079 *** | 16.19 *** | 9.171 *** | 9.848 *** | 14.92 *** | 9.66 *** |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sadaf, R.; Oláh, J.; Popp, J.; Máté, D. An Investigation of the Influence of the Worldwide Governance and Competitiveness on Accounting Fraud Cases: A Cross-Country Perspective. Sustainability 2018, 10, 588. https://doi.org/10.3390/su10030588

Sadaf R, Oláh J, Popp J, Máté D. An Investigation of the Influence of the Worldwide Governance and Competitiveness on Accounting Fraud Cases: A Cross-Country Perspective. Sustainability. 2018; 10(3):588. https://doi.org/10.3390/su10030588

Chicago/Turabian StyleSadaf, Rabeea, Judit Oláh, József Popp, and Domicián Máté. 2018. "An Investigation of the Influence of the Worldwide Governance and Competitiveness on Accounting Fraud Cases: A Cross-Country Perspective" Sustainability 10, no. 3: 588. https://doi.org/10.3390/su10030588

APA StyleSadaf, R., Oláh, J., Popp, J., & Máté, D. (2018). An Investigation of the Influence of the Worldwide Governance and Competitiveness on Accounting Fraud Cases: A Cross-Country Perspective. Sustainability, 10(3), 588. https://doi.org/10.3390/su10030588